AS MICRO NOTES

22

AS MICRO REVISION PACK

-

Upload

lija-rahman -

Category

Documents

-

view

228 -

download

0

description

AS Micro notes according to the OCR specification

Transcript of AS MICRO NOTES

AS MICRO

REVISION

PACK

COLOUR CODE TO REVISION GUIDE

GREENHEADING/SUB HEADING

BLUEDEFINITION

ORANGEEXPLAINING A CONCEPT

What is Economics?the study of how to allocate scarce resources in

the most effective way.

Economics ProblemScarce resources

Unlimited wants

Choice

MICROECONOMICSStudy of households and firms making decisions

in the market.

MACROECONOMICSStudy of issues that affects economies as a

whole.

FACTORS OF PRODUCTION

Things that are available to the economy and are used to

produce the goods and services.

LABOURThis is human resources that is available to the economy.

Quality and quantity are a key consideration.

CAPITALAny physical resource covering anything that can be

regarded as a man made aid for production. Machines and

infrastructure.

LANDland is used to create the products such as factories and

buildings

ENTREPRENEURSHIPPure human capital, people who come up with the ideas

OPPORTUNITY

COSTthe cost of the next best alternative, which is

forgone when a choice is made.

SPECIALISATION

Concentration of workers to a specific job of goods and

services.

ADVANTAGES OF SPECIALISATION An increase in output

Widening of the range of goods and services.

Exchange between developed and developing

countries

RISKS OF SPECIALISATION If a country has finite resources, they would run out

eventually

Bad weather may wipe out a years worth of crops

The taste of the consumers may change with in time

Any political reasons may effect the outcome of

specialisation

PCC- Reasons Two reasons for change in the PPC Curve

More resources for production

Economic growth

Technological changes

PCC – OPPORTUNITY COST PPC shows the opportunity cost by

choosing to increase the production

of one of the variables. For example,

if they decide to produce

more cars, then the

opportunity cost is less

television sets are

produced.

PPC CURVES

Shows maximum quantities at different

combinations at current resources

C=underproduction as it is

inefficient

D= is above the amount of

which they can produce with

their resources

A/B= possible combinations

If steep- devoting to

the X axis

If flat- devoting to Y

axis

TRADE OFF - The calculation involved in deciding on

whether to give up one good for another. For example,

having more television the trade off is less cars.

MARKET ECONOMY

In this economy the resources are allocates by the

forces of demand and supply through the price

mechanism.

The government has little interference in the market

economy, but keeps an eye on things.

But they interfere with things such as healthcare and

education so that it can be allocated, as these things

can not be allocated through the price mechanism.

Excess of supply from

firms

Fall in price Firms are willing to

supply less

Increase in price

More firms now willing to supply

Increase in supply

Fall in price

COMMAND ECONOMY

An economic system is which most resources are

state owned and also allocates centrally.

FEATURES:Government has the central role in all

decisions

They decode what is available to the consumer

and the manufacture

Government responsible for all allocations

Prices and wages are also controlled

Ownership of firms and businesses is owned

by the state

THERE IS ALWAYS GOVERNMENT INTERVENTION

CONSUMER SURPLUS

The extra amount that a consumer is willing to

pay for a product above the price that is

actually paid.

For example to go to the cinema it costs £1.50 but the person is willing to pay £4, the

surplus for the first visit is £3.50.

For the second trip he is willing to pay £3 for

the same admission fee, the surplus is £1.50.

When demand for five trip, he will receive a

surplus of £5.05. ( add up all the extra

surpluses)

CONSUMER SURPLUS CONTINUED

Consumer surplus can be presented

on the demand curve, showing the

additional money which the consumer

would be willing to pay.

If the market price were to change

then the consumer surplus would also

change.

WHAT EFFECTS THE DEMAND CURVE?

It is clear that price effect demand a lot

For example the purpose of a sale so to

get the consumers to spend more.

BUT THERE ARE OTHER FACTORS Consumer income

The prices of other products

Tastes and fashion

THESE ARE ALL NON-PRICE FACTORS

STRONG GOVERNMENT WEAK

WEAK MARKET STRONG

MIXED ECONOMY

Resources are allocated through a mixture of

government intervention and market

demand and supply

EXAMPLECZECH REPUBLICtransformed into a mixed economy from a

command economy.

Resulted in

Increase in GDP by 5-7 percent

Economic growth

Increase in production

Increase in aggregate demand

COMMAND ECONOMY MARKET ECONOMY

No

rth

Ko

rea

Ch

ina

Alb

an

ia

UK

FR

AN

CE

HU

NG

AR

Y

Sin

ga

po

re

USA

Allocation of Resources

DEMAND

NOTIONAL DEMANDThe desire for a product

EFFECTIVE DEMAND The willingness and ability to buy a product

CETERIS PARIBUSassuming all other variables are the same

RELATIONSHIP BETWEEN PRICE AND QUANTITY DEMANDED Inverse relationship between price and quantity

demanded

Lower price=more demanded

Higher price=less demanded

NOTE – consumers are rational as the stated above

so that they can save money

DEMAND CURVE

Representation of this relationship between

price and quantity demanded

The data for the demand curve is derived

from a demand schedule.

DEMAND SCHEDULE data used to create a demand curve

When there is a change in demand due to price change, it is called movement along the demand curve.

EXTENSION

CONTRACTION

CONSUMER INCOME

this is a great influence, because if there is a low income then

the consumers would be less willing to buy products.

If the price rises and is greater than the income, then the

real income has fallen.

This is not great as the ability to pay for the goods and

services has fallen.

