Asia and Pacific Economic Outlook - International … and Pacific Economic Outlook Medium-Term...

19

Asia and Pacific Economic Outlook Medium-Term Challenges in the Region: Implications of the “New Mediocre” OAP Economic Issues Seminar Ranil Salgado Assistant Director, Regional Studies Division Asia & Pacific Department, IMF December 5, 2016 Key messages and roadmap 2 •Asia remains the main engine of global growth. •In the medium-term, Asia needs to prepare for the risk of a “new mediocre” in advanced economies. •The global trade slowdown and anti-trade sentiment can hit Asia hard—Asia needs more balanced and inclusive growth. •May need to re-assess projections given developments since October projections.

Transcript of Asia and Pacific Economic Outlook - International … and Pacific Economic Outlook Medium-Term...

Asia and Pacific Economic OutlookMedium-Term Challenges in the Region:

Implications of the “New Mediocre”

OAP Economic Issues Seminar

Ranil SalgadoAssistant Director, Regional Studies Division

Asia & Pacific Department, IMFDecember 5, 2016

Key messages and roadmap

2

•Asia remains the main engine of global growth.

•In the medium-term, Asia needs to prepare for the risk of a “new mediocre” in advanced economies.

•The global trade slowdown and anti-trade sentiment can hit Asia hard—Asia needs more balanced and inclusive growth.

•May need to re-assess projections given developments since October projections.

3

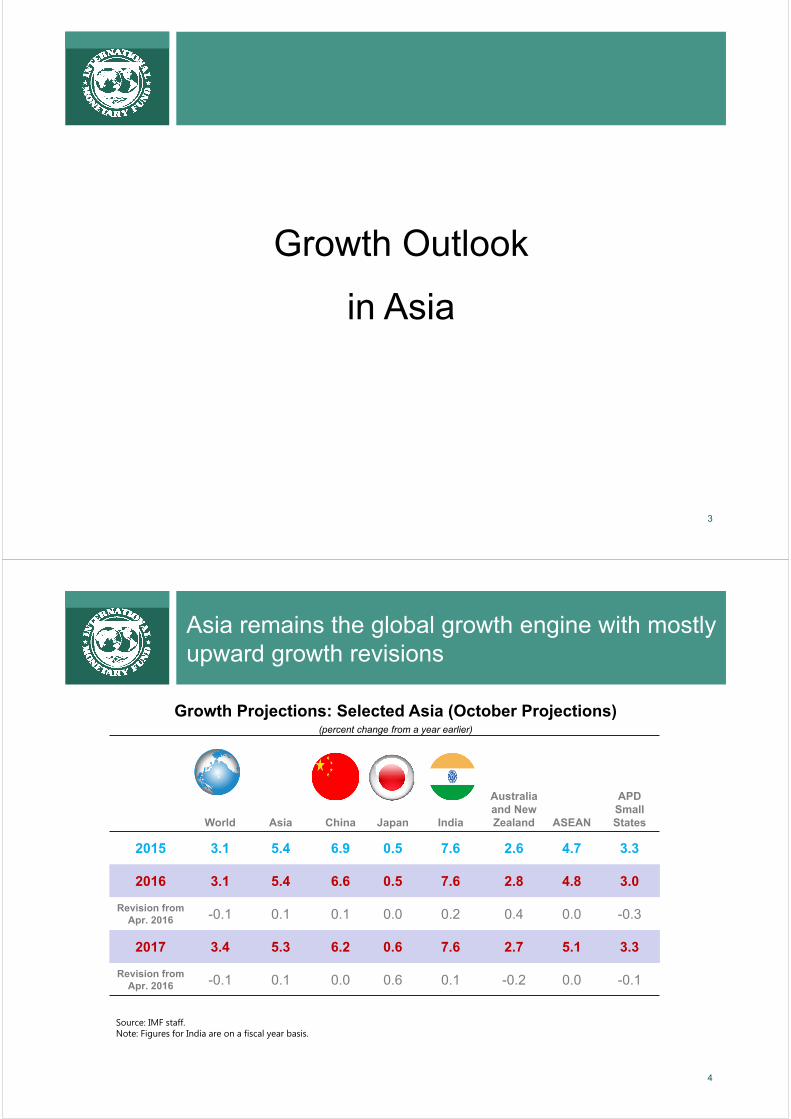

Growth Outlook

in Asia

Asia remains the global growth engine with mostly upward growth revisions

4

Growth Projections: Selected Asia (October Projections)(percent change from a year earlier)

World Asia China Japan India

Australiaand New Zealand ASEAN

APD Small States

2015 3.1 5.4 6.9 0.5 7.6 2.6 4.7 3.3

2016 3.1 5.4 6.6 0.5 7.6 2.8 4.8 3.0

Revision fromApr. 2016 -0.1 0.1 0.1 0.0 0.2 0.4 0.0 -0.3

2017 3.4 5.3 6.2 0.6 7.6 2.7 5.1 3.3

Revision from Apr. 2016 -0.1 0.1 0.0 0.6 0.1 -0.2 0.0 -0.1

Source: IMF staff.Note: Figures for India are on a fiscal year basis.

