ata O CNESSCONSI - VINCI · Isle of Wight road network (4) 821 km of roads and 767 km of pavements...

11

Key data CONCESSIONS Revenue (1) (in €m) Net income attributable to owners of the parent (in €m) Ebitda (2) (in €m and as a percentage of revenue (1) ) Net financial debt (3) (in €m) Capital employed (3) (in €m) Operating income from ordinary activities (in €m and as a percentage of revenue (1) ) Revenue (1) by geographical area (as a percentage) (1) Excluding concession subsidiaries’ revenue derived from works carried out by non-Group companies. See glossary (page 368). (2) Cash flows from operations before tax and financing costs. See glossary (page 368). (3) At 31 December. France 80% Portugal 11% Americas 4% Rest of the world 5% 4,710 3,251 4,963 3,429 2017 2017 2017 2017 2017 2017 2018 2018 2018 2018 2018 2018 7,261 1,923 27,029 31,115 68.4% 47.2% 6,945 1,689 27,145 29,605 67.8% 46.8%

Transcript of ata O CNESSCONSI - VINCI · Isle of Wight road network (4) 821 km of roads and 767 km of pavements...

Key data

CONCESSIONS

Revenue (1)

(in €m)

Net income attributable to owners of the parent(in €m)

Ebitda (2)

(in €m and as a percentage of revenue (1) )

Net financial debt (3) (in €m)

Capital employed (3) (in €m)

Operating income from ordinary activities(in €m and as a percentage of revenue (1) )

Revenue (1) by geographical area(as a percentage)

(1) Excluding concession subsidiaries’ revenue derived from works carried out by non-Group companies. See glossary (page 368).(2) Cash flows from operations before tax and financing costs. See glossary (page 368).(3) At 31 December.

France 80% Portugal 11% Americas 4% Rest of the world 5%

4,710 3,2514,963 3,429

2017

2017 2017 2017

2017 20172018

2018 2018 2018

2018 2018

7,261

1,923 27,029 31,115

68.4% 47.2%6,945

1,689 27,145 29,605

67.8% 46.8%

P U B L I C - P R I V AT E P A R T N E R S H I P S O F V I N C I ’ S C O N C E S S I O N S B U S I N E S S W O R L D W I D E

Infrastructure Description Country Share capital held

End of contract

Motorway and road infrastructure Network under concessionArcos (A355 – western Strasbourg bypass) (1) 24 km France 100% 2070 Arcour (A19) 101 km France 100% 2070ASF network (excl. Puymorens Tunnel) 2,731 km France 100% 2036Cofiroute network (excl. A86 Duplex Tunnel) 1,100 km France 100% 2034Escota network 471 km France 99% 2032Fredericton–Moncton highway (2) 195 km Canada 25% 2028Regina Bypass (1) 61 km Canada 38% 2049Bogotá–Girardot motorway (1) 141 km (3) Colombia 50% 2042A4 motorway 45 km Germany 50% 2037A5 motorway 60 km Germany 54% 2039A7 motorway (1) 60 km Germany 50% 2047A9 motorway 47 km Germany 50% 2031Athens–Corinth–Patras motorway 201 km Greece 30% 2038Maliakos–Kleidi motorway 230 km Greece 15% 2038Highway 2000 East-West 50 km Jamaica 13% 2036Lima expressway 25 km Peru 100% 2049Moscow–St Petersburg motorway (MSP 0) 43 km (Moscow–Sheremetyevo) Russia 50% 2040Moscow–St Petersburg motorway (MSP 7 and 8) (1) 138 km (St Petersburg–Veliky Novgorod) Russia 40% 2041R1 (PR1BINA) expressway 51 km Slovakia 50% 2041Newport Southern Distributor Road 10 km United Kingdom 50% 2042Isle of Wight road network (4) 821 km of roads and 767 km of pavements United Kingdom 50% 2038Hounslow Borough road network (4) 432 km of roads and 762 km of pavements United Kingdom 50% 2037

