ASX 200 Cumulative Price Returns AUSTRALIA …...Energy Materials Financials Information … 20...

15

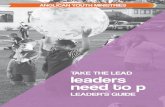

Please refer to page 14 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures . AUSTRALIA ASX 200 Cumulative Price Returns ASX 200 Daily Price Returns Australian Equity Market Performance Source: IRESS, Macquarie Research, April 2016 4 April 2016 Macquarie Securities (Australia) Limited Australian Equity Strategy March Equity Market Review Key developments / changes: ASX200 rises 4.1% posting strongest positive return since Oct-15; March returns unable to offset combined January (-5.5%) and February (-2.5%) losses with ASX200 1Q16 still in negative territory (-4.0%); NTM market P/E up from 14.8x to 15.6x (LTA ~14x), 2016 Industrial EPSg slipped from +0.2% to -0.2% and 2017 EPSg steady at +12%; A$ continued its appreciation, rising 7% versus the US$ - now at its highest level since July 2015; Commodity prices were stronger on an improving Chinese growth outlook and further US$ weakness - oil rises 14%; Banks (led by ANZ) drove a mid-month correction on worsening resource sector impairment charges but finished in the green; Domestic economic data was better than expected led by 4Q15 GDP and the labour market which showed a dip in the unemployment rate; The federal budget has been brought forward and the Senate recalled to consider legislation potentially triggering a double dissolution election; The Federal Reserve backed down from its rate hike path implicitly suggesting the “mistake” would be moving early not late; Australian Equities – what a difference a month makes...or does it?: Equities underwent a sizeable rebound through March, rising 4.1% to post the strongest monthly return since October 2015. However, it was not enough to recoup the combined declines suffered through January and February with the ASX200 finishing 1Q16 down 4.0%. As we have become accustomed, daily price returns were extreme, reflecting shifty sentiment rather than sustained changes in economic or earnings fundamentals. A dovish shift by the Federal Reserve set equities and emerging market risk assets on a higher path into the final day of the month (the ASX200 rose 1.4%) but it was strength in the commodity based sectors – Energy and Materials – that provided the positive platform for the overall market return through March. Politics remains a talking point with BREXIT and US presidential elections continuing to dominate global headlines; at a domestic level the federal budget has been brought forward by a week, and the Senate has been recalled to consider legislation which could potentially trigger a double dissolution election in July (dismissed by the market without much fanfare or concern); banks led an intra-month sell-off on the back of ANZ’s announcement of a worse-than- expected resources sector impairment charge. Performance across sectors was consistent with the overall positive market tone as Healthcare, Utilities and Telco’s were laggards against the cyclical sectors (Materials and Consumer Discretionary) – see Fig 2. However, outside of the resources, this was a tilt against specific defensive names (particularly healthcare which was dragged lower by CSL, RMD, RHC and Utilities which saw relative underperformance by AGL and APA) rather than on the back of an improving domestic growth picture irrespective of a tick higher in the terms of trade. 0% 1% 2% 3% 4% 5% 6% 7% 1-Mar 8-Mar 15-Mar 22-Mar 29-Mar ASX 200 Cumulative Price Returns 4.1% -2.0% -1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 1-Mar 8-Mar 15-Mar 22-Mar 29-Mar Daily ASX 200 Returns 6.2 6.0 5.9 5.6 5.4 5.1 4.8 4.7 4.7 4.7 4.6 3.0 2.3 1.3 0.4 0 2 4 6 8 Energy Materials Financials IT 20 Leaders Cons. Disc S&P/ASX 300 S&P/ASX 200 Telcos S&P/ASX 100 50 Leaders Cons. Staples Industrials Utilities Health Care Total return (%), March

Transcript of ASX 200 Cumulative Price Returns AUSTRALIA …...Energy Materials Financials Information … 20...

Please refer to page 14 for important disclosures and analyst certification, or on our website www.macquarie.com/research/disclosures.

AUSTRALIA

ASX 200 Cumulative Price Returns

ASX 200 Daily Price Returns

Australian Equity Market Performance

Source: IRESS, Macquarie Research, April 2016

4 April 2016 Macquarie Securities (Australia) Limited

Australian Equity Strategy March Equity Market Review Key developments / changes:

ASX200 rises 4.1% posting strongest positive return since Oct-15;

March returns unable to offset combined January (-5.5%) and February

(-2.5%) losses with ASX200 1Q16 still in negative territory (-4.0%);

NTM market P/E up from 14.8x to 15.6x (LTA ~14x), 2016 Industrial

EPSg slipped from +0.2% to -0.2% and 2017 EPSg steady at +12%;

A$ continued its appreciation, rising 7% versus the US$ - now at its

highest level since July 2015;

Commodity prices were stronger on an improving Chinese growth outlook

and further US$ weakness - oil rises 14%;

Banks (led by ANZ) drove a mid-month correction on worsening resource

sector impairment charges but finished in the green;

Domestic economic data was better than expected led by 4Q15 GDP and

the labour market which showed a dip in the unemployment rate;

The federal budget has been brought forward and the Senate recalled to

consider legislation potentially triggering a double dissolution election;

The Federal Reserve backed down from its rate hike path implicitly

suggesting the “mistake” would be moving early not late;

Australian Equities – what a difference a month makes...or does it?:

Equities underwent a sizeable rebound through March, rising 4.1% to post the

strongest monthly return since October 2015. However, it was not enough to

recoup the combined declines suffered through January and February with

the ASX200 finishing 1Q16 down 4.0%.

As we have become accustomed, daily price returns were extreme, reflecting

shifty sentiment rather than sustained changes in economic or earnings

fundamentals. A dovish shift by the Federal Reserve set equities and

emerging market risk assets on a higher path into the final day of the month

(the ASX200 rose 1.4%) but it was strength in the commodity based

sectors – Energy and Materials – that provided the positive platform for

the overall market return through March.

Politics remains a talking point with BREXIT and US presidential elections

continuing to dominate global headlines; at a domestic level the federal budget

has been brought forward by a week, and the Senate has been recalled to

consider legislation which could potentially trigger a double dissolution election

in July (dismissed by the market without much fanfare or concern); banks led an

intra-month sell-off on the back of ANZ’s announcement of a worse-than-

expected resources sector impairment charge.

Performance across sectors was consistent with the overall positive

market tone as Healthcare, Utilities and Telco’s were laggards against

the cyclical sectors (Materials and Consumer Discretionary) – see Fig 2.

