Asia Pacific Oils and Fats Situation...

38

Asia Pacific Oils and Fats Situation Overview Mohammad Hafezh bin Abdul Rahman Market Analyst, Asia Pacific Region

Transcript of Asia Pacific Oils and Fats Situation...

Asia Pacific Oils and Fats Situation Overview

Mohammad Hafezh bin Abdul Rahman

Market Analyst, Asia Pacific Region

Executive Summary

Oils and Fats Overview

Oils and fats situation in the Asia Pacific Region

Palm oil situation in the region

Economics

Macro views

Potentials in the Region

Conclusions

PART I: OILS AND FATS OVERVIEW Oils and fats situation in the Asia Pacific region

('000 T) 2009 2010 2011 2012 2013E 2014F

Opening Stock 5,245.8 4,886.5 4,958.1 6,708.1 8,410.9 6,382.4 Production 50,864.4 52,026.1 56,021.6 59,586.4 62,099.4 64,545.3 Import 5,867.1 6,849.0 8,306.0 8,276.7 6,796.1 7,322.4 Export 38,053.0 38,838.1 40,627.5 42,300.0 45,799.2 47,236.4 Consumption 19,038.4 20,078.6 21,961.2 23,880.9 25,390.8 26,940.9 Ending Stock 4,885.9 4,848.0 6,697.2 8,410.9 6,382.4 4,072.8 Stock Usage Ratio 8.6% 8.2% 10.7% 12.7% 9.0% 5.5%

Production of oils and fats in the region has shown strong growth in terms of volume where it records a 5% CAGR in 2009 – 2013 period. Palm oil made up of 72% of total oils and fats production in 2013

Stock to use ratio are expected to hit its lowest point in 2014 indicating that more consumption and less stock for oils and fats in the region due to increased biofuel mandates in Indonesia, Malaysia, Thailand and also Philippines

Consumption also increases due to increase in population, improved GDP which lead to increased per capita consumption spurring growth in various sector – food industry, oleochemicals, feed

Supply and Demand of Oils & Fats in the Region

Taking Palm Oil Out of the Asia Pacific Oils and Fats Supply

ASIA PACIFIC (‘000 MT) CAGR (2007-2013)

2007 2008 2009 2010 2011 2012 2013E 2014F Opening Stock 533.1 572.5 528.6 507.6 562.7 708.5 920.4 703.6 Production 6,478.1 6,716.9 6,669.2 7,349.2 7,055.3 7,742.4 8,129.7 8,314.8 3.06% Import 4,213.3 4,272.0 4,168.3 4,545.0 5,420.9 5,680.9 5,268.0 5,819.4 5.11% Export 1,702.5 1,779.3 1,466.6 2,003.1 1,791.1 1,810.7 2,278.6 2,171.3 1.03% Consumption 8,949.8 9,252.8 9,392.6 9,836.0 10,553.8 11,413.5 11,601.9 12,029.6 4.14% Ending Stock 572.2 529.3 506.9 562.7 697.6 920.4 703.6 636.9 Stock Usage Ratio 5.4% 4.8% 4.7% 4.8% 5.7% 7.0% 5.1% 4.5%

IF you take palm oil of the production equation it is observed that that growth in production has not been able to cope with growth in consumption in the region

Export also show a very small growth as local consumption increases. Imports recorded strong growth, in tandem with strong growth in demand

Imports of oils and fats in the region consist of 12.01% of the global oils and fats import. That is a decrease from the 2012 where total imports are 13.44% of global oils and fats imports

This could be due to drop in consumption growth due to weakness in the global economy as production growth is on the decline

10.71% 11.94%

14.07% 13.44%

12.01%

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00%

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000

2009 2010 2011 2012 2013

Oils and Fats Import ('000 MT)

Global O&F Imports Asia Pacific O&F Imports AP - Global Ratio

Imports of Oils and Fats in the Region

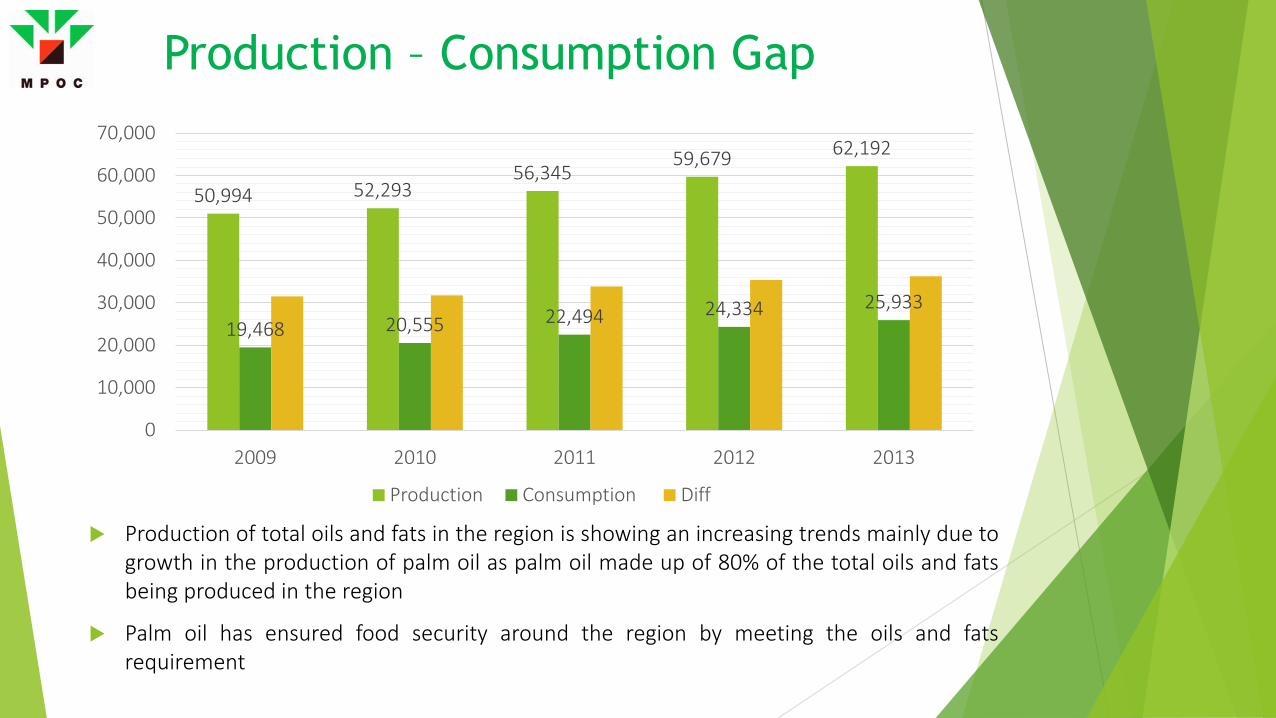

50,994 52,293 56,345

59,679 62,192

19,468 20,555 22,494 24,334 25,933

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2009 2010 2011 2012 2013

Production Consumption Diff

Production – Consumption Gap

Production of total oils and fats in the region is showing an increasing trends mainly due to growth in the production of palm oil as palm oil made up of 80% of the total oils and fats being produced in the region

Palm oil has ensured food security around the region by meeting the oils and fats requirement

31,526 31,738 33,851 35,345 36,259

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2009 2010 2011 2012 2013

Production Consumption Diff

Production – Consumption Gap

The production – consumption gap is widening in the region due to various demand factors i.e. increasing GDP, women empowerment – participation in labour, increased disposable income, lifestyle changes, industrialization and globalization

The huge consumption demand will not likely to diminish due to pressure from growing population and continued economic growth in the region

