ASIAN JOURNAL OF RESEARCH IN BUSINESS … · Due to this they offer the benefit of trading like a...

29

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307 AJRBEM Journal of Asian Research Consortium 48 http://www.aijsh.org A Peer Reviewed International Journal of Asian Research Consortium AJRBEM: ASIAN JOURNAL OF RESEARCH IN BUSINESS ECONOMICS AND MANAGEMENT EXCHANGE TRADED FUNDS: AN INDIAN PERSPECTIVE MR.PRASANNA K.BARAL* *Sr.Faculty in Commerce, Kalinga Bharati Resdential College, Pira Bazar, Bhanpur, Gopalpur, Cuttack, Odisha. ABSTRACT The last two decades witnessed new product innovations in the financial markets across the globe. Designing of new innovative financial products which promise to meet investors’ return expectations as market conditions and global risk appetite change is of a great challenge for the professionals in the financial markets. In recent years, investors are looking for alternative investment vehicles to structured products which gave birth to a new kind of cost and tax-efficient financial instrument, i.e. Exchange Traded Funds popularly known as, ETFs. The investment professionals are always in search of new and sophisticated investment strategies and ETFs can provide them new ways to form building blocks of investment strategies. The present paper studies the growth trend of ETFs and a comparative study of Index based ETFs and Gold based ETFs in India. KEYWORDS: Index based ETFs; Gold based ETFs, Sophisticated investment strategies,structured product. ______________________________________________________________________________ 1. INTRODUCTION ETFs are one of the most innovative new financial products to emerge from the financial industry in the last two decades. Since the launch of the first ETF in the Canada in 1990, ETFs have opened a new panorama of investment opportunities. Exchange-traded funds (ETFs) have gained a wider acceptance as financial instruments whose unique advantages over mutual funds have caught the eye of many investors. These instruments are beneficial for investors that find it difficult to master the tricks of the trade of analyzing and picking stocks for their portfolio.

Transcript of ASIAN JOURNAL OF RESEARCH IN BUSINESS … · Due to this they offer the benefit of trading like a...

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 48

http://w

ww.aijsh.org

A P e e r R e v i e w e d I n t e r n a t i o n a l J o u r n a l o f A s i a n R e s e a r c h C o n s o r t i u m

AJRBEM:

A S I A N J O U R N A L O F R E S E A R C H I N B U S I N E S S

E C O N O M I C S A N D M A N A G E M E N T

EXCHANGE TRADED FUNDS: AN INDIAN PERSPECTIVE

MR.PRASANNA K.BARAL*

*Sr.Faculty in Commerce,

Kalinga Bharati Resdential College, Pira Bazar, Bhanpur,

Gopalpur, Cuttack, Odisha.

ABSTRACT The last two decades witnessed new product innovations in the financial markets across the globe. Designing of new innovative financial products which promise to meet investors’ return expectations as market conditions and global risk appetite change is of a great challenge for the professionals in the financial markets. In recent years, investors are looking for alternative investment vehicles to structured products which gave birth to a new kind of cost and tax-efficient financial instrument, i.e. Exchange Traded Funds popularly known as, ETFs. The investment professionals are always in search of new and sophisticated investment strategies and ETFs can provide them new ways to form building blocks of investment strategies. The present paper studies the growth trend of ETFs and a comparative study of Index based ETFs and Gold based ETFs in India. KEYWORDS: Index based ETFs; Gold based ETFs, Sophisticated investment strategies,structured product.

______________________________________________________________________________

1. INTRODUCTION

ETFs are one of the most innovative new financial products to emerge from the financial industry in the last two decades. Since the launch of the first ETF in the Canada in 1990, ETFs have opened a new panorama of investment opportunities. Exchange-traded funds (ETFs) have gained a wider acceptance as financial instruments whose unique advantages over mutual funds have caught the eye of many investors. These instruments are beneficial for investors that find it difficult to master the tricks of the trade of analyzing and picking stocks for their portfolio.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 49

http://w

ww.aijsh.org

Exchange Traded Funds are essentially Index Funds that are listed and traded on exchanges like stocks. Until the development of ETFs, this was not possible before. Globally, ETFs have opened a whole new way of investment opportunities to Retail as well as Institutional Money Managers. They enable investors to gain broad exposure to entire stock markets in different Countries and specific sectors with relative ease, on a real-time basis and at a lower cost than many other forms of investments.

2. OBJECTIVES

1: To study the concept of Exchange Traded Funds.

2: To study the growth trend of Exchange Traded Funds.

3: To make a comparative study of Index based ETFs Vis-À-Vis Gold based ETFs in Indian.

3. LITERATURE REVIEW

Kostovetsky (2003), studied relative performance of the ETFs and Index mutual funds from the investors’ point of view. He reported key areas of differences between the two to lie in management fees, shareholders transaction fees, taxation efficiency, and the qualitative factors transaction convenience, short selling, and ability to margin. His core finding was that Index mutual funds are better suited for small investors and ETFs are preferable by large investors.

Johnson, W.L. (2008), studied 20 foreign country ETFs and the underlying index returns from 1997 to 2006 for the existence and sources of daily and monthly tracking errors. He found except for one case, market segmentation/integration of the foreign country was a significant source of tracking error. He also concluded “variables such as foreign index positive returns relative to the US index and whether the foreign exchange trades 12 simultaneously with the US markets were significant explanatory variables in the correlation coefficients between ETFs and their underlying home index”.

Rompotis (2009a), evaluated performance and trading characteristics of 73 iShare ETFs from October 3, 2005 to September 29, 2006 covering 250 daily observations. The finding was that iShares fail to accurately replicate the performance of their underlying indexes, they trade at a premium to their NAV, their tracking errors 13 are strongly correlated with the expenses and risk, and that the premium was correlated positively with tracking error and negatively with the volume.

Rompotis (2009b), studied 20 vanguard ETFs and 12 Vanguard index mutual funds belonging to the same family in order to examine the existence and reasons for interfamily competition between ETFs and Index mutual funds sponsored by the same entity. The study’s main findings were that ETFs and index mutual funds on average present similar returns and risks, both of these investment vehicles produce lower returns than their benchmarks, they both have low tracking errors, and their tracking errors are positively correlated with expenses.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 50

http://w

ww.aijsh.org

4. RESEARCH METHODOLOGY

The data for the study has been derived basically from secondary sources. The secondary sources include internet, journals, magazines and publications of various research bodies like, SEBI, ICAR, NSE, BSE and Handbook of BlackRock. The parameters for evaluating the performance are Risk, Return, Expenses Ratio, and Reward to Variability. The statistical tools like Standard Deviation, Beta, Sharpe Ratio and Treynors ratio are used for data analysis. The data has been properly analysed and interpreted to draw conclusion and inferences.

5. EXCHANGE TRADED FUNDS: CONCEPTUAL BACKGROUND

ETFs are index tracking open ended registered funds or unit investment trusts that invest in a portfolio of stocks designed to track the performance and dividend yield of a specific index. They are essentially mutual fund schemes or index funds that are listed and traded on exchanges like stocks. Due to this they offer the benefit of trading like a stock. They are priced continually and can be bought or sold throughout the trading day.

An ETF is a basket of stocks that reflects the composition of an Index, like S&P CNX Nifty or BSE Sensex. The ETFs trading value is based on the net asset value of the underlying stocks that it represents. Think of it as a Mutual Fund that you can buy and sell in real-time at a price those changes throughout the day. As it tracks a Benchmark Index, the return expectation is the same as that of the Index. For example, if for a particular period, say from 1st February 2012 to 31st of March 2012, the ROI on Nifty is 10%, then the NAV of the ETF that tracks Nifty should also be around 10%. The minor difference in return between the NAV and the Benchmark Indices could be because of the fact that there would be some cost involved in managing the ETF.

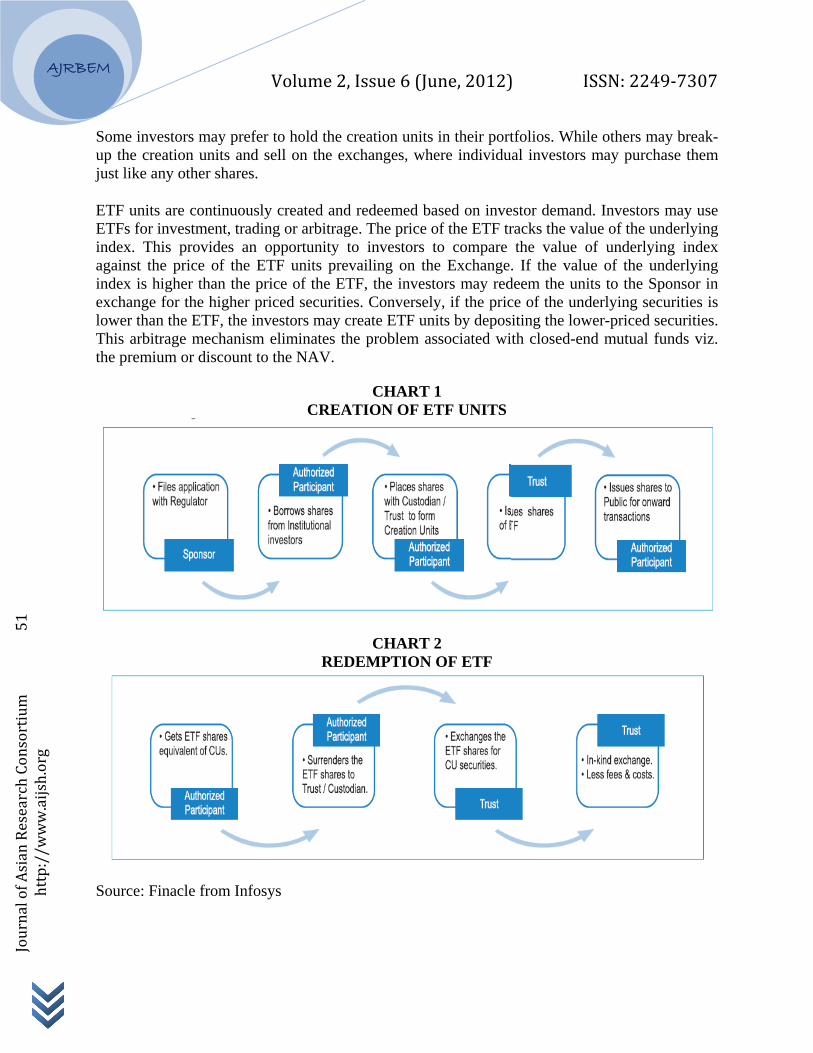

CREATION AND REDEMPTION OF ETF

ETFs are different from Mutual funds in the sense that ETF units are not sold to the public for cash. Instead, the Asset Management Company that sponsors the ETF (Fund) takes the shares of companies comprising the index from various categories of investors like authorized participants, large investors and institutions. In turn, it issues them a large block of ETF units. Since dividend may have accumulated for the stocks at any point in time, a cash component to that extent is also taken from such investors. In other words, a large block of ETF units called a "Creation Unit" is exchanged for a "Portfolio Deposit" of stocks and "Cash Component".

The number of outstanding ETF units is not limited, as with traditional mutual funds. It may increase if investors deposit shares to create ETF units; or it may reduce on a day if some ETF holders redeem their ETF units for the underlying shares. These transactions are conducted by sending creation / redemption instructions to the Fund. The Portfolio Deposit closely approximates the proportion of the stocks in the index together with a specified amount of Cash Component. This "in-kind" creation / redemption facility ensures that ETFs trade close to their fair value at any given time.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 51

http://w

ww.aijsh.org

Some investors may prefer to hold the creation units in their portfolios. While others may break-up the creation units and sell on the exchanges, where individual investors may purchase them just like any other shares.

ETF units are continuously created and redeemed based on investor demand. Investors may use ETFs for investment, trading or arbitrage. The price of the ETF tracks the value of the underlying index. This provides an opportunity to investors to compare the value of underlying index against the price of the ETF units prevailing on the Exchange. If the value of the underlying index is higher than the price of the ETF, the investors may redeem the units to the Sponsor in exchange for the higher priced securities. Conversely, if the price of the underlying securities is lower than the ETF, the investors may create ETF units by depositing the lower-priced securities. This arbitrage mechanism eliminates the problem associated with closed-end mutual funds viz. the premium or discount to the NAV.

CHART 1 CREATION OF ETF UNITS

CHART 2 REDEMPTION OF ETF

Source: Finacle from Infosys

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 52

http://w

ww.aijsh.org

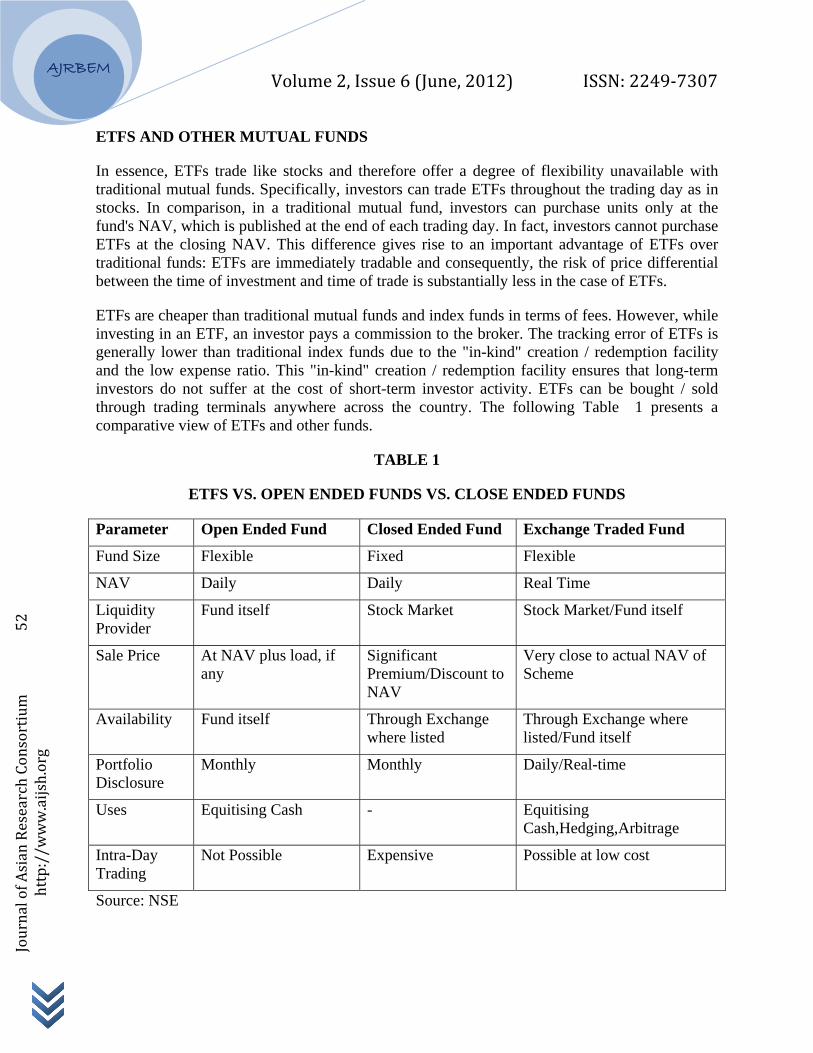

ETFS AND OTHER MUTUAL FUNDS

In essence, ETFs trade like stocks and therefore offer a degree of flexibility unavailable with traditional mutual funds. Specifically, investors can trade ETFs throughout the trading day as in stocks. In comparison, in a traditional mutual fund, investors can purchase units only at the fund's NAV, which is published at the end of each trading day. In fact, investors cannot purchase ETFs at the closing NAV. This difference gives rise to an important advantage of ETFs over traditional funds: ETFs are immediately tradable and consequently, the risk of price differential between the time of investment and time of trade is substantially less in the case of ETFs.

