Assignment on Intermediate Macro Economic (ECN 303). USED

6

Page 1 Of 6 Assignment On ECN 303 Submitted By Bernard Okpe, ASSIGNMENT ON INTERMEDIATE MACROECONOMIC (ECN 303 ) BERNARD OKPE DEPARTMENT & FACULTY: ECONOMICS & SOCIAL SCIENCES QUESTION: ENUMERATE AND EXPLAIN IN DETAILS ALL THE CONTESTING ISSUES BETWEEN THE CAPITALIST AND KEYNESIAN CONTROVERSIES INTRODUCTION KEYNESIAN ECONOMICS: Keynesian economics also called Keynesianism and Keynesian theory is a school of macroeconomic thought based on the ideas of 20th-century English economist John Maynard Keynes. Keynesian economics argues that private sector decisions sometimes lead to inefficient macroeconomic outcomes and, therefore, advocate (Placeholder1) active policy responses by the public sector, including monetary policy actions by the central bank and fiscal policy actions by the government to stabilize output over the business cycle. The theories forming the basis of Keynesian economics were first presented in The General Theory of Employment, Interest and Money, published in 1936; the interpretations of Keynes are contentious, and several schools of thought claim his legacy. They economists who are in favor of general intervention by the state in the aggregate economy are named as Keynesian economists (Alvin Nansen, Paul Samuelson, Tinburgen, R. Frisch etc.). CLASSICAL ECONOMICS: Classical economics is widely regarded as the first modern school of economic thought. Its major developers include Adam Smith, Jean-Baptiste Say, David Ricardo, Thomas Malthus and John Stuart Mill. Adam Smith's The Wealth of Nations in 1776 is usually considered to mark the beginning of classical economics. The school was active into the mid-19th century and was followed by neoclassical economics in Britain beginning around 1870, or, in Marx's definition by "vulgar political economy" from the 1830s. The definition of classical economics is debated, particularly the period 1830 – 70 and the connection to neoclassical economics. The term "classical economics" was coined by Karl Marx to refer to Ricardian economics – the economics of David Ricardo and James Mill and their predecessors – but usage was subsequently extended to include the followers of Ricardo. They are economists who generally oppose government intervention in the functioning of aggregate economy are named as classical economists. THE CONTESTING ISSUES BETWEEN THE KEYNESIAN AND CAPITALIST ECONOMICS The main points of contesting issues between the cla ssical and Ke ynesian controversies are discussed in brief as enumerated and discuss below: 1. Different view on the Unemployment theory 2. Different view on Market Behavior ( activities Demand And Supply in and economy 3. Different view on Saving And Investment / Equality between Saving and Investment

-

Upload

bernardokpe -

Category

Documents

-

view

218 -

download

0

Transcript of Assignment on Intermediate Macro Economic (ECN 303). USED

8/4/2019 Assignment on Intermediate Macro Economic (ECN 303). USED

http://slidepdf.com/reader/full/assignment-on-intermediate-macro-economic-ecn-303-used 1/6

Page 1 Of 6 Assignment On ECN 303 Submitted By Bernard Okpe,

ASSIGNMENT ON INTERMEDIATE MACROECONOMIC (ECN 303 )

BERNARD OKPE

DEPARTMENT & FACULTY: ECONOMICS & SOCIAL SCIENCES

QUESTION: ENUMERATE AND EXPLAIN IN DETAILS ALL THE CONTESTING ISSUES

BETWEEN THE CAPITALIST AND KEYNESIAN CONTROVERSIES

INTRODUCTION

KEYNESIAN ECONOMICS: Keynesian economics also called Keynesianism and Keynesiantheory is a school of macroeconomic thought based on the ideas of 20th-century English economist

John Maynard Keynes. Keynesian economics argues that private sector decisions sometimes lead toinefficient macroeconomic outcomes and, therefore, advocate (Placeholder1) active policyresponses by the public sector, including monetary policy actions by the central bank and fiscal

policy actions by the government to stabilize output over the business cycle. The theories forming

the basis of Keynesian economics were first presented in The General Theory of Employment,Interest and Money, published in 1936; the interpretations of Keynes are contentious, and several

schools of thought claim his legacy. They economists who are in favor of general intervention by

the state in the aggregate economy are named as Keynesian economists (Alvin Nansen, Paul

Samuelson, Tinburgen, R. Frisch etc.).