DISPOSABLE INCOMEIncome after taxes such as the state benefits and income tax

REAL DISPOSABLE INCOME after all the taxes taken of and the addition of state benefits.

NORMAL GOODSGoods for which an increase in income leads to an increase in

demand. INFERIOR GOODSGoods for which an increase in income leads to a fall in

demand, such as basic foods.

THE PRICES OF OTHER PRODUCTS

The demand for a particular product can be affected

by a change in price from another but similar product

SUBSTITUTES Competing goods

If the a substitute for bread goes down in price then

the original bread would loose demand as the

substitute is cheaper.

COMPLEMENTSGoods for which there is a joint demand

If the price for airplanes increases, therefore leading

to an decrease in holidays, there would a decrease in

demand as there is an increase in price. This shows that complements, the price and the demand there is a inverse relationship.

TASTES AND FASHION Consumers tastes and fashions

always changes over time.

This can result in a change in

demand or price because of a

change in price.

All these key points, result in a change in demand, resulting in a shift on the demand curve

Change in demand due to Effect on the demand curve

An increase in consumer income A rise in in price of substitutesA fall in the price of complementsA positive change in tastes and fashion

A shift to the RIGHT

A fall in consumer income A fall in the price of substitutesA rise in the price of complementsA negative change in tastesand fashion

A shift to the LEFT

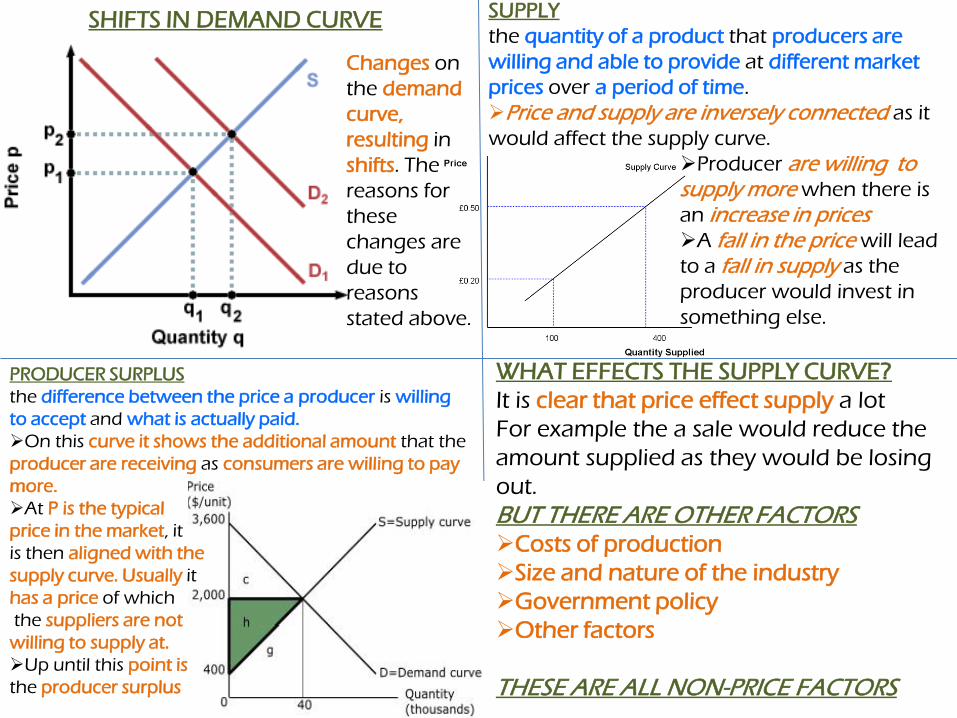

PRODUCER SURPLUS

the difference between the price a producer is willing

to accept and what is actually paid.

On this curve it shows the additional amount that the

producer are receiving as consumers are willing to pay

more.

At P is the typical

price in the market, it

is then aligned with the

supply curve. Usually it

has a price of which

the suppliers are not

willing to supply at.

Up until this point is

the producer surplus

SHIFTS IN DEMAND CURVE

Changes on

the demand

curve,

resulting in

shifts. The

reasons for

these

changes are

due to

reasons

stated above.

SUPPLY

the quantity of a product that producers are

willing and able to provide at different market

prices over a period of time.

Price and supply are inversely connected as it

would affect the supply curve.

Producer are willing tosupply more when there is

an increase in pricesA fall in the price will lead

to a fall in supply as the

producer would invest in

something else.

WHAT EFFECTS THE SUPPLY CURVE?

It is clear that price effect supply a lot

For example the a sale would reduce the

amount supplied as they would be losing

out.

BUT THERE ARE OTHER FACTORS Costs of production

Size and nature of the industry

Government policy

Other factors

THESE ARE ALL NON-PRICE FACTORS

COSTS OF PRODUCTION

the obvious factors are the factors of

production.

Change in the cost of resources

Change in cost of labour

Efficiency from labour to capital

A increase in this factors would lead to an increase market price .

A decrease in these factors would lead to a decrease in the market price.

SIZE OF NATURE OF INDUSTRY

For example there is a lot of competition in

the food industry.

So an increase in the prices would lead to

a great impact on the supply

On other remarkets if there is an increase

in resources then it would result in little or

no effects on the profits.

GOVERNMENT POLICY

All companies are effected by this as they all

have to pay VAT.

If there was an increase is passed onto the

consumers through an increase in price. This

then effects the willingness of producers to

supply.

Health and safety can lead to an increase in

cost for production.

However the government can provide

subsidies to farmers so that the costs are reduced

and so then the prices to customers. This then

leads to an increase in supply.