ETFs are cheaper than traditional mutual funds and index funds in terms of fees. However, while investing in an ETF, an investor pays a commission to the broker. The tracking error of ETFs is generally lower than traditional index funds due to the "in-kind" creation / redemption facility and the low expense ratio. This "in-kind" creation / redemption facility ensures that long-term investors do not suffer at the cost of short-term investor activity. ETFs can be bought / sold through trading terminals anywhere across the country. The following Table 1 presents a comparative view of ETFs and other funds.

TABLE 1

ETFS VS. OPEN ENDED FUNDS VS. CLOSE ENDED FUNDS

Parameter Open Ended Fund Closed Ended Fund Exchange Traded Fund

Fund Size Flexible Fixed Flexible

NAV Daily Daily Real Time

Liquidity Provider

Fund itself Stock Market Stock Market/Fund itself

Sale Price At NAV plus load, if any

Significant Premium/Discount to NAV

Very close to actual NAV of Scheme

Availability Fund itself Through Exchange where listed

Through Exchange where listed/Fund itself

Portfolio Disclosure

Monthly Monthly Daily/Real-time

Uses Equitising Cash - Equitising Cash,Hedging,Arbitrage

Intra-Day Trading

Not Possible Expensive Possible at low cost

Source: NSE

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 53

http://w

ww.aijsh.org

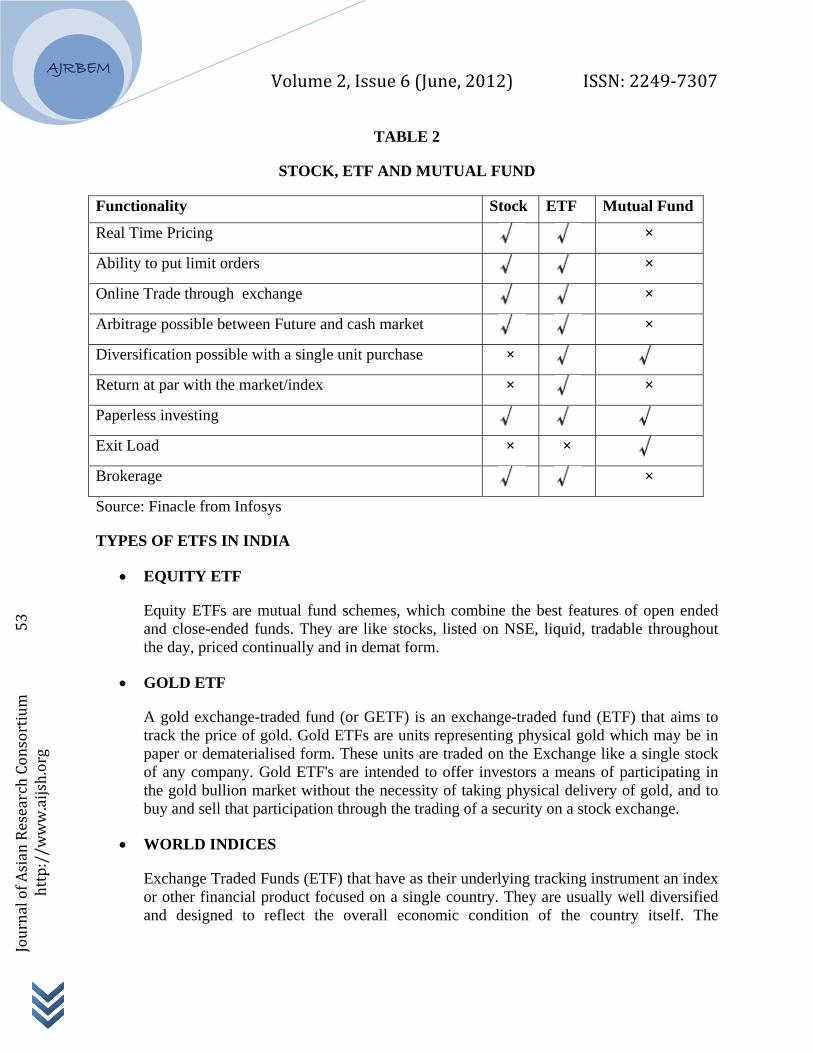

TABLE 2

STOCK, ETF AND MUTUAL FUND

Functionality Stock ETF Mutual Fund

Real Time Pricing ×

Ability to put limit orders ×

Online Trade through exchange ×

Arbitrage possible between Future and cash market ×

Diversification possible with a single unit purchase × Return at par with the market/index × ×

Paperless investing Exit Load × × Brokerage ×

Source: Finacle from Infosys

TYPES OF ETFS IN INDIA

• EQUITY ETF

Equity ETFs are mutual fund schemes, which combine the best features of open ended and close-ended funds. They are like stocks, listed on NSE, liquid, tradable throughout the day, priced continually and in demat form.

• GOLD ETF

A gold exchange-traded fund (or GETF) is an exchange-traded fund (ETF) that aims to track the price of gold. Gold ETFs are units representing physical gold which may be in paper or dematerialised form. These units are traded on the Exchange like a single stock of any company. Gold ETF's are intended to offer investors a means of participating in the gold bullion market without the necessity of taking physical delivery of gold, and to buy and sell that participation through the trading of a security on a stock exchange.

• WORLD INDICES

Exchange Traded Funds (ETF) that have as their underlying tracking instrument an index or other financial product focused on a single country. They are usually well diversified and designed to reflect the overall economic condition of the country itself. The

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 54

http://w

ww.aijsh.org

underlying index chosen is often the major index of the principal exchange within the country.

• DEBT ETF

Debt ETFs that invest in bonds or debt securities are known as bond or debt ETFs. They thrive during economic recessions because investors pull their money out of the stock market and into bonds (for example, government treasury bonds or those issues by companies regarded as financially stable). These ETFs are linked to money or debt funds, with the aim of providing money market returns.

Liquid BeES (Goldman Sachs Liquid Exchange Traded Scheme) is the first money market ETF (Exchange Traded Fund) in the world. The investment objective of the Scheme is to provide money market returns. Liquid BeES will invest in a basket of call money, short-term government securities and money market instruments of short and medium maturities. It is listed and traded on the NSE - Capital Market Segment and is settled on a T+2 Rolling basis.

HOW TO INVEST IN ETFS

Trading in ETF is very simple. It is similar to how you trade in equity shares. One can trade from his existing trading account with his broker or register himself with a broker having membership of the NSE/BSE,fill up the KYC form, open a demat account, post margins and then commence trading.

Select an ETF Log into your Trading A/c Place an Order

or call your NSE/BSE broker

ETFs are in dematerialized form and settle like any other shares in T+2 rolling settlement.

6. EXCHANGE TRADED FUNDS: THE GLOBAL GROWTH TREND

They first ETF came into existence in the USA in 1993. It took several years for them to attract public interest. But once they did, the volumes took off with a vengeance. About 60% of trading volumes on the American Stock Exchange are from ETFs. The most popular ETFs are QQQs (Cubes) based on the Nasdaq-100 Index, SPDRs (Spiders) based on the S&P 500 Index, iSHARES based on MSCI Indices and TRAHK (Tracks) based on the Hang Seng Index. The average daily trading volume in QQQ is around 89 million shares.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 55

http://w

ww.aijsh.org

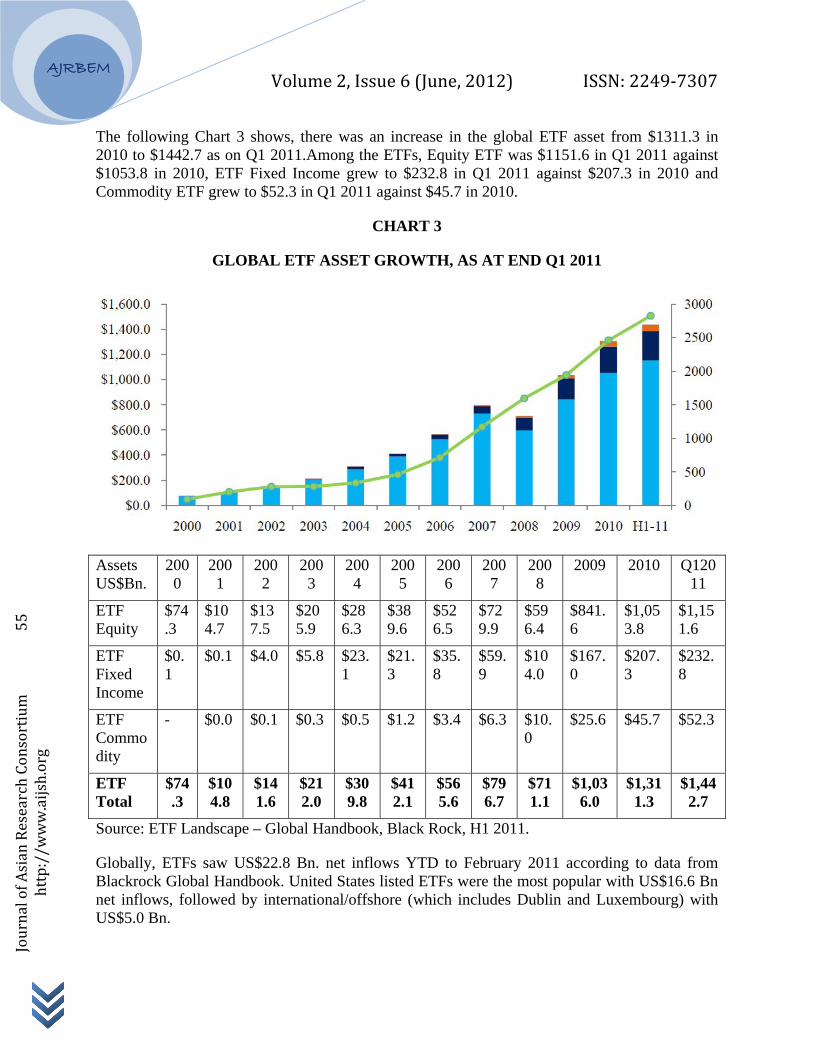

The following Chart 3 shows, there was an increase in the global ETF asset from $1311.3 in 2010 to $1442.7 as on Q1 2011.Among the ETFs, Equity ETF was $1151.6 in Q1 2011 against $1053.8 in 2010, ETF Fixed Income grew to $232.8 in Q1 2011 against $207.3 in 2010 and Commodity ETF grew to $52.3 in Q1 2011 against $45.7 in 2010.

CHART 3

GLOBAL ETF ASSET GROWTH, AS AT END Q1 2011

Assets US$Bn.

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009 2010 Q12011

ETF Equity

$74.3

$104.7

$137.5

$205.9

$286.3

$389.6

$526.5

$729.9

$596.4

$841.6

$1,053.8

$1,151.6

ETF Fixed Income

$0.1

$0.1 $4.0 $5.8 $23.1

$21.3

$35.8

$59.9

$104.0

$167.0

$207.3

$232.8

ETF Commodity

- $0.0 $0.1 $0.3 $0.5 $1.2 $3.4 $6.3 $10.0

$25.6 $45.7 $52.3

ETF Total

$74.3

$104.8

$141.6

$212.0

$309.8

$412.1

$565.6

$796.7

$711.1

$1,036.0

$1,311.3

$1,442.7

Source: ETF Landscape – Global Handbook, Black Rock, H1 2011.

