Asset Management Lecture 14. Outline for today Evaluating hedge funds Marking timing: are mutual...

19

Asset Management Lecture 14

-

date post

21-Dec-2015 -

Category

Documents

-

view

218 -

download

1

Transcript of Asset Management Lecture 14. Outline for today Evaluating hedge funds Marking timing: are mutual...

Asset Management

Lecture 14

Outline for today

Evaluating hedge fundsMarking timing: are mutual funds

successful or not?Style analysis for mutual funds

Evaluating Hedge Funds

Hedge funds rarely serve as an investor’s overall

portfolio.Capture temporarily mispriced securitiesLess concerned with diversificationAlpha-drivenSharp-ratio is not appropriate for evaluation

Evaluating Hedge Funds

When mixing a hedge fund H with a baseline passive portfolio M, the optimal position of the H in the overall portfolio P would be

0

0

)1(1 HH

HH w

ww

2

20

)(

)(

M

M

H

H

H RE

ea

w

i

n

iiH w

1

Evaluating Hedge Funds

When the hedge fund is optimally combined with the baseline portfolio, the improvement in the Sharpe measure will be determined by its information ratio:

2

2 2

( )H

P MH

S Se

An example of actual performance measurement

Which portfolio to choose?

•If the portfolio stands for the entire investment fund

•If the portfolio is only a subportfolio of a larger fund

•If this is an active portfolio to be mixed with the index

Difficulties in evaluating hedge funds

Risk profile and investment strategy change rapidly

Investment in illiquid assets: liquidity premium and pricing error

Long-term risk-returnSurvivorship bias

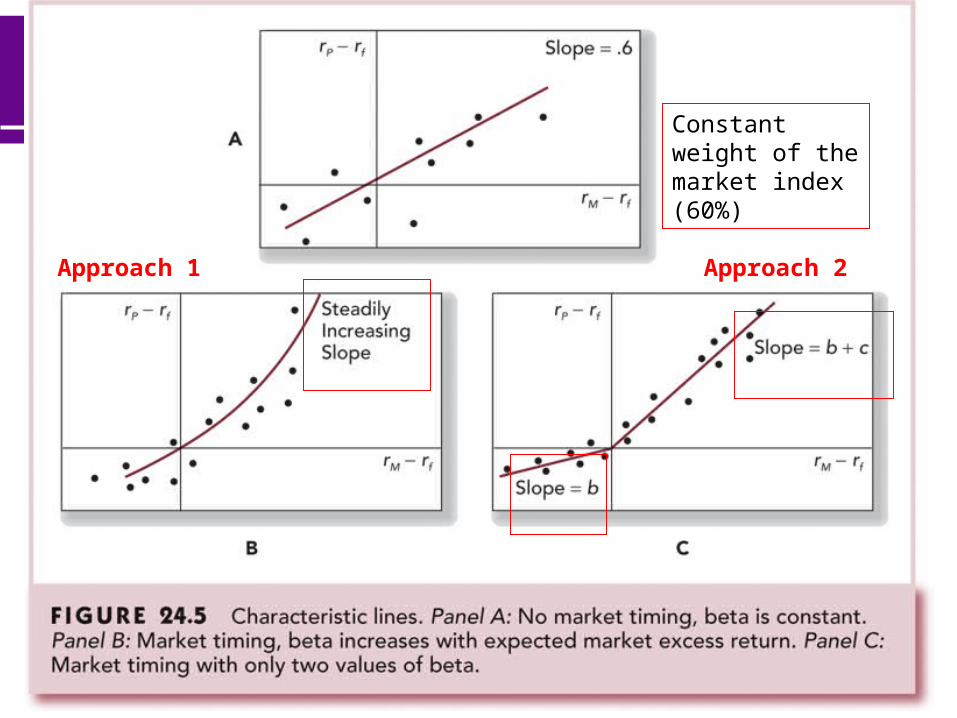

Market Timing

market timing involves shifting funds between a market-

index portfolio and a safe assetHigh-beta vs. low-beta strategy

Constant weight of the market index (60%)

Approach 1

Market Timing

Treynor and Mazuy:

Test for a group of mutual funds but found little evidence

2( ) ( )P f M f M f Pr r a b r r c r r e

Constant weight of the market index (60%)

