India–Pakistan Trade: Perspectives from the Automobile Sector in Pakistan

0

AUTOMOBILE INDUSTRY OF PAKISTAN

(INFORMATION PACKAGE)

1

Segments of Automobile Industry

Pakistan Automobile Industry operates in following ranges of products:

• Cars & Light Commercial Vehicles (LCVs)/Pickups.

• Two and three wheelers.

• Tractors.

• Trucks & Buses.

• Vendor Industry.

2

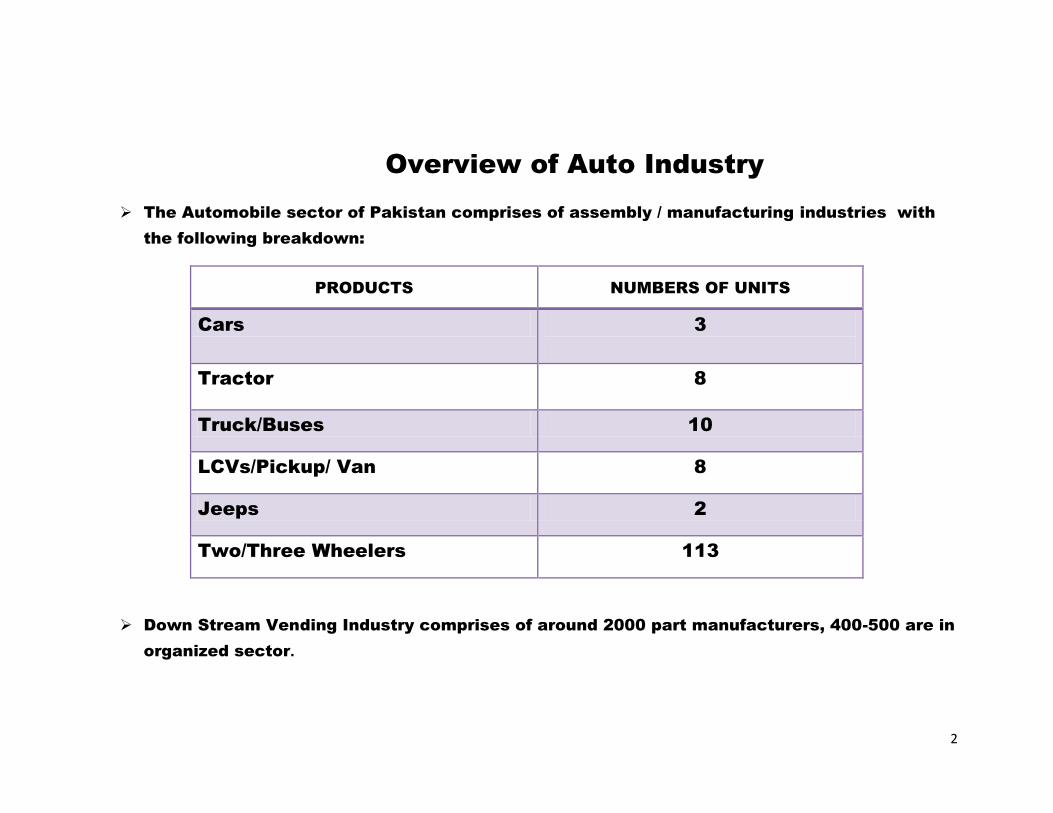

Overview of Auto Industry

The Automobile sector of Pakistan comprises of assembly / manufacturing industries with

the following breakdown:

PRODUCTS NUMBERS OF UNITS

Cars 3

Tractor 8

Truck/Buses 10

LCVs/Pickup/ Van 8

Jeeps 2

Two/Three Wheelers 113

Down Stream Vending Industry comprises of around 2000 part manufacturers, 400-500 are in

organized sector.

3

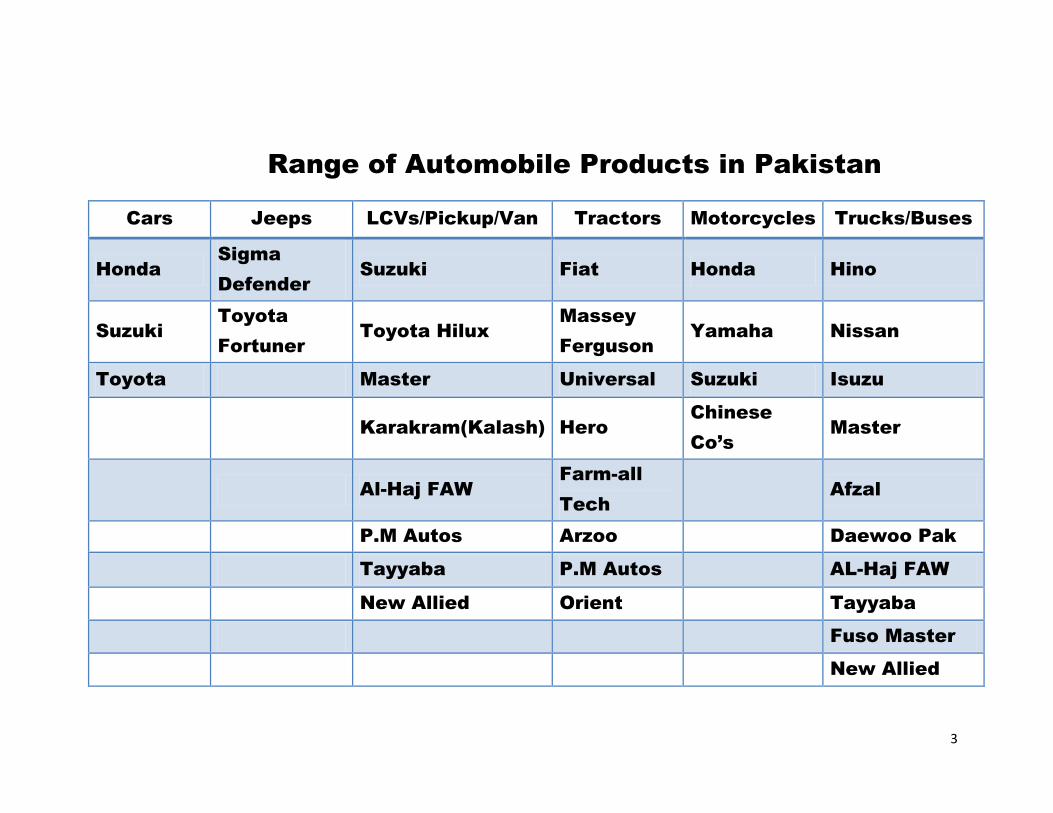

Range of Automobile Products in Pakistan

Cars Jeeps LCVs/Pickup/Van Tractors Motorcycles Trucks/Buses

Honda

Sigma

Defender

Suzuki Fiat Honda Hino

Suzuki

Toyota

Fortuner

Toyota Hilux

Massey

Ferguson

Yamaha Nissan

Toyota Master Universal Suzuki Isuzu

Karakram(Kalash) Hero

Chinese

Co’s

Master

Al-Haj FAW

Farm-all

Tech

Afzal

P.M Autos Arzoo

Daewoo Pak

Tayyaba P.M Autos

AL-Haj FAW

New Allied Orient

Tayyaba

Fuso Master

New Allied

4

Market Share % (2014-15)

