Audi259 example 2(basic illustration)

18

A Life Insurance lllustration #2065877638 V2015.8.0 ClearVantage (L-19E) Your illustration is organized as follows: Section 1 - General Policy and Agent Information Section 2 - Description of Basic Policy Benefits Section 3 - Description of Additional Benefits Section 4 - Definition of Terms Section 5 - Signature Page and Summary of Values Section 6 - Additional Notes Section 1 - General Policy and Agent Information Product Description Policy Type: Indexed Flexible Premium Adjustable Life Policy Product Name: ClearVantage (L-19E) Form Number: L-19E State of Issue: IL Insured Name: Audi 529 Age/Sex: 30 Male Class: Preferred Plus Non-Tobacco Policy Owner Name: Audi 529 Agent Name: Blake Erickson Home Office Address: 111 East Wacker Drive, Suite 2100 Chicago, IL 60601-4508 Premium Premium Frequency: Annual Initial Planned Periodic Premium: $9,000.00 See -Section 6- for Variable Premium Information Premium Allocation: Credit Option 1 - 0% Credit Option 2 - 50% Credit Option 3 - 50% Rates Initial Short-Term Accumulation Value Interest Rate: 4.40% Initial Interest Rate (Credit Option 1): 4.40% Initial Participation Rate (Credit Option 2): 100% Initial Annual Index Cap Rate (Credit Option 3): 9.3% Benefit Information Initial Specified Amount: $2,000,000 Initial Death Benefit Option: B - Increasing Death Benefit Riders: None THIS IS AN ILLUSTRATION ONLY. IT IS NOT A CONTRACT. Prepared on: 6/9/2015 Prepared by: Blake Erickson THIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED Page 1 of 18

-

Upload

blake-erickson -

Category

Documents

-

view

214 -

download

2

description

Â

Transcript of Audi259 example 2(basic illustration)

A Life Insurance lllustration #2065877638V2015.8.0

ClearVantage(L-19E)

Your illustration is organized as follows:Section 1 - General Policy and Agent InformationSection 2 - Description of Basic Policy BenefitsSection 3 - Description of Additional BenefitsSection 4 - Definition of TermsSection 5 - Signature Page and Summary of ValuesSection 6 - Additional Notes

Section 1 - General Policy and Agent Information

Product Description Policy Type: Indexed Flexible Premium Adjustable Life Policy

Product Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529

Age/Sex: 30 MaleClass: Preferred Plus Non-Tobacco

Policy Owner Name: Audi 529

Agent Name: Blake Erickson

Home Office Address: 111 East Wacker Drive, Suite 2100Chicago, IL 60601-4508

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See -Section 6- for Variable Premium InformationPremium Allocation: Credit Option 1 - 0% Credit Option 2 - 50% Credit Option 3 - 50%

Rates Initial Short-Term Accumulation Value Interest Rate: 4.40%

Initial Interest Rate (Credit Option 1): 4.40%Initial Participation Rate (Credit Option 2): 100%Initial Annual Index Cap Rate (Credit Option 3): 9.3%

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

THIS IS AN ILLUSTRATION ONLY. IT IS NOT A CONTRACT.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 1 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 2 - Description of Basic Policy Benefits

This illustration is based on a life insurance product that is referred to as an Indexed Flexible Premium Adjustable Life. This individual life insurance policy allows the Owner flexibility in both premium payments and death benefits.

Premium Outlay The Owner has the option to vary the amount and timing of the Planned Periodic Premium as long as the premiums are sufficient to keep the policy in force and do not violate the maximum limitations imposed by tax law. The illustration assumes that premium payments are made at the beginning of the modal period. If actual premium payments are different than the Planned Periodic Premiums or the payment dates are not consistent with the assumptions in the illustration, then the policy values will be different than those in this illustration. Note that if premium payments are suspended, then policy charges will continue to be applied against the policy values. Additional premiums may be required to keep the policy in force.

Because the policy owner may choose to pay different premiums in the future, and credits to the policy will vary over time, the policy value should be regularly monitored to ensure the funding level and performance remain consistent with the policy owner's goals. A current illustration may be requested annually without charge.

Death Benefits A death benefit will be provided to the designated beneficiary upon the death of the insured. The death benefit is based on the Policy Specified Amount, Death Benefit Option, and Accumulation Account. The Owner may request changes in the Policy Specified Amount and/or Death Benefit Option after the first policy year. Increases in Specified Amount or Option changes may require the insured to submit evidence of insurability. This illustration is based on an Increasing Death Benefit Option. The death benefit is equal to the greater of the Policy Specified Amount plus the Accumulation Account or the Accumulation Account multiplied by the minimum death benefit corridor factor (refer to the Policy's Table of Minimum Death benefits). Death benefits are illustrated at the end of the year.

Policy Values The Owner is entitled to receive the Cash Surrender Value upon surrender. The Cash Surrender Value equals the Total Accumulation Value (which equals the sum of the Short-Term Accumulation Value and the Credit Option Accumulation Values) less the total of the Surrender Charge and any current indebtedness.

Lapse Basis During the first 15 policy years, the Owner must pay at least the Minimum Premium. Payment of the Minimum Premium will guarantee coverage during this period. Thereafter, the policy will continue in force as long as the Cash Surrender Value is greater than zero.

Income Options There are two ways the Owner may withdraw money from the contract without surrendering the policy:

1) You may borrow funds from the policy through a Policy Loan.

2) You may permanently withdraw funds from the policy using a Partial Withdrawal. The Cash Surrender Value of the policy will be reduced by the amount of the Partial Withdrawal plus an administrative charge of $25. If the Death Benefit Option is A (Level Benefit), then the Policy Specified Amount will also be reduced by the amount of the Partial Withdrawal and a pro-rata surrender charge will be imposed against the Accumulation Account.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 2 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 2 - Description of Basic Policy Benefits

Withdrawals will reduce your Index Credits.

Non-Guaranteed Elements

The actual interest rate, participation rate, cap rate, cost of insurance and expense charge used to determine the policy values are set by the insurance company and are not guaranteed. The current charges are based on current company expectations as to future experience. There are maximum limits on the policy charges and minimum guaranteed interest rates. The non-guaranteed elements in this policy are described below.

FIXED INTEREST RATE: The fixed interest rate is the interest rate credited to the Short-Term Accumulation Value or the Credit Option 1 - Fixed Rate Strategy. The fixed interest rate may exceed the guaranteed minimum fixed interest rate. We may change the rate monthly.

