Asia’s tsunami: the impact - Economist Intelligence...

28

Special Report Special Report Special Report Special Report Asia’s tsunami: the impact January January January January 2005 2005 2005 2005 The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom

Transcript of Asia’s tsunami: the impact - Economist Intelligence...

Special ReportSpecial ReportSpecial ReportSpecial Report

Asia’s tsunami: the impact

JanuaryJanuaryJanuaryJanuary 2005200520052005

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence UnitThe Economist Intelligence UnitThe Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where thelatest analysis is updated daily; through printed subscription products ranging from newsletters to annualreference works; through research reports; and by organising seminars and presentations. The firm is amember of The Economist Group.

LondonLondonLondonLondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkNew YorkNew YorkNew YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongHong KongHong KongHong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryElectronic deliveryElectronic deliveryElectronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databasesand as direct feeds to corporate intranets. For further information, please contact your nearest EconomistIntelligence Unit office

CopyrightCopyrightCopyrightCopyright© 2005 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, theEconomist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-7106

Symbols for tablesSymbols for tablesSymbols for tablesSymbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

EIU Special Report January 2005 © The Economist Intelligence Unit Limited 2005

ContentsContentsContentsContents

1 At-a-glance: countries most affected by the tsunami

4 Overview: implications of the tsunami

7 Indonesia: crisis-management test for Yudhoyono

10 Sri Lanka: the biggest economic impact

12 Thailand: a shock to the tourism industry

16 India: limited economic toll

18 In focus: debt deferral after the tsunami

21 Asia: the impact on industries

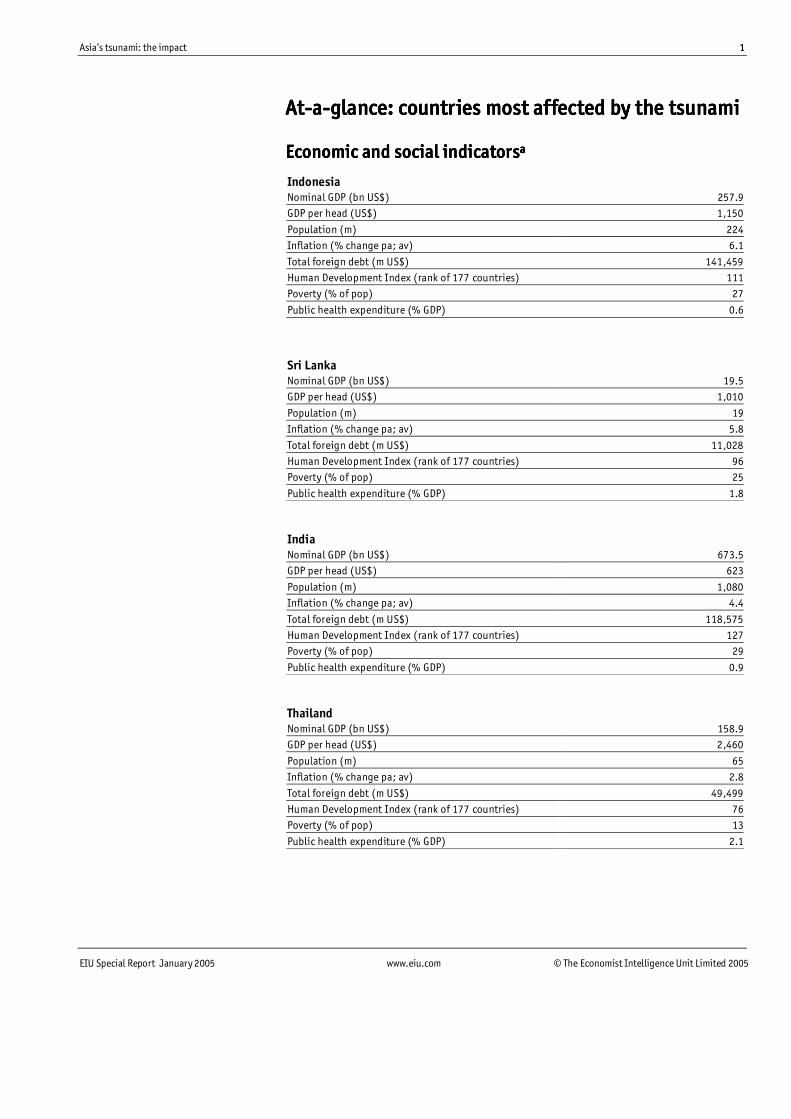

Asia’s tsunami: the impact 1

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

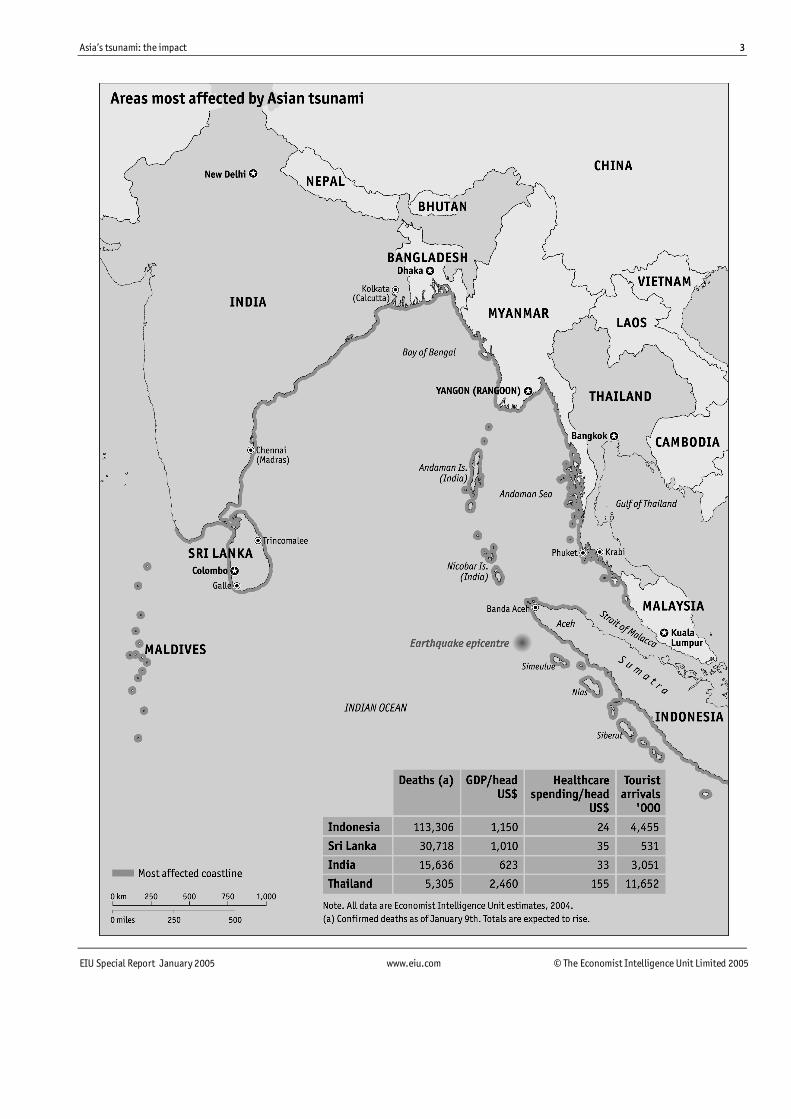

At-a-glance: countries most affected by the tsunamiAt-a-glance: countries most affected by the tsunamiAt-a-glance: countries most affected by the tsunamiAt-a-glance: countries most affected by the tsunami

Economic and social indicatorsEconomic and social indicatorsEconomic and social indicatorsEconomic and social indicatorsaaaa

IndonesiaNominal GDP (bn US$) 257.9GDP per head (US$) 1,150

Population (m) 224Inflation (% change pa; av) 6.1

Total foreign debt (m US$) 141,459Human Development Index (rank of 177 countries) 111Poverty (% of pop) 27

Public health expenditure (% GDP) 0.6

Sri LankaNominal GDP (bn US$) 19.5GDP per head (US$) 1,010

Population (m) 19Inflation (% change pa; av) 5.8

Total foreign debt (m US$) 11,028Human Development Index (rank of 177 countries) 96Poverty (% of pop) 25

Public health expenditure (% GDP) 1.8

IndiaNominal GDP (bn US$) 673.5GDP per head (US$) 623

Population (m) 1,080Inflation (% change pa; av) 4.4

Total foreign debt (m US$) 118,575Human Development Index (rank of 177 countries) 127Poverty (% of pop) 29

Public health expenditure (% GDP) 0.9

ThailandNominal GDP (bn US$) 158.9GDP per head (US$) 2,460

Population (m) 65Inflation (% change pa; av) 2.8

Total foreign debt (m US$) 49,499Human Development Index (rank of 177 countries) 76Poverty (% of pop) 13

Public health expenditure (% GDP) 2.1

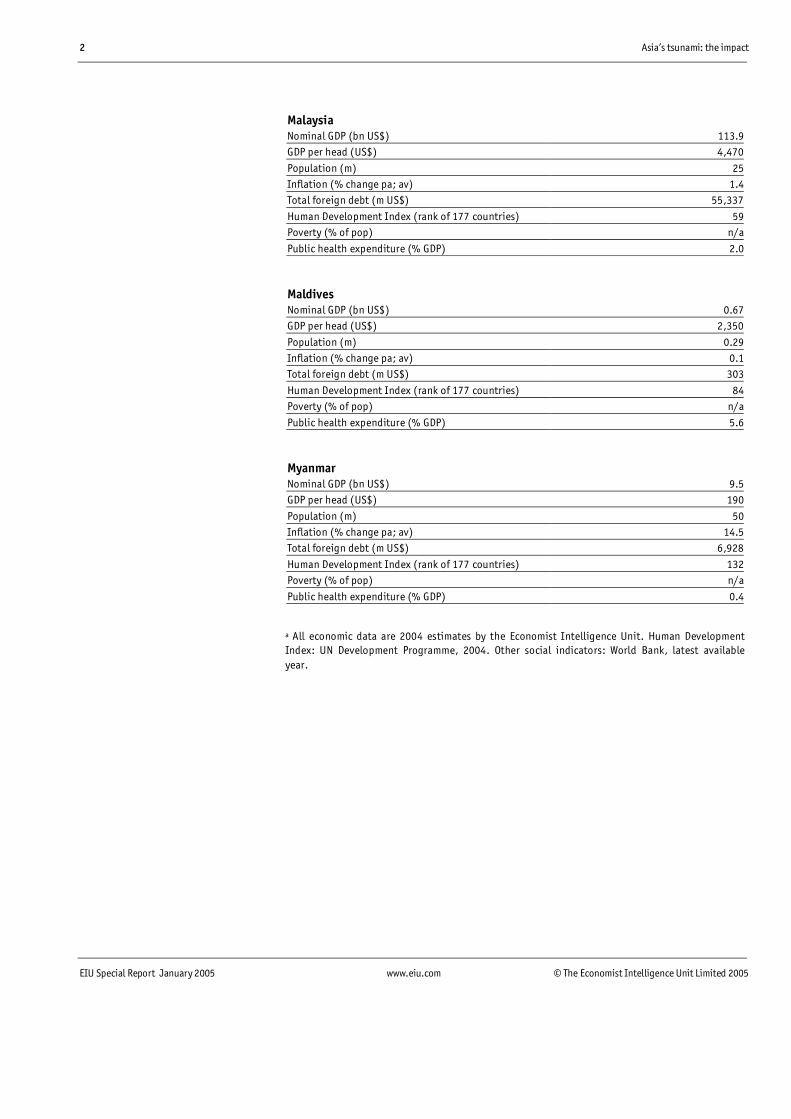

2 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

MalaysiaNominal GDP (bn US$) 113.9GDP per head (US$) 4,470

Population (m) 25Inflation (% change pa; av) 1.4Total foreign debt (m US$) 55,337

