Audit Readiness Guidebook - New York City Charter School Center

79

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK Audit Readiness Guidebook Internal Control Audits by the New York Office of the State Comptroller 1

Transcript of Audit Readiness Guidebook - New York City Charter School Center

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Audit Readiness Guidebook Internal Control Audits by the New York Office of the State Comptroller

1

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Dedication The Center for Charter School Excellence dedicates this guidebook to the fiscal staff and management of Charter Schools in New York City and throughout the country.

Charter school fiscal staff and management’s commitment to ensuring charter schools meet their financial and regulatory requirements help the charter schools they serve to fulfill their missions.

A note of thanks The Center for Charter School Excellence would like to thank the following people and organizations for their contributions and commitment to the development and distribution of this guidebook.

Center for Charter School Excellence

Matt Candler, Chief Operating Officer Vinice Davis, Director of School Operations Tony Lopez, VP for Leadership and Resource Development Tracy Wright, Administrative Assistant Fiscal Management Associates, LLC

Wendy Pomeroy, Senior Consultant and Lead Author Hilda H. Polanco, Managing Director Stuart Cohen, Manager, Consulting and Training Services Dipty Jain, Senior Consultant Sarah Walker, Intern

1 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 1

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Legal notice: The contents of this publication are believed to be accurate. However, this publication is not and should not be considered, or relied upon, as a substitute for the services of an experienced accountant/auditor in reviewing, analyzing and addressing accounting/auditing and/or fiscal related issues. Notwithstanding anything in this publication or any communications or writing to the contrary, it is expressly understood and agreed by the Center for Charter School Excellence (CCSE) that Fiscal Management Associates, LLC shall not be deemed liable in contract or in tort for any damages, harm or injuries arising out of or relation to CCSE’s use or reliance on this publication, including but not limited to any and all direct, consequential and/or incidental damages and expenses incurred by NYC Charter Schools or any third-party. It is further understood and agreed by CCSE that Fiscal Management Associates, LLC shall not be deemed liable for the content of any websites referred to or references in this publication. Material in this publication is subject to change without notice. Copyright © 2006 Fiscal Management Associates, LLC. New York, NY 10018. All rights reserved. Any reproduction (including any portion thereof) of this publication by any person for any use of this publication other than CCSE must be pursuant to the prior written approval of Fiscal Management Associates, LLC. No trademark, copyright or other notice should be altered, removed or excluded from copies of this publication, including any portions thereof.

2 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 2

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Table of Contents i. Background…………………………………………………... 5

Why are we being audited? When will it happen? What is being audited? What are the stakes?

ii. How do we prepare?............................................. 8

What is being audited - the key high-risk audit areas Learn what details the Comptroller may focus on in each audit area Establish and prepare the team (Board, Management and

Staff)Complete a Self-Assessment to identify potential areas of weakness

Create an Audit-Prep Workplan iii. How do we live through it?................................... 16

The 7 Steps to the audit process and how to respond iv. How do we handle the results?............................. 29

Create a Corrective Action Plan Understand how the audit is distributed publicly

v. Appendix………………………………….…………………… 32

Section 1: Self-Assessment Checklist Section 2: Comptroller’s Findings for School District Audits Section 3: Audit-Prep Workplan template Section 4: How Do We Live Through It? Checklist Section 5: Tips for Working with the Auditors Section 6: Corrective Action Plan template Section 7: Sample Comptroller Document Request Section 8: List of Website Resources in this Guidebook Section 9: OSC What to Expect from an Audit

3 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 3

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

How to use this guidebook.

This guidebook is designed logically. Look for these symbols throughout the guidebook:

√√ ACTION ITEM

APPENDIX REFERENCE

4 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 4

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

i. Background

1. Why are we being audited? 2. When will it happen?

3. What is being audited?

4. What are the stakes?

1. Why are we being audited?

In June 2005, the New York State legislature passed the School District Accountability Act1 to improve school district and charter school internal control structures and to increase the effectiveness of fiscal oversight mechanisms. This Act was legislated in response to several high-profile New York State public school district accounting scandals.

• The legislation requires the Office of the State Comptroller (Comptroller) to audit each school district, charter school and BOCES2 by March 31, 20103.

• The results of these audits will be reported to the Governor, legislature and media, and will posted on the Comptroller’s website4, accessible to the general public.

1 See chapter 263 of the Laws of 2005, New York State Legislature. 2 Board of CooperativeEducational Services (BOCES) 3 Charter Schools Institute, Reference Guide for Audits of Charter Schools Authorized by the State University Board of Trustees, 2nd Edition, State University of New York, July 2006. http://www.newyorkcharters.org

4 See http://www.osc.state.ny.us/localgov/audits/2006/schools/index.htm.

5 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 5

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Charter Schools are included in the School Accountability Act because they are designated as public schools and fall under the authority of the Comptroller for audits.

Who is being audited? The Charter School is being audited, -- the organization with the

Charter.

The charter school Trustees have ultimate fiscal responsibility for oversight of the fiscal integrity of the school.

2. When will it happen?

• All charter schools must be audited before March 31, 2010.

• Schools are selected for audit based on date of charter, oldest to newest.

• The order of the audits can also be influenced by other factors. For example,

o the Comptroller could choose to audit an individual charter school more than once before March 31, 2010, if it finds significant concerns that require a follow-up audit.

o schools associated with the same charter/education management organization (CMO/EMO) may be scheduled concurrently or in close succession; and

o taxpayer complaints, allegations of improprieties or other relevant information that comes to the Comptroller’s attention through newspaper articles, or certain financial indicators.

• The school will get just one week notice from the Comptroller prior to the start of the audit.

3. What is being audited?

The Comptroller will be looking at internal control systems.

Internal control systems are designed to identify and address key areas of fiscal risk. Internal control systems exist to prevent loss of school assets.

6 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 6

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Internal control audits have a different focus from financial statement audits. Auditors review the same financial documents and processes, but ask different questions.

Audits of internal control5 determine:

o Are fiscal polices and procedures and other internal control systems sufficiently in place to safeguard the assets of the organization?

Audits of financial statements determine:

o Are financial statements of the organization a reasonable representation of its financial condition?

o Are there potential weaknesses in the organization’s internal control systems?

4. What are the stakes?

The Comptroller’s Audit Report is publicly distributed to:

State Chartering authorizers (SED, SUNY, or DOE)

NYC Director of the Division of the Budget

NYC Mayor’s Office of Operations

Governor & state legislative leaders

Posted on Comptroller’s website, available to the general public

Media, often with press release

Because the distribution of the report is accessible to the general public and directly distributed to the media, government regulators and legislators, there are potential impacts for

the reputation of charter schools in general with potential for future legislation and increased regulation;

the individual charter school, including the chartering authorizer renewal process, the financial audit process by the school’s external auditors, ease of access to private and public funding.

5 AU319, American Institute of Certified Public Accountants (AICPA) professional standards.

7 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 7

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

ii. How do we prepare?

1. Know what is being audited - the key high-risk audit areas

2. Learn what details the Comptroller may focus on in each audit area

3. Establish and prepare the school team (Board, Management, Staff).

4. Complete a Self-Assessment to identify potential areas of weakness

5. Create an Audit-Prep Workplan.

√√ 1. What is being audited - the key high-risk audit areas.

The Comptroller has selected six key high-risk areas of fiscal operations to focus their charter school audits.

Appendix, Section 2 includes samples of findings from the Comptroller’s findings from Final Audit Reports of school districts in greater detail.

Appendix, Section 1 is the Self-Assessment Checklist which provides even greater detail on the possible questions the Comptroller may ask.

These key high-risk audit areas are:

1. Fiscal oversight by the Board of Trustees

2. Procurement and contracting

3. Cash disbursements and expenditures

4. Payroll and personnel

5. Fixed assets, equipment and inventories

6. Government Contract Reporting – school enrollment

8 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 8

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

The Comptroller may expand the review to additional areas if the Comptroller’s audit team determines risk in other areas that they believe requires assessment.

√√ 2. Learn what details the Comptroller may focus on in each key area

As of the publication date of this Guidebook6, the Comptroller had not released a Final Audit Report for a charter school. However the Comptroller has released Final Audit Reports for many public school districts across New York State.

The findings published in these audits provide a strong indication of what the Comptroller may focus on for each key audit area.

This section provides a summary of common findings from recent internal control audits of school districts.

