Audit reporting common mistakes therein - WIRC · PDF fileAudit reporting & common mistakes...

49

0 Audit reporting & common mistakes therein Presented by : C.A. Sandeep Shah

Transcript of Audit reporting common mistakes therein - WIRC · PDF fileAudit reporting & common mistakes...

00

Audit reporting &

common mistakes thereinPresented by :C.A. Sandeep Shah

1

What are we covering today

1

• Relevant Standard on Auditing• Reporting requirements under Companies Act, 2013• Other key points including recent changes• Common mistakes in Auditor’s Report

Reporting standards� SA 700 (Revised) – Forming an Opinion and Reporting on Financial

Statements

� SA 705 – Modification to the Opinion in the Independent Auditor’s Report

� SA 706 – Emphasis of Matter Paragraphs and Other Matter Paragraphs inthe Independent Auditor’s Report

Key points on Reporting Standards• Compliance with auditing standards is mandatory under section 143 (9) & (10) of

Companies Act 2013

• Applies to audit of general purpose Financial Statements– Not to reviews, compilation or agreed upon procedures

• Consistency in format of audit report with clear heading promotes credibility in the global markets

• Management and Auditors Responsibilities paragraph are elaborated– Reduces the ‘expectation gap’ in regard to scope of auditor

• It deals with how to form an audit opinion, reach audit conclusions and issuedifferent types of audit reports– Guidance given for scenarios in which opinions are to be given as ‘Emphasis of

matter’ or ‘Qualification’ or ‘Adverse Opinion’

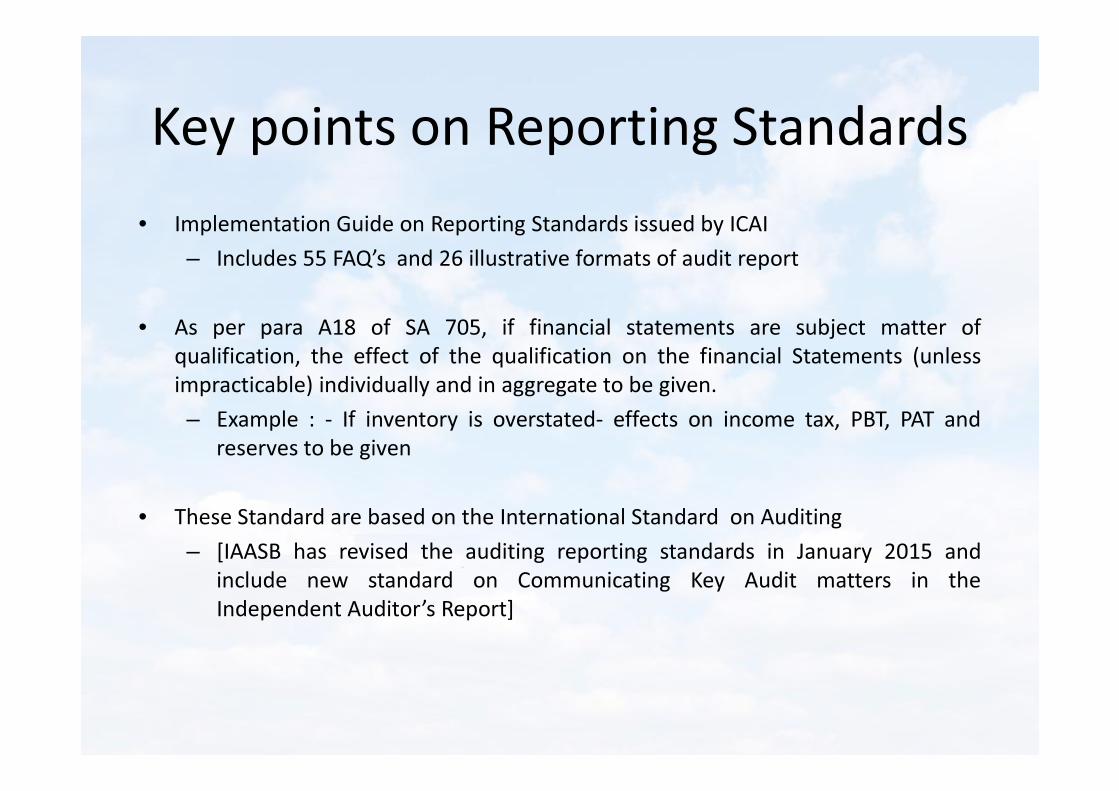

Key points on Reporting Standards• Implementation Guide on Reporting Standards issued by ICAI

– Includes 55 FAQ’s and 26 illustrative formats of audit report

• As per para A18 of SA 705, if financial statements are subject matter ofqualification, the effect of the qualification on the financial Statements (unlessimpracticable) individually and in aggregate to be given.– Example : - If inventory is overstated- effects on income tax, PBT, PAT and

reserves to be given

• These Standard are based on the International Standard on Auditing– [IAASB has revised the auditing reporting standards in January 2015 and

include new standard on Communicating Key Audit matters in theIndependent Auditor’s Report]

Type of Modified Opinion

34

Nature of Matter Giving Rise to the Modification

Auditor’s Judgment about the Pervasiveness of the Effects or Possible Effects on the Financial StatementsMaterial but Not Pervasive

