ASX ANNOUNCEMENT Tuesday 12 November 2013 For personal … · 11/12/2013 · financial year. The...

58

ASX ANNOUNCEMENT Tuesday 12 November 2013 The Manager Company Announcements Office Australian Securities Exchange Level 45, South Tower Rialto 525 Collins Street MELBOURNE VIC 3000 ELECTRONIC LODGEMENT Dear Sir or Madam 2013 Annual General Meeting – Chairman, CEO and Remuneration Committee Chairman addresses In accordance with ASX Listing Rule 3.13.3, please find attached the addresses and accompanying slide presentation to be given by Asciano’s Chairman, Chief Executive Officer and Remuneration Committee Chairman at the Annual General Meeting to be held today at 10.00am. Yours faithfully Fiona Mead Company Secretary For personal use only

Transcript of ASX ANNOUNCEMENT Tuesday 12 November 2013 For personal … · 11/12/2013 · financial year. The...

ASX ANNOUNCEMENT

Tuesday 12 November 2013

The Manager Company Announcements Office Australian Securities Exchange Level 45, South Tower Rialto 525 Collins Street MELBOURNE VIC 3000 ELECTRONIC LODGEMENT

Dear Sir or Madam

2013 Annual General Meeting – Chairman, CEO and Remuneration Committee Chairman addresses

In accordance with ASX Listing Rule 3.13.3, please find attached the addresses and accompanying slide presentation to be given by Asciano’s Chairman, Chief Executive Officer and Remuneration Committee Chairman at the Annual General Meeting to be held today at 10.00am. Yours faithfully

Fiona Mead Company Secretary

For

per

sona

l use

onl

y

Annual General Meeting

12 November 2013

AGM Speeches

*Slide 1 – Asciano Limited – Annual General Meeting*

MALCOLM BROOMHEAD:

Good Morning Ladies and Gentlemen.

My name is Malcolm Broomhead, Chairman of Asciano Limited. On behalf of my fellow

Directors, I welcome you to our company’s 2013 Annual General Meeting. I also welcome

shareholders listening to our meeting today through our webcast facilities.

Before we start, can you please ensure your mobile phones are switched off or to silent.

*Slide 2 – Evacuation Instructions*

I also want to make sure you are familiar with the evacuation procedures we will follow in the

unlikely event of an emergency.

In the event of an emergency, you will hear an evacuation alarm. Please follow the

instructions of the wardens and assemble at the primary evacuation point for the Exhibition

Centre, which is shown in the colour red and labelled as area number one on the slide

behind me.

**Slide 3 – Asciano Limited – Annual General Meeting**

This is a properly constituted meeting and a quorum is present. I therefore declare the 2013

Annual General Meeting of Asciano Limited open.

Let me start by introducing my fellow Directors, our Chief Financial Officer and our Company

Secretary.

Seated on my immediate right, is Fiona Mead our Company Secretary. Next along is John

Mullen, our CEO and Managing Director. Next to John is Roger Burrows, our Chief

Financial Officer. Next to Roger are our Non-Executive Directors, Chris Barlow, Peter

George, Shirley In’t Veld, Geoff Kleemann, Bob Edgar and Ralph Waters.

Our Auditor, KPMG, is present today, represented by lead auditor, Mr Steven Gatt.

Also present today are a number of Asciano’s senior leadership team, who will be available

to answer any questions you may have following the close of the formal meeting. I

encourage all of you to take this opportunity to engage with our senior managers to learn

more about the performance of our business.

For

per

sona

l use

onl

y

**Slide 4 – Disclaimer**

The Notice of Meeting was distributed to shareholders on 10 October 2013 and with your

consent, I propose to take the notice as being read. I also draw your attention to the

disclaimer slide which you can now see in front of you.

**Slide 5 – Agenda**

I will start the meeting today with some brief comments on our performance in the 2013

financial year and then provide an overview of Asciano’s ongoing development around its

four core values of Safety, Customer, People and Teamwork, and Performance. I will also

make some comments on the area of sustainability where we have taken some steps this

year. I would then like to touch on the current business environment and the reforms we

believe need to be made to assist Australian business to continue to compete and grow in

the increasingly competitive global marketplace.

I will then ask our Managing Director and CEO, John Mullen, to run through some of the key

operational highlights from 2013 and provide an update on trading conditions for the first

quarter of the 2014 financial year. We will then provide the opportunity for those present to

ask questions on the presentations or any other topics of general interest in the Company’s

activities.

Following question time we will move into the formal business of the meeting. The Chairman

of the Remuneration Committee, Mr Chris Barlow, will address the meeting when we

consider the resolution relating to the Remuneration Report. I ask that any questions relating

to the Remuneration Report be held till this time.

The next items of business are to consider the re-election of directors after which we will

consider the item relating to the grant of rights to the Chief Executive Officer.

I note that voting on all resolutions will be conducted by a poll. I will then formally close the

meeting following which light refreshments will be served.

**Slide 6 – Chairman’s Address**

The 2013 financial year has been another successful one for Asciano. Our Managing

Director and CEO, John Mullen, has completed his second full year as CEO and under his

leadership, we have achieved another strong result and continued the successful execution

of our five year strategic business plan.

This is my fourth year at Asciano, and I am honoured to lead the Board of a company which

plays such an important role in Australia’s economy.

For

per

sona

l use

onl

y

**Slide 7 – Year in Review**

Throughout 2013, we have implemented a number of strategic business initiatives to

improve the company’s performance. We also continue to embed our core values of

Performance, Customer, Safety and People and Teamwork, and I would like now to provide

a brief summary of highlights from the last year in each of these areas.

Performance

In terms of financial performance, I am pleased to report that Asciano has continued to

deliver strong year-on-year revenue and earnings growth. Despite difficult macroeconomic

conditions, underlying net profit after tax and minority interests increased to $348.1 million,

an increase of 39%. John will go through the result in more detail however I am also pleased

to report that on the basis of the strength of the result we declared a fully franked final

dividend of 6.25 cents per share, a 56.3% increase over the same period in the previous

financial year. The final dividend takes the full year dividend paid to a fully franked 11.5

cents per share. The dividend policy introduced by the Board in 2011 has been reviewed

and out payout ratio band will be expanded from 20 to 30% to 20 to 40% of net profit before

material items, a decision reflecting the Board’s confidence in Asciano’s improving cash flow

profile.

Customer

In the customer space, we have continued to invest in major projects to boost customer

service, productivity and efficiency and place the business in a strong position to capitalise

on a recovery in markets.

The ongoing investment in the business is an example of continued private sector

investment in new infrastructure to continue to drive productivity improvements across our

industry. We remain committed to working with government on new projects and regulatory

reforms that will further enhance the efficiency of Australia’s transport and logistics network,

a subject I will touch on a little later.

Finally in the customer space, over the last year we have also significantly increased our

focus on developing a customer centric culture, acknowledging that first-class customer

service is vital to our ongoing success. We introduced our first ever Group-wide customer

survey to help us understand what we do well and where we need to focus more and we

have a plan in place in order to address some of those areas where we need to improve.

Safety

Improving safety performance has continued to be a focus for the Board and Senior

Leadership Team. As you know, our safety goal is to ensure all our employees return Home

Safely Every Day. Over the last year we have taken steps to strengthen our overarching

safety management framework, improve our safety management and reporting systems and

further enhance our safety culture.

While there is still work to do, it is pleasing that our safety performance is moving in the right

For

per

sona

l use

onl

y

direction. Across the Company in 2013, I’m pleased to say we achieved a 20.5%

improvement in our recordable injury frequency rate performance and a 32.3% improvement

in our lost time injury frequency rate performance.

A priority for the next year is the implementation of our Critical Safety Essentials program,

which is aimed at better isolation and management of our critical operational safety risks.

People & Teamwork

Finally, efforts to further develop our company culture, to improve our employee engagement

and to strengthen our leadership right across the business have remained an important

priority for John and his team.

Over the last year we have continued our efforts to build leadership capability and engage

our people through a shared vision and unified culture. Key initiatives have included the

rollout of Values Workshops across the business to heighten the awareness and

understanding of our business values and how our employees can live them every day,

along with the implementation of new development programs for our executive and emerging

leaders.

These initiatives are an important part of our ongoing development as a leading organisation

in the Australian transport and logistics industry. It is pleasing to see that our second

Company-wide employee engagement survey showed that engagement amongst our

employees continues to improve.

**Slide 8 – Sustainability**

We are also pleased that this year we have launched our inaugural Sustainability Report to

provide greater transparency on our economic, environment and social performance. Many

of these non-financial issues are becoming a greater priority and focus for our key

stakeholders, including our customers, employees and for many of you, our shareholders.

