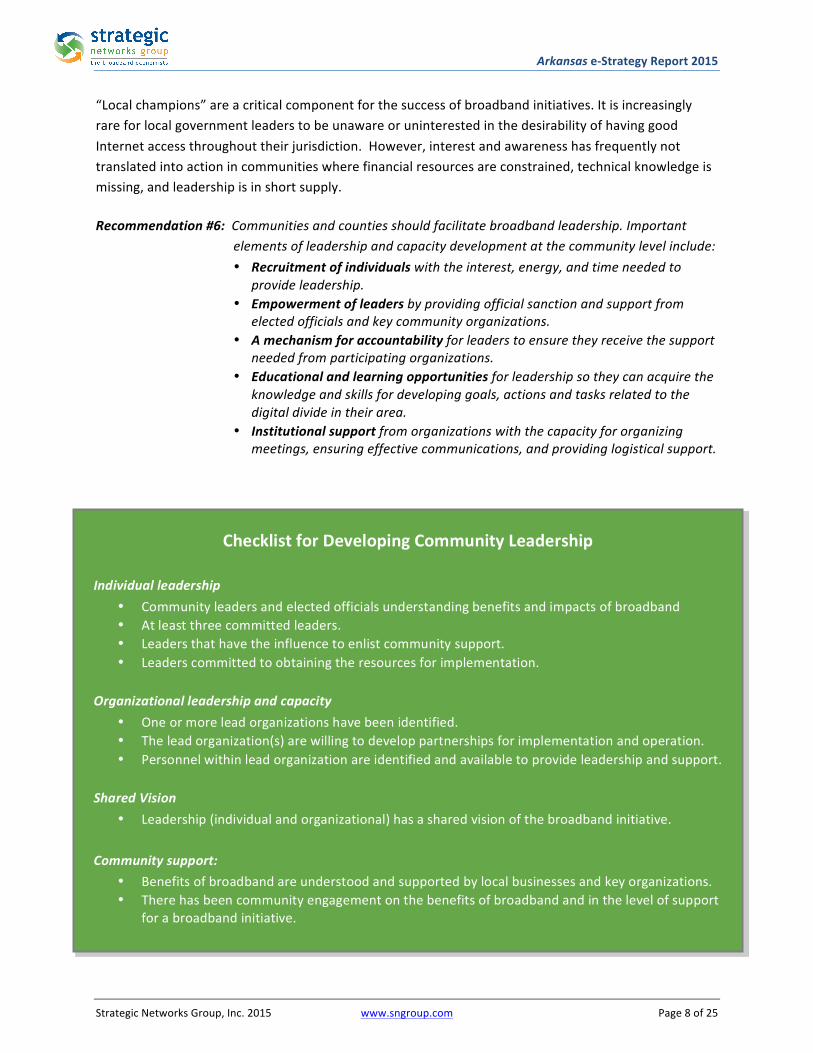

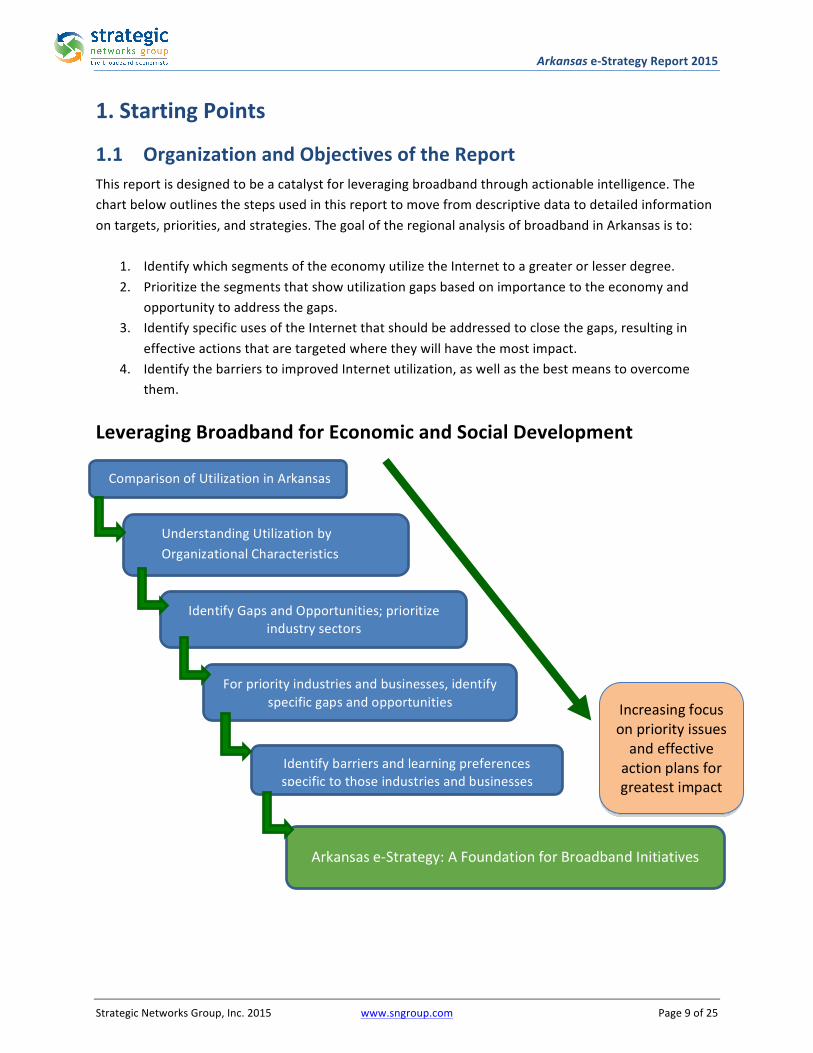

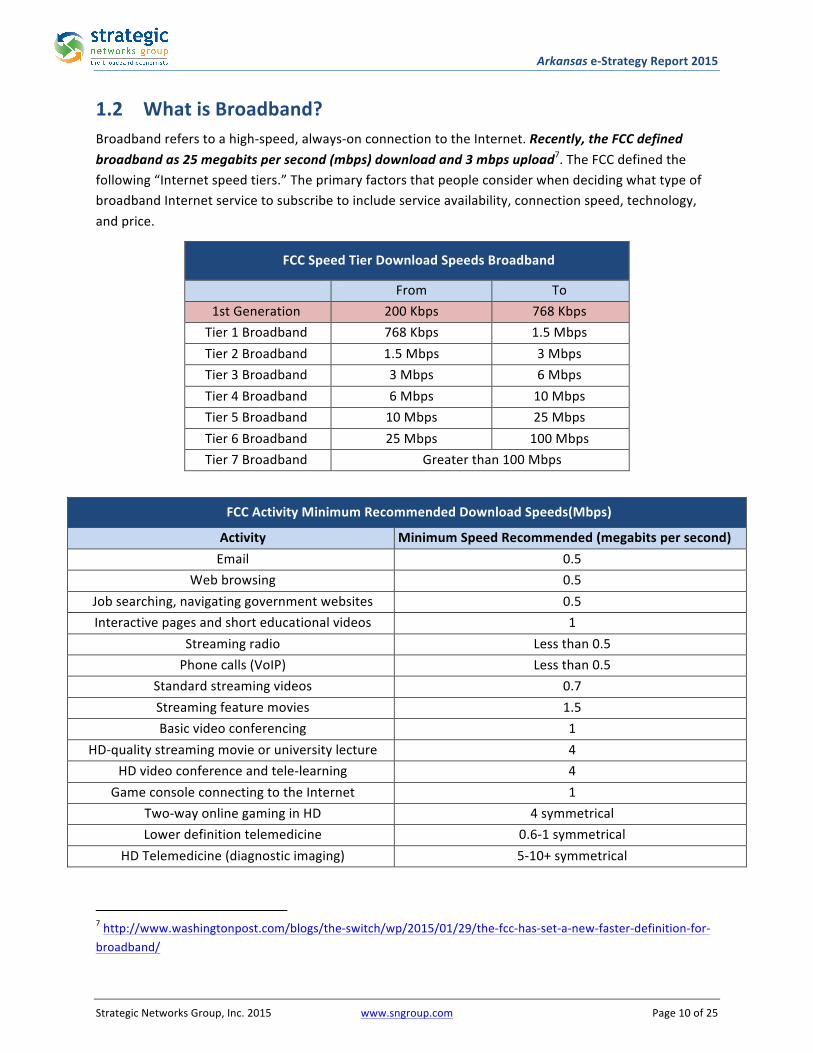

Aqua eSolutions, Soluciones Software Sector Textil y Moda - Aqua eFashion

Upload

truonghanhCategory

view

219download

1

StateofArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page1of36

ArkansaseSolutionsBenchmarkingReport

March2015

Preparedfor

StrategicNetworksGroup,Inc.|www.sngroup.com|CONFIDENTIAL

StateofArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page2of36

TableofContents

ExecutiveSummary..................................................................................................................4

1 OrganizationalAssessment...............................................................................................81.1 RespondentProfile.................................................................................................................81.2 OrganizationalConnectivityCharacteristics..........................................................................11

1.2.1 InternetSpeeds...................................................................................................................111.2.2 Cost.....................................................................................................................................151.2.3 Satisfaction..........................................................................................................................15

