Aswath Damodaran - stern.nyu.eduadamodar/podcasts/cfUGspr16/Session15.pdf · higher NPV ¤ Compute...

40

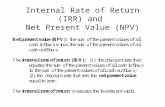

Will the benefits persist if investors hedge the risk instead of the firm? No Yes No Yes Can marginal investors hedge this risk cheaper than the firm can? No Yes Is there a significant benefit in terms of higher expected cash flows or a lower discount rate? No Yes Is there a significant benefit in terms of higher cash flows or a lower discount rate? What is the cost to the firm of hedging this risk? Negligible High Do not hedge this risk. The benefits are small relative to costs Hedge this risk. The benefits to the firm will exceed the costs Hedge this risk. The benefits to the firm will exceed the costs Let the risk pass through to investors and let them hedge the risk. Hedge this risk. The benefits to the firm will exceed the costs Indifferent to hedging risk Cash flow benefits - Tax benefits - Better project choices Discount rate benefits - Hedge "macro" risks (cost of equity) - Reduce default risk (cost of debt or debt ratio) Survival benefits (truncation risk) - Protect against catastrophic risk - Reduce default risk Value Trade Off Earnings Multiple - Effect on multiple Earnings - Level - Volatility X Pricing Trade Aswath Damodaran 264

Transcript of Aswath Damodaran - stern.nyu.eduadamodar/podcasts/cfUGspr16/Session15.pdf · higher NPV ¤ Compute...

Will the benefits persist if investors hedge the risk instead of the firm?

NoYes

NoYes

Can marginal investors hedge this risk cheaper

than the firm can?

NoYes

Is there a significant benefit in terms of higher expected cash flows or a lower discount rate?

NoYes

Is there a significant benefit in terms of higher cash flows or a lower discount rate?

What is the cost to the firm of hedging this risk?

Negligible High

Do not hedge this risk. The benefits are small relative to costs

Hedge this risk. The benefits to the firm will exceed the costs

Hedge this risk. The benefits to the firm will exceed the costs

Let the risk pass through to investors and let them hedge the risk.

Hedge this risk. The benefits to the firm will exceed the costs

Indifferent to hedging risk

Cash flow benefits- Tax benefits- Better project choices

Discount rate benefits- Hedge "macro" risks (cost of equity)- Reduce default risk (cost of debt or debt ratio)

Survival benefits (truncation risk)- Protect against catastrophic risk- Reduce default risk

Value Trade Off

Earnings Multiple- Effect on multiple

Earnings- Level- Volatility

X

Pricing Trade

AswathDamodaran264

265

AcquisitionsandProjects

AswathDamodaran

265

¨ Anacquisitionisaninvestment/projectlikeanyotherandalloftherulesthatapplytotraditionalinvestmentsshouldapplytoacquisitionsaswell.Inotherwords,foranacquisitiontomakesense:¤ ItshouldhavepositiveNPV.Thepresentvalueoftheexpectedcashflows

fromtheacquisitionshouldexceedthepricepaidontheacquisition.¤ TheIRRofthecashflowstothefirm(equity)fromtheacquisition>Costof

capital(equity)ontheacquisition¨ Inestimatingthecashflowsontheacquisition,weshouldcountin

anypossiblecashflowsfromsynergy.¨ Thediscountratetoassessthepresentvalueshouldbebasedupon

theriskoftheinvestment(targetcompany)andnottheentityconsideringtheinvestment(acquiringcompany).

266

TataMotorsandHarmanInternational

AswathDamodaran

266

¨ HarmanInternationalisapubliclytradedUSfirmthatmanufactureshighendaudioequipment.TataMotorsisanautomobilecompany,basedinIndia.

¨ TataMotorsisconsideringanacquisitionofHarman,withaneyeonusingitsaudioequipmentinitsIndianautomobiles,asoptionalupgradesonnewcars.

267

EstimatingtheCostofCapitalfortheAcquisition(nosynergy)

AswathDamodaran

267

1. Currency:EstimatedinUS$,sincecashflowswillbeestimatedinUS$.2. Beta:HarmanInternationalisanelectroniccompanyandweusetheunleveredbeta

(1.17)ofelectronicscompaniesintheUS.3. EquityRiskPremium:ComputedbasedonHarman’soperatingexposure:

4. Debtratio&costofdebt:TataMotorsplanstoassumetheexistingdebtofHarmanInternationalandtopreserveHarman’sexistingdebtratio.Harmancurrentlyhasadebt(includingleasecommitments)tocapitalratioof7.39%(translatingintoadebttoequityratioof7.98%)andfacesapre-taxcostofdebtof4.75%(basedonitsBBB- rating).