For this reason, the launch of the report is an important development for Asciano. The report

was launched last month as part of our online 2013 Annual Reporting suite and measures

our performance in managing our key sustainability issues during the 2013 financial year.

The report is also an important part in the development of our broader sustainability

program, which is being overseen by Shirley In’t Veld and the Board Sustainability

Committee. Over the last year we have been busy building the foundations of this program

and I am pleased that at this year’s AGM we will be providing more information to

shareholders on our approach in this area of our business.

Shirley and a number of our team will be at our sustainability booth down in the foyer after

today’s meeting to provide you more information on our sustainability approach and

performance. I encourage you to visit the booth and to access and provide feedback on our

2013 Sustainability Report.

**Slide 9 – Board Matters and Corporate Governance**

The role of the Board of Directors is to continue to generate shareholder value through

oversight of Asciano’s strategic plan and management, and by ensuring appropriate risk

controls are maintained. All members of the Board are unified in our goal of seeing the

For

per

sona

l use

onl

y

company continue to deliver strong performance.

For this reason, I am committed to ensuring we have a mix of Directors with the right skills

and experiences, and that we continue to have stability in leadership at a Board level. In this

respect, I advise that Mr Peter George, who resigns under Article 9.2(a) of our Constitution,

is standing today for re-election.

Peter has made a substantial contribution to Asciano, having served on the Board since the

Company was listed in 2007. Peter was Chair of Asciano’s Audit and Risk Management

between 2007 and 2012, overseeing a substantial improvement in the Company’s financial

processes and risk management systems during this time. He has remained a member of

this Committee, along with the Nomination and Succession Planning Committee, and our

Sustainability Committee.

Today we will ask you to continue our strong leadership at a Board level by re-electing Peter

George as a Non-Executive Director. You will hear more about Peter’s skills and experience

later in the meeting.

**Slide 10 – Business Environment

In closing, I would like to make some comments about the business environment in which

we operate and the microeconomic reforms that we believe can support further efficiency

and productivity improvements across our industry.

As you know, Asciano is an important driver of Australia’s economy. We handle and haul the

millions of tonnes of commodities, goods, products and other materials that keep Australian

businesses and households running. Asciano is also a barometer of the productivity of

Australia’s supply chain and the efficiency of Australia’s broader business operating

environment.

The Board and management team are committed to elevating the efficiency and productivity

of our operations and we continue to take steps to elevate our performance. For example, in

our container terminals division, service performance hit an all-time high in the last quarter,

with 97% on-time coastal window performance, while labour productivity has also improved.

Our $348 million investment in the Port Botany redevelopment project will further elevate the

productivity and efficiency of our terminal operations.

Yet we continue to be burdened by an over-regulated industrial relations environment. While

we are committed to working with all our employees to create harmonious, balanced and

productive workplaces, we believe some changes could be made to the current industrial

relations regulatory framework to promote productivity and improve Australia’s

competitiveness in the global economy. For this reason, we support the new Coalition

Government’s commitment to reviewing and improving the Fair Work Act through the

Australian Productivity Commission. However, it is important to move toward appropriate

change sooner rather than later.

The focus of reforms should be on providing employers with greater flexibility in agreement

making and the ability to work directly with their employees to agree and implement

For

per

sona

l use

onl

y

workplace agreements that meet both parties’ needs. More specifically, if we are to address

some of the current challenges, it is essential that all parties be held to common standards

and that appropriate recourse be available when these standards are not met.

In addition, the circumstances under which protected action can be taken also need to be

reviewed. Under the current laws, confirmed in recent case law, the concept of ‘genuinely

trying to reach an agreement’ is very loose and takes no account of whether claims are

unrealistic, aggressive or whether negotiations have gone as far as they can. This promotes

drawn out negotiations and sets up an adversarial environment between employee and

employer, which in turn has a negative impact on workplace productivity. Similarly,

bargaining content should be restricted to matters between the employee and employer, with

a focus on what our employees’ need, not on what interests their bargaining representative

may wish to pursue outside the employment relationship.

These changes are critical if the nation is to maintain our competitiveness and standard of

living.

Efforts to boost productivity and efficiency also continue to be a focus in our Pacific National

Rail division. The business has set a target of achieving 95% on-time arrivals for its freight

services, a target that represents a transformative change for an industry that has for too

long accepted service unreliability as the norm. It is pleasing to note that over the last 6

months, the business has achieved a significant improvement in on-time performance, for

example, achieving 88% of freight on time in our Intermodal business. However, there is

clearly still a long way to go to demonstrate that rail can be as efficient and reliable as other

forms of freight transport.

Yet, here too, the industry is burdened by over regulation and limited by an infrastructure

and competition policy framework that has failed to promote productivity in the freight

network. For example, efforts to move toward national regulation of the rail industry, such as

through the establishment of a National Rail Safety Regulator, have been slow to be

implemented, and have not been focussed where they would have the greatest benefit. A

freight train travelling from Brisbane to Perth still goes through six access providers, with six

different access agreements, operating under five economic regulatory regimes.

Similarly, while we know the benefits of moving freight via rail can only be achieved with

infrastructure that can accommodate heavier and longer trains, the length and stacking of

containers on trains continues to be limited by the need to travel through tunnels on the

metropolitan network and by the length of passing loops along key freight routes. Greater

investment in new rail infrastructure, such as through an inland rail network on the east coast

of Australia, would help unlock the productivity benefits of rail while leading to better social

outcomes, such as through reduced congestion, better road safety and improved

environmental outcomes.

As a major rail and truck operator, Asciano also believes that to drive freight efficiency the

government must press forward on the Heavy Vehicle Charging and Investment Reform

agenda. If the supply side and direct charging reform processes proceed together, then

these reforms will deliver economic efficiency and widen the funding base for additional

investment in new roads infrastructure.

For

per

sona

l use

onl

y

Finally, with regard to competition policy in the rail industry, governments around Australia

must continue to support increased competition between operators by maintaining the

benefits of ownership separation between below and above rail assets and, where this is not

the case, ensure strong and effective access regulation is in place. This is particularly

important in Queensland, where the consultation process has commenced on Aurizon’s new

below rail network access undertaking. It is important the regulator in Queensland continues

to remain vigilant in protecting the benefits that above rail competition has delivered and, for

this reason, Asciano and our coal customers strongly oppose the undertaking as it is

currently drafted.

**Slide 11 – Outlook**

John will go through the outlook and business prospects for Asciano over the next twelve

months, however I will conclude by saying that, as you know, Asciano’s performance

remains inextricably linked to the strength of the Australian economy and demand for

Australia’s mineral and agricultural commodities in overseas markets.

The diversity of our portfolio of businesses will continue to provide a buffer in what we

believe will be an uncertain economic environment and our business improvement and

efficiency initiatives will again to be a focus over the course of the next year. John and his

Senior Leadership Team will also continue to ensure customer service and safety remain

a priority.

In closing, on behalf of the Board of Directors, I would like to thank all our shareholders for

their ongoing support. I would also like to acknowledge and thank John and his Senior

Leadership Team, along with all Asciano’s employees, for their efforts in helping us achieve

another year of strong performance.

I will now hand over to our Managing Director and CEO, John Mullen.

JOHN MULLEN:

**Slide 12 – CEO Address

Thank you Malcolm and good morning everyone.

Firstly I would like to add my thanks to all of our employees who contributed to another good

year of growth in fiscal year 13 despite the tough economic head winds which had a major

impact on our Pacific National Rail and Terminals divisions in the second half of the year. I

would also like to thank our customers and other key stakeholders for working with us and

supporting us through what have been challenging times for everyone. Lastly, deep thanks

also to our shareholders for continuing to support us on the Asciano journey.

Today I would like to give you an overview of the fiscal year 13 operating highlights and the

progress we have made against the key five year targets we established in September 2011

to drive shareholder value. I will then give you an update on trading conditions for the first

For

per

sona

l use

onl

y

few months of FY14 across our divisions.

**Slide 13 – 2013 Highlights

Asciano again reported good growth in the fiscal 13 year despite very weak market

conditions in 2 of our major divisions. I believe that this result demonstrates:

The underlying strength of the company’s operating businesses

The relatively defensive nature of our businesses in tough times

Our cost reduction and business improvement focus and delivery

Our competitive position which enabled us to maintain our existing customers and win

new business, and finally

Despite the tough times two of our divisions are reporting good organic growth; our Coal

division which reported a 7.8% increase in volumes and our Bulk Ports & Autocare

businesses which reported significant growth in vehicle movements, storage days, and

volumes at some ports.

