Assumptions to the Annual Energy Outlook 2009

190

Report #:DOE/EIA-0554(2009) Release date: March 2009 Next release date: March 2010 Assumptions to the Annual Energy Outlook 2009

Transcript of Assumptions to the Annual Energy Outlook 2009

Report #:DOE/EIA-0554(2009)

Release date: March 2009

Next release date: March 2010

Assumptions to the Annual Energy Outlook 2009

1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2. Macroeconomic Activity Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3. International Energy Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

4. Residential Demand Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

5. Commercial Demand Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

6. Industrial Demand Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

7. Transportation Demand Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

8. Electricity Market Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

9. Oil and Gas Supply Module. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

10. Natural Gas Transmission and Distribution Module . . . . . . . . . . . . . . . . . . . . 123

11. Petroleum Market Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

12. Coal Market Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

13. Renewable Fuels Module . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

Appendix A: Handling of Federal and Selected State Legislationand Regulation In the Annual Energy Outlook . . . . . . . . . . . . . . . . . . . . . . . . 169

Contents

IntroductionThis report presents the major assumptions of the National Energy Modeling System (NEMS) used togenerate the projections in the Annual Energy Outlook 20091 (AEO2009), including general features of themodel structure, assumptions concerning energy markets, and the key input data and parameters that arethe most significant in formulating the model results. Detailed documentation of the modeling system isavailable in a series of documentation reports.2

The National Energy Modeling System

The projections in the AEO2009 were produced with the NEMS, which is developed and maintained by theOffice of Integrated Analysis and Forecasting of the Energy Information Administration (EIA) to provideprojections of domestic energy-economy markets in the long term and perform policy analyses requested bydecisionmakers in the White House, U.S. Congress, offices within the Department of Energy, including DOEProgram Offices, and other government agencies. The Annual Energy Outlook (AEO) projections are alsoused by analysts and planners in other government agencies and outside organizations.

The time horizon of NEMS is approximately 25 years, the period in which the structure of the economy andthe nature of energy markets are sufficiently understood that it is possible to represent considerablestructural and regional detail. Because of the diverse nature of energy supply, demand, and conversion inthe United States, NEMS supports regional modeling and analysis in order to represent the regionaldifferences in energy markets, to provide policy impacts at the regional level, and to portray transportationflows. The level of regional detail for the end-use demand modules is the nine Census divisions. Otherregional structures include production and consumption regions specific to oil, natural gas, and coal supplyand distribution, the North American Electric Reliability Council (NERC) regions and subregions forelectricity, and the Petroleum Administration for Defense Districts (PADDs) for refineries. Maps illustratingthe regional formats used in each module are included in this report. Only selected regional results arepresented in the AEO2009, which predominately focuses on the national results. Complete regional anddetailed results are available on the EIA Forecasts and Analyses Home Page (http://www.eia.doe.gov/oiaf/aeo/index.html)

For each fuel and consuming sector, NEMS balances the energy supply and demand, accounting for theeconomic competition between the various energy fuels and sources. NEMS is organized and implementedas a modular system (Figure 1). The modules represent each of the fuel supply markets, conversion sectors,and end-use consumption sectors of the energy system. NEMS also includes a macroeconomic and aninternational module. The primary flows of information between each of these modules are the deliveredprices of energy to the end user and the quantities consumed by product, region, and sector. The deliveredprices of fuel encompass all the activities necessary to produce, import, and transport fuels to the end user.The information flows also include other data such as economic activity, domestic production, andinternational petroleum supply availability.

The integrating module of NEMS controls the execution of each of the component modules. To facilitatemodularity, the components do not pass information to each other directly but communicate through acentral data storage location. This modular design provides the capability to execute modules individually,thus allowing decentralized development of the system and independent analysis and testing of individualmodules. This modularity allows use of the methodology and level of detail most appropriate for each energysector. NEMS solves by calling each supply, conversion, and end-use demand module in sequence until thedelivered prices of energy and the quantities demanded have converged within tolerance, thus achieving aneconomic equilibrium of supply and demand in the consuming sectors. Solution is reached annually throughthe projection horizon. Other variables are also evaluated for convergence such as petroleum productimports, crude oil imports, and several macroeconomic indicators.

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 1

Report #:DOE/EIA-0554(2009)

Release date: March 2009

Next release date: March 2010

Each NEMS component also represents the impact and cost of Federal legislation and regulation that affect thesector and reports key emissions. NEMS generally reflects all current legislation and regulation that are definedsufficiently to be modeled as of November 5, 2008, such as the Energy Improvement and Extension Act of 2008(EIEA2008), the biofuel provisions of the Food, Conservation, and Energy Act of 2008, the EnergyIndependence and Security Act of 2007 (EISA2007), the Energy Policy Act of 2005, Military ConstructionAppropriations Act of 2005, the Working Families Tax Relief Act of 2004, and the America Jobs Creation Actof 2004, and the costs of compliance with regulations such as new stationary diesel regulations issued by theU.S. Environmental Protection Agency (EPA) on July 11, 2006, which limit emissions of nitrogen oxides,particulate matter, sulfur dioxide, carbon monoxide, and hydrocarbons to the same levels required by theEPA’s nonroad diesel engine regulations and court decisions that impact regulations such as the recentdecisions by the D.C. Circuit of the U.S. Court of Appeals on February 8, 2008, to vacate the Clean AirMercury Rule (CAMR) and on July 11, 2008, to vacate the Clean Air Interstate Rule (CAIR).3 The NEMScomponents also reflect selected State legislation and regulations where implementing regulations are clearsuch as the October 2008 decision by the California Air Resources Board (CARB) on California’s LowCarbon Fuel Standard (LCFS) requiring a 10-percent ethanol blend, by volume, in gasoline,. However, thepotential impacts of pending or proposed legislation, regulations, and standards—or of sections oflegislation that have been enacted but that require implementing regulations or appropriation of funds thatare not provided or specified in the legislation itself—are not reflected in NEMS. A list of the specific Federaland selected State legislation and regulations included in the AEO, including how they are incorporated, is providedin Appendix A..

Component Modules

The component modules of NEMS represent the individual supply, demand, and conversion sectors ofdomestic energy markets and also include international and macroeconomic modules. In general, themodules interact through values representing the prices of energy delivered to the consuming sectors andthe quantities of end-use energy consumption. This section provides brief summaries of each of themodules.

Macroeconomic Activity Module

The Macroeconomic Activity Module (MAM) provides a set of macroeconomic drivers to the energymodules, and there is a macroeconomic feedback mechanism within NEMS. Key macroeconomic variables

2 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Oil and GasSupply Module

Natural GasTransmission

and DistributionModule

Coal MarketModule

RenewableFuels Module

Supply

ResidentialDemand Module

CommercialDemandModule

TransportationDemand Module

IndustrialDemand Module

Demand

ElectricityMarketModule

PetroleumMarketModule

Conversion

MacroeconomicActivityModule

InternationalEnergyModule

Integrating

Module

Figure 1. National Energy Modeling System

Source: Energy Information Administration, Office of Integrated Analysis and Forecasting.

used in the energy modules include gross domestic product (GDP), disposable income, value of industrialshipments, new housing starts, new light-duty vehicle sales, interest rates, and employment. The MAMmodule uses the following models from Global Insight, Inc.: Macroeconomic Model of the U.S. Economy,National Industry Model, and National Employment Model. In addition, EIA has constructed a RegionalEconomic and Industry Model to project regional economic drivers and a Commercial Floorspace Model toproject 13 floorspace types in 9 Census divisions. The accounting framework for industrial value ofshipments uses the North American Industry Classification System (NAICS)..

International ModuleThe International Module represents the response of world oil markets (supply and demand) to assumedworld oil prices. The results/outputs of the module are a set of crude oil and product supply curves that areavailable to U.S. markets for each case/scenario analyzed. The petroleum import supply curves are madeavailable to U.S. markets through the Petroleum Market Module (PMM) of NEMS in the form of 5 categoriesof imported crude oil and 17 international petroleum products, including supply curves for oxygenates andunfinished oils. The supply-curve calculations are based on historical market data and a world oilsupply/demand balance, which is developed from reduced-form models of international liquids supply anddemand, current investment trends in exploration and development, and long-term resource economics for221 countries/territories. The oil production estimates include both conventional and unconventional supplyrecovery technologies.

Residential and Commercial Demand ModulesThe Residential Demand Module projects energy consumption in the residential sector by housing type andend use, based on delivered energy prices, the menu of equipment available, the availability of renewablesources of energy, and housing starts. The Commercial Demand Module projects energy consumption inthe commercial sector by building type and nonbuilding uses of energy and by category of end use, based ondelivered prices of energy, availability of renewable sources of energy, and macroeconomic variablesrepresenting interest rates and floorspace construction.

Both modules estimate the equipment stock for the major end-use services, incorporating assessments ofadvanced technologies, including representations of renewable energy technologies, and the effects of bothbuilding shell and appliance standards, including the recently enacted provisions of the EISA2007. TheCommercial Demand Module incorporates combined heat and power (CHP) technology. The modules alsoinclude projections of distributed generation. Both modules incorporate changes to “normal” heating andcooling degree-days by Census division, based on a 10-year average and on State-level populationprojections. The Residential Demand Module projects an increase in the average square footage of bothnew construction and existing structures, based on trends in the size of new construction and the remodelingof existing homes.

