ASKMORE Plus

15

If you want to know more, ASKMORE TM modeFinance’s credit report. Almost every day millions of people around the world are wondering the real creditworthiness of the companies with which they are in business. Every day these questions remain unanswered. modeFinance TM now aims to answer these questions in a simple, complete and immediate way. ASKMORE TM is the modeFinance TM product which gives the chance to evaluate the credit risk for every company from all around the world. ASKMORE TM plans 2 types of reports: Basic Plus ASKMORE TM Plus: This is the most comprehensive and detailed report prepared by modeFinance TM ’ s analysts. It includes modeFinance TM ’ s MORE Credit Ratings and MORE Credit Limit, plus all essential information including financial statements of the last three years and descriptive information. The added value of this report is the deep financial analysis made by modeFinance TM ’ s analysts, with market overview, industry drivers, trends and competitive enviroment. This report type is ideally suited for having a deeper knowledge about the financial status of the company. modeFinance TM Headquarter Building A - AREA Science Park Padriciano 99 - 34149 Trieste - Italy Ph.: +39 040 375 5337 Fax: +39 040 375 6741 info@modefinance.com askMORE TM is a registered mark of modeFinance TM PPG VIETNAM COMPANY LIMITED Friday, 10 June 2011 MORE Credit Rating key D C CC CCC B BB BBB A AA AAA MORE Credit Rating key D C CC CCC B BB BBB A AA AAA not available non return extremly pathological pathological high danger weak sufficient adequate good very strong extremely strong Company name PPG VIETNAM COMPANY LIMITED Identification number mFCR0004136 Country Vietnam ZIP code and city - Ho Chi Minh City Address Flr 17, Fedeco Tower, Unit 1701, 81 - 85 Ham Nghi Str, Nguyen Thai Binh Ward - District 1 - Ho Chi Minh City - Vietnam (84 - 8) 38233014 / 38233013 / 38274182 / 38272332 http://www.ppg.com [email protected] Legal form Foreign invested company Account Unconsolidated Incorporation date 2000 NACE 2 Sector 2030 - Manufacture of paints, varnishes and similar coatings, printing ink and mastics Listed Status Active MORE Credit limit 120,000 e 31/12/2009 31/12/2008 31/12/2007 Turnover (th e) 4,663 3,672 - Rating CCC CC C Probability of default 15.00% 41.00% 65.00% Confidence Level 100% 100% 50% Solvency ratios Leverage ratio -3.17 -3.45 -3.23 Total asset/Total liabilties 0.68 0.71 0.69 Liquidity ratios Current Ratio 0.54 0.54 0.54 Quick Ratio 0.24 0.23 0.21 Profitability and economic equili- brium ratios Return on investement ROI (%) -6.00 -13.94 - Return on equity ROE (%) -13.59 -37.25 - Asset turnover 1.48 1.10 - Interest paid weight 0.00 -0.09 - Gross Profit/Operating revenue 0.25 0.19 - Interest Coverage ratios EBIT interest coverage ratio +Inf -1.19 - Analysis and trend of financial strength

-

Upload

modefinance -

Category

Documents

-

view

214 -

download

0

description

modeFinance ASKMORE Credit Report Plus version

Transcript of ASKMORE Plus

If you want to know more, ASKMORE TM

modeFinance’s credit report.

Almost every day millions of peoplearound the world are wondering the realcreditworthiness of the companies withwhich they are in business. Every daythese questions remain unanswered.modeFinance

TM

now aims to answer thesequestions in a simple, complete andimmediate way.

ASKMORETM

is the modeFinanceTM

product which gives the chance toevaluate the credit risk for every companyfrom all around the world.

ASKMORETM plans 2 types of reports:

Basic Plus

ASKMORETM

Plus:This is the most comprehensive anddetailed report prepared bymodeFinance

TM ’ s analysts. Itincludes modeFinance

TM

’ s MORE CreditRatings and MORE Credit Limit, plus allessential information including financialstatements of the last three years anddescriptive information. The added valueof this report is the deep financial analysismade by modeFinance TM ’ s analysts, withmarket overview, industry drivers, trendsand competitive enviroment.This report type is ideally suited for havinga deeper knowledge about the financialstatus of the company.