1.3 BroadbandUtilizationandBenefits......................................................................................161.3.1 UtilizationPatterns..............................................................................................................161.3.2 BroadbandandDecidingWheretoLocate.........................................................................201.3.3 BroadbandBenefitsandImpacts........................................................................................21

1.4 BarriersandAdoptionIssues................................................................................................221.4.1 BarrierstoAdoption............................................................................................................221.4.2 ExpertiseandKnowledgeIssues.........................................................................................221.4.3 SkillsAcquisition..................................................................................................................23

1.5 FinancialandEmploymentImpactsfromInternetUse..........................................................24

2 Benchmarks....................................................................................................................262.1 TheDigitalEconomyIndex...................................................................................................262.2 UtilizationBenchmarks.........................................................................................................27

3 ComparativeAnalysis......................................................................................................30

StateofArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page3of36

ListofFigures

Figure1–ResponsesbyRegion.....................................................................................................................8Figure2-ResponsesbyLevelofUrbanization..............................................................................................8Figure3-ResponsesbyEmploymentSizeofOrganization(NumberofEmployees)...................................9Figure4-ResponsesbyIndustrySector.....................................................................................................10Figure5–HowBusinessesandNonprofitOrganizationsConnecttotheInternetinArkansas.................11Figure6–Speed-TestResultsforAverageUploadSpeeds(businessesandnonprofitorganizations).......12Figure7-Speed-TestResultsforAverageDownloadSpeeds(businessesandnonprofitorganizations)...12Figure8–AverageUploadSpeedsbySector...............................................................................................13Figure9–Speed-TestResultsbyTypeofConnectivity(allsectors)...........................................................13Figure10–DownloadSpeeds(mbps)byConnectionandLevelofUrbanization(allsectors)....................14Figure11–UploadSpeeds(mbps)byConnectionandLevelofUrbanization(allsectors).........................14Figure12–InternetCostsbyTypeofConnection(allsectors)...................................................................15Figure13–eCommerceUsesofBroadband...............................................................................................16Figure14–eProcessUsesofBroadband....................................................................................................17Figure15–BusinessUtilizationofMobileInternet....................................................................................18Figure16–UseofWeb-enabledMobileDevices.......................................................................................18Figure17–PercentageofBusinessesUsingCloudBasedServices............................................................19Figure18–MotivatingDriversofAdoptionofCloudServices...................................................................19Figure19-Mobileapplicationsusedbybusinesses...................................................................................20Figure20–ImportanceofBroadbandBenefitsforBusinesses..................................................................21Figure21–BarrierstoGreaterBusinessesUseoftheInternet..................................................................22Figure22–PreferredMethodsforAcquiringInternalKnowledge.............................................................23Figure23–AnnualRevenuesandCostSavingsfromInternetUtilization..................................................24Figure24–SummaryofEmploymentImpactsofBusinessResponses(FullandPartTimecombined).....25Figure25–SummaryofEmploymentImpactsSpecifictoInternetUse(FullandPartTimecombined)...25Figure26-SummaryofEmploymentImpactsSpecifictoInternetUse(FullandPartTimecombined)....27Figure27–UtilizationBenchmarks(DEi)forBusinessesbyLevelofUrbanization....................................28Figure28–UtilizationBenchmarks(DEi)forBusinessesbyRegion...........................................................28Figure29–UtilizationBenchmarks(DEi)forBusinessesbySizeofBusiness.............................................29Figure30–UtilizationBenchmarks(DEi)byIndustrySector......................................................................29Figure31-Differentindustrysectorsfrommetropolitanareas.................................................................31Figure32-Differentindustrysectorsfromnon-metropolitanareas.........................................................31Figure33-Businessesfromfivedifferentsizerangesinmetropolitanareas............................................32Figure34-Businessesfromfivedifferentsizerangesinnon-metropolitanareas.....................................32

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page4of36

ExecutiveSummaryThiseSolutionsBenchmarking(eSB)ReportisadocumentationofdatacollectedinArkansasbetweenNovember2014andFebruary2015.Thissummaryprovidesanunderstandingofcurrentbroadbandaccess,adoptionandutilizationpatternsaroundthestate.

ResponseLevels:Atotalof1,532organizationscontributedtothebroadbandbenchmarkingeffort.Theorganizationsconsistedof1,236commercialbusinesses,95governmententitiesand201non-profitorganizations.BusinessesandOrganizationsConnectivity:Whileonly1.5%ofrespondentsfailedtomeettheoriginalFCCdefinitionofbroadband(768kbpsormoreinatleastonedirection),speedtestresultsduringtheassessmentshowedthatahighpercentageofrespondentsweresignificantlybelowtherecentlyannouncedFCCstandardforbroadband1.Ofthosetakingthespeedtest,63.1%haduploadspeedsoflessthanthenewstandardof3mbps,while80%failedtomeetthenewdownloadstandardof25mbps.Inrecentyears,wirelessnetworksandmobiledeviceshaveincreasinglybecomeafactorinhowpeoplecommunicate,andhowbusinessesandorganizationsbringefficiencytotheiroperations.Over83%ofbusinessesuseasmartphoneand76.8%useaweb-enabledlaptopcomputer.Lookingtocapitalizeonthesenewerchannelsofcommunications,47.6%ofbusinesseshavenonethelessrecognizedtheimportanceofmobilesappsandhavetailoredtheirexistingwebsitestomobiledevices.Further,26.9%percentofbusinessesareplanningtooptimizetheirwebsitesformobilebrowsers.InternetUtilizationPatterns:Almost80%ofbusinessesusetheInternettopurchasegoodsandservicesonline.Incontrast,only40.3%ofbusinessessellgoodsandservicesonlineandjustover36.8%deliverservicesandcontentonline.Section1.3looksatthelevelofadoptionofdifferenttypesofInternetapplications,aswellascloudsolutions,useofmobileservices,andwhichimpactsofInternetusearemostvaluedbytheirusers.Barriers:SecurityandprivacyconcernsarethetwobarrierstoInternetutilizationthatratethehighestinimportance,with40%and29%ofbusinesses,respectively,ratingthemasveryimportantbarriers.FinancialandEmploymentImpactsofInternetUse:Whileover1,682newpositionswerecreatedbyrespondingbusinessesinthepreceding12months,thesebusinessesalsoexperiencedsizeablejobreductions,resultinginanetjobincreaseof1,290positions.ThenetjobincreaseattributedtousingtheInternetwas461positionsor29.4%ofallnewjobs.Section1.5outlinesemploymentimpacts,aswellasreportedimpactsonrevenuesandcostsinrespondingorganizations.

1http://www.washingtonpost.com/blogs/the-switch/wp/2015/01/29/the-fcc-has-set-a-new-faster-definition-for-broadband/

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page5of36

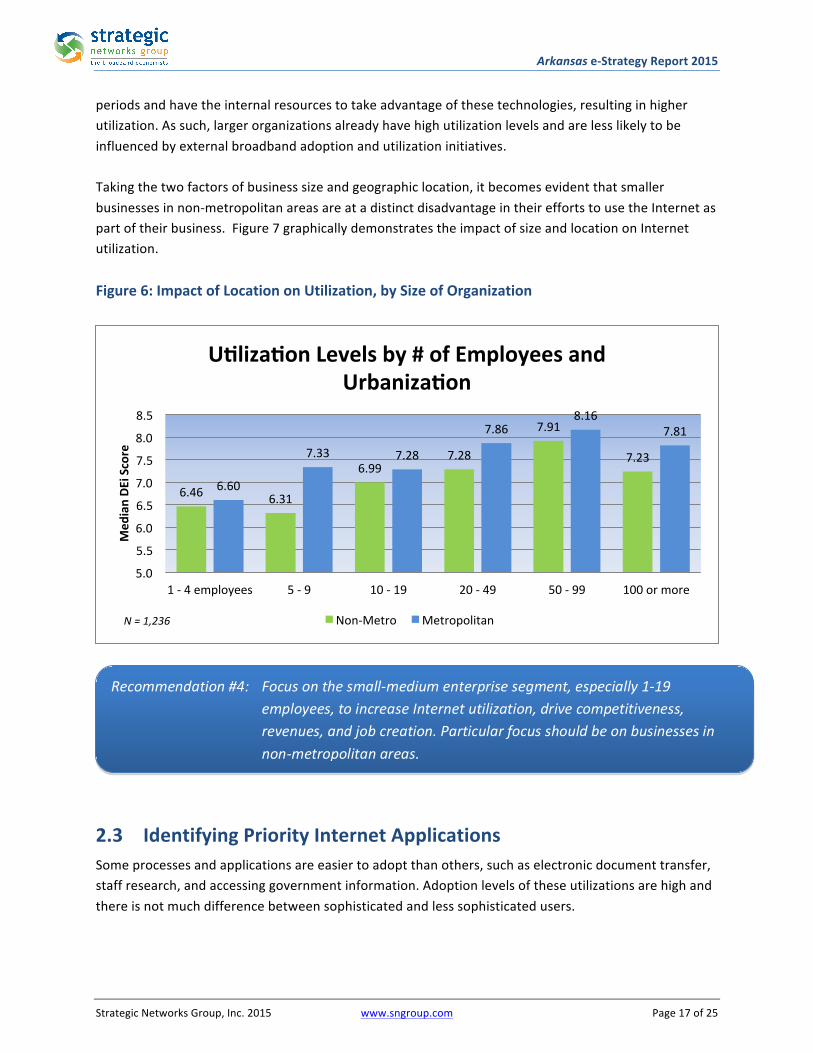

BenchmarksforOrganizations:Section2providesstatewidebenchmarkingtocomparehowdifferentregionsandindustrysectorsutilizetheInternet.KeyconclusionsarethatsizeofbusinessandgeographiclocationarekeyfactorsinthelevelofInternetutilization.LargerandmoremetropolitanbusinessesutilizetheInternetmorethansmallerandmoreruralbusinesses.Inessence,thereisadigitaldivideorutilizationgap,betweensmallandlargebusinesses.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page6of36

