Audited Preliminary Results For Year Ended ... - Micro … · Audited Preliminary Results For Year...

68

Audited Preliminary Results For Year Ended 30 April 2016 Kevin Loosemore, Mike Phillips, Stephen Murdoch, Nils Brauckmann 14th July 2016

Transcript of Audited Preliminary Results For Year Ended ... - Micro … · Audited Preliminary Results For Year...

Audited Preliminary ResultsFor Year Ended 30 April 2016

Kevin Loosemore, Mike Phillips,

Stephen Murdoch, Nils Brauckmann

14th July 2016

Safe Harbour Statement

• The following presentation is being made only to, and is only directed at, persons to whom such presentation may lawfully be communicated (“relevant persons”). Any person who is not a relevant person should not act or rely on this presentation or any of its contents. Information in the following presentation relating to the price at which relevant investments have been bought or sold in the past or the yield on such investments cannot be relied upon as a guide to the future performance of such investments.

• This presentation does not constitute an offering of securities or otherwise constitute an invitation or inducement to any person to underwrite, subscribe for or otherwise acquire securities in Micro Focus International plc (the “Company”) or any company which is a subsidiary of the Company.

• The release, publication or distribution or this presentation in certain jurisdictions may be restricted by law, and therefore persons in such jurisdictions into which this presentation is released, published or distributed should inform themselves about, and observe, such restrictions.

• Certain statements contained in this presentation constitute forward-looking statements. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding the Company’s financial condition, business strategy, plans and objectives, are forward-looking statements. These forward-looking statements can be identified by the use of forward-looking terminology, including the terms “believes”, “estimates”, “anticipates”, “expects”, “intends”, “may”, “will”, or “should” or, in each case, their negative or other variat ions or comparable terminology. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future. Such risks, uncertainties and other factors include, among others: the level of expenditure committed to development and deployment applications by organisations; the level of deployment-related turnover expected by the Company; the degree to which organisations adopt web-enabled services; the rate at which large organisations migrate applications from the mainframe environment; the continued use and necessity of the mainframe for business critical applications; the degree of competition faced by the Company; growth in the information technology services market; general economic and business conditions, particularly in the United States; changes in technology and competition; and the Company’s ability to attract and retain qualified personnel. These forward-looking statements speak only as at the date of this presentation. Except as required by the Financial Conduct Authority, or by law, the Company does not undertake any obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future events, or otherwise.

2

Agenda

Overview and Outlook

Financial Review

Micro Focus Operations

SUSE Operations

Question and Answer

3

Overview

Kevin Loosemore

Executive Chairman

Overview

Results at the high end of management expectations

Total Shareholder Return strategy continues

• Final Dividend increased by 50.7% to 49.74 cents (2015: 33.00

cents)

• Full Year Dividend increased by 37.8% to 66.68 cents

(2015: 48.40 cents)

• Return of Value to shareholders in 2017

5

Preview Questions – A Range of Topics

• Is there any change in strategy?

• How and when are you going to return excess cash?

• Is the TAG acquisition delivering as planned?

• What’s the plan re acquisitions?

6

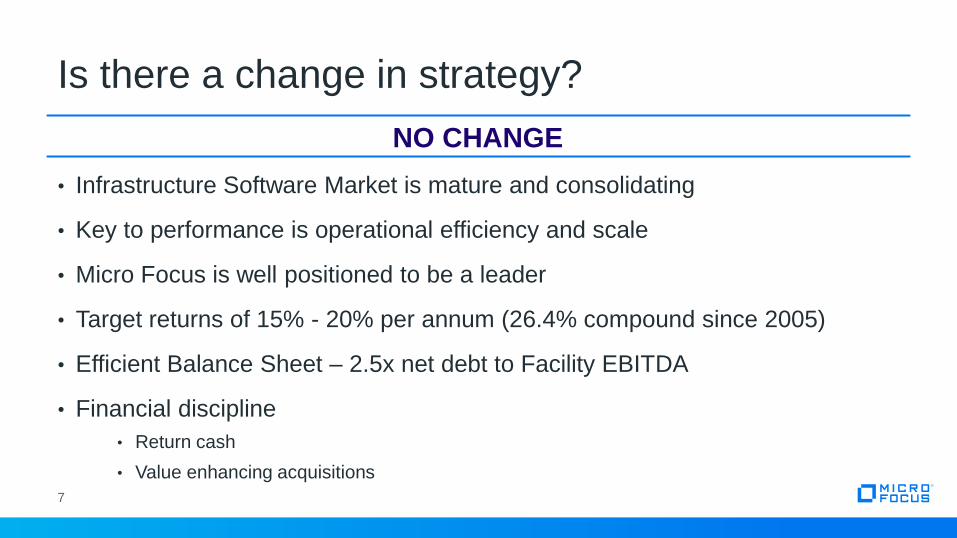

• Infrastructure Software Market is mature and consolidating

• Key to performance is operational efficiency and scale

• Micro Focus is well positioned to be a leader

• Target returns of 15% - 20% per annum (26.4% compound since 2005)

• Efficient Balance Sheet – 2.5x net debt to Facility EBITDA

• Financial discipline

• Return cash

• Value enhancing acquisitions

7

Is there a change in strategy?

NO CHANGE

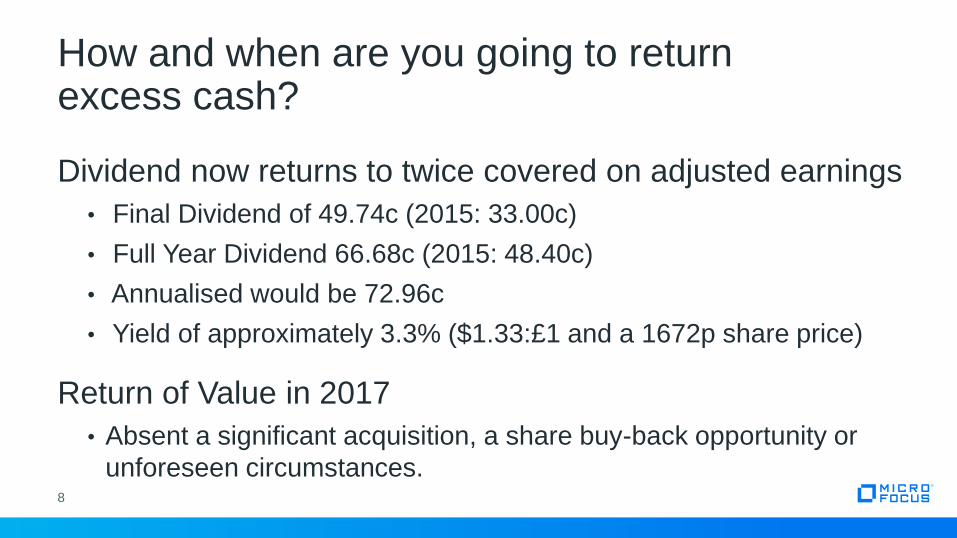

Dividend now returns to twice covered on adjusted earnings

• Final Dividend of 49.74c (2015: 33.00c)

• Full Year Dividend 66.68c (2015: 48.40c)

• Annualised would be 72.96c

• Yield of approximately 3.3% ($1.33:£1 and a 1672p share price)

Return of Value in 2017

• Absent a significant acquisition, a share buy-back opportunity or

unforeseen circumstances.8

How and when are you going to return excess cash?

TAG was acquired in November 2014 – as at 1 July 2016:

• Micro Focus shareholders have seen 91.4% return on their holding pre

announcement

• Wizard has exited its 40% stake

• TAG management had all their shares vest in 2014 together with additional deal

bonuses and retention bonuses

• Micro Focus management stock vests in November 2017 if performance conditions

are met

9

Is the TAG acquisition delivering as planned?

• From announcement to 1 July 2016 Market Capitalization has increased by 216.3%

• Shareholders approved a pool of 2.50% of equity as management incentive

• The Micro Focus Board only used 1.43%

• If incentive fully vests then as at 1 July 2016 management will receive c2.1% of the increase in Market Capitalization

• This is very favourable for shareholders compared to other companies’ schemes

• The Micro Focus Board will seek to use this as a model going forward

10

Is the TAG acquisition delivering as planned?