Industrial Demand ModuleThe Industrial Demand Module projects the consumption of energy for heat and power and for feedstocksand raw materials in each of 21 industries, subject to the delivered prices of energy and macroeconomicvariables representing employment and the value of shipments for each industry. As noted in the descriptionof the MAM, the value of shipments is based on NAICS. The industries are classified into threegroups—energy-intensive manufacturing, non-energy-intensive manufacturing, and nonmanufacturing. Ofthe eight energy-intensive industries, seven are modeled in the Industrial Demand Module, with componentsfor boiler/steam/cogeneration, buildings, and process/ assembly use of energy. Bulk chemicals are furtherdisaggregated to organic, inorganic, resins, and agricultural chemicals. A generalized representation ofcogeneration and a recycling component are also included. The use of energy for petroleum refining ismodeled in the PMM, and the projected consumption is included in the industrial totals.

Transportation Demand ModuleThe Transportation Demand Module projects consumption of fuels in the transportation sector, includingpetroleum products, electricity, methanol, ethanol, compressed natural gas, and hydrogen, by transportationmode, vehicle vintage, and size class, subject to delivered prices of energy fuels and macroeconomicvariables representing disposable personal income, GDP, population, interest rates, and industrial

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 3

shipments. Fleet vehicles are represented separately to allow analysis of the Energy Policy Act of 1992(EPACT1992) and other legislation and legislative proposals. The transportation demand module alsoincludes a component to assess the penetration of alternative-fuel vehicles. EPACT2005 and EIEA2008 arereflected in the assessment of the impact of tax credits on the purchase of hybrid gas-electric,alternative-fuel, and fuel-cell vehicles. The corporate average fuel economy and biofuel representation in themodule reflect standards proposed by the National Highway Traffic Safety Administration and provisions inEISA2007.

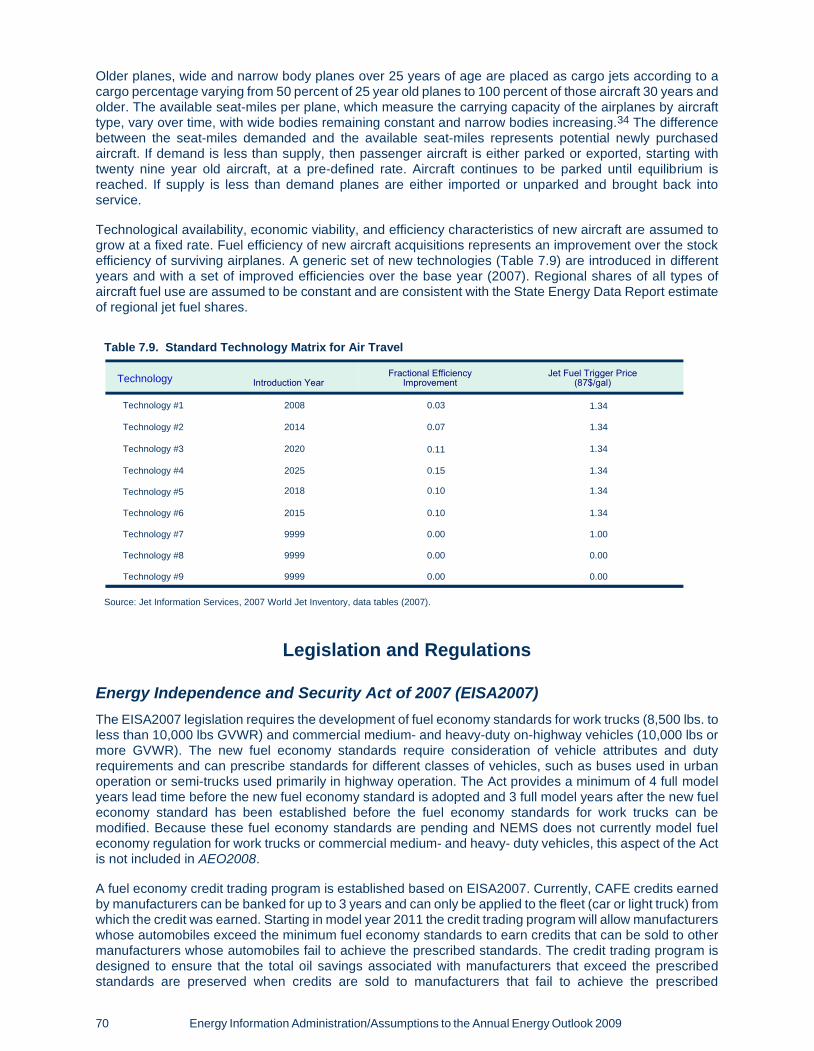

The air transportation component explicitly represents air travel in domestic and foreign markets andincludes the industry practice of parking aircraft in both domestic and international markets to reduceoperating costs, as well as the movement of aging aircraft from passenger to cargo markets4. For passengertravel and air freight shipments, the model represents regional fuel use in regional, narrow-body, andwide-body aircraft. An infrastructure constraint is also modeled and can potentially limit overall growth inpassenger and freight air travel to levels commensurate with industry-projected infrastructure expansionand capacity growth.

Electricity Market Module

The Electricity Market Module (EMM) represents generation, transmission, and pricing of electricity, subjectto delivered prices for coal, petroleum products, natural gas, and biofuels; costs of generation by allgeneration plants, including capital costs and macroeconomic variables for costs of capital and domesticinvestment; environmental emissions laws and regulations; and electricity load shapes and demand. Thereare three primary submodules—capacity planning, fuel dispatching, and finance and pricing.

All specifically identified options promulgated by the EPA for compliance with the Clean Air Act Amendmentsof 1990 (CAAA90) are explicitly represented in the capacity expansion and dispatch decisions; those thathave not been promulgated (e.g., fine particulate proposals) are not incorporated. All financial incentives forpower generation expansion and dispatch specifically identified in EPACT2005 have been implemented.Several States, primarily in the Northeast, have recently enacted air emission regulations for carbon dioxide(CO2) that affect the electricity generation sector, and these regulations are represented in AEO2009.

Although Federal legislation restricting greenhouse gas (GHG) emissions are not currently in place,regulators and the investment community are beginning to push energy companies to invest in lessGHG-intensive technologies. This was captured in the AEO2009 reference case through a 3-percentagepoint increase in the cost of capital when evaluating investments in new coal-fired power plants withoutcarbon control and sequestration, and new coal-to-liquids plants.

Renewable Fuels Module

The Renewable Fuels Module (RFM) includes submodules representing renewable resource supply andtechnology input information for central-station, grid-connected electricity generation technologies, includingconventional hydroelectricity, biomass (wood, energy crops, and biomass co-firing), geothermal, landfill gas,solar thermal electricity, solar photovoltaics (PV), and wind energy. The RFM contains renewable resourcesupply estimates representing the regional opportunities for renewable energy development. Investment taxcredits for renewable fuels are incorporated, as currently enacted. This includes a permanent 10-percent taxcredit for business investment in solar energy (thermal non-power uses as well as power uses) andgeothermal power (only available to those projects not accepting the production tax credit). In addition, themodule reflects the increase in the tax credit to 30 percent for solar energy systems installed before January1, 2017 and the extension of the credit to individual homeowners under EIEA2008.

Production tax credits for wind, geothermal, landfill gas, and some types of hydroelectric and biomass-fueledplants are also represented. They provide a tax credit of up to 2.0 cents per kilowatthour for electricityproduced in the first 10 years of plant operation. For AEO2009, new plants coming on line before January 1,2010, are eligible to receive the credit. AEO2009 also accounts for new renewable energy capacity resultingfrom State renewable portfolio standard programs, mandates, and goals, as described in Assumptions to theAnnual Energy Outlook 2009 5.

4 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Oil and Gas Supply ModuleThe Oil and Gas Supply Module (OGSM) represents domestic crude oil and natural gas supply within anintegrated framework that captures the interrelationships among the various sources of supply: onshore,offshore, and Alaska by both conventional and unconventional techniques, including natural gas recoveryfrom coalbeds and low-permeability formations of sandstone and shale. The framework analyzes cash flowand profitability to compute investment and drilling for each of the supply sources, based on the prices forcrude oil and natural gas, the domestic recoverable resource base, and the state of technology. Oil and gasproduction functions are computed for 12 supply regions, including 3 offshore and 3 Alaskan regions. Themodule also represents foreign sources of natural gas, including pipeline imports and exports to Canada andMexico, and liquefied natural gas (LNG) imports and exports.

Crude oil production quantities are input to the PMM in NEMS for conversion and blending into refinedpetroleum products. Supply curves for natural gas are input to the Natural Gas Transmission andDistribution Module (NGTDM) for use in determining natural gas prices and quantities. International LNGsupply sources and options for construction of new regasification terminals in Canada, Mexico, and theUnited States as well as expansions of existing U.S. regasification terminals are represented, based on theprojected regional costs associated with international natural gas supply, liquefaction, transportation, andregasification and world natural gas market conditions.

Natural Gas Transmission and Distribution ModuleThe NGTDM represents the transmission, distribution, and pricing of natural gas, subject to end-usedemand for natural gas and the availability of domestic natural gas and natural gas traded on theinternational market. The module tracks the flows of natural gas and determines the associated capacityexpansion requirements in an aggregate pipeline network, connecting the domestic and foreign supplyregions with 12 U.S. demand regions. The flow of natural gas is determined for both a peak and off-peakperiod in the year. Key components of pipeline and distributor tariffs are included in separate pricingalgorithms. The module also represents foreign sources of natural gas, including pipeline imports andexports to Canada and Mexico, and imports and exports LNG.