CLASSICAL ECONOMICS: Classical economics is widely regarded as the first modern school of

economic thought. Its major developers include Adam Smith, Jean-Baptiste Say, David Ricardo,Thomas Malthus and John Stuart Mill. Adam Smith's The Wealth of Nations in 1776 is usually

considered to mark the beginning of classical economics. The school was active into the mid-19th

century and was followed by neoclassical economics in Britain beginning around 1870, or, inMarx's definition by "vulgar political economy" from the 1830s. The definition of classical

economics is debated, particularly the period 1830 – 70 and the connection to neoclassical

economics. The term "classical economics" was coined by Karl Marx to refer to Ricardianeconomics – the economics of David Ricardo and James Mill and their predecessors – but usage

was subsequently extended to include the followers of Ricardo. They are economists who generally

oppose government intervention in the functioning of aggregate economy are named as classical

economists.

THE CONTESTING ISSUES BETWEEN THE KEYNESIAN AND CAPITALIST ECONOMICS

The main points of contesting issues between the classical and Keynesian controversies arediscussed in brief as enumerated and discuss below:

1. Different view on the Unemployment theory

2. Different view on Market Behavior ( activities Demand And Supply in and economy

3. Different view on Saving And Investment / Equality between Saving and Investment

8/4/2019 Assignment on Intermediate Macro Economic (ECN 303). USED

http://slidepdf.com/reader/full/assignment-on-intermediate-macro-economic-ecn-303-used 2/6

Page 2 Of 6 Assignment On ECN 303 Submitted By Bernard Okpe,

4. Different view on Money and Prices

5. Different view on Demand for Money

6. Different view on Short and Long Run Analysis

7. Different view on the role of State on Achieving High Level of Income and Employment

8. Different view on General Versus Special Theory

9. Different view on Inflation

1. Different view on the Unemployment theory: The classical economists explainedunemployment using traditional partial equilibrium supply and demand analysis. According to

them:

"Unemployment results when there is an excess supply of labor at a particular higher wage level.

By accepting lower wages, the unemployed workers will go back to their jobs and the equilibrium

between demand for labor and supply of labor will be established in the labor market in the longperiod. This equilibrium in the economy is always associated with full employment level.

According to the classical economists, unemployment results when the wage level of the workers is

above the equilibrium wage level and as a result, thereof, the quantity of labor supplied is higher

than quantity of labor demanded. The difference between the two (supply and demand) isunemployment.

J. M. Keynes and his followers, however, reject the fundamental classical theory of full

employment equilibrium in the economy. They consider it as unrealistic. According them:

"Full employment is a rare phenomenon in the capitalistic economy. The unemployment occurs,

they say, when the aggregate demand function intersects the aggregate supply function at a point of

less than full employment level. Keynes suggested that in the short period, the government can raiseaggregate demand in the economy through public investment programmes to reduce

unemployment".

According to Keynesian theory, changes in aggregate demand, whether anticipated or unanticipated,

have their greatest short-run effect on real output and employment, not on prices. This idea is

portrayed, for example, in phillips curves that show inflation rising only slowly when

unemployment falls. Keynesians believe that what is true about the short run cannot necessarily beinferred from what must happen in the long run, and we live in the short run. They often quote

Keynes’s famous statement, “In the long run, we are all dead,” to make the point.

Fig 1-Short term Phillips curve

Fig.1-The short term phillips curve: inflation is inversely related to unemployment. When unemployment

rises, inflation drops; when unemployment drops, inflation rises.

8/4/2019 Assignment on Intermediate Macro Economic (ECN 303). USED

http://slidepdf.com/reader/full/assignment-on-intermediate-macro-economic-ecn-303-used 3/6

Page 3 Of 6 Assignment On ECN 303 Submitted By Bernard Okpe,

This is a rough estimation of a short-term Phillips curve. As you can see, inflation is inverselyrelated to unemployment. The long-term Phillips curve, however, is different. Economists have

noted that in the long run, there seems to be no correlation between inflation and unemployment.

