Auditing construction contract change orders - Baker · PDF fileAuditing construction contract...

36

Auditing construction contract change orders Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

Transcript of Auditing construction contract change orders - Baker · PDF fileAuditing construction contract...

Auditing construction contract change orders

Baker Tilly refers to Baker Tilly Virchow Krause, LLP,an independently owned and managed member of Baker Tilly International.

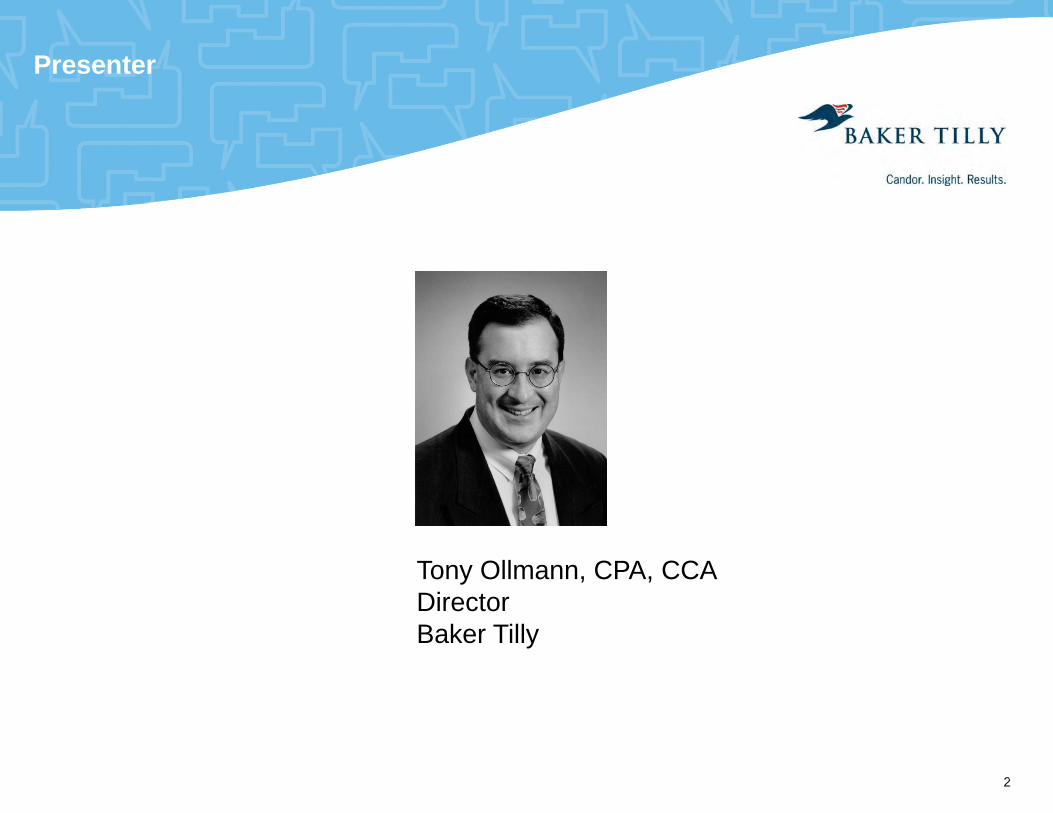

Presenter

Tony Ollmann, CPA, CCADirectorDirectorBaker Tilly

22

Auditing construction contract change orders

Baker Tilly refers to Baker Tilly Virchow Krause, LLP,an independently owned and managed member of Baker Tilly International. © 2013 Baker Tilly Virchow Krause, LLP

About Baker Tilly

> Established in 1931> One of the top 20 largest accounting and> One of the top 20 largest accounting and

advisory firms in the United States according to Accounting Today’s 2013 list of “Top 100 Firms”

> More than 1,400 professionals> Baker Tilly Virchow Krause, LLP is the largest

US Baker Tilly International independentUS Baker Tilly International independent member firm

> Baker Tilly International is the eighth largest public accounting network with representationpublic accounting network with representation in more than 131 countries

> Convenient, seamless resource for worldwide needs

4

needs

4

About Baker Tilly

From concept and funding to controls and compliance, Baker Tilly has more than 250 dedicated construction and real estate industry professionals to assist with your facility development

j t th h ll t f th d l t lif lproject through all stages of the development lifecycle.

55

Overview

Today’s topics: What are change orders?

Auditing construction contract change orders

Audit risks

Change order red flags

Change order testing

Case studies

6

Learning objectives

> Learn how to identify change orders> Learn how to decompose a change order> Determine the underlying change order driver> Understand the risk associated with different types of change orders> Develop strategies for auditing change orders and managing