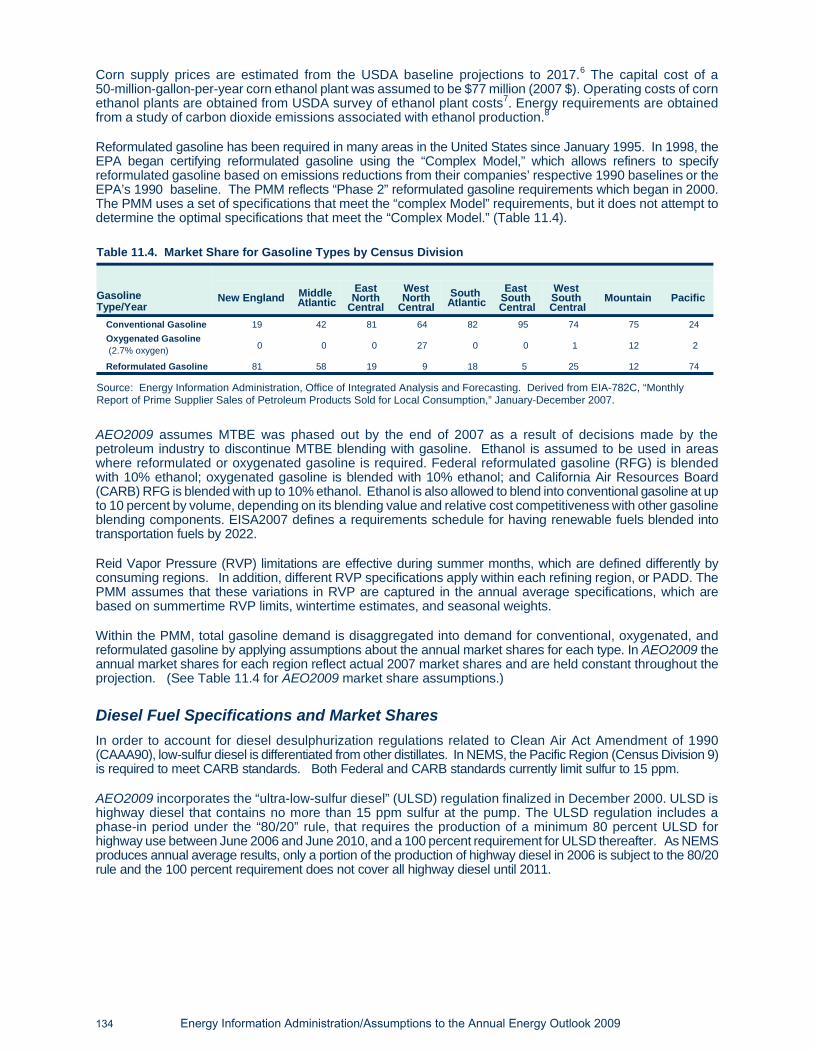

Petroleum Market ModuleThe PMM projects prices of petroleum products, crude oil and product import activity, and domestic refineryoperations (including fuel consumption), subject to the demand for petroleum products, the availability andprice of imported petroleum, and the domestic production of crude oil, natural gas liquids, and biofuels(ethanol, biodiesel, and biomass-to-liquids (BTL)). The module represents refining activities in the fivePADDs, as well as a less detailed representation of refining activities in the rest of the world. It explicitlymodels the requirements of EISA2007 and CAAA90 and the costs of automotive fuels, such as conventionaland reformulated gasoline, and includes the production of biofuels for blending in gasoline and diesel.

AEO2009 represents regulations that limit the sulfur content of all nonroad and locomotive/marine diesel to15 parts per million (ppm) by mid-2012. The module also reflects the new renewable fuels standard (RFS) inEISA2007 that requires the use of 36 billion gallons per year of biofuels by 2022 if achievable, with cornethanol limited to 15 billion gallons per year. Demand growth and regulatory changes necessitate capacityexpansion for refinery processing units. U.S. end-use prices are based on the marginal costs of production,plus markups representing the costs of product marketing, importing, transportation and distribution as wellas applicable State and Federal taxes6. Refinery capacity expansion at existing sites is permitted in eachE85, a blend of up to 85 percent ethanol by volume. In the AEO2009, the level of allowable non-E85 ethanolblending in California was raised from 5.7 percent to 10 percent in recent regulatory changes7 which haveset a framework for E10 emission standards. of the five refining regions modeled.

Fuel ethanol and biodiesel are included in the PMM, because they are commonly blended into petroleumproducts. The module allows ethanol blending into gasoline at 10 percent or less by volume (E10), as well asE85, a blend of up to 85 percent ethanol by volume. In the AEO2009, the level of allowable non-E85 ethanolblending in California was raised from 5.7 percent to 10 percent in recent regulatory changes8 which haveset a framework for E10 emission standards.

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 5

Both domestic and imported ethanol count toward the RFS. Domestic ethanol production is modeled fromtwo feedstocks: corn and cellulosic materials. Corn-based ethanol plants are numerous (more than 150 arenow in operation, possessing a total production capacity of more than 10 billion gallons annually) and arebased on a well-known technology that converts sugar into ethanol. Ethanol from cellulosic sources is a newtechnology with no pilot plants in operation; however, DOE awarded grants (up to $385 million) in 2007 toconstruct capacity totaling 147 million gallons per year, which AEO2009 assumes will be operational startingin 2012. Imported ethanol may be produced from cane sugar or bagasse, the cellulosic byproduct of sugarmilling. The sources of ethanol are modeled to compete on an economic basis and to meet the EISA2007renewable fuels mandate.

Coal Market Module

The Coal Market Module (CMM) simulates mining, transportation, and pricing of coal, subject to end-usedemand for coal differentiated by heat and sulfur content. U.S. coal production is represented in the CMM by40 separate supply curves—differentiated by region, mine type, coal rank, and sulfur content. The coalsupply curves include a response to capacity utilization of mines, mining capacity, labor productivity, andfactor input costs (mining equipment, mining labor, and fuel requirements), and other mine supply costs.Projections of U.S. coal distribution are determined by minimizing the cost of coal supplied, given coaldemands by demand region and sector, environmental restrictions, and accounting for minemouth prices,transportation rates, and coal supply contracts. Over the projection horizon, coal transportation rates in theCMM are projected to vary in response to changes in railroad investment and market share (for westernrates only).

The CMM produces projections of U.S. steam and metallurgical coal exports and imports, in the context ofworld coal trade. The CMM determines the pattern of world coal trade flows that minimizes the productionand transportation costs of meeting a specified set of regional world coal import demands, subject toconstraints on export capacities and trade flows. The international coal market component of the modulecomputes trade in 3 types of coal for 17 export and 20 import regions. U.S. coal production and distributionare computed for 14 supply and 14 demand regions.

Cases for the Annual Energy Outlook 2009

In preparing projections for the AEO2009, EIA evaluated a wide range of trends and issues that could havemajor implications for U.S. energy markets between now and 2030. Besides the reference case, theAEO2009 presents detailed results for four alternative cases that differ from each other due to fundamentalassumptions concerning the domestic economy and world oil market conditions. These alternative casesinclude the following:

• Economic Growth - In the reference case, real GDP grows at an average annual rate of 2.5 percentfrom 2007 through 2030, supported by a 2.0 percent per year growth in productivity in nonfarmbusiness and a 0.9 percent per year growth in nonfarm employment. In the high economic growthcase, real GDP is projected to increase by 3.0 percent per year, with productivity and nonfarmemployment growing at 2.4 percent and 1.3 percent per year, respectively. In the low economicgrowth case, the average annual growth in GDP, productivity and nonfarm employment is 1.8, 1.5and 0.5 percent, respectively.

• Price Cases – For purposes of the AEO2009, the world oil price is defined by the price of light,low-sulfur crude oil delivered in Cushing, Oklahoma. In the reference case, world oil prices increasequickly after the recession ends, reaching $110 per barrel in 2015 ($128 per barrel in nominal terms),as growth in world oil demand rebounds and investment in production capacity lags this expansion indemand. After 2015, real prices rise gradually as demand continues to grow and higher cost suppliesare brought to market. In 2030, the average real price of crude oil is $130 per barrel in 2007 dollars, orabout $189 per barrel in nominal dollars. The reference case represents EIA’s current judgmentabout the most likely behavior of key Organization of Petroleum Exporting Country (OPEC) membersin the mid term. In the projection, OPEC countries increase production at a rate that keeps theirmarket share of world liquids production at approximately 41 percent through 2030. The low and highprice cases define a wide range of potential price paths, which in 2030 span from $50 to $200 perbarrel in real dollars. These cases reflect differences in the assumptions about access to energy

6 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

resources, production costs, and changes in OPEC behavior. The low price case assumes greatereconomic access to world crude oil resources that are less expensive to produce and a future marketwhere all oil and natural gas production becomes more competitive and plentiful than the referencecase. The high price case assumes that the production of conventional crude oil will cost more than inthe reference case and will be limited due to increased restrictions on economic access to non-OPECresources and OPEC decisions to further limit its production.

In addition to these four cases, and the reference case, 31 additional alternative cases presented in Table1.1 that explore the impact of changing key assumptions on individual sectors.

Many of the side cases were designed to examine the impacts of varying key assumptions for individualmodules or a subset of the NEMS modules, and thus the full market consequences, such as theconsumption or price impacts, are not captured. In a fully integrated run, the impacts would tend to narrowthe range of the differences from the reference case. For example, the best available technology side case inthe residential demand assumes that all future equipment purchases are made from a selection of the mostefficient technologies available in a particular year. In a fully integrated NEMS run, the lower resulting fuelconsumption would have the effect of lowering the market prices of those fuels with the concomitant impactof increasing economic growth, thus stimulating some additional consumption. The results of single model orpartially integrated cases should be considered the maximum range of the impacts that could occur with theassumptions defined for the case.