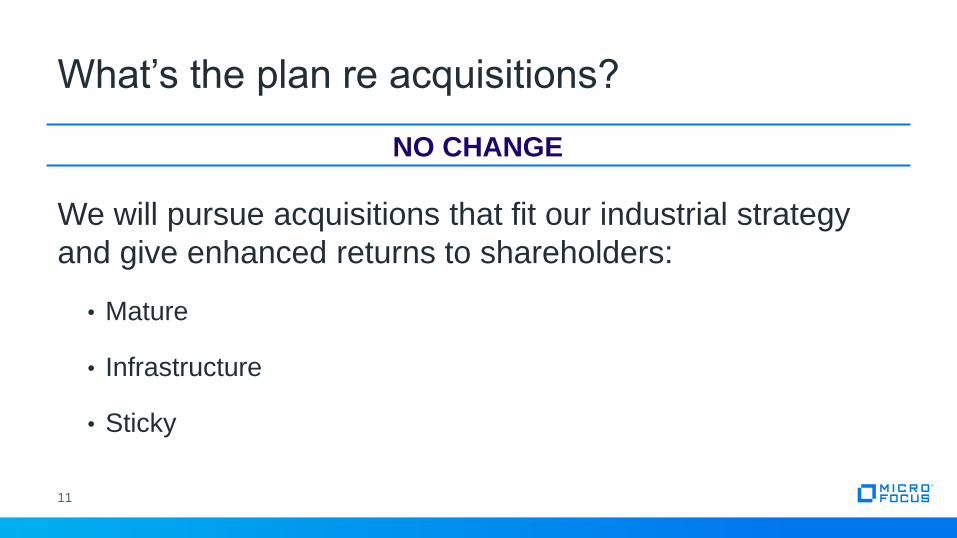

We will pursue acquisitions that fit our industrial strategy

and give enhanced returns to shareholders:

• Mature

• Infrastructure

• Sticky

11

What’s the plan re acquisitions?

NO CHANGE

Creating Greater Flexibility for M&A

At the AGM we will be seeking additional flexibility to avoid

being at a competitive disadvantage:

• Resolution: Grant the Board authority to implement an ASG

scheme in the event of an acquisition that can deliver shareholders

returns of 50% to 100% over three years

• Resolution: Grant the Board authority to allocate an additional 10%

of share capital in the event of an appropriate acquisition

12

• Consistent double digit shareholder returns

• Revenue in FY17 minus 2% to zero

• Compared to FY16 CCY pro-forma with Serena

• FY17 revenue exit rate flat with FY16 and anticipate

revenue growth in FY18

• Maintain target net debt at 2.5 times Facility EBITDA

• Appropriate value enhancing acquisitions13

Outlook

Financial Review

Mike Phillips

CFO

Results at a Glance

15

FY 2016

$m

FY 2015

$mChange

Total Revenue at Constant Currency 1,245.0 804.0 54.9%

- Licence 304.8 251.5 21.2%

- Maintenance 644.5 425.5 51.5%

- Subscriptions 248.9 94.9 162.3%

- Consultancy 46.8 32.1 45.8%

Total Reported Revenue 1,245.0 834.5 49.2%

NON GAAP MEASURES

Adjusted EBITDA

Constant Currency 546.8 344.0 59.0%

Reported 546.8 357.6 52.9%

Underlying Adjusted EBITDA

Constant Currency 532.5 334.7 59.1%

Reported 532.5 348.3 52.9%

STATUTORY MEASURES

Pre-tax profit

Constant Currency 195.4 81.3 140.3%

Reported 195.4 91.4 113.8%

Net debt 1,078.0 1,403.5 -23.2%

Earnings per share Cents Cents

Diluted 71.61 56.71 26.3%

Adjusted diluted 146.70 129.43 13.3%

Dividend per share 66.68 48.40 37.8%

On a pro-forma CCY basis to provide a better comparison of performance

• Total revenues of $1,245.0m (2015: pro-forma CCY $1,270.7m), a reduction of 2.0%, at the top of the range of management’s guidance

• Growth in SUSE subscription and consultancy revenues

• Offset by anticipated declines in Micro Focus revenues

• Adjusted EBITDA of $546.8m (2015: pro-forma CCY $499.3m), an increase of 9.5%

• Underlying Adjusted EBITDA of $532.5m (2015: pro-forma CCY $486.8m), an increase of 9.4%

Growth in Adjusted diluted earnings per share of 13.3% to 146.70 cents (2015: 129.43 cents)

Acquisition of Serena Software Inc. (“Serena”) announced on 22 March 2016

• Purchase price of $540.0m on a cash and debt free basis,

• Funded by existing and extended revolving credit facility of $375m and a placing of 10.87m shares at a price of 1,455 pence raising £158.2m ($225.7m) gross and £156.1m ($222.7m) net.

• Completion of the Serena acquisition took place on 2 May 2016

• Revenue of $162.3m and Underlying Adjusted EBITDA of $80.9m in the year ended 31 January 2016

16

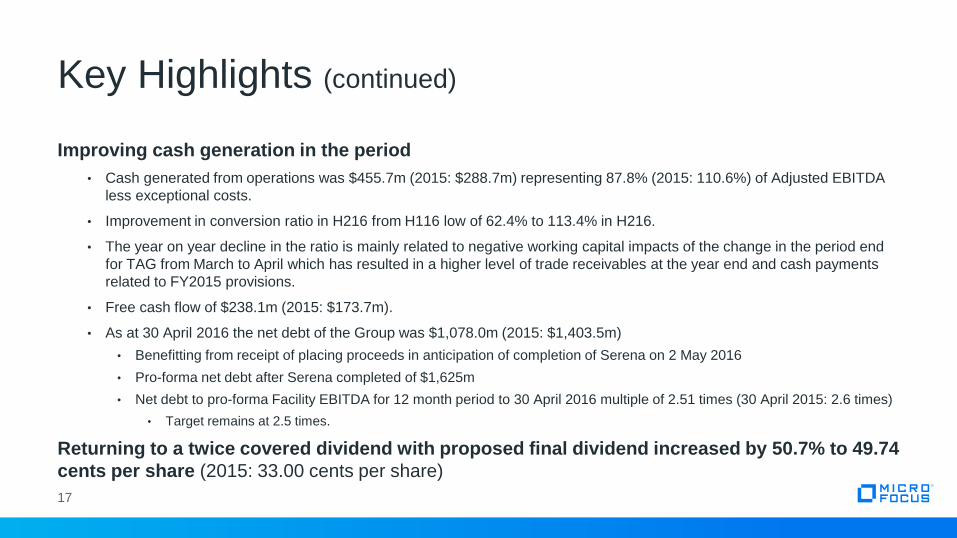

Key Highlights

Improving cash generation in the period

• Cash generated from operations was $455.7m (2015: $288.7m) representing 87.8% (2015: 110.6%) of Adjusted EBITDA

less exceptional costs.

• Improvement in conversion ratio in H216 from H116 low of 62.4% to 113.4% in H216.

• The year on year decline in the ratio is mainly related to negative working capital impacts of the change in the period end

for TAG from March to April which has resulted in a higher level of trade receivables at the year end and cash payments

related to FY2015 provisions.

• Free cash flow of $238.1m (2015: $173.7m).

• As at 30 April 2016 the net debt of the Group was $1,078.0m (2015: $1,403.5m)

• Benefitting from receipt of placing proceeds in anticipation of completion of Serena on 2 May 2016

• Pro-forma net debt after Serena completed of $1,625m

• Net debt to pro-forma Facility EBITDA for 12 month period to 30 April 2016 multiple of 2.51 times (30 April 2015: 2.6 times)

• Target remains at 2.5 times.

Returning to a twice covered dividend with proposed final dividend increased by 50.7% to 49.74

cents per share (2015: 33.00 cents per share)

17

Key Highlights (continued)

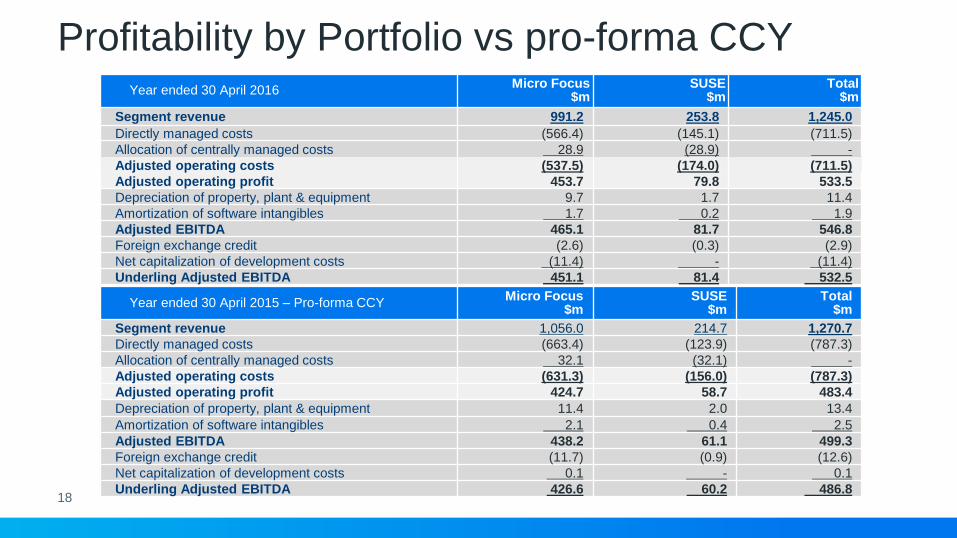

Profitability by Portfolio vs pro-forma CCY

18

Year ended 30 April 2015 – Pro-forma CCYMicro Focus

$mSUSE

$mTotal

$m

Segment revenue 1,056.0 214.7 1,270.7

Directly managed costs (663.4) (123.9) (787.3)

