ASIAN DEVELOPMENT BANK · Bogor and Palembang Urban Development Project, Loan I 292-lNO: Eastern...

69

ASIAN DEVELOPMENT BANK PCR: INO 24068 11 PROJECT COMPLETION REPORT [ii 1:1 CENTRAL JAVA AND Di. YOGYAKARTA URBAN DEVELOPMENT (SECTOR) PROJECT (Loan No. 1198-INO) Ii II I 'I.] I,i May 2000

Transcript of ASIAN DEVELOPMENT BANK · Bogor and Palembang Urban Development Project, Loan I 292-lNO: Eastern...

ASIAN DEVELOPMENT BANK PCR: INO 24068

11

PROJECT COMPLETION REPORT

[ii 1:1

CENTRAL JAVA AND Di. YOGYAKARTAURBAN DEVELOPMENT (SECTOR) PROJECT

(Loan No. 1198-INO)

Ii

II I 'I.] I,i

May 2000

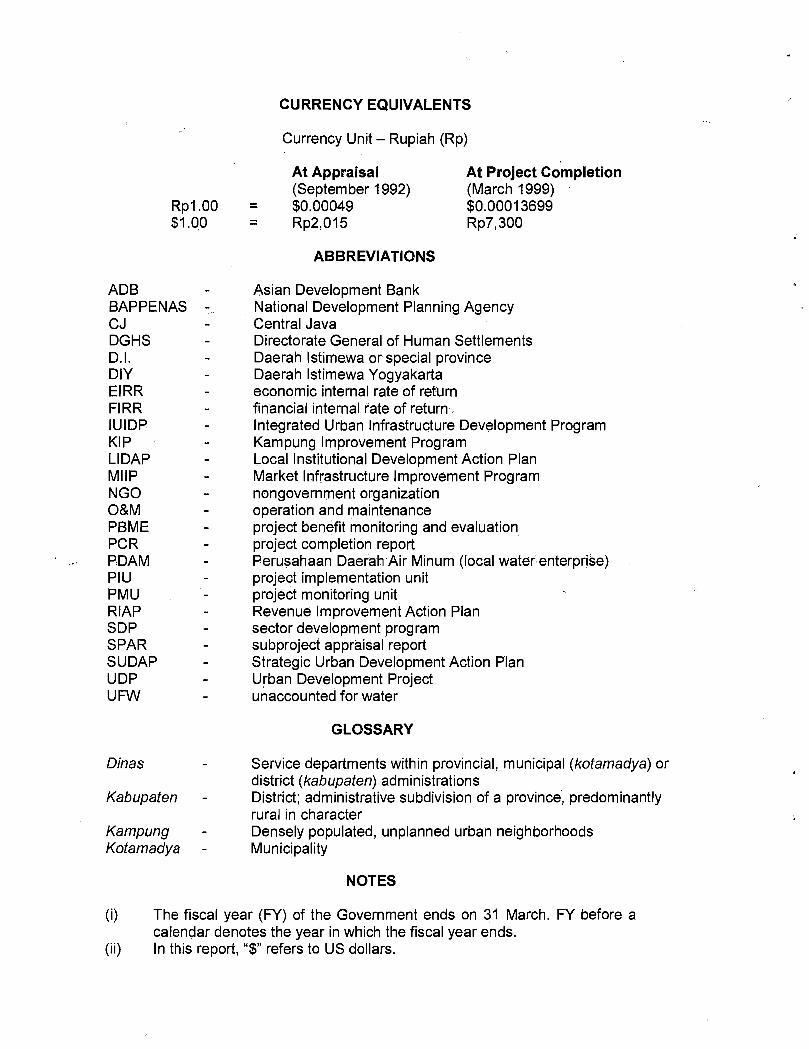

CURRENCY EQUIVALENTS

Currency Unit - Rupiah (Rp)

At Appraisal At Project Completion(September1992) (March 1999)

Rpl.00 = $0.00049 $0.00013699

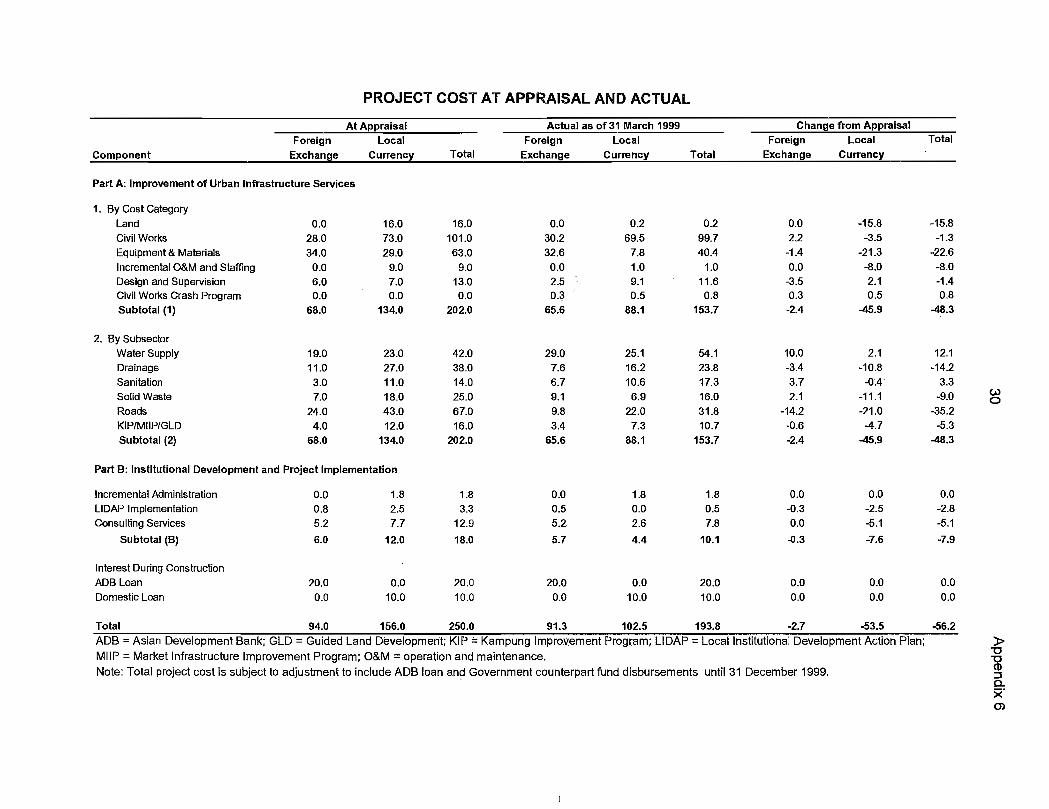

$1.00 = Rp2,015 Rp7,300

ABBREVIATIONS

ADB - Asian Development Bank

BAPPENAS - National Development Planning AgencyCJ - Central JavaDGHS - Directorate General of Human SettlementsDi. - Daerah Istimewa or special provinceDIY - Daerah Istimewa YogyakartaEIRR - economic internal rate of returnFIRR - financial internal rate of returnIUIDP - Integrated Urban Infrastructure Development ProgramKIP - Kampung Improvement ProgramLIDAP - Local Institutional Development Action PlanMIIP - Market Infrastructure Improvement ProgramNGO - nongovernment organizationO&M - operation and maintehancePBME - project benefit monitoring and evaluationPCR - project completion reportPDAM - Perusahaan Daerah Air Minum (local water enterprise)PIU - project implementation unitPMU - project monitoring unitRIAP - Revenue Improvement Action PlanSDP - sector development programSPAR - subproject appraisal reportSUDAP - Strategic Urban Development Action PlanUDP - Urban Development ProjectUFW - unaccounted for water

GLOSSARY

Dinas - Service departments within provincial, municipal (kotamadya) ordistrict (kabupaten) administrations

Kabupaten - District; administrative subdivision of a province, predominantlyrural in character

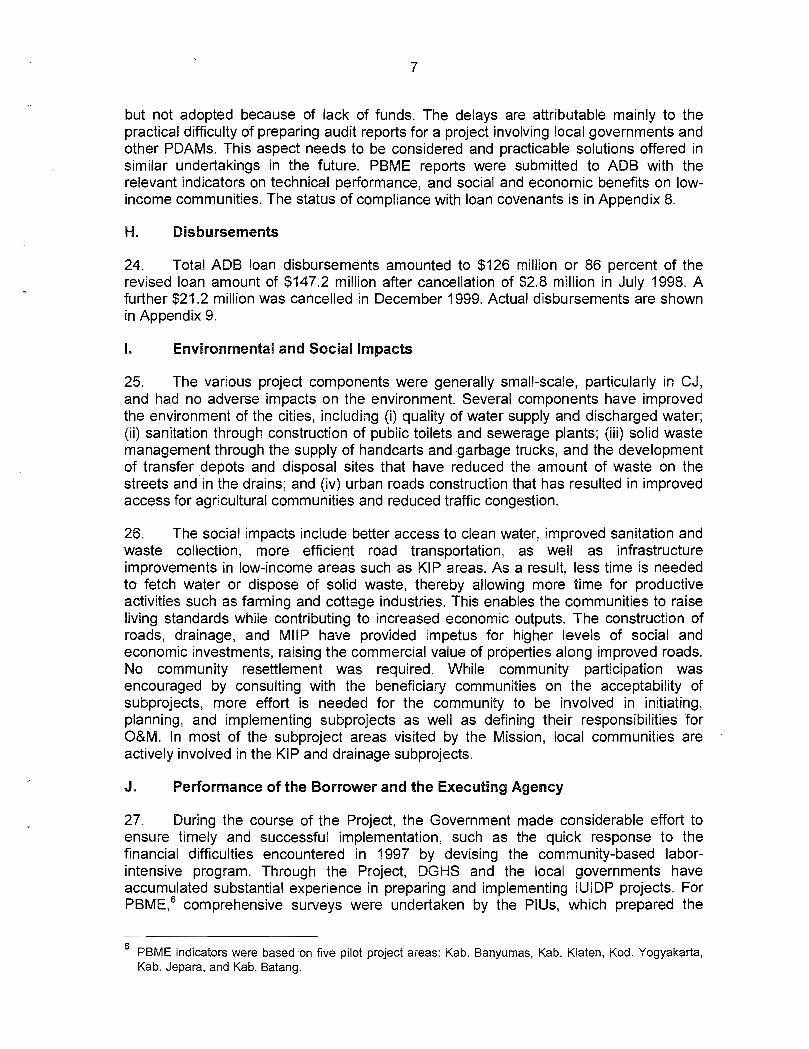

Kampung - Densely populated, unplanned urban neighborhoodsKotamadya - Municipality

NOTES

(i) The fiscal year (FY) of the Government ends on 31 March. FY before acalendar denotes the year in which the fiscal year ends.

(ii) In this report, "$" refers to US dollars.