modeFinanceTM HeadquarterBuilding A - AREA Science ParkPadriciano 99 - 34149 Trieste - ItalyPh.: +39 040 375 5337Fax: +39 040 375 [email protected]

askMORETM is a registered mark of modeFinanceTM

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAAnot

available

non return extremlypathological

pathological highdanger

weak sufficient adequate good very

strongextremely

strong

Company name PPG VIETNAM COMPANY LIMITED

Identification number mFCR0004136

Country Vietnam

ZIP code and city - Ho Chi Minh City

Address Flr 17, Fedeco Tower, Unit 1701, 81 - 85 Ham Nghi Str, Nguyen Thai Binh

Ward - District 1 - Ho Chi Minh City - Vietnam

(84 - 8) 38233014 / 38233013 / 38274182 / 38272332

http://www.ppg.com

Legal form Foreign invested company

Account Unconsolidated

Incorporation date 2000

NACE 2 Sector 2030 - Manufacture of paints, varnishes and similar coatings, printing ink

and mastics

Listed

Status Active

MORE Credit limit 120,000 e

31/12/2009 31/12/2008 31/12/2007

Turnover (th e) 4,663 3,672 -

Rating CCC CC C

Probability of default 15.00% 41.00% 65.00%

Confidence Level 100% 100% 50%

Solvency ratios

Leverage ratio -3.17 -3.45 -3.23

Total asset/Total liabilties 0.68 0.71 0.69

Liquidity ratios

Current Ratio 0.54 0.54 0.54

Quick Ratio 0.24 0.23 0.21

Profitability and economic equili-

brium ratios

Return on investement ROI (%) -6.00 -13.94 -

Return on equity ROE (%) -13.59 -37.25 -

Asset turnover 1.48 1.10 -

Interest paid weight 0.00 -0.09 -

Gross Profit/Operating revenue 0.25 0.19 -

Interest Coverage ratios

EBIT interest coverage ratio +Inf -1.19 -

Analysis and trend of financial

strength

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

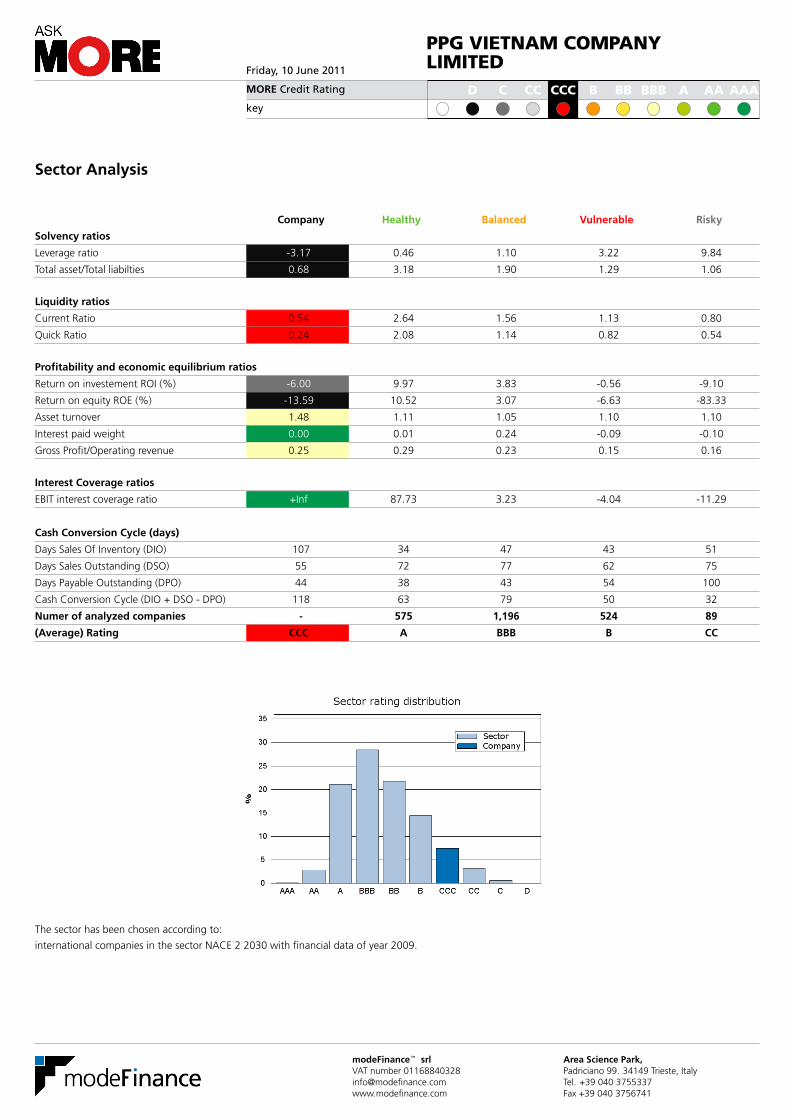

Sector Analysis

Company Healthy Balanced Vulnerable Risky

Solvency ratios

Leverage ratio -3.17 0.46 1.10 3.22 9.84

Total asset/Total liabilties 0.68 3.18 1.90 1.29 1.06

Liquidity ratios

Current Ratio 0.54 2.64 1.56 1.13 0.80

Quick Ratio 0.24 2.08 1.14 0.82 0.54

Profitability and economic equilibrium ratios

Return on investement ROI (%) -6.00 9.97 3.83 -0.56 -9.10

Return on equity ROE (%) -13.59 10.52 3.07 -6.63 -83.33

Asset turnover 1.48 1.11 1.05 1.10 1.10

Interest paid weight 0.00 0.01 0.24 -0.09 -0.10

Gross Profit/Operating revenue 0.25 0.29 0.23 0.15 0.16

Interest Coverage ratios

EBIT interest coverage ratio +Inf 87.73 3.23 -4.04 -11.29

Cash Conversion Cycle (days)

Days Sales Of Inventory (DIO) 107 34 47 43 51

Days Sales Outstanding (DSO) 55 72 77 62 75

Days Payable Outstanding (DPO) 44 38 43 54 100

Cash Conversion Cycle (DIO + DSO - DPO) 118 63 79 50 32

Numer of analyzed companies - 575 1,196 524 89

(Average) Rating CCC A BBB B CC

The sector has been chosen according to:

international companies in the sector NACE 2 2030 with financial data of year 2009.