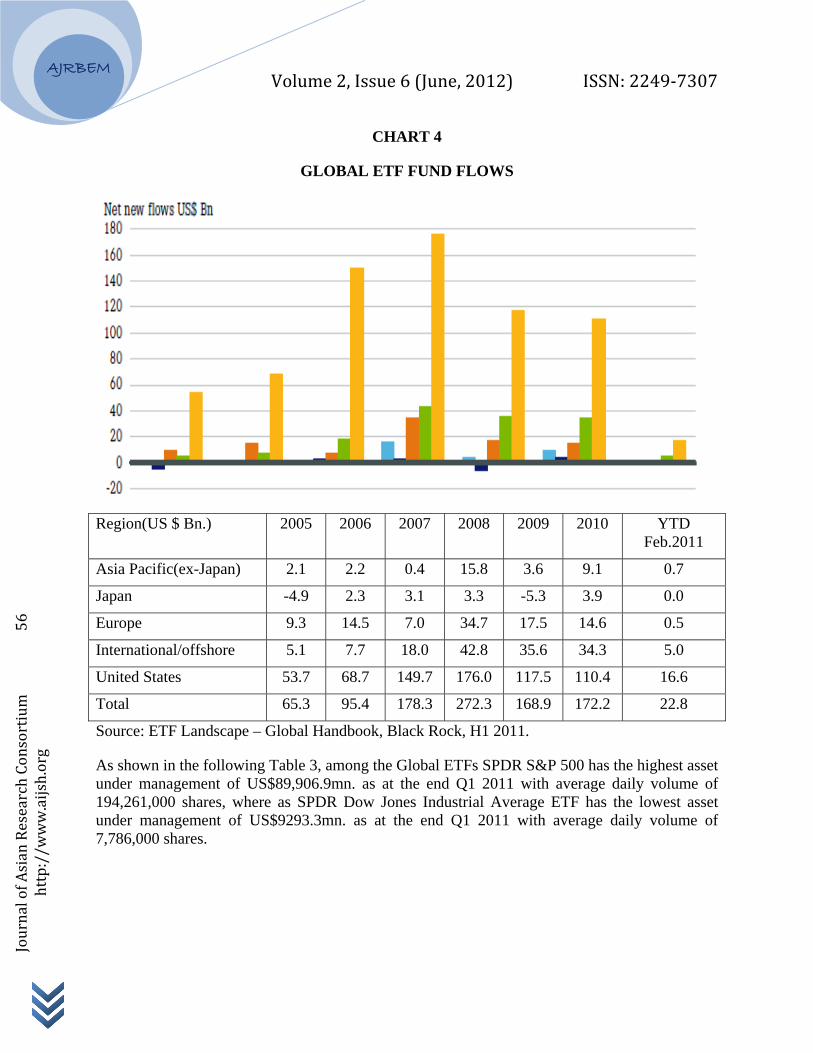

Globally, ETFs saw US$22.8 Bn. net inflows YTD to February 2011 according to data from Blackrock Global Handbook. United States listed ETFs were the most popular with US$16.6 Bn net inflows, followed by international/offshore (which includes Dublin and Luxembourg) with US$5.0 Bn.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 56

http://w

ww.aijsh.org

CHART 4

GLOBAL ETF FUND FLOWS

Region(US $ Bn.) 2005 2006 2007 2008 2009 2010 YTD Feb.2011

Asia Pacific(ex-Japan) 2.1 2.2 0.4 15.8 3.6 9.1 0.7

Japan -4.9 2.3 3.1 3.3 -5.3 3.9 0.0

Europe 9.3 14.5 7.0 34.7 17.5 14.6 0.5

International/offshore 5.1 7.7 18.0 42.8 35.6 34.3 5.0

United States 53.7 68.7 149.7 176.0 117.5 110.4 16.6

Total 65.3 95.4 178.3 272.3 168.9 172.2 22.8

Source: ETF Landscape – Global Handbook, Black Rock, H1 2011.

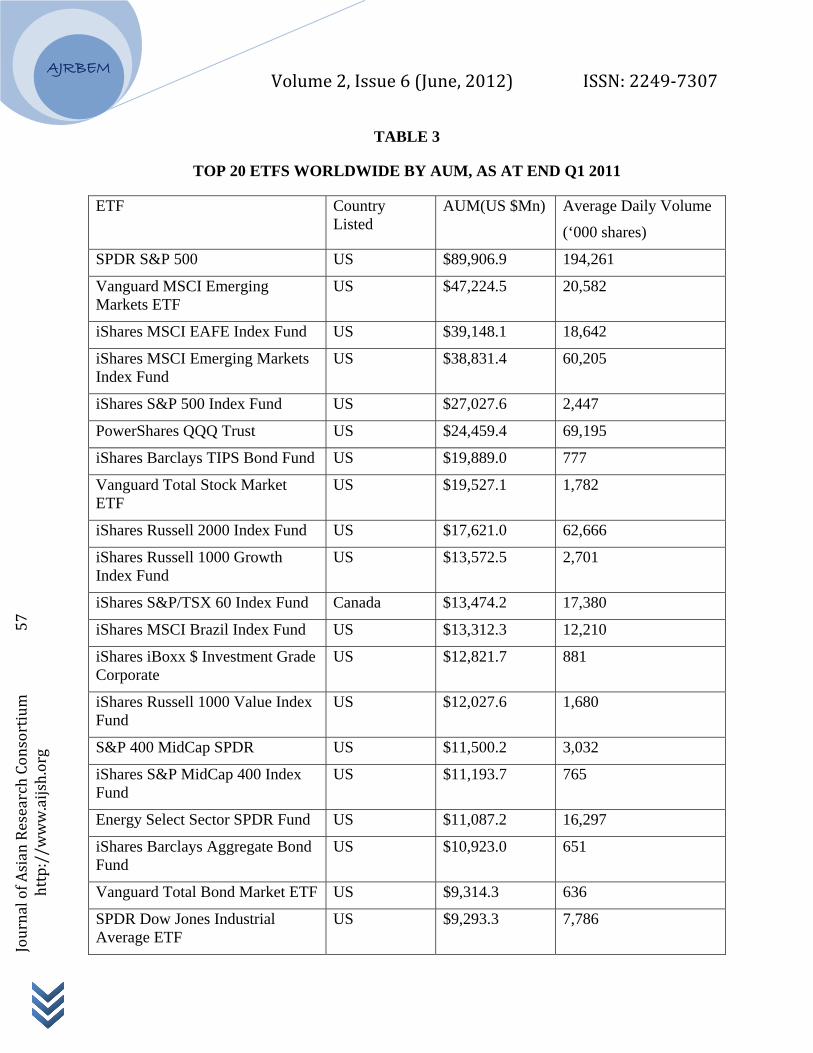

As shown in the following Table 3, among the Global ETFs SPDR S&P 500 has the highest asset under management of US$89,906.9mn. as at the end Q1 2011 with average daily volume of 194,261,000 shares, where as SPDR Dow Jones Industrial Average ETF has the lowest asset under management of US$9293.3mn. as at the end Q1 2011 with average daily volume of 7,786,000 shares.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 57

http://w

ww.aijsh.org

TABLE 3

TOP 20 ETFS WORLDWIDE BY AUM, AS AT END Q1 2011

ETF Country Listed

AUM(US $Mn) Average Daily Volume

(‘000 shares)

SPDR S&P 500 US $89,906.9 194,261

Vanguard MSCI Emerging Markets ETF

US $47,224.5 20,582

iShares MSCI EAFE Index Fund US $39,148.1 18,642

iShares MSCI Emerging Markets Index Fund

US $38,831.4 60,205

iShares S&P 500 Index Fund US $27,027.6 2,447

PowerShares QQQ Trust US $24,459.4 69,195

iShares Barclays TIPS Bond Fund US $19,889.0 777

Vanguard Total Stock Market ETF

US $19,527.1 1,782

iShares Russell 2000 Index Fund US $17,621.0 62,666

iShares Russell 1000 Growth Index Fund

US $13,572.5 2,701

iShares S&P/TSX 60 Index Fund Canada $13,474.2 17,380

iShares MSCI Brazil Index Fund US $13,312.3 12,210

iShares iBoxx $ Investment Grade Corporate

US $12,821.7 881

iShares Russell 1000 Value Index Fund

US $12,027.6 1,680

S&P 400 MidCap SPDR US $11,500.2 3,032

iShares S&P MidCap 400 Index Fund

US $11,193.7 765

Energy Select Sector SPDR Fund US $11,087.2 16,297

iShares Barclays Aggregate Bond Fund

US $10,923.0 651

Vanguard Total Bond Market ETF US $9,314.3 636

SPDR Dow Jones Industrial Average ETF

US $9,293.3 7,786

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 58

http://w

ww.aijsh.org

Source: ETF Landscape – Global Handbook, Black Rock, H1 2011.

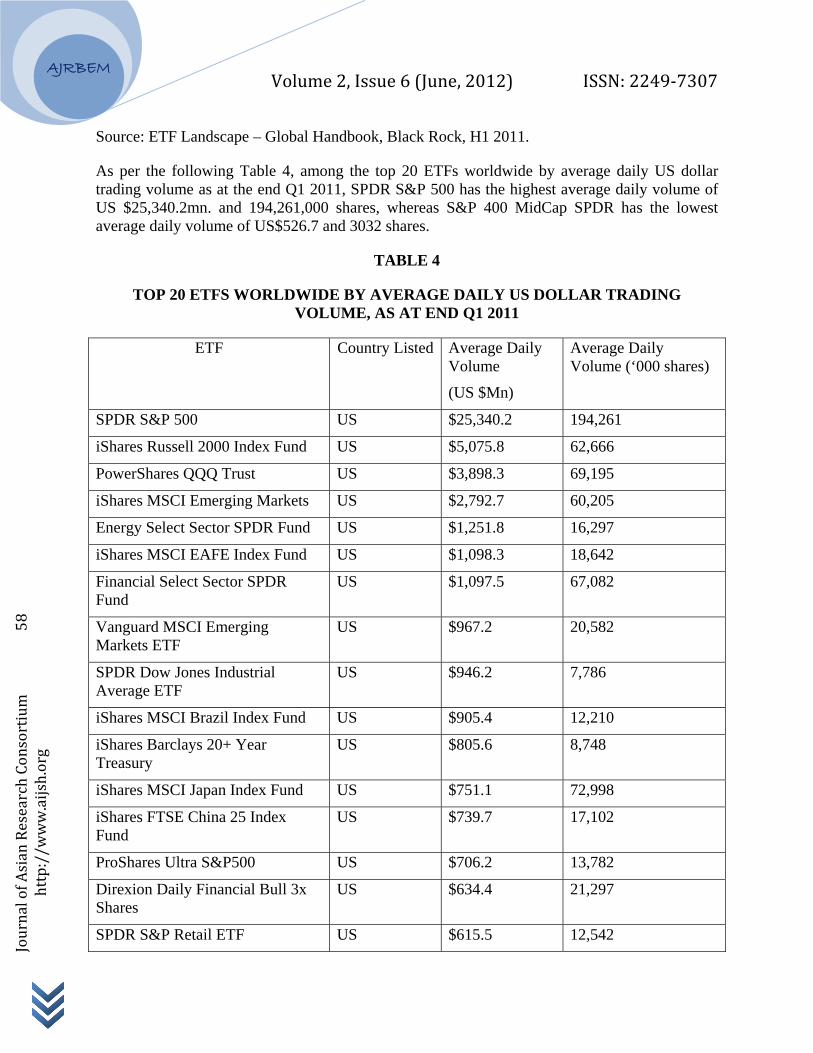

As per the following Table 4, among the top 20 ETFs worldwide by average daily US dollar trading volume as at the end Q1 2011, SPDR S&P 500 has the highest average daily volume of US $25,340.2mn. and 194,261,000 shares, whereas S&P 400 MidCap SPDR has the lowest average daily volume of US$526.7 and 3032 shares.

TABLE 4

TOP 20 ETFS WORLDWIDE BY AVERAGE DAILY US DOLLAR TRADING VOLUME, AS AT END Q1 2011

ETF Country Listed Average Daily Volume

(US $Mn)

Average Daily Volume (‘000 shares)

SPDR S&P 500 US $25,340.2 194,261

iShares Russell 2000 Index Fund US $5,075.8 62,666

PowerShares QQQ Trust US $3,898.3 69,195

iShares MSCI Emerging Markets US $2,792.7 60,205

Energy Select Sector SPDR Fund US $1,251.8 16,297

iShares MSCI EAFE Index Fund US $1,098.3 18,642

Financial Select Sector SPDR Fund

US $1,097.5 67,082

Vanguard MSCI Emerging Markets ETF

US $967.2 20,582

SPDR Dow Jones Industrial Average ETF

US $946.2 7,786

iShares MSCI Brazil Index Fund US $905.4 12,210

iShares Barclays 20+ Year Treasury

US $805.6 8,748

iShares MSCI Japan Index Fund US $751.1 72,998

iShares FTSE China 25 Index Fund

US $739.7 17,102

ProShares Ultra S&P500 US $706.2 13,782

Direxion Daily Financial Bull 3x Shares

US $634.4 21,297

SPDR S&P Retail ETF US $615.5 12,542

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 59

http://w

ww.aijsh.org

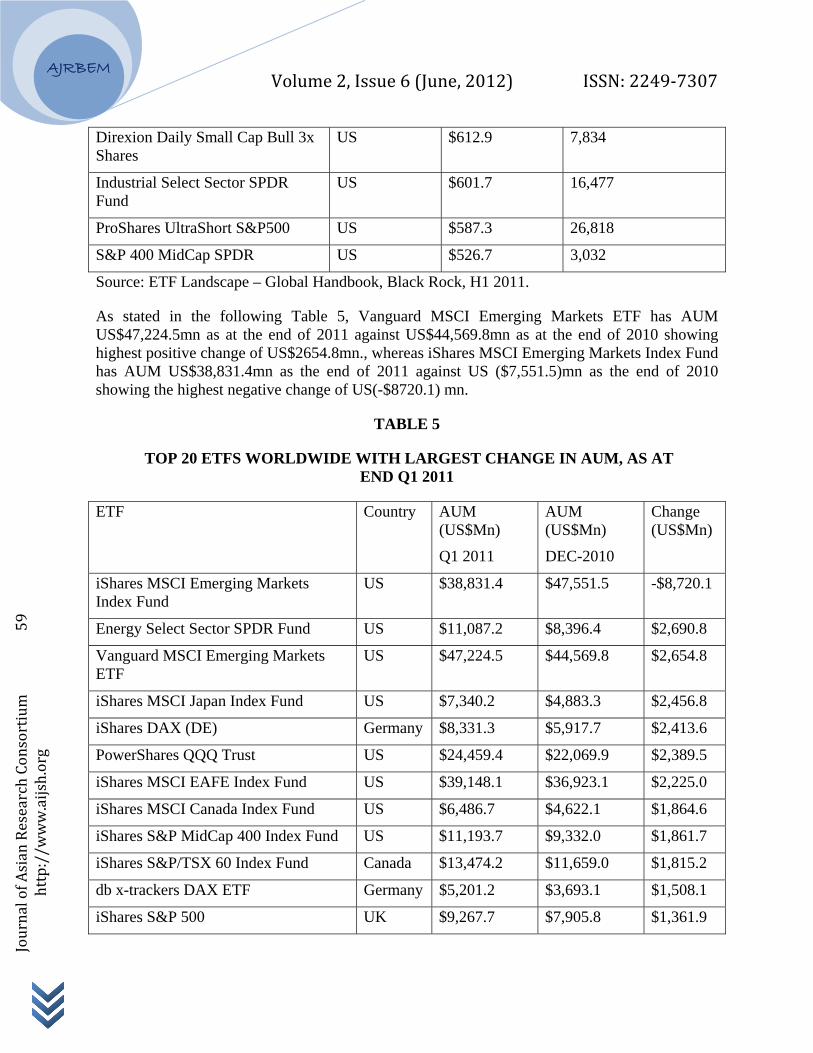

Direxion Daily Small Cap Bull 3x Shares

US $612.9 7,834

Industrial Select Sector SPDR Fund

US $601.7 16,477

ProShares UltraShort S&P500 US $587.3 26,818

S&P 400 MidCap SPDR US $526.7 3,032

Source: ETF Landscape – Global Handbook, Black Rock, H1 2011.