OTHER FACTORS

Bad wheatear

Scarcity of resources

Items such as these depends on the sorts of

products produced.

Change in supply due to Effect on the supply curve

A fall in raw materials costAn improvement in labour efficiency A reduction in the rate of indirect taxA positive technological advanceAny other positive factors

A shift to the RIGHT

An increase in the cost of raw materials An increase in labour costAn increase in the rate of indirect taxA failed technological advanceAny other negative effects

A shift to the LEFT

Changes on

the supply

curve,

resulting in

shifts. The

reasons for

these changes

are due to

reasons stated

above.

HOW PRICES ARE DETERMINED?

This is done through the use of equilibrium

price. Also known as clearing price.

EQUILIBRIUM PRICEThis is the market price where demand and

supply are equal.

EQUILIBRIUM QUANTITY The quantity that is demanded and supplied at

the equilibrium price.

DISEQUILIBRIUM When the market is unstable, when demand

and supply is not equal.

Surplus- an

excess supply

over demand

Shortage- an

excess of

demand over

supply

When demand is greater than

supply, then the price will rise.

EFFECTS OF CHANGE IN DEMAND OR SUPPLY ON

THE EQUILIBRIUM POSITION

with in a market position is subject to change. There

are three reasons for this:

A CHANGE IN DEMANDThis would change the demand and shift the curve so

that there is a change in equilibrium

A CHANGE IN SUPPLY This would change the supply and would cause a shift

on the curve so that there is a change in equilibrium

MORE OR LESS CHANGE IN A SIMULTANEOUS CHANGE IN DEMAND AND SUPPLYThis means that there is a change in both demand and

supply but then cancel each other out.

ELASTICITY

The extent to which buyers and sellers respond

to a change in market conditions

PRICE ELASTICITY OF DEMAND (PED)Measures the response when the quantity

demanded of a product changes due to the

price.

Price elasticity =Of demand

PED > 1 =ELASTIC

PED <1 = INELASTIC

PED = 1 = change in price is proportionate to the

change in demand

% change in quantity demanded

% change in price

PRICE ELASTICWhere the percentage change in the

quantity demanded is sensitive to a

change in price

PRICE INELASTICwhere the percentage change in the

quantity demanded is insensitive to a

change in price.

There are three things that determine the

price elasticity of demand.

% change in price of product B

% change in income

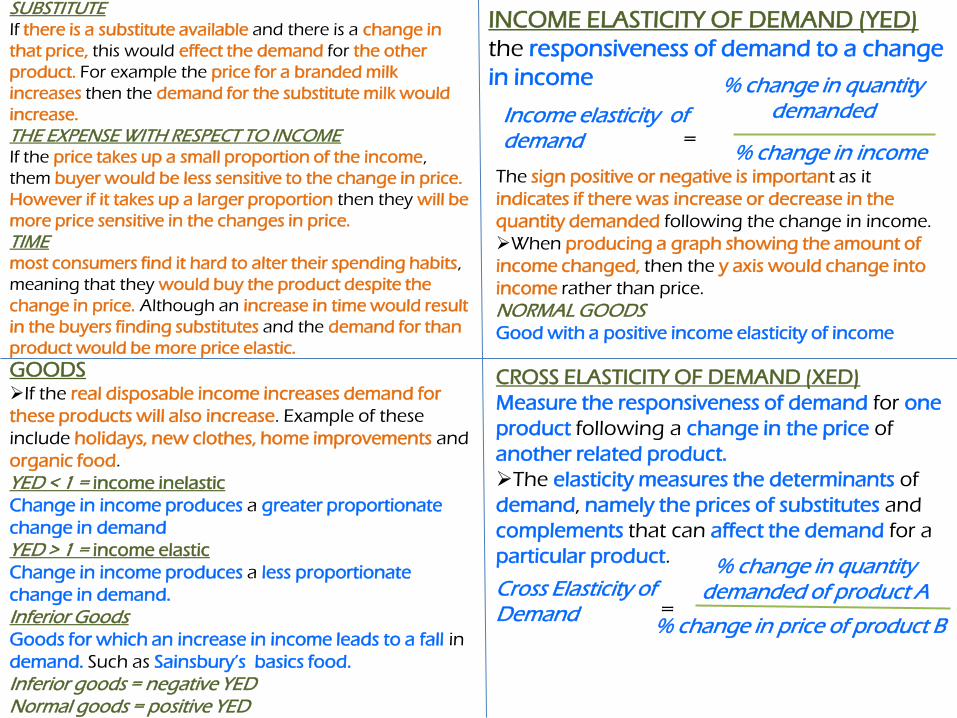

SUBSTITUTE If there is a substitute available and there is a change in

that price, this would effect the demand for the other

product. For example the price for a branded milk

increases then the demand for the substitute milk would

increase.

THE EXPENSE WITH RESPECT TO INCOMEIf the price takes up a small proportion of the income,

them buyer would be less sensitive to the change in price.

However if it takes up a larger proportion then they will be

more price sensitive in the changes in price.

TIMEmost consumers find it hard to alter their spending habits,

meaning that they would buy the product despite the

change in price. Although an increase in time would result

in the buyers finding substitutes and the demand for than

product would be more price elastic.

INCOME ELASTICITY OF DEMAND (YED)

the responsiveness of demand to a change

in income

Income elasticity of demand =

% change in quantity demanded

The sign positive or negative is important as it

indicates if there was increase or decrease in the

quantity demanded following the change in income.

When producing a graph showing the amount of

income changed, then the y axis would change into

income rather than price.

