ATM BANKING AND CUSTOMER...

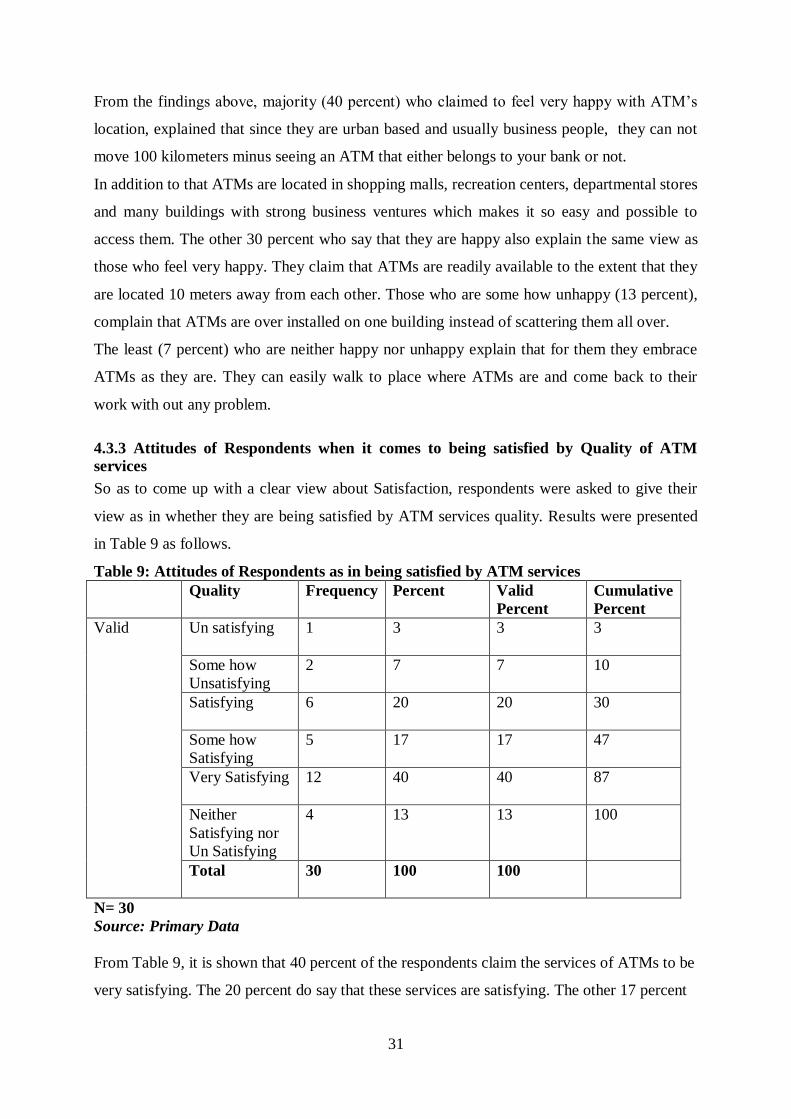

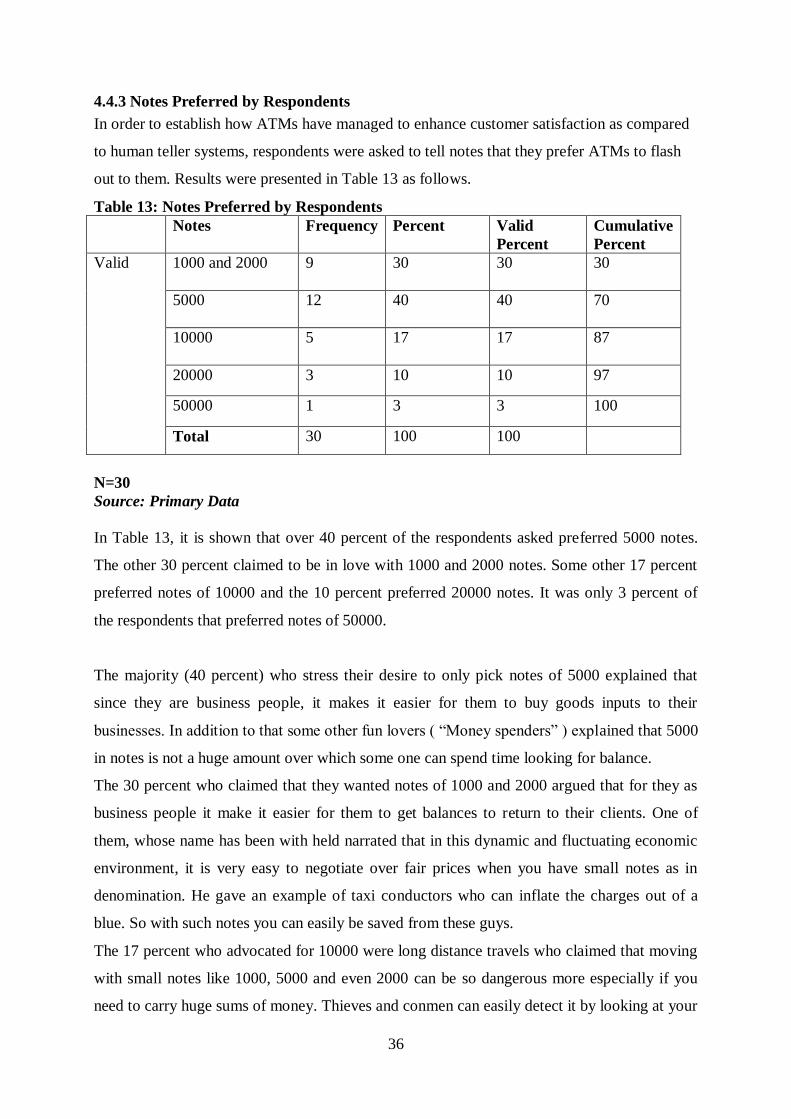

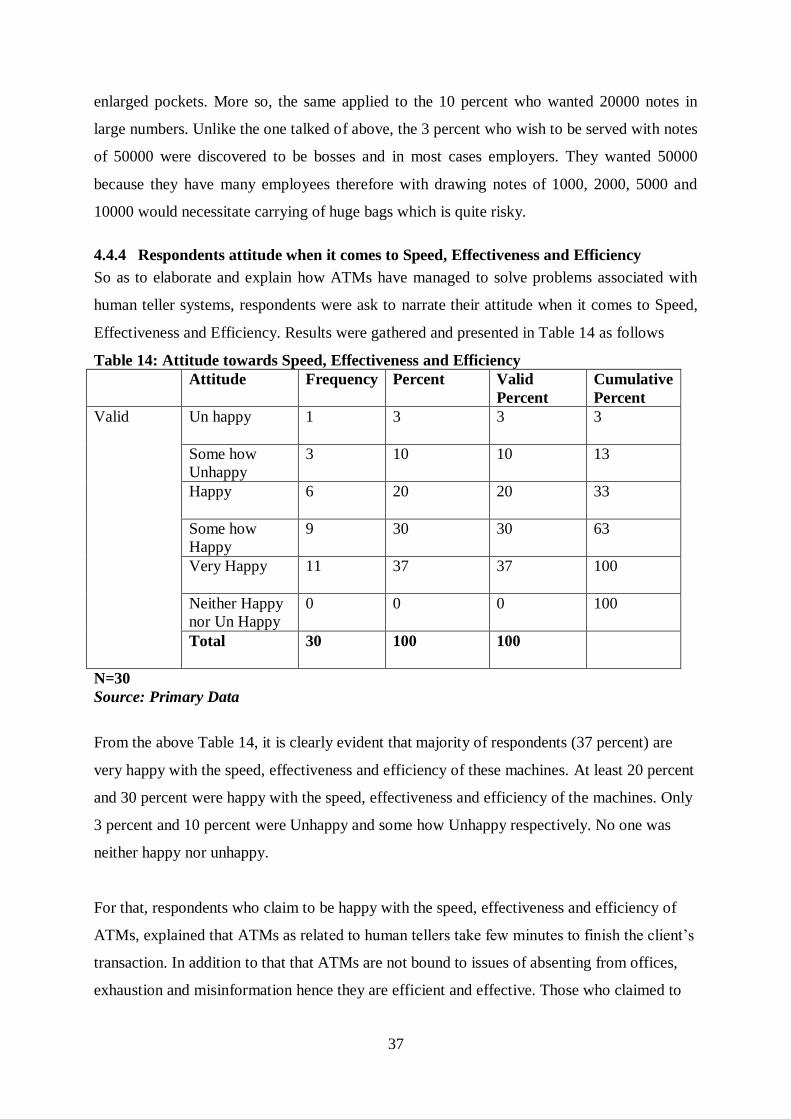

62

ATM BANKING AND CUSTOMER SATISFACTION A CASE OF STANBIC BANK’S ATM BY BAGERENGA JEREMIA. 07/U/7217/EXT 207015083 Contacts, Mobiles: 0755 748494/ 0702628185 Email: [email protected] SUPER VISOR Dr. MUYINDA PAUL BIREVU. A RESEARCH REPORT SUBMITTED TO DEPARTMENT OF LIFE LONG LEARNING AND DISTANCE EDUCATION IN PARTIAL FULFILLMENT OF THE REQUIREMENT OF THE AWARD OF THE BACHELOR OF COMMERCE DEGREE OF MAKARERE UNIVERSITY AUGUST 2011

Transcript of ATM BANKING AND CUSTOMER...

i

ATM BANKING AND CUSTOMER SATISFACTION

A CASE OF STANBIC BANK’S ATM

BY

BAGERENGA JEREMIA.