Asia: Risks to the outlook

5

Near-term:

•Weak global recovery and global trade slowdown

•Sudden tightening of global financial conditions (asynchronous monetary policies in AEs, de-risking)

•China rebalancing, if bumpy

•Natural disasters and geopolitical tensions

Medium-term:

•“New mediocre” in advanced economies

Developments since October Projections: e.g. Upside surprises in Q3 growth, U.S. elections, and India “demonetization”

Asia’s growth has moderated in recent years…

6

2

3

4

5

6

7

8

9

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Outturn 2010 20112012 2013 20142015

Asia: GDP Growth Outturns vs. WEO Projections 1/ (Year-over-year percent change)

Sources: IMF, WEO database; and IMF staff calculations.1/ 5-yr forward projections from October WEO in each year.

2

3

4

5

6

7

8

9

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Outturn 2010 20112012 2013 20142015

World: GDP Growth Outturns vs. WEO Projections 1/ (Year-over-year percent change)

Sources: IMF, WEO database; and IMF staff calculations.1/ 5-yr forward projections from October WEO in each year.

… which may be due to growth convergence, but other factors as well

7

Japan

KoreaIndonesia Malaysia

PhilippinesThailand

ChinaIndia

0

2

4

6

8

10

12

0 10000 20000 30000 40000 50000GDP per capita, PPP

Real GDP per Capita Growth: 2010-2015 (percent)

Sources: IMF, World Economic Outlook database; and IMF staff calculations.Note: Red dots represent major Asian countries, and yellow lines indicate top 10 percentile GDP growth rate within each income group.

Top 10 percentile thresholds

Recent Developments

8

• Upside surprises in Q3 growth• Primarily in U.S. and Japan, but also in parts of

emerging Asia

• U.S. elections• Tighter financial conditions • But too early to assess overall impact

• India “demonetization”

• Other: e.g., Japan and Korea

Market reaction to U.S. presidential elections

-10 -5 0 5 10 15

PhilippinesIndonesiaIndiaMalaysiaSri LankaVietnamKoreaHong Kong SARThailandTaiwan POCNew ZealandMongoliaChinaSingaporeAustraliaJapanMexicoBrazilTurkeyColombiaChileSouth AfricaCzech RepublicHungaryPolandBulgariaRussia

Nov 9 Nov 10 - Dec 1 sum

Selected Asia: Stock Market Index(Percent change; in local currency)

Sources: Bloomberg L.P.; Haver Analytics; and IMF staff calculations.

-12 -9 -6 -3 0 3

JapanMalaysiaAustraliaNew ZealandIndonesiaSingaporeKoreaIndiaThailandPhilippinesMongoliaVietnamChinaTaiwan POCSri LankaHong Kong SAR

MexicoTurkeyPolandHungarySouth AfricaCzech RepublicBulgariaRussiaChile

Nov 9 Nov 10 - Dec 1 sum

Selected Asia: Bilateral FX Rate against USD(Percent change; positive=local currency appreciation)

10

What Does the “New Mediocre”

Mean For Asia?

Asia is diverse but there are three broad groups in relation to the “new mediocre”

11

•Group 1 (Japan): stagnation has been present for more than two decades, well before other advanced economies were hit.

•Group 2 (China, Korea, Singapore, and Thailand): looming rapid aging and demographics pressures; slowdown in productivity growth.

•Group 3 (India and other fast growing economies, such as Indonesia, Malaysia, Vietnam): not at risk of stagnation domestically but can be affected through spillovers.

Signs of the “new mediocre” in Asia?

12

•Long-term interest rates declining?

•Natural (or neutral) interest rates declining?

•Low inflation becoming more common?

•Demographics becoming a headwind?

•Productivity growth declining?

•Trade slowdown in Asia?

Long-term rates have fallen significantly in some cases, but not everywhere

13

-5.0

-4.5

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

Selected Asia: Change in 10-year Government Bond Yields (Percentage points; Sep 2016 compared to 2000-07 average)

-5.0

-4.5

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

Selected Asia: Change in Central Bank Policy Rates (Percentage points; Sep 2016 compared to 2000-07 average)

Sources: Bloomberg; and IMF staff calculations.

Natural interest rates have declined in some cases, but not everywhere

14

Source: Staff estimates based on a TVP-VAR for three variables – real GDP growth, inflation and a measure of real rate. Note: The conditional long horizon forecast (over 5 years) of the observed real rate is used as a measure of neutral rate.

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

US UK Japan Korea Australia Indonesia China Malaysia

Selected Asia: Estimated Natural Real Interest Rates(Percent)

1990-99 2000-07 2016 Q2

Low inflation becoming more common across the region

15

0

20

40

60

80

100

2000

M1

2002

M1

2004

M1

2006

M1

2008

M1

2010

M1

2012

M1

2014

M1

2016

M1

Inflation rate below 2%Inflation rate below 1%Inflation rate below 0%

Asia: Number of Countries by Headline Inflation Rates (Percent of 22 Asian countries)

2016

M6

Sources: CEIC Data Company Ltd.; Haver Analytics; and IMF staff calculations.