However, outside of the resources, this was a tilt against specific defensive

names (particularly healthcare which was dragged lower by CSL, RMD, RHC

and Utilities which saw relative underperformance by AGL and APA) rather

than on the back of an improving domestic growth picture irrespective of a tick

higher in the terms of trade.

0%

1%

2%

3%

4%

5%

6%

7%

1-Mar 8-Mar 15-Mar 22-Mar 29-Mar

ASX 200 Cumulative Price Returns

4.1%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

1-Mar 8-Mar 15-Mar 22-Mar 29-Mar

Daily ASX 200 Returns

6.2

6.0

5.9

5.6

5.4

5.1

4.8

4.7

4.7

4.7

4.6

3.0

2.3

1.3

0.4

0 2 4 6 8

Energy

Materials

Financials

IT

20 Leaders

Cons. Disc

S&P/ASX 300

S&P/ASX 200

Telcos

S&P/ASX 100

50 Leaders

Cons. Staples

Industrials

Utilities

Health Care

Total return (%),March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 2

Global Equities: It was a positive month for global equity markets (MSCI World +6.5%)

but with significant dispersion across regions and markets (MSCI Europe +1.0% vs MSCI

Asia-X +11.1%) – see Fig. 1. Lat Am was driven by strong local currency and US$ returns

from Brazil (Bovespa +17%) as commodity prices and the real appreciated significantly;

Asia was led higher by China (SHCOMP +12%), Hong Kong (Hang Seng +9%) and India

(Sensex +10%) but its commodity sensitive markets (Indonesia and Malaysia were

regional laggards despite a significant weakening in the MYR); Europe was the global

laggard (Euro Stoxx +2%) as France (CAC +1%) primarily offset a strong Germany (+5%);

the UK was kept in check by ongoing BREXIT concerns (FTSE100 +1%); and the US took

a strong lead from the rise in energy equities and later from Yellen’s dovish communication

that drove both bonds and equities higher (S&P500 +7%).

Fig 1 Global Equity Market Performance Fig 2 Australian Equity Market Performance

Source: IBES, Macquarie Research, April 2016

Economics: There were two domestic economic surprises over March. The release of

4Q15 GDP data revealed that the economy grew by 3.0%YoY, which we estimate is 50bp

higher than the RBA had factored into their February Statement on Monetary Policy

forecasts. A decline in the household savings rate, to the lowest since 3Q08, supported

household demand against a weak income backdrop. Whilst production (GDP) rose by

3.0%YoY, income (GDI) rose just 0.3%YoY, and continues to exert a strain on non-mining

domestic sectors. (See: Aussie Macro Moment – GDP Wrap 4Q15: Production delivers,

while income withers).

The second piece of better-than-expected domestic economic news came from the labour

market. Despite weaker jobs growth, the unemployment rate dipped back down to 5.8% -

in line with our estimate of the RBA’s expectations. (See: Aussie Macro Moment - Labour

force: Does no jobs + lower UR + weaker participation = winning?) The unemployment rate

outcome and firmer GDP release saw market pricing for near-term RBA rate cuts reduced.

The perceived firmer tone of the domestic data was put in sharp contrast by a more dovish

turn from the US Federal Reserve. The FOMC halved their rate hike guidance (from four

hikes in 2016 to two) at the March meeting, resulting in significant downward pressure on

the US$. The A$ surged as the weaker Fed compounded A$ support that had emerged

following the rise in iron ore prices in early March. (See: The Macquarie Weekly – RBA

chill vs A$ thrill). The A$ has appreciated 12.2% since its mid-January low of US$0.6827,

to finish March at US$0.7657.

13.3

11.8

8.7

6.9

6.8

5.5

5.0

4.7

4.6

2.7

1.3

0 2 4 6 8 10 12 14

MSCI EM

Shanghai Composite

Hang Seng

MSCI World

S&P500

MSCI Korea

German DAX

S&P /ASX 200

Nikkei 225

EuroStoxx

FTSE 100

Total return (%),March

6.2

6.0

5.9

5.6

5.4

5.1

4.8

4.7

4.7

4.7

4.6

3.0

2.3

1.3

0.4

0 2 4 6 8

Energy

Materials

Financials

Information …

20 Leaders

Consumer …

S&P/ASX 300

S&P/ASX 200

Telecommuni…

S&P/ASX 100

50 Leaders

Consumer …

Industrials

Utilities

Health Care

Total return (%),March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 3

There were also developments in the domestic political landscape. The federal

budget has been brought forward by a week, and the Senate has been recalled to consider

legislation which could potentially trigger a double dissolution election in July. There are

signs that the threat of an early election has driven an increased level of uncertainty

amongst consumers. Consumer sentiment weakened in March, and there was a major

souring of consumer appetite for real estate investment, and a swing towards conservatism

with a near record proportion of consumers preferring to pay off debt, rather than

invest. Business confidence appears to have improved, although the data was for

February, and not factored in the upswing in the A$ and recent domestic developments.

Currencies: AUD rose 7% in March, up 11% from mid Jan lows vs USD (TWD +4.9%).

The DXY declined a further 3.5% over March, putting it down 4% for the quarter (its worst

quarter since 2010). Joining the BoJ in introducing a negative interest rate was the ECB

earlier through March, which did not drive a weaker Euro but instead a slight rise

(EURUSD +0.9%), after Draghi’s indication that they had reached their limits on rate cuts.

EM and commodity linked currencies generally rallied strongly – in line with stronger

commodity prices - MYR (+8%), KRW (+9%), INR (+3%).