NORMAL GOODSGood with a positive income elasticity of income

GOODSIf the real disposable income increases demand for

these products will also increase. Example of these

include holidays, new clothes, home improvements and

organic food.

YED < 1 = income inelastic

Change in income produces a greater proportionate

change in demand

YED > 1 = income elastic

Change in income produces a less proportionate

change in demand.

Inferior GoodsGoods for which an increase in income leads to a fall in

demand. Such as Sainsbury’s basics food.

Inferior goods = negative YED Normal goods = positive YED

CROSS ELASTICITY OF DEMAND (XED)

Measure the responsiveness of demand for one

product following a change in the price of

another related product.

The elasticity measures the determinants of

demand, namely the prices of substitutes and

complements that can affect the demand for a

particular product.

Cross Elasticity of Demand

% change in quantity demanded of product A

=

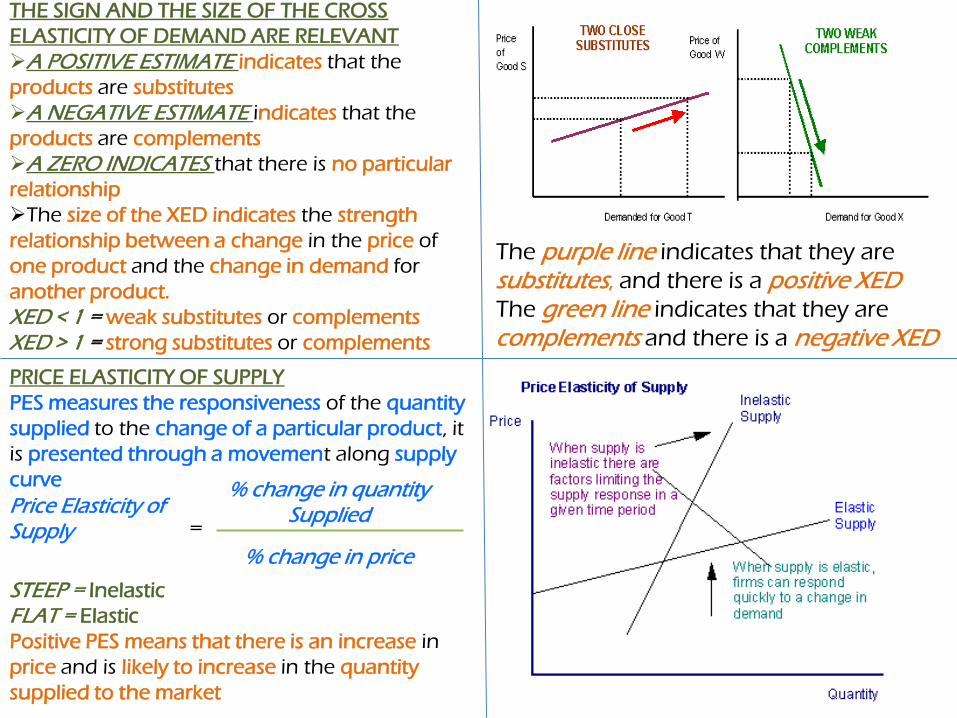

THE SIGN AND THE SIZE OF THE CROSS

ELASTICITY OF DEMAND ARE RELEVANT

A POSITIVE ESTIMATE indicates that the

products are substitutes

A NEGATIVE ESTIMATE indicates that the

products are complements

A ZERO INDICATES that there is no particular

relationship

The size of the XED indicates the strength

relationship between a change in the price of

one product and the change in demand for

another product.