Allocation of centrally managed costs 32.1 (32.1) -

Adjusted operating costs (631.3) (156.0) (787.3)

Adjusted operating profit 424.7 58.7 483.4

Depreciation of property, plant & equipment 11.4 2.0 13.4

Amortization of software intangibles 2.1 0.4 2.5

Adjusted EBITDA 438.2 61.1 499.3

Foreign exchange credit (11.7) (0.9) (12.6)

Net capitalization of development costs 0.1 - 0.1

Underling Adjusted EBITDA 426.6 60.2 486.8

Year ended 30 April 2016Micro Focus

$mSUSE

$mTotal

$m

Segment revenue 991.2 253.8 1,245.0

Directly managed costs (566.4) (145.1) (711.5)

Allocation of centrally managed costs 28.9 (28.9) -

Adjusted operating costs (537.5) (174.0) (711.5)

Adjusted operating profit 453.7 79.8 533.5

Depreciation of property, plant & equipment 9.7 1.7 11.4

Amortization of software intangibles 1.7 0.2 1.9

Adjusted EBITDA 465.1 81.7 546.8

Foreign exchange credit (2.6) (0.3) (2.9)

Net capitalization of development costs (11.4) - (11.4)

Underling Adjusted EBITDA 451.1 81.4 532.5

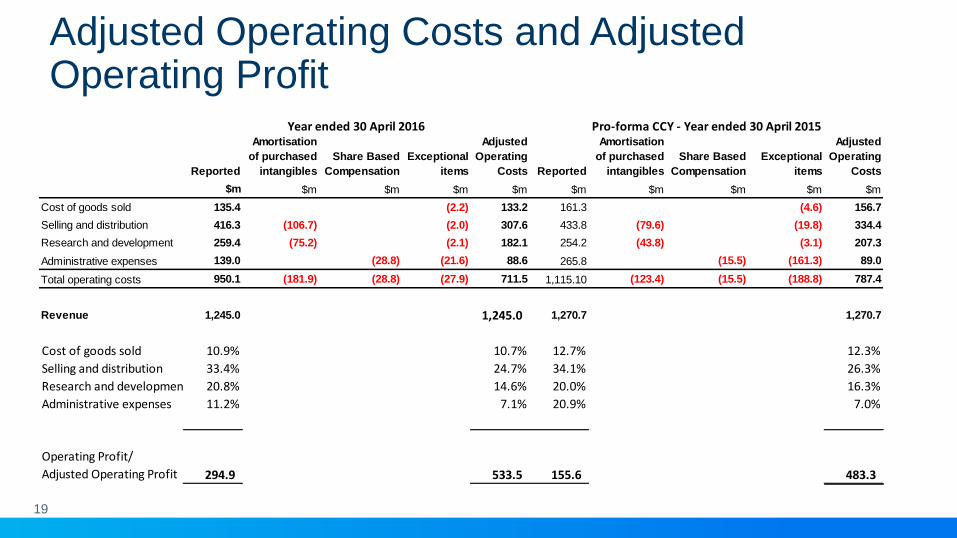

Adjusted Operating Costs and Adjusted Operating Profit

19

Reported

Amortisation

of purchased

intangibles

Share Based

Compensation

Exceptional

items

Adjusted

Operating

Costs Reported

Amortisation

of purchased

intangibles

Share Based

Compensation

Exceptional

items

Adjusted

Operating

Costs

$m $m $m $m $m $m $m $m $m $m

Cost of goods sold 135.4 (2.2) 133.2 161.3 (4.6) 156.7

Selling and distribution 416.3 (106.7) (2.0) 307.6 433.8 (79.6) (19.8) 334.4

Research and development 259.4 (75.2) (2.1) 182.1 254.2 (43.8) (3.1) 207.3

Administrative expenses 139.0 (28.8) (21.6) 88.6 265.8 (15.5) (161.3) 89.0

Total operating costs 950.1 (181.9) (28.8) (27.9) 711.5 1,115.10 (123.4) (15.5) (188.8) 787.4

Revenue 1,245.0 1,245.0 1,270.7 1,270.7

Cost of goods sold 10.9% 10.7% 12.7% 12.3%

Selling and distribution 33.4% 24.7% 34.1% 26.3%

Research and development 20.8% 14.6% 20.0% 16.3%

Administrative expenses 11.2% 7.1% 20.9% 7.0%

Operating Profit/

Adjusted Operating Profit 294.9 533.5 155.6 483.3

Year ended 30 April 2016 Pro-forma CCY - Year ended 30 April 2015

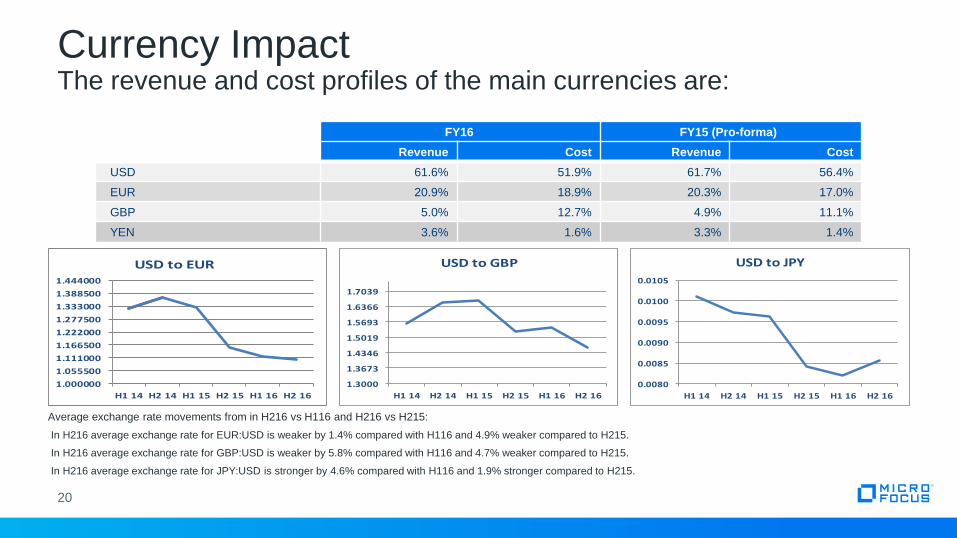

Currency ImpactThe revenue and cost profiles of the main currencies are:

20

FY16 FY15 (Pro-forma)

Revenue Cost Revenue Cost

USD 61.6% 51.9% 61.7% 56.4%

EUR 20.9% 18.9% 20.3% 17.0%

GBP 5.0% 12.7% 4.9% 11.1%

YEN 3.6% 1.6% 3.3% 1.4%

Average exchange rate movements from in H216 vs H116 and H216 vs H215:

In H216 average exchange rate for EUR:USD is weaker by 1.4% compared with H116 and 4.9% weaker compared to H215.

In H216 average exchange rate for GBP:USD is weaker by 5.8% compared with H116 and 4.7% weaker compared to H215.

In H216 average exchange rate for JPY:USD is stronger by 4.6% compared with H116 and 1.9% stronger compared to H215.

1.000000

1.055500

1.111000

1.166500

1.222000

1.277500

1.333000

1.388500

1.444000

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

USD to EUR

1.3000

1.3673

1.4346

1.5019

1.5693

1.6366

1.7039

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

USD to GBP

0.0080

0.0085

0.0090

0.0095

0.0100

0.0105

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

USD to JPY

FY15 Pro-forma CCY Revenue and Underlying Adjusted EBITDA

21

Revenue

$m

Costs

$m

Underlying

Adjusted EBITDA

$m

As reported at actual rates of exchange 1,320.7 817.7 503.0

Based on FY16 currency rates 1,270.7 783.9 486.8

Currency Impact (3.8)% 4.1% (3.2)%

Pro-forma is year to 30 April 15

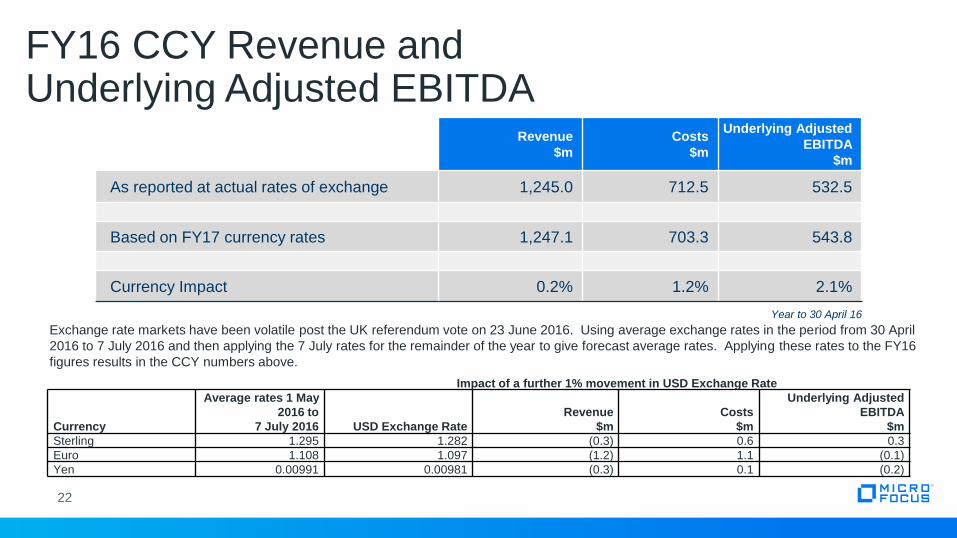

FY16 CCY Revenue and Underlying Adjusted EBITDA

22

Revenue

$m

Costs

$m

Underlying Adjusted

EBITDA

$m

As reported at actual rates of exchange 1,245.0 712.5 532.5

Based on FY17 currency rates 1,247.1 703.3 543.8

Currency Impact 0.2% 1.2% 2.1%

Year to 30 April 16

Exchange rate markets have been volatile post the UK referendum vote on 23 June 2016. Using average exchange rates in the period from 30 April

2016 to 7 July 2016 and then applying the 7 July rates for the remainder of the year to give forecast average rates. Applying these rates to the FY16

figures results in the CCY numbers above.