Market Share % Car Motorcycle Truck Buses Tractors Jeeps

LCVs/

Pick Ups

Japanese 100 41 69 62 0 62 96

Non Japanese 0 59 31 38 100 38 4

5

Major Joint Ventures for Automobile

COMPANY JOINT VENTURE PRODUCT

Indus Motor Co. Toyota & Daihatsu, Japan Corolla & Cuore Cars

Atlas Honda Ltd. Honda, Japan Honda Cars/ Motorcycle

Pak Suzuki Motor Co. Suzuki, Japan Cars, Van, Jeep, Pickup

Suzuki Motorcycle Suzuki, Japan Suzuki Motorcycle

Master Motor Corp. Yuejin & Faw, China LCVs, Buses

Sind Engineering Ltd. Dong Feng, China LCVs, Bus

Tayyaba Motors China Trucks

Fuso Master Motors China Truck & Buses

Sigma Motors Ltd. Land Rover, UK Jeeps

New Allied Motors China Truck / Buses / mini van

Al-Hajj Faw Motors China Truck /pickup / X-PV

Afzal Motors Daewoo, Korea Buses

Karakoram Motors Changan, China LCVs

6

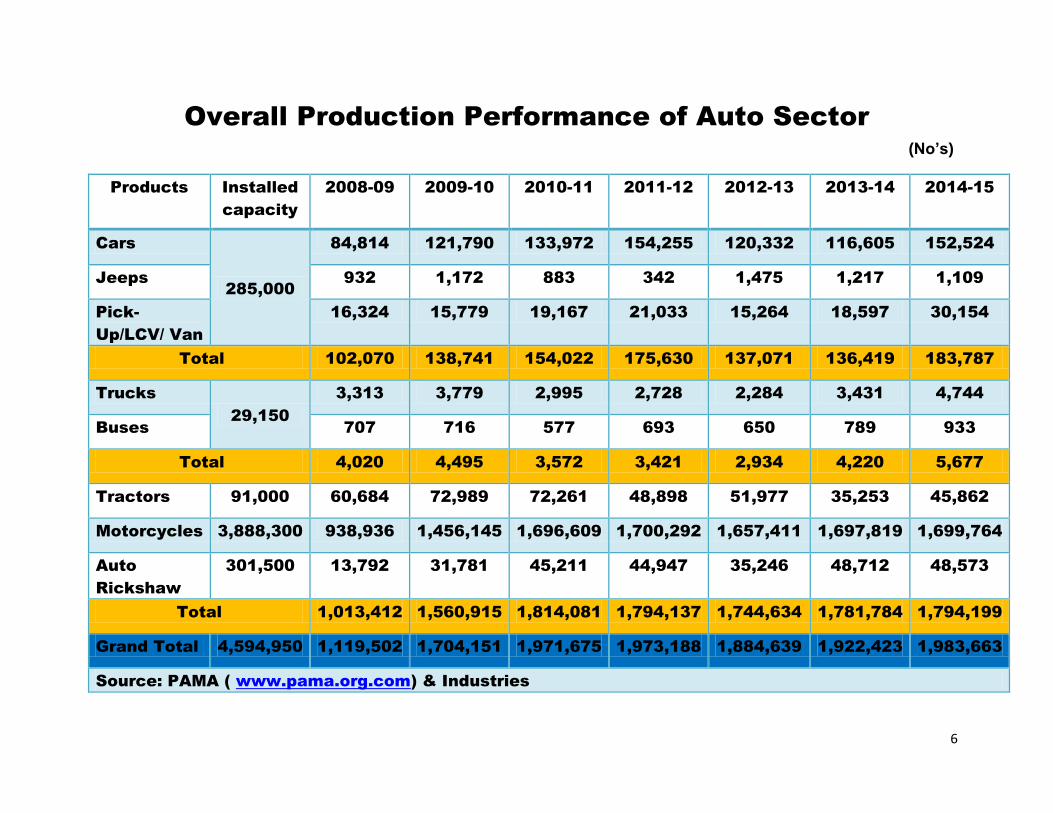

Overall Production Performance of Auto Sector

(No’s)

Products Installed

capacity

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Cars

285,000

84,814 121,790 133,972 154,255 120,332 116,605 152,524

Jeeps 932 1,172 883 342 1,475 1,217 1,109

Pick-

Up/LCV/ Van

16,324 15,779 19,167 21,033 15,264 18,597 30,154

Total 102,070 138,741 154,022 175,630 137,071 136,419 183,787

Trucks

29,150

3,313 3,779 2,995 2,728 2,284 3,431 4,744

Buses 707 716 577 693 650 789 933

Total 4,020 4,495 3,572 3,421 2,934 4,220 5,677

Tractors 91,000 60,684 72,989 72,261 48,898 51,977 35,253 45,862

Motorcycles 3,888,300 938,936 1,456,145 1,696,609 1,700,292 1,657,411 1,697,819 1,699,764

Auto

Rickshaw

301,500 13,792 31,781 45,211 44,947 35,246 48,712 48,573

Total 1,013,412 1,560,915 1,814,081 1,794,137 1,744,634 1,781,784 1,794,199

Grand Total 4,594,950 1,119,502 1,704,151 1,971,675 1,973,188 1,884,639 1,922,423 1,983,663

Source: PAMA ( www.pama.org.com) & Industries

7

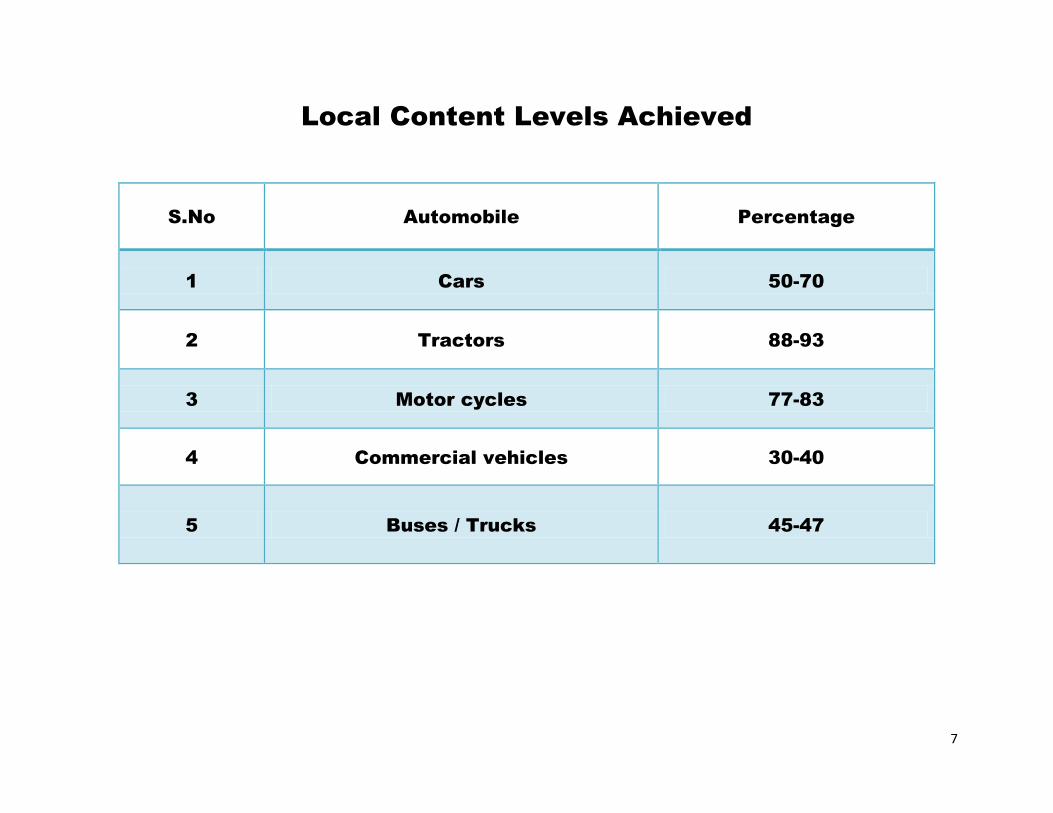

Local Content Levels Achieved

S.No Automobile Percentage

1 Cars 50-70

2 Tractors 88-93

3 Motor cycles 77-83

4 Commercial vehicles 30-40

5 Buses / Trucks 45-47

8

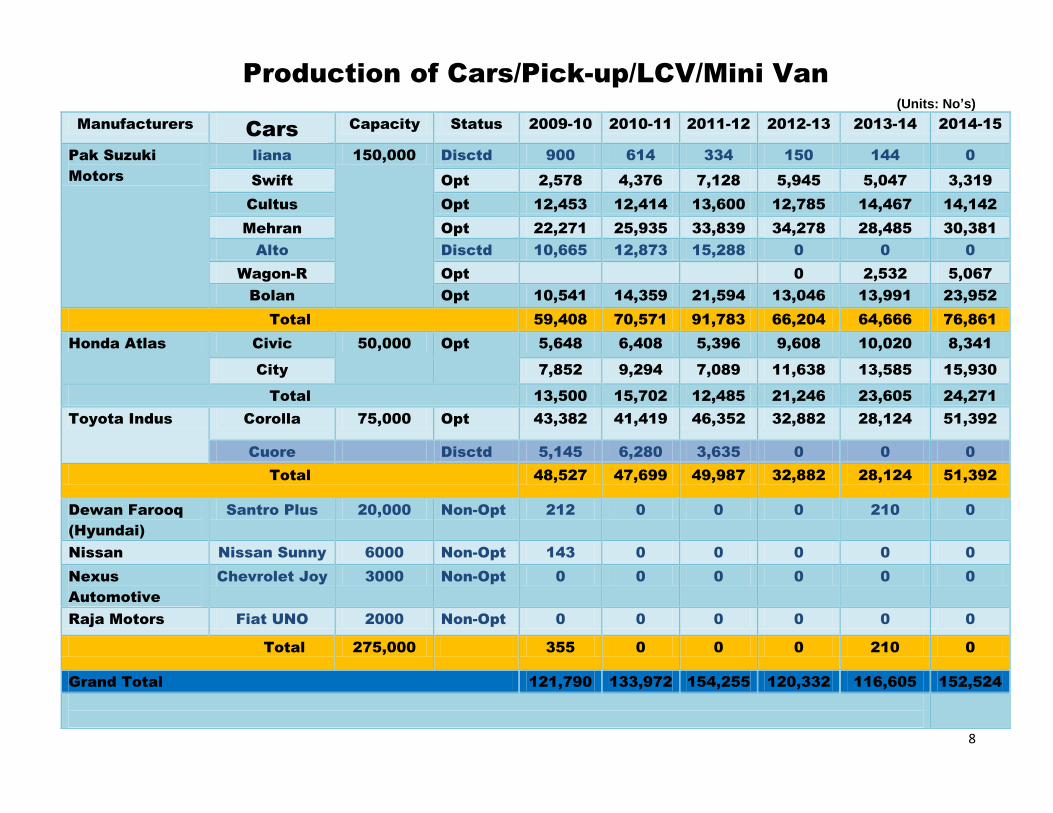

Production of Cars/Pick-up/LCV/Mini Van

(Units: No’s)