Road bridges and tunnelsA86 Duplex Tunnel Rueil Malmaison–Jouy en Josas/Versailles (11 km) France 100% 2086Prado Carénage Tunnel Tunnel in Marseille (2.5 km) France 33% 2025Prado Sud Tunnel Tunnel in Marseille (1.5 km) France 59% 2055Puymorens Tunnel Tunnel in the Pyrenees (5.5 km) France 100% 2037Confederation Bridge Prince Edward Island–mainland Canada 20% 2032Charilaos Trikoupis Bridge Peloponnese–mainland Greece 57% 2039Tagus bridges Two bridges in Lisbon Portugal 41% 2030Ohio River Bridges – East End Crossing Bridges and a tunnel linking Kentucky to Indiana United States 33% 2051

AirportsChambéry, Clermont Ferrand, Grenoble, Poitiers-Biard, Pays d‘Ancenis (5) France 100% 2019 to 2029Lyon-Bron, Lyon-Saint Exupéry France 31% 2047Nantes Atlantique, Saint Nazaire Montoir France 85% 2065 (6)

Rennes, Dinard (5) France 49% 2024Toulon-Hyères France 100% 2040Salvador de Bahia Brazil 100% 2047Phnom Penh, Siem Reap, Sihanoukville Cambodia 70% 2040Santiago de Chile (1) Chile 40% 2035Liberia Costa Rica 45% 2030Santo Domingo (Las Américas and La Isabela), Puerto Plata, Samaná (Presidente Juan Bosch et Arroyo Barril), Barahona

Dominican Republic 100% 2030

Kansai, Itami, Kobe Japan 40% 2060Lisbon, Porto, Faro, Beja, Ponta Delgada, Horta, Flores,Santa Maria, Funchal, Porto Santo Portugal 100% 2063Belgrade (Nikola Tesla) Serbia 100% 2043Stockholm-Skavsta Sweden 90% Freehold propertyBelfast International United Kingdom 100% 2993Atlantic City, New Jersey (7) United States 2021Hollywood Burbank, California (7) United States 2022Macon Downtown, Georgia (7) United States 2022Middle Georgia Regional, Georgia (7) United States 2022Orlando Sanford, Florida United States 100% 2039

Rail infrastructureGSM-Rail Wireless communication system over 16,000 km of rail line France 30% 2025Rhônexpress Light rail system (23 km) in Lyon France 35% 2038SEA HSL High-speed rail line (302 km) between Tours and Bordeaux France 33% 2061

StadiumsBordeaux (Matmut Atlantique) 42,000 seats France 50% 2045Le Mans (MMArena) 25,000 seats France 100% 2043Nice (Allianz Riviera) 36,000 seats France 50% 2041Stade de France 80,000 seats France 67% 2025Queen Elizabeth Olympic Park stadium 57,000 seats United Kingdom 100% 2019 (8)

Other public amenitiesAutomation of river dams (Bameo) (1) 31 dams on the Aisne and Meuse rivers France 50% 2043Car Rental Center, Nice-Côte d’Azur Airport 60,000 sq. metre building France 100% 2040Martinique BRT system 2.5 km France 100% 2035Public lighting in Goussainville France 100% 2026Public lighting in Rouen (Lucitea) France 100% 2027

(1) Under construction.(2) Maintenance contract.(3) Including 65 km to be widened.(4) Upgrade, maintenance and upkeep contract.

(5) Service, management or public service contracts.(6) The concession grantor has expressed its intention to terminate the concession contract before expiry date.(7) Service contract.

The PPPs listed below are managed within the Concessions business of VINCI. Other PPPs (mainly buildings) are managed within VINCI’s Contracting business.

(8) On 21 January 2019, VINCI Stadium sold its shares in its operating subsidiary LS185 to E20, a subsidiary of the London Legacy Development Corporation and owner of the London stadium occupied by Premier League soccer club West Ham United (WHU).

Key data

VINCI AUTOROUTES

VINCI Autoroutes’ competitive position (4)

Motorway networks under concession in Europe (in km)

Source: internal studies, company literature.

Revenue (1) by network(in €m)

(1) Excluding concession subsidiaries’ revenue derived from works carried out by non-Group companies. See glossary (page 368).