CONTENTS

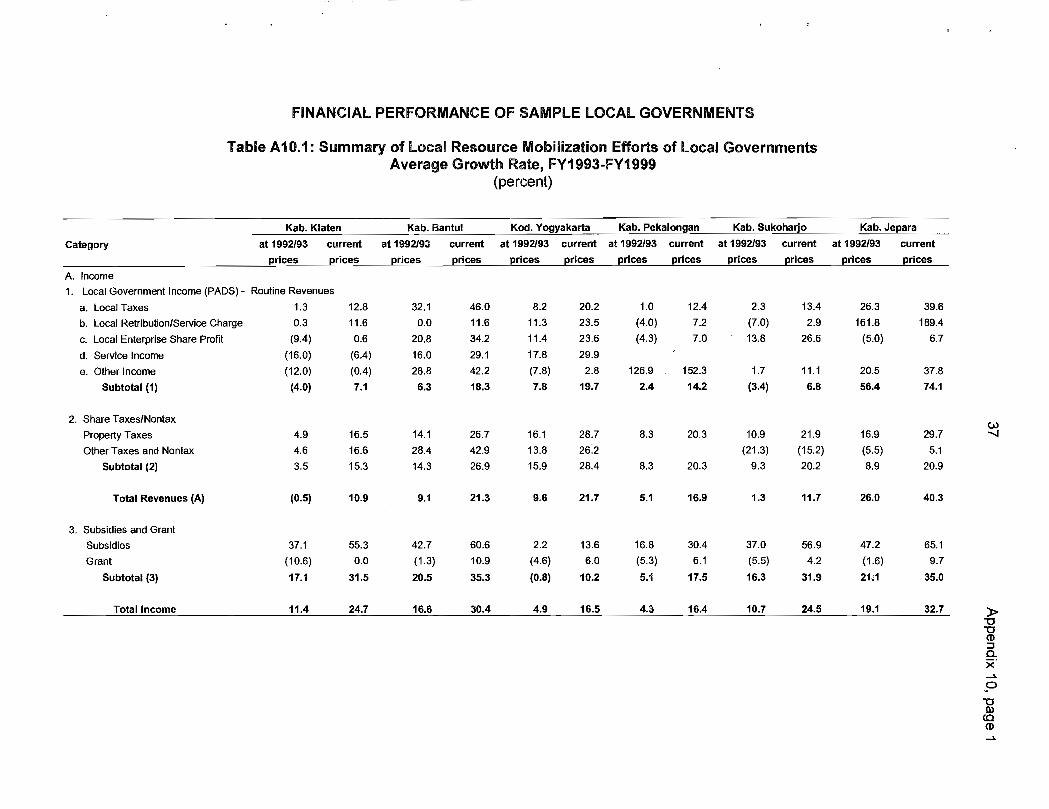

Page

BASIC DATA

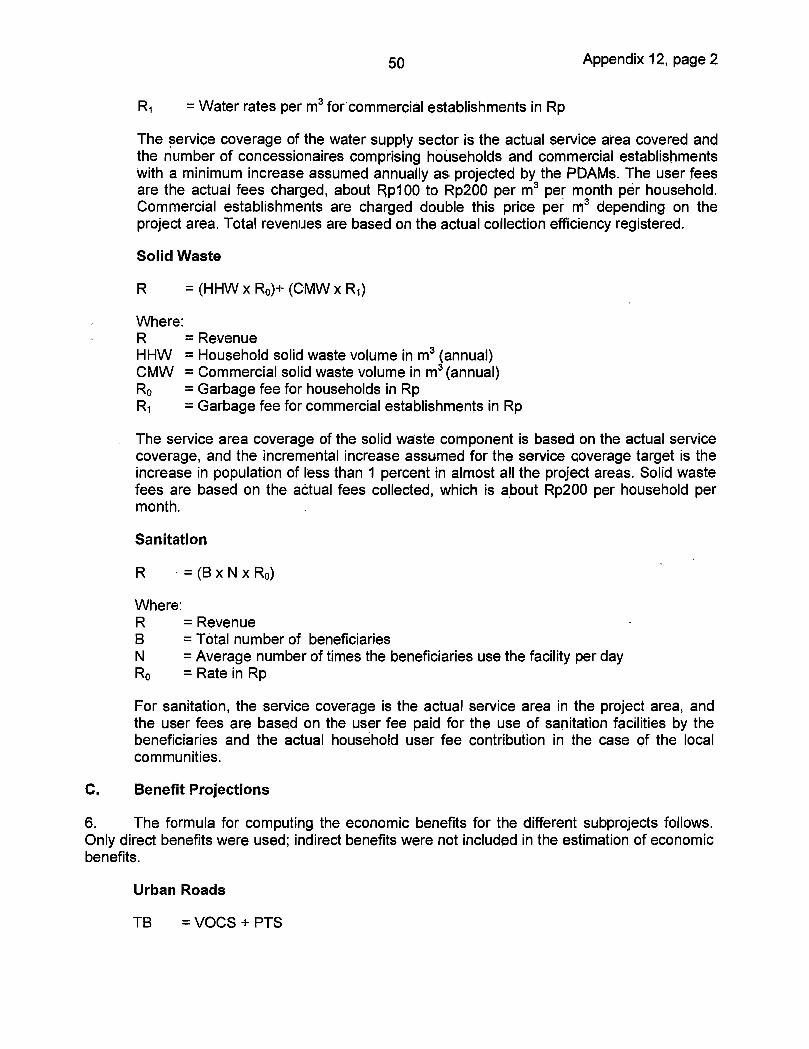

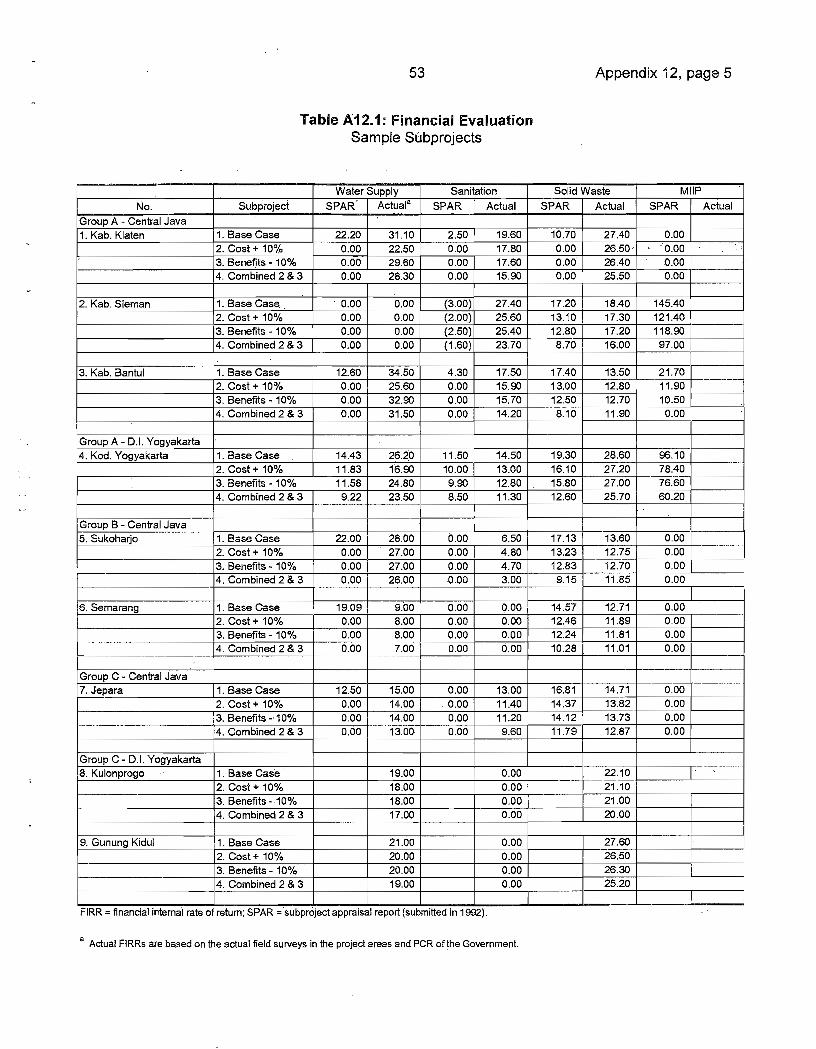

II

MAP vii

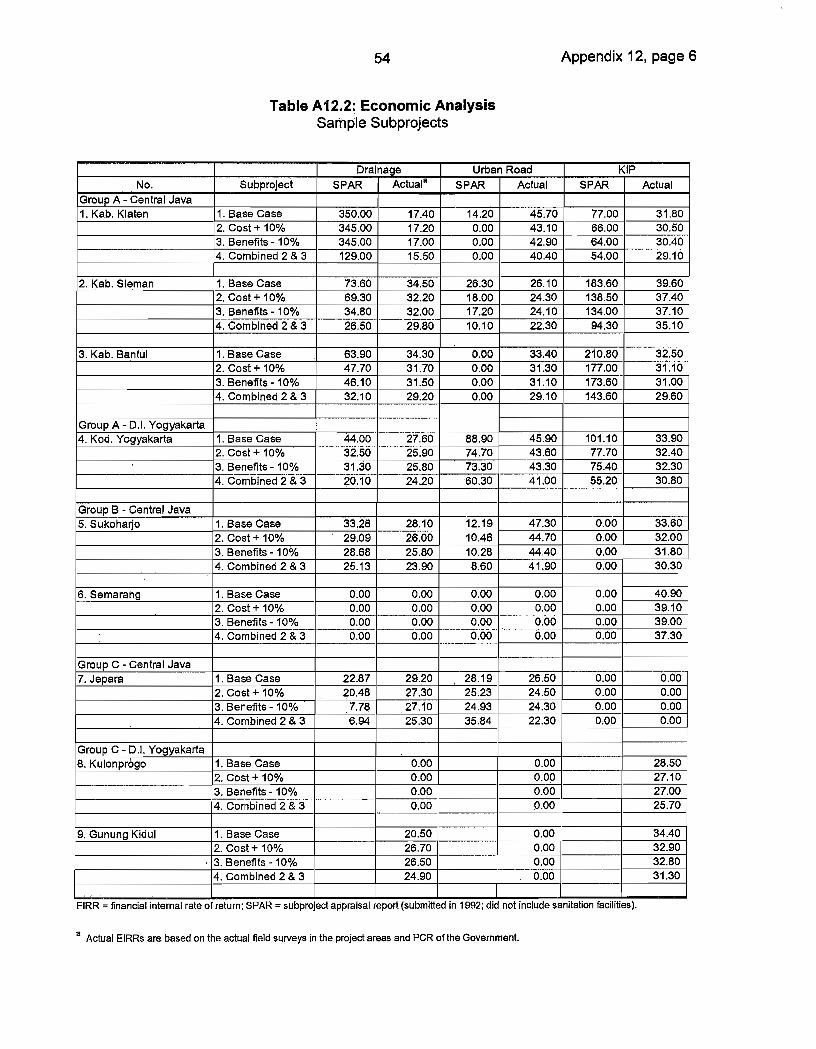

I. PROJECT DESCRIPTION

I

II. EVALUATION OF IMPLEMENTATION

1

A. Project Components 1

B. Implementation Arrangements

4C. Project Costs and Financing

5

D. Project Schedule

6E. Engagement of Consultants and Procurement of Goods and

Services

6F. Performance of Consultants, Contractors, and Suppliers

6

G. Conditions and Covenants

6H. Disbursements

7I. Environmental and Social Impacts

7

J. Performance of the Borrower and the Executing Agency

7K. Performance of ADB

8

III. EVALUATION OF INITIAL PERFORMANCE AND BENEFITS

8

A. Financial Performance

8B. Economic Performance

9

C. Attainment of Benefits

9

IV. CONCLUSIONS AND RECOMMENDATIONS

14

A. Conclusions

14B. Lessons Learned

15C. Recommendations

16

APPENDIXES

18

BASIC DATA

B.

Loan Identification

1. Country2. Loan Number3. Project Title

4. Borrower5. Executing Agency

6. Amount of Loan

7. PCR Number

Loan Data

1. Appraisal- Date Started- Date Completed

2. Loan Negotiations- Date Started- Date Completed

3. Date of Board Approval

4. Date of Loan Agreement

5. Date of Loan Effectiveness- In Loan Agreement-Actual

6. Closing Date- In Loan Agreement- Actual- Number of Extensions

7. Terms of Loan- Interest Rate- Maturity- Grace Period

8. Terms of Relending- Interest Rate- Maturity- Grace Period

Indonesia1198-INOCentral Java and D.l. Yogyakarta UrbanDevelopment (Sector) ProjectRepublic of IndonesiaDirectorate General of Human Settlements(DGHS) in Ministry of Public Works (MPW)$150.0 million in ordinary capital resources(OCR)INO 564

24 July 199214 August 1992

26 October 199229 October 1992

26 November 1992

10 February 1993

11 May 199324 March 1993

30 September 199831 March 19991I

Variable25 years5 years

11.75 percent220 years5 years

The loan account is kept open, pending settlement by the Borrower of $0.21 million related to disbursements.2

Includes banking fee of 0.75 percent per annum.

Appraisal Estimate

94.0

• 156.0

250.0

($ millionActual

91.3

102.5

193.8

mi

9. Disbursements

a. Dates

Initial Disbursement Final Disbursement Time Interval29 September 1993 13 December 1999 6.2 years

Closing Date Time IntervalEffective Date Original Actual, (from original (from actual

closing date) closing date)24 March 1993 30 September 1998 31 March 1999 5.5 years 6.0 years

b. Amount($ million)

Reallocation

Original and Amount UndisbursedCategory Allocation Cancellation Disbursed Balance

I Civil Works 54.5 (1.3) 53.2 0

1A Equipment&Materials 12.0 17.9 29.9 0(ICB/IS)

lB Equipment and Materials 35.6 (32.9) •2.5 0(LCB)

