Assumption Governance and Management - SOA · PDF fileSession 93: Assumption Governance and...

46

Session 93 PD, Assumption Governance and Management Moderator: Matthew P. Clark, FSA, CERA, MAAA Presenters: Matthew P. Clark, FSA, CERA, MAAA Nick Fiechter, FSA, MAAA Maria Rose Itteilag; Theresa M. Resnick, FSA, MAAA SOA Antitrust Disclaimer SOA Presentation Disclaimer

Transcript of Assumption Governance and Management - SOA · PDF fileSession 93: Assumption Governance and...

Session 93 PD, Assumption Governance and Management

Moderator:

Matthew P. Clark, FSA, CERA, MAAA

Presenters: Matthew P. Clark, FSA, CERA, MAAA

Nick Fiechter, FSA, MAAA Maria Rose Itteilag;

Theresa M. Resnick, FSA, MAAA

SOA Antitrust Disclaimer SOA Presentation Disclaimer

Session 93: Assumption Governance and ManagementAdvantages of a Formal Assumption Process Framework

Matthew Clark, FSA, MAAA, CERA, CFAMaria Itteilag

Society of Actuaries – 2016 Annual Meeting

October 25, 2016

Copyright © 2016 Deloitte Development LLC. All rights reserved. 2

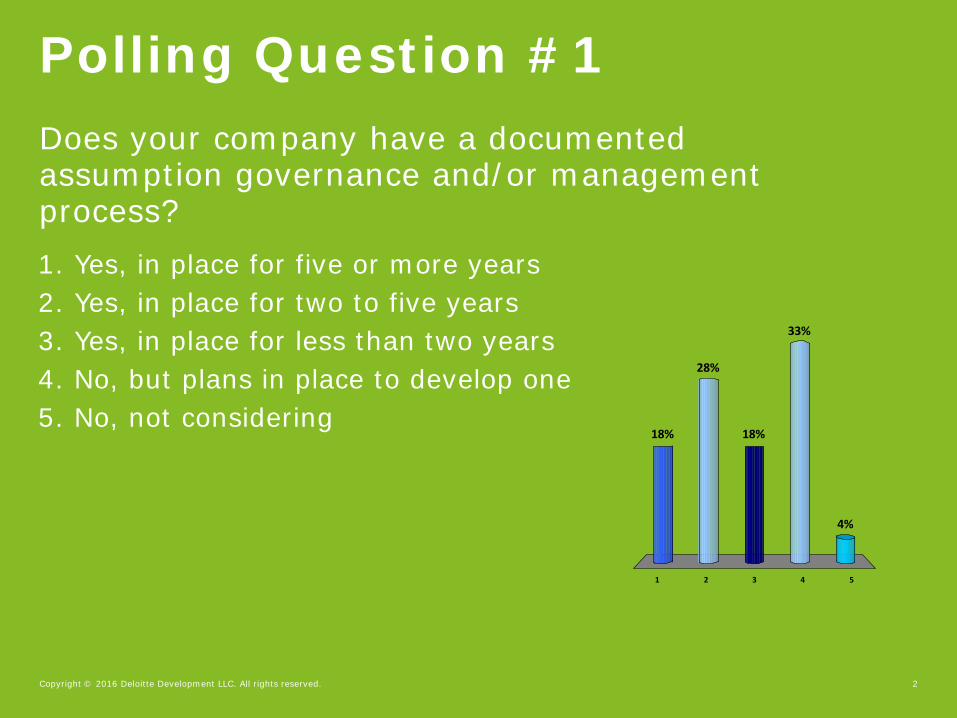

Polling Question #1Does your company have a documented assumption governance and/or management process?

1 2 3 4 5

18%

28%

4%

33%

18%

1. Yes, in place for five or more years2. Yes, in place for two to five years3. Yes, in place for less than two years4. No, but plans in place to develop one5. No, not considering

Copyright © 2016 Deloitte Development LLC. All rights reserved. 3

What is driving the opportunity for a change in an insurer’s approach for managing and setting actuarial assumptions?

Challenges Impacting Insurers

• Evolving and changing regulatory requirements

• Increased requests from multiple stakeholders

• Appetite for insight into results and expectations

• Organizational structures are fragmented and processes outdated

• Lack of consistency across assumptions and their use

• Inconsistent tools and data used to support assumption setting process

• Lack of credible data

• Incomplete and inconsistent documentation

• Ability to reproduce process and/or results over time

• Multiple locations and/or jurisdictions

Macro Challenges Micro Challenges

Too many cooks and too many kitchens

Copyright © 2016 Deloitte Development LLC. All rights reserved. 4

Who are the key stakeholders interested in assumptions and why?

Interested Parties in Assumptions

Appointed Actuary

Chief Actuary

CRO / Risk

Pricing Executive

CFO / Finance

CAO / Controller

Stakeholder

• GAAP financial accuracy• Earnings stability

• GAAP best estimate• Financial plan (e.g.

sales)

• Solvency• Statutory compliance

• Cash Flow Testing• Prudent best estimate

(e.g. AG 43)

• Profitability • New business

• Overall compliance and accuracy

• All actuarial

• Statutory capital compliance

• Risk mitigation and tail risk

• Economic capital• Embedded value

• Compliance • External auditor

Area of Concern Area of Focus

Copyright © 2016 Deloitte Development LLC. All rights reserved. 5

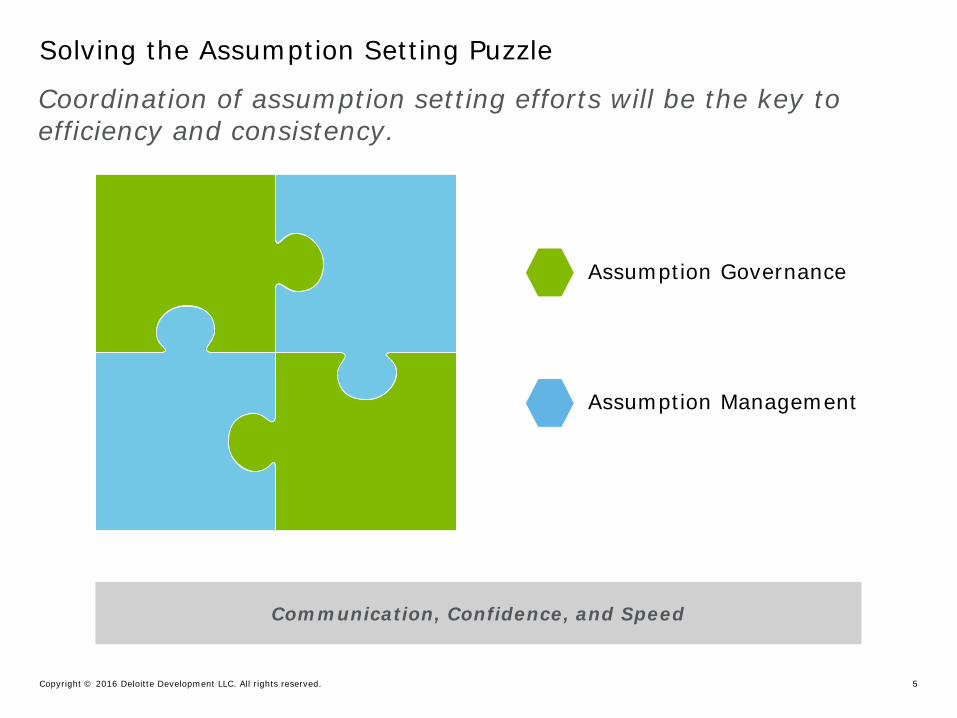

Coordination of assumption setting efforts will be the key to efficiency and consistency.

Solving the Assumption Setting Puzzle

Communication, Confidence, and Speed

Assumption Governance

Assumption Management

Copyright © 2016 Deloitte Development LLC. All rights reserved. 6

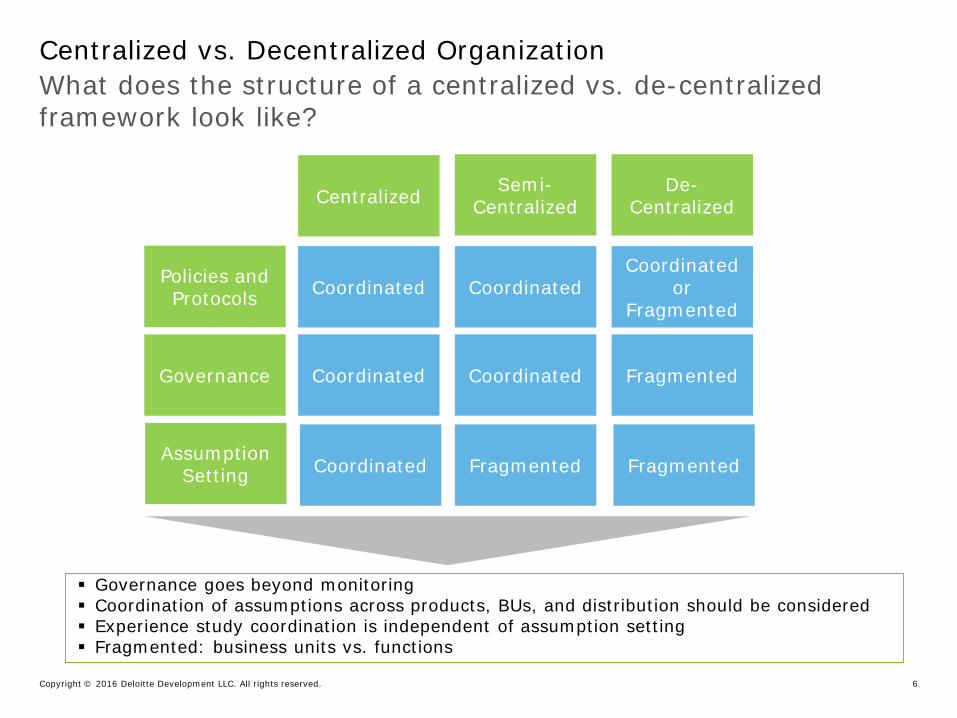

What does the structure of a centralized vs. de-centralized framework look like?

