Asia Pacific Dailyasiaresearch.daiwacm.com/eg/cgi-bin/files/Daily01Jul16.pdfSee important...

29

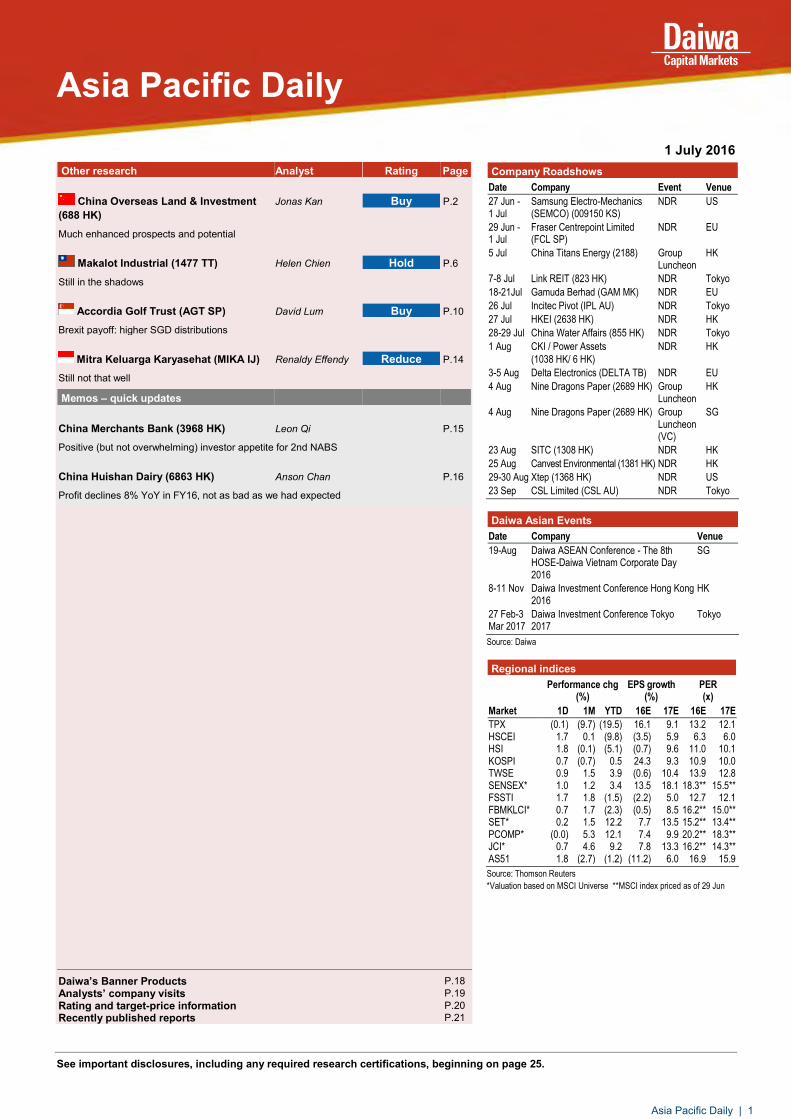

Asia Pacific Daily See important disclosures, including any required research certifications, beginning on page 25. 1 July 2016 Other research Analyst Rating Page China Overseas Land & Investment (688 HK) Jonas Kan Buy P.2 Much enhanced prospects and potential Makalot Industrial (1477 TT) Helen Chien Hold P.6 Still in the shadows Accordia Golf Trust (AGT SP) David Lum Buy P.10 Brexit payoff: higher SGD distributions Mitra Keluarga Karyasehat (MIKA IJ) Renaldy Effendy Reduce P.14 Still not that well Memos – quick updates China Merchants Bank (3968 HK) Leon Qi P.15 Positive (but not overwhelming) investor appetite for 2nd NABS China Huishan Dairy (6863 HK) Anson Chan P.16 Profit declines 8% YoY in FY16, not as bad as we had expected Daiwa’s Banner Products P.18 Analysts’ company visits P.19 Rating and target-price information P.20 Recently published reports P.21 Company Roadshows Date Company Event Venue 27 Jun - 1 Jul Samsung Electro-Mechanics (SEMCO) (009150 KS) NDR US 29 Jun - 1 Jul Fraser Centrepoint Limited (FCL SP) NDR EU 5 Jul China Titans Energy (2188) Group Luncheon HK 7-8 Jul Link REIT (823 HK) NDR Tokyo 18-21Jul Gamuda Berhad (GAM MK) NDR EU 26 Jul Incitec Pivot (IPL AU) NDR Tokyo 27 Jul HKEI (2638 HK) NDR HK 28-29 Jul China Water Affairs (855 HK) NDR Tokyo 1 Aug CKI / Power Assets (1038 HK/ 6 HK) NDR HK 3-5 Aug Delta Electronics (DELTA TB) NDR EU 4 Aug Nine Dragons Paper (2689 HK) Group Luncheon HK 4 Aug Nine Dragons Paper (2689 HK) Group Luncheon (VC) SG 23 Aug SITC (1308 HK) NDR HK 25 Aug Canvest Environmental (1381 HK) NDR HK 29-30 Aug Xtep (1368 HK) NDR US 23 Sep CSL Limited (CSL AU) NDR Tokyo Daiwa Asian Events Date Company Venue 19-Aug Daiwa ASEAN Conference - The 8th HOSE-Daiwa Vietnam Corporate Day 2016 SG 8-11 Nov Daiwa Investment Conference Hong Kong 2016 HK 27 Feb-3 Mar 2017 Daiwa Investment Conference Tokyo 2017 Tokyo Source: Daiwa Regional indices Performance chg (%) EPS growth (%) PER (x) Market 1D 1M YTD 16E 17E 16E 17E TPX (0.1) (9.7) (19.5) 16.1 9.1 13.2 12.1 HSCEI 1.7 0.1 (9.8) (3.5) 5.9 6.3 6.0 HSI 1.8 (0.1) (5.1) (0.7) 9.6 11.0 10.1 KOSPI 0.7 (0.7) 0.5 24.3 9.3 10.9 10.0 TWSE 0.9 1.5 3.9 (0.6) 10.4 13.9 12.8 SENSEX* 1.0 1.2 3.4 13.5 18.1 18.3** 15.5** FSSTI 1.7 1.8 (1.5) (2.2) 5.0 12.7 12.1 FBMKLCI* 0.7 1.7 (2.3) (0.5) 8.5 16.2** 15.0** SET* 0.2 1.5 12.2 7.7 13.5 15.2** 13.4** PCOMP* (0.0) 5.3 12.1 7.4 9.9 20.2** 18.3** JCI* 0.7 4.6 9.2 7.8 13.3 16.2** 14.3** AS51 1.8 (2.7) (1.2) (11.2) 6.0 16.9 15.9 Source: Thomson Reuters *Valuation based on MSCI Universe **MSCI index priced as of 29 Jun Asia Pacific Daily | 1

-

Upload

hoangduong -

Category

Documents

-

view

220 -

download

0

Transcript of Asia Pacific Dailyasiaresearch.daiwacm.com/eg/cgi-bin/files/Daily01Jul16.pdfSee important...

Asia Pacific Daily

See important disclosures, including any required research certifications, beginning on page 25.

1 July 2016 Other research Analyst Rating Page

China Overseas Land & Investment (688 HK)

Jonas Kan Buy P.2

Much enhanced prospects and potential

Makalot Industrial (1477 TT) Helen Chien Hold P.6

Still in the shadows

Accordia Golf Trust (AGT SP) David Lum Buy P.10

Brexit payoff: higher SGD distributions

Mitra Keluarga Karyasehat (MIKA IJ) Renaldy Effendy Reduce P.14

Still not that well Memos – quick updates

China Merchants Bank (3968 HK) Leon Qi P.15

Positive (but not overwhelming) investor appetite for 2nd NABS

China Huishan Dairy (6863 HK) Anson Chan P.16

Profit declines 8% YoY in FY16, not as bad as we had expected

Daiwa’s Banner Products P.18 Analysts’ company visits P.19 Rating and target-price information P.20 Recently published reports P.21

Company Roadshows Date Company Event Venue

27 Jun - 1 Jul

Samsung Electro-Mechanics (SEMCO) (009150 KS)

NDR US

29 Jun - 1 Jul

Fraser Centrepoint Limited (FCL SP)

NDR EU

5 Jul China Titans Energy (2188) Group Luncheon

HK

7-8 Jul Link REIT (823 HK) NDR Tokyo

18-21Jul Gamuda Berhad (GAM MK) NDR EU

26 Jul Incitec Pivot (IPL AU) NDR Tokyo

27 Jul HKEI (2638 HK) NDR HK

28-29 Jul China Water Affairs (855 HK) NDR Tokyo

1 Aug CKI / Power Assets

(1038 HK/ 6 HK)

NDR HK

3-5 Aug Delta Electronics (DELTA TB) NDR EU

4 Aug Nine Dragons Paper (2689 HK) Group Luncheon

HK

4 Aug Nine Dragons Paper (2689 HK) Group Luncheon (VC)

SG

23 Aug SITC (1308 HK) NDR HK

25 Aug Canvest Environmental (1381 HK) NDR HK

29-30 Aug Xtep (1368 HK) NDR US

23 Sep CSL Limited (CSL AU) NDR Tokyo

Daiwa Asian Events Date Company Venue

19-Aug Daiwa ASEAN Conference - The 8th HOSE-Daiwa Vietnam Corporate Day 2016

SG

8-11 Nov Daiwa Investment Conference Hong Kong 2016

HK

27 Feb-3 Mar 2017

Daiwa Investment Conference Tokyo 2017

Tokyo

Source: Daiwa

Regional indices

Performance chg (%)

EPS growth (%)

PER (x)

Market 1D 1M YTD 16E 17E 16E 17E

TPX (0.1) (9.7) (19.5) 16.1 9.1 13.2 12.1 HSCEI 1.7 0.1 (9.8) (3.5) 5.9 6.3 6.0 HSI 1.8 (0.1) (5.1) (0.7) 9.6 11.0 10.1 KOSPI 0.7 (0.7) 0.5 24.3 9.3 10.9 10.0 TWSE 0.9 1.5 3.9 (0.6) 10.4 13.9 12.8 SENSEX* 1.0 1.2 3.4 13.5 18.1 18.3** 15.5** FSSTI 1.7 1.8 (1.5) (2.2) 5.0 12.7 12.1 FBMKLCI* 0.7 1.7 (2.3) (0.5) 8.5 16.2** 15.0** SET* 0.2 1.5 12.2 7.7 13.5 15.2** 13.4** PCOMP* (0.0) 5.3 12.1 7.4 9.9 20.2** 18.3** JCI* 0.7 4.6 9.2 7.8 13.3 16.2** 14.3** AS51 1.8 (2.7) (1.2) (11.2) 6.0 16.9 15.9

Source: Thomson Reuters

*Valuation based on MSCI Universe **MSCI index priced as of 29 Jun

Asia Pacific Daily | 1

See important disclosures, including any required research certifications, beginning on page 5

China Financials

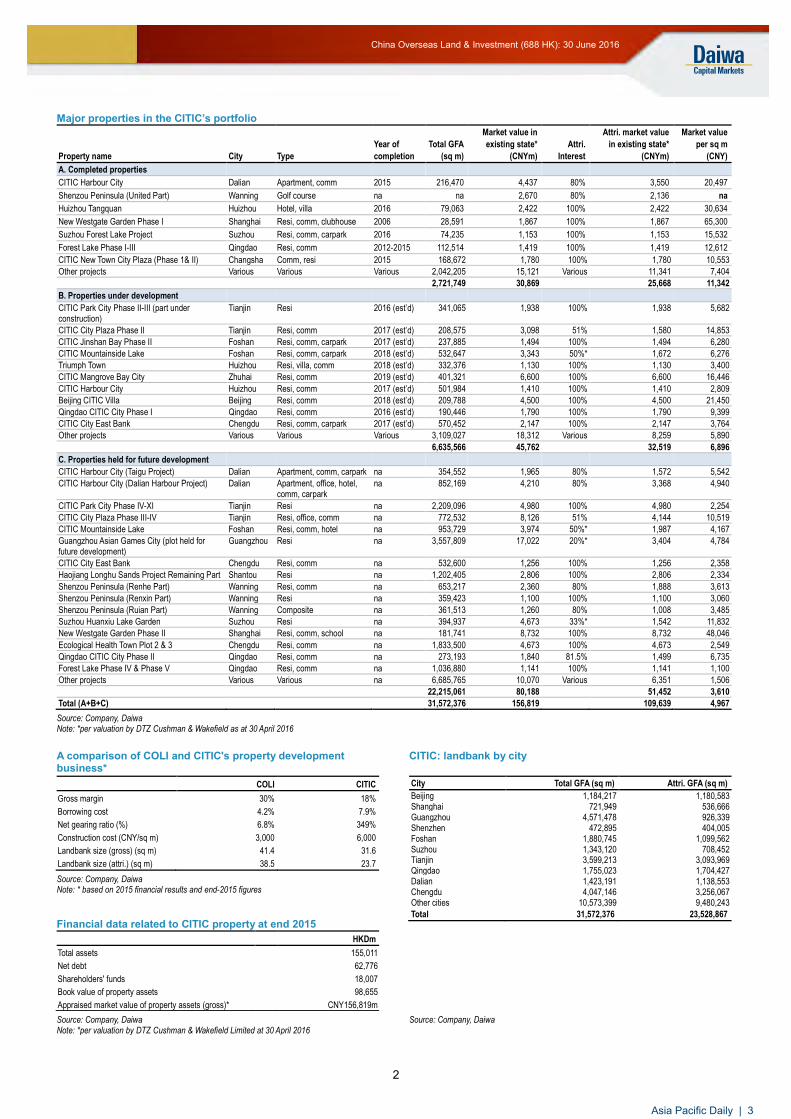

What's new: We attended an analyst meeting organised by China Overseas Land & Investment (COLI) on the Circular it has just released related to its planned acquisition of CITIC’s property assets. The meeting reinforced our view that this is an important strategic deal which will further strengthen COLI’s long-term potential in the China property sector. What's the impact: Notably strengthened potential in various key markets. We see as positive that the actual size of CITIC’s landbank (31.6m sq m gross) has turned out to be larger than the figure announced in March 2016 (24m sq m gross) and that CITIC also has sizeable landbank in COLI’s major markets. Effectively, the deal will boost COLI’s landbank in 10 major cities (the 4 tier-1 cities plus Tianjin, Dalian, Qingdao, Suzhou, Foshan, Chengdu) by 1.4x to 14m sq m, thereby making it an even stronger player in these cities. End-2016E NAV revised up. We now factor in only a moderate new contribution from CITIC’s projects, but see room for stronger earnings and NAV uplift if COLI can quickly realise the full value of CITIC’s landbank and the synergies it could bring to its existing operation. Overall, we are revising up our 2016-18E EPS by 1-8%. In terms of NAV, we are revising up our end-2016E NAV by 3.1% to HKD39.80. While we estimate COLI’s net gearing ratio will rise from 6.8% at end-2015 to 36% post transaction, we see 36% as still a manageable level. Greatest significance is at the strategic level and relating to long-term prospects. We see this deal as a major M&A deal in China property in that it is about realising the value associated with a strong, efficient and low-financing cost player merging with another one at a comparable scale, but scores lower in all these metrics (see p.2); and we think there could be many such opportunities in China property in the years to come. Our read is that CITIC has highly valued the long-term benefits associated with having a major stake in COLI and we think this also highlights the “currency value” that could be commanded by the stronger players in China property. In all, we believe M&A will become an important supplementary driver for COLI’s earnings and business growth in the years ahead. What we recommend: We reiterate our Buy (1) rating and raise our 12-month TP to HKD31.80 (from HKD30.90), based on an unchanged 20% discount applied to our revised end-2016E NAV of HKD39.80. The key risk to our call is the deal not getting approval from the Chinese Government. How we differ: We believe COLI has now opened up M&A as a new growth engine, but this may have yet to be recognised by the market.