Manufacturers Cars

Capacity Status 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Pak Suzuki

Motors

liana 150,000 Disctd 900 614 334 150 144 0

Swift Opt 2,578 4,376 7,128 5,945 5,047 3,319

Cultus Opt 12,453 12,414 13,600 12,785 14,467 14,142

Mehran Opt 22,271 25,935 33,839 34,278 28,485 30,381

Alto Disctd 10,665 12,873 15,288 0 0 0

Wagon-R Opt 0 2,532 5,067

Bolan Opt 10,541 14,359 21,594 13,046 13,991 23,952

Total 59,408 70,571 91,783 66,204 64,666 76,861

Honda Atlas Civic 50,000 Opt 5,648 6,408 5,396 9,608 10,020 8,341

City 7,852 9,294 7,089 11,638 13,585 15,930

Total 13,500 15,702 12,485 21,246 23,605 24,271

Toyota Indus Corolla 75,000 Opt 43,382 41,419 46,352 32,882 28,124 51,392

Cuore Disctd 5,145 6,280 3,635 0 0 0

Total 48,527 47,699 49,987 32,882 28,124 51,392

Dewan Farooq

(Hyundai)

Santro Plus 20,000 Non-Opt 212 0 0 0 210 0

Nissan Nissan Sunny 6000 Non-Opt 143 0 0 0 0 0

Nexus

Automotive

Chevrolet Joy 3000 Non-Opt 0 0 0 0 0 0

Raja Motors Fiat UNO 2000 Non-Opt 0 0 0 0 0 0

Total 275,000 355 0 0 0 210 0

Grand Total 121,790 133,972 154,255 120,332 116,605 152,524

9

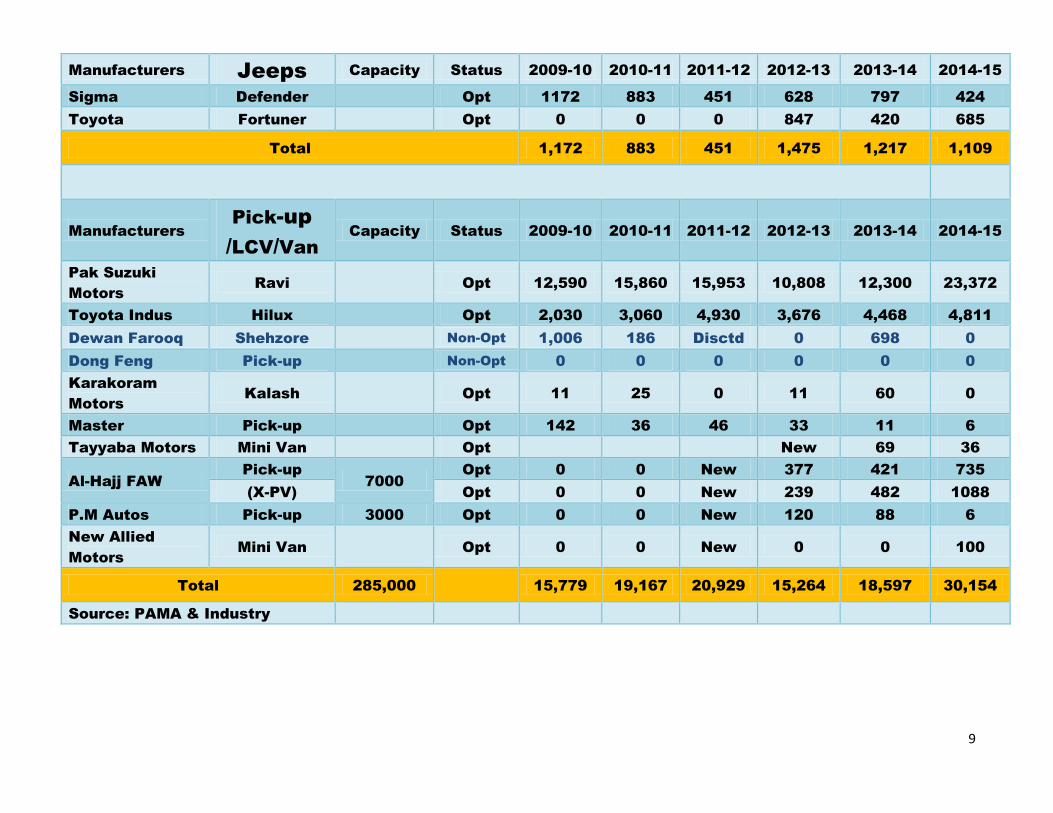

Manufacturers Jeeps Capacity Status 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Sigma Defender

Opt 1172 883 451 628 797 424

Toyota Fortuner

Opt 0 0 0 847 420 685

Total 1,172 883 451 1,475 1,217 1,109

Manufacturers

Pick-up

/LCV/Van

Capacity Status 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Pak Suzuki

Motors

Ravi

Opt 12,590 15,860 15,953 10,808 12,300 23,372

Toyota Indus Hilux

Opt 2,030 3,060 4,930 3,676 4,468 4,811

Dewan Farooq Shehzore

Non-Opt 1,006 186 Disctd 0 698 0

Dong Feng Pick-up

Non-Opt 0 0 0 0 0 0

Karakoram

Motors

Kalash

Opt 11 25 0 11 60 0

Master Pick-up

Opt 142 36 46 33 11 6

Tayyaba Motors Mini Van

Opt

New 69 36

Al-Hajj FAW

Pick-up

7000

Opt 0 0 New 377 421 735

(X-PV) Opt 0 0 New 239 482 1088

P.M Autos Pick-up 3000 Opt 0 0 New 120 88 6

New Allied

Motors

Mini Van

Opt 0 0 New 0 0 100

Total 285,000

15,779 19,167 20,929 15,264 18,597 30,154

Source: PAMA & Industry

10

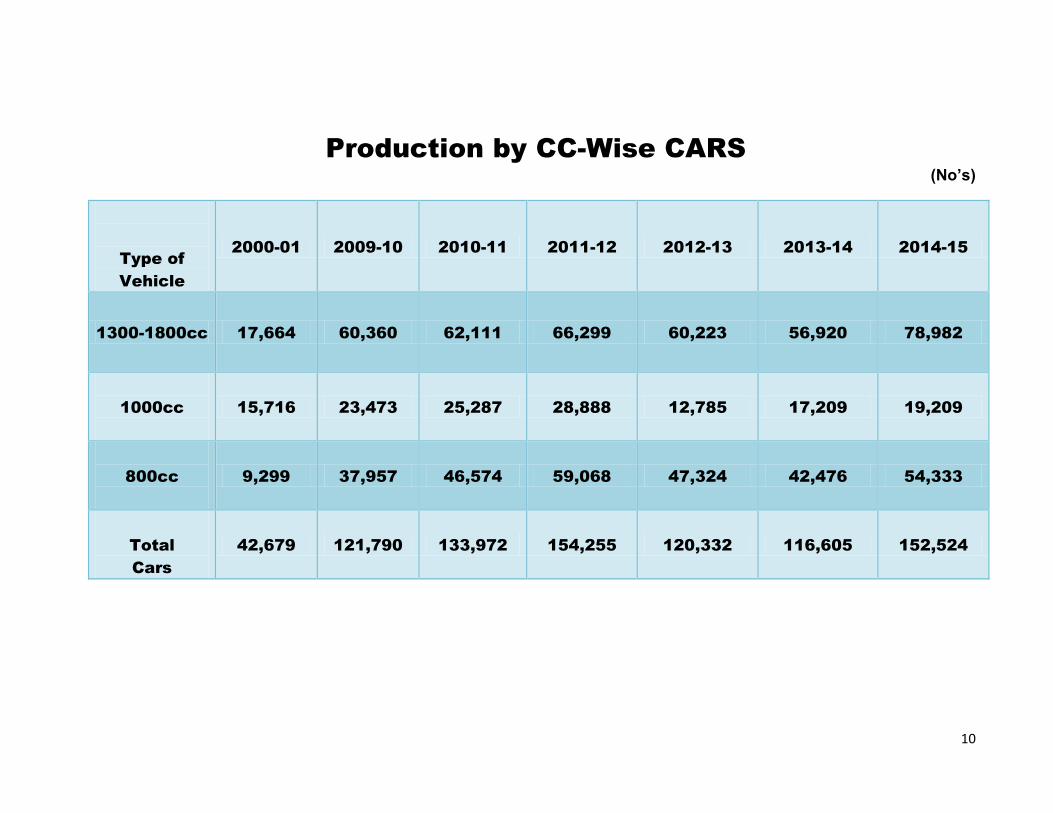

Production by CC-Wise CARS

(No’s)