IntroductionThiseSolutionsBenchmarking(eSB)ReportisasummaryreportthatprovidesinsightsintocurrentInternetaccess,adoptionandutilizationpatternsacrossArkansas.OnbehalfofConnectArkansas,SNGreachedouttocommercialandnon-commercialorganizationsacrossthestatetoencourageparticipationintheonlineassessment.Businesses,non-profitorganizationsandsomegovernmententitieswereaskedtocompleteaself-assessmentintheformofanonlinesurveythatcollectedinformationontheavailabilityofbroadband(high-speedInternetaccess),howbroadbandisbeingusedintheorganization,alongwithquestionsthatwouldhelpidentifybenefits,driversandbarrierstoadoptionandutilization.Whileitisnotpossibletoincludeeveryquestionandresponsefromtheassessmenthere,thiseSBreportprovidesinsightsintokeyfindingsthatpointtogapsandopportunitiesforincreasingbroadbandutilization.Inadditiontotheinformationpresentedinthisreport,allthedatacollectedthroughthisinitiativeisavailablethroughanonlineplatformcalledtheDigitalEconomyAnalyticsPlatform(DEAP),whichthestaffofConnectArkansascanaccess.TheinsightscontainedwithinthiseSBreportshouldbeusedasaguidefordevelopinganoverallbroadbandutilizationstrategy.Thereportisorganizedintothefollowingsections:

• IntroductionandMethodologyOverview–Abriefdescriptionofthebenchmarkinginitiative,anoverviewofthekeymethodsused,andscopeofresearchandanalysis.

• KeyFindings–SummaryandhighlightsfromdataprovidedbyArkansasbusinesses.

• BenchmarksforAnalysisofInternetUtilization–Asabenchmarkingprocess,SNGhascreated

theDigitalEconomyIndex(DEi)tocompareInternetusebetweengroupsbyvariouscharacteristics,suchasindustry,businesssize,andgeographiclocation.Benchmarkscreatereferencepointsagainstwhichtheperformanceofanyestablishmentorgroupcanbecompared.

• MethodologyOverview–Thecoremethodologyisfoundedonprimaryresearchconsistingof

datacollectionthroughanonlineself-assessmentofbothcommercialandnon-commercialorganizations.InformationwascollecteddirectlyfromInternetusersinthefollowingcategories:userprofile,Internetutilization,InternetbenefitsandbarrierstoInternetuse.

Theorganizationalassessmentsweremadeavailableforonlineaccessthroughoneoftwomeans:

• Individualbusinessesandnon-commercialorganizations2wereinvitedtoparticipateviadirectemailinvitationssentfromalarge,statewidecontactlist.

2Thisreportcategorizesorganizationsintofourareas:businesses,non-profitorganizations,andgovernmententities.Theterm“non-commercialorganizations”includesbothnon-profitorganizationsandgovernmententities.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page7of36

• Businessesandnon-commercialorganizationswereencouragedthroughavarietyofcommunicationschannelstoaccessaweblinktotheonlineassessment.

Emailinvitationsweresentdirectlyto34,300organizationsacrossArkansas,providingaccesstotheonlineassessment.TheinitialemailinvitationwassentonNovember20th,2014andreminderemailsweresentroughlyeverysevendayswiththeassessmentsprocessclosingonFebruary18th,2015.Atotalof1,532organizationscontributedtothebroadbandbenchmarkingeffort.Theorganizationsconsistedof1,236commercialbusinesses,95governmententitiesand201non-profitorganizations.ThiseSolutionsBenchmarkingReportprovidesaveryusefuloverviewofInternetconnectivityandutilizationcharacteristicsinArkansas.AdditionaldatafromtheassessmentandbenchmarkingeffortisprovidedthroughtheArkansasDEAPwebsite,whichisdescribedinAppendixB.Themajorityofrespondentsfullycompletedtheassessments.However,partiallycompletedassessmentsareincludedintheanalysisonthebasisthattheresponsesprovidedarevalidandusefuleveniftherespondentchosenottocompletetheentireassessment.Therefore,everydatachartinthisreportindicatestheN=valuethatprovidesthenumberofdatapointsincludedtogenerateeachparticularfigure.FurtherdetailsonthemethodologyareprovidedinAppendixAwithabriefGlossaryofreportterminologyinAppendixB.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page8of36

IsolatedSmallTown8%

Metropolitan59%

Micropolitan22%

SmallTown11%

1 OrganizationalAssessmentAccesstoandeffectiveuseoftheInternethasbecomeanessentialelementinthesurvivalandsuccessofbothcommercialandnon-commercialorganizationsintoday’seconomyaswellassocietyasawhole.ThissectionidentifieskeyfindingsrelatedtohoworganizationsandbusinessesusetheInternet,whattypesofbenefitstheyvaluemost,andwhichbarrierspreventmoreeffectiveuse.ThereportpaysspecialattentiontoInternetusebybusinesses.Thefindingsarebrokendownbykeyrespondentcharacteristicssuchasindustrysector,employmentsizeandconnectivitytype.

