ASHK Evening Talk - actuaries.org.hk · ASHK Evening Talk Actuaries in Insurtech Innovation ... Apr...

37

ASHK Evening Talk Actuaries in Insurtech Innovation Fred Ngan, Michael Chan Co-founders Coherent Capital Advisors Ltd. & Seasonalife Ltd. Thursday, 20 October 2016 1 Strictly Confidential.

Transcript of ASHK Evening Talk - actuaries.org.hk · ASHK Evening Talk Actuaries in Insurtech Innovation ... Apr...

ASHK Evening TalkActuaries in Insurtech Innovation

Fred Ngan, Michael Chan

Co-founders

Coherent Capital Advisors Ltd. & Seasonalife Ltd.

Thursday, 20 October 2016

1Strictly Confidential.

Agenda

2Strictly Confidential

1. The world is changing fast

2. Insurance (might) (finally) too

3. What others are trying

4. Our role as actuaries?

1. The world is changing fast

Look around

4Strictly Confidential

> 65%of people in Hong Kong would miss their phones more than their walletsSource: Research Now NPS survey, 2015

Demo: Web Visualizations

5Strictly Confidential

Demo: Web Visualizations

6Strictly Confidential

How Customers Make Choices

7Strictly Confidential

Clay Christensen:What job did you hire that product to do?

Getting information

Getting serviced

Being Engaged

2. Insurance (might) (finally) too

2.1. Pressures from customer expectations

Life insurance has an image problem.Insurance is a “misunderstood industry” – it promotes a meaningful social good but is often seen as a “necessary evil”

Finding information: Quality, independent information? Simple features and terms? Unbiased advice?

Ease of getting serviced: Modern user experience? Fast processes?

Engagement: Frequent touch points? Delightful experiences?

of premiums are paid to agents as commission

of respondents are satisfied with their interactions with insurance service providersSource: Morgan Stanley 2014

> 20% < 60%

10Strictly Confidential

Average Net Promoter Score for life insurers in Hong KongSource: Bain & Co 2014

< -30

Consumer trust across industries

11Strictly ConfidentialSource: Edelman Trust Barometer

0% 10% 20% 30% 40% 50% 60% 70% 80%

Financial Advisory

Insurance

Financial Services (Aggregate)

Credit Cards

Banks

Chemicals

Energy

Metals

Food & Beverage

Consumer Electronics

Technology

Trust in Industries (Global)

Customer experience – Geographical

12Strictly Confidential

Source: Capgemini and Efma (2015)

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Developing APAC

Developed APAC

Europe

North America

Customers with Positive Experience

Customer experience – Generational

13Strictly Confidential

0% 10% 20% 30% 40% 50% 60% 70%

Developing APAC

Developed APAC

Europe

North America

Customers with Positive Experience

Other Gen Y

Source: Capgemini and Efma (2016)