Impact of a further 1% movement in USD Exchange Rate

Currency

Average rates 1 May

2016 to

7 July 2016 USD Exchange Rate

Revenue

$m

Costs

$m

Underlying Adjusted

EBITDA

$m

Sterling 1.295 1.282 (0.3) 0.6 0.3

Euro 1.108 1.097 (1.2) 1.1 (0.1)

Yen 0.00991 0.00981 (0.3) 0.1 (0.2)

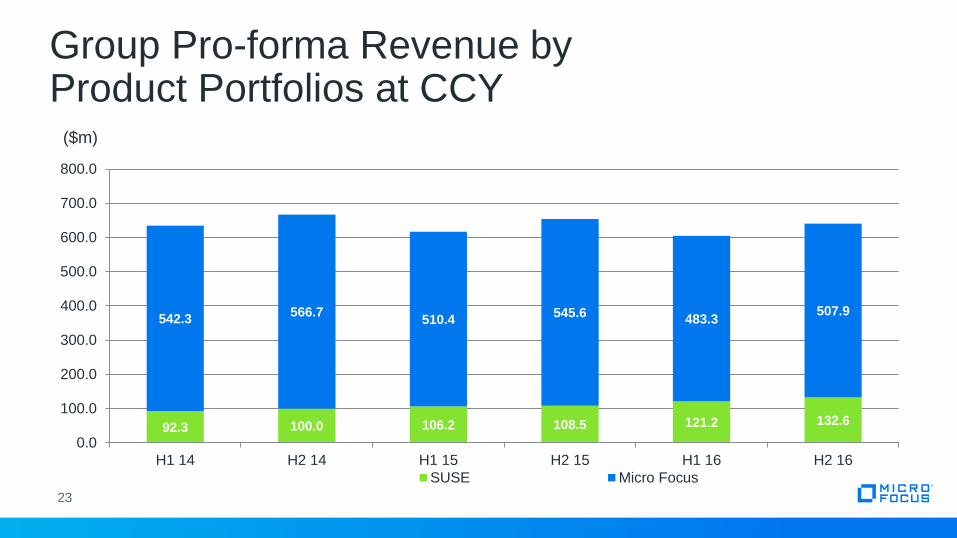

Group Pro-forma Revenue by Product Portfolios at CCY

23

($m)

92.3 100.0 106.2 108.5 121.2 132.6

542.3566.7

510.4545.6

483.3507.9

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

SUSE Micro Focus

FY 2016 Revenue by Portfolio Group

24

Year ended 30 April 2016As Reported

Year ended 30 April 2015Pro-forma CCY 1

Year ended 30 April 2016 Pro-forma CCY Growth

Year ended 30 April 2015As reported

$m $m % $m

Micro Focus Product Portfolio

Licence 304.8 320.3 (4.8%) 261.0

Maintenance 644.5 686.3 (6.1%) 440.6

Consultancy 41.9 49.4 (15.2%) 31.8

991.2 1,056.0 (6.1%) 733.4

SUSE Product Portfolio

Subscription 248.9 210.5 18.2% 98.2

Consultancy 4.9 4.2 16.7% 2.9

253.8 214.7 18.2% 101.1

Total Revenue

Licence 304.8 320.3 (4.8%) 261.0

Maintenance 644.5 686.3 (6.1%) 440.6

Subscription 248.9 210.5 18.2% 98.2

Consultancy 46.8 53.6 (12.7%) 34.7

Revenue 1,245.0 1,270.7 (2.0%) 834.5 1 Unaudited

SUSE

• Total Contract Value (“TCV”)

• The value of the invoiced amount on any contract (“Billings”)

• Weighted Average Contract Period

• For the contracts signed and/or invoiced in the period the weighted average invoice period in months

• Annual Contract Value (“ACV”)

• The first 12 months value of the TCV in the period. Billings less than 12 months are included in full

SUSE and Micro Focus

• Subscription and maintenance contract renewal rates are not being provided

• Our methodology is still being refined in order to accommodate data from our multiple systems

• Trending the maintenance revenues provides the best guidance for those revenue streams

25

Metrics Being Provided

Group Pro-forma Revenue at CCY by Type($m)

26

COBOL Development & Mainframe Solutions

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

Maintenance Licence Services

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

Maintenance Licence Services

Host Connectivity

Group Pro-forma Revenue at CCY by Type($m)

27

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

Maintenance Licence Services

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

Maintenance Licence Services

Identity & Access Security Development & IT Operations Management Tools

Group Pro-forma Revenue at CCY by Type($m)

28

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

Maintenance Licence Services

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

H1 14 H2 14 H1 15 H2 15 H1 16 H2 16

Subscription Services

Collaboration & Networking SUSE

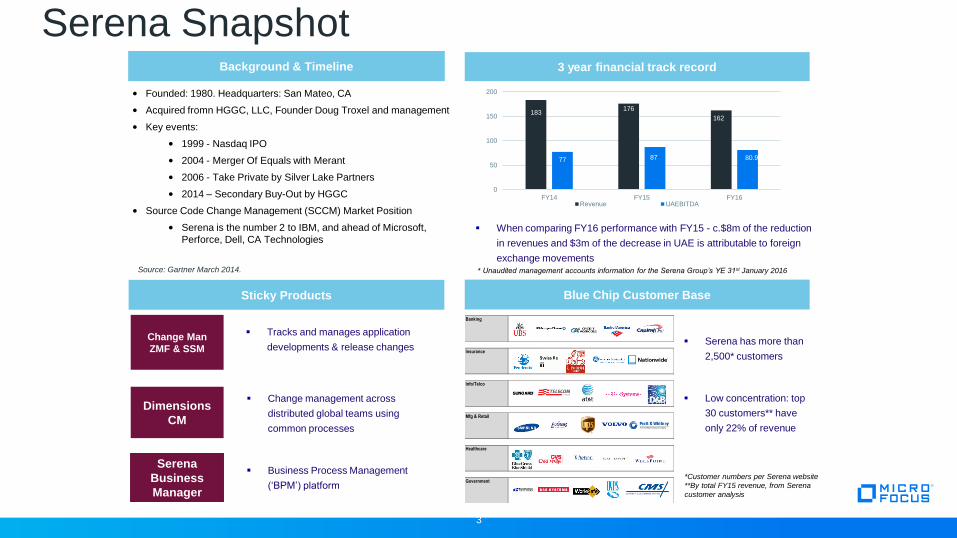

Serena SnapshotBackground & Timeline 3 year financial track record

• Founded: 1980. Headquarters: San Mateo, CA

• Acquired fromn HGGC, LLC, Founder Doug Troxel and management

• Key events:

• 1999 - Nasdaq IPO

• 2004 - Merger Of Equals with Merant

• 2006 - Take Private by Silver Lake Partners

• 2014 – Secondary Buy-Out by HGGC

• Source Code Change Management (SCCM) Market Position

• Serena is the number 2 to IBM, and ahead of Microsoft,

Perforce, Dell, CA Technologies

Sticky Products

3

Blue Chip Customer Base

Banking

Insurance

Info/Telco

Mfg & Retail

Healthcare

Government

Tracks and manages application

developments & release changesChange Man

ZMF & SSM

Serena

Business

Manager

Business Process Management

(‘BPM’) platform

Dimensions

CM

Change management across

distributed global teams using

common processes

Serena has more than

2,500* customers

Low concentration: top

30 customers** have

only 22% of revenue

*Customer numbers per Serena website

**By total FY15 revenue, from Serena

customer analysis

* Unaudited management accounts information for the Serena Group’s YE 31st January 2016Source: Gartner March 2014.