07/U/7217/EXT

207015083

Contacts, Mobiles: 0755 748494/ 0702628185

Email: [email protected]

SUPER VISOR

Dr. MUYINDA PAUL BIREVU.

A RESEARCH REPORT SUBMITTED TO DEPARTMENT OF LIFE LONG

LEARNING AND DISTANCE EDUCATION IN PARTIAL FULFILLMENT OF THE

REQUIREMENT OF THE AWARD OF THE BACHELOR OF COMMERCE

DEGREE OF

MAKARERE UNIVERSITY

AUGUST 2011

i

DECLARATION

I, BAGERENGA JEREMIA hereby declare that this report is my own original piece of work

and that it has not been presented and will not be presented to any other University/ institution

of higher learning for a similar or any other degree.

Signature…………………………………………..

BAGERENGA JEREMIA.

Date………………………………………………

ii

APPROVAL

I certify that Mr. ………………………………………. carried out this research under my

supervision and is submitted with my approval.

…………………………… ……………………………………..

Dr. Muyinda Paul Birevu Date

Supervisor

iii

DEDICATION

I dedicate this research report to my late parents who passionately loved me, guided me and

sacrificed all they had for my well being. Your love will always endure in me and may you

rest in eternal peace.

iv

ACKNOWLEDGEMENT

“And in this I give advise; it is to your own advantage not to only be doing what you began a

year ago; but now you also must complete the doing of it; that as there was readiness to desire

it, there may also be completion of what you have.” 2 CORINTHIANS 8: 10-11.

For this I thank the almighty God for his provision and blessings granted me. And also thank

him for enabling me to finish what I began four years ago.

Unforgettable and sincere gratitude proceeds to my supervisor Dr. Muyinda Paul Birevu for

his wonderful and professional guidance extended to me during the study.

Unimaginable thanks go to my uincle and sponsor Mr. Peter Kibazo plus the headmaster St

Gerald High School Mr. Kaggwa Gerald. You have been so reliable and providing to me

during this entire course may the almighty God repay you abundantly.

I also extend my appreciation to my family, brother, sister, my Jaajas and Uncles that you

have been there for me.

I can’t forget get my close friends, groupments and Coursements, Harriet, Ivan, Dorothy,

Diana, Florence, Allan, and Bridget. I appreciate you all may God avail you with every thing

that you desire in this world.

Sincere acknowledgement and gratitude go to all the staff and non staff clients of Stanbic

Bank ltd for being so helpful to me by sparing a little of their precious time to answer my

questionnaires and interviews.

My final appreciation goes to head of department and B COM Ext Coordinators Mr.

Nazarious, Mr. Kajumbura, Ms Jamia and the rest thank you all.

May the almighty God bless you all!!!

v

TABLE OF CONTENT

DECLARATION .....................................................................................................................i

APPROVAL .......................................................................................................................... ii

DEDICATION ..................................................................................................................... iii

ACKNOWLEDGEMENT ..................................................................................................... iv

TABLE OF CONTENT .......................................................................................................... v

LIST OF TABLES ............................................................................................................. viii

LIST OF FIGURES ............................................................................................................... ix

ABBREVIATIONS AND ACRONYMS ................................................................................ x

ABSTRACT .......................................................................................................................... xi

CHAPTER ONE ................................................................................................................... 1

1.0 INTRODUCTION .......................................................................................................... 1

1.1 Back ground. .................................................................................................................... 1

1.2 Statement of the problema................................................................................................. 3

1.3 Purpose of the study .......................................................................................................... 3

1.4 Objectives ......................................................................................................................... 4

1.5 Research Questions ........................................................................................................... 4

1.6 Scope of the study ............................................................................................................. 4

1.6.1 Geographical Scope ....................................................................................................... 4

1.6.2 Variable/ Content Scope ................................................................................................ 4

1.6.3 Time scope .................................................................................................................... 4

1.6 Significance of the study. .................................................................................................. 5

CHAPTER TWO .................................................................................................................. 6

2.0 LITERATURE REVIEW ............................................................................................... 6

2.1 Introduction. ..................................................................................................................... 6

2.2 ATM Banking. .................................................................................................................. 6

2.3 ATMs and how they work. ................................................................................................ 6

2.4 Origin and Development of ATMs. ................................................................................... 8

2.5) Contribution of ATMs ..................................................................................................... 9

2.5.1) Contributions to Banks ................................................................................................. 9

2.5.2) Contributions to Customers ........................................................................................ 10

2.5.3 Contribution to economic growth and development...................................................... 10

vi

2.6 ATM safety and Security ................................................................................................ 11

2.7 Stanbic’s auto bank and other services ............................................................................ 13

2.7.1 The Visa Debit Card .................................................................................................... 14

2.8 ATM Fees and charges. .................................................................................................. 14

2.9 Customer Satisfaction ..................................................................................................... 16

2.9.1 Measuring of Customer satisfaction ............................................................................. 17

2.9.2 Relation ship between ATM Banking and Customer Satisfaction ................................. 22

CHAPTER THREE ............................................................................................................ 23

3.0 METHODOLOGY ....................................................................................................... 23

3.1 Introduction .................................................................................................................... 23

3.2 Study Design .................................................................................................................. 23

3.3 Area of Study .................................................................................................................. 23

3.4 Population ...................................................................................................................... 23

3.5 Sample Size and Selection Method ................................................................................. 23

3.6 Data Collection Tools/ Methods ...................................................................................... 24

3.7 Data Management ........................................................................................................... 24

3.7.1Editing and Validation .................................................................................................. 24

3.7.2Analysis ........................................................................................................................ 24

3.8 Limitation of the Study ................................................................................................... 25

3.8.1 Slow/ non response. ..................................................................................................... 25

3.8.2 Finance ........................................................................................................................ 25

3.8.3 Time ............................................................................................................................ 25

CHAPTER FOUR .............................................................................................................. 26

4.0 PRESENTATION, INTERPRETATION AND DISCUSSION OF FINDINDS ........ 26

4.1 Introduction .................................................................................................................... 26

4.2 Findings on Personal Information ................................................................................... 26

4.2.1 Gender of Respondents ................................................................................................ 26

4.2.2 Age Distribution of Clients .......................................................................................... 27

4.2.3 Education Status of Client ............................................................................................ 28

4.3 Findings on the Indicators of Satisfaction. ....................................................................... 29

4.3.1 Frequency of Time Respondents Visit their ATMs in a Day ......................................... 29

4.3.2 Respondents feelings about the Location of ATMs ...................................................... 30

vii

4.3.3 Attitudes of Respondents when it comes to being satisfied by Quality of ATM services

............................................................................................................................................. 31

4.3.4 Inconveniencing Habits of ATMs ................................................................................ 32

4.4 Findings on how ATMs have managed to solve problems associated with Human Teller

Systems. ............................................................................................................................... 34

4.4.1 Reasons for Using ATMs ............................................................................................. 34

4.4.2 Services Provided by ATMs to Clients. ........................................................................ 35

4.4.3 Notes Preferred by Respondents ................................................................................... 36