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

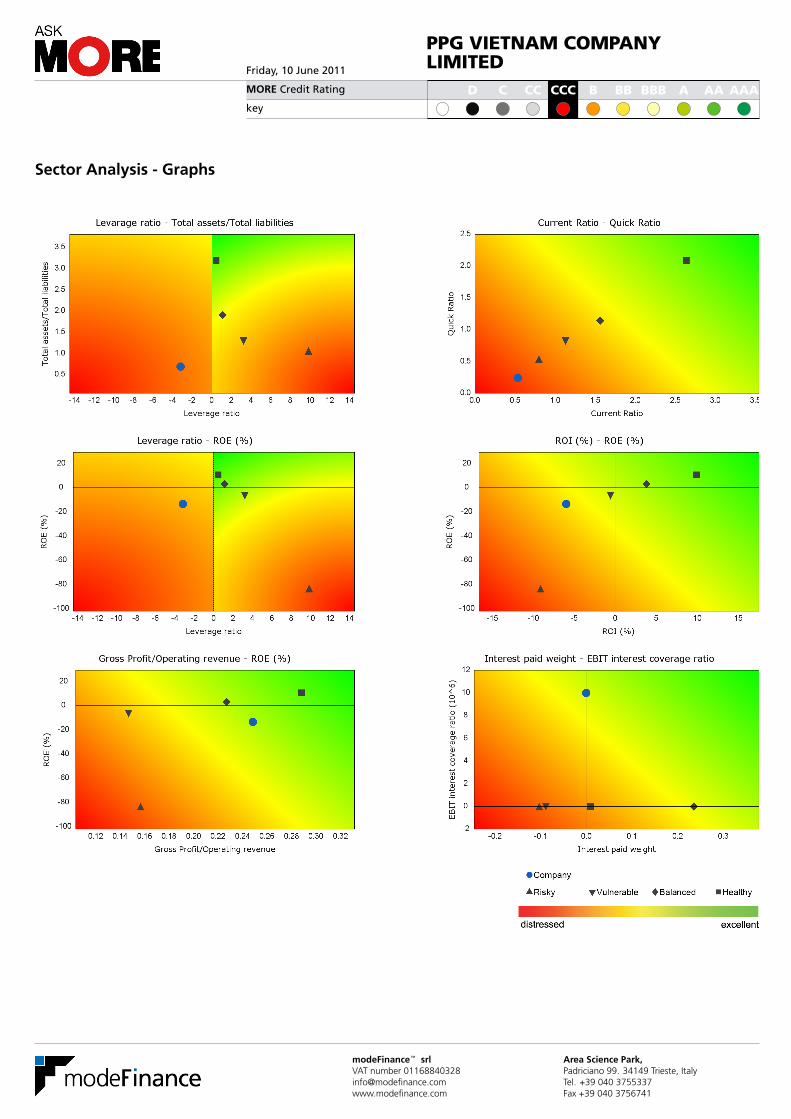

Sector Analysis - Graphs

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

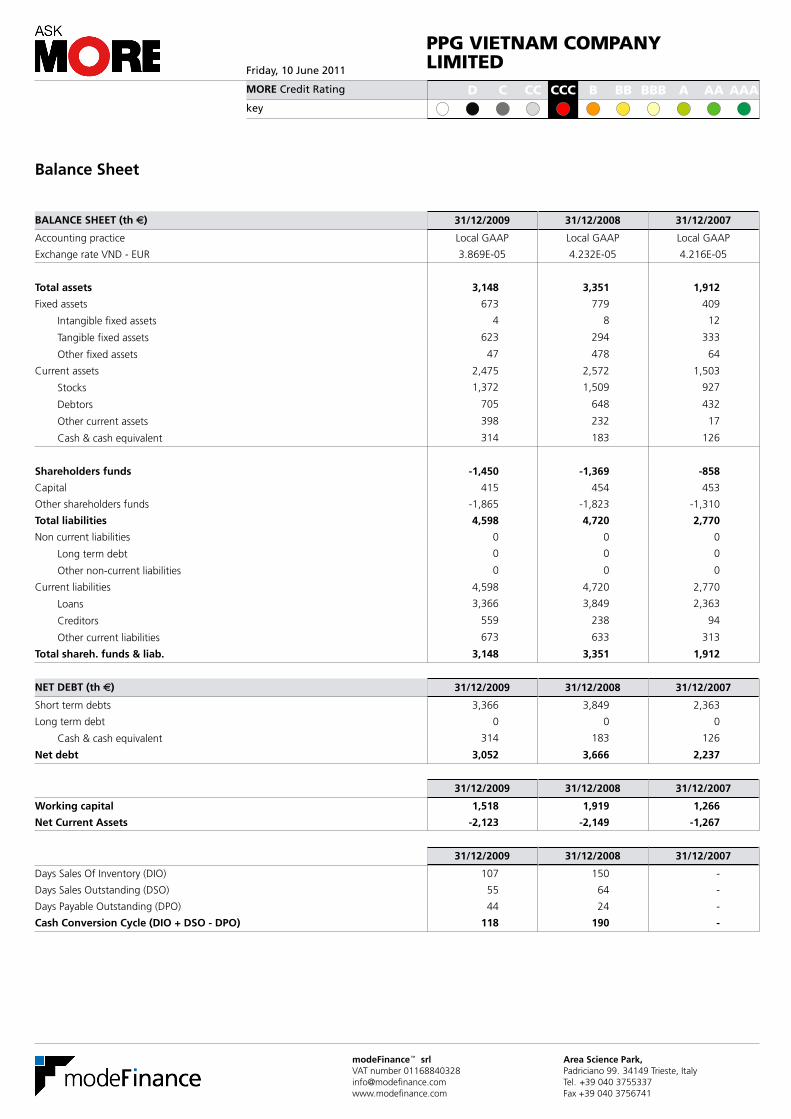

Balance Sheet

BALANCE SHEET (th e) 31/12/2009 31/12/2008 31/12/2007

Accounting practice Local GAAP Local GAAP Local GAAP

Exchange rate VND - EUR 3.869E-05 4.232E-05 4.216E-05

Total assets 3,148 3,351 1,912

Fixed assets 673 779 409

Intangible fixed assets 4 8 12

Tangible fixed assets 623 294 333

Other fixed assets 47 478 64

Current assets 2,475 2,572 1,503

Stocks 1,372 1,509 927

Debtors 705 648 432

Other current assets 398 232 17

Cash & cash equivalent 314 183 126

Shareholders funds -1,450 -1,369 -858

Capital 415 454 453

Other shareholders funds -1,865 -1,823 -1,310

Total liabilities 4,598 4,720 2,770

Non current liabilities 0 0 0

Long term debt 0 0 0

Other non-current liabilities 0 0 0

Current liabilities 4,598 4,720 2,770

Loans 3,366 3,849 2,363

Creditors 559 238 94

Other current liabilities 673 633 313

Total shareh. funds & liab. 3,148 3,351 1,912

NET DEBT (th e) 31/12/2009 31/12/2008 31/12/2007

Short term debts 3,366 3,849 2,363

Long term debt 0 0 0

Cash & cash equivalent 314 183 126

Net debt 3,052 3,666 2,237

31/12/2009 31/12/2008 31/12/2007

Working capital 1,518 1,919 1,266

Net Current Assets -2,123 -2,149 -1,267

31/12/2009 31/12/2008 31/12/2007

Days Sales Of Inventory (DIO) 107 150 -

Days Sales Outstanding (DSO) 55 64 -

Days Payable Outstanding (DPO) 44 24 -