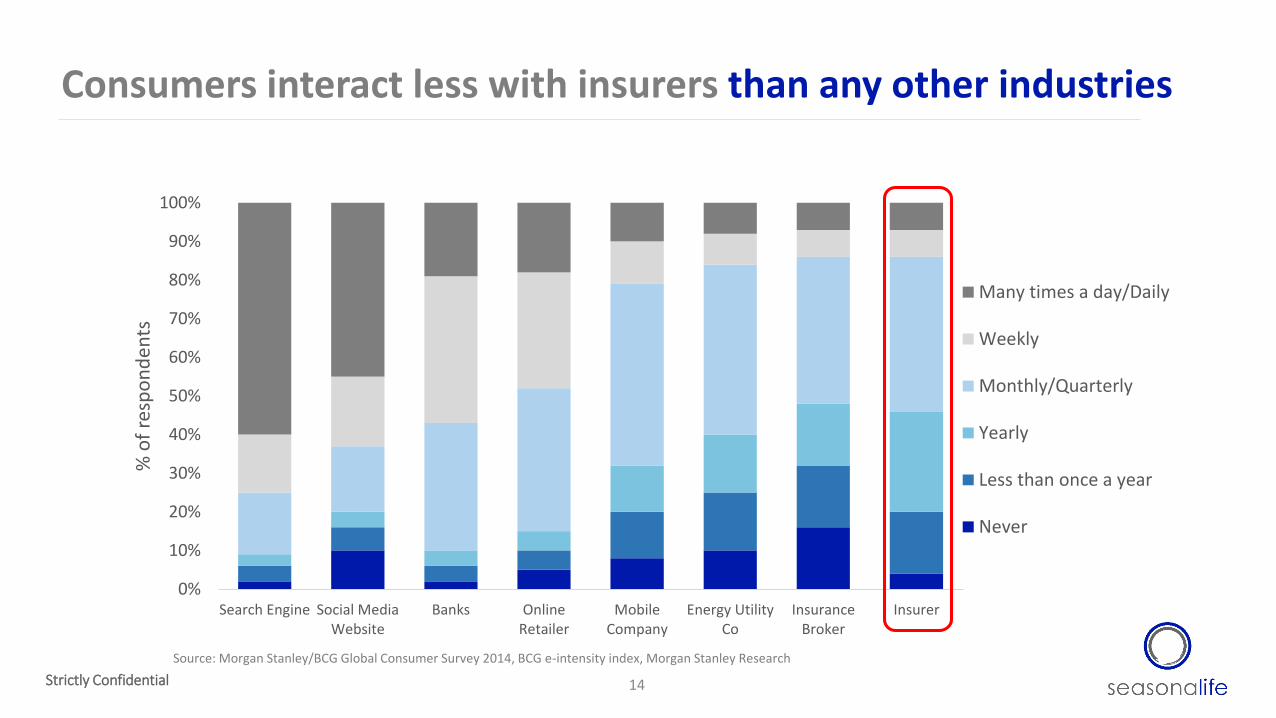

Consumers interact less with insurers than any other industries

14Strictly Confidential

Source: Morgan Stanley/BCG Global Consumer Survey 2014, BCG e-intensity index, Morgan Stanley Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Search Engine Social MediaWebsite

Banks OnlineRetailer

MobileCompany

Energy UtilityCo

InsuranceBroker

Insurer

% o

f re

spo

nd

ents

Many times a day/Daily

Weekly

Monthly/Quarterly

Yearly

Less than once a year

Never

Insurance online experience lags behind

15Strictly Confidential

Source: BCG digital satisfaction survey March 2013, Morgan Stanley Research

15.2

11.811.1

10.08.9 8.5 8.5

8.0

5.85.0

4.3 4.2 4.1 4.0 3.8 3.8

Per

son

alB

anki

ng

On

line

Mer

cha…

Med

iaR

etai

l

Elec

tro

nic

s R

etai

l

Ap

par

elR

etai

l

Air

lines

Inve

stm

en

ts

Ho

tels

Sup

erm

arke

ts

Elec

tric

ity,

Gas

,…

Au

tom

ob

ile

s

Go

vern

men

t…

Hea

lth

Car

e…

Insu

ran

ce

Rea

lEs

tate

Telc

o &

Cab

le

Rel

ativ

e sa

tisf

acti

on

uti

lity

sco

re

Consumer satisfaction with online experience, by industry

Average ~7.3

Hong Kong…

16Strictly Confidential

-100%

-50%

0%

50%

100%

150%

200%M

exi

co

Ch

ina

Fran

ce

Jap

an

Spai

n

Ind

on

esi

a

Bra

zil

Sou

th K

ore

a

Can

ada

US

Mal

aysi

a

Au

stra

lia

Po

lan

d

UK

Ge

rman

y

Sin

gap

ore

Ital

y

Ho

ng

Ko

ng

Change in number of channels used per customer for P&C product purchase, 2016 vs. 2014

Digital

Phone

In-person

Source: Bain/Research Now NPS surveys, 2013-14 and 2016; Bain/SSI NPS survey 2013-14

