Audit Planning & Audit Program Pertemuan 13-14 Matakuliah: A0294/Audit SI Lanjutan Tahun: 2009.

38

Audit Planning & Audit Program Pertemuan 13-14 Matakuliah : A0294/Audit SI Lanjutan Tahun : 2009

-

Upload

eric-gilday -

Category

Documents

-

view

221 -

download

1

Transcript of Audit Planning & Audit Program Pertemuan 13-14 Matakuliah: A0294/Audit SI Lanjutan Tahun: 2009.

Audit Planning & Audit Program Pertemuan 13-14

Matakuliah : A0294/Audit SI Lanjutan Tahun : 2009

Bina Nusantara University 2

Learning Outcomes

Pada akhir pertemuan ini, diharapkan mahasiswa akan mampu :• Menjelaskan audit planning• Menjelaskan audit program

Bina Nusantara University 3

Audit Planning Process

• Strategic/tactical audit planning• Engagement letter• Risk assessment• Preliminary evaluation of internal controls• Audit plan, program and scope• Classification, scope of audit

Bina Nusantara University 4

Strategic/tactical Audit Planning

• Short term– Takes into account audit issues that will be covered during

the year

• Long term– Relates to audit plans that will take into account risk

related issues regarding changes in the organization’s IT strategic direction that will affect the organization’s IT environment

Bina Nusantara University 5

Areas to be audited

• Enables management• Ensures that relevant information• Establishes a basis for effectively managing the audit

departement• Provides a summary of how the individual audit subject is

related to the overall organization as well as to the business plans

Bina Nusantara University 6

Steps to perform audit planning

• Gain an understanding of the business's mission, objectives, purpose and processes, which include information and processing requirements, such as availability, integrity, security and business technology– Touring key organization facilities– Reading background material including industry publications,

annual reports and independent financial analysis reports– Reviewing long term strategic plans– Interviewing key managers to understand business issues– Reviewing prior reports

• Identify stated contents, such as policies, standards and required guidelines, procedures, and organization structure

Bina Nusantara University 7

Steps to perform audit planning

• Evaluate risk assessment and any privacy impact analysis carried out by management

• Perform a risk analysis• Conduct an internal control review• Set the audit scope and audit objectives• Develop the audit approach or audit strategy• Assign personnel resources to the audit and

address engagement logistics

Bina Nusantara University 8

Risk Assessment

• Risk assessment method• Areas to be audited• Use of risk assessment in audit planning (S11,

G13, P1)

Bina Nusantara University 9

Risk Assessment Method

• Qualitative and Quantitative Methods• Semiquantitative Analysis Methods• Quantitative Analysis Methods

Bina Nusantara University 10

Audit Program• Obtaining and recording and understanding of the audit

area/subject• Risk assessment and general audit plan and schedule• Detailed audit planning• Preliminary review of the audit area/subject• Evaluating the audit area/subject• Compliance testing (often referred to as test of controls)• Substantive testing• Reporting (communicating results)• Follow up

Bina Nusantara University 11

PLANNING

• PREPLAN– CLIENT ACCEPTANCE OR CONTINUATION

• INVESTIGATION

– REASONS FOR AUDIT– ENGAGEMENT LETTER– SELECT STAFF

Bina Nusantara University 12

• OBTAIN BACKGROUND INFORMATION– Knowledge of Client Industry– Tour Client Facilities– Identify Related Parties– Needs For Specialists

• CLIENT LEGAL OBLIGATIONS– Charter And By Laws– Minutes Of Meetings– Contracts

• PRELIMINARY ANALYTICAL REVIEW

Bina Nusantara University 13

WORKING PAPERS

• PURPOSES OF WORKING PAPERS– Planning Audit– Record Evidence Gathered– Basis For Audit Report– Basis For Review

• CONTENT AND ORGANIZATION– Permanent Files– Current Files

Bina Nusantara University 14

– WORKING TRIAL BALANCEGrouped Trial Balance– LEAD SCHEDULESFor Each Major Category, Listing Of All Account Type– ADJUSTING AND RECLASSIFICATION ENTRIES– SUPPORTING SCHEDULES

• ANALYSIS• TRIAL BALANCE OR LIST• RECONCILIATION• TEST OF REASONABLENESS• SUMMARY OF PROCEDURES• SUPPORTING DOCUMENTS• OUTSIDE DOCUMENTATION