Human Development Index (rank of 177 countries) 59Poverty (% of pop) n/a

Public health expenditure (% GDP) 2.0

MaldivesNominal GDP (bn US$) 0.67GDP per head (US$) 2,350

Population (m) 0.29Inflation (% change pa; av) 0.1Total foreign debt (m US$) 303

Human Development Index (rank of 177 countries) 84Poverty (% of pop) n/a

Public health expenditure (% GDP) 5.6

MyanmarNominal GDP (bn US$) 9.5GDP per head (US$) 190

Population (m) 50Inflation (% change pa; av) 14.5Total foreign debt (m US$) 6,928

Human Development Index (rank of 177 countries) 132Poverty (% of pop) n/a

Public health expenditure (% GDP) 0.4

a All economic data are 2004 estimates by the Economist Intelligence Unit. Human DevelopmentIndex: UN Development Programme, 2004. Other social indicators: World Bank, latest availableyear.

Asia’s tsunami: the impact 3

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

4 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Overview: implications of the tsunamiOverview: implications of the tsunamiOverview: implications of the tsunamiOverview: implications of the tsunamiThe December 26th Indian Ocean tsunami is now thought to have killed morethan 160,000 people. But whilst rescuers and aid agencies struggle to bring aidto the survivors, the region’s financial markets are strangely serene. Stockmarkets have not plummeted; currencies have not collapsed. Instead, thefinancial markets appear to expect the current miseries to be easily overcome.

Is this simple callousness, or have the financial markets got it right? On anarrow analysis, investors and traders have made the right call. Despite themisery, the impact on regional GDP growth rates this year is likely to bemodest.

The situation in Indonesia illustrates this most clearly. Indonesia hasexperienced by far the highest number of deaths (over 113,000), but most ofthose killed were on the margins of the formal economy. Taken as a whole, theprovince of Aceh (where the brunt of the disaster has been felt) accounts foronly around 4% of Indonesian GDP, and much of this contribution comes froman LNG plant on the north coast that has survived unscathed. Indonesia isalready benefiting from the direct provision of aid. It is also likely to be a majorgainer from a proposal by creditor countries to suspend external debtrepayments, if agreed to. The Economist Intelligence Unit’s downward revisionto the overall Indonesia GDP growth forecast is therefore just 0.3 percentagepoints. GDP growth in Indonesia this year is still likely to be around 5.4%.

Asian tsunami casualty toll aDeaths Missing

Indonesia 113,306 10,000+

Sri Lanka 30,718 5,000+India 10,022 5,617Thailand 5,305 3,498

Somalia 114 n/aMaldives 82 26

Malaysia 68 6Myanmar 59 n/a

Tanzania 10 n/aBangladesh 2 n/aKenya 1 n/a

Seychelles Unconfirmed reports of deaths n/aTotal 159,687 n/a

a As of January 9th. All figures are expected to rise.

Sources: World Health organisation; UN; Reuters; CNN

The impact on Thailand’s growth will be larger, even though the country hassuffered fewer casualties. Thailand is much wealthier in per capita terms thanIndonesia, and foreign donors are therefore likely to be less generous. Thetourist industry accounts for a greater share of GDP in Thailand (at least 6-7%)than in other countries in the region, and many of its major resorts have beenaffected by the tsunami, unlike in Indonesia. The latest disaster comes after anumber of other shocks, especially the 2003 outbreak of Severe AcuteRespiratory Syndrome (SARS) and repeated incidents last year of Avian ‘flu’.

Have the markets got it right?

Asia’s tsunami: the impact 5

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

We therefore have reduced our 2005 Thai GDP forecast by more than onepercentage point, to around 4.3%.

A somewhat larger reduction is likely for the Sri Lankan GDP growth forecast,taking it down to around 4.2% for 2005 from 5.6% previously. Whilst the easternprovince of Sri Lanka is of less overall economic importance than the westernprovince (where most industry is based), it still accounts for a substantialvolume of tourist revenues. There is also direct political risk here: if the TamilTigers believe the central government is not dealing with the situation fairly,they could hinder reconstruction efforts.

We are not reducing our growth forecast for India at all. The othermacroeconomic indicators are also likely to remain broadly unchanged. At thestate level, the fiscal position of Andhra Pradesh and Tamil Nadu maydeteriorate slightly (India historically has been reluctant to accept foreign aid)but any such fiscal problems should be more than manageable. Elsewhere inthe region, Myanmar probably was more badly affected by the tsunami than itsgovernment initially admitted, but this is unlikely to be reflected in thepublished economic data. The economic impact on Malaysia will be minimal,with official financial institutions maintaining a slightly eerie calm.

Although the impact on the region’s GDP data will be modest, it is worthhighlighting a number of potential economic problems ahead.

First, domestic consumption will be dented in sectors. The effects of this maybe most evident in Thailand where (due to the country’s relative wealth) morespending is discretionary. Thai vehicle assemblers have already warned of afall-off in motor sales.

Second, although experience suggests that spending soon bounces back, aprolonged slump in consumer spending might uncover other weaknesses inregional economies. This may pose a much greater threat to domestic financialsystems than the direct effects of the disaster. (Local insurance firms, forexample, seem to have had only a minimal exposure.)

Third, tourism remains vulnerable. The scientific consensus is that the tsunamiwas a one-off event, and that a repeat is extremely unlikely. But some touristsmay not trust such an analysis, and prefer to stay away. (Also, quiteunderstandably, they may not want to holiday in places where many haverecently perished.) So, even if facilities can be quickly rebuilt, the tourismindustry in some countries may lose its lustre.

Fourth, the onset of disease could cause significant economic disruption.Outbreaks of typhoid or cholera would both scare off tourists and delayreconstruction. They would also tarnish the region’s reputation for effectivepublic health management.

Longer-term economic effects may hinge around political developments. ForIndonesia’s new president, Susilo Bambang Yudhoyono, the situation providesboth opportunities and threats. It provides the opportunity to prove his owncompetence, to increase the public standing of the army (if it can help provideaid effectively), and to deepen relations with the US and Australia.

Risks are looming

6 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

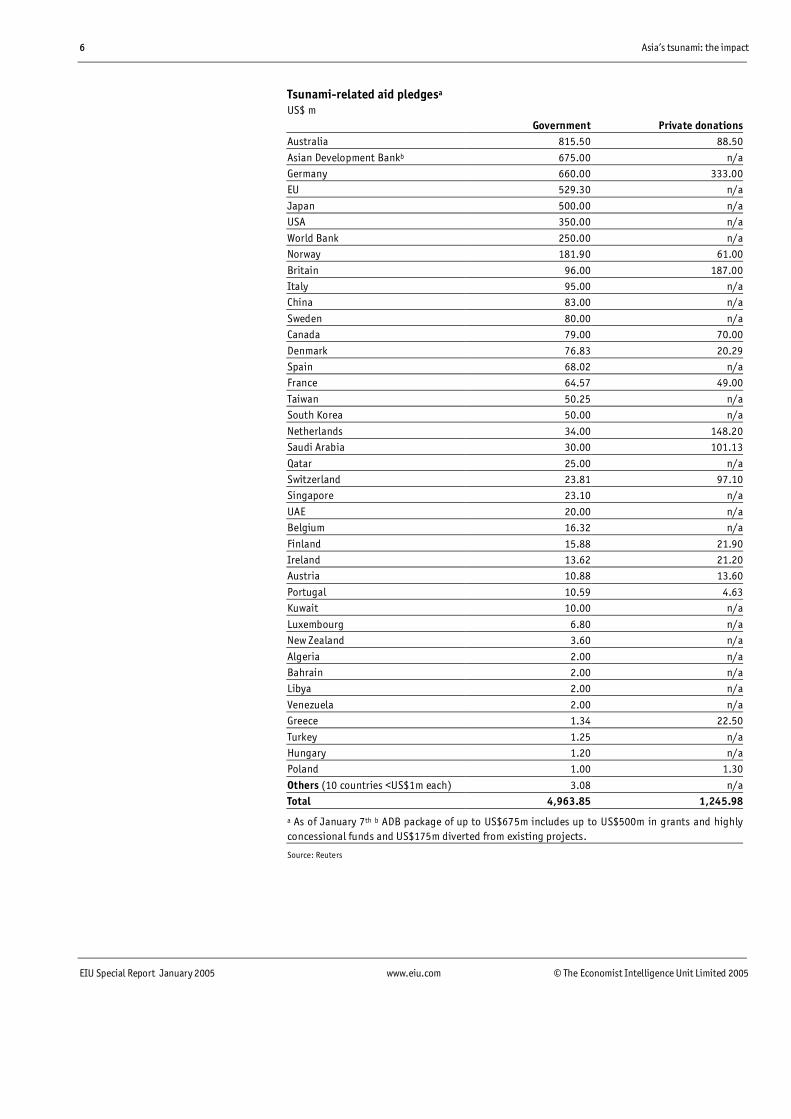

Tsunami-related aid pledgesa

US$ mGovernment Private donations

Australia 815.50 88.50

Asian Development Bankb 675.00 n/aGermany 660.00 333.00EU 529.30 n/a

Japan 500.00 n/aUSA 350.00 n/a

World Bank 250.00 n/aNorway 181.90 61.00

Britain 96.00 187.00Italy 95.00 n/aChina 83.00 n/a

Sweden 80.00 n/aCanada 79.00 70.00

Denmark 76.83 20.29Spain 68.02 n/aFrance 64.57 49.00

Taiwan 50.25 n/aSouth Korea 50.00 n/a

Netherlands 34.00 148.20Saudi Arabia 30.00 101.13

Qatar 25.00 n/aSwitzerland 23.81 97.10Singapore 23.10 n/a

UAE 20.00 n/aBelgium 16.32 n/a

Finland 15.88 21.90Ireland 13.62 21.20Austria 10.88 13.60

Portugal 10.59 4.63Kuwait 10.00 n/a

Luxembourg 6.80 n/aNew Zealand 3.60 n/a

Algeria 2.00 n/aBahrain 2.00 n/aLibya 2.00 n/a

Venezuela 2.00 n/aGreece 1.34 22.50

Turkey 1.25 n/aHungary 1.20 n/aPoland 1.00 1.30

Others (10 countries <US$1m each) 3.08 n/aTotal 4,963.85 1,245.98

a As of January 7th b ADB package of up to US$675m includes up to US$500m in grants and highlyconcessional funds and US$175m diverted from existing projects.