2.2. Industry drivers

18Strictly Confidential

Value-creation shifts from assets to liabilities as markets mature

Macro trends: US$60 trillion insurance protection

gap across Asia Growing middle class and

savings Increased medical spending,

far above overall inflation Aging population: retirement

solutions

Regulatory capital updates tend to favor insurance over investment risks

Rise of ‘big data’ and analytics should further differentiate risk selection capabilities

5%15%

54% 59%

100%95% 100%85%

46% 41%

US Japan Korea Indonesia China India

Liabilities

Asset

Contribution to Earnings (before tax, extraordinary loss, and dividends provisions)

Source: McKinsey research

19Strictly Confidential

200

14333

20 5

Poolablerisks

Equity/feeproducts

Spread Investment Total

US Insurer Earnings by Risk, 2000-2011(USD billions)

It pays to go back to basics

108

Average Capital Deployed (USD billions)

36 28 58 230Source: AM Best, McKinsey

3. What others are trying

Insurance technology is booming (overheating?)Investment deals in “insurtech” in 2016 YTD have already surpassed 2015

21Strictly Confidential

$130 $348 $269 $859 $1,740 $1,393

$931

26

46

63

91

118 120

2011 2012 2013 2014 2015 2016 YTD

Insurance Tech Financing History2011 – 2016 YTD

Dollars ($M) ZhongAn ($M) DealsSource: CB Insights

Company Date Latest Funding Company Description

Jan – 2016 $1.8mm (Seed) Insurance document management

Jan – 2016 $2mm (Seed) Personalized car insurance

Feb – 2016 $2mm (Seed) Travel insurance

Feb – 2016 $400mm (Series C) Health insurance

Mar – 2016 $31m Chinese online insurance agency

Mar – 2016 $3.9mm (Seed) On-demand insurance

Mar – 2016 $13mm (Seed) Small business insurance

Mar – 2016 $2mm (Seed) Business insurance management platform

Mar – 2016 $4mm (Series A) Pet insurance

Apr – 2016 $25.5mm (Series C) On-demand insurance

May – 2016 $160mm Data-driven health insurance

Sep – 2016 $28mm Mobile insurance policy management

Sep – 2016 $50mm Pay-per-mile car insurance

22

2016 has been a busy year for insurtech funding

Increasing number of deals made by the industry

23Strictly Confidential

14

27 61 56

2012 2013 2014 2015 2016 YTD

Tech startup investments by insurers/reinsurers2012 – 2016 YTD (Sep 2016)

2012 2013 2014 2015 2016 YTDSource: CB Insights

Company Insurance company Date Description

Cathay Insurance Sep-2015 Invested $188mm for 60% of the Shanghai-based company

CPIC Allianz Health insurance

Jul-2015 Formed strategic partnership to jointly promote health reform policies and explore commercial insurance services

eBaoTech Jul-2015 Partnered to launch eBaoCloud, an internet insurance cloundplatform.

Ping An Insurance Dec-2014 Founders of the two companies were among group of investors purchasing a $4.7bn stake in the insurance company

Zhong An Insurance Feb-2013 Founded by Alibaba, Tencent and Ping An Insurance for the first digital insurer in China, which raised $934mm in Jun-2015 and sold 1.6bn insurance policies

CITIC Guoan Group Sep-2015 Set up a joint venture for online insurance

Taikang Life Mar-2014 Allowing WeChat users to buy and gift health insurance to their friends

Bai An Insurance Nov-2015 Baidu, Allianz and investor Hillhouse launched the digital insurance company Bai An

Golo Jan-2015 Set up by Baidu and Ping An for vehicle telematics

AIRIO Life Insurance Sep-2012 Acquired and rebranded to Rakuten Life in 2013.