PART I: OILS AND FATS OVERVIEW Palm oil situation in the region

79.72%

79.10%

80.86% 80.62% 80.77%

78.00%

78.50%

79.00%

79.50%

80.00%

80.50%

81.00%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2009 2010 2011 2012 2013

Total Oils and Fats Production Palm Oil Production

Percentage of Oils and Fats Production

Palm Oil Production in the Region

Palm oil is the major oils and fats produced in the region, commanding around 80% of total oils and fats production for the last 5 years

Due to suitable planting climate, countries in the region opted to plant oil palm as gives the best yield per hectare which reflected to better dollar per hectare return for their farmers

Oil palm has also shown resilience which makes it easy to plant with trees produces yield as fast as 30 months. The only difference is the yield per hectare that depends on proper plantation management

Palm Oil Producing Countries

Palm Oil Production 2009 2010 2011 2012 2013 Indonesia 21,200 22,400 24,300 26,900 28,400

Malaysia 17,566 16,993 18,912 18,785 19,217

Philippines 90 92 87 98 106

Thailand 1,310 1,360 1,650 1,780 1,970

Solomon Isl 25 29 32 33 37

Papua/NGuinea 460 488 580 520 500

TOTAL 40,651 41,362 45,561 48,116 50,230

Palm oil’s main producer in the region is Indonesia, Malaysia and Thailand which are also the world’s top 3 palm oil producers

Growth in palm oil production correlates with the growth of oils and fats production and import in the region

Palm oil will continue to record strong growth in production which is shown in the 4.32% CAGR in the last 5 years. While Indonesia’s growth record a growth of 6.2%, Thailand showed the strongest growth with 8.1%. Production of palm oil in AP region made up of 90% of global palm oil production

Palm Oil Exports VS Global Oils and Fats Exports

41 38 36 34 34

64 67 68 73 75

63.67%

56.38% 53.08%

46.34% 44.67%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012 2013

Palm Oil Exports in Asia Pacific Global Oils and Fats Exports Percentage

In 2009, palm oil export in the region made up of 63.67% of the total global oils and fats export. This is due to strong demand from outside the region especially from India, Pakistan and EU

However, the trend showed a decline in percentage of total oils and fats exported as export of palm oil has slowly been reduced due to increased local consumptions over the years through population demand for food coupled with government’s policy for biofuel blends

Mil

MT

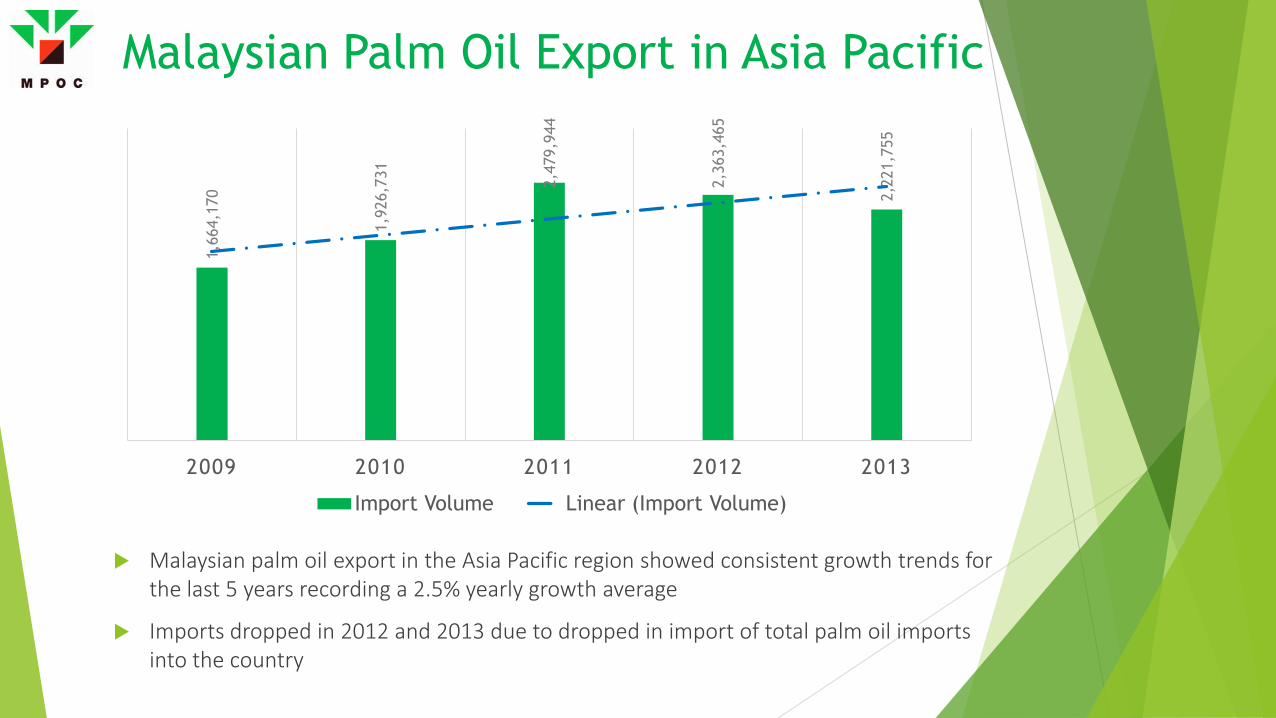

Malaysian Palm Oil Export in Asia Pacific

Malaysian palm oil export in the Asia Pacific region showed consistent growth trends for the last 5 years recording a 2.5% yearly growth average

Imports dropped in 2012 and 2013 due to dropped in import of total palm oil imports into the country

1,66

4,17

0

1,92

6,73

1

2,47

9,94

4

2,36

3,46

5

2,22

1,75

5

2009 2010 2011 2012 2013

Import Volume Linear (Import Volume)