In light of the current environment, there has been, and continues to be, an increased focus

on our business improvement program and accelerating returns to shareholders from the

significant capital investment program we have made over the last few years:

For example we reduced capital expenditure by 30% or $200m compared to the previous

corresponding period

Free cashflow after capital expenditure was positive ($11m) before acquisitions and

dividend. This is 2 years earlier than committed to the market

In 2013 our BIP came in $45.7m well ahead of our budget of $25m. This means that we

have achieved cumulative benefits of $82m since FY12. As a result, we remain on track

to meet and probably exceed the $150m target we set in 2011

Terminals did a particularly good job in terms of reducing costs in the face of a difficult

environment. Operating costs declined 4.4% despite wages increases of 4.25% including

superannuation and a 7.6% increase in lease expenses

Our balance sheet metrics continue to improve

ROCE was up again to 11.0%. 3 divisions are now at or ahead of our Group WACC. The

Terminals division reported a ROCE of 7.2% however the return on the physical assets

in the business was 25.8%

Excluding legacy goodwill group ROCE now exceeds 18%

Despite the climate, the Company continued to invest in the business to maintain its

competitive position and to establish a platform for growth when the market improves. We

have not been sitting on our hands...

In Pacific National Coal we have developed two new facilities at; Greta in NSW and

Nebo in North Queensland both world class and innovative rail provisioning and

maintenance facilities

Port Botany container port redevelopment currently underway; State-of-the-art

technology and facilities

For

per

sona

l use

onl

y

In Pacific National Rail our Perth, Sydney, and Melbourne terminals have been upgraded

and we have commenced a significant locomotive repowering

Complete overhaul and modernisation of Asciano’s IT platforms

The Bulk and Automotive Port Services division has completed the C3 and Mountain

Industries acquisitions.

**Slide 14 –Status Against Five Year Objectives- growth

Asciano is now two and a half years into a 5 year strategic plan aimed at improving

shareholder returns following a difficult past through improvements across a broad range of

metrics including:

Financial Performance

Balance Sheet

Investor returns

Cultural and structural.

As I discussed last year we established multiple objectives for the five year plan and given

the difficulties in forecasting volume growth in the current environment we were never going

to hit every one every year however I am pleased to report that:

We are continuing to hit most metrics most years

Where one metric such as EBIT is below the 15% CAGR forecast, the corollary is that

we have made faster progress on free cashflow & ROCE

We are comfortable that our turnaround is on track and our overall objectives will be

achieved

A few examples of the business meeting its targets include:

Overall Group revenue growth is holding up quite well despite really challenging

economic conditions impacting two of our divisions, Pacific National Rail and Terminals

& Logistics

Our cost structure remains a focus given the current environment and we believe that it

is in good shape with our business improvement program on track and ahead of

expectations

EBIT growth in FY13 was 12% however given the current weak trading conditions we do

not believe we will meet this target in FY14. However over the five years we still believe

we will average growth rate of 10-15% which is a reasonable result in this environment.

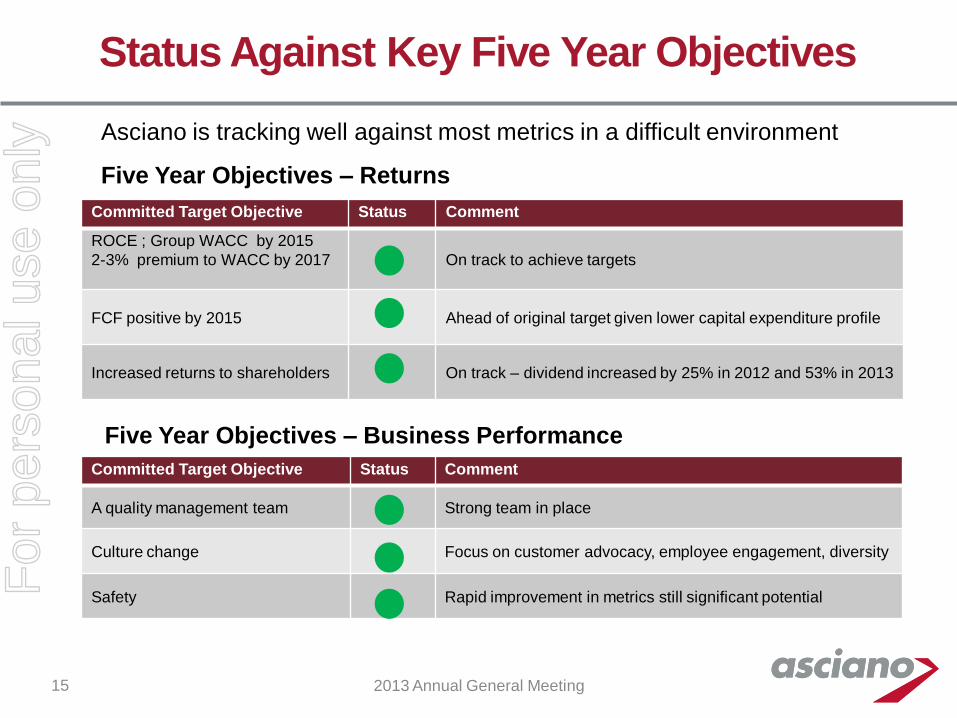

**Slide 15 –Status Against Five Year Objectives – returns and business performance

Whilst earnings growth is not quite as good as originally forecast due to the weaker than

anticipated trading environment there has been better than expected performance in other

areas:

Tough economic times have meant cutting costs and pruning back capital expenditure

This has resulted in the Company reaching a free cashflow positive position excluding

acquisitions 2 years ahead of plan

For

per

sona

l use

onl

y

As a result of the stronger cashflow dividends have been increased by 25% in 2012 and

53% in 2013.

We established a number of other objectives outside of financial objectives including:

Establishing a quality management team

Culture change which has included a number of major programmes around Customer,

Employee Engagement and Diversity; and

Safety which despite quantum levels of improvement over the last couple of years

remains a key focus across the Group and where we expect to make further significant

gains over the next few years.

**Slide 16 – Update – Pacific National Coal

Moving to the trading conditions in the first quarter of the 2014 fiscal year.

As you can see from this slide our Coal haulage division has had an excellent start to the

fiscal year reporting a 16.5% increase in tonnage hauled in the first quarter compared to the

same quarter last year, driven by organic growth in the NSW market and new contracts and

organic growth in the Queensland market.

Indications are that the current strong haulage volumes will continue into the end of this

calendar year.

As highlighted previously, changed planning and operational processes within PN Coal and

the broader Hunter Valley Coal Chain have yielded significant throughput benefits for the

division and more importantly our customers with very strong coal haulage volumes

delivered in the Hunter Valley in the first four months of the financial year (17% NTK

increase compared to pcp). This is further demonstrated by average cycle times for Pacific

National Coal in the central Hunter Valley and Gunnedah Basin being reduced by ~8% over

the last two months compared to the previous corresponding period as a result of the

changed processes, supported by recently completed port infrastructure expansions,

liberating the benefits of the Greta train support facility and consistent availability of coal for

haulage. This level of performance has significantly reduced the historical gap between

consolidated contracted volumes and delivered volumes, including performance in October

which set a new performance record and exceeded contracted volumes.

This month the division has commenced a new 8.5mtpa contract in Queensland with Rio

Tinto Australia from its Hail Creek and Kestral mines in Queensland.

The commencement date for the 4pmtpa haulage contract with Bandanna Energy for its

proposed Spring Creek mine in Queensland has been delayed until 1 January 2016.

**Slide 17 – Update –Pacific National Rail

Turning now to our intermodal and bulk rail haulage division Pacific National Rail.

For

per

sona

l use

onl

y

The weak trading conditions experienced in the second half of fiscal year 13 have continued

into the start of the 2014 fiscal year.

Intermodal volumes were down 2.6% in the first quarter compared to the previous

corresponding quarter driven by very weak volumes travelling east-west across the country.

Steel volumes and north-south volumes were stronger however this was not sufficient to

offset the negative leverage in the business caused by lower volumes on the dominant east-

west route.

Bulk volumes were down significantly on the same period last year however we expect to

make up most of this volume over the remainder of the year as good export grain harvests in

Victoria and Southern NSW are hauled and we commence additional services secured over

the last six months.

New contracts secured over the last few weeks in both Bulk and Intermodal make us more

confident that the Pacific National Rail FY14 full year EBIT result will now only be below last

year in the order of 5%, the bottom end of the range we released with our quarterly result

announcement to the market in October.

**Slide 18 – Update – Terminals and Logistics

Moving to our Terminals & Logistics division, container lifts were up 6.3% for the first quarter

compared to the previous corresponding period which reflected a swing back to Patrick in

market share with three month rolling market share moving back to approximately 49%.

Underlying container market growth for the period was in the order of 2% and has remained

volatile into the second quarter of the fiscal year.

Based on feedback from our key customers we continue to forecast 1-2% market growth in

container volumes for the FY14 year.

The benefits that flowed from the better than anticipated container volumes in the first

quarter were offset by weak rail volumes in the Logistics business which experienced similar

market conditions to Pacific National Rail’s intermodal business.