1C Consulting Services (ICB) 10.6 (1.7) 8.9 0

1D Consulting Services (LCB) 17.3 (6.6) 10.7 0

1 E Civil Works Crash Program 0.0 (0.8) 0.8 0

03 Interest During Construction 20.0 0.0 20.0 0

Total 150.0 24,0 126.0 0

9. Local Costs (Financed)

- Amount- Percentage of Local Costs- Percentage of Total Cost

C. Project Data

1. Project Cost

Cost

Foreign Exchange

Local Currency

Total

$34.7 million.24 percent18 percent

iv

2. Financing Plan($ million)

Item Appraisal Estimate Actual

Foreign Local Total Foreign Local Total

A Implementation Costs

Borrower-financed 0.0 90.0 90.0 0.0 57.8 57.8

ADB-financed 74.0 56.0 130.0 71.3 34.7 106.0

Subtotal (A) 74.0 146.0 220.0 71.3 92.5 163.8B Interest During Construction

Borrower-financed' 0.0 100 10.0 0.0 10.0 10.0

ADB-financed 20.0 0.0 20.0 20.0 0.0 20.0

Subtotal (B) 20.0 10.0 30.0 20.0 10.0 30.0

Total 94.0 156.0 250.0 91.3 102.5 193.8

3. Cost Breakdown by Project Components($ million)

Item Appraisal Estimate Actual

Foreign Local Total Foreign Local Total

Part AImprovement Of Urban Infrastructure and Services

1. By Cost Category

Land 0.0 16.0 16.0 0.0 0.2 0.2

Civil Works 28.0 73.0 101.0 30.2 69.5 100.0

Equipment and Materials 34.0 29.0 63.0 32.6 7.,8 40.4

Incremental O&M and 0.0 9.0 9.0 0.0 1.0 1.0Staffing

Design and Supervision 6.0 7.0 13.0 2.5 9.1 11.6

Civil Works Crash 0 0 0 0 0 0 0 3 0 5 0 8Program

Subtotal (1) . 68.0 134.0 202.0 65.6 88.1 153.7

2. By Subsector

Water Supply 19.0 23.0 42.0 29.0, 25.1 54.6

Drainage 11.0 27.0 38.0 7.6 16.2 23.9

Sanitation ' 3.0 11.0 14.0 6.7, 10.6 17.4

Solid Waste 7.0 18.0 25.0, 9.1:H 6.9 16.2

Roads 24.0 43.0 67.0 9.8 22.0 32.0

KIP/MIIP/Guided Land 4.0 12.0 16.0 .4 7.3 10.7Development

Subtotal (2) 68.0 134.0 202.0 65.6 88.1 153.7

V

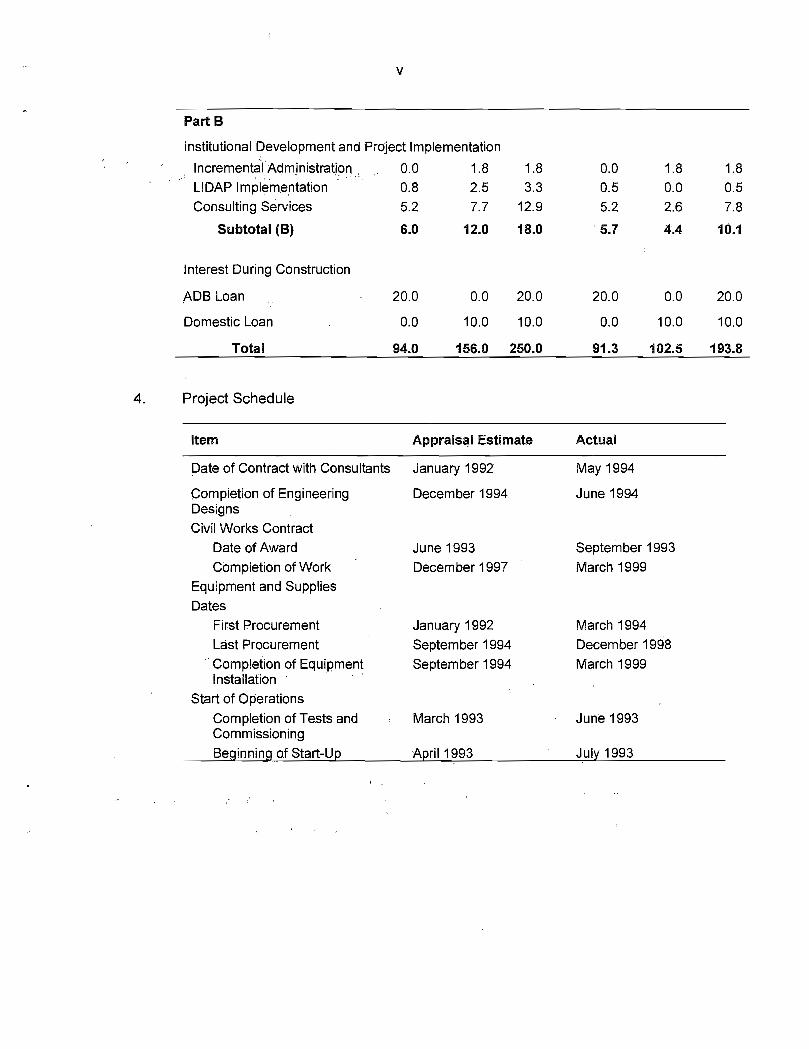

Part B

Institutional Development and Project Implementation

Incremental Administration 0 0 1 8 1 8 0 0LIDAP Implementation 0.8 2.5 3.3 0.5Consulting Services 5.2 7.7 12.9 5.2

Subtotal (B) 6.0 12.0 18.0 5.7

Interest Durina Construction

1.8 1.8

0.0 0.5

2.6 7.8

4.4 10.1

ADB Loan 20.0 0.0 20.0 20.0 0.0 20.0

Domestic Loan 0.0 10.0 10.0 0.0 10.0 10.0

Total 94.0 156.0 250.0 91.3 102.5 193.8

Project Schedule

Item Appraisai Estimate Actual

Date of Contract with Consultants January 1992 May 1994

Completion of Engineering December 1994 June 1994DesignsCivil Works Contract

Date of AWard June 1993 September 1993Completion of Work December 1997 March 1999

Equipment and SuppliesDates

First Procurement January 1992 March 1994Last Procurement September 1994 December 1998Completion of Equipment September 1994 March 1999Installation

Start of Operations

• Completionof Tests and March 1993 June 1993CommissioningBeginning of Start-Up April 1993 • • July 1993

vi

0. Data on ADB Missions

Name of MissiOn

No.of No.ofDate PersonS Person-

Specialization ofMembers1

Appraisal 24 Jul-14 Aug 1992 5 110 b, d, e, f, i

Review223 May-I Jun 1994 2 20 a, i

Review327 Sep-9 Oct 1993 2 26 a, f

Review48-13 Dec 1994 1 6 a

Midterm Review530 Jul-11 Aug 1995 3 39 a, h, i

Review61-14 Dec 1995 2 28 a, g

Review76-20 Dec 1996 3 45 a, b, g

Review816-26Jun 1997 2 22 a,i

SPAM915-19 Dec 1997 1 5 a

SLAM 1 ° 12-l4Jan 1998 5 15 a,g

SPAM 1131 Aug-I Sep 1998 3 6 a, b, g

Review1223-27 Nov 1998 2 10 a, b

Project Completion Review 6-17 Dec 1999 4 39 b, C, h, i

Total 371I

a-engineer/project officer, b-urban development specialist, c-urban economist 1 d-financial analyst, e-counsel,f-programs officer, g-project implementation officer, h-project administration supporting staff/assistant projectanalyst, i-staff consultant.

2 Undertaken in conjunction with Loan 1077-lNO: Botabek Urban Development Project.Undertaken in conjunction with Loan 1077-INO: Botabek Urban Development Project.Undertaken in conjunction with Loan 768-INO: Second Bandung Urban Development Project.Undertaken in conjunction with midterm review of Loan 1 077-INO: Botabek Urban Development Project.

6 Undertaken in conjunction with Loan 1111 -INO: Bogor and Palembang Urban Development Project.Undertaken in conjunction with Loan 1111 -INO: Bogor and Palembang Urban Development Project.

8 Special Project Administration Mission in conjunction with Loan 111 1-INO: Bogor and Palembang UrbanDevelopment Project.Special Loan Administration Mission in conjunction with Loan 1111-lNO: Bogor and Palembang UrbanDevelopment Project.

Loan Administration Mission; also joined in by the project manager, programs manager, and residentrepresentative, Indonesia Resident Mission (IRM).Special Loan Administration Mission in conjunction with Special Project Administration Mission for Loan Illi-INO:Bogor and Palembang Urban Development Project, Loan I 292-lNO: Eastern Islands Urban Development (Sector)Project, Loan 1384-INO: West Java Urban Development (Sector) Project.

12 in conjunction with Loan 1111-INO: Bogor and Palembang Urban Development Project.

INDONESIA

CENTRAL JAVA AND D.IYOGYAKARTAURBAN DEVELOPMENT PROJECT

(as completed)

705

WEST

JAVA

iICi0T0ioi.

I Subproject Location

® National Capital

Municipal Boundary

— — Provincial Boundary SOS

International Boundary

Boundaries are not necessarily authoritative.

109°Ei1O°E 130°E

INDONESIA

- 5°Th\ South cliiiia Sea Philippine Sea5°N-

/ / eJebea Sea

ç

k{_-.J PACnICOCEAIs 0

0

JAKARTA Java Seas

- -

J®ri /

lOoS0

Arefura Sea10 S

IND!AN OCEAN

110°E 130°E

tU0E

Jepara

"4KUdus 'Pati

Rembang

/ ) ! I/ Demak

/ ," - —./ 1 " I Kendal / \

/'J----7°S -

,! Tegal / Pekalongan Batang ,' , ' 1 \ Blora j/ Brebes Pemalang

emarang Grobogan / E A ST J A V A- I - - - - -

I I /' i_

'- -. .. .- )..I ___ I(--

Temanggung // / / Salatiga I IN--' \ Purbolingga I /CENTRLAVN'II ( -- Srageri

/ ' i3anjarnegara 'r'. III\ Banyumas / cç' / \

) Wonosobo Magelang Boyolali "p- 0 10 20 30 40 50-' LIIacap ••__ ,,. ..----..' .'-- __%_. I -,

"--I / I 'i 'Sj 'v' "s .. : " ' Karanganyar

Kebumen"\ Puorejo / ''Sleman! Kiaten Sukohrjo

/ / c ' / I

- C.. / II

•< ,-// KuIonprog' "'

I / YOGYA.KARTA / wonogiri •../- Bantul \-8°S

/ Gunung Kidul18

I'I

IIILWIE

I. PROJECT DESCRIPTION

1. The objectives of the Project were to (i) improve the urban environment andurban living conditions, in particular, in the low-income areas; and (ii) minimizeimpediments to economic growth by providing infrastructure in the subsectors coveredunder the Integrated Urban Infrastructure Development Program (IUIDP). The Projectalso aimed to strengthen (i) the capabilities of the provincial and local governmentsconcerned in urban management, local resource mobilization and financialmanagement, institutional assessment, and human resources and organizationaldevelopment, and (ii) their administrative capabilities in planning, project implementation,environmental management, operation and maintenance (O&M), and land management.

2. The Project helped the Government of Indonesia achieve its urban sectorobjectives and targets, and provided funds for its urban infrastructure investment plan inthe provinces of Central Java (CJ) and D.I. Yogyakarta (DIY). The Project funded 37local governments as compared with 38 envisaged at appraisal. The 37 subprojectsconsisted of 7 group A 1 (4 in CJ Urban Development Project [UDP] and 3 in DIY UDP),22 group B (all in CJ UDP), and 8 group C (6 in CJ UDP and 2 in DIY UDP) subprojects.The Project covered 64 secondary cities and 173 urban infrastructure componentsincluding water supply (27), urban roads (26), sanitation (25), Kampung ImprovementProgram/Market Infrastructure Improvement Program (KIP/MIIP) (32), solid waste (34),and drainage (29). In accordance with the principles of the IUIDP approach, the Projectaimed at combining the physical, subsectoral, and institutional linkages of the various.project components.

3. The Project consisted of two main parts:

(I) Part A - Improve urban infrastructure of the standard IUIDP subsectors:water supply, wastewater treatment and sanitation, solid wastemanagement, urban roads, urban drainage, KIP, MIIP, and landdevelopment. Provide consulting services for detailed engineering designand construction supervision.

(ii) Part B - Strengthen (a) the institutional capabilities of the central,provincial, and local governments in urban management, local resourcemobilization, and financial management; and (b) their technicaladministration capabilities in planning, environmental management, O&M,and land management.

IL EVALUATION OF IMPLEMENTATION

A. Project Components

4. A chronology of the milestone events of project implementation is in Appendix 1,and an outline of the project components as appraised and actually implemented is inAppendix 2. The targets at appraisal were revised in 1995.after completion of all thesubproject appraisals for group A, B, and C subprojects.

The subprojects were divided into three groups based on a set of selection criteria established atappraisal. Group A subprojects comprised those that met all the selection criteria. GroupA subprojectswere larger in scale, ranging from Rp18,000 million ($8.8 million equivalent) to Rp67,000. million ($33million equivalent). Group B subprojects comprised those that met the selection criteria but subprojectsummaries were not prepared at appraisal. Group C comprised subprojects that had not yet met theselection criteria at appraisal. Group B and C subprojects were smaller in scale with the majority underRplO,000 million ($4.9 million equivalent). All values based on Rpl.00 = $O.00049.

2

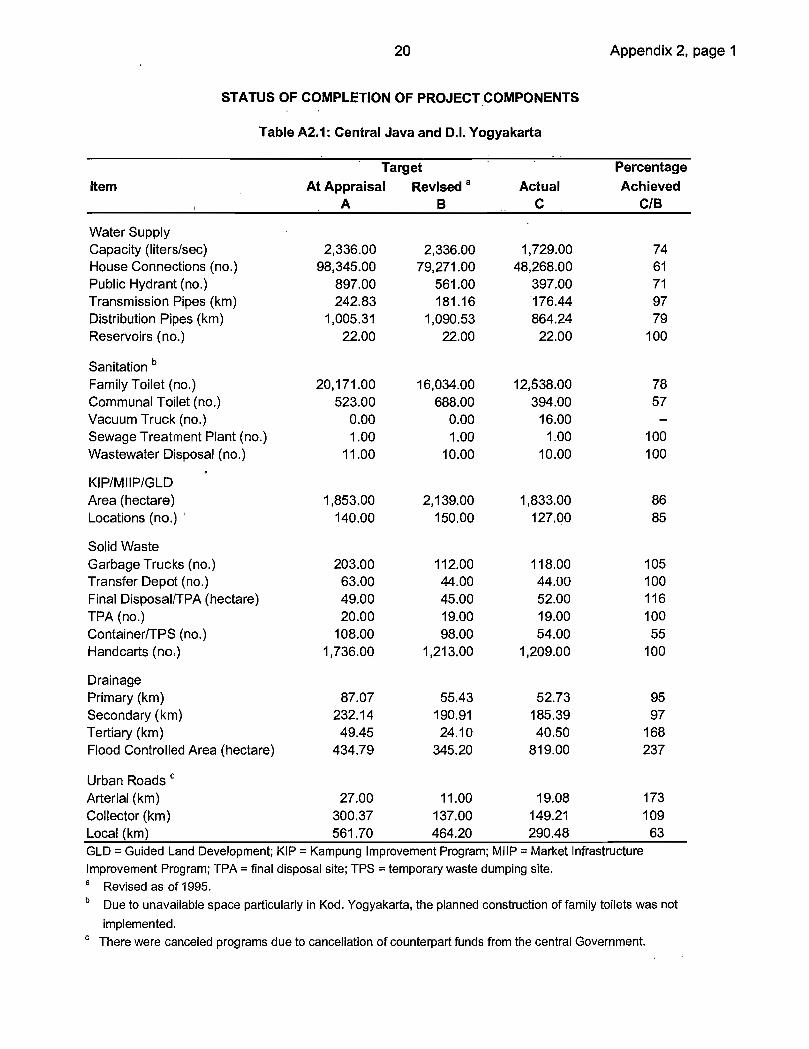

5. The allocation of funds by province and by subsector is presented in Appendix 3.Seventy-two percent of the total infrastructure project cost was allocated to CJ, 28percent to DIY. In terms of sector distribution, water supply had the highest share (34percent) of the total project cost, while KIP/MIIP had the least funding with only 6 percentof the total cost. In terms of allocation of funds by subproject group, group A subprojects(in CJ and DIY) obtained 48.7 percent, group B subprojects (in CJ only) 42.9 percent,and group C subprojects (in CJ and DIY) 8.4 percent. The investments in CJ werespread over many small rural subprojects, whereas in DIY these were shared by a fewrelatively large subprojects in a more urban setting. Due to the large number ofsubprojects in CJ, implementation was slower than in DIY because staff in many localgovernments in CJ were unfamiliar with the procedures. Project implementation wasaffected by the economic and financial crisis from late 1997, resulting in fundingshortages in the local governments and other implementing agencies concerned.Notwithstanding these difficulties, the physical components were largely completed inaccordance with the revised targets in both CJ and DIY, as shown in Appendix 2.