Material and Pervasive

Financial statements are materially misstated

Qualified opinion Adverse opinion

Inability to obtain sufficient appropriate audit evidence

Qualified opinion Disclaimer of opinion

Very subjective and based on auditors judgement - EOM vs Qualification

Difficulty for users of financial statements having EOM but not qualification

Reporting requirements under the Companies Act, 2013

6

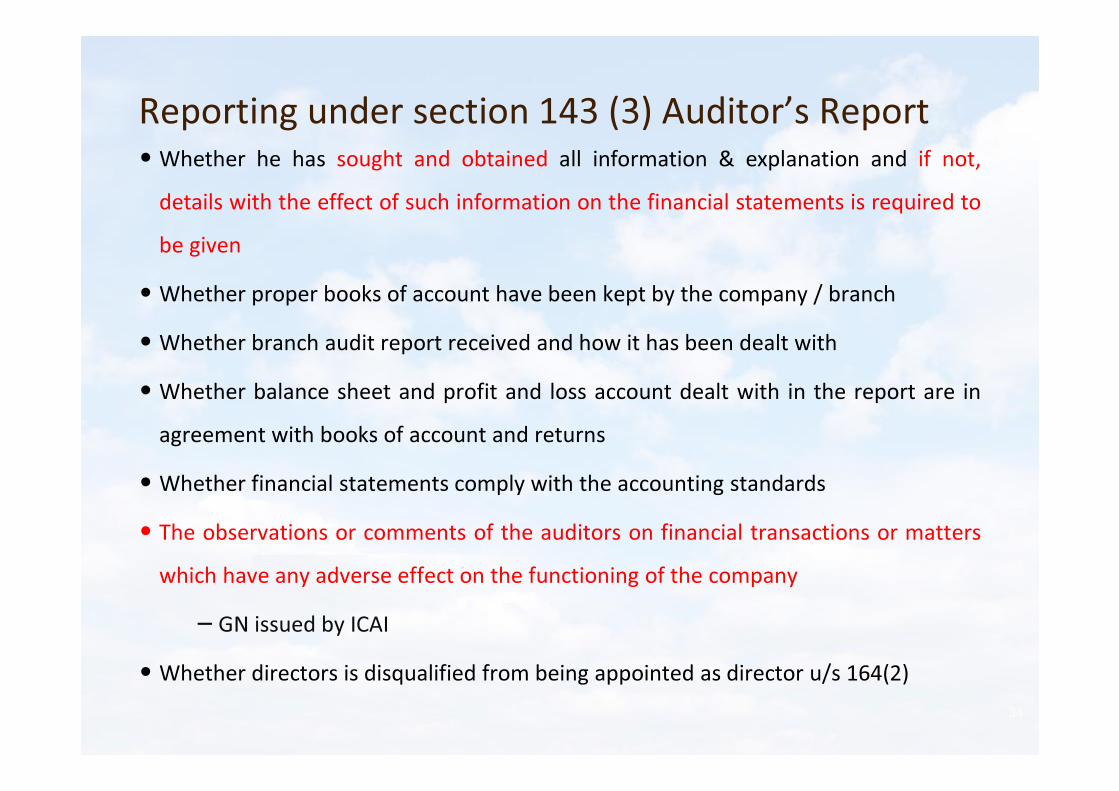

Reporting under section 143 (3) Auditor’s Report • Whether he has sought and obtained all information & explanation and if not,

details with the effect of such information on the financial statements is required tobe given

• Whether proper books of account have been kept by the company / branch• Whether branch audit report received and how it has been dealt with• Whether balance sheet and profit and loss account dealt with in the report are in

agreement with books of account and returns• Whether financial statements comply with the accounting standards• The observations or comments of the auditors on financial transactions or matters

which have any adverse effect on the functioning of the company– GN issued by ICAI

• Whether directors is disqualified from being appointed as director u/s 164(2)34

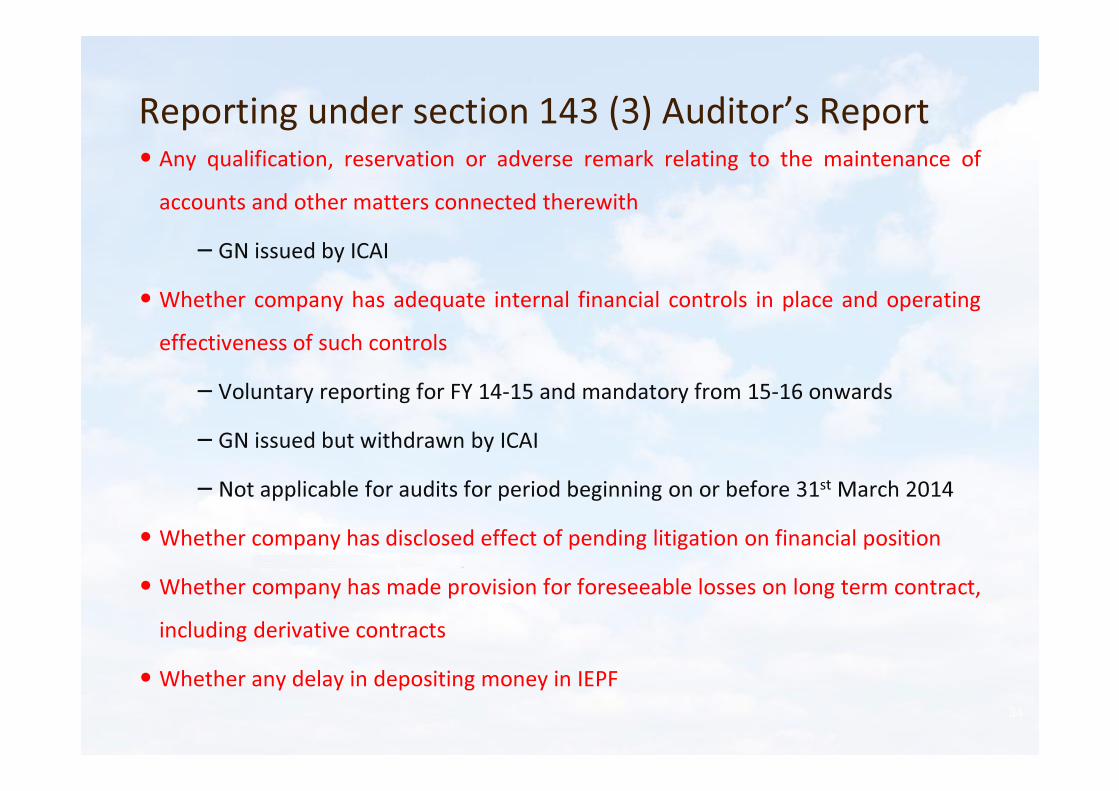

Reporting under section 143 (3) Auditor’s Report• Any qualification, reservation or adverse remark relating to the maintenance of

accounts and other matters connected therewith– GN issued by ICAI

• Whether company has adequate internal financial controls in place and operatingeffectiveness of such controls

– Voluntary reporting for FY 14-15 and mandatory from 15-16 onwards– GN issued but withdrawn by ICAI– Not applicable for audits for period beginning on or before 31st March 2014