When comparing FY16 performance with FY15 - c.$8m of the reduction

in revenues and $3m of the decrease in UAE is attributable to foreign

exchange movements

183176

162

77 87 80.9

0

50

100

150

200

FY14 FY15 FY16Revenue UAEBITDA

FY16 CCY Revenue and Underlying Adjusted EBITDA for the Enlarged Group

30

Revenue

$m

Costs

$m

Underlying Adjusted

EBITDA

$m

Serena – year ended 31 January 2016 162.3 81.4 80.9

Restated on FY17 currency rates 161.1 80.1 81.0

Existing Group 1,247.1 703.3 543.8

Enlarged Group FY16 at FY17 currency rates 1,408.2 783.4 624.8

FY17 revenue guidance of minus 2% to zero% off the FY16 CCY revenues would give a range of $1,380.0m to $1,408.2m.

Exceptional Costs

31

2016

$m

2015

$m

Acquisition costs 0.5 26.9

Pre-acquisition costs 5.6 -

Property costs 6.0 18.2

Severance costs (4.8) 30.7

Impairment of Intangible Assets - 11.6

Impairment of prepayments - 1.7

Royalty provision release (3.0) -

Integration costs 23.6 7.6

Accelerated amortization of facility fees - 2.4

Total 27.9 99.1

Summary Balance Sheet

32

30 April 2016

$m

30 April 2015

$m

Non-current assets 3,681.3 3,879.6

Inventories 0.1 0.1

Trade and other receivables 268.2 218.7

Current tax receivables 18.0 -

Cash and cash equivalents 667.2 241.3

Assets classified as held for sale 0.9 0.9

Total assets 4,635.7 4,340.6

Liabilities

Current liabilities

Trade and other payables 188.1 161.4

Borrowings 275.3 125.7

Provisions 10.5 49.3

Current tax liabilities 22.4 67.9

Deferred income 565.5 583.7

Non-current liabilities

Deferred income 196.5 194.9

Borrowings 1,470.0 1,519.1

Retirement benefit obligations 31.7 32.7

Long-term provisions 14.3 17.9

Other non-current liabilities 3.7 5.3

Deferred tax liabilities 264.0 304.6

Total liabilities 3,042.0 3,062.5

Net assets 1,593.7 1,278.1

Cash Conversion

33

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

200.0%

-150

-100

-50

0

50

100

150

200

250

300

350

6m-Apr 13 6m-Oct 13 6m-Apr 14 6m-Oct 14 6m-Apr 15 6m-Oct 15 6m-Apr 16

$m

Provisions Movement (non Cash)

Changes in Working Capital (including cash movements on Provisions)

Net cash generated from operating activities before changes in working capital and provisions

Cash Conversion %

Changes in Working Capital

34

0

5

10

15

20

25

30

35

40

45

50

55

60

65

(140)

(120)

(100)

(80)

(60)

(40)

(20)

0

20

40

60

80

100

120

6m-Apr 13 6m-Oct 13 6m- Apr 14 6m-Oct 14 6m-Apr 15 6m-Oct 15 6m-Apr 16

Days S

ale

s O

uts

tan

din

g

Trade Debtors Deferred Income Provision (cash element) TAG Acq Costs Others DSO

$2.6m $28.5m

Net Change in Working Capital

$6.0m

$m

$(8.7)m $(19.5)m $(17.0)m $(106.4)m

• Reported effective tax rate (“ETR”) in the period is 16.6% (2015: minus 11.0%)

• Adjusted ETR in the period is 23.1% (2015: 21.2%) in line with guidance range of 21% to 25%

35

Taxation

Year ended30 April 2016

$mETR

Year ended30 April 2015

$mETR

Profit before tax (PBT) 195.4 91.4

Share based compensation 28.8 15.5

Amortization of purchased intangibles 181.9 88.3

Exceptional costs 27.9 96.7

Exceptional finance costs - 2.4

Adjusted PBT 434.0 294.3

Tax (charge) / credit as reported (32.4) 16.6% 10.0 (11.0)%

Tax on adjusted items (67.8) (62.5)

Other tax items (below) - (9.9)

Adjusted tax charge (100.2) 23.1% (62.4) 21.2%

Other tax items in the prior year included the recognition of deferred tax assets relating to tax credits as a result of the TAG acquisition ($5.1m) and the recognition of UK patent box benefits

relating to the year ended 30 April 2014 ($4.8m)

Adjusted ETR (23.1%) for the year is higher than the previous year (21.2%) and the

first half of the year (21.0%)

• Primarily due to the one-off taxation in the US of foreign earnings of TAG

The Group’s medium term (3 year) Adjusted ETR is expected to rise during the

period from 23% to 27% of Adjusted Profit Before Tax

• Higher than previous guidance of 21% to 25%, primarily due to the impact of anticipated

legislative changes to restrict the deductibility of interest expenses in the UK, which are expected

to come into effect from April 2017

• Increase in forecast rate also reflects wider uncertainty regarding the impact of the OECD’s

Base Erosion and Profit Shifting (“BEPS”) project

• Serena acquisition is not expected to have a significant impact on ETR

• Brexit is not expected to have a significant impact on ETR at this stage

36

Taxation

Taxes paid during the year were $79.3m (2015: net receipt $1.8m) reflecting

the following:

• $24.5m paid under Accelerated Payment Notice issued by HMRC in relation to historic UK tax

claim, where discussions with HMRC are ongoing

• $27.2m paid in the US in respect of Federal income tax liabilities for FY15 and FY16

• Tax liabilities for those years are now expected to be significantly lower than anticipated when those

payments were made, which accounts for the majority of the current tax receivables on the balance

sheet of $18.0m. This will reduce Group cash tax payable in FY17.

• Reduction is due to the offset of deferred tax assets, so no impact on Group ETR.

• $17.0m was received in the US in the prior year relating to the settlement of tax audits and

historic overpayments

37

Taxation

Profitability by Portfolio vs pro-forma CCY

38

Year ended 30 April 2015 – Pro-forma CCYMicro Focus

$mSUSE

$mTotal

$m

Segment revenue 1,056.0 214.7 1,270.7

Directly managed costs (663.4) (123.9) (787.3)

Allocation of centrally managed costs 32.1 (32.1) -

Adjusted operating costs (631.3) (156.0) (787.3)

Adjusted operating profit 424.7 58.7 483.4

Depreciation of property, plant & equipment 11.4 2.0 13.4

Amortization of software intangibles 2.1 0.4 2.5

Adjusted EBITDA 438.2 61.1 499.3

Foreign exchange credit (11.7) (0.9) (12.6)

Net capitalization of development costs 0.1 - 0.1

Underling Adjusted EBITDA 426.6 60.2 486.8

Year ended 30 April 2016Micro Focus

$mSUSE

$mTotal

$m

Segment revenue 991.2 253.8 1,245.0

Directly managed costs (566.4) (145.1) (711.5)

Allocation of centrally managed costs 28.9 (28.9) -

Adjusted operating costs (537.5) (174.0) (711.5)

Adjusted operating profit 453.7 79.8 533.5

Depreciation of property, plant & equipment 9.7 1.7 11.4

Amortization of software intangibles 1.7 0.2 1.9

Adjusted EBITDA 465.1 81.7 546.8

Foreign exchange credit (2.6) (0.3) (2.9)

Net capitalization of development costs (11.4) - (11.4)

Underling Adjusted EBITDA 451.1 81.4 532.5

FY16 Micro Focus Portfolio Update

Stephen Murdoch

CEO

• Delivered financial commitments

• Restructured four TAG business units and original Micro Focus into two portfolios: SUSE & Micro Focus

• Delivered significant levels of synergies

• Moved from annual bookings focus to quarterly revenue cadence

• Simplified branding from six brands to Micro Focus and SUSE

• Rationalized property portfolio from 128 offices to 83 offices

• Created a comprehensive IT systems strategy for the Group

• Strengthened the team

• New HR director, new Director of Finance, new IT leaders in infrastructure and operations

• New Global Channels leader, new GTM operations leader, new leader for APJ overall and for ANZ

• Serena Acquisition

40

FY16: A Year of Significant Progress and Change

Micro Focus Pro-forma revenue at CCY

41

Year ended 30 April 2016

As Reported

Year ended 30 April 2015

Pro-forma CCY 1

Year ended 30 April 2016

Growth$m $m %

CDMSLicence 104.7 105.9 (1.1%)Maintenance 145.2 141.9 2.3%Consultancy 8.9 8.1 9.9%

258.8 255.9 1.1%Host ConnectivityLicence 89.9 94.6 (5.0%)Maintenance 105.4 105.8 (0.4%)Consultancy 2.9 4.0 (27.5%)

198.2 204.4 (3.0%)Identity, Access & SecurityLicence 52.4 43.1 21.6%Maintenance 142.2 147.0 (3.3%)Consultancy 22.1 27.6 (19.9%)

216.7 217.7 (0.5%)

Development & IT Operations Management Tools

Licence 33.9 41.8 (18.9%)Maintenance 121.3 136.7 (11.3%)Consultancy 2.2 2.8 (21.4%)