Bina Nusantara University 15

• PREPARATION OF WORKING PAPERS– HEADING– INDEXING AND CROSS-REFERENCING– INDICATE AUDIT WORK PERFORMED– TICK MARKS– OBJECTIVE OF PREPARING WORK PAPER– CONCLUSIONS

• OWNERSHIP OF WORK PAPERS• CONFIDENTIALITY

Bina Nusantara University 16

PLANNING

• PREPLAN– CLIENT ACCEPTANCE OR CONTINUATION

• INVESTIGATION

– REASONS FOR AUDIT– ENGAGEMENT LETTER– SELECT STAFF

Bina Nusantara University 17

• OBTAIN BACKGROUND INFORMATION– KNOWLEDGE OF CLIENT INDUSTRY– TOUR CLIENT FACILITIES– IDENTIFY RELATED PARTIES– NEED FOR SPECIALISTS

• CLIENT LEGAL OBLIGATIONS– CHARTER AND BYLAWS– MINUTES OF MEETINGS– CONTARCTS

• PRELIMINARY ANALYTICAL REVIEW

Bina Nusantara University 18

WORKING PAPERS

• PURPOSES OF WORKING PAPERS– PLANNING AUDIT– RECORD EVIDENCE GATHERED– BASIS FOR AUDIT REPORT– BASIS FOR REVIEW

• CONTENT AND ORGANIZATION– PERMANENT FILES– CURRENT FILES

Bina Nusantara University 19

WORKING PAPERS

• Functions:1. Assignment and coordinating audit

work2. Supervising and reviewing the work of

assistants3. Supporting the report4. Complying with the stds of field work5. Planning and conducting the next audit

Bina Nusantara University 20

TYPES OF WORKING PAPERS

• Administrative working papers– Audit plan– Audit program– Time budget– Internal control documentation

• Working trial balance• Lead schedules• Adjusting journal entries

Bina Nusantara University 21

Types of Working Papers

• Supporting schedules• Analysis of a ledger account• Corroborating documents

Bina Nusantara University 22

ORGANIZATION

• Current files – one file per year • Permanent file – preserves working papers that

show relatively few or no changes– Articles of incorporation– Bylaws– Leases– Pension plans, labor contracts– Tax returns

Bina Nusantara University 23

TYPES OF TESTS

• PROCEDURES TO OBTAIN UNDERSTANDING OF INTERNAL CONTROL– INQUIRIES OF CLIENT– READ POLICY AND PROCEDURES MANUALS– EXAMINE DOCUMENTS– OBSERVE PERSONNEL

• TESTS OF CONTROL– OBSERVE PERSONNEL– REPERFORM PROCEDURES

• WAS PROCEDURE PERFORMED?• WAS IT PERFORMED CONSISTENTLY• WHO PERFORMED IT?

Bina Nusantara University 24

• SUBSTANTIVE TESTS OF TRANSACTIONS– TEST FOR DOLLAR MISSTATEMENT– SATISFY ALL SIX TRANSACTION-RELATED OBJECTIVES

FOR EACH CLASS OF TRANSACTIONS• RECORED SALES OCCURRED• RECORDED SALES ARE COMPLETE• RECORDED SALES ARE ACCURATE• RECORDED SALES ARE IN CORRECT TIME PERIOD• RECORDED SALES ARE PROPERLY CLASSIFIED• RECORDED SALES ARE ACCURATELY SUMMARIZED