construction professionals

7

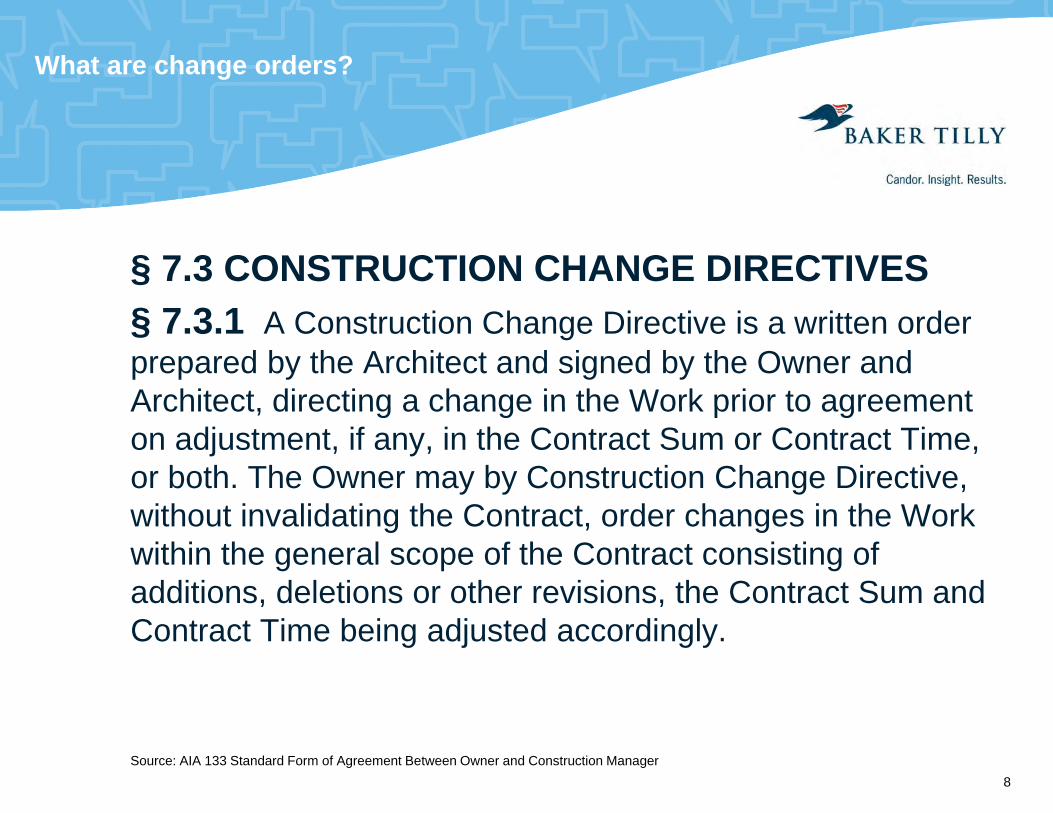

What are change orders?

§ 7.3 CONSTRUCTION CHANGE DIRECTIVES§ 7.3.1 A Construction Change Directive is a written order prepared by the Architect and signed by the Owner and Architect directing a change in the Work prior to agreementArchitect, directing a change in the Work prior to agreement on adjustment, if any, in the Contract Sum or Contract Time, or both. The Owner may by Construction Change Directive,

ith t i lid ti th C t t d h i th W kwithout invalidating the Contract, order changes in the Work within the general scope of the Contract consisting of additions, deletions or other revisions, the Contract Sum and Contract Time being adjusted accordingly.

Source: AIA 133 Standard Form of Agreement Between Owner and Construction Manager8

What are change orders?

Change orders are referred to in a number of ways:> Ch d> Change orders> Change directives> RFI> Engineering change notice> Field change request

All amount to the same thing an owner’sAll amount to the same thing, an owner s authorization to change the terms of the prevailing contract

9

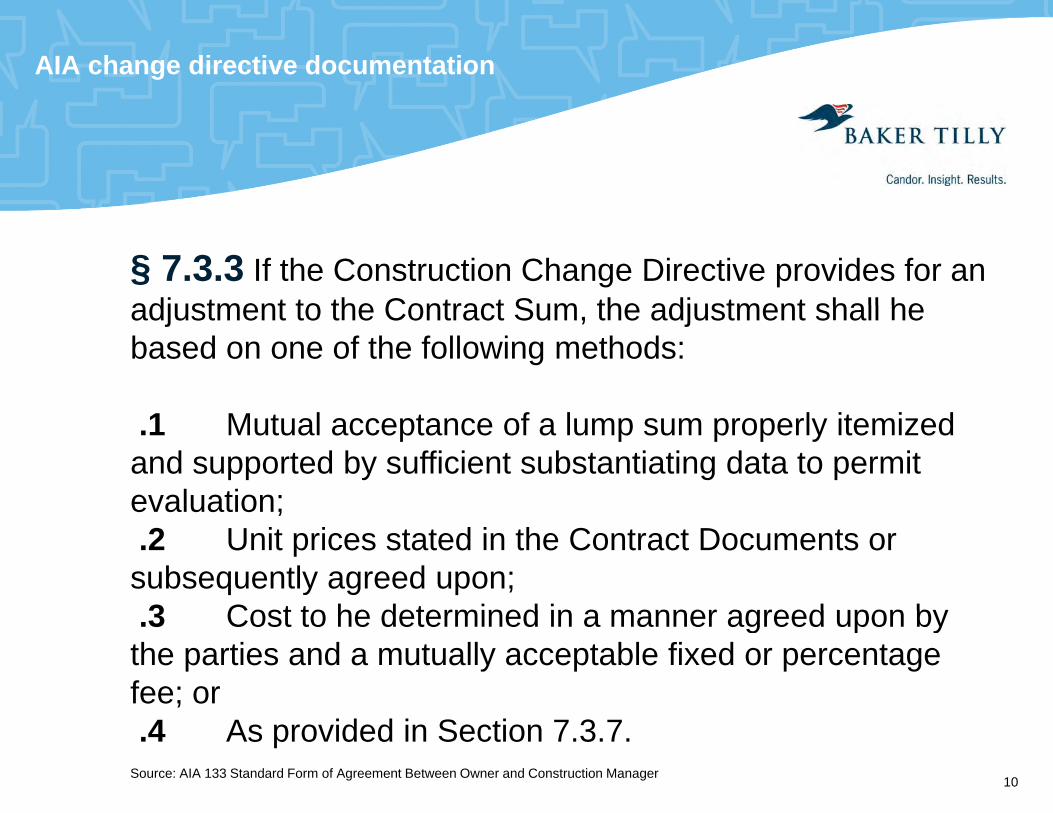

AIA change directive documentation

§ 7.3.3 If the Construction Change Directive provides for an adjustment to the Contract Sum the adjustment shall headjustment to the Contract Sum, the adjustment shall he based on one of the following methods:

.1 Mutual acceptance of a lump sum properly itemized and supported by sufficient substantiating data to permit evaluation;evaluation;.2 Unit prices stated in the Contract Documents or subsequently agreed upon;3 Cost to he determined in a manner agreed upon by.3 Cost to he determined in a manner agreed upon by

the parties and a mutually acceptable fixed or percentage fee; or.4 As provided in Section 7.3.7.

Source: AIA 133 Standard Form of Agreement Between Owner and Construction Manager 10

Why do change orders occur?