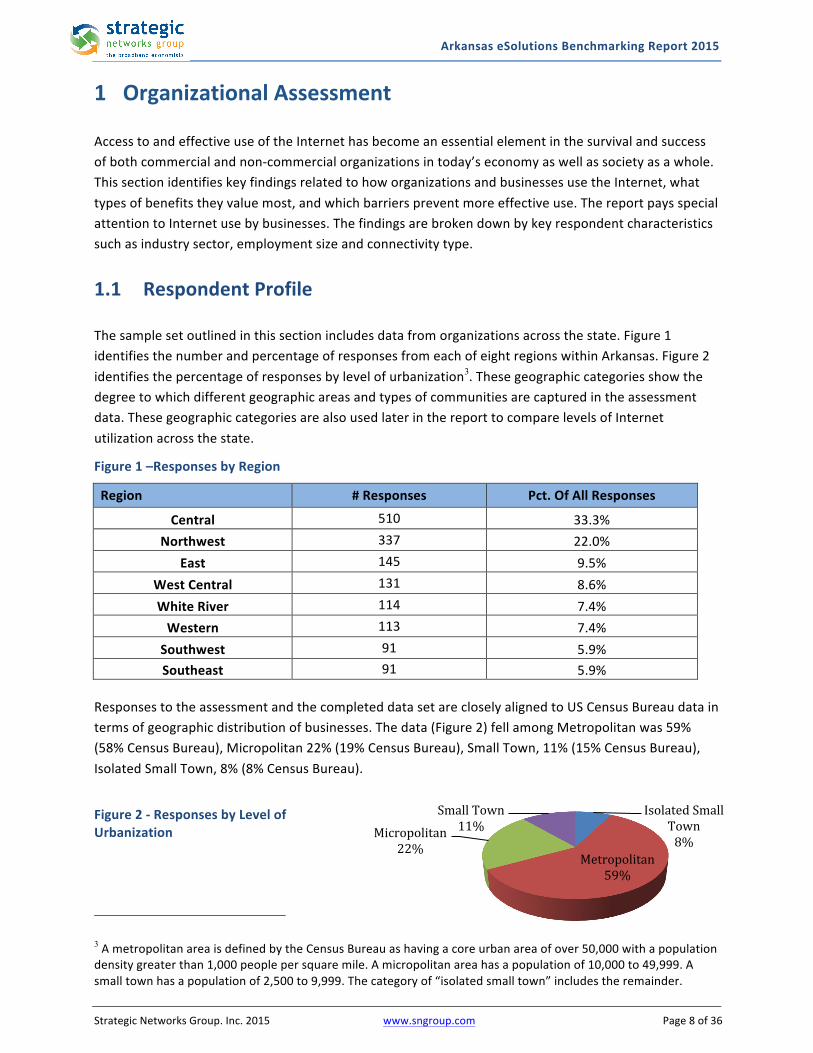

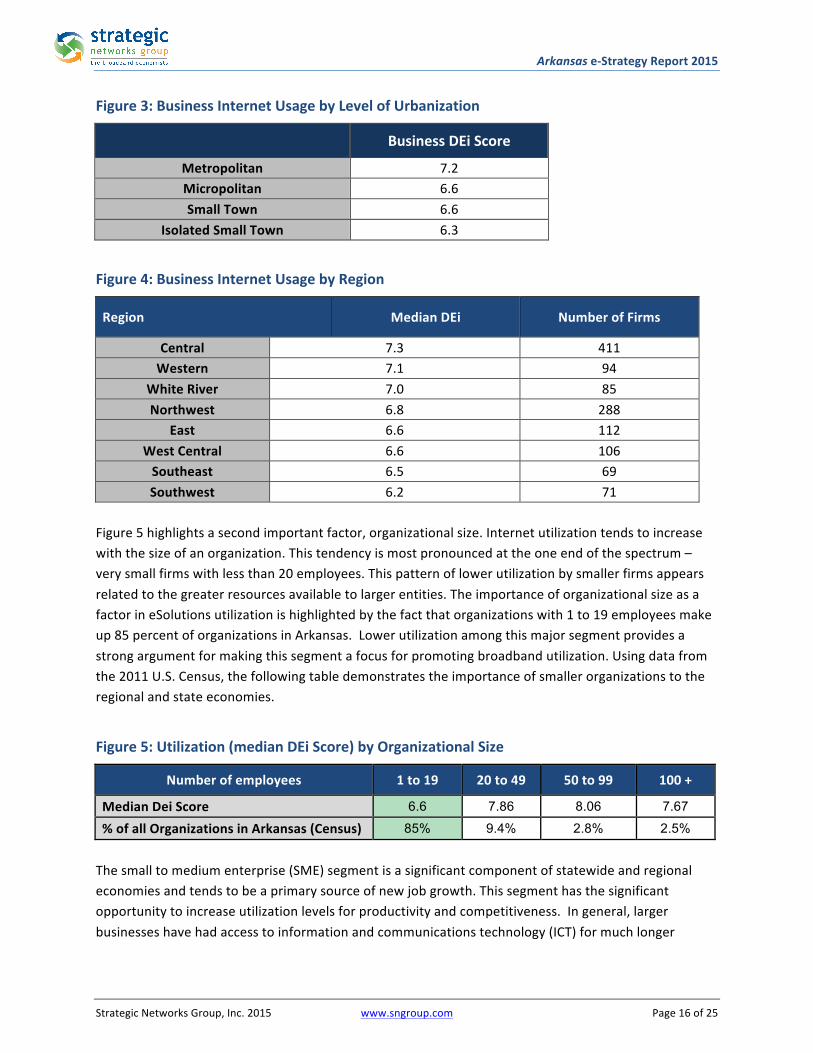

1.1 RespondentProfileThesamplesetoutlinedinthissectionincludesdatafromorganizationsacrossthestate.Figure1identifiesthenumberandpercentageofresponsesfromeachofeightregionswithinArkansas.Figure2identifiesthepercentageofresponsesbylevelofurbanization3.Thesegeographiccategoriesshowthedegreetowhichdifferentgeographicareasandtypesofcommunitiesarecapturedintheassessmentdata.ThesegeographiccategoriesarealsousedlaterinthereporttocomparelevelsofInternetutilizationacrossthestate.

Figure1–ResponsesbyRegion

Region #Responses Pct.OfAllResponses

Central 510 33.3%Northwest 337 22.0%

East 145 9.5%WestCentral 131 8.6%WhiteRiver 114 7.4%Western 113 7.4%Southwest 91 5.9%Southeast 91 5.9%

ResponsestotheassessmentandthecompleteddatasetarecloselyalignedtoUSCensusBureaudataintermsofgeographicdistributionofbusinesses.Thedata(Figure2)fellamongMetropolitanwas59%(58%CensusBureau),Micropolitan22%(19%CensusBureau),SmallTown,11%(15%CensusBureau),IsolatedSmallTown,8%(8%CensusBureau).

Figure2-ResponsesbyLevelofUrbanization

3AmetropolitanareaisdefinedbytheCensusBureauashavingacoreurbanareaofover50,000withapopulationdensitygreaterthan1,000peoplepersquaremile.Amicropolitanareahasapopulationof10,000to49,999.Asmalltownhasapopulationof2,500to9,999.Thecategoryof“isolatedsmalltown”includestheremainder.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page9of36

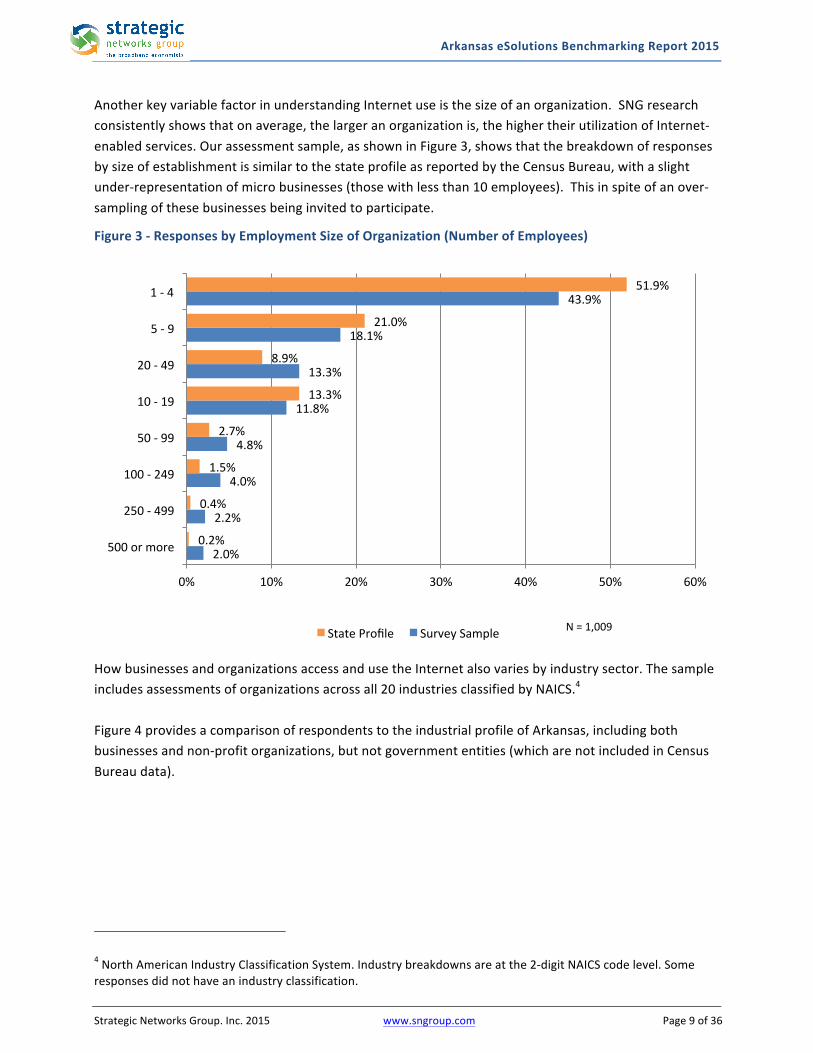

AnotherkeyvariablefactorinunderstandingInternetuseisthesizeofanorganization.SNGresearchconsistentlyshowsthatonaverage,thelargeranorganizationis,thehighertheirutilizationofInternet-enabledservices.Ourassessmentsample,asshowninFigure3,showsthatthebreakdownofresponsesbysizeofestablishmentissimilartothestateprofileasreportedbytheCensusBureau,withaslightunder-representationofmicrobusinesses(thosewithlessthan10employees).Thisinspiteofanover-samplingofthesebusinessesbeinginvitedtoparticipate.

Figure3-ResponsesbyEmploymentSizeofOrganization(NumberofEmployees)

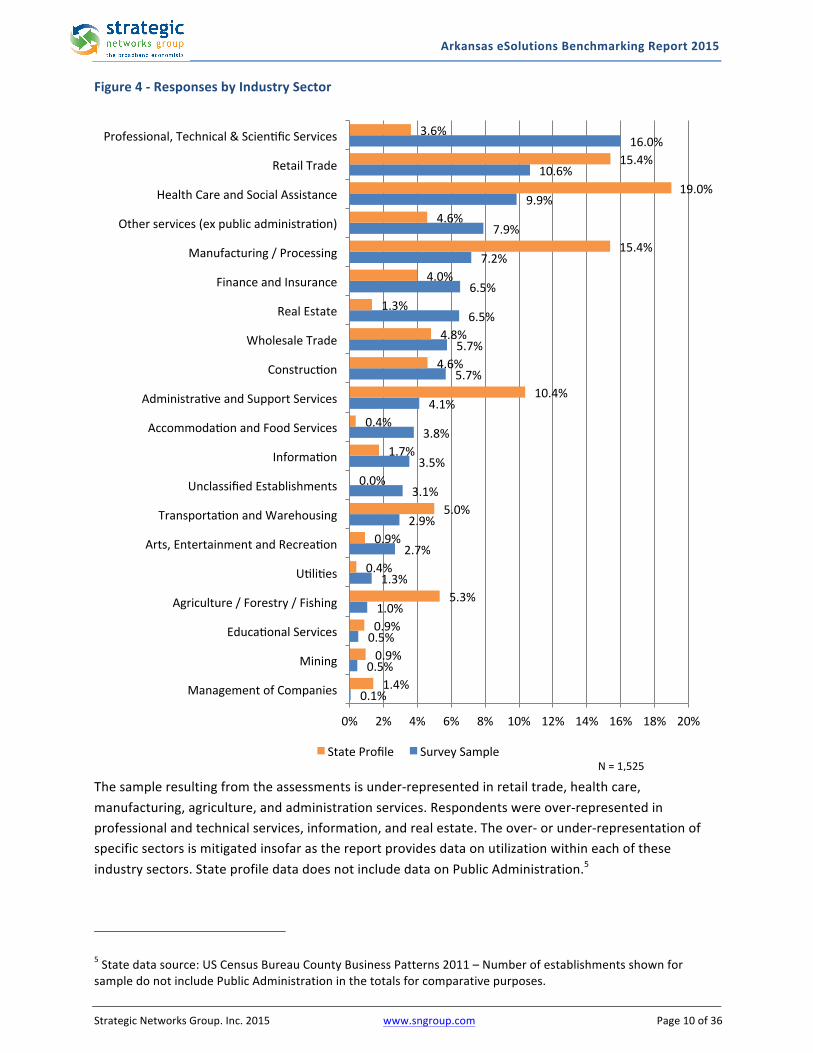

HowbusinessesandorganizationsaccessandusetheInternetalsovariesbyindustrysector.Thesampleincludesassessmentsoforganizationsacrossall20industriesclassifiedbyNAICS.4Figure4providesacomparisonofrespondentstotheindustrialprofileofArkansas,includingbothbusinessesandnon-profitorganizations,butnotgovernmententities(whicharenotincludedinCensusBureaudata).