Cash Conversion Cycle (DIO + DSO - DPO) 118 190 -

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Income Statement

INCOME STATEMENT (th e) 31/12/2009 31/12/2008 31/12/2007

Accounting practice Local GAAP Local GAAP Local GAAP

Exchange rate VND - EUR 3.869E-05 4.232E-05 4.216E-05

Sales 4,705 3,672 -

Revenues growth (%) 28.1 - -

Other revenues +/- variation in inventories and contract in progress + Fixed assets

own construction capitalized-42 0 -

Operating revenue / turnover 4,663 3,672 -

Total operating costs 4,452 3,723 -

Costs growth (%) - - -

Service costs - - -

Material costs - - -

Costs of employees - - -

EBITDA - - -

Depreciation - - -

EBIT 210 -50 -

Financial P/L -400 -458 -

Financial revenue 9 2 -

Financial expenses 408 460 -

Interest paid 0 42 -

P/L before tax -189 -509 -

Extr. and other P/L -8 -1 -

Extr. and other revenue 0 0 -

Extr. and other expenses 8 1 -

P/L before tax + Extr. and other P/L -197 -510 -

Taxation 0 0 -

P/L for period -197 -510 -

31/12/2009 31/12/2008 31/12/2007

Costs of Good Sold 3,505 2,982 -

Gross Profit 1,158 691 -

Other Operating Expenses 948 741 -

31/12/2009 31/12/2008 31/12/2007

Cash flow - - -

Added value - - -

31/12/2009 31/12/2008 31/12/2007

Number of employees - - -

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Evolutions and trends

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Qualitative information

Full overview PPG VIETNAM COMPANY LIMITED (Vietnamese Name: CONG TY TNHH PPG VIETNAM)is a wholly owned foreign