Centralized vs. Decentralized Organization

Coordinated CoordinatedCoordinated

or Fragmented

Coordinated Fragmented Fragmented

Coordinated Coordinated Fragmented

Policies and Protocols

Centralized Semi-Centralized

De-Centralized

Governance

Assumption Setting

Governance goes beyond monitoring Coordination of assumptions across products, BUs, and distribution should be considered Experience study coordination is independent of assumption setting Fragmented: business units vs. functions

Copyright © 2016 Deloitte Development LLC. All rights reserved. 7

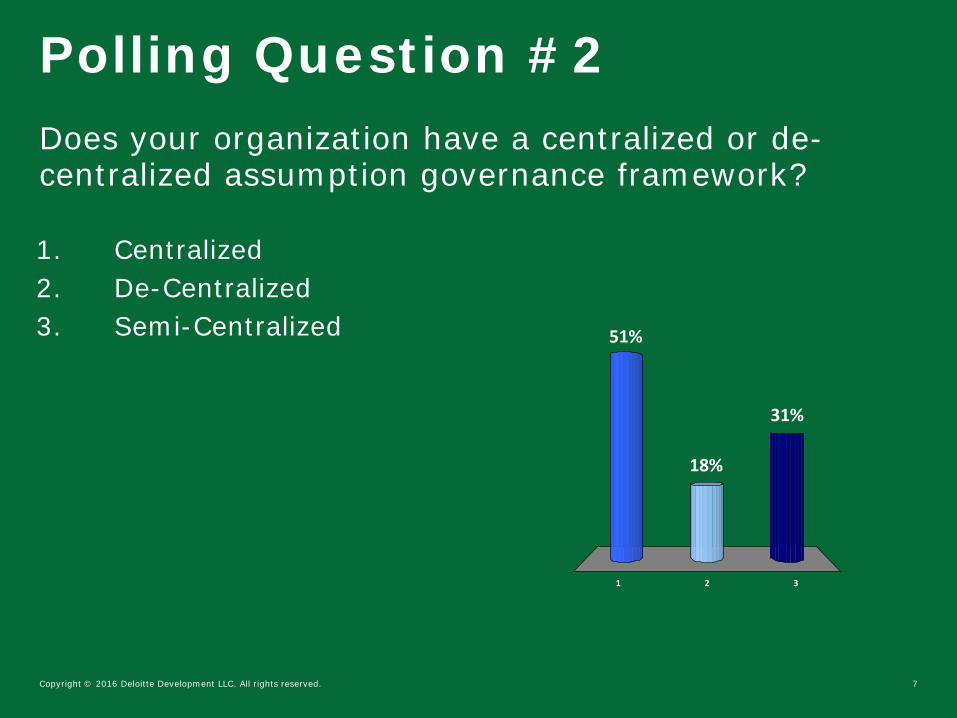

Polling Question #2Does your organization have a centralized or de-centralized assumption governance framework?

1 2 3

51%

31%

18%

1. Centralized2. De-Centralized3. Semi-Centralized

Assumption Governance

Copyright © 2016 Deloitte Development LLC. All rights reserved. 9

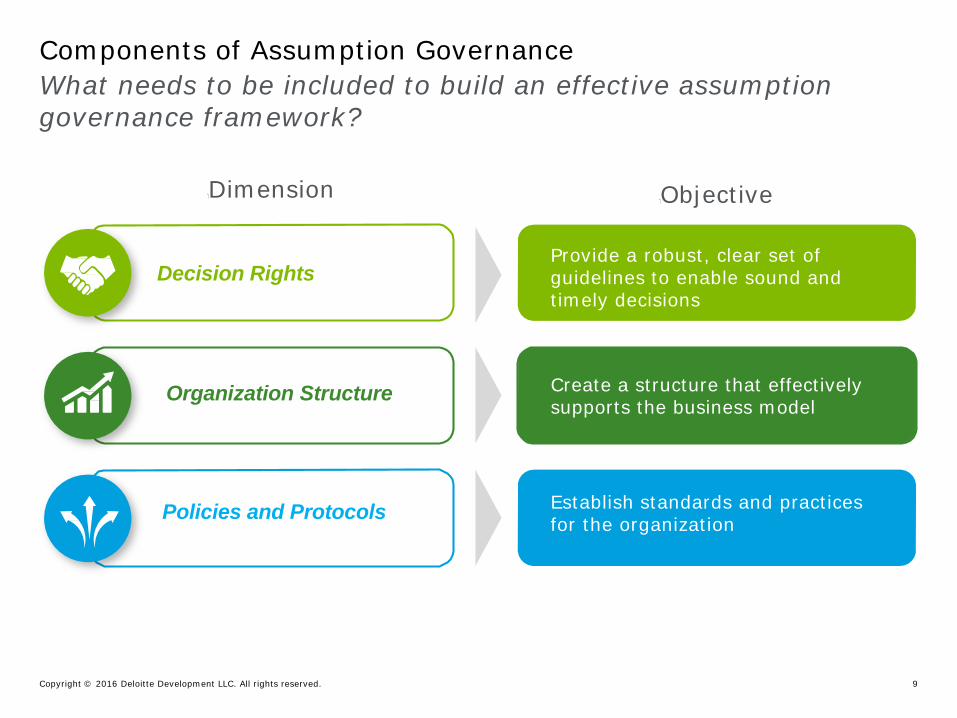

What needs to be included to build an effective assumption governance framework?

Components of Assumption Governance

Decision Rights

Create a structure that effectively supports the business model

Establish standards and practices for the organization

Provide a robust, clear set of guidelines to enable sound and timely decisions

Organization Structure

Policies and Protocols

DimensionObjective

Copyright © 2016 Deloitte Development LLC. All rights reserved. 10

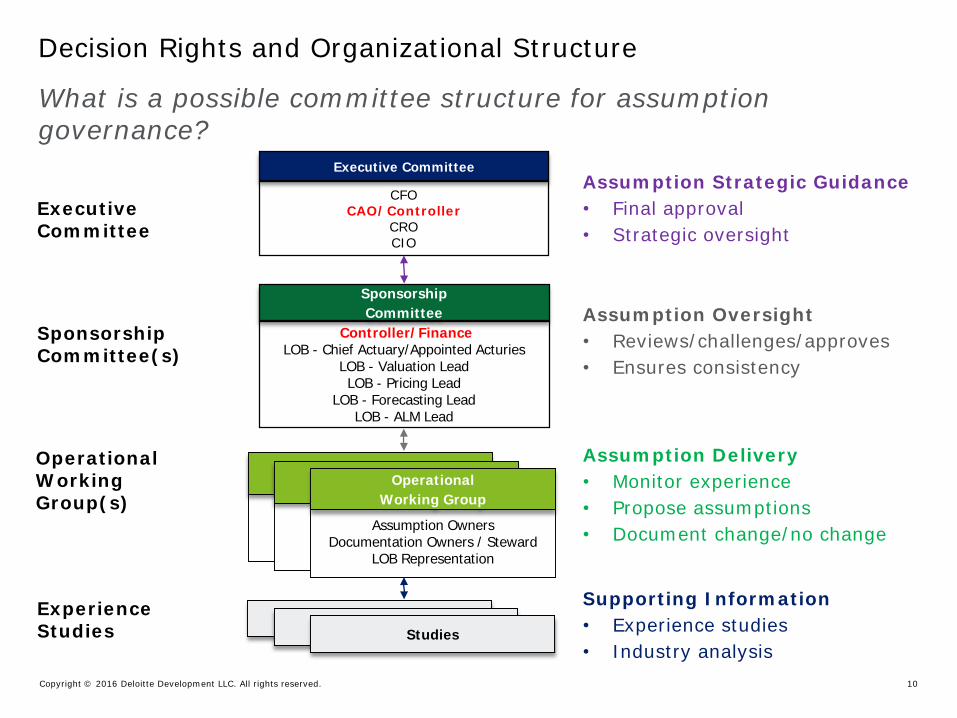

Decision Rights and Organizational Structure

Chief ActuaryValuation LeadPricing Lead

Forecasting LeadALM Lead

CFOCAO/Controller

CROCIO

Sponsorship Committee(s)

OperationalWorking Group(s)

Controller/FinanceLOB - Chief Actuary/Appointed Acturies

LOB - Valuation LeadLOB - Pricing Lead

LOB - Forecasting LeadLOB - ALM Lead

Sponsorship Committee

Executive Committee

Executive Committee

Experience Studies

Chief ActuaryValuation LeadPricing Lead

Forecasting LeadALM Lead

Assumption OwnersDocumentation Owners / Steward

LOB Representation

Operational Working Group

What is a possible committee structure for assumption governance?

Assumption Delivery• Monitor experience• Propose assumptions• Document change/no change

Assumption Oversight• Reviews/challenges/approves• Ensures consistency

Assumption Strategic Guidance• Final approval• Strategic oversight

Studies

Supporting Information• Experience studies• Industry analysis

Copyright © 2016 Deloitte Development LLC. All rights reserved. 11

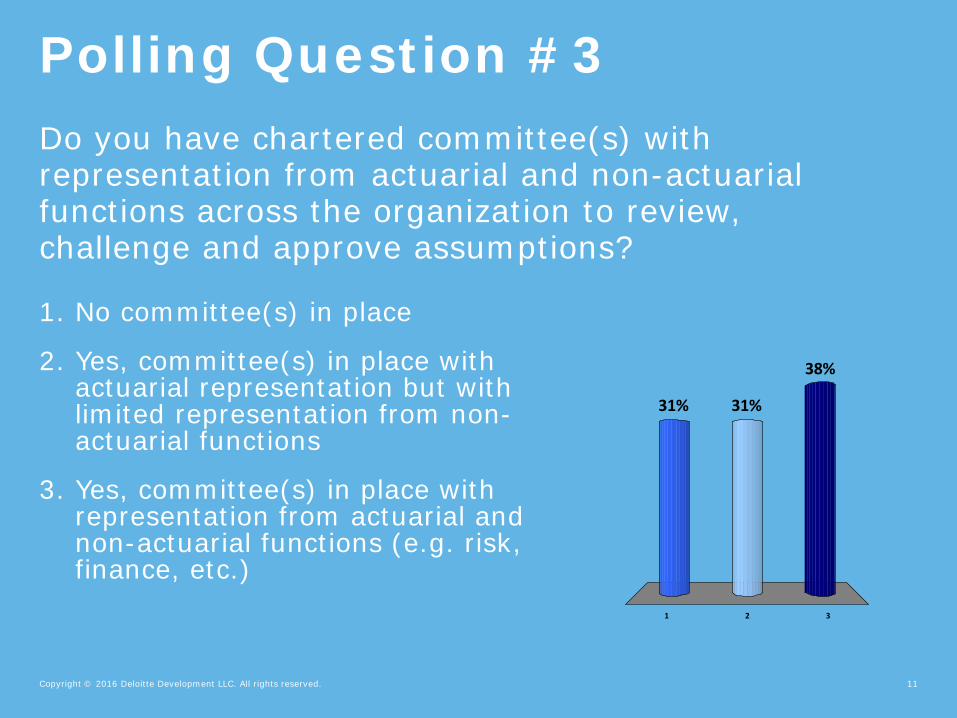

Polling Question #3Do you have chartered committee(s) with representation from actuarial and non-actuarial functions across the organization to review, challenge and approve assumptions?