4NorthAmericanIndustryClassificationSystem.Industrybreakdownsareatthe2-digitNAICScodelevel.Someresponsesdidnothaveanindustryclassification.

2.0%

2.2%

4.0%

4.8%

11.8%

13.3%

18.1%

43.9%

0.2%

0.4%

1.5%

2.7%

13.3%

8.9%

21.0%

51.9%

0% 10% 20% 30% 40% 50% 60%

500ormore

250-499

100-249

50-99

10-19

20-49

5-9

1-4

StateProfile SurveySample N=1,009

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page10of36

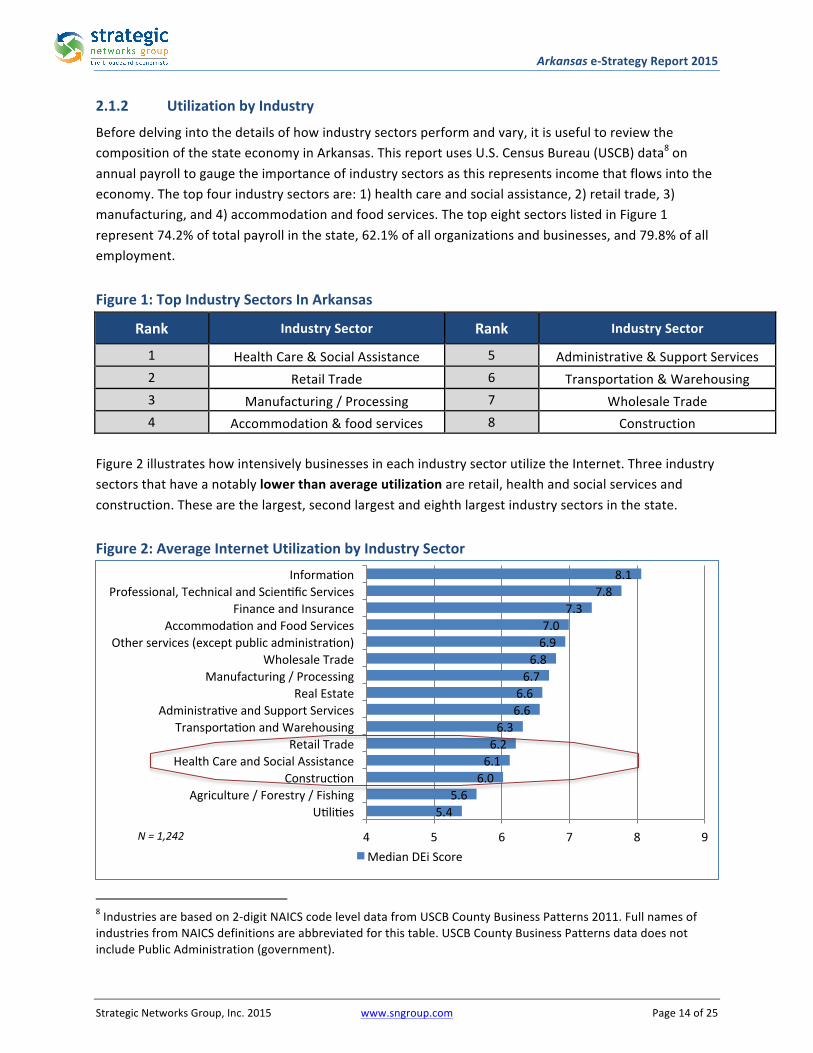

Figure4-ResponsesbyIndustrySector

Thesampleresultingfromtheassessmentsisunder-representedinretailtrade,healthcare,manufacturing,agriculture,andadministrationservices.Respondentswereover-representedinprofessionalandtechnicalservices,information,andrealestate.Theover-orunder-representationofspecificsectorsismitigatedinsofarasthereportprovidesdataonutilizationwithineachoftheseindustrysectors.StateprofiledatadoesnotincludedataonPublicAdministration.5 5Statedatasource:USCensusBureauCountyBusinessPatterns2011–NumberofestablishmentsshownforsampledonotincludePublicAdministrationinthetotalsforcomparativepurposes.

0.1%

0.5%

0.5%

1.0%

1.3%

2.7%

2.9%

3.1%

3.5%

3.8%

4.1%

5.7%

5.7%

6.5%

6.5%

7.2%

7.9%

9.9%

10.6%

16.0%

1.4%

0.9%

0.9%

5.3%

0.4%

0.9%

5.0%

0.0%

1.7%

0.4%

10.4%

4.6%

4.8%

1.3%

4.0%

15.4%

4.6%

19.0%

15.4%

3.6%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

ManagementofCompanies

Mining

EducaionalServices

Agriculture/Forestry/Fishing

Uiliies

Arts,EntertainmentandRecreaion

TransportaionandWarehousing

UnclassifiedEstablishments

Informaion

AccommodaionandFoodServices

AdministraiveandSupportServices

Construcion

WholesaleTrade

RealEstate

FinanceandInsurance

Manufacturing/Processing

Otherservices(expublicadministraion)

HealthCareandSocialAssistance

RetailTrade

Professional,Technical&ScienificServices

StateProfile SurveySampleN=1,525

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page11of36

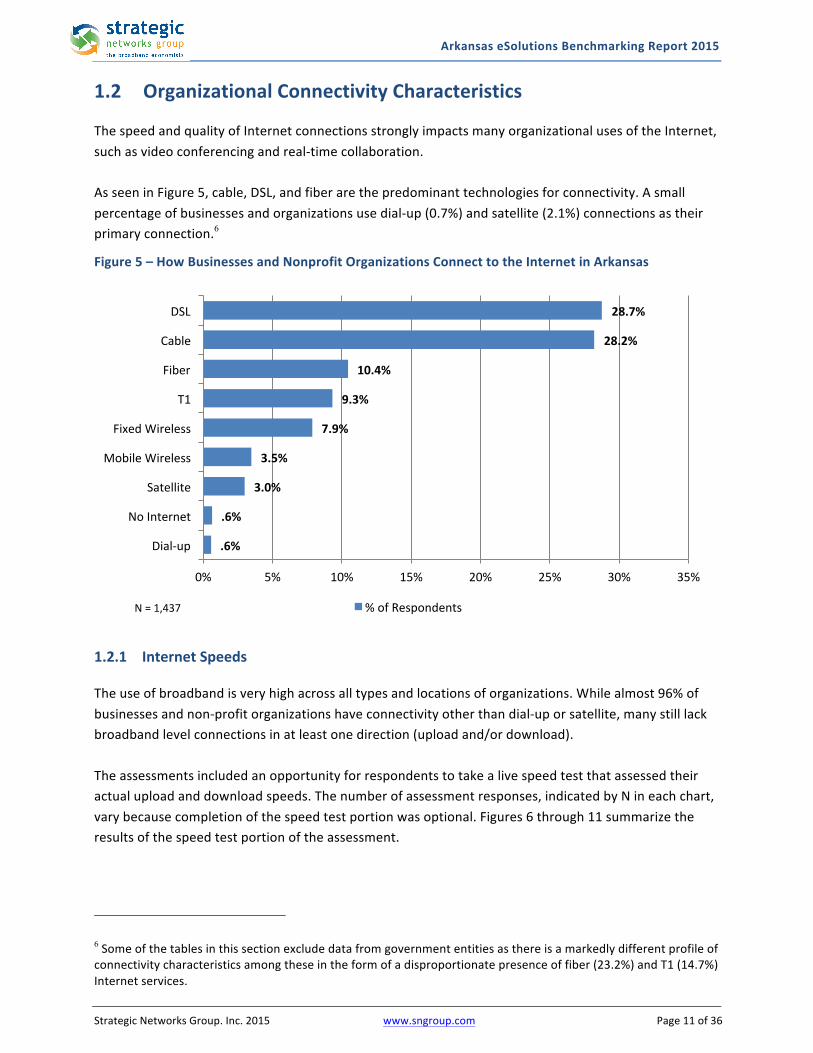

1.2 OrganizationalConnectivityCharacteristics ThespeedandqualityofInternetconnectionsstronglyimpactsmanyorganizationalusesoftheInternet,suchasvideoconferencingandreal-timecollaboration.AsseeninFigure5,cable,DSL,andfiberarethepredominanttechnologiesforconnectivity.Asmallpercentageofbusinessesandorganizationsusedial-up(0.7%)andsatellite(2.1%)connectionsastheirprimaryconnection.6

Figure5–HowBusinessesandNonprofitOrganizationsConnecttotheInternetinArkansas

1.2.1 InternetSpeedsTheuseofbroadbandisveryhighacrossalltypesandlocationsoforganizations.Whilealmost96%ofbusinessesandnon-profitorganizationshaveconnectivityotherthandial-uporsatellite,manystilllackbroadbandlevelconnectionsinatleastonedirection(uploadand/ordownload).Theassessmentsincludedanopportunityforrespondentstotakealivespeedtestthatassessedtheiractualuploadanddownloadspeeds.Thenumberofassessmentresponses,indicatedbyNineachchart,varybecausecompletionofthespeedtestportionwasoptional.Figures6through11summarizetheresultsofthespeedtestportionoftheassessment.