Imports of Oils and Fats and Palm Oil in the Region

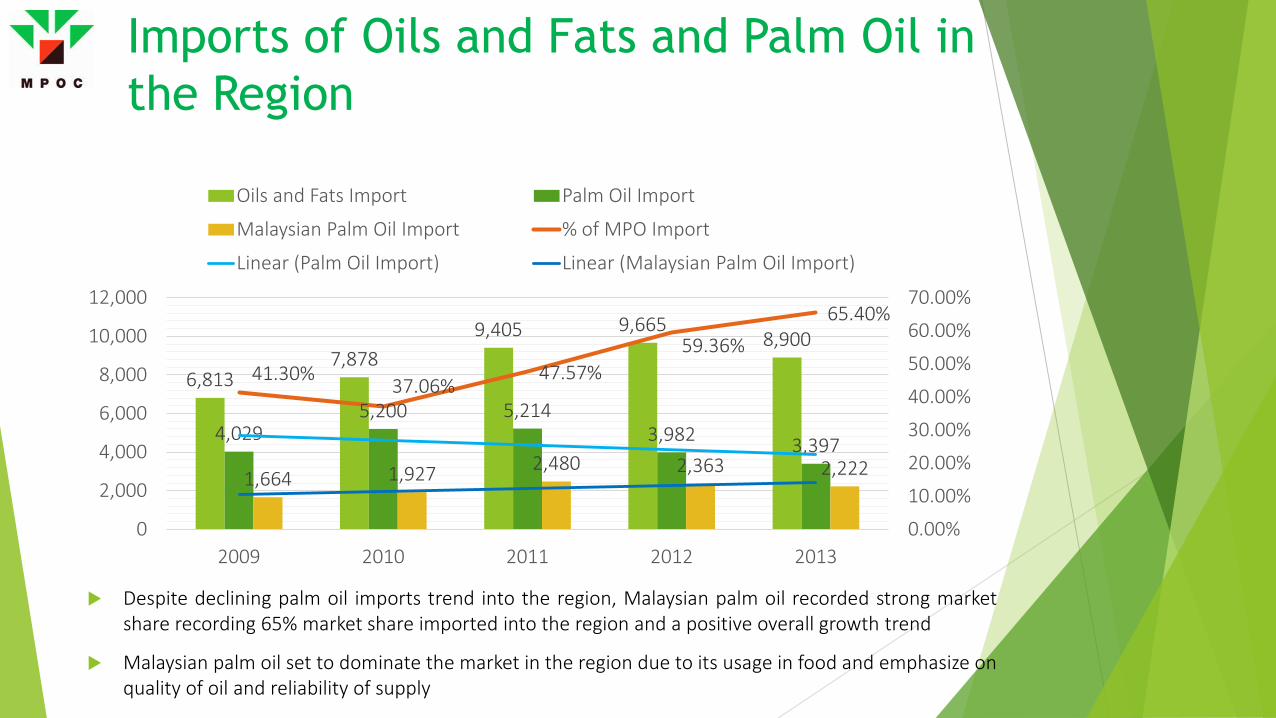

6,813 7,878

9,405 9,665 8,900

4,029 5,200 5,214

3,982 3,397

1,664 1,927 2,480 2,363 2,222

41.30% 37.06% 47.57%

59.36% 65.40%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

0

2,000

4,000

6,000

8,000

10,000

12,000

2009 2010 2011 2012 2013

Oils and Fats Import Palm Oil Import

Malaysian Palm Oil Import % of MPO Import

Linear (Palm Oil Import) Linear (Malaysian Palm Oil Import)

Despite declining palm oil imports trend into the region, Malaysian palm oil recorded strong market share recording 65% market share imported into the region and a positive overall growth trend

Malaysian palm oil set to dominate the market in the region due to its usage in food and emphasize on quality of oil and reliability of supply

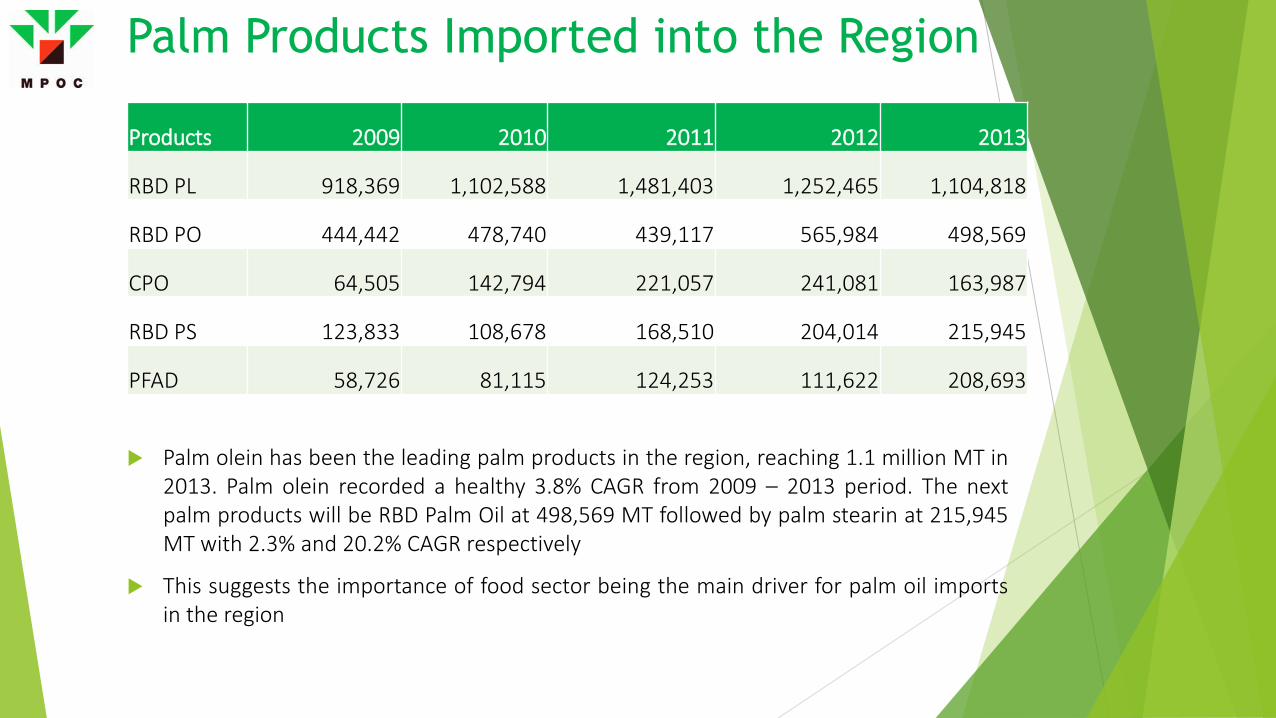

Products 2009 2010 2011 2012 2013

RBD PL 918,369 1,102,588 1,481,403 1,252,465 1,104,818

RBD PO 444,442 478,740 439,117 565,984 498,569

CPO 64,505 142,794 221,057 241,081 163,987

RBD PS 123,833 108,678 168,510 204,014 215,945

PFAD 58,726 81,115 124,253 111,622 208,693

Palm olein has been the leading palm products in the region, reaching 1.1 million MT in 2013. Palm olein recorded a healthy 3.8% CAGR from 2009 – 2013 period. The next palm products will be RBD Palm Oil at 498,569 MT followed by palm stearin at 215,945 MT with 2.3% and 20.2% CAGR respectively

This suggests the importance of food sector being the main driver for palm oil imports in the region

Palm Products Imported into the Region

PART II: ECONOMICS Macro views of the region that affect supply and demand of oils and fats

