ASM International Conference - Global and Local Biotechnology Industry

19

The Global and Local Biotechnology Industry ASMIC, June 2010 • © 2010 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the prior written approval and consent of Frost & Sullivan.

-

Upload

frost-sullivan -

Category

Health & Medicine

-

view

3.600 -

download

2

Transcript of ASM International Conference - Global and Local Biotechnology Industry

The Global and Local Biotechnology Industry

ASMIC, June 2010

• © 2010 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the prior written approval and consent of Frost & Sullivan.

2

“Sometimes people ask me what field I'd be in if not computers. I think I'd be working in biotechnology”

Bill Gates

New York Times, June 18, 1996

3

AGENDA

Global Biotechnology OverviewGlobal Biotechnology Overview11

Benchmarking successful biotechnology clustersBenchmarking successful biotechnology clusters22

Malaysia in the context of biotechnologyMalaysia in the context of biotechnology33

4

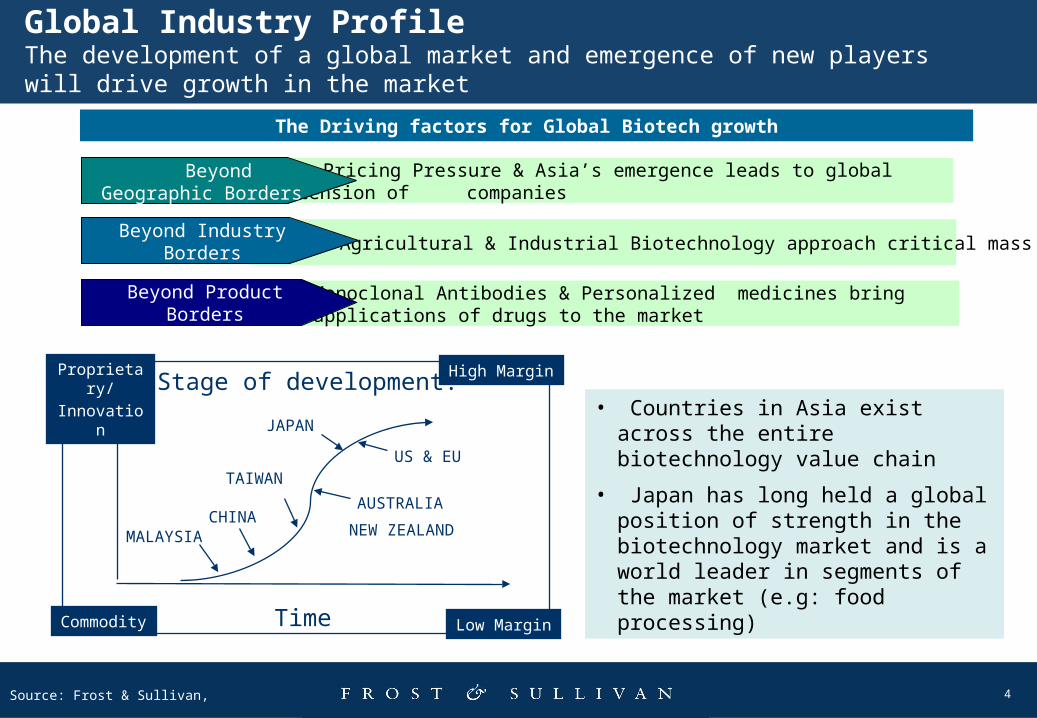

Global Industry Profile The development of a global market and emergence of new players will drive growth in the market

Agricultural & Industrial Biotechnology approach critical mass

Pricing Pressure & Asia’s emergence leads to global extension of companies

Beyond Geographic Borders

Beyond Industry Borders

Monoclonal Antibodies & Personalized medicines bring new applications of drugs to the market

Beyond Product Borders

The Driving factors for Global Biotech growth

Stage of development:

Time

CHINA

TAIWAN

MALAYSIA

AUSTRALIA

NEW ZEALAND

JAPAN

US & EU

Source: Frost & Sullivan, DataMonitor

• Countries in Asia exist across the entire biotechnology value chain

• Japan has long held a global position of strength in the biotechnology market and is a world leader in segments of the market (e.g: food processing)