Growing interest from tech industry heavyweights

24Strictly Confidential

Source: CB Insights

Lateral movements from fintechFintech entrepreneurs moving to insurance

25Strictly Confidential

Source: CBI Insights

Fintech companies entering insurance

Marketplace Lending

Mobile Billing

Digital Banking

Insurance talent moving into insurance tech

26Strictly Confidential

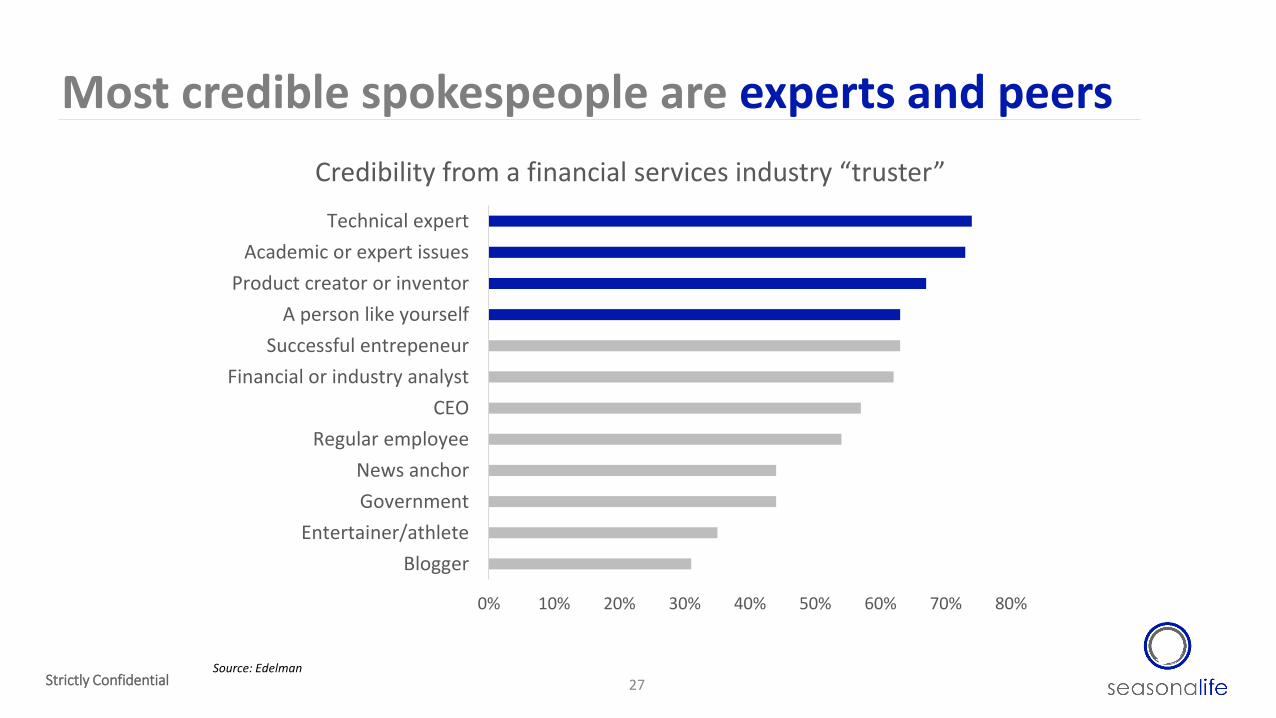

Most credible spokespeople are experts and peers

27Strictly Confidential

0% 10% 20% 30% 40% 50% 60% 70% 80%

Blogger

Entertainer/athlete

Government

News anchor

Regular employee

CEO

Financial or industry analyst

Successful entrepeneur

A person like yourself

Product creator or inventor

Academic or expert issues

Technical expert

Credibility from a financial services industry “truster”

Source: Edelman

4. Our role as actuaries?

Seasonalife

29Strictly Confidential

Who are we Our mission is to be people’s “private actuary” to help make insurance simple and friendly

again.

An online platform for millennials to research, evaluate and purchase insurance products in a smarter way

Moving towards the insurance robo-advisor

Hybrid approach (online plus in-person) delivers more value than in-person or digital alone

Demo: user engagement

30Strictly Confidential

Closing Thoughts

Innovation is a culture

Take risks as an organization and on a personal level

Think digitally

Focus on the customer

Insurance takes a team to deliver –disruptive vs. cooperative

Look backwards and forwards:

Insurance was once a high-tech industry

Actuaries were ‘data scientists’ before it became hot

How many times can we miss the boat?