4.4.4 Respondents attitude when it comes to Speed, Effectiveness and Efficiency............... 37

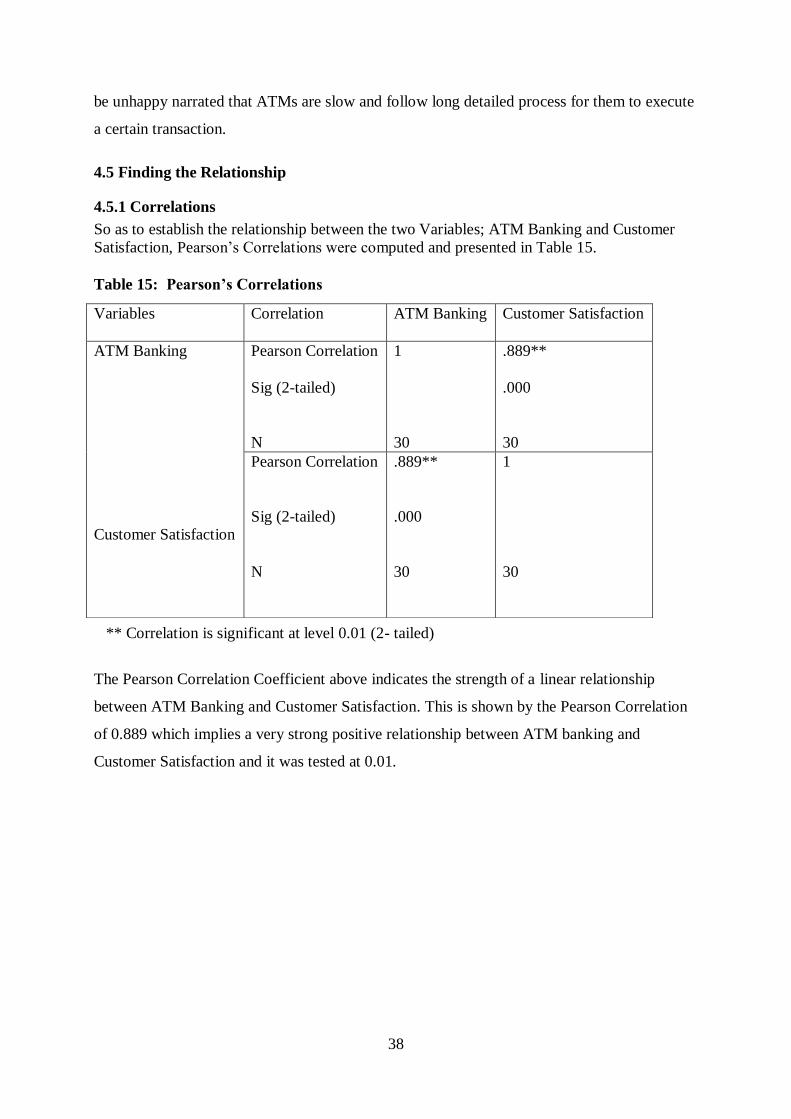

4.5 Finding the Relationship ................................................................................................. 38

4.5.1 Correlations ................................................................................................................. 38

CHAPTER FIVE ................................................................................................................ 39

5.0 SUMMARY, RECOMMENDATIONS AND CONCLUSIONS ................................. 39

5.1 Introduction .................................................................................................................... 39

5.2 Summary ........................................................................................................................ 39

5.3 Conclusion ...................................................................................................................... 39

5.4 Recommendations........................................................................................................... 40

5.5 Areas of Further Research ............................................................................................... 41

REFERENCE ..................................................................................................................... 42

APPENDIX I ....................................................................................................................... 44

The Questionnaire. ............................................................................................................. 44

APPENDIX II ..................................................................................................................... 48

Interview Guide. ................................................................................................................. 48

APPENDIX III .................................................................................................................... 49

Introductory Letter. ........................................................................................................... 49

viii

LIST OF TABLES

Table 1: Fees Charged on Deposits ....................................................................................... 15

Table 2: Fees Charged on Withdrawing ................................................................................ 16

Table 3: Liket Scale of Measuring Satisfaction. .................................................................... 18

Table 4: Gender of Respondents ........................................................................................... 26

Table 5: Age Distribution of Respondents............................................................................. 27

Table 6: Education Status of Clients ..................................................................................... 28

Table 7: Frequency of Time Respondents Visit their ATMs in a Day .................................... 29

Table 8: Feelings of Respondents when it comes to Location of ATMs................................. 30

Table 9: Attitudes of Respondents as in being satisfied by ATM services ............................. 31

Table 10: Habits of ATMs That Inconvenience Clients ......................................................... 32

Table 11: Reasons for Using ATMs ...................................................................................... 34

Table 12: Services Provided by ATMs to Clients .................................................................. 35

Table 13: Notes Preferred by Respondents ............................................................................ 36

Table 14: Attitude towards Speed, Effectiveness and Efficiency ........................................... 37

Table 15: Pearson’s Correlations ......................................................................................... 38

ix

LIST OF FIGURES

Figure 1: A graph showing needs that not fulfilled, well fulfilled, the satisfied and

dissatisfied. ........................................................................................................................... 21

x

ABBREVIATIONS AND ACRONYMS

1) ACSI- American Customer Satisfaction Index

2) NCR- National Cash Register Company

3) PIN - Personal Identification Number

2) SCI - Service & Computer Industries

3) ATM- Automated Teller Machine

4) CCTV - Closed- Circuit Television

4) ISP - Internet Service Provider

5) US - United States of America

6) UK - United Kingdom

7) i.e - That is to say

8) GB - Great Britain

9) Shs - Shillings

10) Ltd – Limited

xi

ABSTRACT

The researcher was interested in finding the indicators of satisfaction among the clients who

use ATMs, ways through which ATMs have managed to solved problems associated with in-

house banking or human teller systems of banking and the relationship between ATM banking

and customer satisfaction,

So as to come up with good findings, the researcher used a simple random sampling and

purposive sampling design to select respondents. The study covered 30 respondents who

composed of 25 non-staff customers and 5 staff members. Data was collected with the help of

questionnaires, interviews and sometimes observation. Mean while presentation was done

using tables, showing frequencies and percentages. All people living in and around

Nakulabye, business and non-business people plus some Bank staff members who possessed

technical information were taken to be the study population. The most common limitations

were basically Finance, Slow/ non response and Time.

From findings, it was revealed that many ATM card holders visit their ATMs so frequently

that they end up being unable to count the number of time and the location of ATMs was seen

to be very good since the majority of respondents admitted to be happy with it. More still,

majority of respondents admitted that the services of ATMs are indeed very satisfying and

these were the findings that indicated satisfaction. But majority of respondents pointed out

machine break down as the most inconveniencing habit of ATMs that needed continuous

attention.

Further more, it was seen that ATMs provided convenient and highly flexible services since it

was the reason that majority gave for using them. Majority of respondent admitted that they

use ATMs to withdraw and deposit and mostly preferred notes in 5000 denomination. More

so, many respondents claimed to be happy with the speed, effectiveness and efficiency of

these machines and these were the findings that helped to show how ATMs have managed to

solve problems associated with human teller systems.

Lastly, it was found out that there was a strong positive relationship between ATM banking

and customer satisfaction. This was got as r = 0.889.

xii

From the study, it was recommended that banks should educate ATM users on proper and

effective usage, install more ATMs, provide an emergency toll free 24hours number and

standby generators in periods of load shading. In addition to that, more security guards and

CCTV cameras should be put at ATMs and also guiding notes put inside the machines. The

dirty notes and those in bad condition should be sorted out by banks. Lastly security officers

put on ATMs should be trained to help stuck clients.

In the conclusion, it was established that ATMs have provided the best possible banking

services as compared to main banks or even branches as it comes to customer satisfaction.

This has been through providing convenient, flexible and effective less costly services which

are speedy and efficient. This is more evident from the significant relation ship that is there

between the two variables under study of r = 0.889

.

1

CHAPTER ONE

1.0 INTRODUCTION

Of recent due to economic liberalization and technological advancement, various changes

have been taking place in the financial services industry particularly the banking industry.

Eventually uncountable innovations and inventions have come up.

The year 1997 was a very significant one in the history of Uganda’s banking industry. Since

automation was introduced in this year. Standard Chartered Bank had the first machine

installed in Uganda. It was installed by NCR an American Information Giant company

represented in Uganda by SCI.

So at this point of view financial service provider particularly commercial banks had to come

up with the idea of Automated Teller Machine banking, as a tool to ensure that customers are

satisfied to maximum capacity.

1.1 Back ground.

According to wikimedia (2011), an Automated Teller Machine (ATM) is a computerized

telecommunications device that provides the clients of a financial institution like a bank with

access to their accounts in a public place without need of a human clerk. An ATM machine

can be also referred to as cash point or a hole in the wall machine. They are also known by

various names that is, one can refer to them as automatic banking machines or cash machines.

Very current and sophiscated ATMs operate by inserting a plastic ATM card with magnetic

stripe that contains a unique card numbers and some important information for security

purposes. These may be information like expiration date or card verification value (CVV) and

authentication is provided when the customer enters the personal identification number (PIN)

in the machine.

The idea of developing an ATM started way back in 1930s through independent, simultaneous

efforts and endeavors from scholars in Spain Sweden, the US and UK. So in 1939 Luther

George Simijan started on the work to invent the first ATM. It has been however testified that

many of his prototypes were not successful not until 1959 when his 132nd

patent (US

3079603) brought it into existence. In addition to that, there has also been proven comments

2

from experts that people like James Good fellow of Scotland, John D White of Docutel,

Donald Wetzel also of Docutel and John Shepherd- Barron have to be also talked about when

it comes to the invention of ATMs. (Wikimedia, 2011)

When these ATMS where introduced in Uganda’s banking sector a few years back many

users were very skeptical and frequently asked themselves how they could reconcile with

anonymous withdrawals and deposits, most especially the safety of their cash in case the

ATM cards happened to land in wrong hands and the proceeding satisfaction that could result

from using these machines.

Bloomskiny (2003), considered customer satisfaction as the degree to which customer

expectations of a product or service are met or exceeded. Individual customers have different

perceptions and reasons as to why they decide to purchase or get access to the service. So

customer satisfaction becomes the key performance indicator of the service which the firm is

providing to its clients or customers.

Shelagh (2005) observes that performance of banks and their embedded services like ATMs in

general can not easily be measured and justified. For example it can not be based no the

number of transactions carried out or even on the value of transactions carried out. This

definitely makes customer satisfaction ambiguous and abstract to study since the state of

satisfaction depend on other key issues like psychological perception and physical

consumption of the service (using ATMs as per this topic).