> Owner initiated change to the project> Contingency expenditureg y p> Change in construction conditions> Change in specifications> Change in building code> Change in building code> Change in market conditions

11

Change in specifications

Due to completion of construction documents, h i b ildi d fi d t i lchanges in building code or refined materials

specifications additional labor and materials are required to deliver the scope of workare required to deliver the scope of work

Resulting from:Resulting from:> Bids based on incomplete construction documents> Regulatory design review demands design changes> Equipment specified is modified or changed

12

Change in market conditions

The cost of procuring construction services, li d i t t i ll diff tsupplies and equipment are materially different

than the estimated costs

Resulting from:> Dramatic material shortages> Dramatic material shortages> Labor shortages> Commodity price speculation

13

Change in field conditions

Construction conditions are not what was t d t d t th t texpected or reported to the contractors

M i l dMay include:> Unusually inclement or adverse weather> Unreported soil conditionsp> Environmental hazards

14

Owner initiated change orders

Represent new or additional work not planned f i th ti t dfor in the estimated scope

M lt iMay result in:> Increase to the GMP> Change to the construction scheduleg> Use of contractor’s contingency budget> Use of owner’s contingency budget> Reduction to another part of the project budget> Reduction to another part of the project budget

15

Change order audit risks

Audit risk categories> U th i d h d> Unauthorized change orders> Unnecessary change orders> Redundant or duplicate change orders> Overpriced change orders

16

Unauthorized change orders

Work that is performed and charged for without h i b th i d b thhaving been authorized by the owner

Wh d thi h ?Why does this happen?> Miscommunication> Procrastination> Budget overruns> Schedule delays> Rework> Rework> Warranty work> Quality issues

17

Unnecessary change orders

Change orders that have been properly d b t d li t l t thapproved but deliver no apparent value to the

project

Resulting from > Existing scope> Existing scope> Unnecessary add on

18

Overpriced change orders

Change orders that have been approved but i d f th f k dare overpriced for the scope of work proposed

O i i fOverpricing comes from:> Inflated labor rates> Inflated hours> Exaggerated profit margins> Compounded fee computation (fee on fee)

19

Contingency budgets and allowances

Contractors contingency: Contractor’s budget f i b d t hfor in scope budget changes

O ’ ti O ’ b d t fOwner’s contingency: Owner’s budget for scope changes

Allowances: Segregated construction budget dedicated for a specific use that may not havededicated for a specific use that may not have a budget and contract or GMP time.