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 7

Case name Description Integrationmode

Reference Baseline economic growth (2.5 percent per year from 2007through 2030), world oil price, and technology assumptions.Complete projection tables in Appendix A.

Fully integrated

Low Economic Growth GDP grows at an average annual rate of 1.8 percent from 2007through 2030. Other energy market assumptions are the same asin the reference case. Partial projection tables in Appendix B.

Fully integrated

High Economic Growth GDP grows at an average annual rate of 3.0 percent from 2007through 2030. Other energy market assumptions are the same asin the reference case. Partial projection tables in Appendix B.

Fully integrated

Low Oil Price More optimistic assumptions for economic access to non-OPECresources and the behavior of the OPEC than in the referencecase. World light, sweet crude oil prices are $50 per barrel in2030, compared with $130 per barrel in the reference case (2007dollars). Other assumptions are the same as in the referencecase. Partial projection tables in Appendix C.

Fully integrated

High Oil Price More pessimistic assumptions for economic access to non-OPECresources and OPEC behavior than in the reference case. Worldlight, sweet crude oil prices are about $200 per barrel (2007dollars) in 2030. Other assumptions are the same as in thereference case. Partial projection tables in Appendix C..

Fully integrated

Residential:2009 Technology

Future equipment purchases based on equipment available in2009. Existing building shell efficiencies fixed at 2009 levels.Partial projection tables in Appendix D.

With commercial

Residential: HighTechnology

Earlier availability, lower costs, and higher efficiencies assumedfor more advanced equipment. Building shell efficiencies for newconstruction meet ENERGY STAR requirements after 2016.Partial projection tables in Appendix D.

With commercial

Residential: BestAvailable Technology

Future equipment purchases and new building shells based onmost efficient technologies available by fuel. Building shellefficiencies for new construction meet the criteria for most efficientcomponents after 2009. Partial projection tables in Appendix D.

With commercial

Commercial:2009 Technology

Future equipment purchases based on equipment available in2009. Building shell efficiencies fixed at 2009 levels. Partialprojection tables in Appendix D.

With residential

Table 1.1. Summary of AEO2009 Cases

8 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Case name Description Integrationmode

Commercial:HighTechnology

Earlier availability, lower costs, and higher efficienciesassumed for more advanced equipment. Building shellefficiencies for new and existing buildings increase by8.8 and 6.3 percent, respectively, from 2003 values by2030. Partial projection tables in Appendix D.

With residential

Commercial: BestAvailable Technology

Future equipment purchases based on most efficienttechnologies available by fuel. Building shell efficiencies fornew and existing buildings increase by 10.5 and 7.5 percent,respectively, from 2003 values by 2030. Partial projectiontables in Appendix D.

With residential

Industrial: 2009Technology

Efficiency of plant and equipment fixed at 2009 levels.Partial projection tables in Appendix D.

Standalone

Industrial:High Technology

Earlier availability, lower costs, and higher efficienciesassumed for more advanced equipment. Partial projectiontables in Appendix D.

Standalone

Transportation:Low Technology

Assumes advanced technologies are more costly and lessefficient then in reference case. Partial projection tables inAppendix D

Standalone

Transportation:High Technology

Assumes advanced technologies are less costly and moreefficient then in reference case. Partial projection tables inAppendix D.

Standalone

Electricity: Low Nuclear Cost New nuclear capacity assumed to have 25 percent lowercapital and operating costs in 2030 than in the referencecase. Partial projection tables in Appendix D.

Fully Integrated

Electricity: High Nuclear Cost Costs for new nuclear technology assumed not to improvefrom 2009 levels in the reference case. Existing nuclearplants are assumed to retire after 55 years. Partial projectiontables in Appendix D.

Fully Integrated

Electricity: Low FossilTechnology Cost

Capital and operating costs for all new fossil-fired generatingtechnologies improve by 25 percent in 2030 from referencecase values. Partial projection tables in Appendix D.

Fully Integrated

Electricity: High FossilTechnology Cost

Costs for new advanced fossil generating technologiesassumed not to improve over time from 2009. Partialprojection tables in Appendix D.

Fully Integrated

Renewable Fuels: HighRenewable TechnologyCost

New renewable generating technologies assumed not toimprove over time from 2009. Partial projection tables inAppendix D.

Fully integrated

Renewable Fuels: LowRenewable TechnologyCost

Levelized cost of energy for non-hydropower renewablegenerating technologies declines by 25 percent in 2030from reference case values. Partial projection tables inAppendix D.

Fully integrated

Renewable Fuels:Production Tax CreditExtension

PTC for certain renewable generation is assumed to beextended to projects constructed through2016.

Fully integrated

Oil and Gas:Rapid Technology

Cost, finding rate, and success rate parameters adjustedfor 50-percent more rapid improvement than in thereference case. Partial projection tables in Appendix D.

Fully integrated

Oil and Gas:Slow Technology

Cost, finding rate, and success rate parameters adjustedfor 50-percent slower improvement than in the referencecase. Partial projection tables in Appendix D.

Fully integrated

Oil and Gas: HighLNG Supply

LNG imports exogenously set to a factor times the referencecase levels from 2010 forward, with remaining assumptionsfrom the reference case. The factor starts at 1.0 in 2010 andincreases linearly to 5.0 by 2030. Partial projection tables inAppendix D.

Fully Integrated

Table 1.1. Summary of AEO2009 Cases (cont.)

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 9

Case name Description Integrationmode

Oil and Gas: LowLNG Supply

LNG imports held constant at 2009 levels, with remainingassumptions from the reference case. Partial projectiontables in Appendix D.

Fully Integrated

Oil and Gas: ANWR The Arctic National Wildlife Refuge (ANWR) in Alaskais opened to Federal oil and natural gas leasing, withremaining assumptions from the reference case. Partialprojection tables in Appendix D.

Fully Integrated

Oil and Gas:No Alaska Pipeline

A natural gas pipeline from the North Slope of Alaskato the Lower 48 States is assumed not to be built duringthe projection period.

Fully Integrated

Coal: Low Coal Cost Productivity growth rates for coal mining are assumedto be higher than in the reference case, and coal miningwages, mine equipment, and coal transportation ratesare assumed to be lower. Partial projection tables inAppendix D.

Fully Integrated

Coal: High Coal Cost Productivity growth rates for coal mining are assumed to belower than in the reference case, and coal mining wages,mine equipment, and coal transportation rates are assumedto be higher. Partial projection tables in Appendix D.

Fully integrated

Integrated 2009Technology

Combination of the residential, commercial, and industrial2009 technology cases; and the electricity high fossiltechnology cost, high renewable technology cost, and highnuclear cost cases. Partial projection tables in Appendix D

Fully integrated

Integrated HighTechnology

Combination of the residential, commercial, industrial, andtransportation high technology cases; and the electricitylow fossil technology cost, low renewable technology cost,and low nuclear cost cases. Partial projection tables inAppendix D.

Fully integrated

Electricity: Frozen PlantCosts

Base overnight costs for all new electric generatingtechnologies are assumed to be frozen at 2012 levels.Cost decreases due to learning still occur, but no declinesin costs due to commodity price changes are assumed.

Fully Integrated

Electricity: High PlantCapital Costs

Base overnight costs for all new electric generatingtechnologies are assumed to continue increasing through-out the projection, reaching 25 percent above 2012 costsin 2030. Cost decreases due to learning can still occur andmay partially offset these increases.

Fully Integrated

Electricity: Falling PlantCapital Costs

Base overnight costs for all new electric generatingtechnologies are assumed to fall more rapidly than in thereference case, reaching 25 percent below the referencecase costs in 2030.

Fully Integrated

No GHG Expectations Assumes that a greenhouse gas emission reduction policyis not enacted and markets do not alter their investmentdecisions in anticipation of such a policy.

Fully Integrated

Cap and Trade Assumes a greenhouse gas emission reduction policysimilar to that proposed in S.2191, the Lieberman-WarnerClimate Security Act of 2007 is implemented

Fully Integrated

No 2008 Tax Legislation Removes EIEA2008 tax legislation from reference case. Fully Integrated

Table 1.1. Summary of AEO2009 Cases (cont.)

Carbon Dioxide Emissions

Carbon dioxide emissions from energy use are dependent on the carbon content of the fossil fuel, thefraction of the fuel consumed in combustion, and the consumption of that fuel. The product of the carboncontent at full combustion and the combustion fraction yields an adjusted carbon emission factor for eachfossil fuel. The emissions factors are expressed in millions of metric tons carbon dioxide emitted perquadrillion Btu of energy use, or equivalently, in kilograms carbon dioxide per million Btu. The adjustedemissions factors are multiplied by the energy consumption of the fossil fuel to arrive at the carbon dioxideemissions projections.