6Someofthetablesinthissectionexcludedatafromgovernmententitiesasthereisamarkedlydifferentprofileofconnectivitycharacteristicsamongtheseintheformofadisproportionatepresenceoffiber(23.2%)andT1(14.7%)Internetservices.

.6%

.6%

3.0%

3.5%

7.9%

9.3%

10.4%

28.2%

28.7%

0% 5% 10% 15% 20% 25% 30% 35%

Dial-up

NoInternet

Satellite

MobileWireless

FixedWireless

T1

Fiber

Cable

DSL

%ofRespondentsN=1,437

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page12of36

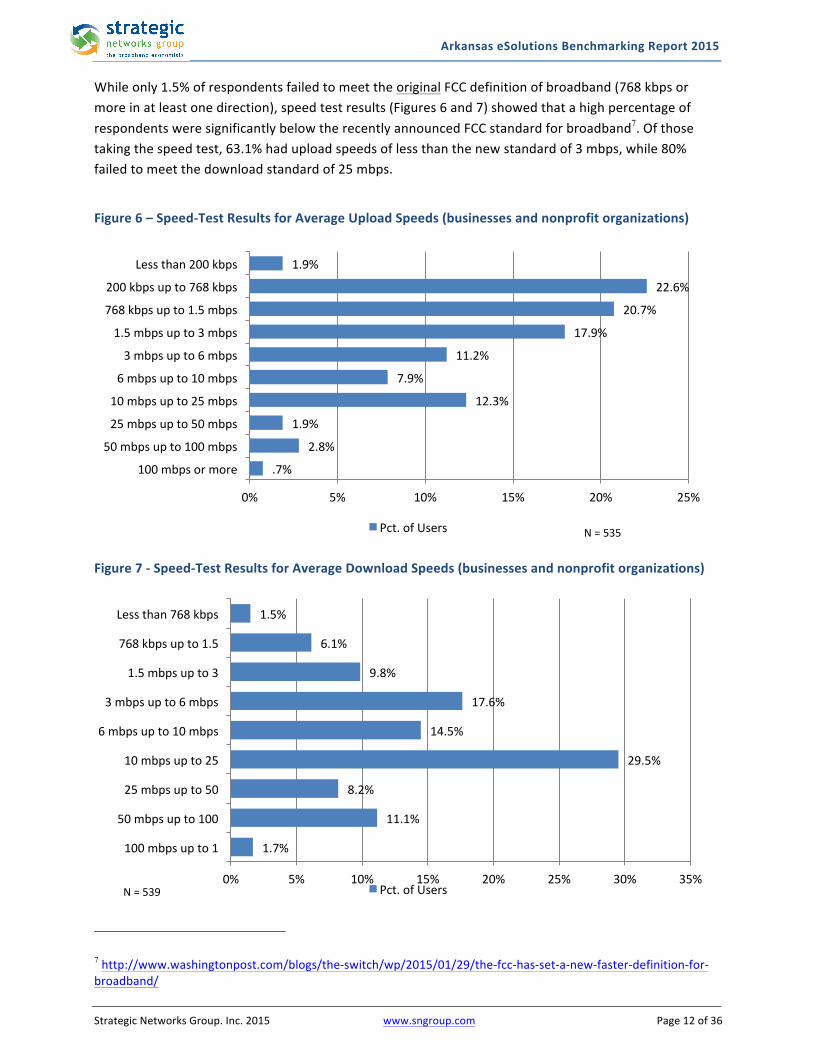

Whileonly1.5%ofrespondentsfailedtomeettheoriginalFCCdefinitionofbroadband(768kbpsormoreinatleastonedirection),speedtestresults(Figures6and7)showedthatahighpercentageofrespondentsweresignificantlybelowtherecentlyannouncedFCCstandardforbroadband7.Ofthosetakingthespeedtest,63.1%haduploadspeedsoflessthanthenewstandardof3mbps,while80%failedtomeetthedownloadstandardof25mbps.

Figure6–Speed-TestResultsforAverageUploadSpeeds(businessesandnonprofitorganizations)

Figure7-Speed-TestResultsforAverageDownloadSpeeds(businessesandnonprofitorganizations)

7http://www.washingtonpost.com/blogs/the-switch/wp/2015/01/29/the-fcc-has-set-a-new-faster-definition-for-broadband/

.7%

2.8%

1.9%

12.3%

7.9%

11.2%

17.9%

20.7%

22.6%

1.9%

0% 5% 10% 15% 20% 25%

100mbpsormore

50mbpsupto100mbps

25mbpsupto50mbps

10mbpsupto25mbps

6mbpsupto10mbps

3mbpsupto6mbps

1.5mbpsupto3mbps

768kbpsupto1.5mbps

200kbpsupto768kbps

Lessthan200kbps

Pct.ofUsers N=535

1.7%

11.1%

8.2%

29.5%

14.5%

17.6%

9.8%

6.1%

1.5%

0% 5% 10% 15% 20% 25% 30% 35%

100mbpsupto1

50mbpsupto100

25mbpsupto50

10mbpsupto25

6mbpsupto10mbps

3mbpsupto6mbps

1.5mbpsupto3

768kbpsupto1.5

Lessthan768kbps

Pct.ofUsersN=539

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page13of36

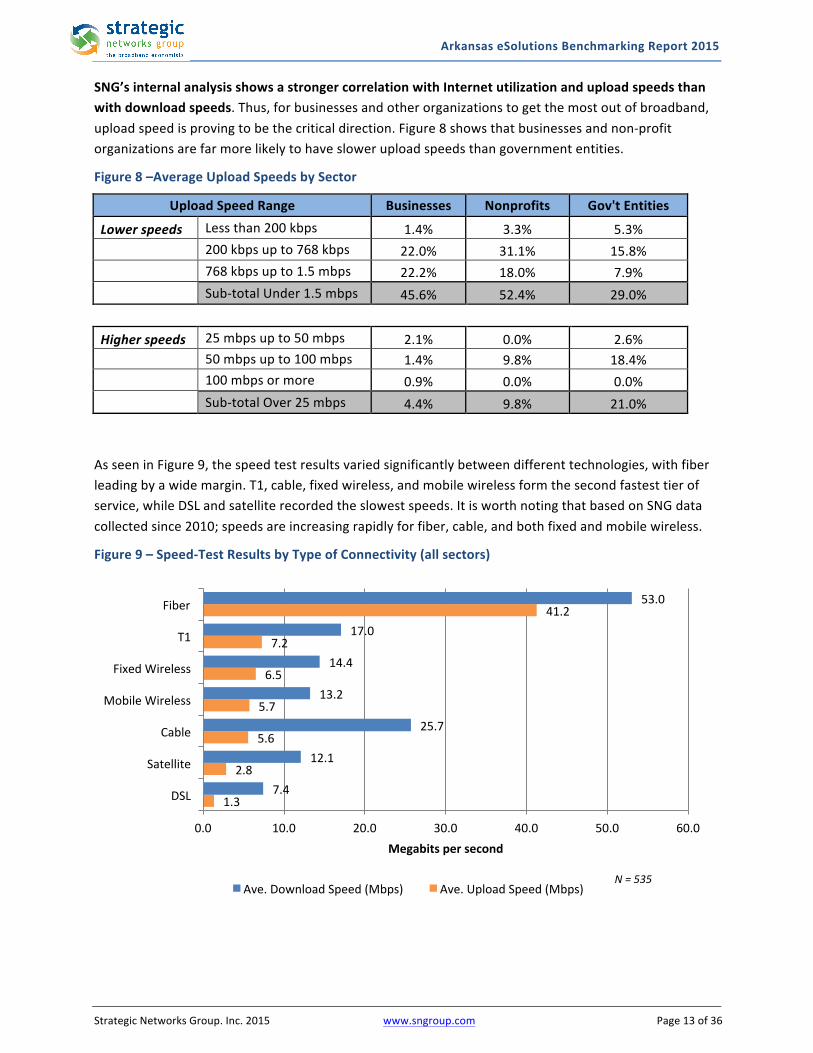

SNG’sinternalanalysisshowsastrongercorrelationwithInternetutilizationanduploadspeedsthanwithdownloadspeeds.Thus,forbusinessesandotherorganizationstogetthemostoutofbroadband,uploadspeedisprovingtobethecriticaldirection.Figure8showsthatbusinessesandnon-profitorganizationsarefarmorelikelytohavesloweruploadspeedsthangovernmententities.