Commodity

Proprietary/

Innovation

Low Margin

High Margin

5

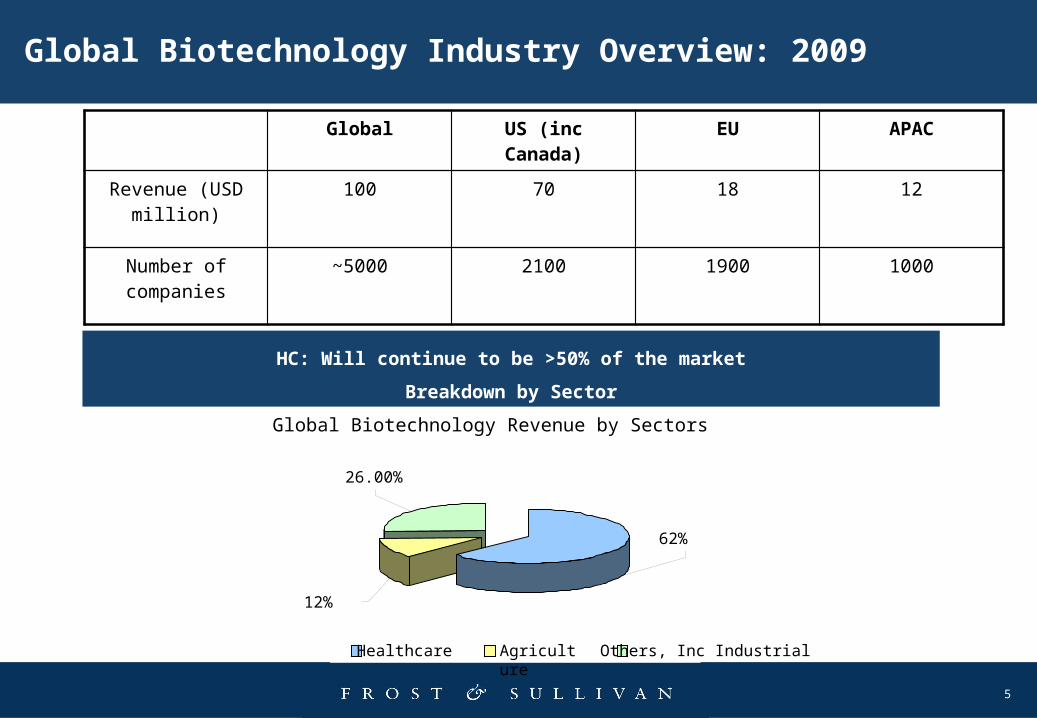

Global Biotechnology Industry Overview: 2009

Global US (inc Canada)

EU APAC

Revenue (USD million)

100 70 18 12

Number of companies

~5000 2100 1900 1000

Global Biotechnology Revenue by Sectors

12%

26.00%

62%

Healthcare Agriculture Others, Inc Industrial

HC: Will continue to be >50% of the market

Breakdown by Sector

6

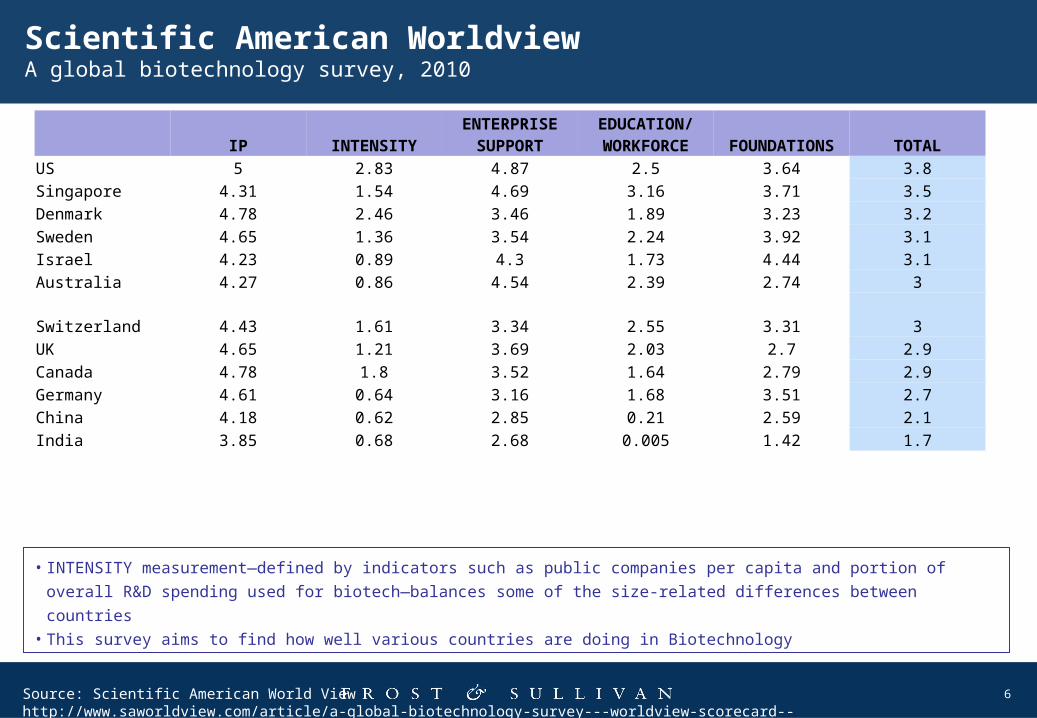

Scientific American WorldviewA global biotechnology survey, 2010

IP INTENSITYENTERPRISE

SUPPORTEDUCATION/WORKFORCE FOUNDATIONS TOTAL

US 5 2.83 4.87 2.5 3.64 3.8

Singapore 4.31 1.54 4.69 3.16 3.71 3.5

Denmark 4.78 2.46 3.46 1.89 3.23 3.2

Sweden 4.65 1.36 3.54 2.24 3.92 3.1

Israel 4.23 0.89 4.3 1.73 4.44 3.1

Australia 4.27 0.86 4.54 2.39 2.74 3

Switzerland 4.43 1.61 3.34 2.55 3.31 3

UK 4.65 1.21 3.69 2.03 2.7 2.9

Canada 4.78 1.8 3.52 1.64 2.79 2.9

Germany 4.61 0.64 3.16 1.68 3.51 2.7

China 4.18 0.62 2.85 0.21 2.59 2.1

India 3.85 0.68 2.68 0.005 1.42 1.7

Source: Scientific American World Viewhttp://www.saworldview.com/article/a-global-biotechnology-survey---worldview-scorecard--