(2) Cash flows from operations before tax and financing costs. See glossary (page 368).(3) At 31 December.(4) Controlled company networks.

Atlantia Eiffage Brisa

Revenue (1)

(in €m)

Ebitda (2)

(in €m and as a percentage of revenue (1) )

Operating income from ordinary activities(in €m and as a percentage of revenue (1) )

Net income attributable to owners of the parent(in €m)

Net financial debt (3) (in €m)

Capital employed (3) (in €m)

3,850 2,6853,895 2,686

2017

2017 2017 2017

2017 20172018

2018 2018 2018

2018 2018

5,356

1,468

6,711 2,476 1,628

20,345 21,132

72.7% 50.2%5,277

1,325 20,954 21,319

73.0% 50.9%

ASF 3,095 58% Cofiroute 1,441 27% Escota 750 14% Arcour 70 1%

and others

4,443

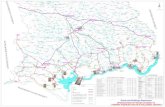

VINCI Autoroutes

Aix en Provence

Limoges

Besançon

Amiens

CaenChâlons en Champagne

Metz

Nancy

Reims

Bourges

Poitiers

Montargis

Sens

Rueil Malmaison

Versailles

Laval

Alençon

La Roche/Yon

Vannes

Brest

Quimper

Angers

Le Mans

Tours

Niort

Montpellier

Narbonne

Arles

PérigueuxBrive la Gaillarde

Bayonne

Pau

Perpignan

Nîmes

Toulon

Fréjus

Nice

Orange

Valence

Grenoble

Chambéry

Roanne

Saint Étienne

Gap

Montauban

La RochelleRochefort

Saintes

Blois

Orléans

Chartres

Cholet

Tarbes

Saint Gaudens

Albi

Cahors

Manosque

Digne les Bains

Agen

Clermont Ferrand

Nantes

Paris

Dijon

Strasbourg

Monaco

Lyon

Lille

Rouen

Rennes

Bordeaux

Toulouse

Cherbourg en Cotentin

Le Havre

Foix

Menton

Marseille

Annecy

Thonon les Bains

Colmar

MulhouseA11

A81

A28

A11

A71

A10A85A85

A28

A10 A19

A86

A11

A87

A83A10

A10

A837

A63A641

A64

A645

A64

A66

A9

A61

A680

A68

A20

A89

A62

A89A72

A46

A7

A709

A75

A9A54

A51

A52

A501

A50A520

A57

A500

A8

A355

A7

A89

2017

2017

2018

2018

3,845

1,441

3,815

1,400

(1) Excluding concession subsidiaries’ revenue derived from works carried out by non-Group companies. See glossary (page 368).

A S F G R O U P ( A S F A N D E S C O TA )(in €m and as a percentage of revenue (1))

Revenue (1) Ebitda (2) Net financial debt (3)

C O F I R O U T E(in €m and as a percentage of revenue (1))

Revenue (1) Ebitda (2) Net financial debt (3)

2,749

1,048

2,758

1,075

2017

2017

2017

2017

2018

2018

2018

2018

71.7%

74.6%

9,927

3,637

72.1%

74.9%

10,356

3,773

Motorway concessions of VINCI Autoroutes in France

ASF Cofiroute Escota Arcour Arcos A86 Duplex

Traffic 2018

(in millions of kilometres

travelled)

2018/2017change

ASF 31,822 –0.5%Escota 7,048 –3.2%Cofiroute 11,838 +1.0%Arcour 348 +5.9%Total 51,056 –0.5%

(2) Cash flows from operations before tax and financing costs. See glossary (page 368).(3) At 31 December.