0

20

40

60

80

100

2000

M1

2002

M1

2004

M1

2006

M1

2008

M1

2010

M1

2012

M1

2014

M1

2016

M1

Inflation rate below 2%Inflation rate below 1%Inflation rate below 0%

Advanced Economies: Number of Countries by Headline Inflation Rates (Percent of 33 countries)

2016

M6

Sources: IMF, Global Data Source; and IMF staff calculations.

Demographics: A headwind for some, a dividend for others

16

Asia: Potential Growth Impact of Demographics Trends(Percentage point impact on real GDP growth; average over 2020-50)

Asia: Old-Age Dependency Ratios(Percent)

Source: Staff estimates based on UN Population Prospects: 2015 Revision (medium-fertility variant) and IMF (2016). Note: Migration projections follow historical trends. The growth impact estimates are based on the assumptions of unchanged labor force participation by cohort, constant capital-to-labor ratio, and TFP growth unchanged from historical average.

Source: UN Population Prospects: 2015 Revision. Based on the medium-fertility variant scenario (with migration).

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Phili

ppin

es

Indi

a

Indo

nesi

a

Mal

aysi

a

Viet

nam

New

Zea

land

Aust

ralia

Thai

land

Sing

apor

e

Kore

a

Chin

a

Japa

n

Hon

g Ko

ng, S

AR

Without migration

With migration

0

10

20

30

40

50

60

70

80

90

Phili

ppin

esIn

dia

Indo

nesi

aM

alay

sia

WO

RLD

Viet

nam

Aust

ralia

New

Zea

land

Hig

h-in

com

e co

untr

ies

Chin

aTh

aila

ndSi

ngap

ore

Hon

g Ko

ng S

ARKo

rea

Japa

n

2005 2020 2050

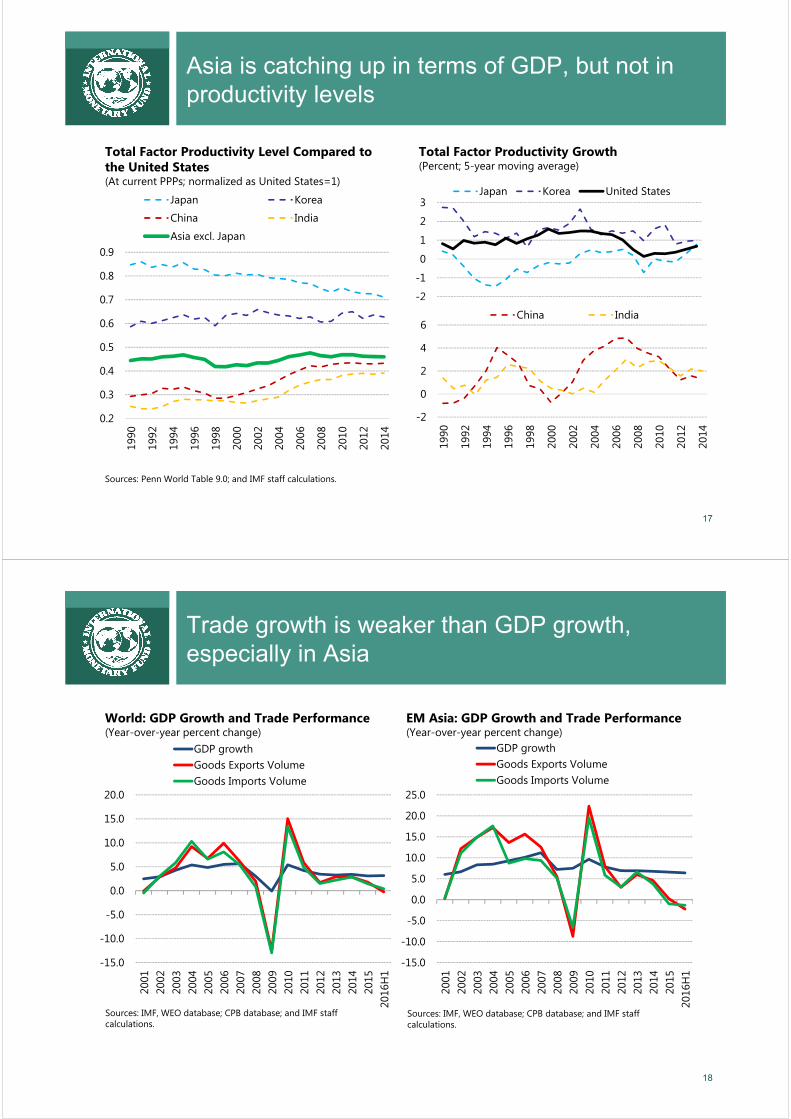

Asia is catching up in terms of GDP, but not in productivity levels

17

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Japan Korea

China India

Asia excl. Japan

Total Factor Productivity Level Compared to the United States(At current PPPs; normalized as United States=1)

Sources: Penn World Table 9.0; and IMF staff calculations.