LeveredBeta=1.17(1+(1-.40)(.0798))=1.226CostofEquity=2.75%+1.226(6.13%)=10.26%

CostofCapital=10.26%(1-.0739)+4.75%(1-.40)(.0739)=9.67%

268

EstimatingCashflows- FirstSteps

AswathDamodaran

268

¨ OperatingIncome:Thefirmreportedoperatingincomeof$201.25milliononrevenuesof$4.30billionfortheyear.Addingbacknon-recurringexpenses(restructuringchargeof$83.2millionin2013)andadjustingincomefortheconversionofoperatingleasecommitmentstodebt,weestimatedanadjustedoperatingincomeof$313.2million.Thefirmpaid18.21%ofitsincomeastaxesin2013andwewillusethisastheeffectivetaxrateforthecashflows.

¨ Reinvestment:Depreciationin2013amountedto$128.2million,whereascapitalexpendituresandacquisitionsfortheyearwere$206.4million.Non-cashworkingcapitalincreasedby$272.6millionduring2013butwas13.54%ofrevenuesin2013.

269

Bringingingrowth

¨ WewillassumethatHarmanInternationalisamaturefirm,growing2.75%inperpetuity.

¨ Weassumethatrevenues,operatingincome,capitalexpendituresanddepreciationwillallgrow2.75%fortheyearandthatthenon-cashworkingcapitalremain13.54%ofrevenuesinfutureperiods.

AswathDamodaran

269

270

ValueofHarmanInternational:BeforeSynergy

AswathDamodaran

270

¨ Earlier,weestimatedthecostofcapitalof9.67%astherightdiscountratetoapplyinvaluingHarmanInternationalandthecashflowtothefirmof$166.85millionfor2014(nextyear),assuminga2.75%growthrateinrevenues,operatingincome,depreciation,capitalexpendituresandtotalnon-cashworkingcapital.Wealsoassumedthatthesecashflowswouldcontinuetogrow2.75%ayearinperpetuity.

¨ Addingthecashbalanceofthefirm($515million)andsubtractingouttheexistingdebt($313million,includingthedebtvalueofleases)yieldsthevalueofequity inthefirm:

¨ ValueofEquity =ValueofOperatingAssets+Cash– Debt

=$2,476+$515- $313million=$2,678million

¨ ThemarketvalueofequityinHarmaninNovember2013was$5,428million.

¨ TotheextentthatTataMotorspaysthemarketprice,itwillhavetogeneratebenefitsfromsynergythatexceed$2750million.

MeasuringInvestmentReturnsII.InvestmentInteractions,OptionsandRemorse…

Lifeistooshortforregrets,right?

AswathDamodaran 271

272

Independentinvestmentsaretheexception…

AswathDamodaran

272

¨ Inalloftheexampleswehaveusedsofar,theinvestmentsthatwehaveanalyzedhavestoodalone.Thus,ourjobwasasimpleone.Assesstheexpectedcashflowsontheinvestmentanddiscountthemattherightdiscountrate.

¨ Intherealworld,mostinvestmentsarenotindependent.Takinganinvestmentcanoftenmeanrejectinganotherinvestmentatoneextreme(mutuallyexclusive)tobeinglockedintotakeaninvestmentinthefuture(pre-requisite).

¨ Moregenerally,acceptinganinvestmentcancreatesidecostsforafirm’sexistinginvestmentsinsomecasesandbenefitsforothers.

273

I.MutuallyExclusiveInvestments

AswathDamodaran

273

¨ Wehavelookedathowbesttoassessastand-aloneinvestmentandconcludedthatagoodinvestmentwillhavepositiveNPVandgenerateaccountingreturns(ROCandROE)andIRRthatexceedyourcosts(capitalandequity).

¨ Insomecases,though,firmsmayhavetochoosebetweeninvestmentsbecause¤ Theyaremutuallyexclusive:Takingoneinvestmentmakestheother

oneredundantbecausetheybothservethesamepurpose¤ Thefirmhaslimitedcapitalandcannottakeeverygoodinvestment

(i.e.,investmentswithpositiveNPVorhighIRR).¨ Usingthetwostandarddiscountedcashflowmeasures,NPV

andIRR,canyielddifferentchoiceswhenchoosingbetweeninvestments.