XED < 1 = weak substitutes or complements

XED > 1 = strong substitutes or complements

The purple line indicates that they are

substitutes, and there is a positive XEDThe green line indicates that they are

complements and there is a negative XED

PRICE ELASTICITY OF SUPPLY

PES measures the responsiveness of the quantity

supplied to the change of a particular product, it

is presented through a movement along supply

curve

Price Elasticity of Supply

% change in quantity Supplied

% change in price

=

STEEP = Inelastic

FLAT = Elastic

Positive PES means that there is an increase in

price and is likely to increase in the quantity

supplied to the market

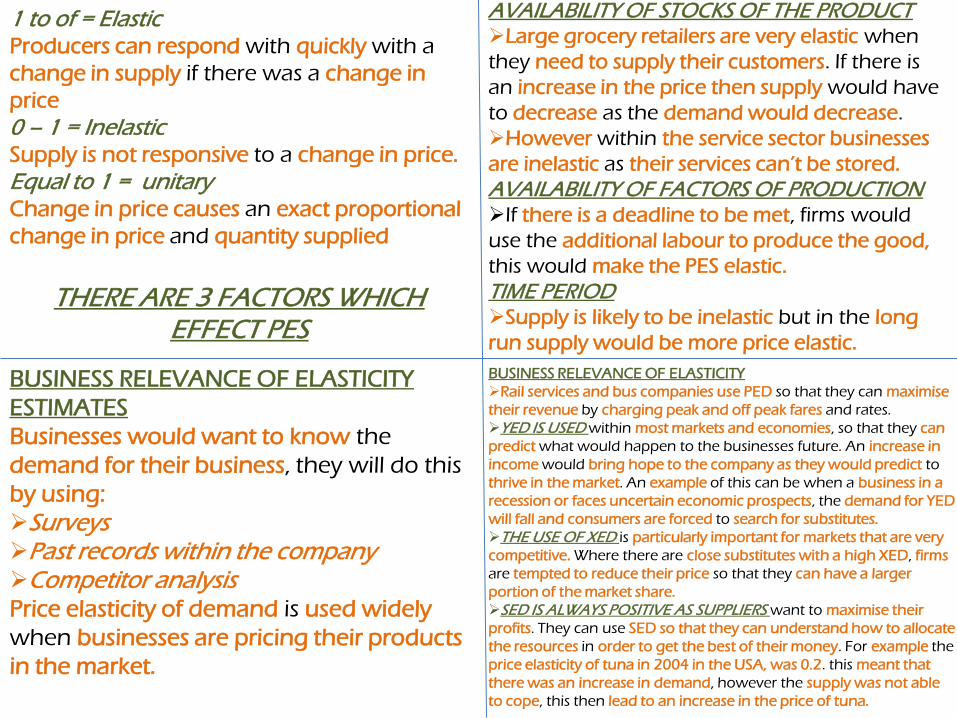

1 to of = Elastic Producers can respond with quickly with a

change in supply if there was a change in

price

0 – 1 = Inelastic Supply is not responsive to a change in price.

Equal to 1 = unitary Change in price causes an exact proportional

change in price and quantity supplied

THERE ARE 3 FACTORS WHICH EFFECT PES

AVAILABILITY OF STOCKS OF THE PRODUCT Large grocery retailers are very elastic when

they need to supply their customers. If there is

an increase in the price then supply would have

to decrease as the demand would decrease.

However within the service sector businesses

are inelastic as their services can’t be stored.

AVAILABILITY OF FACTORS OF PRODUCTION If there is a deadline to be met, firms would

use the additional labour to produce the good,

this would make the PES elastic.

TIME PERIODSupply is likely to be inelastic but in the long

run supply would be more price elastic.

BUSINESS RELEVANCE OF ELASTICITY

ESTIMATES

Businesses would want to know the

demand for their business, they will do this

by using:

SurveysPast records within the companyCompetitor analysis Price elasticity of demand is used widely

when businesses are pricing their products

in the market.

BUSINESS RELEVANCE OF ELASTICITY

Rail services and bus companies use PED so that they can maximise

their revenue by charging peak and off peak fares and rates.

YED IS USED within most markets and economies, so that they can

predict what would happen to the businesses future. An increase in

income would bring hope to the company as they would predict to

thrive in the market. An example of this can be when a business in a

recession or faces uncertain economic prospects, the demand for YED

will fall and consumers are forced to search for substitutes.

THE USE OF XED is particularly important for markets that are very

competitive. Where there are close substitutes with a high XED, firms

are tempted to reduce their price so that they can have a larger

portion of the market share.

SED IS ALWAYS POSITIVE AS SUPPLIERS want to maximise their

profits. They can use SED so that they can understand how to allocate

the resources in order to get the best of their money. For example the

price elasticity of tuna in 2004 in the USA, was 0.2. this meant that

there was an increase in demand, however the supply was not able

to cope, this then lead to an increase in the price of tuna.

ALLOCATIVE EFFICIENCY

EFFICIENCY- where the best use of resources is

made for the benefit of consumers

ALLOCATIVE EFFICIENCY- where consumer

satisfaction is maximised.

to achieve allocative efficiency the quantity

supplied must be equal to the quantity demanded,

in other words there needs to be a function of

equilibrium position.

This means that there is not being too much

supplied when there is a limited amount of

demand.

Or in other words the demand is not being met as

there is not enough supplies going around.

MARKET FAILURE

MARKET FAILURE- where the free markets

mechanism fails to achieve economic

efficiency.

PRODUCTIVE EFFICIENCY- where

production takes place using the least

amount of scarce resources

ECONOMIC EFFICIENCY- where both

allocative and productive efficiency are

achieved

INFORMATION FAILURE

A lack of information resulting in consumers and

producers making decisions that no maximise welfare

If there is not a lack of information then the market

would work efficiently, however if there is a lack then

there would be market failure, as there would a

inefficient allocation of resources.

The problem of information failure is that the

consumers and the producers make the decisions and

are based on the lack of ignorance due to inaccurate or

incomplete information. Example of this:

When consumers are not fully aware of the full

benefits

Persuasive advertising

Misleading product claims

ASYMMETRIC INFORMATION

In some situations a problem of information failure, it is called

asymmetric information. This occurs when the information is

not shared equally between the two parties carrying out a

transaction.

Example of this:

HEALTH CARE- when visiting the doctor, you don't

have the same medical knowledge, you rely on the

doctor and his competence to diagnosis the problem

ENVIRONMENT- as individuals we know little about

the consequences, however specialists are employed

so that they can carry out research and studies.