1 2 3

31%

38%

31%

1. No committee(s) in place

2. Yes, committee(s) in place with actuarial representation but with limited representation from non-actuarial functions

3. Yes, committee(s) in place with representation from actuarial and non-actuarial functions (e.g. risk, finance, etc.)

Copyright © 2016 Deloitte Development LLC. All rights reserved. 12

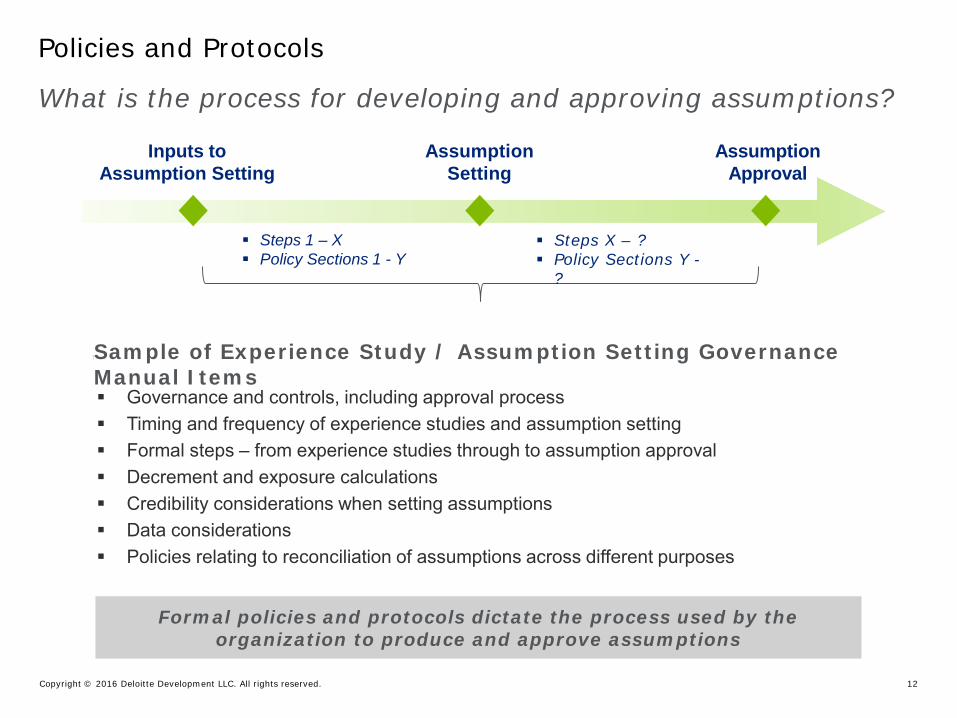

Policies and Protocols

What is the process for developing and approving assumptions?

Formal policies and protocols dictate the process used by the organization to produce and approve assumptions

Inputs to Assumption Setting

Assumption Setting

Assumption Approval

Governance and controls, including approval process Timing and frequency of experience studies and assumption setting Formal steps – from experience studies through to assumption approval Decrement and exposure calculations Credibility considerations when setting assumptions Data considerations Policies relating to reconciliation of assumptions across different purposes

Steps 1 – X Policy Sections 1 - Y

Steps X – ? Policy Sections Y -

?

Sample of Experience Study / Assumption Setting GovernanceManual Items

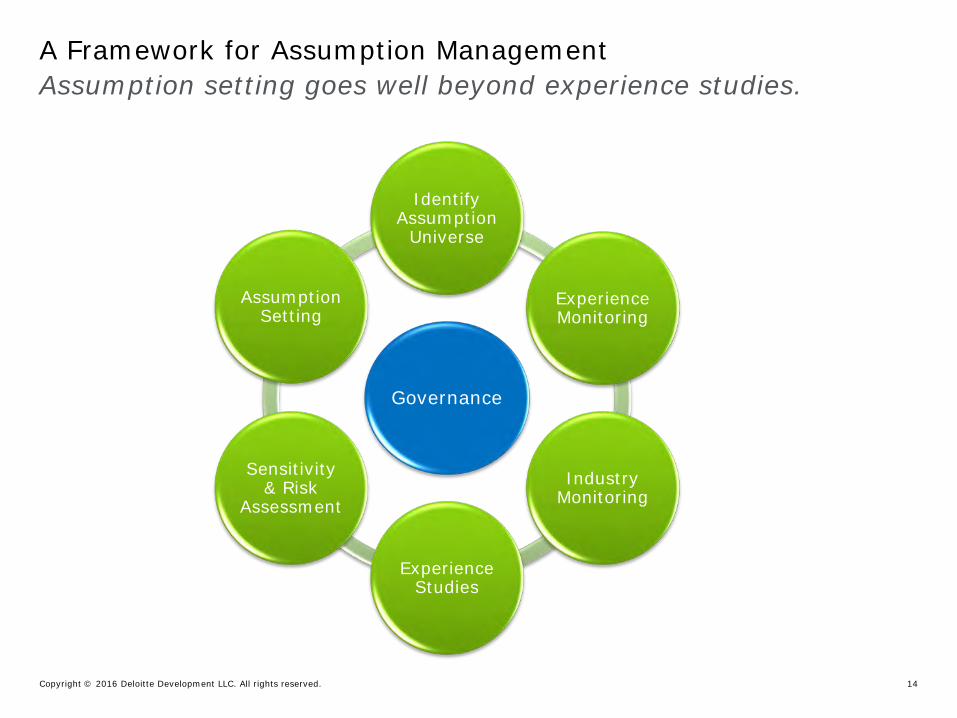

Assumption Management

Copyright © 2016 Deloitte Development LLC. All rights reserved. 14

Assumption setting goes well beyond experience studies. A Framework for Assumption Management

Governance

Identify Assumption

Universe

Experience Monitoring

Industry Monitoring

Experience Studies

Sensitivity & Risk

Assessment

Assumption Setting

Copyright © 2016 Deloitte Development LLC. All rights reserved. 15

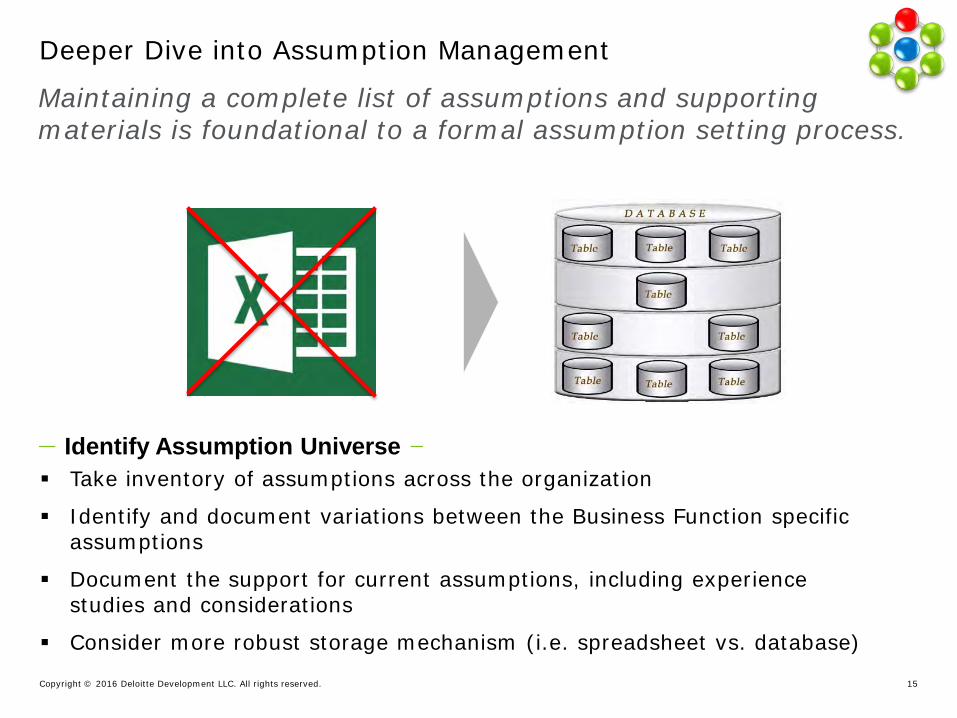

Maintaining a complete list of assumptions and supporting materials is foundational to a formal assumption setting process.

Deeper Dive into Assumption Management

Identify Assumption Universe Take inventory of assumptions across the organization

Identify and document variations between the Business Function specific assumptions

Document the support for current assumptions, including experience studies and considerations

Consider more robust storage mechanism (i.e. spreadsheet vs. database)

Copyright © 2016 Deloitte Development LLC. All rights reserved. 16

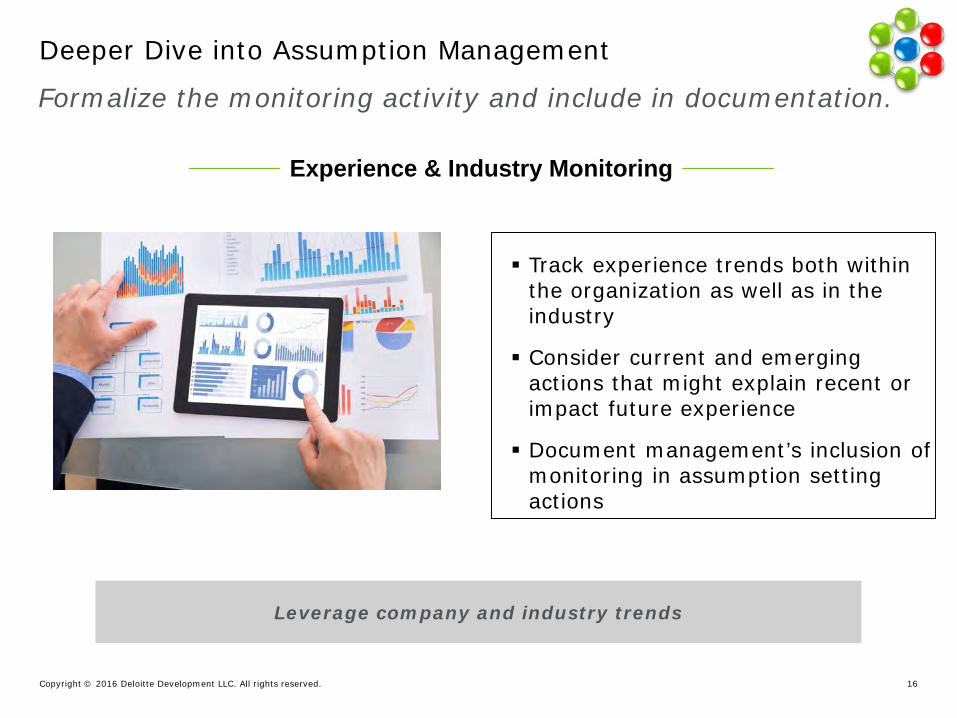

Deeper Dive into Assumption Management

Formalize the monitoring activity and include in documentation.