Source: Reuters

Asia’s tsunami: the impact 7

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

But each of these opportunities could, if mishandled, turn into a threat. Somebold decisions, and a certain generosity of spirit, may also be needed. Forexample, the civil infrastructure of Aceh must now be rebuilt—with luck, MrYudhoyono will do this by cooperating closely with local officials rather thanby shipping in dubious figures from Jakarta. The continued presence of foreignaid agencies may help ensure a more determined approach to the Acehinsurgency.

In Thailand, the prime minister, Thaksin Shinawatra, may see the disaster asmore of a threat than an opportunity: normally ebullient, he has beenremarkably quiet in recent days. He must face an election soon but (barringsome bizarre error of judgement) seems certain to win it. Both these leaders,and their peers, must also eventually face up to the very evident failure of theAssociation of South-east Asian Nations (ASEAN) to deal with the disastereffectively.

All of these calculations mean little, of course, to the millions now directlyaffected by the disaster. For them, the provision of direct aid will remaincritical. The crisis illustrates how far aggregate economic data can fail to reflectmajor human problems.

Indonesia: crisis-management test for YudhoyonoIndonesia: crisis-management test for YudhoyonoIndonesia: crisis-management test for YudhoyonoIndonesia: crisis-management test for YudhoyonoIndonesia was closest to the epicentre of the earthquake, and has thereforesuffered the most physical damage and heaviest human casualties. Dealingswiftly and efficiently with the disaster will be an important test for Indonesia'snew president, Susilo Bambang Yudhoyono. Disaster relief also adds a newdimension to the central government's campaign against separatist rebels in thenorthern Sumatran province of Aceh, one of the areas hardest hit by the tidalwaves. However, it is far from certain that the Indonesian authorities will beable to grasp the opportunity for political reconciliation that disaster reliefcould offer.

Effective co-ordination of relief is especially important in Indonesia's case--perhaps more so than in some of the other countries affected by the tsunami--because the damage is so much greater, in absolute terms, than anywhere else.As of January 10th the official death toll stood at over 113,000 and largestretches of the west coast of Sumatra are devastated. The difficulty of access tothe hardest-hit areas is hampering the provision of emergency supplies. This islikely to result in substantial further increases in the number of casualties asvictims succumb to injuries sustained during the tsunami or as disease breaksout among the survivors.

The macroeconomic impact on Indonesia is unlikely to be severe incomparison with the shocking human toll, even though much of northernSumatra's economy and infrastructure will have to be rebuilt from scratch. Theprovince of Aceh accounts for barely 4% of GDP and the bulk of this isaccounted for by output from a liquefied natural gas (LNG) plant that has notbeen affected by the tsunami. The majority of the affected population weresubsistence farmers or fisherman. Furthermore, the impact on tourism--in anycase a less important sector of the economy compared with Thailand--will not

Relief must be well-coordinated

8 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

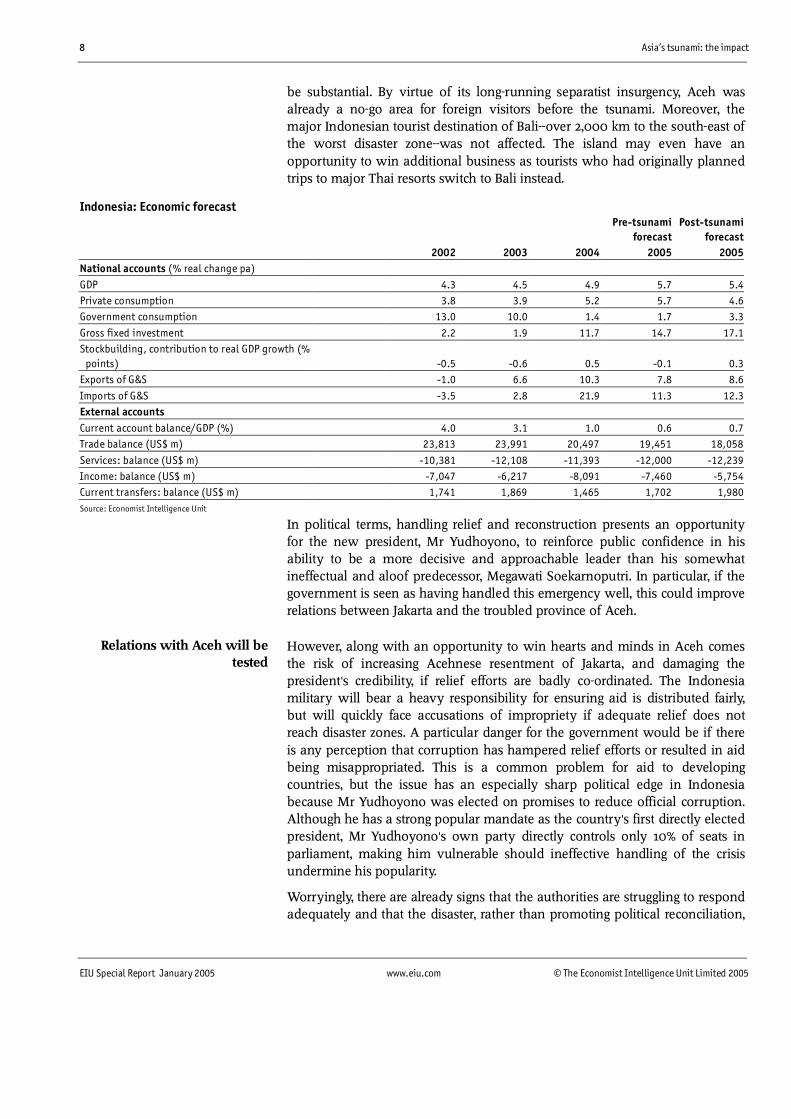

be substantial. By virtue of its long-running separatist insurgency, Aceh wasalready a no-go area for foreign visitors before the tsunami. Moreover, themajor Indonesian tourist destination of Bali--over 2,000 km to the south-east ofthe worst disaster zone--was not affected. The island may even have anopportunity to win additional business as tourists who had originally plannedtrips to major Thai resorts switch to Bali instead.

Indonesia: Economic forecastPre-tsunami

forecastPost-tsunami

forecast2002 2003 2004 2005 2005

National accounts (% real change pa)

GDP 4.3 4.5 4.9 5.7 5.4Private consumption 3.8 3.9 5.2 5.7 4.6Government consumption 13.0 10.0 1.4 1.7 3.3

Gross fixed investment 2.2 1.9 11.7 14.7 17.1Stockbuilding, contribution to real GDP growth (%

points) -0.5 -0.6 0.5 -0.1 0.3Exports of G&S -1.0 6.6 10.3 7.8 8.6

Imports of G&S -3.5 2.8 21.9 11.3 12.3External accountsCurrent account balance/GDP (%) 4.0 3.1 1.0 0.6 0.7Trade balance (US$ m) 23,813 23,991 20,497 19,451 18,058

Services: balance (US$ m) -10,381 -12,108 -11,393 -12,000 -12,239Income: balance (US$ m) -7,047 -6,217 -8,091 -7,460 -5,754Current transfers: balance (US$ m) 1,741 1,869 1,465 1,702 1,980Source: Economist Intelligence Unit

In political terms, handling relief and reconstruction presents an opportunityfor the new president, Mr Yudhoyono, to reinforce public confidence in hisability to be a more decisive and approachable leader than his somewhatineffectual and aloof predecessor, Megawati Soekarnoputri. In particular, if thegovernment is seen as having handled this emergency well, this could improverelations between Jakarta and the troubled province of Aceh.

However, along with an opportunity to win hearts and minds in Aceh comesthe risk of increasing Acehnese resentment of Jakarta, and damaging thepresident's credibility, if relief efforts are badly co-ordinated. The Indonesiamilitary will bear a heavy responsibility for ensuring aid is distributed fairly,but will quickly face accusations of impropriety if adequate relief does notreach disaster zones. A particular danger for the government would be if thereis any perception that corruption has hampered relief efforts or resulted in aidbeing misappropriated. This is a common problem for aid to developingcountries, but the issue has an especially sharp political edge in Indonesiabecause Mr Yudhoyono was elected on promises to reduce official corruption.Although he has a strong popular mandate as the country's first directly electedpresident, Mr Yudhoyono's own party directly controls only 10% of seats inparliament, making him vulnerable should ineffective handling of the crisisundermine his popularity.

Worryingly, there are already signs that the authorities are struggling to respondadequately and that the disaster, rather than promoting political reconciliation,

Relations with Aceh will betested

Asia’s tsunami: the impact 9

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

is adding to tensions between the rebel Free Aceh Movement (GAM) and thecentral government. This, in turn, is further complicating relief efforts. (Infairness, the extreme devastation and remoteness of the areas affected havealso contributed to the chaos. For example, most emergency supplies have hadto be flown in through Banda Aceh, the provincial capital, via a single airstrip.)Balancing the conflicting agendas of the local population, Indonesian securityforces, central government, and foreign aid workers and troops is a particulardifficulty.

Although GAM declared a truce immediately after the tsunami, there remainconcerns that either it or the Indonesian security forces (or both) may attemptto use the post-tsunami chaos as cover for military activity. On January 9ththere were reports of gunfire near the UN relief headquarters in Banda Aceh,and there have also been reports of clashes elsewhere in the disaster zone. Therole and actions of the Indonesian armed forces have been a constant source ofcontention. The military has been accused in some quarters of denying ordelaying relief to rebel areas, and of focusing on maintaining security at theexpense of helping with the clean-up or with burying the dead. If theseallegations are true, it will increase further the local resentment of the military.Hard-line generals in Jakarta may see the tsunami-related disruption as anopportunity to strike at rebel forces weakened by the disaster. The US hasagreed to provide spare parts for Indonesian military transport planes, partiallylifting an embargo on arms sales originally imposed in response to Indonesianatrocities in East Timor. Naturally, this has raised concerns that the planes maylater be used in operations against GAM, rather than in relief efforts asintended.

Foreign relief efforts raise just as many issues as the domestic response. First,the Indonesian military will remain reluctant to grant foreign aid workers andtroops access to the disaster areas, ostensibly owing to concerns about theirsecurity but probably also, in reality, to avoid scrutiny of its anti-insurgencycampaign. There have been conflicting reports as to how much accessforeigners currently have, although at least one account has their movementsrestricted to Banda Aceh and the north-west Sumatran town of Meulaboh(now, sadly, famous for having been flattened by the tsunami). Clearly, thegreater the restrictions imposed on the movements of those bringing food andmedical supplies, the slower relief efforts will progress and the greater thelikelihood that local residents will be dissatisfied with the government's reliefprogramme.