-2

-1

0

1

2

3

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Japan Korea United States

Total Factor Productivity Growth(Percent; 5-year moving average)

-2

0

2

4

6

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

China India

Trade growth is weaker than GDP growth, especially in Asia

18

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

H1

GDP growthGoods Exports VolumeGoods Imports Volume

World: GDP Growth and Trade Performance(Year-over-year percent change)

Sources: IMF, WEO database; CPB database; and IMF staff calculations.

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

H1

GDP growthGoods Exports VolumeGoods Imports Volume

EM Asia: GDP Growth and Trade Performance(Year-over-year percent change)

Sources: IMF, WEO database; CPB database; and IMF staff calculations.

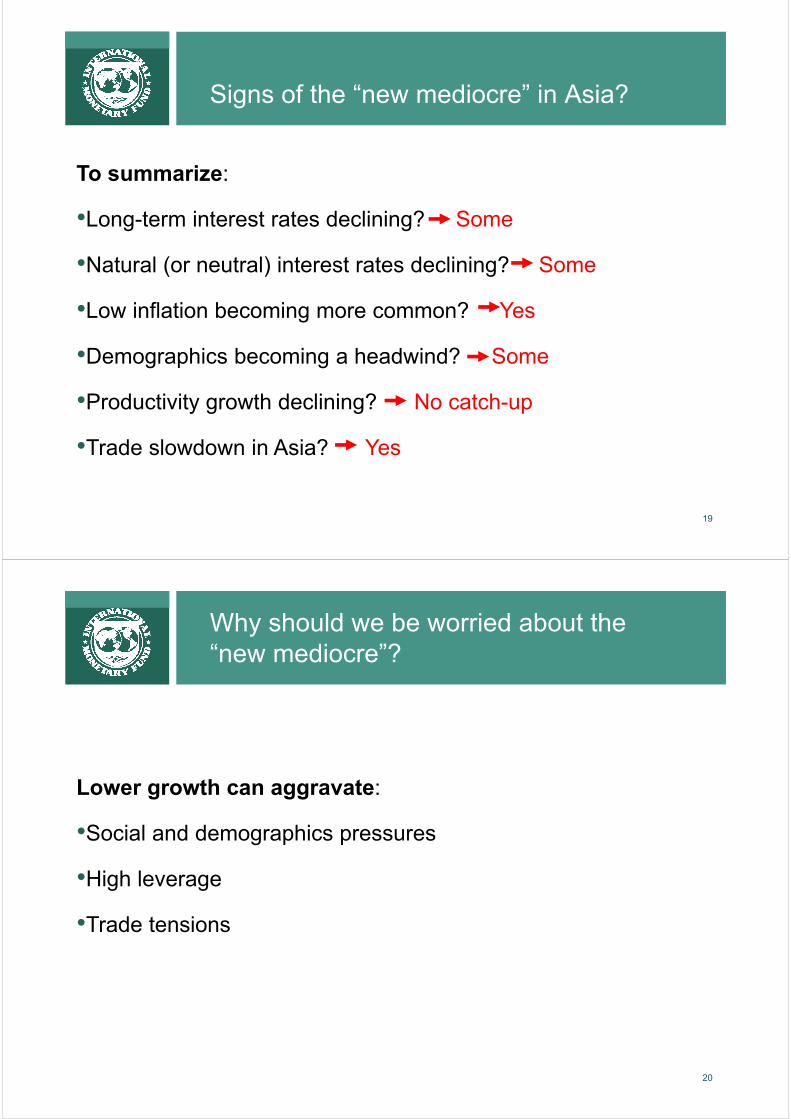

Signs of the “new mediocre” in Asia?

19

To summarize:

•Long-term interest rates declining? Some

•Natural (or neutral) interest rates declining? Some

•Low inflation becoming more common? Yes

•Demographics becoming a headwind? Some

•Productivity growth declining? No catch-up

•Trade slowdown in Asia? Yes

Why should we be worried about the “new mediocre”?

20

Lower growth can aggravate:

•Social and demographics pressures

•High leverage

•Trade tensions

Income inequality in Asia has already risen and social spending in Asia is relatively low

21

-5 0 5 10 15 20

China

India

Emerging and Developing Europe

Industrial Asia

NIEs

LICs Asia

OECD

ASEAN-5

Middle East and North Africa

Latin America and the Caribbean

Sub-Saharan Africa

Change in Income Inequality(Net Gini Index; change from 1990 to 2013; simple average across regions)

Sources: SWIID Version 5.0; IMF, WEO database; and IMF staff calculations.

0

5

10

15

20

25

30

Adva

nced

Eco

nom

ies

Emer

ging

Eur

ope

Latin

Am

eric

a

Mid

dle

East

and

Nor

th A

fric

a

Asia

Sub-

Saha

ran

Afric

a

Social Protection

Health

Education

Composition of Social Spending(Percent of GDP; year of 2010 or latest)

Sources: Organization for Economic Cooperation and Development; Eurostat; Asian Development Bank; IMF, World Economic Outlook; United Nations; World Health Organization; World Bank; and IMF staff calculations.