company invested by PPG INDUSTRIAL SECURITIES INC based in USA (PPG Industries Inc. is a global manufacturer

and supplier of coatings, chemicals and glass that operates 120 manufacturing locations in 23 countries worldwi-

de). It is specialized in manufacturing and distributing paints for automobiles, architecture and industrial products.

Its investment ceritificate no is 472043000648 (granted on 29 Aug 2008 by Dong Nai Industrial Zones Authority).

Tax code is 3600478837. The number of total employees is 40.

History PPG was established on October, 2000. On August 29th, 2008 the subject changed investment license number

from No. 57/GP - KCN - DN to No. 472043000648. On 11 Feb 2009, the subject changed its address from “Floor

10th, Room 5, Sai Gon Centre, No. 65 Le Loi Str, Dist 1, Hochiminh City” to No. 81 - 85, Ham Nghi Str, Nguyen

Thai Binh Ward, Dist. 1, Hochiminh City. The total investment capital and the chartered capital were raised to USD

22,333,000 and USD 3,700,000 respectively on March 2010.

Primary business line The subject is specialized in manufacturing and trading paint and materials for paint production industry.

Secondary business line Not available.

Main activity Manufacture and coating.

Secondary activity Distribution.

Main products and services Paints and coatings for automobiles, architecture and industrial products.

Size estimate The total number of the employees is 40.

Strategy, organization and policy Not available.

Strategic alliances Not available.

Membership of a network Not available.

Main brand names Not available.