20

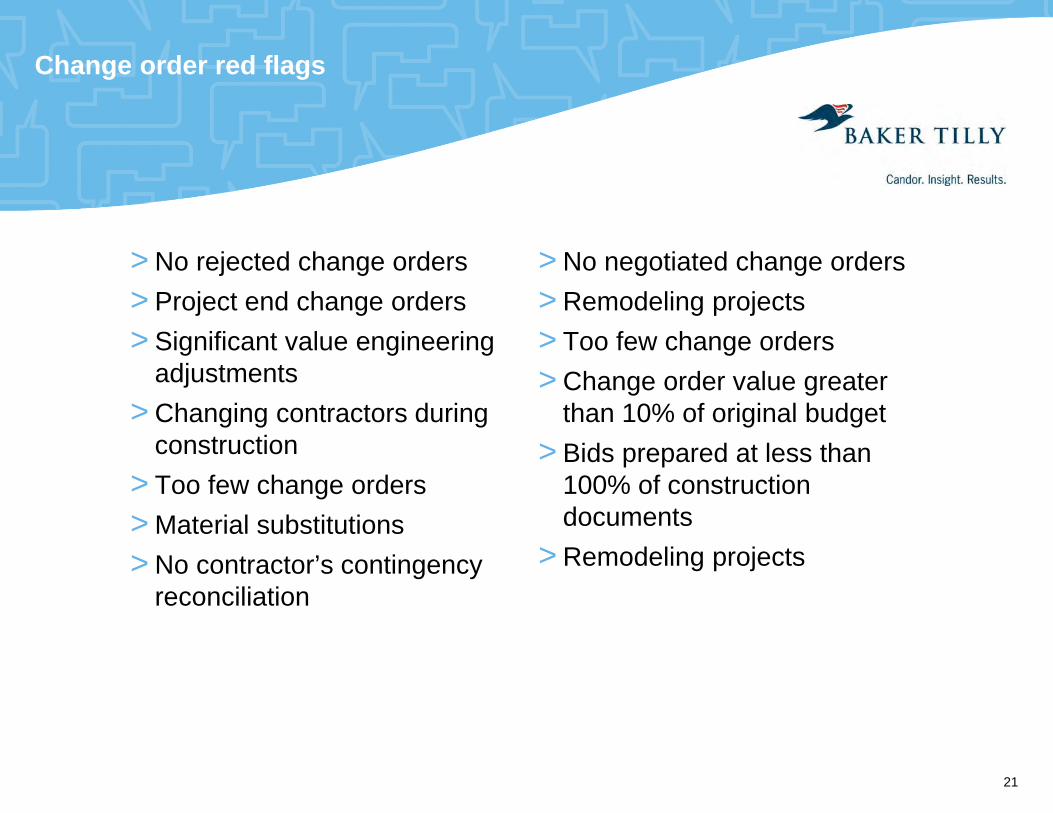

Change order red flags

> No rejected change orders> Project end change orders

> No negotiated change orders> Remodeling projects> Project end change orders

> Significant value engineering adjustments

> Ch i t t d i

> Remodeling projects> Too few change orders> Change order value greater

th 10% f i i l b d t> Changing contractors during construction

> Too few change orders

than 10% of original budget> Bids prepared at less than

100% of construction d t> Material substitutions

> No contractor’s contingency reconciliation

documents> Remodeling projects

21

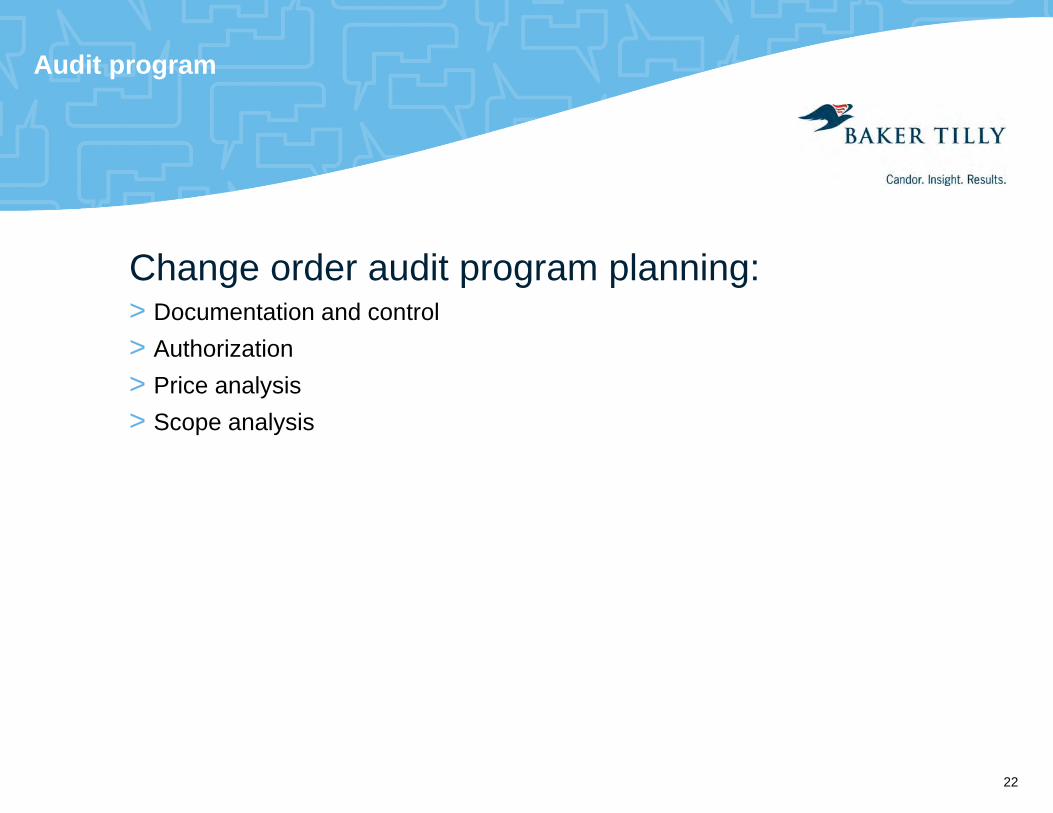

Audit program

Change order audit program planning:> D t ti d t l> Documentation and control> Authorization> Price analysis> Scope analysis

22

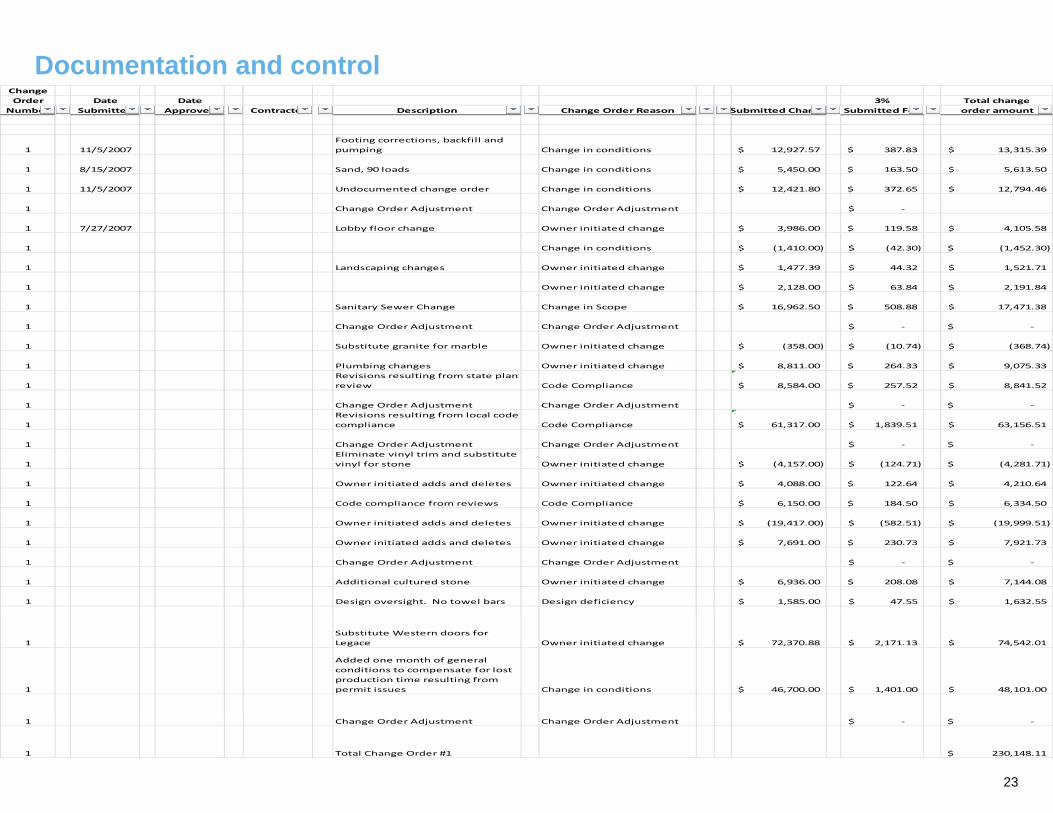

Documentation and controlChangeOrder Date Date 3% Total changeOrder Date Date 3% Total change

Number Submitted Approved Contractor Description Change Order Reason Submitted Change Submitted Fee order amount

1 11/5/2007Footing corrections, backfill and pumping Change in conditions 12,927.57$ 387.83$ 13,315.39$

1 8/15/2007 Sand, 90 loads Change in conditions 5,450.00$ 163.50$ 5,613.50$

1 11/5/2007 Undocumented change order Change in conditions 12,421.80$ 372.65$ 12,794.46$

1 Change Order Adjustment Change Order Adjustment ‐$

1 7/27/2007 Lobby floor change Owner initiated change 3,986.00$ 119.58$ 4,105.58$

1 Change in conditions (1,410.00)$ (42.30)$ (1,452.30)$

1 Landscaping changes Owner initiated change 1,477.39$ 44.32$ 1,521.71$

1 Owner initiated change 2,128.00$ 63.84$ 2,191.84$

1 S it S Ch Ch i S 16 962 50$ 508 88$ 17 471 38$1 Sanitary Sewer Change Change in Scope 16,962.50$ 508.88$ 17,471.38$

1 Change Order Adjustment Change Order Adjustment ‐$ ‐$

1 Substitute granite for marble Owner initiated change (358.00)$ (10.74)$ (368.74)$

1 Plumbing changes Owner initiated change 8,811.00$ 264.33$ 9,075.33$

1Revisions resulting from state plan review Code Compliance 8,584.00$ 257.52$ 8,841.52$

1 Change Order Adjustment Change Order Adjustment ‐$ ‐$1 Change Order Adjustment Change Order Adjustment $ $

1Revisions resulting from local code compliance Code Compliance 61,317.00$ 1,839.51$ 63,156.51$

1 Change Order Adjustment Change Order Adjustment ‐$ ‐$

1Eliminate vinyl trim and substitute vinyl for stone Owner initiated change (4,157.00)$ (124.71)$ (4,281.71)$