274

ComparingProjectswiththesame(orsimilar)lives..

AswathDamodaran

274

¨ Whencomparingandchoosingbetweeninvestmentswiththesamelives,wecan¤ Computetheaccountingreturns(ROC,ROE)oftheinvestmentsandpicktheonewiththehigherreturns

¤ ComputetheNPVoftheinvestmentsandpicktheonewiththehigherNPV

¤ ComputetheIRRoftheinvestmentsandpicktheonewiththehigherIRR

¨ Whileitiseasytoseewhyaccountingreturnmeasurescangivedifferentrankings(andchoices)thanthediscountedcashflowapproaches,youwouldexpectNPVandIRRtoyieldconsistentresultssincetheyarebothtime-weighted,incrementalcashflowreturnmeasures.

275

Case1:IRRversusNPV

AswathDamodaran

275

¨ Considertwoprojectswiththefollowingcashflows:Year Project1CF Project2CF0 -1000 -10001 800 2002 1000 3003 1300 4004 -2200 500

276

Project’sNPVProfile

AswathDamodaran

276

277

Whatdowedonow?

AswathDamodaran

277

¨ Project1hastwointernalratesofreturn.Thefirstis6.60%,whereasthesecondis36.55%.Project2hasoneinternalrateofreturn,about12.8%.

¨ Whyaretheretwointernalratesofreturnonproject1?

¨ Ifyourcostofcapitalis12%,whichinvestmentwouldyouaccept?a. Project1b. Project2

¨ Explain.

278

Case2:NPVversusIRR

AswathDamodaran

278

Cash Flow

Investment

$ 350,000

$ 1,000,000

Project A

Cash Flow

Investment

Project B

NPV = $467,937IRR= 33.66%

$ 450,000 $ 600,000 $ 750,000

NPV = $1,358,664IRR=20.88%

$ 10,000,000

$ 3,000,000 $ 3,500,000 $ 4,500,000 $ 5,500,000

279

Whichonewouldyoupick?

AswathDamodaran

279

¨ Assumethatyoucanpickonlyoneofthesetwoprojects.YourchoicewillclearlyvarydependinguponwhetheryoulookatNPVorIRR.Youhaveenoughmoneycurrentlyonhandtotakeeither.Whichonewouldyoupick?a. ProjectA.Itgivesmethebiggerbangforthebuckandmore

marginforerror.b. ProjectB.Itcreatesmoredollarvalueinmybusiness.

¨ IfyoupickA,whatwouldyourbiggestconcernbe?

¨ IfyoupickB,whatwouldyourbiggestconcernbe?

280

CapitalRationing,UncertaintyandChoosingaRule

AswathDamodaran

280

¨ Ifabusinesshaslimitedaccesstocapital,hasastreamofsurplusvalueprojectsandfacesmoreuncertaintyinitsprojectcashflows,itismuchmorelikelytouseIRRasitsdecisionrule.¤ Small,high-growthcompaniesandprivatebusinessesaremuchmorelikelytouseIRR.

¨ Ifabusinesshassubstantialfundsonhand,accesstocapital,limitedsurplusvalueprojects,andmorecertaintyonitsprojectcashflows,itismuchmorelikelytouseNPVasitsdecisionrule.

¨ Asfirmsgopublicandgrow,theyaremuchmorelikelytogainfromusingNPV.

281

Thesourcesofcapitalrationing…

AswathDamodaran

281

Cause Number of firms Percent of total Debt limit imposed by outside agreement 10 10.7 Debt limit placed by management external to firm

3 3.2

Limit placed on borrowing by internal management

65 69.1

Restrictive policy imposed on retained earnings

2 2.1

Maintenance of target EPS or PE ratio 14 14.9

282

AnAlternativetoIRRwithCapitalRationing

AswathDamodaran

282

¨ TheproblemwiththeNPVrule,whenthereiscapitalrationing,isthatitisadollarvalue.Itmeasuressuccessinabsoluteterms.

¨ TheNPVcanbeconvertedintoarelativemeasurebydividingbytheinitialinvestment.Thisiscalledtheprofitabilityindex.¤ ProfitabilityIndex(PI)=NPV/InitialInvestment

¨ Intheexampledescribed,thePIofthetwoprojectswouldhavebeen:¤ PIofProjectA=$467,937/1,000,000 =46.79%¤ PIofProjectB=$1,358,664/10,000,000 =13.59%¤ ProjectAwouldhavescoredhigher.