22

Corporate debt is relatively high in emerging Asia and household debt has risen rapidly in several cases

0

5

10

15

20

25

30

35

China Asia excludingChina

Latin America Europe,Middle East,and Africa

2010 2011 2013 2014 2015E

Emerging Market Firms: Debt-Potentially-at-Risk(Percent; share of total debt if ICR<2)

Source: April 2016 GFSR.Note: Asia excluding China= India, Indonesia, Malaysia, the Philippines, and Thailand.

-20 -10 0 10 20 30

USSpain

PortugalGermany

UKAustria

IndiaJapan

New ZealandNetherlands

ItalyIndonesia

FranceSingapore

BelgiumHong Kong SAR

KoreaAustralia

SwitzerlandCanadaSweden

ChinaNorway

MalaysiaThailand

Change in Household Debt to GDP Ratio (Percentage points; from end-2007 to end-2015)

Sources: BIS and IMF staff estimates.

The global trade slowdown and anti-trade sentiment could hit Asia hard

23

0

1

2

3

4

5

6

Asia

Indu

stria

l Asi

a

NIE

s

ASEA

N-4

Chin

a

Indi

a

1990-99 2000-15 2016-20 (proj.)

Selected Asia: Contribution of Exports to Real GDP Growth (Year-over-year; percentage points)

Sources: IMF, World Economic Outlook database; and IMF staff calculations.Note: ASEAN-4 includes Indonesia, Malaysia, the Philippines, and Thailand. Industrial Asia includes Australia, Japan, and New Zealand. NIEs include: Hong Kong SAR, Korea, Singapore, and Taiwan Province of China.

24

Implications for Monetary,

Fiscal, and Structural Policies

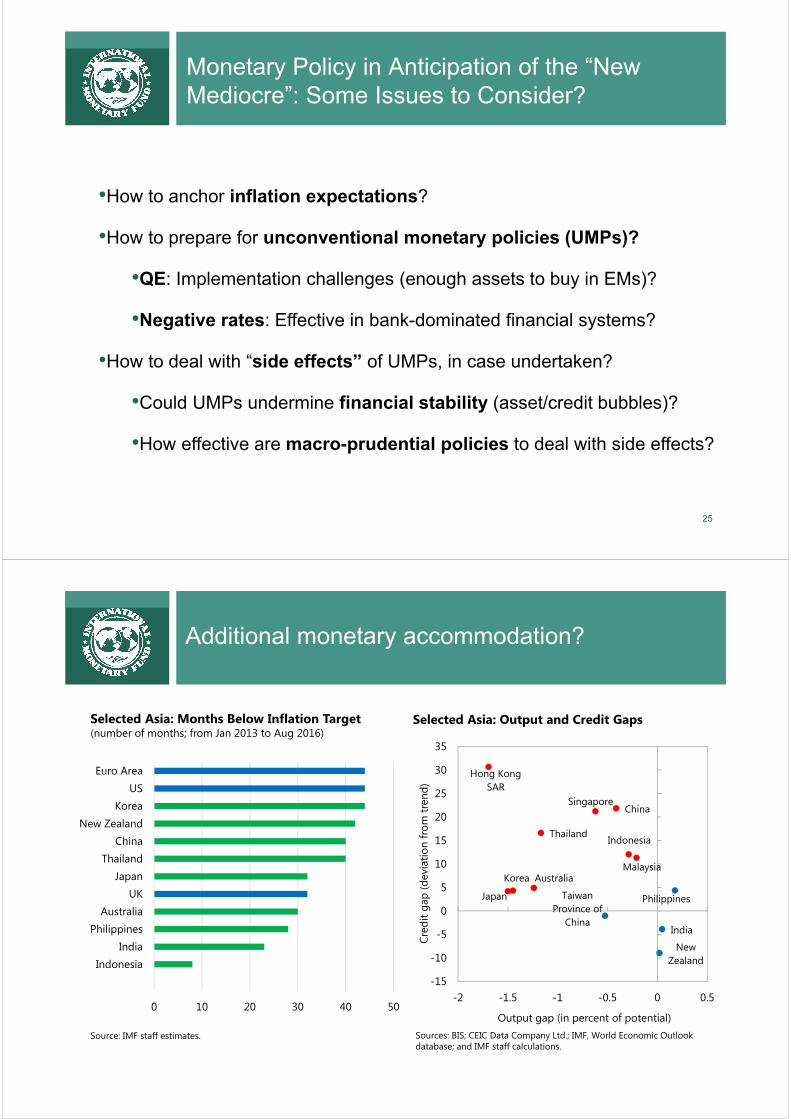

Monetary Policy in Anticipation of the “New Mediocre”: Some Issues to Consider?

25

•How to anchor inflation expectations?

•How to prepare for unconventional monetary policies (UMPs)?

•QE: Implementation challenges (enough assets to buy in EMs)?

•Negative rates: Effective in bank-dominated financial systems?

•How to deal with “side effects” of UMPs, in case undertaken?

•Could UMPs undermine financial stability (asset/credit bubbles)?