PARTICIPATION RATE - The Participation Rate represents the participation in the Index and in the percentage We use to calculate the Index Credit. The Participation Rate is declared by Us on each Allocation Date of the Short-Term Accumulation Value, transfers or renewals allocated to Credit Option 2. It is guaranteed for the term period and can never be less than 10%. The current Participation Rate for Credit Option 2 – S&P 500® Index One-Year Monthly Averaging with Participation Rate Strategy is 100%.

ANNUAL INDEX CAP RATE: The Annual Index Cap Rate is declared by Us on each Allocation Date and is the rate We use to calculate the Index Credit for Account Value allocated to Credit Option 3. It is guaranteed for the term period. The Cap Rate will never be less than 3.00%. The current Annual Cap Rate for Credit Option 3 – S&P 500® Index One-Year Point-To-Point with Cap Strategy is 9.3%.

TERM PERIOD: The term period is a one-year period beginning on each Allocation Date.

COST OF INSURANCE - We will establish current monthly Cost of Insurance rates. The current monthly cost of insurance rates will not be greater than the guaranteed monthly cost of insurance rates.

EXPENSE CHARGE: We will establish the premium expense charge, the monthly expense charge and the per unit expense charge. The non-guaranteed scale of expense charges will never be greater than the scale that is guaranteed. We may change the non-guaranteed scale at any time.

WEIGHTED AVERAGE INDEX CREDIT RATE: The Weighted Average Index Credit Rate shown on the non-guaranteed illustrated values page is based on the premium allocated to Credit Options 2 and 3. The premium allocation strategy is shown on page 1 of this illustration. The illustration assumes that the weighted average index credit will continue unchanged for all the years shown. This is not likely to occur, and the actual results may be more or less favorable than those shown.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 3 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 2 - Description of Basic Policy Benefits

Credit Options and Accumulation Value Credit

CREDIT OPTION 1 – FIXED RATE STRATEGY: We will calculate interest for the Credit Option Accumulation Value based on the interest rate set by Us. The Credit Option 1 fixed interest rate will never be less than the guaranteed minimum interest rate of 1%. Additional interest, if any, paid over the guaranteed minimum interest rate will be in an amount and by a method determined by Us.

CREDIT OPTION 2 – S&P 500® INDEX ONE-YEAR MONTHLY AVERAGING WITH PARTICIPATION RATE STRATEGY: We will calculate an Index Credit for the Credit Option Accumulation Value based on performance of the Standard & Poor's 500® Composite Stock Price Index* (S&P 500®). The credit will be paid on each Allocation Date. The Index Crediting Rate will never be less than 1% and will be calculated as follows:

1) The Index Average for the Term Period, DIVIDED BY2) the Index Value on the Allocation Date, MINUS3) one, TIMES4) the Participation Rate.

Credit Option 2 assumes a non-guaranteed index credit rate of 7.12% which is based on the historical monthly performance of the S&P 500® during the past 25 years, substituting the guaranteed minimum Index Credit Rate of 1% whenever the Index return is less.

CREDIT OPTION 3 – S&P 500® INDEX ONE-YEAR POINT-TO-POINT WITH CAP STRATEGY: We will calculate an Index Credit for the Credit Option Accumulation Value based on performance of the Standard & Poor's 500® Composite Stock Price Index* (S&P 500®). The credit will be paid on each Allocation Date. The Index Crediting Rate will never be less than 1%, and will be calculated as the lesser of 1) and 2) as follows:

1) Equals:a. the Index Value at the end of the Term Period, DIVIDED BYb. the Index Value on the Allocation Date, MINUSc. one (1).2) the Annual Index Cap Rate.

Credit Option 3 assumes a non-guaranteed index credit rate of 6.64% which is based on the historical monthly performance of the S&P 500® during the past 25 years, substituting the guaranteed minimum Index Credit Rate of 1% whenever the Index return is less.

INDEX CREDIT ENHANCEMENT – For all credit options, excluding the Fixed Rate Credit Option, and for all term periods that begin after the fifteenth Policy Anniversary, We will add an index credit enhancement to each Index Credit. The Index Credit Enhancement percentage is 0.25%.

FIXED RATE CREDIT OPTION ENHANCEMENT – For the Fixed Rate Credit Option and the Short-Term Accumulation Value, if the interest rate declared by Us exceeds the guaranteed minimum interest rate, then We will increase the annualized declared interest rate by 0.25% after the fifteenth Policy Anniversary. This increase will not apply to any loaned Accumulation Value.

*"S&P®", "S&P 500®", "Standard & Poor's 500®", and "500®" are trademarks of the McGraw-Hill Companies, Inc. and have been licensed for use by Bankers Life and Casualty Company. The policy is not sponsored, endorsed, sold or promoted by Standard & Poor's and Standard & Poor's makes no representation regarding the advisability of purchasing this product.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 4 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 2 - Description of Basic Policy Benefits

The S&P 500® does not include dividends.

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - N O T I C E - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -THIS ILLUSTRATION INCLUDES VALUES THAT ARE NOT GUARANTEED. THE ILLUSTRATION ASSUMESTHAT THE CURRENTLY ILLUSTRATED NON-GUARANTEED ELEMENTS WILL CONTINUE UNCHANGED

FOR ALL YEARS SHOWN. THIS IS NOT LIKELY TO OCCUR, AND THE ACTUAL RESULTS MAY BE MOREOR LESS FAVORABLE THAN THOSE SHOWN.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 5 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 3 - Description of Additional Benefits

The policy as illustrated contains no riders or other additional benefits.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 6 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 4 - Definition of Terms

The column headings and key terms shown in the illustration of values are defined below.

SHORT-TERM ACCUMULATION VALUE (STAV), at issue, equals the net initial premium less any initial monthly deductions. The Net Premium is the paid premium less the premium expense charge. On the transfer date, the amount in the STAV is transferred to the COAV according to the policyholder selected allocation percentages. On each monthly anniversary during the year, deductions are applied proportionally to the STAV and COAV. Any new premium is directed to the STAV until the next monthly transfer date. A fixed interest rate is credited daily, using a rate declared by Us, on any net premium remaining in the STAV until the next monthly transfer date. The STAV fixed interest rate will never be less than the guaranteed minimum interest rate of 1%.

CREDIT OPTION ACCUMULATION VALUE (COAV) is the sum of all amounts transferred from the STAV to the COAV, plus any interest and index credits, and less any pro rata charge for insurance and expenses, as well as any prorated partial withdrawals and/or policy loans. Surrender charges, however, are not considered. This illustration assumes: 0% of the net premium from the STAV is allocated to the COAV Credit Option 1 50% of the net premium from the STAV is allocated to the COAV Credit Option 2 50% of the net premium from the STAV is allocated to the COAV Credit Option 3

These values are shown as of end of each policy year.