Key data

VINCI AIRPORTS

Revenue (1) by business activity(as a percentage)

Revenue (1) by geographical area(as a percentage)

Revenue (1)

(in €m)

Ebitda (2)

(in €m and as a percentage of revenue (1) )

Operating income from ordinary activities(in €m and as a percentage of revenue (1) )

Net income attributable to owners of the parent(in €m)

Net financial debt (3) (in €m)

Capital employed (3) (in €m)

Aviation services 54% Non-aviation services 27% Security/assistance for PRM (4) 10% Ground handling 9%

Portugal 52% France 21% Cambodia 14% Dominican Republic 8% Other 5%

(1) Excluding concession subsidiaries’ revenue derived from works carried out by non-Group companies. See glossary (page 368).(2) Cash flows from operations before tax and financing costs. See glossary (page 368).

808 563

941 689

2017

2017

2017

2017 2017

20172018

2018

2018

2018 2018

2018

1,607

465

58.6%

4,951 6,994

42.9%1,409

345

57.3%

4,048 5,783

39.9%

(3) At 31 December.(4) Persons with reduced mobility.

VINCI Airports is the leading private operator and one of the top four

international players in the airport sector with 45 airports operated worldwide.

The main listed companies in the sector are Aena, Groupe ADP and Fraport.In Europe, VINCI Airports operates 10 airports in Portugal (55.3 million

passengers) and 12 airports in France (19.9 million passengers), including

Lyon-Saint Exupéry (11 million passengers). VINCI Airports has also been operating

Belfast International Airport in the United Kingdom (6.3 million passengers) and Stockholm Skavsta Airport in Sweden

(2.2 million passengers) since August 2018, and Nikola Tesla Airport in Belgrade, Serbia (5.6 million passengers)

A I R P O R T S A N D P A S S E N G E R T R A F F I C M A N A G E D45 airports and 195.2 million passengers managed in 2018 (1)

Source: internal studies, company literature.

1 airport in Chile

1 airport in Brazil

since December 2018. On 27 December 2018, VINCI Airports signed an agreement

to purchase a 50.01% stake from the current shareholders of London Gatwick,

a freehold property airport. The deal should be finalised during the first half of 2019.In Asia, VINCI Airports operates the three

airports in Cambodia (10.6 million passengers) and holds the concession, as part of a consortium with Japanese

partners, for the three airports in the Kansai region of Japan

(48.3 million passengers).In Latin America, VINCI Airports holds

concessions for Deputado Luís Eduardo Magalhães Airport in Salvador, Brazil (8 million passengers), Daniel Oduber Quirós International Airport in Liberia,

Costa Rica (1.1 million passengers) and six airports in the Dominican Republic (5 million passengers).

In Chile, VINCI Airports, in a consortium with Groupe ADP and Astaldi, operates Santiago Arturo Merino Benítez Airport

(23.3 million passengers).In the United States, VINCI Airports

has been operating five airports under concession or management contracts

since August 2018 (9.5 million passengers).

5 airports in the United States

10 airports in Portugal

12 airports in France

3 airports in Cambodia

3 airports in Japan

(1) Excluding ADP and London Gatwick. (2) Data in millions of passengers and 2018/2017 change.

i iC O M P E T I T I V E P O S I T I O N

1 airport in Costa Rica

6 airports in the Dominican Republic

1 airport in Sweden

1 airport in the United Kingdom

5.6 (2)

+5.4%

1 airport in Serbia

55.3 (2)

+6.8%19.9 (2)

+9.4%2.2 (2)

+3.9%

48.3 (2)

+3.7%

9.5 (2)

+8.7%

5.0 (2)

–2.0%

1.1 (2)

+3.4%23.3 (2)

+8.8%

8.0 (2)

+4.6%

6.3 (2)

+7.5%

10.6 (2)

+20.1%

Key data

CONTRACTING

Revenue(in €m)

Net income attributable to owners of the parent (in €m)

Ebitda (1)

(in €m and as a percentage of revenue )

Net financial debt (2) (in €m)

Capital employed (2) (in €m)

Operating income from ordinary activities(in €m and as a percentage of revenue)

Revenue by geographical area(as a percentage)

1,6291,260

1,815 1,472

2017

2017

2017

2017

2017 20172018

2018 2018 2018

2018 2018

35,769

849 (908) 6,233

5.1% 4.1%32,830

793

477

4,348

5.0% 3.8%

France 52% Germany 8% United Kingdom 6% Central and Eastern Europe 6% Rest of Europe 10% Americas 8% Africa 4% Rest of the world 6%

NB: data does not include VINCI Immobilier.(1) Cash flows from operations before tax and financing costs. See glossary (page 368).(2) At 31 December.