2. Different view on Market Behavior (activities Demand and Supply in and economy: According to Say's Law 'Supply creates its own demand', is central to the classic vision of the

economy. According to French classical economist, J. B. Say, the production of goods and servicesgenerates expenditure sufficient to ensure that they are sold in the market. There is no deficiency of demand for goods and hence no need to unemploy workers. According to him, full employment is a

normal condition of market economy.

The long-term classical model does not solve short term problems. In the short term, there are

always various fluctuations that move demand and supply out of balance of each other. There must

be a mechanism to equalize them again.

Fig -2 Classical adjustment model

Fig .2.-If there is disequilibrium between supply and demand, the supply can never change. The price level simply

moves until the demand is equal to supply.

Suppliers in the classical model never change how much they supply; they just change their pricesso that people will buy them. No matter what, supply is an independent concept. Suppliers will

always produce how much they want to produce at a given time. Demand, however, can move by

changes to the price level so that all that is produced is actually bought.

J. M. Keynes has strongly refuted Say's Law of Market with the help of effective demand. Effective

demand is the level of aggregate demand which is equal to aggregate supply. Whenever there is

deficiency in aggregate demand (C + I), a part of the goods produced remain unsold in the marketwhich lead to general over production of goods and services in the market. When all the goods

produced in the market are not sold, the firms lay off workers. The deficiency in demand for goods

creates unemployment in the economy.

8/4/2019 Assignment on Intermediate Macro Economic (ECN 303). USED

http://slidepdf.com/reader/full/assignment-on-intermediate-macro-economic-ecn-303-used 4/6