Type of

Vehicle

2000-01 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

1300-1800cc 17,664 60,360 62,111 66,299 60,223 56,920 78,982

1000cc

15,716 23,473 25,287 28,888 12,785 17,209 19,209

800cc

9,299 37,957 46,574 59,068 47,324 42,476 54,333

Total

Cars

42,679 121,790 133,972 154,255 120,332 116,605 152,524

11

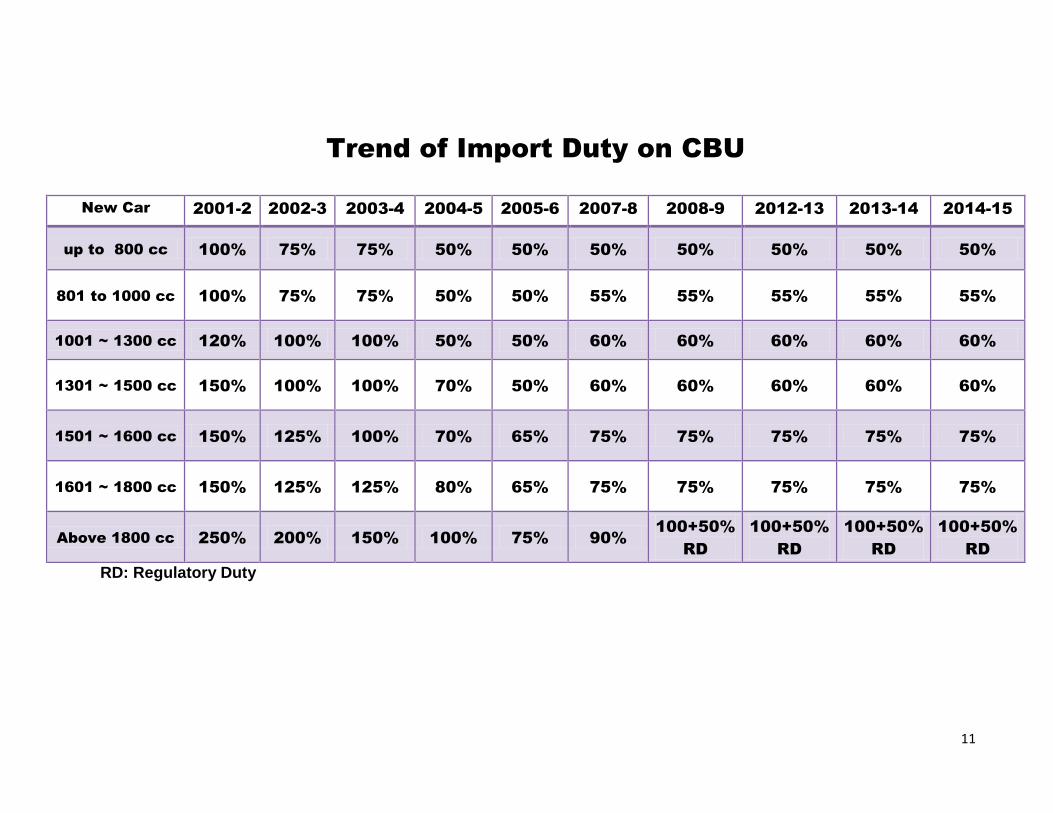

Trend of Import Duty on CBU

New Car 2001-2 2002-3 2003-4 2004-5 2005-6 2007-8 2008-9 2012-13 2013-14 2014-15

up to 800 cc 100% 75% 75% 50% 50% 50% 50% 50% 50% 50%

801 to 1000 cc 100% 75% 75% 50% 50% 55% 55% 55% 55% 55%

1001 ~ 1300 cc 120% 100% 100% 50% 50% 60% 60% 60% 60% 60%

1301 ~ 1500 cc 150% 100% 100% 70% 50% 60% 60% 60% 60% 60%

1501 ~ 1600 cc 150% 125% 100% 70% 65% 75% 75% 75% 75% 75%

1601 ~ 1800 cc 150% 125% 125% 80% 65% 75% 75% 75% 75% 75%

Above 1800 cc 250% 200% 150% 100% 75% 90%

100+50%

RD

100+50%

RD

100+50%

RD

100+50%

RD

RD: Regulatory Duty

12

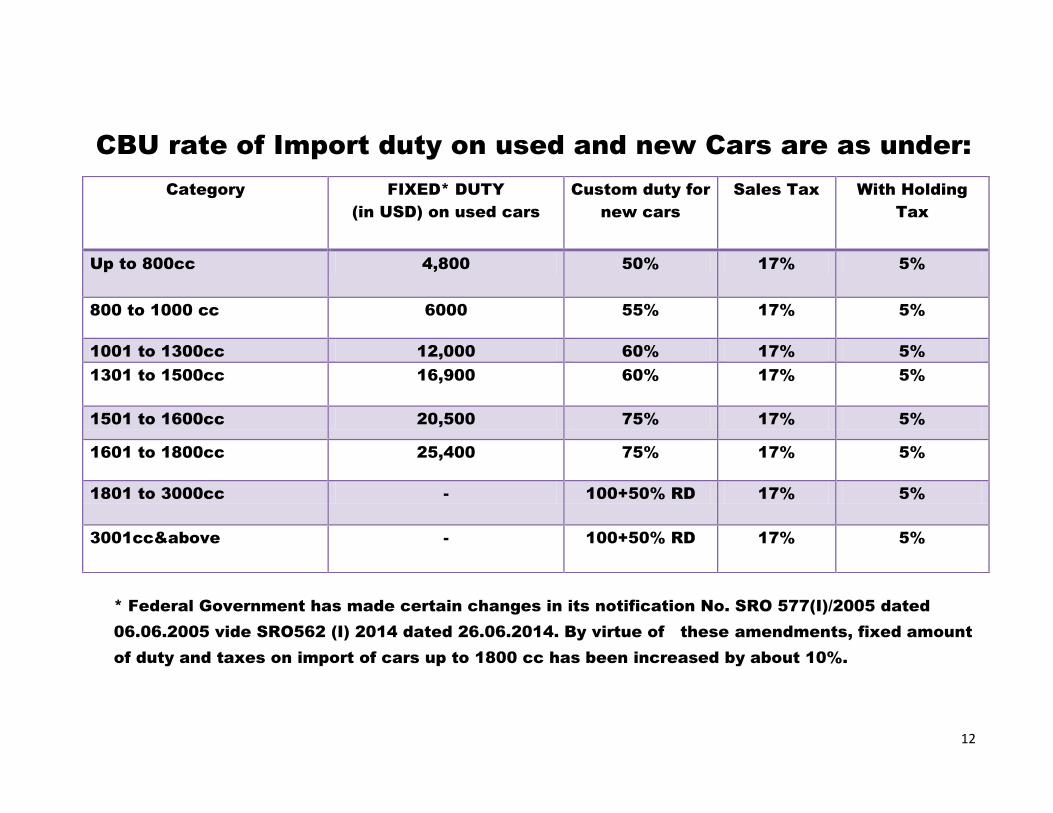

CBU rate of Import duty on used and new Cars are as under:

* Federal Government has made certain changes in its notification No. SRO 577(I)/2005 dated

06.06.2005 vide SRO562 (I) 2014 dated 26.06.2014. By virtue of these amendments, fixed amount

of duty and taxes on import of cars up to 1800 cc has been increased by about 10%.