1. Water Supply

6. The water supply components in CJ and DIY included the construction offacilities to supply an additional capacity of 1,730 liters per second, over 48,200 newwater connections, nearly 400 public hydrants, 22 reservoirs, and over 880 kilometers ofpipes. All these subcomponents were generally completed as designed except for theinstallation of house connections and pipelines (including tertiary distribution) inKabupaten (Kab.) Semarang (CJ group B). The problem in Perusahaan Daerah AirMinum (PDAM) Kab. Semarang was due to the overly optimistic investment plan startingwith capital investment from the central Government loan, followed by self-financedhouse connections. With limited borrowing capacity, house connection works weredelayed. As a result, over 50 percent of the water supply components in Kab. Semaranghave yet to be installed.

2. Sanitation

7. This component was mainly implemented in DIY. Over 12,500 family toilets wereconstructed, 16 sludge trucks were purchased, a sewerage treatment unit was installed,and 394 communal toilets and 10 wastewater disposal facilities were installed. Thedemand for low-cost sanitation components, particularly the communel toilets, wasoverestimated in the more urbanized areas, particularly for Kotamadya (Kod.)Yogyakarta where there were no appropriate sites available. As household incomelevels rose, the demand for individual in-house facilities replaced that for the publicfacilities provided by the Project. Sludge equipment in Kab. Klaten was underutilized,partly due to inadequate awareness of the potential beneficiaries.

3. Kampung Improvement Program, Market Infrastructure ImprovementProgram, and Guided Land Development

8. The KIP and MIIP were generally successfully implemented, despite theirdispersed locations. A combined total of 127 sites and 1,833 hectares (ha) of KIP/MIIPwere improved. The achievement was close to the estimated target (140 sites, 1,853 ha)at appraisal but lower than the revised target (150 sites, 2,139 ha). Furthermore, the KIPand MllP facilities have been adequately maintained as a result of strong communityparticipation, with minimum financial support from the local government. It was likewise

3

noted that additional improvements to the Asian Development Bank (ADB)-funded KIPand MIIP facifities were largely undertaken by the communities. Land development, e.g.,guided land development, to support low-income housing programs was one of theproject components at appraisal. Implementation of this component was incorporatedinto the KIP and MIIP subprojects.

4. Solid Waste

9. This component was mainly implemented in the more urbanized areas in group A(CJ and DIY) and group B municipalities and districts. Some 1,210 handcarts and 118garbage trucks were purchased; 44 transfer depots and 19 disposal sites (52 hectares)were developed; and 54 container units were provided. The Project supported a two-stage collection process typical, in Indonesian towns. This involved locally organizedcollections from within residential areas, temporary storage in container units or transferstations, and local government transfer to final dump sites. The approach is sound, andthe facilities provided have been fully utilized. A solid waste fee is collected frOm bothdomestic households and commercial establishments. Collection is higher in the largercities such as Kod. Yogyakarta than in less urbanized areas.

10. About 53 kilometers of primary drains, 185 kilometers of secondary drains, and40 kilometers of tertiary drains were constructed. Flood control areas cover 819hectares, more than double the revised target. The component supported part of thedrainage master plans in some cities such as Kod. Yogyakarta and Kab. Klaten. In someproject areas in small municipalities, drainage is integrated with community-based KIPand urban road components.

6. Urban Roads.

11. Nineteen kilometers of arterial roads, 149 kilometers of collector roads, and 290kilometers of local roads were built. The component met about 75 percent of the targetsin both CJ and DIY. This was partly due to the cancellation of the central Government'scounterpart funds for some of the subprojects. Road maintenance is largely shared byprovincial and local governments. Some communities are involved in maintaining localroads.

7. Community-Based Labor-Intensive Work

12. At the onset of the drastic economic and financial downturn, the Governmentquickly responded with a community-based labor-intensive work program to help themost vulnerable poor communities and maintain social stability. The program was addedto the Project in February 1998 for $1.5 million. The program was similar to the KIP, butwas based on community initiatives using labor from the beneficiary and neighboringcommunities. Details of the program were presented in several reports.2

2 Memorandum of understanding (MOU) between the Government and ADB dated 14 January 1998, back-to-office report (BTOR) dated 10 February 1998, and BTOR, by the Indonesian Resident Mission, dated 9December 1998.

4

8. Institutional Support

13. All packages under the institutional support component were essentiallycompleted in both CJ and DIY. In , DIY a similar institutional capacity-building project,funded by a bilateral assistance (Swiss Development Corporation), was implemented incoordination with ADB. This arrangement resulted in more responsive institutionalsupport to the local governments in DIY. However, in the case of CJ, due to the greaternumber of municipalities involved, some packages encountered delays, particularly thesupport for subproject preparation to local governments. There was also sloW progressin preparing institutional and financial action plans. Appendix 4 gives an overview of theactual implementation of the institutional support components compared with estimatesat appraisal. A specific coordinator was appointed by the Directorate General of HumanSettlements (DGHS) to strengthen the institutional activities and to speed upimplementation. Progress was made but local governments feel there is a need for moreintensive skills transfer and interaction with the consultants, particularly for the RevenueImprovement Action Plan (RIAP) and Local Institutional Development Action Plan(LIDAP). The financially capable local governments, mostly in the group A districts andmunicipalities, had no problem implementing institutional capacity-building resources aswell as financial management and revenue enhancement programs. In DIY province,Kod. Yogyakarta jointly implemented these measures with smaller and financiallyweaker local governments. In CJ, due to the limited resources and the larger number ofdistricts and municipalities covered, difficulties were encountered in obtaining consensusand support from local governments on the implementation of financial managementmeasures.

14. Experience and knowledge gained by project management unit (PMU) andproject implementation unit (PIU) staff from the training and institutional strengtheningprograms have in general been good; their capability to work on future urbandevelopment projects is increased. While DGHS, the Executing Agency, has compliedwith the loan covenant on submitting project benefit monitoring and evaluation (PBME)reports, regular benefit monitoring and evaluation must be continued to ensure effectiveimplementation of the LIDAP3 and RIAP.

B. Implementation Arrangements

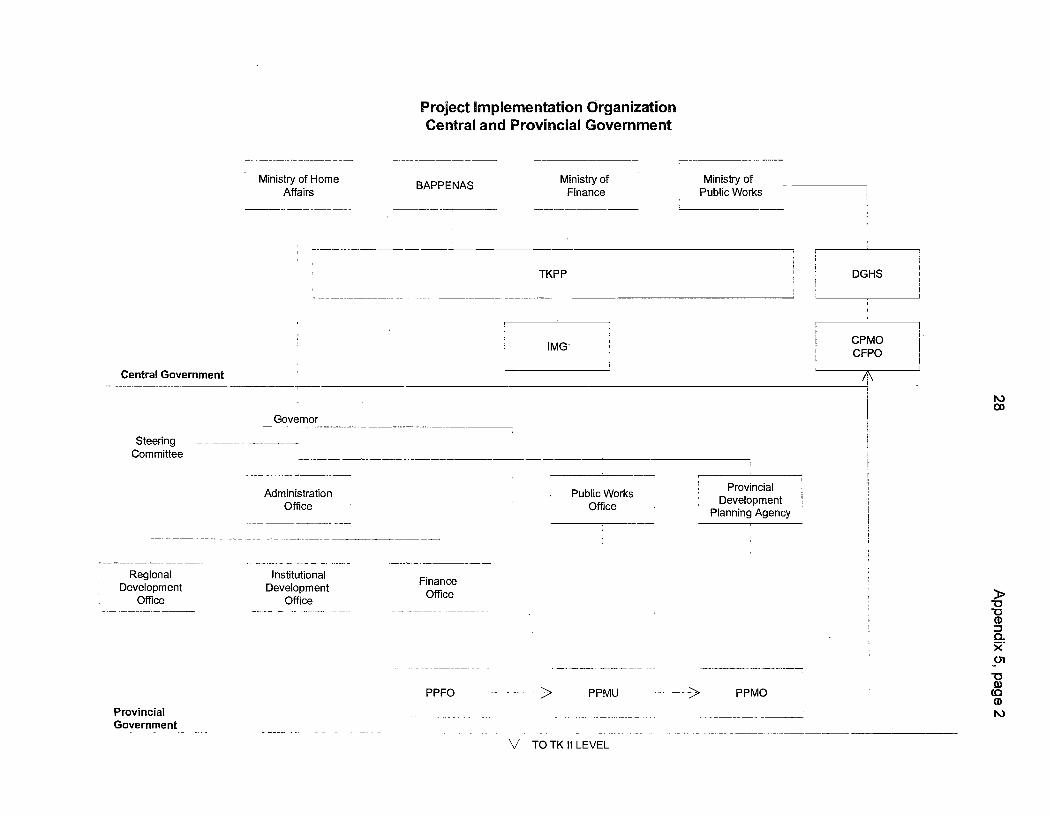

15. DGHS of the Ministry of Public Works was the lead Executing Agency for theProject. The Central Project Management Office under DGHS provided overall projectimplementation supervision, monitoring, and coordination of subproject implementation.Policy coordination was provided by an interministerial committee, the NationalCoordination Team for Urban Development, under the national development planningboard, BAPPENAS. The Ministry of Home Affairs (MOHA) was responsible forinstitutional development support for local governments concerned and handled RIAPsand LIDAPs at the central level. The provincial governments, through their provincialPMUs, provincial project management offices (PMOs), and provincial project financeoffices (PFOs), played a key role in coordinating all local governments and assisting

For example, following the pilot projects undertaken for six subproject areas, it was realized that the localgovernments have difficulty implementing the action plans. The Ministry of Home Affairs initiated a studyto prepare strategic urban development action plans (SUDAPs) for six other subproject areas. TheSUDAPs were prepared by the local governments, local communities, and NGOs, setting out the vision aswell as preparing urban development action plans to realize the vision. The SUDAPs were found to bemore appropriate for implementation by the local governments.

5

them in both planning and implementing the subprojects. At the local level, the PMUs,PMOs, PFOs, and PlUs were established for subproject implementation. Appendix 5presents the overall organization structure for CJ and DIY-UDP project implementationat the central and local government levels. The complex implementation arrangementsresulted in substantial delays in some institutional support packages. The delays wererelated to (i) complex government procedures at the central, provincial, and local levels,and inadequate interagency coordination; (ii) insufficient numbers of skilled staff; and (iii)inadequate counterpart funds.

16. The Project's implementation arrangements were decentralized in accordancewith the !UIDP concept. The sector project format was a major contributing factor. Allproject offices were set up basically within the existing organizational structure. This wasaimed at facilitating the transition from implementation to O&M.

C. Project Costs and Financing

17. Actual project costs totaled $193.8 million equivalent 4 or 78 percent of the $250.0million projected at appraisal (Appendix 6). The actual foreign exchange and localcurrency costs were $91.3 million and $102.5 million equivalent, or 97 percent and 66percent of the estimates at appraisal. The lower local currency cost was due to thedevaluation of the Indonesia rupiah.

18. Actual ADB financing was $126 million, which is 84 percent of the loan amount of$150 million. The fluctuation of the rate of foreign exchange and inadequate counterpartfunding resulted in cancellation of $2.8 million in July 1998 as part of the portfoliorestructuring exercise to ease the Government's financial situation at the onset of the1997 financial downturn. A further $21.2 million was cancelled in December 1999.

Table 1: Financing Plan($ miUion)

Appraisal Estimate Actual Change from AppraisalForeign Local Total Foreign Local Total Foreign Local Total

Borrower- 0.0Financed

% of change

ADB- 94.0Financed

% of change

Total

100 100

56.0 150.0

0.0 67.8 67.8

91.3 34.7 126.0

0.0 (32.2) (32.2)

(32%) (32%)

(2.7) (21.3) (24.0)

(16%)

(56.2)94.0 156.0 250.0 91.3

(3%) (38%)

102.5 193.8 (2.7) (53.5)

% of change (3%) (34%) (22%)

The total project cost is subject to downward adjustment of $0.21 million, which was disbursed but is duefor reimbursement by the Borrower.

6

D. Project Schedule

19. The Project was originally scheduled to start in March 1993 and be completed bySeptember 1998, an implementation period of 66 months Actual project completion wasextended by six months to 31 March 1999. The actual project implementation scheduleas compared with the appraisal target is in Appendix 7. There was substantial delay inthe start-up of project implementation, i.e., three months for group A subprojects andnine months for groups B and C. Full-scale implementation for group A subprojectsstarted in 1995, whereas subprojects in groups B and C commenced in early 1996. Themain causes were overambitious targets at the planning stage and delays in therecruitment of the implementation advisers and finalization of the Government'sguidelines for the project implementation and borrowing procedures under the subsidiaryloan agreements. In many cases, finalizing subsidiary loan agreements (SLAs) took oneto two years. Availability of local counterpart funds also affected timely procurementaction, and consequently implementation.

E. Engagement of Consultants and Procurement of Goods and Services

20. Consulting services were provided for subproject preparation advisory services,and implementation support for the central, provincial, and local governments. Therewere delays in engaging consultants due to the time taken to determine complex workrequirements and clear internal Government procedures for the purpose. The matter is asystemic sector issue and needs to be dealt with in that light at an appropriate forum.

21. For local procurement (local competitive bidding), applicable Governmentprocedures were followed. The availability of counterpart funds often delayed thecontract awards to a varying degree, but not substantially. One case of irregularactivities involving procurement was found by the state auditor (BPKP). At their request,ADB investigated the matter and appropriate actions were taken by the Government andADB.5

F. Performance of Consultants, Contractors, and Suppliers

22. Except in isolated cases, the performance of consultants, contractors, andsuppliers was satisfactory. Consultant support was particularly important for thepreparation of the pilot LIDAPs and RIAPs. While the performance of the consultantswas found to be acceptable, there could be improvements in the transfer of knowledgefrom the consultants to the implementing agencies, through more systematic feedbackassessment to ensure that skills transfer has been successfully met. It is recommendedthat the central, provincial, and local governments keep an updated database ofconsultants, contractors, and suppliers, and an assessment of their performance onGovernment-funded projects for future reference.