• INTENSITY measurement—defined by indicators such as public companies per capita and portion of overall R&D

spending used for biotech—balances some of the size-related differences between countries• This survey aims to find how well various countries are doing in Biotechnology

7

Source: http://bharatbook.com; www.frost.com

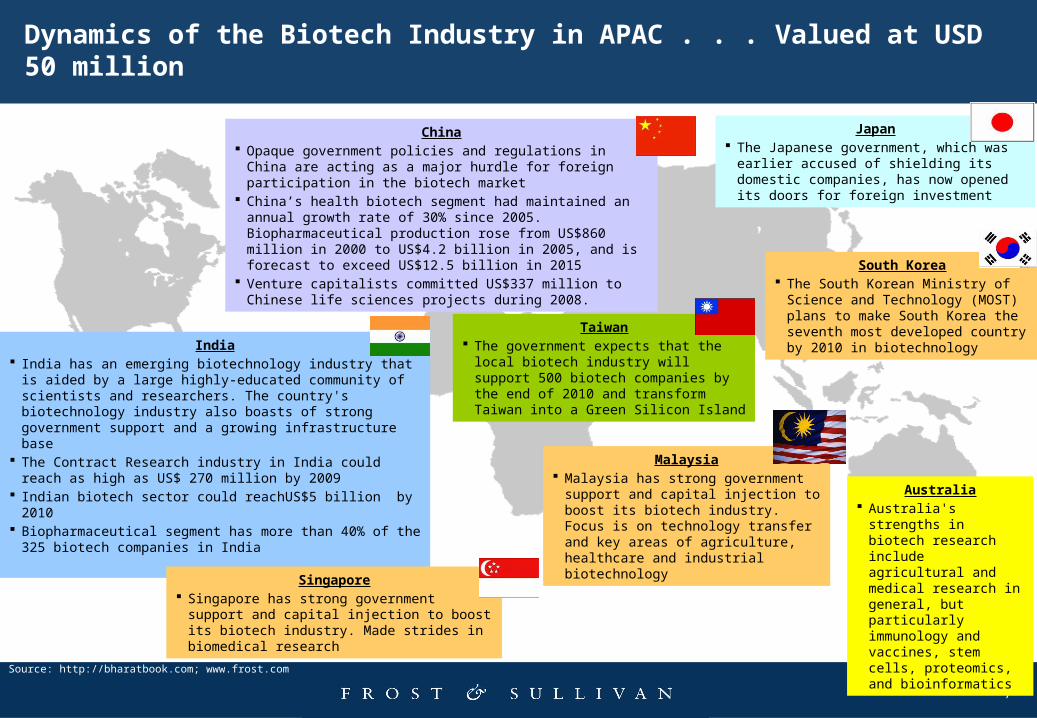

Dynamics of the Biotech Industry in APAC . . . Valued at USD 50 million

India India has an emerging biotechnology industry that is aided

by a large highly-educated community of scientists and researchers. The country's biotechnology industry also boasts of strong government support and a growing infrastructure base

The Contract Research industry in India could reach as high as US$ 270 million by 2009

Indian biotech sector could reachUS$5 billion by 2010 Biopharmaceutical segment has more than 40% of the 325 biotech

companies in India

Japan The Japanese government, which was

earlier accused of shielding its domestic companies, has now opened its doors for foreign investment

China Opaque government policies and regulations in China are

acting as a major hurdle for foreign participation in the biotech market

China’s health biotech segment had maintained an annual growth rate of 30% since 2005. Biopharmaceutical production rose from US$860 million in 2000 to US$4.2 billion in 2005, and is forecast to exceed US$12.5 billion in 2015

Venture capitalists committed US$337 million to Chinese life sciences projects during 2008.

Australia Australia's strengths in

biotech research include agricultural and medical research in general, but particularly immunology and vaccines, stem cells, proteomics, and bioinformatics

South Korea The South Korean Ministry of

Science and Technology (MOST) plans to make South Korea the seventh most developed country by 2010 in biotechnology

Taiwan The government expects that the local

biotech industry will support 500 biotech companies by the end of 2010 and transform Taiwan into a Green Silicon Island

Singapore Singapore has strong government support

and capital injection to boost its biotech industry. Made strides in biomedical research

Malaysia Malaysia has strong government

support and capital injection to boost its biotech industry. Focus is on technology transfer and key areas of agriculture, healthcare and industrial biotechnology

8

AGENDA

Global Biotechnology OverviewGlobal Biotechnology Overview11

Benchmarking successful biotechnology clustersBenchmarking successful biotechnology clusters22

Malaysia in the context of biotechnologyMalaysia in the context of biotechnology33