Figure8–AverageUploadSpeedsbySector

UploadSpeedRange Businesses Nonprofits Gov'tEntities

Lowerspeeds Lessthan200kbps 1.4% 3.3% 5.3% 200kbpsupto768kbps 22.0% 31.1% 15.8% 768kbpsupto1.5mbps 22.2% 18.0% 7.9% Sub-totalUnder1.5mbps 45.6% 52.4% 29.0%

Higherspeeds 25mbpsupto50mbps 2.1% 0.0% 2.6% 50mbpsupto100mbps 1.4% 9.8% 18.4% 100mbpsormore 0.9% 0.0% 0.0% Sub-totalOver25mbps 4.4% 9.8% 21.0%AsseeninFigure9,thespeedtestresultsvariedsignificantlybetweendifferenttechnologies,withfiberleadingbyawidemargin.T1,cable,fixedwireless,andmobilewirelessformthesecondfastesttierofservice,whileDSLandsatelliterecordedtheslowestspeeds.ItisworthnotingthatbasedonSNGdatacollectedsince2010;speedsareincreasingrapidlyforfiber,cable,andbothfixedandmobilewireless.

Figure9–Speed-TestResultsbyTypeofConnectivity(allsectors)

1.3

2.8

5.6

5.7

6.5

7.2

41.2

7.4

12.1

25.7

13.2

14.4

17.0

53.0

0.0 10.0 20.0 30.0 40.0 50.0 60.0

DSL

Satellite

Cable

MobileWireless

FixedWireless

T1

Fiber

Megabitspersecond

Ave.DownloadSpeed(Mbps) Ave.UploadSpeed(Mbps)N=535

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page14of36

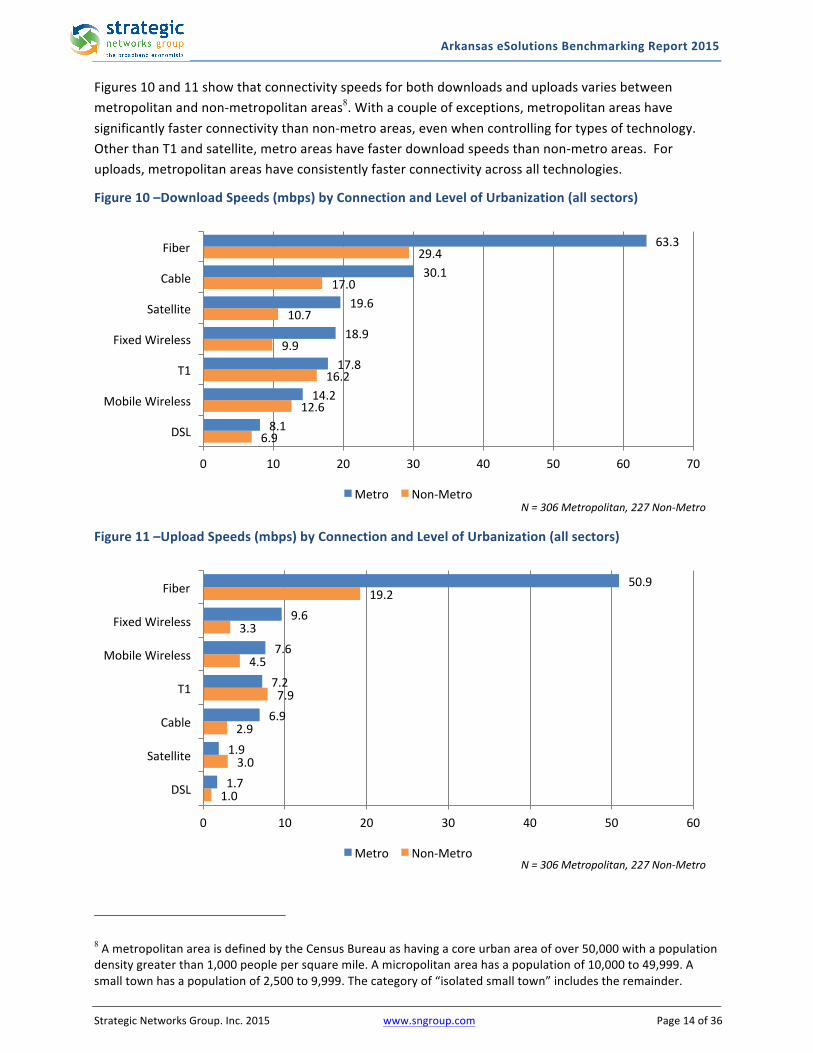

Figures10and11showthatconnectivityspeedsforbothdownloadsanduploadsvariesbetweenmetropolitanandnon-metropolitanareas8.Withacoupleofexceptions,metropolitanareashavesignificantlyfasterconnectivitythannon-metroareas,evenwhencontrollingfortypesoftechnology.OtherthanT1andsatellite,metroareashavefasterdownloadspeedsthannon-metroareas.Foruploads,metropolitanareashaveconsistentlyfasterconnectivityacrossalltechnologies.

Figure10–DownloadSpeeds(mbps)byConnectionandLevelofUrbanization(allsectors)

Figure11–UploadSpeeds(mbps)byConnectionandLevelofUrbanization(allsectors)

8AmetropolitanareaisdefinedbytheCensusBureauashavingacoreurbanareaofover50,000withapopulationdensitygreaterthan1,000peoplepersquaremile.Amicropolitanareahasapopulationof10,000to49,999.Asmalltownhasapopulationof2,500to9,999.Thecategoryof“isolatedsmalltown”includestheremainder.

6.9

12.6

16.2

9.9

10.7

17.0

29.4

8.1

14.2

17.8

18.9

19.6

30.1

63.3

0 10 20 30 40 50 60 70

DSL

MobileWireless

T1

FixedWireless

Satellite

Cable

Fiber

Metro Non-MetroN=306Metropolitan,227Non-Metro

1.0

3.0

2.9

7.9

4.5

3.3

19.2

1.7

1.9

6.9

7.2

7.6

9.6

50.9

0 10 20 30 40 50 60

DSL

Satellite

Cable

T1

MobileWireless

FixedWireless

Fiber

Metro Non-MetroN=306Metropolitan,227Non-Metro

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page15of36

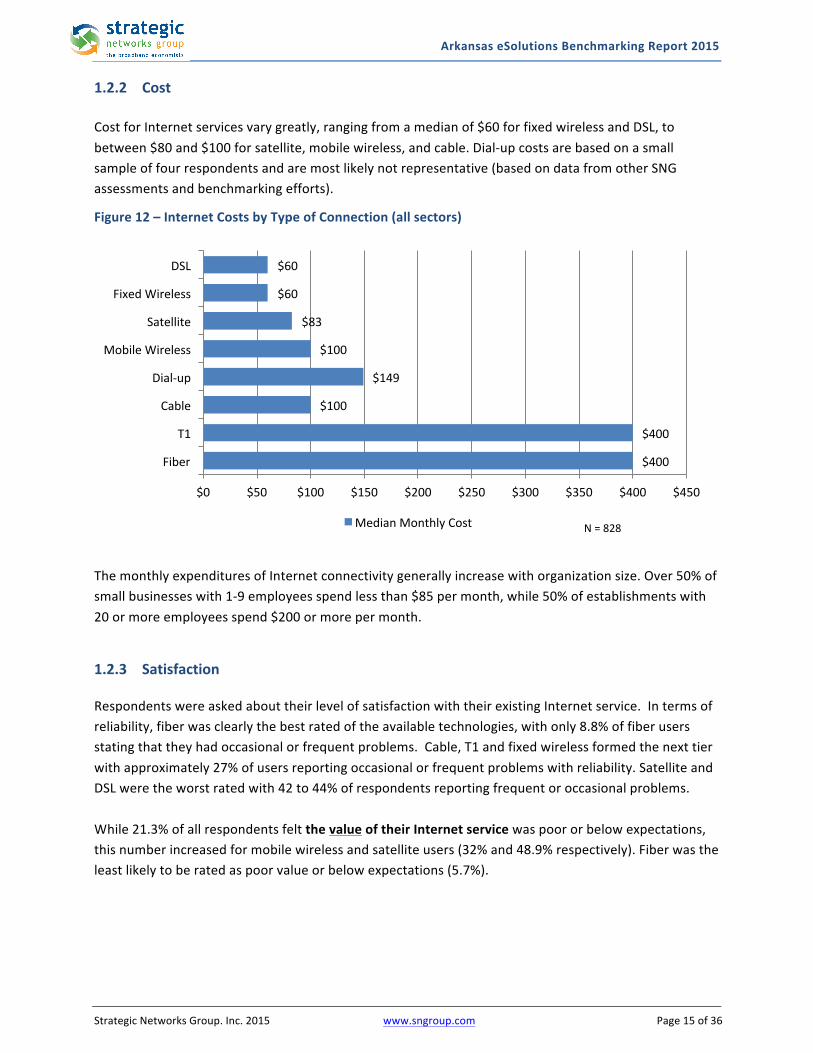

1.2.2 CostCostforInternetservicesvarygreatly,rangingfromamedianof$60forfixedwirelessandDSL,tobetween$80and$100forsatellite,mobilewireless,andcable.Dial-upcostsarebasedonasmallsampleoffourrespondentsandaremostlikelynotrepresentative(basedondatafromotherSNGassessmentsandbenchmarkingefforts).