• Whether company has disclosed effect of pending litigation on financial position• Whether company has made provision for foreseeable losses on long term contract,

including derivative contracts• Whether any delay in depositing money in IEPF

34

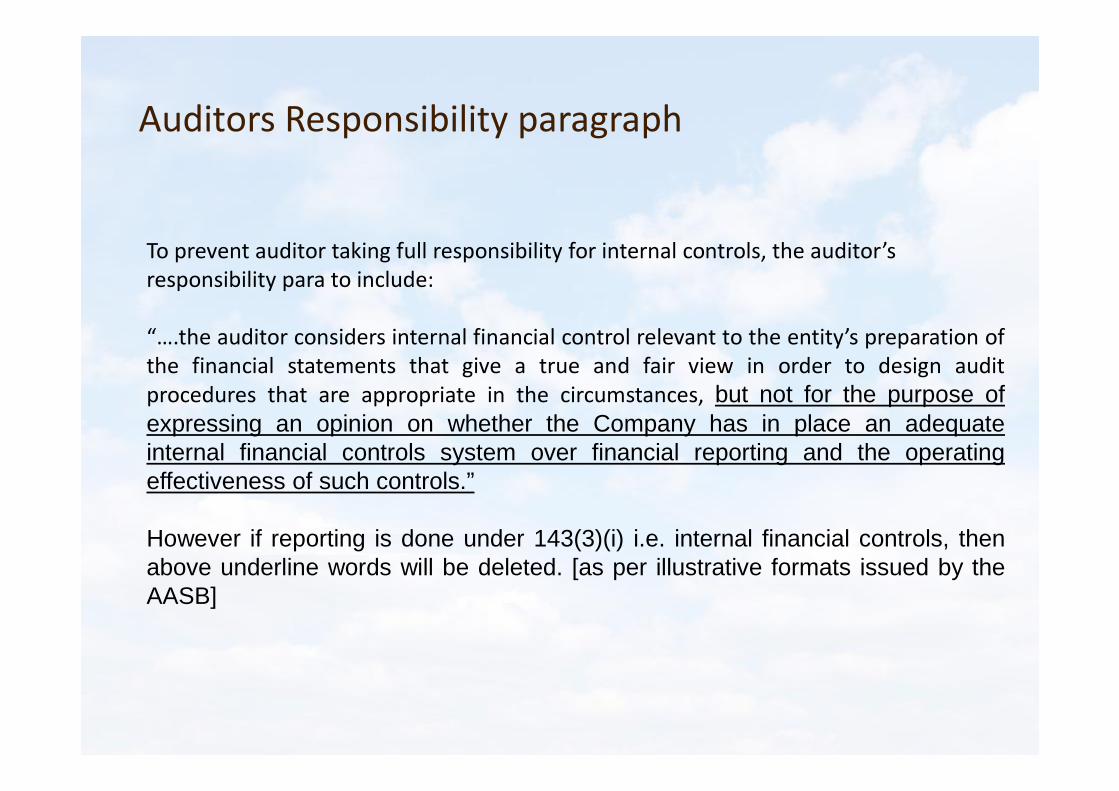

To prevent auditor taking full responsibility for internal controls, the auditor’s responsibility para to include:

“….the auditor considers internal financial control relevant to the entity’s preparation ofthe financial statements that give a true and fair view in order to design auditprocedures that are appropriate in the circumstances, but not for the purpose ofexpressing an opinion on whether the Company has in place an adequateinternal financial controls system over financial reporting and the operatingeffectiveness of such controls.”

However if reporting is done under 143(3)(i) i.e. internal financial controls, thenabove underline words will be deleted. [as per illustrative formats issued by theAASB]

Auditors Responsibility paragraph

CARO Reporting under section 143 (11)• CARO 2015 notified on 10th April 2015 replacing CARO 2003• It is applicable to all companies including foreign companies for the FY

commencing from 1st April 2014 and onwards except following companies:a. Banking company, Insurance company, Non-profit making company under

section 8 of the Act, One person company, small company andb. Private company having paid up capital and reserves not more than Rs. 50

lacs, loan from bank / financial institution not exceeding Rs. 25 lacs andturnover not exceeding Rs. 5 crore at any point of time during the year (all 3conditions must be satisfied).

• CARO 2015 is now also applicable to consolidated financial statements• Guidance note issued by ICAI for reporting under CARO 2015. Also to continue to

apply earlier GN on CARO 2013 to the extent relevant.34

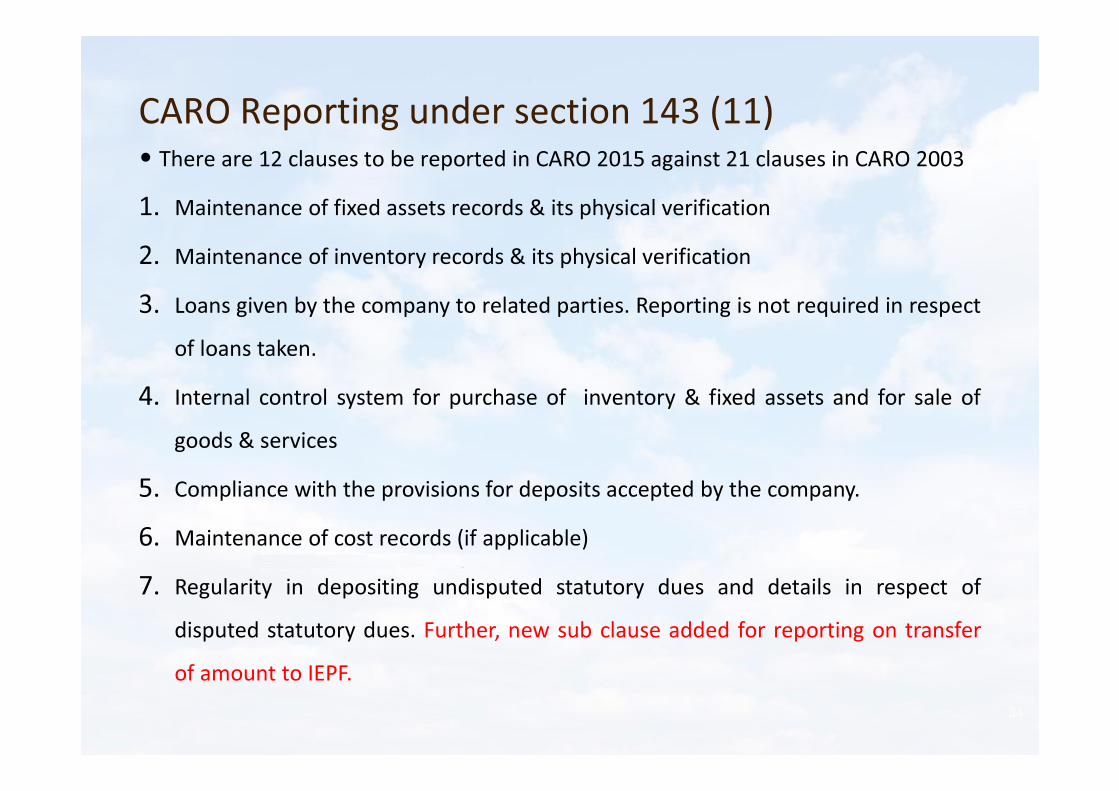

CARO Reporting under section 143 (11)• There are 12 clauses to be reported in CARO 2015 against 21 clauses in CARO 20031. Maintenance of fixed assets records & its physical verification2. Maintenance of inventory records & its physical verification3. Loans given by the company to related parties. Reporting is not required in respect