It therefore becomes important to note that liquidity is the main and important service that the

bank should offer to its clients or customers. This makes clients to demand 24- hour access to

cash and other financial services through out the year.

According to information got from Standard Bank of South Africa (2009), Stanbic bank is a

member of Standard Bank group which is a universal bank and full service financial group

offering transactional banking, saving, borrowing, investment, insurance, risk management,

wealth management and advisory services.

In Uganda, Stanbic Bank was founded as the National Bank of India in 1906. It went through

several name changes like Grindlays Bank before being bought by Standard Bank Group.

3

In October 1993 it re-established it’s self in Uganda. Stanbic Bank is licensed as a merchant

bank, Stock broker and financial adviser by the Uganda capital markets authority which

licensed the Uganda Securities Exchange (USE) in June 1997.

In February 2002 it bought 90% shares in Uganda Commercial Bank (UCB) which was a

largely government owned retail bank that operated country wide with over 67 branches

across the country.

Stanbic Bank Uganda limited is one of the 22 commercial banks in Uganda that are licensed

by Bank of Uganda. It is by far the largest commercial bank by assets. It has an estimated

asset valuation of US 991 million Dollars which is approximately 23% of the total assets in

Uganda as of June 2010. It maintains the largest branch network in the country which

accounts for about 16% of the bank branches in the country. It employs over 1339 individuals

(employees) as of 2008 and it’s one of the few Uganda commercial banks with internet

banking.

According to Mr. Philip Odera, the general manager of Stanbic Bank ltd, the bank operates

over 138 ATMs country wide through over 71 branches that are widely dispersed through out

the country. So question that now moves across the minds of clients and customers is not

availability of the facilities but the extent to which the facilities are able to satisfy their desires

and needs. Shelagh (2005) warned that banks should not be taken up by the presence of e-cash

(ATMs) to neglect the provision of their sore banking functions and roles necessary to satisfy

their customers at large.

1.2 Statement of the problem.

Despite of the extensive manpower, resources and efforts employed by banks in distributing

ATMs, it’s still very unclear as to whether clients have gained any satisfaction from the use of

these machines. Auto teller centers and premise are characterized by very long cues, machine

break down, confiscation of customer’s cards and a wide range of consistent problems.

1.3 Purpose of the study

The purpose of this study is to determine the extent to which ATM Banking facilities have

contributed to customer satisfaction in the banking business.

4

1.4 Objectives

i. To find out the indicators of satisfaction among the clients who use ATMs.

ii. To find out how ATMs have managed to solved problems associated with in-house banking

or human teller systems of banking.

iii. To find out the relationship between ATM banking and customer satisfaction in banks.

1.5 Research Questions

i. What are the indicators of satisfaction among the clients who use ATMs?

ii. How has ATMs manage to solve the problems associated with in-house banking or human

teller systems of banking?

iii. What is the relationship between ATM banking and customer satisfaction in banks?

1.6 Scope of the study

1.6.1 Geographical Scope

Geographically the study will take place at Stanbic’s Auto Bank in Nakulabye near Total

Petrol station along Kampala-Hoima road in Lubaga Division Kampala district of Uganda.

1.6.2 Variable/ Content Scope

The study is to consist of two variables; the independent variable and the dependent variable.

The independent variable is ATM banking well as the dependent variable is customer

satisfaction. Under the dependent variable (customer satisfaction), the research will basically

rotate around three (3) indicators of satisfaction and these are:

Number of transactions,

Value of transactions and

Frequency of usage.

1.6.3 Time scope

The study will cover a time scope of four years from 2007 to 2011.

5

1.6 Significance of the study.

i. The study will open direct and coordinated bank customers towards gaining the greatest

ever satisfaction from appropriately using the ATMs.

ii. The study will help Stanbic bank management by highlighting those critical areas that still

need more efforts so as to make the service better.

iii. This study will help academic researchers, the government and any one interested to

expand on it so as to make further research.

iv. The study is one of the pre-requisites that the researcher has to under go so as to attain the

bachelors of commerce degree in Makerere University.

6

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction.

It in is this chapter that already studied literature of global and national perception of the

subject under study is reviewed. It involves looking at studied literature, citations embodying

journals, reports, publications, text books and written speeches concerning ATM

banking/services and customer satisfaction. The role of ATMs, level of satisfaction and

relationship between ATM banking and Customer satisfaction were also looked at. All

literature looked at has to provide an important basis on which to relate on so as to make valid

and constructive sounding conclusion while conducting the study.

2.2 ATM Banking.

As per say, ATM banking can simply mean any efforts to carry out various services provided

by the bank using ATMs. Such services include transactions like making deposits, with

drawings, inquiries on balances in accounts, financial statements among others. From ancient

banking services and studies ATM banking accrued from a banking system known as Lobby

banking. The Dictionary of banking defines lobby banking as a system of banking that was

introduced in 1970s where by customers could deposit, with draw, request cheque books,

statements and balances while using ATMs

ATM banking is a bank service that is defined by its composure or functionality. A service as

defined by Simpson et al., (1989), should be an action of serving, helping or benefiting others.

ATMs like Auto banks have been spotted to offer a wide range of activities aimed at serving or

helping customers of clients.

According to Auerbach, ATM banking and its associated services, has been responsible for the

development of other banking systems like Branch banking. Since ATMs are usually located at

separate structures away from the main offices of the bank.

2.3 ATMs and how they work.

ATMs are known by various names to various scholars. The New Oxford Dictionary of

English relates to ATMs as Telecommunications Asynchronous Transfer Mode while other

scholars relate them to Automatic Banking Machines. (ABMs) and others as Cash Machines.

Bloomskiny (2003) proscribes ATMs as electric machines from which customers can with

7

draw paper money using an encoded plastic card. This definition has the most critical

illustration of ATMs since ATMs are known for paper money and not coins. More so for one

to access any service of an ATM, he/ she must have a plastic card which is usually referred to

as an ATM card. Further more, the Dictionary of Banking also pronounces them as machines

that permit the holder of the appropriate magnetic encoded card to obtain funds/cash at any

place of convenience any time of the day including nights.

According to Wikimedia (2011), someone can consider an ATM to be a hole in the wall

machine that is a computerized telecommunications device that permits and provides the

clients of the main bank with access to their cash or financial services in a public place with

out need of a cashier or human clerk or bank teller at any time or period of the day.

In summary therefore, all that is known about ATMs is reflected in the commonality of certain

elements in the definition of ATMs that is, "Machines that permits clients to make financial

transactions using a plastic card or ATM card so as to be assured of 24hours, 7days access to

cash." Hence customers are enabled to obtain online balance on accounts inquiries, cheque

books and Mini or full statements requests well as others can facilitate bill payments.

ATMs are activated by the customer who is identified by inserting/swiping a plastic ATM card

about 85mm by 45mm through them. ATM cards are demarcated with Magnetic stripe that

holds user's account details like account number, name of the client, bank sort codes among

others and a chip that contains a unique card number and some security information such as

the expiration date. Authentication or approval is provided when the customers entering a

personal identification number (PIN). (Wikimedia, 2011).

Discovery communications (2011), considers an ATM to be a computer and so it works like

one. It has a small display unit just like a monitor and a numerical key pad that is similar to key

board though it may not look exactly like it. It works on a program that is written or designed

by the bank and with this program one (the client) can freely do anything with it but the bank

usually follows its patterns and proceedings. In moist cases they start by asking customer of

his/ her convenient language. Inserting the card and respective passwords prompts the use of

the machine.

The ATM itself is a data terminal with six devices, two of which are input devices while other

8

four are out put devices. It therefore has to connect to a host processor which is an internet

service provider (ISP) so as to enable connection with other various ATMs.

2.4 Origin and Development of ATMs.

The idea to invent or come up with a cash dispensing machine developed in early 1930s and it

developed through independent and simultaneous efforts plus some other research from

specialists in Japan, United States, Sweden and United Kingdom. In the United State alone, the

credit was given to Luther George Simijan for having developed and built the first cash

dispensing machine. According to proven and sustainable evidence, Simijan must have started

working on the device before 1959 this is because his 132nd patent (US 3079603) was first

filled on 30th June 1960 and was granted on February 1963. (Wikimedia 2011)

Consequently, authors like Miller (2008) argue that Simijan built an ancient but not so

successful version of ATM in 1930s. More research showed that Simijan did not endeavor to

register the relevant patents of this machine but his basic idea was and remained to create a

hole in the wall machine that allowed customers to make financial transactions.

Simijan called the roll out of his machine Bankograph and an experimental one was first

installed in the New York City around the 1961 by City Bank of New York. The machine was

eventually removed in only 6 months since it lacked acceptance. This Bankograph was an

automated deposit machine accepting coins cash and cheques but it did not bear any cash

dispensing features. The first cash dispensing device was sighted in Tokyo Japan in 1966 but

very little was and is still known about this device. Scholars believed that this machine might

have been activated by a credit card rather than accessing current account balances.

Still in United States, another specialist Donald Wetzel who was the head of department at an

automated baggage handling company pioneered the first networked ATM in the US (Dallas-

Texas) on 2nd

September 1969. According to substantial information gathered his first ATM

was installed by chemical Bank in Rockville center New York. It was given name Docuteller.