Leverage company and industry trends

Track experience trends both within the organization as well as in the industry

Consider current and emerging actions that might explain recent or impact future experience

Document management’s inclusion of monitoring in assumption setting actions

Experience & Industry Monitoring

Copyright © 2016 Deloitte Development LLC. All rights reserved. 17

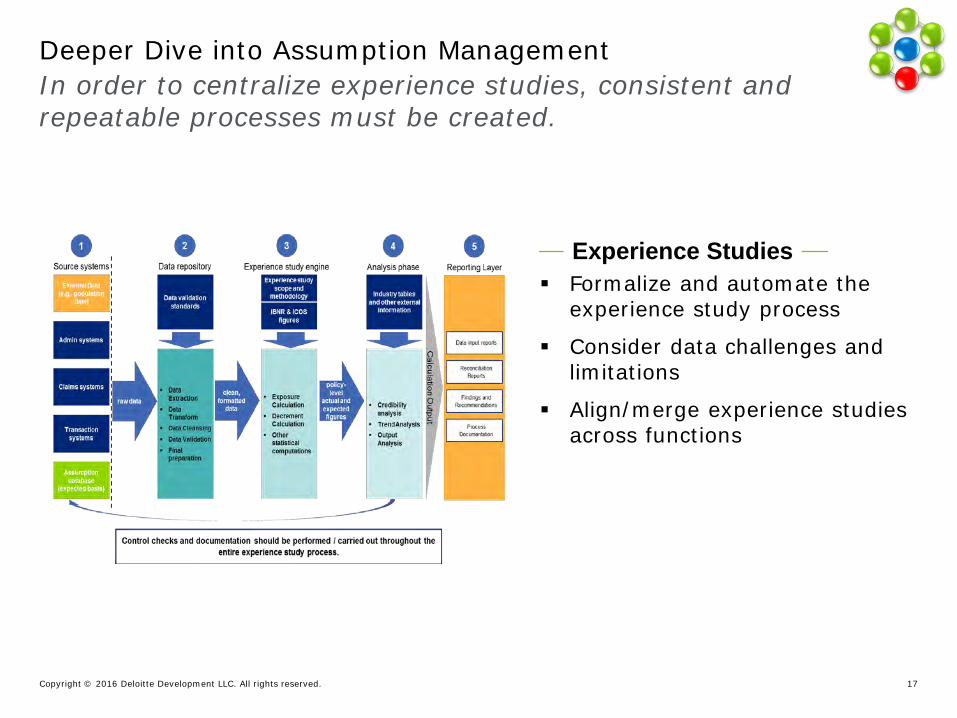

In order to centralize experience studies, consistent and repeatable processes must be created.

Deeper Dive into Assumption Management

Experience Studies Formalize and automate the

experience study process

Consider data challenges and limitations

Align/merge experience studies across functions

Copyright © 2016 Deloitte Development LLC. All rights reserved. 18

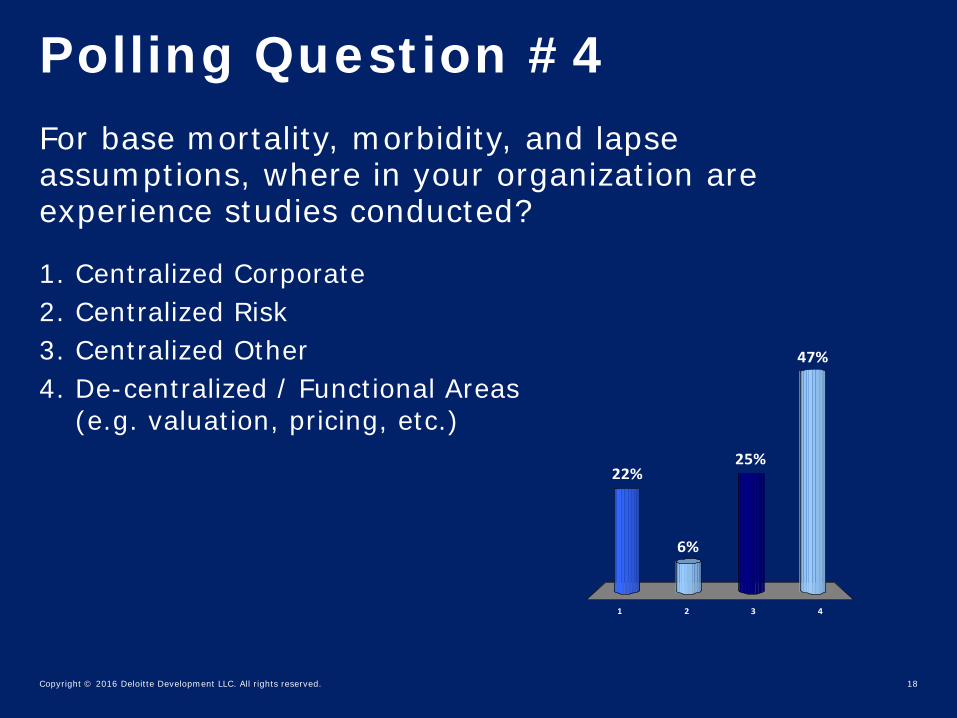

Polling Question #4For base mortality, morbidity, and lapse assumptions, where in your organization are experience studies conducted?

1 2 3 4

22%

47%

25%

6%

1. Centralized Corporate2. Centralized Risk3. Centralized Other4. De-centralized / Functional Areas

(e.g. valuation, pricing, etc.)

Copyright © 2016 Deloitte Development LLC. All rights reserved. 19

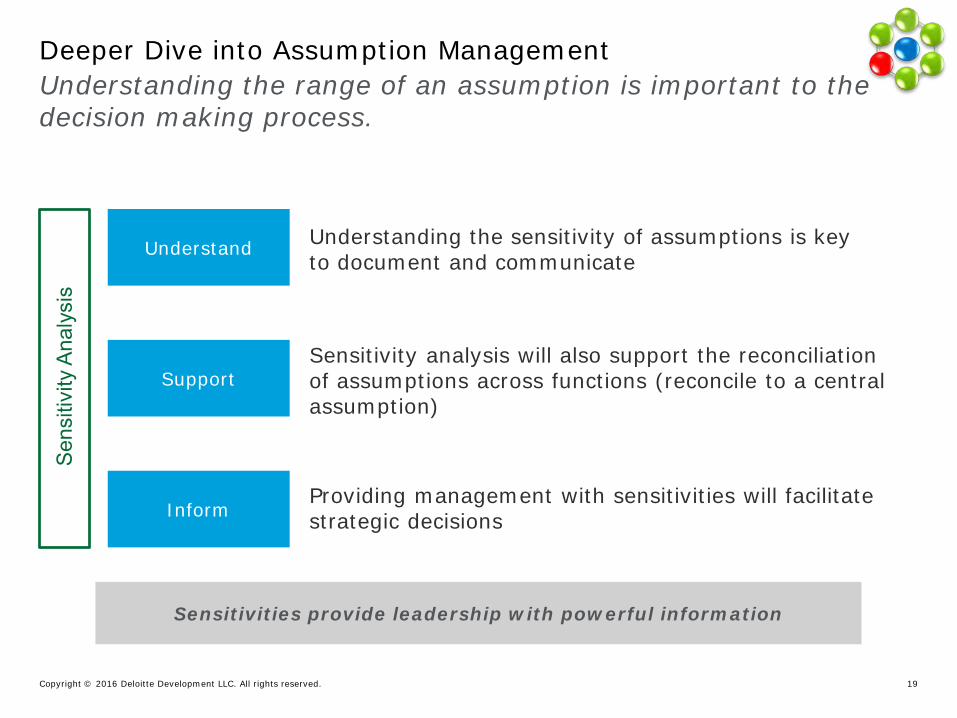

Understanding the range of an assumption is important to the decision making process.

Deeper Dive into Assumption Management

Understanding the sensitivity of assumptions is key to document and communicate

Providing management with sensitivities will facilitate strategic decisions

Sensitivity analysis will also support the reconciliation of assumptions across functions (reconcile to a central assumption)

Sens

itivi

ty A

naly

sis

Sensitivities provide leadership with powerful information

Understand

Inform

Support

Copyright © 2016 Deloitte Development LLC. All rights reserved. 20

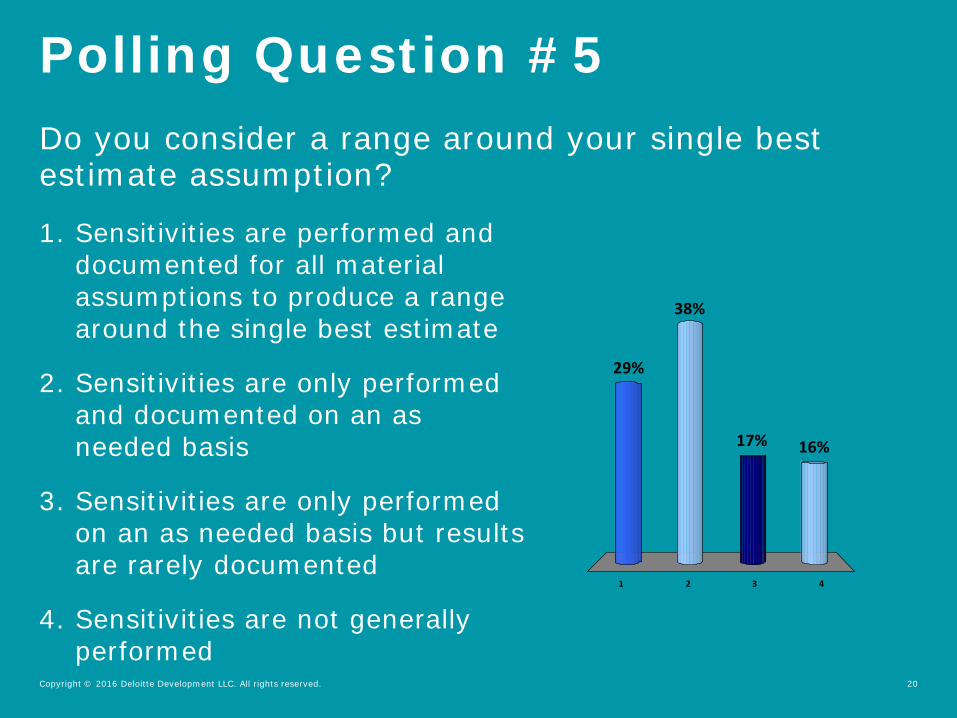

Polling Question #5Do you consider a range around your single best estimate assumption?

1 2 3 4

29%

16%17%

38%

1. Sensitivities are performed and documented for all material assumptions to produce a range around the single best estimate

2. Sensitivities are only performed and documented on an as needed basis

3. Sensitivities are only performed on an as needed basis but results are rarely documented

4. Sensitivities are not generally performed

Copyright © 2016 Deloitte Development LLC. All rights reserved. 21

HR & Talent Strategy

Do you have comprehensive HR & Talent strategies in place?

Quality of Hire

Are you attracting and hiring the right people?