30 June 2016

Much enhanced prospects and potential

CITIC deal should notably strengthen COLI’s potential in key markets We view it as a major M&A deal in China property TP raised 3% to HKD31.80; end-2016E NAV now HKD39.80

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

China Overseas Land & Investment (688 HK)

Target price: HKD31.80 (from HKD30.90)

Share price (29 Jun): HKD23.05 | Up/downside: +37.9%

Jonas Kan, CFA(852) 2848 4439

Forecast revisions (%)Year to 31 Dec 16E 17E 18E

Revenue change 6.8 7.5 8.7

Net profit change 1.3 4.4 7.8

Core EPS (FD) change 1.3 4.4 7.8

90

99

108

116

125

20

22

24

26

28

Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

Share price performance

Ch Ov Land (LHS) Relative to HSI (RHS)

(HKD) (%)

12-month range 20.65-27.65

Market cap (USDbn) 32.54

3m avg daily turnover (USDm) 53.08

Shares outstanding (m) 10,956

Major shareholder China Overseas Holdings (55.1%)

Financial summary (HKD)Year to 31 Dec 16E 17E 18E

Revenue (m) 173,390 204,251 232,658

Operating profit (m) 48,753 58,116 66,753

Net profit (m) 33,870 39,530 45,020

Core EPS (fully-diluted) 3.091 3.608 4.109

EPS change (%) 10.6 16.7 13.9

Daiwa vs Cons. EPS (%) (7.2) (4.6) (2.6)

PER (x) 7.5 6.4 5.6

Dividend yield (%) 2.9 3.1 3.4

DPS 0.660 0.720 0.790

PBR (x) 1.0 0.9 0.8

EV/EBITDA (x) 6.5 5.4 4.6

ROE (%) 15.5 15.1 15.2

Asia Pacific Daily | 2

2

China Overseas Land & Investment (688 HK): 30 June 2016

Major properties in the CITIC’s portfolio

Market value in Attri. market value Market value

Year of Total GFA existing state* Attri. in existing state* per sq m

Property name City Type completion (sq m) (CNYm) Interest (CNYm) (CNY)

A. Completed properties

CITIC Harbour City Dalian Apartment, comm 2015 216,470 4,437 80% 3,550 20,497

Shenzou Peninsula (United Part) Wanning Golf course na na 2,670 80% 2,136 na

Huizhou Tangquan Huizhou Hotel, villa 2016 79,063 2,422 100% 2,422 30,634

New Westgate Garden Phase I Shanghai Resi, comm, clubhouse 2006 28,591 1,867 100% 1,867 65,300

Suzhou Forest Lake Project Suzhou Resi, comm, carpark 2016 74,235 1,153 100% 1,153 15,532

Forest Lake Phase I-III Qingdao Resi, comm 2012-2015 112,514 1,419 100% 1,419 12,612

CITIC New Town City Plaza (Phase 1& II) Changsha Comm, resi 2015 168,672 1,780 100% 1,780 10,553

Other projects Various Various Various 2,042,205 15,121 Various 11,341 7,404

2,721,749 30,869 25,668 11,342

B. Properties under development

CITIC Park City Phase II-III (part under construction)

Tianjin Resi 2016 (est’d) 341,065 1,938 100% 1,938 5,682

CITIC City Plaza Phase II Tianjin Resi, comm 2017 (est’d) 208,575 3,098 51% 1,580 14,853

CITIC Jinshan Bay Phase II Foshan Resi, comm, carpark 2017 (est’d) 237,885 1,494 100% 1,494 6,280

CITIC Mountainside Lake Foshan Resi, comm, carpark 2018 (est’d) 532,647 3,343 50%* 1,672 6,276

Triumph Town Huizhou Resi, villa, comm 2018 (est’d) 332,376 1,130 100% 1,130 3,400

CITIC Mangrove Bay City Zhuhai Resi, comm 2019 (est’d) 401,321 6,600 100% 6,600 16,446

CITIC Harbour City Huizhou Resi, comm 2017 (est’d) 501,984 1,410 100% 1,410 2,809

Beijing CITIC Villa Beijing Resi, comm 2018 (est’d) 209,788 4,500 100% 4,500 21,450

Qingdao CITIC City Phase I Qingdao Resi, comm 2016 (est’d) 190,446 1,790 100% 1,790 9,399

CITIC City East Bank Chengdu Resi, comm, carpark 2017 (est’d) 570,452 2,147 100% 2,147 3,764

Other projects Various Various Various 3,109,027 18,312 Various 8,259 5,890

6,635,566 45,762 32,519 6,896

C. Properties held for future development

CITIC Harbour City (Taigu Project) Dalian Apartment, comm, carpark na 354,552 1,965 80% 1,572 5,542

CITIC Harbour City (Dalian Harbour Project) Dalian Apartment, office, hotel, comm, carpark

na 852,169 4,210 80% 3,368 4,940

CITIC Park City Phase IV-XI Tianjin Resi na 2,209,096 4,980 100% 4,980 2,254

CITIC City Plaza Phase III-IV Tianjin Resi, office, comm na 772,532 8,126 51% 4,144 10,519

CITIC Mountainside Lake Foshan Resi, comm, hotel na 953,729 3,974 50%* 1,987 4,167

Guangzhou Asian Games City (plot held for future development)

Guangzhou Resi na 3,557,809 17,022 20%* 3,404 4,784

CITIC City East Bank Chengdu Resi, comm na 532,600 1,256 100% 1,256 2,358

Haojiang Longhu Sands Project Remaining Part Shantou Resi na 1,202,405 2,806 100% 2,806 2,334

Shenzou Peninsula (Renhe Part) Wanning Resi, comm na 653,217 2,360 80% 1,888 3,613

Shenzou Peninsula (Renxin Part) Wanning Resi na 359,423 1,100 100% 1,100 3,060

Shenzou Peninsula (Ruian Part) Wanning Composite na 361,513 1,260 80% 1,008 3,485

Suzhou Huanxiu Lake Garden Suzhou Resi na 394,937 4,673 33%* 1,542 11,832

New Westgate Garden Phase II Shanghai Resi, comm, school na 181,741 8,732 100% 8,732 48,046

Ecological Health Town Plot 2 & 3 Chengdu Resi, comm na 1,833,500 4,673 100% 4,673 2,549

Qingdao CITIC City Phase II Qingdao Resi, comm na 273,193 1,840 81.5% 1,499 6,735

Forest Lake Phase IV & Phase V Qingdao Resi, comm na 1,036,880 1,141 100% 1,141 1,100

Other projects Various Various na 6,685,765 10,070 Various 6,351 1,506

22,215,061 80,188 51,452 3,610

Total (A+B+C) 31,572,376 156,819 109,639 4,967

Source: Company, Daiwa Note: *per valuation by DTZ Cushman & Wakefield as at 30 April 2016

A comparison of COLI and CITIC's property development business*

CITIC: landbank by city

COLI CITIC

Gross margin 30% 18%

Borrowing cost 4.2% 7.9%

Net gearing ratio (%) 6.8% 349%

Construction cost (CNY/sq m) 3,000 6,000

Landbank size (gross) (sq m) 41.4 31.6

Landbank size (attri.) (sq m) 38.5 23.7

Source: Company, Daiwa Note: * based on 2015 financial results and end-2015 figures

Financial data related to CITIC property at end 2015

HKDm

Total assets 155,011

Net debt 62,776

Shareholders' funds 18,007

Book value of property assets 98,655

Appraised market value of property assets (gross)* CNY156,819m

City Total GFA (sq m) Attri. GFA (sq m)

Beijing 1,184,217 1,180,583 Shanghai 721,949 536,666 Guangzhou 4,571,478 926,339 Shenzhen 472,895 404,005 Foshan 1,880,745 1,099,562 Suzhou 1,343,120 708,452 Tianjin 3,599,213 3,093,969 Qingdao 1,755,023 1,704,427 Dalian 1,423,191 1,138,553 Chengdu 4,047,146 3,256,067 Other cities 10,573,399 9,480,243

Total 31,572,376 23,528,867

Source: Company, Daiwa Note: *per valuation by DTZ Cushman & Wakefield Limited at 30 April 2016

Source: Company, Daiwa

Asia Pacific Daily | 3

3

China Overseas Land & Investment (688 HK): 30 June 2016

Financial summary Key assumptions

Profit and loss (HKDm)

Cash flow (HKDm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Recognized sales vol. ('000 sq m GFA) 4,290 5,400 6,628 7,780 12,260 14,300 16,800 19,000

Completed investment properties (m sq

ft)4 5 7 14 19 20 22 24

Gross rental income (HKDm) 373 585 858 1,643 1,915 2,280 2,560 2,890

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Property development 49,432 61,407 78,615 134,022 143,695 167,849 198,312 226,318

Property rental 373 585 858 1,643 1,915 2,280 2,560 2,890

Other Revenue 1,527 2,589 2,996 2,840 2,464 3,261 3,379 3,450

Total Revenue 51,332 64,581 82,469 138,505 148,074 173,390 204,251 232,658

Other income 1,109 225 904 2,651 2,877 1,650 1,680 1,720

COGS (30,660) (39,855) (55,647) (99,196) (105,763) (121,049) (141,953) (161,463)

SG&A (1,177) (1,124) (1,486) (1,933) (2,182) (2,722) (3,103) (3,215)

Other op.expenses (720) (912) (1,331) (2,057) (2,031) (2,516) (2,759) (2,947)

Operating profit 19,884 22,914 24,909 37,970 40,975 48,753 58,116 66,753

Net-interest inc./(exp.) (106) 220 (290) (545) (574) (584) (626) (689)

Assoc/forex/extraord./others 3,988 6,288 3,773 1,261 977 4,998 4,666 5,850

Pre-tax profit 23,765 29,422 28,392 38,686 41,378 53,167 62,156 71,914

Tax (8,207) (10,590) (9,297) (15,163) (13,077) (18,756) (22,063) (26,304)

Min. int./pref. div./others (94) (110) (135) (551) (739) (541) (563) (590)

Net profit (reported) 15,464 18,722 18,960 22,972 27,562 33,870 39,530 45,020

Net profit (adjusted) 13,020 15,800 18,960 22,972 27,562 33,870 39,530 45,020

EPS (reported)(HKD) 1.892 2.291 2.320 2.811 2.795 3.091 3.608 4.109

EPS (adjusted)(HKD) 1.593 1.933 2.320 2.811 2.795 3.091 3.608 4.109

EPS (adjusted fully-diluted)(HKD) 1.595 1.936 2.320 2.811 2.795 3.091 3.608 4.109

DPS (HKD) 0.330 0.410 0.470 0.550 0.610 0.660 0.720 0.790

EBIT 19,884 22,914 24,909 37,970 40,975 48,753 58,116 66,753

EBITDA 19,942 22,984 24,993 38,061 41,070 48,853 58,219 66,860

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Profit before tax 23,765 29,422 28,392 38,686 41,378 53,167 62,156 71,914

Depreciation and amortisation 58 70 84 91 95 100 103 107

Tax paid (8,308) (11,225) (8,367) (13,647) (11,769) (16,880) (19,857) (23,674)

Change in working capital (4,604) (8,543) 2,315 7,680 39,621 11,230 11,850 11,850

Other operational CF items (3,696) 2,212 (747) 795 996 (983) (775) (1,304)

Cash flow from operations 7,216 11,936 21,677 33,605 70,320 46,634 53,477 58,893

Capex (164) (172) (30,145) (33,973) (81,326) (127,210) (42,960) (46,960)

Net (acquisitions)/disposals (8,625) (7,346) 0 0 0 0 0 0

Other investing CF items 0 0 0 0 0 0 0 0

Cash flow from investing (8,788) (7,518) (30,145) (33,973) (81,326) (127,210) (42,960) (46,960)

Change in debt 7,482 2,518 0 0 0 0 0 0

Net share issues/(repurchases) 0 0 0 0 42,806 29,724 0 0

Dividends paid (2,585) (3,157) (3,678) (4,495) (5,916) (7,231) (7,998) (8,655)

Other financing CF items (990) (1,362) (1,236) (1,358) (1,383) (1,380) (1,380) (1,380)

Cash flow from financing 3,907 (2,001) (4,913) (5,853) 35,507 21,113 (9,378) (10,035)

Forex effect/others 0 0 0 0 0 0 0 0

Change in cash 2,335 2,417 (13,381) (6,221) 24,501 (59,464) 1,139 1,898

Free cash flow 7,052 11,765 (8,467) (368) (11,006) (80,576) 10,517 11,933

Asia Pacific Daily | 4

4

China Overseas Land & Investment (688 HK): 30 June 2016

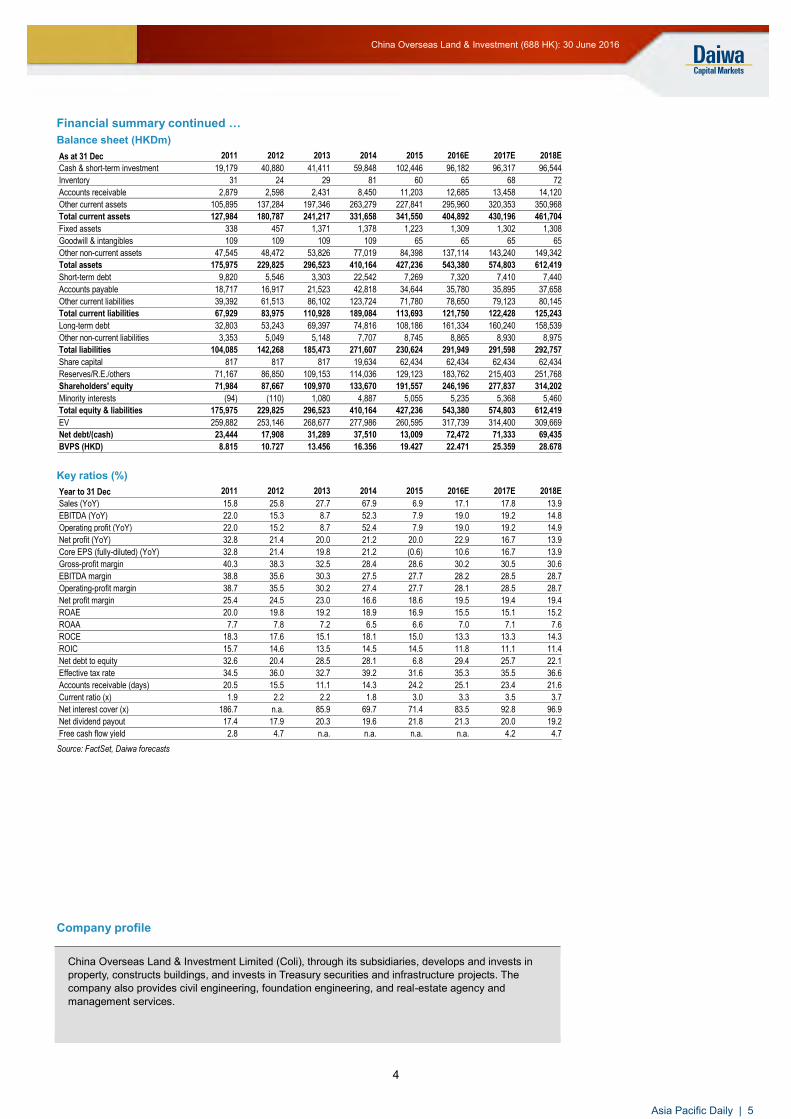

Financial summary continued … Balance sheet (HKDm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

As at 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Cash & short-term investment 19,179 40,880 41,411 59,848 102,446 96,182 96,317 96,544

Inventory 31 24 29 81 60 65 68 72

Accounts receivable 2,879 2,598 2,431 8,450 11,203 12,685 13,458 14,120

Other current assets 105,895 137,284 197,346 263,279 227,841 295,960 320,353 350,968

Total current assets 127,984 180,787 241,217 331,658 341,550 404,892 430,196 461,704