Main domestic country Not available.

Main foreign countries or regions PPG imports materials from Australia, USA, Japan, Malaysia, Thailand, and China (Payment method is T/T). The

subject at the moment does not export.

Main production sites The company has a factory in the following address: No. 103/5 AMATA Industrial Zone - Bien Hoa City - Dong Nai

Province - Vietnam (Tel: (84 - 61) 3936761). The premises and facilities of the subject are normal. Its main factory

is located at Amata Industrial Zone with 800m2 and production capacity about 100,000 tons/ a year. It also has

a small workshop at Bien Hoa 1 Industrial Zone, Dong Nai Province. The subject co - operates in production with

Dong Nai Paint corporation. It has a factory in Yen Phong Industrial Zone, Bac Ninh Province - Northern Province.

Besides, the subject also gets much support from the parent company. The subject has refused the local provider

to give them more detailed information about factories.

Main distribution sites Not available.

Main sales representation sites Not available.

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Main customers The subject provided products for many manufacturers such as Blue Corp Steel, Hoa Sen Steel, Pos Vina, BP, LG

gas, and Shell gas.

The products of its parent company are supplied for automobile assemblers in Vietnam such as Mercedes, Ford,

Truong Hai Auto, VMC, ISUZU, SAMCO, and Daewoo., etc.

Auditor/Advisor/Bank

name type address

CITI BANK Bank No. 115 Nguyen Hue Str, Ben Nghe Ward, District 1 - Ho Chi Minh City -

Vietnam (Tel:(84 - 8) 8242118 )

JOINT STOCK COMMERCIAL BANK FOR FO-

REIGN TRADE OF VIETNAM HO CHI MINH

BRANCH

Bank No. 29 Ben Chuong Duong - District 1 - Ho Chi Minh City - Vietnam

(Tel:(84 - 8) 3829 7245 - 3823 0310 - 3823 0311 )

Board

name date of birth nationality function

Mr. SEKMAKAS VIKTORAS RIMAS - Malaysian General Director

Mr. NGUYEN DINH LONG - Vietnamese Managing Director

Mr. PHAN THU DINH - - Purchasing Manager

Ms. VO THI THUY HANG - Vietnamese Chief Accountant

Sharehoders (the first twenty shareholders ordered by Direct %))

PPG INDUSTRIES SECURITIES, INC. Rating: -

Country ISO code US Operating revenue (MIL $) -

NACE Rev. 2, Core code - Total Assets (MIL $) -

Direct % 100.00 Number of Employees -

Total % - Information date 05/2011

Address: 1, PPG Place, 15272 PITTSBURGH, United States of America, Tel: (412) 434 - 3131

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Subsidiaries (the first twenty subsidiaries ordered by Direct %)

Not available.

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

modeFinance analyst comments

General comment MORE ratings assigned to PPG Vietnam is CCC for the year 2009. The company is extremely weak in solvency and

liquidity. Inspite of the sales’ increase in 2009, high cost structure and financial expenses have led to losses at the

end of the year. Even when compared with the sector average values, the company’s situation is quite risky.

Solvency In terms of solvency, PPG is in a quite risky position (please see negative shareholders’ funds in balance sheet).

Negative shareholders’ funds is due to the negative retained earnings in three years. The liabilities are only com-

posed of current liabilities (mostly short term debts - loans) which makes company’s financial situation even more

delicate.

Profitability The total sales value has increased by 41% (according to the original income statements) from 2008 to 2009 which

is an impressive progress; and also the company succeded to increase its gross profit from 691 theto 1,158 th e.

The EBIT value was negative (- 50 the) in 2008 and turned into a positive value (210 the). However, the financial

expenses lead to a financial loss in 2009 as well as the situation in 2008. Finally, the company finishes the year

2009 with a loss of - 197 the(that is less than the loss of - 510 thein 2008); hence both ROI and ROE keep their

negative values. The progress in asset turnover (from 1,10 to 1,48) can be explained by the increase in the sales

showing that the company increased its efficiency in using the assets to increase the sales. Gross Profit margin has

improved by a rise from sufficient levels to adequate levels.