Page 4 Of 6 Assignment On ECN 303 Submitted By Bernard Okpe,

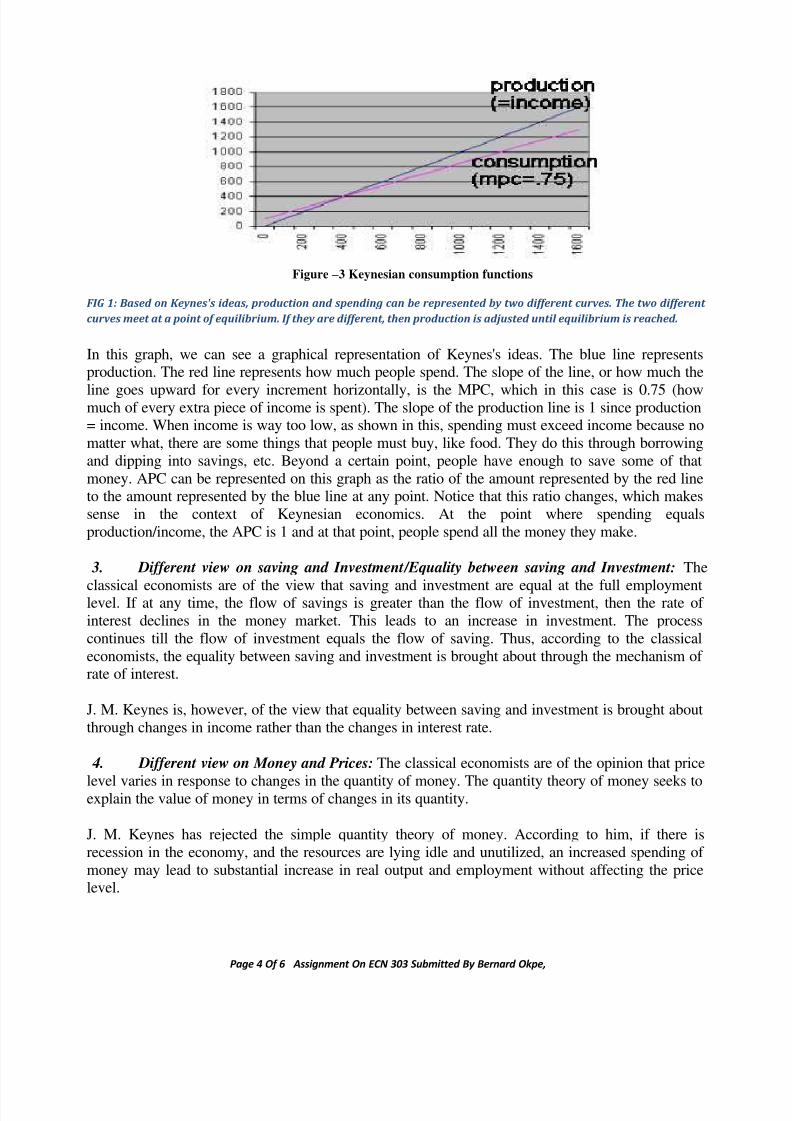

Figure – 3 Keynesian consumption functions

FIG 1: Based on Keynes's ideas, production and spending can be represented by two different curves. The two different

curves meet at a point of equilibrium. If they are different, then production is adjusted until equilibrium is reached.

In this graph, we can see a graphical representation of Keynes's ideas. The blue line representsproduction. The red line represents how much people spend. The slope of the line, or how much the

line goes upward for every increment horizontally, is the MPC, which in this case is 0.75 (howmuch of every extra piece of income is spent). The slope of the production line is 1 since production= income. When income is way too low, as shown in this, spending must exceed income because no

matter what, there are some things that people must buy, like food. They do this through borrowing

and dipping into savings, etc. Beyond a certain point, people have enough to save some of that

money. APC can be represented on this graph as the ratio of the amount represented by the red lineto the amount represented by the blue line at any point. Notice that this ratio changes, which makes

sense in the context of Keynesian economics. At the point where spending equals

production/income, the APC is 1 and at that point, people spend all the money they make.

3. Different view on saving and Investment/Equality between saving and Investment: The

classical economists are of the view that saving and investment are equal at the full employmentlevel. If at any time, the flow of savings is greater than the flow of investment, then the rate of

interest declines in the money market. This leads to an increase in investment. The process

continues till the flow of investment equals the flow of saving. Thus, according to the classical

economists, the equality between saving and investment is brought about through the mechanism of rate of interest.

J. M. Keynes is, however, of the view that equality between saving and investment is brought about

through changes in income rather than the changes in interest rate.

4. Different view on Money and Prices: The classical economists are of the opinion that price

level varies in response to changes in the quantity of money. The quantity theory of money seeks toexplain the value of money in terms of changes in its quantity.

J. M. Keynes has rejected the simple quantity theory of money. According to him, if there is

recession in the economy, and the resources are lying idle and unutilized, an increased spending of

money may lead to substantial increase in real output and employment without affecting the pricelevel.

8/4/2019 Assignment on Intermediate Macro Economic (ECN 303). USED

http://slidepdf.com/reader/full/assignment-on-intermediate-macro-economic-ecn-303-used 5/6

Page 5 Of 6 Assignment On ECN 303 Submitted By Bernard Okpe,

5. Different view on Demand for Money: According to classical economists, money is onlydemanded to make regular expenditure under the need transactions demand.

The Keynesian economists are of the view that people hold money for transaction as well asspeculative purposes. So far 'transaction demand' for money is concerned; it is a function of income.

The higher the income, the higher is the transaction demand for money and vice versa. The

speculative demand for money is a function of rate of interest. The higher the interest rate, the loweris the money balances which the nation holds for speculative purposes and vice versa.

6. Different view on Short and Long Run Analysis: The classicists believed that a marketeconomy, through flexible interest rates, wages, and prices, return to a state of full employment in

the long run.

J. M. Keynes played a major role in suggesting as to how the government can reduce cyclical

fluctuations through stabilization policies. Keynes analysis of economic problems is confined to

short run. Keynes says, 'Let us forget the long run and focus on the short run. In the long run, we are

all dead'.