Since it was designed by Donald Wetzel and his company Docutel.

According to information delivered by Miller (2008), Donald in an interview admitted that it

took him over five million to build his ATM- Docuteller and he worked with specialists like

Tom Baines (a medical engineer) and George Chastain (an electrical engineer).

9

Having heard this, very simultaneous and independent efforts by engineers in Sweden and

Great Britain/ UK sparked the development of self instigated cash machines in the early 1960s.

The first by their efforts was put in use by the Barclays Bank in Enfield Town in the north of

London on 27th June 1967. John Shepherd-Barron who was the managing director of Dela Rue

instruments is basically credited for the invention of this machine

With a vision to get the machine widely published or presented in the face of the public John

Shepherd-Barron used a comedy actor Reg Varney who used the machine first in UK’s history.

The design of this machine was based on special cheques that matched with personal

identification number since the idea of plastic cards had not been invented as yet. The idea of

PIN stored on the card was developed by a British engineer who was working with west

Minster Bank's smith industries (Smith's industries). He was known as James Good Fellow and

he invented or concluded it in 1965. He was eventually awarded with patent GB 1197183 that

was filed on 2nd May 1966 by Anthony Davies. In record, this patent is taken to be the earliest

instance of a complete currency dispenser system. (Wikimedia, 2011).

To be more specific and particular, James worked as a development engineer with Smith's

industries Ltd, this enable him to be awarded a project to develop an automatic cash dispenser

machine in 1965.He was to collaborate with partner companies like Chubb lock and safe

company who where to provide the secure physical housing and the mechanical dispenser

system jointly. James was eventually able to come up with a system that could accept a

machine readable encrypted card to which numerical key pad was added.

2.5) Contribution of ATMs

According to Shelagh (2005), from mid to late 1990s there has been a continued rapid growth

in the use of cards (ATM card) instead of cheques and other services. This definitely means

that the world has been steadily recognizing the benefits or contributions that ATMs are

providing to the economy, customers and the banks that operate them.

2.5.1) Contributions to Banks

According to Scridon et al. (2010), ATMs have become the most common instrument through

which banks can offer the possibility of conducting routine operations like cash with drawals

and deposits, bill payments, transfers between accounts among others.

More sill ATMs have been seen to help banks to save enormous amounts of money since they

10

work minus employees and their maintenance costs are significantly less. Now that customers

have become accustomed to them, bank has encouraged their use and both customers and

banks are bound to gain greatly.

According to Ruhangayebera (2011), banks have been spotted considering ATM banking as a

core element of their service delivery. This is because embarking on ATMs to deriver these

services is basic assurance of customer satisfaction combined with efficient competitiveness

and hence proper competition.

2.5.2) Contributions to Customers

Since Whiting (1985) brought out the fact that ATMs are mostly installed at post offices,

super markets, shops, busy streets, recreation centers and other places frequently accessed by

customers, ATMs have eased and facilitated cash services to clients there by providing

convenience and assurance of access to cash for over 24 hours a day.

Further more, when it comes to safer depositing and withdrawing by customers, ATMs are

credited. More still customers can easily perform bill payment (water and electricity

specifically) while accessing account information and request for cheque books, full and mini

statements hence keeping them aware of their financial positions

According to Stanbic Bank ltd (2009), Auto banks (ATMs) have enable customers to put the

management of financial affairs on finger tips. This has enable them to enjoy a wide range of

flexibility to do banking minus going to branches or offices and also link their various accounts

to one card which can easily be managed. That is, with one ATM card a customer can link his

primary account onto 3 other secondary accounts at any depot or service site. Such accounts

can be current, call or even savings account. So he/she can quickly and easily check for the

details of his/her account with out need for visiting a branch or office as per say.

In summary, ATMs have been credited with the fact that they have helped customers to

eliminate unnecessary paper work that is involved with stream banking.

2.5.3 Contribution to economic growth and development

ATMs were introduced way back in 1997 but ever since then they have been denoted to confer

great contribution to the general economic growth and development at large.

11

According to Capro et al., (1998), ATMs have provided efficient, low cost, safe and widely

available means of making and receiving payments so they have helped to mobilize domestic

savings and contributions in a very safe and efficient manner.

Ruhangayebare (2011) observed that despite of the many problems and challenges ATMs have

faced, they have greatly improved banking services in Uganda. The card technology has

enabled the development of services in previously unreached areas there by stimulating local-

rural economies and encouraging investments and tourist spending.

According to a certain ATM user Uganda has got great potentials for growth while utilizing the

new banking system (ATM banking) with out having to significantly up grade the existing

infrastructure. ATMs are important channels for banking in an environment where the

communication infrastructure is insufficient.

Since international standards have also agreed to honor ATM cards transactions, they can be

based on for extensive growth in international transactions and trade in future.

The non traditional players like cellular operators and retailers are bound to benefit greatly

since ATM cards have allowed these operators to offer banking facilities in areas where the

facility may not have been previously possible.

In addition to that, the business sector has been greatly boosted by the transactions of ATMs.

That is, buyers can purchase using Visa debit cards, while the extravagant one can not be

stopped to spend due to exhaustion of cash at hand. They simply rash to near by ATMs

withdraw another dime and spend it all over. This is a very big boost to the business sector and

economic growth at large.

In a nut shell, a variety of studies have established that ATMs will provide Africa’s best

chance of catching up with the rest of the world.

2.6 ATM safety and Security

ATM safety and security looks at how the machines should be designed to make sure that

clients are not bound to loose their money from illegal practices such as fraud and thefty.

12

According to Shelagh (2005), customers are so concerned about the security and safety of the

system and such concerns can in one way or another slow down the desire for the service

hence banks should endeavor to make sure that ATMs are safe and secure.

In addition to that, ever since these machines were introduced in Uganda, users have been so

skeptical about their safety and security including their privacy. Hence they frequently asked

questions on how they could recover losses that are brought about by with drawings from

illegal and unauthorized personnel.

Consequently, for safety and security purposes, ATMs are placed in public and open places

like streets, near administration blocks, petrol stations and other locations with in which

specialist guards/ personnel are installed nearer to the premises of machine. Such persons are

charged with matters of helping, guarding and directing clients on proper user of the

machines. But in many cases these guys have been reported to be source of worries to

customer in that they cram the PIN and other information of customer and collaborate with

conmen and thugs to steal client’s money. Alternatively these security officers have a

tendency of asking unrelated questions to clients which inconveniences them.

So as to over look these threats, Judith Nabakooba a police spokes woman has always advised

Uganda’s commercial banks to install security cameras at their ATM country wide. She

continues to argue that if cameras are put in place, police can easily arrest thieves who steal

peoples’ ATM cards and use them illegally. She adds that police has recently arrested so

many people in connection with ATM-bank robbery.

In relation to the above, Stanbic Bank ltd (2011) has spotted some important ATM safety and

security tips that customers should look out for and these are as follows:

Customers should only use ATMs in well lit high traffic areas. In case lights are not working

properly, they should not use such machines instead they should report to the bank as soon as

possible so as to rectify the problem and ensure better service delivery. More so they should

stay alert look for suspicious individuals and in case they happen to feel any discomfort they

should trust their instincts and leave the place as soon as possible to avoid what may come up

next.

13

In addition to the above, clients should have their ATM cards ready in their hands before the

transaction. Opening of wallets or money purses can at times be time consuming and not only

that it can easily expose your valuables to potential thieves. Further more the client must

endeavor never to ever tell any one his/her PIN and still they should always remember to

cover the key pad when typing in the PIN. This helps to minimize fraud and risks of

cramming your PIN by the client behind you and even criminals.

Be worried of any body who offers to help you out even if you are experiencing a difficult in

one way or another. The best way to go through this is using the security personnel since the

bank can easily truck this fellow. Further more always remember to pick or get back your

ATM card and please try to observe the card you get back to ensure that it is yours.

Lastly don’t count or expose your money after your transaction. After receiving your money

and making sure it is of the right amount that you requested, pick your receipt and leave

immediately.

2.7 Stanbic’s auto bank and other services

Auto banks are ATMs that are owned and ran by Stanbic Bank Ltd. They offer a wide range

of activities or services just like any other ATM. They accept deposits, allow withdrawals,

mini and full statements, check account balances, and inter account money transfers among

others.

So as to enjoy any of the above services of Auto Banks, one has to first open an account with

Stanbic Bank Ltd. Stanbic Bank embraces three categories of accounts and these include

Savings account

Transac plus and

Pure save.

This therefore means that the requirement to have an Auto Bank service will depend on the

type of account that one decides to run with the bank. The client will be required to fill an Auto

Bank request form and after only two(2) days he/ she will be issued with an Auto bank card

and his password or PIN will be given to him and such number will be kept as secret as

possible by the systems of the bank.