There have also been reports that Java-based Islamic militants unconnectedwith GAM have infiltrated the disaster zone and may attack Western aidworkers or troops. US and Australian forces are participating in relief effortsand would make obvious targets. Even if this does not occur, the presence ofUS and Australian forces will have to be handled delicately as the populationof Aceh is one of Indonesia's most conservatively Islamic. The UN has said itdoes not expect aid workers to be attacked, but even assuming this claim iscorrect, there remains a possibility that such workers will be caught in crossfireif fighting erupts between GAM and the Indonesian military.

10 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

The Economist Intelligence Unit is now forecasting GDP growth in Indonesia of5.4%, down from 5.7% previously. We had been expecting strong growth thisyear owing to a more stable political environment and the revival of foreignand domestic investment. Following the tsunami, we now expect growth inprivate consumption to be lower (4.6% compared with 5.7% previously) becauseof weaker consumer sentiment. This will be offset to some extent by strongerinvestment growth, particularly stockbuilding, as reconstruction efforts progress.Our forecast for import demand in 2005 has been raised because of theincrease in investment, but imports will come from a low base. Our forecast forthe current-account surplus has been raised slightly owing to higher transfercredits in the form of official grants and private sector financial assistance.Unlike in Thailand and Sri Lanka, Indonesia’s tourism industry—concentratedfar to the east in Bali—will be unaffected by the tsunami. We therefore expectno significant effect on Indonesia’s services exports.

Sri Lanka: the biggest ecSri Lanka: the biggest ecSri Lanka: the biggest ecSri Lanka: the biggest ecoooonomic impactnomic impactnomic impactnomic impactSri Lanka faces significant economic and political challenges in the wake of theIndian Ocean tsunami disaster. The country so far is reported to have thesecond-highest death toll after Indonesia, numbering more than 30,000 andexpected to rise further. By virtue of its small size, the Sri Lankan economy isless well equipped to absorb the disaster, while political problems may limitthe extent to which the government will be able to implement rehabilitationprogrammes. The gravity of Sri Lanka's plight will ensure, however, that itreceives generous foreign assistance; private transfers from Sri Lankans overseaswill also prove important.

Sri Lanka has a population of just 19m and an estimated GDP in 2004 of justUS$19.5bn, so the estimated scale of devastation is proportionately muchgreater there than in India or possibly even Indonesia. But, as with othercountries, the disaster has largely missed major urban areas and importantindustrial assets. This will lessen the longer-term economic impact.

It is difficult at this stage to estimate the cost of reconstruction, although it isclear that most of it will have to be met from external aid and transfers, invarious forms. The government certainly is not in a strong position to pay forrepairs or to provide fiscal stimulus to areas ravaged by the tsunami. It wasalready running a budget deficit of over 8% of GDP before the disaster.Government debt is equivalent to just over 100% of GDP, compared with 58%for Indonesia and 60% even for perennially cash-strapped India.

Tourism and fishing will be the industries hardest hit. Fishing accounts forbarely 3% of GDP (at 1996 constant factor-cost prices), according to central bankdata, so lost output from this sector will not have a major direct impact on themacroeconomy--the social and indirect economic costs are likely to be higher,however, given the heavy death toll in fishing communities. Although fishingboats may be relatively easy to replace, their crews may not be.

Tourism will take time to recover. Beach resorts on the south coast have beenbadly affected. First indications are that tourist bookings have droppeddramatically, but that the effects of this have been partially offset by the short-

Overall impact onthe economy

Asia’s tsunami: the impact 11

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

term influx of foreign relief workers needing accommodation. The underlyingquestion is how quickly foreign tourists can overcome their understandablereluctance to return to the scene of tragedy. This is likely to play a bigger role indetermining the speed of the recovery than the speed of reconstruction. Luckily,many of the larger hotels suffered relatively little damage, with estimatessuggesting many of these could be back in operation within a few weeks. Inthis sense, the tsunami is unlikely to have a sustained dampening effect ontourism in the same way that a resumption of the island's civil war could beexpected to have. Indeed, the ceasefire between the government and theLiberation Tigers of Tamil Eelam (LTTE, or Tamil Tigers) has keen the key factorin the revival of the island's tourist industry over the past two years. The sectordirectly accounts for 4.6% of GDP, according to the World Travel & TourismCouncil, employed around 300,000 people in 2004 and is a major foreign-exchange earner.

Sri Lanka: Economic forecastPre-tsunami

forecastPost-tsunami

forecast2002 2003 2004 2005 2005

National accounts (% real change pa)

GDP 4.0 5.9 5.2 5.6 4.2Private consumption 6.8 6.5 6.0 5.9 3.5

Government consumption 4.3 3.8 5.6 5.0 8.0Gross fixed investment 5.3 17.9 8.0 8.5 18.0Stockbuilding, contribution to real GDP growth (%

points) 0.3 -0.2 -0.1 0.0 0.1Exports of G&S 6.3 4.8 11.3 9.6 8.0Imports of G&S 11.6 10.4 11.9 9.8 13.0

External accountsCurrent account balance/GDP (%) -1.6 -0.9 -5.1 -5.2 -3.9Trade balance (US$ m) -795.8 -871.6 -1,778 -1,916 -2,230

Services: balance (US$ m) -316 -301.2 -196 -121 -521Income: balance (US$ m) -252.5 -192.3 -205 -213 -213

Current transfers: balance (US$ m) 1,097 1,205 1,177 1,164 2,164

Source: Economist Intelligence Unit

Managing the disaster could have interesting and possibly unsettling politicaldimensions. Initial hopes were that it would present an opportunity for co-operation between the government and the LTTE, if a geographical balancingact could be maintained. . As much of the devastation took place in the east,which is dominated by Tamil and Muslim communities, the government willhave to remain wary of being accused of overly focusing its relief efforts in thesouth of the country (where local residents are largely from the majoritySinhalese population). There is also the potential for the involved groups to usethis as an effort to consolidate their political support; it is possible, for example,that the LTTE will stifle government efforts to provide aid in the east of thecountry. The LTTE sees the east as territory under its control, and the group willnot wish to see the government improving its popularity among the localpopulation—the questions who will control foreign aid related to the peace

12 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

process, for example, has been a major sticking point between the two sidessince negotiations first started.

Stresses may now be coming to a head. On January 7th, the Tamil Tigers weredemanding the removal of government troops from welfare camps. This is apity, as reconstruction efforts will require the use of military resources by boththe government and the Tamil Tigers. If there is a breakdown of relations, thereis a risk that the LTTE could attempt to exploit the situation to manoeuvre itsforces for tactical advantage while government troops are occupied with thepost-tsunami clean-up. (Previously the Sri Lankan army has accused the LTTEof using the lull in hostilities covertly to build up military installations, inviolation of the ceasefire.) However, this risk is balanced by the fact that LTTE-held areas in the east have also been badly affected, so the Tamil rebels' owntroops will be busy with relief efforts as well.

Hopes that the urgency of the situation could also, at least temporarily, lessenthe acrimony between the government and opposition should also not beoverplayed. Relations between the administration of Chandrika Kumaratunga,the president and leader of the People's Alliance (PA)-led government, and theopposition United National Party (UNP) have been very poor in recent months,a situation not conducive to effective government or to progress towards alasting political solution with the LTTE. The underlying sources of frictionbetween the government and the UNP will not disappear during thereconstruction process, however, so it cannot be assumed that any détente willbe permanent. Unseemly haggling over the distribution of aid also looks likely.For example, an ally of the PA, the Marxist Janatha Vimukthi Peramuna (JVP),has set up its own relief fund. Although this clearly has humanitarian motives,a political element cannot be ruled out (the JVP has traditionally had strongsupport in the south of the country, and makes much of its focus on the poor).

Our forecast is based on the assumption that differences between thegovernment and the LTTE do not erupt into renewed conflict, stopping thereconstruction process. On this assumption, we forecast a sharp pick-up infixed investment growth this year to 18% (previous forecast 8.5%), and a moremodest increase in government consumption. However the effects of this onoverall growth will be more than offset by slower services exports growth,dragging GDP growth down to around 4.2% this year (previous forecast 5.6%).The country’s current-account position will be bolstered by inward transfers,which will more than outweigh the fall in revenue from tourism exports. Afreeze on interest payments on much official debt, if it happens, will also help.We are now forecasting a current-account deficit of US$800m in 2005 (previousforecast US$1,080m).

Thailand: a shock to the tourism industryThailand: a shock to the tourism industryThailand: a shock to the tourism industryThailand: a shock to the tourism industryThe tsunami that hit Thailand on December 26th was first and foremost ahuman tragedy, with more than 5,000 people killed, around half of whomwere foreign tourists. On January 9th more than 3,000 people were stillreported missing.

Asia’s tsunami: the impact 13

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

There have been no definitive estimates of the cost of damage to buildings andinfrastructure in the six provinces affected by the tsunami—Phuket, Krabi,Ranong, Phang Nga, Satun and Trang. However, the Tourism Authority ofThailand (TAT) has produced some estimates. According to the TAT, the cost ofdamage to the two most seriously affected areas, Khao Lak (in Phang Nga) andPhi Phi island (in Krabi), totals Bt12bn (US$300m) and Bt2.8bn respectively.Khao Lak (which has developed rapidly over the past few years, with majorinternational hotel chains, such as Sofitel and Le Meriden, recently openinglarge-scale luxury hotels) suffered the most serious devastation in terms ofpeople killed and damage to hotels--few of the hotels in Khao Lak, which had atotal of around 6,000 rooms, were left standing. Similarly, on the island of PhiPhi, which had around 4,000 hotel rooms, few hotels remained.

In Phuket, which has around 32,000 hotel rooms, the damage was less severe.Indeed, a number of popular bays around the island were seriously affected bythe waves. Initial surveys of hotels around the island indicated that less than20% had suffered serious damage, and one week following the tsunami around15% of hotels reportedly remained closed. According to the TAT, total damagecosts on Phuket are estimated at Bt16bn, excluding damage to public utilitiesand roads and the power grid.

The insurance industry has been slow to react to the event. However, the finalamount of insurance paid out to those affected by the disaster will not reflectthe full extent of the damage. Many small business affected by the tsunamiwere not insured, and those that were may not have adequate coverage.

Although the tsunami hit during the peak holiday season in Thailand andaffected some of the most popular tourist resorts, initial concerns over the long-term impact on the tourism industry may be overblown.

There is no doubt that the region is important for the tourism industry.According to the TAT in 2003 the six affected provinces recorded tourismrevenue of Bt76bn from foreign visitors (around 25% of the total tourismrevenue generated by foreign tourists of Bt310bn), nearly Bt60bn of which wasearned in Phuket. Other sources have estimated that the region accounts foraround 30% of tourism revenue. According to the TAT loss of revenue potentialfollowing the disaster is estimated at Bt39.5bn, most of which (Bt20.8bn) isaccounted for by loss of revenue in Phuket. The Association of Thai TravelAgents (ATTA) estimates lost revenue at around Bt30bn. Prior to the disaster,TAT had forecast that revenue from foreign tourists would rise from Bt310bn in2003 to Bt384bn in 2004 and Bt450bn in 2005, with foreign tourist arrivalsjumping from 10m in 2003 to 12m in 2004 and 13.4m in 2005.

