Assignment - lms3.e-careers.com

6

Transcript of Assignment - lms3.e-careers.com

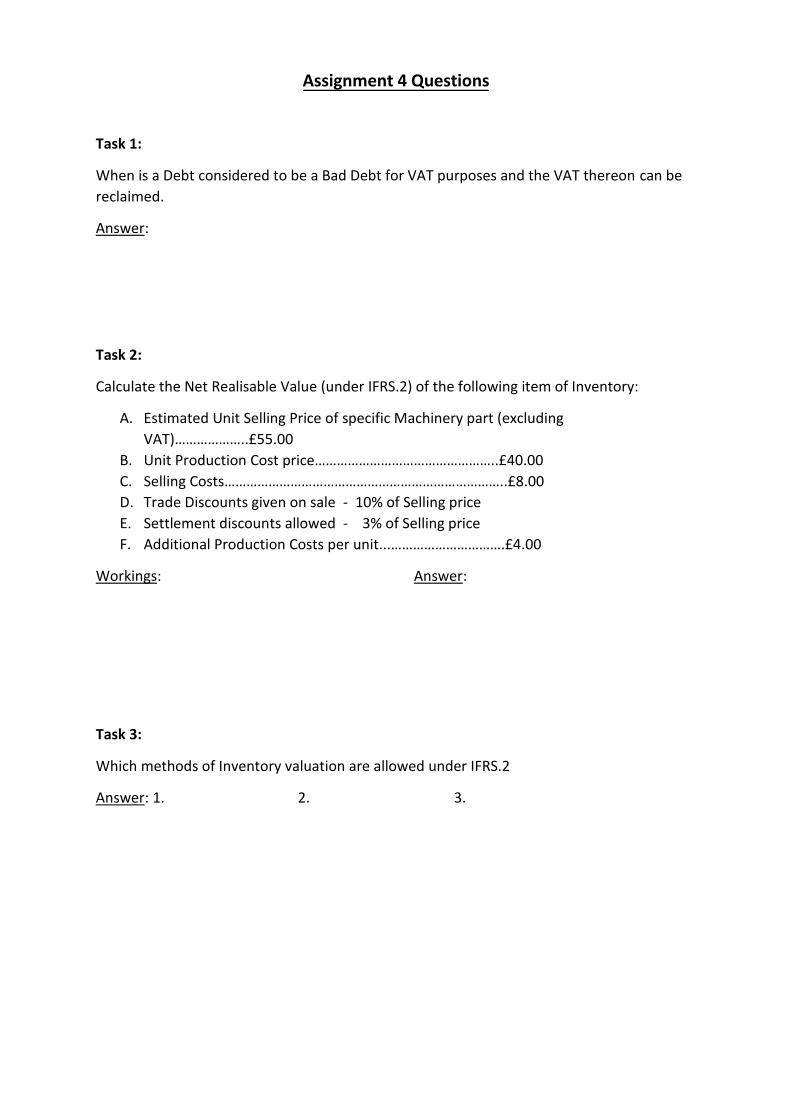

Assignment 4 Questions

Task 1:

When is a Debt considered to be a Bad Debt for VAT purposes and the VAT thereon can be

reclaimed.

Answer:

Task 2:

Calculate the Net Realisable Value (under IFRS.2) of the following item of Inventory:

A. Estimated Unit Selling Price of specific Machinery part (excluding

VAT)………………..£55.00

B. Unit Production Cost price…………………………………………..£40.00

C. Selling Costs…………………………………………………………………..£8.00

D. Trade Discounts given on sale - 10% of Selling price

E. Settlement discounts allowed - 3% of Selling price

F. Additional Production Costs per unit...………………………….£4.00

Workings: Answer:

Task 3:

Which methods of Inventory valuation are allowed under IFRS.2

Answer: 1. 2. 3.