Common findings across all areas:

Lack of policies or procedures;

Lack of segregation of duties – one person has control of too many successive steps in an accounting process

Inadequate record keeping; and

Lack of conformity to established policies and procedures.

Segregation of Duties:

Small organizations are often challenged in the area of segregation of duties.

√√ Discuss with your auditor how compensating controls can be used when limited staffing makes segregation very difficult.

√√ Compensating Controls in small organizations are usually accomplished by adding procedures or assigning duties outside the accounting department. For example, 1) add review and authorization steps (by School Leader or Board Treasurer) between key sequential activities currently done by one fiscal employee, or 2) assign receipt of goods and review of packing slips to a school employee outside the accounting process, for example, the receptionist or office assistant.

6 November 2006.

9 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 9

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Common findings by risk area:

Risk Area Common Findings in Comptroller Audits of School Districts

Board Oversight Policies and procedures for fiscal oversight are not established. Established policies are not enforced or updated. Decisions and actions during board meetings are not

documented or retained.

Procurement and Contracting

Competitive bidding requirements and policies are not followed for purchases or contracts.

Sole-sourced contracts are not properly documented to explain exceptions to established bidding policies.

Purchases are made without proper authorization, or without adequate records of authorization.

The school’s tax exemption form is not used for purchases resulting in payment of sales tax.

Disbursements and Expenditures

Questionable expenditures and reimbursements are found in the areas of employee termination payments, meals and refreshments, credit card payments, travel expenses, and cell phone use.

Security over check writing is not in place.

Payroll and Personnel

Personnel files are not complete or not kept up-to-date. Terminated employees remain on payroll records, even if

deemed inactive. Time sheets are not kept, and employee leave is not tracked

properly.

Fixed Assets, Equipment and Inventories

Fixed assets are not properly recorded and tagged. No periodic physical inventory is performed to ensure assets

exist. Asset dispositions are not recorded. Relationship between school assets and assets owned by

“Friends of” organization for school use, are clearly documented.

Revenue School enrollment and attendance records do not properly support the school’s enrollment report to Department of Education for DOE funding.

Accounts receivable collections – school is not collecting 100% of lunch program receivables.

10 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 10

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

√√ 3. Establish and Prepare the School Team (Board, Management and Staff)

I

I

I

I

√√

√√

√√

11 ©

Charter School Activities: If you have not yet done so, create the team to assist with the audit. The team should include the Board Chair and Treasurer, School Leader and Fiscal Leader. Possible Ex-officio team members:

o If your school has a Charter/education management Organization (CMO/EMO), or outsourced fiscal management agency, that provides fiscal services to the school, include a representative from the CMO/EMO.

o The schools’ external auditor and lawyer.

Orient team members to the audit process and their role in the audit. bl h h h ll d d f h d

Sample AGENDA for the first school audit team meeting

. Review this audit guidebook.

I. Schedule meeting times to complete the Self-Assessment Checklist and Audit-Prep Workplan.

II. Assign roles and responsibilities to completing the tasks within established deadlines.

V. Determine what will be needed and who will be the group’s point person.

2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 11

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

√√ 4. Complete a Self-Assessment of potential areas of weakness – turn to the Self-Assessment Checklist in Appendix 1.

The best way to prepare for the Comptroller’s audit (and similar reviews by other auditors, government grantors and oversight agencies), is to be “audit-ready” year round.

“Audit-ready” means:

• The organization regularly reviews and updates its fiscal policies and procedures, taking into account how changes (due to growth, funding sources, etc.) may affect key risk areas.

• The organization has effective internal control systems in place to identify and address key areas of fiscal risk, so that losses to school assets are prevented.

Fiscal Policies and Procedures are the foundation for internal control for all organizations. The school’s policies and procedures must effectively address each of the areas of audit risk addressed in the Comptroller’s audit.

The Comptroller’s audits of school districts have routinely found that the school district’s policies and procedures are either inadequate or not fully implemented.

Charter School Activities:

√√ If the school’s current policies and procedures are not adequate, take steps to update and improve them.

√√ Create a school audit team, including the School Leader, Board Chair and Treasurer, and Finance Leader.

12 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 12

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Turn to the Appendix, Section 1. Meet with the school’s audit team to complete the Self-Assessment Checklist. Use this opportunity to strengthen your board, executive and front line staff team.

The completed Self-Assessment Checklist acts as a road map to ensuring the school’s internal control systems are in alignment with the Comptroller’s expectations. The questions in the Appendix Self-Assessment Checklist are the types of questions charter schools are likely to be asked during the audit. 7

The Recommendations in the Self-Assessment Checklist list sample procedures that can be implemented to address internal control risks. The recommendations are not meant to be a comprehensive guide to implementing internal control systems.

A sample question from the Self-Assessment Checklist:

Fiscal oversight by the Board of Trustees

Internal Control Risk

Recommended Control

Yes, in place

Yes, but needs

improvement

No,

not in place

Benefits

Does the Board (including the Finance Committee) keep adequate documentation of its meetings?8

Board Secretary (or other appointed record-keeper) is responsible for taking minutes so that every meeting has a corresponding set of minutes.

Meeting minutes are sent to the Chartering Authorizer within 30 days of the Board Meeting.

Minutes serve as a record of Board decisions and can document compliance with regulatory issues as well as be a crucial record of analysis of issues.

7 Based on FMA’s research of the Comptroller audit plans for charter schools. 8 Meetings of the school board of trustees must conform to the Open Meetings Law. Minutes must be created within 2 weeks of the meeting (Public Officers Law § 106) and one week for executive session minutes consisting of any vote matters and recordation. A copy of the minutes must be sent to the charter school chartering authorizer (SUNY, SED, DOE) within 30 days of the board's meeting and may be in draft format so long as they are approved at the next meeting. 13 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 13

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

√√ 5. Create an Audit-Prep Workplan

√√ Rene

√√ Co

As

√√ Beth

√√ In

Sampl

Audit Area

Board Over-sight:

Minutes

14 © 20

Charter School Activities:

view the responses to the Self-Assessment Checklist to identify areas in ed of improvement

mplete the Audit-Prep Workplan

udit-Prep Workplan template is in Appendix, Section 3. See the ample entry below.

gin improving the school’s internal control systems prior to the start of e audit!

clude the school team in all activities

e Audit-Prep Workplan entry:

Current Condition/ Risk Areas

Audit-Prep Activities Complete by date

Staff Responsible & Resources Required

Board keeps minutes of its meetings, but they are not timely, not signed by the Secretary, and not maintained in a “Board Minutes Binder” located in the school’s business office. Minutes are also not submitted to the chartering authorizer as required.

The Board Secretary will complete minutes within two weeks of meetings, sign, and give to school administrative assistant who will file in the Board Minutes Binder.

Copies are submitted to the chartering authorizer, and documentation of the submission is retained in the Board Minutes binder.

A process is instituted whereby minutes of the prior meeting are approved before commencement of the current meeting.

Immediately

Board Secretary, with support from school assistant for mailing & filing.

Compliance with Board minutes procedures are reviewed by Board Finance committee annually.

06 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 14

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Important resources for developing the Pre-Audit Workplan:

The Self-Assessment Checklist should act as the first resource in developing the Audit-Prep Workplan. The Self-Assessment Checklist identifies the school’s areas of potential weakness. The second column offers sample Recommended Procedures and the right column of the Checklist describes the Benefits to having systems and procedures for each area.

The Comptroller recommends reviewing applicable sections in the State Comptroller’s Local Government Management Guide. This guide is available in PDF form at: http://www.osc.state.ny.us/localgov/pubs/lgmg/internal_control_nc.pdf

Review the Comptroller’s Audit findings from completed audits of School Districts.

Samples of Comptroller’s findings from school district audits are in Appendix, Section 2 and online at http://www.osc.state.ny.us/localgov/audits/2006/schools/index.htm

15 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 15

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

iii. How do we live through it? 7 Steps to the Audit Process, and how to respond. The typical audit process followed by the Comptroller includes 7 steps which are outlined in a pamphlet that the Comptroller will likely provide at the commencement of the audit:9

1. Notice

2. Opening Conference

3. Audit Survey

4. Field work Phase

5. Preliminary Audit Findings

6. Closing Conference

7. Draft and Final Audit Report

See the Appendix, Section 4 for a summary of this chapter “Checklist: How do we live through it?”