Category FIXED* DUTY

(in USD) on used cars

Custom duty for

new cars

Sales Tax With Holding

Tax

Up to 800cc 4,800 50% 17% 5%

800 to 1000 cc 6000 55% 17% 5%

1001 to 1300cc 12,000 60% 17% 5%

1301 to 1500cc 16,900 60% 17% 5%

1501 to 1600cc 20,500 75% 17% 5%

1601 to 1800cc 25,400 75% 17% 5%

1801 to 3000cc - 100+50% RD 17% 5%

3001cc&above - 100+50% RD 17% 5%

13

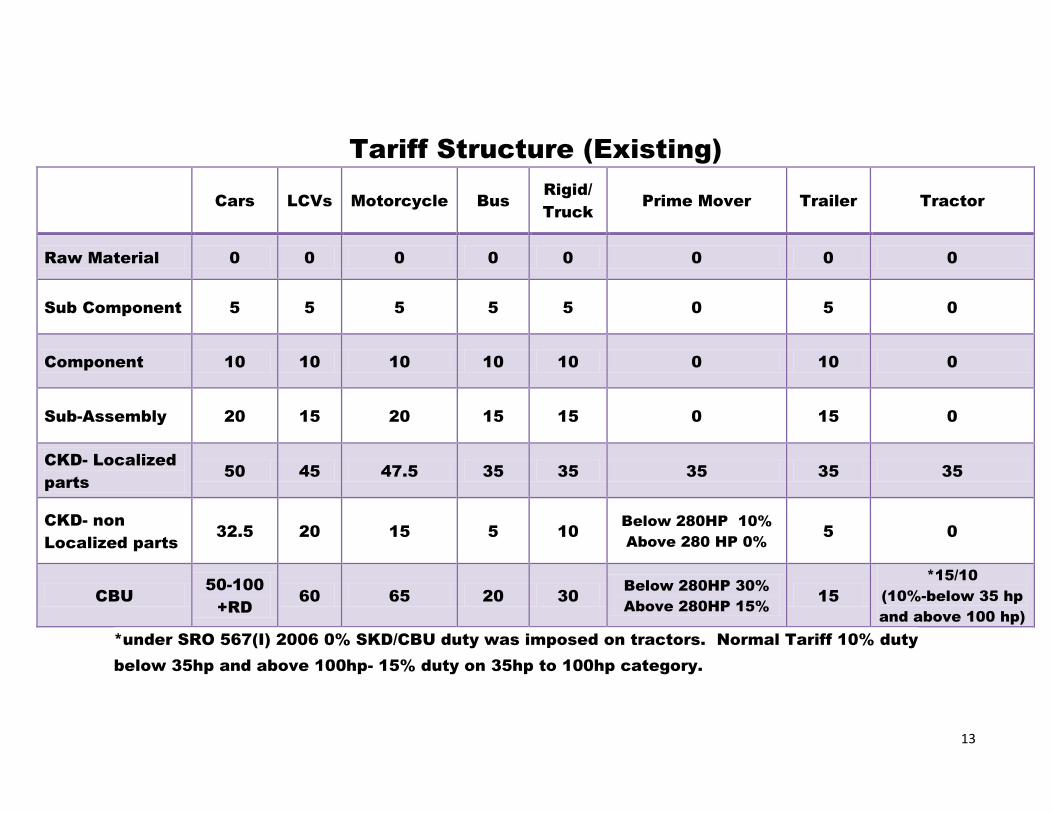

Tariff Structure (Existing)

Cars LCVs Motorcycle Bus

Rigid/

Truck

Prime Mover Trailer Tractor

Raw Material 0 0 0 0 0 0 0 0

Sub Component 5 5 5 5 5 0 5 0

Component 10 10 10 10 10 0 10 0

Sub-Assembly 20 15 20 15 15 0 15 0

CKD- Localized

parts

50 45 47.5 35 35 35 35 35

CKD- non

Localized parts

32.5 20 15 5 10

Below 280HP 10%

Above 280 HP 0%

5 0

CBU

50-100

+RD

60 65 20 30

Below 280HP 30%

Above 280HP 15%

15

*15/10

(10%-below 35 hp

and above 100 hp)

*under SRO 567(I) 2006 0% SKD/CBU duty was imposed on tractors. Normal Tariff 10% duty

below 35hp and above 100hp- 15% duty on 35hp to 100hp category.

14

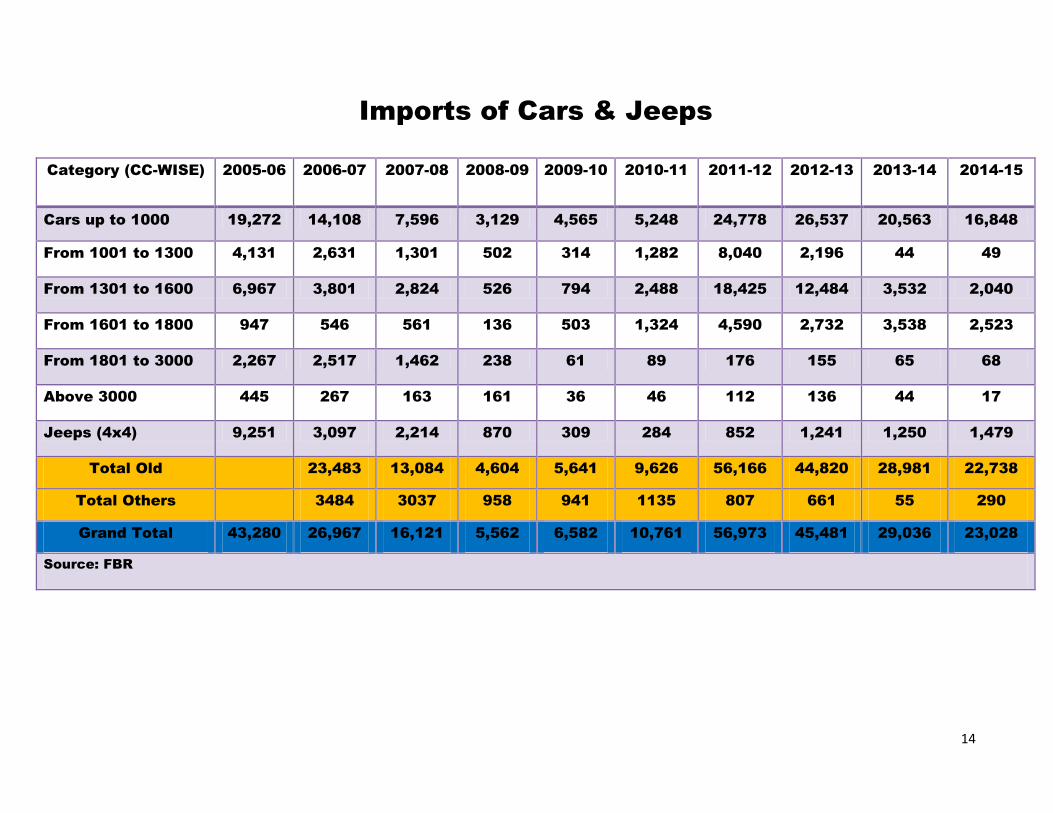

Imports of Cars & Jeeps

Category (CC-WISE) 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Cars up to 1000 19,272 14,108 7,596 3,129 4,565 5,248 24,778 26,537 20,563 16,848

From 1001 to 1300 4,131 2,631 1,301 502 314 1,282 8,040 2,196 44 49

From 1301 to 1600 6,967 3,801 2,824 526 794 2,488 18,425 12,484 3,532 2,040

From 1601 to 1800 947 546 561 136 503 1,324 4,590 2,732 3,538 2,523

From 1801 to 3000 2,267 2,517 1,462 238 61 89 176 155 65 68

Above 3000 445 267 163 161 36 46 112 136 44 17

Jeeps (4x4) 9,251 3,097 2,214 870 309 284 852 1,241 1,250 1,479

Total Old 23,483 13,084 4,604 5,641 9,626 56,166 44,820 28,981 22,738

Total Others 3484 3037 958 941 1135 807 661 55 290

Grand Total 43,280 26,967 16,121 5,562 6,582 10,761 56,973 45,481 29,036 23,028

Source: FBR

15

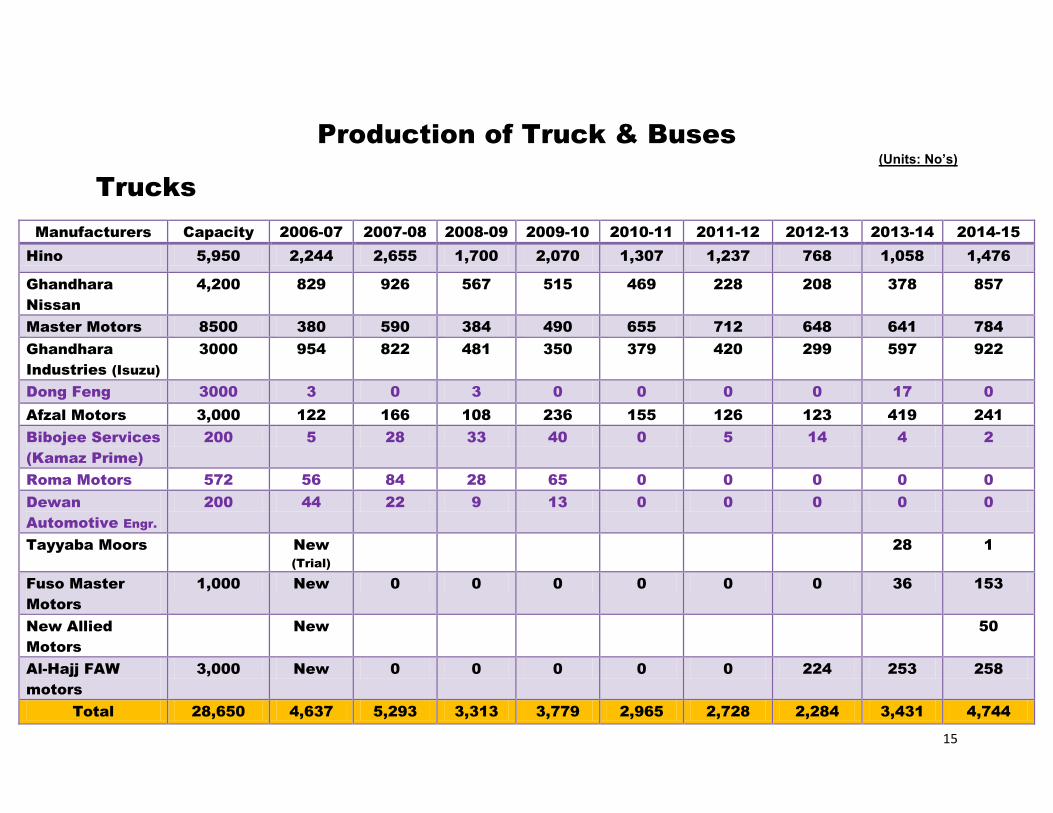

Production of Truck & Buses

(Units: No’s)

Trucks

Manufacturers Capacity 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Hino 5,950 2,244 2,655 1,700 2,070 1,307 1,237 768 1,058 1,476

Ghandhara

Nissan

4,200 829 926 567 515 469 228 208 378 857

Master Motors 8500 380 590 384 490 655 712 648 641 784

Ghandhara

Industries (Isuzu)

3000 954 822 481 350 379 420 299 597 922

Dong Feng 3000 3 0 3 0 0 0 0 17 0

Afzal Motors 3,000 122 166 108 236 155 126 123 419 241

Bibojee Services

(Kamaz Prime)

200 5 28 33 40 0 5 14 4 2

Roma Motors 572 56 84 28 65 0 0 0 0 0

Dewan

Automotive Engr.