•How effective are macro-prudential policies to deal with side effects?

Additional monetary accommodation?

Selected Asia: Months Below Inflation Target(number of months; from Jan 2013 to Aug 2016)

Source: IMF staff estimates.

0 10 20 30 40 50

IndonesiaIndia

PhilippinesAustralia

UKJapan

ThailandChina

New ZealandKorea

USEuro Area

Japan

Australia

New Zealand

Hong Kong SAR

Korea

Singapore

Taiwan Province of

China

Indonesia

Malaysia

Philippines

Thailand

China

India

-15

-10

-5

0

5

10

15

20

25

30

35

-2 -1.5 -1 -0.5 0 0.5

Cred

it ga

p (d

evia

tion

from

tren

d)

Output gap (in percent of potential)Sources: BIS; CEIC Data Company Ltd.; IMF, World Economic Outlook database; and IMF staff calculations.

Selected Asia: Output and Credit Gaps

Fiscal policy for demand support?

27

Japan

Australia New Zealand

Hong Kong SAR

Korea

Singapore

Taiwan POC

Indonesia

Malaysia

Philippines

Thailand

Vietnam

China

India

-5

0

5

10

15

20

25

-2.0 -1.0 0.0 1.0

Curr

ent

Acc

ount

Bal

ance

(p

erce

nt o

f G

DP;

201

6)

Output Gap (percent of GDP; 2016)

Selected Asia: Need for Demand Support

Sources: IMF WEO database; and IMF staff calculations.

AustraliaNew

Zealand

Hong Kong SAR Korea

Indonesia

Malaysia

Philippines

Thailand

Vietnam

China

India

0

50

100

150

200

250

300

0 20 40 60 805-

Year

CD

S Sp

read

s(b

asis

poi

nts;

201

6M1-

M3

aver

age)

General Government Gross Debt (percent of GDP; 2016)

Selected Asia: Fiscal Space

Sources: IMF WEO database; and IMF staff calculations.Note: Japan is not shown due to scale.

Structural reforms to boost productivity growth?

28

•Advanced Asia: Infrastructure investment (Australia); product market reforms (Australia, Japan, and Korea); labor market reforms (Japan, and Korea).

•Emerging Asia: Raising public investment efficiency (India); labor market reforms (India, Indonesia); product market reforms (China, India); resolving corporate debt overhang (China);

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Ger

man

yJa

pan

Uni

ted

Stat

esAu

stra

liaKo

rea

Fran

ceIta

lyN

ew Z

eala

ndSp

ain

Port

ugal

Colo

mbi

aIn

done

sia

Turk

eyRu

ssia

Sout

h Af

rica

Chin

aIn

dia

Advanced economies Emerging economies

Source: OECD. Note: The reform responsiveness indicator reflects the share of policy recommendations from the OECD's "Going for Growth" reports on which the country has taken significant action.

Reforms Responsiveness Indicator(2011-15 average)