CONSUMER PURCHASE- thinking that you made a

good deal but then realising that there are strings

attached

INSURANCE- the seller relies on the his knowledge

on whether to sell the policy

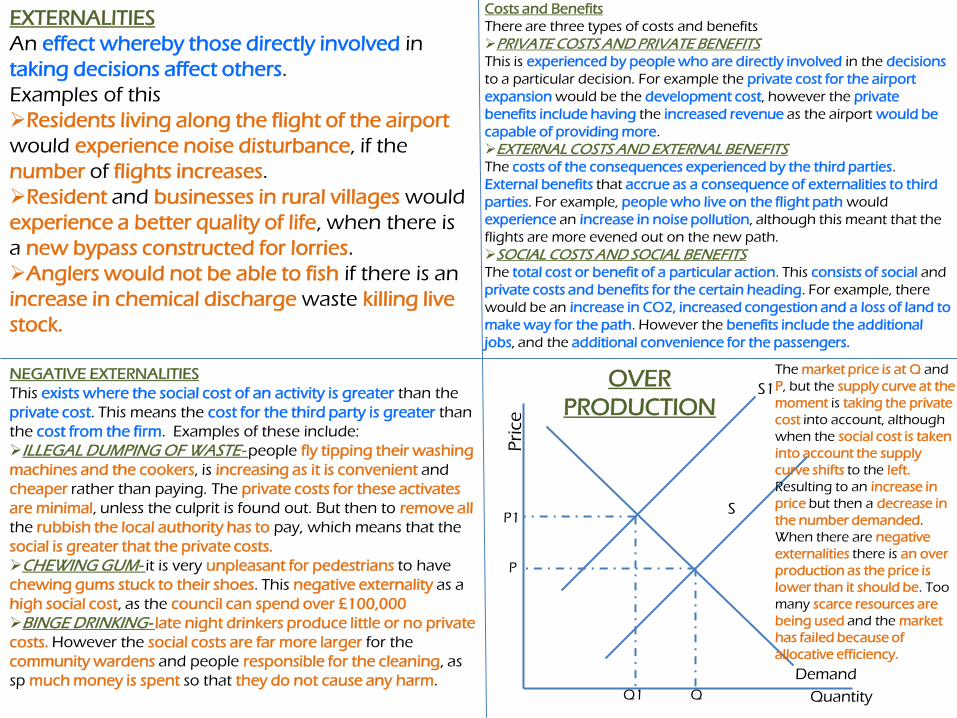

EXTERNALITIES

An effect whereby those directly involved in

taking decisions affect others.

Examples of this

Residents living along the flight of the airport

would experience noise disturbance, if the

number of flights increases.

Resident and businesses in rural villages would

experience a better quality of life, when there is

a new bypass constructed for lorries.

Anglers would not be able to fish if there is an

increase in chemical discharge waste killing live

stock.

Costs and Benefits

There are three types of costs and benefits

PRIVATE COSTS AND PRIVATE BENEFITSThis is experienced by people who are directly involved in the decisions

to a particular decision. For example the private cost for the airport

expansion would be the development cost, however the private

benefits include having the increased revenue as the airport would be

capable of providing more.

EXTERNAL COSTS AND EXTERNAL BENEFITS The costs of the consequences experienced by the third parties.

External benefits that accrue as a consequence of externalities to third

parties. For example, people who live on the flight path would

experience an increase in noise pollution, although this meant that the

flights are more evened out on the new path.

SOCIAL COSTS AND SOCIAL BENEFITS The total cost or benefit of a particular action. This consists of social and

private costs and benefits for the certain heading. For example, there

would be an increase in CO2, increased congestion and a loss of land to

make way for the path. However the benefits include the additional

jobs, and the additional convenience for the passengers.

NEGATIVE EXTERNALITIES

This exists where the social cost of an activity is greater than the

private cost. This means the cost for the third party is greater than

the cost from the firm. Examples of these include:

ILLEGAL DUMPING OF WASTE- people fly tipping their washing

machines and the cookers, is increasing as it is convenient and

cheaper rather than paying. The private costs for these activates

are minimal, unless the culprit is found out. But then to remove all

the rubbish the local authority has to pay, which means that the

social is greater that the private costs.

CHEWING GUM- it is very unpleasant for pedestrians to have

chewing gums stuck to their shoes. This negative externality as a

high social cost, as the council can spend over £100,000

BINGE DRINKING- late night drinkers produce little or no private

costs. However the social costs are far more larger for the

community wardens and people responsible for the cleaning, as

sp much money is spent so that they do not cause any harm. Quantity

Pri

ce

Demand

S

S1

The market price is at Q and

P, but the supply curve at the

moment is taking the private

cost into account, although

when the social cost is taken

into account the supply

curve shifts to the left.

Resulting to an increase in

price but then a decrease in

the number demanded.

When there are negative

externalities there is an over

production as the price is

lower than it should be. Too

many scarce resources are

being used and the market

has failed because of

allocative efficiency.

QQ1

P1

P

OVER

PRODUCTION

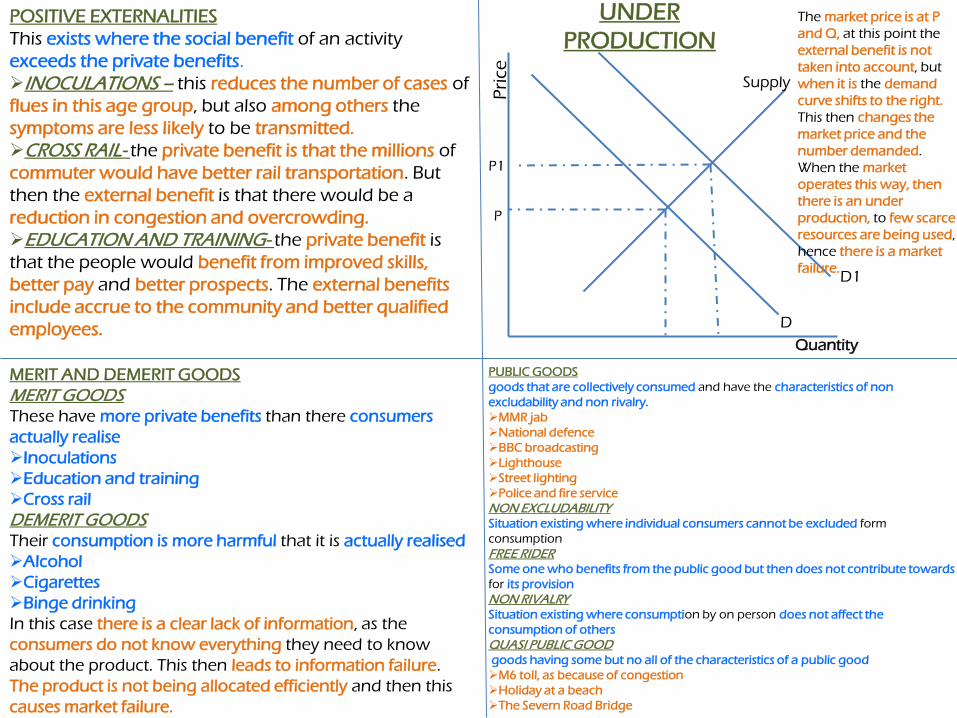

POSITIVE EXTERNALITIES

This exists where the social benefit of an activity

exceeds the private benefits.