200 44 22 9 13 0 0 0 0 0

Tayyaba Moors New

(Trial)

28 1

Fuso Master

Motors

1,000 New 0 0 0 0 0 0 36 153

New Allied

Motors

New 50

Al-Hajj FAW

motors

3,000 New 0 0 0 0 0 224 253 258

Total 28,650 4,637 5,293 3,313 3,779 2,965 2,728 2,284 3,431 4,744

16

Buses

Blue line shows non operational units

Manufacturers 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Hino 744 887 515 484 394 468 420 477 484

Ghandhara

Nissan

31 54 0 30 0 6 0 6 18

Master 5 8 0 19 1 22 4 14 11

Ghandhara

Industries (Isuzu)

205 182 136 95 95 72 98 61 80

Dong Feng 8 15 11 0 0 0 0 0 0

Afzal Motors 0 0 0 37 43 30 2 20 9

Fuso Master

Motors

31 95

Daewoo Pak

Motors

80 14 45 43 51 95 126 180 236

Total 1,073 1,160 707 708 584 693 650 789 933

17

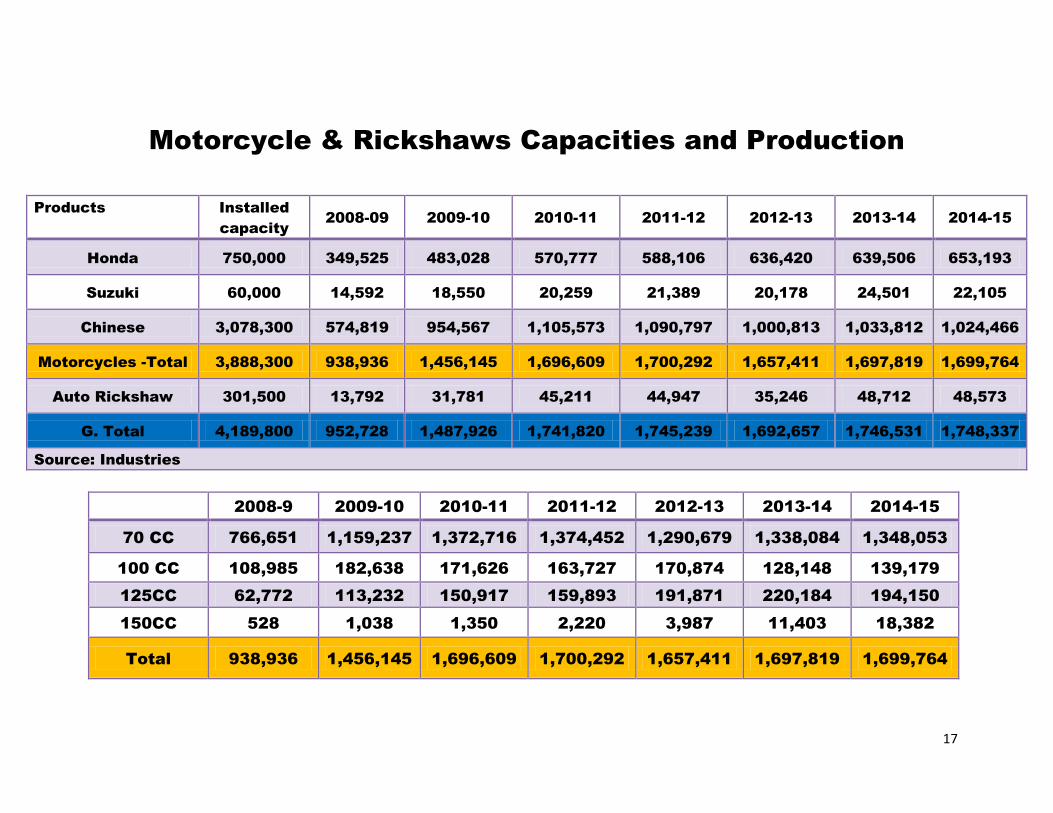

Motorcycle & Rickshaws Capacities and Production

Products Installed

capacity

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Honda 750,000 349,525 483,028 570,777 588,106 636,420 639,506 653,193

Suzuki 60,000 14,592 18,550 20,259 21,389 20,178 24,501 22,105

Chinese 3,078,300 574,819 954,567 1,105,573 1,090,797 1,000,813 1,033,812 1,024,466

Motorcycles -Total 3,888,300 938,936 1,456,145 1,696,609 1,700,292 1,657,411 1,697,819 1,699,764

Auto Rickshaw 301,500 13,792 31,781 45,211 44,947 35,246 48,712 48,573

G. Total 4,189,800 952,728 1,487,926 1,741,820 1,745,239 1,692,657 1,746,531 1,748,337

Source: Industries

2008-9 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

70 CC 766,651 1,159,237 1,372,716 1,374,452 1,290,679 1,338,084 1,348,053

100 CC 108,985 182,638 171,626 163,727 170,874 128,148 139,179

125CC 62,772 113,232 150,917 159,893 191,871 220,184 194,150

150CC 528 1,038 1,350 2,220 3,987 11,403 18,382

Total 938,936 1,456,145 1,696,609 1,700,292 1,657,411 1,697,819 1,699,764

18

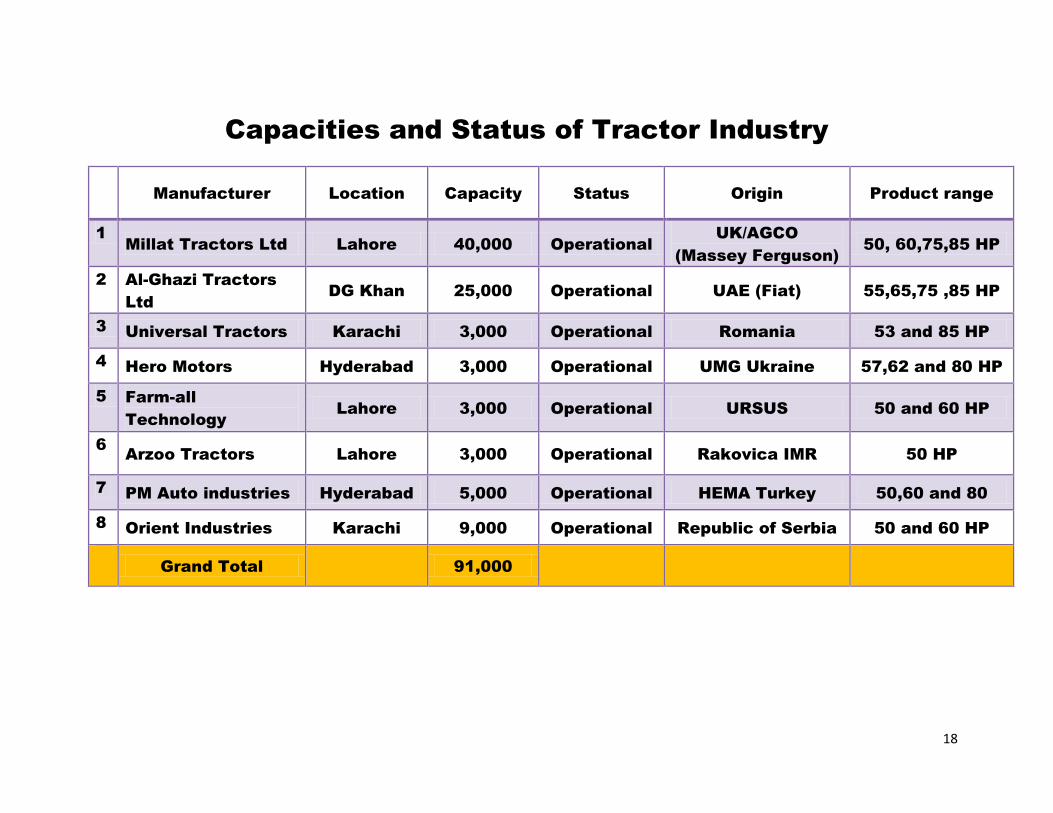

Capacities and Status of Tractor Industry

Manufacturer Location Capacity Status Origin Product range

1

Millat Tractors Ltd Lahore 40,000 Operational

UK/AGCO

(Massey Ferguson)