7. Different view on the role of State on Achieving High Level of Income and Employment: The classical economists are of the view that in commodity and labor market, the price mechanismworks with reasonable promptness. The supply adjusts to demand through the flexible interest rates,

wages and prices and the economic system returns to a state of full employment in the long runwithout government intervention.

J. M. Keynes puts less faith in market forces. He stressed and argued for more direct intervention by

the state to increase/decrease aggregate demand to achieve certain national economic goals. J. M.Keynes considered fiscal policy as a steering wheel for moving the economy to a state of higher

level of employment and price stability more quickly. If aggregate income is low and below the

target national income, then appropriate expansionary fiscal policy should be adopted.Expansionary fiscal policy involves decreasing taxes and increasing government spending. In case

the aggregate income is higher or above the potential level, then contractionary fiscal policy i.e.

increasing taxes and decreasing government spending should be taken up by the state.

8. Different view on General Versus Special Theory: The classical theory is based on four

unrealistic assumptions (i) role of the government in the economy should be minimum (ii) all pricesand wages and markets are flexible (iii) any problem in the macroeconomic is temporary (v) the

market force come to the rescue and correct itself. The market mechanism eliminates over

production and unemployment and establishes full employment in the long run. The classical theory

relates only to the special case of full employment.

J. M. Keynesian theory is a general theory. It has a wider application on all such situations of

unemployment, partial employment and near full employment.

9. Different view on Inflation: In the classical view of inflation, the only thing that causes

inflation is, in reality, changes in the money supply. Remember the classical quantity theory of money: (money supply) x (velocity) = (price level) x (amount of output). And remember that the

classics assume that velocity and output are independent and relatively constant. Thus, as money

supply rises, that naturally ups the price level, too, and increase in price level is inflation.The

8/4/2019 Assignment on Intermediate Macro Economic (ECN 303). USED

http://slidepdf.com/reader/full/assignment-on-intermediate-macro-economic-ecn-303-used 6/6

Page 6 Of 6 Assignment On ECN 303 Submitted By Bernard Okpe,

classical economists believe that there is a natural rate of unemployment, the equilibrium level of unemployment of the economy.

As opposed to the Classics, who view inflation as a problem of ever-increasing money supply,Keynesians concentrate on the institutional problems of people increasing their price levels,

Keynesians argue that firms raise wages to keep their workers happy. Firms then have to pay for

that and keep making a profit by subsequently raising the prices. This causes an increase in bothwages and prices and demands an increase of money supply to keep the economy running. So, thegovernment then issues more and more money to keep up with inflation. This differs from the

classical model.

CONCLUSION:

We can conclude that the Says law is the major difference between the Keynes theory and the

classical economists, the classical economist support the Says law and also advocate for a free

market economy while Keynes argues that the government can solve the problem of unemployment

in an economy through an increase in spending to increase the aggregate demand that results to

lower unemployment levels.

REFERENCES MATERIAL:

1. Clark, B. (1998). Political-economy: A comparative approach. Westport, CT: Preager.2. Friedman, David D. (2002). "Crime," The Concise Encyclopedia of Economics.

3. Blaug, Mark (2007). "The Social Sciences: Economics," Microeconomics, The New

Encyclopædia Britannica, v. 27, pp. 347 – 49. Chicago. ISBN 0-85229-423-94. Varian, Hal R. (1987). "Microeconomics", The New Palgrave: A Dictionary of Economics, v. 3,

pp. 461 – 63. London and New York: Macmillan and Stockton. ISBN 0-333-37235-2

5. Buchanan, James M. (1987). "Opportunity cost", The New Palgrave: A Dictionary of

Economics, v. 3, pp. 718 – 21.6. The Economist, Economics A-Z, "Opportunity Cost." Accessed 3 Aug. 2010

7. Montani, Guido (1987), "scarcity," The New Palgrave: A Dictionary of Economics, v. 4, p. 254.

8. Samuelson, Paul A.; William D. Nordhaus (2004). Economics. McGraw-Hill. ch. 1, p. 5(quotation) and sect. C,"The Production-Possibility Frontier," pp. 9 – 15; ch. 2, "Efficiency" sect.;

ch. 8, sect. D, "The Concept of Efficiency.".