of loans taken.4. Internal control system for purchase of inventory & fixed assets and for sale of

goods & services5. Compliance with the provisions for deposits accepted by the company.6. Maintenance of cost records (if applicable)7. Regularity in depositing undisputed statutory dues and details in respect of

disputed statutory dues. Further, new sub clause added for reporting on transferof amount to IEPF.

34

CARO Reporting under section 143 (11)8. Accumulated losses and cash loss of the company during the current and

immediately preceding year9. Default in repayment of dues to financial institution or bank or debenture holders10.Guarantee given by the company for loans taken by others from banks and

financial institutions, the terms whereof are prejudicial to the interest of thecompany

11.Application of term loans for the purpose for which they were obtained12.Nature and amount involved in fraud on or by the company reported during the

year

34

• If CARO is not applicable it has to be stated in the audit report.

• There was mixed practice – some auditors mentioned non-applicability for eachclause separately, and others clubbed all non-applicable clauses in an openingparagraph. ICAI permits both practices .

13

Fraud Reporting

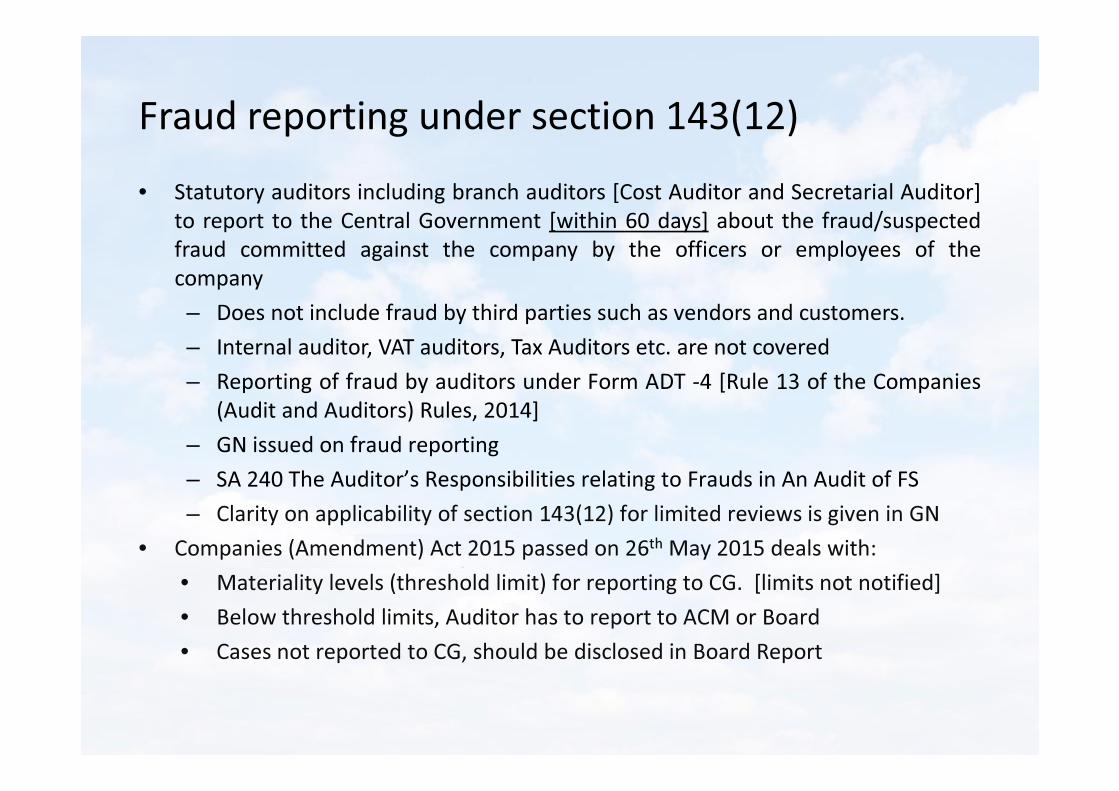

Fraud reporting under section 143(12)• Statutory auditors including branch auditors [Cost Auditor and Secretarial Auditor]

to report to the Central Government [within 60 days] about the fraud/suspectedfraud committed against the company by the officers or employees of thecompany– Does not include fraud by third parties such as vendors and customers.– Internal auditor, VAT auditors, Tax Auditors etc. are not covered– Reporting of fraud by auditors under Form ADT -4 [Rule 13 of the Companies

(Audit and Auditors) Rules, 2014]– GN issued on fraud reporting– SA 240 The Auditor’s Responsibilities relating to Frauds in An Audit of FS– Clarity on applicability of section 143(12) for limited reviews is given in GN

• Companies (Amendment) Act 2015 passed on 26th May 2015 deals with:• Materiality levels (threshold limit) for reporting to CG. [limits not notified]• Below threshold limits, Auditor has to report to ACM or Board• Cases not reported to CG, should be disclosed in Board Report