The division is currently focused on the redevelopment of our container terminal at Port

Botany in Sydney including the development of the land adjacent to the existing terminal

called the “knuckle” and the automation of the site. This project is on schedule and on

budget, and we continue to expect to go live with the automated site in the middle of 2014.

**Slide 19 – Bulk and Automotive Port Services

Finally moving to our fourth business division the Bulk and Automotive Port Services

division.

This division is expected to report further growth in earnings in FY14 although at a lower

growth rate than in FY13.

For

per

sona

l use

onl

y

The division has continued to benefit from the ongoing strong growth in imported car

volumes both in stevedoring and in the storage and handling areas of our business.

The division has also benefited from the contribution of 100% ownership of the C3 business

which is performing above the expectations we had at the time of the acquisition.

However, stevedoring activity levels over the quarter were impacted by lower volumes on the

Agility contract servicing the Gorgon project in Western Australia. Stevedoring activity levels

at other ports were mixed over the quarter.

The acquisition of Mountain Industries was completed at the end of October and will

contribute positively to earnings in FY14.

**Slide 20 – Medium Term Note Issue

Turning to the balance sheet, I am pleased to report that our finance team has continued to

manage our debt profile to ensure that we have access to diversified funding sources with

long term tenure to match the profile of the cashflows generated by the business.

On September 20 we settled an offering of 10 year medium term notes to the value of

GBP300m which has extended our weighted average debt maturity profile to 5.6 years1.

Naturally we had a call to make between cheaper, short term bank debt or more expensive

longer term debt that provides greater risk mitigation for the future. Whilst there was a

negative impact on our interest costs, we elected to take the safer routes of longer term debt

and remain conservative in our outlook. Our interest cover, however, remains very

respectable at over 5 times so we are confident that this was the right decision.

The proceeds from this raising will be used to reduce senior indebtedness outstanding under

Asciano’s shorter term banking facilities.

**Slide 21 – Outlook

Finally then, let me turn to the outlook for the business for the remainder of FY14.

We continue to believe that the Company is well positioned to report further growth in EBIT.

Pacific National Coal and our Bulk and Automotive Ports division are both expected to report

growth in revenue and EBIT for the full year driven by new contracts, the contribution from

recent acquisitions and underlying market growth.

Consistent with all our previous communication, however, we believe FY14 will be another

challenging year for both Pacific National Rail and our Terminals & Logistics division given

that domestic economic demand is expected to continue to be soft and consumption trends

volatile.

Overall, we continue to expect results in line with previous announcements to the market for

growth in both revenue and EBIT for the year, albeit at a slower rate of growth than we saw

in 2013.

1 As at 30 September 2013

For

per

sona

l use

onl

y

We continue to focus on the things that are within our control and in particular on costs and

our business improvement program, capital expenditure levels, asset efficiency, and

improving the returns on capital invested.

We will continue to focus on synergies and efficiencies across the business with a number of

new programs commenced over the last six months.

Despite the environment, we will continue to invest in our businesses to ensure that the

underlying assets are well maintained and are positioned to drive productivity and customer

service improvements and to ensure that the business is well positioned to capture both

organic and inorganic growth opportunities that we expect to emerge over the medium term.

Even with the restraints that we are imposing on ourselves in respect of capital expenditure,

by the time we finish the current capital expenditure programme we will have completely

renewed the physical assets of our business from the difficult days of under-investment in

the past, and will have assets, equipment, and premises of which our customers, our

employees, and our shareholders can be proud.

We remain comfortable with the current group structure however we will always look at

opportunities that could add value to the business and make economic sense; and as

demonstrated over the last twelve months we are prepared to make acquisitions where they

meet strict return hurdles and are accretive for shareholders.

Thank you again for your attendance today and your ongoing support as shareholders and I

will now hand you back to Malcolm for a question and answer session and the more formal

part of the meeting.

MALCOLM BROOMHEAD:

**Slide 22 – Questions**

Ladies and Gentlemen, before we move to the formal items of business to be considered at

today’s meeting, you will now have the opportunity to ask questions or make comments of a

general nature. I would ask that you hold any questions specifically related to the

Remuneration Report until we deal with that item when they will be addressed by Mr Barlow,

the Chairman of the Remuneration Committee.

I would like to ask shareholders present today to remember that this is a meeting for all

shareholders. If any shareholder has a question relating to their personal circumstances, this

can be raised with the Company and Computershare representatives present in the

registration area after the meeting.

For those present who are eligible to and who wish to ask a question, please move to one of

the microphones which are located in the room. I ask that you show your handset or your red

card to the microphone attendant and give them your name. If we can’t answer your

question in full today we will work to provide you with a response after the meeting. Please

limit yourself to one question at a time.

For

per

sona

l use

onl

y

<Questions from the audience>

Ladies and Gentlemen, I will now turn to the formal business of the meeting.

**Slide 23 – Formal Business of the Meeting**

There are 4 items of business before this meeting today.

In order to ensure that the views of all shareholders are taken into account I will declare a

poll on all items of business before the meeting where a vote is required. I will declare each

poll to be open individually following discussion of that item. Voting on the poll for each

motion will remain open until voting has been completed on that resolution. I will show a

slide for each resolution which shows the proxy position with respect to that resolution and I

will also declare the manner in which I intend to vote undirected proxies. I will then show the

interim result of the poll for that resolution once voting has been completed.

**Slide 24 – Computershare instruction**

When you registered for the meeting you would have been given a white plastic smartcard. If

you have not already done so, please insert your card into the slot at the top of the handset

with the barcode at the bottom and facing towards you.

When inserted correctly a welcome message will appear briefly on screen. Then you will be

returned to the holding screen where your name will now appear at the top of the display.

Once voting begins, your voting options will appear on the handset screen. To vote FOR the

resolution, press 1; to vote AGAINST, press 2 or if you wish to ABSTAIN from voting, press

3.

The word ‘received’ will appear briefly on screen confirming your vote has been cast.

You will then be returned to the voting options, the vote you selected will now be indicated

by a cross.

If you wish to change your mind simply select a new option by pressing 1,2 or 3. Your

original vote will be cancelled and your new selection will be counted.

Any appointed proxies should vote in the same method, that is to press 1,2 or 3. This will

cast any open votes you have available; instructions given to you by the shareholder will

automatically be cast as directed when the poll is closed.

Once a poll is closed the results will be displayed on screen showing the combination of

votes cast in the room and proxies received prior to the meeting. If any shareholder has a

query regarding the voting process or use of the handsets, please raise your hand and a

Computershare representative will come and assist you.

The results of the poll will be available immediately after voting on that resolution is

completed and will also be announced on the ASX and on the Company’s website following

the conclusion of the meeting.

For

per

sona

l use

onl

y

I appoint Scott Hudson of Computershare Investor Services as the Independent Returning

Officer.

The persons entitled to vote on this poll are all shareholders, representatives and attorneys

of shareholders, and proxyholders. All persons entitled to vote will be provided with a

handset.

Before we proceed with the formal business, as you would probably be aware, the laws that

apply to voting on resolutions relating to the remuneration of key management personnel

changed last year. In general, the Company’s key management personnel (which includes

the directors and those executives who are disclosed in the Remuneration Report) as well as

their closely related parties are prohibited from voting any undirected proxies on such

resolutions. There are also some specific rules regarding the Remuneration Report

resolution which I will mention when we get to that Item of Business.

If there is any person present who believes they are entitled to vote but have not registered

to vote, would you please raise your hand and a member of Computershare’s staff will assist

you.

If you require any assistance throughout the meeting, Asciano and Computershare staff are

here to assist you.

**Slide 25 - Formal Business**

I turn now to the first Item of Business on the agenda, the consideration of the Financial

Statements and Reports for the Company. The Corporations Act requires the Board to lay

the Financial Report, the Director’s Report and the Auditor’s Report for the last financial year

before the Annual General Meeting. The Corporations Act does not however require a vote

of shareholders on this resolution.

**Slide 26- Financial Statements**

I now turn to the floor and ask for any other questions from those present concerning the

Company reports.

[Questions from the floor on the Accounts]

If there are no further questions I declare that the reports have been received and

considered at the meeting.

In accordance with the Notice of Meeting I now move onto Item 2, adoption of the

Company’s Remuneration Report for the financial year ended 30 June 2013. I note that,

while the vote on this item is advisory only and does not bind the Company or its directors,

the Board and Remuneration Committee certainly takes into consideration the feedback we

receive from shareholders.

I would like to introduce Mr Chris Barlow, the Chairman of our Remuneration Committee.

For

per

sona

l use

onl

y

Chris will take a few minutes to provide you with a brief summary of the approach we have

taken to our Remuneration arrangements and Remuneration Report this year.