TOTAL ACCUMULATION VALUE equals the sum of the STAV and the COAV.

CASH SURRENDER VALUE is the amount available to the Owner upon surrender of the policy. It is equal to the Total Accumulation Value less any applicable surrender charges and any outstanding loan balance.

NET LOANS is the Net Policy Loan activity during the policy year. This amount equals the Policy Loans taken less loan repayments and loan interest paid by the policy owner. Loan interest charged to the policy is not included in this column. Illustration assumes Policy Loans and loan repayments occur at the beginning of each policy year. If the amount of repayments and interest payments exceeds the amount of new Policy Loans distributed during that year, this value will be negative.

CUMULATIVE PREMIUM OUTLAY is the sum of all premiums paid less the sum of all paid distributions to the policyholder via withdrawal or policy loans. If the amount of projected paid distributions is greater than the amount of projected paid premiums, this value will be negative for a given duration. The sum of any loan interest payments is not considered a paid premium.

MINIMUM INITIAL PREMIUM (MIP) is the minimum initial premium required to guarantee coverage for 15 years or attained age 95, whichever occurs first.

MAXIMUM ANNUAL PREMIUM (MAP) is a premium limit defined by the Deficit Reduction Act of 1984 (DEFRA). The MAP amount is not an annual premium maximum, but rather an annual amount for calculating the cumulative limit. The maximum annual premium that can be paid into the policy each year is $48,858.04. This premium is based on the policy, as issued, and ignores any future policy adjustments, Policy Loans or Partial Withdrawals that may be reflectedin the illustration. This premium, if paid in all years, will NOT guarantee coverage until maturity age 121.

MAXIMUM SINGLE PREMIUM (MSP) is the only exception to the MAP limit. To avoid violating DEFRA guidelines, paid premiums in any year must be less than the greater of the cumulative MAP and the MSP.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 7 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 4 - Definition of Terms

MODIFIED ENDOWMENT PREMIUM (MEP) is a premium limit defined in Section 7702 of the IRS code that defines MEC policies. A MEC is still a life insurance contract. However, lifetime distributions from it, either by loan or partial withdrawal, are taxed to the extent they represent accumulated interest which is deemed distributed first. Death benefits can still be received by named beneficiaries free of income tax under current law if the policy is properly arranged and managed. The MEP amount is not an annual premium maximum, but rather an annual amount for calculating the cumulative MEC limit. If the cumulative premium actually paid during the first seven years exceeds the cumulative MEP premium, the policy becomes a MEC.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 8 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 5A - Signature Page

Product Description Policy Type: Indexed Flexible Premium Adjustable Life PolicyProduct Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529Age/Sex/Class: 30 Male Preferred Plus Non-Tobacco

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See - Section 6 - for Variable Premium Information

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

Summary of ValuesValues Based on

Guaranteed ElementsNon-Guaranteed Values

Based on Midpoint ElementsNon-Guaranteed Values

Based on Assumed Elements

STAV Fixed Interest Rate 1.00% 2.70% 4.40%Credit Opt 1 Fixed Interest Rate 1.00% 2.70% 4.40%

Credit Opts 2, 3 Index Credit 1.00% 3.94% 6.88%

Year 5 Cash Surrender Value 0 0 0Death Benefit 2,016,678 2,021,347 2,025,975

Cumulative Premium Outlay 45,000 45,000 45,000

Year 10 Cash Surrender Value 4,522 17,653 31,637Death Benefit 2,031,953 2,045,084 2,059,069

Cumulative Premium Outlay 90,000 90,000 90,000

Year 20 Cash Surrender Value 42,865 113,884 207,678Death Benefit 2,042,865 2,113,884 2,207,678

Cumulative Premium Outlay 180,000 180,000 180,000

Age 70 Cash Surrender Value 434,254 1,269,541 2,562,011Death Benefit 2,817,445 3,011,350 3,305,396

Cumulative Premium Outlay 1,119,807 1,119,807 1,119,807

Year coverage will expire 43 48 91

THIS ILLUSTRATION IS NOT COMPLIANT WITH THE NAIC MODEL BECAUSE OF POLICY LOANS, AND PARTIAL WITHDRAWALS, AND DEATH BENEFIT OPTION CHANGES, AND PREMIUM AMOUNT OR TIMING CHANGES.

SEE SECTION THREE AND/OR SIX FOR DETAILS. USE OF THESE PAGES IS FOR INFORMATIONAL PURPOSES ONLY AND IS NOT INTENDED TO CREATE PUBLIC INTEREST IN THE SALE OF LIFE INSURANCE.The above summary assumes a premium allocation of 0% to Credit Option 1, 50% to Credit Option 2 and 50% to Credit Option 3. The policy may lapse prior to policy maturity (Age 121).

"S&P®", "S&P 500®", "Standard & Poor's 500®", and "500" are trademarks of the McGraw-Hill Companies, Inc. and have been licensed for use by Bankers Life and Casualty Company. The policy is not sponsored, endorsed, sold or promoted by Standard & Poor's and Standard & Poor's makes no representation regarding the advisability of purchasing this product.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 9 of 18