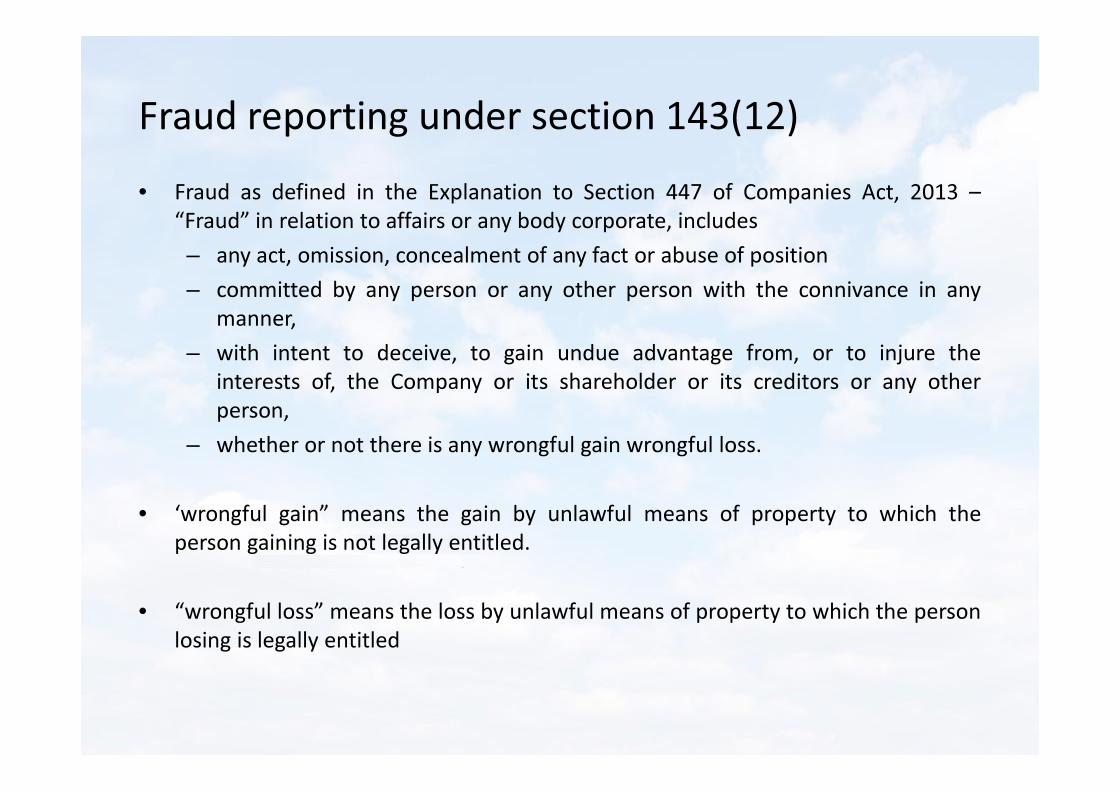

Fraud reporting under section 143(12)• Fraud as defined in the Explanation to Section 447 of Companies Act, 2013 –

“Fraud” in relation to affairs or any body corporate, includes– any act, omission, concealment of any fact or abuse of position– committed by any person or any other person with the connivance in any

manner,– with intent to deceive, to gain undue advantage from, or to injure the

interests of, the Company or its shareholder or its creditors or any otherperson,

– whether or not there is any wrongful gain wrongful loss.

• ‘wrongful gain” means the gain by unlawful means of property to which theperson gaining is not legally entitled.

• “wrongful loss” means the loss by unlawful means of property to which the personlosing is legally entitled

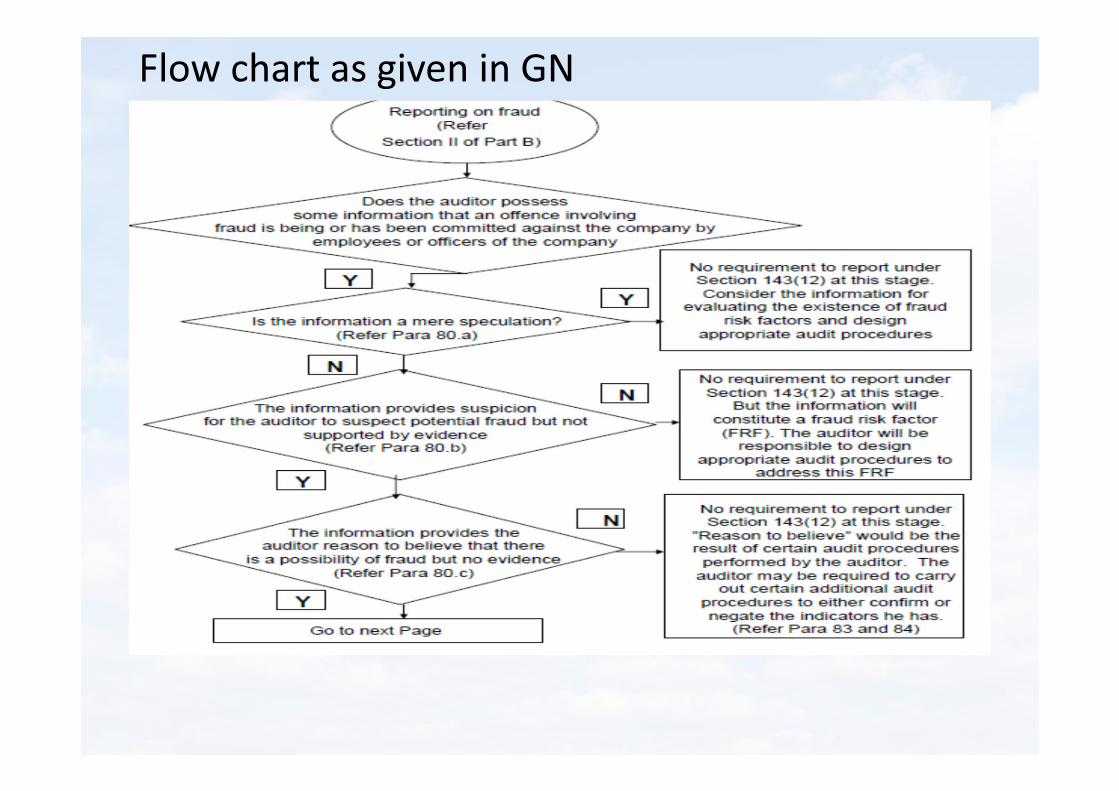

Flow chart as given in GN

(continued) Flow chart as given in GN

Past cases of frauds – widely debated in forums1. National Spot Exchange Limited (NSEL)2. Financial Technologies (India) Limited (FITL)3. Reebok4. Lilliput kidswear5. Satyam Computer Services6. Wipro7. Dena Bank8. Oriental Bank of Commerce (OBC)

34

20

Other Key Points – including Recent Updates• Requirement of italic or bold is done away.• Any matter required to be included in the audit report u/s 143 is answered in the

negative or with a qualification, the report shall state the reasons therefor• Clarification issued by ICAI on Auditor’s Report in respect of FS for accounting year

beginning before 1st April 2014– Auditor should report on the relevant clauses only for that part of the FY upto

which the concerned provisions of the CA 1956 were in force (i.e. upto 31st

March 2014)– To clearly bring out the facts in ‘Other Matters’ paragraph

• Auditor shall pay for damages to the Company, statutory bodies or authorities orany other persons for loss arising out of incorrect or misleading of particularsmade in his report.