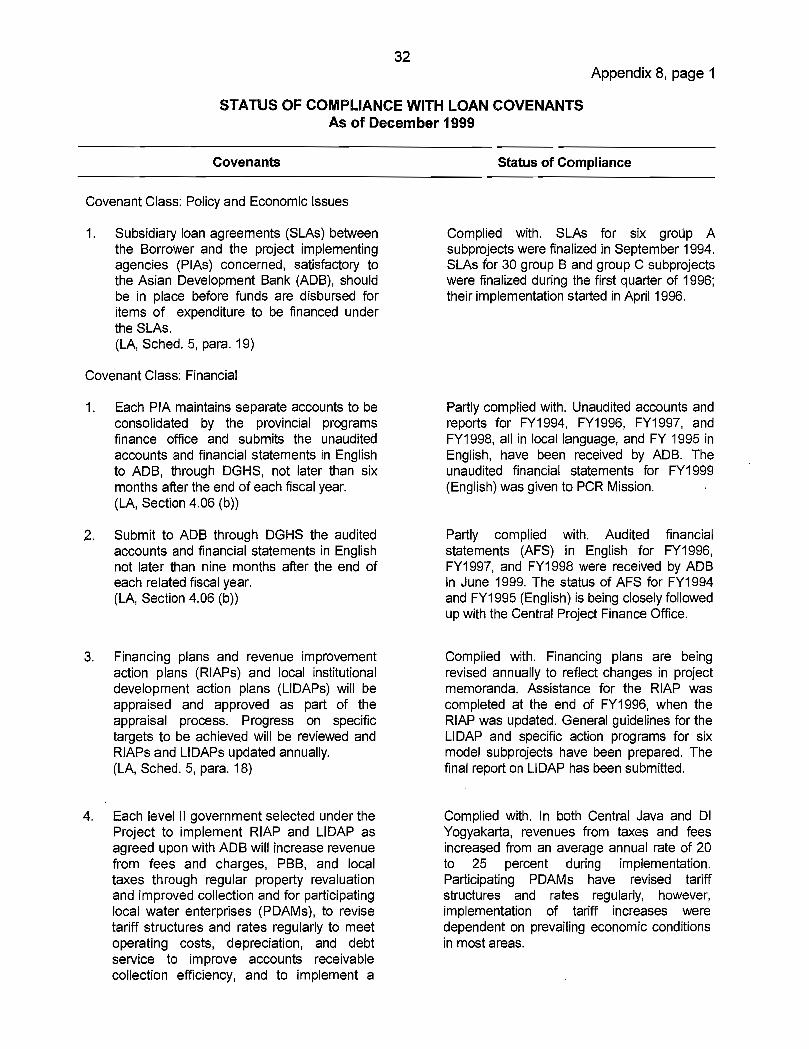

G. Conditions and Covenants

23. The conditions and covenants under the Loan Agreement were generallycomplied with. However, submission of audit reports was not satisfactory, as they wereoften late and untranslated. ADB's suggestion to use private auditors was considered

The ADB Review Committee on Anticorruption conducted an independent investigation of the case. Thereport was communicated to the Government with a request to reimburse $207,741 to ADB.

7

but not adopted because of lack of funds. The delays are attributable mainly to thepractical difficulty of preparing audit reports for a project involving local governments andother PDAM5. This aspect needs to be considered and practicable solutions offered insimilar undertakings in the future. PBME reports were submitted to ADB with ther&evant indicators on technical performance, and social and economic benefits on low-income communities. The status of compliance with loan covenants is in Appendix 8.

H. Disbursements

24. Total ADB loan disbursements amounted to $126 million or 66 percent of therevised loan amount of $147.2 million after cancellation of $2.8 million in July 1998. Afurther $21.2 million was cancelled in December 1999. Actual disbursements are shownin Appendix 9.

I. Environmental and Social Impacts

25. The various project components were generally small-scale, particularly in CJ,and had no adverse impacts on the environment. Several components have improvedthe environment of the cities, including (i) quality of water supply and discharged water;(ii) sanitation through construction of public toilets and sewerage plants; (iii) solid wastemanagement through the supply of handcarts and garbage trucks, and the developmentof transfer depots and disposal sites that have reduced the amount of waste on thestreets and in the drains; and (iv) urban roads construction that has resulted in improvedaccess for agricultural communities and reduced traffic congestion.

26. The social impacts include better access to clean water, improved sanitation andwaste collection, more , efficient road transportation, as well as infrastructureimprovements in low-income areas such as KIP areas. As a result, less time is neededto fetch water or dispose of solid waste, thereby allowing more time for productiveactivities such as farming and cottage industries. This enables the communities to raiseliving standards while contributing to increased economic outputs. The construction ofroads, drainage, and MIIP have provided impetus for higher levels of social andeconomic investments, raising the commercial value of properties along improved roads.No community resettlement was required. While community participation wasencouraged by consulting with the beneficiary communities on the acceptability ofsubprojects, more effort is needed for the community to be involved in initiating,planning, and implementing subprojects as well as defining their responsibilities "forO&M. In most of the subproject areas visited by the Mission, local communities areactively involved in the KIP and drainage subprojects.

J. Performance of the Borrower and the Executing Agency

27. During the course of the Project, the Government made considerable effort toensure timely and successful implementation, such as the quick response to thefinancial difficulties encountered in 1997 by devising the community-based labor-intensive program. Through the Project, DGHS and the local governments haveaccumulated substantial experience in preparing and implementing IUIDP projects. ForPBME, 6 comprehensive surveys were undertaken by the PlUs, which prepared the

6 PBME ndicators were based on five pilot project areas: Kab. Banyumas, Kab. Klaten, Kod. Yogyakarta,Kab. Jepara, and Kab. Batang.

8

relevant baseline data and monitoredwas undertaken in close coordinationdirection of DGHS, and was effectivetimely corrective actions.

K. Performance of ADB

the changes far project evaluation. This activitywith the Qentral and provincial PMUs under thein identifying project deficiencies and facilitating

28. During implementation, ADB provided a total input of 371 staff days and fielded12 review missions. Ten of the review missions were undertaken together with thereview of other projects. While the missions enabled ADB to support physical projectimplementation, more efforts could have been made on institutional development texamine development impacts. The project design was generally adequate. Theassessment of the implementation capacity of the participating agencies may have beensomewhat overoptimistic. The Indonesia Resident Mission assisted with disbursementsand Government liaison.

III. EVALUATION OF INITIAL PERFORMANCE AND BENEFITS

A. Financial Performance

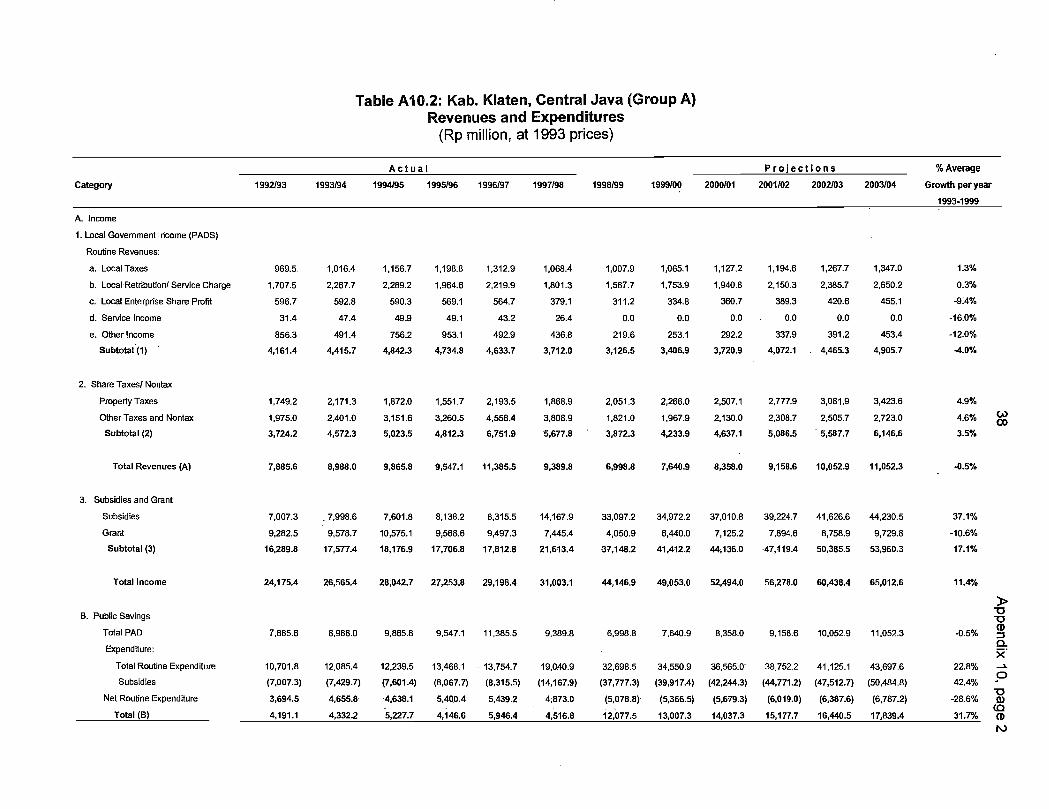

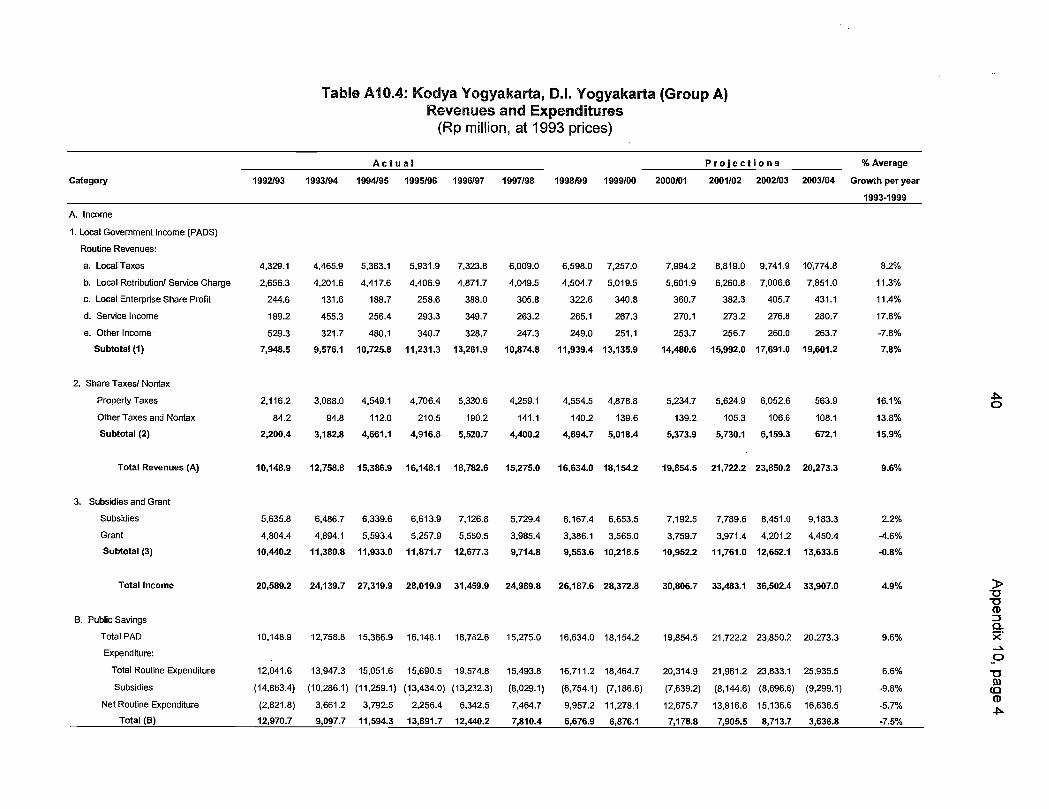

29. One of the project objectives was to improve the financial capacity of localagencies. A major target was to improve the financial resource mobilization at the locallevel by increasing user charges and property taxation, and improving financialmanagement. Among sample local governments, 7 local revenues increased, in realterms, from 1.3 percent to 26 percent between FY1993 and FY1999 (Appendix 10).Contributing factors include more intensive revenue collection efforts (higher collectionefficiency), more defined revenue targets, and strict monitoring by the governments. Inall the sample local governments, local revenues ranged from 46 percent of total incomefor Kab. Klaten to 72 percent for Kod. Yogyakarta, and about 50-60 percent of totalincome for the others. 8 About 60-90 percent of total income was spent on routineexpenditures, such as improvement in services, leaving minimal surplus operatingincome for capital expenditures. The RIAP helped the local governments to focus on theneed for financial improvements, although some measures had been implemented to alimited extent due to economic difficulties encountered in the financial crisis since late1997.

30. Financial targets set for the PDAMs at appraisal included improving customercollections to about 90 percent of accounts receivables. Collection efficiency hasimproved to about 88 percent at present. Tariff increases were implemented by most ofthe PDAMs until the financial crisis in 1997 and 1998. In some cases the tariff increasewas substantial. PDAM Kod. Yogyakarta was permitted to increase the tariff by 75percent in phases; from Rp200 to Rp350 per cubic meter for households, allowing themto cover their debt service. However, the proposed tariff increase in Kab. Semarang wasnot approved in view of the pending financial restructuring. The financial performance ofsample PDAMs is in Appendix 11. Financial projections allow for tariff increases in 2000

Sample governments include Kab. Klaten, Kod. Yogyakarta and Kab. Bantul under group A, Kab.Pekalongan and Kab. Sukoharjo under group B, and Kab. Jepara under group C. PDAMS include PDAMKab. Kiaten and PDAM Kod. Yogyakarta under group A, POAM Kab. Pekalongan under group B, andPDAM Kab. Jepara under Group C.

The other sources of local government income comprised subsidies and grants from the central andprovincial governments.

9

in most PDAMs. With the current economic crisis, however, it is now unlikely that theseincreases will be implemented expeditiously. In most municipalities, it is understood thatthe increases will be implemented in phases in consultation with water users.