1 Owner initiated adds and deletes Owner initiated change 4,088.00$ 122.64$ 4,210.64$

1 Code compliance from reviews Code Compliance 6,150.00$ 184.50$ 6,334.50$

1 Owner initiated adds and deletes Owner initiated change (19,417.00)$ (582.51)$ (19,999.51)$

1 Owner initiated adds and deletes Owner initiated change 7,691.00$ 230.73$ 7,921.73$

1 Change Order Adjustment Change Order Adjustment ‐$ ‐$

1 Additional cultured stone Owner initiated change 6,936.00$ 208.08$ 7,144.08$

1 Design oversight. No towel bars Design deficiency 1,585.00$ 47.55$ 1,632.55$

1Substitute Western doors for Legace Owner initiated change 72,370.88$ 2,171.13$ 74,542.01$

1

Added one month of general conditions to compensate for lost production time resulting from permit issues Change in conditions 46,700.00$ 1,401.00$ 48,101.00$

1 Change Order Adjustment Change Order Adjustment ‐$ ‐$

1 Total Change Order #1 230,148.11$

23

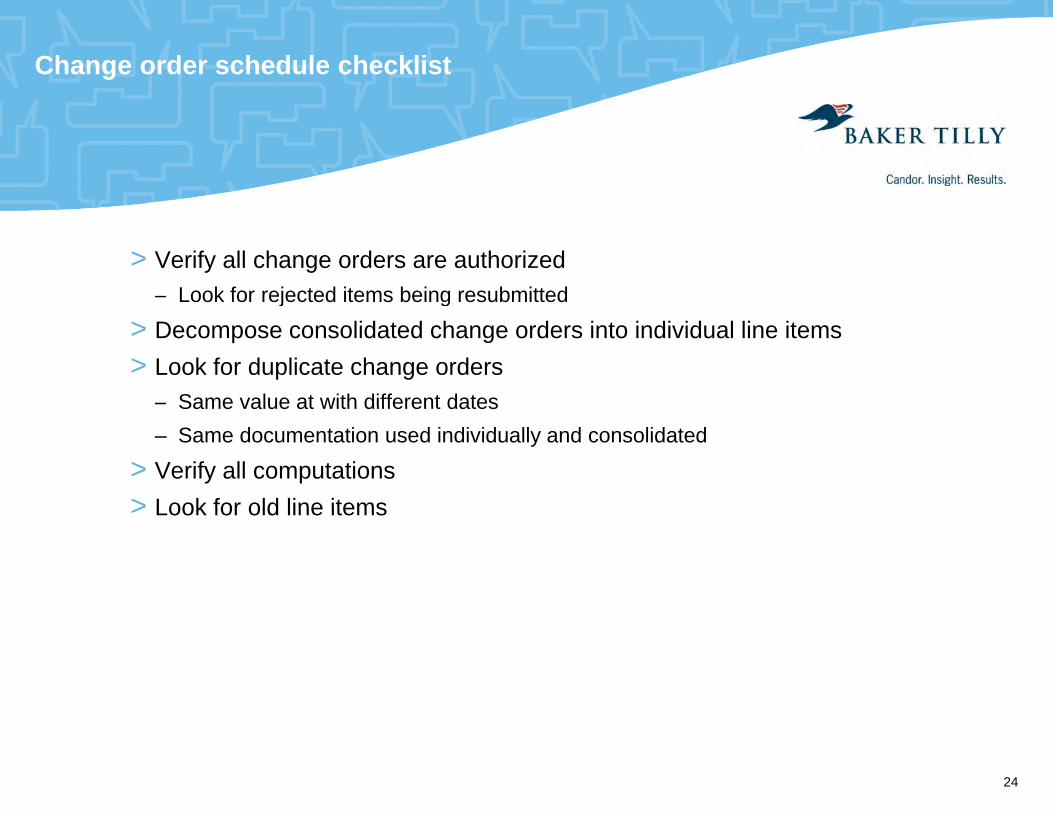

Change order schedule checklist

> Verify all change orders are authorized– Look for rejected items being resubmittedj g

> Decompose consolidated change orders into individual line items> Look for duplicate change orders

– Same value at with different datesSame value at with different dates– Same documentation used individually and consolidated