Step 1. Notice

About one week before starting the audit, the Comptroller will provide the charter school with written notice. In the notice the Comptroller says, “The

9 Office of the State Comptroller, Information and Protocols Regarding the Conduct of Audits, April 2005, based on GAO-03-673G, the Yellow Book, Government Auditing Standards, 2003 Revision, US GAO.

16 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 16

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

audit process is an integral part of the government’s system of “checks and balances” which provides an objective, independent review of the program stewardship and fosters accountability to the citizens of New York.”

The Comptroller may also include a list of documents the Comptroller wants you to assemble and provide at the Opening Conference. A sample list is in Appendix, Section 7

The time covered in the document request usually starts with the previous fiscal year, and continues to the present, however, some requests may include all documents since the school’s inception.

Charter School Activities: - Notice

√√ Assemble and organize the documents requested by the Comptroller for the Opening Conference.

√√ If the school has a contract with a Charter or Education Management Organization (CMO/EMO) or fiscal outsourcing firm to provide fiscal services for the school – plan how records that may be kept at the CMO/EMO, will be made available for the auditors.

√√ If not already done, complete the Self-Assessment Checklist and Audit-Prep Workplan.

√√ If not already done, review the school’s written Policies and Procedures, comparing them to current fiscal practices to determine if there are inconsistencies.

√ If the school does not have written Policies and Procedures, or if they are insufficient, begin the process of updating them.

√ If the school’s fiscal practices are inconsistent with written Polices and Procedures, correct the inconsistencies.

√ Do not wait for the Comptroller’s notice to begin review of your policies and procedures, this is a process that you should begin right away.

Review “Tips for Working with the Auditors”1 Appendix, Section 5, and use them to prepare for the audit.

17 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 17

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Step 2. Opening Conference

The Comptroller’s audit team will convene an opening conference, either in person or by conference call, with the goal of establishing a climate where charter school officials and other top management are informed about the audit process and also given an opportunity for input. The Comptroller’s audit team members usually include an Auditor-In Charge (AIC) and staff auditors (2 – 4 in normal circumstances).

During the opening conference the following areas will be addressed:

Meet the Comptroller’s Audit Team.

Scope of the audit, including the program areas under review and the time period to be covered. The audits are likely to cover a one or two year period (including year-to-date for the current fiscal year), although the audit period could be expanded if discrepancies are uncovered.

Identification of any previously known improprieties.

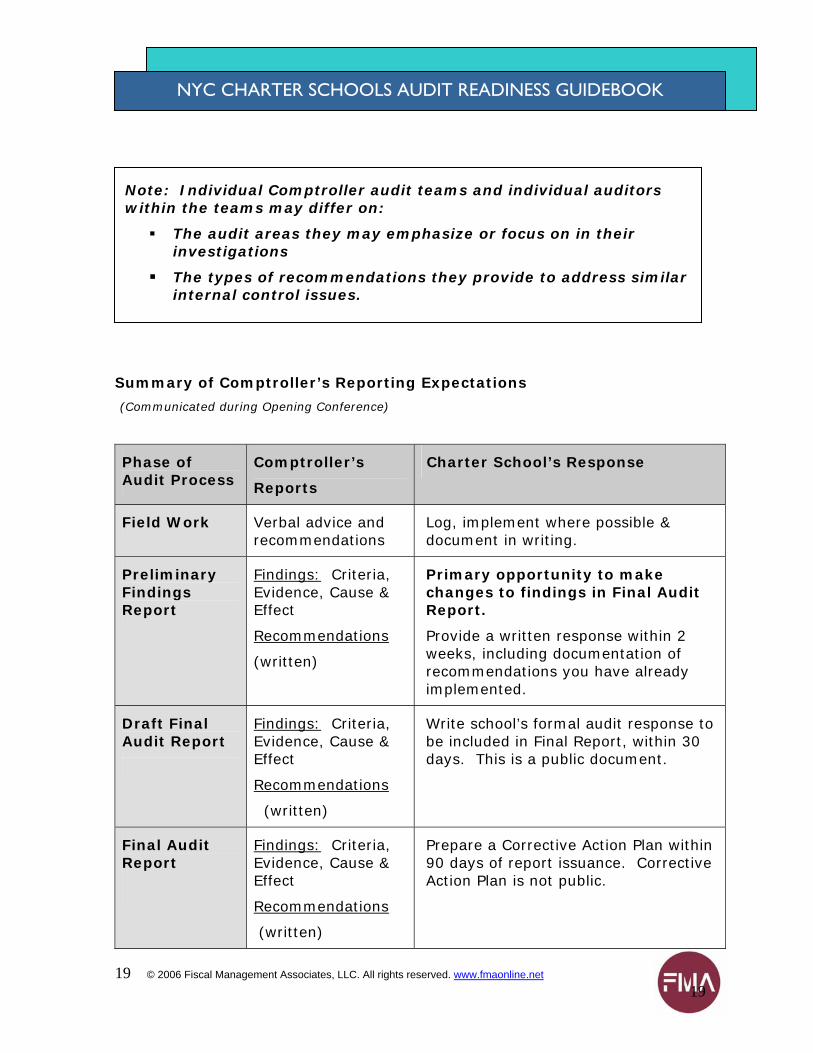

Review of standard reporting procedures for the Comptroller’s recommendations to the school, including the need for responses from the charter school at each stage of report issuance. (See table, next page)

A table summarizing the Comptroller’s reporting expectations is on the next page, and also included in the “How do we live through it? Checklist” in the Appendix, Section 4.

Receive from the school, the documents requested by the Comptroller in the Notice statement, and provide a list of additional documents needed by the Comptroller by the beginning of the fieldwork phase.

18 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 18

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Summary of Comptroller’s Reporting Expectations

(Communicated during Opening Conference)

Phase of Audit Process

Comptroller’s

Reports

Charter School’s Response

Field Work Verbal advice and recommendations

Log, implement where possible & document in writing.

Preliminary Findings Report

Findings: Criteria, Evidence, Cause & Effect

Recommendations

(written)

Primary opportunity to make changes to findings in Final Audit Report.

Provide a written response within 2 weeks, including documentation of recommendations you have already implemented.

Draft Final Audit Report

Findings: Criteria, Evidence, Cause & Effect

Recommendations

(written)

Write school’s formal audit response to be included in Final Report, within 30 days. This is a public document.

Final Audit Report

Findings: Criteria, Evidence, Cause & Effect

Recommendations

(written)

Prepare a Corrective Action Plan within 90 days of report issuance. Corrective Action Plan is not public.

Note: Individual Comptroller audit teams and individual auditors within the teams may differ on:

The audit areas they may emphasize or focus on in their investigations

The types of recommendations they provide to address similar internal control issues.

19 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 19

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Step 3. Audit Survey

The Comptroller’s audit team will conduct a survey of the charter school’s organizational and program information before the audit begins. The objective is to develop a more complete understanding of the charter school’s internal control risks and the areas to be audited.

However, note that prior to starting audits of New York state charter schools, the Comptroller researched general audit risks for charter schools.10

Charter School Activities – Opening Conference

√√ Ensure attendance by the school leaders including Board Chair & Treasurer, School Leader, Finance Leader, and CMO/EMO representative, if the school has a Charter/education management Organization.

√√ Ask questions to: clarify areas to be audited, stages of the audit process; how communications will proceed and understand the opportunities for the school to act on early findings

√√ Use the list of required documents provided by the Comptroller in the Opening Conference, to organize your files for the auditor’s inspection during the Fieldwork phase.

√√ If the school has a CMO/EMO, clarify how the auditors will access any records that may be maintained by the CMO/EMO.

10 The Comptroller’s research included a review of (1) all legislation and regulations that relate to charter schools, (2) the Comptroller’s audit of NY City Department of Education’s monitoring of charter schools, (3) correspondence with state auditors in other states on internal control risks areas in charter schools, and (4) audits of closed charter schools.

20 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 20

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Charter School Activities: - Audit Survey

√√ Fill out and return the Comptroller’s audit survey.

√√ Provide organization and program documents that may be requested.

Step 4. Field Work Phase

This phase consists of the focused audit effort and will probably comprise the most amount of time, encompassing a series of visits from the Comptroller’s over a time period of two weeks to over 3 months.

An auditor-in-charge (AIC) supervises the audit team’s day-to-day activities.