Organization & Governance

Are your HR and Talent functions staffed and organized to deliver

high-quality services?

Stakeholders

Who are the interested parties?

Communication

How will assumptions be disseminated once developed

and approved?

Change Management

How will the new assumptions be utilized and placed into actuarial

systems?

Technology

Do you know the technology optionsavailable to you to manage your

human capital?

Talent Capabilities

Do you have the right talent, skills,and capabilities in the workforce?

HR & Talent Analytics

Are you tracking and analyzing the right information effectively?

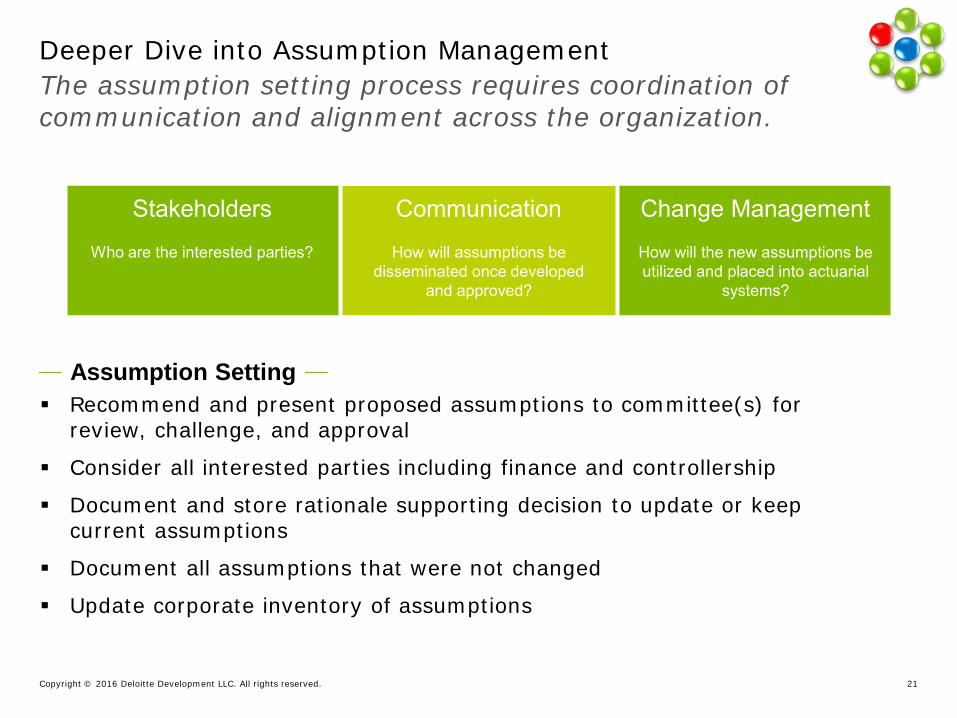

The assumption setting process requires coordination of communication and alignment across the organization.

Deeper Dive into Assumption Management

Assumption Setting Recommend and present proposed assumptions to committee(s) for

review, challenge, and approval

Consider all interested parties including finance and controllership

Document and store rationale supporting decision to update or keep current assumptions

Document all assumptions that were not changed

Update corporate inventory of assumptions

Copyright © 2016 Deloitte Development LLC. All rights reserved. 22

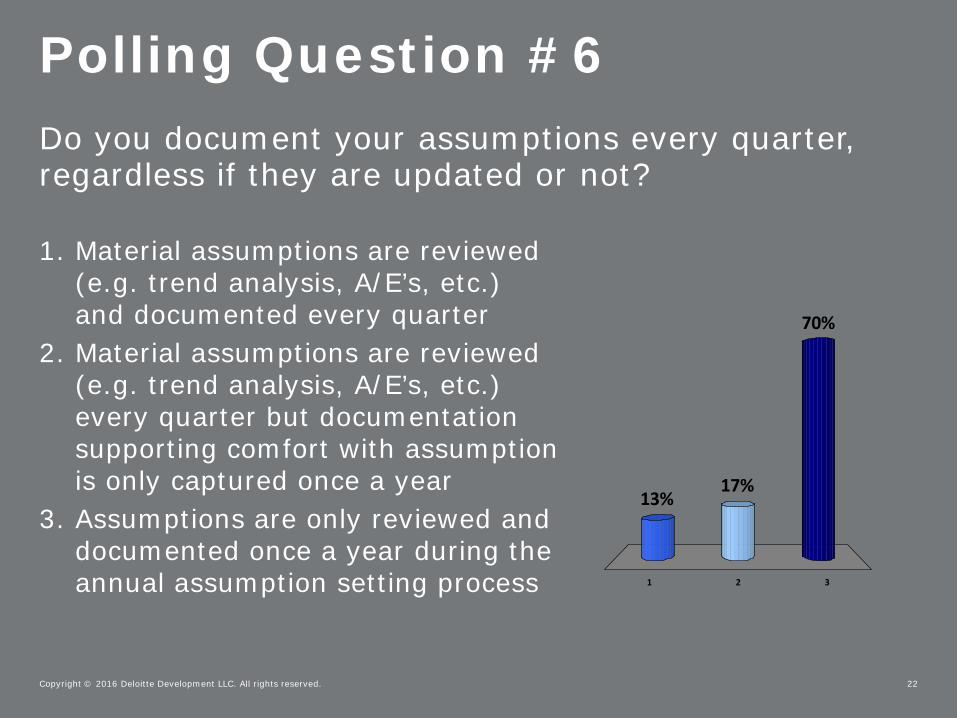

Polling Question #6Do you document your assumptions every quarter, regardless if they are updated or not?

1 2 3

13%

70%

17%

1. Material assumptions are reviewed (e.g. trend analysis, A/E’s, etc.) and documented every quarter

2. Material assumptions are reviewed (e.g. trend analysis, A/E’s, etc.) every quarter but documentation supporting comfort with assumption is only captured once a year

3. Assumptions are only reviewed and documented once a year during the annual assumption setting process

Copyright © 2016 Deloitte Development LLC. All rights reserved. 23

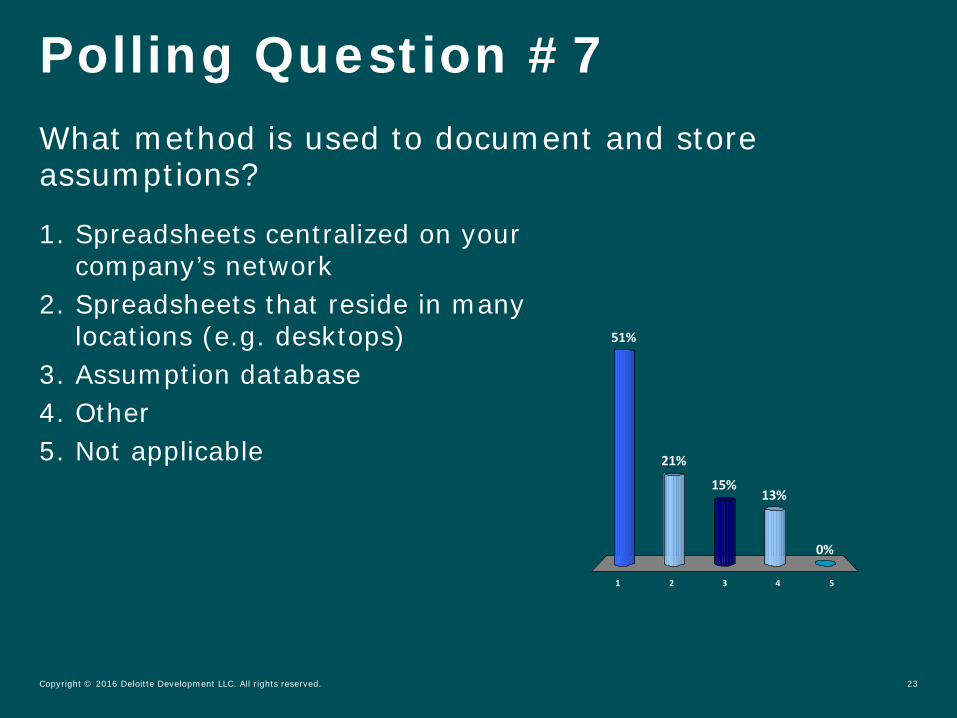

Polling Question #7What method is used to document and store assumptions?

1 2 3 4 5

51%

21%

0%

13%15%

1. Spreadsheets centralized on your company’s network

2. Spreadsheets that reside in many locations (e.g. desktops)

3. Assumption database4. Other5. Not applicable

Copyright © 2016 Deloitte Development LLC. All rights reserved. 24

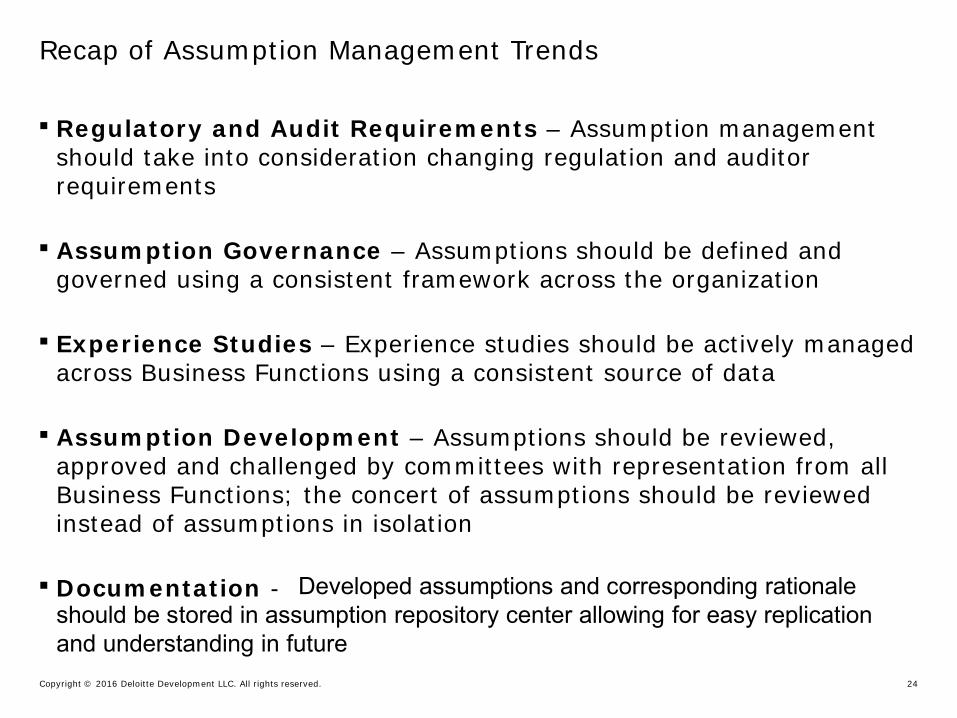

Recap of Assumption Management Trends

Regulatory and Audit Requirements – Assumption management should take into consideration changing regulation and auditor requirements

Assumption Governance – Assumptions should be defined and governed using a consistent framework across the organization

Experience Studies – Experience studies should be actively managed across Business Functions using a consistent source of data

Assumption Development – Assumptions should be reviewed, approved and challenged by committees with representation from all Business Functions; the concert of assumptions should be reviewed instead of assumptions in isolation

Documentation - Developed assumptions and corresponding rationale should be stored in assumption repository center allowing for easy replication and understanding in future

Copyright © 2016 Deloitte Development LLC. All rights reserved.