9

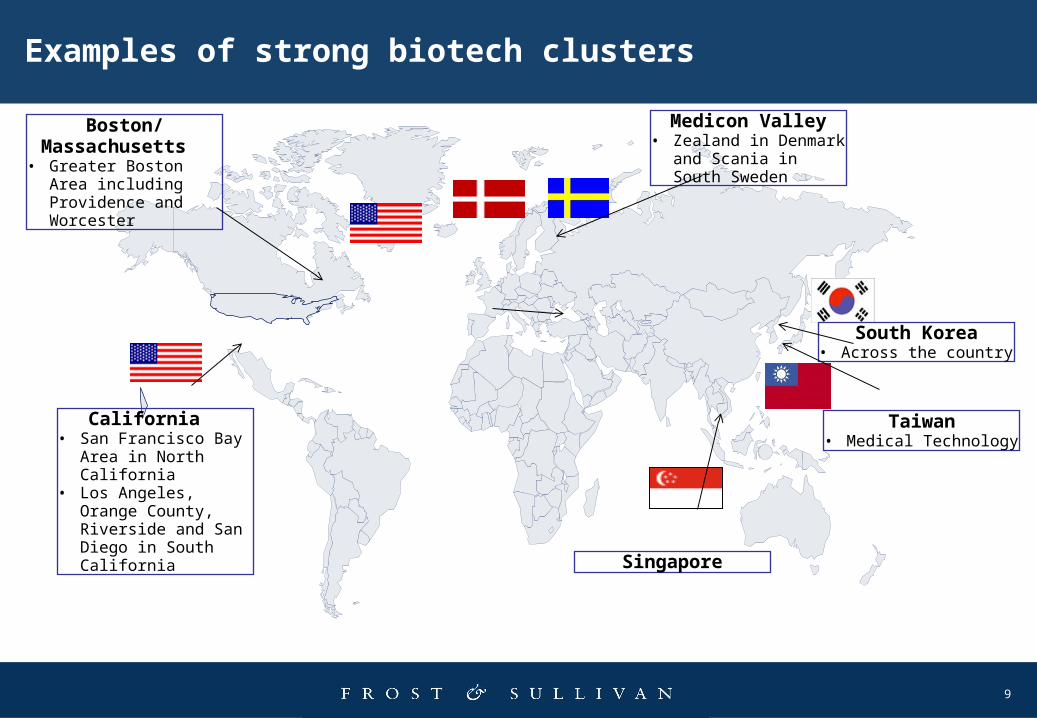

Examples of strong biotech clusters

California • San Francisco Bay

Area in North California

• Los Angeles, Orange County, Riverside and San Diego in South California

Boston/ Massachusetts

• Greater Boston Area including Providence and Worcester

Medicon Valley• Zealand in Denmark

and Scania in South Sweden

South Korea• Across the country

Singapore

Taiwan• Medical Technology

10

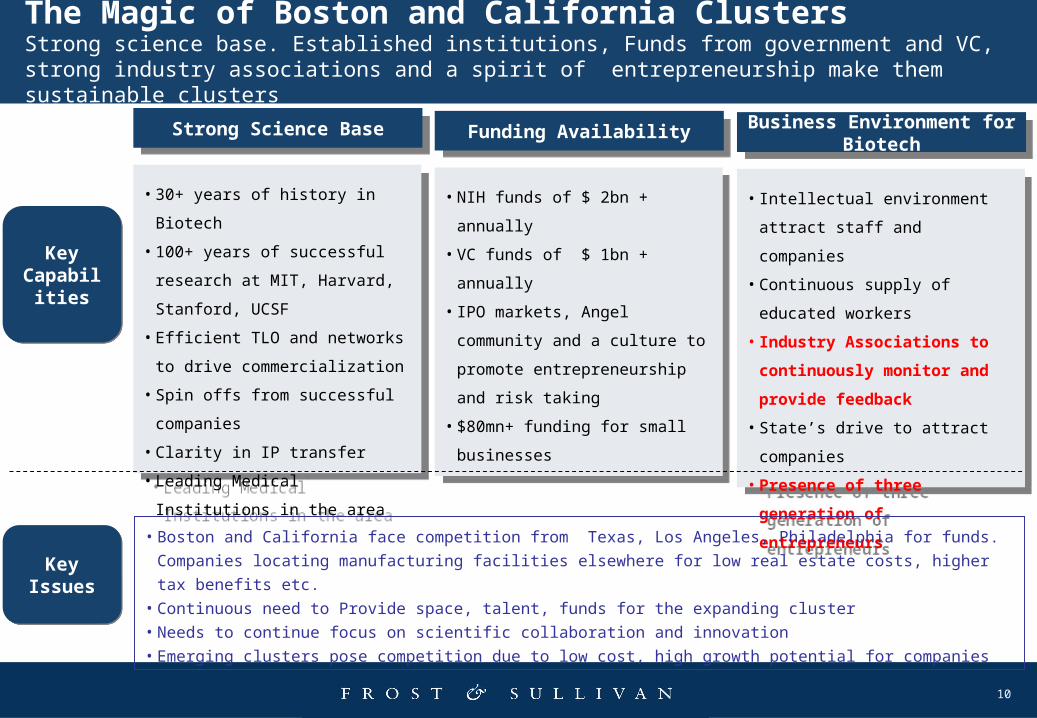

The Magic of Boston and California ClustersStrong science base. Established institutions, Funds from government and VC, strong industry associations and a spirit of entrepreneurship make them sustainable clusters