VINCI ENERGIESFRANCE

VINCI Energies is the leader in a fragmented market in which the top six players account for only around 50% of the market. Its main

competitors are Engie Energie Services, Spie, Eiffage Énergie, Bouygues Energies

& Services and Snef.

EUROPEVINCI Energies is a leading electrical

engineering and installation company. It ranks among the top players in Germany, where it has a strong position (revenue of

€2 billion in 2018), Switzerland, Scandinavia (Sweden, Finland and Norway), Belgium,

Netherlands, Portugal and Romania. In the information and communication

technologies sector, VINCI Energies operates mainly in France, Germany,

Netherlands, Portugal, Spain, Switzerland, Italy, Sweden, United Kingdom, Belgium

and Austria.

OUTSIDE EUROPEVINCI Energies operates in Africa, where it

is market leader in Morocco. It also operates in the Middle East, Asia and South America. VINCI Energies has a solid foothold

in New Zealand and Australia. With the acquisition of PrimeLine Utility Services, VINCI Energies established a significant

position in services for energy infrastructure and telecommunications operators

in North America at the beginning of 2018.

Source: company literature.

EUROVIAFRANCE

Eurovia is one of the leaders in the road and rail works market with Colas and

Eiffage Infrastructures. The market is otherwise shared by a large number of

local and regional contractors.Eurovia is market leader in aggregates,

where its competitors include roadworks companies and cement groups such as

LafargeHolcim, GSM (HeidelbergCement Group) and Cemex, along with several

hundred local producers.

GERMANYEurovia GmbH is one of the sector’s

main players with Strabag, in a market made up mainly of numerous regional

players. In addition, Eurovia’s rail works subsidiary ETF has expanded into

Germany by acquiring THG Baugesellschaft mbH.

UNITED KINGDOMEurovia UK, through its subsidiary

Ringway, is a major player in long-term road maintenance contracts. Its main

competitors are Amey (Ferrovial group), Kier and Balfour Beatty. Eurovia UK also operates in conventional roadworks in

competition with Balfour Beatty and Tarmac (CRH Group),

Aggregate Industries (LafargeHolcim), Hanson (Heidelberg) and Conway.

CZECH REPUBLICEurovia CS is among the leaders in road and rail works. Its main competitors are

Skanska, Metrostav and Strabag.

NORTH AMERICAIn Canada, Eurovia is one of the major players in road infrastructure works in Quebec, Alberta and British Columbia, mainly through subsidiaries Eurovia Québec Construction, Carmacks and BA Blacktop. Its main competitors are

subsidiaries of Colas, CRH and LafargeHolcim, as well as local

companies.In the United States, the acquisition of

Lane Construction’s Plants & Paving division complements the activities

Eurovia carries out through its subsidiaries Hubbard Construction and Blythe Construction in the south-east (Florida, Georgia, North Carolina and

South Carolina). This acquisition doubles Eurovia’s size and makes it one of the

market leaders in roadworks on the east coast of the United States. Its main

competitors are Archer Western Contractors (Walsh Group) for

construction works and Preferred Materials (CRH) for the manufacture and

application of asphalt concrete.

Source: company literature.

VINCI CONSTRUCTIONFRANCE

VINCI Construction is the leader in a market estimated to be worth revenue of around

€200 billion, ahead of Bouygues Construction, Eiffage Construction, Fayat, NGE and Spie Batignolles. The remaining

market is divided among several medium-sized regional companies (including

Demathieu Bard and Léon Grosse) and a large number of small contractors.

UNITED KINGDOMVINCI Construction UK is a company of significant size in the United Kingdom,

especially in the building and civil engineering sectors. Its main competitors are

Balfour Beatty, Kier, Laing O’Rourke and Interserve. The British market is estimated to

be worth revenue of around £150 billion.