35

Other Key Points – including Recent Updates• Qualifications / observations / comments on Financial transactions which have

adverse effect on company’s functioning to be read at AGM and kept forinspection

• Auditor shall attend AGM, unless expressly exempted by the company – he canalso be represented by a representative

• The AASB issued illustrative formats of Independent Auditor’s Report onstandalone and CFS under the Companies Act, 2013.

– Audit report on CFS will now be addressed to Members of the Company– In case of CFS, Components auditors reports also to be considered including

CARO• The Standing Committee on Finance has raised the concern of conflict of mandate

with regard to disciplinary matters between the NFRA and ICAI.35

Other Key Points – including Recent Changes• Sec 146-Auditor (or authorised representative) to attend all generalmeeting unless exempted by Company (general penalty can be levied u/s450). If company fails to give notice- minimum fine 25000 & extend upto5.00 lac, every officer imprisonment upto 1 year or with minimum fine ofRs. 10,000 & extend upto 1.00 lac or both

•As per Rules, criminal liability of audit firm shall devolve only on theconcerned partner who acted in fraudulent manner. Liability of fine will beon the firm.

370

Quality Review Board• As per the QRB activity report for the year 2012-2013, followings aspects are

covered in regard to audit reporting

– Whether auditor has appropriately dealt with in his report the deviations fromaccounting standards

– Where audit report is qualified• Qualification to be clear and unambiguous manner• Whether quantified ? If not, whether adequate justifications is provided• Whether the auditor has considered the overall effect of the qualifications

on the true and fair view presented by the financial statements

– Compliance with SA in preparation of audit report

Audit report under clause 41 of listing agreement• Format of the LRR and audit report is given in listing agreement

– However there no paragraph headings as per SA

• Qualifications in report - the company shall by way of note state how the same hasbeen resolved, and if not resolved reasons therefor and the steps that they intend totake in the matter

• Quarterly Financial Results will be treated as incomplete if the same is notaccompanied with the LRR or the audit report as the case may be

• Timeline given for quarterly closure and year end closure of accounts. [60 days forlast quarter audited results] However, Audit Report need not be submitted inrespect of audited final quarter and year end financial results

34

SEBI – Mechanism to process qualified annualreports filed by listed entities

34

Listed companies to file form A (unqualified/Matter of Emphasis) orform B (Qualified/Subject To/Except For Audit Report) along withannual report with stock exchangeListed companies to file form A (unqualified/Matter of Emphasis) orform B (Qualified/Subject To/Except For Audit Report) along withannual report with stock exchange

SEBI – Qualified Audit Report review Committee (QARC) if finds the qualification significant and explanation by companies unsatisfactory then refer audit report to FRRBSEBI – Qualified Audit Report review Committee (QARC) if finds the qualification significant and explanation by companies unsatisfactory then refer audit report to FRRB

If ICAI – FRRB opines that qualification is justified, SEBI may mandaterestatement of accounts of the entity and require the entity toinform its shareholders through an announcement to the respectivestock exchange

If ICAI – FRRB opines that qualification is justified, SEBI may mandaterestatement of accounts of the entity and require the entity toinform its shareholders through an announcement to the respectivestock exchange

ICAI announcement on Reporting on ComponentsComponent Component is Material

to financial statement (Yes / No)

Disclosure in Principal Auditor’s Report

Unaudited No Optional disclosure[if reported, ‘Other Matters’]

Audited by another auditor

No Optional disclosure[if disclosed, ‘Other Matters’]

Audited by another auditor

Yes Disclosure to be made in‘Other Matters’

Unaudited Yes Report to be modified

Withdrawing Auditors Report

• Financial Technologies (India) Ltd – where the audit report for the year ended 31st March 2013 was withdrawn due to purported payment crisis and withdrawal of the audit report at one of its Subsidiaries– Standard on Auditing (SA) 560, which allows an auditor to change his opinion

if ‘subsequent events’ require it. ?

• Essar Oil Ltd – where the audit reports for 3 years were re-issued pursuant to thecompany amending its FS (post-adoption by the members) for reversal of eligibilityof subsidy pursuant to the order of the Hon’ble Supreme Court after obtainingapproval of Ministry of Corporate Affairs

• Nagarjuna Fertilizers and Chemicals Ltd – where the audit report for the year ended 31st March 2013 was re-issued pursuant to the company amending its FS (pre-adoption by the members) for reversal of dividend declaration

• Others like Lillliput, Tata Finance Limited

Some of the companies having Name of listed company No of qualification EOM

Air India Limited* 11 4MCX Stock Exchange Limited 3 1Steel Authority of IndiaLimited 1 10Tech Mahindra Limited 1 4Unitech Limited 1 3MTNL 1 1Spice Jet Limited 1 1BSNL 31 2

* F.Y. 2012-13

30

Common mistakes• Auditor’s Comment• Auditor has signed the Auditor’s

report prior to the date when the financial statements were signed and authenticated by the director of the company.

• Auditor has mentioned his membership number “F” is prefixed to Auditor’s Report.

• Opening paragraphs of the Auditors Report states to have “examined the attached Balance Sheet…”

• Requirements• SA – 700 (Para – 26) Since the Auditor’s

responsibility is to report on the FinancialStatements as prepared and presented by themanagement, the auditor should not date thereport earlier than that the date on which theFinancial Statements are signed or approvedby management.

• SA – 700 (Para – 28) Neither Institute allotsMembership Number to its members with anyprefix like “F” or “A” nor SA 700 permits to useof such prefixes with the membership numberin the Auditors Report.

• Term ‘examined’ signifies wider function thanthe actual responsibility of the auditor. Auditorshould have used the word ‘audited’ ratherthan using the word ‘examined’ to reflect hiscorrect responsibility.

Common mistakes (contd..)• Auditor’s Comment• In the Auditor’s Reports no reference was

made to the Cash Flow Statement in opening paragraph and opinion paragraph

• Noted that, although the auditors havequalified their report with regard to non-compliance of certain accountingstandards; they have omitted to report thequantification of the possible effect eitherindividually or in aggregate.