29

Country Specific Issues

Main Policy Challenges

30

Policy recommendationsMain Challenge

ChinaTackle the corporate debt problem; reduce reliance on

credit/investment stimulus; guard against financial risksCredit growth

Japan A comprehensive and coordinated policy packageReflation and

fiscal sustainability

IndiaContinue to implement structural reform to boost potential

growth; enhance resilience of corporates/banks

Corporate and banking sector strains

AUS and NZL

Accommodative monetary and fiscal policies, structural

reforms

Adjust to lower commodity prices

ASEAN-5

Continue to build policy buffers and to implement structural

reforms, and use macro prudential policies, as needed

Tighter external environment

Asian FDEs

Strengthen macro policy frameworks furtherMacro vulnerabilities

SmallStates

Build resilience and enhance growth potential

Natural disasters/climate change and withdrawal

of CBRs

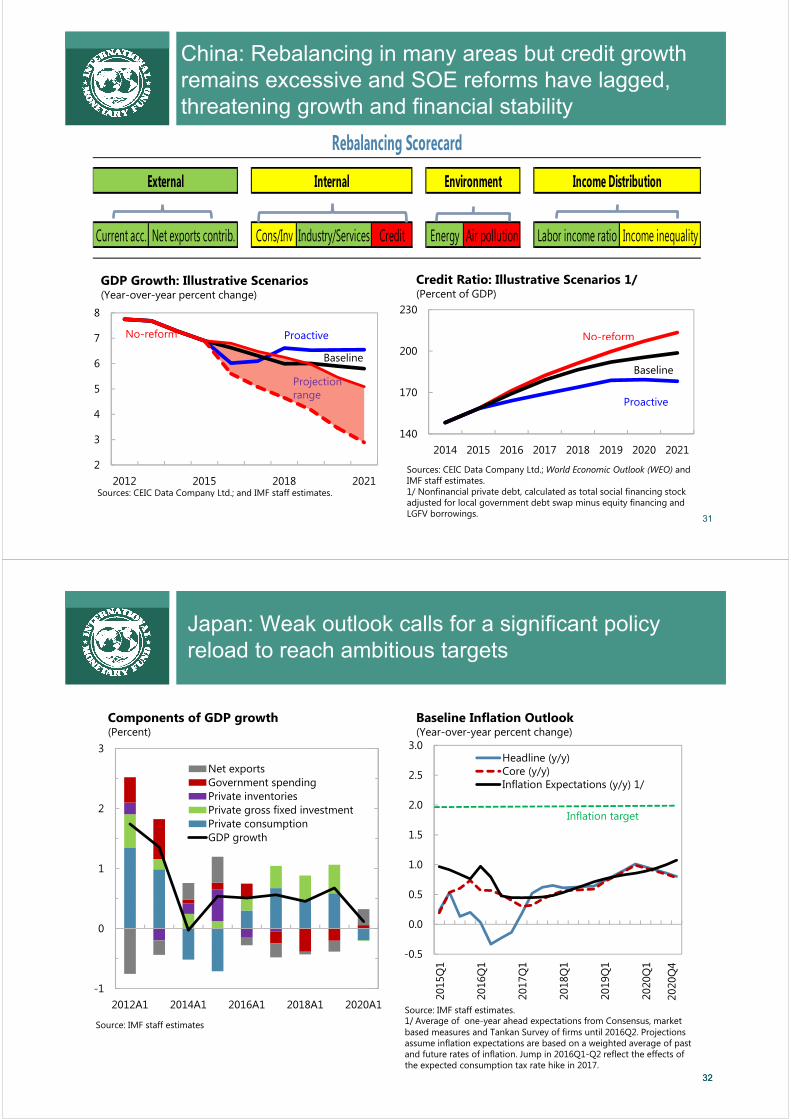

China: Rebalancing in many areas but credit growth remains excessive and SOE reforms have lagged, threatening growth and financial stability

31

Current acc. Net exports contrib. Cons/Inv Industry/Services Credit Energy Air pollution Labor income ratio Income inequality

Rebalancing Scorecard

External Internal Environment Income Distribution

2

3

4

5

6

7

8

2012 2015 2018 2021

GDP Growth: Illustrative Scenarios(Year-over-year percent change)

Sources: CEIC Data Company Ltd.; and IMF staff estimates.

Projection range

ProactiveNo-reform

Baseline

140

170

200

230

2014 2015 2016 2017 2018 2019 2020 2021

Credit Ratio: Illustrative Scenarios 1/(Percent of GDP)

Sources: CEIC Data Company Ltd.; World Economic Outlook (WEO) and IMF staff estimates.1/ Nonfinancial private debt, calculated as total social financing stock adjusted for local government debt swap minus equity financing and LGFV borrowings.

No-reform

Proactive

Baseline

Japan: Weak outlook calls for a significant policy reload to reach ambitious targets

3232

-1

0

1

2

3

2012A1 2014A1 2016A1 2018A1 2020A1

Net exportsGovernment spendingPrivate inventoriesPrivate gross fixed investmentPrivate consumptionGDP growth

Components of GDP growth(Percent)

Source: IMF staff estimates

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2015

Q1

2016

Q1

2017

Q1

2018

Q1

2019

Q1

2020

Q1

Headline (y/y)Core (y/y)Inflation Expectations (y/y) 1/

Baseline Inflation Outlook(Year-over-year percent change)

Source: IMF staff estimates. 1/ Average of one-year ahead expectations from Consensus, market based measures and Tankan Survey of firms until 2016Q2. Projections assume inflation expectations are based on a weighted average of past and future rates of inflation. Jump in 2016Q1-Q2 reflect the effects of the expected consumption tax rate hike in 2017.