50, 60,75,85 HP

2 Al-Ghazi Tractors

Ltd

DG Khan 25,000 Operational UAE (Fiat) 55,65,75 ,85 HP

3 Universal Tractors Karachi 3,000 Operational Romania 53 and 85 HP

4 Hero Motors Hyderabad 3,000 Operational UMG Ukraine 57,62 and 80 HP

5 Farm-all

Technology

Lahore 3,000 Operational URSUS 50 and 60 HP

6 Arzoo Tractors Lahore 3,000 Operational Rakovica IMR 50 HP

7 PM Auto industries Hyderabad 5,000 Operational HEMA Turkey 50,60 and 80

8 Orient Industries Karachi 9,000 Operational Republic of Serbia 50 and 60 HP

Grand Total

91,000

19

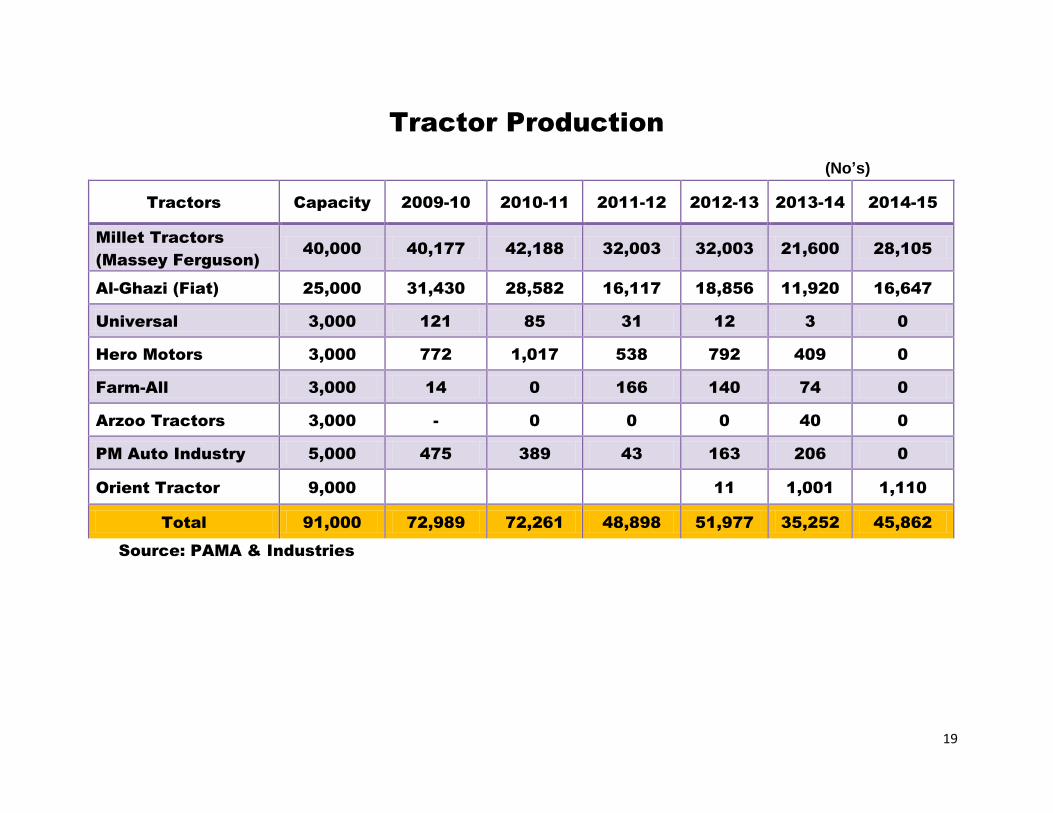

Tractor Production

(No’s)

Tractors Capacity 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

Millet Tractors

(Massey Ferguson)

40,000 40,177 42,188 32,003 32,003 21,600 28,105

Al-Ghazi (Fiat) 25,000 31,430 28,582 16,117 18,856 11,920 16,647

Universal 3,000 121 85 31 12 3 0

Hero Motors 3,000 772 1,017 538 792 409 0

Farm-All 3,000 14 0 166 140 74 0

Arzoo Tractors 3,000 - 0 0 0 40 0

PM Auto Industry 5,000 475 389 43 163 206 0

Orient Tractor 9,000

11 1,001 1,110

Total 91,000 72,989 72,261 48,898 51,977 35,252 45,862

Source: PAMA & Industries

20

Indigenous Capabilities

Down Stream Vending Industry comprises of around 2000 part

manufacturers,

400 are in organized sector.

Capable in producing:

o Interior trims

o Plastic Parts

o Forgings

o Casting

o Machined Parts

o Rubber Parts

o Electrical parts

21

Vendor Industry Technical Collaboration

Components Vendors in Pakistan Collaborating Partners

Shock absorbers M/s Honda Atlas Ltd

M/s Agri Auto Ind

Showa, Japan, Kayaba

Radiators M/s Alwin Engg.

M/s Loads Pvt. Ltd

U.E. Radiators, Japan

Toyo Radiator Japan

Car A/C M/s Sanpak, M/s Thal

Engg

Sanden, Japan, Denso

Radio Cassette Player M/s Automate Ind Panasonic Thailand

Lamps M/s Techno Pak Koito, Japan

Spark Plugs M/s Shaigan Electric NGK, Japan

Glass M/s NGS Pak NGS, Japan

Steering Case set M/s Polymer & Precision I.S. Seiseki, Japan

Brake Drum Assembly M/s Alsons Auto Ltd Nissin Kogyo, Japan

22

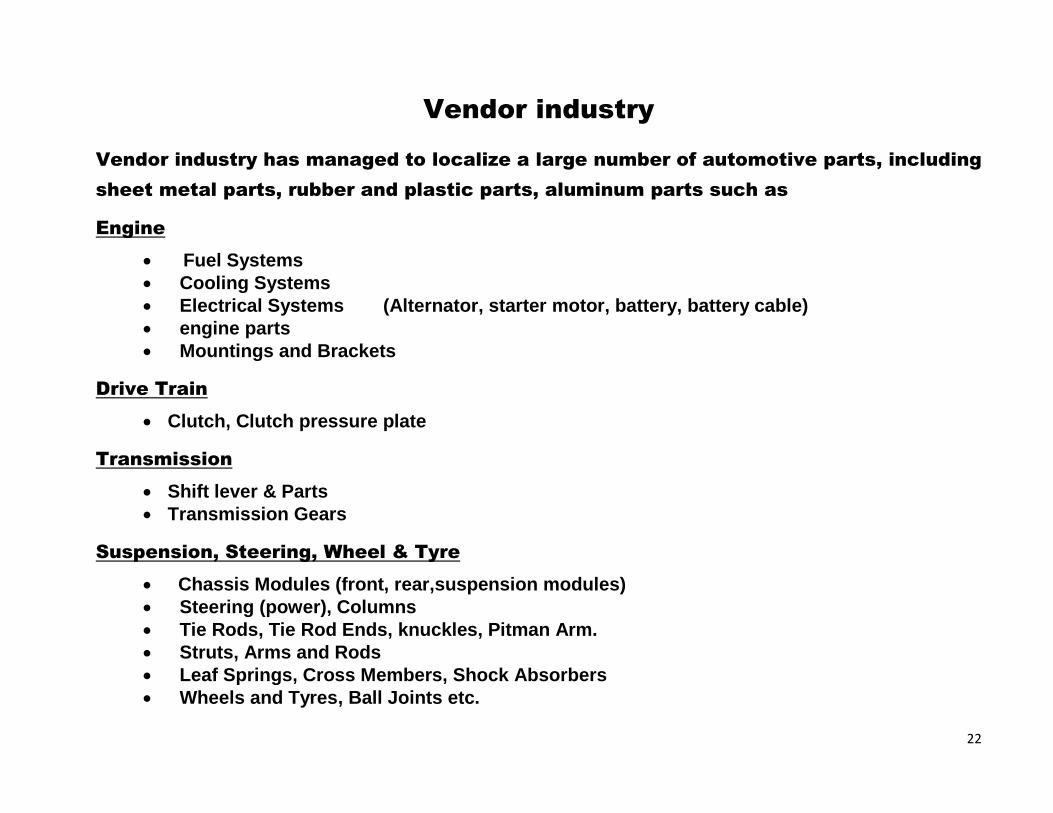

Vendor industry

Vendor industry has managed to localize a large number of automotive parts, including

sheet metal parts, rubber and plastic parts, aluminum parts such as

Engine

Fuel Systems

Cooling Systems

Electrical Systems (Alternator, starter motor, battery, battery cable)

engine parts

Mountings and Brackets

Drive Train

Clutch, Clutch pressure plate

Transmission

Shift lever & Parts

Transmission Gears

Suspension, Steering, Wheel & Tyre

Chassis Modules (front, rear,suspension modules)

Steering (power), Columns

Tie Rods, Tie Rod Ends, knuckles, Pitman Arm.

Struts, Arms and Rods

Leaf Springs, Cross Members, Shock Absorbers

Wheels and Tyres, Ball Joints etc.