As stated in the following Table 5, Vanguard MSCI Emerging Markets ETF has AUM US$47,224.5mn as at the end of 2011 against US$44,569.8mn as at the end of 2010 showing highest positive change of US$2654.8mn., whereas iShares MSCI Emerging Markets Index Fund has AUM US$38,831.4mn as the end of 2011 against US ($7,551.5)mn as the end of 2010 showing the highest negative change of US(-$8720.1) mn.

TABLE 5

TOP 20 ETFS WORLDWIDE WITH LARGEST CHANGE IN AUM, AS AT END Q1 2011

ETF Country AUM (US$Mn)

Q1 2011

AUM (US$Mn)

DEC-2010

Change (US$Mn)

iShares MSCI Emerging Markets Index Fund

US $38,831.4 $47,551.5 -$8,720.1

Energy Select Sector SPDR Fund US $11,087.2 $8,396.4 $2,690.8

Vanguard MSCI Emerging Markets ETF

US $47,224.5 $44,569.8 $2,654.8

iShares MSCI Japan Index Fund US $7,340.2 $4,883.3 $2,456.8

iShares DAX (DE) Germany $8,331.3 $5,917.7 $2,413.6

PowerShares QQQ Trust US $24,459.4 $22,069.9 $2,389.5

iShares MSCI EAFE Index Fund US $39,148.1 $36,923.1 $2,225.0

iShares MSCI Canada Index Fund US $6,486.7 $4,622.1 $1,864.6

iShares S&P MidCap 400 Index Fund US $11,193.7 $9,332.0 $1,861.7

iShares S&P/TSX 60 Index Fund Canada $13,474.2 $11,659.0 $1,815.2

db x-trackers DAX ETF Germany $5,201.2 $3,693.1 $1,508.1

iShares S&P 500 UK $9,267.7 $7,905.8 $1,361.9

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 60

http://w

ww.aijsh.org

iShares Russell 1000 Value Index Fund US $12,027.6 $10,697.1 $1,330.5

iShares MSCI Brazil Index Fund US $13,312.3 $12,012.5 $1,299.9

Market Vectors Russia ETF US $3,934.0 $2,638.5 $1,295.5

Vanguard Total Stock Market ETF US $19,527.1 $18,236.0 $1,291.1

Vanguard Dividend Appreciation ETF US $5,850.6 $4,608.9 $1,241.7

iShares S&P 500 Index Fund US $27,027.6 $25,799.2 $1,228.4

db x-trackers MSCI Emerging Market TRN Index ETF

Germany $5,068.8 $6,263.3 -$1,194.5

iShares iBoxx $ High Yield Corporate Bond Fund

US $8,561.5 $7,376.7 $1,184.8

Source: ETF Landscape – Global Handbook, Black Rock, H1 2011.

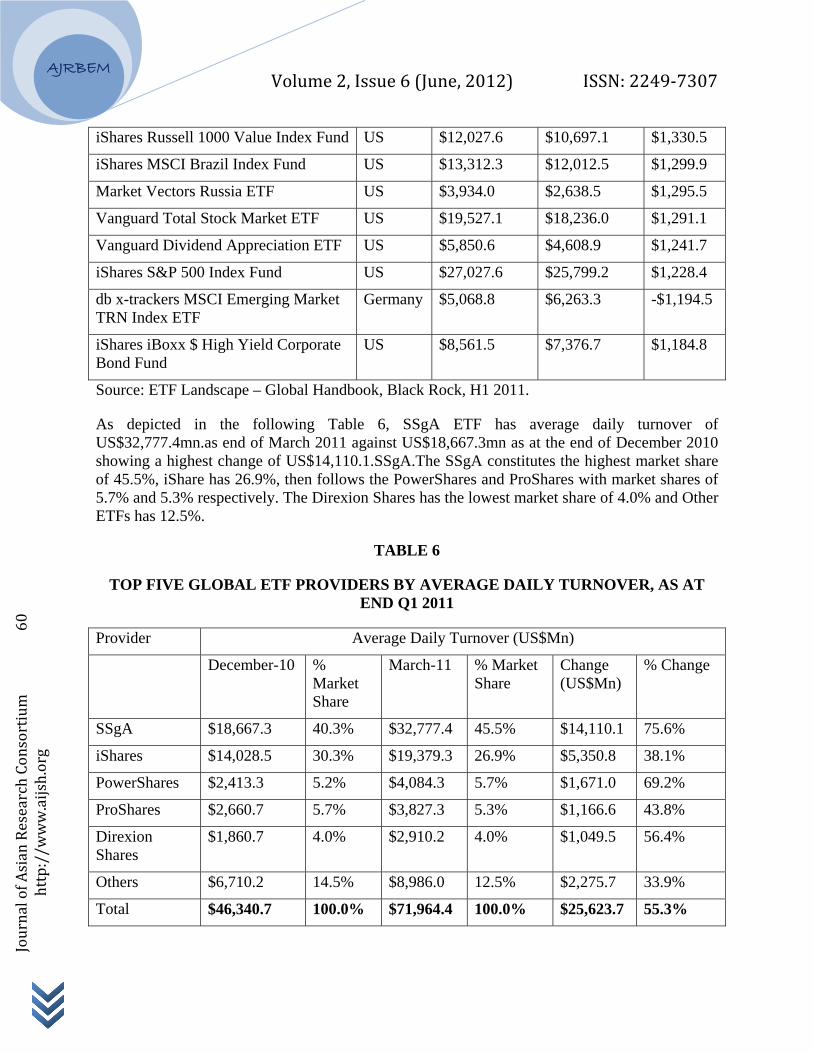

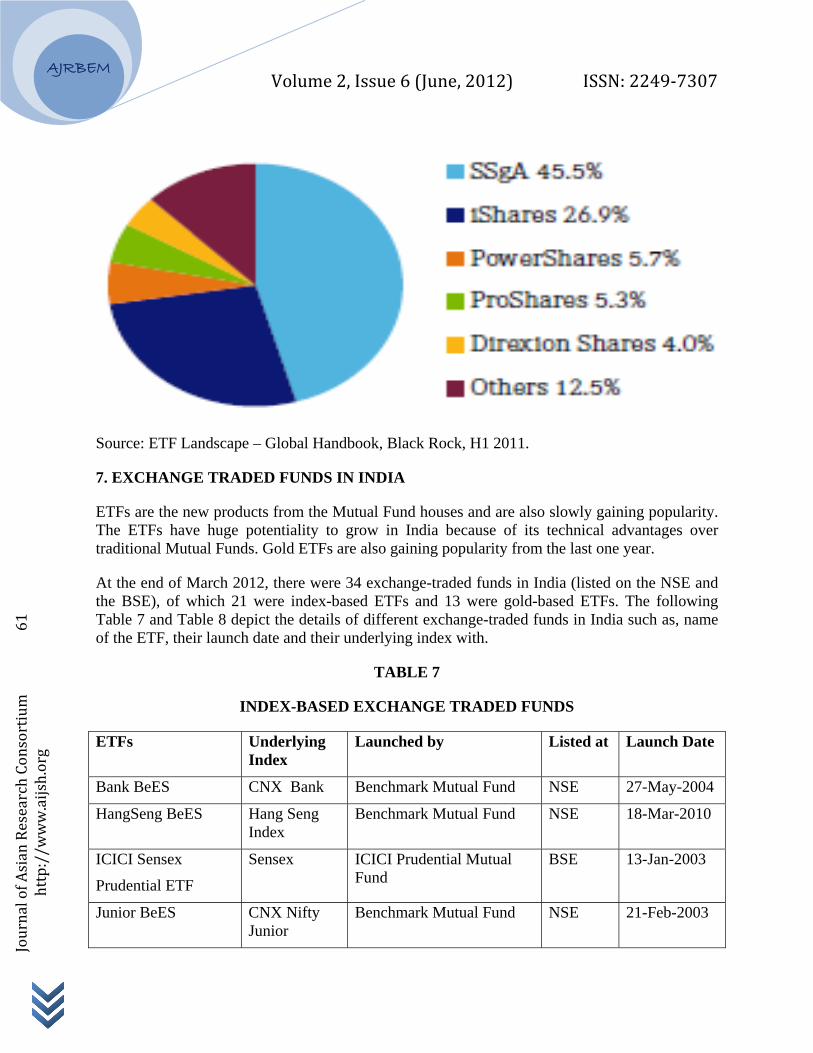

As depicted in the following Table 6, SSgA ETF has average daily turnover of US$32,777.4mn.as end of March 2011 against US$18,667.3mn as at the end of December 2010 showing a highest change of US$14,110.1.SSgA.The SSgA constitutes the highest market share of 45.5%, iShare has 26.9%, then follows the PowerShares and ProShares with market shares of 5.7% and 5.3% respectively. The Direxion Shares has the lowest market share of 4.0% and Other ETFs has 12.5%.

TABLE 6

TOP FIVE GLOBAL ETF PROVIDERS BY AVERAGE DAILY TURNOVER, AS AT END Q1 2011

Provider Average Daily Turnover (US$Mn)

December-10 % Market Share

March-11 % Market Share

Change (US$Mn)

% Change

SSgA $18,667.3 40.3% $32,777.4 45.5% $14,110.1 75.6%

iShares $14,028.5 30.3% $19,379.3 26.9% $5,350.8 38.1%

PowerShares $2,413.3 5.2% $4,084.3 5.7% $1,671.0 69.2%

ProShares $2,660.7 5.7% $3,827.3 5.3% $1,166.6 43.8%

Direxion Shares

$1,860.7 4.0% $2,910.2 4.0% $1,049.5 56.4%

Others $6,710.2 14.5% $8,986.0 12.5% $2,275.7 33.9%

Total $46,340.7 100.0% $71,964.4 100.0% $25,623.7 55.3%

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 61

http://w

ww.aijsh.org

Source: ETF Landscape – Global Handbook, Black Rock, H1 2011.

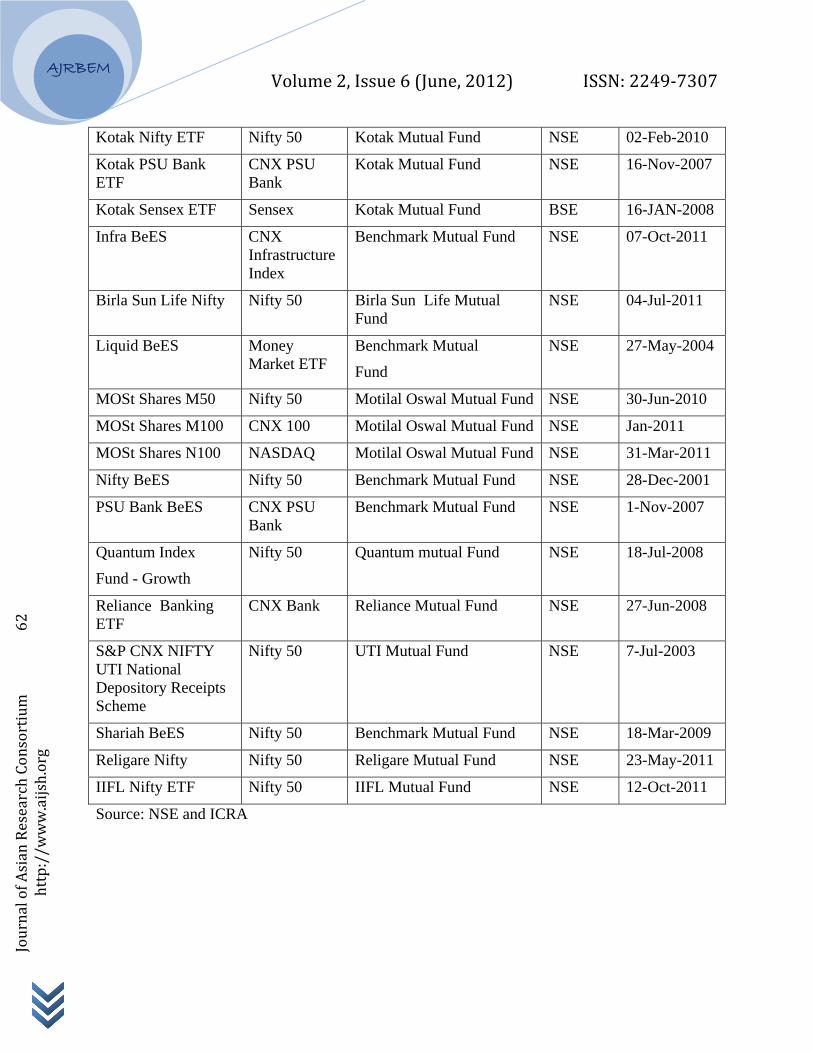

7. EXCHANGE TRADED FUNDS IN INDIA

ETFs are the new products from the Mutual Fund houses and are also slowly gaining popularity. The ETFs have huge potentiality to grow in India because of its technical advantages over traditional Mutual Funds. Gold ETFs are also gaining popularity from the last one year.

At the end of March 2012, there were 34 exchange-traded funds in India (listed on the NSE and the BSE), of which 21 were index-based ETFs and 13 were gold-based ETFs. The following Table 7 and Table 8 depict the details of different exchange-traded funds in India such as, name of the ETF, their launch date and their underlying index with.