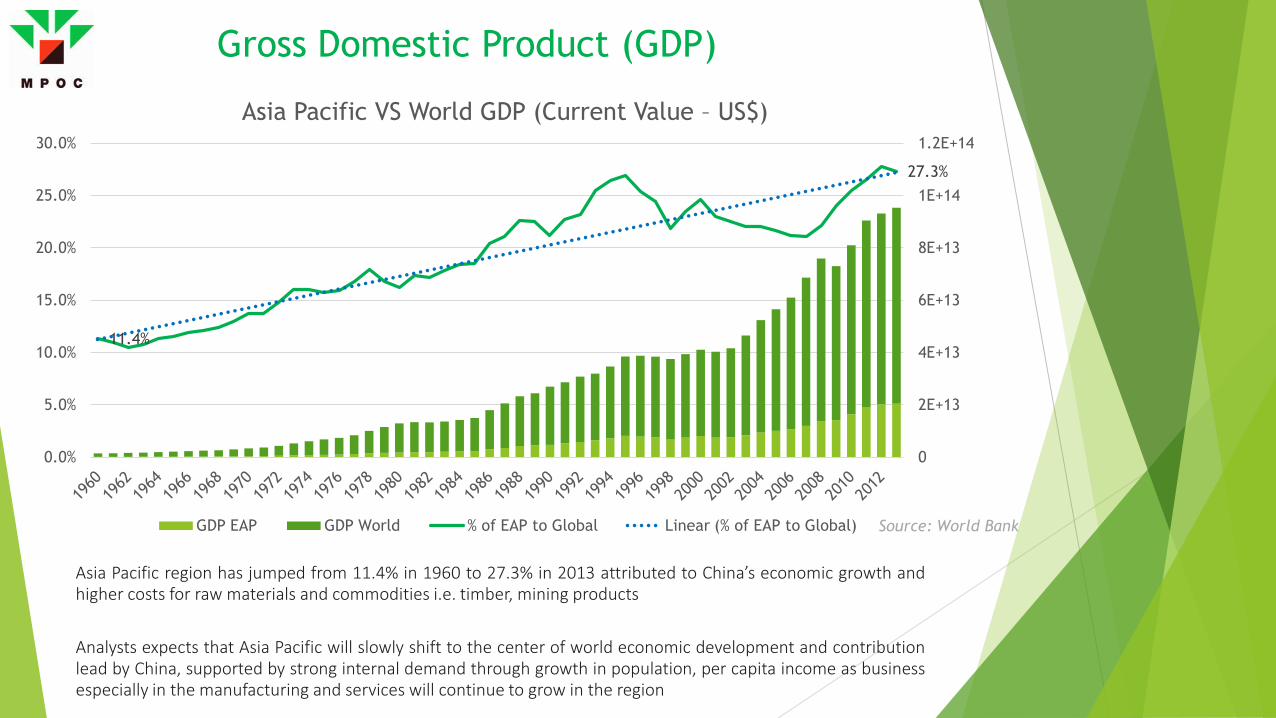

11.4%

27.3%

0

2E+13

4E+13

6E+13

8E+13

1E+14

1.2E+14

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Asia Pacific VS World GDP (Current Value – US$)

GDP EAP GDP World % of EAP to Global Linear (% of EAP to Global)

Gross Domestic Product (GDP)

Asia Pacific region has jumped from 11.4% in 1960 to 27.3% in 2013 attributed to China’s economic growth and higher costs for raw materials and commodities i.e. timber, mining products Analysts expects that Asia Pacific will slowly shift to the center of world economic development and contribution lead by China, supported by strong internal demand through growth in population, per capita income as business especially in the manufacturing and services will continue to grow in the region

Source: World Bank

Rapid urbanization as most of the countries in the Asia Pacific region are experiencing high manufacturing and services growth. The gap of income between urban and rural employment has also drive rural – urban migration This will affect the production of oils and fats as countries can start to afford imported goods

Increased Urbanization due to Higher Participation in Manufacturing and Services Sector

0

10

20

30

40

50

60

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Export (% of GDP) Urban Population (% of total)

Agricultural Employment Linear (Export (% of GDP)) Source: World Bank

% of

Tot

al E

mpl

oym

ent

/ Po

pula

tion

Rapid urbanization as most of the countries in the Asia Pacific region are experiencing high manufacturing and services growth. So does the ratio of women in manufacturing and services industry has increased. In line with the UN Millennium Development Goals no 3 – to promote gender equality and empower women. World Bank also reported that as of 2012, 68% of the total female population are now participating in labour force

Increased Female Participation in the Services and Manufacturing Sector

0

10

20

30

40

50

60

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Urban Population (% of total) Agricultural Employment Source: World Bank

% of

Tot

al E

mpl

oym

ent

/ Po

pula

tion

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

38

40

42

44

46

48

50

52

54

Total Agriculture Land Annual Changes Linear (Annual Changes)

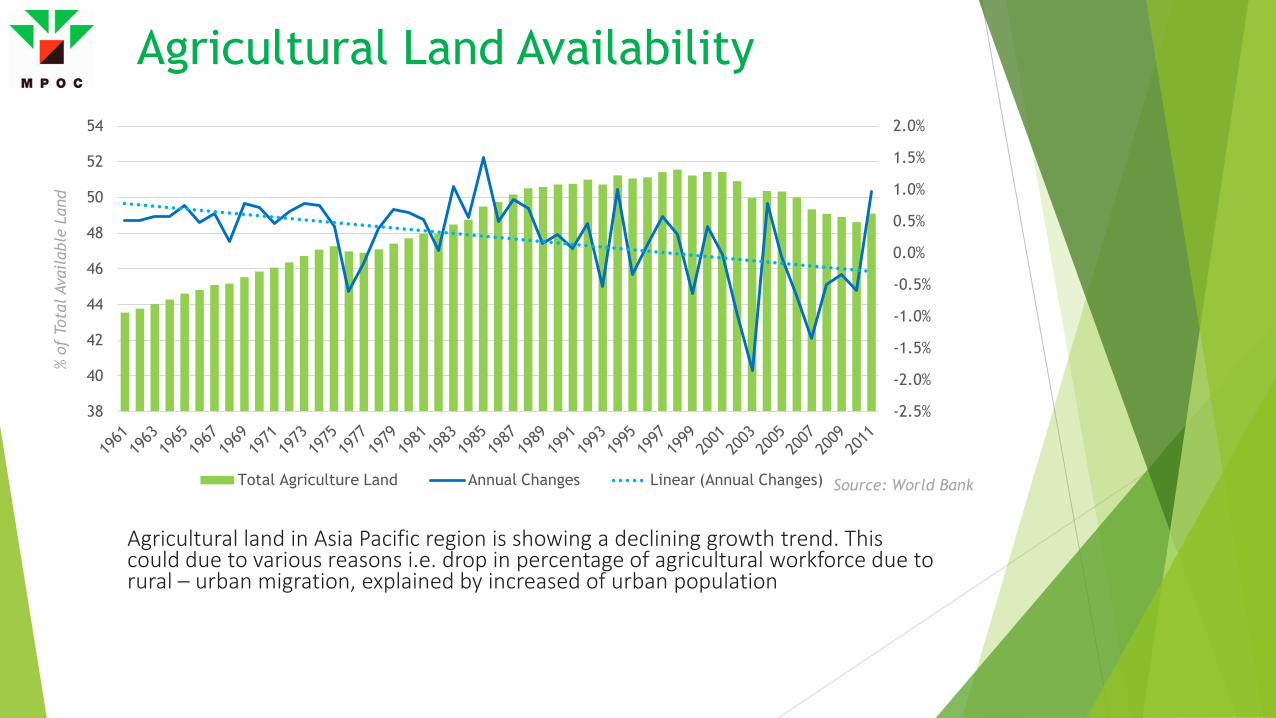

Agricultural land in Asia Pacific region is showing a declining growth trend. This could due to various reasons i.e. drop in percentage of agricultural workforce due to rural – urban migration, explained by increased of urban population

Agricultural Land Availability

Source: World Bank

% of

Tot

al A

vail

able

Lan

d

Changes in Agricultural Land Growth and Production of Oils and Fats

48.3

48.4

48.5

48.6

48.7

48.8

48.9

49

49.1

49.2

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2008 2009 2010 2011 2012

Agricultural Land O&F Production Growth Linear (Agricultural Land)

There is a direct relationship between agricultural land availability and growth of oils and fats production.