About Deloitte - Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

This publication contains general information only, and none of the member firms of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collective, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

Theresa Resnick,VP and Appointed ActuaryAllstate Life Companies

Session 93, Assumption Governance and ManagementOctober 25, 2016

27

+//G_L#%@-//(a-b)

28

“We got it from Product.”

29

30

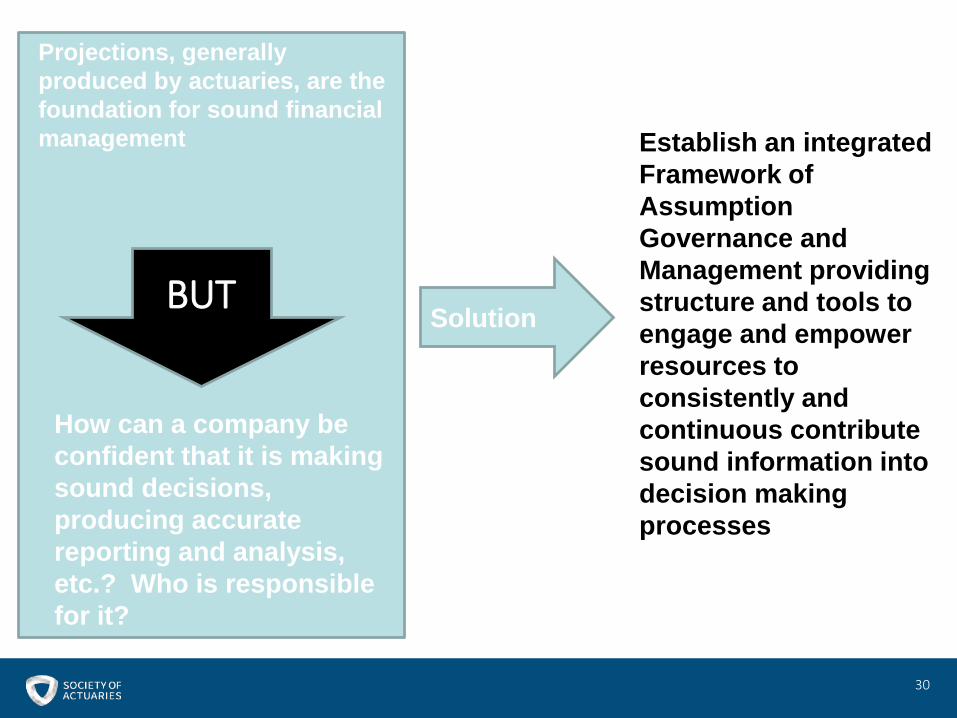

Projections, generally produced by actuaries, are the foundation for sound financial management

How can a company be confident that it is making sound decisions, producing accurate reporting and analysis, etc.? Who is responsible for it?

Solution

Establish an integrated Framework of Assumption Governance and Management providing structure and tools to engage and empower resources to consistently and continuous contribute sound information into decision making processes

BUT

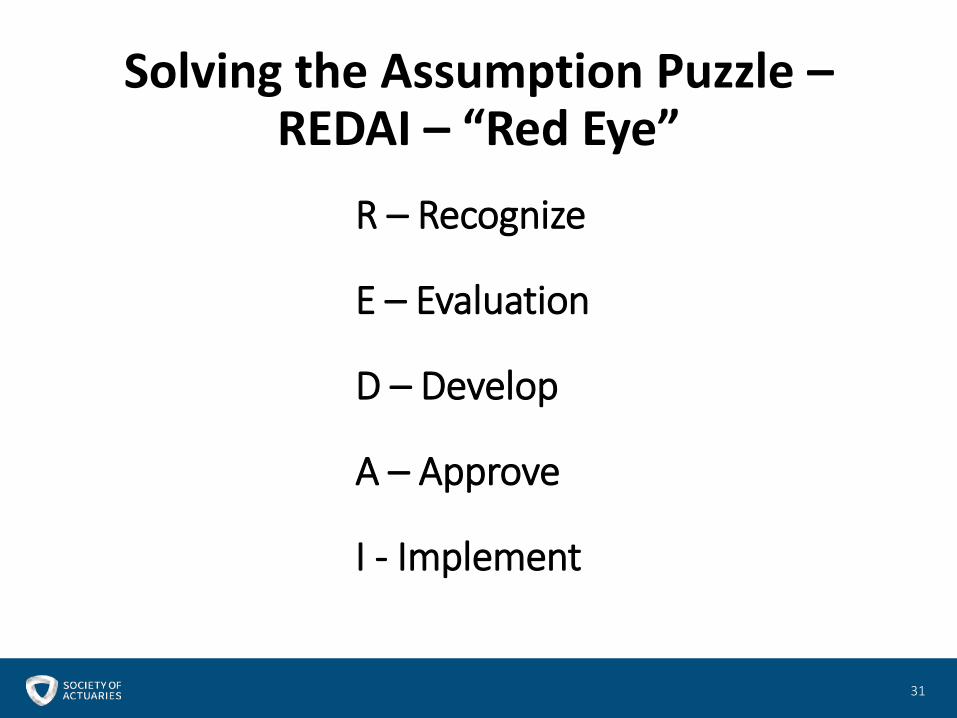

Solving the Assumption Puzzle –REDAI – “Red Eye”

31

R – Recognize

E – Evaluation

D – Develop

A – Approve

I - Implement

Solving the Assumption Puzzle

32

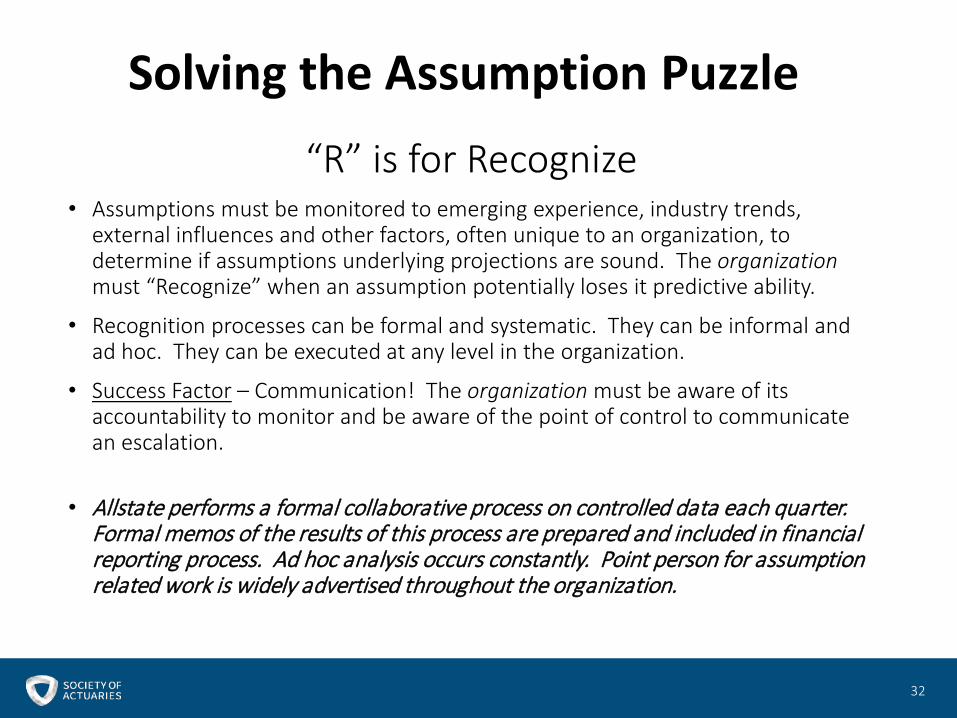

“R” is for Recognize• Assumptions must be monitored to emerging experience, industry trends,

external influences and other factors, often unique to an organization, to determine if assumptions underlying projections are sound. The organizationmust “Recognize” when an assumption potentially loses it predictive ability.

• Recognition processes can be formal and systematic. They can be informal and ad hoc. They can be executed at any level in the organization.

• Success Factor – Communication! The organization must be aware of its accountability to monitor and be aware of the point of control to communicate an escalation.

• Allstate performs a formal collaborative process on controlled data each quarter. Formal memos of the results of this process are prepared and included in financial reporting process. Ad hoc analysis occurs constantly. Point person for assumption related work is widely advertised throughout the organization.

33

“E” is for Evaluate• When an organization “Recognizes” that an assumption has the potential to

produce misleading analysis, the assumption is escalated to “Evaluate.” Internal data, external data, trends, external factors, etc. are evaluated to determine if the assumption should be replaced.

• Evaluation processes can be quick and informal. They can be complex and elaborate. They can be executed at any level in the organization.

• Success Factor – Sound Data and Analysis! Data and analysis must be controlled and internally consistent with its expected projection capabilities.

• Allstate generally performs a evaluation following company protocols once an assumption is escalated. An evaluation is a formal study, with data validated to controlled sources, vetted by experts and peer reviewers, with the study documented following company protocols. Protocols developed in house and in conjunction with audit partners satisfying both external reporting requirements and internal management due diligence.

Solving the Assumption Puzzle

34

“D” is for Develop• An “Evaluation” does not necessarily result in a revised assumption. A new

assumption may be “Developed” to replace an assumption which no longer is predictive.

• Assumption may be “Developed” from internal and external data, may be industry data, or any number of methods to produce sound projections.

• Success Factor – Rationale! Documentation must provide the rationale to support the predictability of the assumption and the model.

• Allstate develops assumptions using many different methods. Assumption Development is formally documented, vetted by experts and peer reviewers, following company protocols. Protocols developed in house and in conjunction with audit partners satisfying both external reporting requirements and internal management due diligence.

Solving the Assumption Puzzle

35

“A” is for Approve• Management is accountable for the activity of its organization. Though

management is accountable, it cannot perform all activities. Management can establish a source of assumptions for use in projections and require its use. Management “approves” assumptions and provides a control framework for the use of these assumptions in projections.

• Success Factor – Accountability, Control and Empowerment! Practitioners understand self accountability for the soundness of projections. Processes are established and controls performed to assure that projections are based on the set of assumptions approved for use. Practitioners are empowered to select assumptions with any deviations from approved assumptions disclosed to management.

• Allstate approves assumptions through a committee reporting its actions to the Board. Practitioners have the ultimate accountability for projections produced and are empowered to select assumptions. Deviations from assumptions are disclosed with supporting rationale to the approval committee. Appointed Actuary reports deviations directly to the Board.