Approach 1 Approach 2

Market Timing

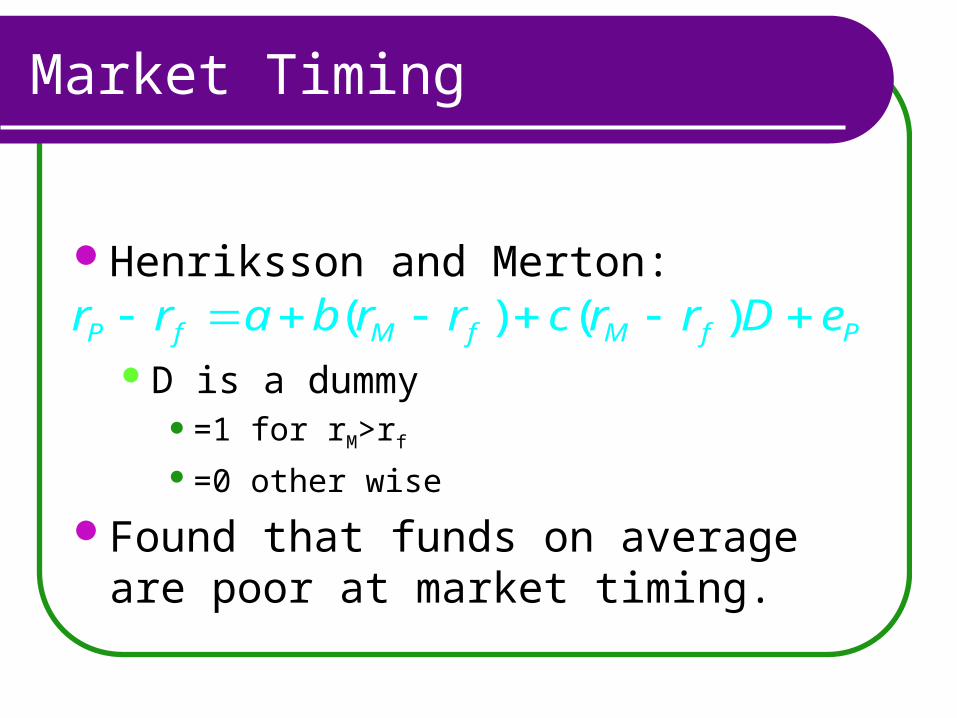

Henriksson and Merton:

D is a dummy=1 for rM>rf

=0 other wise

Found that funds on average are poor at market timing.