Source: World Bank

PART III: POTENTIALS IN THE REGION Areas that are available for increased oils & fats uptake through Malaysian palm oil

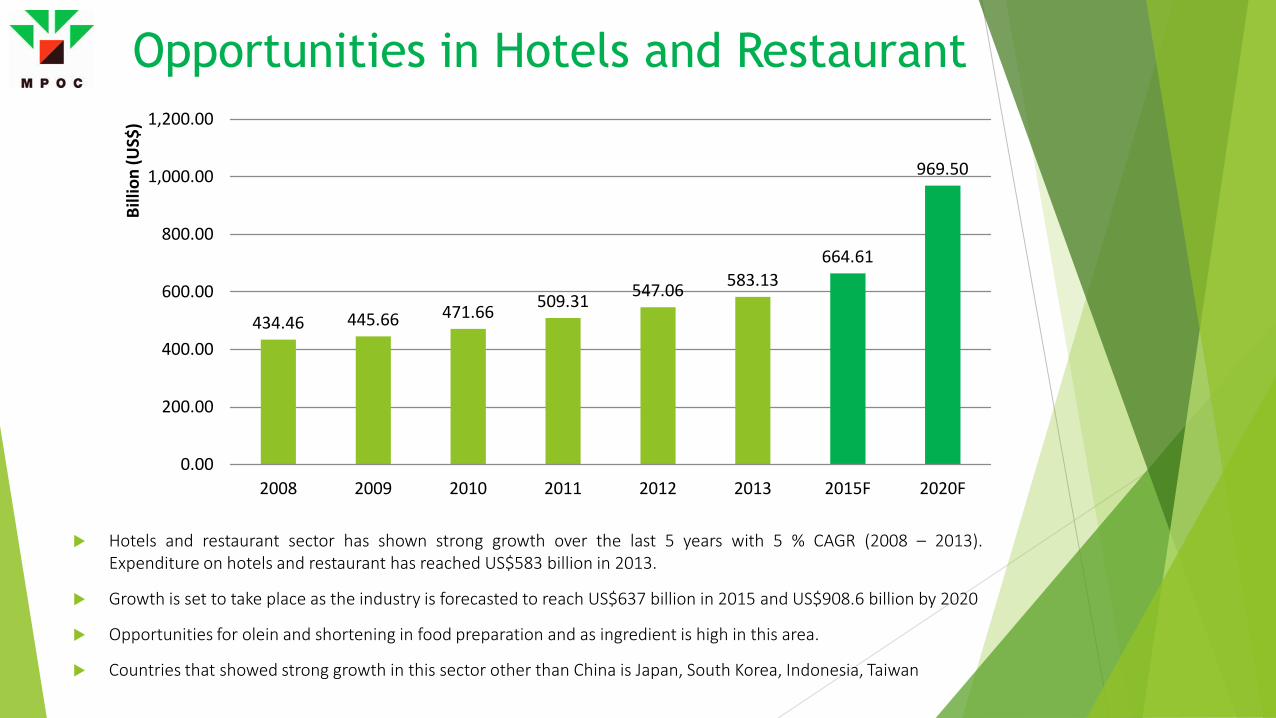

434.46 445.66 471.66 509.31 547.06 583.13 664.61

969.50

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

2008 2009 2010 2011 2012 2013 2015F 2020F

Billi

on (U

S$)

Opportunities in Hotels and Restaurant

Hotels and restaurant sector has shown strong growth over the last 5 years with 5 % CAGR (2008 – 2013). Expenditure on hotels and restaurant has reached US$583 billion in 2013.

Growth is set to take place as the industry is forecasted to reach US$637 billion in 2015 and US$908.6 billion by 2020

Opportunities for olein and shortening in food preparation and as ingredient is high in this area.

Countries that showed strong growth in this sector other than China is Japan, South Korea, Indonesia, Taiwan

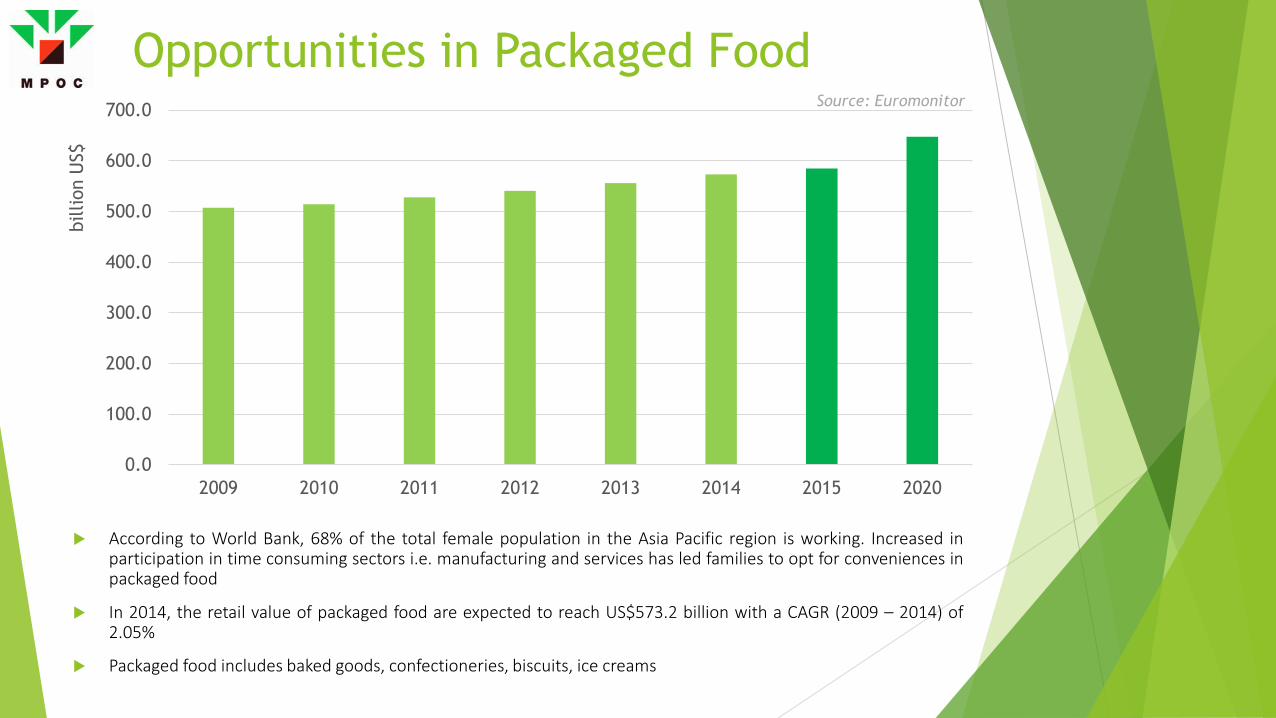

Opportunities in Packaged Food

According to World Bank, 68% of the total female population in the Asia Pacific region is working. Increased in participation in time consuming sectors i.e. manufacturing and services has led families to opt for conveniences in packaged food

In 2014, the retail value of packaged food are expected to reach US$573.2 billion with a CAGR (2009 – 2014) of 2.05%