A Life Insurance lllustration #2065877638V2015.8.0

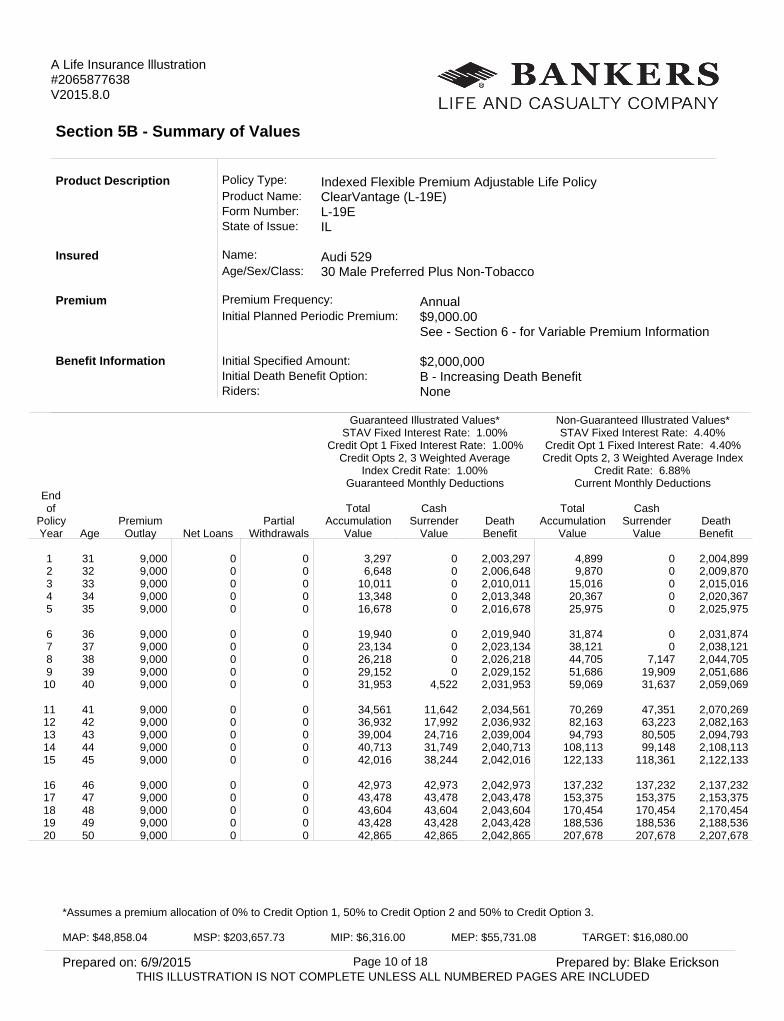

Section 5B - Summary of Values

Product Description Policy Type: Indexed Flexible Premium Adjustable Life PolicyProduct Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529Age/Sex/Class: 30 Male Preferred Plus Non-Tobacco

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See - Section 6 - for Variable Premium Information

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

Guaranteed Illustrated Values*

STAV Fixed Interest Rate: 1.00%Credit Opt 1 Fixed Interest Rate: 1.00%

Credit Opts 2, 3 Weighted AverageIndex Credit Rate: 1.00%

Guaranteed Monthly Deductions

Non-Guaranteed Illustrated Values*STAV Fixed Interest Rate: 4.40%

Credit Opt 1 Fixed Interest Rate: 4.40%Credit Opts 2, 3 Weighted Average Index

Credit Rate: 6.88%Current Monthly Deductions

Endof

PolicyYear Age

PremiumOutlay Net Loans

PartialWithdrawals

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

1 31 9,000 0 0 3,297 0 2,003,297 4,899 0 2,004,8992 32 9,000 0 0 6,648 0 2,006,648 9,870 0 2,009,8703 33 9,000 0 0 10,011 0 2,010,011 15,016 0 2,015,0164 34 9,000 0 0 13,348 0 2,013,348 20,367 0 2,020,3675 35 9,000 0 0 16,678 0 2,016,678 25,975 0 2,025,975 6 36 9,000 0 0 19,940 0 2,019,940 31,874 0 2,031,8747 37 9,000 0 0 23,134 0 2,023,134 38,121 0 2,038,1218 38 9,000 0 0 26,218 0 2,026,218 44,705 7,147 2,044,7059 39 9,000 0 0 29,152 0 2,029,152 51,686 19,909 2,051,68610 40 9,000 0 0 31,953 4,522 2,031,953 59,069 31,637 2,059,069

11 41 9,000 0 0 34,561 11,642 2,034,561 70,269 47,351 2,070,26912 42 9,000 0 0 36,932 17,992 2,036,932 82,163 63,223 2,082,16313 43 9,000 0 0 39,004 24,716 2,039,004 94,793 80,505 2,094,79314 44 9,000 0 0 40,713 31,749 2,040,713 108,113 99,148 2,108,11315 45 9,000 0 0 42,016 38,244 2,042,016 122,133 118,361 2,122,133

16 46 9,000 0 0 42,973 42,973 2,042,973 137,232 137,232 2,137,23217 47 9,000 0 0 43,478 43,478 2,043,478 153,375 153,375 2,153,37518 48 9,000 0 0 43,604 43,604 2,043,604 170,454 170,454 2,170,45419 49 9,000 0 0 43,428 43,428 2,043,428 188,536 188,536 2,188,53620 50 9,000 0 0 42,865 42,865 2,042,865 207,678 207,678 2,207,678

*Assumes a premium allocation of 0% to Credit Option 1, 50% to Credit Option 2 and 50% to Credit Option 3.

MAP: $48,858.04 MSP: $203,657.73 MIP: $6,316.00 MEP: $55,731.08 TARGET: $16,080.00

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 10 of 18

A Life Insurance lllustration #2065877638V2015.8.0

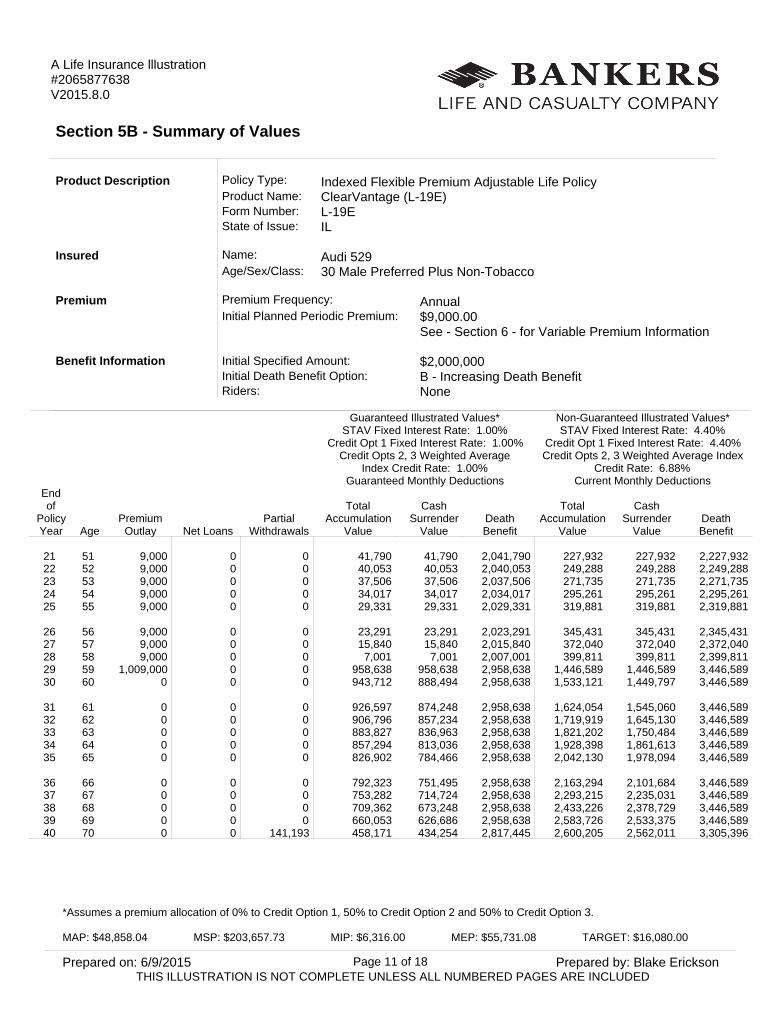

Section 5B - Summary of Values

Product Description Policy Type: Indexed Flexible Premium Adjustable Life PolicyProduct Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529Age/Sex/Class: 30 Male Preferred Plus Non-Tobacco