23

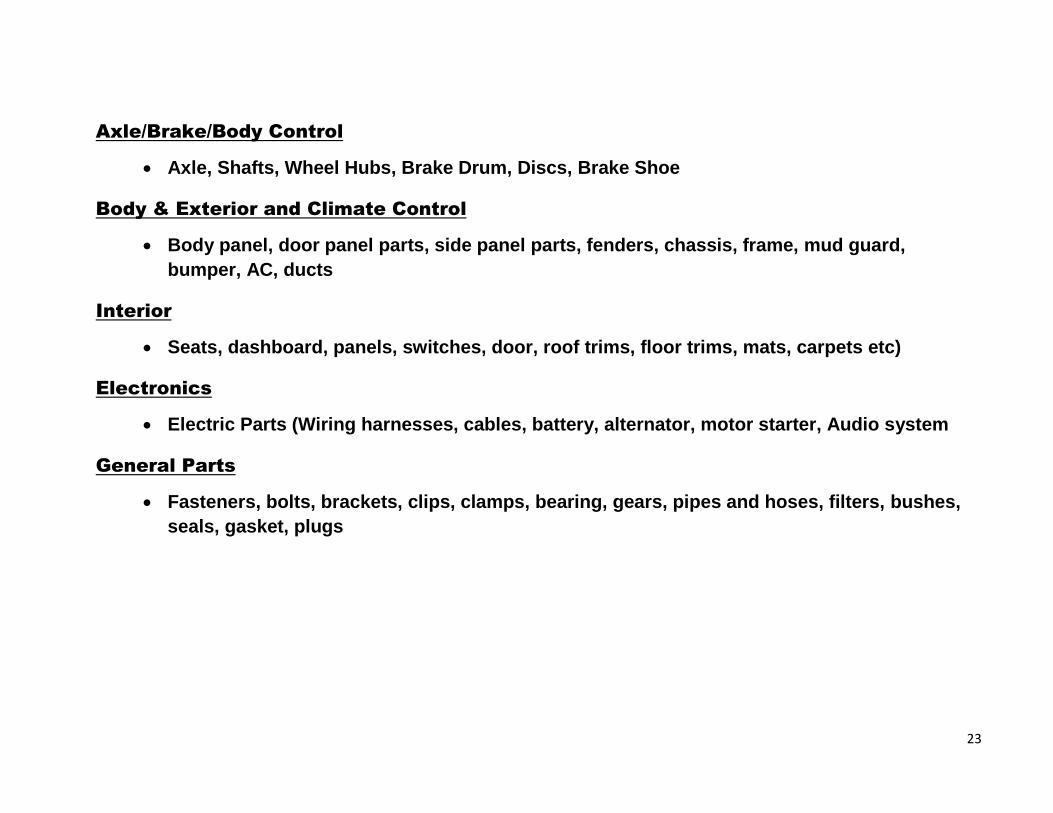

Axle/Brake/Body Control

Axle, Shafts, Wheel Hubs, Brake Drum, Discs, Brake Shoe

Body & Exterior and Climate Control

Body panel, door panel parts, side panel parts, fenders, chassis, frame, mud guard,

bumper, AC, ducts

Interior

Seats, dashboard, panels, switches, door, roof trims, floor trims, mats, carpets etc)

Electronics

Electric Parts (Wiring harnesses, cables, battery, alternator, motor starter, Audio system

General Parts

Fasteners, bolts, brackets, clips, clamps, bearing, gears, pipes and hoses, filters, bushes,

seals, gasket, plugs

24

Auto policies

In Pakistan auto sector is regulated through:

Tariff Based System (TBS) for Automotive Sector

Auto Industry Development Program (AIDP)

Tariff Based System (TBS) for Automotive Sector

As of July 1st 2006, the deletion programs for the Automotive Sector have

been replaced by the Tariff Based System (TBS) through following SRO’s

o [SRO 656 (I) / 2006 dated June 22, 2006 (For OEMs)]

o [SRO 693 (I) / 2006 dated July 1, 2006 (For OEMS)]

o [SRO 655(I) / 2006 dated June 22, 2006 (For Vendors)]

The basic framework of Tariff Based System is as under:

Imports in CKD condition would be allowed only to assemblers having adequate assembly facilities and registered as such by the concerned Federal Government Agency.

In Parts/ components indigenized by June 2004 have been placed at higher rate of Customs Duty i.e. 50% for cars

Parts not indigenized would be allowed at CKD rate of Custom Duty i.e. 32.5% for cars.

25

Auto Industry Development Program (AIDP)

Government has approved the long term auto policy (five year tariff plan for Cars/LCVs) on

January 2007 while the non-tariff incentive part of the policy comprises of technology

acquisition, Human Resource Development, Auto Cluster Development and new entrant

policy were approved by Government in November 2007.

Auto Industry Investment Policy (AIIP) under AIDP

Auto Industry Investment Policy (AIIP) Under AIDP facilitate new Entrant which mean a

potential assembler / manufacturer of global significance who had no assembly /

manufacturing of similar vehicles in Pakistan in the past and intends to assemble /

manufacture a vehicle by himself or through an agreement with a Pakistani company.

(AIDP is available at www.engineeringpakistan.com)

Benefits

New Entrants will be allowed to import 100% CKD kit, at the leviable customs duty

applicable to non localized parts, for a period of three years from the start of

assembly/manufacturing.

NOTE: Government is going to announce new auto policy soon which is expected to be more open

and investor friendly

26

New Entrant Policy for Motorcycle Industry with New Technology

The minimum investment for any New Entrant with new technology will be US$ 100 million

“New Technology” will be defined by the Engineering Development Board and would be

approved by the ECC on the recommendations of the Committee comprising

representatives from BOI, Ministry of Commerce and chaired by Secretary Industries.

The Committee shall also be empowered to decide on proposals relating to introduction of

new technologies by the existing manufacturers as well as the localization plans.

The new entrant shall have the incentive of importing localized CKD kit in any form at

custom duty leviable on non- localized CKD Kit (10%) in any form for a period of five years

subject to localization plan.

The additional Custom Duty leviable shall not be charged on sub-components and

components imported in any kit form.

The Concessions shall be withdrawn on parts localized by the new entrant each year, in

accordance to the approved localization plan.

At the start of commercial production by new entrants, localization level shall be kept at a

minimum of 25%.

By the end of five years, localization level shall reach a minimum of 85% at an average rate

of at least 15% per annum each for the subsequent four years.

27

Investment Opportunities in Auto Sector

Small Car Segment

As present Pakistan is having extremely low ratio of 16 cars / 1000 persons.

Low cars/1000 person ratio offers a huge potential for car sales in Pakistan

Government is focusing on bringing new investment in auto sector to increase competition

in the local market with the aim to enhance volumes by offering more incentives to new

investors under new entrant policy in the draft Automotive Development Policy.

The new investor package under new policy is at finalization stage

At present, the small cars segment in Pakistan is characterized by no competition (only Pak

Suzuki),

High prices, and quality issues.

As a result there is a huge potential for further investment to cater for existing and future

growing demand.

Pakistan is producing around 1.7 million motor cycles every year, while total number of

motorcycles on road has exceeded 20 million.

At least one percent of these motorcycle riders have the ability to graduate from bike to

small car every year.

This will lead to a potential of additional annual demand of 200,000 units of small cars a

year to be filled through new investors.

Pakistan offers huge opportunities for investment in small car segment of Pakistan.

28

Cars above 1800 CC

The Auto industry presently is manufacturing cars up to 1800 CC only

The demand for higher capacity cars is being met through imports of new and used cars.

New investment in this sector may fill the gap.

Tractor industry

At present, there are eight manufacturers operating in the sector out of which two players i.e. Al-Ghazi Tractor Ltd and Millat Tractors Ltd are dominating market with the market share of over 96%

Still there is a supply demand gap in high horse power segment of more than 85 HP and below 50 HP

Motorcycle industry

At present around 100 motorcycle manufacturers are operating in the country with an installed capacity of 3.19 million units.

Despite having large production capacity of Motorcycle in the country, still motorcycle sector needs to diversify its product range to:

o Higher CC segment such as 150 cc and above, o Automatic scooters and o Mopeds in future as well.

29

Investment Opportunities in Auto Parts Industry

o Around 45% of Auto parts are not made locally.

o Car sub-assemblies, assemblies, components are presently being imported.

D-8 countries can consider manufacturing of following parts and components

for OEMs in Pakistan.

o High-tech technology to manufacture certain critical components (engine gearing &

transmission parts) in Pakistan for local consumption and to supply to regional hubs.

o Brake discs and pads

o Brake lining

o Clutch discs and clutch assemblies/facings

o Spark plugs

o Halogen lamps

o Shock absorbers

o Sheet metal and plastic parts etc

Market size is sufficient for establishment of units for local manufacturing of aforesaid parts and components i.e. for both OEMs and the aftermarket.

30

DISCLAMER

This information package aims at enabling the investors to make a preliminary

assessment and information contained in this publication is for information

purposes only. All the material included in this document is based on

data/information gathered from various sources. Although, due care and diligence

has been taken to compile this document, however, the contained information may

vary and it should not be relied upon as such. Investors are expected to make their

own investment decisions

31