August 26, 1961 Public Finance, Economic Growth and Redistribution of … · August 26, 1961 Public...

6

August 26, 1961 Public Finance, Economic Growth and Redistribution of Income in India (1951-52 to 1960-61) V K R V Rao Public finance plays an important role in the promotion of economic growth by the transfer of income that, it effects from the private sector to the public sector, the incidence of such transfer and the objec- tives on which such transferred income is employed. The following note is a preliminary attempt at looking at India's experience during the first decade of our planning from this angle. The general conclusion that emerges is that the redistribution of income effected by taxation was not such as to discourage either individual investment or enterprise. Moreover, income transferred to the public sector was increasingly used to finance economic and social overheads which, in turn, increased the opportunities for investment, enterprise and earnings in the private sector. [The note is based on a paper read by the author at the Seventh General Conference of the Inter- national Association for Research in Income and Wealth, held at Tutzing, Germany, from August 4 to 10, 196i:| NO comprehensive study has been made so far of the structure of income distribution in India- The only data relating to distribution are the income-tax statistics, but these deal only with non-agricultural income and cover only a small pro portion of the total working force. No similar statistics are available either for agricultural income or for the non-agricultural income not sub- ject to income-tax. Data of a sug- gestive character, which could be used for making a rough estimate of distribution by broad categories, is available in a miscellaneous col- lection of official documents and reports as well as some non-official surveys, but these have not yet been brought together and processed for the purpose. In any case, even this miscellaneous data does not give scope for making a study of changes in the distribution of in- come over time; and it is practi- cally impossible to establish quanti- tative estimates of any redistribu- tion effected through public finance covering all income categories. The only statistics of distribution by income ranges available over time is that given by the income tax data; and it is in respect of these that it is possible to look at the effect of taxation on redistri- bution. All other references to the * The writer of this paper is engaged at present in making such a study and hopes to present his prelimi- nary estimates of the distribution of income in India by the end of 1961. redistributive effect of public finance will have to be in general terms and cannot be given a quantitative content in terms of income ranges* Rise in Developmental Expenditure Table 1 gives the figures of the total tax revenues raised by the Centra) and State governments during the last ten years and the proportion they constituted of the national income during that period. It will be seen from the Table that there has been a significant rise in the absolute amount of income transferred from the private to the public sector. There has also been a noticeable rise in the proportion of the national income taken by taxation, though this is far below (he corresponding figures for the developed economics. That this re- distribution of income between the public and private sector has been used for the promotion of economic growth is seen from Table 2, which gives the figures of Central and Stale expenditure during the last ten years classified under develop- mental and non-developmental ex- penditure. Expenditure on developmental and social services, which means all public expenditure of a recurring kind incurred on social and econo- mic overheads (and, of course, ex- cludes the much larger volume of capital expenditure) rose steadily from 30.8 per cent of total public expenditure during the first year of the First Five Year Plan period to 41.1- per cent during the last year of the Second Five Year Plan period These ten years also saw a rise in the proportion of national income used for such public ex- penditure from 2.4 per cent to 5.7 per m i l . The increase in the abso- lute figures of this expenditure was as much as 246 per cent. While it is a matter for satisfac- tion that public expenditure during the period showed this decisive trend towards an increase in the share THE ECONOMIC WEEKLY

Transcript of August 26, 1961 Public Finance, Economic Growth and Redistribution of … · August 26, 1961 Public...

August 26 , 1961

Public Finance, Economic Growth and Redistribution of Income in India

(1951-52 to 1960-61) V K R V Rao

Public finance plays an important role in the promotion of economic growth by the transfer of income that, it effects from the private sector to the public sector, the incidence of such transfer and the objectives on which such transferred income is employed.

The following note is a preliminary attempt at looking at India's experience during the first decade of our planning from this angle.

The general conclusion that emerges is that the redistribution of income effected by taxation was not such as to discourage either individual investment or enterprise.

Moreover, income transferred to the public sector was increasingly used to finance economic and social overheads which, in turn, increased the opportunities for investment, enterprise and earnings in the private sector.