The timeframe for recovery from the devastation depends on the area inquestion. The ATTA secretary-general, Chidchai Sakornbadee, reportedly saidthat it should not take more than a month to "recover from this disaster".However, this is only likely to be the case for Phuket. The rebuilding effort inthe resorts of Khao Lak and Phi Phi will take at least a year, possibly two, andtourists are not expected to return to the area for some time. However, manyresort areas in Phuket were unaffected, and those that were affected are in theprocess of returning to normal. Local businesses have complained that

Cost of the damage

Impact on tourism

14 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

international media coverage has focused solely on the devastation and has notreported on the fact that many areas are operating as normal. The future impacton the tourism industry largely depends on the perceived extent of damage tothe region. The TAT is expected to implement promotional campaigns in aneffort to restore the confidence of tourists planning to visit the region.

Despite reported cancellations, foreign tourists continue to arrive and the long-term impact on the region is not expected to be severe. This is primarilybecause the tsunami may be viewed as a one-off occurrence that is unlikely tobe repeated in the near future, unlike the outbreak of Severe Acute RespiratorySyndrome (SARS) in early to mid-2003, which disrupted travel and economicactivity throughout Asia because of fears of the rapid spread of the respiratorydisease.

Also, other major tourist destinations, including beach resorts (such as KohSamui and Pattaya) around the Gulf of Thailand, which was not affected by thetsunamis, are operating normally and will be in a position to cater to touristsswitching destinations from resorts along the coast of the Andaman Sea. Also,destinations and attractions in Bangkok and the north and northeast willcontinue to receive foreign and local tourists.

The economic impact on Thailand will show up mainly through damage to thetourism industry, which accounts for around 6% of GDP. The government’sinitial estimate is that the tsunami and its aftermath will result in GDP growthfalling by 0.3 percentage points. The Economist Intelligence Unit, based on apreliminary economic reforecast for 2005, believes the impact on GDP will begreater: we are lowering our forecast for real GDP this year from 5.5% to 4.3%.We are expecting a substantial decline in private consumption in the firstquarter of the year; tourism accounts for at least 10% of employment inThailand, and the disruption is likely to reduce personal income and henceconsumer spending. Already, some Thai industries, including car manufacturers,are predicting a substantial slump in sales in the coming weeks. We wouldexpect private consumption to rebound in the second quarter, but this will notfully compensate for the initial downturn; a weak first quarter, in GDP terms,lowers the base of activity for the rest of the year, resulting in much lowergrowth. We are forecasting 2005 growth in private consumption of 3.9%, downfrom our previous forecast of 6%.

Exports will also be hurt by the effects of the tsunami on the tourism industry.(Tourism is recorded as a service export.) We are now forecasting a 9.7% declinein services exports in national accounts terms in 2005 and overall growth inexports of goods and services of 3.7%, down from our previous forecast of 5.7%.Although we believe the tourism industry in Thailand will recover over time,tourists may be reluctant to return to an area where so many people died, andwhere the risk of disease may persist for some time. We are basing ourassessment in part on the reaction to the outbreak of SARS in parts of east Asia,including, Thailand, in 2003. Tourism suffered heavily because of SARS.Imports will also rise to help with reconstruction, providing a further drag onGDP.

Overall impact on economy

Asia’s tsunami: the impact 15

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

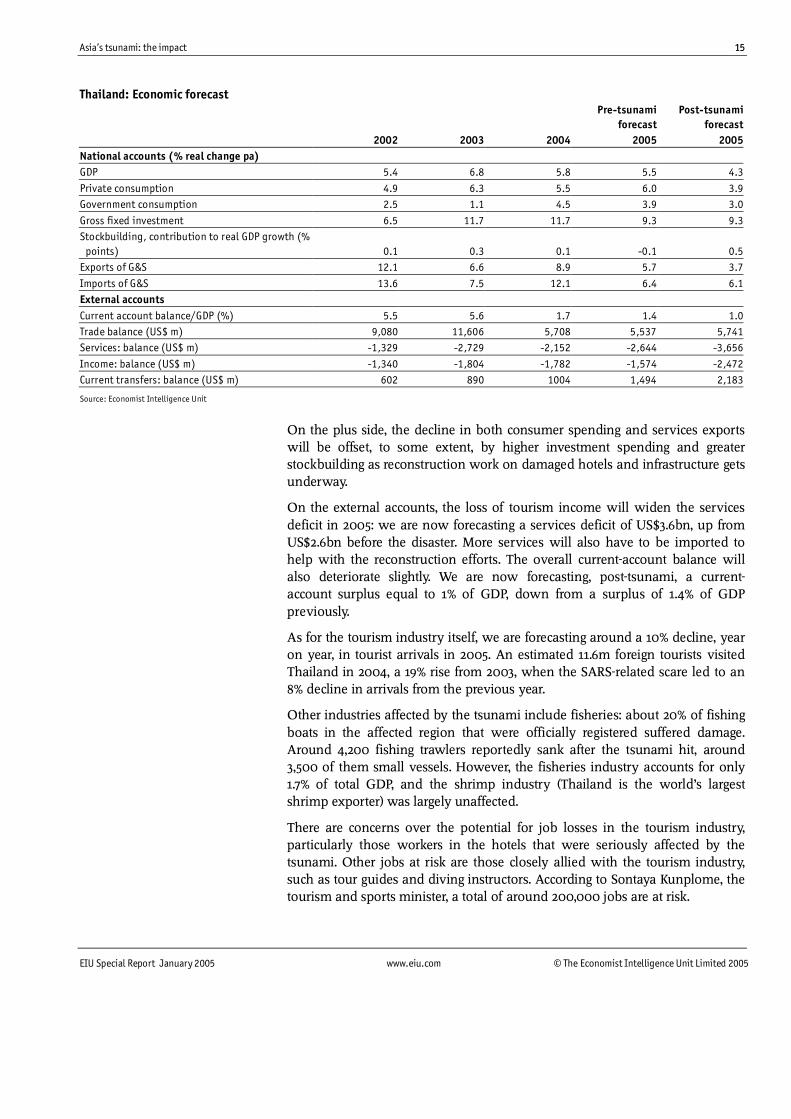

Thailand: Economic forecastPre-tsunami

forecastPost-tsunami

forecast2002 2003 2004 2005 2005

National accounts (% real change pa)GDP 5.4 6.8 5.8 5.5 4.3

Private consumption 4.9 6.3 5.5 6.0 3.9Government consumption 2.5 1.1 4.5 3.9 3.0

Gross fixed investment 6.5 11.7 11.7 9.3 9.3Stockbuilding, contribution to real GDP growth (%

points) 0.1 0.3 0.1 -0.1 0.5Exports of G&S 12.1 6.6 8.9 5.7 3.7

Imports of G&S 13.6 7.5 12.1 6.4 6.1External accountsCurrent account balance/GDP (%) 5.5 5.6 1.7 1.4 1.0Trade balance (US$ m) 9,080 11,606 5,708 5,537 5,741Services: balance (US$ m) -1,329 -2,729 -2,152 -2,644 -3,656

Income: balance (US$ m) -1,340 -1,804 -1,782 -1,574 -2,472Current transfers: balance (US$ m) 602 890 1004 1,494 2,183

Source: Economist Intelligence Unit

On the plus side, the decline in both consumer spending and services exportswill be offset, to some extent, by higher investment spending and greaterstockbuilding as reconstruction work on damaged hotels and infrastructure getsunderway.

On the external accounts, the loss of tourism income will widen the servicesdeficit in 2005: we are now forecasting a services deficit of US$3.6bn, up fromUS$2.6bn before the disaster. More services will also have to be imported tohelp with the reconstruction efforts. The overall current-account balance willalso deteriorate slightly. We are now forecasting, post-tsunami, a current-account surplus equal to 1% of GDP, down from a surplus of 1.4% of GDPpreviously.

As for the tourism industry itself, we are forecasting around a 10% decline, yearon year, in tourist arrivals in 2005. An estimated 11.6m foreign tourists visitedThailand in 2004, a 19% rise from 2003, when the SARS-related scare led to an8% decline in arrivals from the previous year.

Other industries affected by the tsunami include fisheries: about 20% of fishingboats in the affected region that were officially registered suffered damage.Around 4,200 fishing trawlers reportedly sank after the tsunami hit, around3,500 of them small vessels. However, the fisheries industry accounts for only1.7% of total GDP, and the shrimp industry (Thailand is the world’s largestshrimp exporter) was largely unaffected.

There are concerns over the potential for job losses in the tourism industry,particularly those workers in the hotels that were seriously affected by thetsunami. Other jobs at risk are those closely allied with the tourism industry,such as tour guides and diving instructors. According to Sontaya Kunplome, thetourism and sports minister, a total of around 200,000 jobs are at risk.

16 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

The prime minister, Thaksin Shinawatra, has reiterated that the country is notin need of international financial aid, but has called for technical assistance. OnDecember 28th the government announced that it had set aside Bt23bn to helpfinance the relief and rebuilding efforts in the affected areas. In addition tooffering income tax exemptions for those affected by the devastation andreductions in land and local administration taxes, the government will providefunds for assistance and compensation of those affected, occupationalrehabilitation and medium and long term loans for reviving business in theregion.

The Bank of Thailand and Ministry of Finance have also agreed to disburse upto Bt30bn in soft loans over a one-year period with interest rates of less than2%. The loans will be offered through local financial institutions. It is likely thatthe government will initiate additional support programmes for those harmedby the disaster.

Thaksin visited the affected region on the day the waves hit. He has sincevisited the region on a regular basis and has been widely praised for his efforts.According to a local survey, more than 54% of respondents said theirsatisfaction with Thaksin had risen following the tsunami. There has beenstrong criticism of the government from locals in fishing villages that wereseverely damaged by the tsunami, claiming that foreign tourists receivedpreferential treatment with financial and non-financial assistance.

There has also been some criticism of the government’s failure to provide awarning of the impending tsunami even though it was reportedly in a positionto do so. Thaksin has since called for an investigation and has appointed SmithThamsarote, a former head of the Meteorological Department, to head a panelto establish an advanced warning system. Thaksin is keen to put such a systemin place with or without international support.

Although there have been calls from some quarters for the forthcomingelection to be delayed, the Election Commission has stated that the electionwill go ahead as planned on February 6th. Recent events are unlikely to haveaffected Thaksin’s chances of being re-elected by a strong majority.