Strong Science BaseStrong Science Base

• 30+ years of history in Biotech

• 100+ years of successful research

at MIT, Harvard, Stanford, UCSF

• Efficient TLO and networks to drive

commercialization

• Spin offs from successful

companies

• Clarity in IP transfer

• Leading Medical Institutions in the

area

• 30+ years of history in Biotech

• 100+ years of successful research

at MIT, Harvard, Stanford, UCSF

• Efficient TLO and networks to drive

commercialization

• Spin offs from successful

companies

• Clarity in IP transfer

• Leading Medical Institutions in the

area

Funding AvailabilityFunding Availability

• NIH funds of $ 2bn + annually

• VC funds of $ 1bn + annually

• IPO markets, Angel community and

a culture to promote

entrepreneurship and risk taking

• $80mn+ funding for small

businesses

• NIH funds of $ 2bn + annually

• VC funds of $ 1bn + annually

• IPO markets, Angel community and

a culture to promote

entrepreneurship and risk taking

• $80mn+ funding for small

businesses

Business Environment for Biotech

Business Environment for Biotech

• Intellectual environment attract

staff and companies

• Continuous supply of educated

workers

• Industry Associations to

continuously monitor and

provide feedback

• State’s drive to attract companies

• Presence of three generation of

entrepreneurs

• Intellectual environment attract

staff and companies

• Continuous supply of educated

workers

• Industry Associations to

continuously monitor and

provide feedback

• State’s drive to attract companies

• Presence of three generation of

entrepreneurs

• Boston and California face competition from Texas, Los Angeles, Philadelphia for funds. Companies

locating manufacturing facilities elsewhere for low real estate costs, higher tax benefits etc.• Continuous need to Provide space, talent, funds for the expanding cluster• Needs to continue focus on scientific collaboration and innovation• Emerging clusters pose competition due to low cost, high growth potential for companies

Key Capabiliti

es

Key Capabiliti

es

Key Issues

Key Issues

11

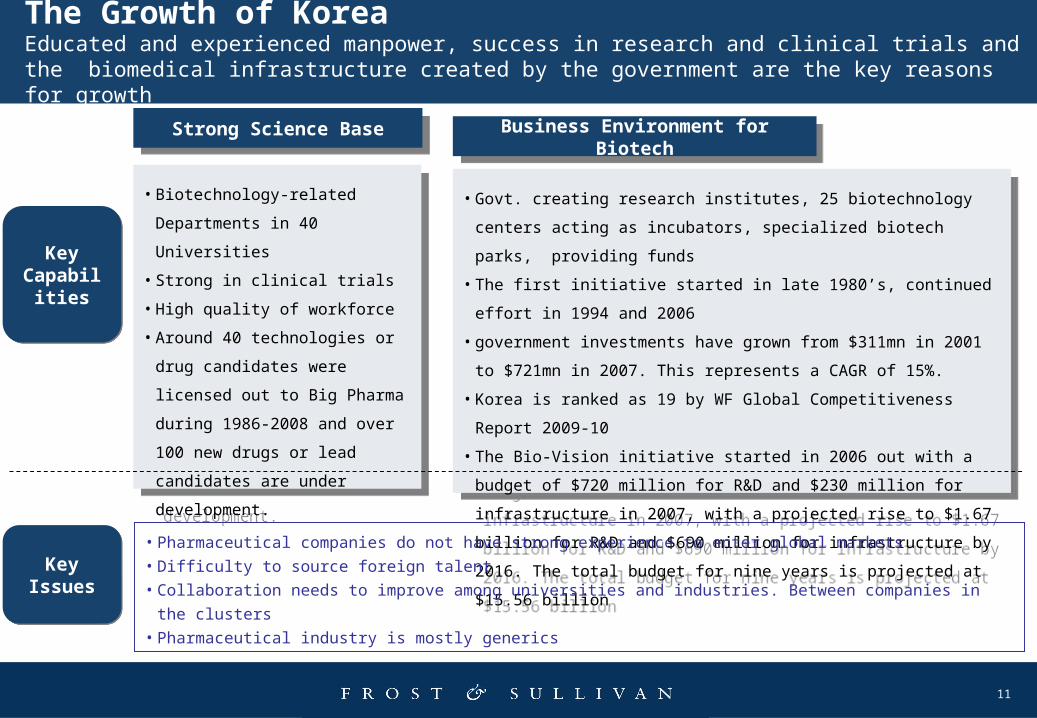

The Growth of Korea Educated and experienced manpower, success in research and clinical trials and the biomedical infrastructure created by the government are the key reasons for growth

Strong Science BaseStrong Science Base

• Biotechnology-related Departments

in 40 Universities

• Strong in clinical trials

• High quality of workforce

• Around 40 technologies or drug

candidates were licensed out to Big

Pharma during 1986-2008 and over

100 new drugs or lead candidates

are under development.

• Biotechnology-related Departments

in 40 Universities

• Strong in clinical trials

• High quality of workforce

• Around 40 technologies or drug

candidates were licensed out to Big

Pharma during 1986-2008 and over

100 new drugs or lead candidates

are under development.