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 4

Fig 3 Market and sector performance (S&P/ASX 300)

Sector No S&P Sector

Price Index

% Change Accum Index

% Change % of S&P 300 AMV $m

Daily Turn $m 1 Mth 12 Mth 1 Mth 12 Mth 31/03/16 29/02/16 31/03/15

25 Consumer Discretionary 2060.9 4.2 1.1 16682.8 5.1 5.0 5.3 5.1 4.3 71724 329.2

30 Consumer Staples 8533.4 2.2 -9.3 75838.6 3.0 -5.1 7.2 7.3 6.8 98532 303.6

10 Energy 7960.9 5.7 -28.2 61333.1 6.2 -25.2 4.1 4.0 4.4 55257 325.1

40 Financials 5726.6 5.6 -17.7 63797.5 5.9 -13.1 45.9 45.5 48.1 625708 1721.3

65 - Financials ex Property 6426.4 6.3 -21.7 68594.9 6.7 -17.1 37.6 37.0 41.1 512362 1409.5

60 - Property Trusts (GICS) 1338.5 2.4 6.0 41478.2 2.5 11.4 8.3 8.5 7.0 113345 311.9

35 Health Care 16000.1 -0.5 -0.3 104804.1 0.4 1.9 6.8 7.3 6.1 93169 352.2

20 Industrials 5099.9 1.7 8.9 45657.4 2.3 12.8 8.4 8.6 7.3 114732 418.9

45 Information Technology 871.5 4.8 -5.9 6178.9 5.6 -2.9 1.2 1.2 1.0 16840 60.7

15 Materials 7259.3 5.4 -20.5 54293.5 6.0 -17.2 13.0 12.9 14.4 177657 965.4

50 Telecomm. Services 1910.8 1.8 -11.7 25309.8 4.7 -6.9 5.5 5.6 5.7 74989 197.5

55 Utilities 6808.4 1.0 6.2 79089.3 1.3 11.5 2.5 2.5 2.0 33442 94.6

26 20 Leaders 2936.8 4.8 -20.6 54307.5 5.4 -16.3 59.7 58.6 65.3 812724 2197.8

31 50 Leaders 5072.7 4.1 -16.3 47421.3 4.6 -12.1 78.8 78.8 81.9 1072937 3184.0

25 S&P/ASX 100 4207.3 4.1 -14.6 11877.6 4.7 -10.4 90.6 90.9 92.2 1234485 4062.8

51 S&P/ASX 200 5082.8 4.1 -13.7 47018.6 4.7 -9.6 97.7 97.8 98.0 1330099 4637.3

52 S&P/ASX 300 5043.6 4.2 -13.4 46466.2 4.8 -9.3 100.0 100.0 100.0 1362050 4768.5

Source: IRESS, Macquarie Research, April 2016

Fig 4 Sector & industry performance (S&P/ASX300)

Sector No S&P Sector

Price Index

% Change Accum Index

% Change % of S&P 300 AMV $m

Daily Turn $m 1 Mth 12 Mth 1 Mth 12 Mth 31/03/16 29/02/16 31/03/15

2510 Automobiles & Components 1322.5 -0.2 21.2 1384.5 -0.2 22.6 0.1 0.1 0.1 1033 2.4

4010 Banks 7611.4 6.5 -25.5 84483.6 6.5 -21.0 27.8 27.3 31.8 378776 919.6

2010 Capital Goods 2244.2 7.4 7.5 21625.8 9.4 12.4 0.5 0.5 0.5 6873 61.8

2020 Comm. & Profess. Services 2480.7 1.2 -2.2 19566.7 2.2 1.0 2.9 3.0 2.7 39629 144.5

2520 Cons. Durables & Apparel 547.9 5.9 -10.9 4730.2 6.9 -7.3 0.1 0.1 0.1 1488 4.7

2530 Consumer Services 6980.9 3.5 0.4 66956.3 4.2 4.0 3.1 3.0 2.5 41643 176.7

4020 Diversified Financials 6993.4 3.7 -9.0 68761.0 4.5 -4.7 3.8 3.8 3.5 51143 214.4

1010 Energy 7960.9 5.7 -28.2 61333.1 6.2 -25.2 4.1 4.0 4.4 55257 325.1

3010 Food & Drug Retailing 12030.0 2.3 -13.6 104514.5 3.0 -9.4 5.6 5.7 5.8 76247 188.3

3020 Food Beverage & Tobacco 5846.6 0.9 12.4 51571.0 1.5 15.9 1.4 1.4 0.9 18836 88.3

3510 Health Care Equip & Serv. 8346.3 0.0 -11.3 59380.0 0.8 -8.8 3.1 3.3 3.0 41990 211.8

3030 Household & Pers. Products 1142.5 9.2 25.7 1225.0 11.2 30.9 0.3 0.2 0.1 3448 27.0

4030 Insurance 3612.4 7.6 -7.5 34557.4 9.2 -2.8 5.3 5.2 5.2 72507 238.5

1510 Materials 7259.3 5.4 -20.5 54293.5 6.0 -17.2 13.0 12.9 14.4 177657 965.4

2540 Media 1462.2 6.0 -7.1 10495.7 8.2 -2.8 0.9 0.9 0.8 12230 68.4

3520 Pharm. Biotech. & Life Sc. 30927.5 -0.8 10.8 185954.4 0.0 12.7 3.8 4.0 3.1 51179 140.4

4040 Real Estate 3143.7 2.7 4.4 39123.1 2.8 9.6 9.1 9.2 7.7 123282 348.9

2550 Retailing 4882.5 4.7 11.2 44387.9 5.6 15.7 1.1 1.1 0.9 15330 77.1

4530 Semi & Semicond. Equip. 0.0 0.0 0.0 0 0.0

4510 Software & Services 1048.8 4.9 -5.0 7625.2 5.7 -2.0 1.2 1.1 1.0 16840 60.6

4520 Tech. Hardware & Equip. 0.0 0.0 0.0 0 0.2

5010 Telecommunication Services 1910.8 1.8 -11.7 25309.8 4.7 -6.9 5.5 5.6 5.7 74989 197.5

2030 Transportation 9526.9 1.5 17.4 90259.9 1.6 21.6 5.0 5.1 4.2 68229 212.6

5510 Utilities 6808.4 1.0 6.2 79089.3 1.3 11.5 2.5 2.5 2.0 33442 94.6

Source: IRESS, Macquarie Research, April 2016

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 5

Fig 5 Top 10 and bottom 10 performances (ASX100)

S&P Code

Company Price ($) Total Returns % % S&P 100 % S&P 300 Liquidity

Factor (%)