CHRIS BARLOW:

**Slide 27 – Chairman of Remuneration Committee Address**

Thank you Malcolm and good morning to you all.

In presenting the Asciano Remuneration Report, I would like again to reinforce how we link

our reward structure to key drivers of the business and then outline what has been achieved

by the management team in the last financial year.

As I said last year, our approach to remuneration is based on clearly linking management

reward with outcomes that matter to our shareholders.

This year, our management team has delivered a really strong performance in challenging

economic times and so as you would expect there are strong rewards for the achievement of

the goals set by the Board.

PAUSE

In the 2013 financial year, we carried out a clean sheet review of our remuneration

framework with Ernst & Young, and we considered various alternatives, but ultimately we

decided stability was best for our shareholders and management and so made no

substantial changes.

As a result we continue to use both short and long term incentive plans to reward

performance.

**Slide 28 – Short Term Incentive Plan**

Let me start with the Short Term plan.

We have maintained our balanced scorecard approach and continue to prioritise our targets

around financial performance, safety, customer and individual performance. We allocated

our targets like this.

Earnings before Interest and Tax was our measure of financial success and was weighted

at 50%. The very important safety improvements targets constituted 15%, while customer

service and individual performance goals accounted for 15% and 20% respectively of

potential STI.

There is a deferral component in this plan that requires 25% of the award to be allocated in

share rights. This helps to ensure our management team’s interests are well aligned to those

of our shareholders. In simple terms, if your shares do well so do theirs.

For

per

sona

l use

onl

y

**Slide 29 – Short Term Incentive Plan Results**

Now let’s look at what the Short Term Plan delivered. As you have heard; last year, despite

some challenging operating conditions, Asciano delivered excellent performance against our

set goals. You can see this reflected in the corresponding STI payments made to the

Company’s executive team.

In particular, we saw excellent performance from our Coal and Ports & General Stevedoring

divisions which have delivered particularly strong rewards for both David Irwin and Philip

Tonks. For David, this includes the additional retention incentive we put in place two years

ago, in part responding to investor feedback regarding the importance of maintaining him in

the role, heading our newest and rapidly expanding business.

We are pleased to see that he has achieved the targets set against this additional incentive.

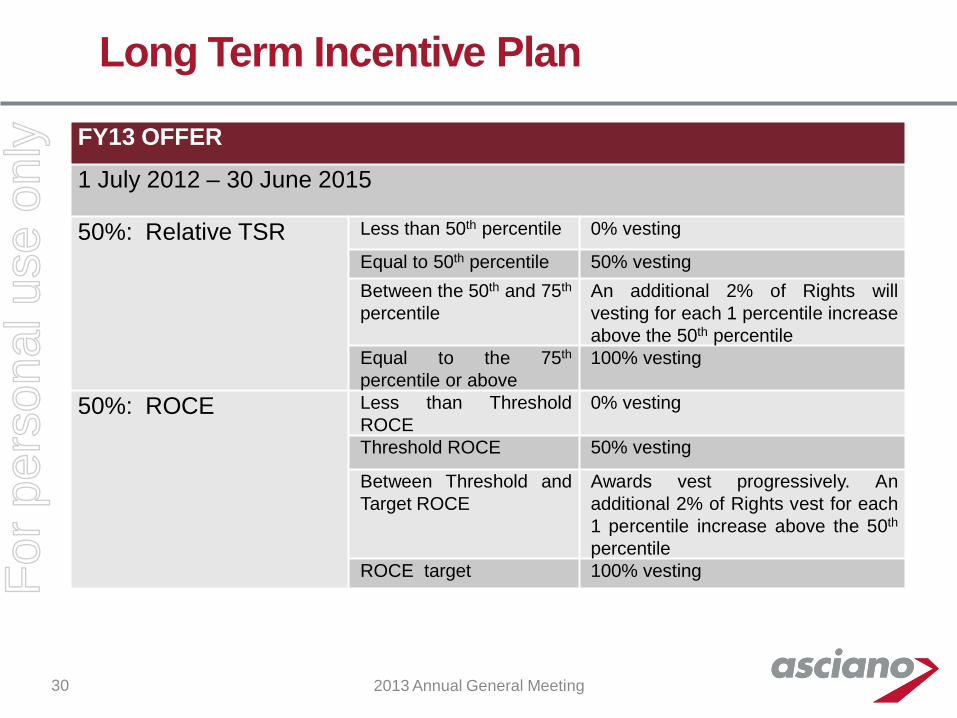

**Slide 30 – Long Term Incentive Plan**

Turning now to our long term incentive scheme which is designed to align our executive’s

interests with those of our shareholders.

In 2013, we maintained a consistent approach to our plan using two measures, Return on

Capital Employed and Relative Total Shareholder Return

With the vesting of our FY10 LTI Plan we are now seeing our strong performance start to

deliver some value for our management team. Of course this value is linked to share price,

demonstrating again the alignment between our reward process and shareholder value.

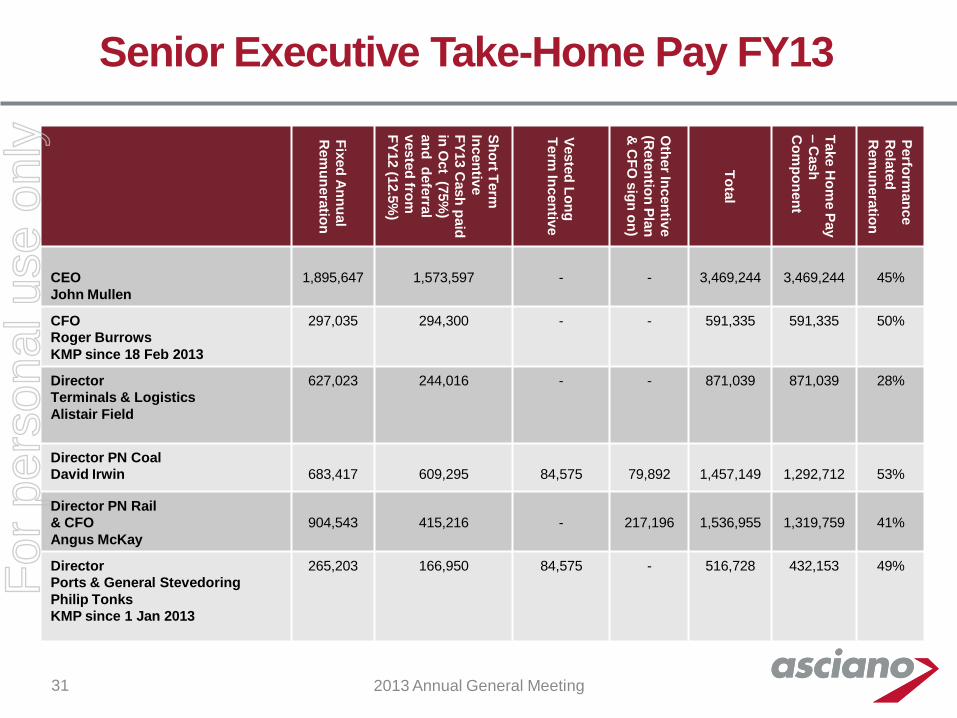

**Slide 31 – **Senior Executive Take Home Pay FY13**

As John Mullen has indicated, next year we believe will be a tough year and demonstrating

constraint in relation to pay is essential. The CEO, CFO and the Board are leading by

example and having no salary increases in FY14. In addition the average increases across

our Key Management Personnel will only be 1.8%.

**Slide 32 – FY14 Remuneration Structure **

The remuneration structure introduced in the 2012 financial year has proven particularly

effective in aligning our executive reward with Asciano’s achievements. The correlation

between the company’s strong performance and the higher rewards to management from

their at risk pay component is clear for all to see.

We will continue to focus on driving and rewarding executive performance to deliver the

Company’s strategy and business objectives and ultimately the growth in wealth of its

shareholders.

I will take it that you have all read the detailed information included in our Remuneration

Report and I hope this demonstrates our commitment to being open and transparent in our

Remuneration policy and outcomes.

For

per

sona

l use

onl

y

**Slide 33 - Questions from the floor on the Remuneration Report**

Thank you for your attention. I will be happy to take any questions you may have.

For

per

sona

l use

onl

y

ANNUAL GENERAL MEETING

2013

For

per

sona

l use

onl

y

In the event of an emergency, please take your

instructions from the venue wardens who will guide you

to an evacuation point.

Emergency Evacuation Procedures

2013 Annual General Meeting 2

For

per

sona

l use

onl

y

ANNUAL GENERAL MEETING

2013

For

per

sona

l use

onl

y

• This presentation includes “forward-looking statements.” These can be identified by words such as “may”, “should”,

“anticipate”, “believe”, “intend”, “estimate” and “expect”. Statements which are not based on historic or current facts may be

forward-looking statements.