Fixed assets 338 457 1,371 1,378 1,223 1,309 1,302 1,308

Goodwill & intangibles 109 109 109 109 65 65 65 65

Other non-current assets 47,545 48,472 53,826 77,019 84,398 137,114 143,240 149,342

Total assets 175,975 229,825 296,523 410,164 427,236 543,380 574,803 612,419

Short-term debt 9,820 5,546 3,303 22,542 7,269 7,320 7,410 7,440

Accounts payable 18,717 16,917 21,523 42,818 34,644 35,780 35,895 37,658

Other current liabilities 39,392 61,513 86,102 123,724 71,780 78,650 79,123 80,145

Total current liabilities 67,929 83,975 110,928 189,084 113,693 121,750 122,428 125,243

Long-term debt 32,803 53,243 69,397 74,816 108,186 161,334 160,240 158,539

Other non-current liabilities 3,353 5,049 5,148 7,707 8,745 8,865 8,930 8,975

Total liabilities 104,085 142,268 185,473 271,607 230,624 291,949 291,598 292,757

Share capital 817 817 817 19,634 62,434 62,434 62,434 62,434

Reserves/R.E./others 71,167 86,850 109,153 114,036 129,123 183,762 215,403 251,768

Shareholders' equity 71,984 87,667 109,970 133,670 191,557 246,196 277,837 314,202

Minority interests (94) (110) 1,080 4,887 5,055 5,235 5,368 5,460

Total equity & liabilities 175,975 229,825 296,523 410,164 427,236 543,380 574,803 612,419

EV 259,882 253,146 268,677 277,986 260,595 317,739 314,400 309,669

Net debt/(cash) 23,444 17,908 31,289 37,510 13,009 72,472 71,333 69,435

BVPS (HKD) 8.815 10.727 13.456 16.356 19.427 22.471 25.359 28.678

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Sales (YoY) 15.8 25.8 27.7 67.9 6.9 17.1 17.8 13.9

EBITDA (YoY) 22.0 15.3 8.7 52.3 7.9 19.0 19.2 14.8

Operating profit (YoY) 22.0 15.2 8.7 52.4 7.9 19.0 19.2 14.9

Net profit (YoY) 32.8 21.4 20.0 21.2 20.0 22.9 16.7 13.9

Core EPS (fully-diluted) (YoY) 32.8 21.4 19.8 21.2 (0.6) 10.6 16.7 13.9

Gross-profit margin 40.3 38.3 32.5 28.4 28.6 30.2 30.5 30.6

EBITDA margin 38.8 35.6 30.3 27.5 27.7 28.2 28.5 28.7

Operating-profit margin 38.7 35.5 30.2 27.4 27.7 28.1 28.5 28.7

Net profit margin 25.4 24.5 23.0 16.6 18.6 19.5 19.4 19.4

ROAE 20.0 19.8 19.2 18.9 16.9 15.5 15.1 15.2

ROAA 7.7 7.8 7.2 6.5 6.6 7.0 7.1 7.6

ROCE 18.3 17.6 15.1 18.1 15.0 13.3 13.3 14.3

ROIC 15.7 14.6 13.5 14.5 14.5 11.8 11.1 11.4

Net debt to equity 32.6 20.4 28.5 28.1 6.8 29.4 25.7 22.1

Effective tax rate 34.5 36.0 32.7 39.2 31.6 35.3 35.5 36.6

Accounts receivable (days) 20.5 15.5 11.1 14.3 24.2 25.1 23.4 21.6

Current ratio (x) 1.9 2.2 2.2 1.8 3.0 3.3 3.5 3.7

Net interest cover (x) 186.7 n.a. 85.9 69.7 71.4 83.5 92.8 96.9

Net dividend payout 17.4 17.9 20.3 19.6 21.8 21.3 20.0 19.2

Free cash flow yield 2.8 4.7 n.a. n.a. n.a. n.a. 4.2 4.7

Company profile

China Overseas Land & Investment Limited (Coli), through its subsidiaries, develops and invests in property, constructs buildings, and invests in Treasury securities and infrastructure projects. The company also provides civil engineering, foundation engineering, and real-estate agency and management services.

Asia Pacific Daily | 5

See important disclosures, including any required research certifications, beginning on page 5

Taiwan Consumer Discretionary

What's new: We had a call with Makalot’s management on 30 June to get an update on its business outlook for 2H16. We expect the headwinds in its mass market products segment to continue, on lower orders from Kohl’s, Target, etc. However, we expect orders for its sportswear segment to keep growing on increased orders from Gap group, Under Armour and its other clients. What's the impact: Mass market orders still suffering, but sportswear orders should grow faster. We now forecast orders from Kohl’s and Target to decline by 15-20% YoY in 2016 (vs. previous forecast of 5-10% YoY decline) on softer end demand. However, we now expect 20% of its 2016 total revenue from sportswear orders (previously 18%), translating into 70% YoY revenue growth in 2016, up from 12% in 2015, on orders from Under Armour (golf and running series), Gap fit and Old Navy active. Focusing on shipment growth in 2H16. Given the weak industry outlook, Makalot now targets to focus on shipment growth in 2H16 instead of ASP growth. Besides, we expect the likely 8 new clients on its 2016 order book, including Joe Fresh (Canada-based), Oakley (US), SanMar (US), Cabela’s (US), along with a Japanese and a US client, and two potential pure sportswear clients to offset some of the order decline from its existing clients in the mass market segment. New JV plant in 2H16 should help tap the upstream space. Makalot plans to set up a second JV fabric mill in Vietnam (targets to start mass production in October 2016), which would focus on synthetic knitted base fabric for performance sportswear, to grow its sportswear segment. Earnings revisions. We cut our 2016-18E revenue by 5.6-7.3% and net profit by 13.0-16.0% as we factor in weaker-than-expected demand from mass market products and rush orders; the gross margin is likely to suffer from lower utilisation and low ASP orders. What we recommend: We reiterate our Hold (3) rating on Makalot but cut our 12-month target price to TWD142 (from TWD170). Our new TP is based on a 2016-17E EPS (previously 2016E EPS) and PER of 15x (from 16x), which is below the stock’s past 5-year average PER of 18x, ranging at 11-29x. We expect improving ROE (19.8-25.5% over 2016-18E) and dividend yields (5.0-6.9% over 2016-18E) to provide a floor for the shares. Key upside/downside risks: better/worse-than-expected sales growth from its main clients. How we differ: Our 2016-18E EPS are 10.1-17.2% below consensus, as we are less positive on Makalot’s gross margin expansion in 2016-18.

30 June 2016

Still in the shadows

Overall demand from mass market products continues to be weak… …however, sportswear orders remain solid Reiterating our Hold (3) rating; lowering TP to TWD142

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

Makalot Industrial (1477 TT)

Target price: TWD142.00 (from TWD170.00)

Share price (30 Jun): TWD150.50 | Up/downside: -5.6%

Helen Chien(886) 2 8758 6254

Forecast revisions (%)Year to 31 Dec 16E 17E 18E

Revenue change (5.6) (7.3) (7.3)

Net profit change (16.0) (15.9) (13.0)

Core EPS (FD) change (16.1) (16.0) (13.1)

60

80

100

120

140

140

178

215

253

290

Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

Share price performance

Makalot In (LHS)Relative to TWSE Index (RHS)

(TWD) (%)

12-month range 141.50-289.50

Market cap (USDbn) 0.92

3m avg daily turnover (USDm) 8.58

Shares outstanding (m) 198

Major shareholder Li-Pian Zhou (Chairman) (4.0%)

Financial summary (TWD)Year to 31 Dec 16E 17E 18E

Revenue (m) 23,583 25,233 27,757

Operating profit (m) 2,145 2,547 2,996

Net profit (m) 1,753 2,051 2,439

Core EPS (fully-diluted) 8.631 10.102 12.010

EPS change (%) (18.9) 17.0 18.9

Daiwa vs Cons. EPS (%) (17.2) (14.9) (10.1)

PER (x) 17.4 14.9 12.5

Dividend yield (%) 5.0 5.8 6.9

DPS 7.5 8.8 10.4

PBR (x) 3.5 3.3 3.0

EV/EBITDA (x) 10.2 8.5 7.2

ROE (%) 19.8 23.0 25.5

Asia Pacific Daily | 6

2

Makalot Industrial (1477 TT): 30 June 2016

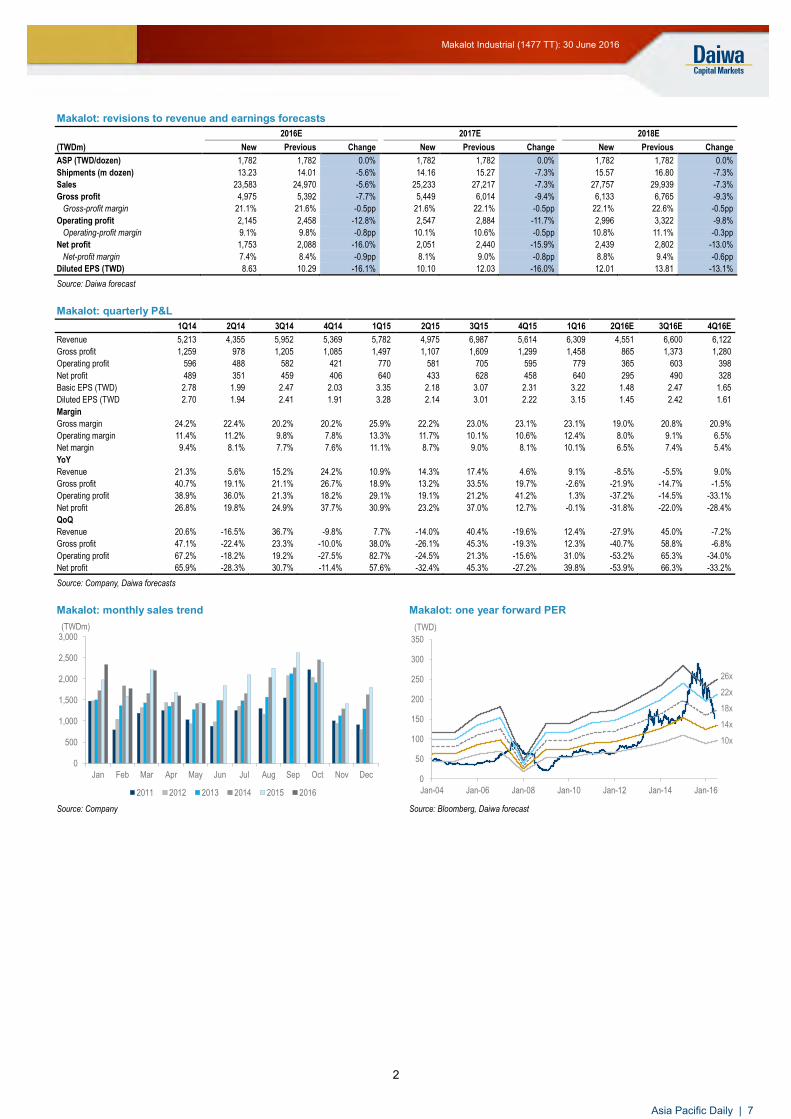

Makalot: revisions to revenue and earnings forecasts

2016E 2017E 2018E

(TWDm) New Previous Change New Previous Change New Previous Change

ASP (TWD/dozen) 1,782 1,782 0.0% 1,782 1,782 0.0% 1,782 1,782 0.0%

Shipments (m dozen) 13.23 14.01 -5.6% 14.16 15.27 -7.3% 15.57 16.80 -7.3%

Sales 23,583 24,970 -5.6% 25,233 27,217 -7.3% 27,757 29,939 -7.3%

Gross profit 4,975 5,392 -7.7% 5,449 6,014 -9.4% 6,133 6,765 -9.3%

Gross-profit margin 21.1% 21.6% -0.5pp 21.6% 22.1% -0.5pp 22.1% 22.6% -0.5pp

Operating profit 2,145 2,458 -12.8% 2,547 2,884 -11.7% 2,996 3,322 -9.8%

Operating-profit margin 9.1% 9.8% -0.8pp 10.1% 10.6% -0.5pp 10.8% 11.1% -0.3pp

Net profit 1,753 2,088 -16.0% 2,051 2,440 -15.9% 2,439 2,802 -13.0%

Net-profit margin 7.4% 8.4% -0.9pp 8.1% 9.0% -0.8pp 8.8% 9.4% -0.6pp

Diluted EPS (TWD) 8.63 10.29 -16.1% 10.10 12.03 -16.0% 12.01 13.81 -13.1%

Source: Daiwa forecast

Makalot: quarterly P&L

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16E 3Q16E 4Q16E

Revenue 5,213 4,355 5,952 5,369 5,782 4,975 6,987 5,614 6,309 4,551 6,600 6,122

Gross profit 1,259 978 1,205 1,085 1,497 1,107 1,609 1,299 1,458 865 1,373 1,280

Operating profit 596 488 582 421 770 581 705 595 779 365 603 398

Net profit 489 351 459 406 640 433 628 458 640 295 490 328

Basic EPS (TWD) 2.78 1.99 2.47 2.03 3.35 2.18 3.07 2.31 3.22 1.48 2.47 1.65

Diluted EPS (TWD 2.70 1.94 2.41 1.91 3.28 2.14 3.01 2.22 3.15 1.45 2.42 1.61

Margin

Gross margin 24.2% 22.4% 20.2% 20.2% 25.9% 22.2% 23.0% 23.1% 23.1% 19.0% 20.8% 20.9%

Operating margin 11.4% 11.2% 9.8% 7.8% 13.3% 11.7% 10.1% 10.6% 12.4% 8.0% 9.1% 6.5%

Net margin 9.4% 8.1% 7.7% 7.6% 11.1% 8.7% 9.0% 8.1% 10.1% 6.5% 7.4% 5.4%

YoY

Revenue 21.3% 5.6% 15.2% 24.2% 10.9% 14.3% 17.4% 4.6% 9.1% -8.5% -5.5% 9.0%

Gross profit 40.7% 19.1% 21.1% 26.7% 18.9% 13.2% 33.5% 19.7% -2.6% -21.9% -14.7% -1.5%

Operating profit 38.9% 36.0% 21.3% 18.2% 29.1% 19.1% 21.2% 41.2% 1.3% -37.2% -14.5% -33.1%

Net profit 26.8% 19.8% 24.9% 37.7% 30.9% 23.2% 37.0% 12.7% -0.1% -31.8% -22.0% -28.4%

QoQ

Revenue 20.6% -16.5% 36.7% -9.8% 7.7% -14.0% 40.4% -19.6% 12.4% -27.9% 45.0% -7.2%

Gross profit 47.1% -22.4% 23.3% -10.0% 38.0% -26.1% 45.3% -19.3% 12.3% -40.7% 58.8% -6.8%

Operating profit 67.2% -18.2% 19.2% -27.5% 82.7% -24.5% 21.3% -15.6% 31.0% -53.2% 65.3% -34.0%

Net profit 65.9% -28.3% 30.7% -11.4% 57.6% -32.4% 45.3% -27.2% 39.8% -53.9% 66.3% -33.2%

Source: Company, Daiwa forecasts

Makalot: monthly sales trend Makalot: one year forward PER

Source: Company Source: Bloomberg, Daiwa forecast

0

500

1,000

1,500

2,000

2,500

3,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(TWDm)

2011 2012 2013 2014 2015 2016

0

50

100

150

200

250

300

350

Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

(TWD)

22x

1

1

26x

14x

18x

10x

Asia Pacific Daily | 7

3

Makalot Industrial (1477 TT): 30 June 2016

Financial summary Key assumptions

Profit and loss (TWDm)

Cash flow (TWDm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

ASP (TWD) (dozen) 1,853.4 1,732.2 1,704.2 1,800.3 1,800.3 1,782.3 1,782.3 1,782.3