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See - Section 6 - for Variable Premium Information

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

Guaranteed Illustrated Values*

STAV Fixed Interest Rate: 1.00%Credit Opt 1 Fixed Interest Rate: 1.00%

Credit Opts 2, 3 Weighted AverageIndex Credit Rate: 1.00%

Guaranteed Monthly Deductions

Non-Guaranteed Illustrated Values*STAV Fixed Interest Rate: 4.40%

Credit Opt 1 Fixed Interest Rate: 4.40%Credit Opts 2, 3 Weighted Average Index

Credit Rate: 6.88%Current Monthly Deductions

Endof

PolicyYear Age

PremiumOutlay Net Loans

PartialWithdrawals

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

21 51 9,000 0 0 41,790 41,790 2,041,790 227,932 227,932 2,227,93222 52 9,000 0 0 40,053 40,053 2,040,053 249,288 249,288 2,249,28823 53 9,000 0 0 37,506 37,506 2,037,506 271,735 271,735 2,271,73524 54 9,000 0 0 34,017 34,017 2,034,017 295,261 295,261 2,295,26125 55 9,000 0 0 29,331 29,331 2,029,331 319,881 319,881 2,319,881

26 56 9,000 0 0 23,291 23,291 2,023,291 345,431 345,431 2,345,43127 57 9,000 0 0 15,840 15,840 2,015,840 372,040 372,040 2,372,04028 58 9,000 0 0 7,001 7,001 2,007,001 399,811 399,811 2,399,81129 59 1,009,000 0 0 958,638 958,638 2,958,638 1,446,589 1,446,589 3,446,58930 60 0 0 0 943,712 888,494 2,958,638 1,533,121 1,449,797 3,446,589

31 61 0 0 0 926,597 874,248 2,958,638 1,624,054 1,545,060 3,446,58932 62 0 0 0 906,796 857,234 2,958,638 1,719,919 1,645,130 3,446,58933 63 0 0 0 883,827 836,963 2,958,638 1,821,202 1,750,484 3,446,58934 64 0 0 0 857,294 813,036 2,958,638 1,928,398 1,861,613 3,446,58935 65 0 0 0 826,902 784,466 2,958,638 2,042,130 1,978,094 3,446,589

36 66 0 0 0 792,323 751,495 2,958,638 2,163,294 2,101,684 3,446,58937 67 0 0 0 753,282 714,724 2,958,638 2,293,215 2,235,031 3,446,58938 68 0 0 0 709,362 673,248 2,958,638 2,433,226 2,378,729 3,446,58939 69 0 0 0 660,053 626,686 2,958,638 2,583,726 2,533,375 3,446,58940 70 0 0 141,193 458,171 434,254 2,817,445 2,600,205 2,562,011 3,305,396

*Assumes a premium allocation of 0% to Credit Option 1, 50% to Credit Option 2 and 50% to Credit Option 3.

MAP: $48,858.04 MSP: $203,657.73 MIP: $6,316.00 MEP: $55,731.08 TARGET: $16,080.00

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 11 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 5B - Summary of Values

Product Description Policy Type: Indexed Flexible Premium Adjustable Life PolicyProduct Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529Age/Sex/Class: 30 Male Preferred Plus Non-Tobacco

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See - Section 6 - for Variable Premium Information

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

Guaranteed Illustrated Values*

STAV Fixed Interest Rate: 1.00%Credit Opt 1 Fixed Interest Rate: 1.00%

Credit Opts 2, 3 Weighted AverageIndex Credit Rate: 1.00%

Guaranteed Monthly Deductions

Non-Guaranteed Illustrated Values*STAV Fixed Interest Rate: 4.40%

Credit Opt 1 Fixed Interest Rate: 4.40%Credit Opts 2, 3 Weighted Average Index

Credit Rate: 6.88%Current Monthly Deductions

Endof

PolicyYear Age

PremiumOutlay Net Loans

PartialWithdrawals

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

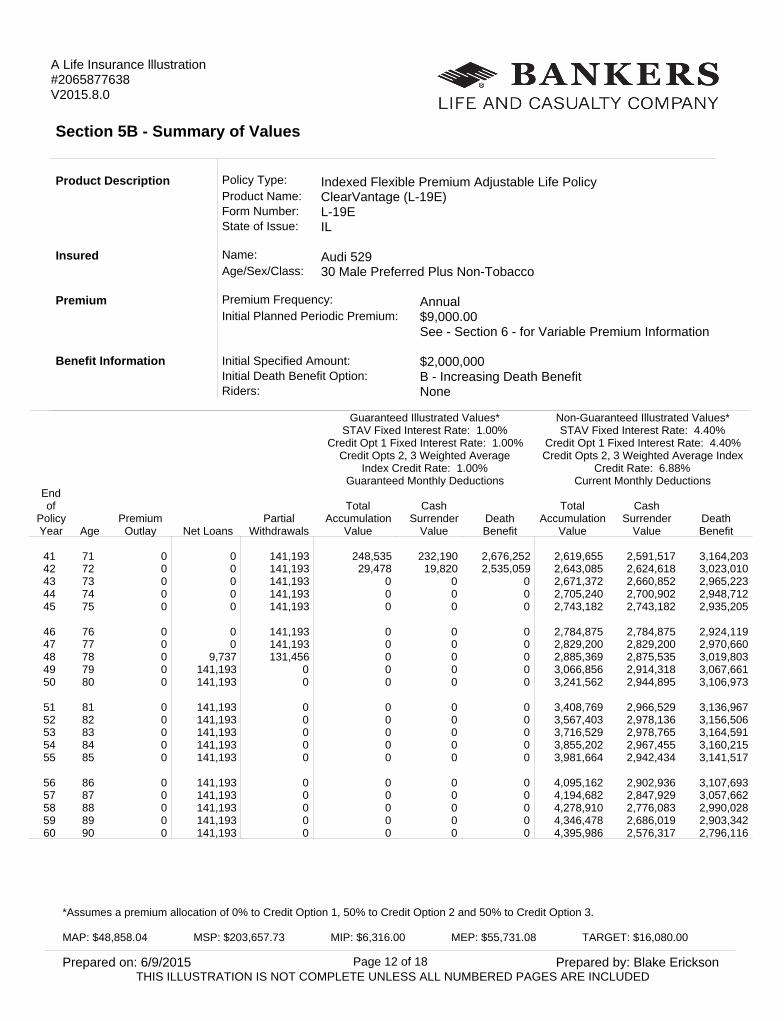

41 71 0 0 141,193 248,535 232,190 2,676,252 2,619,655 2,591,517 3,164,20342 72 0 0 141,193 29,478 19,820 2,535,059 2,643,085 2,624,618 3,023,01043 73 0 0 141,193 0 0 0 2,671,372 2,660,852 2,965,22344 74 0 0 141,193 0 0 0 2,705,240 2,700,902 2,948,71245 75 0 0 141,193 0 0 0 2,743,182 2,743,182 2,935,205