For fuel uses of energy, the combustion fractions are assumed to be 1.00 in keeping with internationalconventions.9 Previously, a small fraction of the carbon content of the fuel was assumed to remainunoxidized. The carbon dioxide in nonfuel use of energy, such as for asphalt and petrochemical feedstocks,is assumed to be sequestered in the product and not released to the atmosphere. For energy categories thatare mixes of fuel and nonfuel uses, the combustion fractions are based on the proportion of fuel use. Anycarbon dioxide emitted by biogenic renewable sources, such as biomass and alcohols, is consideredbalanced by the carbon dioxide sequestration that occurred in its creation. Therefore, following convention,net emissions of carbon dioxide from biogenic renewable sources are taken as zero, and no emissioncoefficient is reported. In calculating carbon dioxide emissions for motor gasoline, the direct emissions fromrenewable blending stock (ethanol) is omitted. Similarly, direct emissions from biodiesel are omitted fromreported carbon dioxide emissions. Table 1.2 presents the assumed carbon dioxide coefficients at fullcombustion, the combustion fractions, and the adjusted carbon dioxide emission factors used for AEO2009.

10 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 11

Fuel Type

Carbon Dioxide Coefficient

at FullCombustion

CombustionFraction

AdjustedEmissions

FactorPetroleum

Motor Gasoline (net of ethanol) 70.88 1.000 70.88

Liquefied Petroleum Gas

Used as Fuel 63.00 1.000 63.00

Used as Feedstock 61.44 0.200 12.29

Jet Fuel 70.88 1.000 70.88

Distillate Fuel (net of biodiesel) 73.15 1.000 73.15

Residual Fuel 78.80 1.000 78.80

Asphalt and Road Oil 75.61 0.000 0.00

Lubricants 74.21 0.500 37.11

Petrochemical Feedstocks 69.85 0.386 26.93

Kerosene 72.31 1.000 72.31

Petroleum Coke 102.12 0.782 79.87

Petroleum Still Gas 64.20 1.000 64.20

Other Industrial 74.54 1.000 74.54

Coal

Residential and Commercial 95.35 1.000 95.35

Metallurgical 93.71 1.000 93.71

Coke 114.14 1.000 114.14

Industrial Other 93.98 1.000 93.98

Electric Utility1 94.70 1.000 94.70

Natural Gas

Used as Fuel 53.06 1.000 53.06

Used as Feedstocks 53.06 0.523 27.73

Table 1.2. Carbon Dioxide Emission Factors (million metric tons carbon dioxide equivalent per quadrillion Btu)

1Emission factors for coal used for electricity generation are specified by coal supply region and types of coal, so the average carbon dioxide contentsfor coal varies throughout the projection. The 2007 average is 94.70.

Source: Energy Information Administration, Emissions of Greenhouse Gases in the United States 2007, DOE/EIA-0573(2007), (Washington, DC,December 2008).

[1] Energy Information Administration, Annual Energy Outlook 2009 (AEO2009), DOE/EIA-0383(2009),(Washington, DC, February 2009).

[2] NEMS documentation reports are available on the EIA Homepage (http://tonto.eia.doe.gov/reports/reports_kindD.asp?type=model documentation).

[3] On December 23, 2008, after the November 5 cutoff date for inclusion of changes in Federal and Statelaws and regulations in AEO2009, the United States Court of Appeals for the District of Columbia issued anew ruling that remanded but did not vacate CAIR, noting that "Allowing CAIR to remain in effect until it isreplaced by a rule consistent with our opinion would at least temporarily preserve the environmental values."Source: United States Court of Appeals for the District of Columbia Circuit, No. 05-1244, web sitewww.epa.gov/airmarkets/progsregs/cair/docs/CAIRRemandOrder.pdf. This change allows the EPA tomodify CAIR to address the objections raised by the Court in its earlier decision while leaving the rule inplace. The change is not reflected in AEO2009.

[4] Jet Information Services, Inc., World Jet Inventory Year-End 2006 (Utica, NY, March 2007); and personalcommunication from Stuart Miller (Jet Information Services).

[5] Energy Information Administration, Assumptions to the Annual Energy Outlook 2009, DOE/EIA-0554(2009) (Washington, DC, February 2009), web site www.eia.doe.gov/oiaf/aeo/assumption

[6] For gasoline blended with ethanol, the tax credit of 51 cents (nominal) per gallon of ethanol is assumed tobe available for 2008. However, this tax credit is reduced to 45 cents as mandated by the “Food,Conservation, and Energy Act of 2008” (the “Farm Bill”) starting in 2009 (the year after the annual U.S.ethanol consumption surpasses 7.5 billion gallons); the tax credit is set to expire after 2010. In addition,modeling updates include the Farm Bill’s mandated extension of the 54 cent/gallon import tariff to Dec. 31,2010. Finally, again in accordance with the Farm Bill, a new cellulosic producer’s tax credit of $1.01/gallon isimplemented in the model (valid through 2012); however, this tax credit is reduced by the aforementionedblender’s tax credit amount. Thus, in 2009 and 2010, the cellulosic producer’s tax credit is modeled as $1.01- $0.45 = $0.56/gallon, and in 2011 and 2012 it is $1.01/gallon. http://www.arb.ca.gov/regact/2007/carfg07/carfg07.htm.

[7] Energy Information Administration, Assumptions to the Annual Energy Outlook 2009, DOE/EIA-0554(2009) (Washington, DC, February 2009), web site www.eia.doe.gov/oiaf/aeo/assumption.

[8] Energy Information Administration, Assumptions to the Annual Energy Outlook 2009, DOE/EIA-0554(2009) (Washington, DC, February 2009), web site www.eia.doe.gov/oiaf/aeo/assumption

[9] The Intergovernmental Panel on Climate Change 2006, 2006 IPCC Guidelines For National GreenhouseGas Inventories, prepared by the National Greenhouse Gas Inventories Program, published: IGES, Japan,2006.

12 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Notes and Sources

Macroeconomic Activity ModuleThe Macroeconomic Activity Module (MAM) represents the interaction between the U.S. economy as awhole and energy markets. The rate of growth of the economy, measured by the growth in grossdomestic product (GDP) is a key determinant of the growth in demand for energy. Associated economicfactors, such as interest rates and disposable income, strongly influence various elements of the supply anddemand for energy. At the same time, reactions to energy markets by the aggregate economy, such as aslowdown in economic growth resulting from increasing energy prices, are also reflected in this module. Adetailed description of the MAM is provided in the EIA publication, Model Documentation Report:Macroeconomic Activity Module (MAM) of the National Energy Modeling System, DOE/EIA-M065(2008),(Washington, DC, January 2008).

Key Assumptions

The output of the U.S. economy, measured by GDP, is expected to increase by 2.5 percent between 2007and 2030 in the reference case. Two key factors help explain the growth in GDP: the growth rate of nonfarmemployment and the rate of productivity change associated with employment. As Table 2.1 indicates, realGDP growth slows during the first three years of the forecast, reflecting the current economic recession,shows higher growth for the first ten years as the economy recovers, and then returns to its long-run growthpath. In the reference case, real GPD grows by 0.7 percent for the first three years, 2.8 percent for therecovery period and 2.6 percent for the final ten years. Both the high and low macroeconomic growth casesshow similar patterns of early lower growth, recovery and settling back into their respective long-run growthtrends. In the near term from 2007 through 2010, the growth in nonfarm employment is low at -0.4 percentcompared with 2.4 percent in the second half of the 1990s, while the economy is expected to experienceproductivity growth of 1.8 percent. Over the projection period, nonfarm employment is expected to grow by0.9 percent per year. Nonfarm employment, a measure of demand for nonfarm labor, is generally morevolatile than the labor force, a measure of labor supply. The latter depends upon the pro jec t ion ofpopulation and labor force participation rate. The Census Bureau’s middle series population projection isused as a basis for population growth for the AEO2009. Total population is expected to grow by 0.9percent per year between 2007 and 2030, and the share of population over 65 is expected to increase overtime. However, the share of the labor force in the population over 65 is also projected to increase in theprojection period.

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 13

Assumptions 2007-2010 2010-2020 2020-2030 2007-2010GDP (Billion Chain-Weighted $2000)

High Growth 1.7 3.3 3.2 3.0

Reference 0.7 2.8 2.6 2.5

Low Growth -0.2 2.3 1.9 1.8

Nonfarm Employment

High Growth 0.8 1.5 1.2 1.3

Reference -0.4 1.2 1.0 0.9

Low Growth -1.6 0.8 0.8 0.5

Productivity

High Growth 2.3 2.3 2.5 2.4

Reference 1.8 1.9 2.1 2.0

Low Growth 1.5 1.4 1.5 1.5

Table 2.1. Growth in Gross Domestic Product, Nonfarm Employmemt and Productivity(Percent per Year)

Source: Energy Information Administration, AEO2009 National Energy Modeling System runs: AEO2009.d120908a;LM2009.d120908a; and hm2009.d120908a.

Report #:DOE/EIA-0554(2009)Release date: March 2009Next release date: March 2010

To achieve the reference case’s long-run 2.5 percent economic growth, there is an anticipated steadygrowth in labor productivity. The improvement in labor productivity reflects the positive effects of a growingcapital stock as well as technological change over time. Nonfarm labor productivity is expected to remainbetween 1.9 and 2.0 percent for the remainder of the projection period from 2007 through 2030. Businessfixed investment as a share of nominal GDP is expected to grow over the last 10 years of the projection. Theresulting growth in the capital stock and the technology base of that capital stock helps to sustain productivitygrowth of 2.0 percent from the 2007 to 2030.

To reflect the uncertainty in projection of economic growth, the AEO2009 uses high and low economicgrowth cases along with the reference case to project the possible impacts on energy markets. The higheconomic growth case incorporates higher population, labor force and productivity growth rates than thereference case. Due to the higher productivity gains, inflation and interest rates are lower compared to thereference case. Investment, disposable income, and industrial production are increased. Economic outputis projected to increase by 3.0 percent per year between 2007 and 2030. The low economic growth caseassumes lower population, labor force, and productivity gains, with resulting higher prices and interest ratesand lower industrial output growth. In the low economic growth case, economic output is expected toincrease by 1.8 percent per year over the projection horizon.