AMV (A$m) 1 Mth 12 Mth 31/03/16 29/02/16 31/03/16 29/02/16

Top 10

SGM SIMS METAL MANAGEMENT LIMITED 8.6 30.1 -28.3 0.09 0.11 0.09 81 1437

WOR WORLEYPARSONS LIMITED 5.4 28.1 -41.4 0.08 0.09 0.07 91 1178

FMG FORTESCUE METALS GROUP LTD 2.6 26.5 32.7 0.35 0.29 0.32 0.27 55 4338

STO SANTOS LIMITED 4.0 21.8 -32.3 0.52 0.42 0.47 0.38 90 6404

PRY PRIMARY HEALTH CARE LIMITED 3.8 19.3 -28.8 0.14 0.14 0.12 0.12 89 1670

MPL MEDIBANK PRIVATE LIMITED 2.9 18.3 30.7 0.65 0.59 0.59 0.53 100 8069

S32 SOUTH32 LIMITED 1.5 17.2 0.63 0.56 0.57 0.51 100 7796

DOW DOWNER EDI LIMITED 3.8 15.3 -8.7 0.14 0.12 0.12 0.11 100 1669

ORG ORIGIN ENERGY LIMITED 5.1 14.9 -45.3 0.72 0.65 0.65 0.59 100 8875

BOQ BANK OF QUEENSLAND LIMITED. 12.1 14.9 -6.7 0.37 0.34 0.33 0.30 100 4555

Bottom 9

SRX SIRTEX MEDICAL LIMITED 28.92 -9.63 40.00 0.13 0.16 0.12 0.14 100 1655

RMD RESMED INC 7.43 -8.16 -18.78 0.36 0.52 0.33 0.47 100 4463

RHC RAMSAY HEALTH CARE LIMITED 61.36 -6.66 -7.15 0.64 0.72 0.58 0.66 64 7911

CTX CALTEX AUSTRALIA LIMITED 34.02 -4.98 0.69 0.74 0.83 0.67 0.76 100 9185

DLX DULUXGROUP LIMITED 6.28 -3.83 1.64 0.19 0.21 0.18 0.19 100 2393

NCM NEWCREST MINING LIMITED 16.96 -3.09 26.85 1.05 1.13 0.95 1.03 100 12946

TTS TATTS GROUP LIMITED 3.78 -2.83 -0.75 0.45 0.48 0.41 0.44 100 5522

AZJ AURIZON HOLDINGS LIMITED 3.96 -2.70 -13.15 0.67 0.72 0.61 0.66 100 8313

DMP DOMINO'S PIZZA ENTERPRISES LIMITED 57.48 -2.18 56.31 0.29 0.31 0.27 0.29 73 3627

Source: IRESS, Macquarie Research, April 2016

Fig 6 Market & sector EPSg (%) & P/E multiples

Macquarie bottom up EPSg (%) Macquarie bottom up PERs(x)

Macquarie EPSg (%), June pro-rated FY15A FY16E FY17E FY18E FY15A FY16E FY17E

All Companies -2.3 -8.8 14.2 9.3 15.0 16.4 14.3

Market (ex res) 5.8 0.3 7.7 6.1 15.5 15.3 14.2

Banks 2.0 0.1 2.9 3.8 12.0 11.9 11.6

Property Trusts 6.1 5.8 6.2 6.0 18.9 17.8 16.8

Resources -30.7 -56.0 91.5 30.2 12.3 28.7 15.0

Industrials (All Cos ex Res, LPTs, Banks) 9.6 -0.4 12.5 8.2 18.0 18.1 16.1

S&P/ASX 100 -2.0 -9.6 12.7 8.8 14.8 16.3 14.4

Small Companies -7.0 2.3 31.6 13.4 16.9 17.4 13.3

Small Industrials 0.8 5.2 9.4 8.5 16.6 15.7 14.4

Small Resources -35.4 -15.7 167.1 25.6 19.3 27.8 10.6

Source: IRESS, Macquarie Research, April 2016

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 6

Fig 7 Recovery in commodity prices +ve for Energy... Fig 8 ... and Materials too.

Source: IBES, Macquarie Research, April 2016

Energy & Materials

In general commodity prices held if not extended their recent run with oil significantly higher (WTI 14%),

LME metals had mixed performance over the month with copper +3% and tin +4% while others have gone

backwards. Other more notable outperformers include Steel (+19%) and Iron Ore (+10%). Precious

metals rose further in March carrying on with their early year momentum as the risk off trade continues.

Broadly speaking, (ex Energy) price trends were supported by continued USD weakness and signs that

Chinese growth momentum continues to improve (or at least is not getting worse) although specifically

this was not sufficient to offset individual metal demand/supply fundamentals which saw for instance

Aluminium, Lead and Nickel weaken over the month.

Over the quarter, it was more a case of two halves for most metals markets. A poor January, followed by a

sharp recovery in February which was sustained into March (link to our Commodities team’s note). The

best performer was Iron ore, which had a relatively weak start then surged notably to end the quarter up

24%. Crude oil also went through a roller coaster ride – down +20% YTD by mid Jan and (for WTI) hitting

a new low in mid Feb, before both Brent and WTI recovered thereafter, ending the quarter up 6% and 3%,

respectively. Within LME metals, tin was the best performer, +16% for the quarter followed by zinc up

12%. Copper was the other gainer, adding 3%. All three had been down more than 5% in early Jan but

staged a sharp recovery from Feb. Gold was a clear outperformer among the precious metals, gaining

17% over the quarter (best performance since 1986).

Among the Energy names, the outperformers were SXY (+60.5%), SEH (+44.4%) and AWE (+39.2%).

SEH has reported 2015 results which were below expectations but share price trended higher on growing

confidence on its resource base. On the other hand, CTX (-5%) was a major underperformer on the back

of weak refining margins and higher AUDUSD working against Lytton profitability.

In the Materials (+6.0%) space, standouts were FMG (+26.5%), S32 (+17.2%), BSL (13.3%), CSR

(11.5%) and BHP (+9.6%).

o FMG was a standout despite Moody’s credit rating downgrade - Moody’s downgraded FMG’s

credit rating by one notch from Ba2 to Ba3 and left the rating on negative outlook. The downgrade

implies that FMG will not make material debt reduction in the near term, even though Moody’s

expects FMG to maintain a solid liquidity profile and to be free cash flow positive in the forecast

period.

o The sector also saw a couple of resignations. RIO (+6.0%) announced that from 1 Jul-16 Sam

Walsh will step down as CEO (after three years in that position), and will be succeeded by Jean-

Sebastien Jacques (previously head of RIO’s Copper and Coal business). MRE sees Jacques’

appointment as a key indicator of RIO’s wish to move itself away from being so closely tied to iron

ore and push towards its copper aspirations. ILU (+0.3%) advised that MD and CEO David Robb

will leave the role in 2H16. The company has begun succession planning.