Solving the Assumption Puzzle

36

“I” is for Implement• Newly Developed assumptions must be carefully implemented into an

organizations projection processes.

• Success Factor – Control and Internal Consistency! Communication processes for use of an assumption are controlled. Addition of the assumption into a projection model must be controlled. Sound judgment regarding the internal consistency of the assumption into a model must be controlled.

• Allstate implements assumptions through the Gatekeeper Communication Tool thoroughly tracking assumption through the REDAI process, with final communication to the governing committee on the Implementation success. Model Assumption Change Controls are formally executed. Approved assumptions are stored in a centralized production Assumptions Management Systems Database.

Solving the Assumption Puzzle

37

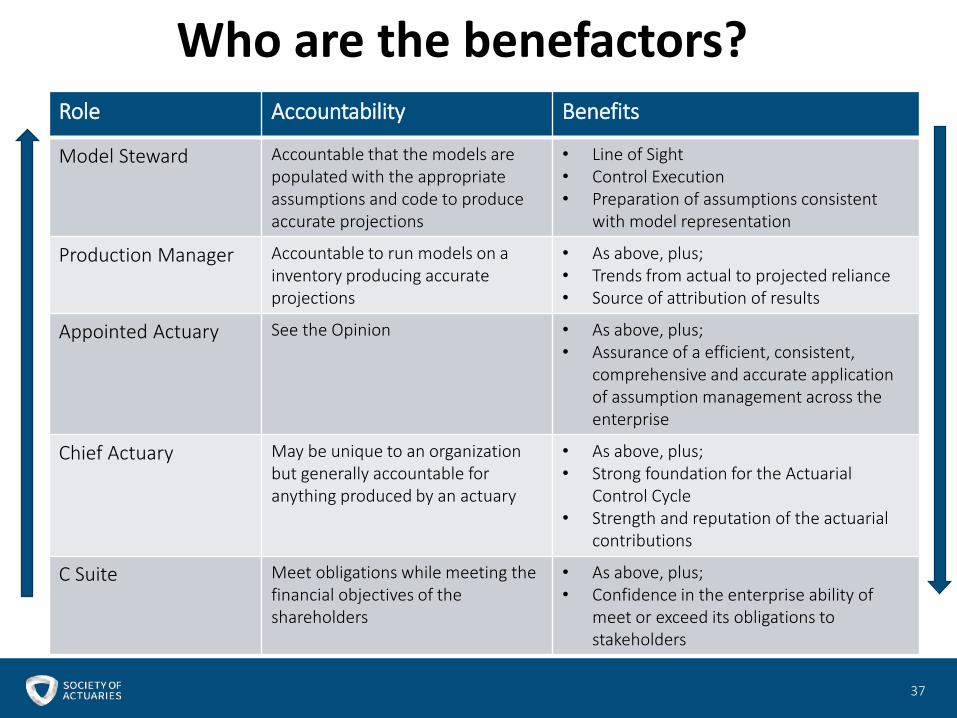

Who are the benefactors?Role Accountability Benefits

Model Steward Accountable that the models are populated with the appropriate assumptions and code to produce accurate projections

• Line of Sight• Control Execution• Preparation of assumptions consistent

with model representation

Production Manager Accountable to run models on a inventory producing accurate projections

• As above, plus;• Trends from actual to projected reliance• Source of attribution of results

Appointed Actuary See the Opinion • As above, plus;• Assurance of a efficient, consistent,

comprehensive and accurate application of assumption management across the enterprise

Chief Actuary May be unique to an organization but generally accountable for anything produced by an actuary

• As above, plus;• Strong foundation for the Actuarial

Control Cycle• Strength and reputation of the actuarial

contributions

C Suite Meet obligations while meeting the financial objectives of the shareholders

• As above, plus;• Confidence in the enterprise ability of

meet or exceed its obligations to stakeholders

38

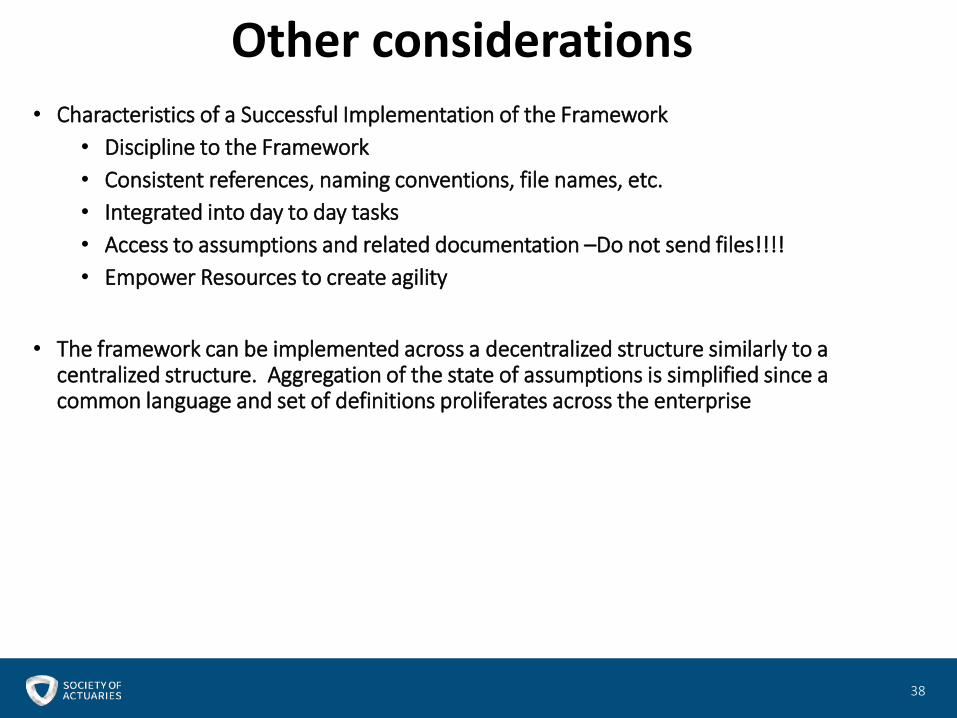

• Characteristics of a Successful Implementation of the Framework• Discipline to the Framework• Consistent references, naming conventions, file names, etc.• Integrated into day to day tasks• Access to assumptions and related documentation –Do not send files!!!!• Empower Resources to create agility

• The framework can be implemented across a decentralized structure similarly to a centralized structure. Aggregation of the state of assumptions is simplified since a common language and set of definitions proliferates across the enterprise

Other considerations

39

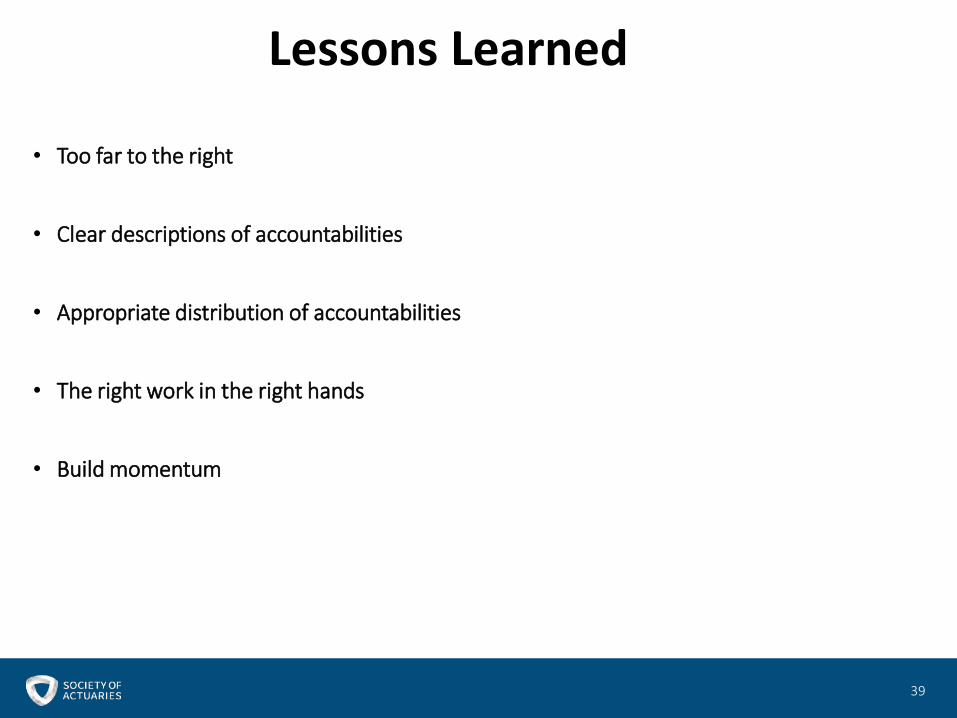

• Too far to the right

• Clear descriptions of accountabilities

• Appropriate distribution of accountabilities

• The right work in the right hands

• Build momentum

Lessons Learned

©2014 Lincoln National CorporationFor Internal Use Only

ASSUMPTION MANAGEMENT:NAVIGATING A DECENTRALIZED PROCESSSOA Annual Meeting, Las Vegas Nevada

Session 93, Panel Discussion

Nick Fiechter FSA, MAAACorporate Actuary

Lincoln Financial Group

OCTOBER 25, 2016

Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates.For Professional Training Use Only. Not for use with the General Public. LCN-1598463-092016

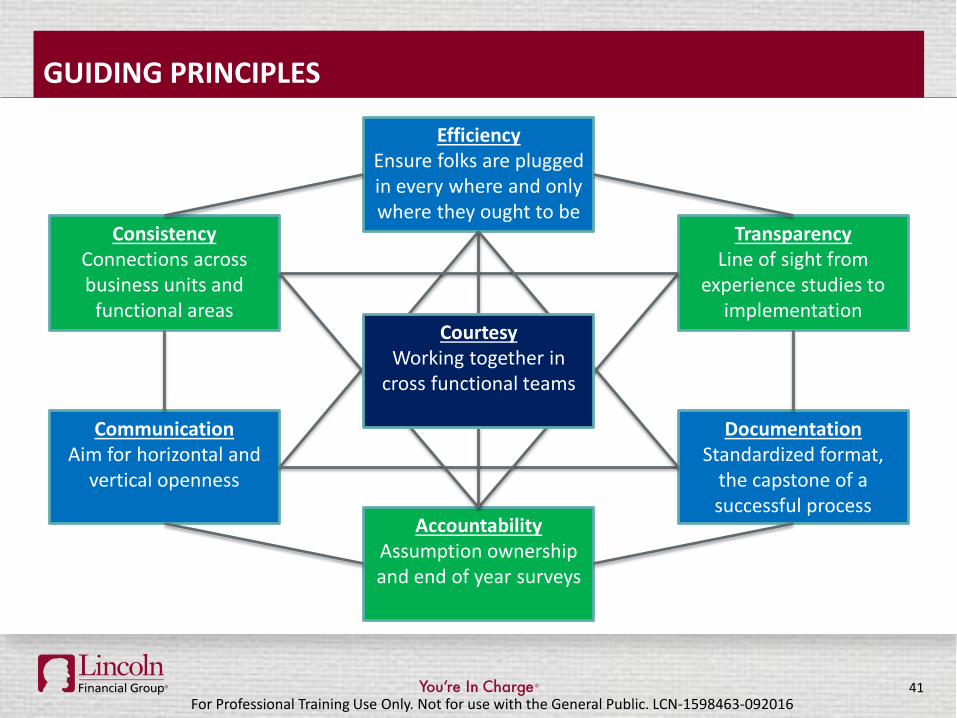

GUIDING PRINCIPLES

41

ConsistencyConnections across business units and

functional areas

EfficiencyEnsure folks are plugged in every where and only where they ought to be