Business Environment for BiotechBusiness Environment for Biotech

• Govt. creating research institutes, 25 biotechnology centers acting as

incubators, specialized biotech parks, providing funds

• The first initiative started in late 1980’s, continued effort in 1994 and 2006

• government investments have grown from $311mn in 2001 to $721mn in

2007. This represents a CAGR of 15%.

• Korea is ranked as 19 by WF Global Competitiveness Report 2009-10

• The Bio-Vision initiative started in 2006 out with a budget of $720 million

for R&D and $230 million for infrastructure in 2007, with a projected rise to

$1.67 billion for R&D and $690 million for infrastructure by 2016. The total

budget for nine years is projected at $15.56 billion

• Govt. creating research institutes, 25 biotechnology centers acting as

incubators, specialized biotech parks, providing funds

• The first initiative started in late 1980’s, continued effort in 1994 and 2006

• government investments have grown from $311mn in 2001 to $721mn in

2007. This represents a CAGR of 15%.

• Korea is ranked as 19 by WF Global Competitiveness Report 2009-10

• The Bio-Vision initiative started in 2006 out with a budget of $720 million

for R&D and $230 million for infrastructure in 2007, with a projected rise to

$1.67 billion for R&D and $690 million for infrastructure by 2016. The total

budget for nine years is projected at $15.56 billion

• Pharmaceutical companies do not have strong experience to enter global markets• Difficulty to source foreign talent• Collaboration needs to improve among universities and industries. Between companies in the clusters• Pharmaceutical industry is mostly generics

Key Capabiliti

es

Key Capabiliti

es

Key Issues

Key Issues

12

Taiwan Clusters

• 17TH IN World, 1st in Asia

Knowledge Economy

Development by WB (2008)

• 6th in World, 2nd in Asia

Innovation Ranking by EIU

(2007-11)

• 17TH IN World, 5th in Asia Global

Competitiveness Index (2008-

09)

• 1st Industry Cluster Development

Global Competitiveness Index ,

WEF 2006-09

Source:, Ministry of Economic Affairs Taiwan, 2009

13

AGENDA

Global Biotechnology OverviewGlobal Biotechnology Overview11

Benchmarking successful biotechnology clustersBenchmarking successful biotechnology clusters22

Malaysia in the context of biotechnologyMalaysia in the context of biotechnology33

14

DR

IVER

S

Availability of Research grants and Govt support

Cost-competitive labor

Rich biodiversity

Cost effective leading to potentially higher profit margins

Market demand as acceptability of biotech in all areas increases

Good infrastructure, good transportation network

National Biotechnology Policy

BioNexus Status

RES

TR

AIN

TS

Structural and background as manufacturing country

Time to build technology background

Insufficient funding

Human resource

Lack of financial loans from financial institutions

Malaysia’s Biotechnology Industry:Overall Market Drivers and Restraints

15

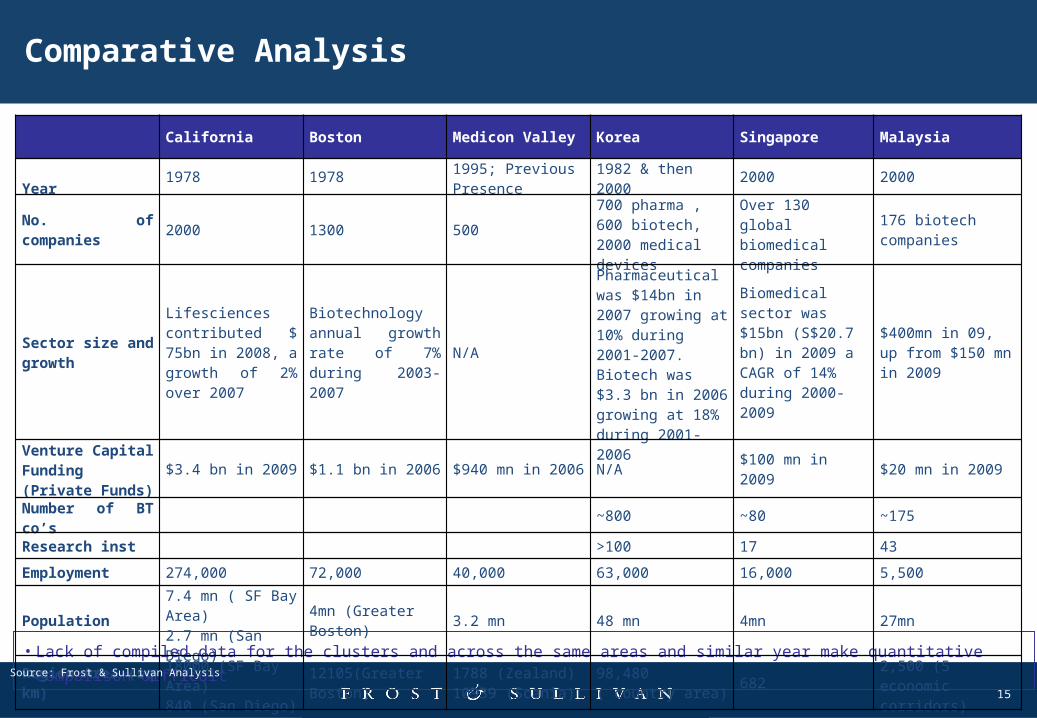

Comparative Analysis

• Lack of compiled data for the clusters and across the same areas and similar year make quantitative comparison difficult