Stanbic Bank endeavors to avail clients of the bank with high degree of flexibility and

14

convenient quality services by Auto banks thought the country. The bank has managed to

install over 138 ATMs across the country. Particularly there are 71 branches in Kampala alone

with over 56 Auto banks while the rest are evenly dispersed to the rest of the country in areas

of the north, West, East, South and the Central. (Stanbic bank ltd, 2009)

2.7.1 The Visa Debit Card

A visa debit card is a plastic card that is linked to your account and is used to do transactions

such as with drawing of cash from an ATM and paying for goods at merchant stores that have

a point of sale terminal. It offers convenience of managing and accessing one’s money and

paying for goods wherever one may be in Uganda or even across the world.

The Visa debit card is so safe and convenient because it relieves the client of carrying lots of

money with him/her when traveling which limits the threat of thieves. The card is readily

accepted by over a million ATMs else where in the world and any merchant store where the

visa sign is displayed.

For a Stanbic Bank client to apply for the card, he/she needs to own a transact plus account.

(Stanbic bank ltd, 2011).

2.8 ATM Fees and charges.

According to Wikimedia (2011), ATM fees are usage fees and are fees charged by banks and

inter bank networks on customers for using their ATMs. In some instances, the fees may end

up being born by non members of the bank who use its ATMs but there are other cases when

these fees apply to both none and members of the bank. There are basically two types of fees

that banks may charge for their ATMs and these are as follows:

Surcharges

Foreign fee.

A surcharge is a fee that is imposed by the ATM owner (the bank) to a client or customer who

uses the machine.

A foreign fee is charged by the card issuer to the customer for conducting transactions on

machines that are outside their network of machines.

On average, ATM transactions are charged cheaply going from shillings 200 to 300 per

15

transaction but this widely depends on the bank that is making the transaction. It normally

takes about 2 days for this transaction to reflect on the account of the client.

From evidence published by Bank of Uganda in the month of April 2011, the following

charges were charged by various commercial banks. These were the fees charge on deposits

Table 1: Fees Charged on Deposits

Bank Fees

DTB

Tropical Bank

Crane Bank

400

300 and 500

2000

For other banks, cash deposits were very free of charge.

The fee that was charged on withdrawing is as follows:

16

Table 2: Fees Charged on Withdrawing

Banks Fees

Barclays Bank

Fina Bank

Standard Chartered Bank

800

800

800

Cairo Bank

Topical Bank

250

300

UBA

Crane Bank

Bank of Baroda

Equity Bank

600

600

600

600

Stanbic Bank 700

DTB

Eco Bank

400

400

The rest 500

Barclays bank managed to charge Shs 5000 for the use of non-Barclays ATM while Stanbic

bank charged no fees at all.

Many clients in retaliation have risen up to oppose these fees since many of them claim that

these fees are costly and high compared to human teller system charges. But banks in defense

argue that they charge such fees to cover for the high costs associated with owning and

operating these machines.

2.9 Customer Satisfaction

Due to a phenomenon growth in the service providing industry, various scholars and

theoretical analysts have come up to define and link customer satisfaction to the customer

service that is being provided. A customer may be taken to be an individual, house hold or any

organization that purchases or goes for goods or services generated with in the economy by

another person or firm.

According to Whiting (1985), there are a variety of bank customers who may be targeted when

it comes to customer satisfaction and these may be:

Married women. When we analyze the ruling in a case of Savory and co Vs Lloyds Bank Ltd

17

(1932) the bank has to define the details of the women customers. (Pg 113).

Minors (under 18 years), Joint organizations, Individual customers, Clubs and societies,

Partnerships and companies.

Customer satisfaction is a frequently used term in marketing. Bloomskiny (2003)

looks at it as the degree to which customer expectation of a product/ service is met or

exceeded. It therefore important to understand that both corporate and individual client/

customers have different reasons and expectations for purchasing or going after the service or

product hence customer satisfaction efforts should target these reasons or expectations.

According to Wikimedia (2011), Customer satisfaction is a measure of how products and

services supplied by a firm meet or surpass customers’ expectations. It can basically be seen in

terms of number/ percentage of total customers whose reported experience with a firm’s

products or services’ ratings exceed or meet specified satisfaction goals. Hence it is a key

performance indicator with in the business and is often part of the balanced score card.

Customer satisfaction provides a leading indicator of the consumer’s purchase intensions and

loyalty hence data collected on customer satisfaction should provides the basis on which

market perceptions and overall industry perception can be illustrated.

Understanding or administering customer satisfaction can be done by the aid of customer

satisfaction survey and below is a reason for doing this.

It sends and reveals a message to employees so that they attend to customers and ensure that

customers gain a positive experience with the firm’s goods and services

Besides sales and increments in market shares customer satisfaction is and has become a very

crucial indicator of how likely the firm’s customer will make future purchases.

2.9.1 Measuring of Customer satisfaction

Shelagh (2005) observes that the performance and efforts of banks and ATMs towards

customer satisfaction can not easily be measured and justified. That is to say could it be

measured on number of transactions, value of transactions or frequency of usage?

18

In addition to that, it is also very important to understand that customer satisfaction is an

ambiguous and abstract concept and the true manifestation of the state of satisfaction will vary

from person to person product/service to product/ service. The state of satisfaction depends on

a number of both psychological and physical variables which correlate with satisfaction

behaviors such as return and recommended rate.

Measuring customer satisfaction provides an indication of how successful the organization is

when it comes to providing the product or service to the market at large. Customer satisfaction

can be measured at individual level but it’s always reported at an aggregate level and can be

measured along various dimensions.

According to Parasuraman et al. (1991), the usual measure of customer satisfaction involves a

survey with a set of statements using Liket technique or scale. A customer is asked to evaluate

each statement in terms of their perception and expectation of the organization being measured.

General satisfaction is measured on five point scale.

Table 3: Liket Scale of Measuring Satisfaction.

Very

dissatisfied

Some what

dissatisfied

Neither satisfied

Nor dissatisfied

Some what

satisfied

Very satisfied

1 2 3 4 5

The above table is a semantic differential scale and regardless of the scale, the objective of the

study remains to measure customer’s perceived satisfaction with their experience of a firm’s

offering. It’s therefore essential and important for a firm to measure customer’s perceived

satisfaction with their experience. Good reliability and low error variance makes good quality

services produce satisfaction levels.

A semantic differential scale is a type of scale designed to measure the connotative meaning of

objects, events and concepts. The connotations/connotative are used to deriver attitudes and

psychological beliefs. In real senses, attitude should be expressed towards a given object, event

or concept.

19

It was designed by Charles E. Osgood. A respondent may be asked to choose his/ her position

as it lies on a scale between two or more bipolar adjectives like good- Evil, Valuable- Worth

less, Adequate- inadequate,

According to Wirtz et al. (2003), there is compatible Sematic differential scale i.e. the six item

seven point semantic differential scale that is so consistently proved to perform best across

both products and service provision. It basically loaded basis of high customer satisfaction with

highest item reliable and lowest as per say for error variance.

In the six items, respondent’s evaluation of most recent experience with ATM’s services and

how it was come up with is based on the comparison between those independent variables.

Below is an outlay.

“Please me to displease me”, “Very satisfied with very dissatisfied with”, “contented with to

disgusted with”, “did a good job for me to did a poor job or me”, “wise choice to poor choice”

and “happy with to unhappy with”

Various methods can be used to measure customer satisfaction. These are as follows

The first one to discuss is the American customer satisfaction index. (ACSI). ACSI is an

economic indicator that measures the satisfaction of consumers across the US economy. It was

produced by the American customer satisfaction index, a private company based in Ann Arbor

Michigan. It’s also a scientific standard of customer satisfaction measure. It is usually reliable

in predicting Gross domestic product (GDP) and personnel consumption expenditure growth.

Next is the Kano model which is the theory of product development and customer satisfaction

that was developed in 1980s by Professor Noriaki Kano. Noriaki Kano was a professor in the

Tokyo University of Science, an educator, lecturer, writer and consultant in the field of quality

management. He developed a customer satisfaction model that simply rank scheme

distinguishes between essential and differential attributes related to concepts of service quality.

According to Noriaki et al. (1984) the model classifies customer preference in to five

categories and these are as follows;

Attractive

One dimension

Must be

20

Indifferent

Reverse

These categories have been translated in to English using different names (delighters/ exciters,

satisfiers/ dissatisfiers etc). But all refer to the original articles written by Kano.

For attractive quality, it very evident that customer satisfaction is fully achieved when these

attributes are met but failure to meet them does not cause dissatisfaction. They are not

normally expected and normally delight customers unknowingly.

For one dimension quality there is always satisfaction when fulfilled and dissatisfaction when

not fulfilled. These are known to customers and firms usually strive for them.

Under the must be quality, there is a tendency of taking them for granted when fulfilled but

result in dissatisfaction when not fulfilled.

For indifferent quality there is neither good nor bad attributes that do not either result into

customer satisfaction or dissatisfaction.

Reverse quality symbolizes attributes of a view that a high degree of achievement may result in

dissatisfaction since not all customers are alike. That is to say, there are some customers who

prefer high technology while others the basic model of products. These will be un satisfied

with many extra features on the product.

To strengthen their view they used a graph to illustrate the needs that are not fulfilled, those

that are well fulfilled, the satisfied and dissatisfied.

21

Figure 1: A graph showing needs that not fulfilled, well fulfilled, the satisfied and

dissatisfied.