TransparencyLine of sight from

experience studies to implementation

DocumentationStandardized format,

the capstone of a successful process

CommunicationAim for horizontal and

vertical openness

AccountabilityAssumption ownership and end of year surveys

CourtesyWorking together in

cross functional teams

For Professional Training Use Only. Not for use with the General Public. LCN-1598463-092016

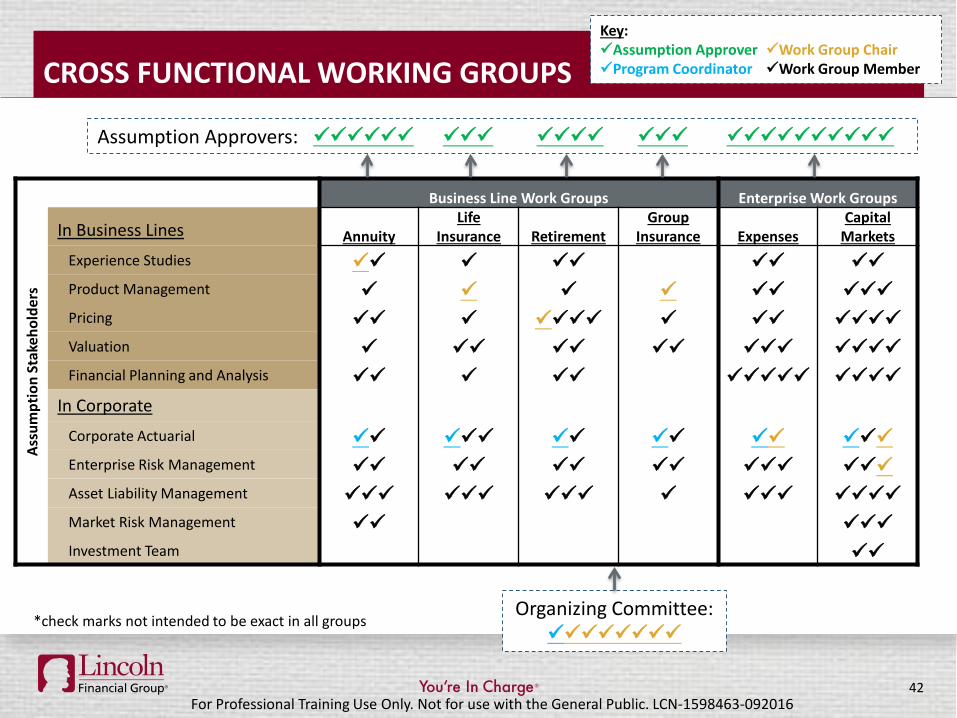

CROSS FUNCTIONAL WORKING GROUPS

42

Assu

mpt

ion

Stak

ehol

ders

Business Line Work Groups Enterprise Work Groups

In Business Lines AnnuityLife

Insurance RetirementGroup

Insurance ExpensesCapital

MarketsExperience Studies Product Management Pricing Valuation Financial Planning and Analysis

In Corporate

Corporate Actuarial Enterprise Risk Management Asset Liability Management Market Risk Management Investment Team

Organizing Committee:

Assumption Approvers:

Key:Assumption ApproverProgram Coordinator

Work Group ChairWork Group Member

*check marks not intended to be exact in all groups

For Professional Training Use Only. Not for use with the General Public. LCN-1598463-092016

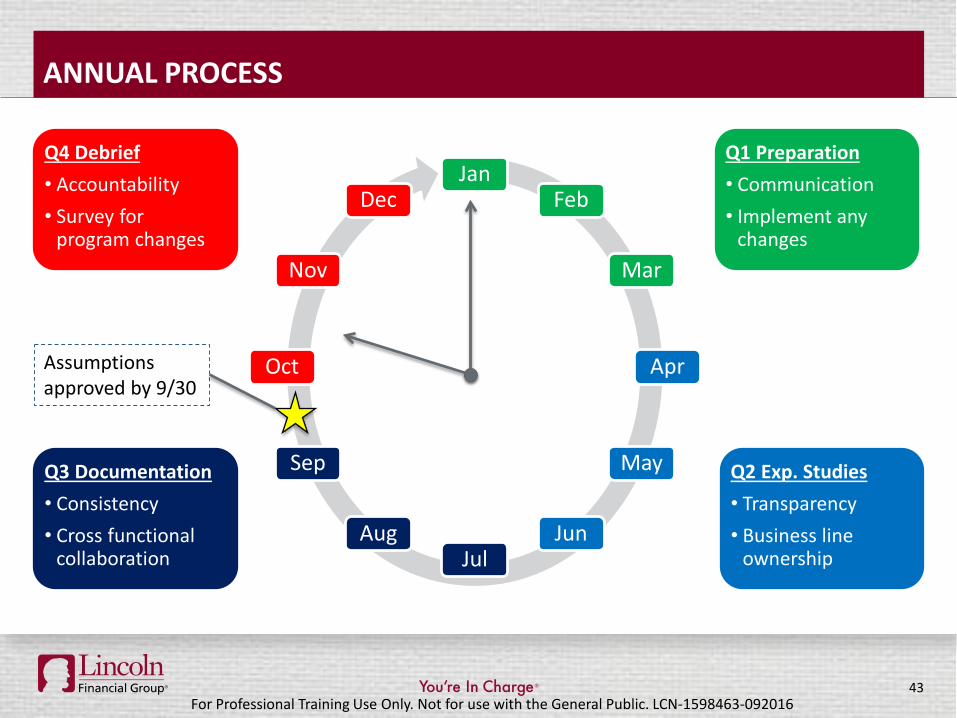

ANNUAL PROCESS

43

JanFeb

Mar

Apr

May

JunJul

Aug

Sep

Oct

Nov

Dec

Q4 Debrief• Accountability• Survey for

program changes

Q3 Documentation• Consistency• Cross functional

collaboration

Q2 Exp. Studies• Transparency• Business line

ownership

Q1 Preparation• Communication• Implement any

changes

Assumptions approved by 9/30

For Professional Training Use Only. Not for use with the General Public. LCN-1598463-092016

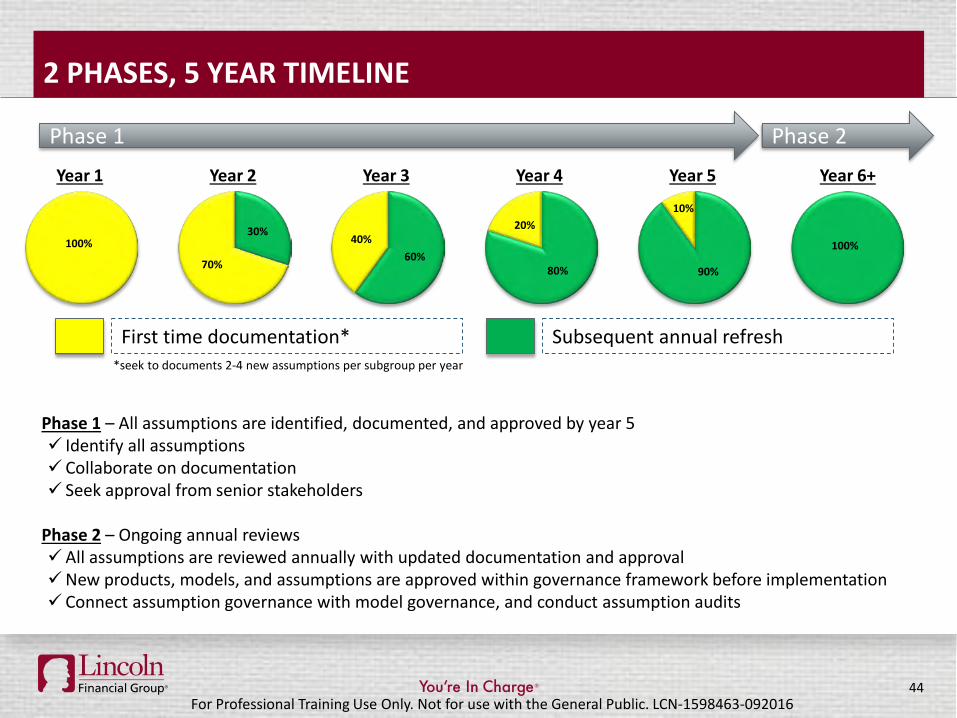

2 PHASES, 5 YEAR TIMELINE

44

First time documentation*

Phase 1 – All assumptions are identified, documented, and approved by year 5 Identify all assumptions Collaborate on documentation Seek approval from senior stakeholders

Phase 2 – Ongoing annual reviewsAll assumptions are reviewed annually with updated documentation and approvalNew products, models, and assumptions are approved within governance framework before implementation Connect assumption governance with model governance, and conduct assumption audits

30%

70%60%

40%

80%

20%

90%

10%

100% 100%

Phase 1 Phase 2

Year 1 Year 6+Year 2 Year 3 Year 4 Year 5

Subsequent annual refresh*seek to documents 2-4 new assumptions per subgroup per year

For Professional Training Use Only. Not for use with the General Public. LCN-1598463-092016

45

LOOKING FORWARD

1. Clearer Definition of Scope and Ownership with Build out of Assumption Database• Stronger build out of the existing assumption grid• Ensure all assumptions are covered, are reviewed within the correct subgroup

and have a specific individual assumption steward to monitor2. Assumption Audits and Alignment with Model Governance

• Depth – follow a specific assumption through the process to ensure accuracy from the experience studies through to model outputs

• Breadth - conduct cross-functional reviews to ensure consistent and aligned assumption outputs across models

3. Actual to Expected Monitoring and Wider use of Credibility Theory• Define tolerable bands to periodically compare experience against historical

assumptions used, feedback loop improves accountability• Tolerable bands based on standard deviation and diminishing ‘funnel of doubt’

over time

For Professional Training Use Only. Not for use with the General Public. LCN-1598463-092016