Shipments (m dozen) 8.2 9.2 10.5 11.6 13.0 13.2 14.2 15.6

Consolidated gross margin (%) 20.9 19.9 19.9 21.7 23.6 21.1 21.6 22.1

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

US 13,870 14,168 15,785 18,215 18,893 18,394 19,177 20,540

Japan 0 159 896 1,358 3,153 3,773 4,542 5,551

Other Revenue 1,253 1,540 1,230 1,316 1,313 1,415 1,514 1,665

Total Revenue 15,123 15,867 17,911 20,889 23,359 23,583 25,233 27,757

Other income 0 0 0 0 0 0 0 0

COGS (11,966) (12,712) (14,344) (16,362) (17,847) (18,608) (19,784) (21,624)

SG&A (1,709) (1,671) (1,943) (2,440) (2,861) (2,830) (2,902) (3,137)

Other op.expenses 0 0 0 0 0 0 0 0

Operating profit 1,449 1,484 1,624 2,087 2,650 2,145 2,547 2,996

Net-interest inc./(exp.) (23) (8) (38) (45) (28) (22) (62) (35)

Assoc/forex/extraord./others (20) (38) 61 52 69 30 34 34

Pre-tax profit 1,406 1,438 1,647 2,095 2,691 2,153 2,520 2,996

Tax (293) (261) (304) (389) (514) (400) (469) (557)

Min. int./pref. div./others (2) (1) (1) (0) (18) 0 0 0

Net profit (reported) 1,111 1,175 1,342 1,705 2,159 1,753 2,051 2,439

Net profit (adjusted) 1,111 1,175 1,342 1,705 2,159 1,753 2,051 2,439

EPS (reported)(TWD) 6.639 6.887 7.716 9.268 10.898 8.815 10.316 12.265

EPS (adjusted)(TWD) 6.639 6.887 7.716 9.268 10.898 8.815 10.316 12.265

EPS (adjusted fully-diluted)(TWD) 6.375 6.634 7.382 8.959 10.642 8.631 10.102 12.010

DPS (TWD) 5.887 6.012 7.486 8.291 9.520 7.492 8.769 10.425

EBIT 1,449 1,484 1,624 2,087 2,650 2,145 2,547 2,996

EBITDA 1,632 1,677 1,827 2,347 2,955 2,562 2,990 3,467

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Profit before tax 1,406 1,438 1,647 2,095 2,691 2,153 2,520 2,996

Depreciation and amortisation 183 193 203 260 305 417 443 471

Tax paid (293) (261) (281) (337) (452) (400) (469) (557)

Change in working capital (817) 878 (575) (800) 933 1,301 237 236

Other operational CF items (2) 17 (2) 72 100 28 52 25

Cash flow from operations 476 2,264 993 1,291 3,576 3,499 2,782 3,170

Capex (394) (252) (3,238) (470) (766) (803) (771) (771)

Net (acquisitions)/disposals 26 5 2 38 18 0 0 0

Other investing CF items (9) (2) (144) (99) (33) 33 33 33

Cash flow from investing (377) (249) (3,380) (530) (780) (770) (738) (738)

Change in debt 139 353 1,183 (1,100) (97) 1,197 (300) (300)

Net share issues/(repurchases) 0 0 0 2,115 0 0 0 0

Dividends paid (734) (994) (1,029) (1,311) (1,473) (1,886) (1,490) (1,744)

Other financing CF items 0 4 18 (16) 19 0 0 0

Cash flow from financing (595) (637) 171 (312) (1,551) (689) (1,790) (2,044)

Forex effect/others 63 (43) 42 99 97 0 0 0

Change in cash (433) 1,336 (2,175) 547 1,342 2,039 255 388

Free cash flow 83 2,012 (2,245) 821 2,811 2,696 2,011 2,399

Asia Pacific Daily | 8

4

Makalot Industrial (1477 TT): 30 June 2016

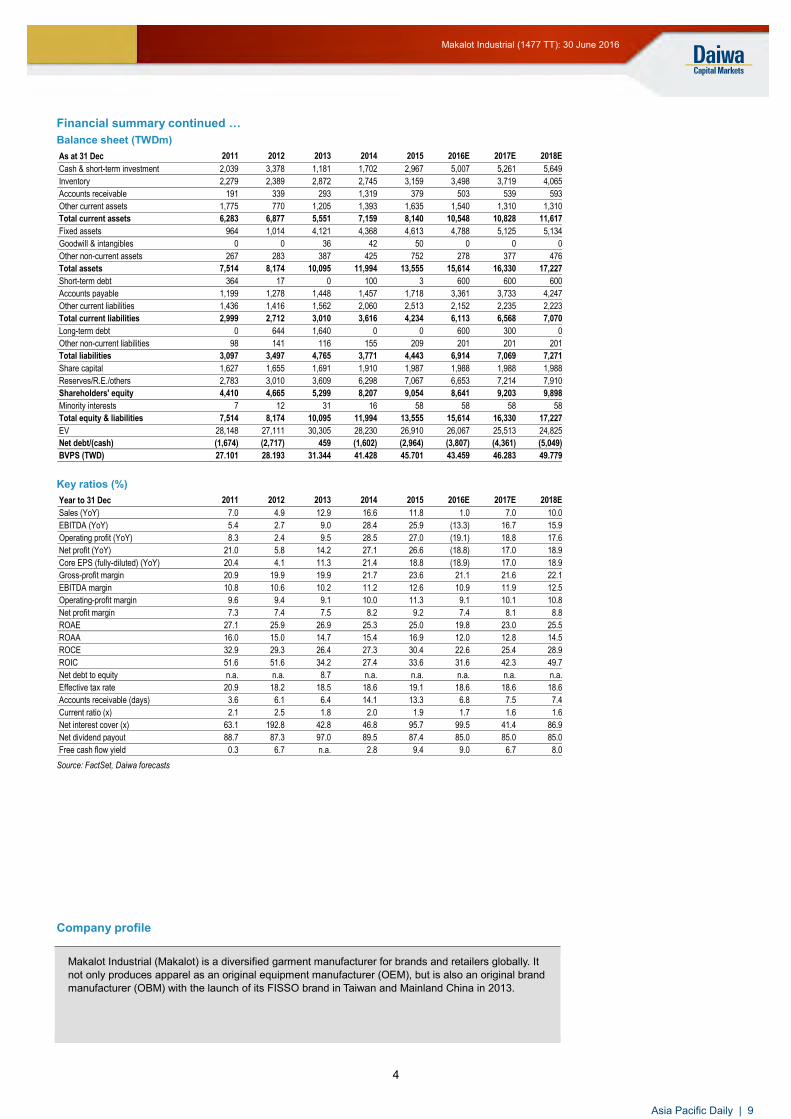

Financial summary continued … Balance sheet (TWDm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

As at 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Cash & short-term investment 2,039 3,378 1,181 1,702 2,967 5,007 5,261 5,649

Inventory 2,279 2,389 2,872 2,745 3,159 3,498 3,719 4,065

Accounts receivable 191 339 293 1,319 379 503 539 593

Other current assets 1,775 770 1,205 1,393 1,635 1,540 1,310 1,310

Total current assets 6,283 6,877 5,551 7,159 8,140 10,548 10,828 11,617

Fixed assets 964 1,014 4,121 4,368 4,613 4,788 5,125 5,134

Goodwill & intangibles 0 0 36 42 50 0 0 0

Other non-current assets 267 283 387 425 752 278 377 476

Total assets 7,514 8,174 10,095 11,994 13,555 15,614 16,330 17,227

Short-term debt 364 17 0 100 3 600 600 600

Accounts payable 1,199 1,278 1,448 1,457 1,718 3,361 3,733 4,247

Other current liabilities 1,436 1,416 1,562 2,060 2,513 2,152 2,235 2,223

Total current liabilities 2,999 2,712 3,010 3,616 4,234 6,113 6,568 7,070

Long-term debt 0 644 1,640 0 0 600 300 0

Other non-current liabilities 98 141 116 155 209 201 201 201

Total liabilities 3,097 3,497 4,765 3,771 4,443 6,914 7,069 7,271

Share capital 1,627 1,655 1,691 1,910 1,987 1,988 1,988 1,988

Reserves/R.E./others 2,783 3,010 3,609 6,298 7,067 6,653 7,214 7,910

Shareholders' equity 4,410 4,665 5,299 8,207 9,054 8,641 9,203 9,898

Minority interests 7 12 31 16 58 58 58 58

Total equity & liabilities 7,514 8,174 10,095 11,994 13,555 15,614 16,330 17,227

EV 28,148 27,111 30,305 28,230 26,910 26,067 25,513 24,825

Net debt/(cash) (1,674) (2,717) 459 (1,602) (2,964) (3,807) (4,361) (5,049)

BVPS (TWD) 27.101 28.193 31.344 41.428 45.701 43.459 46.283 49.779

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Sales (YoY) 7.0 4.9 12.9 16.6 11.8 1.0 7.0 10.0

EBITDA (YoY) 5.4 2.7 9.0 28.4 25.9 (13.3) 16.7 15.9

Operating profit (YoY) 8.3 2.4 9.5 28.5 27.0 (19.1) 18.8 17.6

Net profit (YoY) 21.0 5.8 14.2 27.1 26.6 (18.8) 17.0 18.9

Core EPS (fully-diluted) (YoY) 20.4 4.1 11.3 21.4 18.8 (18.9) 17.0 18.9

Gross-profit margin 20.9 19.9 19.9 21.7 23.6 21.1 21.6 22.1

EBITDA margin 10.8 10.6 10.2 11.2 12.6 10.9 11.9 12.5

Operating-profit margin 9.6 9.4 9.1 10.0 11.3 9.1 10.1 10.8

Net profit margin 7.3 7.4 7.5 8.2 9.2 7.4 8.1 8.8

ROAE 27.1 25.9 26.9 25.3 25.0 19.8 23.0 25.5

ROAA 16.0 15.0 14.7 15.4 16.9 12.0 12.8 14.5

ROCE 32.9 29.3 26.4 27.3 30.4 22.6 25.4 28.9

ROIC 51.6 51.6 34.2 27.4 33.6 31.6 42.3 49.7

Net debt to equity n.a. n.a. 8.7 n.a. n.a. n.a. n.a. n.a.

Effective tax rate 20.9 18.2 18.5 18.6 19.1 18.6 18.6 18.6

Accounts receivable (days) 3.6 6.1 6.4 14.1 13.3 6.8 7.5 7.4

Current ratio (x) 2.1 2.5 1.8 2.0 1.9 1.7 1.6 1.6

Net interest cover (x) 63.1 192.8 42.8 46.8 95.7 99.5 41.4 86.9

Net dividend payout 88.7 87.3 97.0 89.5 87.4 85.0 85.0 85.0

Free cash flow yield 0.3 6.7 n.a. 2.8 9.4 9.0 6.7 8.0

Company profile

Makalot Industrial (Makalot) is a diversified garment manufacturer for brands and retailers globally. It not only produces apparel as an original equipment manufacturer (OEM), but is also an original brand manufacturer (OBM) with the launch of its FISSO brand in Taiwan and Mainland China in 2013.

Asia Pacific Daily | 9

See important disclosures, including any required research certifications, beginning on page 5

Japan Financials

What's new: AGT’s unit price has been lacklustre post-Brexit, which would seem at odds with the strong price recovery seen by most of the other Singapore-listed yield stocks (now trading even higher than their 23 June [pre-Brexit] close). We see this as another example of the market ignoring the merits of AGT. We reiterate our Buy (1) rating on the stock. What's the impact: In retrospect, it is probably not surprising that many yield stocks in Singapore are performing better after Brexit as the outcome has lowered expectations of Fed rate hikes, prolonging the low overall interest-rate environment. From 23-29 June, the 10-year SGS yield fell by 14bps to 1.9%. The combination of high yield and perceived defensiveness is apparently in vogue again, but the market has neglected the unit price of AGT, which has barely budged. We believe the pricing discrepancy is unjustified because the Brexit fallout provides AGT with one clear benefit over the other Singapore-listed yield stocks: a stronger JPY that translates directly into higher DPU forecasts. According to Daiwa’s Yen 4Sight report, 28 June 2016, we expect a stronger JPY and have lowered our JPY:USD forecast for end-1Q17 to 102 from 110. Using our new forecast and the spot SGD:USD rate of 1.35, we lower our JPY:SGD assumption (for all periods) to 75.6 from 79.9, and revise up our DPU forecasts by 5.7% for FY17-19. We also raise our DDM-derived 12-month TP to SGD0.90 from SGD0.89 (including the 2HFY16 dividend). Furthermore, we don’t believe investors should assume that AGT will be neglected forever. AGT has been the best-performing stock (excluding privatisations) under our coverage in Singapore YTD (15% YTD vs. 6.3% for the FSTREI and -3.1% for the FSSTI). At some stage, we expect the market to price in the positive fundamentals from a stronger JPY. Finally, another positive unit-price catalyst could come from unit buybacks. AGT raised the possibility of using retained income for unit buybacks in its 3QFY16 results presentation (announced on 10 February 2016). Judging by AGT’s deep discounts to NAV and fair value, we believe unit buybacks, if implemented from FY17, could be highly DPU accretive. What we recommend: We reaffirm our Buy (1) rating and believe its recurrent DPU yields of 11.6-12% cannot be ignored for long. A downside risk would be unforeseen weather-related disruptions on operating performance in the coming months. How we differ: We are the only research house to cover AGT.

30 June 2016

Brexit payoff: higher SGD distributions

s

A stronger JPY vs. the SGD is a positive Brexit outcome for AGT Revising up our DPU forecasts for FY17-19 by 5.7% Reaffirming our Buy (1) rating with a higher TP of SGD0.90

Source: Daiwa forecasts

Financial summary (JPY)

Year to 31 Mar 17E 18E 19E

Revenue (bn) 52.72 52.42 52.48

Operating profit (bn) 8.68 8.42 8.47

Net profit (bn) 5.58 5.36 5.41

Core EPS (fully-diluted) 5.073 4.878 4.920

EPS change (%) (14.4) (3.8) 0.9

Daiwa vs Cons. EPS (%) n.a. n.a. n.a.

PER (x) 8.9 9.3 9.2

Dividend yield (%) 12.0 11.6 11.7

DPU 5.452 5.260 5.295

DPU (SGD) 0.0721 0.0696 0.0700

PBR (x) 0.6 0.6 0.6

EV/EBITDA (x) 6.9 7.0 6.8

ROE (%) 6.8 6.6 6.7

Source: FactSet, Daiwa forecasts

Accordia Golf Trust (AGT SP)

Target price: SGD0.900 (from SGD0.890)

Share price (29 Jun): SGD0.600 | Up/downside: +50.0%

David Lum, CFA(65) 6329 2102

Forecast revisions (%)Year to 31 Mar 17E 18E 19E

Revenue change - - -

Net profit change - - -

Core EPS (FD) change - - -

80

89

98

106

115

0.45

0.51

0.58

0.64

0.70

Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

Share price performance

Accordia G (LHS) Relative to FSSTI (RHS)

(SGD) (%)

12-month range 0.480-0.690

Market cap (USDbn) 0.48

3m avg daily turnover (USDm) 0.91

Shares outstanding (m) 1,099

Major shareholder Accordia Golf (28.9%)

Asia Pacific Daily | 10

2

Accordia Golf Trust (AGT SP): 30 June 2016

AGT: earnings and DPU-forecast changes AGT: Daiwa DDM valuation

JPYbn FY17E FY17E

FY18E FY18E

FY19E FY19E

Year to March Prev New Chg Prev New Chg Prev New Chg

Revenue 52.55 52.72 0.0% 52.44 52.42 0.0% 52.48 52.48 0.0%

Expenses (42.12) (44.04) 0.0% (42.06) (44.00) 0.0% (44.01) (44.01) 0.0%

Operating profit 10.44 8.68 0.0% 10.39 8.42 0.0% 8.47 8.47 0.0%

Net profit 7.89 5.58 0.0% 7.84 5.36 0.0% 5.41 5.41 0.0%

EBITDA 13.84 12.09 0.0% 13.79 11.83 0.0% 11.89 11.89 0.0%

Distribution 6.02 5.99 0.0% 5.97 5.78 0.0% 5.82 5.82 0.0%

DPU (JPY) 5.478 5.452 0.0% 5.433 5.260 0.0% 5.295 5.295 0.0%

Distribution (SGDm) 70.01 79.27 5.7% 69.43 76.48 5.7% 72.84 76.99 5.7%

DPU (SGD) 0.0637 0.0721 5.7% 0.0632 0.0696 5.7% 0.0663 0.0700 5.7%

DPU yield

12.0%

11.6%

11.7%

Cost of equity 7.5%

Long-term growth rate -0.5%

Effective cap rate 8.0%

PV of 10-year DPU forecasts (SGD) 0.49

PV of terminal value (SGD) 0.41

DDM valuation (SGD) 0.90

Source: Daiwa forecasts

Source: Daiwa estimates

Daiwa Securities group subsidiary Daiwa PI Partners Co.Ltd. has extended to Accordia Golf Co, Ltd.(“Accordia Golf”) a loan facility with stock acquisition rights. Another Daiwa Securities group subsidiary, Daiwa Real Estate Asset Management Co. Ltd., has entered into an asset management agreement to provide advice to a godo kaisha SPC established for the purpose of acquiring from Accordia Golf shares in Accordia Golf subsidiaries owning golf courses. Daiwa Real Estate Asset Management Co. Ltd. owns a 51% stake in the trustee-manager that assumes the role of trustee and asset manager of Accordia Golf Trust, a tokumei kumiai (silent partnership) investor in the SPC. (Accordia Golf owns a 49% stake in the trustee-manager). When Accordia Golf Trust was listed on the Singapore Exchange, Daiwa Securities group was one of the underwriters and sellers of Accordia Golf Trust units in Japan and abroad (Daiwa Securities Co. Ltd. was sole seller in Japan). As a joint global coordinator, Daiwa Securities group subsidiary Daiwa Capital Markets Singapore Limited provided general advice concerning Accordia Golf Trust, including with regard to structuring the trust vehicle.