31 Financial reevaluation was undertaken for the revenue-generating projects,including water supply, solid waste, and sanitation components. The results werecompared with those in the subproject appraisal reports (SPARs) submitted to ADB priorto project implementation. Appendix 12 presents the methodology and summary resultsof the financial internal rate of return (FIRR) and econornicinternal rate of return (EIRR)calculations, which are based on actual field data. Generally, FIRRs for water supplywere higher than those at appraisal, due to successful implementation of water supplyprojects, particularly in increasing production capacity and expanding service coverage.Only PDAM Kab. Semarang registered an FIRR below the weighted average cost ofcapital because of the delays encountered in house connections. The higher FIRRresults in Kab. Klaten, Bantul, and Kod. Yogyakarta were due to periodic increases andsubstantial adjustments in water tariff.

32. Solid waste management components have shown better results in the sampledistricts due to a larger number of households and effective community-based feecollection systems. For sanitation, the FlRRs were generall.y above the weightedaverage cost of capital. Local communities collect sanitation fees for the district, and aportion of the fees is kept. by the communities to maintain the facilities. Managementimprovement for O&M of solid waste and sanitation infrastructure is needed to reduceexpenditure on O&M.

B. Economic Performance

33. The economic internal rates of return (EIRRs) were reevaluated for nonrevenuegenerating components (urban. roads, drainage, and KIP/MIIP). The main assumptionsand the methodology adopted for the economic reevaluation, and detailed discussion ofthe results are also shown, in Appendix 12. Urban roads projects are generally separatedfrom drainage projects in the areas visited. For drainage, SPAR estimates wererelatively higher comparedwith actual EIRRs due to optimistic target benefits, e.g., muchhigher land value being assumed. For urban roads, the project benefits were realizedand in the more urbanized areas, benefits were higher than appraised. KIP/MIIPcomponents were also economically justified as a result of a higher increase in landvalues, in view of the estimated 12 percent opportunity cost of capital in 'Indonesia

C. Attainment of Benefits

Improvement in Urban Infrastructure and Services

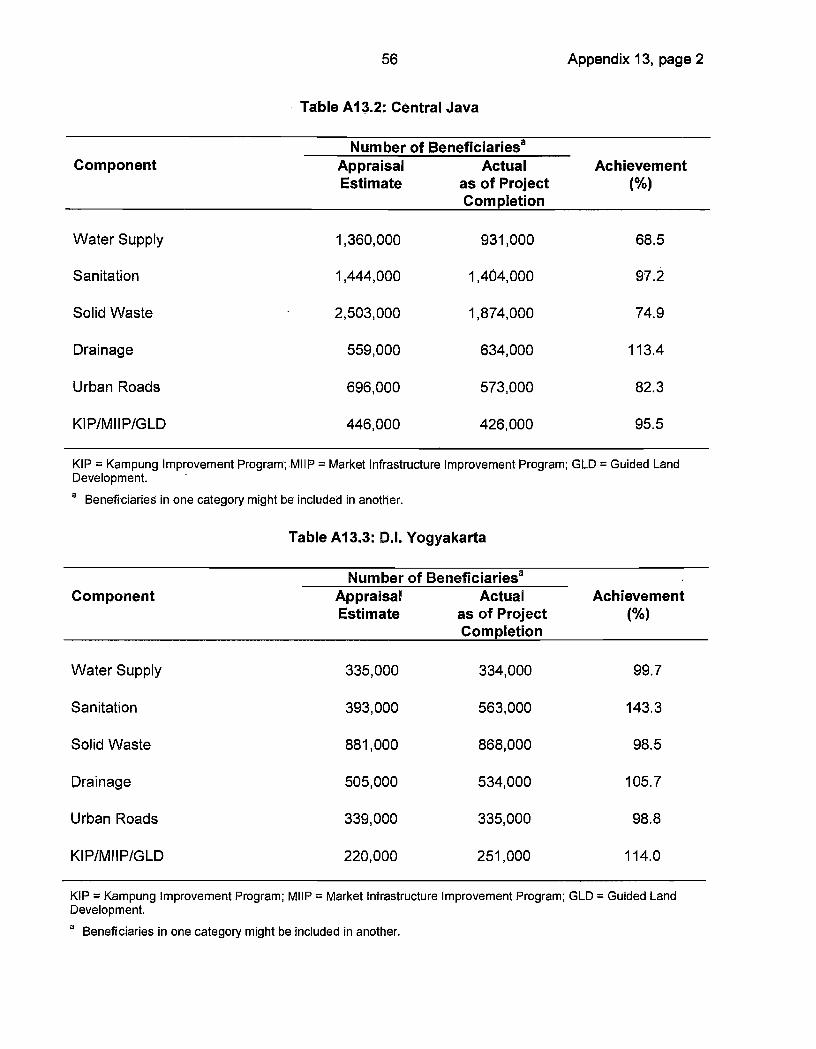

34. Overall, the targets were met. A total of 8.7 million people9 are estimated to havebenefited from improved access to urban services as a result of the Project. This isabout 90 percent of the appraisal target of 9.7 million. The labor-intensive work programhelped mitigate the intensified poverty situation after the financial downturn in 1997. Thebeneficiary coverage for the different subproject components are summarized for eachsector in Appendix 13.

The number of beneficiaries is the aggregate of the number of people who have benefited from eachsubsector.

10

a. Water Supply

35. The water supply components benefited some 1.26 million persons (in 31districts), about 75 percent of the target. Service coverage for domestic users rose froman average of 33 percent to 47 perOent in CJ. Service coverage for hondomestic usersincreased from an average of 75 percent to 91 percent.

36. Water supply facilities installed under the Project are well maintained. However,improvements in the operational and financial performance of the PDAMs throughprudent management with the support of RIAPs and LIDAPs is necessary. The financial,crisis has affected the performance of smaller PDAMs. Progress has been made in UFWreduction, noW averaging about 27 percent in the project area, compared to averagesfrom 35 to 60 percent nationwide. The emphasis on UFW reduction efforts needs to becontinued and a periodic leakage investigation program should be established.10

b. Sanitation

37. About 1.97 million people are benefiting from the sanitation program,representing 107 percent of the estimated target at appraisal. Overall, this componenthas resulted in a cleaner environment and healthier conditions for the project areas,particularly in the more remote rural communities where poor families cannot afford tobuild toilets in their homes. While O&M is largely the responsibility of local communities,there is room for improvement by raising public awareness of the benefits of publicsanitation facilities, and by charging modest user fees.

c. KIP, MIIP, and Guided Land Development

38. Over 677,000 persons benefited from the three components, meeting theappraised target. KIP and MIIP resulted in better access roads, drainage, and solidwaste collection in various local communities covering 25 districts. The KIP and MIIPcomponents were well implemented because of extensive community participation, andbenefited the low-income populations in the project areas.

d. Solid Waste

39. Despite difficulties in locating appropriate disposal sites, some 2.74 millionpersons, or about 81 percent of the target during appraisal, benefited from the solidwaste management subproject. The increased level of services and reduced amoUnt ofwaste on the streets have had a positive impact on public health. Communityparticipation has been successful in the O&M of solid waste facilities in mostcommunities.

10 ADB has provided further assistance in the water supply sector. TA 3137-lNO: Water Supply andSanitation Sector Project, for $600,000, approved on 22 December 1998, provides assistance tooperationalize the Government's policy and regulations governing PDAMs. The scope includes (i)identifying capacity-building requirements for local governments and PDAM5; (ii) recommending steps toreduce UFW; (iii) determining needs for maintenance and rehabilitation of existing water supply andsanitation facilities; (iv) strengthening the regulatory and legal frameworks; and (v) providing institutionalstrengthening to facilitate increased public participation, transparency, governance, financing capability,and sustainable development.

11

e. Drainage

40. This component was implemented in 32 districts and municipalities, andbenefited about 1.17 million persons, about 10 percent more than the target at appraisal.Drainage improvement included construction of new drainage linkages and upgrading ofexisting drainage systems. Routine maintenance of drainage systems is largelyundertaken by the local communities with the local government providing periodicmaintenance checks.

Urban Roads

41. About 0.9 million people or 88 percent of the appraised target benefited fromimproved urban roads. The improvements and new construction have had a positiveimpact by reducing congestion and vehicle time-savings in the urban areas, as well asimproving accessibility to the urban markets for the agricultural communities.

2. Integrated Urban Development and Management

42. The IUIDP was aimed at decentralizing urban development, enhancing the urbanfinancial resource base and financial management, and improving urban managementcapacity at the local levels, Through the provision of training as part of the institutionaldevelopment and capacity building components of the Project, progress was made in theinstitutional strengthening of local governments. However, more still needs to be done atthe local government level, in terms of planning for long-term development programsand the delivery of services. In particular, urban economic development planning at thelocal level still relies on public rather than private investment. While the RIAP and LIDAPhave been effective, a more focused approach through the Strategic UrbanDevelopment Action Plan (SUDAP) was found to be more appropriate (footnote 3). TheSUDAP is a planning approach aimed at enhancing urban management and urbanperformance by involving all stakeholders, i.e., all levels of government, professionalorganizations, nongovernment organizations (NGO5), business organizations,community groups, etc., to identify a vision for the region or municipality. Thus, specificneeds of stakeholders, deficiencies in existing public facilities and services, and localapproach in project design were identified in the pilot plans.

43. Insufficient funding and inadequate programming are still common weaknessesin some local governments. The new local autonomy policy to be implemented in 2000will transfer more responsibility and accountability to the local governments. The centralGovernment may need to provide local governments with more training andassistancéin rehabilitating and upgrading existing infrastructure, as well as improving O&M toensure sustainability of benefits. Communities must be involved to ensure thatinfrastructure projects meet actual demand and willingness to pay for services. The ADBCommunity and Local Government Support Sector Development Program loans 11 areexpected to stimulate local autonomy and fiscal decentralization.

Loan 1 677-INO: Community and Local Government Support Sector Development Program (poHcy loan),for $200 million, approved on 25 March 1999; and Loan 1678-INO: Community and Local GovernmentSupport Sector Development Program (investment project loan), for $120 million, approved on 25 March1999, focus on increasing of community participation in subprojebt formulation, planning, andimplementation, and policy initiatives to reform local government structures.

12

3. Training and Institutional Strengthening

44. While local governments have gained valuable experience in subprojectappraisal, as well as in the planning and executing of projects, efforts to enhance thecapability of local governments in preparing, evaluating, and approving subprojectsshould be continued. Institutional strengthening for DIY achieved better results due toearlier capacity building support from the Swiss Development Corporation. TheGovernment should develop a program to avoid losing trained staff to other agencies.Further efforts in this area, such as the ADB-funded loan project on capacity building,12may be utilized. It is recommended that selection Of participants for workshops andtraining should be carefully' made. Seminar and training materials should also beupgraded by incorporating lessons learned from previous training programs.

4. Participatory Development

45. The Project aimed to increase community ownership of subprojects. While therehas been active community participation in the KIP, public involvement in the O&M ofother public infrastructure and services varies. Each PIU was expected to undertake apublic information and public awareness campaign focusing on the use of projectfacilities and to encourage active community participation. The success of thesecampaigns varies and further efforts to promote community involvement are required.

5. Sustainability of Benefits

46. Institutional capacity building at the local level under the Project has improvedthe capability of local government officials in urban infrastructure development andfinancial management. The existing Government policy on decentralization of urban•infrastructure and services assumes greater mobilization of local fund resources andborrowing capacity. Due to the current economic situation and limited budget at all levelsof Government, there is a need for the local governments to improve their O&Mefficiency.

47. Although the Project has achieved its objectives to improve urban livingconditions in the project area, sustainability of project benefits has been affected by theeconomic crisis since mid-1997. Cutbacks in consumption have led to falling waterrevenues and lower tax collections for some districts and municipalities. O&M costs haveincreased due to inflation. Imported items were particularly affected by the currencydevaluation, and this has had a severe impact on PDAM operations. Declining revenuesand increasing O&M costs caused cash flow problems for some PDAMs. Constraints onlocal government expenditures are impeding future investments and the allocatioh ofsufficient funds for O&M and debt service. However, the situation is expected to improveas the economy stabilizes.

48. Under the Government's new initiatives, which focus on local autonomy anddecentralization, there will be a different environment for implementation of futureprojects and an enhanced need for capacity building at the local level. Three TAs' 3 wereapproved under the ADB loan, Community and Local Government Support Sector

12 Loan 1572-INO: Capacity Building in Urban Infrastructure Management, for $42 million, approved on 4November 1997.

13 TA 3177-lNO: Capacity Building to Support Decentralized Administrative Systems, for $500,000,approved on 25 March 1999; TA 31 78-INO: Capacity Building to Support District Level BudgetarySystems, for $460,000, approved on 25 March 1999; and TA 3179-INO: Capacity Building onParticipatory Planning, Monitoring, and Evaluation, for $540,000, approved on 25 March 1999.

13

Dev&opment Program (footnote 11). The TAs will provide capacity building at the locallevel to support implementation of the Government's initiatives. By improving thecapacity for community-based activities, the TAs are expected to strengthen thedecentralization efforts, thereby enhancing cost effectiveness and promotingsustainability of benefits.

6. Community Participation

49. Community participation was initially limited to determining the location of projectfacilities, such as public taps, family toilets, communal toilets, and temporary wastedumping sites under the subsectors of water supply, sanitation, solid waste, and KIP. Atthe construction stage, community-based labor was used in physical works. Tostrengthen community participation, an intensive public information campaign needs tobe undertaken by the local governments prior to project completion to increase people'sawareness of the O&M benefits. The communities, particulary those in less urbanizedareas, need to become more involved in initiating, planning, and implementingsubprojects. In some communities, a community organization for managing solid wastecollectively was formed to collect fees and to manage the collection and transportation of•the waste to the transfer stations. Transport of the waste from the transfer station to thefinal disposal site is undertaken by the local public works agencies. Such organizationstructure reduces the burden on the local governments in operations administration andshould be encouraged.

50. The Project benefited the poor communities within the project area, particularlysmaller municipalities, which have much lower tax revenues and thus cannot afford toprovide adequate infrastructure facilities to the poor in remote areas. The poor compriseabout 20-40 percent of the population in these municipalities.