On the first day of the fieldwork, the Comptroller’s audit team will likely:

o expect all the requested documents to be available;

o ask to see the school’s fiscal policies and procedures right away;

o meet or schedule time to meet with the school leader, Board Chair and all fiscal staff.

During the audit, the Comptroller’s audit team will require unrestricted access to records.11

The Comptroller’s audit team will likely review 100% (ALL) of the charter school records for the time period audited. In some cases, the Comptroller may choose several audit areas, such as Payroll and Personnel, to review 100% of the records, but do less than 100% sampling in other areas.

Early Findings. During the field-work phase, auditors will share their verbal observations regarding areas of potential weakness and recommendations for improvements.

11 According to Information and Protocols Regarding the Conduct of Audits, “The Comptroller’s right to access information required for audit purposes is derived from the State Constitution, State Finance Law and General Municipal Law. Some records may include information that various laws define as confidential and/or proprietary information in your custody. Furthermore, the Comptroller is subject to legal sanctions of those laws that establish the confidentiality and/or proprietary of the information.”

21 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 21

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Charter School Activities: - Fieldwork

Review “Tips for working with the auditors” Appendix, Section 5.

√√ Organize the charter school fiscal records for the possibility of 100% testing ensuring immediate access to these records should they be requested.

√√ Take careful note of the auditor’s verbal recommendations and keep a log of the recommendations.

√√ Implement those recommendations that you can, as soon as possible.

√√ Document the changes you have implemented and copy auditors.

√√ Discuss accomplished changes with the auditors and follow up with documented changes in writing.

Step 5. Preliminary Audit Findings

During the fieldwork phase the Comptroller’s audit team will discuss the findings and conclusions with representatives from the school’s Board, finance and management staff.

After on-site fieldwork is completed, the Comptroller may ask additional questions and request additional documents.

One to six months after completion of fieldwork, the Comptroller will send the school the Comptroller’s Preliminary Audit Findings. A copy of the Preliminary Audit Findings may also be provided by the Comptroller to the chartering authorizer.

√√ The school is usually given just two weeks to respond in writing to the preliminary audit findings.

22 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 22

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Comptroller’s Audit Report Format

The Comptroller’s Preliminary Findings Report, Draft Final Audit Report and the Final Audit Report will generally follow this format:

1. Objectives

a. The report will lay out the audit objectives. These will likely be expressed in a short statement: For example:

Did the charter school implement adequate internal control policies and procedures to protect and account for the charter school’s assets?

2. Scope and Methodology

a. The scope is the key audit risk areas:

i. Fiscal oversight by Trustees

ii. Disbursements and Expenditures

iii. Procurement and Contracting

iv. Payroll and Personnel

v. Fixed Assets – Equipment and Inventories

b. Methodology12 The report will identify what percentage of records were reviewed. This may be 100% of all records, or 100% of some audit areas, such as Payroll and Personnel, but less than 100% in other areas.

3. Audit Results

a. The report will state the Comptroller’s conclusions about the capacity of the school’s systems of internal control in relation to the criteria set forth on internal control standards by the US Government Accounting Office (GAO) and the NY State Comptroller.

b. The report will contain information on any deficiencies in internal control, fraud, illegal acts, and violations of provisions of contracts or grant agreements and abuse. The report will often discuss:

i. Criteria used to assess the deficiencies.

ii. Evidence of what the auditors found to show the scope or extent of the condition.

12 The methodology follows generally accepted government auditing standards (GASAS).

23 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 23

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

iii. Cause of the deficiencies.

iv. Effect or impact of the deficiencies found.

Auditors differ in their style and approach to writing the report findings. The best format for reporting findings is described above and includes discussions criteria, evidence, cause and effect for each finding.

Important:

√√ If the Preliminary Findings Report you receive does not discuss criteria, evidence, cause and effect, contact the auditors and ask the auditor to expand the draft findings to provide more detail.

√√ This is important because generalized findings may convey an impression of greater risk than may actually be the case when the finding is judged in the context of the specific evidence the auditors found to support their general findings.

Example:

In one instance, the auditors found Petty Cash was off by $2.00 and that the Business Manager did not always complete the Petty Cash log entry at the time cash was disbursed, but later in the day.

Without the specific evidence, described above (only one instance and only $2.00 discrepancy), a generalized Comptroller finding which might be misleading.

The auditors will encourage early implementation of accepted audit recommendations and will request you to respond and document what you have already implemented in the school’s written response.

√√ Recognition of actions you have taken to implement the Comptroller’s recommendations may provide the Comptroller’s audit team with sufficient information to adjust the Preliminary Audit Findings and impact the findings reported in the Final Audit Report!

24 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 24

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Charter School Activities: - Preliminary Findings

√√ This is the school’s primary opportunity to impact the wording of findings that will appear in the Final Audit Report.

√√ The school has just two weeks to respond.

√√ CAREFULLY, review the written Preliminary Audit Findings.

√√ Consider consulting with school’s external auditor and/or lawyer.

√√ Compare the preliminary findings to the log of verbal recommendations received from the Comptroller’s audit team and which the school developed during the field work phase.

√√ Clarify any errors or misunderstandings that may arise in the auditors’ processing of information.

√√ Respond to the Preliminary Audit Findings, within two weeks.

√√ In your response, provide written documentation of the recommendations you have implemented to date and errors of fact.

√√ Consider re-writing the Preliminary Findings or providing specific edit suggestions to give to Comptroller

√√ Maintain ongoing communication and contact with the auditors.

25 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 25

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Step 6. Closing Conference

The Comptroller will schedule a closing conference, in person or by conference call, to meet with representatives of the charter school to discuss the audit results. Since most of the preliminary findings will be provided and discussed during the audit fieldwork, the closing conference will primarily be a broad summary of audit results and the steps the school has taken to address the findings.

S

Ar

Wf

2

Charter School Activities: - Closing Conference

This is the school’s opportunity to:

√√ emphasize the actions the charter school has already taken to respond to the Comptroller preliminary verbal and written recommendations;

√√ provide related documentation; and

√√ Update the Comptroller’s audit team on the status of their implementation.

tep 7a. Draft and Final Audit Report

pproximately one to two months after the closing conference, the charter school eceives a copy of the Draft Final Audit Report.

ithin 30 days of receiving the Draft Final Audit Report, the school should ormally respond to the audit findings.

6 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 26

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

Aftewrirec

ChaFin

In d

√√

√√

√√ RF

√√ Rom

√√ Iecd

√√ Did

27

Charter School Activities: - Draft Final Audit Report

Interpret the Comptroller’s Draft Final Audit Report. Assemble the school’s audit team and carefully review the report.

Note any questions to ask the Comptroller’s audit team to help you understand and interpret the report.

r reviewing the Comptroller’s Draft Final Audit Report, the school must te its response and send it to the Comptroller within 30 days of eiving the Draft.

rter School Activities: - School’s Formal Response to Auditor dings

rafting the charter’s school’s formal response,

eview the items that the school has corrected prior to receiving the Draft inal Audit Report.

eview the auditor’s findings for accuracy. This process provides an pportunity for the school to correct factual errors which may have been ade by the auditors.

f you believe the findings in the report need greater detail, lack sufficient vidence to show the context, or think that different wording would better ommunicate the audit findings, contact the Comptroller’s audit team and iscuss these issues with them.

raft the school’s formal public response to the auditor, which will be ncluded as an Appendix to the Comptroller’s Final Audit Report – a public ocument!

© 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 27

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

A recommended format for the school’s formal response13:

• Use the school’s letterhead.

• Note and correct any errors of fact.

• List each recommendation made by the Comptroller and follow each recommendation with your response.

• If possible, begin your response with “We accept the Comptroller’s recommendation…” and describe in detail what the school has already done and plans to do to address the Comptroller’s recommendations.

• If you cannot accept the Comptroller’s recommendation without reservation, consider beginning your response to the Comptroller’s specific recommendation with “We accept the Comptroller’s recommendation with the following reservations,” and describe your reservations or concerns, plus what you have done to address the concerns the Comptroller has raised.

7b. Final Audit Report

The Comptroller will publish the Final Audit Report one to two months after the school provides its formal response. The Comptroller:

Posts on the Comptroller’s website

Sends copies of the Governor and legislative leaders

Release copies to the media, possible with a press release.