46 76 0 0 141,193 0 0 0 2,784,875 2,784,875 2,924,11947 77 0 0 141,193 0 0 0 2,829,200 2,829,200 2,970,66048 78 0 9,737 131,456 0 0 0 2,885,369 2,875,535 3,019,80349 79 0 141,193 0 0 0 0 3,066,856 2,914,318 3,067,66150 80 0 141,193 0 0 0 0 3,241,562 2,944,895 3,106,973

51 81 0 141,193 0 0 0 0 3,408,769 2,966,529 3,136,96752 82 0 141,193 0 0 0 0 3,567,403 2,978,136 3,156,50653 83 0 141,193 0 0 0 0 3,716,529 2,978,765 3,164,59154 84 0 141,193 0 0 0 0 3,855,202 2,967,455 3,160,21555 85 0 141,193 0 0 0 0 3,981,664 2,942,434 3,141,517

56 86 0 141,193 0 0 0 0 4,095,162 2,902,936 3,107,69357 87 0 141,193 0 0 0 0 4,194,682 2,847,929 3,057,66258 88 0 141,193 0 0 0 0 4,278,910 2,776,083 2,990,02859 89 0 141,193 0 0 0 0 4,346,478 2,686,019 2,903,34260 90 0 141,193 0 0 0 0 4,395,986 2,576,317 2,796,116

*Assumes a premium allocation of 0% to Credit Option 1, 50% to Credit Option 2 and 50% to Credit Option 3.

MAP: $48,858.04 MSP: $203,657.73 MIP: $6,316.00 MEP: $55,731.08 TARGET: $16,080.00

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 12 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 5B - Summary of Values

Product Description Policy Type: Indexed Flexible Premium Adjustable Life PolicyProduct Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529Age/Sex/Class: 30 Male Preferred Plus Non-Tobacco

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See - Section 6 - for Variable Premium Information

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

Guaranteed Illustrated Values*

STAV Fixed Interest Rate: 1.00%Credit Opt 1 Fixed Interest Rate: 1.00%

Credit Opts 2, 3 Weighted AverageIndex Credit Rate: 1.00%

Guaranteed Monthly Deductions

Non-Guaranteed Illustrated Values*STAV Fixed Interest Rate: 4.40%

Credit Opt 1 Fixed Interest Rate: 4.40%Credit Opts 2, 3 Weighted Average Index

Credit Rate: 6.88%Current Monthly Deductions

Endof

PolicyYear Age

PremiumOutlay Net Loans

PartialWithdrawals

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

61 91 0 141,193 0 0 0 0 4,426,110 2,445,639 2,666,94562 92 0 141,193 0 0 0 0 4,442,507 2,299,627 2,477,32763 93 0 141,193 0 0 0 0 4,445,384 2,138,470 2,271,83164 94 0 141,193 0 0 0 0 4,452,202 1,979,614 2,068,65865 95 0 141,193 0 0 0 0 4,464,872 1,824,953 1,869,602

66 96 0 141,193 0 0 0 0 4,475,715 1,666,792 1,711,54967 97 0 141,193 0 0 0 0 4,484,541 1,504,924 1,549,76968 98 0 141,193 0 0 0 0 4,491,280 1,339,261 1,384,17469 99 0 141,193 0 0 0 0 4,495,855 1,169,711 1,214,67070 100 0 141,193 0 0 0 0 4,498,439 996,429 1,041,413

71 101 0 0 0 0 0 0 4,500,392 963,362 1,008,36672 102 0 0 0 0 0 0 4,501,673 929,273 974,28973 103 0 0 0 0 0 0 4,502,236 894,112 939,13474 104 0 0 0 0 0 0 4,502,035 857,829 902,85075 105 0 0 0 0 0 0 4,501,024 820,377 865,387

76 106 0 0 0 0 0 0 4,499,160 781,706 826,69877 107 0 0 0 0 0 0 4,496,390 741,761 786,72578 108 0 0 0 0 0 0 4,492,657 700,483 745,40979 109 0 0 0 0 0 0 4,487,907 657,810 702,68980 110 0 0 0 0 0 0 4,482,078 613,680 658,501

*Assumes a premium allocation of 0% to Credit Option 1, 50% to Credit Option 2 and 50% to Credit Option 3.

MAP: $48,858.04 MSP: $203,657.73 MIP: $6,316.00 MEP: $55,731.08 TARGET: $16,080.00

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 13 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 5B - Summary of Values

Product Description Policy Type: Indexed Flexible Premium Adjustable Life PolicyProduct Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529Age/Sex/Class: 30 Male Preferred Plus Non-Tobacco

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See - Section 6 - for Variable Premium Information

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

Guaranteed Illustrated Values*

STAV Fixed Interest Rate: 1.00%Credit Opt 1 Fixed Interest Rate: 1.00%

Credit Opts 2, 3 Weighted AverageIndex Credit Rate: 1.00%

Guaranteed Monthly Deductions

Non-Guaranteed Illustrated Values*STAV Fixed Interest Rate: 4.40%

Credit Opt 1 Fixed Interest Rate: 4.40%Credit Opts 2, 3 Weighted Average Index

Credit Rate: 6.88%Current Monthly Deductions

Endof

PolicyYear Age

PremiumOutlay Net Loans

PartialWithdrawals

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

81 111 0 0 0 0 0 0 4,475,109 568,027 612,77882 112 0 0 0 0 0 0 4,466,936 520,784 565,45383 113 0 0 0 0 0 0 4,457,494 471,880 516,45584 114 0 0 0 0 0 0 4,446,714 421,244 465,71185 115 0 0 0 0 0 0 4,434,528 368,803 413,148

86 116 0 0 0 0 0 0 4,420,864 314,482 358,69087 117 0 0 0 0 0 0 4,405,650 258,205 302,26188 118 0 0 0 0 0 0 4,388,816 199,896 243,78489 119 0 0 0 0 0 0 4,370,289 139,479 183,18290 120 0 0 0 0 0 0 4,350,002 76,885 120,385

91 121 0 0 0 0 0 0 4,327,954 12,105 55,385

*Assumes a premium allocation of 0% to Credit Option 1, 50% to Credit Option 2 and 50% to Credit Option 3.