Comparison with the sector Both solvency (leverage: - 3,17 and total assets/total liabilities: 0,68) and liquidity (current ratio: 0,54 and quick

ratio: 0,24) indicators show that the subject is closer to the risky levels in the sector. Both ROI and ROE indicators

are also around risky levels. The company having a gross profit margin with a value of 0,25 is between healthy

levels and balanced levels explanining that it is closer to the succesful companies within the same sector. Cash

Conversion Cycle (118 days) is longer than the sector, this is mainly due to the long day sales of inventory (107

days).

Other comments Both current (0,54) and quick ratio (0,24) are in high danger levels. Also in comparison with the sector, these levels

are even below risky levels indicating the company is not in a liquid position at all. One other piece of information

is that the given website (www. ppg. com) belongs to the parent company of the subject.

Comments from local provider The rating assigned by local provider to the company is B (Average: The company’s stability is expected to be

IMPAIRED by adverse changes in circumstances and economic conditions). The local provider stated as: Based

on the financial data, the total sales were considerably increased from VND 86,820,000,000 in 2008 to VND

121,614,000,000 in 2009. The subject made loss over the last few years in a decreasing trend. The global

recession and credit crisis could continue to have negative impact on its results of operations and cash flows. It

has been facing with difficulties in business in economic crisis. However now the subject’s business status is stable

again. Moreover, there is also another aspect related to the loss at the end of the year. The FDI (foreign direct

investment) companies operating in Vietnam which is that they accept to make loss on accounting basis to transfer

profit back to the parent company in the foreign market and to avoid paying corporate tax in Vietnam.

Payment history According to the provider, the Trade morality is “Normal“; liquidity is “Low“, Payment Status is “Limited” and

Financial Situation is “Below Average“. There were no records found regarding Litigation and Bankruptcy. The

subject has the capacity to meet small financial commitments. The payment methods of the subject are Document

Against Payment (D/P) and Letter of Credit (L/C).

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

ASKMORE rating guide

General vision A credit rating is an opinion of the general creditworthiness of an obligor (issuer rating), or the creditworthiness of

an obligor in respect of a specific debt security, or other financial obligation (issue rating), based on relevant risk

factors.

The Multi Objective Rating Evaluation (MORE) model is essentially used to assess the level of distress of industrial

companies by using data included in financial statements.

The basic idea of the model is to analyze a set of financial and economic ratios in a predictive corporate bankruptcy

model with the purpose of creating a fundamental credit rating model for each industrial sector. Results of the

model are obtained by applying newly developed numerical methodologies, drawing together financial theory,

data mining and engineering design methodologies. The heart of MORE is a multi dimensional and multi objective

algorithm that produces a classification of each company, by taking into account any attributes (such as sector and

country) characterizing a firm.

The model gives the opportunity to assign a rating to a company even without considering a complete data analysis

and allows to process quality information. It induces a better understanding of a company’s strength and weakness

thanks to sophisticated data mining tools and taking into account the analyst knowledge.

The MORE rating vision is to look at the fundamental economics of the company. The main idea is to evaluate the

rating observing every aspect of the economical and financial behavior of the company: better is the equilibrium

between the different aspects, better will be the final rating.

This is done studying, evaluating and aggregating the most important sections of the financial and economic

behavior of a company such as: profitability, liquidity, solvency, interest coverage and efficiency.

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Rating scale

Rating class Rating macro class Assessment

AAA

Healthy

The company’s capacity to meet its financial commitments is extremely strong. The company shows an excellent

economic and financial flow and fund equilibrium.

AAThe company has very strong creditworthiness. It also has a good capital structure and economic and financial

equilibrium. Difference from AAA is slight.

AThe company has a high solvency. The company is however more susceptible to the adverse effects of changes in

circumstances and economic conditions than companies in higher rated categories.

BBB

Balanced

Capital structure and economic equilibrium are considered adequate. The company’s capacity to meet its financial

commitments could be affected by serious unfavourable events.

BBA company rated BB is more vulnerable than companies rated BBB. Furthermore the company faces major ongoing

uncertainties or exposure to adverse business, financial, or economic conditions.

B

Vulnerable

The company presents vulnerable signals with regards to its fundamentals. Adverse business, financial, or economic

conditions will be likely to impair the company’s capacity or willingness to meet its financial commitments.

CCC

A company rated CCC has a dangerous disequilibrium on the capital structure and on its economic and financial

fundamentals. Adverse market events and an inadequate management could affect with high probability the

company’s solvency.