• Forward-looking statements are based on assumptions regarding Asciano’s financial position, business strategies, plans and

objectives of management for future operations and development and the environment in which Asciano will operate.

• Forward-looking statements are based on current views, expectations and beliefs as at the date they are expressed and which

are subject to various risks and uncertainties. Actual results, performance or achievements of Asciano could be materially

different from those expressed in, or implied by, these forward-looking statements. The forward-looking statements contained

in this presentation are not guarantees or assurances of future performance and involve known and unknown risks,

uncertainties and other factors, many of which are beyond the control of Asciano, which may cause the actual results,

performance or achievements of Asciano to differ materially from those expressed or implied by the forward-looking

statements. For example, the factors that are likely to affect the results of Asciano include general economic conditions in

Australia; exchange rates; competition in the markets in which Asciano does and will operate; weather and climate conditions;

and the inherent regulatory risks in the businesses of Asciano. The forward-looking statements contained in this presentation

should not be taken as implying that the assumptions on which the projections have been prepared are correct or exhaustive.

• Asciano disclaims any responsibility for the accuracy or completeness of any forward-looking statement. Asciano disclaims any

responsibility to update or revise any forward-looking statement to reflect any change in Asciano’s financial condition, status or

affairs or any change in the events, conditions or circumstances on which a statement is based, except as required by law.

• The projections or forecasts included in this presentation have not been audited, examined or otherwise reviewed by the

independent auditors of Asciano. Unless otherwise stated, all amounts are based on A-IFRS and are in Australian

Dollars. Certain figures may be subject to rounding differences. Any market share information in this presentation is based on

management estimates based on internally available information unless otherwise indicated.

• You must not place undue reliance on these forward-looking statements.

• This presentation is not an offer or invitation for subscription or purchase of, or a recommendation of securities. The securities

referred to in these materials have not been and will not be registered under the United States Securities Act of 1933 (as

amended) and may not be offered or sold in the United States absent registration or an exemption from registration.

Disclaimer

2013 Annual General Meeting 4

For

per

sona

l use

onl

y

AGENDA

FORMAL BUSINESS

1. Chairman’s address

2. CEO’s address

3. Outlook

4. Questions

5. Formal business of the meeting

For

per

sona

l use

onl

y

CHAIRMAN’S ADDRESS Mr Malcolm Broomhead

For

per

sona

l use

onl

y

• Performance – Strong revenue and earnings growth

– Underlying revenue up 10.6% to $3.6 billion

– Underlying NPAT up 39.2% to $348.1 million

– Full year dividend fully franked 11.5 cents per share

• Customer – New state-of-the-art maintenance facilities

– Port Botany redevelopment project

– Development of customer centric culture

• Safety – 20.5% improvement in RIFR

– 32.3% improvement in LTIFR

• People & Teamwork – Focus on improving leadership capability and employee engagement

Year in Review

2013 Annual General Meeting 7

For

per

sona

l use

onl

y

• Inaugural sustainability report launched

• Greater transparency on economic, environment and

social performance

• Development of broader sustainability program

Sustainability

2013 Annual General Meeting 8

For

per

sona

l use

onl

y

• Board committed to delivering shareholder value

• Stability in leadership at Board level

• Re-election of Peter George as Non-Executive

Director: – Board member since 2007

– Chair of Asciano’s Audit and Risk Committee 2007-2012

– Member of Nomination and Succession Planning Committee and

Sustainability Committee and remains a member of the Audit and

Risk Committee.

Board Matters and Corporate Governance

2013 Annual General Meeting 9

For

per

sona

l use

onl

y

• Asciano barometer of productivity of Australia’s supply chain

• Board committed to elevating the efficiency and productivity of our

operations

• Over-regulated industrial relations environment

• Importance of general regulatory reform

• Maintenance of strong competition policy

Business Environment

2013 Annual General Meeting 10

For

per

sona

l use

onl

y

• Performance linked to strength of Australia’s economy

• Diversity of business activities provides buffer against weak

economic backdrop

• Focus on business improvement and efficiency initiatives

• Customer service and safety operational priorities

Outlook

2013 Annual General Meeting 11

For

per

sona

l use

onl

y

CEO’S ADDRESS

Mr John Mullen

For

per

sona

l use

onl

y

Strong result in 2013 with continued progress across most metrics

2013 Highlights

2013 Annual General Meeting 13

Financial Operational

• Underlying Revenue up 10.6%¹,² • Business diversification proving valuable

• EBIT up 12.5%¹ • Strong improvements in service performance

• Underlying NPAT & EPS up by 39.1%¹ • Rail, Coal, BAPS returns at or above WACC

• ROCE up to 11.0% • Terminals well above WACC ex goodwill

• BIP $45.7m cost reduction v target $25m • New contract wins – no major losses

• Capex 30% lower than plan • Major EA negotiations complete

• Operating cashflow up 11.3% to $988m • 32.3% improvement in LTIFR

• Free cashflow positive pre acquisitions • Continued investment in asset renewal

• 56.3% increase in final dividend on pcp • Tough conditions in Rail & Terminals

1. Pre material items

2. Net of Coal access For

per

sona

l use

onl

y

Asciano is tracking well against most metrics in a difficult environment

Five Year Objectives - Growth

Status Against Key Five Year Objectives

2013 Annual General Meeting 14

Target Objective Status Comment

Revenue Growth

5 year CAGR of 10%

• Coal volumes strong but pipeline slowing – expect 10 to

13% growth, net of access over the 5 years

• Rail on track historically but market very weak at present

• Terminals slow in 2013 but some signs of growth in 2014

• BAPS to continue strongly albeit slower than FY13

Operating Cost

5 year CAGR of 8%

• High fixed cost business impacts outcome in weak

volume environment

• Low growth divisions delivering lower or flat costs v pcp

Business Improvement Programme

$150m over 5 years to FY16 • Expected to exceed expectations

EBIT Growth

5 year CAGR of 15%

• Tracking between 10-15% 5 year CAGR to FY16 in a

very weak trading environment. Well positioned to benefit

from any cyclical economic upswing For

per

sona

l use

onl

y

Asciano is tracking well against most metrics in a difficult environment

Five Year Objectives – Returns

Status Against Key Five Year Objectives

Five Year Objectives – Business Performance

2013 Annual General Meeting 15

Committed Target Objective Status Comment

ROCE ; Group WACC by 2015

2-3% premium to WACC by 2017

On track to achieve targets

FCF positive by 2015 Ahead of original target given lower capital expenditure profile

Increased returns to shareholders On track – dividend increased by 25% in 2012 and 53% in 2013

Committed Target Objective Status Comment

A quality management team Strong team in place

Culture change Focus on customer advocacy, employee engagement, diversity

Safety Rapid improvement in metrics still significant potential For

per

sona

l use

onl

y

Growth driven by new contracts and strong volume growth across all regions

Update – Pacific National Coal

2013 Annual General Meeting 16

Net tonne kilometres increased 32.7% compared to the pcp reflecting a full period impact

from new contracts commenced over the last twelve months and strong organic growth in

volumes in all regions

Tonnes hauled versus contracted across the two regions for the quarter improved

significantly to 86.7% from 79.7% in the pcp

Expect strong volumes to continue through the second quarter benefiting from the

commencement in November 2013 of a new 8.5m tonne contract with Rio Tinto Coal

Australia

3 Months ended: Sept. ‘12 Sept. ‘13 %Chg

Net Tonne Kms (m) 5,330 7,071 32.7

Tonnes (m) 32.7 38.1 16.5

For

per

sona

l use

onl

y

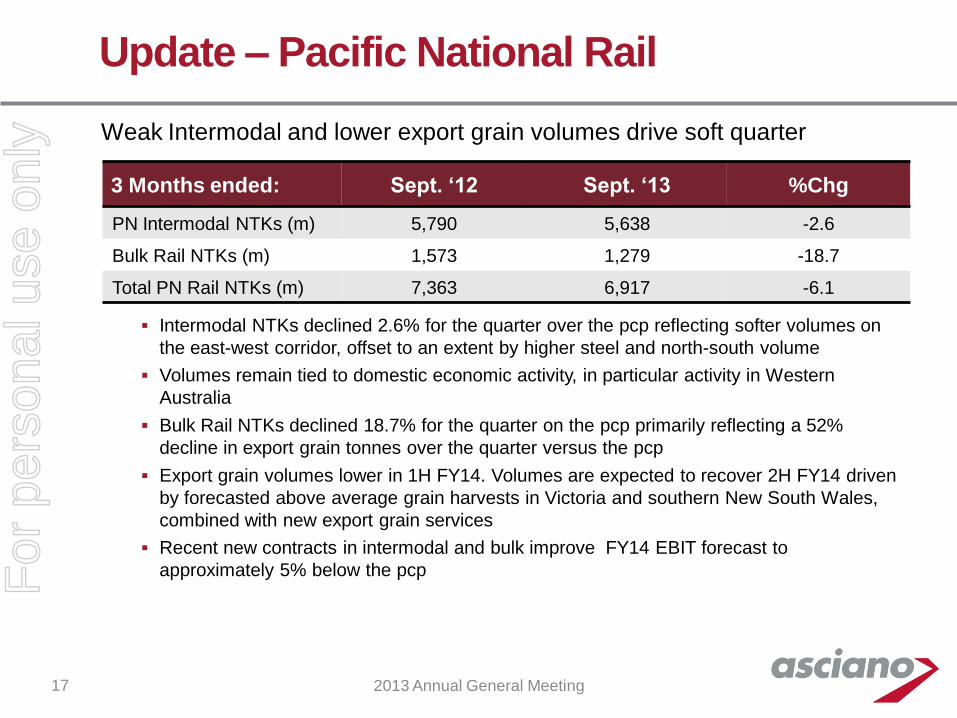

Weak Intermodal and lower export grain volumes drive soft quarter

Update – Pacific National Rail

Intermodal NTKs declined 2.6% for the quarter over the pcp reflecting softer volumes on