Asia Pacific Daily | 11

3

Accordia Golf Trust (AGT SP): 30 June 2016

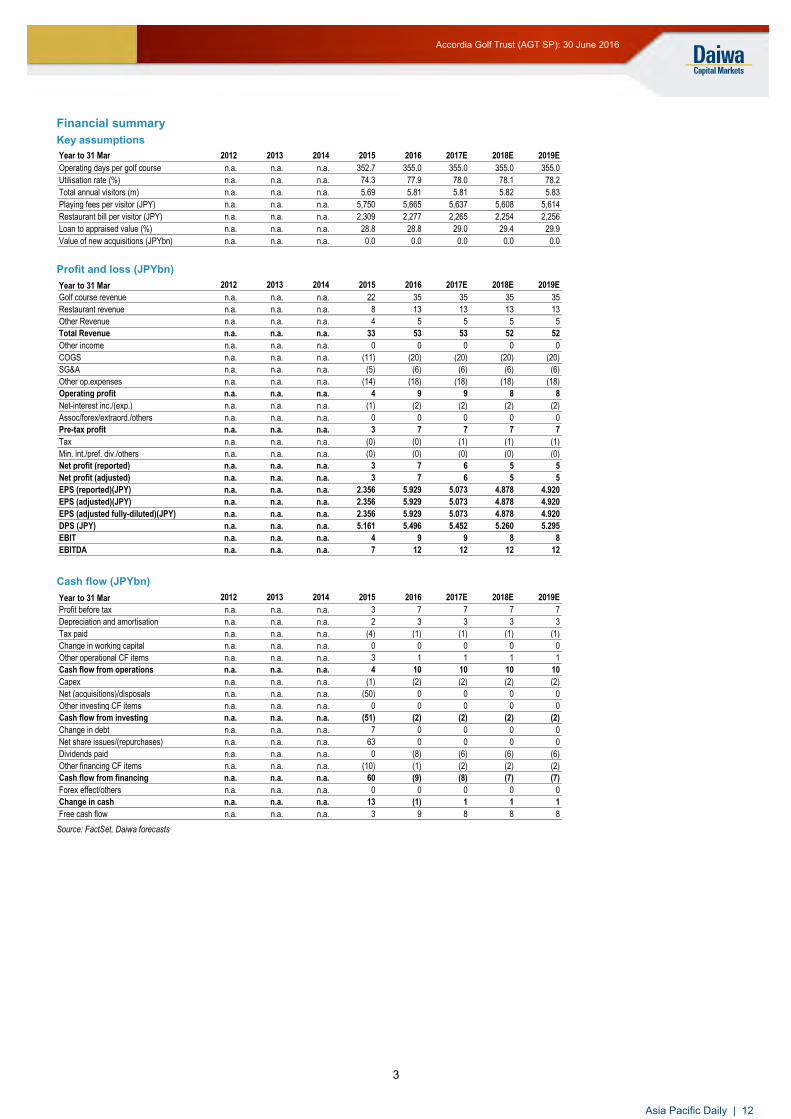

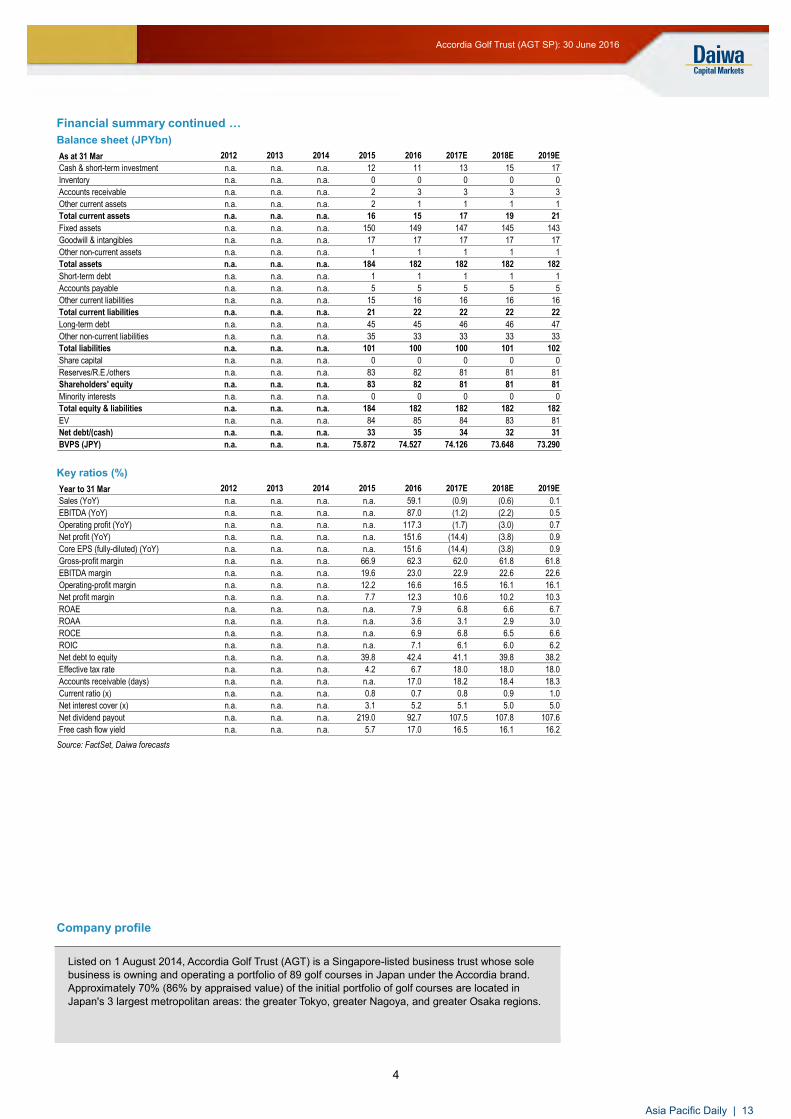

Financial summary Key assumptions

Profit and loss (JPYbn)

Cash flow (JPYbn)

Source: FactSet, Daiwa forecasts

Year to 31 Mar 2012 2013 2014 2015 2016 2017E 2018E 2019E

Operating days per golf course n.a. n.a. n.a. 352.7 355.0 355.0 355.0 355.0

Utilisation rate (%) n.a. n.a. n.a. 74.3 77.9 78.0 78.1 78.2

Total annual visitors (m) n.a. n.a. n.a. 5.69 5.81 5.81 5.82 5.83

Playing fees per visitor (JPY) n.a. n.a. n.a. 5,750 5,665 5,637 5,608 5,614

Restaurant bill per visitor (JPY) n.a. n.a. n.a. 2,309 2,277 2,265 2,254 2,256

Loan to appraised value (%) n.a. n.a. n.a. 28.8 28.8 29.0 29.4 29.9

Value of new acquisitions (JPYbn) n.a. n.a. n.a. 0.0 0.0 0.0 0.0 0.0

Year to 31 Mar 2012 2013 2014 2015 2016 2017E 2018E 2019E

Golf course revenue n.a. n.a. n.a. 22 35 35 35 35

Restaurant revenue n.a. n.a. n.a. 8 13 13 13 13

Other Revenue n.a. n.a. n.a. 4 5 5 5 5

Total Revenue n.a. n.a. n.a. 33 53 53 52 52

Other income n.a. n.a. n.a. 0 0 0 0 0

COGS n.a. n.a. n.a. (11) (20) (20) (20) (20)

SG&A n.a. n.a. n.a. (5) (6) (6) (6) (6)

Other op.expenses n.a. n.a. n.a. (14) (18) (18) (18) (18)

Operating profit n.a. n.a. n.a. 4 9 9 8 8

Net-interest inc./(exp.) n.a. n.a. n.a. (1) (2) (2) (2) (2)

Assoc/forex/extraord./others n.a. n.a. n.a. 0 0 0 0 0

Pre-tax profit n.a. n.a. n.a. 3 7 7 7 7

Tax n.a. n.a. n.a. (0) (0) (1) (1) (1)

Min. int./pref. div./others n.a. n.a. n.a. (0) (0) (0) (0) (0)

Net profit (reported) n.a. n.a. n.a. 3 7 6 5 5

Net profit (adjusted) n.a. n.a. n.a. 3 7 6 5 5

EPS (reported)(JPY) n.a. n.a. n.a. 2.356 5.929 5.073 4.878 4.920

EPS (adjusted)(JPY) n.a. n.a. n.a. 2.356 5.929 5.073 4.878 4.920

EPS (adjusted fully-diluted)(JPY) n.a. n.a. n.a. 2.356 5.929 5.073 4.878 4.920

DPS (JPY) n.a. n.a. n.a. 5.161 5.496 5.452 5.260 5.295

EBIT n.a. n.a. n.a. 4 9 9 8 8

EBITDA n.a. n.a. n.a. 7 12 12 12 12

Year to 31 Mar 2012 2013 2014 2015 2016 2017E 2018E 2019E

Profit before tax n.a. n.a. n.a. 3 7 7 7 7

Depreciation and amortisation n.a. n.a. n.a. 2 3 3 3 3

Tax paid n.a. n.a. n.a. (4) (1) (1) (1) (1)

Change in working capital n.a. n.a. n.a. 0 0 0 0 0

Other operational CF items n.a. n.a. n.a. 3 1 1 1 1

Cash flow from operations n.a. n.a. n.a. 4 10 10 10 10

Capex n.a. n.a. n.a. (1) (2) (2) (2) (2)

Net (acquisitions)/disposals n.a. n.a. n.a. (50) 0 0 0 0

Other investing CF items n.a. n.a. n.a. 0 0 0 0 0

Cash flow from investing n.a. n.a. n.a. (51) (2) (2) (2) (2)

Change in debt n.a. n.a. n.a. 7 0 0 0 0

Net share issues/(repurchases) n.a. n.a. n.a. 63 0 0 0 0

Dividends paid n.a. n.a. n.a. 0 (8) (6) (6) (6)

Other financing CF items n.a. n.a. n.a. (10) (1) (2) (2) (2)

Cash flow from financing n.a. n.a. n.a. 60 (9) (8) (7) (7)

Forex effect/others n.a. n.a. n.a. 0 0 0 0 0

Change in cash n.a. n.a. n.a. 13 (1) 1 1 1

Free cash flow n.a. n.a. n.a. 3 9 8 8 8

Asia Pacific Daily | 12

4

Accordia Golf Trust (AGT SP): 30 June 2016

Financial summary continued … Balance sheet (JPYbn)

Key ratios (%)

Source: FactSet, Daiwa forecasts

As at 31 Mar 2012 2013 2014 2015 2016 2017E 2018E 2019E

Cash & short-term investment n.a. n.a. n.a. 12 11 13 15 17

Inventory n.a. n.a. n.a. 0 0 0 0 0

Accounts receivable n.a. n.a. n.a. 2 3 3 3 3

Other current assets n.a. n.a. n.a. 2 1 1 1 1

Total current assets n.a. n.a. n.a. 16 15 17 19 21

Fixed assets n.a. n.a. n.a. 150 149 147 145 143

Goodwill & intangibles n.a. n.a. n.a. 17 17 17 17 17

Other non-current assets n.a. n.a. n.a. 1 1 1 1 1

Total assets n.a. n.a. n.a. 184 182 182 182 182

Short-term debt n.a. n.a. n.a. 1 1 1 1 1

Accounts payable n.a. n.a. n.a. 5 5 5 5 5

Other current liabilities n.a. n.a. n.a. 15 16 16 16 16

Total current liabilities n.a. n.a. n.a. 21 22 22 22 22

Long-term debt n.a. n.a. n.a. 45 45 46 46 47

Other non-current liabilities n.a. n.a. n.a. 35 33 33 33 33

Total liabilities n.a. n.a. n.a. 101 100 100 101 102

Share capital n.a. n.a. n.a. 0 0 0 0 0

Reserves/R.E./others n.a. n.a. n.a. 83 82 81 81 81

Shareholders' equity n.a. n.a. n.a. 83 82 81 81 81

Minority interests n.a. n.a. n.a. 0 0 0 0 0

Total equity & liabilities n.a. n.a. n.a. 184 182 182 182 182

EV n.a. n.a. n.a. 84 85 84 83 81

Net debt/(cash) n.a. n.a. n.a. 33 35 34 32 31

BVPS (JPY) n.a. n.a. n.a. 75.872 74.527 74.126 73.648 73.290

Year to 31 Mar 2012 2013 2014 2015 2016 2017E 2018E 2019E

Sales (YoY) n.a. n.a. n.a. n.a. 59.1 (0.9) (0.6) 0.1

EBITDA (YoY) n.a. n.a. n.a. n.a. 87.0 (1.2) (2.2) 0.5

Operating profit (YoY) n.a. n.a. n.a. n.a. 117.3 (1.7) (3.0) 0.7

Net profit (YoY) n.a. n.a. n.a. n.a. 151.6 (14.4) (3.8) 0.9

Core EPS (fully-diluted) (YoY) n.a. n.a. n.a. n.a. 151.6 (14.4) (3.8) 0.9

Gross-profit margin n.a. n.a. n.a. 66.9 62.3 62.0 61.8 61.8

EBITDA margin n.a. n.a. n.a. 19.6 23.0 22.9 22.6 22.6

Operating-profit margin n.a. n.a. n.a. 12.2 16.6 16.5 16.1 16.1

Net profit margin n.a. n.a. n.a. 7.7 12.3 10.6 10.2 10.3

ROAE n.a. n.a. n.a. n.a. 7.9 6.8 6.6 6.7

ROAA n.a. n.a. n.a. n.a. 3.6 3.1 2.9 3.0

ROCE n.a. n.a. n.a. n.a. 6.9 6.8 6.5 6.6

ROIC n.a. n.a. n.a. n.a. 7.1 6.1 6.0 6.2

Net debt to equity n.a. n.a. n.a. 39.8 42.4 41.1 39.8 38.2

Effective tax rate n.a. n.a. n.a. 4.2 6.7 18.0 18.0 18.0

Accounts receivable (days) n.a. n.a. n.a. n.a. 17.0 18.2 18.4 18.3

Current ratio (x) n.a. n.a. n.a. 0.8 0.7 0.8 0.9 1.0

Net interest cover (x) n.a. n.a. n.a. 3.1 5.2 5.1 5.0 5.0

Net dividend payout n.a. n.a. n.a. 219.0 92.7 107.5 107.8 107.6

Free cash flow yield n.a. n.a. n.a. 5.7 17.0 16.5 16.1 16.2

Company profile

Listed on 1 August 2014, Accordia Golf Trust (AGT) is a Singapore-listed business trust whose sole business is owning and operating a portfolio of 89 golf courses in Japan under the Accordia brand. Approximately 70% (86% by appraised value) of the initial portfolio of golf courses are located in Japan's 3 largest metropolitan areas: the greater Tokyo, greater Nagoya, and greater Osaka regions.