60.5

44.4

39.2

29.7

28.1

23.6

21.8

19.1

14.9

11.1

6.2

2.4

2.0

-5.0

-12.3

-12.4

-30 -10 10 30 50 70

SXY

SEH

AWE

PDN

WOR

BPT

STO

WHC

ORG

FAR

Energy

WPL

OSH

CTX

KAR

LNG

Energy sector total return (%), March

26.5

17.2

13.3

11.5

9.7

9.6

9.6

7.9

6.0

6.0

5.8

5.5

2.4

0.3

-0.3

-1.5

-3.1

-3.8

-10 -5 0 5 10 15 20 25 30

FMG

S32

BSL

CSR

BHP

ORA

IPL

ORI

Materials

RIO

BLD

ABC

AMC

ILU

JHX

AWC

NCM

DLX

Materials sector total return (%), March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 7

o ORI (+7.9%) announced changes in segment reporting which reflect the company’s new

operating model that moves to a more regional structure (whereby regions are accountable for

service delivery, operational & financial performance). The effect of these changes is that

Australian profits fall pre and post, due to inclusion of loss-making Indonesian business, cyanide

exports allocated to offshore and higher attributable support costs. North American and LatAm

EBIT increases mainly due to inclusion of Hub profits as does Europe/Africa, which now includes

Asia (ex Indo) and relevant cyanide earnings.

ORI is doing what it can in terms of self-help initiatives (with net $60m of transformation benefits

targeted in FY16) and has a good geographic and end-market diversity. The company did not

provide any update to guidance or any trading update - this implies that existing guidance (for

modest EBIT growth) still stands.

o DLX (-3.8%) was the key underperformer. Sherwin-Williams announced a bid for Valspar, which

has potential to disrupt the Australian paint market in time. The US$113 per share (or

US$11.3bn) all-cash offer has been approved by both companies' Boards. MRE analysts note

that this is not a positive development for DLX but also not one that will impact immediately.

Fig 9 TOX a standout in Commercial Services Fig 10 Traffic not enough to drive Transportation

Source: IBES, Macquarie Research, April 2016

Industrials

A positive month for Commercial Services (+2.2 %), although the sector underperformed the market, led

by TOX (+25.8%), DOW (+15.3%), SIQ (+15.0%), MMS (+14.0%), PRG (+13.0%) and CAB (+12.8%).

o TOX (A$3.00, OP, TP A$3.45) announced its intention to acquire Worth recycling for $70m

(funding with $24m in equity and $46m in debt - at a 5.4x EBITDA acquisition multiple, in line with

its recent large acquisition). Worth, a NSW-based liquid waste and industrial services business,

appears to be a good fit for TOX, operating in similar business lines and further geographically

diversifying the business. The acquisition is expected to settle in Mar-16 and be 13% EPS

accretive on a FY16E pro forma basis.

o DOW (+15.3%) had a good run in March similar to broader contractors/resources sector. The

company is currently trading at a ~33% PER discount to the market (source FactSet), which

compares with its 10-year average of 25% discount. There is an upcoming potentially positive

catalyst re NSW Intercity trains which is expected in Apr-16 (DOW is 1 of 4 bidders), although it is

also twin-edged with $10-15m of bid costs if unsuccessful.

o Underperformers for the month were CLH (-10.5%), CWY (-5.1%), IPH (-3.7%), SGF (-1.9%) and

BXB (-1.8%).

25.8

15.3

15.0

14.0

13.0

12.8

10.4

8.8

7.5

7.3

4.3

4.3

2.6

2.5

2.2

-1.8

-1.9

-3.7

-5.1

-10.5

-15 -10 -5 0 5 10 15 20 25 30

TOX

DOW

SIQ

MMS

PRG

CAB

REC

CCP

SPO

ALQ

MIN

SEK

BRS

SAI

Commerical Services

BXB

SGF

IPH

CWY

CLH

Commercial Services sector total return (%), March

30.0

6.3

5.4

4.0

3.7

3.6

1.6

1.0

0.0

-2.7

-10 -5 0 5 10 15 20 25 30 35

MRM

QUB

QAN

AIA

SYD

MQA

Transportation

AIO

TCL

AZJ

Transport sector total return (%), March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 8

Transport (+1.6%) underperformed the market this month, dragged lower by AZJ (-2.7%). Key sector

outperformers included MRM (+30.0%), QAN (+5.4%), AIA (+4.0%), SYD (+3.7%) and MQA (+3.6%).

SYD’s outperformance captures the company’s near-term earnings surge. The company reported its

February traffic numbers this month - traffic growth is well above trend growth of 3-5% internationally

(China is a key driver with US, Japan, Korea and Europe all strong performers also); capacity growth of

~10-11% is still forecast over the coming two quarters; and domestic growth of ~4% is an added bonus.

Fig 11 Retail continues to shine Fig 12 A positive surprise from Media

Source: IBES, Macquarie Research, April 2016

Consumer Discretionary

Retail (+5.6%) outperformed the market this month, continuing to benefit from the uptick in consumer

sentiment and favourable retail trading conditions despite the mid-month political uncertainty. Stand-out

performers included:

o PMV (+28.4%) reported 1H16 Retail EBIT $90.7m (vs. MRE forecasts of $77m) and NPAT

$71.5m (vs. MRE forecasts $63.3m). All Smiggle regions reported strong, positive LFL sales.

Smiggle UK continues to trade ahead of management expectations and PMV has upgraded its

store rollout target. Portmans also delivered a positive surprise (total sales growth of +19%),

attributable to solid product execution from the recently installed merchandise team.

o KMD (+6.0%) reported 1H16 NPAT of $9.4m at the top end of guidance, showing good

improvement in both sales (total sales +9.3%) and margins (EBITDA +222% and gross margins

expansion of 350bp to 62.8%). Management confirmed they remain committed to the previous

NPAT forecast of $30.2m and the focus remains on leveraging existing assets in Australasia and

employing a capital light expansion model in international markets.

o Other key positive contributors for the month included PBG (+14.9%), AMA (+13.5%), RCG

(+9.0%), SUL (+7.6%) and JBH (+6.6%)

o MYR (+3.5%) underperformed the sector despite a positive 1H16 result but managed to stay in

positive territory. The company reported 1H16 NPAT of $59.7m and FY16 guidance was

tightened to the upper end of the range to $66-72m (previously $64-72m). While guidance is

based on the expectation that there will not be significant deterioration in consumer sentiment,

the challenge remains with the execution in store and further network rationalisation (particularly

as DJs and speciality retailers continue to aggressively roll out stores and take market share).

1H16 dividend payout ratio reduced to 50-60% NPAT (previously 70-80% NPAT) vs. MRE

forecast of no dividend.

o The sector was pulled back by ADH (-5.2%), HVN (-1.7%) and BAP (-0.9%).