TABLE 7

INDEX-BASED EXCHANGE TRADED FUNDS

ETFs Underlying Index

Launched by Listed at Launch Date

Bank BeES CNX Bank Benchmark Mutual Fund NSE 27-May-2004

HangSeng BeES Hang Seng Index

Benchmark Mutual Fund NSE 18-Mar-2010

ICICI Sensex

Prudential ETF

Sensex ICICI Prudential Mutual Fund

BSE 13-Jan-2003

Junior BeES CNX Nifty Junior

Benchmark Mutual Fund NSE 21-Feb-2003

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 62

http://w

ww.aijsh.org

Kotak Nifty ETF Nifty 50 Kotak Mutual Fund NSE 02-Feb-2010

Kotak PSU Bank ETF

CNX PSU Bank

Kotak Mutual Fund NSE 16-Nov-2007

Kotak Sensex ETF Sensex Kotak Mutual Fund BSE 16-JAN-2008

Infra BeES CNX Infrastructure Index

Benchmark Mutual Fund NSE 07-Oct-2011

Birla Sun Life Nifty Nifty 50 Birla Sun Life Mutual Fund

NSE 04-Jul-2011

Liquid BeES Money Market ETF

Benchmark Mutual

Fund

NSE 27-May-2004

MOSt Shares M50 Nifty 50 Motilal Oswal Mutual Fund NSE 30-Jun-2010

MOSt Shares M100 CNX 100 Motilal Oswal Mutual Fund NSE Jan-2011

MOSt Shares N100 NASDAQ Motilal Oswal Mutual Fund NSE 31-Mar-2011

Nifty BeES Nifty 50 Benchmark Mutual Fund NSE 28-Dec-2001

PSU Bank BeES CNX PSU Bank

Benchmark Mutual Fund NSE 1-Nov-2007

Quantum Index

Fund - Growth

Nifty 50 Quantum mutual Fund NSE 18-Jul-2008

Reliance Banking ETF

CNX Bank Reliance Mutual Fund NSE 27-Jun-2008

S&P CNX NIFTY UTI National Depository Receipts Scheme

Nifty 50 UTI Mutual Fund NSE 7-Jul-2003

Shariah BeES Nifty 50 Benchmark Mutual Fund NSE 18-Mar-2009

Religare Nifty Nifty 50 Religare Mutual Fund NSE 23-May-2011

IIFL Nifty ETF Nifty 50 IIFL Mutual Fund NSE 12-Oct-2011

Source: NSE and ICRA

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 63

http://w

ww.aijsh.org

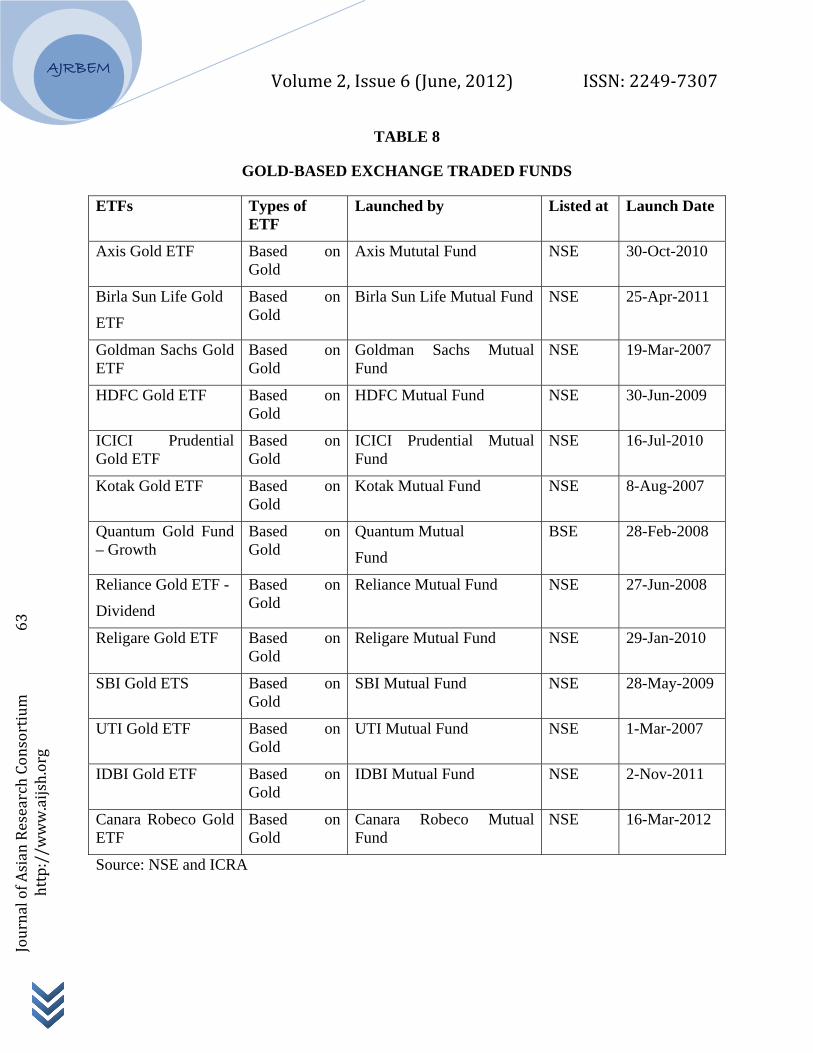

TABLE 8

GOLD-BASED EXCHANGE TRADED FUNDS

ETFs Types of ETF

Launched by Listed at Launch Date

Axis Gold ETF Based on Gold

Axis Mututal Fund NSE 30-Oct-2010

Birla Sun Life Gold

ETF

Based on Gold

Birla Sun Life Mutual Fund NSE 25-Apr-2011

Goldman Sachs Gold ETF

Based on Gold

Goldman Sachs Mutual Fund

NSE 19-Mar-2007

HDFC Gold ETF Based on Gold

HDFC Mutual Fund NSE 30-Jun-2009

ICICI Prudential Gold ETF

Based on Gold

ICICI Prudential Mutual Fund

NSE 16-Jul-2010

Kotak Gold ETF Based on Gold

Kotak Mutual Fund NSE 8-Aug-2007

Quantum Gold Fund – Growth

Based on Gold

Quantum Mutual

Fund

BSE 28-Feb-2008

Reliance Gold ETF -

Dividend

Based on Gold

Reliance Mutual Fund NSE 27-Jun-2008

Religare Gold ETF Based on Gold

Religare Mutual Fund NSE 29-Jan-2010

SBI Gold ETS Based on Gold

SBI Mutual Fund NSE 28-May-2009

UTI Gold ETF Based on Gold

UTI Mutual Fund NSE 1-Mar-2007

IDBI Gold ETF Based on Gold

IDBI Mutual Fund NSE 2-Nov-2011

Canara Robeco Gold ETF

Based on Gold

Canara Robeco Mutual Fund

NSE 16-Mar-2012

Source: NSE and ICRA

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 64

http://w

ww.aijsh.org

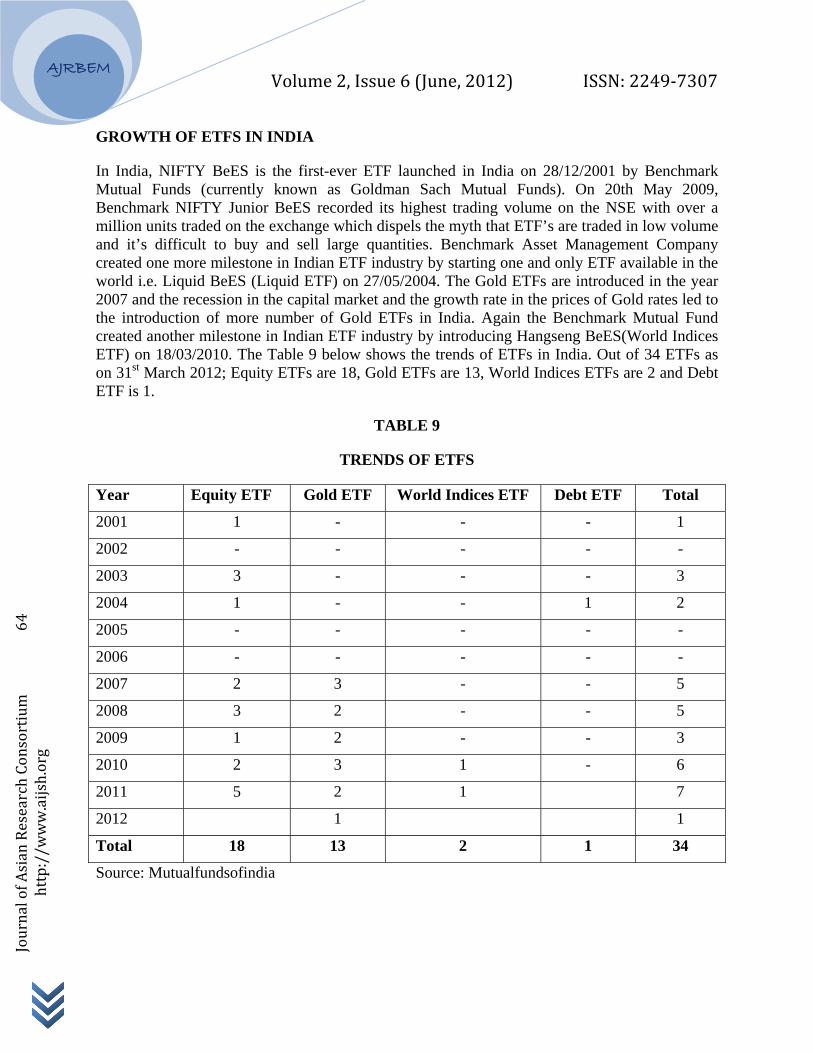

GROWTH OF ETFS IN INDIA

In India, NIFTY BeES is the first-ever ETF launched in India on 28/12/2001 by Benchmark Mutual Funds (currently known as Goldman Sach Mutual Funds). On 20th May 2009, Benchmark NIFTY Junior BeES recorded its highest trading volume on the NSE with over a million units traded on the exchange which dispels the myth that ETF’s are traded in low volume and it’s difficult to buy and sell large quantities. Benchmark Asset Management Company created one more milestone in Indian ETF industry by starting one and only ETF available in the world i.e. Liquid BeES (Liquid ETF) on 27/05/2004. The Gold ETFs are introduced in the year 2007 and the recession in the capital market and the growth rate in the prices of Gold rates led to the introduction of more number of Gold ETFs in India. Again the Benchmark Mutual Fund created another milestone in Indian ETF industry by introducing Hangseng BeES(World Indices ETF) on 18/03/2010. The Table 9 below shows the trends of ETFs in India. Out of 34 ETFs as on 31st March 2012; Equity ETFs are 18, Gold ETFs are 13, World Indices ETFs are 2 and Debt ETF is 1.

TABLE 9

TRENDS OF ETFS

Year Equity ETF Gold ETF World Indices ETF Debt ETF Total

2001 1 - - - 1

2002 - - - - -

2003 3 - - - 3

2004 1 - - 1 2

2005 - - - - -

2006 - - - - -

2007 2 3 - - 5

2008 3 2 - - 5

2009 1 2 - - 3

2010 2 3 1 - 6

2011 5 2 1 7

2012 1 1

Total 18 13 2 1 34

Source: Mutualfundsofindia

AJRB

Journal of Asian Research Consortium 65

http://w

ww.aijsh.org

BEM

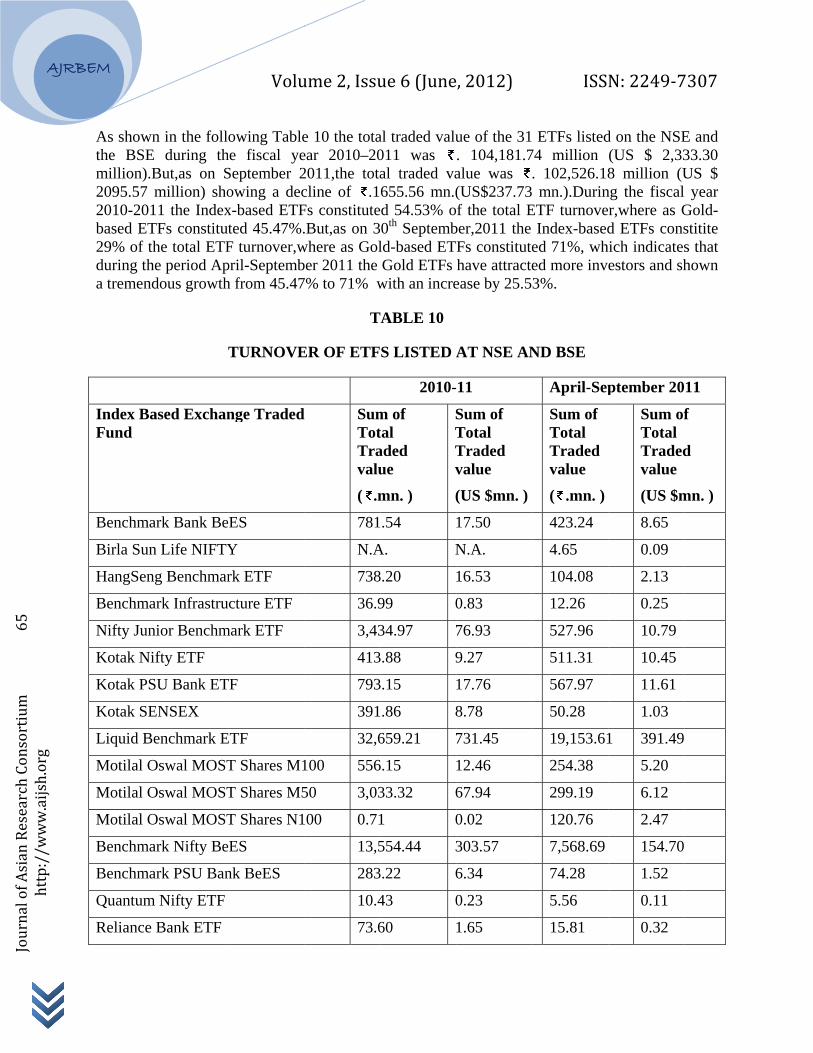

As shownthe BSEmillion).B2095.57 2010-201based ET29% of tduring tha tremend

Index BaFund

Benchma

Birla Sun

HangSen

Benchma

Nifty Jun

Kotak Ni

Kotak PS

Kotak SE

Liquid B

Motilal O

Motilal O

Motilal O

Benchma

Benchma

Quantum

Reliance

n in the follE during thBut,as on Smillion) sho

11 the IndexTFs constitutthe total ETFhe period Apdous growth

ased Exchan

ark Bank Be

n Life NIFTY

ng Benchmar

ark Infrastru

nior Benchm

ifty ETF

SU Bank ET

ENSEX

Benchmark E

Oswal MOST

Oswal MOST

Oswal MOST

ark Nifty Be

ark PSU Ban

m Nifty ETF

Bank ETF

Volu

owing Tablehe fiscal yeSeptember 2owing a decx-based ETFted 45.47%.F turnover,wpril-Septembh from 45.47

TURNOVE

nge Traded

eES

Y

rk ETF

ucture ETF

mark ETF

TF

ETF

T Shares M1

T Shares M5

T Shares N1

eES

nk BeES

ume 2, Issu

e 10 the totaear 2010–202011,the totacline of .1Fs constitute.But,as on 3

where as Golber 2011 the 7% to 71% w

T

ER OF ETF

d SumTotTravalu

( .m

781

N.A

738

36.9

3,43

413

793

391

32,6

100 556

50 3,03

00 0.71

13,5

283

10.4

73.6

ue 6 (June

al traded valu011 was al traded va655.56 mn.(d 54.53% o0th Septembld-based ETGold ETFs

with an incre

ABLE 10

S LISTED A

2010-

m of tal aded ue

mn. )

STTv

(

.54

A. N

8.20

99 0

34.97 7

.88 9

.15

.86 8

659.21 7

6.15

33.32 6

1 0

554.44 3

.22 6

43 0

60

, 2012)

ue of the 31. 104,181.7alue was (US$237.73f the total E

ber,2011 the Fs constitutehave attracte

ease by 25.5

AT NSE AN

-11

Sum of Total Traded value

(US $mn. )

17.50

N.A.