CENTRAL EUROPEVINCI Construction operates in the region

through its medium-sized local subsidiaries, notably in Poland, the Czech Republic and Slovakia. Its main competitors are Strabag,

Skanska and Porr, as well as Budimex in Poland and Metrostav in the Czech Republic.

AFRICAOperating in 24 countries, Sogea-Satom is a major player in Central Africa, West Africa, Equatorial Africa and East Africa. Its main

competitors are European, Asian (particularly Chinese) and African companies.

OCEANIABy acquiring HEB Construction in 2015,

VINCI Construction became a major player in New Zealand’s infrastructure market. Since

the end of 2017, VINCI Construction has ramped up its presence in Australia with the

acquisition of Seymour Whyte.

SPECIALIST MARKETSSoletanche Freyssinet is world leader in

specialist civil engineering, active on a very fragmented market. Its competitors include

Trevi, Bauer and Keller in special foundations, and VSL (a Bouygues subsidiary) in

prestressing and stay cable systems. Entrepose is a global operator in the design

and construction of complex industrial projects in the oil, gas and energy recovery

sectors. Its main competitors include Saipem (ENI Group) and CB&I.

Source: Euroconstruct, November 2018 (market size);company literature.

i iC O M P E T I T I V E P O S I T I O N S

Key data

VINCI ENERGIES

Revenue by business activity(as a percentage)

Revenue by geographical area(as a percentage)

Revenue (in €m)

Ebitda (1)

(in €m and as a percentage of revenue)

Operating income from ordinary activities(in €m and as a percentage of revenue)

Net income attributable to owners of the parent(in €m)

Net financial debt (2) (in €m)

Capital employed (2) (in €m)

627 615

749 727

2017

2017

2017

20172017

20172018

2018

2018

20182018

2018

12,603

398

5.9%

3,9811,330

5.8%10,759

361

5.8%

3,083700

5.7%

(1) Cash flows from operations before tax and financing costs. See glossary (page 368).(2) At 31 December.

Industry 29% Infrastructure 27% Building solutions 26% Information and communication 18%

technologies

France 46% Germany 16% Scandinavia 6% Rest of Europe 20% Americas 5% Africa 3% Rest of the world 4%

Revenue by business activity(as a percentage)

Revenue by geographical area(as a percentage)

Revenue (in €m)

Ebitda (1)

(in €m and as a percentage of revenue)

Operating income from ordinary activities(in €m and as a percentage of revenue)

Net income attributable to owners of the parent(in €m)

Net financial debt (2) (in €m)

Capital employed (2) (in €m)

455 301

513 345

2017

2017

2017

2017

2017

20172018

2018

2018

2018 2018

2018

8,934

220

5.7%

(331) 1,676

3.9%8,112

216

5.6%

229

877

3.7%

(1) Cash flows from operations before tax and financing costs. See glossary (page 368).(2) At 31 December.

Works 69% Industry 14% Quarries 10% Services 7%

France 56% Germany 10% United Kingdom 6% Central and Eastern Europe 12% Rest of Europe 2% United States 5% Canada 6% Central and South America 3%

Key data

EUROVIA

Key data

VINCI CONSTRUCTION

Revenue by business activity(as a percentage)

Revenue by geographical area(as a percentage)

Revenue (in €m)

Ebitda (1)

(in €m and as a percentage of revenue)

Operating income from ordinary activities(in €m and as a percentage of revenue)

Net income attributable to owners of the parent(in €m)

Net financial surplus (2) (in €m)

Capital employed (2) (in €m)

547

344

553 400

2017

2017

2017

2017 2017

20172018

2018

2018

2018 2018

2018

14,231

231

3.9%

752 576

2.8%13,960

216

3.9%

948 387

2.5%

(1) Cash flows from operations before tax and financing costs. See glossary (page 368).(2) At 31 December.

Building 37% Specialist activities and complex projects 37% Civil and hydraulic engineering 26%

France 54% United Kingdom 10% Central and Eastern Europe 6% Rest of Europe 3% Americas 8% Africa 7% Oceania 7% Rest of the world 5%