MAP: $48,858.04 MSP: $203,657.73 MIP: $6,316.00 MEP: $55,731.08 TARGET: $16,080.00

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 14 of 18

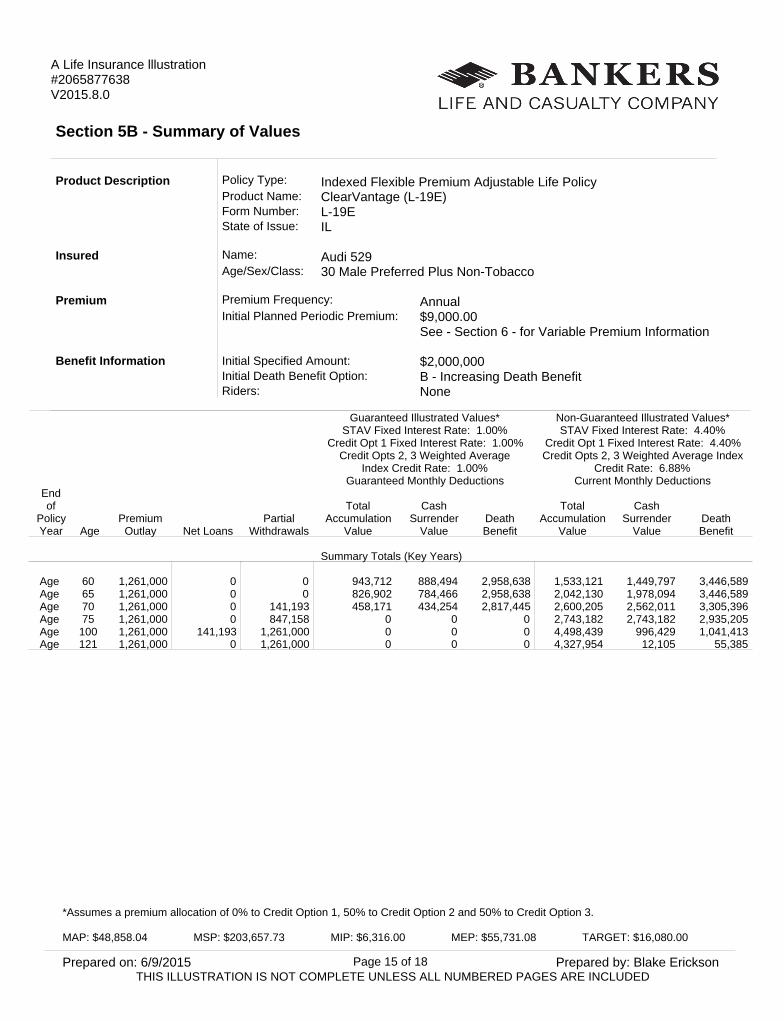

A Life Insurance lllustration #2065877638V2015.8.0

Section 5B - Summary of Values

Product Description Policy Type: Indexed Flexible Premium Adjustable Life PolicyProduct Name: ClearVantage (L-19E)Form Number: L-19EState of Issue: IL

Insured Name: Audi 529Age/Sex/Class: 30 Male Preferred Plus Non-Tobacco

Premium Premium Frequency: AnnualInitial Planned Periodic Premium: $9,000.00

See - Section 6 - for Variable Premium Information

Benefit Information Initial Specified Amount: $2,000,000Initial Death Benefit Option: B - Increasing Death BenefitRiders: None

Guaranteed Illustrated Values*

STAV Fixed Interest Rate: 1.00%Credit Opt 1 Fixed Interest Rate: 1.00%

Credit Opts 2, 3 Weighted AverageIndex Credit Rate: 1.00%

Guaranteed Monthly Deductions

Non-Guaranteed Illustrated Values*STAV Fixed Interest Rate: 4.40%

Credit Opt 1 Fixed Interest Rate: 4.40%Credit Opts 2, 3 Weighted Average Index

Credit Rate: 6.88%Current Monthly Deductions

Endof

PolicyYear Age

PremiumOutlay Net Loans

PartialWithdrawals

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

TotalAccumulation

Value

CashSurrender

ValueDeathBenefit

Summary Totals (Key Years)

Age 60 1,261,000 0 0 943,712 888,494 2,958,638 1,533,121 1,449,797 3,446,589Age 65 1,261,000 0 0 826,902 784,466 2,958,638 2,042,130 1,978,094 3,446,589Age 70 1,261,000 0 141,193 458,171 434,254 2,817,445 2,600,205 2,562,011 3,305,396Age 75 1,261,000 0 847,158 0 0 0 2,743,182 2,743,182 2,935,205Age 100 1,261,000 141,193 1,261,000 0 0 0 4,498,439 996,429 1,041,413Age 121 1,261,000 0 1,261,000 0 0 0 4,327,954 12,105 55,385

*Assumes a premium allocation of 0% to Credit Option 1, 50% to Credit Option 2 and 50% to Credit Option 3.

MAP: $48,858.04 MSP: $203,657.73 MIP: $6,316.00 MEP: $55,731.08 TARGET: $16,080.00

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 15 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 6 - Additional Notes

Interest AdjustedIndexes (5.00%) Surrender Net Payment

10 Years 20 Years 10 Years 20 YearsCurrent 3.22 1.46 4.39 4.33

Guaranteed 4.24 3.80 4.41 4.40

An explanation of the intended use of these indexes is provided in the "Life Insurance Buyer's Guide."

Tax Notice The information above was written to support the sales and marketing of insurance policies offered by Bankers Life and Casualty Company. Based on your particular circumstances, you should seek advice from an independent tax adviser. You cannot rely upon or use the information above for the purposes of avoiding any tax or tax penalty that may be imposed by the Internal Revenue Service.

Tax Premiums Federal law places limits on how quickly premiums may be paid into a life insurance contract and how much money may be accumulated inside a life insurance contract based on the contract’s death benefit, in order to permit the policy to qualify for favorable tax treatment as life insurance under current law. Future policy changes such as face amount adjustments, rider/option additions and deletions, and Partial Withdrawals may require that applicable limits be adjusted to assure continued compliance.