14 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

International Energy ModuleThe International Energy Module (IEM) performs two tasks in all NEMS runs. First, the module readsexogenously global and U.S.A. petroleum liquids supply and demand curves (1 curve per year; 2008-2030;approximated, isoelastic fit to previous NEMS results). These quantities are not modeled directly in NEMS.Previous versions of the IEM adjusted these quantities after reading in initial values. In an attempt to moreclosely integrate the AEO2009 with IEO2008 and the STEO some functionality was removed from IEM while a newalgorithm was implemented. Based on the difference between U.S. total petroleum liquids production(consumption) and the expected U.S. total liquids production (consumption) at the current WTI price, curves forglobal petroleum liquids consumption (production) were adjusted for each year. According to previousoperations, a new WTI price path was generated. An exogenous oil supply module, Generate World OilBalances (GWOB), was also used in IEM to provide annual regional (country) level production detail forconventional and unconventional liquids.

The second task of the IEM is to interact with the PMM module during runs to determine changes in the WTI price andthe supply prices of crude oils and petroleum products for import to the United States in response to changes in U.S.import requirements. As a result of the interaction with PMM, this module also determines new values for oilproduction in the world, along with a report for crude oil, light and heavy refined products imports by source.

Key Assumptions

The level of oil production by countries in the Organization of Petroleum Exporting Countries (OPEC) is a key factorinfluencing the world oil price projections incorporated into AEO2009. Non-OPEC production, worldwideregional economic growth rates and the associated regional demand for oil are additional factors affecting theworld oil price.

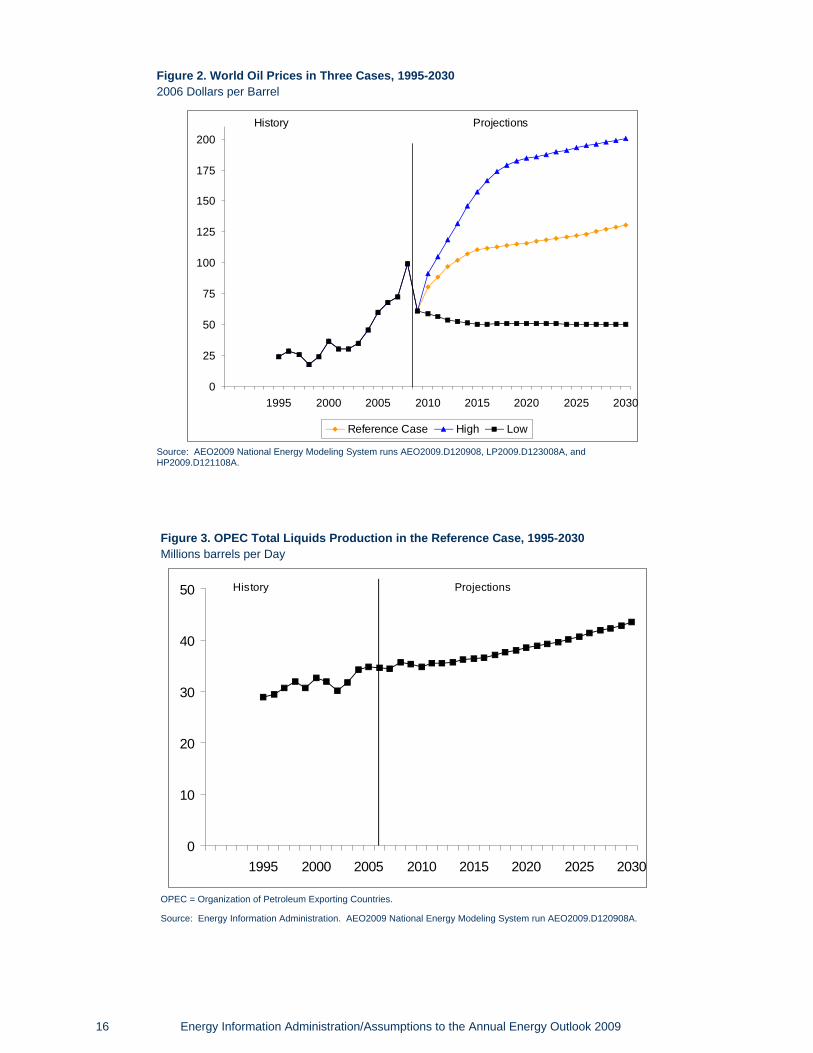

The world oil price is the annual average U.S. cost of imported low-sulfur light crude oil in PADD2. For the low,reference, and high oil price cases, prices reach $50, $130 and $200 per barrel in 2030, respectively, in 2007dollars. The reference case assumes that OPEC producers will continue to demonstrate a disciplined productionapproach. The low oil price case reflects a market where all oil production becomes more competitive andplentiful. The high oil price case could result from a more cohesive and market-assertive OPEC that reducesoverall production volumes. Thethree price scenarios are shown in Figure 2.

OPEC oil production is assumed to increase throughout the reference case projection, enabling theorganization to maintain an approximately constant market share over the projection period (Figure 3). OPECis assumed to be an important source of additional production because its member nations hold a major portionof the world’s total reserves—exceeding 927 billion barrels, about 70 percent of the world’s estimated total, atthe beginning of 2008.1

The reference case values for OPEC production are shown in Figure 3. Iraq oil production is assumed to notmaintain steady growth until after 2015. By 2030, Iraq is expected to increase production capacity to 4 millionbarrels per day with likely investment help from foreign sources. Non-OPEC liquids production is expected toincrease by just under one percent per year over the projection period, as advances in both exploration andextraction technologies result in an upward trend. The non-OPEC production path for the reference case isshown in Figure 4.

The non-U.S. oil production projections in the AEO2009 begin with country-level assumptions regarding oilresources. These resource estimates are taken in part from the USGS World Petroleum Assessment of2000 as well as from PennWell Publishing Company Oil and Gas Journal, summary of which is shown inTable 3.1.

The reference case growth rates for GDP for various regions in the world are shown in Table 3.2. Except for theUnited States, the GDP growth rate assumptions for non U.S. country/regions are taken from IEO2008.

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 15

Report #:DOE/EIA-0554(2009)Release date: March 2009Next release date: March 2010

16 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

0

25

50

75

100

125

150

175

200

1995 2000 2005 2010 2015 2020 2025 2030

Reference Case High Low

History Projections

Figure 2. World Oil Prices in Three Cases, 1995-2030

2006 Dollars per Barrel

Source: AEO2009 National Energy Modeling System runs AEO2009.D120908, LP2009.D123008A, andHP2009.D121108A.

0

10

20

30

40

50

1995 2000 2005 2010 2015 2020 2025 2030

History Projections

Figure 3. OPEC Total Liquids Production in the Reference Case, 1995-2030

Millions barrels per Day

OPEC = Organization of Petroleum Exporting Countries.

Source: Energy Information Administration. AEO2009 National Energy Modeling System run AEO2009.D120908A.

The values for growth in oil demand in the International Energy Module, which depend upon the oil pricelevels as well as GDP growth rates, are shown in Table 3.3 for the reference case by regions.

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 17

0

10

20

30

40

50

60

70

1995 2000 2005 2010 2015 2020 2025 2030

History Projections

Figure 4. Non-OPEC Total Liquids Production in the Reference Case, 1995-2030

Millions barrels per Day

OPEC = Organization of Petroleum Exporting Countries.

Source: Energy Information Administration. AEO2009 National Energy Modeling System run AEO2008.D120908A.

18 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Region Proved Oil Reserves

Western Hemisphere 321.1

Western‘Europe 13.2

Asia-Pacific 34.3

Eastern Europe and F.S.U. 100

Middle East 748.3

Africa 114.8

Total World 1331.7

Total OPEC 927.5

Table 3.1. Worldwide Oil Reserves as of January 1, 2008(Billion Barrels)

Source: PennWell Corporation, Oil and Gas Journal, Vol 105. 48 (Dec 24, 2007).

Region Average Annual Percentage Change

OECD 2.3

OECD North America 2.6

OECD Europe 2.3

OECD Asia 1.8

Non-OECD 5.2

Non-OECD Europe and Eurasia 4.4

Non-OECD Asia 5.8

Middle East 4.0

Africa 4.5

Central and South America 3.9

Total World 4.0

Table 3.2. Average Annual Real Gross Domestic Product Rates, 2004-2030 (2000 Purchasing PowerParity Weights and Prices)

Source: For the U.S., Energy Informatin Administration, National Energy Modeling System run AEO2009.D120908A; for other countries, GlobalInsight, Inc., World Overview (Lexington, MA, January 2008)

Region Oil Demand Growth

OECD 0.02%

OECD North America 0.25%

OECD Europe 0.31%

OECD Asia -0.21%

Non-OECD 2.00%

Non-OECD Europe and Eurasia 1.07%

Non-OECD Asia 2.56%

Middle East 2.07%

Africa 1.38%

Central and South America 1.23%

Total World 0.94%

Table 3.3. Average Annual Growth Rates for Total Liquids Demand in the Reference Case, 2004-2030(Percent per Year)

Source: Energy Information Administration, AEO2008 National Energy Modeling System run: AEO2009.D120908A; and IEO2008 System for theAnalysis of Global Energy Markets (2008).