[The note is based on a paper read by the author at the Seventh General Conference of the Inter-national Association for Research in Income and Wealth, held at Tutzing, Germany, from August 4 to 10, 196i : |

NO comprehensive study has been made so far of the structure of

income d i s t r ibu t ion in India- The o n l y data relat ing to d i s t r i bu t ion are the income-tax statistics, but these deal only w i t h non-agr icul tura l income and cover only a small p r o po r t ion of the total w o r k i n g force. No s imi l a r statistics are available either for ag r icu l tu ra l income or for the non-agricul tural income not subject to income-tax. Data of a suggestive character, wh ich could be used for m a k i n g a rough estimate of d i s t r ibu t ion by broad categories, is avai lable in a miscellaneous collection of official documents and reports as we l l as some non-official surveys, but these have not yet been brought together and processed for the purpose. In any case, even this miscellaneous data does not give scope for mak ing a study of changes in the d i s t r ibu t ion of income over t i m e ; and it is prac t i cally impossible to establish quant itative estimates of any redis t r ibut ion effected through publ ic finance covering a l l income categories. The on ly statistics of d i s t r ibu t ion by income ranges available over t ime is that given by the income tax data; and it is in respect of these that i t is possible to look at the effect of taxat ion on redistr i bu t ion . All other references to the

* The writer of this paper is engaged at present in making such a study and hopes to present his preliminary estimates of the distribution of income in India by the end of 1961.

redis t r ibut ive effect of publ ic finance w i l l have to be in general terms and cannot be given a quanti ta t ive content in terms of income ranges*

Rise in Developmental Expenditure Table 1 gives the figures of the

total tax revenues raised by the Centra) and State governments d u r i n g the last ten years and the p ropor t ion they constituted of the nat ional income d u r i n g tha t per iod . I t w i l l be seen f rom the Table that there has been a significant rise in the absolute amount of income transferred f rom the private to the publ ic sector. There has also been a noticeable rise in the p ropor t ion of the national income taken by taxat ion, though this is far below (he corresponding figures for the developed economics. That this red i s t r ibu t ion of income between the pub l ic and private sector has been used for the promot ion of economic g rowth is seen f rom Table 2, which gives the figures of Central and Stale expenditure du r ing the last

ten years classified under developmental and non-developmental expendi ture .

Expendi ture on developmental and social services, wh ich means a l l publ ic expenditure of a r ecu r r ing k i n d incur red on social and economic overheads (and, of course, excludes the much larger volume of capi ta l expendi ture) rose steadily f rom 30.8 per cent of total pub l i c expenditure d u r i n g the f i rs t year of the First Five Year Plan per iod to 41.1- per cent d u r i n g the last year of the Second Five Year P lan period These ten years also saw a rise in the p ropor t ion of nat ional income used for such publ ic expenditure f rom 2.4 per cent to 5.7 per m i l . The increase in the absolute figures of this expenditure was as much as 246 per cent.

Whi le it is a matter for satisfact ion that publ ic expendi ture d u r i n g the per iod showed this decisive t rend towards an increase in the share

THE ECONOMIC WEEKLY

August 26, 1961 T H E E C O N O M I C W E E K L Y

going to developmental and social services, i ts effect on red is t r i bu t ion of personal incomes also tu rns on the nature of the taxat ion raised to f inance th is expendi ture . Tab le 3 summarises the pos i t ion f o r the f i rs t and last years of the ten year pe r iod .

The Tab le reveals a decl ine in the impor tance of d i rect taxat i on and an increase in that o f in -d i rec t taxat ion. As taxes on income and proper ty const i tute the real ly progressive element in pub l i c f inance, i t appears that the t ransfer of income f r o m the pr iva te to the pub l i c sector has been more at the expense of the consumpt ion of the poor than that of the well- to-do. I t is t rue that taxes on commodit ies and services also conta in an element of progression in so far as they f a l l on l u x u r y consumpt ion, but this does not upset the conclusion that wh i le the bulk of the incidence of commodi ty taxat ion has been on the real surplus of the well-to-do classes, in the case of masses, it has been at the cost of their basic consumpt ion . In any case, res t r ic t ion on the consumpt ion of the poor has been p l a y i n g an impor tan t role in the f inanc ing of the social and economic overheads created by the state d u r i n g the ten years of p l ann ing .