28.4

14.9

13.5

9.0

7.6

6.6

6.0

5.6

5.4

4.5

3.5

3.1

2.9

2.5

0.8

-0.9

-1.7

-5.2

-10 -5 0 5 10 15 20 25 30 35

PMV

PBG

AMA

RCG

SUL

JBH

KMD

Retail

WEB

TRS

MYR

AHG

CCV

TGA

TME

BAP

HVN

ADH

Retail sector total return (%), March

19.4

14.3

12.0

9.7

9.2

8.6

8.2

8.0

7.6

5.5

4.7

2.3

0.2

-1.5

-5.0

-10 -5 0 5 10 15 20 25

SKT

FXJ

SGN

NEC

APN

SWM

Media

APO

NWS

OML

REA

SXL

VRL

TEN

PRT

Media sector total return (%), March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 9

Media

A solid month for Media (+8.2%) led by SKT (+19.4%), FXJ (+14.3%), SGN (+12.0%), NEC (+9.7%), APN

(+9.2%) and SWM (+8.6%). While timing remains uncertain, momentum behind media ownership

reforms continued with legislation now tabled in Parliament and currently being reviewed by a

Senate Committee that will report back on 12 May. Accordingly, positioning by media companies

continued, with NEC announcing the acquisition of a 9.99% stake in Southern Cross Media Group at

$1.15/sh. Negative contributors for the month were PRT (-5.0%) and TEN (-1.5%).

Fig 13 Consumer Services trade in line with market Fig 14 ACX expansion in Europe, drives IT sector

Source: IBES, Macquarie Research, April 2016

Consumer Services (+4.2%) performed in line with the market, with the sector’s positive return driven by

RFG (+22.7%), AAD (+15.4%), GEM (+12.3%), SKC (+11.5%), CWN (+10.1%), CTD (+9.9%), SGR

(+8.8%), NVT (+8.3%), MTR (+7.1%) and FLT (+5.9%).

o AAD (15.3%) announced strategic initiatives including selling Marinas (which comprises seven

marinas and >1,300 berths) and the relocation of capital to Main Event. Following the sale, ASAS

expects to roll out 11 Main Event sites in FY17 vs previous guidance of eight.

o Negative contributors for the month were TTS (-2.8%), DMP (-2.2%) and TAH (-0.5%).

Information Technology

The outperformance of the IT (+5.7%) sector was predominantly attributable to the strong performance of

ACX (+27.1%).

o ACX (A$6.22, OP, TP A$6.60) announced the acquisition of CONJECT, a cloud and mobile

collaboration service provider in Europe, for $93m, funded by a fully underwritten placement to

raise A$120m. The acquisition is in line with the company’s strategy to consolidate its leadership

position in Europe and gives ACX a leading market share in Germany and the UK, with improved

entry points into France and Russia.

o Other corporate action in the sector was announced by CAR (+2.5%) (A$11.60, OP, TP

A$12.05). The company acquired an 83% stake in Chile’s leading automotive classified portal,

Chileautos, for US$15m (funded by cash and debt). The stake adds to CAR’s existing regional

interests and its investment in another market further indicates its willingness to look offshore to

develop potential longer-term growth drivers. The acquisition is expected to be EPS-accretive in

the first year of ownership and make a small positive contribution to EBITDA. Carsales holds an

option to acquire the remaining 17% stake from the existing owners at any point over the next

four years.

22.7

15.4

12.3

11.5

10.1

9.9

8.8

8.3

7.1

5.9

4.2

3.0

2.4

-0.5

-2.2

-2.8

-5 0 5 10 15 20 25

RFG

AAD

GEM

SKC

CWN

CTD

SGR

NVT

MTR

FLT

Consumer Services

ALL

IVC

TAH

DMP

TTS

Consumer Services sector total return (%), March

27.1

10.5

9.9

8.5

7.8

7.5

7.0

7.0

5.7

4.1

3.2

2.6

2.5

-0.1

-1.0

-1.2

-9.2

-51.8

-60 -50 -40 -30 -20 -10 0 10 20 30 40

ACX

IRE

MYO

IFM

NXT

CPU

HSN

ALU

IT

RKN

GBT

TNE

CAR

ISD

SMX

LNK

CSV

1PG

IT sector total return (%), March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 10

o Other positive contributors to the sector included IRE (+10.5%), MYO (+9.9%), IFM (+8.5%), NXT

(+7.8%), CPU (+7.5%), HSN (+7.0%), and ALU (+7.0%).

Fig 15 Both Majors & Regionals deliver +ve returns Fig 16 Blue sky for Div Financials

Source: IBES, Macquarie Research, April 2016

Financials

Banks (+6.5%) outperformed with both major and regionals helping overturn last month’s losses. Key

performers included BOQ (+14.9%), GMA (+14.7%), CYB (+8.5%), NAB (+8.5%), BEN (+7.6%) and CBA

(+6.8%). ANZ (+4.7%) underperformed the sector after providing an update on its credit impairment

guidance for 1H16 to be “at least $100m” above its earlier guidance of ~$800m (which equates to ~1% of

MRE FY16 earnings expectations). ANZ highlighted that the downgrade had been driven by a small

number of Australian and multi-national resources related exposures. This announcement suggests that

the deterioration ANZ has seen is likely to have implications for the banking sector.

In March, the Basel Committee also released a consultation paper on potential changes to the advanced

internal ratings based (A-IRB) approach. Overall, the announcement was broadly neutral to positive for

the majors, given no material adverse changes. APRA's Insights - Issue 1 for 2016 highlighted that the

time frame to build capital levels is seemingly extended... "APRA’s domestic consultation is unlikely to

begin before 2017, with local implementation of these reforms following over a number of years."

In the Div Financials (+4.5%), BLA (+21.5%) announced the agreement between Blue Sky Private Real

Estate (a division of BLA) and a subsidiary of Goldman Sachs Group, to establish a new student

accommodation joint venture in Australia and New Zealand. The company is targeting a portfolio between

5,000-10,000 beds that is expected to represent a total end value of ~$750m-$1.5bn in fee earning assets

under management for BLA in the student accommodation sector.

Other outperformers in the sector included FXL (+12.0%), CGF (11.6%), IMF (+10.3%), IFL (+9.6%), ECX

(+8.2%) and PPT (+8.1%). Underperformers for the month included PAC (-11.2%), HFA (-0.1%), ASX

(+0.9%), MQg (+2.8%) and MFG (+3.4%).