13 The recommended format is based on a review of formal responses by school districts to the State Comptroller audit, available on the Comptroller website: http://www.osc.state.ny.us/

28 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 28

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

iv. How do we handle the results?

1. Create a Corrective Action Plan

2. Understand how is the audit distributed publicly

This chapter describes how the school can handle the results of the Comptroller’s audit.

Approximately one to two months after the Comptroller has received the Charter School’s formal response to its Draft Final Audit Report, the Final Audit Report will be issued by the Comptroller.

The report will be mailed to the school with copies to the Governor and legislative leaders, as mandated by State Law. The Final Audit Report is a public document, it is posted on the Comptroller’s website, and the Comptroller may also release the report, together with a press release, directly to the media.

29 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 29

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

1. Create a Corrective Action Plan

Once the report has been released publicly in its final version, the school is required to implement the auditor’s recommendations by developing a Corrective Action Plan. This must be completed 90 days after the school receives its Final Audit Report.

√√ The Corrective Action Plan is the school’s 90-day follow-up report to the State Comptroller. It describes the corrective actions taken to implement the recommendations contained in the report, and where not implemented, the reasons.

√√ In addition to giving the Corrective Action Plan to the Comptroller, the school must send copies of the report to other state officials, as described in the Comptroller final report letter.

Sample Charter School Corrective Action Plan

Comptroller Recommendations

Corrective Action Activities

Completed by date(s)

Staff responsible & resources needed

1. All checks should be generated from the computer accounting system to avoid entering information and reduce the possibility of errors.

Board adopts and implements recommendation as a policy. Limit authorized check signers to ED, CFO & Treasurer. Orient authorized signers to new policy. Review monthly to ensure compliance.

30 days to draft, adopt and implement new policy, by Jan 31, 200X

ED, CFO, Bookkeeper, Board Treasurer

2. All fixed assets, including computer equipment and other technology items should be tagged and recorded by tag number in a fixed asset ledger.

Develop fixed asset ledger & tag all fixed assets.

COMPLETED CFO & Bookkeeper

30 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 30

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

See Appendix, Section 6 for a recommended Corrective Action Plan template.

The Comptroller suggests that for guidance in preparing the Corrective Action Plan, charter schools may refer to applicable sections in the publication issued by the of the State Comptroller entitled Local Government Management Guide. Available in PDF form on the web at http://www.osc.state.ny.us/localgov/pubs/lgmg/internal_control_nc.pdf. The Local Government Management Guide has questionnaires on internal control audit areas that can aid with self-assessment and developing corrective action plans.

2. Understand how the audit is distributed publicly

1. The Draft Final Audit Reports are distributed to the charter school, with copies provided to:

a. Director of the Division of the Budget, and

b. Mayor’s Office of Operations, for schools in New York City

2. The Final Audit Reports are public documents available to any interested parties.

a. Most final reports are provided to media representatives, some with accompanying press releases.

b. The reports are also posted on the Comptroller web site at http://www.osc.state.ny.us/localgov/audits/2006/schools/index.htm

√√ You may not be done yet! Possible Follow-up Audits – One Year Later

About one year following the issuance of the Comptroller’s final report, the Comptroller may schedule a follow-up audit to asses the extent the charter school has implemented the recommendations in the final report. These audits generally take less time to complete.

31 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 31

32

© 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net 32

NYC CHARTER SCHOOLS AUDIT READINESS GUIDEBOOK

v. Appendix Appendix

4. How Do We Live Through It? Checklist

8. List of Website Resources in this Guidebook

7. Sample Comptroller Documents Requested

3. Audit-Prep Workplan Template

2. Comptroller’s Findings for School District Audits

1. Self-Assessment Checklist1. Self-Assessment Checklist

6. Post-Audit Corrective Action Plan Template

5. Tips for Working with the Auditors

9. OSC Pamphlet: What to Expect from the Audit

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

1. Fiscal Oversight by the Board of Trustees

a. Is the Board of Trustees aware and knowledgeable of its fiscal responsibilities?

Policies and procedures manuals for cash receipts, revenues, purchases, disbursements, financial reporting, personnel, assets, liabilities, treasury, and governance are drafted, annually updated, and approved by the Board.

Finance/Audit committee members are trained on their fiscal responsibilities.

Finance/Audit Committee charters exist which state the responsibilities of those committees.

Knowledge of a school’s fiscal responsibilities and activities allows the Board to provide more effective financial oversight in accordance with its fiduciary responsibilities.

b. Does the Board have sufficient awareness and input into the budgeting and monitoring processes of the school?

The Board reviews and approves the 5-year and annual operating, cash, and capital budgets.

The Finance/Audit Committee of the Board receives and reviews budget to actual variance reports on a monthly basis, and reports financial condition to the Board on a quarterly basis.

Participation in the budgeting process enhances the Board’s ability to effectively guide a school.

If budget-to-actual financial statements are monitored frequently, revenue shortfalls and expense overruns can be better anticipated and planned.

c. Does the Board (including the Finance, Audit and Governance Committees) keep adequate

Board Secretary (or other appointed record-keeper) is responsible for taking minutes so that every meeting has a corresponding set of

Minutes serve as a record of Board decisions and can document compliance with regulatory issues

33 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

documentation of its meetings and decisions?14

minutes. Board minutes include accompanying documentation of information used for decision making (financial statements, leases, contracts, etc)

The Board should review and approve the minutes of the previous meeting at the start of the next Board meeting.

Meeting minutes are sent to the Chartering Authorizer within 30 days of the Board Meeting.

as well as be a crucial record of analysis of issues.

d. Does the Board have oversight of the school’s bidding practices to help ensure the best combination of price, quality, and service for purchases?

A competitive bidding policy is drafted and approved by the Board. The policy should be designed to set approval levels; guard against favoritism, extravagance, fraud, and corruption among vendors; and to foster honest competition to ensure that resources are expended efficiently.

A well-controlled, Board-monitored procurement process allows the school to obtain purchases of the right quality, from the right source, and at the right price.

e. Do all Board of Trustees sign conflict-of-interest statements and written disclosures of conflicts on an annual basis?

Board members sign written conflict-of-interest statements on an annual basis to facilitate disclosure of any financial interests and maintain a high level of integrity from self-dealing issues. Policies include procedures for disclosing potential conflicts and fair decision making processes for Board members when conflicts arise.

A signed Conflict of interest policy helps ensure that Board members are aware of and follow proper procedures for disclosing financial interests that relate to the school.

f. Are the Trustees aware of significant changes in the school’s

The Trustees should receive regular reports on recent employee new hires, terminations and

Personnel are one of the most significant aspects of the schools’

14 Meetings of the school board of trustees must conform to the Open Meetings Law. Minutes must be created within 2 weeks of the meeting (Public Officers Law § 106) and one week for executive session minutes consisting of any vote matters and recordation. A copy of the minutes must be sent to the charter school chartering authorizer (SUNY, SED, DOE) within 30 days of the board's meeting and may be in draft format so long as they are approved at the next meeting.

34 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

personnel? resignations.

program, Ensures adequate oversight by the Board.

g. Are cash assets in bank accounts properly safeguarded?

The Board considers an investment policy for the collateralization of bank balances over $100,000.

35 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

2. Procurement and Contracting

a. Does the purchasing system facilitate the best combination of price, quality and service and deter the existence of inappropriate buyer-vendor relationships/ arrangements for both private and government vendors?

A Competitive Bidding Policy is implemented that includes:

Organizational procedures on minimum purchase amounts (i.e. $500) for which a bid must be obtained.

The number of bids to be obtained.

Bid approval levels and processes.

Self interested transactions.

Sole sourced vendor policy where bids are not or cannot be obtained.

For purchases that must be competitively bid, a Request for Proposal (RFP) process is in place. Written original bid documentation supporting vendor selection and vendor invoice are adequately maintained and independently reviewed.

Board members and employees sign written conflict-of-interest statements to maintain a high level of integrity from self-dealing issues.

A thorough analysis is completed before a vendor is added to the vendor masterfile, including vendor background and legitimacy of vendor.

Ongoing quality assurance of the vendor masterfile is performed, including:

• Review of company name and address on to ensure there are no duplicate vendors.

• Review of selected transactions by

Documentation such as purchase orders and solicitation of price quotes reduces the possibility of unauthorized purchases, ensures purchases are made at the lowest possible cost, provides evidence that staff is adhering to the school’s procurement policy, and facilitates more effective management of the budget.