Guideline Level Premium: $48,858.04Guideline Single Premium: $203,657.73MEC Premium (7-Pay Test): $55,731.08

THIS ILLUSTRATION HAS BEEN CHECKED AGAINST THE GUIDELINE PREMIUM TEST.THIS ILLUSTRATION HAS BEEN CHECKED AGAINST THE 7-PAY TEST.

Policy Loans Loan Interest charged on this policy is 6.54% in arrears. The pro rata portion of the STAV and COAV backing the Policy Loan will earn their respective guaranteed interest rates. The guaranteed interest rate for the STAV and Credit Option 1 is 1.00%. The guaranteed index credit for Credit Option 2 is 1.00%. The guaranteed index credit for Credit Option 3 is 1.00%. A preferred loan option is available on this contract beginning in the eleventh policy year. The maximum amount which may be borrowed at a preferred loan rate of interest may not exceed 15% of the Cash Surrender Value at the end of the prior policy year less any existing preferred loan. If the maximum amount is not lent during a policy year, the balance may not be carried over to subsequent years. Preferred loans are charged interest equal to 1.00%.This illustration assumes future Policy Loans.It is assumed that policy loan interest is not paid by the policyholder out-of-pocket.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 16 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 6 - Additional Notes

Partial Withdrawals You may surrender part of this policy for cash by Notice to Us at any time after the first Policy Year. The minimum partial withdrawal that may be made is $500.00. The amount that may be withdrawn may not exceed the Cash Surrender Value. The deduction will be made on a pro-rata basis from the Short-Term Accumulation Value and the Credit Option Accumulation Values based on the proportion of each account to the Total Accumulation Value.

After the first Policy Year, you are eligible for a Free Partial Withdrawal. A Free Partial Withdrawal is a partial withdrawal made without incurring a surrender charge. The Free Partial Withdrawal amount each Policy Year is equal to 10% of the Total Accumulation Value as of the date of the partial withdrawal less any prior Free Partial Withdrawal taken during that Policy Year. If less than 10% is withdrawn during any Policy Year, the remaining amount does not roll over to future policy years. Surrender charges will not be reduced if a Free Partial Withdrawal is taken.

All charges due to partial withdrawals will be imposed against the Short-Term Accumulation Value and the Credit Option Accumulation Values based on the proportion of each account to the Total Accumulation Value.This illustration assumes future Partial Withdrawals.

Surrender Charges This policy has surrender charges during the first 15 policy years. The Surrender Charge amount is described in the insurance policy. Any subsequent increases made to the Specified Amount of this policy that have been approved will initiate a separate 15-year surrender charge period based on the attained age of the insured at the time of increase and the amount of increase in excess of the previous Specified Amount.

Requested Policy Changes

We will not automatically process a change in premium, death benefit, Death Benefit Option and/or rider/option termination before expiration. A written request must be submitted for consideration of the desired change.

Non-Level Premiums and/or Additional Deposits

This policy assumes a non-level premium payment pattern and/or additional deposits. Premiums may vary if selected by you or as a result of forced compliance with guideline premiums. The regular premium outlay and any additional deposits by policy year are summarized as follows:

Policy Year(s) Regular Annual Premium1 to 28 $9,000.00

29 $1,009,000.00 30 to 91 $.00

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 17 of 18

A Life Insurance lllustration #2065877638V2015.8.0

Section 6 - Additional Notes

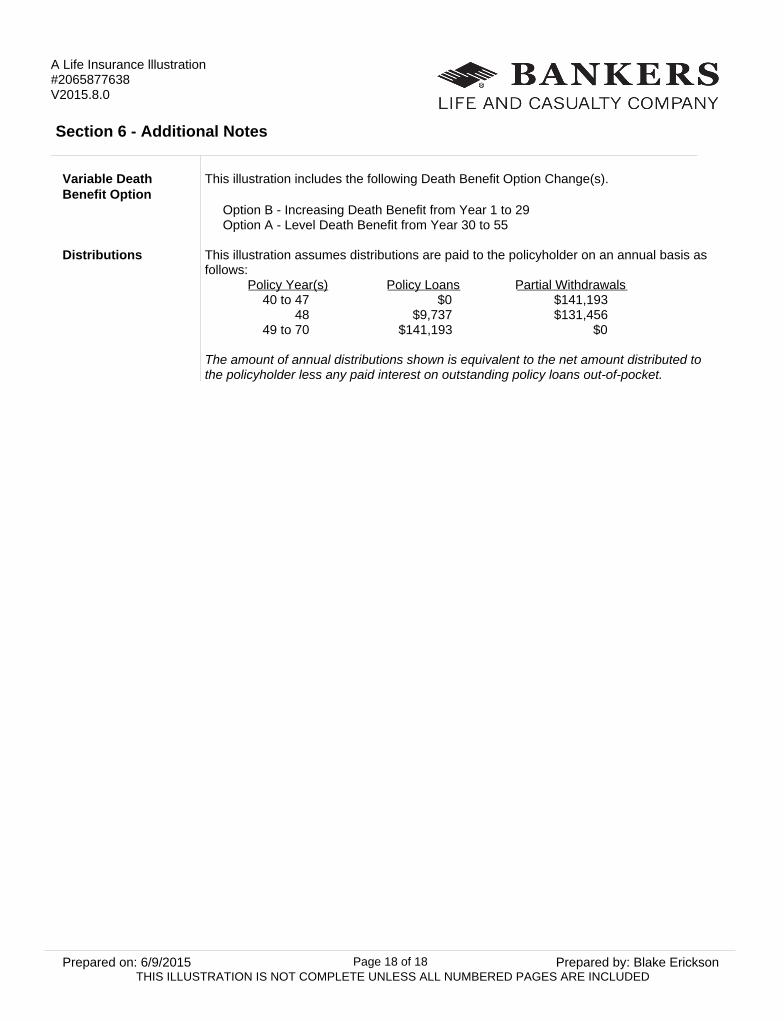

Variable Death Benefit Option

This illustration includes the following Death Benefit Option Change(s).

Option B - Increasing Death Benefit from Year 1 to 29 Option A - Level Death Benefit from Year 30 to 55

Distributions This illustration assumes distributions are paid to the policyholder on an annual basis as follows:

Policy Year(s) Policy Loans Partial Withdrawals40 to 47 $0 $141,193

48 $9,737 $131,456 49 to 70 $141,193 $0

The amount of annual distributions shown is equivalent to the net amount distributed to the policyholder less any paid interest on outstanding policy loans out-of-pocket.

Prepared on: 6/9/2015 Prepared by: Blake EricksonTHIS ILLUSTRATION IS NOT COMPLETE UNLESS ALL NUMBERED PAGES ARE INCLUDED

Page 18 of 18