Packaged food includes baked goods, confectioneries, biscuits, ice creams

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

2009 2010 2011 2012 2013 2014 2015 2020

billi

on U

S$

Source: Euromonitor

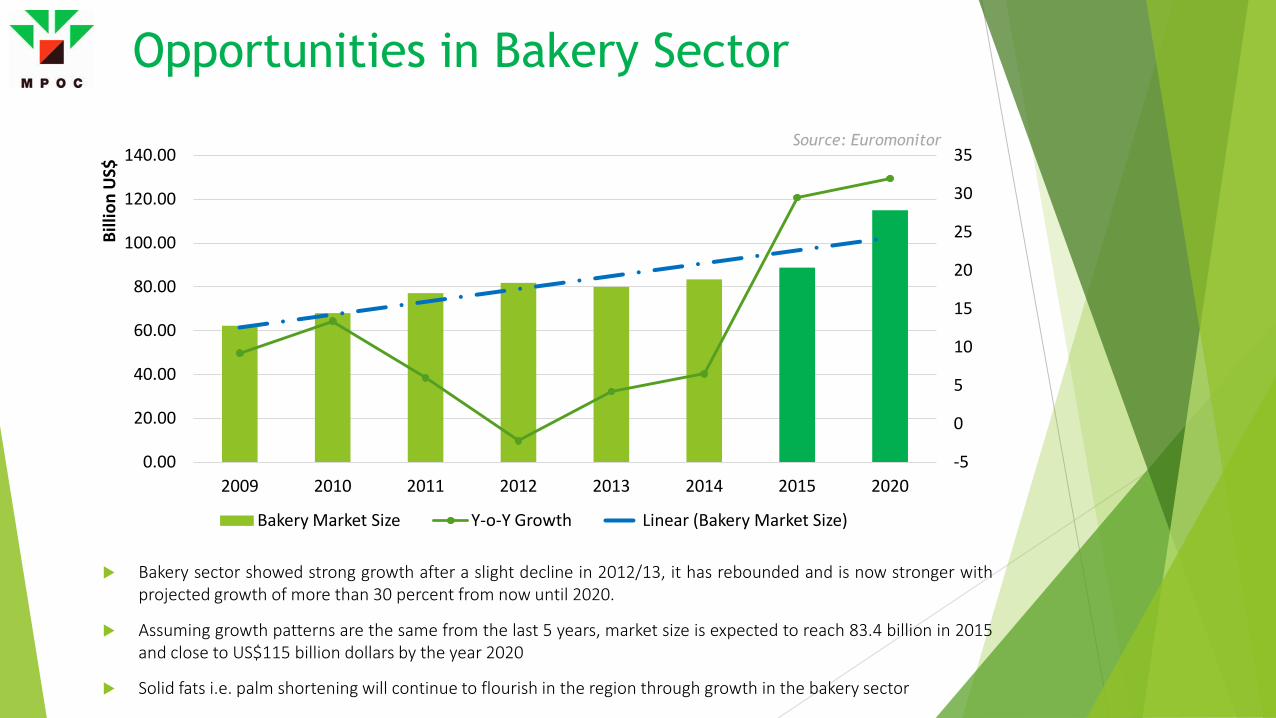

Opportunities in Bakery Sector

-5

0

5

10

15

20

25

30

35

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

2009 2010 2011 2012 2013 2014 2015 2020

Billi

on U

S$

Bakery Market Size Y-o-Y Growth Linear (Bakery Market Size)

Bakery sector showed strong growth after a slight decline in 2012/13, it has rebounded and is now stronger with projected growth of more than 30 percent from now until 2020.

Assuming growth patterns are the same from the last 5 years, market size is expected to reach 83.4 billion in 2015 and close to US$115 billion dollars by the year 2020

Solid fats i.e. palm shortening will continue to flourish in the region through growth in the bakery sector

Source: Euromonitor

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

2008 2009 2010 2011 2012 2013 2015 2020

Billi

on U

S$

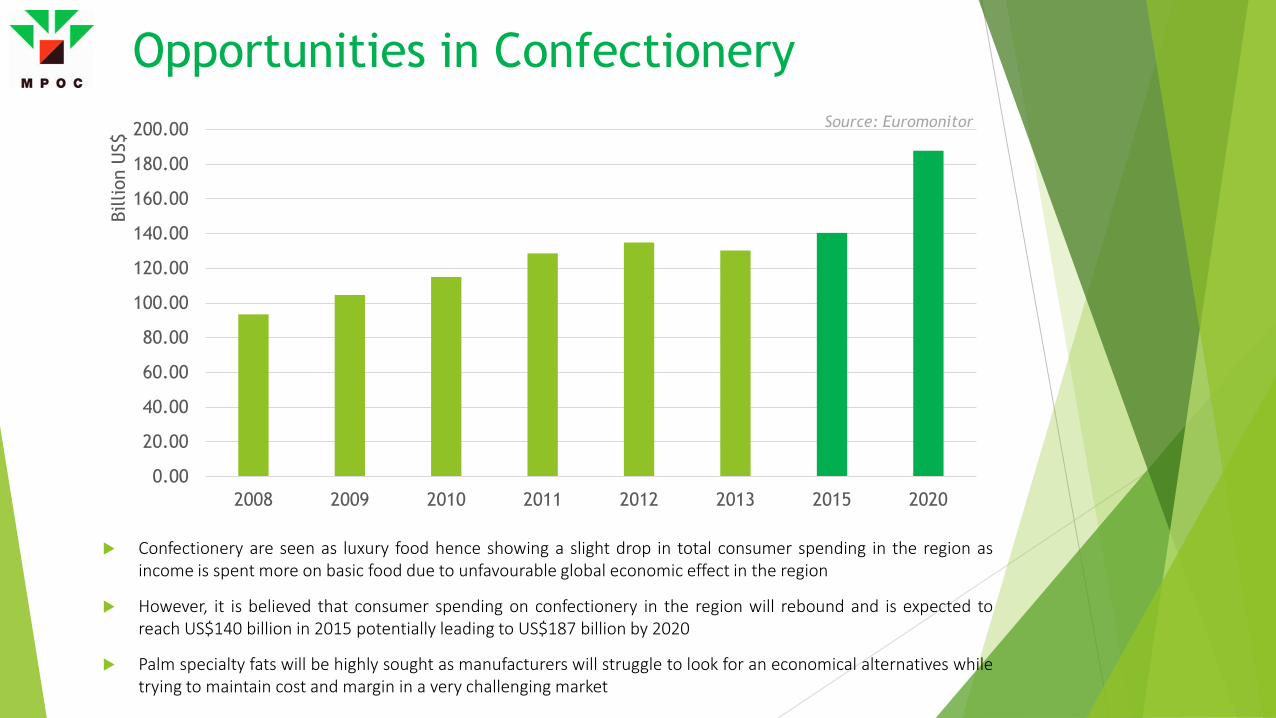

Opportunities in Confectionery

Confectionery are seen as luxury food hence showing a slight drop in total consumer spending in the region as income is spent more on basic food due to unfavourable global economic effect in the region

However, it is believed that consumer spending on confectionery in the region will rebound and is expected to reach US$140 billion in 2015 potentially leading to US$187 billion by 2020

Palm specialty fats will be highly sought as manufacturers will struggle to look for an economical alternatives while trying to maintain cost and margin in a very challenging market