Periodic review of purchasing practices and vendor transactions significantly improves disbursement controls and reduces the likelihood of fraud and conflict-of-interest issues.

36 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

management.

Purchase orders are prepared for all purchases which include:

• vendor name

• address

• ship to information

• order date

• unique purchase order number

• benefit of the purchase for the school

• tax exemption form to exempt sales tax

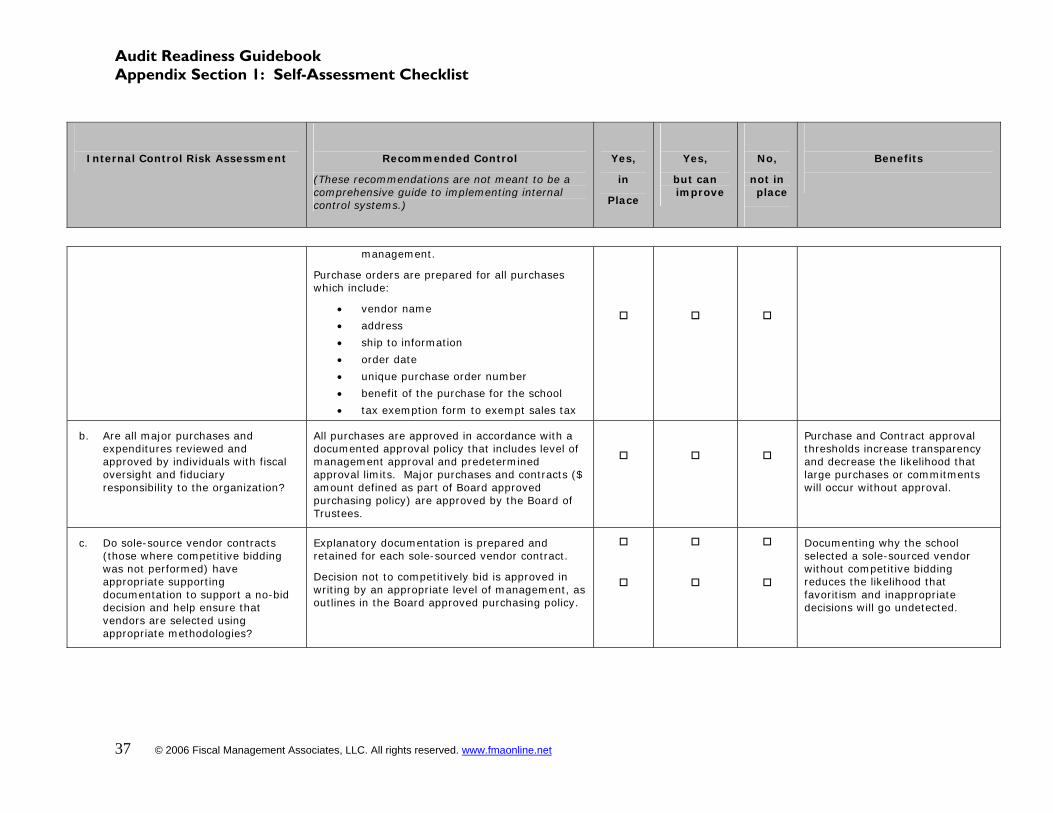

b. Are all major purchases and expenditures reviewed and approved by individuals with fiscal oversight and fiduciary responsibility to the organization?

All purchases are approved in accordance with a documented approval policy that includes level of management approval and predetermined approval limits. Major purchases and contracts ($ amount defined as part of Board approved purchasing policy) are approved by the Board of Trustees.

Purchase and Contract approval thresholds increase transparency and decrease the likelihood that large purchases or commitments will occur without approval.

c. Do sole-source vendor contracts (those where competitive bidding was not performed) have appropriate supporting documentation to support a no-bid decision and help ensure that vendors are selected using appropriate methodologies?

Explanatory documentation is prepared and retained for each sole-sourced vendor contract.

Decision not to competitively bid is approved in writing by an appropriate level of management, as outlines in the Board approved purchasing policy.

Documenting why the school selected a sole-sourced vendor without competitive bidding reduces the likelihood that favoritism and inappropriate decisions will go undetected.

37 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

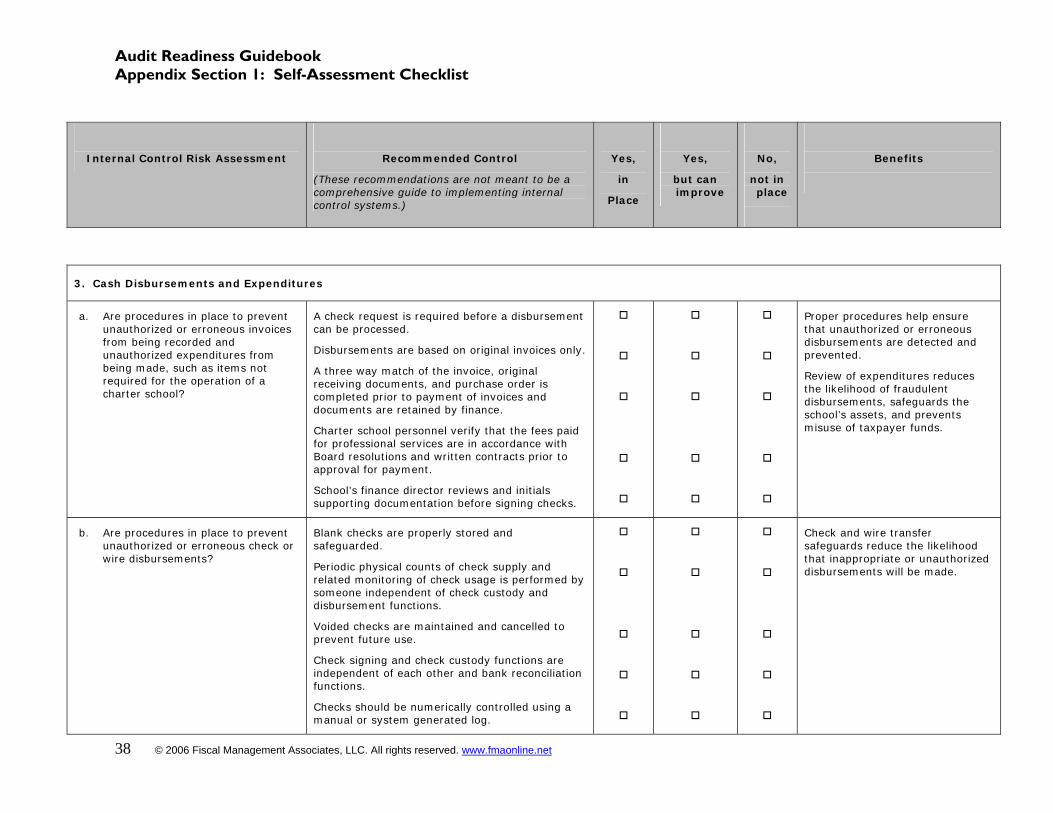

3. Cash Disbursements and Expenditures

a. Are procedures in place to prevent unauthorized or erroneous invoices from being recorded and unauthorized expenditures from being made, such as items not required for the operation of a charter school?

A check request is required before a disbursement can be processed.

Disbursements are based on original invoices only.

A three way match of the invoice, original receiving documents, and purchase order is completed prior to payment of invoices and documents are retained by finance.

Charter school personnel verify that the fees paid for professional services are in accordance with Board resolutions and written contracts prior to approval for payment.

School’s finance director reviews and initials supporting documentation before signing checks.

Proper procedures help ensure that unauthorized or erroneous disbursements are detected and prevented.

Review of expenditures reduces the likelihood of fraudulent disbursements, safeguards the school’s assets, and prevents misuse of taxpayer funds.

b. Are procedures in place to prevent unauthorized or erroneous check or wire disbursements?

Blank checks are properly stored and safeguarded.

Periodic physical counts of check supply and related monitoring of check usage is performed by someone independent of check custody and disbursement functions.

Voided checks are maintained and cancelled to prevent future use.

Check signing and check custody functions are independent of each other and bank reconciliation functions.

Checks should be numerically controlled using a manual or system generated log.

Check and wire transfer safeguards reduce the likelihood that inappropriate or unauthorized disbursements will be made.

38 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

Disbursements should never be made to “cash” or “bearer.”