283

Case3:NPVversusIRR

AswathDamodaran

283

Cash Flow

Investment

$ 5,000,000

$ 10,000,000

Project A

Cash Flow

Investment

Project B

NPV = $1,191,712IRR=21.41%

$ 4,000,000 $ 3,200,000 $ 3,000,000

NPV = $1,358,664IRR=20.88%

$ 10,000,000

$ 3,000,000 $ 3,500,000 $ 4,500,000 $ 5,500,000

284

Whythedifference?

AswathDamodaran

284

¨ Theseprojectsareofthesamescale.BoththeNPVandIRRusetime-weightedcashflows.Yet,therankingsaredifferent.Why?

¨ Whichonewouldyoupick?a. ProjectA.Itgivesmethebiggerbangforthebuckand

moremarginforerror.b. ProjectB.Itcreatesmoredollarvalueinmybusiness.

285

NPV,IRRandtheReinvestmentRateAssumption

AswathDamodaran

285

¨ TheNPVruleassumesthatintermediatecashflowsontheprojectgetreinvestedatthehurdlerate(whichisbaseduponwhatprojectsofcomparableriskshouldearn).

¨ TheIRRruleassumesthatintermediatecashflowsontheprojectgetreinvestedattheIRR.ImplicitistheassumptionthatthefirmhasaninfinitestreamofprojectsyieldingsimilarIRRs.

¨ Conclusion:WhentheIRRishigh(theprojectiscreatingsignificantsurplusvalue)andtheprojectlifeislong,theIRRwilloverstatethetruereturnontheproject.

286

SolutiontoReinvestmentRateProblem

AswathDamodaran

286

287

WhyNPVandIRRmaydiffer..Evenifprojectshavethesamelives

AswathDamodaran

287

¨ AprojectcanhaveonlyoneNPV,whereasitcanhavemorethanoneIRR.

¨ TheNPVisadollarsurplusvalue,whereastheIRRisapercentagemeasureofreturn.TheNPVisthereforelikelytobelargerfor“largescale” projects,whiletheIRRishigherfor“small-scale” projects.

¨ TheNPVassumesthatintermediatecashflowsgetreinvestedatthe“hurdlerate”,whichisbaseduponwhatyoucanmakeoninvestmentsofcomparablerisk,whiletheIRRassumesthatintermediatecashflowsgetreinvestedatthe“IRR”.

288

Comparingprojectswithdifferentlives..

AswathDamodaran

288Project A

-$1500

$350 $350 $350 $350$350

-$1000

$400 $400 $400 $400$400

$350 $350 $350 $350$350

Project B

NPV of Project A = $ 442IRR of Project A = 28.7%

NPV of Project B = $ 478IRR for Project B = 19.4%

Hurdle Rate for Both Projects = 12%

289

WhyNPVscannotbecompared..Whenprojectshavedifferentlives.

AswathDamodaran

289

¨ Thenetpresentvaluesofmutuallyexclusiveprojectswithdifferentlivescannotbecompared,sincethereisabiastowardslonger-lifeprojects.TocomparetheNPV,wehaveto¤ replicatetheprojectstilltheyhavethesamelife(or)¤ convertthenetpresentvaluesintoannuities

¨ TheIRRisunaffectedbyprojectlife.WecanchoosetheprojectwiththehigherIRR.

290

Solution1:ProjectReplication

AswathDamodaran

290

Project A: Replicated

-$1500

$350 $350 $350 $350$350 $350 $350 $350 $350$350

Project B

-$1000

$400 $400 $400 $400$400 $400 $400 $400 $400$400

-$1000 (Replication)

NPV of Project A replicated = $ 693

NPV of Project B= $ 478

291

Solution2:EquivalentAnnuities

AswathDamodaran

291

¨ EquivalentAnnuityfor5-yearproject¤ =$442*PV(A,12%,5years)¤ =$122.62

¨ EquivalentAnnuityfor10-yearproject¤ =$478*PV(A,12%,10years)¤ =$84.60

292

Whatwouldyouchooseasyourinvestmenttool?