Source: Euromonitor

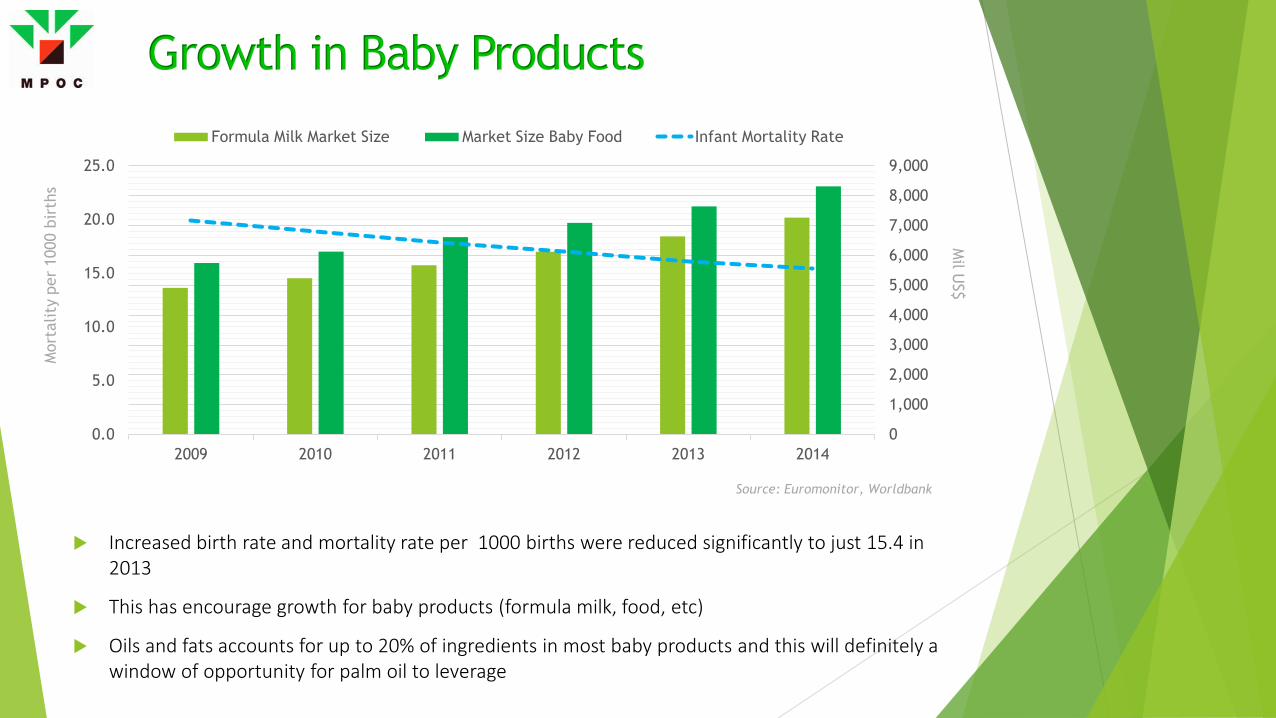

Increased birth rate and mortality rate per 1000 births were reduced significantly to just 15.4 in 2013

This has encourage growth for baby products (formula milk, food, etc)

Oils and fats accounts for up to 20% of ingredients in most baby products and this will definitely a window of opportunity for palm oil to leverage

0.0

5.0

10.0

15.0

20.0

25.0

2009 2010 2011 2012 2013 2014 0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Formula Milk Market Size Market Size Baby Food Infant Mortality Rate

Source: Euromonitor, Worldbank

Mil U

S$

Mor

talit

y pe

r 10

00 b

irth

s

Increased birth rate and mortality rate per 1000 births were reduced significantly to just 15.4 in 2013. Women’s disposable incomes, which can be linked with sales of baby and child-specific products, have been rising, especially in emerging markets.

Philippines, Indonesia , China serves as the biggest potential of baby products in the region

Source: Euromonitor

Opportunities in Soap and Cleaning Products

Soap and cleaning products are good avenues for palm oleochemical sector for growth

Asia Pacific recorded 116.9 billion market size in 2013, recording a strong growth of 7.1% CAGR from 2008 – 2013.

The market is expected to grow to reach US$134 billion in 2015, leading up to US$189 billion by 2020

82.9 82.3 95.9

108.7 115.1 116.9 134.1

189.0

0 20 40 60 80

100 120 140 160 180 200

2008 2009 2010 2011 2012 2013 2015F 2020F

Billi

on ($

US)

Soaps and Cleaning Products Market Size Source: Euromonitor

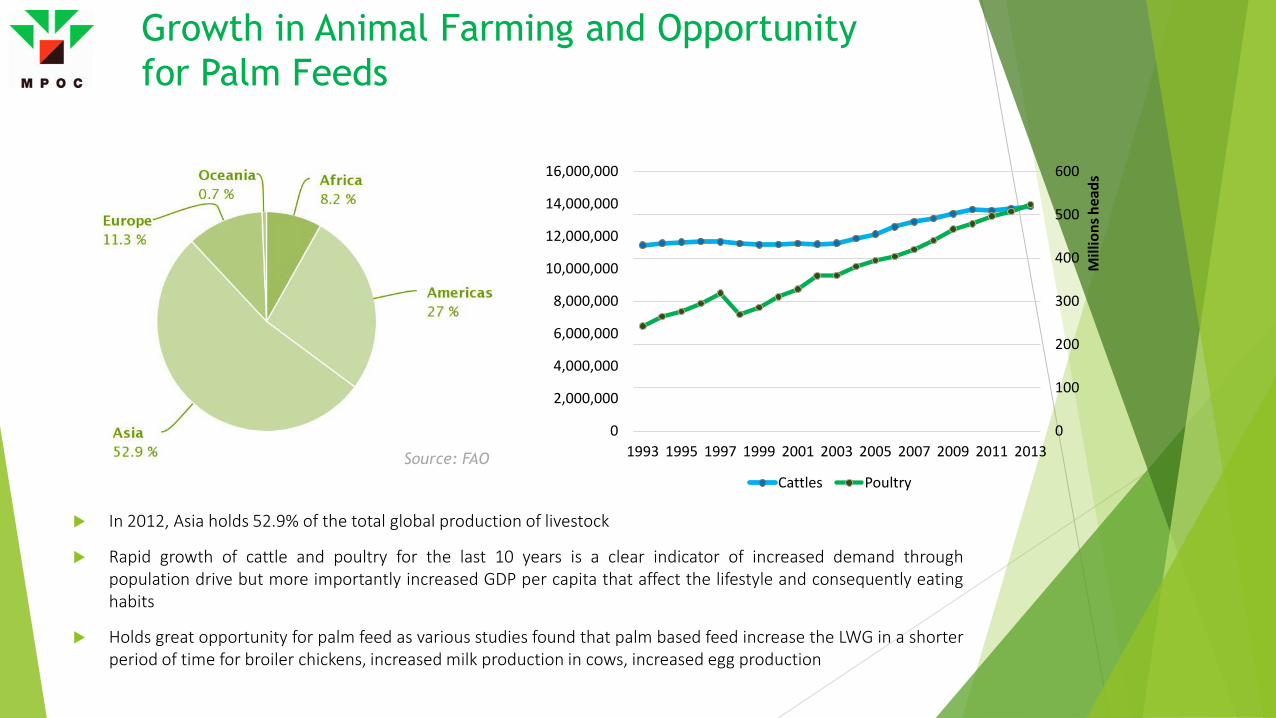

Growth in Animal Farming and Opportunity for Palm Feeds

In 2012, Asia holds 52.9% of the total global production of livestock

Rapid growth of cattle and poultry for the last 10 years is a clear indicator of increased demand through population drive but more importantly increased GDP per capita that affect the lifestyle and consequently eating habits

Holds great opportunity for palm feed as various studies found that palm based feed increase the LWG in a shorter period of time for broiler chickens, increased milk production in cows, increased egg production

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 0

100

200

300

400

500

600

Mill

ions

hea

ds

Cattles Poultry Source: FAO

OBSERVATIONS Asia Pacific is the main producer for most commodities

Demand growth is getting bigger in the region as compared

to other region due to population growth and anticipated stronger economic condition

Asia Pacific countries should look to trade among each other as there are many incentives through joint economic efforts i.e. ASEAN + 3, APEC, and lower transportation costs