INOCULATIONS – this reduces the number of cases of

flues in this age group, but also among others the

symptoms are less likely to be transmitted.

CROSS RAIL- the private benefit is that the millions of

commuter would have better rail transportation. But

then the external benefit is that there would be a

reduction in congestion and overcrowding.

EDUCATION AND TRAINING- the private benefit is

that the people would benefit from improved skills,

better pay and better prospects. The external benefits

include accrue to the community and better qualified

employees. Quantity

Pri

ce

D

P1

P

Supply

D1

The market price is at P

and Q, at this point the

external benefit is not

taken into account, but

when it is the demand

curve shifts to the right.

This then changes the

market price and the

number demanded.

When the market

operates this way, then

there is an under

production, to few scarce

resources are being used,

hence there is a market

failure.

UNDER

PRODUCTION

MERIT AND DEMERIT GOODS

MERIT GOODSThese have more private benefits than there consumers

actually realise

Inoculations

Education and training

Cross rail

DEMERIT GOODSTheir consumption is more harmful that it is actually realised

Alcohol

Cigarettes

Binge drinking

In this case there is a clear lack of information, as the

consumers do not know everything they need to know

about the product. This then leads to information failure.

The product is not being allocated efficiently and then this

causes market failure.

PUBLIC GOODS

goods that are collectively consumed and have the characteristics of non

excludability and non rivalry.

MMR jab

National defence

BBC broadcasting

Lighthouse

Street lighting

Police and fire service

NON EXCLUDABILITYSituation existing where individual consumers cannot be excluded form

consumption

FREE RIDER Some one who benefits from the public good but then does not contribute towards

for its provision

NON RIVALRY Situation existing where consumption by on person does not affect the

consumption of others

QUASI PUBLIC GOODgoods having some but no all of the characteristics of a public good

M6 toll, as because of congestion

Holiday at a beach

The Severn Road Bridge

MERIT GOODS and MARKET FAILURE

Supply

Private

benefit (D)

Social

benefit (D)

When taking the private

benefits into account there is

small amount demanded and

the price is also very low.

However with the full

information, and people being

aware of the social benefits

then the demand should

increase, this would then

increase the price and the

quantity demanded. The

shaded area is the welfare loss

due to information failure.

DE MERIT GOODS and MARKET FAILURE

Demand

Full information

Demand

Private benefit limited

information

Q1Q2Q3Q1 Q2

EXTERNAL

COST

GOVERNMENT INTERVENTION TO CORRECT MARKET FAILURE

Government intervene in the workings of the market

mechanism to correct the market failure, equitable distribution

of wealth and income and the performance of the economy.

NEGATIVE EXTERNALITIES Charges are made for those who fly tip and legislations and

regulations are put in place so that this can decrease. Binge

drinking, in some parts of the country owners have to pay local

levy for the trouble which is caused.

POSITIVE EXTERNALITIESIn the case of inoculations, it is free , by providing subsidies it

increases the number of people taking the vaccination. This is

the same for education and training.

MERIT GOODSThe provision of information and state provision is a way of

which the government seeks to address the problems of under

consumption, so that they can understand the real cost and

benefit.

DEMERIT GOODSThe provision of full information and indirect taxation is

a way of which the government seeks to regulate and

reduce the consumptions of these products.

PUBLIC GOODSThis is done through the use of general tax revenue

and state provision. In some cases such as broadcasting

a charge is made for the consumption. Market failure in

this sector would be corrected if there intervention

would produce a better allocation of resources. There

are two approaches

•Methods that involve manipulations of the market

mechanism, subsides, indirect taxation and the

provision of information

•Non market methods- direct provision and forms of

regulations and control.

Quantity

Pri

ce

Quantity

Pri

ce

TAXATION

There are two types of taxation

DIRECT TAXESThis includes income tax, co operation tax and national insurance

contribution; these taxes come directly from the firms and the

individual.

INDIRECT TAXESThis includes VAT, council tax and business rates are charged on the

ownership of houses and business premises.

The use of indirect taxes can effect the demand and the supply for a

certain product. This is determined by the elasticity of the product. for

example a de merit good has a high consumption, and the

government wishes to intervene, they would first try through the use

of indirect taxes. This would be imposed on the suppliers of the

product, as a result this would increase the making of the product and

would heighten their burden. However, since it is an inelastic product

the suppliers pass on this increase of cost to the consumers, increasing

their burden. This then would lead to a higher market price, but would

result in the same amount of revenue as that increase in income would

be used to pay the tax.

INDIRECT TAXES

Suppliers in a market which affects the cost of

production and therefore effects the market supply at

each price.

Takes on a specific item of consumer spending.

INDIRECT TAXESValue added tax (VAT)- a fixed tax per unit of goods

and services.

However there are some exceptions such a reduced

VAT. This is implanted in for domestic fuel and power

and for children car seats so that individuals can be safe

and follow by the law.