31Strictly Confidential

"My conclusion: Insurtechstartups do not have all the answers but are best positioned to find them."- Tim Kunde Co-founder of Friendsurance

Stay in touch

32Strictly Confidential

[email protected]; [email protected]

Facebook https://www.facebook.com/Seasonalife/

Appendices

Value Chain

34Strictly Confidential

Emerging ecosystems that could threaten traditional insurers along each point of the value chain

Majority of startup funding still in the US

35Strictly Confidential

United States72%

China12%

Europe15%

Others1%

Tech Investments by (Re)insurers by Geography(2012-2016 September)

Source: CBI Insights

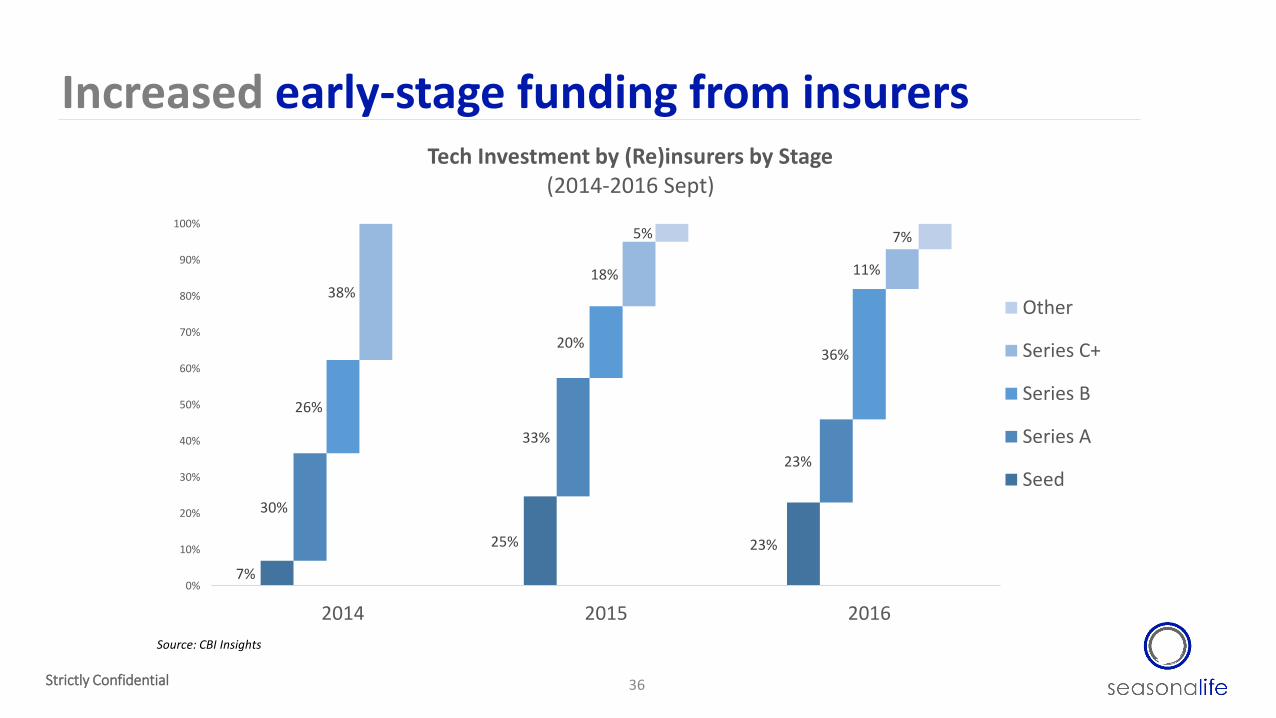

Increased early-stage funding from insurers

36Strictly Confidential

7%

25% 23%

30%

33%

23%

26%

20%36%

38%18% 11%

5% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2015 2016

Tech Investment by (Re)insurers by Stage(2014-2016 Sept)

Other

Series C+

Series B

Series A

Seed

Source: CBI Insights

Sample of distribution startups backed by insurers

37Strictly Confidential

Insurer Insurance Distribution Start-up

Source: CBI Insights