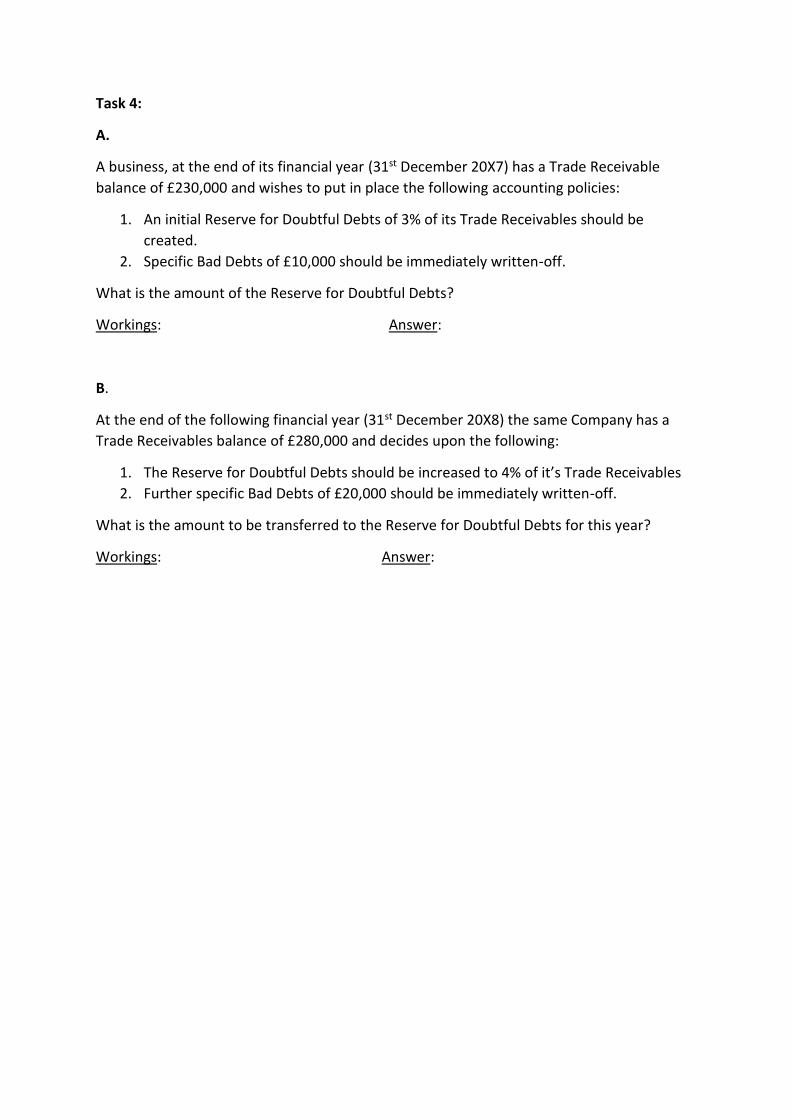

Task 4:

A.

A business, at the end of its financial year (31st December 20X7) has a Trade Receivable

balance of £230,000 and wishes to put in place the following accounting policies:

1. An initial Reserve for Doubtful Debts of 3% of its Trade Receivables should be

created.

2. Specific Bad Debts of £10,000 should be immediately written-off.

What is the amount of the Reserve for Doubtful Debts?

Workings: Answer:

B.

At the end of the following financial year (31st December 20X8) the same Company has a

Trade Receivables balance of £280,000 and decides upon the following:

1. The Reserve for Doubtful Debts should be increased to 4% of it’s Trade Receivables

2. Further specific Bad Debts of £20,000 should be immediately written-off.

What is the amount to be transferred to the Reserve for Doubtful Debts for this year?

Workings: Answer:

Task 5:

You are preparing the Financial Account of Dave Builders Services for the year ended 31st

August 20X8 and are given the following information:

1. An Invoice for the business Electricity account for the period from 1st July 20X8 to

30th September has been received following the year end in the sum of £1077.

Identify the amount and the treatment of this invoice given that it has not previously

appeared in the financial accounts.

Workings: Answer (amount): £ Answer

(treatment):

2. Income is received and entered in the books of account on 20th August 20X8 in

advance of work which is yet to be completed on an ongoing contract in the sum of

£5,000. All previous amount received on account of this contract have been utilised

against work actually completed. How should this item be dealt with in the Accounts

being prepared?

Answer:

3. There is an invoice for Factory Rent in the business records for £4,500 for the period

from 1st March 20X8 for a period of one year which was paid on 30th June 20X8.

Calculate the prepayment for the relevant period.

Workings: Answer:

4. The business is committed to a fixed annual business insurance premium if £1800

the last of which was invoiced on the due date of 1st July 20X7. The next invoice has

not yet been received and entered into the books of the business. What provision, if

any, should be made in relation to this?

Workings: Provision?: Amount (if any):

Task 6:

Using the following words place them in the correct gaps left at questions 6, 7, 8, 9 and 10:

1. Professional Behaviour

2. Fairness

3. Transparency

4. Personal Threats to Independence

5. Independence of Appearance

6. Professional Competence

7. Independence of Mind

8. Due Care

9. Credibility

10. Confidence

11. Quality of Service

Examples of _____________________________________include those which arise due to:

a) Holding a financial interest in a client business such as owning shares.

b) Having undue dependence on the fees for a Client. This can happen where thetotal fees from a Client represent a high proportion of the accountants total fees.

c) Receiving expensive or excessive hospitality and gifts from a Client.

d) Having a close business relationship with a Client

e) Having personal and family relationship with a Client.

f) Undue pressures from Authority or workload.

Task 7:

a) _______________________ is the state of mind which allows an opinion to bemade without being affected by outside influences that compromise professionaljudgement, allowing an individual to act with Integrity and exercise Objectivityand professional scepticism.

b) _______________________ is the avoidance of facts and circumstances that areso significant that a reasonable and informed third party, having knowledge of allrelevant information, would reasonably conclude that a Member’s Integrity,Objectivity or Professional Scepticism had been compromised.

Task 8:

__________________________ means that a Member has the required knowledge and ability to discharge their responsibilities in accordance with current developments in practice, legislation and technique. _______________ means a Member must act diligently and in accordance with applicable technical and professional standards when providing professional services and must not be negligent.

Task 9:

A Professional Accountant should comply with relevant laws and regulations and should avoid any action which is likely to bring the Profession into disrepute. The objectives of the Accountancy Profession are to work to the highest standards of professionalism and to attain the highest levels of performance in addition to meeting the public interest requirements. These professional objectives require four basic principle needs to be met as follows: a) ______________ -.Information and Information Systems must provide credible

information.

b) ______________ – Interested parties, employers and Clients must be able to clearly identify the person as a professional in the accountancy field.

c) ______________ – The professional Accountant should provide all services to

the highest standards of the profession.

d) ______________ - Users of the Professional Accountants services should be able to feel confident that there is a framework of professional ethics which govern the provision of services.

__________________ can be compromised by familiarity with the Client or the pressure which can come from Authoritative Management within the client Company.

Task 10:

_________________is another means of describing “Openness” in the Professional’s dealings with all parties. This would cover all discussions, clarity of information and a lack of withholding of relevant information unless this is deemed necessary.

______________ means a sense of even-handedness. As a Professional Accountant there may be a need to sign-off a Reports or Financial Accounts as showing a “True & Fair View” of the information provided, which means that the Statements present the information faithfully and without any element of bias.