From the figure above the following could be seen:

Performance attributes: are seen as skill, knowledge, ability, or behaviors characteristics that

are associated with Job Performance.

Threshold or Basic attributes: are the main attributes in the Kano model. They are basically

features that products must have in order to meet customer needs. In case they are over looked

the product is completely incomplete.

Excitement attributes: These are for the part unforeseen by the client but the may yield

paramount satisfaction. Having excitement can help the client since it spurs a customer’s

ability to imagine there by discovering his or her needs.

Another method to look at when measuring customer satisfaction is; SERVQUAL or RATER.

This is scientific quality frame work developed by Zeithaml, Parasuraman and Berry in mid

80s. It was initially to measure aspects of service quality like reliability, responsiveness,

competence,

Zeithamal et al. (1990), argues that this method was originally meant to measure the gap

between expectations and experience. But during the early 90s the authors modified the model

to come up with a more meaningful stuff: RATER which stands for;

Dissatisfied

Need not

fulfiled

Satisfied Exicitement

Performance

Need well fulfilled

Basic

22

Reliability

Assurance

Tangibles

Empathy and

Responsiveness

Nyeck at el. (2002) emphasizes that the SERVQUAL measuring tool is and was by far taken

and guaranteed to be the most complete and understandable attempt to conceptualize and

measure service quality as some researchers have been able to examine numerous service

providing industries including the Banking industry and financial services’ providing firms

using the tool.

There are others like Top-box approach and automotive industry rankings by JD Power

associates, Info Quest box by Business to business survey (B2B).

2.9.2 Relation ship between ATM Banking and Customer Satisfaction

It should be noted that technology has of recent improved and various people have managed to

appreciate this. Some time back in Uganda we had few people who owned foreign accounts

and knew about Credit/ debit cards. Today with the introduction of ATM cards in Uganda

people have relied on them to do more shopping, transacting business, effecting payments and

transfers from accounts to accounts.

Sultant Singh (2009) observes that the relationship between ATM banking and customer

satisfaction is one of the few factors on which we can measure the performance of the bank. So

as to ascertain the relationship between the two elements we need look at the effectiveness of

the service towards meeting customers’ expectations and the number of people who frequently

visit the machines in a single day. In addition to this we also need to look at Fees charged plus

customers’ responses about these fees charged.

More to the above, we need to look at various ATM services when considering those factors

that affect choice of ATM and how these inter plays with the satisfaction experience of cleints.

So as to emphasize this, effort should be put in reducing challenges and discomforting events

that happen to clients whenever they use these machines. The bank should make follow ups

with their clients to eliminate any dissatisfaction tendencies.

23

CHAPTER THREE

3.0 METHODOLOGY

3.1 Introduction

This chapter encompasses all the methods to be used in data collection, presentation and

analysis, the study design, study population, sample size and sampling procedure. More still it

looks at data sources, data processing and lastly the limitation or problem that were uncounted

during the study.

3.2 Study Design

The study was designed to be a cross section survey that was both descriptive and analytical

while catering for both qualitative and quantitative data. The major aim for this was to get the

exact facts on ATM banking and the role it plays when it comes to satisfaction of the

customers of the bank.

3.3 Area of Study

The study area was the users of Stanbic bank’s Auto bank from Nakulabye and those in

nearby areas including both staff and non staff clients.

3.4 Population

This included all business and non-business people plus all bank staff members most

especially those who use ATMs and have technical know how/ knowledge.

3.5 Sample Size and Selection Method

A sample was selected from a population using simple random sampling design for equal and

independent chances of selecting respondent. More still a purposive sampling design (a

statistical and probability sampling technique) was also used to select experienced and

knowledge full respondents. So as to avoid and minimize bias, all the individuals were taken

to have equal chances of being chosen to constitute the sample size.

The total sample size comprised of 30 holders of Auto Bank cards. More still it included 25

non-staff customers and 5 staff members who are ATM (Auto bank) users.

24

3.6 Data Collection Tools/ Methods

Primary data was obtained through self administered questionnaires, interviews and even

observation of critical cases (issues) so as to get raw data. Well as Secondary data was

obtained from both internal and external documents. Internal documents mainly comprised of

annual reports and all written plus published documents from the bank under study well as

external documents included journals, articles, written speeches and text books containing

relevant information.

The researcher basically used questionnaires that were self administered on respondents from

the sample. These were of both open end closed end questions and were pre-tested for

accuracy and completeness.

Observations and personal interview with respondents and experts from the bank was also

given consideration in order to further clarify on unclear issues and to increase the

respondents’ rate.

3.7 Data Management

After the collection of data, data was compiled, sorted, edited, classified and coded so as to

bring out interpretable and numerical patterns that could be easy to analyze. It was then

processed and analyzed manually.

The quantitative data was summarized and categorized well as the qualitative data was

extracted, presented and analyzed with the aid of tabulation. Pearson’s Correlation was used

to establish the relationship between the study variables.

3.7.1Editing and Validation

Editing was done at the end of each day on which research was conducted. This was basically

to ensure consistence and accuracy of information provided by respondents and removing of

errors.

3.7.2Analysis

Descriptive statistics like percentages and tables were used to analyze data but for detailed

analysis, Pearson’s Correlation had to be used to relate the two variables.

25

3.8 Limitation of the Study

3.8.1 Slow/ non response.

Respondents were not responding at the required rate or speed. However, this did not impair

the findings. The researcher persisted on following up the appointments and schedules as

agreed upon between the two parties.

3.8.2 Finance

The research proved to be so costly to finance by the researcher especially in this dynamic

economic environment where every thing is costly.

3.8.3 Time

For sure time a lot was not sufficient since during that time there was need to concentrate on

other course unit of the semester with exams also inclusive.

26

CHAPTER FOUR

4.0 PRESENTATION, INTERPRETATION AND DISCUSSION OF FINDINDS

4.1 Introduction

This chapter presents, discusses and interprets the findings to the research problem. The

findings were got from primary sources as shown below.

4.2 Findings on Personal Information

4.2.1 Gender of Respondents

In order to establish the prevalent gender or sex that commonly use ATMs, respondents were

requested to tell their gender/ sex. This could provide important grounds on to which the

relation ship between ATM banking and Customer satisfaction could be found out. Results

were obtained and presented in Table 4 as follows.

Table 4: Gender of Respondents

N= 30

Source: primary Data

From table 4, over 83 percent of the respondents were Males and only 17 percent of them

happened to be Females.

Majority (83 percent) proved to be Male because these constitute the majority of workers.

Very few ladies work. Many of them are house wives. Those few (17 percent), who go to

ATMs are the workers and they basically deposit and not withdraw. In addition to that many

ladies believe in being given and not them to give. So when ever a man takes them out it is

entirely upon him to spend and that is why very many men visit the ATMs as compared to

ladies.

Gender Frequency Percentage Valid

Percent

Cumulative

Percent

Valid Male 25 83 83 83

Female 5 17 17 100

Total 30 100 100

27

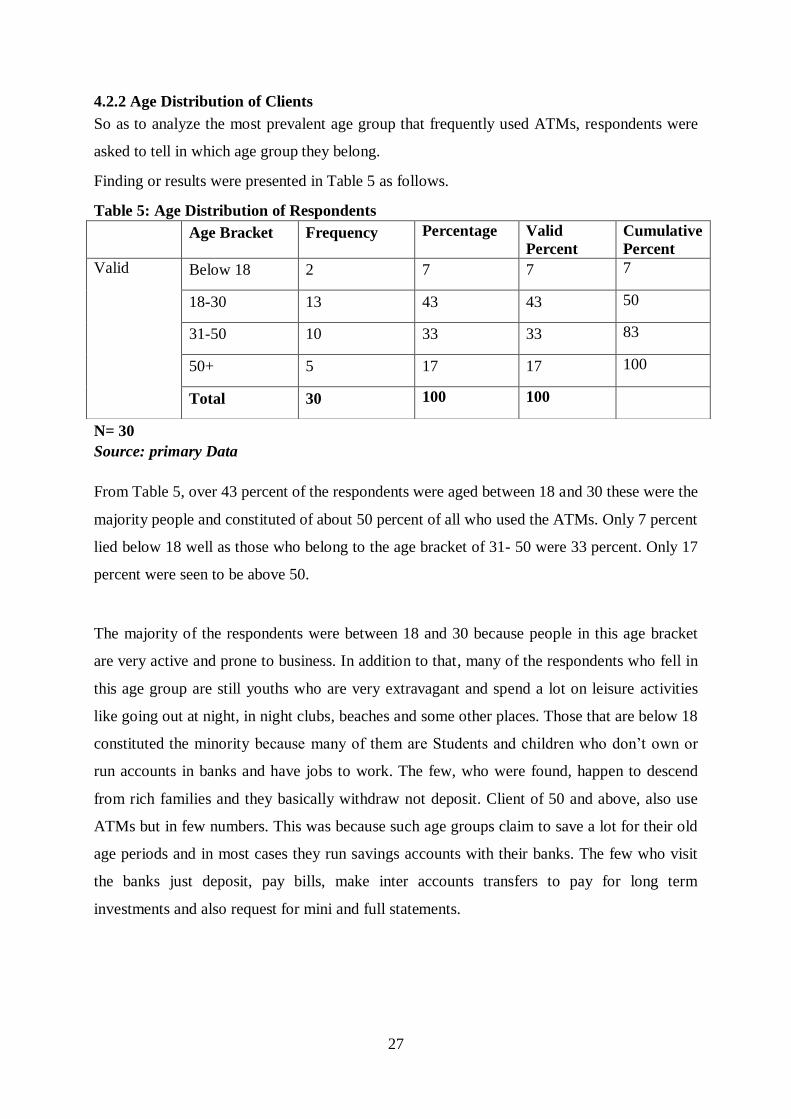

4.2.2 Age Distribution of Clients

So as to analyze the most prevalent age group that frequently used ATMs, respondents were

asked to tell in which age group they belong.