157.4 181.3 (13.2%)Collaboration & NetworkingLicence 23.9 34.9 (31.5%)Maintenance 130.4 154.9 (15.8%)Consultancy 5.8 6.9 (15.9%)

160.1 196.7 (18.6%)Micro Focus Product PortfolioLicence 304.8 320.3 (4.8%)Maintenance 644.5 686.3 (6.1%)Consultancy 41.9 49.4 (15.2%)

991.2 1,056.0 (6.1%)

1 Unaudited

Micro Focus - Profitability vs pro-forma CCY

42

Micro Focus Product Portfolio

Year ended

30 April 2016$m

Year ended 30 April 2015

Pro-forma CCY$m

Segment revenue 991.2 1,056.0

Directly managed costs (586.4) (663.4)

Allocation of centrally managed costs 28.9 32.1

Adjusted operating costs (537.5) (631.3)

Adjusted operating profit 453.7 424.7

Depreciation of property, plant & equipment 9.7 11.4

Amortization of software intangibles 1.7 2.1

Adjusted EBITDA 465.1 438.2

Foreign exchange credit (2.6) (11.7)

Net capitalization of development costs (11.4) 0.1

Underling Adjusted EBITDA 451.1 426.6

Underlying Adjusted EBITDA margin 45.5% 40.4%

Enablers: Clarity of direction & purpose underpinned by great people

LFR: EXECUTION: granular approach via 4 BOX model

MFR: STABILIZATION: improve trends through incremental improvements across the board

CFR: CONSISTENCY: underpin delivery of customer value

Efficiency & Enablement Identify & Close Integrate & Leverage

RemoveComplexity

Re-shape

Deliver FY17 Financial Plan

Balance fixing the short term with re-engineering for the long term

Simplify processes, improve underlying data quality, analytics and reporting

Organizational Model Systems & Application

Model

Simplified Platform for GrowthGo-to Market Acquisitions

FY17 Imperatives: Deliver in 17 and Build for 18+

43

39

• Consistent execution of strategy and four phase plan

• Delivery of our financial plan

• Standardizing systems and simplifying business operations

• Accelerating progress on improving the effectiveness of Go-to-Market

• Highly focused development and product management to optimize the

performance of each sub-portfolio

44

FY17 Priorities

FY16 SUSE Portfolio UpdateLondon, 14th July 2016

Nils Brauckmann

CEO

FY16 – A Successful Year For SUSE

The SUSE growth charter:

“Sustainable, Profitable Revenue Growth Above Market Rate”

All relevant KPIs showed growth

• Revenue of $253.8m with y/y growth of 18.2%

• Deferred revenue balance of $326.8m with y/y growth of 23.3%

• TCV of $301.3m with y/y growth of 14.3%

• ACV of $174.8m with y/y growth of 17.9%

Open source business with market leading profitability

• Underlying Adjusted EBITDA of $81.4m

• y/y increase of 35.2 %

• Profit margin of 32.1% with y/y improvement of 4.1%

4246

FY16 Progress and Expansion

• Expanded headcount across different business functions and

geographies

• Aligned the critical supporting organizations much more tightly with the

SUSE business

• Extended SUSE’s presence and contribution in key open source

projects and relevant industry groups

• Development of SUSE leadership team to support growth charter

4747

SUSE Regional Revenue Performance

48

North America and International had successful years with revenue growing at 24.3% and 17.5% respectively.

APJ, whilst showing a smaller increase of revenues, has a solid foundation to grow from. SUSE now operates

with a dedicated GTM sales organization in this region, and FY16 featured stronger TCV and ACV performance.

Regional Revenue Performance

Year ended

30 April 2016 Actual

$m

Year ended

30 April 2015 Pro-forma CCY 1

$m

Year ended

30 April 2015 Pro-forma

CCY (Decline)/Growth

%

SUSE

North America 108.6 87.4 24.3%

International 115.6 98.4 17.5%

Asia Pacific & Japan 29.6 28.9 2.4%

Total 253.8 214.7 18.2% 1 unaudited

48

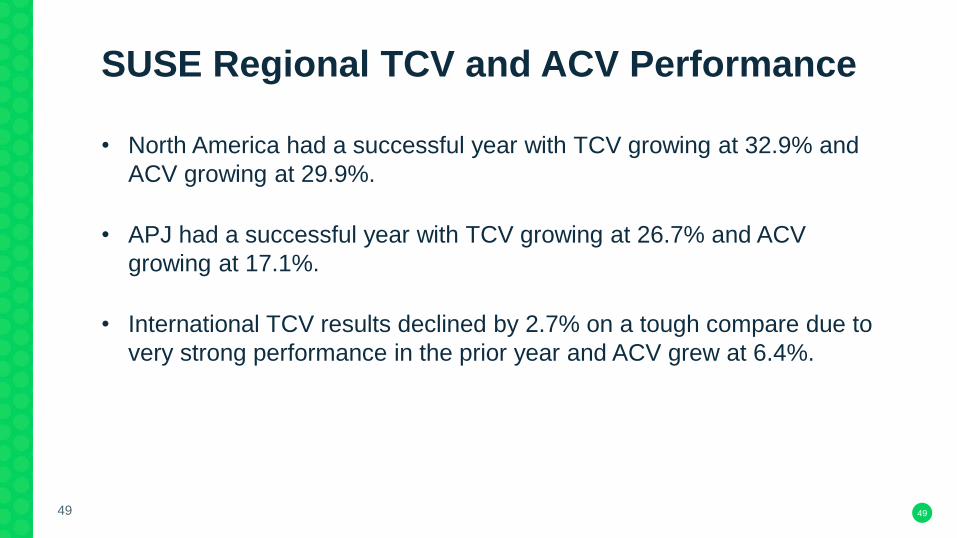

SUSE Regional TCV and ACV Performance

• North America had a successful year with TCV growing at 32.9% and

ACV growing at 29.9%.

• APJ had a successful year with TCV growing at 26.7% and ACV

growing at 17.1%.

• International TCV results declined by 2.7% on a tough compare due to

very strong performance in the prior year and ACV grew at 6.4%.

4949

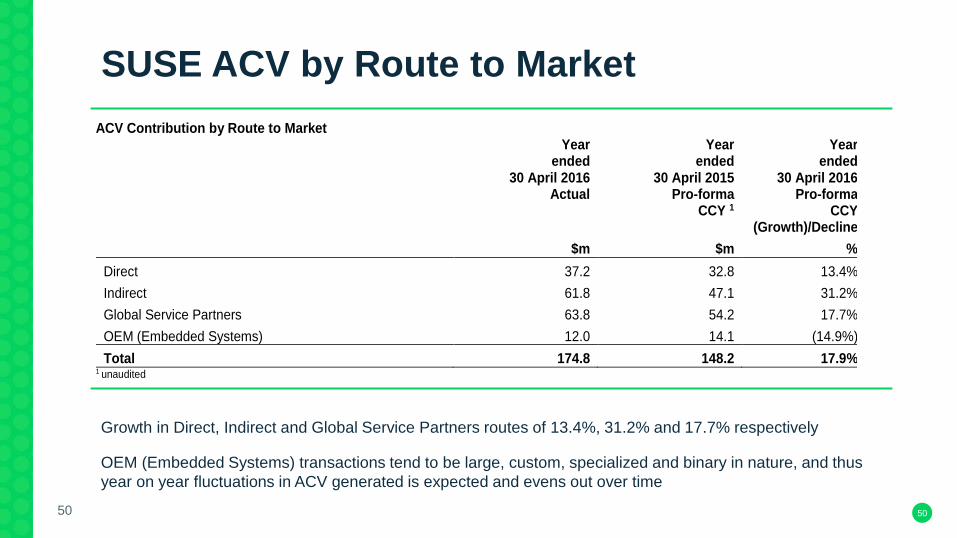

SUSE ACV by Route to Market

50

Growth in Direct, Indirect and Global Service Partners routes of 13.4%, 31.2% and 17.7% respectively

OEM (Embedded Systems) transactions tend to be large, custom, specialized and binary in nature, and thus

year on year fluctuations in ACV generated is expected and evens out over time

ACV Contribution by Route to Market

Year ended

30 April 2016 Actual

Year ended

30 April 2015 Pro-forma

CCY 1

Year ended

30 April 2016 Pro-forma

CCY (Growth)/Decline

$m $m %

Direct 37.2 32.8 13.4%

Indirect 61.8 47.1 31.2%

Global Service Partners 63.8 54.2 17.7%

OEM (Embedded Systems) 12.0 14.1 (14.9%)

Total 174.8 148.2 17.9% 1 unaudited

50

Alliance and GSP Relationship Progress

• Intel includes SUSE Linux Enterprise Server for High Performance

Computing as first commercial Linux in Intel’s HPC Orchestrator solution

• HPE and SUSE are delivering a Software Defined Storage Solution with

SUSE Enterprise Storage on HPE storage-optimized Apollo servers and

HPE general-purpose ProLiant servers

• SAP selected SUSE OpenStack Cloud as the IaaS for SAP HANA Cloud

Platform

• SUSE Linux Enterprise Server is the first commercial Linux to be

supported on IBM LinuxONE

5151

FY17 Outlook

“Sustainable, Profitable Revenue Growth Above Market Rate*”