The dec l in ing importance of d i rect taxat ion in the f inancing of pub l i c expendi ture on economic development is borne out even more clearly when We look at the g rowth of the income assessed to income tax and compare i t w i t h the g rowth of the d i rect taxes pa id by them, both as a p ropo r t i on of nat ional income (See Table 4 ) . Income assessed to income tax has grown as a propor t ion of nat ional i ncome; but the income tax i t pays has actual ly decl ined as a proport i on of nat ional income. Th i s conclusion is not upset even if we take into account the new direct taxe9 on income and p roper ty levied ma in l y d u r i n g the Second P l a n per iod . (See Table 5)

The highest y ie ld of these new taxes is in 1959-60, when i t comes to 0.13 per cent of the nat iona l income of that year A d d i n g this to the p ropor t i on of nat ional i n come pa id ad income tax, the f igure comes to 1.92 per cent wh i ch is s t i l l below the percentage reached in the f i rs t two years of the Plan pe r i od . At best, we can say that t he to ta l o f i l l d i rect taxes as a

THE ECONOMIC WEEKLY August 26, 1961

1375

Augus t 26, 1961 T H E E C O N O M I C W E E K L Y

August 26, 1961

p r o p o r t i o n o f na t ional income pa id by those whose incomes are assessed to income tax is stat ionary over the ten year per iod , w h i l e the propor-t i o n of national income received by th is class has been r i s ing . Th i s is perhaps in l ine w i t h the econo-mies of g rowth , though i t is doubtf u l i f i t i s equally consistent w i t h the social objectives of p l ann ing .

Agricultural Incomes

Incomes assessed to income tax cover only non-agricul tural i n comes. A g r i c u l t u r a l incomes are not subject to income tax or any of the direct taxes imposed by the Centre. They are subject to land revenue w h i c h is levied most ly on a flat rate on land, subject to differences in p r o d u c t i v i t y per acre, whi le the higher incomes among them pay an ag r i cu l tu ra l income tax tha t has a m i l d degree of progression, i t is difficult to compare the incidence of d i rec t taxes on comparable levels of ag r icu l tu ra l and non-agr icul tura l income. But f rom cer ta in rough calculations that I have been able to make, it is my guess that agr icu l tura l households w i t h incomes exceeding Rs 2500 a year were pay ing by way of direct taxes ( i n c l u d i n g both land revenue and a g r i c u l t u r a l income tax) about 5 per cent of thei r income, whereas other households w i t h non-agricultu ra l income exceeding Rs 3000 a year were pay ing about 11 per cent of their income as direct taxes. It is also l i ke ly that the income of this better-off ag r i cu l tu ra l class has been increasing d u r i n g the last ten years as a p r o p o r t i o n of total agr icu l tu ra l income. W h a t seems clear is that the better-off among the agr icu l tu ra l classes are not m a k i n g a p ropor tionate con t r ibu t ion to the financing of publ ic expendi ture on social and economic overheads anywhere comparable to that wh ich is being made by the corresponding income ranges in the non-agr icul tura l sector. M a y be this is a factor opera t ing in the p r o m o t i o n o f economic growth in the agr icu l tu ra l sector, but it does raise grave question of equity in incidence of taxat ion between different sections of the communi ty .