51. In most of the project sites visited, it was noted that the poor benefited the mostfrom the upgrading of local roads and drainage canals, and the provision of family andcommunal toilets in kampungs. There has been a positive impact in terms of the poorpaying lower transport cost per km (30-40 percent lower). Prior to construction of thelocal roads under the Project, children in poor families had to walk severa' kilometers toreach school. Now they are served by public transport. Likewise, farmers used to haveto pay high rent for cargo vehicles because the roads were not paved. With theconstruction of urban roads under the Project, cargo transport vehicles now chargefarmers lower rates to bring their products to market. Statistics indicate that incomes offarmers have increased by about 20-30 percent despite the economic crisis, because ofincreased accessibility to markets.

52. The construction of sanitation facilities improved health conditions of the poorcommunities. Communal toilets were constructed in the kampungs for use by poorfamilies who cannot afford to build their own toilets. The provision of this basic servicehas improved the living conditions of the poor through better prevention of disease. Theavailability of disposal sites for domestic wastes has benefited poor families in terms of acleaner environment. Poverty is reduced where some poor families are employed towork in the landfill and disposal sites providing them with an income source. Thedrainage component has a positive impact on the poor as the reduction in flooding ofmajor agricultural areas has eliminated damage to their homes and property. Many poorfamilies have also been hired as construction laborers in these projects. The costsavings from this component are about Rp200,000 per family.

14

8. Issues and Follow-On Efforts Required

53. The financial and economic crises in Indonesia have resulted in jobs lost,declining incomes, and increasing costs in many of the project towns. Some PDAMs areencountering financial difficulties from increased O&M costs and declining revenues dueto closure of many commercial and business establishments. Furthermore, decreasinglocal government revenue collections have resulted in reduced capital expenditure, thuslimiting future investments and the allocation, of sufficient funds for O&M of urbaninfrastructure. The Government has taken action to improve the situation, includingemployment generation through labor-intensive works, accelerating the decentralizationof government establishing transparent electoral processes, institutionalizing communityparticipation, and increasing NGO involvement. Sustainability of benefits is beingfollowed up by mobilizing community participation in service delivery and maintenance ofexisting facilities. Some of the issues noted in the Project, including the need for strongercommunity participation, increased decentralization, and enhanced capacity building oflocal governments, were addressed in the ADB Sector Development Program loan(footnote 11).

54. There is a need for the provincial government in Central Java to promote the jointundertaking of urban infrastructure facilities for sanitation, solid waste and drainage forôost-effective utilization of resources, cost-efficient O&M, and delivery of services. Thesanitation and solid waste facilities in Kab. Bantul, DIY are a model of such a project. Itis jointly operated by the local governments of Kab. Bantul, Kod. Yogyakarta, and Kab.Sleman; the O&M is the responsibility of the provincial DIY government.

55. Under the local autonomy decree, which promotes decentralization of power andresponsibility to the local governments, the delivery of basic services will rely solely onthe local governments. There is a need to further enhance the institutional and financialcapabilities of the local governments, as well as involve local communities and NGOs inthe provision and maintenance of urban infrastructure facilities. Future projects shouldbe more process-oriented rather than product-oriented, and should provide guidance onmanifesting a transparent and efficient implementation process.

IV. CONCLUSIONS AND RECOMMENDATIONS

A. CoAclusions

56 Notwithstanding the adverse impact on the revenue generation subprojects as aresult of the financial crisis, the Project has largely achieved its objectives and isassessed as generally successful. Most of the project components were completedexcept for some shortfall in water supply (only 61 percent of house connectionsachieved) and sanitation (only 51 percent of communal toilets built). The financial andeconomic viability of selected subcomponents has been generally affirmed in real termsfor revenue generating and nonrevenue generating components. The FIRRs weregenerally higher than the SPAR results at appraisal as a result of expansion of theservice area and more effective collection of user fees through local communityorganizations. The EIRRs were generally lower than estimated at appraisal for urbanroads, KIP, and drainage facilities, but exceeded the opportunity cOst of capital of 12percent. The estimated EIRRs in the SPAR were based on very optimistic conditionsand high economic growth projections. Due to the financial crisis, which resulted indownscaling of some high-impact sector projects, a more moderate level of benefit was

15

obtained. Project facilities are in operation and have for the most part been maintainedby local governments and communities. The financial crisis is likely to have an impact ontheir sustainability. Proposed major water supply tariff increases scheduled for 1999 and2000 have been postponed or revised to a phased program for the majority of thePDAMs, and there is a potential decrease in tax collection by the local governments.Nevertheless, more focus on optimizing existing investments should have a positiveeffect on the maintenance of project facilities. With the newly elected government andthe undertaking of the Reformation Program, Indonesia is expected to return to a morestable economic situation where benefits of the Project will be sustained.

57. As a sector loan, the Project has achieved its objectives to improve the variousurban subsectors under the IUIDP. Importantly, progress was made in strengthening theinstitutional capacities of the provincial and local governments. Government officialsacquired skills and experience in financial management, organization development,project planning and implementation, O&M, and community participation. While there isstill room for further improvement, these skills have prepared local governments to takeon. more responsibilities for urban infrastructure development and management underthe Government's new local autonomy law and decentralization policy.

58. Local communities have benefited from the physical components in upgradingtheir living standards and quality of life. At least 90 percent of the target populationidentified at appraisal . benefited from better urban infrastructure services. Localgovernments have also improved their institutional capacity for planning andimplementing small-scale projects. . Financial management at the local level has alsoimproved as a result of training under the Projedt. As the new Government isdecentralizing greater autonomy and financial responsibilities to local governments, theProject has provided , local officials with strengthened skills in project planning,implementation, and monitoring. In light of the greater emphasis on accountability,autonomy, and effective and efficient service provision at the local government levels,capacity building may still be needed, particularly in the financially weaker districts.

59. Project implementation provides some important lessons (Appendix 14):

(I) Decentralization of responsibility and ownership. Althbugh localcommunities have been involved in initiating planning, and implementingsubprojects under the IUIDP, there needs to be better coordination andsupervision by all levels of Government during implementation. Theinvolvement of beneficiary communities in developing projects will fosterproject ownership, thus ensuring adequate O&M.

(ii) Institutional strengthening at the local level for an IUIDP. Demandanalysis and user surveys for willingness and ability to pay should bedone thoroughly and accurately by the local governments at the outset offuture IUIDPs. Identification of appropriate sites for sanitation facilitiesand consultation with beneficiaries concerned should be undertaken.

(iii) Maintenance of project facilities. Projects should continue to provide astructural approach to identify responsibility for the maintenance of projectfacilities shared by two or more local governments. There should beregular reviews by ADB to ensure proper implementation. Capacity

16

building for O&M at the local levels should be included in the overallproject design.

(iv) Local borrowing capacity. Shortages of central and loôal governmentcounterpart funds can adversely impact on smooth projectimplementation. Mobilization of local sources of funds is critical to theimplementation of new Government policies on deôentralization of urbandevelopment and services and on lOcal autonomy. Future projects shouldcontinue to strengthen the revenue-generating capabilities of localgovernments.

(v) Implementation arrangements. Timely and accountable projectimplementation requires clear delineation of the responsibilities of eachparticipating agency. Technical assistance should have been provided notonly for the planning of the LIDAP but also its implementation.

C. Recommendations

1. Project Related

60. The Government and DGHS should consider the following:

(i) Strengthen linkages with future and related development plans bydecentralizing project planning and design by the local governments.Provide training and institutional strengthening at the local level,particularly in preparing and implementing the LIDAP and RIAP. Thetraining should focus more on specific needs and take into considerationdifferences in absorption capacity for implementing structural andinstitutional changes.

(ii) Improve the financial performance of local governments and weakPDAMs by improving financial management and enhancing userawareness of the need for timely tariff increases to improve revenue tocover O&M expenses and debt service. Recruit professional financialmanager for PDAMs. Mobilize community groups to maintain small-scaleproject facilities.

(iii) Improve auditing procedures of financial statements and their submissionto comply with the loan covenants. Closely coordinate the submission ofthe audited financial statements by the various agencies.

(iv) Provide or develop more effective and extensive public information,education, and communication programs to increase the community'sawareness of the project facilities and their usage, as well as theimportance of O&M of the facilities. Such programs should be designed atthe local level.

2. General

61. The Project has enabled new directions for policy dialogue in the following areas:

(i) Decentralization and Devolution of Authority. In support of theGovernment's new fiscal decentralization law (Law No. 25/1999), whichdecentralizes more power and financial responsibility to the local

17

governments, future projects should (a) emphasize improving the abilityof local governments to deliver sustainable municipal services, ratherthan only on building new infrastructure; (b) balance the provision ofphysical infrastructure with complementary activities to promote economicdevelopment, employment creation, and income generation; (c) promotejoint undertaking of sector projects by two or more local governments tomaximize the use of government financial resources; and (d) design tobetter fit the organizational structure of local and provincial governmentsto ensure efficient implementation and effective mOnitoring and evaluationof project benefits. ADB has provided continued assistance in support ofthe Government's thrust to decentralize urban development activities inaccordance with the newly enacted laws on regional autonomy and fiscaldecentralization.14

(ii) Full Cost Recovery and Loca' Revenue Improvement. Greaterattention should be given to O&M budget provision given the recenteconomic situation. O&M programs should clearly define the maintenanceresponsibilities of local governments and the communities. To encouragelocal governments to make adequate provision for maintenance, it maybe necessary to include this item in the local government expenditurebudget.

(iii) Urban Poverty Reduction. To ensure that benefits' reach areas. of urbanpoverty at the local level, future projects should focus on specific areaswithin cities. Local governments would be responsible for identifyingpriority areas of urban deprivation and for developing urban renewalstrategies for comprehensive improvement and development. A balanceof formal private sector and community-based initiatives with governmentfacilitation would be more cost effective and affordable. The localgovernments should initiate the identification of areas suitable for urbanupgrading, then undertake the work with NGOs, community groups,landowners, and other private entities tO ensure that physical andeconomic benefits of development can be directed to the targeted poorcommunities.

(iv) FoHow-On Project The. country's political and economic situation isexpected to improve over the next few years. There is an opportunity for afollow-on loan project with similar project components in CJ and DIY, but::with better coordination by public agencies, NGOs, the private sector, andlocal communities. The project could provide assistance with theimplementation of the decentralization and local autonomy policies withemphasis on (i) supporting community participation to ensure a demand-driven approach; (ii) increasing public-private partnerships in basicservices; (iii) improving O&M efficiency of existing and new facilities; (iv)improving access of the poor to urban services; and (iv) enhancing thecapacity of local governments in administrative and revenue functions,fiscal planning, and budgetary procedures.

14 TA 3326-INO: Urban SectorDevelopmentin a Decentralized Environment, for $600,000 million, approvedon 8 December 1999. The objective of the TA is to promote more efficient and effective urbandevelopment and management in Indonesia, and to enhance the awareness of local governments of themeasures necessary to meet the requirements of decentralization.

APPENDIXES

25

4,13

27

5,15

30

5,17

31

6,19

32

7,23

36

7,24

37

8,29

44

8,30

18

Number Title Page Cited on(page, para.)

I Chronology of Milestone Events 19 1, 4

2 Status of Completion of Project Components 20 1 4

3 Allocation of Infrastructure Project Investments by Province 23 2, 5and Subsector

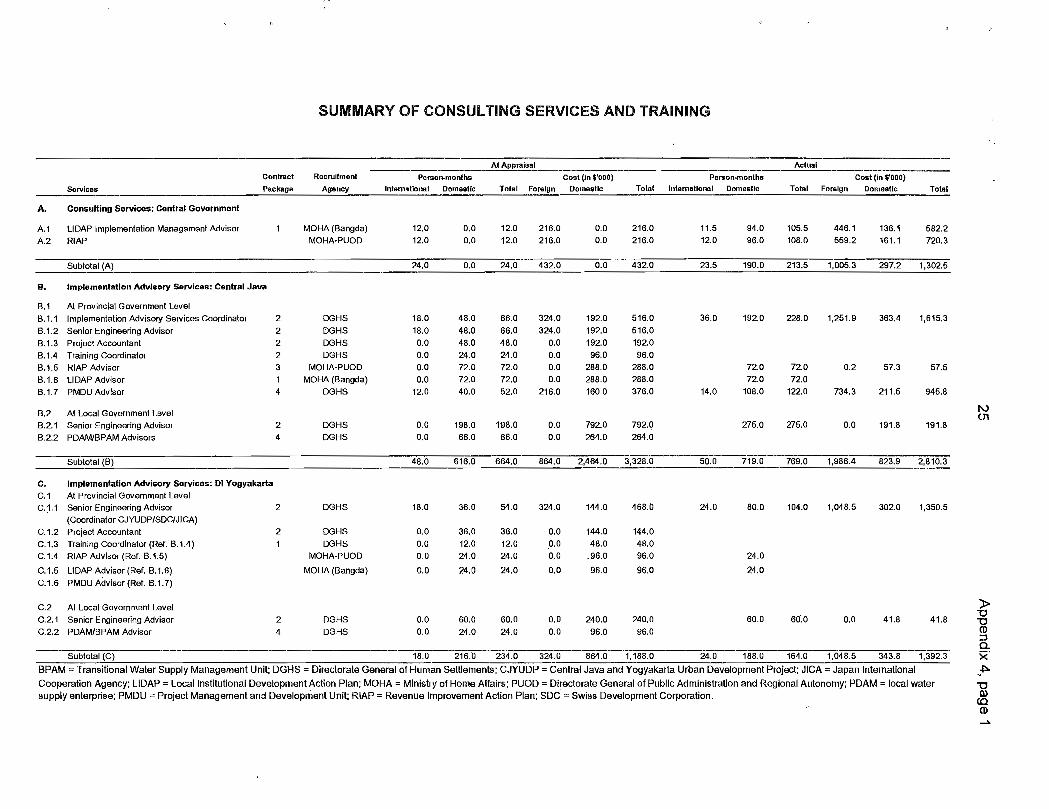

4 Summary of Consulting Services and Training

5 Organization Structure of Project Implementation

6 Project Cost At Appraisal and Actual

7 Project Implementation Schedule

8 Status of Compliance with Loan Covenants

9 Actual Loan Disbursements

10 Financial Performance of Sample Local Governments

11 Financial Statements of Sample Water Supply Enterprises(PDAMs)

12 Economic and Financial Analyses

13 Project Benefits and Impacts

14 Lessons Learned and Actions Taken or To Be Taken

49 9, 31

55 9,34

57 15,59

19

Appendix 1

CHRONOLOGY OF MILESTONE EVENTS

1992 November - Loan approval

1993 February - Loan signing (10 February 1993)1993 March - Loan effectiveness (24 March 1993)1992 July - Actual start of implementation