AswathDamodaran

292

¨ Giventheadvantages/disadvantagesoutlinedforeachofthedifferentdecisionrules,whichonewouldyouchoosetoadopt?a. ReturnonInvestment(ROE,ROC)b. PaybackorDiscountedPaybackc. NetPresentValued. InternalRateofReturne. ProfitabilityIndex

¨ Doyouthinkyourchoicehasbeenaffectedbytheeventsofthelastquarterof2008?Ifso,why?Ifnot,whynot?

293

Whatfirmsactuallyuse..

AswathDamodaran

293

DecisionRule %ofFirmsusingasprimarydecisionrulein1976 1986 1998

IRR 53.6% 49.0% 42.0%AccountingReturn 25.0% 8.0% 7.0%NPV 9.8% 21.0% 34.0%PaybackPeriod 8.9% 19.0% 14.0%ProfitabilityIndex 2.7% 3.0% 3.0%

294

II.SideCostsandBenefits

AswathDamodaran

294

¨ Mostprojectsconsideredbyanybusinesscreatesidecostsandbenefitsforthatbusiness.¤ Thesidecostsincludethecostscreatedbytheuseofresourcesthatthebusinessalreadyowns(opportunitycosts)andlostrevenuesforotherprojectsthatthefirmmayhave.

¤ Thebenefitsthatmaynotbecapturedinthetraditionalcapitalbudgetinganalysisincludeprojectsynergies(wherecashflowbenefitsmayaccruetootherprojects)andoptionsembeddedinprojects(includingtheoptionstodelay,expandorabandonaproject).

¨ Thereturnsonaprojectshouldincorporatethesecostsandbenefits.

295

A.OpportunityCost

AswathDamodaran

295

¨ Anopportunitycostariseswhenaprojectusesaresourcethatmayalreadyhavebeenpaidforbythefirm.

¨ Whenaresourcethatisalreadyownedbyafirmisbeingconsideredforuseinaproject,thisresourcehastobepricedonitsnextbestalternativeuse,whichmaybe¤ asaleoftheasset,inwhichcasetheopportunitycostistheexpectedproceedsfromthesale,netofanycapitalgainstaxes

¤ rentingorleasingtheassetout,inwhichcasetheopportunitycostistheexpectedpresentvalueoftheafter-taxrentalorleaserevenues.

¤ useelsewhereinthebusiness,inwhichcasetheopportunitycostisthecostofreplacingit.

296

Case1:ForegoneSale?

AswathDamodaran

296

¨ AssumethatDisneyownslandinRioalready.Thislandisundevelopedandwasacquiredseveralyearsagofor$5millionforahotelthatwasneverbuilt.Itisanticipated,ifthisthemeparkisbuilt,thatthislandwillbeusedtobuildtheofficesforDisneyRio.Thelandcurrentlycanbesoldfor$40million,thoughthatwouldcreateacapitalgain(whichwillbetaxedat20%).Inassessingthethemepark,whichofthefollowingwouldyoudo:¤ Ignorethecostoftheland,sinceDisneyownsitsalready¤ Usethebookvalueoftheland,whichis$5million¤ Usethemarketvalueoftheland,whichis$40million¤ Other:

297

Case2:IncrementalCost?AnOnlineRetailingVentureforBookscape

AswathDamodaran

297

¨ Theinitialinvestmentneededtostarttheservice,includingtheinstallationofadditionalphonelinesandcomputerequipment,willbe$1million.Theseinvestmentsareexpectedtohavealifeoffouryears,atwhichpointtheywillhavenosalvagevalue.Theinvestmentswillbedepreciatedstraightlineoverthefour-yearlife.

¨ Therevenuesinthefirstyearareexpectedtobe$1.5million,growing20%inyeartwo,and10%inthetwoyearsfollowing.Thecostofthebookswillbe60%oftherevenuesineachofthefouryears.

¨ Thesalariesandotherbenefitsfortheemployeesareestimatedtobe$150,000inyearone,andgrow10%ayearforthefollowingthreeyears.

¨ Theworkingcapital,whichincludestheinventoryofbooksneededfortheserviceandtheaccountsreceivablewillbe10%oftherevenues;theinvestmentsinworkingcapitalhavetobemadeatthebeginningofeachyear.Attheendofyear4,theentireworkingcapitalisassumedtobesalvaged.

¨ Thetaxrateonincomeisexpectedtobe40%.