( ) ( )P f M f M f Pr r a b r r c r r D e

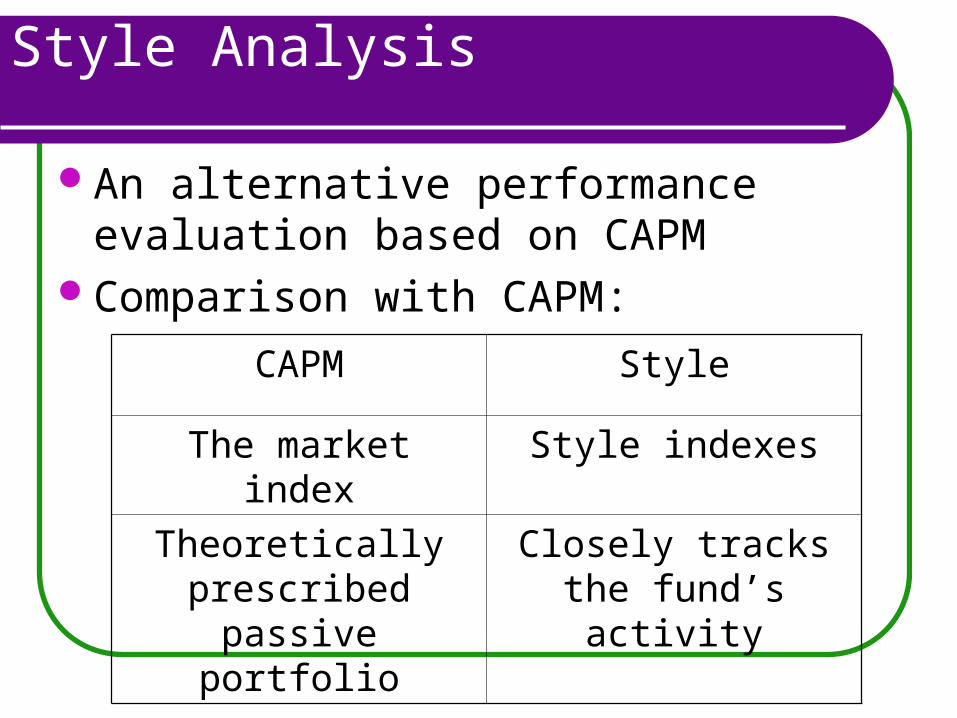

Style Analysis

Introduced by W. Sharpe study of mutual fund performance

Regress fund returns on indexes of a range of assets Style: the regression coefficient on each index R2: percentage of return variability attributable to style 1-R2:

stock selection market timing (changes in asset-class weights)

Over 90% of variation in return could be explained by the funds’ allocations to bills, bonds and stocks

Style Analysis

An alternative performance evaluation based on CAPM

Comparison with CAPM:

CAPM Style

The market index Style indexes

Theoretically prescribed passive

portfolio

Closely tracks the fund’s activity

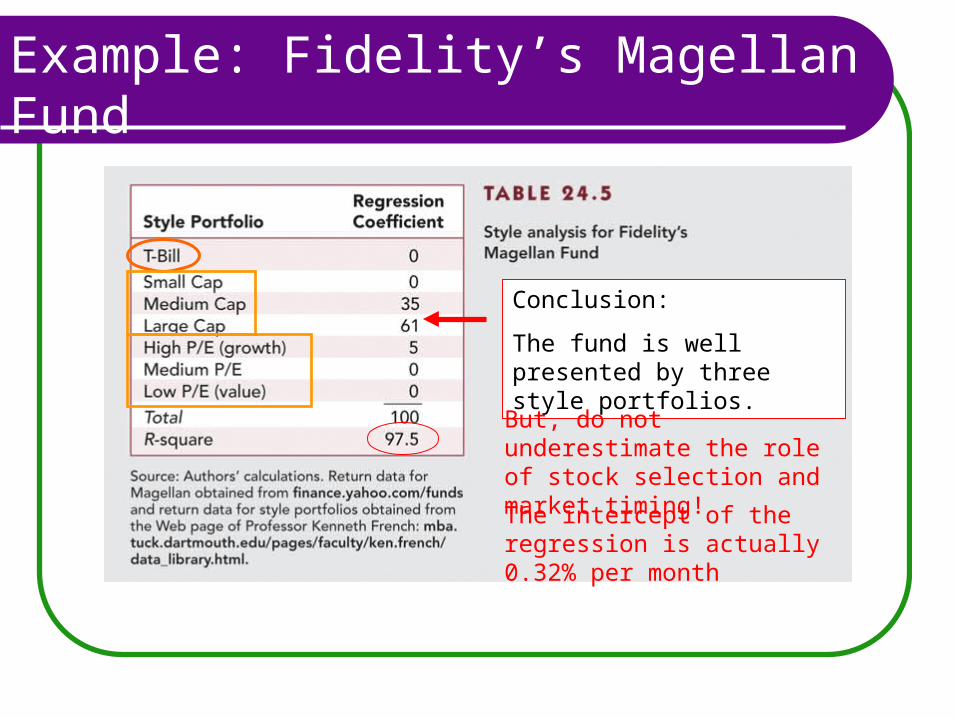

Example: Fidelity’s Magellan Fund

Example: Fidelity’s Magellan Fund

Conclusion:

The fund is well presented by three style portfolios.

But, do not underestimate the role of stock selection and market timing!

The intercept of the regression is actually 0.32% per month

Morningstar

Premier source of information on mutual funds

The risk-adjusted rating is ranked across funds in a style group and stars are awarded

2nd case study

Morningstar, Inc. Discuss the rapid changes in the mutual

fund industry up to the end of 2008. Discuss Morningstar’s rating system. What are the pros and cons of

Morningstar’s rating system? How would you like to improve it?

Deadline: April 19 (Sunday)