Controls are in place to prevent or identify duplicate payments.

All disbursements (check or wire transfers) require signature or authorization by an appropriate level of management.

Bank balances are reconciled to general ledger cash balances on a monthly basis by an individual who has no disbursement processing responsibilities. Reconciliation is formally documented and approved by Finance Director or other appropriate level of management. Any adjustments made to bank balances are approved in writing by an employee not otherwise involved in the cash function or responsible for reconciling the account.

Unopened bank statements are received by someone outside the fiscal area, usually the Executive Director. Executive Director periodically reviews bank statements for unusual disbursements.

Timely bank reconciliations ensure that accounting records are correct and moneys have been properly accounted for. Reconciliations also help identify any inappropriate transactions that remain unrecorded.

c. Are employee cash advances prohibited?

If cash advances are not prohibited, are advances properly approved and documented to reduce the risk of improper use and abuse of company cash?

Employee cash advances are prohibited. Any deviation from this policy is adequately documented and proper procedures are clearly communicated and followed before advance is distributed.

Adequate documentation of the granting of a cash advance includes date, reason and amount of advance, and repayment terms.

Repayments of cash advances by the employee are documented and the outstanding balance is

Proper controls over cash advances increases the likelihood that advances will be issued only in exceptional cases, for appropriate business purposes, and will be repaid in a timely manner.

39 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

© 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net40

appropriately reduced.

Loans to trustees are forbidden.

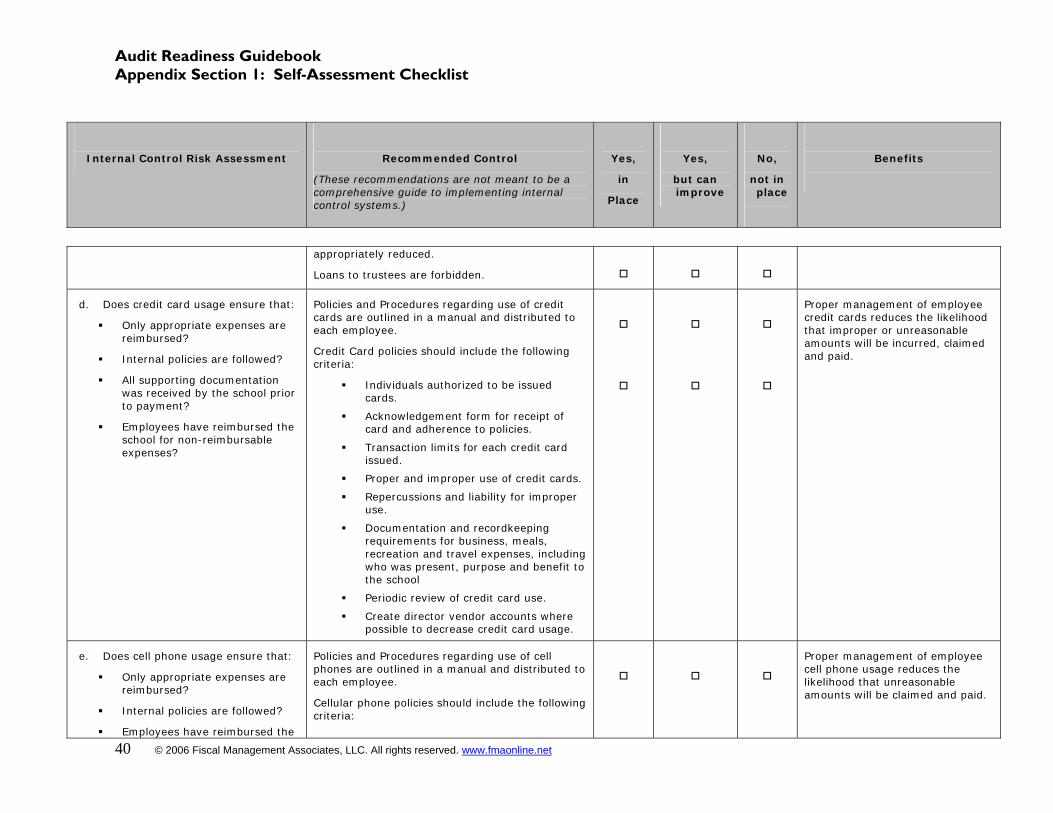

d. Does credit card usage ensure that:

Only appropriate expenses are reimbursed?

Internal policies are followed?

All supporting documentation was received by the school prior to payment?

Employees have reimbursed the school for non-reimbursable expenses?

Policies and Procedures regarding use of credit cards are outlined in a manual and distributed to each employee.

Credit Card policies should include the following criteria:

Individuals authorized to be issued cards.

Acknowledgement form for receipt of card and adherence to policies.

Transaction limits for each credit card issued.

Proper and improper use of credit cards.

Repercussions and liability for improper use.

Documentation and recordkeeping requirements for business, meals, recreation and travel expenses, including who was present, purpose and benefit to the school

Periodic review of credit card use.

Create director vendor accounts where possible to decrease credit card usage.

Proper management of employee credit cards reduces the likelihood that improper or unreasonable amounts will be incurred, claimed and paid.

e. Does cell phone usage ensure that:

Only appropriate expenses are reimbursed?

Internal policies are followed?

Employees have reimbursed the

Policies and Procedures regarding use of cell phones are outlined in a manual and distributed to each employee.

Cellular phone policies should include the following criteria:

Proper management of employee cell phone usage reduces the likelihood that unreasonable amounts will be claimed and paid.

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

school for non-reimbursable expenses?

Individuals authorized to be issued cellular phones.

Procurement methods for obtaining phones.

Expense approval procedures.

Proper and improper usage of cell phones.

Repercussions for improper use and employee liability.

Cell phone usage monitoring techniques and periodic reviews.

f. Are reimbursements for travel expenses managed in such a manner to ensure that:

Only appropriate expenses are reimbursed?

Internal policies are followed?

All supporting documentation was received by the school prior to payment?

Employees have reimbursed the school for non-reimbursable expenses?

Policies and Procedures regarding travel reimbursements are outlined in a manual and distributed to each employee.

Travel and expense policies should include the following criteria:

Definitions of categories of reimbursable travel and expense.

Description of the pre-approval process.

Allowable maximum reimbursement amounts or per diem rates for lodging and meals as published in the Federal Register.

IRS allowed mileage reimbursement rates.

Documentation and substantiation requirements (i.e. the reimbursement process, and employee responsibility for non-reimbursable costs.

Employees must turn in expense reports with original receipts and documentation prior to reimbursement. Documentation must include a

Proper management of employee travel costs reduces the likelihood that unreasonable or unsubstantiated amounts will be incurred, claimed and paid.

41 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

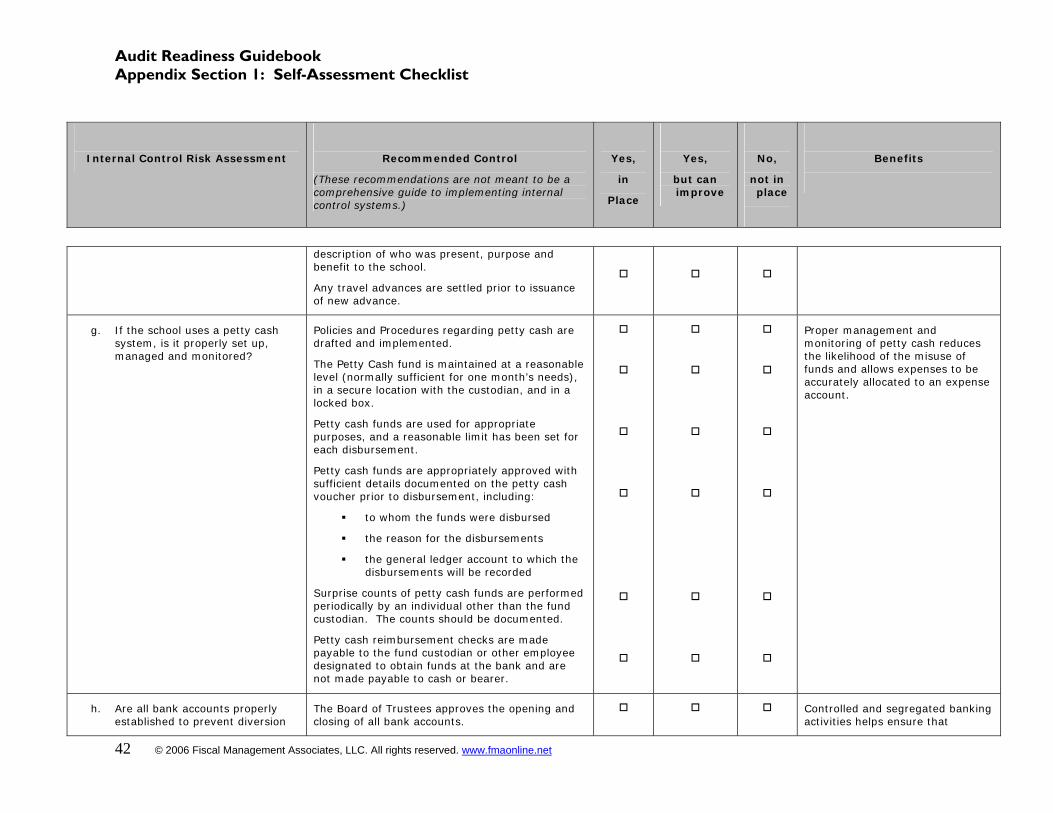

description of who was present, purpose and benefit to the school.