> Verify all computations> Look for old line items> Look for old line items

24

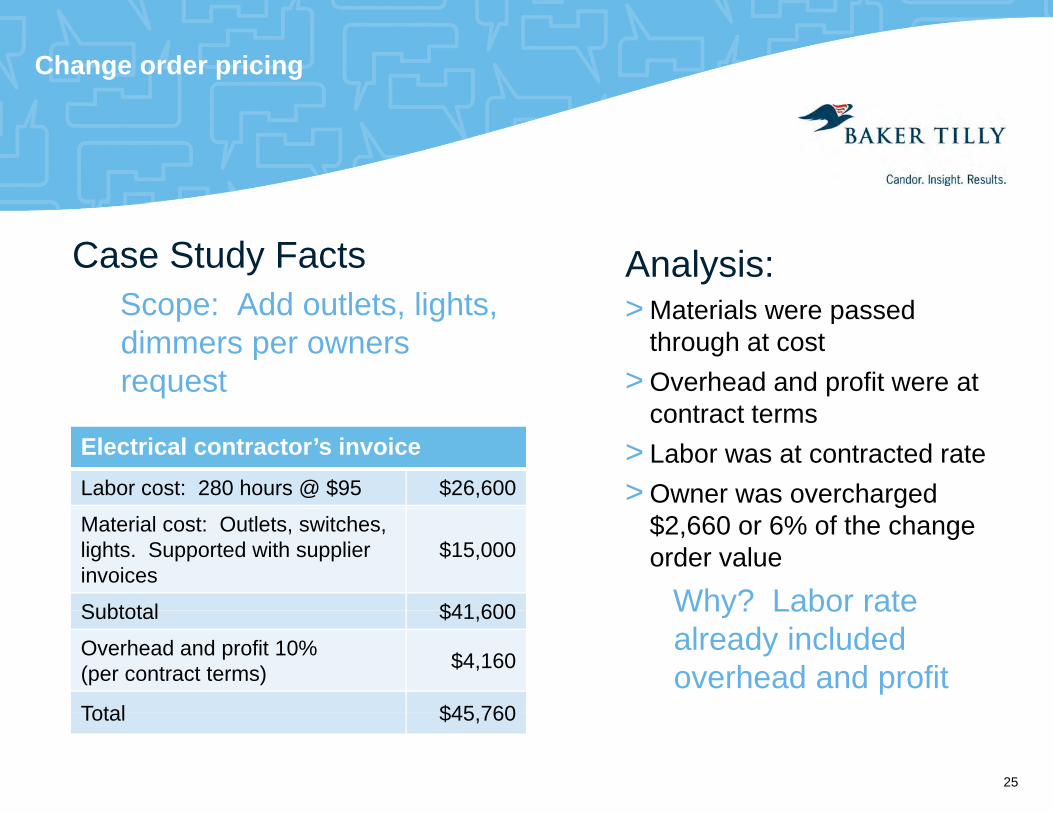

Change order pricing

Case Study FactsScope: Add outlets lights

Analysis:> Materials ere passedScope: Add outlets, lights,

dimmers per owners request

> Materials were passed through at cost

> Overhead and profit were at t t tcontract terms

> Labor was at contracted rate> Owner was overcharged

Electrical contractor’s invoiceLabor cost: 280 hours @ $95 $26,600

$2,660 or 6% of the change order value

Why? Labor rate

Material cost: Outlets, switches, lights. Supported with supplier invoices

$15,000

Subtotal $41 600 Why? Labor rate already included overhead and profit

Subtotal $41,600

Overhead and profit 10%(per contract terms) $4,160

Total $45 760Total $45,760

25

Change order pricing audit checklist

> Request detail backup for lump sum change orders Resources

> TRA SER> Verify labor rates with base contract > Verify hours are appropriate for

scope of work> Verify quantities are appropriate for

> TRA-SER> Equipment Watch> Composite crew rate > Verify quantities are appropriate for

scope of work> OCIP projects make sure to

discount labor rates for owner paid

panalysis

> RS Means> Labor burden analysisworkers compensation insurance

> Negative change orders should include a CM fee credit

> Verify that general conditions

> Labor burden analysis

> Verify that general conditions changed before accepting a GC fee adjustment

26

Polling question #4

AA. Average crew billing rateB. Weighted average crew

billing rate

What is a composite crew rate?

Pl d i th lli ti i th W bE t th i htPlease respond using the polling section in the WebEx screen to the right.

27

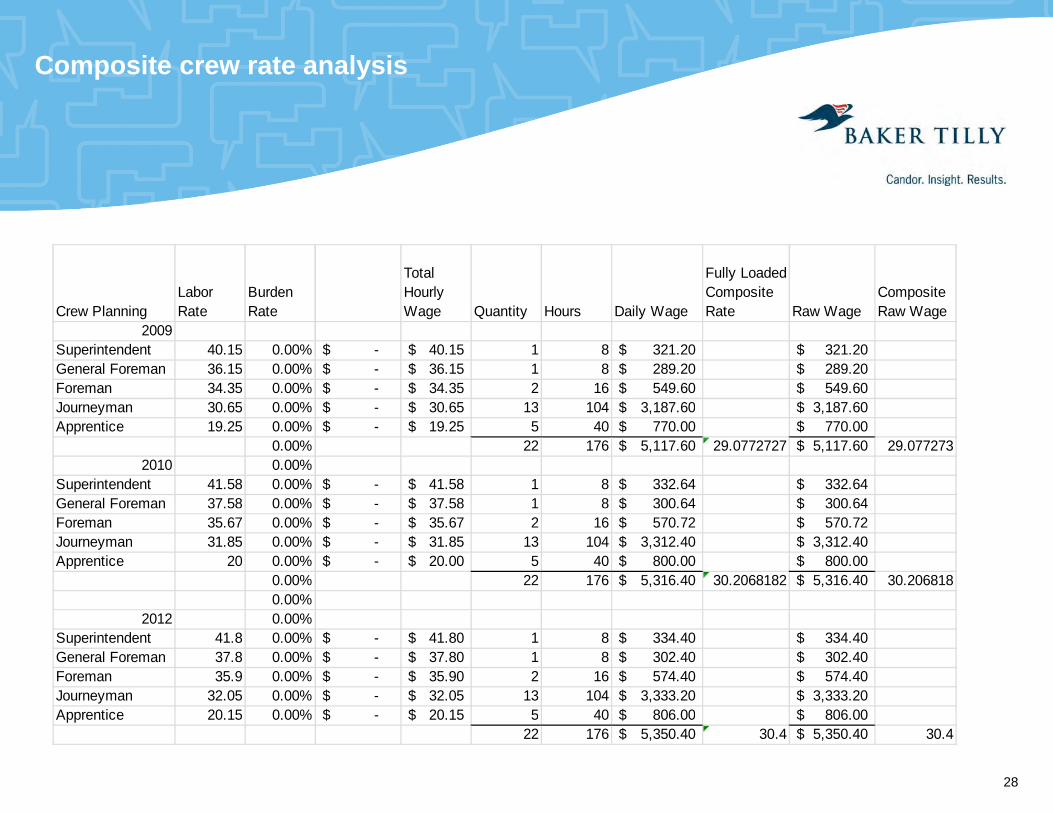

Composite crew rate analysis

Labor Burden Total Hourly

Fully Loaded Composite Composite

Crew Planning Rate Rate Wage Quantity Hours Daily Wage Rate Raw Wage Raw Wage2009

Superintendent 40.15 0.00% -$ 40.15$ 1 8 321.20$ 321.20$ General Foreman 36.15 0.00% -$ 36.15$ 1 8 289.20$ 289.20$ Foreman 34.35 0.00% -$ 34.35$ 2 16 549.60$ 549.60$ Journeyman 30 65 0 00% $ 30 65$ 13 104 3 187 60$ 3 187 60$Journeyman 30.65 0.00% -$ 30.65$ 13 104 3,187.60$ 3,187.60$ Apprentice 19.25 0.00% -$ 19.25$ 5 40 770.00$ 770.00$

0.00% 22 176 5,117.60$ 29.0772727 5,117.60$ 29.0772732010 0.00%

Superintendent 41.58 0.00% -$ 41.58$ 1 8 332.64$ 332.64$ General Foreman 37.58 0.00% -$ 37.58$ 1 8 300.64$ 300.64$ $ $ $ $Foreman 35.67 0.00% -$ 35.67$ 2 16 570.72$ 570.72$ Journeyman 31.85 0.00% -$ 31.85$ 13 104 3,312.40$ 3,312.40$ Apprentice 20 0.00% -$ 20.00$ 5 40 800.00$ 800.00$