• ANALYTICAL PROCEDURES– COMPARISONS OF DATA– FOUR PURPOSES

Bina Nusantara University 25

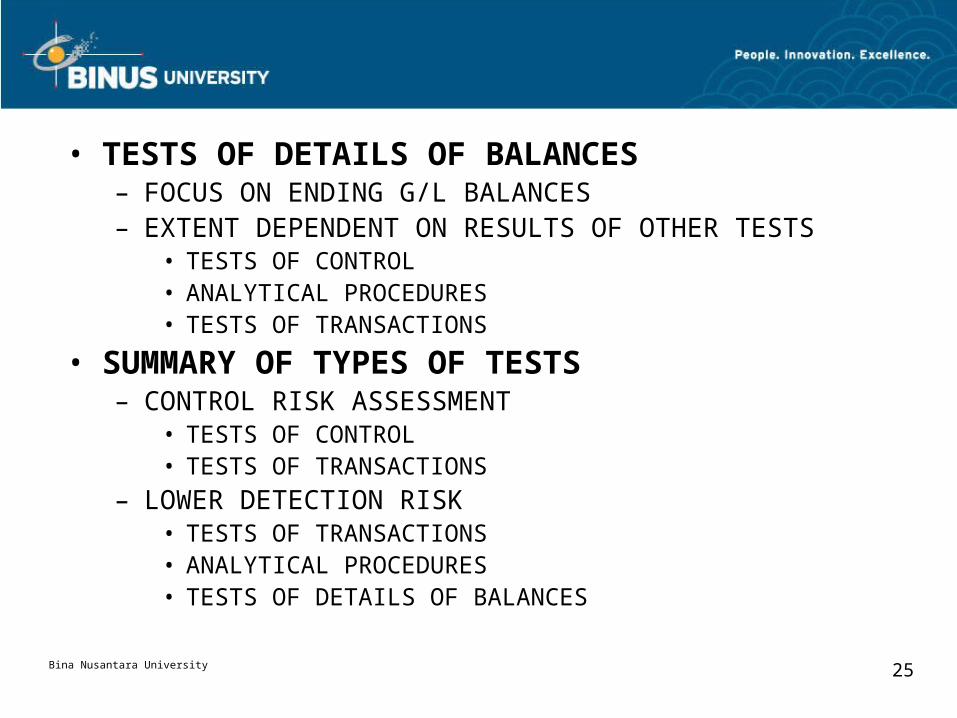

• TESTS OF DETAILS OF BALANCES– FOCUS ON ENDING G/L BALANCES– EXTENT DEPENDENT ON RESULTS OF OTHER TESTS

• TESTS OF CONTROL• ANALYTICAL PROCEDURES• TESTS OF TRANSACTIONS

• SUMMARY OF TYPES OF TESTS– CONTROL RISK ASSESSMENT

• TESTS OF CONTROL• TESTS OF TRANSACTIONS

– LOWER DETECTION RISK• TESTS OF TRANSACTIONS• ANALYTICAL PROCEDURES• TESTS OF DETAILS OF BALANCES

Bina Nusantara University 26

AUDIT EVIDENCE

• Any information that corroborates or refutes an assertion. Must be:– Competent – relevant and valid (Quality)– Sufficient – Quantity

• There is an inverse relationship between competent and sufficiency.

Bina Nusantara University 27

TYPES OF EVIDENCE1. Physical evidence- provides

evidence about existence but needs to be supplemented by other types of evidence.

Bina Nusantara University 28

TYPES OF EVIDENCE

2. Third party representations– Confirmations – effective at providing evidence about

existence.– Lawyers’ Letters – primary source of evidence

regarding lawsuits and litigation.– Reports of specialists

Bina Nusantara University 29

TYPES OF EVIDENCE

3. Documents– Created outside the client and transmitted directly to

the auditors– Created outside the client and held by the client– Created and held within the client

4. Computations5. Analytical reviews6. Oral and written client representation7. Accounting records

Bina Nusantara University 30

TESTS_EVIDENCE Relationship

• RELATIVE COSTS– ANALYTICAL PROCEDURES– PROCEDURES TO OBTAIN UNDERSTANDING OF I/C AND TESTS

OF CONTROL– SUBSTANTIVE TESTS OF TRANSACTIONS– TESTS OF DETAIL OF BALANCES

• RELATION BETWEEN TESTS OF CONTROL AND SUBSTANTIVE TESTS– DEVIATION FROM CONTROL INCREASES RISK OF DOLLAR ERROR

Bina Nusantara University 31

EVIDENCE MIX

• TRADE OFF BETWEEN TESTS OF CONTROL AND SUBSTANTIVE TESTS

Bina Nusantara University 32

AUDIT PLAN (AUDIT PROGRAM)

• Detailed listing of the audit procedures to be performed in the course of the audit (nature, timing, and extent).