16.53

0.83

76.93

9.27

17.76

8.78

731.45

12.46

67.94

0.02

303.57

6.34

0.23

1.65

ISS

ETFs listed74 million . 102,526.18 mn.).Durin

ETF turnoveIndex-based

ed 71%, whed more inv3%.

ND BSE

April-Sep

Sum of Total Traded value

( .mn. )

423.24

4.65

104.08

12.26

527.96

511.31

567.97

50.28

19,153.61

254.38

299.19

120.76

7,568.69

74.28

5.56

15.81

N: 2249‐7

d on the NSE(US $ 2,338 million (U

ng the fiscal r,where as Gd ETFs cons

hich indicatesestors and sh

ptember 20

Sum ofTotal Tradedvalue

(US $m

8.65

0.09

2.13

0.25

10.79

10.45

11.61

1.03

1 391.49

5.20

6.12

2.47

154.70

1.52

0.11

0.32

7307

E and 33.30 US $ year Gold-stitite s that hown

11

f

d

mn. )

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 66

http://w

ww.aijsh.org

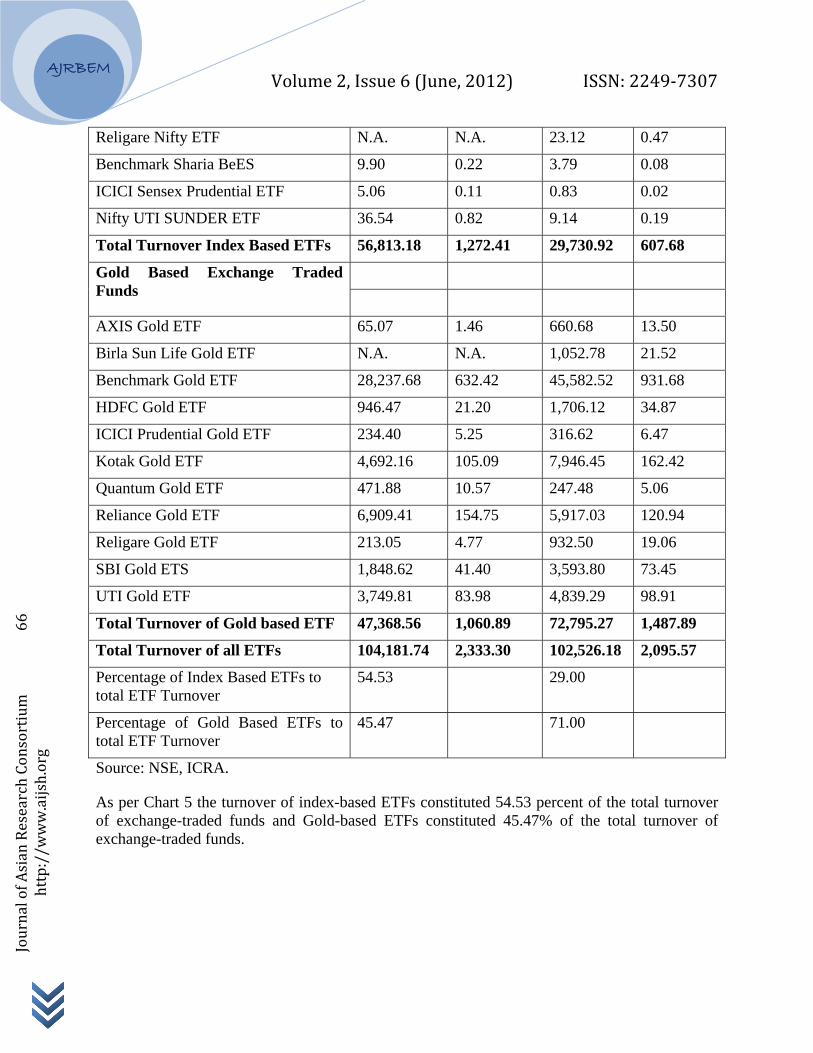

Religare Nifty ETF N.A. N.A. 23.12 0.47

Benchmark Sharia BeES 9.90 0.22 3.79 0.08

ICICI Sensex Prudential ETF 5.06 0.11 0.83 0.02

Nifty UTI SUNDER ETF 36.54 0.82 9.14 0.19

Total Turnover Index Based ETFs 56,813.18 1,272.41 29,730.92 607.68

Gold Based Exchange Traded Funds

AXIS Gold ETF 65.07 1.46 660.68 13.50

Birla Sun Life Gold ETF N.A. N.A. 1,052.78 21.52

Benchmark Gold ETF 28,237.68 632.42 45,582.52 931.68

HDFC Gold ETF 946.47 21.20 1,706.12 34.87

ICICI Prudential Gold ETF 234.40 5.25 316.62 6.47

Kotak Gold ETF 4,692.16 105.09 7,946.45 162.42

Quantum Gold ETF 471.88 10.57 247.48 5.06

Reliance Gold ETF 6,909.41 154.75 5,917.03 120.94

Religare Gold ETF 213.05 4.77 932.50 19.06

SBI Gold ETS 1,848.62 41.40 3,593.80 73.45

UTI Gold ETF 3,749.81 83.98 4,839.29 98.91

Total Turnover of Gold based ETF 47,368.56 1,060.89 72,795.27 1,487.89

Total Turnover of all ETFs 104,181.74 2,333.30 102,526.18 2,095.57

Percentage of Index Based ETFs to total ETF Turnover

54.53 29.00

Percentage of Gold Based ETFs to total ETF Turnover

45.47 71.00

Source: NSE, ICRA.

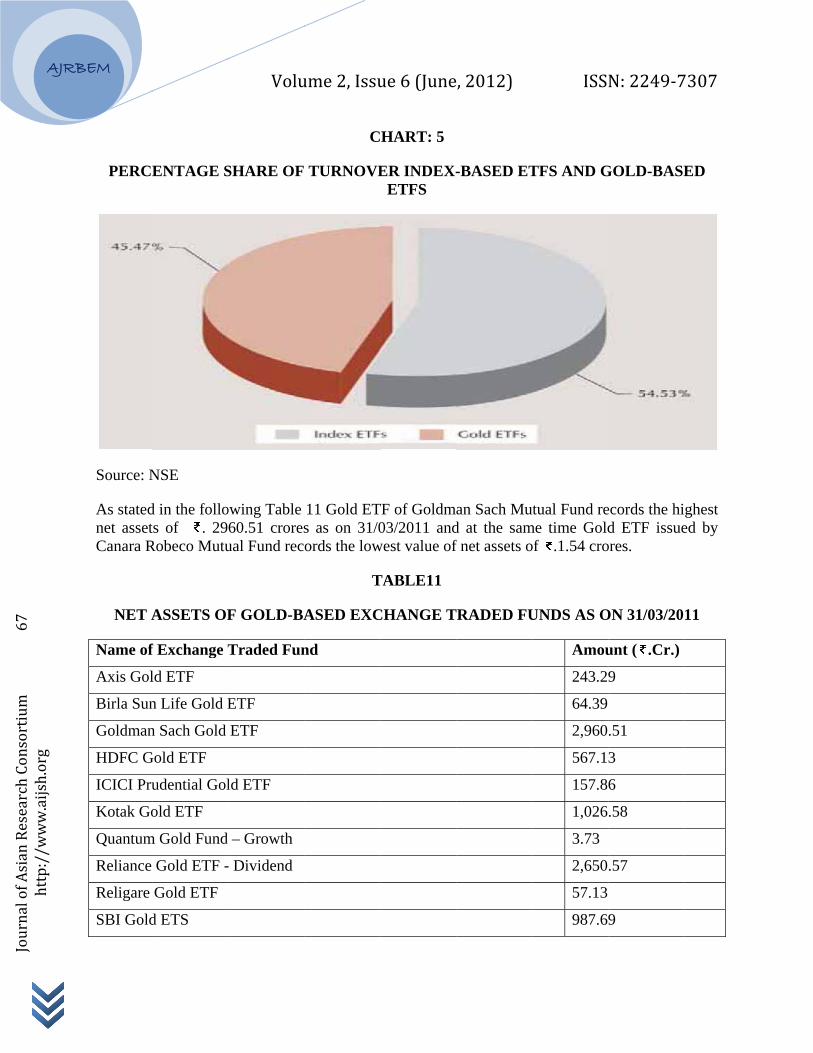

As per Chart 5 the turnover of index-based ETFs constituted 54.53 percent of the total turnover of exchange-traded funds and Gold-based ETFs constituted 45.47% of the total turnover of exchange-traded funds.

AJRB

Journal of Asian Research Consortium 67

http://w

ww.aijsh.org

BEM

PERC

Source: N

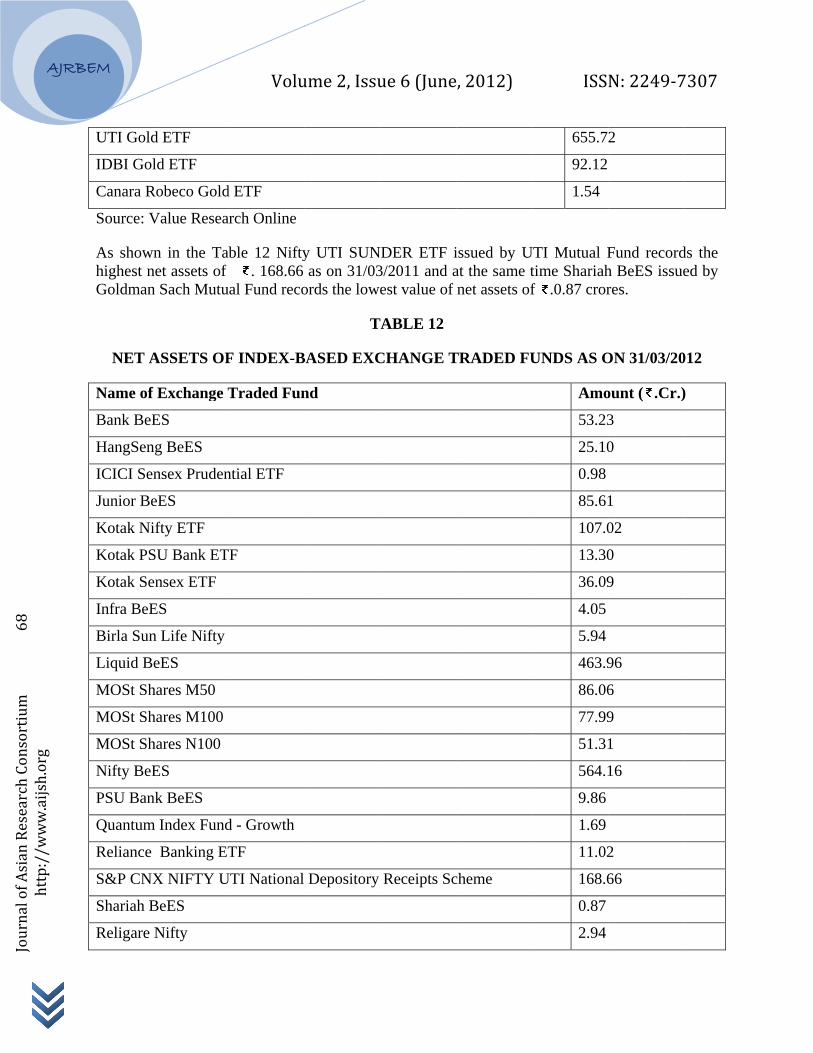

As statednet assetCanara R

NET A

Name of

Axis Gol

Birla Sun

Goldman

HDFC G

ICICI Pru

Kotak Go

Quantum

Reliance

Religare

SBI Gold

ENTAGE S

NSE

d in the follots of . 29Robeco Mutu

ASSETS OF

f Exchange T

ld ETF

n Life Gold E

n Sach Gold

Gold ETF

udential Gol

old ETF

m Gold Fund

Gold ETF -

Gold ETF

d ETS

Volu

SHARE OF

owing Table 60.51 croresual Fund rec

F GOLD-BA

Traded Fun

ETF

ETF

ld ETF

– Growth

- Dividend

ume 2, Issu

C

TURNOVE

11 Gold ETs as on 31/0ords the low

T

ASED EXC

nd

ue 6 (June

HART: 5

ER INDEX-ETFS

TF of Goldm03/2011 and

west value of

TABLE11

CHANGE T

, 2012)

-BASED ET

an Sach Mud at the samf net assets o

RADED FU

ISS

TFS AND G

utual Fund reme time Goldof .1.54 cro

UNDS AS O

Amou

243.2

64.39

2,960

567.1

157.8

1,026

3.73

2,650

57.13

987.6

N: 2249‐7

GOLD-BASE

ecords the hid ETF issue

ores.

ON 31/03/20

unt ( .Cr.)