Asia Pacific Daily | 13

Asiamoney’s2013

Best DomesticEquity House

Corporate flash 30 June 2016

Disclosure: Bahana Securities does and seeks to do business with companies covered in its research reports. Investors should consider this report as only a single factor in making their investment decision.

Please see the important disclaimer information on the back of this report *Based on consensus’ recent changes ↑ (up), ↓ (down), ↔ (unchanged)

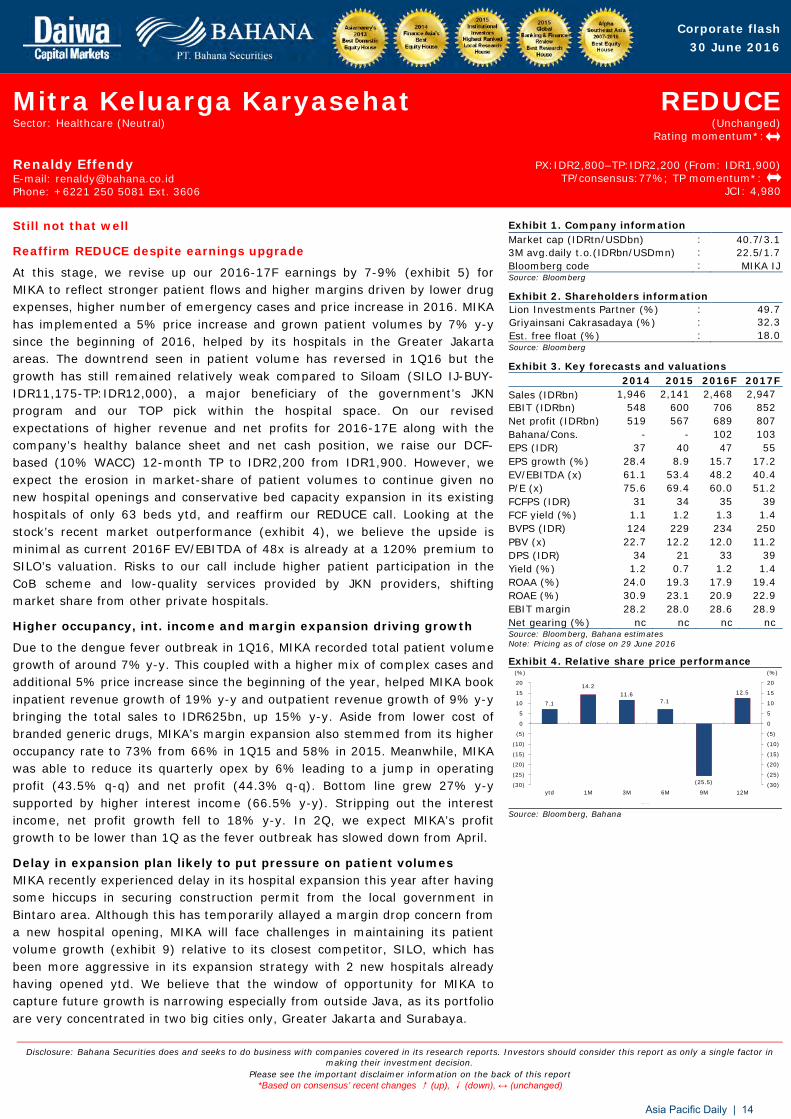

Mitra Keluarga Karyasehat Sector: Healthcare (Neutral)

REDUCE (Unchanged)

Rating momentum*:

Renaldy Effendy E-mail: [email protected] Phone: +6221 250 5081 Ext. 3606

PX:IDR2,800–TP:IDR2,200 (From: IDR1,900) TP/consensus:77%; TP momentum*:

JCI: 4,980

Still not that well

Reaffirm REDUCE despite earnings upgrade

At this stage, we revise up our 2016-17F earnings by 7-9% (exhibit 5) for MIKA to reflect stronger patient flows and higher margins driven by lower drug expenses, higher number of emergency cases and price increase in 2016. MIKA has implemented a 5% price increase and grown patient volumes by 7% y-y since the beginning of 2016, helped by its hospitals in the Greater Jakarta areas. The downtrend seen in patient volume has reversed in 1Q16 but the growth has still remained relatively weak compared to Siloam (SILO IJ-BUY-IDR11,175-TP:IDR12,000), a major beneficiary of the government’s JKN program and our TOP pick within the hospital space. On our revised expectations of higher revenue and net profits for 2016-17E along with the company’s healthy balance sheet and net cash position, we raise our DCF-based (10% WACC) 12-month TP to IDR2,200 from IDR1,900. However, we expect the erosion in market-share of patient volumes to continue given no new hospital openings and conservative bed capacity expansion in its existing hospitals of only 63 beds ytd, and reaffirm our REDUCE call. Looking at the stock’s recent market outperformance (exhibit 4), we believe the upside is minimal as current 2016F EV/EBITDA of 48x is already at a 120% premium to SILO’s valuation. Risks to our call include higher patient participation in the CoB scheme and low-quality services provided by JKN providers, shifting market share from other private hospitals.

Higher occupancy, int. income and margin expansion driving growth

Due to the dengue fever outbreak in 1Q16, MIKA recorded total patient volume growth of around 7% y-y. This coupled with a higher mix of complex cases and additional 5% price increase since the beginning of the year, helped MIKA book inpatient revenue growth of 19% y-y and outpatient revenue growth of 9% y-y bringing the total sales to IDR625bn, up 15% y-y. Aside from lower cost of branded generic drugs, MIKA’s margin expansion also stemmed from its higher occupancy rate to 73% from 66% in 1Q15 and 58% in 2015. Meanwhile, MIKA was able to reduce its quarterly opex by 6% leading to a jump in operating profit (43.5% q-q) and net profit (44.3% q-q). Bottom line grew 27% y-y supported by higher interest income (66.5% y-y). Stripping out the interest income, net profit growth fell to 18% y-y. In 2Q, we expect MIKA’s profit growth to be lower than 1Q as the fever outbreak has slowed down from April.

Delay in expansion plan likely to put pressure on patient volumes MIKA recently experienced delay in its hospital expansion this year after having some hiccups in securing construction permit from the local government in Bintaro area. Although this has temporarily allayed a margin drop concern from a new hospital opening, MIKA will face challenges in maintaining its patient volume growth (exhibit 9) relative to its closest competitor, SILO, which has been more aggressive in its expansion strategy with 2 new hospitals already having opened ytd. We believe that the window of opportunity for MIKA to capture future growth is narrowing especially from outside Java, as its portfolio are very concentrated in two big cities only, Greater Jakarta and Surabaya.

Exhibit 1. Company information Market cap (IDRtn/USDbn) : 40.7/3.1 3M avg.daily t.o.(IDRbn/USDmn) : 22.5/1.7 Bloomberg code : MIKA IJ Source: Bloomberg

Exhibit 2. Shareholders information Lion Investments Partner (%) : 49.7 Griyainsani Cakrasadaya (%) : 32.3 Est. free float (%) : 18.0 Source: Bloomberg

Exhibit 3. Key forecasts and valuations 2014 2015 2016F 2017F Sales (IDRbn) 1,946 2,141 2,468 2,947 EBIT (IDRbn) 548 600 706 852 Net profit (IDRbn) 519 567 689 807 Bahana/Cons. - - 102 103 EPS (IDR) 37 40 47 55 EPS growth (%) 28.4 8.9 15.7 17.2 EV/EBITDA (x) 61.1 53.4 48.2 40.4 P/E (x) 75.6 69.4 60.0 51.2 FCFPS (IDR) 31 34 35 39 FCF yield (%) 1.1 1.2 1.3 1.4 BVPS (IDR) 124 229 234 250 PBV (x)

22.7 12.2 12.0 11.2 DPS (IDR) 34 21 33 39 Yield (%) 1.2 0.7 1.2 1.4 ROAA (%) 24.0 19.3 17.9 19.4 ROAE (%) 30.9 23.1 20.9 22.9 EBIT margin 28.2 28.0 28.6 28.9 Net gearing (%) nc nc nc nc Source: Bloomberg, Bahana estimates Note: Pricing as of close on 29 June 2016

Exhibit 4. Relative share price performance

7.1

14.2 11.6

7.1

(25.5)

12.5

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

(30)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

ytd 1M 3M 6M 9M 12M

(%) (%)

MIKA IJ relative to JCI Source: Bloomberg, Bahana

Asia Pacific Daily | 14

Important disclosures, including any required research certifications, are provided on the last three pages of this report.

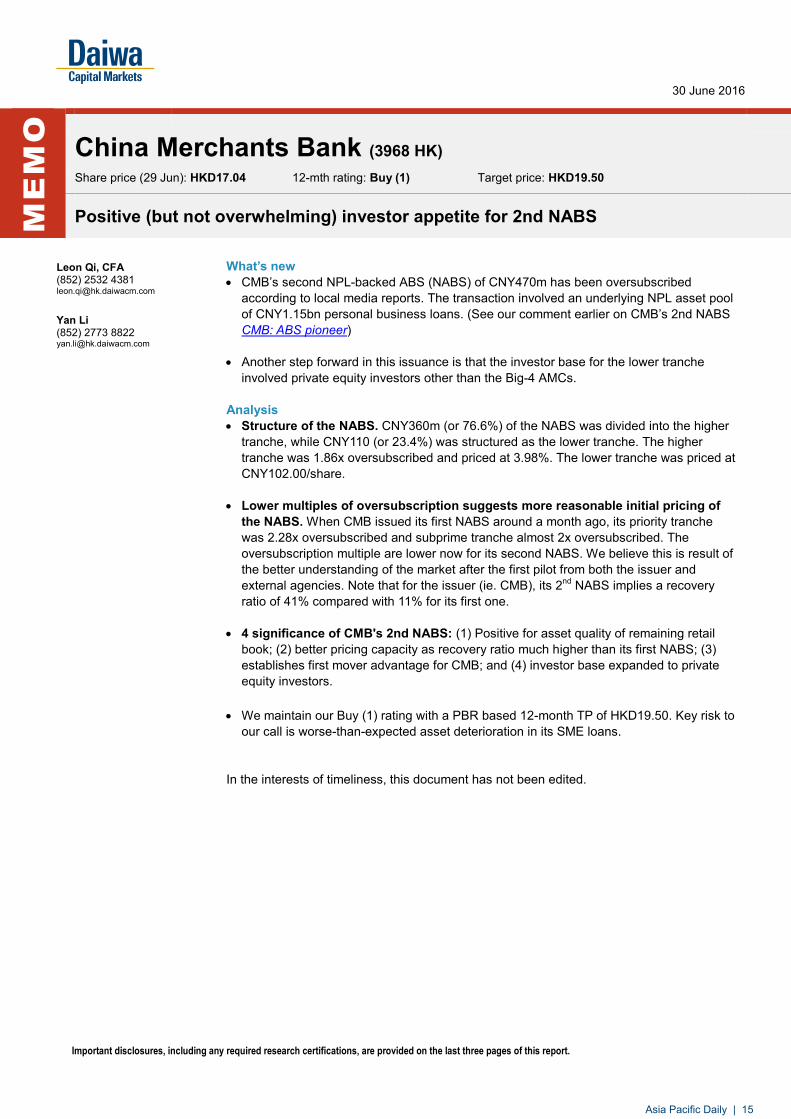

What’s new CMB’s second NPL-backed ABS (NABS) of CNY470m has been oversubscribed

according to local media reports. The transaction involved an underlying NPL asset pool of CNY1.15bn personal business loans. (See our comment earlier on CMB’s 2nd NABS CMB: ABS pioneer)

Another step forward in this issuance is that the investor base for the lower tranche

involved private equity investors other than the Big-4 AMCs. Analysis Structure of the NABS. CNY360m (or 76.6%) of the NABS was divided into the higher

tranche, while CNY110 (or 23.4%) was structured as the lower tranche. The higher tranche was 1.86x oversubscribed and priced at 3.98%. The lower tranche was priced at CNY102.00/share.

Lower multiples of oversubscription suggests more reasonable initial pricing of

the NABS. When CMB issued its first NABS around a month ago, its priority tranche was 2.28x oversubscribed and subprime tranche almost 2x oversubscribed. The oversubscription multiple are lower now for its second NABS. We believe this is result of the better understanding of the market after the first pilot from both the issuer and external agencies. Note that for the issuer (ie. CMB), its 2nd NABS implies a recovery ratio of 41% compared with 11% for its first one.

4 significance of CMB's 2nd NABS: (1) Positive for asset quality of remaining retail

book; (2) better pricing capacity as recovery ratio much higher than its first NABS; (3) establishes first mover advantage for CMB; and (4) investor base expanded to private equity investors.

We maintain our Buy (1) rating with a PBR based 12-month TP of HKD19.50. Key risk to

our call is worse-than-expected asset deterioration in its SME loans. In the interests of timeliness, this document has not been edited.

x

Country

30 June 2016

ME

MO

China Merchants Bank (3968 HK)

Share price (29 Jun): HKD17.04 12-mth rating: Buy (1) Target price: HKD19.50

Positive (but not overwhelming) investor appetite for 2nd NABS

Leon Qi, CFA (852) 2532 4381 [email protected]

Yan Li (852) 2773 8822 [email protected]

Asia Pacific Daily | 15

Important disclosures, including any required research certifications, are provided on the last three pages of this report.