India: limited economic tollIndia: limited economic tollIndia: limited economic tollIndia: limited economic tollAccording to figures released by the Indian government, more than 15,000people were killed or are feared dead on the Indian mainland and on theAndaman and Nicobar islands. The number of people affected is far greater.About 80,000 are sheltered in camps in the state of Tamil Nadu, 30,000 inAndhra Pradesh and over 20,000 in Pondicherry. The Indian government hasdeclared that the search and rescue phase of its relief operation is over and thatthe focus is now on restoring normal life.

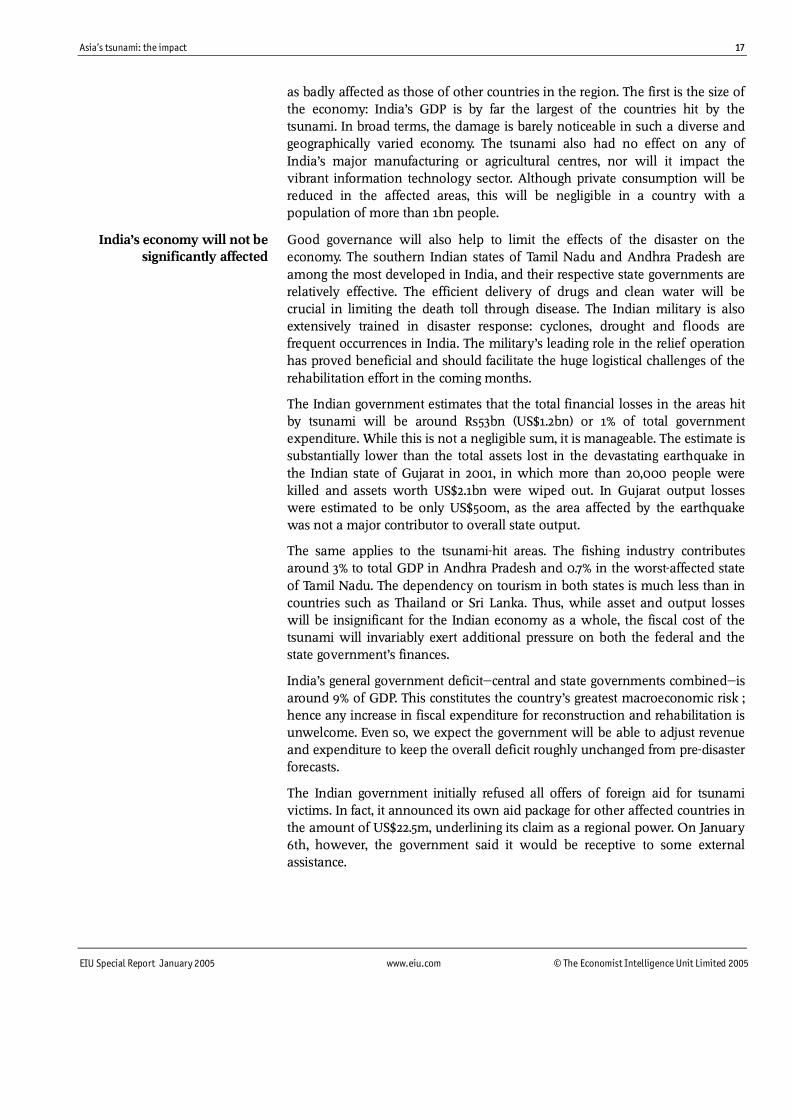

Although the impact of the tsunami on India’s gross domestic product will beinsignificant—we are making no changes to our GDP forecast for 2005—thedisaster has devastated lives, social infrastructure and economic foundations inthe affected areas. There are several reasons why India’s economy will not be

Government policy response

Political implications

Asia’s tsunami: the impact 17

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

as badly affected as those of other countries in the region. The first is the size ofthe economy: India’s GDP is by far the largest of the countries hit by thetsunami. In broad terms, the damage is barely noticeable in such a diverse andgeographically varied economy. The tsunami also had no effect on any ofIndia’s major manufacturing or agricultural centres, nor will it impact thevibrant information technology sector. Although private consumption will bereduced in the affected areas, this will be negligible in a country with apopulation of more than 1bn people.

Good governance will also help to limit the effects of the disaster on theeconomy. The southern Indian states of Tamil Nadu and Andhra Pradesh areamong the most developed in India, and their respective state governments arerelatively effective. The efficient delivery of drugs and clean water will becrucial in limiting the death toll through disease. The Indian military is alsoextensively trained in disaster response: cyclones, drought and floods arefrequent occurrences in India. The military’s leading role in the relief operationhas proved beneficial and should facilitate the huge logistical challenges of therehabilitation effort in the coming months.

The Indian government estimates that the total financial losses in the areas hitby tsunami will be around Rs53bn (US$1.2bn) or 1% of total governmentexpenditure. While this is not a negligible sum, it is manageable. The estimate issubstantially lower than the total assets lost in the devastating earthquake inthe Indian state of Gujarat in 2001, in which more than 20,000 people werekilled and assets worth US$2.1bn were wiped out. In Gujarat output losseswere estimated to be only US$500m, as the area affected by the earthquakewas not a major contributor to overall state output.

The same applies to the tsunami-hit areas. The fishing industry contributesaround 3% to total GDP in Andhra Pradesh and 0.7% in the worst-affected stateof Tamil Nadu. The dependency on tourism in both states is much less than incountries such as Thailand or Sri Lanka. Thus, while asset and output losseswill be insignificant for the Indian economy as a whole, the fiscal cost of thetsunami will invariably exert additional pressure on both the federal and thestate government’s finances.

India’s general government deficit—central and state governments combined—isaround 9% of GDP. This constitutes the country’s greatest macroeconomic risk ;hence any increase in fiscal expenditure for reconstruction and rehabilitation isunwelcome. Even so, we expect the government will be able to adjust revenueand expenditure to keep the overall deficit roughly unchanged from pre-disasterforecasts.

The Indian government initially refused all offers of foreign aid for tsunamivictims. In fact, it announced its own aid package for other affected countries inthe amount of US$22.5m, underlining its claim as a regional power. On January6th, however, the government said it would be receptive to some externalassistance.

India’s economy will not besignificantly affected

18 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

In focus: debt deferral after the tsunamiIn focus: debt deferral after the tsunamiIn focus: debt deferral after the tsunamiIn focus: debt deferral after the tsunamiSome form of external debt relief is likely to be part of the internationalhumanitarian response to the Asian tsunami. Finance ministers from the Groupof Seven industrialised nations on January 7th said they were ready to agree ona suspension of debt payments for countries affected by the disaster and “stoodready to consider all appropriate measures for further assistance”. Japan, one ofthe world’s largest lenders to developing countries, had previously proposed aone-year moratorium on debt service by affected countries. The IMF and WorldBank also officially endorsed a debt moratorium by creditor countries. Talksfocused specifically on debt servicing were to be held on January 12th by theParis Club, a group of wealthy creditor governments.

A debt moratorium, if it is granted, would have a clear purpose: to free upfunds for reconstruction and humanitarian assistance that stricken countriesmight otherwise use for debt repayment. In that sense, a number of vulnerablecountries that were hurt by the tsunami might welcome the overture. Sri Lanka,for one, has said it would accept concessions on debt servicing; Indonesia isalso a likely candidate, although the government has had little to say so far. Butdebt relief is a complicated matter, and it is far from clear if affected countrieswould benefit in the long term.

Debt relief, in fact, does not accurately describe what is being proposed. Debtwould not be written-off, or cancelled; rather, countries would be allowed tosuspend payments—presumably of both principal and interest—for a certainperiod of time, probably one year. (Debt owed to multilateral institutions suchas the IMF and World Bank is not covered by Paris Club restructurings,although World Bank president James Wolfensohn has hinted that the bankmight consider debt relief in this instance.) Deferred payments would still beowed to creditors.

That presents the first problem with the plan: countries that choose to accept adebt moratorium would face larger repayments—a debt “hump”—in futureyears. A suspension of debt payments would carry other risks. Any suspensionof debt payments might cause lenders to question the creditworthiness ofborrowers, although Standard & Poors, a credit-rating agency, has said it wouldnot downgrade tsunami-affected countries that accepted debt deferral.Countries that accepted debt deferral might also raise concerns amonginvestors, who may worry if governments opt for a bail-out rather than face upto difficult economic decisions.

Paris Club creditors that grant a country restructuring or deferral of its officialdebt also typically insist that the country negotiate a similar arrangement withits private-sector creditors. Would the Paris Club insist on such a requirement inthese circumstances? Indonesia does not have large debt obligations to private-sector borrowers, but this could be still an issue for the government.

Paris Club creditors, when offering significant concessions on debt, alsotypically insist that a debtor country be party to an IMF economic programme.Indonesia ended its unpopular IMF programme in 2003 and is unlikely to enterinto a new one. The Paris Club, which is made up of governments, is ultimatelya political institution, and so can make whatever arrangements it chooses with

Debt will not be written-off

Asia’s tsunami: the impact 19

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

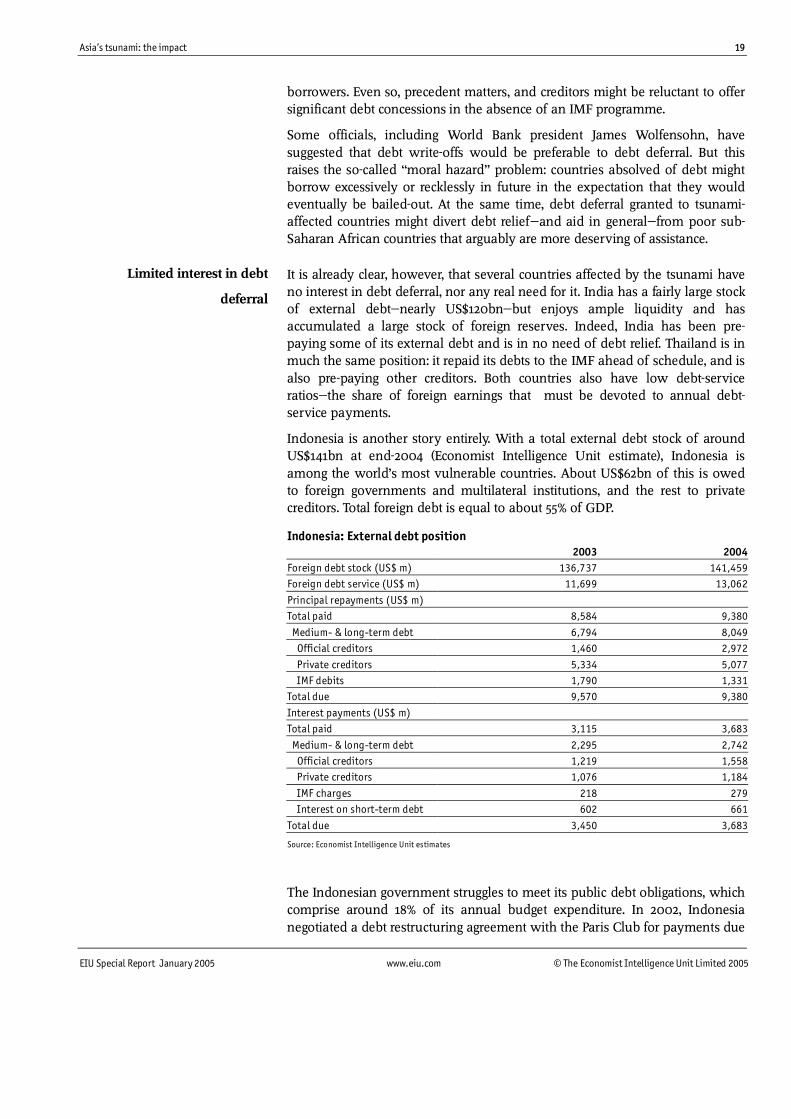

borrowers. Even so, precedent matters, and creditors might be reluctant to offersignificant debt concessions in the absence of an IMF programme.