• In the opinion para, it was mentioned that “In the case of the Profit and Loss Account, of the loss for the year ended on that date”

• Requirements• SA 700 – (Para – 9) The auditor’s report

should identify the cash flow statement as apart of financial statements and further, alsoexpress an opinion on the cash flowstatement audited.

• With regards to SA 700, it is viewed thatwhile expressing opinions other thanunqualified, the auditor should report thereasons for such opinion and should alsoreport the quantitative impact of such onthe financial statements of each, individuallyas well as their aggregate. Where it is notpracticable to quantify the same, theauditor must quantify the same based onestimates provided by the management.

• However there was profit in the currentyear, reference to loss is incorrect.

• Auditors’ comment• “We have audited the attached balance

sheet of X Ltd. as at 31st March, XXXXand profit & Loss Account for the yearended on that date annexed thereto.The financial statements are theresponsibility of the company’smanagement…”

• An unqualified opinion given referring to the following comment :“In our opinion, the balance sheet, theprofit and loss account, the cash flowstatement dealt with by this reportcomply with the accounting standardsreferred to in sub-section (3C) of section211 of the Companies Act 1956”

Requirement• Paragraph 10 of SA 700 requires the

auditor to state the responsibility ofmanagement towards the financialstatement along with their ownresponsibility to express an opinion onthe financial statements based on audit.The latter has been omitted here.

• From the Annual Report of theCompany, there were many non-compliance of Accounting Standards,but still the auditors have given cleanreport.

Common mistakes (contd..)

Common mistakes (contd..)• Auditors’ comment• The auditor had expressed opinion on

the Balance Sheet, the Profit and LossAccount as well as on the accounts ofthe company ‘subject to a note’ statingchange in an accounting policy ofdepreciation method.

• Auditor often omit to state whether thestatements prepared are in conformitywith the financial reporting frameworkand statutory requirements relevant tothe company.

• Requirement• “Subject to” is improper although the

company had made sufficient disclosure ofchange in accounting policy. It was felt thatperhaps auditors were not in agreementwith the management for change indepreciation method. In that case, ‘subjectmatter of qualification’ is ambiguous.

• SA 700 – (Para – 20) The opinionparagraph of the auditor’s report shouldclearly indicate the financial reportingframework used to prepare the FS andstate the auditor’s opinion as to whetherthe FS give a true and fair view inaccordance with the financial reportingframework and, where appropriate,whether the FS comply with the statutoryrequirements.

Common mistakes (contd..)• Auditors’ comment• Report was not addressed to anyone

• Membership no. of auditor was not mentioned in Audit Report, CARO, Balance Sheet, Statement of Profit and Loss.

• Requirement• SA – 700 (Para – 8) The auditor’s report

should be appropriately addressed asrequired by the circumstances ofengagement and applicable laws andregulations. Ordinarily the auditor’s reportis addressed to the authority appointingthe auditor [Under CA 2013, audit reporton CFS will be addressed to Members,earlier it was addressed to Board ofDirectors]

• SA- 700 (Para – 28) The partner/proprietorsigning the audit report should alsomention the membership number assignedby the ICAI. Also required on BS and P&L.

• Firm Registration No. is also required to begiven as per ICAI

Common mistakes (CARO)• Auditors’ comment• None of the fixed assets have been revalued

during the year.

• This audit report is being issued to reviseour Audit Report dated March 29th, 2014for the year ended March 31st, 2014. Thisreport incorporates the amendmentannounced on February 7th, 2014 to theparagraph on “Auditors’ Responsibility”. Italso corrects the heading from Auditors’Report to “Independent Auditors’ Report”.

• The Annexure to the Auditors report isdated 18th June 2014 which is different fromthe revised report.

• In our opinion and according to theinformation and explanations given to us,the Company has not defaulted inrepayment of dues to a financial institutionor banks.

• Requirement• The requirement as above was under

erstwhile MAOCARO.

• The reference to original audit reportdated March 29,2014 for audit for theyear ending 31st March 2014 iserroneous (audit report date prior todate of year end).

• The Annexure to the Auditors report isdated 18th June 2014 which is differentfrom the revised report dated 11th June2014.

• The comment is silent regard to defaultsin repayment to debenture holders

Common mistakes (CARO)• Auditors’ comment• “The management has conducted

physical verification of the fixed assetsduring the year and we are informedthat discrepancies noticed were notmaterial.”

Requirement• The use of words “We are informed

that…”, prima facie creates animpression that no documentaryevidence was available to substantiatethe verification and that the auditor haswholly relied on management’srepresentation. However, the auditor’sduty us to express his opinion and notjust disclose the information given bythe management, hence not as perCARO. [It may start with According toinformation and explanation given tous….]

Common mistakes (CARO)• Auditors’ comment• “All assets not verified but there is a regular

programme of verification. The same isreasonable. Management has explainedthat no material discrepancies werenoticed.”

• “Programme of physical verification isreasonable, though all the assets notverified. Management is in process ofidentifying discrepancies, if any, on suchverification.”

• “Physical verification of the fixed assets is covered under a scheme verification over a period of three years. No serious discrepancy was noticed on such verification during the period.”

Requirement• CARO requires that auditor should use his

judgment to determine discrepancy ismaterial or not. Duty has been caste onauditors to express his opinion. In the givencase, auditor has relied on the management’sexplanation and has not used his judgment.

• Comments are not as per requirement. Itindicates lapse of the policy that physicalverification of even those assets which weretaken for verification is not complete.Inappropriate conclusion made by auditorthat company is having regular programmefor verification.

• The auditor omitted to comment on thereasonableness of the frequency of physicalverification of fixed assets as conducted bythe management.

Common mistakes (CARO)• Auditors’ comment• “The company has maintained proper

records of inventory. No materialdiscrepancies were noticed on physicalverification of inventory except as recordedby excise department as per note…”

• “(a) The parties to whom loans have beengiven by the company are repaying theprincipal amounts as stipulated and interestthereon wherever applicable.

• (d) In case of overdue amounts exceedingRs.1 Lakh reasonable steps have beentaken by the company for recovery ofprincipal amount and interest thereon andnecessary provisions have been madewherever such amounts appear to bedoubtful of recovery”

Requirement• CARO requires the auditor to comment on

whether the discrepancies noticed havebeen adequately dealt with. Here, theauditor has only reported on discrepanciesby referring to the note but he has omittedto comment on whether thosediscrepancies were properly dealt with inthe books of accounts.

• It is observed that the stated comments areproviding contradictory information. If theparties are regular in repaying the principalas well as the interest then the question ofoverdue amounts does not arise.