0.00% 22 176 5,316.40$ 30.2068182 5,316.40$ 30.2068180.00%

2012 0.00%Superintendent 41.8 0.00% -$ 41.80$ 1 8 334.40$ 334.40$ General Foreman 37.8 0.00% -$ 37.80$ 1 8 302.40$ 302.40$ Foreman 35.9 0.00% -$ 35.90$ 2 16 574.40$ 574.40$ Journeyman 32.05 0.00% -$ 32.05$ 13 104 3,333.20$ 3,333.20$ Apprentice 20 15 0 00% $ 20 15$ 5 40 806 00$ 806 00$Apprentice 20.15 0.00% -$ 20.15$ 5 40 806.00$ 806.00$

22 176 5,350.40$ 30.4 5,350.40$ 30.4

28

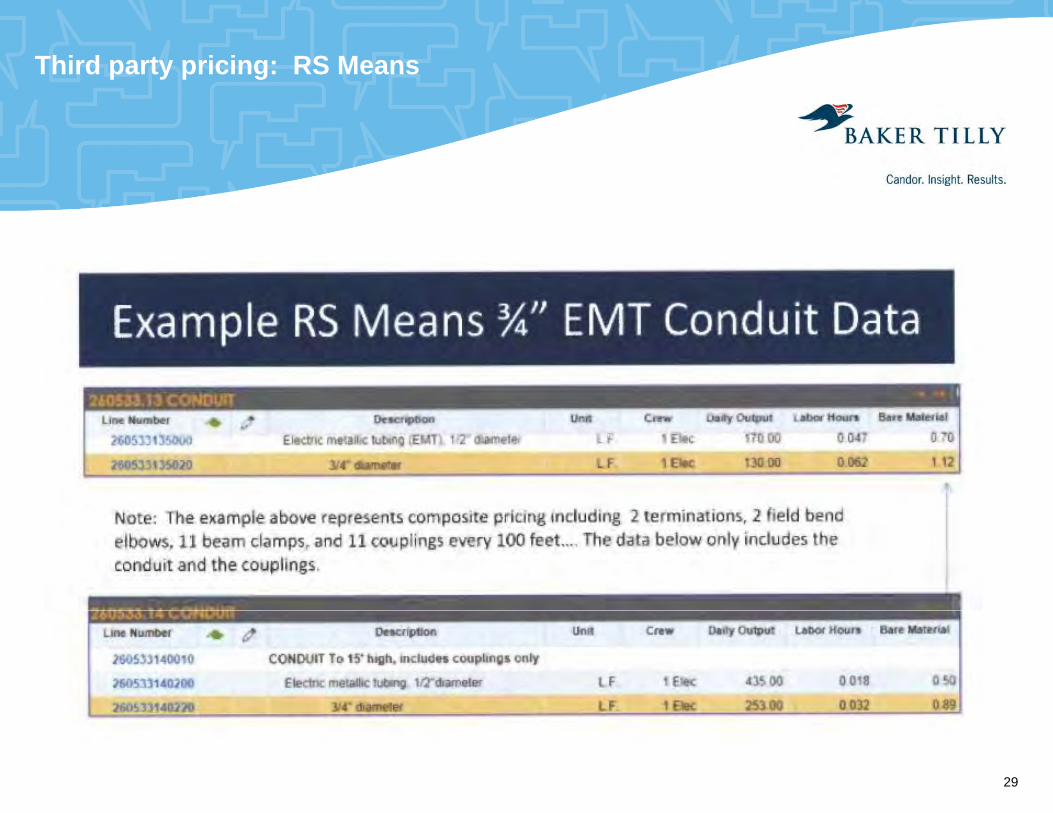

Third party pricing: RS Means

29

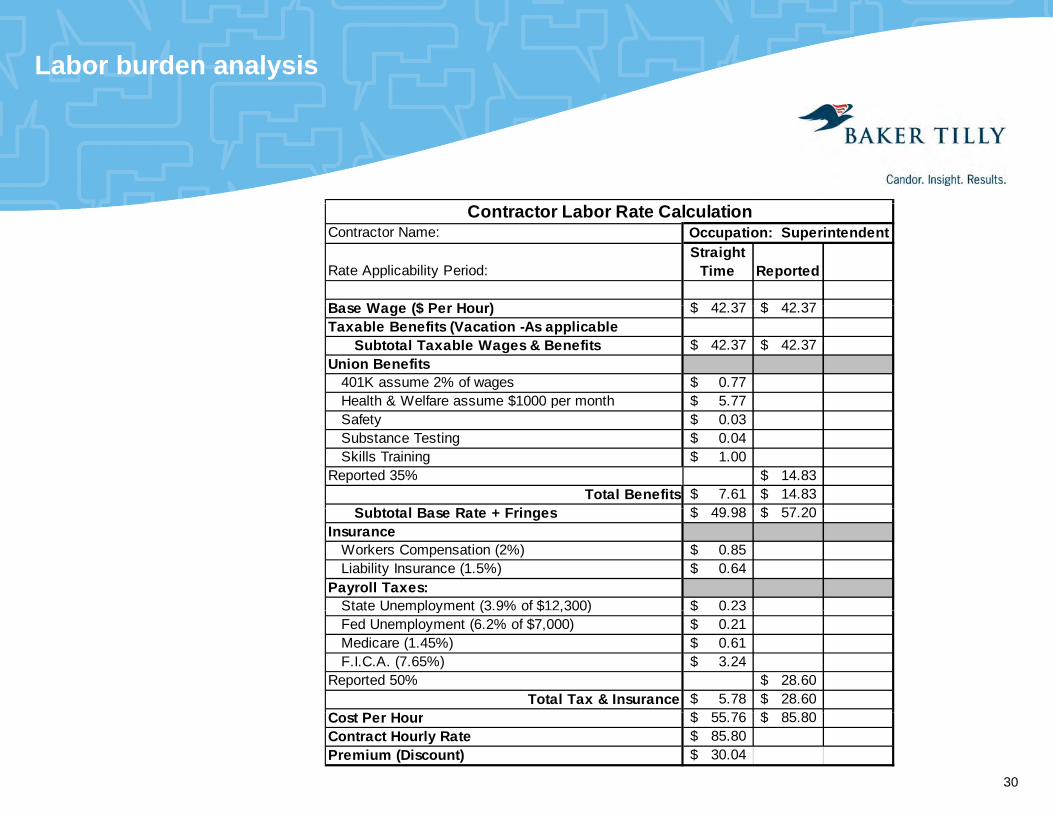

Labor burden analysis

Contractor Name:

Rate Applicability Period:Straight

Time Reported

B W ($ P H ) 42 37$ 42 37$

Contractor Labor Rate CalculationOccupation: Superintendent

Base Wage ($ Per Hour) 42.37$ 42.37$ Taxable Benefits (Vacation -As applicable

Subtotal Taxable Wages & Benefits 42.37$ 42.37$ Union Benefits

401K assume 2% of wages 0.77$ Health & Welfare assume $1000 per month 5.77$ $ p $Safety 0.03$ Substance Testing 0.04$ Skills Training 1.00$

Reported 35% 14.83$ Total Benefits 7.61$ 14.83$

S bt t l B R t F i 49 98$ 57 20$Subtotal Base Rate + Fringes 49.98$ 57.20$ Insurance

Workers Compensation (2%) 0.85$ Liability Insurance (1.5%) 0.64$

Payroll Taxes:State Unemployment (3.9% of $12,300) 0.23$ State U e p oy e t (3 9% o $ ,300) 0 3$Fed Unemployment (6.2% of $7,000) 0.21$ Medicare (1.45%) 0.61$ F.I.C.A. (7.65%) 3.24$

Reported 50% 28.60$ Total Tax & Insurance 5.78$ 28.60$

55 76$ 85 80$Cost Per Hour 55.76$ 85.80$ Contract Hourly Rate 85.80$ Premium (Discount) 30.04$

30

Change order scope analysis

Know what is allowed in the contract!!> E i th h d f th f th h> Examine the change order scope for the source of the change> If you can’t discover the source from the documentation ask the

subcontractor for an explanation.> E l f t i l ll bl h d> Examples of typical non-allowable change orders

– Rework for quality– Rework for plan and specification compliance

I i l d i h l d ifi i– It is already in the plans and specifications– It should have been in the plans and specifications. An owner has a realistic

expectation that the construction drawings will satisfy local and state building code. Design oversight may result in the architect compensating the g g y p gcontractor for rework

31

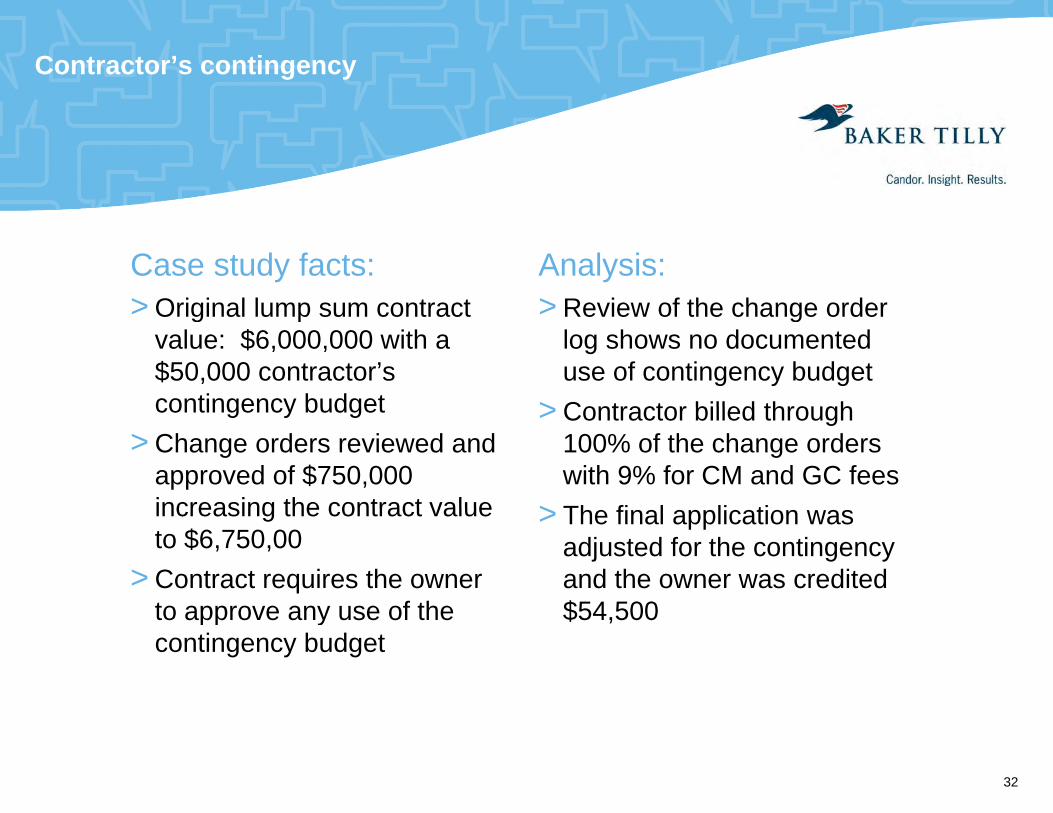

Contractor’s contingency

Case study facts:> Original lump sum contract

Analysis:> Review of the change order> Original lump sum contract

value: $6,000,000 with a $50,000 contractor’s contingency budget

> Review of the change order log shows no documented use of contingency budget

> Contractor billed throughcontingency budget> Change orders reviewed and

approved of $750,000 increasing the contract value

> Contractor billed through 100% of the change orders with 9% for CM and GC fees

> Th fi l li tiincreasing the contract value to $6,750,00

> Contract requires the owner to approve any use of the

> The final application was adjusted for the contingency and the owner was credited $54 500to approve any use of the

contingency budget$54,500

32

Upcoming webinar

Wednesday, June 5Noon to 1:00 PM CT

Subcontract default insuranceGuest Speakers:

Tim Cleary, M3 Insurance and Tim Anderson, Construction Risk Underwriters,

Registration for this event, today’s presentation and other topics in this webinar series can be found at

www.bakertilly.com/construction-audit-webinar

33

Questions?

Tony Ollmann, CPA, CCADirectorDirector608 240 [email protected]

ReminderT lif f th CPE dit t l t th l ti f tTo qualify for the CPE credit, you must complete the evaluation form at the end of the webinar.

34

Disclosure

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this comm nication as intended or ritten to be sed b an ta pa er for thein this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax d i i thi i ti i ti k ti diadvice in this communication in promoting, marketing, or recommending a

partnership or other entity, investment plan, or arrangement to any other party.

Baker Tilly refers to Baker Tilly Virchow Krause LLP an independently owned andBaker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. The information provided here is of a general nature and is not intended to address specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought © 2012 Baker Tilly Virchow Krause LLPbe sought. © 2012 Baker Tilly Virchow Krause, LLP

35