[1] PennWell Corporation, Oil and Gas Journal, Vol. 105.48 (December 24, 2007).

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 19

Notes and Sources

Residential Demand ModuleThe NEMS Residential Demand Module projects future residential sector energy requirements based onprojections of the number of households and the stock, efficiency, and intensity of use of energy-consumingequipment. The Residential Demand Module projections begin with a base year estimate of the housingstock, the types and numbers of energy-consuming appliances servicing the stock, and the “unit energyconsumption” by appliance (or UEC—in million Btu per household per year). The projection process addsnew housing units to the stock, determines the equipment installed in new units, retires existing housingunits, and retires and replaces appliances. The primary exogenous drivers for the module are housing startsby type (single-family, multifamily and mobile homes) and Census Division and prices for each energysource for each of the nine Census Divisions (see Figure 5). The Residential Demand Module also requiresprojections of available equipment and their installed costs over the projection horizon. Over time,

equipment efficiency tends to increase because of general technological advances and also because ofFederal and/or state efficiency standards. As energy prices and available equipment changes over theprojection horizon, the module includes projected changes to the type and efficiency of equipmentpurchased as well as projected changes in the usage intensity of the equipment stock.

The end-use services for which equipment stocks are modeled include space conditioning (heating andcooling), water heating, refrigeration, freezers, dishwashers, clothes washers, lighting, furnace fans, colortelevisions, personal computers, cooking, clothes drying, ceiling fans, coffee makers, spas, home securitysystems, microwave ovens, set-top boxes, home audio equipment, rechargeable electronics, andVCR/DVDs. In addition to the major equipment-driven end-uses, the average energy consumption perhousehold is projected for other electric and nonelectric appliances. The module’s output includes number

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 21

Pacific

East South Central

South Atlantic

MiddleAtlantic

NewEngland

WestSouth

Central

WestNorth

Central EastNorth

CentralMountain

AK

WAMT

WYID

NVUT

CO

AZNM

TX

OK

IA

KS MOIL

IN

KY

TN

MS AL

FL

GA

SC

NC

WV

PA NJ

MD

DE

NY

CT

VT ME

RIMA

NH

VA

WI

MI

OH

NE

SD

MNND

AR

LA

OR

CA

HI

Middle AtlanticNew England

East North CentralWest North Central

PacificWest South CentralEast South Central

South AtlanticMountain

2

4

3

1

Figure 5. United States Census Divisions

Source:Energy Information Administration,Office of Integrated Analysis and Forecasting.

Report #:DOE/EIA-0554(2009)Release date: March 2009Next release date: March 2010

of households, equipment stock, average equipment efficiencies, and energy consumed by service, fuel,and geographic location. The fuels represented are distillate fuel oil, liquefied petroleum gas, natural gas,kerosene, electricity, wood, geothermal, coal, and solar energy.

One of the implicit assumptions embodied in the Residential Demand Module is that, through 2030, there willbe no radical changes in technology or consumer behavior. No new regulations of efficiency beyond thosecurrently embodied in law or new government programs fostering efficiency improvements are assumed.Technologies which have not gained widespread acceptance today will generally not achieve significantpenetration by 2030. Currently available technologies will evolve in both efficiency and cost. In general, atthe same efficiency level, future technologies will be less expensive than those available today in real dollarterms. When choosing new or replacement technologies, consumers will behave similarly to the way theynow behave. The intensity of end-uses will change moderately in response to price changes. Electric enduses will continue to expand, but at a decreasing rate.1

Key Assumptions

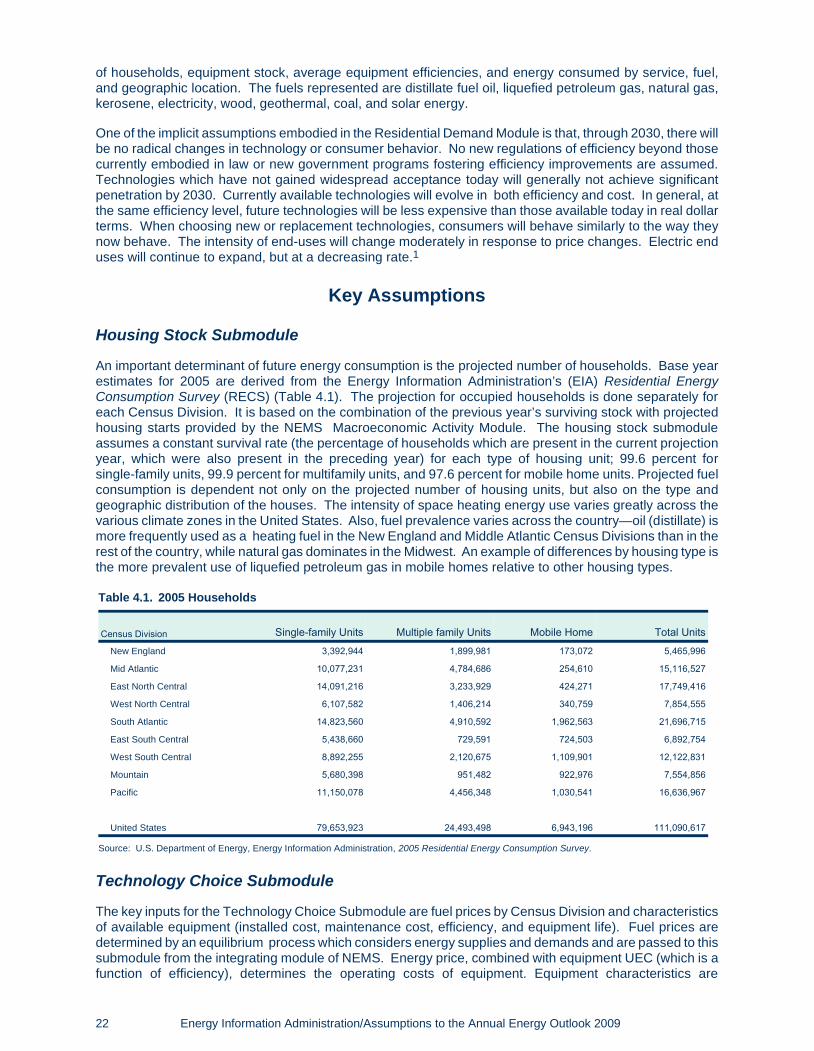

Housing Stock Submodule

An important determinant of future energy consumption is the projected number of households. Base yearestimates for 2005 are derived from the Energy Information Administration’s (EIA) Residential EnergyConsumption Survey (RECS) (Table 4.1). The projection for occupied households is done separately foreach Census Division. It is based on the combination of the previous year’s surviving stock with projectedhousing starts provided by the NEMS Macroeconomic Activity Module. The housing stock submoduleassumes a constant survival rate (the percentage of households which are present in the current projectionyear, which were also present in the preceding year) for each type of housing unit; 99.6 percent forsingle-family units, 99.9 percent for multifamily units, and 97.6 percent for mobile home units. Projected fuelconsumption is dependent not only on the projected number of housing units, but also on the type andgeographic distribution of the houses. The intensity of space heating energy use varies greatly across thevarious climate zones in the United States. Also, fuel prevalence varies across the country—oil (distillate) ismore frequently used as a heating fuel in the New England and Middle Atlantic Census Divisions than in therest of the country, while natural gas dominates in the Midwest. An example of differences by housing type isthe more prevalent use of liquefied petroleum gas in mobile homes relative to other housing types.

Technology Choice Submodule

The key inputs for the Technology Choice Submodule are fuel prices by Census Division and characteristicsof available equipment (installed cost, maintenance cost, efficiency, and equipment life). Fuel prices aredetermined by an equilibrium process which considers energy supplies and demands and are passed to thissubmodule from the integrating module of NEMS. Energy price, combined with equipment UEC (which is afunction of efficiency), determines the operating costs of equipment. Equipment characteristics are

22 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Census Division Single-family Units Multiple family Units Mobile Home Total Units

New England 3,392,944 1,899,981 173,072 5,465,996

Mid Atlantic 10,077,231 4,784,686 254,610 15,116,527

East North Central 14,091,216 3,233,929 424,271 17,749,416

West North Central 6,107,582 1,406,214 340,759 7,854,555

South Atlantic 14,823,560 4,910,592 1,962,563 21,696,715

East South Central 5,438,660 729,591 724,503 6,892,754

West South Central 8,892,255 2,120,675 1,109,901 12,122,831

Mountain 5,680,398 951,482 922,976 7,554,856

Pacific 11,150,078 4,456,348 1,030,541 16,636,967

United States 79,653,923 24,493,498 6,943,196 111,090,617

Table 4.1. 2005 Households

Source: U.S. Department of Energy, Energy Information Administration, 2005 Residential Energy Consumption Survey.

exogenous to the model and are modified to reflect both Federal standards and anticipated changes in themarket place. Table 4.2 lists capital cost and efficiency for selected residential appliances for the years 2007and 2020.

Table 4.3 provides the cost and performance parameters for representative distributed generationtechnologies. The AEO2009 model also incorporates endogenous “learning” for the residential distributedgeneration technologies, allowing for declining technology costs as shipments increase. For fuel cell andphotovoltaic systems, learning parameter assumptions for the AEO2009 reference case result in a 13percent reduction in capital costs each time the number of units shipped to the buildings sectors (residentialand commercial) doubles.