14.9

14.7

8.5

8.5

7.6

6.8

6.5

5.6

5.4

4.7

0 2 4 6 8 10 12 14 16

BOQ

GMA

CYB

NAB

BEN

CBA

Banks

WBC

MOC

ANZ

Banks sector total return (%), March

21.5

12.0

11.6

10.3

9.6

9.6

8.2

8.1

6.5

6.1

6.0

4.5

3.4

2.8

0.9

-0.1

-11.2

-20 -15 -10 -5 0 5 10 15 20 25

BLA

FXL

CGF

IMF

IFL

PTM

ECX

PPT

HGG

BTT

OFX

Div. Financials

MFG

MQG

ASX

HFA

PAC

Div Fins sector total return (%), March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 11

Fig 17 A solid month for Insurance Fig 18 REITs underperform the market

Source: IBES, Macquarie Research, April 2016

Insurance (+9.2%) performed strongly, led by MPL (+18.3%), AMP (+11.5%), NGF (+10.2%) and SDF

(+9.6%). MPL’s outperformance was on the back of its claims growth moderation improving gross margin

and profitability in 1H16 (the sector ex MPL has not seen the same positive trends). Our Insurance team

attributed the moderation in MPL’s claims growth to a combination of (i) increased health fund analytics re

product entitlements (inclu. Fraud detection), (ii) increased exclusions, (iii) improved hospital contracting,

and (iv) switching of adverse risks away from MPL. The company also announced appointed Craig

Drummond as MD and CEO (effective 4 Jul-16).

REITS (+2.8/%) underperformed the market in March. CQR (+6.5%) and LLC (+6.4%) were standout

performers, and other positive contributors were AOG (+5.7%), BWP (+5.6%), IOF (5.5%), CHC (+5.2%)

and CMW (+4.5%). Key negative contributors during March included GTY (-0.6%) and WFD (-0.1%).

Consistent with expectations, MYR announced its intention to close its stores in Brookside, QLD (the

lease due to expire in Sep-16 and trading expected to close in Jan-17). Our REITs team remains cautious

on the retail sector in Australia. Preferences in the REIT sector remain WFD (A$9.76, OP, TP A$11.79),

GMG (A$6.59, OP, TP A$7.06) and CHC (A$4.55, OP, TP A$4.99).

Fig 19 Regulations hurt Health Care Fig 20 Another Staples underperformance

Source: IBES, Macquarie Research, April 2016

18.3

11.5

10.2

9.6

9.2

7.9

6.3

6.1

2.0

0 5 10 15 20

MPL

AMP

NHF

SDF

Insurance

IAG

SUN

QBE

CVO

Insurance sector total return (%), March

6.5

6.4

5.7

5.7

5.6

5.5

5.4

5.2

4.5

2.8

2.8

2.8

2.6

2.5

2.42.3

1.6

1.6

0.9

-0.1

-0.6

-2 -1 0 1 2 3 4 5 6 7

CQR

LLC

MGR

AOG

BWP

IOF

DXS

CHC

CMW

REITs

GMG

ABP

VCX

NSR

SGP

GOZ

GPT

SCG

SCP

WFD

GTY

REITs sector total return (%), March

27.7

19.3

9.2

8.7

7.5

6.5

3.8

1.2

0.9

0.8

0.6

0.5

0.5

0.3

-0.4

-1.3

-6.7

-8.2

-15 -10 -5 0 5 10 15 20 25 30

SIP

PRY

FPH

HSO

NAN

VRT

SHL

EHE

COH

Healthcare

IPD

ANN

API

JHC

GXL

REG

RHC

RMD

Healthcare sector total return (%), March

8.3

6.2

6.0

3.9

3.9

3.0

1.8

1.4

1.4

0.7

-1.6

-3.9

-4.7

-5.1

-8 -6 -4 -2 0 2 4 6 8 10

AAC

CGC

WES

MTS

CCL

Consumer Staples

BGA

TGR

SHV

TWE

WOW

GNC

RIC

BAL

Consumer Staples sector total return (%), March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 12

Healthcare & Consumer Staples

Weakness amongst Healthcare (+0.8%) was led by RMD (-8.2%), RHC (-6.7%) and REG (-1.3%). The

Department of Social Services (DSS) announced the allocation of bed licenses as part of the 2015 Aged

Care Approvals Round. While the announcement was a good result for both REG (-1.3%) and JHC

(+0.3%), being consequently awarded new licenses equivalent to 14% and 8% of current operating

places, respectively, it was not enough to keep their share prices afloat. The announcement was a less

positive outcome for EHE (+1.2%), with the company receiving only 12 new licences (for its Kadina facility

in South Australia).

PRY (+19.3%) (A$3.74, N, TP A$2.75) performed strongly, announcing the sale of its Medical Director

division to private equity company Affinity Partners for $155m, representing a forward multiple of ~8.2x

EBITDA and ~11.4x EBIT. Whilst the transaction will drive earnings downgrades and only has a relatively

modest impact on its gearing, MRE sees it as a good strategic move (the business has been struggling in

recent years) for helping PRY drive focus on its core operations and reducing debt.

Other positive contributors included SIP (+27.7%), FPH (+9.2%) and HSO (+8.7%).

Consumer Staples (+3.0%) underperformed the market, as investors continue to face a long

supermarket turnaround ahead (with increased competition and benign inflation keeping margins

compressed). The sector was predominantly dragged down by BAL (-5.1%), RIC (-4.7%), and WOW

(-1.6%). AAC (+8.3%), CGC (+6.2%), WES (+6.0%), MTS (+3.9%) and CCL (+3.9%) were the only sector

outperformers for the month.

Fig 21 TPM pulls Telcos up Fig 22 Utilities stay relatively flat

Source: IBES, Macquarie Research, April 2016

Utilities & Telco

Utilities (+1.3%) were relatively flat despite strong returns from EWC (+33.3%) and IFN (+30.0%).

AGL (0.3%) announced the sale of Diamantina PS for $151m, marginally above book value, to APA. The

sale is consistent with the $1bn divestment target (with the sale of the solar farm to PARF, AGL will have

reached its target of ~$1bn with the three assets Macarthur WF, Diamantina and PARF).

APA (1.0%) consequently acquired the residual interest in Diamantina PS for $151m and has lifted

EBITDA guidance to $1,300-1,325m (previously $1,275-1,300m). The acquisition is a 15-year investment

with an option for some level of extension longer-term, as Mt Isa will continue to need power irrespective

of whether the mines are continuing. The value-add APA gets is that it can replace project finance debt

with group debt at materially lower rates and defer debt amortisation until the end of the project life. The

approach is similar to QCLNG.