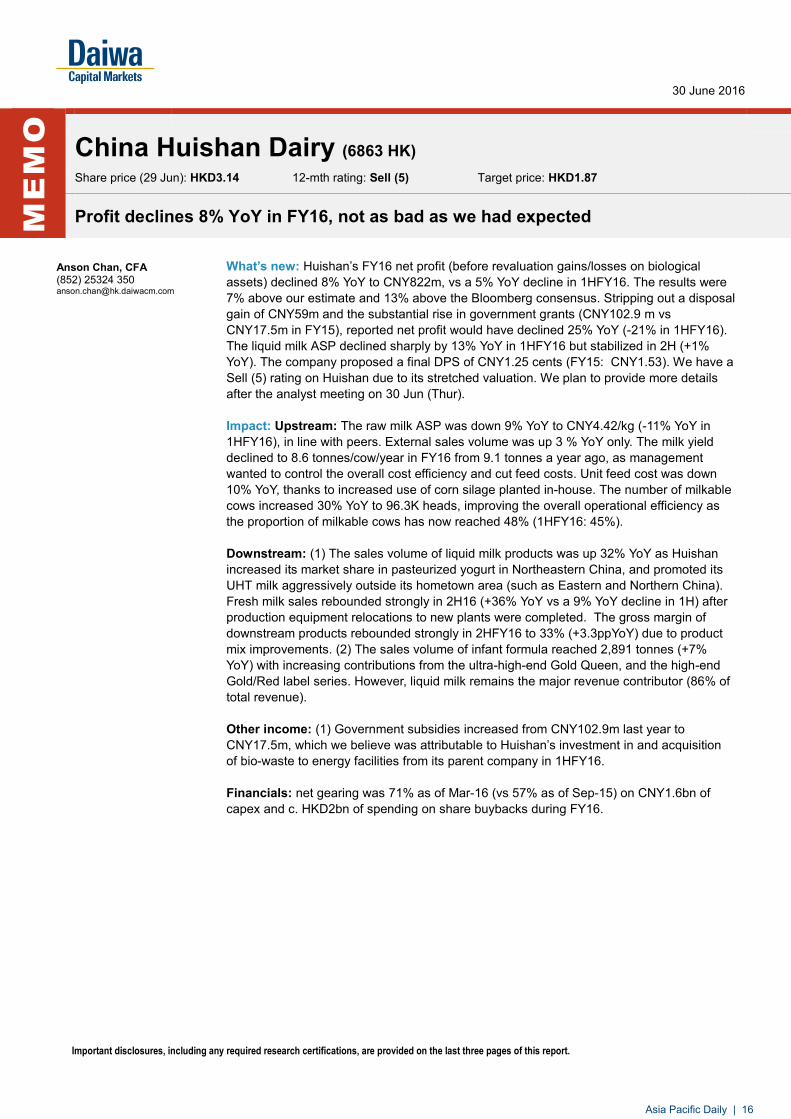

What’s new: Huishan’s FY16 net profit (before revaluation gains/losses on biological assets) declined 8% YoY to CNY822m, vs a 5% YoY decline in 1HFY16. The results were 7% above our estimate and 13% above the Bloomberg consensus. Stripping out a disposal gain of CNY59m and the substantial rise in government grants (CNY102.9 m vs CNY17.5m in FY15), reported net profit would have declined 25% YoY (-21% in 1HFY16). The liquid milk ASP declined sharply by 13% YoY in 1HFY16 but stabilized in 2H (+1% YoY). The company proposed a final DPS of CNY1.25 cents (FY15: CNY1.53). We have a Sell (5) rating on Huishan due to its stretched valuation. We plan to provide more details after the analyst meeting on 30 Jun (Thur). Impact: Upstream: The raw milk ASP was down 9% YoY to CNY4.42/kg (-11% YoY in 1HFY16), in line with peers. External sales volume was up 3 % YoY only. The milk yield declined to 8.6 tonnes/cow/year in FY16 from 9.1 tonnes a year ago, as management wanted to control the overall cost efficiency and cut feed costs. Unit feed cost was down 10% YoY, thanks to increased use of corn silage planted in-house. The number of milkable cows increased 30% YoY to 96.3K heads, improving the overall operational efficiency as the proportion of milkable cows has now reached 48% (1HFY16: 45%). Downstream: (1) The sales volume of liquid milk products was up 32% YoY as Huishan increased its market share in pasteurized yogurt in Northeastern China, and promoted its UHT milk aggressively outside its hometown area (such as Eastern and Northern China). Fresh milk sales rebounded strongly in 2H16 (+36% YoY vs a 9% YoY decline in 1H) after production equipment relocations to new plants were completed. The gross margin of downstream products rebounded strongly in 2HFY16 to 33% (+3.3ppYoY) due to product mix improvements. (2) The sales volume of infant formula reached 2,891 tonnes (+7% YoY) with increasing contributions from the ultra-high-end Gold Queen, and the high-end Gold/Red label series. However, liquid milk remains the major revenue contributor (86% of total revenue). Other income: (1) Government subsidies increased from CNY102.9m last year to CNY17.5m, which we believe was attributable to Huishan’s investment in and acquisition of bio-waste to energy facilities from its parent company in 1HFY16. Financials: net gearing was 71% as of Mar-16 (vs 57% as of Sep-15) on CNY1.6bn of capex and c. HKD2bn of spending on share buybacks during FY16.

x

Country

30 June 2016

ME

MO

China Huishan Dairy (6863 HK)

Share price (29 Jun): HKD3.14 12-mth rating: Sell (5) Target price: HKD1.87

Profit declines 8% YoY in FY16, not as bad as we had expected

Anson Chan, CFA (852) 25324 350 [email protected]

Asia Pacific Daily | 16

China Huishan Dairy (6863 HK)

30 June 2016

2

Results at a glance

CNY m (12 months ended 31-Mar) FY16 FY15 (restated) YoY % Our est. Dev (%) 1HFY16 1HFY15 YoY % 2HFY16 2HFY15 YoY %

Sales of raw milk 947.2 1,028.3 -8 1,006.3 -6 503 554 -9 444 474 -6

Sales of processed products 3,579.3 2,895.0 24 3,463.5 3 1,634 1,441 13 1,945 1,454 34

Revenue 4,527 3,923 15 4,470 1 2,137 1,995 7 2,389 1,929 24

Gross profit 2,533 2,261 12 2,572 -2 1,145 1,138 1 1,388 1,123 24

Other income 182 34 434 202 -10 142 21 583 40 13 202

Selling expense -697 -595 17 -670 4 -330 -302 9 -367 -293 25

Administrative cost -435 -418 4 -408 7 -193 -186 4 -242 -233 4

Operating profit 1,583 1,281 24 1,314 20 1,135 977 16 449 304 47

Finance costs -682 -323 111 -623 9 -351 -156 125 -331 -167 98

Profit-before tax 856 958 -11 814 5 768 821 -6 88 137 -36

Tax -34 -60 -43 -46 -26 -16 -32 -50 -18 -28 -37

Reported net profit 822 898 -8 768 7 754 789 -5 69 109 -37

Net profit (ex-valuation gain) 660 868 -24 827 -20 383 484 -21 276 384 -28

Reported EPS (CNY) 0.060 0.062 -4 0.061 -2 0.054 0.055 -2 0.006 0.008 -14

(%) FY16 FY15 +/-pp Our est. +/-pp 1HFY16 1HFY15 +/-pp 2HFY16E 2HFY15 +/-pp

Gross margin 56.0 57.6 -1.7 57.5 -1.6 53.6 57.1 -3.5 58.1 58.2 -0.1

Net margin 18.2 22.9 -4.7 17.2 1.0 35.3 39.6 -4.3 2.9 5.7 -2.8

FY16 FY15 YoY % Our est. Dev (%) 1HFY16 1HFY15 YoY % 2HFY16E 2HFY15 YoY %

Sales volume (000 tonnes) 700,836 577,071 21 742,574 -6 356,200 279,453 27 344,636 297,618 16

Processed products 482,900 365,302 32 513,864 -6 242,500 168,559 44 240,400 196,743 22

Raw milk 217,936 211,769 3 228,711 -5 113,700 110,894 3 104,236 100,875 3

ASP of raw milk(CNY/kg) 4.42 4.87 -9 4.40 0 4.48 5.03 -11 4.26 4.70 -9

ASP of liquid milk (CNY/kg) 7.77 8.26 -6 7.41 5 7.39 8.50 -13 8.10 8.04 1

Milk yield (Tonne/year) 8.60 9.10 n.a. 8.52 1 8.70 9.10 n.a. n.a. n.a. n.a.

Unit feed cost (CNY/tonne) 1,413 1,573 -10 1,612 -12 1,570 1,648 -5 1,225 1,569 -22

No. of cows 200,892 180,331 11 194,920 3 190,911 162,394 18

No. of milkable cows 96,339 74,389 30 113,070 -15 86,801 65,312 33

Source: Company

Valuation and recommendation: We have a Sell (5) rating on the stock due to its stretched valuation (34x FY17E PER). Our SOTP-based 12-month TP of HKD1.87 includes (1) HKD1.70 (DCF-based) for the upstream business, and (2) HKD0.17 for the downstream business (12x FY16E PER). The key risk to our call: a strong rebound in milk prices. In the interests of timeliness, this document has not been edited.

Asia Pacific Daily | 17

Click for our latest editions

Korea Automobiles and

Components Sector

Korea Automobiles and Components Sector: Electric vehicles and smart cars: reinventing the wheel 23 June 2016

Apple and Tesla’s aggressive moves towards EVs and smart cars herald a new era and should give parts makers’ shares a leg up

We revise up our EV and smart-car forecasts on more stringent regulations, government support and falling component prices

Mando and Hanon (both Buys [1]) are our top picks; we also like HMC (Buy [1]) on a 6-month view

Sung Yop Chung (82) 2 787 9157 ([email protected])

Hong Kong Property Sector

Hong Kong Property Sector: It’s time to be more greedy than fearful 25 May 2016

Challenges abound, but we think the Hong Kong property market is more mature and sophisticated than many observers realise

Corporate fundamentals are stronger than industry fundamentals – a distinction that we think deserves more recognition

Significant investment value could be unlocked if family-owned property companies continue to modernise; reiterating Positive stance

Jonas Kan, CFA (852) 2848 4439 ([email protected])

Singapore Strategy

Singapore Strategy: Navigating choppy markets 8 April 2016

We identify optical communications as a key beneficiary of the rising Big Data/IoT cycle

We flag 2 demand drivers: 1) the continued expansion of global FTTX coverage, and 2) bandwidth upgrades at global datacentres

Food chain value proposition centres on epiwafer-growing — LandMark Opto (Buy [1]); WinSemi (Buy [1]) should also benefit

Ramakrishna Maruvada (65) 6499 6543 ([email protected]) Shane Goh (65) 6499 6546 ([email protected])

Taiwan Industrial PC

Sector

Taiwan Industrial PC Sector: Initiation: now they’re talking 23 March 2016

We highlight the Industrial PC sector as a major beneficiary of the ongoing rise of the Internet of Things (IoT)

The Industrial IoT megatrend, government-led efforts to modernize industrial bases, and M&A should be the key catalysts for the sector

We favour Ennoconn for its strong earnings and Advantech for its industry leadership; concerns over IA demand and opex for Adlink

Steven Tseng (886) 2 8758 6252 ([email protected]) Jack Lin (886) 2 8758 6253 ([email protected])

Daiwa research is available electronically on Bloomberg, Reuters, Thomson One Analytics, FactSet, Capital IQ and Daiwa’s L-ZONE. Please contact your Daiwa sales representative for more information.

Daiwa’s Banner Products

Asia Pacific Daily | 18

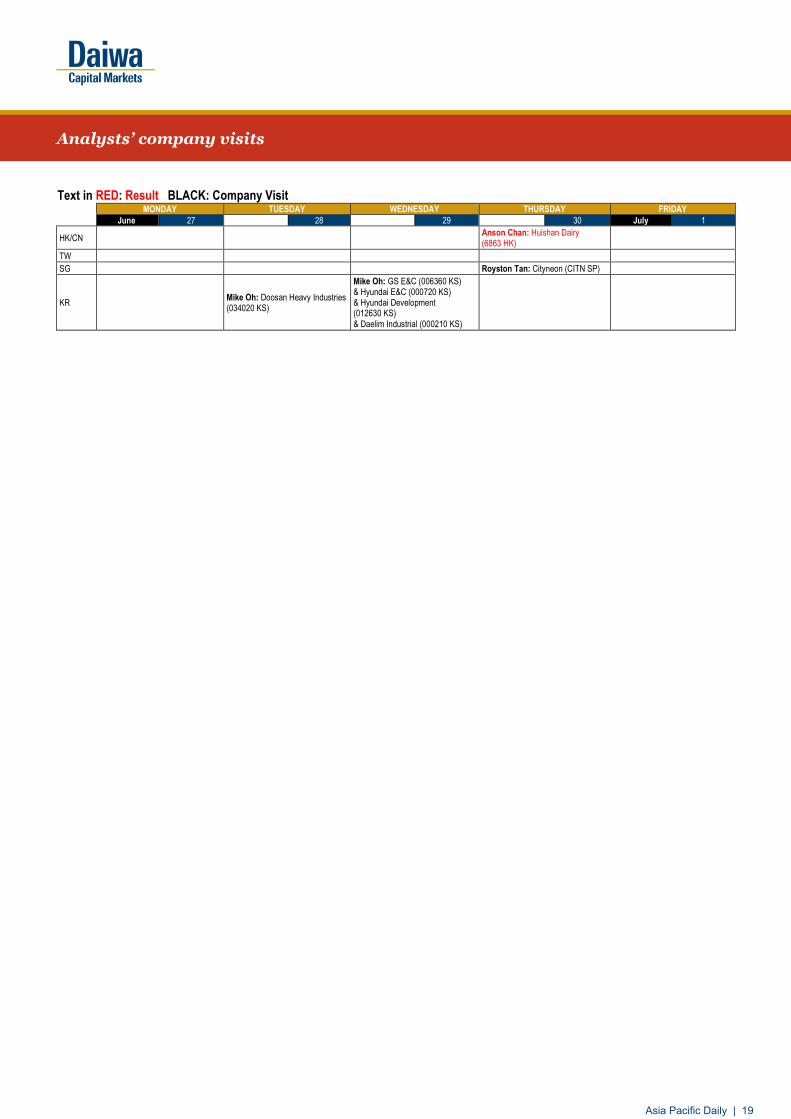

Text in RED: Result BLACK: Company Visit

MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY

June 27 28 29 30 July 1

HK/CN Anson Chan: Huishan Dairy (6863 HK)

TW

SG Royston Tan: Cityneon (CITN SP)

KR Mike Oh: Doosan Heavy Industries (034020 KS)

Mike Oh: GS E&C (006360 KS) & Hyundai E&C (000720 KS) & Hyundai Development (012630 KS) & Daelim Industrial (000210 KS)