the east-west corridor, offset to an extent by higher steel and north-south volume

Volumes remain tied to domestic economic activity, in particular activity in Western

Australia

Bulk Rail NTKs declined 18.7% for the quarter on the pcp primarily reflecting a 52%

decline in export grain tonnes over the quarter versus the pcp

Export grain volumes lower in 1H FY14. Volumes are expected to recover 2H FY14 driven

by forecasted above average grain harvests in Victoria and southern New South Wales,

combined with new export grain services

Recent new contracts in intermodal and bulk improve FY14 EBIT forecast to

approximately 5% below the pcp

2013 Annual General Meeting 17

3 Months ended: Sept. ‘12 Sept. ‘13 %Chg

PN Intermodal NTKs (m) 5,790 5,638 -2.6

Bulk Rail NTKs (m) 1,573 1,279 -18.7

Total PN Rail NTKs (m) 7,363 6,917 -6.1

For

per

sona

l use

onl

y

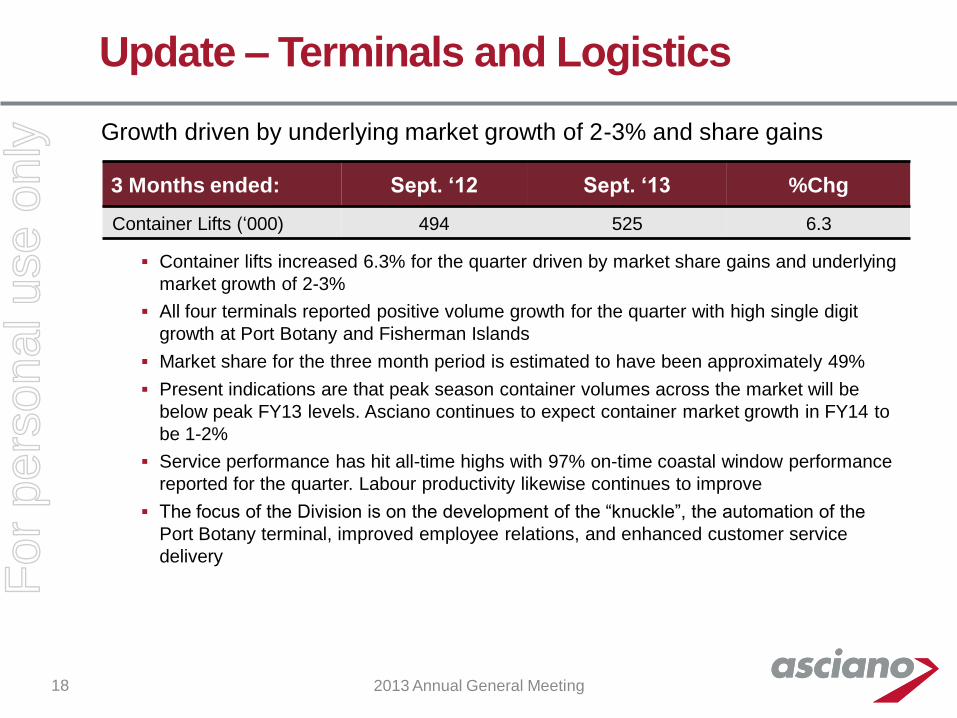

Growth driven by underlying market growth of 2-3% and share gains

Update – Terminals and Logistics

2013 Annual General Meeting 18

3 Months ended: Sept. ‘12 Sept. ‘13 %Chg

Container Lifts (‘000) 494 525 6.3

Container lifts increased 6.3% for the quarter driven by market share gains and underlying

market growth of 2-3%

All four terminals reported positive volume growth for the quarter with high single digit

growth at Port Botany and Fisherman Islands

Market share for the three month period is estimated to have been approximately 49%

Present indications are that peak season container volumes across the market will be

below peak FY13 levels. Asciano continues to expect container market growth in FY14 to

be 1-2%

Service performance has hit all-time highs with 97% on-time coastal window performance

reported for the quarter. Labour productivity likewise continues to improve

The focus of the Division is on the development of the “knuckle”, the automation of the

Port Botany terminal, improved employee relations, and enhanced customer service

delivery

For

per

sona

l use

onl

y

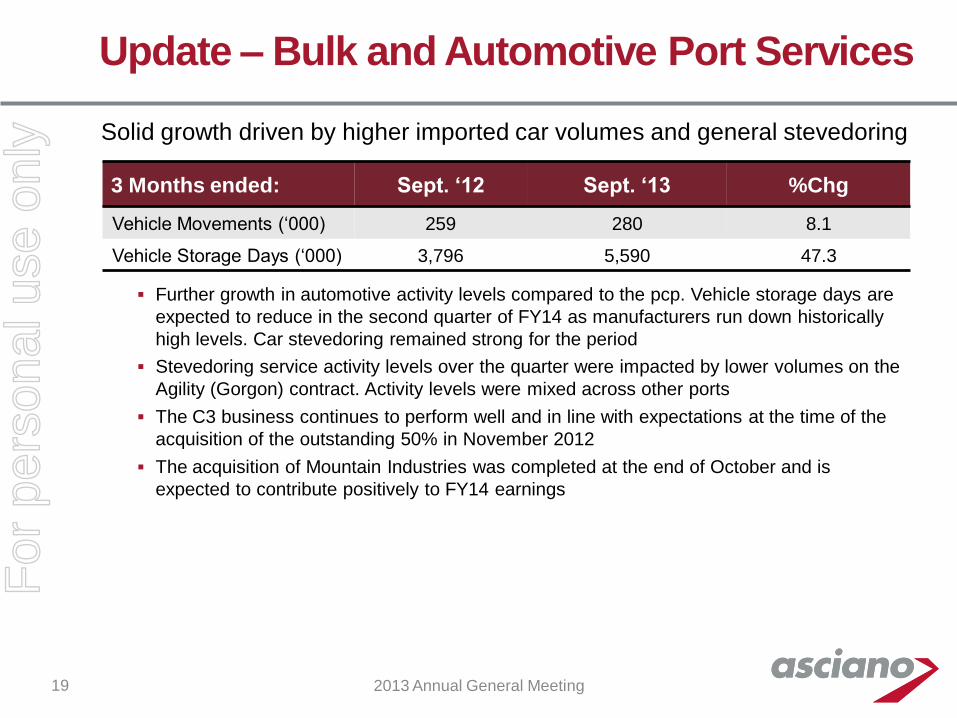

Solid growth driven by higher imported car volumes and general stevedoring

Update – Bulk and Automotive Port Services

Further growth in automotive activity levels compared to the pcp. Vehicle storage days are

expected to reduce in the second quarter of FY14 as manufacturers run down historically

high levels. Car stevedoring remained strong for the period

Stevedoring service activity levels over the quarter were impacted by lower volumes on the

Agility (Gorgon) contract. Activity levels were mixed across other ports

The C3 business continues to perform well and in line with expectations at the time of the

acquisition of the outstanding 50% in November 2012

The acquisition of Mountain Industries was completed at the end of October and is

expected to contribute positively to FY14 earnings

2013 Annual General Meeting 19

3 Months ended: Sept. ‘12 Sept. ‘13 %Chg

Vehicle Movements (‘000) 259 280 8.1

Vehicle Storage Days (‘000) 3,796 5,590 47.3

For

per

sona

l use

onl

y

Issue extends tenure and further diversifies funding sources.