• Growing deferred revenue balance, to be recognized in FY17, is a good

foundation for ongoing growth

• Continued investment in building out the organization to ensure improvements in

execution capacity across all major business functions and geographies

• Further investment in marketing program spend to drive demand generation and

build brand awareness for SUSE (SUSECon - Washington DC, 7-11 November

2016)

* 13-14% market growth in line with SUSE management view of industry analyst estimates 5252

Overview

• Results at the high end of management expectations

• Total Shareholder Return strategy continues

• Final Dividend increased by 50.7% to 49.74 cents (2015: 33.00 cents)

• Full Year Dividend increased by 37.8% to 66.68 cents (2015: 48.40 cents)

• Return of Value to shareholders in 2017

Outlook

• Consistent double digit shareholder returns

• Revenue in FY17 minus 2% to zero

• Compared to FY16 CCY pro-forma with Serena

• FY17 revenue exit rate flat with FY16 and anticipate revenue growth in FY18

• Maintain target net debt at 2.5 times to Facility EBITDA

• Appropriate value enhancing acquisitions

54

Micro Focus Overview and Outlook

Appendix

Consolidated Income Statement

56

Year ended 30 April 2016

$’000

Year ended 30 April 2015

$’000

Revenue 1,245,049 834,539

Cost of sales (135,432) (91,490)

Gross profit 1,109,617 743,049

Selling and distribution costs (416,333) (290,475)

Research and development expenses (259,388) (162,349)

Administrative expenses (138,962) (142,989)

Operating profit 294,934 147,236

Analyzed as:

Adjusted Operating profit 533,514 347,773

Share based compensation (28,793) (15,561)

Amortization of purchased intangibles (181,934) (88,298)

Exceptional items (27,853) (96,678)

Operating profit 294,934 147,236

Share of results of associates (2,190) (788)

Net finance costs (97,348) (55,021)

Profit before tax 195,396 91,427

Taxation (32,424) 10,024

Profit for the period 162,972 101,451

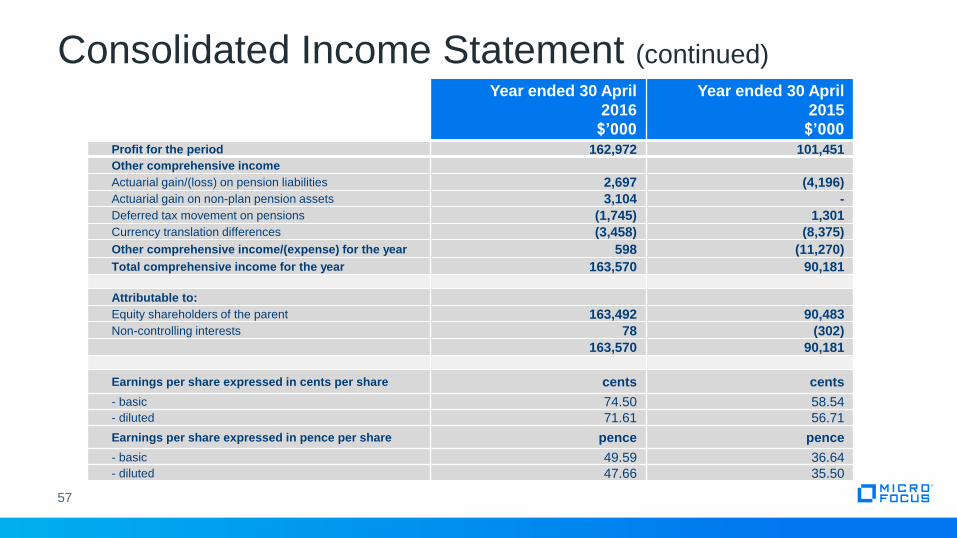

Consolidated Income Statement (continued)

57

Year ended 30 April

2016

$’000

Year ended 30 April

2015

$’000

Profit for the period 162,972 101,451

Other comprehensive income

Actuarial gain/(loss) on pension liabilities 2,697 (4,196)

Actuarial gain on non-plan pension assets 3,104 -

Deferred tax movement on pensions (1,745) 1,301

Currency translation differences (3,458) (8,375)

Other comprehensive income/(expense) for the year 598 (11,270)

Total comprehensive income for the year 163,570 90,181

Attributable to:

Equity shareholders of the parent 163,492 90,483

Non-controlling interests 78 (302)

163,570 90,181

Earnings per share expressed in cents per share cents cents

- basic 74.50 58.54- diluted 71.61 56.71

Earnings per share expressed in pence per share pence pence

- basic 49.59 36.64- diluted 47.66 35.50

Consolidated Balance StatementAs at 30 April 2016

$’000

As at 30 April 2015

$’000

ASSETS

Non-current assets

Goodwill 2,436,168 2,421,745

Other intangible assets 966,555 1,132,221

Property, plant and equipment 40,867 42,896

Investments in associates 12,711 14,901

Long-term pension assets 22,272 14,076

Other non-current assets 4,002 3,909

Deferred tax assets 198,757 249,886

3,681,332 3,879,634

Current assets

Inventories 93 110

Trade and other receivables 268,186 218,645

Current tax receivables 18,016 -

Cash and cash equivalents 667,178 241,324

Assets classified as held for sale 888 888

954,361 460,967

TOTAL ASSETS 4,635,693 4,340,601

LIABILITIES

Current liabilities

Trade and other payables 188,090 161,365

Borrowings 275,256 125,733

Provisions 10,545 49,334

Current tax liabilities 22,426 67,895

Current deferred income 565,480 583,703

1,061,797 988,030

Non-current liabilities

Non-current deferred income 196,483 194,863

Borrowings 1,469,953 1,519,130

Retirement benefit obligations 31,669 32,742

Long-term provisions 14,354 17,919

Other non-current liabilities 3,671 5,264

Deferred tax liabilities 264,038 304,592

1,980,168 2,074,510

TOTAL LIABILITIES 3,041,965 3,062,540

NET ASSETS 1,593,728 1,278,061

58

Balance Sheet (continued)

59

As at 30 April 2016

$’000

As at 30 April 2015

$’000

EQUITY

Ordinary shares 39,573 39,555

Share premium account 190,293 16,087

Merger reserve 988,104 1,168,104

Capital redemption reserve 163,363 163,363

Retained earnings (deficit) 228,344 (96,479)

Foreign currency translation reserve (deficit) (17,006) (13,548)

TOTAL EQUITY ATTRIBUTABLE TO OWNERS OF THE PARENT 1,592,671 1,277,082

Non-controlling interests 1,057 979

TOTAL EQUITY 1,593,728 1,278,061

As reported Year ended 30 April 2016 Year ended 30 April 2015

$'000 % of revenue $'000 % of revenue

Revenue 1,245,049 834,539

Cost of sales (135,432) 10.9% (91,490) 11.0%

Selling and distribution costs (416,333) 33.4% (290,475) 34.8%

Research and development expenses (259,388) 20.8% (162,349) 19.5%

Administrative expenses (138,962) 11.2% (142,989) 17.1%

Total costs (950,115) (687,303)

Operating profit 294,934 147,236

Group Income Statement: Key Ratios

60

EBITDA Reconciliation

61

Year ended

30 April 2016

$’000

Year ended

30 April 2015

$’000

Operating profit 294,934 147,236

Exceptional items 27,853 96,678

Share-based compensation charge 28,793 15,561

Amortization of purchased intangibles 181,934 88,298

Adjusted operating profit 533,514 347,773

Depreciation 11,419 7,674

Amortization of software 1,864 2,189

Adjusted EBITDA 546,797 357,636

EBITDA 509,666 264,986

Amortization of capitalized development costs (19,515) (19,589)

Exceptional items 27,853 96,678

Share-based compensation charges 28,793 15,561

Adjusted EBITDA 546,797 357,636

Adjusted EBITDA less Exceptional items 518,944 260,958

Cash generated from continuing operations 455,730 288,741

Cash conversion ratio = Cash generated from continuing operations

Adjusted EBITDA less Exceptional items87.8% 110.6%

Cash Generated from Operations

62

Year ended 30 April 2016

$’000

Year ended 30 April 2015

$’000

Cash flows from operating activities

Profit after tax 162,972 101,451

Adjustments for:

Net interest 97,348 55,021

Taxation 32,424 (10,024)

Share of results of associates 2,190 788

Operating profit 294,934 147,236

Research and development tax credits (2,041) (2,135)

Depreciation 11,419 7,674

Loss on disposal of property, plant and equipment 109 41

Gain on disposal of intangible assets - (1,603)

Amortization of intangibles 203,313 109,092

Impairment of intangibles - 984

Impairment of long-term assets - 11,642

Share-based compensation 28,793 15,561

Exchange movements (2,915) (87)

Provisions (43,031) 46,485

Changes in working capital:

Inventories 28 39

Trade and other receivables (49,175) 40,127

Payables and other liabilities 30,917 (108,558)

Deferred income (16,603) 21,657

Pension funding in excess of charge to operating profit (18) 586

Cash generated from operations 455,730 288,741

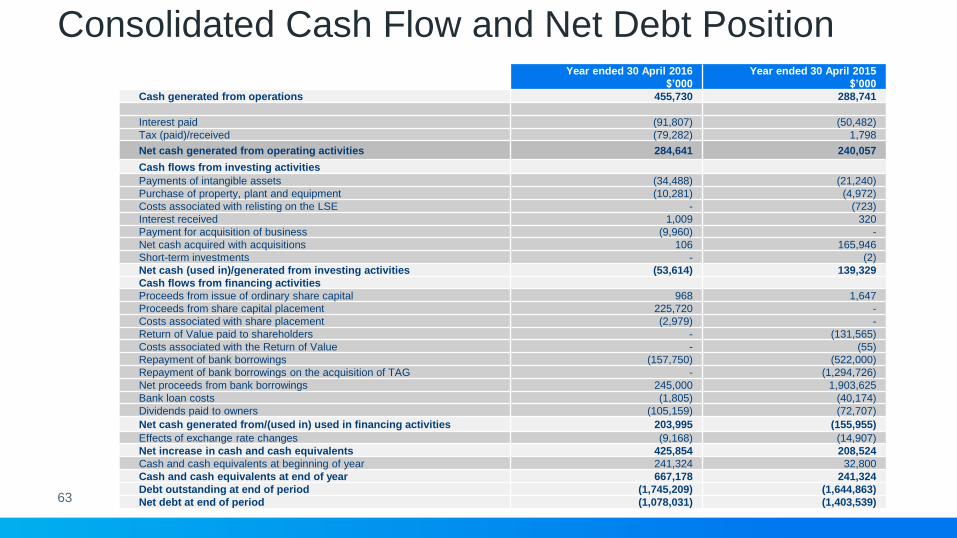

Consolidated Cash Flow and Net Debt Position

63

Year ended 30 April 2016

$’000

Year ended 30 April 2015

$’000

Cash generated from operations 455,730 288,741

Interest paid (91,807) (50,482)

Tax (paid)/received (79,282) 1,798

Net cash generated from operating activities 284,641 240,057

Cash flows from investing activities

Payments of intangible assets (34,488) (21,240)

Purchase of property, plant and equipment (10,281) (4,972)

Costs associated with relisting on the LSE - (723)

Interest received 1,009 320

Payment for acquisition of business (9,960) -

Net cash acquired with acquisitions 106 165,946

Short-term investments - (2)

Net cash (used in)/generated from investing activities (53,614) 139,329

Cash flows from financing activities

Proceeds from issue of ordinary share capital 968 1,647

Proceeds from share capital placement 225,720 -

Costs associated with share placement (2,979) -

Return of Value paid to shareholders - (131,565)

Costs associated with the Return of Value - (55)

Repayment of bank borrowings (157,750) (522,000)

Repayment of bank borrowings on the acquisition of TAG - (1,294,726)

Net proceeds from bank borrowings 245,000 1,903,625

Bank loan costs (1,805) (40,174)

Dividends paid to owners (105,159) (72,707)

Net cash generated from/(used in) used in financing activities 203,995 (155,955)

Effects of exchange rate changes (9,168) (14,907)

Net increase in cash and cash equivalents 425,854 208,524

Cash and cash equivalents at beginning of year 241,324 32,800

Cash and cash equivalents at end of year 667,178 241,324

Debt outstanding at end of period (1,745,209) (1,644,863)

Net debt at end of period (1,078,031) (1,403,539)

Pro-forma Revenues by Geography at Constant Currency

64

Geographic Analysis Revenue

(at constant currency) Year ended 30 April 2016 Year ended 30 April 2015 (Pro-forma) 1

$m % $m %

CDMS

North America 116.2 44.9% 110.6 43.2%

International 108.9 42.1% 114.4 44.7%

Asia Pacific 33.7 13.0% 30.9 12.1%

Total 258.8 100.0% 255.9 100.0%

Host Connectivity

North America 141.0 71.1% 131.8 64.5%

International 48.9 24.7% 59.6 29.2%

Asia Pacific 8.3 4.2% 13.0 6.3%

Total 198.2 100.0% 204.4 100.0%

IAS

North America 108.7 50.2% 115.2 52.9%

International 90.8 41.9% 82.4 37.9%

Asia Pacific 17.2 7.9% 20.1 9.2%

Total 216.7 100.0% 217.7 100.0%

Development & ITOM

North America 79.7 50.6% 100.4 55.4%

International 61.1 38.8% 63.2 34.9%

Asia Pacific 16.6 10.6% 17.7 9.7%

Total 157.4 100.0% 181.3 100.0%

Collaboration & Network

North America 79.6 49.7% 103.4 52.6%

International 67.3 42.0% 75.5 38.4%

Asia Pacific 13.2 8.3% 17.8 9.0%

Total 160.1 100.0% 196.7 100.0%

Micro Focus

North America 525.2 53.0% 561.4 53.2%

International 377.0 38.0% 395.1 37.4%

Asia Pacific 89.0 9.0% 99.5 9.4%

Total 991.2 100.0% 1,056.0 100.0%

SUSE

North America 108.6 42.8% 87.4 40.7%

International 115.6 45.5% 98.4 45.8%

Asia Pacific 29.6 11.7% 28.9 13.5%

Total 253.8 100.0% 214.7 100.0%

TOTAL

North America 633.8 50.9% 648.8 51.1%

International 492.6 39.6% 493.5 38.8%

Asia Pacific 118.6 9.5% 128.4 10.1%

TOTAL 1,245.0 100.0% 1,270.7 100.0%

1 Unaudited

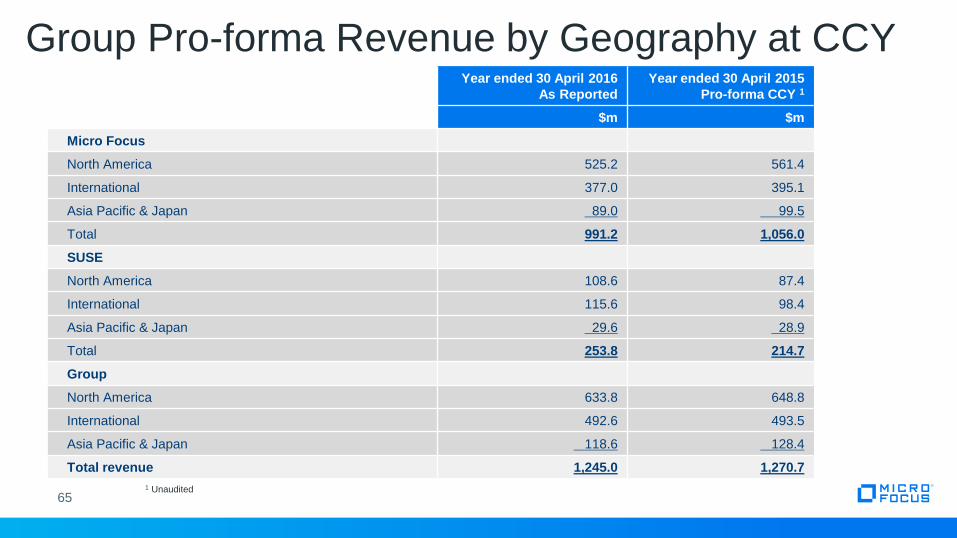

Group Pro-forma Revenue by Geography at CCY

65

Year ended 30 April 2016

As Reported

Year ended 30 April 2015

Pro-forma CCY 1

$m $m

Micro Focus

North America 525.2 561.4

International 377.0 395.1

Asia Pacific & Japan 89.0 99.5

Total 991.2 1,056.0

SUSE

North America 108.6 87.4

International 115.6 98.4

Asia Pacific & Japan 29.6 28.9

Total 253.8 214.7

Group

North America 633.8 648.8

International 492.6 493.5

Asia Pacific & Japan 118.6 128.4

Total revenue 1,245.0 1,270.7

1 Unaudited

North America International(EMEA, LATAM)

APJ

Corporate Operations

Finance IT HR

Product Development

Legal Business Operations & PMO

Field Marketing

Product Management

Go To Market

Product

Development

NA, EMEA & APJ(LATAM from MF

shared team)

Product Management

Field Marketing

Services, Customer Care, Renewals,

Shared Marketing Services, Sales Operations

Channel, Systems

Integrators & OEM Channel, Systems Integrators & Independent Software Vendors

Product Group

Overall Organizational Model: One company with two product portfolios balancing focus with leverage of scale

66

Go To Market

Product Group

SUSE ACV Share by Route to MarketFY16 vs. FY15

67

In aggregate the ACV mix by route to market remained stable in FY16 compared to FY15 as we saw homogenous

contribution to SUSE’s growth from the various routes to market.

67