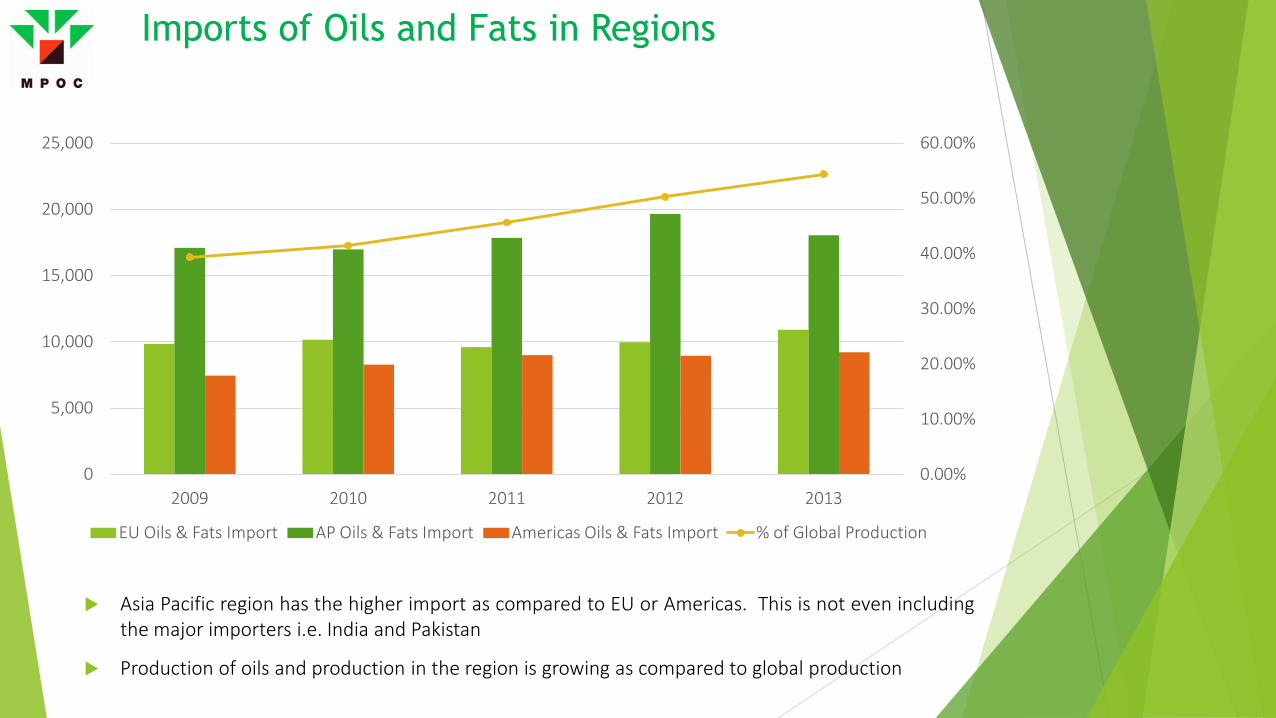

Imports of Oils and Fats in Regions

Asia Pacific region has the higher import as compared to EU or Americas. This is not even including the major importers i.e. India and Pakistan

Production of oils and production in the region is growing as compared to global production

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

0

5,000

10,000

15,000

20,000

25,000

2009 2010 2011 2012 2013

EU Oils & Fats Import AP Oils & Fats Import Americas Oils & Fats Import % of Global Production

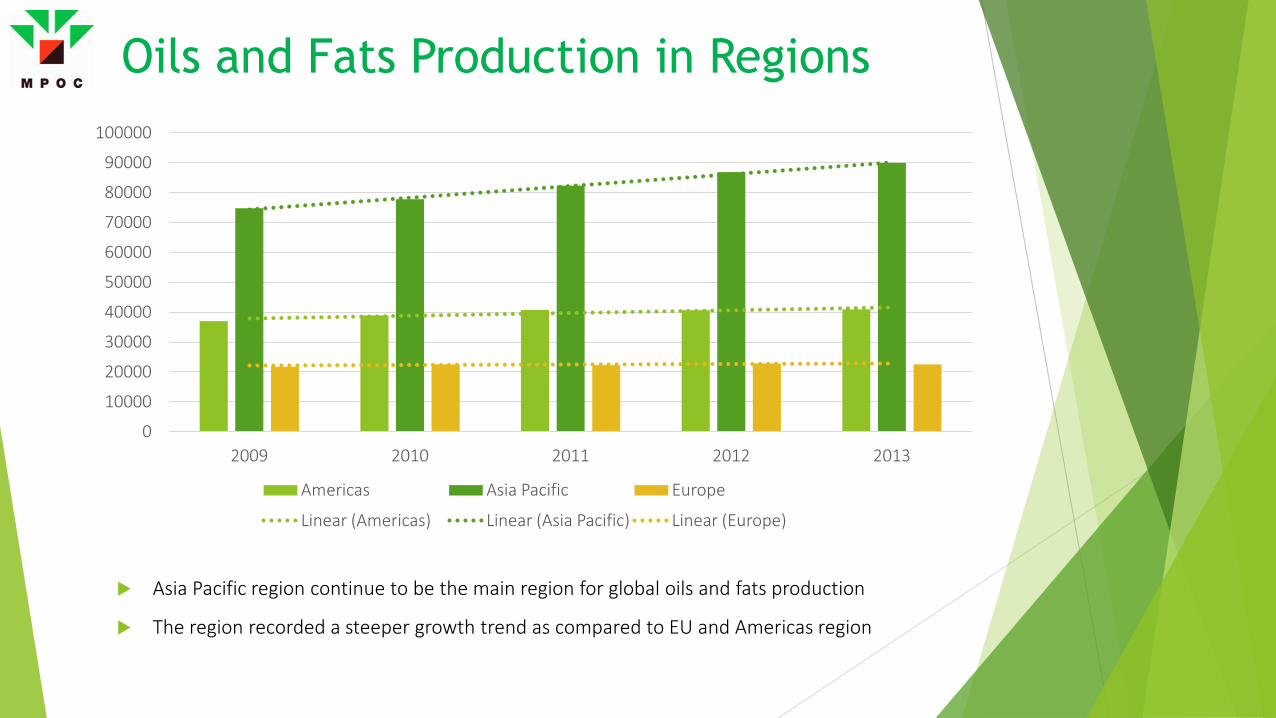

Oils and Fats Production in Regions

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2009 2010 2011 2012 2013

Americas Asia Pacific Europe

Linear (Americas) Linear (Asia Pacific) Linear (Europe)

Asia Pacific region continue to be the main region for global oils and fats production

The region recorded a steeper growth trend as compared to EU and Americas region

CONCLUSIONS Asia Pacific as the growth driver destination and Malaysian palm oil is the viable solution – technically and economically

Conclusions

Global food security has been the main topic for most workgroups at the international, regional and national level. As the world is expected to reach 9 billion by 2050, the scarcity in critical resources such as food should be the focus

Oils and fats in one of the main sectors in food that is important as deficiency in fats has been known to caused various diseases due to inability to absorb important fat soluble vitamins

The Asia Pacific region is one of the important region due to its population and economic growth. The region’s oils and fats needs is not seen to be diminishing in the future and will continue to grow

Decreasing growth in agricultural land is making it increasingly critical to secure food production including in the oils and fats sector. There is a positive correlation between growth in agricultural land and production of oils and fats in the region. A high yielding plant that can optimize the tonnes per hectare is needed

Palm oil fits the description well for high yielding, maximum tonnes per hectares crop

With 80% of total production of oils & fats in the region, the palm oil supply seems to have a critical role in the region. This serves as a great potential for businesses with Malaysian palm oil in the region

This is of course due to palm oil’s nutritional and economical advantages. The trans fat issue that is now a major concern in most developing countries will require most food manufacturers to switch to feedstock that can avoid trans fat at the lowest cost

Again, palm oil will give food manufacturers the advantage due to its naturally semi solid attributes that won’t require partial hydrogenation or interesterification that will increase the cost

Malaysian palm oil has shown increasing imports in the region – quality and reliability

Conclusions

Malaysian palm oil industry can also cater not only in oils segment. Due to better economic position, it’s proven that increased income will increase consumption in meat and poultry. The high livestock production in the region will need food. Feed for food. Palm kernel meal will be a good blend with the current feed formulation as various studies has shown that the appropriate blend of palm kernel meal has been proven to increase meat and milk production in cow, increased LWG within shorter periods of time and increased egg weight for poultries

Oleochemical sectors are also blooming in the region. Soap and detergent sector, baby products are all showing strong growth due to increased disposable income among the female population

Many more opportunities for everyone involved in the supply chain of Malaysian palm oil industry

Conclusions

THANK YOU Email: [email protected]