Finding or results were presented in Table 5 as follows.

Table 5: Age Distribution of Respondents

N= 30

Source: primary Data

From Table 5, over 43 percent of the respondents were aged between 18 and 30 these were the

majority people and constituted of about 50 percent of all who used the ATMs. Only 7 percent

lied below 18 well as those who belong to the age bracket of 31- 50 were 33 percent. Only 17

percent were seen to be above 50.

The majority of the respondents were between 18 and 30 because people in this age bracket

are very active and prone to business. In addition to that, many of the respondents who fell in

this age group are still youths who are very extravagant and spend a lot on leisure activities

like going out at night, in night clubs, beaches and some other places. Those that are below 18

constituted the minority because many of them are Students and children who don’t own or

run accounts in banks and have jobs to work. The few, who were found, happen to descend

from rich families and they basically withdraw not deposit. Client of 50 and above, also use

ATMs but in few numbers. This was because such age groups claim to save a lot for their old

age periods and in most cases they run savings accounts with their banks. The few who visit

the banks just deposit, pay bills, make inter accounts transfers to pay for long term

investments and also request for mini and full statements.

Age Bracket Frequency Percentage Valid

Percent

Cumulative

Percent

Valid Below 18 2 7 7 7

18-30 13 43 43 50

31-50 10 33 33 83

50+ 5 17 17 100

Total 30 100 100

28

4.2.3 Education Status of Client

So as to understand and establish the ease with in which clients find machines and also

perceive or understand them, the education status/ back ground of clients had to be asked.

This could help to later determine the relationship between ATM banking and Customer

satisfaction. Result were obtained and presented in Table 6 below.

Table 6: Education Status of Clients

N=30

Source: Primary Data

It is evident from Table 7 that over 53 Percent of the respondents had at least got some

education up to senior six. 20 percent had joined any tertiary institution well as 17 percent

managed to reach the University. Only 10 percent manage to at least have primary level

education. Well as Zero percent of the respondents were discovered to never have gone to

school.

Majority of respondents found out, proved to have studied the secondary level and because of

this fact, many of them could easily used ATM machines since they could read and interpret

the machine’s instructions during the transactions. In addition to that, such people don’t

neglect jobs and they constitute much of the private working sector. Many of those who pass

through tertiary institutions manage to create small scale jobs that need daily funds and

savings. This is the reason as to why they make 20 percent of respondent who use ATMs.

Graduates (with degrees from the University) also use ATMs but many of these prove to be

risk averse and good speculators who wish to carry their money with them. That is why they

constituted only 17 percent. Lastly many of those who fail to go to school hardly visit/use

ATMs because they find real hardship when it comes to reading instructions of the machine.

Education

Level

Frequency Percentage Valid

Percent

Cumulative

Percent

Valid Primary 3 10 10 10

Secondary 16 53 53 63

Tertiary 6 20 20 83

University 5 17 17 100

Never went to

School

0 0 0 100

Total 30 100 100

29

Mind you, since we are in a modern era where computers have taken a leading role in

executing various tasks these people surely face it hot. This hardens their life and hence

decides to keep their money on account where they visit human tellers/ clerks. From the above

analysis, it was so easy to note that many ATM users claim ATMs to be convenient because

they can read and write.

4.3 Findings on the Indicators of Satisfaction.

4.3.1 Frequency of Time Respondents Visit their ATMs in a Day

Clients were asked to tell the number or frequency of time they visit their ATMs in a day this

could be an indicator of satisfaction among them.1 In this case, results were presented in

Table 7 as follows.

Table 7: Frequency of Time Respondents Visit their ATMs in a Day

N= 30

Source: Primary Data

From Table 7, it was very evident that at least half of those who owned ATM cards used them

a number of times they could hardly count in a day. This brought the percentage of those who

could not count the number of time they go to the machine to about 50 percent per day.

27 percent of the respondents made sure that they visit the ATM twice a day while other 13

percent visited the ATM but once in a day. Only 10 Percent of respondents that had ATMs did

not endeavor to visit in a day.

Since majority of those that own ATM cards were business people who need constant cash

supply to finance their daily business operations, they frequently visited their ATMs for cash

with drawing. Due to this over 50 percent went/ used their ATMs uncountable times.

More so some other small scale business men only visited ATMs twice a day to deposit and

with draw depending on his income status. In most cases, in the morning they withdraw

money to purchase in puts to their business while in the evening they just deposit profits from

Number of

Times

Frequency Percentage Valid

Percent

Cumulative

Percent

Valid Once a day 4 13 13 13

Twice a day 8 27 27 40

Uncountable 15 50 50 90

None at all 3 10 10 100

Total 30 100 100

30

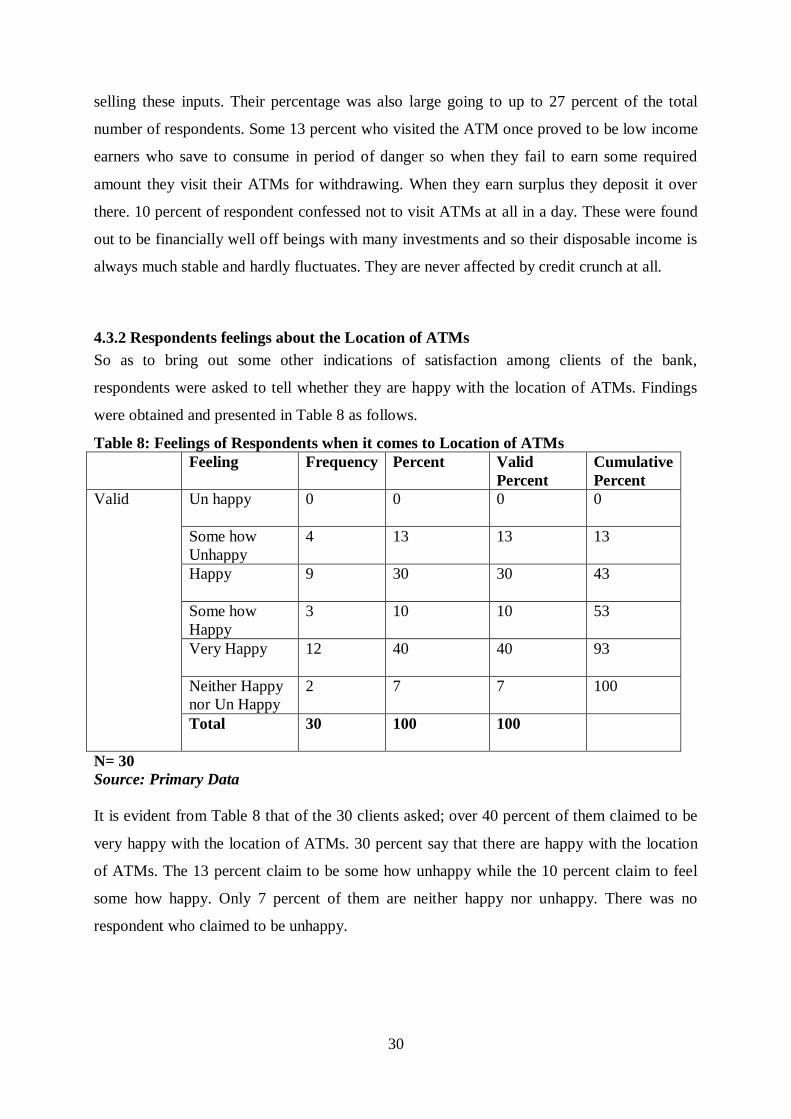

selling these inputs. Their percentage was also large going to up to 27 percent of the total

number of respondents. Some 13 percent who visited the ATM once proved to be low income

earners who save to consume in period of danger so when they fail to earn some required

amount they visit their ATMs for withdrawing. When they earn surplus they deposit it over

there. 10 percent of respondent confessed not to visit ATMs at all in a day. These were found

out to be financially well off beings with many investments and so their disposable income is

always much stable and hardly fluctuates. They are never affected by credit crunch at all.

4.3.2 Respondents feelings about the Location of ATMs

So as to bring out some other indications of satisfaction among clients of the bank,

respondents were asked to tell whether they are happy with the location of ATMs. Findings

were obtained and presented in Table 8 as follows.

Table 8: Feelings of Respondents when it comes to Location of ATMs