California Boston Medicon Valley Korea Singapore Malaysia

Year 1978 1978 1995; Previous Presence 1982 & then 2000 2000 2000

No. of companies 2000 1300 500700 pharma , 600 biotech, 2000 medical devices

Over 130 global biomedical companies

176 biotech companies

Sector size and growth

Lifesciences contributed $ 75bn in 2008, a growth of 2% over 2007

Biotechnology annual growth rate of 7% during 2003-2007

N/A

Pharmaceutical was $14bn in 2007 growing at 10% during 2001-2007. Biotech was $3.3 bn in 2006 growing at 18% during 2001-2006

Biomedical sector was $15bn (S$20.7 bn) in 2009 a CAGR of 14% during 2000-2009

$400mn in 09, up from $150 mn in 2009

Venture Capital Funding (Private Funds)

$3.4 bn in 2009 $1.1 bn in 2006 $940 mn in 2006 N/A $100 mn in 2009 $20 mn in 2009

Number of BT co’s ~800 ~80 ~175

Research inst >100 17 43

Employment 274,000 72,000 40,000 63,000 16,000 5,500

Population7.4 mn ( SF Bay Area)2.7 mn (San Diego)

4mn (Greater Boston) 3.2 mn 48 mn 4mn 27mn

Region Area (sq km)

18000 (SF Bay Area) 840 (San Diego)

12105(Greater Boston)

1788 (Zealand)10939 (Scania)

98,480 ( country area) 682 2,500 (5 economic

corridors)

Source: Frost & Sullivan Analysis

16

Key Attributes of Successful Biotech Clusters

. . . . Priorities for Malaysia

Industry MaturityIndustry Maturity

Funding AvailabilityFunding Availability

• Presence and nature of biotech companies (e.g. Startup, early stage, late development, mature commercial, enabling service)

• Quantity and diversity of lifesciences stakeholders (e.g. R&D, medical devices, clinical trials and manufacturing, supporting industries)

• Growth in Output – stagnated growth, slow growth or faster than industry

• Presence and nature of biotech companies (e.g. Startup, early stage, late development, mature commercial, enabling service)

• Quantity and diversity of lifesciences stakeholders (e.g. R&D, medical devices, clinical trials and manufacturing, supporting industries)

• Growth in Output – stagnated growth, slow growth or faster than industry

• Availability of funding to support early stage company research

• Funding for established biotech companies to invest in additional infrastructure and clinical research to move products into the market place

• Public and Private funding channels

• Availability of funding to support early stage company research

• Funding for established biotech companies to invest in additional infrastructure and clinical research to move products into the market place

• Public and Private funding channels

University/Medical Centre MaturityUniversity/Medical Centre Maturity

Regulatory and Business EnvironmentRegulatory and Business Environment

• Strong research universities and academic medical centers, supported by effective technology transfer offices, as a key source of innovation and talent

• Collaborative relationships between research universities and academic medical centers to sustain invention and innovation

• Areas of Research and Commercialization Success

• Strong research universities and academic medical centers, supported by effective technology transfer offices, as a key source of innovation and talent

• Collaborative relationships between research universities and academic medical centers to sustain invention and innovation

• Areas of Research and Commercialization Success

• Stable and supportive public policy structure• Supportive business environment to retain existing

companies and / or attract new enterprises (e.g., taxes, permitting, costs, IP protection)

• Stakeholder Synergy

• Stable and supportive public policy structure• Supportive business environment to retain existing

companies and / or attract new enterprises (e.g., taxes, permitting, costs, IP protection)

• Stakeholder Synergy

Source: Frost & Sullivan analysis

• Industry Maturity and University/Medical Centre maturity comprises Company and Science Base• Funding Availability Remains Same• Regulatory and Business Environment comprises other seven factors