There is also another exception such as VAT exempt,

where there is no charge. This is implanted into private

education, finance and insurance and health and postal

service.

WHY IMPOSE INDIRECT TAX?

Increase tax revenue and fund the

government findings

It is more fair tax rather than

determining on wealth and income.

To change the demand for goods and

services. (reducing the demand for a de

merit good)

Indirect tax is easy to change and is

flexible.

Also it is harder to avoid, so everyone

has to contribute.

Consumer burden

Producer burden

CONSUMER AND PRODUCER BURDEN

At Q and P, the indirect tax has not been

implanted in resulting in number of Q demanded

and the market price at P. However, when the tax

is put into place, the supply curve shifts to the left,

which results in increase in price but a decrease in

supply at P1 and Q1. the difference between P and

P1 is the consumer burden, which is the extra

money which the consumer has to pay in in order

to get the product. However where Q1 and the

supply pre tax intersect is the producer burden.

And at P2 is the price of which the supplier is

willing to sell at. From P2 and P1 is the total

amount of tax.

THE ARGUMENTS AGAINST INDIRECT TAX

Some of the indirect tax can have a regressive impact

on people who earn a lower income

Tax burden is the heaviest on low income individuals

as large proportions is being spent on small items

This would then result in more unequal distributing of

income as the lower income individual have to spend

more in order to eat.

Higher indirect tax could therefore lead to inflation.

(suppliers passing on the burden and then increasing

the market price.

The indirect tax would cause services to be too

expensive and this would lead to boot legging. People

not following rules and regulations.

Loss of economic welfare as the increase in price

would cause a loss of producer and consumer surplus

Consumer burden

Producer burden

QQ1

P

P1

P2

Demand

Supply pre

tax

Supply post

taxELASTIC

QQ1

P

P1

P2

Demand

Supply pre

tax

Supply post

taxINELASTIC

Quantity

Pri

ce

Quantity

Pri

ce

CONSUMER AND PRODUCER BURDEN

At Q and P, the indirect tax has not been implanted in

resulting in number of Q demanded and the market

price at P. However, when the tax is put into place, the

supply curve shifts to the left, which results in increase

in price but a decrease in supply at P1 and Q1. the

difference between P and P1 is the consumer burden,

which is the extra money which the consumer has to

pay in in order to get the product. However where Q1

and the supply pre tax intersect is the producer

burden. And at P2 is the price of which the supplier is

willing to sell at. From P2 and P1 is the total amount of

tax. However, the product is inelastic meaning that

the producer can pass on the tax to the consumer, this

then increases the market price and should decrease

the demand for the de merit good.

SUBSIDES

It is a payment by the government to producers or consumers of

goods and services, to encourage production and consumption.

THE MAIN PURPOSE IS THEREFORE To reduce the cost in order to provide a higher level of

production or consumption than it would if it was left to the

market.

This is aimed at merit goods which generate positive

externalities

To keep the price of the product low

Boost demand for a certain product to encourage consumption

Reduce the cost of capital investment which would stimulate

long term economic development in the country.

Maintain the service which provides positive externalities

THE EFFECT OF THE SUBSIDY Is to increase the supply

It would decrease the market price and this would result in an

expansion demand

PRODUCER SUBSIDY an input in which subsidies the cost of certain inputs

used in production

Financial support – such a grant or a block of payment

to cover losses made by a business.

FARM SUBSIDIES Under the old common Agricultural Policy, the EU

provides direct payments to the producers based on

output, however now they receive payments in a single

income payment.

Such organic farmers would receive subsidies so that

the price for the product can be cheaper and this would

then increase the demand for the product. This would

help reduce the costs of making the fruits and

vegetables which in return would decrease the price. Demand

Supply

Pre Sub

Supply post

sub

P

P1

Q Q1

The effect of

using the

subsidy is that

the price has

dropped and

this in return

has increased

the supply, To

Q1 and P1.

SUBSIDY EFFECT

Quantity

Pri

ce

GAINERS FROM THE SUBSIDY

Consumers who are able to purchase the product at

a much higher price

Consumers who are the direct recipient of subsides

e.g. Payment of child care

Producers as their producer surplus increases as their

net revenue is higher

LOSER FROM THE SUBSIDY

General tax payers, who must fund for the subsidy

Other producers who are not entitled to the subsidy

Higher government spending, involves an

opportunity cost as the money can be spent on

alternatives

Subsides lead to inefficiencies in production due to

the lack of competitions. The producers are cushioned

by the subsidy.

TRADABLE PERMITS

market based tradable permits are used so that they

correct market failure.

Allows the owners to emit a specific amount of

pollution

Total amount of permits are controlled so that the

they can control the amount of pollution to an

acceptable level

They are bought and then can be sold at a price to be

agreed upon by their owner/purchaser

The incentive for the permit holder is to achieve a

lower level of pollution, any used permits can then be

sold off.

Firms who don’t have sufficient firms to cover their

pollution level would be prosecuted.

Demand

Demand 1

Supply

Supply is completely inelastic, as

there is a limited amount of permits,

so you can pay much higher but you

still would get the same amount.

Which is when there is an increase in

demand for the permits, the quantity

does not change but the price

increases drastically.

Quantity

Pri

ce

![Micro Processors & Micro Controllers Lecture Notesgopalmic.weebly.com/uploads/6/0/3/4/6034310/mpi_full_document.pdfMicro Processors & Micro Controllers Lecture Notes (As Per JNTUK-[R07]](https://static.fdocuments.us/doc/165x107/5aa2476a7f8b9a1f6d8d063d/micro-processors-micro-controllers-lecture-processors-micro-controllers-lecture.jpg)