• Objectives:– Design to accomplish audit objectives with respect to each

major account in the financial statements. These objectives are:

1. Existence or occurrence2. Completeness3. Rights and obligations4. Valuation or allocation5. Presentation and disclosure6. Accuracy7. Cutoff8. Classification

Bina Nusantara University 33

DESIGN AUDIT PROGRAM

• TESTS OF CONTROL AND SUBSTANTIVE TESTS OF TRANSACTIONS– FOUR STEPS

• APPLY TRANSACTION-RELATED OBJECTIVES • IDENTIFY SPECIFIC CONTROLS TO REDUCE RISK• DEVELOP TESTS OF CONTROL • DESIGN SUBSTANTIVE TESTS OF TRANSACTIONS FOR

POTENTIAL MISSTATEMENTS– CONSIDER CONTROL RISK ASSESSMENT

Bina Nusantara University 34

• ANALYTICAL PROCEDURES– AUDITOR JUDGMENT– INDUSTRY-SPECIFIC PROCEDURES

• TESTS OF DETAIL OF BALANCES– SET MATERIALITY LEVEL, ACCEPTABLE AUDIT RISK, AND

ASSESS INHERENT RISK– ASSESS CONTROL RISK– DESIGN TESTS OF BALANCES FOR EACH BALANCE-

RELATED OBJECTIVE

• RELATION OF AUDIT OBJECTIVES

Bina Nusantara University 35

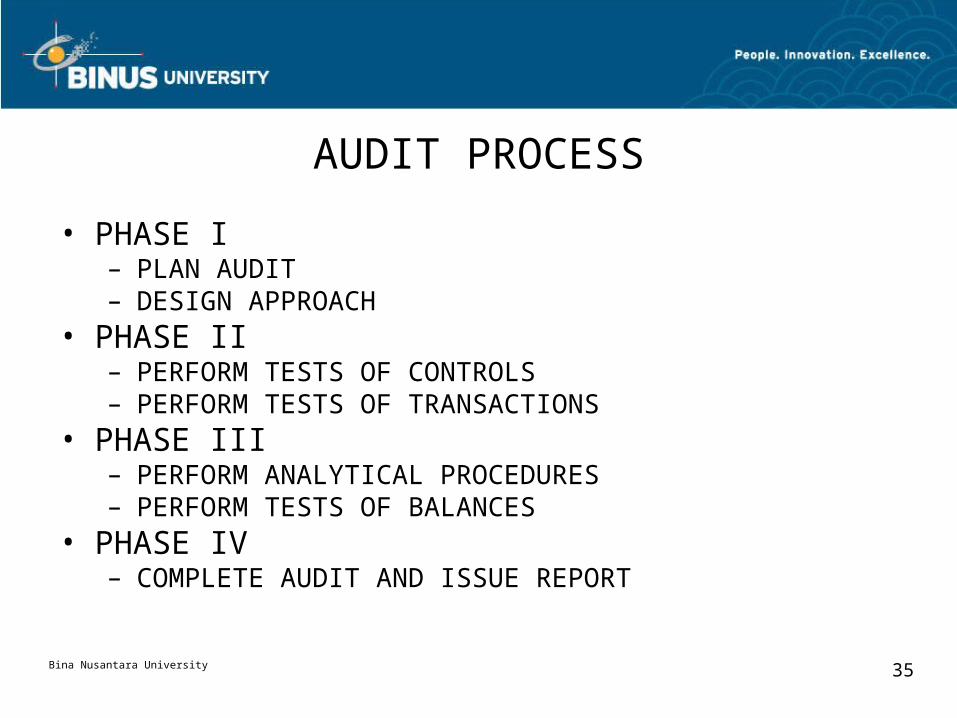

AUDIT PROCESS

• PHASE I– PLAN AUDIT– DESIGN APPROACH

• PHASE II– PERFORM TESTS OF CONTROLS– PERFORM TESTS OF TRANSACTIONS

• PHASE III– PERFORM ANALYTICAL PROCEDURES– PERFORM TESTS OF BALANCES

• PHASE IV– COMPLETE AUDIT AND ISSUE REPORT

Bina Nusantara University 36

AUDIT PROCEDURES

Hal-hal yang perlu dipertimbangkan dalam menyusun rencana kerja audit

– Timing– Nature– Extent – Cost

Bina Nusantara University 37

OTHER CONSIDERATIONS

– Confidential nature– Ownership of working papers– Auditors’ liability– Differences of opinion

Bina Nusantara University 38

THE End