298

Costofcapitalforinvestment

AswathDamodaran

298

¨ Wewillre-estimatethebetaforthisonlineprojectbylookingatpubliclytradedonlineretailers.Theunleveredtotalbetaofonlineretailersis3.02,andweassumethatthisprojectwillbefundedwiththesamemixofdebtandequity(D/E=21.41%,Debt/Capital=17.63%)thatBookscapeusesintherestofthebusiness.WewillassumethatBookscape’staxrate(40%)andpretaxcostofdebt(4.05%)applytothisproject.LeveredBetaOnlineService =3.02[1+(1– 0.4)(0.2141)]=3.41CostofEquityOnlineService =2.75%+3.41(5.5%)=21.48%CostofCapitalOnlineService=21.48%(0.8237)+4.05%(1– 0.4)(0.1763)=18.12%

¨ Thisismuchhigherthanthecostofcapital(10.30%)wecomputedforBookscapeearlier,butitreflectsthehigherriskoftheonlineretailventure.

299

IncrementalCashflowsonInvestment

AswathDamodaran

299

NPV of investment = $76,375

0 1 2 3 4Revenues $1,500,000 $1,800,000 $1,980,000 $2,178,000

Operating ExpensesLabor $150,000 $165,000 $181,500 $199,650Materials $900,000 $1,080,000 $1,188,000 $1,306,800Depreciation $250,000 $250,000 $250,000 $250,000

Operating Income $200,000 $305,000 $360,500 $421,550Taxes $80,000 $122,000 $144,200 $168,620After-tax Operating Income $120,000 $183,000 $216,300 $252,930+ Depreciation $250,000 $250,000 $250,000 $250,000- Change in Working

Capital $150,000 $30,000 $18,000 $19,800 -$217,800+ Salvage Value of

Investment $0Cash flow after taxes -$1,150,000 $340,000 $415,000 $446,500 $720,730Present Value -$1,150,000 $287,836 $297,428 $270,908 $370,203

300

Thesidecosts…

AswathDamodaran

300

¨ Itisestimatedthattheadditionalbusinessassociatedwithonlineorderingandtheadministrationoftheserviceitselfwilladdtotheworkloadforthecurrentgeneralmanagerofthebookstore.Asaconsequence,thesalaryofthegeneralmanagerwillbeincreasedfrom$100,000to$120,000nextyear;itisexpectedtogrow5percentayearafterthatfortheremainingthreeyearsoftheonlineventure.Aftertheonlineventureisendedinthefourthyear,themanager’ssalarywillrevertbacktoitsoldlevels.

¨ ItisalsoestimatedthatBookscapeOnlinewillutilizeanofficethatiscurrentlyusedtostorefinancialrecords.Therecordswillbemovedtoabankvault,whichwillcost$1000ayeartorent.

301

NPVwithsidecosts…

AswathDamodaran

301

¨ Additionalsalarycosts=PVof$34,352

¨ OfficeCosts¤ After-TaxAdditionalStorageExpenditureperYear=$1,000(1– 0.40)=$600¤ PVofexpenditures=$600(PVofannuity,18.12%,4yrs)=$1,610

¨ NPVwithOpportunityCosts=$76,375– $34,352– $1,610=$40,413¨ Opportunitycostsaggregatedintocashflows

Year Cashflows Opportunity costs Cashflow with opportunity costs Present Value0 ($1,150,000) ($1,150,000) ($1,150,000)1 $340,000 $12,600 $327,400 $277,170 2 $415,000 $13,200 $401,800 $287,968 3 $446,500 $13,830 $432,670 $262,517 4 $720,730 $14,492 $706,238 $362,759 Adjusted NPV $40,413

302

Case3:ExcessCapacity

AswathDamodaran

302

¨ IntheValeexample,assumethatthefirmwilluseitsexistingdistributionsystemtoservicetheproductionoutofthenewironoremine.Theminemanagerarguesthatthereisnocostassociatedwithusingthissystem,sinceithasbeenpaidforalreadyandcannotbesoldorleasedtoacompetitor(andthushasnocompetingcurrentuse).Doyouagree?a. Yesb. No

303

AFrameworkforAssessingTheCostofUsingExcessCapacity

AswathDamodaran

303

¨ IfIdonotaddthenewproduct,whenwillIrunoutofcapacity?

¨ IfIaddthenewproduct,whenwillIrunoutofcapacity?

¨ WhenIrunoutofcapacity,whatwillIdo?¤ Cutbackonproduction:costisPVofafter-taxcashflowsfromlostsales

¤ Buynewcapacity:costisdifferenceinPVbetweenearlier&laterinvestment