CC

Risky

The company shows signals of high vulnerability. In the event of adverse market and economic conditions, the

company’s strong disequilibrium could increase.

CThe company shows considerable pathological situations. The company’s capacity to meet its financial

commitments is very low.

D The company has not any longer the capacity to meet its financial commitments.

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Fundamental Credit Rating Ratios

Analysis area Ratio Assessment

Solvency ratios

Leverage ratioThis measures the level of total liabilities of the company in comparison

with equity.

Assets to debtThis indicates company’s solvency. The company shows a level of deficit

when the value of this ratio is under one unit.

Financial ratios Fixed Assets coverage ratioThis is calculated only for holdings. It measures the capital structure i.e.

whether a company covers the fixed assets with long term capital.

Liquidity ratios

Current ratioThis measures whether a company has sufficient short-term assets to cover

its short-term liabilities.

Quick ratioThis compares current liabilities only to those assets that can be readily

turned into cash.

Profitability and economic ratios

Return on Investement(ROI)This measures the profitability of company investments without regard to

the way the investment is financed.

Return on Equity(ROE) This measures the profitability of the equity.

Asset turnover

This indicates the investments turnover with regards to sales. The level

assumed from the ratio depends on the sector in which the company

operates.

Profit margin This indicates the profitability of sales.

Interest coverage ratio Interest Paid coverage

This indicate the ability of the company to cover interest expenses through

the economic margins (Gross profit and EBIT) and through the cash flow

from operating activities.

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

MORE Credit Limit, Probability of default and Confidence Level

MORE Credit Limit MORE Credit limit is the estimation of the amount of maximum credit that is possible to assign on a commercial

relationship with the analyzed company with an outlook of one year.

modeFinance used the following values associated with the company analyzed while computing the credit limit:

• Size;

• Years in Business;

• Average number of suppliers;

• Liquidity of the company and the comparison with its sector;

• The funds dedicated to be paid to suppliers;

• The likelihood that a company may pay its debts in the next 12 months (MORE Ratings).

The credit limit in this report is merely a suggested value of commercial credit limit calculated on the basis of annual

public data. This value should be reviewed by paying attention to the Confidence Level value and by using other

information such as other business information, news... etc; and private information such as the relationship with

client, history of payments, guarantees and the knowledge of the sector.

Probability of default e Confidence

Level

In addition to the MORE Rating, modeFinance also estimates the probability of default and provides a level of

confidence. The probability of default is the degree of certainty (in quantitative terms) that the company will go

into default.

As the probability of default is strongly affected by the economic climate that the company is operating in,

companies in the same MORE class will not necessarily have the same probability of default.

The MORE model can produce a MORE rating even if there is missing data by using an associated confidence level:

Confidence =

∑Available Information∑

Total Information

The level of confidence does not indicate financial confidence in the company. It is a reflection of the variations in

availability of financial data across Europe due to filing regulations and suggests the degree of financial detail the

MORE rating is able to take into account for each company.

For companies with fully populated records a confidence level of 100% would be applied: companies where no

financial data is provided, 0%. This puts the MORE rating in a context for the user and aids interpretation.

PPG VIETNAM COMPANYLIMITEDFriday, 10 June 2011

MORE Credit Rating

key

D C CC CCC B BB BBB A AA AAA

modeFinance TM srlVAT number [email protected]

Area Science Park,Padriciano 99. 34149 Trieste, ItalyTel. +39 040 3755337Fax +39 040 3756741

Notes and disclaimer

NOTES The present analysis was based on the company available financial statements as provided by Bureau Van Dijk

Electronic Publishing - ORBIS database (lack of both Notes to financial statements and Report on operations).

DISCLAIMER All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any

form by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of

the publisher modeFinance. The facts of this report are believed to be correct at the time of publication but cannot

be guaranteed. Please note that the findings, conclusions and recommendations that modeFinance delivers will

be based on information gathered in good faith from both primary and secondary sources, whose accuracy we

are not always in a position to guarantee. As such modeFinance can accept no liability whatever for actions taken

based on any information that may subsequently prove to be incorrect.

Contacts

Company modeFinance

Products MORE rating

Where AREA Science Park

34149 Trieste, via Padriciano 99 - ITALY

Info [email protected]

web www.modefinance.com

Phone +39 040 3755337