Analysts’ company visits

Asia Pacific Daily | 19

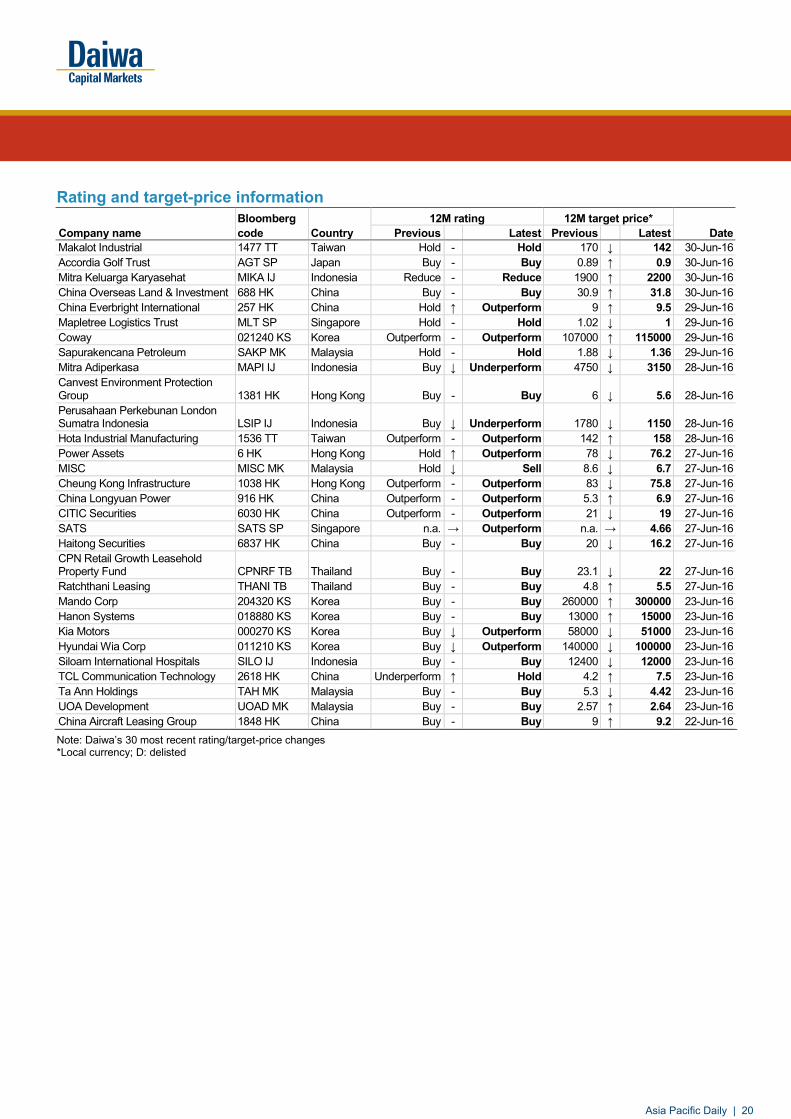

Rating and target-price information

Bloomberg 12M rating 12M target price* Company name code Country Previous Latest Previous Latest Date Makalot Industrial 1477 TT Taiwan Hold - Hold 170 ↓ 142 30-Jun-16 Accordia Golf Trust AGT SP Japan Buy - Buy 0.89 ↑ 0.9 30-Jun-16 Mitra Keluarga Karyasehat MIKA IJ Indonesia Reduce - Reduce 1900 ↑ 2200 30-Jun-16 China Overseas Land & Investment 688 HK China Buy - Buy 30.9 ↑ 31.8 30-Jun-16 China Everbright International 257 HK China Hold ↑ Outperform 9 ↑ 9.5 29-Jun-16 Mapletree Logistics Trust MLT SP Singapore Hold - Hold 1.02 ↓ 1 29-Jun-16 Coway 021240 KS Korea Outperform - Outperform 107000 ↑ 115000 29-Jun-16 Sapurakencana Petroleum SAKP MK Malaysia Hold - Hold 1.88 ↓ 1.36 29-Jun-16 Mitra Adiperkasa MAPI IJ Indonesia Buy ↓ Underperform 4750 ↓ 3150 28-Jun-16 Canvest Environment Protection Group 1381 HK Hong Kong Buy - Buy 6 ↓ 5.6 28-Jun-16 Perusahaan Perkebunan London Sumatra Indonesia LSIP IJ Indonesia Buy ↓ Underperform 1780 ↓ 1150 28-Jun-16 Hota Industrial Manufacturing 1536 TT Taiwan Outperform - Outperform 142 ↑ 158 28-Jun-16 Power Assets 6 HK Hong Kong Hold ↑ Outperform 78 ↓ 76.2 27-Jun-16 MISC MISC MK Malaysia Hold ↓ Sell 8.6 ↓ 6.7 27-Jun-16 Cheung Kong Infrastructure 1038 HK Hong Kong Outperform - Outperform 83 ↓ 75.8 27-Jun-16 China Longyuan Power 916 HK China Outperform - Outperform 5.3 ↑ 6.9 27-Jun-16 CITIC Securities 6030 HK China Outperform - Outperform 21 ↓ 19 27-Jun-16 SATS SATS SP Singapore n.a. → Outperform n.a. → 4.66 27-Jun-16 Haitong Securities 6837 HK China Buy - Buy 20 ↓ 16.2 27-Jun-16 CPN Retail Growth Leasehold Property Fund CPNRF TB Thailand Buy - Buy 23.1 ↓ 22 27-Jun-16 Ratchthani Leasing THANI TB Thailand Buy - Buy 4.8 ↑ 5.5 27-Jun-16 Mando Corp 204320 KS Korea Buy - Buy 260000 ↑ 300000 23-Jun-16 Hanon Systems 018880 KS Korea Buy - Buy 13000 ↑ 15000 23-Jun-16 Kia Motors 000270 KS Korea Buy ↓ Outperform 58000 ↓ 51000 23-Jun-16 Hyundai Wia Corp 011210 KS Korea Buy ↓ Outperform 140000 ↓ 100000 23-Jun-16 Siloam International Hospitals SILO IJ Indonesia Buy - Buy 12400 ↓ 12000 23-Jun-16 TCL Communication Technology 2618 HK China Underperform ↑ Hold 4.2 ↑ 7.5 23-Jun-16 Ta Ann Holdings TAH MK Malaysia Buy - Buy 5.3 ↓ 4.42 23-Jun-16 UOA Development UOAD MK Malaysia Buy - Buy 2.57 ↑ 2.64 23-Jun-16 China Aircraft Leasing Group 1848 HK China Buy - Buy 9 ↑ 9.2 22-Jun-16 Note: Daiwa’s 30 most recent rating/target-price changes *Local currency; D: delisted

Asia Pacific Daily | 20

Recently published reports

Research reports* Subtitle No. of pages

Date of publication

China Everbright International Upgrading: refocusing on its waste-to-energy identity 17 28-Jun-16 China Longyuan Power Utilisation more protected, upside for both EPS & PER 20 27-Jun-16 SATS Multi-pronged growth catalysts 52 27-Jun-16 Singapore Strategy Brexit: surveying the damage 11 24-Jun-16 Samsung Electronics 2Q16E results preview and Investor Forum feedback 21 24-Jun-16 Supalai Public Co Ltd Leading by presales 16 24-Jun-16 Discovery Asia small-cap weekly 20 24-Jun-16 NetEase Initiation: raising its game 45 24-Jun-16 China Autos – PV Weekly Monitor 1-17 June: moderate sales growth 10 23-Jun-16 Korea Automobiles and Components Sector Electric vehicles and smart cars: reinventing the wheel 136 23-Jun-16 Bangkok Airways Pcl Not just a typical airline 20 23-Jun-16 Frasers Centrepoint Initiation: awaiting fruition of capital recycling pipeline 38 22-Jun-16 Frasers Commercial Trust Initiation: a value proposition 25 21-Jun-16 Alibaba Group Investor Day wrap: pedal to the metal 21 20-Jun-16 Discovery Asia small-cap weekly 17 17-Jun-16 Humedix Initiation: attractive play on ageing Asia 22 17-Jun-16 ASEAN Intelligence What matters this week 35 17-Jun-16 Karmarts Pcl Weak growth foundations 16 15-Jun-16 Tesco Lotus Retail Growth. Just a yield story 19 15-Jun-16 Taiwan Financials Sector Still a tough road ahead 32 14-Jun-16 Lifestyle Spin-off to unlock asset value 13 10-Jun-16 PTT Exp. & Production SELL into sentiment rally 13 10-Jun-16 Discovery Asia small-cap weekly 18 10-Jun-16 ASEAN Intelligence What matters this week 35 10-Jun-16 Gunkul Engineering Pcl More potential capacity 12 9-Jun-16 China Autos – PV Weekly Monitor 1-31 May: YoY sales growth fuelled by low base 10 7-Jun-16 Macau Gaming Sector Downgrading: 2H16 looks bleak 52 3-Jun-16 Discovery Asia small-cap weekly 18 3-Jun-16 Glow Energy Pcl SPP replacement benefits 13 3-Jun-16 Global Technology Sector Mid-cycle correction offers re-entry opportunities 29 3-Jun-16 ASEAN Intelligence What matters this week 123 3-Jun-16 Malaysia Strategy Battling perceptions 90 2-Jun-16 Hanwha Techwin Initiation: an empowered consolidator 24 2-Jun-16 COSCO Pacific Downgrading: lack of rebound momentum 14 2-Jun-16

*The 30 most recent reports published by Daiwa

Asia Pacific Markets Closed

Hong Kong China SG Malaysia Korea Taiwan Australia New

Zealand India Thailand Philippines Indonesia

Jun 16 9 9, 10 22 6 9, 10 13 6

Asia Pacific Daily | 21

Daiwa’s Asia Pacific Research Directory HONG KONG Takashi FUJIKURA (852) 2848 4051 [email protected] Regional Research Head John HETHERINGTON (852) 2773 8787 [email protected] Regional Deputy Head of Asia Pacific Research Rohan DALZIELL (852) 2848 4938 [email protected] Regional Head of Asia Pacific Product Management Kevin LAI (852) 2848 4926 [email protected] Chief Economist for Asia ex-Japan; Macro Economics (Regional) Jonas KAN (852) 2848 4439 [email protected] Head of Hong Kong and China Property Cynthia CHAN (852) 2773 8243 [email protected] Property (China) Leon QI (852) 2532 4381 [email protected] Banking (Hong Kong/China); Broker (China); Insurance (China) Anson CHAN (852) 2532 4350 [email protected] Consumer (Hong Kong/China) Adrian CHAN (852) 2848 4427 [email protected] Consumer (Hong Kong/China) Jamie SOO (852) 2773 8529 [email protected] Gaming and Leisure (Hong Kong/China) Dennis IP (852) 2848 4068 [email protected] Power; Utilities; Renewables and Environment (Hong Kong/China) John CHOI (852) 2773 8730 [email protected] Head of Hong Kong and China Internet; Regional Head of Small/Mid Cap Kelvin LAU (852) 2848 4467 [email protected] Head of Automobiles; Transportation and Industrial (Hong Kong/China) Brian LAM (852) 2532 4341 [email protected] Transportation – Railway; Construction and Engineering (China) Thomas HO (852) 2773 8716 [email protected] Custom Products Group PHILIPPINES Patricia Tamase (63) 2 797 3024 [email protected] Banking

SOUTH KOREA Sung Yop CHUNG (82) 2 787 9157 [email protected] Pan-Asia Co-head/Regional Head of Automobiles and Components; Automobiles; Shipbuilding; Steel Mike OH (82) 2 787 9179 [email protected] Banking; Capital Goods (Construction and Machinery) Iris PARK (82) 2 787 9165 [email protected] Consumer/Retail SK KIM (82) 2 787 9173 [email protected] IT/Electronics – Semiconductor/Display and Tech Hardware Thomas Y KWON (82) 2 787 9181 [email protected] Pan-Asia Head of Internet & Telecommunications; Software – Internet/On-line Game Kevin JIN (82) 2 787 9168 [email protected] Small/Mid Cap TAIWAN

Rick HSU (886) 2 8758 6261 [email protected] Head of Regional Technology; Head of Taiwan Research; Semiconductor/IC Design (Regional) Christie CHIEN (886) 2 8758 6257 [email protected] Banking; Insurance (Taiwan); Macro Economics (Regional) Steven TSENG (886) 2 8758 6252 [email protected] IT/Technology Hardware (PC Hardware) Christine WANG (886) 2 8758 6249 [email protected] IT/Technology Hardware (Automation); Pharmaceuticals and Healthcare; Consumer Kylie HUANG (886) 2 8758 6248 [email protected] IT/Technology Hardware (Handsets and Components) Helen CHIEN (886) 2 8758 6254 [email protected] Small/Mid Cap INDIA Punit SRIVASTAVA (91) 22 6622 1013 [email protected] Head of India Research; Strategy; Banking/Finance Saurabh MEHTA (91) 22 6622 1009 [email protected] Capital Goods; Utilities SINGAPORE

Ramakrishna MARUVADA (65) 6499 6543 [email protected] Head of Singapore Research; Telecommunications (China/ASEAN/India) Royston TAN (65) 6321 3086 [email protected] Oil and Gas; Capital Goods David LUM (65) 6329 2102 [email protected] Banking; Property and REITs Shane GOH (65) 64996546 [email protected] Small/Mid Cap (Singapore) Jame OSMAN (65) 6321 3092 [email protected] Telecommunications (ASEAN/India); Pharmaceuticals and Healthcare; Consumer (Singapore)

Asia Pacific Daily | 22

Daiwa’s Offices

Office / Branch / Affiliate Address Tel Fax

DAIWA SECURITIES GROUP INC

HEAD OFFICE Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6753 (81) 3 5555 3111 (81) 3 5555 0661

Daiwa Securities Trust Company One Evertrust Plaza, Jersey City, NJ 07302, U.S.A. (1) 201 333 7300 (1) 201 333 7726

Daiwa Securities Trust and Banking (Europe) PLC (Head Office) 5 King William Street, London EC4N 7JB, United Kingdom (44) 207 320 8000 (44) 207 410 0129

Daiwa Europe Trustees (Ireland) Ltd Level 3, Block 5, Harcourt Centre, Harcourt Road, Dublin 2, Ireland (353) 1 603 9900 (353) 1 478 3469

Daiwa Capital Markets America Inc. New York Head Office Financial Square, 32 Old Slip, New York, NY10005, U.S.A. (1) 212 612 7000 (1) 212 612 7100

Daiwa Capital Markets America Inc. San Francisco Branch 555 California Street, Suite 3360, San Francisco, CA 94104, U.S.A. (1) 415 955 8100 (1) 415 956 1935

Daiwa Capital Markets Europe Limited, London Head Office 5 King William Street, London EC4N 7AX, United Kingdom (44) 20 7597 8000 (44) 20 7597 8600

Daiwa Capital Markets Europe Limited, Frankfurt Branch Neue Mainzer Str. 1, 60311 Frankfurt/Main, Germany (49) 69 717 080 (49) 69 723 340

Daiwa Capital Markets Europe Limited, Paris Representative Office 17, rue de Surène 75008 Paris, France (33) 1 56 262 200 (33) 1 47 550 808

Daiwa Capital Markets Europe Limited, Geneva Branch 50 rue du Rhône, P.O.Box 3198, 1211 Geneva 3, Switzerland (41) 22 818 7400 (41) 22 818 7441

Daiwa Capital Markets Europe Limited, Moscow Representative Office

Midland Plaza 7th Floor, 10 Arbat Street, Moscow 119002, Russian Federation

(7) 495 641 3416 (7) 495 775 6238

Daiwa Capital Markets Europe Limited, Bahrain Branch 7th Floor, The Tower, Bahrain Commercial Complex, P.O. Box 30069, Manama, Bahrain

(973) 17 534 452 (973) 17 535 113

Daiwa Capital Markets Hong Kong Limited Level 28, One Pacific Place, 88 Queensway, Hong Kong (852) 2525 0121 (852) 2845 1621

Daiwa Capital Markets SG Limited 6 Shenton Way #26-08, OUE Downtown 2, SG 068809, Republic of SG

(65) 6220 3666 (65) 6223 6198

Daiwa Capital Markets Australia Limited Level 34, Rialto North Tower, 525 Collins Street, Melbourne, Victoria 3000, Australia

(61) 3 9916 1300 (61) 3 9916 1330

DBP-Daiwa Capital Markets Philippines, Inc 18th Floor, Citibank Tower, 8741 Paseo de Roxas, Salcedo Village, Makati City, Republic of the Philippines

(632) 813 7344 (632) 848 0105

Daiwa-Cathay Capital Markets Co Ltd 14/F, 200, Keelung Road, Sec 1, Taipei, Taiwan, R.O.C. (886) 2 2723 9698 (886) 2 2345 3638

Daiwa Securities Capital Markets Korea Co., Ltd. 20 Fl.& 21Fl. One IFC, 10 Gukjegeumyung-Ro, Yeongdeungpo-gu, Seoul, Korea

(82) 2 787 9100 (82) 2 787 9191

Daiwa Securities Co. Ltd., Beijing Representative Office Room 301/302,Kerry Center,1 Guanghua Road,Chaoyang District, Beijing 100020, People’s Republic of China

(86) 10 6500 6688 (86) 10 6500 3594

Daiwa (Shanghai) Corporate Strategic Advisory Co. Ltd. 44/F, Hang Seng Bank Tower, 1000 Lujiazui Ring Road, Pudong, Shanghai China 200120 , People’s Republic of China

(86) 21 3858 2000 (86) 21 3858 2111

Daiwa Securities Co. Ltd., Bangkok Representative Office 18th Floor, M Thai Tower, All Seasons Place, 87 Wireless Road, Lumpini, Pathumwan, Bangkok 10330, Thailand

(66) 2 252 5650 (66) 2 252 5665

Daiwa Capital Markets India Private Ltd 10th Floor, 3 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra East, Mumbai – 400051, India

(91) 22 6622 1000 (91) 22 6622 1019

Daiwa Securities Co. Ltd., Hanoi Representative Office Suite 405, Pacific Palace Building, 83B, Ly Thuong Kiet Street, Hoan Kiem Dist. Hanoi, Vietnam

(84) 4 3946 0460 (84) 4 3946 0461

DAIWA INSTITUTE OF RESEARCH LTD

HEAD OFFICE 15-6, Fuyuki, Koto-ku, Tokyo, 135-8460, Japan (81) 3 5620 5100 (81) 3 5620 5603

MARUNOUCHI OFFICE Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6756 (81) 3 5555 7011 (81) 3 5202 2021

New York Research Center 11th Floor, Financial Square, 32 Old Slip, NY, NY 10005-3504, U.S.A. (1) 212 612 6100 (1) 212 612 8417

London Research Centre 3/F, 5 King William Street, London, EC4N 7AX, United Kingdom (44) 207 597 8000 (44) 207 597 8550

Asia Pacific Daily | 23