Any travel advances are settled prior to issuance of new advance.

g. If the school uses a petty cash system, is it properly set up, managed and monitored?

Policies and Procedures regarding petty cash are drafted and implemented.

The Petty Cash fund is maintained at a reasonable level (normally sufficient for one month’s needs), in a secure location with the custodian, and in a locked box.

Petty cash funds are used for appropriate purposes, and a reasonable limit has been set for each disbursement.

Petty cash funds are appropriately approved with sufficient details documented on the petty cash voucher prior to disbursement, including:

to whom the funds were disbursed

the reason for the disbursements

the general ledger account to which the disbursements will be recorded

Surprise counts of petty cash funds are performed periodically by an individual other than the fund custodian. The counts should be documented.

Petty cash reimbursement checks are made payable to the fund custodian or other employee designated to obtain funds at the bank and are not made payable to cash or bearer.

Proper management and monitoring of petty cash reduces the likelihood of the misuse of funds and allows expenses to be accurately allocated to an expense account.

h. Are all bank accounts properly established to prevent diversion

The Board of Trustees approves the opening and closing of all bank accounts.

Controlled and segregated banking activities helps ensure that

42 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

of school assets? A separate general ledger account is maintained

for each bank account.

Inactive bank accounts are closed on a timely basis.

Bank accounts have at least 2 signatories, including Board Treasurer, Director of Finance, and upper level school management.

Banks are immediately notified when an authorized signer, including individuals authorized to approve or release wire transfers, leaves the school.

disbursements and withdrawals are properly made.

43 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

4. Payroll and Personnel

a. Are payroll controls in place to prevent opportunities to create "ghost" employees and other payroll related fraud?

Access to create employees in the payroll masterfile is restricted to appropriate personnel independent of payroll processing/disbursements.

All changes and additions to the payroll masterfile are properly documented and approved by management before input to the masterfile.

The payroll masterfile should be reviewed periodically to ensure validity and accuracy.

Effective segregation of duties in the payroll process safeguards the school against fraud and abuse and provides for timely payment to employees.

b. Are methods in place to verify that payroll is processed for work performed, withholdings are properly calculated, and payroll is properly recorded in the accounting system?

Employees prepare timesheets of hours worked and absences that account for the entire workday. Such records should include starting and ending times and meal breaks.

Timesheets are reviewed and approved by a supervisor prior to processing payroll.

Payroll is compliant with the W-4 withholding instructions.

Manual payroll checks are issued non-routinely, only after approval by an appropriate level of management.

Manual payroll checks are processed in the payroll system in the following payroll cycle.

Payroll and related withholdings are recorded in the general ledger, following budgetary cost allocations.

Time sheets reduce likelihood that hourly employees will be paid for hours not authorized or approved. For both salaried and hourly employees, timesheets provide a strong methodology for cost allocation.

c. Are contracts current, vacation leave properly tracked, and terminated

The Board of Trustees reviews school administrator employment contracts and leave

Keeping employment contracts and vacation leave current and

44 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

45 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

employees removed from the system to prevent unauthorized or erroneous payroll disbursements?

records annually.

Vacation time is tracked and vacation balances are communicated to staff on an ongoing basis.

Employee training/education/conference time is tracked.

The payroll register and other key reports are reviewed and approved by management, prior to the payroll being issued.

Period-to-period payroll reconciliation or other analysis of significant changes in payroll is performed each period. Any significant differences are investigated.

updated in the payroll system ensures the likelihood that payroll disbursements are accurate.

d. Are personnel files maintained and stored appropriately, up-to-date, with all documentation required by law?

A personnel file is created for each employee. Personnel files are properly safeguarded and access is restricted to employees with human resources functions who require access.

Personnel files are periodically spot-checked to assure they are up-to-date and contain information that may be required by law, such as background checks and fingerprints. The file should also include a signed application, references, offer letter, salary history, completed W-4, completed I-9, licenses & certifications, authorization for payroll deductions and garnishments, and their resolution.

Maintaining current and accurate personnel files reduces the possibility of inaccurate payroll records due to unrecorded employee changes and hiring of employees who do not have the appropriate clearances.

e. Do employee separation procedures ensure that school assets and information are safeguarded?

All terminations are promptly reported to Payroll and the individual is removed employee from the applicable databases.

All employee badges and keys are collected from terminated employees.

Senior management responsible for oversight of

Efficient and complete employee termination procedures ensure that school assets are returned prior to departure and employee access to the school technology network is terminated.

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

employee separation or Human Resources collects school assets and completes an exit checklist prior to employee departure.

All network and user passwords are changed immediately upon notification of termination.

46 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

© 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net47

5. Equipment and Inventories

a. Are all asset purchases and disposals proper?

Written requests for the purchase of capital assets are supported by sufficient operational and financial justification and are approved based on asset cost by an appropriate level of management.

Major asset disposals are reviewed and approved in accordance with policies and procedures by the school administrator and the grantor. Asset disposal forms are completed and approved prior to disposal. All disposals are recorded in the fixed assets ledger on a timely basis.

Review and approval of asset purchases and disposals will ensure that appropriate levels of management have knowledge of and approve major purchases or disposals.

b. Are fixed assets, specifically high-risk fixed assets, 15 properly protected to prevent property loss or theft?

All fixed assets are tagged upon acquisition with unique identifying numbers. Tags are numerically sequenced and recorded in the related fixed asset subsidiary ledger.

All assets are inventoried on an annual basis against the fixed asset subsidiary ledger. High-risk fixed assets are inventoried more frequently. Any discrepancies are investigated.

Persons other than those who maintain subsidiary records for individual assets are responsible for the custody of the assets.

Physical safeguards and a well-managed fixed asset tracking system reduces the risk of loss of assets due to theft or negligence.

Accurate subsidiary records increases the reliability of fixed asset valuation.

c. Are financial statements supported by the subsidiary fixed asset ledgers and depreciation correctly calculated?

Fixed asset subsidiary ledgers are reconciled to the general ledger control accounts.

Depreciation is calculated in accordance with

Reconciliation of fixed assets accounts to subsidiary ledgers helps ensure complete accounting of acquisitions and disposals of

15 The comptroller’s office has identified higher risk assets to include: technology items such as laptops, vehicles and expensive musical instruments.

Audit Readiness Guidebook Appendix Section 1: Self-Assessment Checklist

Internal Control Risk Assessment Recommended Control

(These recommendations are not meant to be a comprehensive guide to implementing internal control systems.)

Yes,

in

Place

Yes,

but can improve

No,

not in place

Benefits

Finance policies and procedures and Generally Accepted Accounting Principles (GAAP).

Depreciation schedules are reviewed and approved by the Finance Director to ensure that asset categories are assigned appropriate useful lives.

fixed assets.

Proper depreciation ensures that expenses are not over-stated or understated and aids in the planning for future fixed asset expenditures.

d. Are the assets of “Friends of” corporations, which are for use of the school, clearly designated and recorded?

Assets owned by a “Friends of” corporation for use of the school, should be clearly recorded as under the ownership of the “Friends of” corporations.

Ownership of assets is attributed appropriately.

48 © 2006 Fiscal Management Associates, LLC. All rights reserved. www.fmaonline.net