2020

Q4

Inflation target

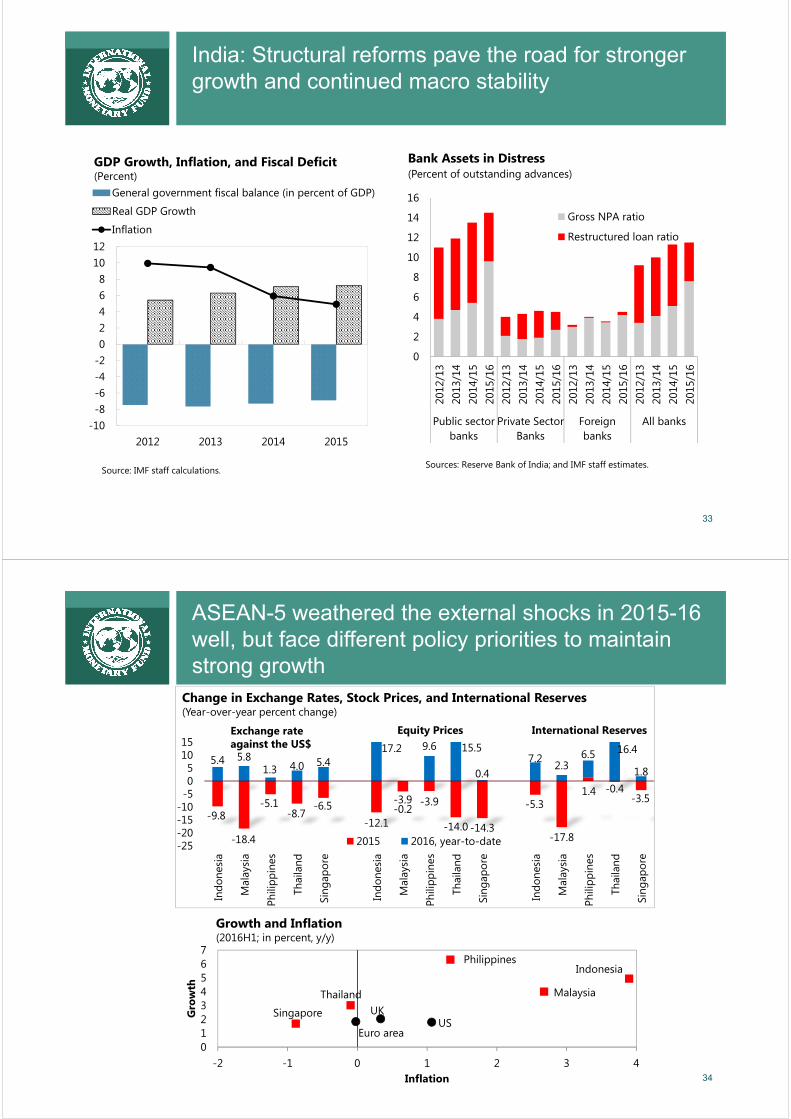

India: Structural reforms pave the road for stronger growth and continued macro stability

33

-10-8-6-4-202468

1012

2012 2013 2014 2015

General government fiscal balance (in percent of GDP)

Real GDP Growth

Inflation

GDP Growth, Inflation, and Fiscal Deficit(Percent)

Source: IMF staff calculations.

0

2

4

6

8

10

12

14

16

2012

/13

2013

/14

2014

/15

2015

/16

2012

/13

2013

/14

2014

/15

2015

/16

2012

/13

2013

/14

2014

/15

2015

/16

2012

/13

2013

/14

2014

/15

2015

/16

Public sectorbanks

Private SectorBanks

Foreignbanks

All banks

Bank Assets in Distress(Percent of outstanding advances)

Gross NPA ratio

Restructured loan ratio

Sources: Reserve Bank of India; and IMF staff estimates.

34

ASEAN-5 weathered the external shocks in 2015-16 well, but face different policy priorities to maintain strong growth

-9.8

-18.4

-5.1-8.7

-6.5-12.1

-3.9 -3.9

-14.0 -14.3

-5.3

-17.8

1.4 -0.4-3.5

5.4 5.81.3 4.0 5.4

17.2

-0.2

9.6 15.5

0.47.2 2.3

6.5 16.4

1.8

-25-20-15-10-505

1015

Indo

nesi

a

Mal

aysi

a

Phili

ppin

es

Thai

land

Sing

apor

e

Indo

nesi

a

Mal

aysi

a

Phili

ppin

es

Thai

land

Sing

apor

e

Indo

nesi

a

Mal

aysi

a

Phili

ppin

es

Thai

land

Sing

apor

e

2015 2016, year-to-date

Equity Prices International ReservesExchange rate against the US$

Change in Exchange Rates, Stock Prices, and International Reserves(Year-over-year percent change)

USUK

Euro area

Indonesia

Malaysia

Philippines

Singapore

Thailand

01234567

-2 -1 0 1 2 3 4

Gro

wth

Inflation

Growth and Inflation(2016H1; in percent, y/y)

35

Other Asian FDEs: Increasing vulnerabilities

Cambodia

Lao P.D.R.

Myanmar

Nepal

Vietnam

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

-40 -20 0 20Fi

scal

Bal

ance

(% o

f G

DP)

Current Account Balance (% of GDP)

Sources: IMF World Economic Outlook database; and IMF staff calculations.Note: The size of the bubbles represents public debt in percent of GDP.

Fiscal and Current Account Balance, 2015

Bangladesh

-6

-4

-2

0

2

4

6

8

10

12

2015 2016 2015 2016 2015 2014 2015

GDP growth Inflation ReservesExport growth

Selected Indicators (Percent)

Sources: IMF World Economic Outlook database and IMF staff calculations.

(y/y)

Small States of the Pacific: Need to build resilience to natural disasters and climate change

0 20 40 60

Palau

Marshall Islands

Kiribati

Timor-Leste

Tuvalu

Micronesia

Caribbean small…

Samoa

Tonga

Solomon Islands

Vanuatu

Fiji

1/ During 1970-2014.Sources: Center for Research on Epidemiology for Disasters, International Disaster Database; IMF staff estimates.

Small Pacific island countries average

Probability of Occurrence of Natural Disasters1

(Percent)

Concluding remarks

37

•Asia remains the main engine of global growth.

•In the medium-term, Asia needs to prepare for the risk of a “new mediocre” in advanced economies.

•The global trade slowdown and anti-trade sentiment can hit Asia hard—Asia needs more balanced and inclusive growth.

•May need to re-assess projections given developments since October projections.