Some officials, including World Bank president James Wolfensohn, havesuggested that debt write-offs would be preferable to debt deferral. But thisraises the so-called “moral hazard” problem: countries absolved of debt mightborrow excessively or recklessly in future in the expectation that they wouldeventually be bailed-out. At the same time, debt deferral granted to tsunami-affected countries might divert debt relief—and aid in general—from poor sub-Saharan African countries that arguably are more deserving of assistance.

It is already clear, however, that several countries affected by the tsunami haveno interest in debt deferral, nor any real need for it. India has a fairly large stockof external debt—nearly US$120bn—but enjoys ample liquidity and hasaccumulated a large stock of foreign reserves. Indeed, India has been pre-paying some of its external debt and is in no need of debt relief. Thailand is inmuch the same position: it repaid its debts to the IMF ahead of schedule, and isalso pre-paying other creditors. Both countries also have low debt-serviceratios—the share of foreign earnings that must be devoted to annual debt-service payments.

Indonesia is another story entirely. With a total external debt stock of aroundUS$141bn at end-2004 (Economist Intelligence Unit estimate), Indonesia isamong the world’s most vulnerable countries. About US$62bn of this is owedto foreign governments and multilateral institutions, and the rest to privatecreditors. Total foreign debt is equal to about 55% of GDP.

Indonesia: External debt position2003 2004

Foreign debt stock (US$ m) 136,737 141,459Foreign debt service (US$ m) 11,699 13,062

Principal repayments (US$ m)Total paid 8,584 9,380

Medium- & long-term debt 6,794 8,049 Official creditors 1,460 2,972

Private creditors 5,334 5,077 IMF debits 1,790 1,331Total due 9,570 9,380

Interest payments (US$ m)Total paid 3,115 3,683

Medium- & long-term debt 2,295 2,742 Official creditors 1,219 1,558 Private creditors 1,076 1,184

IMF charges 218 279 Interest on short-term debt 602 661

Total due 3,450 3,683

Source: Economist Intelligence Unit estimates

The Indonesian government struggles to meet its public debt obligations, whichcomprise around 18% of its annual budget expenditure. In 2002, Indonesianegotiated a debt restructuring agreement with the Paris Club for payments due

Limited interest in debt

deferral

20 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

between March 2002 and December 2003, resulting in a heavy repaymentschedule for 2005. Although foreign donors are contributing generously tocountries affected by the tsunami, the Indonesian government almost certainlywill incur some disaster-related costs this year. There is, however, little leewayin its 2005 budget for this additional expenditure. It is possible, therefore, thatthe government might welcome the “breathing space” that would come with atemporary suspension of its external debt obligations this year.

The Economist Intelligence Unit has re-calculated Indonesia’s debt-serviceposition in the light of probable debt deferral. We are assuming that aroundtwo-thirds of principal owed to official creditors would not have to be repaid in2005, and that two-thirds to three-quarters of interest owed to these creditorswould also not be paid this year. Under this assumption, Indonesia’s 2005debt-service payments would fall from a previously forecast US$12.7bn toUS$9.2bn, for a savings of US$3.5bn. This would reduce Indonesia’s debt-serviceratio to 10.3% in 2005 from a previously forecast 14.5%.

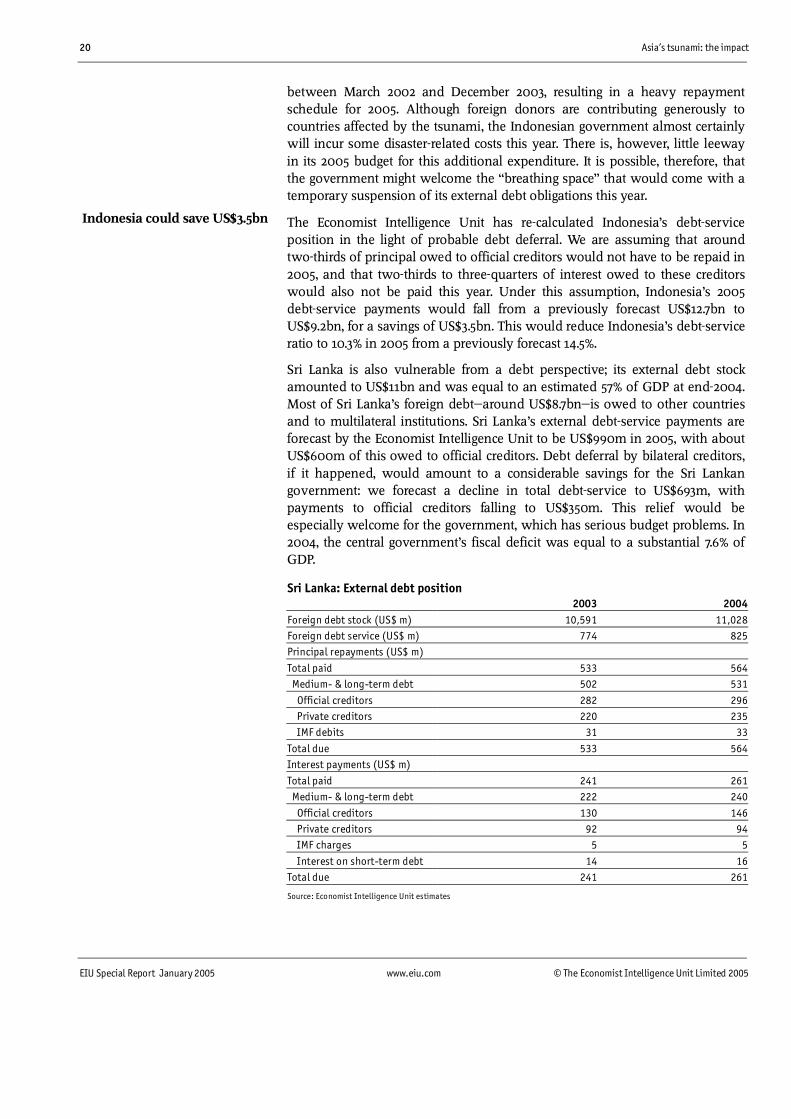

Sri Lanka is also vulnerable from a debt perspective; its external debt stockamounted to US$11bn and was equal to an estimated 57% of GDP at end-2004.Most of Sri Lanka’s foreign debt—around US$8.7bn—is owed to other countriesand to multilateral institutions. Sri Lanka’s external debt-service payments areforecast by the Economist Intelligence Unit to be US$990m in 2005, with aboutUS$600m of this owed to official creditors. Debt deferral by bilateral creditors,if it happened, would amount to a considerable savings for the Sri Lankangovernment: we forecast a decline in total debt-service to US$693m, withpayments to official creditors falling to US$350m. This relief would beespecially welcome for the government, which has serious budget problems. In2004, the central government’s fiscal deficit was equal to a substantial 7.6% ofGDP.

Sri Lanka: External debt position2003 2004

Foreign debt stock (US$ m) 10,591 11,028Foreign debt service (US$ m) 774 825Principal repayments (US$ m)

Total paid 533 564 Medium- & long-term debt 502 531

Official creditors 282 296 Private creditors 220 235 IMF debits 31 33

Total due 533 564Interest payments (US$ m)

Total paid 241 261 Medium- & long-term debt 222 240

Official creditors 130 146 Private creditors 92 94 IMF charges 5 5

Interest on short-term debt 14 16Total due 241 261

Source: Economist Intelligence Unit estimates

Indonesia could save US$3.5bn

Asia’s tsunami: the impact 21

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Asia: the impact on industriesAsia: the impact on industriesAsia: the impact on industriesAsia: the impact on industriesThe death toll from the tsunamis that devastated coastal areas of South andSouth-east Asia on December 26th is rising steadily as relief efforts advance. Atthe same time, governments and companies are also starting to tot up theimpact the disaster will have on various industries, from tourism to retail andfinance. Despite the human tragedy, some of the long-term macroeconomicdamage should be minimised by the positive effects of the reconstruction work.

One reason why the economic impact should be limited is that the tidal wave—caused by what is reckoned to be the world's worst earthquake in 40 years—largely missed the industrial centres of the region. The worst-affected areaswere underdeveloped coastal regions, such as the province of Aceh on thenorthern tip of the Indonesian island of Sumatra, and the remote Andamanand Nicobar islands in the Indian Ocean, which belong to India. The fewindustrialised areas affected are likely to recover relatively quickly. Although thecoastline near the port city of Chennai in south-east India was badly hit, forexample, reports suggest the damage to the city's industrial and portinfrastructure has been limited. The port of Colombo in Sri Lanka is back inoperation.

This has done little to reduce the human toll, however, with many of theregion's poorest farmers and fishermen still unaccounted for. The total numberkilled has exceeded 160,000, including more than 100,000 deaths in Indonesiaand 30,000 in Sri Lanka. More than 5,000 people were confirmed dead inThailand as of January 9th, and over 15,000 are dead or missing in India. Thesefigures could rise rapidly if disease starts to spread among the millions ofpeople now left hungry, thirsty and homeless.

Reconstruction will be a massive and costly undertaking, straining theemergency resources of governments in the region. More than US$5bn hasalready been pledged under an international relief effort, but with the damageso widespread, many of the less-affected regions may have to bear the coststhemselves. Sri Lanka's president, Chandrika Kumaratunga, has said rebuildinginfrastructure in the country could cost almost US$1bn, while Thailand'sgovernment has already committed US$1.5bn in aid, grants and soft loans.Munich Re, the world's biggest reinsurance company, puts the total recovery billfor the region at more than €10bn (US$13.6bn).

Despite the enormous extent of the damage, global financial markets scarcelymoved when news of the tsunami came through. The main reason is thatmany of the damaged facilities were uninsured, minimising the exposure ofWestern and Asian financial services companies. Munich Re reckons that itstotal exposure will be less than €100m (US$136m), while Swiss Re, the world'ssecond-biggest reinsurer, says its exposure should be under US$88m.

Local insurers, too, are not expecting to make significant pay-outs. Muang ThaiInsurance in Thailand, for example, has reported that its total liability in the sixaffected provinces was around Bt380m (US$9.7m), most of which was motorinsurance. Thai Reinsurance, a national reinsurer, said it expects losses of

Insurance

22 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

Bt100m. In Sri Lanka, less than US$50m in claims have been filed so far, withmost of those relating to loss of life rather to property damage.