Common mistakes (CARO)• Auditors’ comment• “In our opinion and according to the

information and explanation given to usduring the course of audit, there areadequate internal control procedurescommensurate with the size of thecompany and nature of the businesswith regard to the purchase of inventoryand fixed assets…”

• “In our opinion, there is an adequateinternal control procedurecommensurate with the size of thecompany and nature of business, forpurchase and sale of strores, rawmaterial including components, plantand machinery, equipment and similarassets.”

Requirement• The auditor has commented upon ‘Internal

Control Procedures’ instead of ‘Internal ControlSystem’ as required by CARO. It is further notedthat ‘System’ is a broader terms, as it refers toboth ‘procedures’ and ‘policies’. Hence reportingonly on ‘procedures’ cannot be considered tocomply with reporting of CARO.

• Further, the auditor has reported only in contextof purchase of inventory and fixed assets but hasomitted to report on adequacy of internalcontrol system w.r.t. sale of goods and services.

• As per CARO, the auditor is required to repot ontwo aspects. Firstly, on the adequacy of theinternal control in regard to purchase ofinventory and fixed assets and for sale of goodsand services and secondly, whether there was acontinuing failure to correct major weakness insuch internal controls. It is frequently noted thatwhilst the auditors comment on the first part,they often omit to report on the second aspect.

Common mistakes (CARO)• Auditors’ comment• “The company is regular in depositing

undisputed statutory dues includingprovident fund, investor education andprotection fund, employee stateinsurance, income tax, sales tax, wealthtax, custom duty, excise duty, Cess andother statutory dues with theappropriate authorities. Late deposit ifany has been attached in the Form 3CDattached.”

• It has been noticed that the auditor has reported only in context of ‘undisputed’ statutory dues and is silent on ‘disputed’ statutory dues.

Requirement• It is noted that whereas CARO requires

‘disclosure of amount’ which are in arrearsfor the period of more than 6 months, theauditor has simply reported the means i.e.Form 3CD where such information isavailable. It was further viewed that Form3CD is a pert of Tax Audit Report and hencethe requisite information for neitheravailable in CARO report or in the financialstatements attached. Accordingly, theauditor has not complied with thereporting requirement.

• As per clause (vii)(b) of CARO, the auditor isrequired to report on specified statutorydues that have not been deposited onaccount of any dispute. In case there are nodues which have not been deposited onamount of dispute then the auditor shallexplicitly report it, rather being silent on it.

Common mistakes (CARO)• Auditors’ comment• “The company has no accumulated and

cash losses at the end of the financial year.”

• “According to the information andexplanations given to us, no fraud on orby the company has been noticed orreported during the course of our audit”

Requirement• The auditor has not complied with CARO as

it is to be noted that although the auditorhas reported with regards to currentfinancial year but has omitted to report onthe status of the cash losses ‘in theimmediately preceding financial year’.

• Further, the auditors have not reportedwhether such accumulated losses are lessthan 50% of its net worth or not.

• The use of words ‘during the course of ouraudit’ indicates that the scope of the auditorwas restricted only to frauds noticed orreported during the course of their audit,whereas the auditor is required to report onany fraud noticed or reported on or by thecompany during the year.

Common mistakes (CARO)• Auditors’ comment• “There was no disposal of a substantial

part of fixed assets during the year”

• “The Company has not accepted anydeposits from the public”

Requirement• The requirement as per CARO is to report on If

a substantial part of fixed assets have beendisposed off during the year, whether it hasaffected the going concern. However theauditors have not reported about goingconcern.

• The requirement as per CARO is to also reporton if an order has been passed by CompanyLaw Board or National Company Law Tribunalor Reserve Bank of India or any Court or anyother Tribunal whether the same has beencomplied with or not. However the auditorshave not reported in regard to the aboverequirement.

Common mistakes (CARO)• Auditors’ comment• “In our opinion, the Company is not

dealing in or trading in shares,securities, debentures and otherinvestments. Accordingly, the provisionsof Clause 4(xiv) of the Order are notapplicable to the Company.”

• “The company is not dealing in ortrading in shares, securities, debenturesand other investments. Therefore, theprovisions of clause (xiv)………are notapplicable”

• “The company has not made anypreferential allotment of shares duringthe year”

Requirement• As per the requirement of CARO, reporting is

also required for whether the shares,securities, debentures and other investmentshave been held by the company, in its ownname except to the extent of the exemption,if any, granted under section 49 of the Act.However the company has not reported inregard to above matter.

• However the company is disclosing theinvestment income as income fromoperations. Hence this clause will beapplicable to the company.

• However during the year shares are allottedto KMP (directors) as per related partydisclosures.

Common mistakes (CARO)• Auditors’ comment• Where each of such transaction (excluding

loans reported under paragraph (iii) above)is in excess of `5 lakhs in respect of anyparty, the transactions have been made atprices which are prima facie reasonablehaving regard to the prevailing marketprices at the relevant time.

• In case of an NBFCAccording to the information and explanationsgiven to us, the Company has not accepted anydeposit from the public during the year. Inrespect of unclaimed deposits, the Companyhas complied with the provisions of Sections58A, 58AA or any other relevant provisions ofthe Companies Act, 1956 and the Companies(Acceptance of Deposits) Rules, 1975, asapplicable to the Company, with regard to thedeposits accepted from the public prior to 1November, 2006.

Requirement

• The requirement to report is with referenceto aggregate transactions above 5.00 lacs inrespect of each party and not only thosetransactions which is above 5.00 lacs

• Since the Company is a NBFC, the applicableRule will be “Non-Banking FinancialCompanies Acceptance of Public Deposits(Reserve Bank) Directions, 1998”

– In case the company is registered underHousing Finance company, theapplicable Rule will be NHB DirectionsRules 2010.

• Auditors’ comment

• According to the information andexplanations provided by themanagement, we are of the opinion thatthe particulars of contracts orarrangements referred to in section 301of the Act that need to be entered intothe register maintained under section301 have been so entered. Accordingly,sub clause (b) of clause (v) of the Orderis not applicable to the Company for thecurrent period

• Requirement

• The comment in underline is not inaccordance with the requirement ofCARO. If the transactions have beenentered in the register maintained u/s301, the auditor should havecommented that none of thetransactions in respect of each party arein excess of Rs. 5.00 lacs and hence subclause (b) is not applicable

Common mistakes (CARO)

47