9

.51

3

6

.58

.57

9

7307

ED

ghest ed by

11

AJRB

Journal of Asian Research Consortium 68

http://w

ww.aijsh.org

BEM

UTI Gold

IDBI Go

Canara R

Source: V

As showhighest nGoldman

NET A

Name of

Bank BeE

HangSen

ICICI Se

Junior Be

Kotak Ni

Kotak PS

Kotak Se

Infra BeE

Birla Sun

Liquid B

MOSt Sh

MOSt Sh

MOSt Sh

Nifty BeE

PSU Ban

Quantum

Reliance

S&P CN

Shariah B

Religare

d ETF

ld ETF

Robeco Gold

Value Resea

wn in the Tanet assets of n Sach Mutu

ASSETS OF

f Exchange T

ES

ng BeES

ensex Pruden

eES

ifty ETF

SU Bank ET

ensex ETF

ES

n Life Nifty

BeES

hares M50

hares M100

hares N100

ES

nk BeES

m Index Fund

Banking ET

X NIFTY U

BeES

Nifty

Volu

d ETF

arch Online

able 12 Nifty . 168.66

ual Fund reco

F INDEX-B

Traded Fun

ntial ETF

TF

d - Growth

TF

UTI National

ume 2, Issu

y UTI SUNas on 31/03

ords the lowe

T

BASED EXC

nd

Depository

ue 6 (June

NDER ETF i3/2011 and aest value of

ABLE 12

CHANGE T

Receipts Sc

, 2012)

issued by Uat the same tnet assets of

TRADED FU

cheme

ISS

655.72

92.12

1.54

UTI Mutual Ftime Shariahf .0.87 cror

UNDS AS O

Amo

53.23

25.10

0.98

85.61

107.0

13.30

36.09

4.05

5.94

463.9

86.06

77.99

51.31

564.1

9.86

1.69

11.02

168.6

0.87

2.94

N: 2249‐7

2

Fund recordh BeES issueres.

ON 31/03/20

ount ( .Cr.)

3

0

1

02

0

9

96

6

9

1

16

2

66

7307

ds the ed by

012

)

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 69

http://w

ww.aijsh.org

IIFL Nifty ETF 28.22

Source: Value Research Online

8. PERFORMANCE EVALUATION OF INDEX BASED ETFS VIS-À-VIS GOLD BASED ETFS

The performance evaluation of ETFs and Index Funds is made with the help of select parameters viz., Return, Risk and Expenses Ratio.

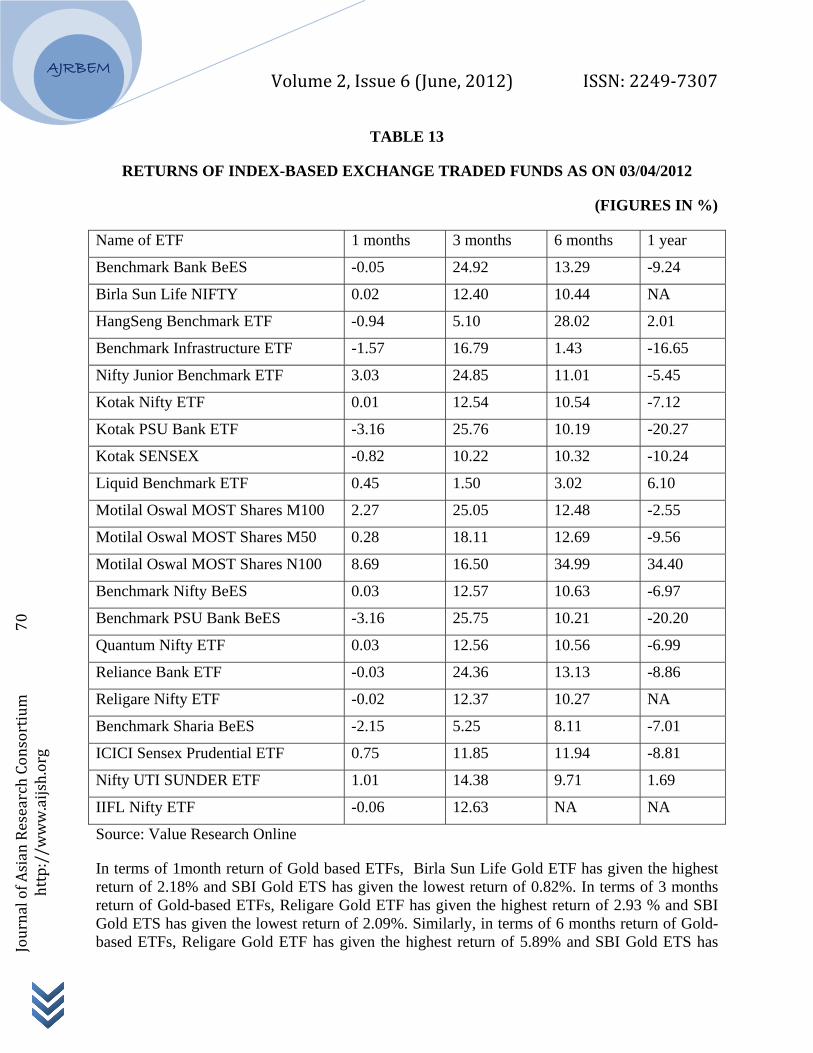

RETURNS OF ETFS IN INDIA

Performance of ETFs in terms of returns measures both the short term performance and long term performance. The short term performance is expressed in terms of 1month return, 3months return and 6 months return whereas, the long term performance is expressed in terms of 1 year return. In terms of 1month return of index-based ETFs, MOST Shares N100 ETF issued by Motilal Oswal Mutual Fund has given the highest return of 8.69% and Kotak PSU Bank ETF of Kotak Mahindra Mutual Fund and PSU Bank BeES ETF of Goldman Sach Mutual Fund have given the lowest return of -3.16%. In terms of 3 months return of index-based ETFs, Kotak PSU Bank ETF of Kotak Mahindra Mutual Fund has given the highest return of 25.76 % and Liquid Benchmark ETF of Goldman Sach Mutual Fund has given the lowest return of 1.50%. Similarly, in terms of 6 months return of index-based ETFs, Motilal Oswal MOST Shares N100 has given the highest return of 34.99 % and Benchmark Infrastructure ETF of Goldman Sach Mutual Fund has given the lowest return of 1.43%.So far as long term performance is concerned, except three ETFs such as HangSeng Benchmark ETF, Liquid Benchmark ETF and Motilal Oswal MOST Shares N100 all other ETFs have negative performance. Motilal Oswal MOST Shares N100 has given the highest return of 34.40 in terms of 1 year return and Benchmark Bank BeES of Goldman Sach Mutual Funds has given the highest negative return of -9.24 in terms of longterm performance.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 70

http://w

ww.aijsh.org

TABLE 13

RETURNS OF INDEX-BASED EXCHANGE TRADED FUNDS AS ON 03/04/2012

(FIGURES IN %)

Name of ETF 1 months 3 months 6 months 1 year

Benchmark Bank BeES -0.05 24.92 13.29 -9.24

Birla Sun Life NIFTY 0.02 12.40 10.44 NA

HangSeng Benchmark ETF -0.94 5.10 28.02 2.01

Benchmark Infrastructure ETF -1.57 16.79 1.43 -16.65

Nifty Junior Benchmark ETF 3.03 24.85 11.01 -5.45

Kotak Nifty ETF 0.01 12.54 10.54 -7.12

Kotak PSU Bank ETF -3.16 25.76 10.19 -20.27

Kotak SENSEX -0.82 10.22 10.32 -10.24

Liquid Benchmark ETF 0.45 1.50 3.02 6.10

Motilal Oswal MOST Shares M100 2.27 25.05 12.48 -2.55

Motilal Oswal MOST Shares M50 0.28 18.11 12.69 -9.56

Motilal Oswal MOST Shares N100 8.69 16.50 34.99 34.40

Benchmark Nifty BeES 0.03 12.57 10.63 -6.97

Benchmark PSU Bank BeES -3.16 25.75 10.21 -20.20

Quantum Nifty ETF 0.03 12.56 10.56 -6.99

Reliance Bank ETF -0.03 24.36 13.13 -8.86

Religare Nifty ETF -0.02 12.37 10.27 NA

Benchmark Sharia BeES -2.15 5.25 8.11 -7.01

ICICI Sensex Prudential ETF 0.75 11.85 11.94 -8.81

Nifty UTI SUNDER ETF 1.01 14.38 9.71 1.69

IIFL Nifty ETF -0.06 12.63 NA NA

Source: Value Research Online

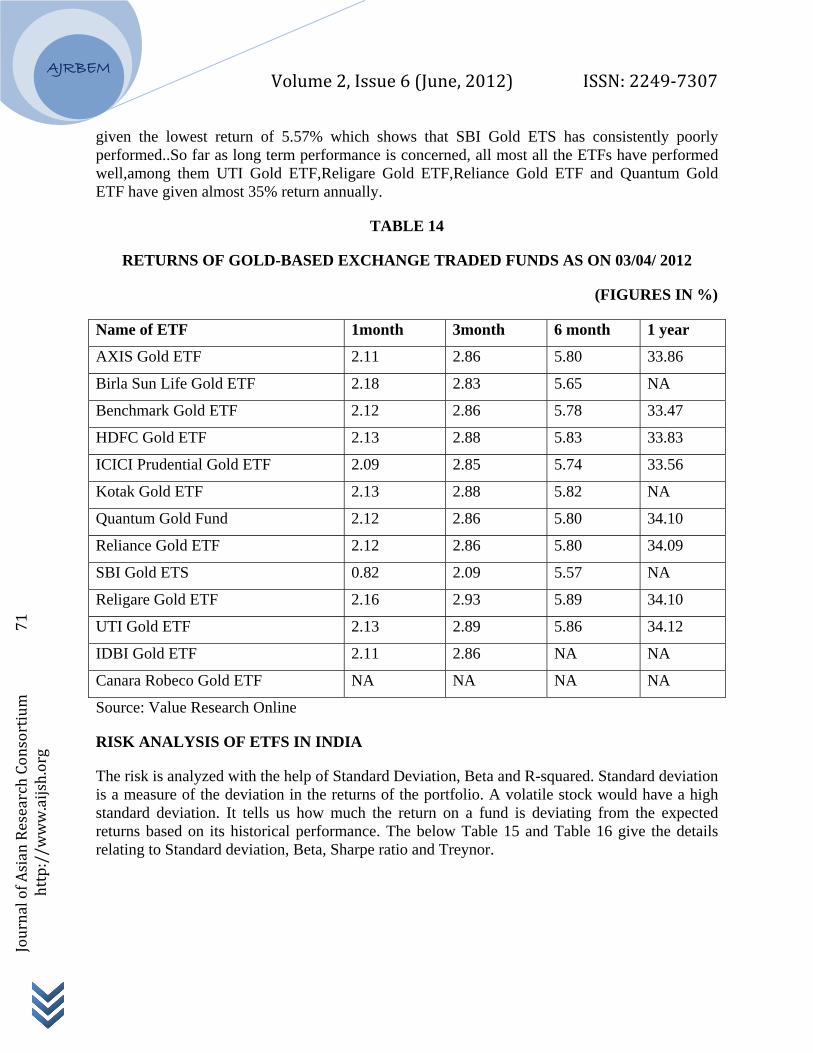

In terms of 1month return of Gold based ETFs, Birla Sun Life Gold ETF has given the highest return of 2.18% and SBI Gold ETS has given the lowest return of 0.82%. In terms of 3 months return of Gold-based ETFs, Religare Gold ETF has given the highest return of 2.93 % and SBI Gold ETS has given the lowest return of 2.09%. Similarly, in terms of 6 months return of Gold-based ETFs, Religare Gold ETF has given the highest return of 5.89% and SBI Gold ETS has

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 71

http://w

ww.aijsh.org

given the lowest return of 5.57% which shows that SBI Gold ETS has consistently poorly performed..So far as long term performance is concerned, all most all the ETFs have performed well,among them UTI Gold ETF,Religare Gold ETF,Reliance Gold ETF and Quantum Gold ETF have given almost 35% return annually.

TABLE 14

RETURNS OF GOLD-BASED EXCHANGE TRADED FUNDS AS ON 03/04/ 2012

(FIGURES IN %)

Name of ETF 1month 3month 6 month 1 year

AXIS Gold ETF 2.11 2.86 5.80 33.86

Birla Sun Life Gold ETF 2.18 2.83 5.65 NA

Benchmark Gold ETF 2.12 2.86 5.78 33.47

HDFC Gold ETF 2.13 2.88 5.83 33.83

ICICI Prudential Gold ETF 2.09 2.85 5.74 33.56

Kotak Gold ETF 2.13 2.88 5.82 NA

Quantum Gold Fund 2.12 2.86 5.80 34.10

Reliance Gold ETF 2.12 2.86 5.80 34.09

SBI Gold ETS 0.82 2.09 5.57 NA

Religare Gold ETF 2.16 2.93 5.89 34.10

UTI Gold ETF 2.13 2.89 5.86 34.12

IDBI Gold ETF 2.11 2.86 NA NA

Canara Robeco Gold ETF NA NA NA NA

Source: Value Research Online

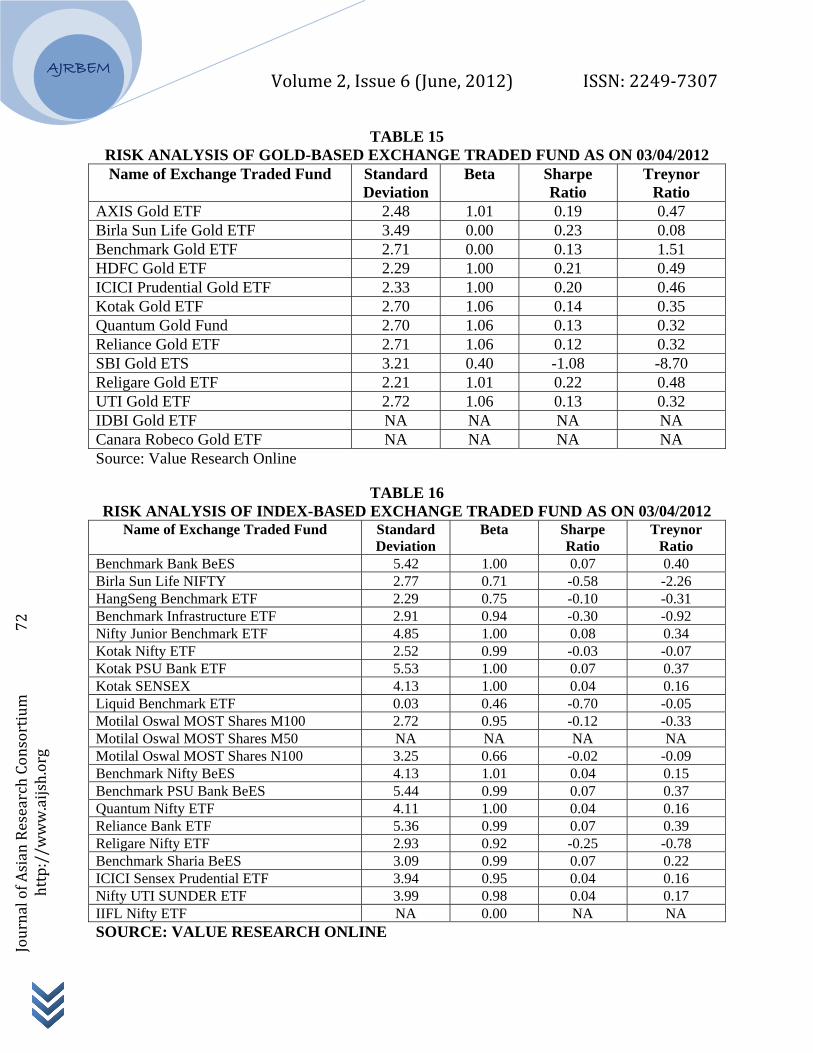

RISK ANALYSIS OF ETFS IN INDIA

The risk is analyzed with the help of Standard Deviation, Beta and R-squared. Standard deviation is a measure of the deviation in the returns of the portfolio. A volatile stock would have a high standard deviation. It tells us how much the return on a fund is deviating from the expected returns based on its historical performance. The below Table 15 and Table 16 give the details relating to Standard deviation, Beta, Sharpe ratio and Treynor.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 72

http://w

ww.aijsh.org

TABLE 15 RISK ANALYSIS OF GOLD-BASED EXCHANGE TRADED FUND AS ON 03/04/2012 Name of Exchange Traded Fund Standard