The Residential Demand Module projects equipment purchases based on a nested choice methodology.The first stage of the choice methodology determines the fuel and technology to be used, the second stagedetermines the efficiency of the selected equipment type. The equipment choices for cooling, water heating,and cooking are linked to the space heating choice for new construction. Technology and fuel choice forreplacement equipment uses a nested methodology similar to that for new construction, but includes (inaddition to the capital and installation costs of the equipment) explicit costs for technology switching (e.g.,costs for installing gas lines if switching from electricity or oil to gas, or costs for adding ductwork if switchingfrom electric resistance heat to central heating types). Also, for replacements, there is no linking of fuelchoice for water heating and cooking as is done for new construction. Technology switching uponreplacement is allowed for space heating, air conditioning, water heating, cooking and clothes drying.

Once the fuel and technology choice for a particular end use is determined, the second stage of the choicemethodology determines efficiency. In any given year, there are several available prototypes of varyingefficiency (minimum standard, medium low, medium high and highest efficiency). Efficiency choice is basedon a functional form and coefficients which give greater or lesser importance to the installed capital cost (firstcost) versus the operating cost. Generally, within a technology class, the higher the first cost, the lower theoperating cost. For new construction, efficiency choices are made based on the costs of both the heatingand cooling equipment and the building shell characteristics.

The parameters for the second stage efficiency choice are calibrated to the most recently available shipmentdata for the major residential appliances. Shipment efficiency data are obtained from industry associationswhich monitor shipments such as the Association of Home Appliance Manufacturers. Because of thiscalibration procedure, the model allows the relative importance of first cost versus operating cost to vary bygeneral technology and fuel type (e.g., natural gas furnace, electric heat pump, electric central airconditioner, etc.). Once the model is calibrated, it is possible to calculate (approximately) the apparent

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 23

Equipment TypeRelative

Performance1

2007Installed Cost

($2007)2 Efficiency3

2020Installed Cost

($2007)2 Efficiency3

Approximate Hurdle Rate

Electric Heat Pump MinimumBest

$3,800$6,700

13.017.0

$3,800$6,700

13.020.0

15%

Natural Gas Furnace MinimumBest

$1,900$3,050

0.800.96

$1,900$2,700

0.800.96

15%

Room Air Conditioner MinimumBest

$310$925

9.811.7

$310$875

9.812.0

140%

Central Air Conditioner MinimumBest

$3,000$5,700

13.021.0

$3,000$5,750

13.023.0

15%

Refrigerator (23.9 cubic ft in adjusted volume)

MinimumBest

$550$950

510417

$550$1000

510417

19%

Electric Water Heater MinimumBest

$400$1,400

0.902.4

$400$1,700

0.902.4

30%

Solar Water Heater N/A $3,500 2.0 $4,000 2.0 30%

Table 4.2. Installed Cost and Efficiency Ratings of Selected Equipment

1Minimum performance refers to the lowest efficiency equipment available. Best refers to the highest efficiency equipment available.2Installed costs are given in 2007 dollars in the original source document.3Efficiency measurements vary by equipment type. Electric heat pumps and central air conditioners are rated for cooling performance using theSeasonal Energy Efficiency Ratio (SEER); natural gas furnaces are based on Annual Fuel Utilization Efficiency; room air conditioners are based onEnergy Efficiency Ratio (EER); refrigerators are based on kilowatt-hours per year; and water heaters are based on Energy Factor (delivered Btudivided by input Btu).

Source: Navigant Consulting, EIA Technology Forecast Updates, Reference Number 20070831.1September 2007.

discount rates based on the relative weight given to the operating cost savings versus the weight given to thehigher cost of more efficient equipment. Hurdle rates in excess of 30 percent are common in the ResidentialDemand Module. The prevalence of such high apparent hurdle rates by consumers has led to the notion ofthe “efficiency gap” that is, there are many investments that could be made that provide rates of return inexcess of residential borrowing rates (15 to 20 percent for example). There are several studies whichdocument instances of apparent high discount rates.2 Once equipment efficiencies for a technology and fuelare determined, the installed efficiency for its entire stock is calculated.

Appliance Stock Submodule

The Appliance Stock Submodule is an accounting framework which tracks the quantity and averageefficiency of equipment by end use, technology, and fuel. It separately tracks equipment requirements fornew construction and existing housing units. For existing units, this module calculates equipment whichsurvives from previous years, allows certain end uses to further penetrate into the existing housing stock andcalculates the total number of units required for replacement and further penetration. Air conditioning andclothes drying are the two end uses not considered to be “fully penetrated.”

Once a piece of equipment enters into the stock, an accounting of its remaining life is begun. It is assumedthat all appliances survive a minimum number of years after installation. A fraction of appliances areremoved from the stock once they have survived for the minimum number of years. Between the minimumand maximum life expectancy, all appliances retire based on a linear decay function. For example, if anappliance has a minimum life of 5 years and a maximum life of 15 years, one tenth of the units (1 divided by15 minus 5) are retired in each of years 6 through 15. It is further assumed that, when a house is retired fromthe stock, all of the equipment contained in that house retires as well; i.e., there is no secondhand market forthis equipment. The assumptions concerning equipment lives are given in Table 4.4.

24 Energy Information Administration/Assumptions to the Annual Energy Outlook 2009

Technology Type Year of Introduction

AverageGenerating

Capacity (kW)

ElectricalEfficiency

CombinedEfficiency

(Elec. + Thermal)

Installed Capital

Cost ($2005 per

KW of Capacity)1

ServiceLife

Years

Solar Photovoltaic

2007 3.0 0.16 N/A $8,930 30

2010 3.5 0.18 N/A $8,467 30

2015 4.0 0.20 N/A $7,310 30

2020 5.0 0.22 N/A $6,154 30

2030 5.0 0.25 N/A $3,840 30

Fuel Cell 2007 10 0.308 0.697 $8,062 20

2010 10 0.320 0.699 $6,199 20

2015 10 0.335 0.705 $4,819 20

2020 10 0.350 0.712 $3,440 20

2030 10 0.360 0.723 $1,886 20

Table 4.3. Capital Cost and Performance Parameters of Selected Residential Distributed Generation Technologies

1Installed costs are given in 2005 dollars in the original source document.

Source: Solar Technology Specifications: Solar Energy Industries Association, Our Solar Power Future - The U.S. Photovoltaic Industry Roadmapthrough 2030 and Beyond (SEIA, September 2004). Fuel cells: Discovery Insights, LLC, "Installed Costs for Small CHP Systems - Estimates andProjections" (April 2005).

Fuel Consumption SubmoduleEnergy consumption is calculated by multiplying the vintage equipment stocks by their respective UECs.The UECs include adjustments for the average efficiency of the stock vintages, short term price elasticity ofdemand and “rebound” effects on usage (see discussion below), the size of new construction relative to theexisting stock, people per household and shell efficiency and weather effects (space heating and cooling).The various levels of aggregated consumption (consumption by fuel, by service, etc.) are derived from thesedetailed equipment-specific calculations.

Equipment Efficiency

The average energy consumption of a particular technology is initially based on estimates derived fromRECS 2005. Appliance efficiency is either derived from a long history of shipment data (e.g., the efficiency ofconventional air-source heat pumps) or assumed based on engineering information concerning typicalinstalled equipment (e.g., the efficiency of ground-source heat pumps). When the average efficiency iscomputed from shipment data, shipments going back as far as 20 to 30 years are combined withassumptions concerning equipment lifetimes. This allows for not only an average efficiency to becalculated, but also for equipment retirements to be vintaged—older equipment tends to be lower inefficiency and also tends to get retired before newer, more efficient equipment. Once equipment is retired,the Appliance Stock and Technology Choice Modules determine the efficiency of the replacementequipment. It is often the case that the retired equipment is replaced by substantially more efficientequipment.

As the stock efficiency changes over the simulation interval, energy consumption decreases in inverseproportion to efficiency. Also, as efficiency increases, the efficiency rebound effect (discussed below) willoffset some of the reductions in energy consumption by increased demand for the end-use service. Forexample, if the stock average for electric heat pumps is now 10 percent more efficient than in 2005, then allelse constant (weather, real energy prices, shell efficiency, etc.), energy consumption per heat pump wouldaverage about only 9 percent less.

Adjusting for the Size of Housing Units

Information derived from RECS 2005 indicates that new construction (post-1990) is on average roughly 26percent larger than the existing stock of housing. Estimates for the size of each new home built in theprojection period vary by type and region, and are determined by a log-trend projection based on historicaldata from the Bureau of the Census.3 For existing structures, it is assumed that about 1 percent ofhouseholds that existed in 2005 add about 600 square feet to the heated floor space in each year of theprojection period.4 The energy consumption for space heating, air conditioning, and lighting is assumed toincrease with the square footage of the structure. This results in an increase in the average size of thehousing stock from 1,632 to 1,934 square feet from 2005 through 2030.

Energy Information Administration/Assumptions to the Annual Energy Outlook 2009 25

Equipment Minimum Life Maximum Life

Heat Pumps 7 21

Central Forced-Air Furnaces 10 25

Hydronic Space Heaters 20 30

Room Air Conditioners 8 16

Central Air Conditioners 7 21

Gas Water Heaters 4 14

Electric Water Heaters 5 22

Cooking Stoves 16 21

Clothes Dryers 11 20

Refrigerators 7 26

Freezers 11 31

Table 4.4. Minimum and Maximum Life Expectancies of Equipment

Source: Lawrence Berkeley Laboratory, Baseline Data for the Residential Sector and Development of a Residential Forecasting Database, May1994, and analysis of RECS 2001 data.

Adjusting for Weather and Climate