(advance action)

1993 September - First disbursement

1998 July - Reallocation of loan proceeds1998 July - Cancellation of loan savings

1998 September - Original date of physical completion

1998 September - Original date of loan closing1999 March - First extension of loan closing date1999 March - Physical completion

- Final disbursement

- Cancellation of $21.2 million from ordinarycapital resources

- Closing of loan account1

1999 December - Project completion review by the AsianDevelopment Bank

1 The loan account is kept open pending settlement by the Borrower of $0.21 million related to disbursements.

20,171.00523.00

0.001.00

11.00

1,853.00140.00

16,034.00688.00

0.001.00

10.00

2,139.00150.00

12,538.00394.00

16.001.00

10.00

1,833.00127.00

8685

7857

100100

203.0063.0049.0020.00

108.001,736.00

112.0044.0045.0019.0098.00

1,213.00

118.0044.0052.0019.0054.00

1,209.00

10510011610055

100

87.07

55.43

52.73

95

232.14

190.91

185.39

97

49.45

24.10

40.50

168

434.79

345.20

819.00

237

20

Appendix 2, page 1

STATUS OF COMPLETION OF PROJECT COMPONENTS

Table A2.1: Central Java and Di. Yogyakarta

Target Percentage

Item At Appraisal Revised a Actual AchievedA B C C/B

Water SupplyCapacity (Uters/sec)

2,336.00

2,336.00

1,729.00

74House Connections (no.)

98,345.00

79,271.00

48,268.00

61Public Hydrant (no.)

897.00

561.00

397.00

71Transmission Pipes (km)

242.83

181.16

17644

97Distribution Pipes (km)

1,005.31

1,090.53

864.24

79Reservoirs (no.)

22.00

22.00

22.00

100

Sanitation b

Family Toilet (no.)Communal Toilet (no.)Vacuum Truck (no.)Sewage Treatment Plant (no.)Wastewater Disposal (no.)

KIP/MIIP/GLDArea (hectare)Locations (no.)

Solid WasteGarbage Trucks (no.)Transfer Depot (no.)Final DisposallTPA (hectare)TPA (no.)Container/TPS (no.)Handcarts (no)

DrainagePrimary (km)Secondary (krn)Tertiary (km)Flood Controlled Area (hectare)

Urban Roads C

Arterial (km) 27.00 11.00 19.08 173Collector (km) 300.37 137.00 149.21 109Local (km) 561.70 464.20 290.48 63GLD = Guided Land Development; KIP = Kampung Improvement Program; MIIP = Market InfrastructureImprovement Program; TPA = final disposal site; TPS = temporary waste dumping site.a Revised as of 1995.b Due to unavailable space particularly in Kod. Yogyakarta, the planned construction of family toilets was not

implemented.C There were canceled programs due to cancellation of counterpart funds from the central Government.

21 Appendix 2, page 2

Tábe A2.2: Central Java

Target PercentageItem At Appraisal Revised a Actual Achieved

A B C C/B

Water SupplyCapacity (liters/sec) 1,751.00 1,751.00 1,144.00 65House Connections (no.) 98,345.00 75,439.00 43,479.00 58Public Hydrant (no.) 897.00 377.00 239.00 63Transmission Pipes (km) 242.83 176.24 171,52 97Distribution Pipes (km) 1,005.31 909.99 713.14 78Reservoirs (no.) 22.00 20.00 19.00 95

SanitationFamilyToilet(no.) . 7,771.00 4,514.00 4,514.00 100Communal Toilet (no.) 521.00 686.00 394.00. 57Vacuum Truck (no.) 0.00 ' 0.00 10.00 -Sewage Treatment'Plant (no.) 0,00 0.00 ' 0.00 -Wastewater Disposal (no.) ' 11.00 10.00 10.00 100

KIP/MUP/GLDArea (hectare) '1,155.00 ' ' 1,313,00 1,165.00 89Locations (no.) " 102.00 ' 112.00 94.00 . 84

Solid WasteGarbage Trucks (no.) 181.00 91.00 90.00 99Transfer Depot (no.) , 59.00 40.00 41.00 , 103Final DisposalITPA (hectare) , 38.00 . 34.00 '35.60 105TPA(no.) ". 18.00 ' 17.00. 17.00 , . 100,Container/TPS (no.) ' 26.00 . 16.00 5.00 31Handcarts (no.) "1,199.00 676.00 696.00 103

DrainagePrimary (km) , ' 72.00 44.76 35.12 78Secondary (km) , 191.00 147.40 123.43 84Tertiary (km) 34.00 , 16.75 , 15.99 95Flood Controlled Area (hectare) 418.00 327.00 ' 819.00 " 250

Urban Roads b

Arterial (km) ' " , " 27.00 ' 11.00 10.85 99Collector (km) ' ". 264.00 , 137.00 137.49 ' 100Local (km) . 389.00... '' ' . 289.00 ,289.00 100GLD = Guided Land Development; KIP = KampuAg Improvement Program; MIIP = Market InfrastructureImprovement Program; IPA = final disposal site; TPS = temporary waste dumping site.a Revised as of 1995.b There were canceled programs due to cancellation of counterpart funds from the central Government.

12,400.002.000.001.000.00

11,520.002.000.001.000.00

8,024.00 70

0.00 0

6.00 -

1.00 100

0.00 -

13375

1451006096

28.003.00

16.002.00

49.00513.00

21.004.00

11.002.00

82.00537.00

22.004.00

11.002.00

82.00537.00

15.07

10.67

17.61

165

41.14

43.51

61.96

142

15.45

7.35

24.51

333

16.79

18.20

0.09

0

22

Appendix 2, page 3

Table A2.3: 0.1. Yogyakarta

Target PercentageItem At Appraisal Revised a Actual Achieved

A B C C/B

Water SupplyCapacity (liters/sec) 585.00 585.00 585.00 100House Connections (no) 3 832 00 3,832 00 4,789 00 125Public Hydrant (no.) 184.00 184.00 158.00 86Transmission Pipes (km) 4.50 4.92 4.92 100Distribution Pipes (km) 180.04 180.54 171.10 95Reservoirs (no.) 2.00 2.00 3.00 150

Sanitation b

Family Toilet (no.)Communal Toilet (no.)Vacuum Truck (no.)Sewage Treatment Plant (no.)Wastewater Disposal (no.)

KIP/MIIP/GLDArea (hectare)

698.00

826.00

668.00

81Locations (no.)

38.00

38.00

5.00

13

Solid WasteGarbage Trucks (no.)Transfer Depot (no.)Final Disposal/TPA (hectare)TPA (no.)Container/TPS (no.)Handcarts (no.)

DrainagePrimary (km)Secondary (km)Tertiary (km)Flood Controlled Area (hectare)

Urban Roads C

Arterial (km) 0.00 0.00 8.23 -Collector(km) 36.37 0.00 11.72 -Local (km) 172.70 175.20 1.48GLD = Guided Land Development; KIP = Kampung Improvement Program; MIIP Market InfrastructureImprovement Program TPA = final disposal site TPS = temporary waste dumping sitea Revised as of 1995.b Due to unavailable space particularly in Kod. Yogyakarta, the planned construction of family toilets was not

implemented.There were canceled programs due to cancellation of counterpart funds from the central Government.

11,076

5,477

0

1,631

3,832

0

136

40,478

39,137

0

1,204

0

0

136

4,061

857

0

1,700

311

757

435

4,902

0

926

1,186

1,555

1,098

136

21,732

5,472

1,398

3,280

7,987

3,068

527

9,713

9,645

0

0

0

0

68

8,932

6,325

0

1,126

751

526

204

6,972

3,574

58

788

1,532

952

68

11,489

5,893

100

1,932

2,478

790

296

7,536

562

0

1,067

4,815

814

279

15,915

1,266

764

3,753

6,329

3,650

152

4,810

0

640

1401

0

2,702

68

4,116

0

388

665

2,178

817

68

9,599

5,217

373

1,215

1,245

1,412

136

5,525

2,356

389

363

1,806

611

0

3,979

0

404

637

1,962

908

68

9,482

3,805

122

710

3,397

1,092

355

3,598

0

812

854

0

292

1,640

3,265

880

0

834

0

1,130

420

4,334

0

141

792

1,536

1,247

619

1,089

1,021

0

0

0

0

68

4,419

2,525

1,131

763

0

0

0

197,022

94,013

7,646

25,900

41,715

21.868

5,880

1,770

0

0

663

0

0

642

10,210

5,827

465

1,047

1,840

1,093

0

2,675

2,675

404

0

0

0

0

7,330

4,990

0

753

904

605

0

3,896

0

78

861

1,149

993

893

2,482

0

0

626

629

393

587

28,363

13,492

947

3,950

4,522

3,084

2,122

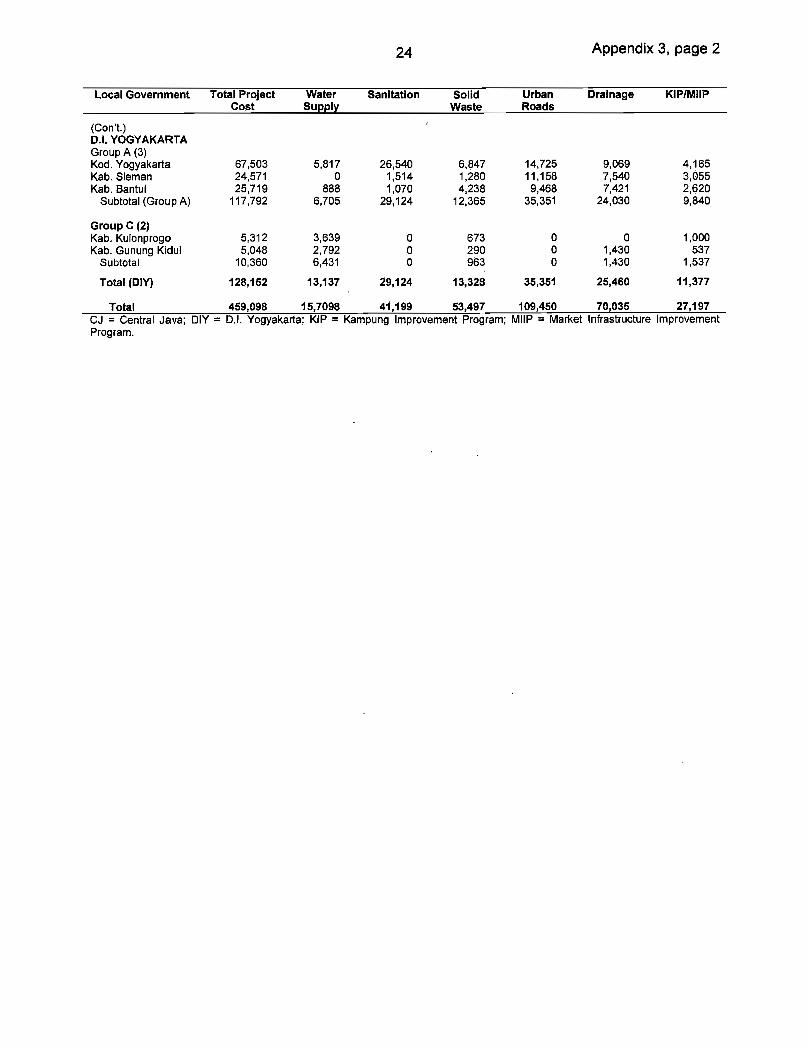

23 Appendix 3, page 1

llI

1. Of the total infrastructure project cost of Rp459.1 billion, Central Java obtained Rp330.9billion, or 72 percent of the' total infrastructure cost, while Di. Yogyakarta's share is Rpl 28.1billion, or 28 percent of total infrastructure project cost. The D.l. Yogyakarta project areacomprises five local governments, while Central Java has 35 local governments. Table A3presents the various project amounts by local government.

2. In terms of sectoral distribution of infrastructure projects, water supply has the largestshare of 34 percent of the total cost; urban roads, 24 percent; drainage, 15 percent; solid waste,12 percent; sanitation, 9 percent; and Kampung Improvement Program/Market InfrastructureImprovement Program (KIP/MIIP), 6 .percent. Table A3 presents the various projects bysubsector.

Table A3. Project Cost of Infrastructure for Central Java and Di. Yogyakarta(Rp million)

Local Government Total Project Water Sanitation Solid Urban Drainage KIP/MIIPCost Supply Waste Roads

CENTRAL JAVAGroup A (4)Kab. Klaten 18,306 3,509 213 1,068 8,316 3,000 2,200Kab. Banyumas 34,534 16,277 942 2,691 7,755 4,769 2,100Kab. Cilacap 31,575 10,789 1,590 2,773 5,589 8,670 2,164Kod. Pekalongan 21,146 5,881 737 3,787 6,203 3,184 1,354

Subtotal (Group A) 105,561 36,456 3,482 10,319 27,863 19,623 7,818

Group B (22)Kab. KendalKab. SemarangKab. BrebesKab. TegalKab. PemalangKab. WonogiriKab. Boyo!aliKab. SukoharjoKab. BatangKab. PekalonganKod. TegalKab. KudusKab. GroboganKab. PatiKab. BloraKab. KaranganyarKab. TemanggungKab. WonosoboKab. KebumenKab. PurworejoKab. BanjarnegaraKod. Magelang

Subtotal (Group B)