Deviation Beta Sharpe

Ratio Treynor

Ratio AXIS Gold ETF 2.48 1.01 0.19 0.47 Birla Sun Life Gold ETF 3.49 0.00 0.23 0.08 Benchmark Gold ETF 2.71 0.00 0.13 1.51 HDFC Gold ETF 2.29 1.00 0.21 0.49 ICICI Prudential Gold ETF 2.33 1.00 0.20 0.46 Kotak Gold ETF 2.70 1.06 0.14 0.35 Quantum Gold Fund 2.70 1.06 0.13 0.32 Reliance Gold ETF 2.71 1.06 0.12 0.32 SBI Gold ETS 3.21 0.40 -1.08 -8.70 Religare Gold ETF 2.21 1.01 0.22 0.48 UTI Gold ETF 2.72 1.06 0.13 0.32 IDBI Gold ETF NA NA NA NA Canara Robeco Gold ETF NA NA NA NA Source: Value Research Online

TABLE 16 RISK ANALYSIS OF INDEX-BASED EXCHANGE TRADED FUND AS ON 03/04/2012

Name of Exchange Traded Fund Standard Deviation

Beta Sharpe Ratio

Treynor Ratio

Benchmark Bank BeES 5.42 1.00 0.07 0.40 Birla Sun Life NIFTY 2.77 0.71 -0.58 -2.26 HangSeng Benchmark ETF 2.29 0.75 -0.10 -0.31 Benchmark Infrastructure ETF 2.91 0.94 -0.30 -0.92 Nifty Junior Benchmark ETF 4.85 1.00 0.08 0.34 Kotak Nifty ETF 2.52 0.99 -0.03 -0.07 Kotak PSU Bank ETF 5.53 1.00 0.07 0.37 Kotak SENSEX 4.13 1.00 0.04 0.16 Liquid Benchmark ETF 0.03 0.46 -0.70 -0.05 Motilal Oswal MOST Shares M100 2.72 0.95 -0.12 -0.33 Motilal Oswal MOST Shares M50 NA NA NA NA Motilal Oswal MOST Shares N100 3.25 0.66 -0.02 -0.09 Benchmark Nifty BeES 4.13 1.01 0.04 0.15 Benchmark PSU Bank BeES 5.44 0.99 0.07 0.37 Quantum Nifty ETF 4.11 1.00 0.04 0.16 Reliance Bank ETF 5.36 0.99 0.07 0.39 Religare Nifty ETF 2.93 0.92 -0.25 -0.78 Benchmark Sharia BeES 3.09 0.99 0.07 0.22 ICICI Sensex Prudential ETF 3.94 0.95 0.04 0.16 Nifty UTI SUNDER ETF 3.99 0.98 0.04 0.17 IIFL Nifty ETF NA 0.00 NA NA SOURCE: VALUE RESEARCH ONLINE

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 73

http://w

ww.aijsh.org

STANDARD DEVIATION

It is found that among the Gold-Based ETFs, Birla Sun Life Gold ETF is having the highest risk i.e. 3.49per cent and HDFC Gold ETF has the lowest risk i.e. 2.29 per cent. In the case of Index-Based ETF, Kotak PSU Bank ETF has the highest risk i.e., 5.53 per cent and Liquid Benchmark ETF has lowest risk i.e.0.03 per cent. The standard deviations of the Index-Based ETFs are higher than the Gold-Based ETFs. It means that the deviation of expected return is more in Index-Based ETFs than Gold-Based ETFs.

BETA VALUE

Beta measures the systematic risk and explains the nature of the volatility of the security return with that of the market return. If beta values are less than one, it means that Funds risk is less than the market risk; if it is one, it means the Funds risk is same as that of the market risk and if the beta is more than one, the risk of the Funds is greater than that of the market. Most of the Gold-Based ETFs have the beta values equal to 1 or more than 1, implying volatility in the returns of the ETFs is as same as that of the market or higher volatility in the returns of the ETFs. But, on the other hand, most of the Index-Based ETFs have the beta less than 1, implying lower volatility in the returns of the ETFs.

SHARPE RATIO

It shows the return to variability. Higher the ratio, better performance, in terms of the return for the risk taken. It is found that all the Gold-Based ETFs are showing a positive Sharpe ratio except SBI Gold ETS. But most of the Index-Based ETFs are showing negative Shrape ratio. According to Sharpe ratio, Gold ETFs are giving better performance for extra risk taken by the investors.

TREYNOR RATIO

This r ratio relates excess return over the risk-free rate to the additional risk taken; however, systematic risk is used instead of total risk. The higher the Treynor ratio, the better the performance of the portfolio under analysis. It is found that all the Gold-Based ETFs are showing positive Treynor ratio except SBI Gold ETS.But.most of Index-Based ETFs are showing negative Treynor ratio. According to Treynor ratio, Gold ETFs are giving better performance for extra market risk taken by the investors.

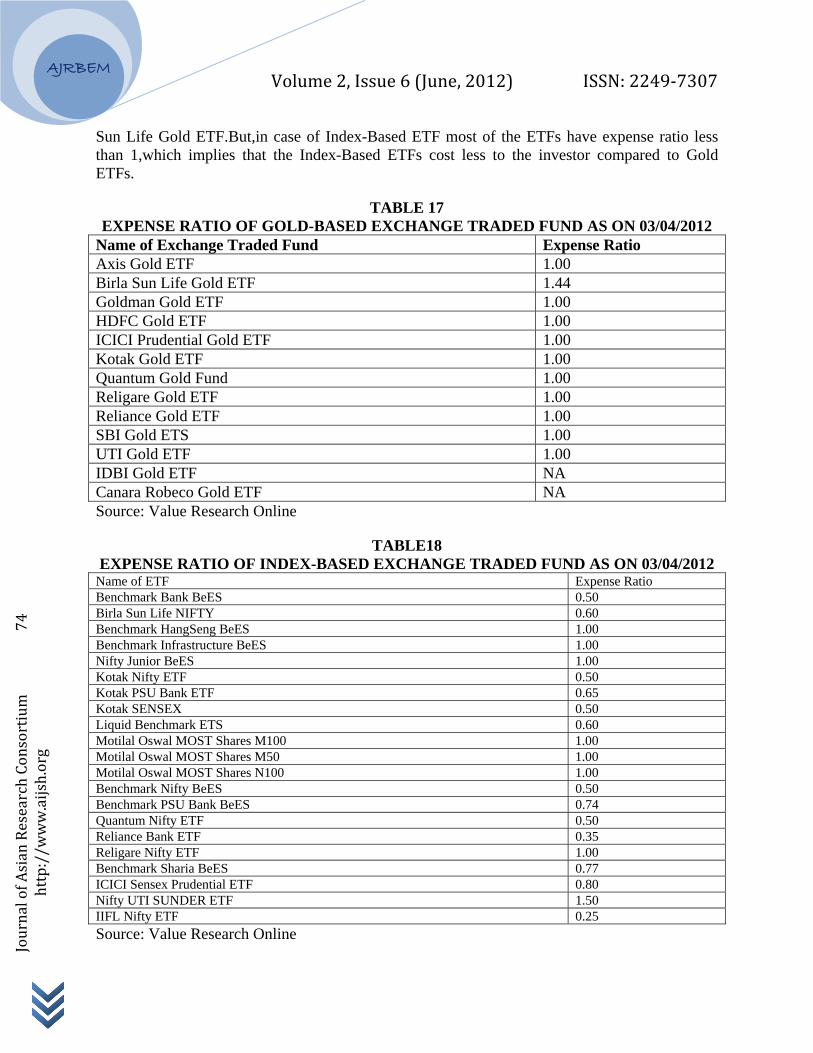

EXPENSES RATIO OF EXCHANGE TRADED FUNDS IN INDIA

An expense ratio tells as to how much a Fund costs. The amount is skimmed from the investors account and goes towards paying a Fund’s total annual expenses. It is expressed as a percentage of a Fund’s Net Assets. If an investor invests in an ETF with an expenses ratio of 0.20 per cent and has invested Rs.10, 000 in that fund, the investor has to pay Rs.20 a year in expenses. The tables below give the details of expenses ratio of the select schemes of ETFs as on 3rd April, 2012. It is found that almost all the Gold-Based ETFs have equal expense ratio except Birla Sun Life Gold ETF, which implies that all the Gold ETFs cost equally to the investor except Birla

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 74

http://w

ww.aijsh.org

Sun Life Gold ETF.But,in case of Index-Based ETF most of the ETFs have expense ratio less than 1,which implies that the Index-Based ETFs cost less to the investor compared to Gold ETFs.

TABLE 17 EXPENSE RATIO OF GOLD-BASED EXCHANGE TRADED FUND AS ON 03/04/2012

Name of Exchange Traded Fund Expense Ratio Axis Gold ETF 1.00 Birla Sun Life Gold ETF 1.44 Goldman Gold ETF 1.00 HDFC Gold ETF 1.00 ICICI Prudential Gold ETF 1.00 Kotak Gold ETF 1.00 Quantum Gold Fund 1.00 Religare Gold ETF 1.00 Reliance Gold ETF 1.00 SBI Gold ETS 1.00 UTI Gold ETF 1.00 IDBI Gold ETF NA Canara Robeco Gold ETF NA Source: Value Research Online

TABLE18 EXPENSE RATIO OF INDEX-BASED EXCHANGE TRADED FUND AS ON 03/04/2012

Name of ETF Expense Ratio Benchmark Bank BeES 0.50 Birla Sun Life NIFTY 0.60 Benchmark HangSeng BeES 1.00 Benchmark Infrastructure BeES 1.00 Nifty Junior BeES 1.00 Kotak Nifty ETF 0.50 Kotak PSU Bank ETF 0.65 Kotak SENSEX 0.50 Liquid Benchmark ETS 0.60 Motilal Oswal MOST Shares M100 1.00 Motilal Oswal MOST Shares M50 1.00 Motilal Oswal MOST Shares N100 1.00 Benchmark Nifty BeES 0.50 Benchmark PSU Bank BeES 0.74 Quantum Nifty ETF 0.50 Reliance Bank ETF 0.35 Religare Nifty ETF 1.00 Benchmark Sharia BeES 0.77 ICICI Sensex Prudential ETF 0.80 Nifty UTI SUNDER ETF 1.50 IIFL Nifty ETF 0.25 Source: Value Research Online

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 75

http://w

ww.aijsh.org

9. FINDINGS OF THE STUDY

1: ETFs have given better opportunity for the small investors in terms of diversified portfolio with a small amount of money. Benchmark AMC issued more number of ETFs than other AMCs.

2: All the ETFs have shown tremendous growth both globally and in India in the year 2011-12 compared to the year 2010-11.

2: Expense ratios of Gold ETFs are same. But compared to Index ETFs expense ratios of Gold ETFs are more. So, Index ETFs are cost less compared to Gold ETFs.

3: According to Treynor ratio, Gold ETFs are giving better performance for extra market risk taken by the investors compared to Index ETFs.

4: According to Sharpe ratio, Gold ETFs are giving better performance for extra risk taken by the investors compared to Index ETFs.

5: Most of the Gold-Based ETFs have the beta values equal to 1 or more than 1, implying volatility in the returns of the ETFs is as same as that of the market or higher volatility in the returns of the ETFs. But, on the other hand, most of the Index-Based ETFs have the beta less than 1, implying lower volatility in the returns of the ETFs.

10. CONCLUSION

ETFs are one of the most successful products introduced on exchanges in recent years. The ETFs are gaining popularity day by day compared to other forms of investments. The Asset Management Companies (AMCs) are putting their continuous efforts to innovate new ETF products. As the variety of financial indices is increasing, there has been a corresponding increase in the spectrum of ETF varieties available in the market. Due to recent increasing volatility in the equity markets the investment in gold has become the new ray of hope for investors. Therefore, there is a huge potentiality for the introduction of more gold ETF products in India. However, the ETFs can become a best investment alternative, provided, awareness is created among the investor.

REFERENCES

1: BlackRock-ETF Landscape Industry Review End Q1 2011.

2: Johnson, W. F. (2008). Tracking errors of exchange traded funds. Journal of Asset Management.

3: Kostovetsky, L. (2003). Index mutual funds and Exchange-traded funds: A comparison of two methods of passive investment. The Journal of Portfolio Management.

Volume 2, Issue 6 (June, 2012) ISSN: 2249‐7307

AJRBEM

Journal of Asian Research Consortium 76

http://w

ww.aijsh.org

4: Rompotis, G., G. (2009a). Performance and trading characteristics of iShares: An evaluation. The Icfai Journal of Applied Finance.

5: Rompotis, G., G. (2009b). Interfamily competition on index tracking: The case of the vanguard ETFs and index funds. Journal of Asset Management.

6: National Stock Exchanges of India Ltd.- Indian Securities Market A Review, Vol.XIV.2011.

7: Exchange Traded Funds-Challenging the Dominance of Mutual Funds-A Deloitte Research Report

WEBSITES

www.valurresearch.com

www.nseindia.com

www.bseindia.com

www.benchmarkfunds.com

www.amfiindia.com

www.mutualfundsindia.com

www.investiopedia.com