The positive announcement was not enough, however, to see AGL and APA outperform the sector.

8.0

7.6

5.4

4.7

4.5

2.7

2.3

-1.5

-4 -2 0 2 4 6 8 10

TPM

SPK

SDA

Telcos

TLS

VOC

CNU

AYS

Telcos sector total return (%), March

33.3

30.0

1.9

1.7

1.3

1.0

0.4

0.3

-0.7

-4 1 6 11 16 21 26 31 36

EWC

IFN

SKI

AST

Utilities

APA

DUE

AGL

EPW

Utilities sector total return (%), March

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 13

In the telecoms (+4.7 %) sector, TPM (+8.0%) outperformed after announcing a solid 1H result and

strong momentum from iiNet cost-out, which is expected to drive earnings over the medium term. The

company reported 1H16 EBITDA of $368.8, up 56% on pcp (due in part to the iiNet acquisition and its

cost synergies) and ~2% ahead of MRE estimates. An interim dividend of 7cps was declared, up 27%.

Positive returns were also delivered by SPK (+7.6%) and SDA (+5.4%).

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 14

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand Outperform – return >3% in excess of benchmark return Neutral – return within 3% of benchmark return Underperform – return >3% below benchmark return Benchmark return is determined by long term nominal GDP growth plus 12 month forward market dividend yield

Macquarie – Asia/Europe Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie – South Africa Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie - Canada Outperform – return >5% in excess of benchmark return Neutral – return within 5% of benchmark return Underperform – return >5% below benchmark return

Macquarie - USA Outperform (Buy) – return >5% in excess of Russell 3000 index return Neutral (Hold) – return within 5% of Russell 3000 index return Underperform (Sell)– return >5% below Russell 3000 index return

Volatility index definition*

This is calculated from the volatility of historical price movements. Very high–highest risk – Stock should be expected to move up or down 60–100% in a year – investors should be aware this stock is highly speculative. High – stock should be expected to move up or down at least 40–60% in a year – investors should be aware this stock could be speculative. Medium – stock should be expected to move up or down at least 30–40% in a year. Low–medium – stock should be expected to move up or down at least 25–30% in a year. Low – stock should be expected to move up or down at least 15–25% in a year. * Applicable to Asia/Australian/NZ/Canada stocks only

Recommendations – 12 months Note: Quant recommendations may differ from Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following adjustments made: Added back: goodwill amortisation, provision for catastrophe reserves, IFRS derivatives & hedging, IFRS impairments & IFRS interest expense Excluded: non recurring items, asset revals, property revals, appraisal value uplift, preference dividends & minority interests EPS = adjusted net profit / efpowa* ROA = adjusted ebit / average total assets ROA Banks/Insurance = adjusted net profit /average total assets ROE = adjusted net profit / average shareholders funds Gross cashflow = adjusted net profit + depreciation *equivalent fully paid ordinary weighted average number of shares All Reported numbers for Australian/NZ listed stocks are modelled under IFRS (International Financial Reporting Standards).

Recommendation proportions – For quarter ending 31 December 2015

AU/NZ Asia RSA USA CA EUR Outperform 50.68% 61.04% 53.16% 47.90% 65.22% 43.59% (for global coverage by Macquarie, 5.33% of stocks followed are investment banking clients)

Neutral 31.51% 24.66% 34.18% 47.70% 29.71% 34.62% (for global coverage by Macquarie, 5.02% of stocks followed are investment banking clients)

Underperform 17.81% 14.30% 12.66% 4.39% 5.07% 21.79% (for global coverage by Macquarie, 3.78% of stocks followed are investment banking clients)

Company-specific disclosures: Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures.

Analyst certification: We hereby certify that all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. The Analysts responsible for preparing this report receive compensation from Macquarie that is based upon various factors including Macquarie Group Limited (MGL) total revenues, a portion of which are generated by Macquarie Group’s Investment Banking activities. General disclosure: This research has been issued by Macquarie Securities (Australia) Limited ABN 58 002 832 126, AFSL 238947, a Participant of the ASX and Chi-X Australia Pty Limited. This research is distributed in Australia by Macquarie Wealth Management, a division of Macquarie Equities Limited ABN 41 002 574 923 AFSL 237504 ("MEL"), a Participant of the ASX, and in New Zealand by Macquarie Equities New Zealand Limited (“MENZ”) an NZX Firm. Macquarie Private Wealth’s services in New Zealand are provided by MENZ. Macquarie Bank Limited (ABN 46 008 583 542, AFSL No. 237502) (“MBL”) is a company incorporated in Australia and authorised under the Banking Act 1959 (Australia) to conduct banking business in Australia. None of MBL, MGL or MENZ is registered as a bank in New Zealand by the Reserve Bank of New Zealand under the Reserve Bank of New Zealand Act 1989. Apart from Macquarie Bank Limited ABN 46 008 583 542 (MBL), any MGL subsidiary noted in this research, , is not an authorised deposit-taking institution for the purposes of the Banking Act 1959 (Australia) and that subsidiary’s obligations do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of that subsidiary, unless noted otherwise. This research contains general advice and does not take account of your objectives, financial situation or needs. Before acting on this general advice, you should consider the appropriateness of the advice having regard to your situation. We recommend you obtain financial, legal and taxation advice before making any financial investment decision. This research has been prepared for the use of the clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient, you must not use or disclose this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. This research is based on information obtained from sources believed to be reliable, but the Macquarie Group does not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. The Macquarie Group accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. The Macquarie Group produces a variety of research products, recommendations contained in one type of research product may differ from recommendations contained in other types of research. The Macquarie Group has established and implemented a conflicts policy at group level, which may be revised and updated from time to time, pursuant to regulatory requirements; which sets out how we must seek to identify and manage all material conflicts of interest. The Macquarie Group, its officers and employees may have conflicting roles in the financial products referred to in this research and, as such, may effect transactions which are not consistent with the recommendations (if any) in this research. The Macquarie Group may receive fees, brokerage or commissions for acting in those capacities and the reader should assume that this is the case. The Macquarie Group‘s employees or officers may provide oral or written opinions to its clients which are contrary to the opinions expressed in this research. Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures © Macquarie Group

Macquarie Wealth Management Australian Equity Strategy

4 April 2016 15