Medium Term Note Issue

$’m

FY24 FY23 FY22 FY21 FY20 FY19 FY18 FY17 FY16 FY15

380

FY14

US$ 144a Reg S Bonds

Drawn bank facilities as at 30 September 2013

Undrawn bank facilities as at 30 September 2013

GBP Medium Term Note Program

429

728

643

243

514

650

270

In September 2013 Asciano settled an offering of 10 year medium term notes to the value of

GBP300m (A$514m). The notes were issued at an all in rate swapped back to Australian dollars of

7.9%

The issue extended Asciano’s weighted average debt maturity to 5.6 years

Proceeds will be used to reduce senior indebtedness outstanding under Asciano’s bank facilities

1. As at 30 September 2013

2013 Annual General Meeting 20

380

For

per

sona

l use

onl

y

Outlook

2013 Annual General Meeting 21

Further growth in EBIT in FY14 expected despite soft domestic

economic conditions

• Difficult market conditions to continue but Asciano still forecasting earnings growth in FY14

– PN Rail market growth -4% to 0%, FY14 EBIT now expected to be approximately 5% below pcp

– Terminals & Logistics market growth 1-2% with the Division benefiting from swing in market share

– Coal revenues to benefit from strong market growth and contribution from new contracts

– BAPS growth to continue albeit at slower rate than 2013 but boosted by C3 and Mountain Industries

– Further growth in EBIT overall, but growth rate lower than FY13

• Increased focus on cost control, business and asset efficiency, and improved returns

– Despite lower top line growth, on track to deliver our ROCE targets

– Continuing to drive towards improved shareholder payouts and TSR growth

• Focus on working with our customers to innovate and adapt our service offerings

– Multiple programs to improve service performance and the competitive position of the Company

• Continue to develop currently expanding synergies across the Group

– Further supply chain integration of existing divisions

• Continue to generate value through acquisitions, partnerships and joint ventures

– Acquisition of C3 and Mountain Industries adding significant value

– Additional opportunities being sought

For

per

sona

l use

onl

y

QUESTIONS

For

per

sona

l use

onl

y

FORMAL BUSINESS OF THE MEETNG

For

per

sona

l use

onl

y

Casting your vote

• Ensure that the smart card is inserted and

that the handset displays a welcome

message.

• When the poll opens, the handset will

display the voting options, being;

– 1 to vote FOR the resolution

– 2 to vote AGAINST the resolution

– 3 to ABSTAIN your vote

• Press the appropriate button on the handset

to register your intentions

How to Vote

2013 Annual General Meeting 24

For

per

sona

l use

onl

y

FORMAL BUSINESS OF THE MEETNG

For

per

sona

l use

onl

y

“To receive and consider the consolidated Financial Report of the Company as well as the reports of the Directors and the Auditors for the financial year ended 30 June 2013.”

FINANCIAL

STATEMENTS AND

REPORTS

ITEM

1

For

per

sona

l use

onl

y

CHAIRMAN OF REMUNERATION COMMITTEE’S ADDRESS Mr Chris Barlow

For

per

sona

l use

onl

y

Short Term Incentive Plan

Asciano FY13 Short Term Incentive Plan Measures

EBIT 50% 90% of target must be achieved before

any payment. Overachievement is

uncapped.

SAFETY 15% Threshold must be achieved for 10%

payment. Target 15% payment. Stretch

22.5% payment . (Progressive payment

between Threshold and Stretch.)

CUSTOMER

SATISFACTION

15% Threshold must be achieved for any

payment. Maximum payment is 15%

PERSONAL GOALS 20% Each goal weighted. Maximum payment

is 20%.

2013 Annual General Meeting 28

For

per

sona

l use

onl

y

Short Term Incentive Results

Division

EBIT

(50%

weighting)

Safety

(15% weighting)

Customer

(15%

weighting)

Personal

Goals

(20%

weighting)

STI

Outcome

PN Coal 55% 12% (above Threshold) 15% (Target) 20% (Target) 102%

PN Rail 47% 0% (Not Met) 10%

(Threshold) 20% (Target) 77%

Terminals &

Logistics 44%

16% (above Target)

15% (Target) 20% (Target) 95%

Ports &

General

Stevedoring

130% 18% (above Target) 0% (below

Threshold) 20% (Target) 168%

Asciano

Group

49%

16%

(above Target)

13% (above

Threshold )

20% (Target)

98%

2013 Annual General Meeting 29

For

per

sona

l use

onl

y

Long Term Incentive Plan

FY13 OFFER

1 July 2012 – 30 June 2015

50%: Relative TSR Less than 50th percentile 0% vesting

Equal to 50th percentile 50% vesting

Between the 50th and 75th

percentile

An additional 2% of Rights will

vesting for each 1 percentile increase

above the 50th percentile

Equal to the 75th

percentile or above

100% vesting

50%: ROCE Less than Threshold

ROCE

0% vesting

Threshold ROCE 50% vesting

Between Threshold and

Target ROCE

Awards vest progressively. An

additional 2% of Rights vest for each

1 percentile increase above the 50th

percentile

ROCE target 100% vesting

2013 Annual General Meeting 30

For

per

sona

l use

onl

y

Senior Executive Take-Home Pay FY13

Fix

ed

An

nu

al

Rem

un

era

tion

Sh

ort T

erm

Incen

tive

FY

13 C

ash

paid

in O

ct (7

5%

)

an

d d

efe

rral

veste

d fro

m

FY

12 (1

2.5

%)

Veste

d L

on

g

Term

Incen

tive

Oth

er In

cen

tive

(Rete

ntio

n P

lan

& C

FO

sig

n o

n)

To

tal

Take H

om

e P

ay

– C

ash

Co

mp

on

en

t

Perfo

rman

ce

Rela

ted

Rem

un

era

tion

CEO

John Mullen

1,895,647

1,573,597

-

-

3,469,244

3,469,244

45%

CFO

Roger Burrows

KMP since 18 Feb 2013

297,035 294,300 - - 591,335 591,335 50%

Director

Terminals & Logistics

Alistair Field

627,023 244,016 - - 871,039 871,039 28%

Director PN Coal

David Irwin

683,417

609,295

84,575

79,892

1,457,149

1,292,712

53%

Director PN Rail

& CFO

Angus McKay

904,543

415,216

-

217,196

1,536,955

1,319,759

41%

Director

Ports & General Stevedoring

Philip Tonks

KMP since 1 Jan 2013

265,203 166,950 84,575 - 516,728 432,153 49%

2013 Annual General Meeting 31

For

per

sona

l use

onl

y

FY14 Remuneration Structure

LTI (c)

FAR (a)

Total remuneration a + b + c

FAR (a)

FY14 Construct

Total remuneration a + b + c

STI Deferral (b*25%)

STI Cash (b*75%)

LTI (c)

No change

No change

No change

FY13 Construct

STI MEASURES (No change)

EBIT

Safety

Customer

Personal Objectives

STI Deferral (b*25%)

STI Cash (b*75%)

2013 Annual General Meeting 32

For

per

sona

l use

onl

y

QUESTIONS

For

per

sona

l use

onl

y

FORMAL BUSINESS OF THE MEETING

For

per

sona

l use

onl

y

REMUNERATION

REPORT

“To adopt the remuneration report for the financial year ended 30 June 2013.”

ITEM

2

For

per

sona

l use

onl

y

RE-ELECTION OF DIRECTOR ADDRESS

Mr Peter George

For

per

sona

l use

onl

y

“To consider and , if thought fit, pass the following resolution as an ordinary resolution: That Mr Peter George, who retires under Article 9.2(a) of the Company’s constitution and, being eligible, offers himself for election, be re-elected as a Director of the Company.”

RE-ELECTION OF

DIRECTOR

ITEM

3

For

per

sona

l use

onl

y

“To consider and , if thought fit, pass the following

resolution as an ordinary resolution:

That approval be given for the grant of a maximum of

473, 348 rights to acquire shares in the Company to the

Managing Director and Chief Executive Officer, Mr John

Mullen, in accordance with the rules of the Asciano Limited

Long Term Incentive Plan and that approval be given for

the purposes of sections 200B and 200E of the

Corporations Act 2001 for the giving of benefits to Mr John

Mullen under the Plan, on the terms summarised in the

Explanatory Notes.”

GRANT OF RIGHTS TO

CHIEF EXECUTIVE

OFFICER

– 2014 FINANCIAL YEAR

ITEM

4

For

per

sona

l use

onl

y

CLOSE OF MEETING

For

per

sona

l use

onl

y

![For personal use only - ASX · 2008. 10. 21. · ]Fully franked final dividend of 12.00 cents, up 17.1% on last year]Total dividend payout for the year of 23.00 cents, 13.6% higher](https://static.fdocuments.us/doc/165x107/60d3e4c923a0ca2272084d7d/for-personal-use-only-2008-10-21-fully-franked-final-dividend-of-1200-cents.jpg)