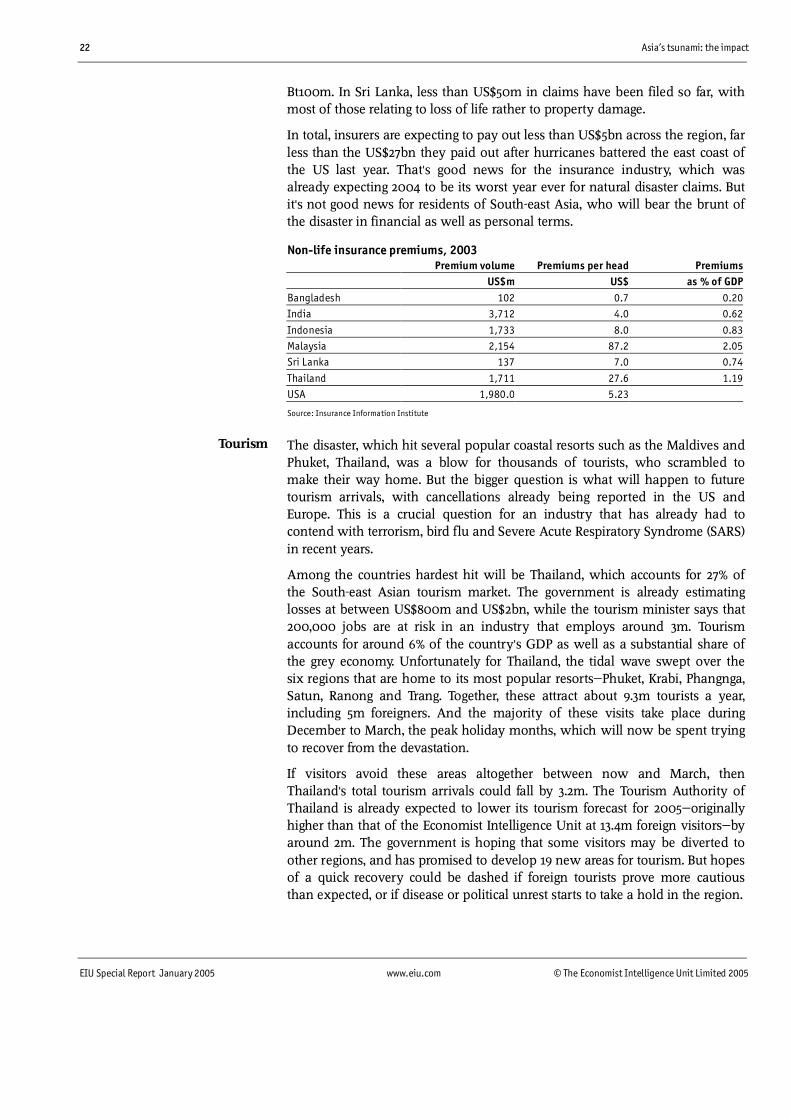

In total, insurers are expecting to pay out less than US$5bn across the region, farless than the US$27bn they paid out after hurricanes battered the east coast ofthe US last year. That's good news for the insurance industry, which wasalready expecting 2004 to be its worst year ever for natural disaster claims. Butit's not good news for residents of South-east Asia, who will bear the brunt ofthe disaster in financial as well as personal terms.

Non-life insurance premiums, 2003Premium volume Premiums per head Premiums

US$m US$ as % of GDPBangladesh 102 0.7 0.20India 3,712 4.0 0.62

Indonesia 1,733 8.0 0.83Malaysia 2,154 87.2 2.05Sri Lanka 137 7.0 0.74

Thailand 1,711 27.6 1.19USA 1,980.0 5.23

Source: Insurance Information Institute

The disaster, which hit several popular coastal resorts such as the Maldives andPhuket, Thailand, was a blow for thousands of tourists, who scrambled tomake their way home. But the bigger question is what will happen to futuretourism arrivals, with cancellations already being reported in the US andEurope. This is a crucial question for an industry that has already had tocontend with terrorism, bird flu and Severe Acute Respiratory Syndrome (SARS)in recent years.

Among the countries hardest hit will be Thailand, which accounts for 27% ofthe South-east Asian tourism market. The government is already estimatinglosses at between US$800m and US$2bn, while the tourism minister says that200,000 jobs are at risk in an industry that employs around 3m. Tourismaccounts for around 6% of the country's GDP as well as a substantial share ofthe grey economy. Unfortunately for Thailand, the tidal wave swept over thesix regions that are home to its most popular resorts—Phuket, Krabi, Phangnga,Satun, Ranong and Trang. Together, these attract about 9.3m tourists a year,including 5m foreigners. And the majority of these visits take place duringDecember to March, the peak holiday months, which will now be spent tryingto recover from the devastation.

If visitors avoid these areas altogether between now and March, thenThailand's total tourism arrivals could fall by 3.2m. The Tourism Authority ofThailand is already expected to lower its tourism forecast for 2005—originallyhigher than that of the Economist Intelligence Unit at 13.4m foreign visitors—byaround 2m. The government is hoping that some visitors may be diverted toother regions, and has promised to develop 19 new areas for tourism. But hopesof a quick recovery could be dashed if foreign tourists prove more cautiousthan expected, or if disease or political unrest starts to take a hold in the region.

Tourism

Asia’s tsunami: the impact 23

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

The other country to suffer badly will be Sri Lanka, where the tourism sectoraccounts for 4.6% of GDP and employs 400,000 people. The tsunami struck thecrucial beach resorts on the south coast of the country, and the damage willtake months to clear. Yet fortunately, many of the larger hotels sufferedrelatively little damage, with some estimates suggesting many of these could beback in operation within one month. Indeed, Sri Lanka's tourist board claimsthat of the 7,682 rooms affected by the tsunami, around half are already back infull operation. Barring any setbacks, the tsunami is expected to have less of animpact on the tourism industry than the SARS epidemic of 2003 or anyresumption of Sri Lanka's civil war.

In Indonesia, too, optimists are hoping that, as a one-off event, the tsunami willnot damage tourism as badly as the 2002 Bali bomb did. Although Indonesiawas among the countries hardest hit by the tsunami, its tourist industry isrelatively small and its most popular destinations—including Bali—are locatedwell away from the main disaster zone. The island is even hoping to win someadditional business if tourists who had originally planned trips to major Thairesorts switch to Bali instead. The main stumbling block remains the continuedterrorist threat, after bombs were found on a bus over the Christmas period.With many foreign embassies again warning tourists to stay away fromIndonesia, a recovery could prove slower than expected.

Larger countries such as India are also hoping that they can divert tourists awayfrom the battered regions, minimising the economic impact. The eastern cost ofIndia, where some hotels were damaged, is popular with domestic visitors. Butforeigners tend to prefer Goa on the west coast and the states of northern India.

Given the location of the tsunami, few other sectors will be directly affected.Although large areas of agricultural land were damaged, especially inIndonesia, these were mainly subsistence farms that were not part of theofficial economy. The tea plantations in India and Sri Lanka are mainly onhigher ground and thus escaped damage, although exports could be disruptedby damage to infrastructure. In Sri Lanka, the fishing industry, which accountedfor around 3% of GDP, will take some time to recover. As well as the damage toboats, ports and other infrastructure, local fishermen will have to contend witha drop in demand for their fish, with locals convinced that they will have beenfeeding on the tsunami dead.

As far as other industries are concerned, the biggest question is how badly thetsunami and its after-effects will hit consumer spending. In Thailand, theFederation of Thai Industries has been issuing gloomy predictions about theautomotive industry, for example, saying that production could drop by 12%from the original projections as sales slump. The federation expects a total lackof demand from the six regions worst affected by the disaster, where rebuildinghomes and businesses will take priority. The costs of the rebuilding work couldalso hit spending power in other regions, it claims, as locals try to help outfamily and friends.

There may be a touch of politics in these dire warnings, given that Thailand'selections are due in mid-February. The warnings also have to be seen in thecontext of record high growth in the automotive industry. Car production in the

The wider economy

24 Asia’s tsunami: the impact

EIU Special Report January 2005 www.eiu.com © The Economist Intelligence Unit Limited 2005

year to November 2004 rose a massive 23% on the year before, thanks tobooming exports and domestic sales. Production had been expected to showanother 25% leap in 2005, to over 1.1m, before the tsunami struck, so even thenew gloomier forecast represents healthy growth on 2004.

The same is true for the Thai economy in general, which has been growingstrongly. The work and income generated by the reconstruction efforts and bygovernment aid should help to mitigate the dent in domestic demand and intourism arrivals. And with industrial damage limited, Thailand's manufacturingsector should still be able to respond to the strong demand from exportmarkets. Nevertheless, there is a risk that the tsunami will take the edge off therecent consumer spending boom, especially in the weeks immediately after thedisaster. For that reason, although the finance ministry is expecting the tsunamito shave just 0.3 percentage points off GDP growth in 2005, the EconomistIntelligence Unit expects a reduction of around 1.2 percentage points.

In Sri Lanka, the central bank is predicting that GDP growth will drop 0.5percentage points during 2005, to around 5.5%, as the country continues itsstrong economic recovery from the civil war. The Economist Intelligence Unit isforecasting a larger impact from the tsunami, with GDP growing by onlyaround 4.2%. The tourism sector will suffer for some time, and the disruption tothose who work in the industry will reduce consumer spending. Up to 100,000fisherman are now unemployed, and this to will reduce private consumption.

In Indonesia and India, the economic impact could be even lighter, after aninitial downturn in early 2005 gives way to higher growth. The Aceh region ofIndonesia contributes just 4% of the country's GDP, most of which comes froma liquified natural gas terminal that remains in operation. The EconomistIntelligence Unit therefore has downgraded its forecast for Indonesia's 2005GDP growth by just 0.3 percentage points.

This optimistic scenario depends on the right political climate, however, andcould be undermined by infighting or renewed turmoil. Indonesia isparticularly prone to allegations of corruption, given that its new president,Susilo Bambang Yudhoyono, was elected on the back of a "clean hands"campaign. In Sri Lanka, the worry is that the devastation and the sudden influxin aid could endanger the ceasefire between the government and the LiberationTigers of Tamil Eelam (LTTE, or Tamil Tigers). The Tamils see the eastern coast,which was worst affected by the tsunami, as their territory and could blockgovernment attempts to send aid. Yet at the same time there will be deepresentment if the government-friendly south is seen to be getting more.

The other big risk is that diseases such as cholera and typhus take hold amongthe millions of people left homeless by the disaster. If that happens, then thedeath toll would rise still further and the economy would take far longer torecover. The next few months will therefore be crucial as the relief efforts getunderway, and foreign tourists decide where to take their holidays. If all goeswell, then the economic impact can be limited—although that will be littleconsolation to those who have lost their family, friends and homes.