17

Setting the stage…

33

44

55

66

22

11

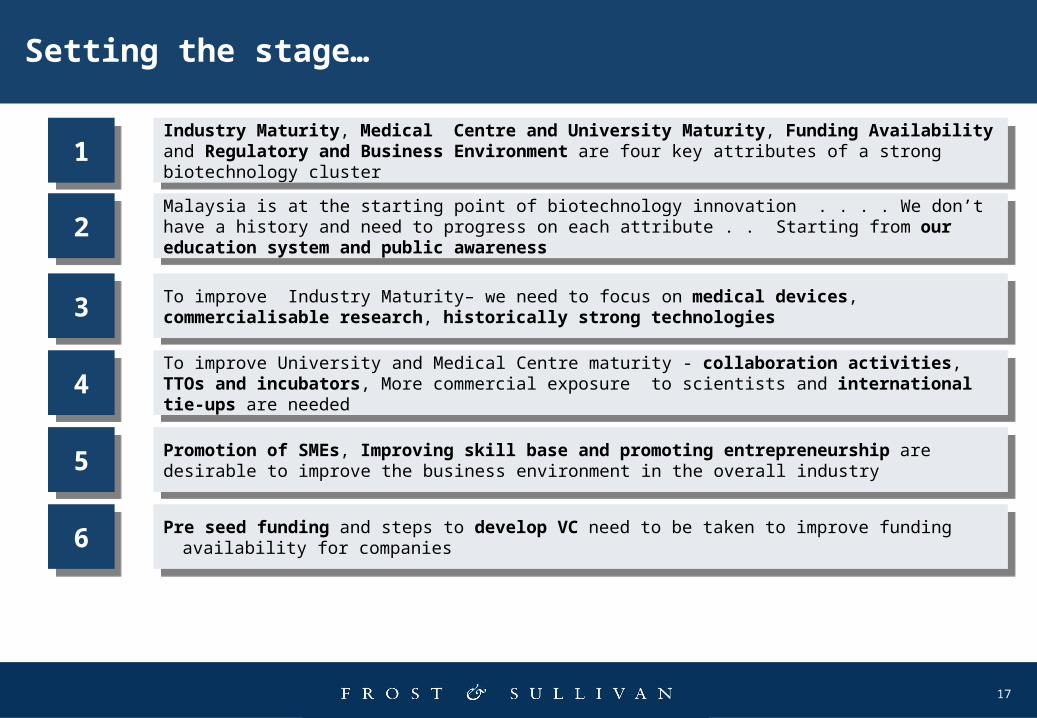

To improve Industry Maturity– we need to focus on medical devices, commercialisable research, historically strong technologies

To improve Industry Maturity– we need to focus on medical devices, commercialisable research, historically strong technologies

To improve University and Medical Centre maturity - collaboration activities, TTOs and incubators, More commercial exposure to scientists and international tie-ups are needed

To improve University and Medical Centre maturity - collaboration activities, TTOs and incubators, More commercial exposure to scientists and international tie-ups are needed

Promotion of SMEs, Improving skill base and promoting entrepreneurship are desirable to improve the business environment in the overall industry

Promotion of SMEs, Improving skill base and promoting entrepreneurship are desirable to improve the business environment in the overall industry

Pre seed funding and steps to develop VC need to be taken to improve funding availability for companiesPre seed funding and steps to develop VC need to be taken to improve funding availability for companies

Malaysia is at the starting point of biotechnology innovation . . . . We don’t have a history and need to progress on each attribute . . Starting from our education system and public awareness

Malaysia is at the starting point of biotechnology innovation . . . . We don’t have a history and need to progress on each attribute . . Starting from our education system and public awareness

Industry Maturity, Medical Centre and University Maturity, Funding Availability and Regulatory and Business Environment are four key attributes of a strong biotechnology cluster

Industry Maturity, Medical Centre and University Maturity, Funding Availability and Regulatory and Business Environment are four key attributes of a strong biotechnology cluster

18

Proactive commercialization in Research and Academic Centers – Learning from Yale University

Technology Transfer at Yale University

Technology Transfer at Yale University ImpactImpact

• Only six biotech companies in 1993• The hard work of seeking appropriate investors

eventually paid off, and in 1998, after two years

of effort, the first round of financing was

concluded with $20 million for five companies.• Today the Connecticut cluster employs 17,985

people directly and 35,857 through indirect and

induced employment. It consists of 49

biotechnology companies. Five of the biotech

companies are publicly traded: Alexion

Pharmaceuticals, Neurogen, Curagen,

Gennesiance, and Vion Pharmaceuticals. Of

the biotech companies, 24 companies, or 49%,

of the biotechnology cluster in New Haven

were created after 1996 with technology, ideas,

or founders from Yale and with the help of the

OCR.

• Only six biotech companies in 1993• The hard work of seeking appropriate investors

eventually paid off, and in 1998, after two years

of effort, the first round of financing was

concluded with $20 million for five companies.• Today the Connecticut cluster employs 17,985

people directly and 35,857 through indirect and

induced employment. It consists of 49

biotechnology companies. Five of the biotech

companies are publicly traded: Alexion

Pharmaceuticals, Neurogen, Curagen,

Gennesiance, and Vion Pharmaceuticals. Of

the biotech companies, 24 companies, or 49%,

of the biotechnology cluster in New Haven

were created after 1996 with technology, ideas,

or founders from Yale and with the help of the

OCR.

• High support–high selectivity policies needed for entrepreneurially

underdeveloped environments• Provided facilities like creation of business plan, providing mentoring

support, promotion of success stories, having entrepreneurial

courses in curriculum, incentives for starting up, getting

entrepreneurs to set up in the region and chasing VCs• Gregory Gardiner, a former Pfizer executive took charge of Office of

Cooperative Research in 1982• An important goal for the Yale OCR was to identify new ideas,

cultivate venture funding for them, and facilitate their development

into companies that become part of the New Haven economy. • Increased exposure of researchers to commercial ideas• The renewed OCR established direct contacts with venture capital

firms. The goal was not only to persuade venture capital firms of the

relevance of university technology but also to convince them to

create ventures in New Haven

• High support–high selectivity policies needed for entrepreneurially

underdeveloped environments• Provided facilities like creation of business plan, providing mentoring

support, promotion of success stories, having entrepreneurial

courses in curriculum, incentives for starting up, getting

entrepreneurs to set up in the region and chasing VCs• Gregory Gardiner, a former Pfizer executive took charge of Office of

Cooperative Research in 1982• An important goal for the Yale OCR was to identify new ideas,

cultivate venture funding for them, and facilitate their development

into companies that become part of the New Haven economy. • Increased exposure of researchers to commercial ideas• The renewed OCR established direct contacts with venture capital

firms. The goal was not only to persuade venture capital firms of the

relevance of university technology but also to convince them to

create ventures in New Haven

Source: University Commercialization Strategies in the Development of Regional Bioclusters , Shiri M. Breznitz, Rory P. O’Shea, and Thomas J. Allen published in Journal of Product Innovation Management 2008