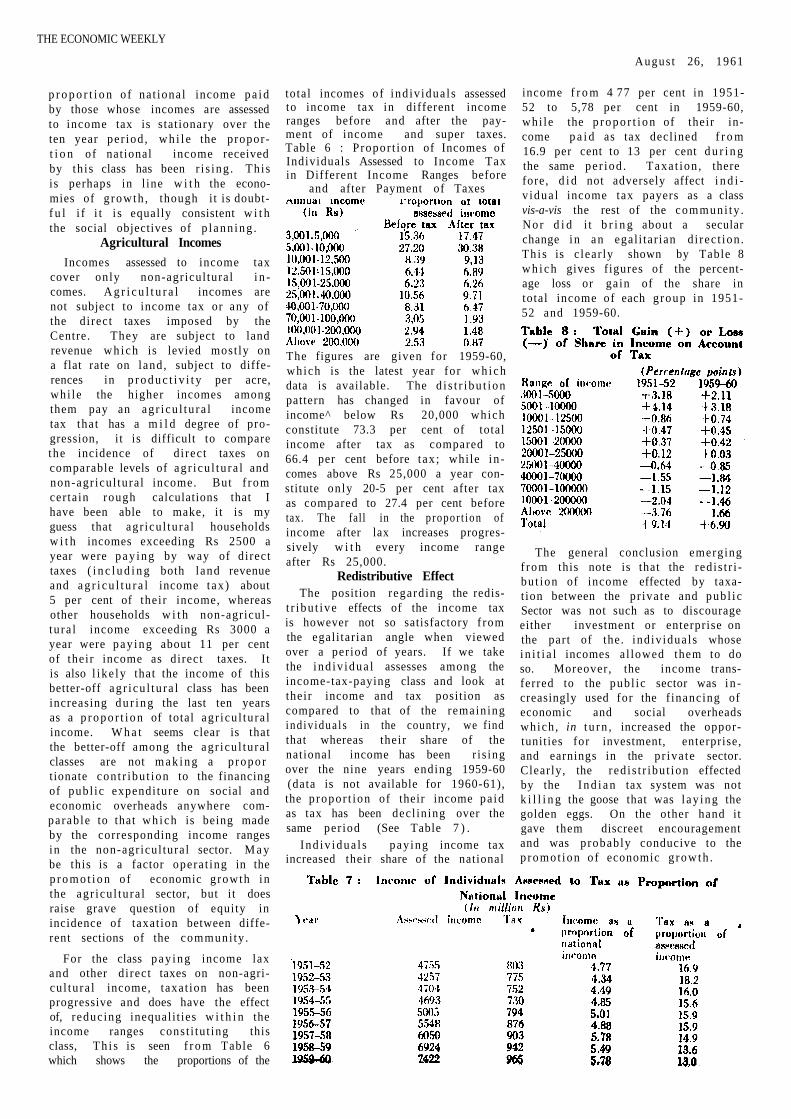

For the class pay ing income lax and other di rect taxes on non-agricu l tura l income, taxat ion has been progressive and does have the effect of, reducing inequali t ies w i t h i n the income ranges const i tu t ing this class, T h i s is seen f r o m Table 6 which shows the proportions of the

The figures are given for 1959-60, which is the latest year for wh ich data is available. The d i s t r i bu t ion pattern has changed in favour of income^ below Rs 20,000 which constitute 73.3 per cent of total income after tax as compared to 66.4 per cent before tax ; while i n comes above Rs 25,000 a year constitute only 20-5 per cent after tax as compared to 27.4 per cent before tax. The fall in the p ropor t ion of income after lax increases progressively w i t h every income range after Rs 25,000.

Redistributive Effect The position regarding the redis-

t r i bu t ive effects of the income tax is however not so satisfactory f rom the egali tar ian angle when viewed over a period of years. If we take the i nd iv idua l assesses among the income-tax-paying class and look at their income and tax posit ion as compared to that of the remaining ind iv idua l s in the country, we find that whereas their share of the national income has been r is ing over the nine years ending 1959-60 (data is not available for 1960-61), the p ropor t ion of their income pa id as tax has been decl ining over the same per iod (See Table 7 ) .

I nd iv idua l s pay ing income tax increased their share of the national

THE ECONOMIC WEEKLY

The general conclusion emerging f rom this note is that the red is t r i -bu t ion of income effected by taxat ion between the pr ivate and pub l i c Sector was not such as to discourage either investment or enterprise on the part of the. ind iv idua ls whose i n i t i a l incomes a l lowed them to do so. Moreover, the income transferred to the publ ic sector was i n creasingly used for the f inancing of economic and social overheads which , in t u r n , increased the opportunities for investment, enterprise, and earnings in the p r iva te sector. Clearly, the red i s t r ibu t ion effected by the I n d i a n tax system was not k i l l i n g the goose that was l ay ing the golden eggs. On the other hand it gave them discreet encouragement and was probably conducive to the p romot ion of economic g rowth .

total incomes o f ind iv idua l s assessed to income tax in different income ranges before and after the payment of income and super taxes. Table 6 : Propor t ion of Incomes of Individuals Assessed to Income Tax in Different Income Ranges before

and after Payment of Taxes

income f r o m 4 77 per cent in 1951-52 to 5,78 per cent in 1959-60, whi le the p r o p o r t i o n of their in-come p a i d as tax declined f r o m 16.9 per cent to 13 per cent d u r i n g the same pe r iod . Taxa t ion , there fore, d i d not adversely affect i n d i v idua l income tax payers as a class vis-a-vis the rest of the communi ty . Nor d i d i t b r i n g about a secular change in an egal i tar ian d i rec t ion . Th i s is c lear ly shown by Table 8 w h i c h gives figures of the percentage loss or gain of the share in total income of each g roup in 1951-52 and 1959-60.

Augus t 26, 1 9 6 1

THE ECONOMIC WEEKLY

![INCOME-TAX ACT, 1961€¦ · INCOME-TAX ACT, 1961 * [43 OF 1961] [AS AMENDED BY FINANCE ACT, 2008] An Act to consolidate and amend the law relating to income-tax and super-tax BE](https://static.fdocuments.us/doc/165x107/6097f37f4534cb51153b4a4c/income-tax-act-1961-income-tax-act-1961-43-of-1961-as-amended-by-finance.jpg)