Figure12–InternetCostsbyTypeofConnection(allsectors)

ThemonthlyexpendituresofInternetconnectivitygenerallyincreasewithorganizationsize.Over50%ofsmallbusinesseswith1-9employeesspendlessthan$85permonth,while50%ofestablishmentswith20ormoreemployeesspend$200ormorepermonth.

1.2.3 SatisfactionRespondentswereaskedabouttheirlevelofsatisfactionwiththeirexistingInternetservice.Intermsofreliability,fiberwasclearlythebestratedoftheavailabletechnologies,withonly8.8%offiberusersstatingthattheyhadoccasionalorfrequentproblems.Cable,T1andfixedwirelessformedthenexttierwithapproximately27%ofusersreportingoccasionalorfrequentproblemswithreliability.SatelliteandDSLweretheworstratedwith42to44%ofrespondentsreportingfrequentoroccasionalproblems.While21.3%ofallrespondentsfeltthevalueoftheirInternetservicewaspoororbelowexpectations,thisnumberincreasedformobilewirelessandsatelliteusers(32%and48.9%respectively).Fiberwastheleastlikelytoberatedaspoorvalueorbelowexpectations(5.7%).

$400

$400

$100

$149

$100

$83

$60

$60

$0 $50 $100 $150 $200 $250 $300 $350 $400 $450

Fiber

T1

Cable

Dial-up

MobileWireless

Satellite

FixedWireless

DSL

MedianMonthlyCost N=828

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page16of36

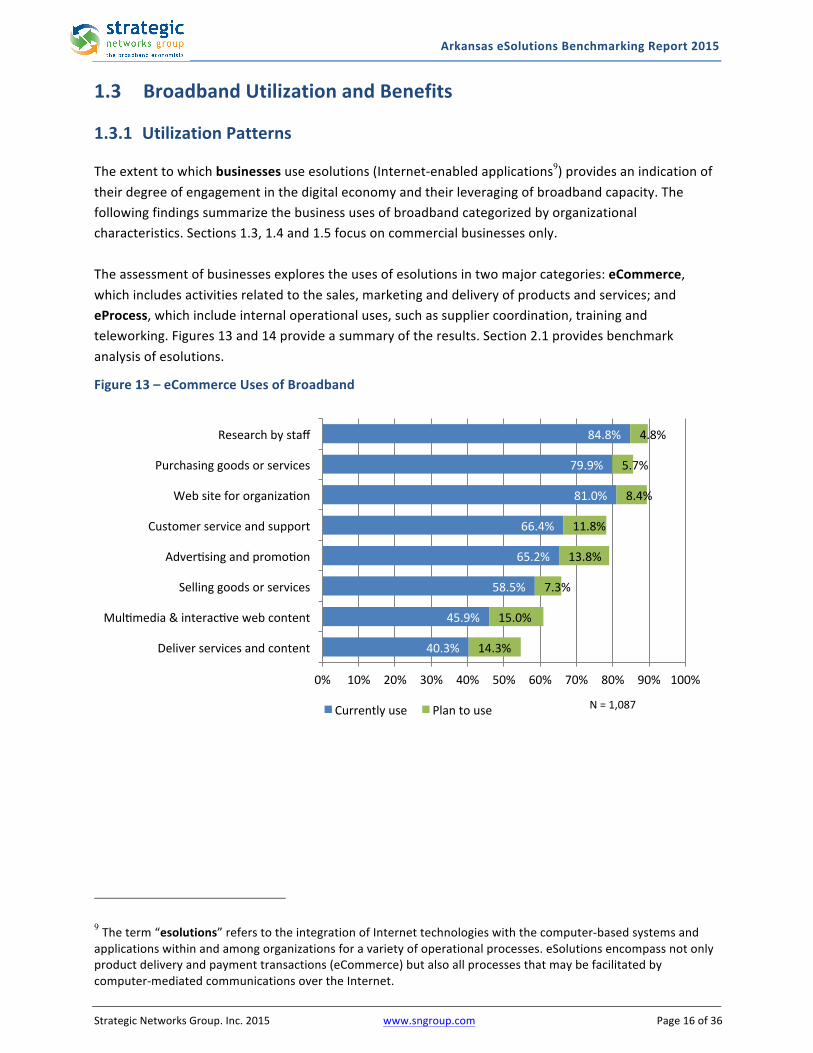

1.3 BroadbandUtilizationandBenefits1.3.1 UtilizationPatternsTheextenttowhichbusinessesuseesolutions(Internet-enabledapplications9)providesanindicationoftheirdegreeofengagementinthedigitaleconomyandtheirleveragingofbroadbandcapacity.Thefollowingfindingssummarizethebusinessusesofbroadbandcategorizedbyorganizationalcharacteristics.Sections1.3,1.4and1.5focusoncommercialbusinessesonly.Theassessmentofbusinessesexplorestheusesofesolutionsintwomajorcategories:eCommerce,whichincludesactivitiesrelatedtothesales,marketinganddeliveryofproductsandservices;andeProcess,whichincludeinternaloperationaluses,suchassuppliercoordination,trainingandteleworking.Figures13and14provideasummaryoftheresults.Section2.1providesbenchmarkanalysisofesolutions.

Figure13–eCommerceUsesofBroadband

9Theterm“esolutions”referstotheintegrationofInternettechnologieswiththecomputer-basedsystemsandapplicationswithinandamongorganizationsforavarietyofoperationalprocesses.eSolutionsencompassnotonlyproductdeliveryandpaymenttransactions(eCommerce)butalsoallprocessesthatmaybefacilitatedbycomputer-mediatedcommunicationsovertheInternet.

40.3%

45.9%

58.5%

65.2%

66.4%

81.0%

79.9%

84.8%

14.3%

15.0%

7.3%

13.8%

11.8%

8.4%

5.7%

4.8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Deliverservicesandcontent

Mulimedia&interacivewebcontent

Sellinggoodsorservices

Adverisingandpromoion

Customerserviceandsupport

Websitefororganizaion

Purchasinggoodsorservices

Researchbystaff

Currentlyuse Plantouse N=1,087

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page17of36

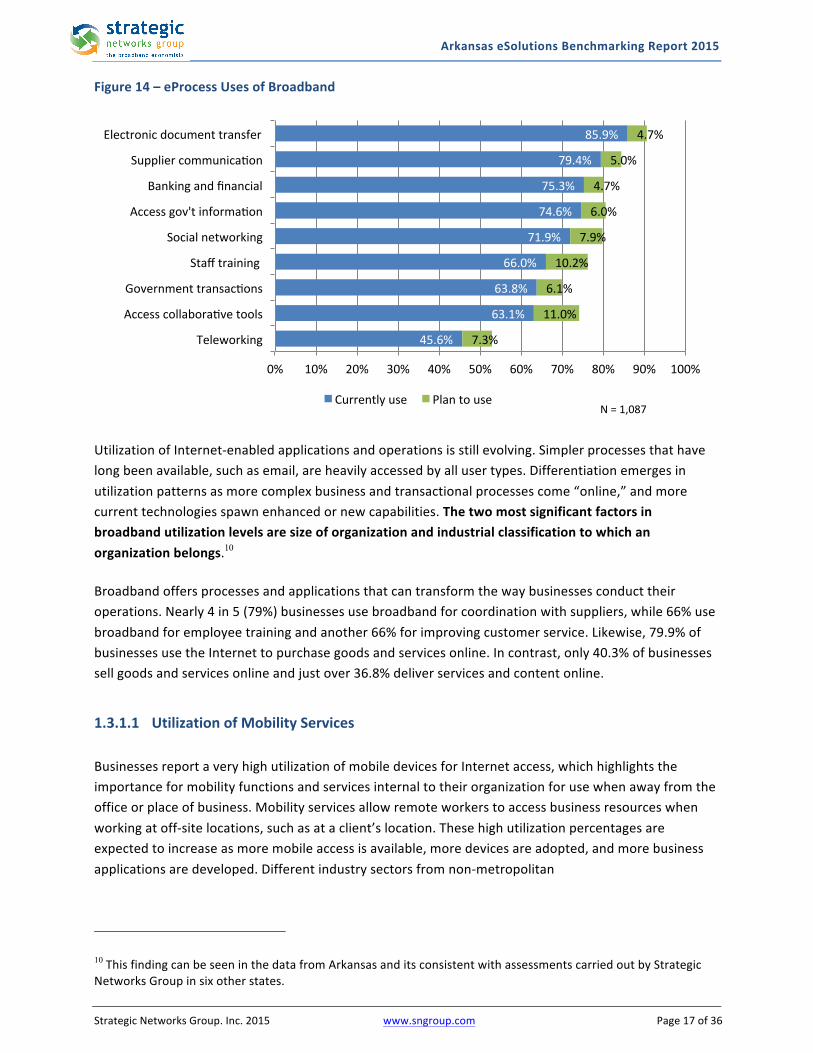

Figure14–eProcessUsesofBroadband

UtilizationofInternet-enabledapplicationsandoperationsisstillevolving.Simplerprocessesthathavelongbeenavailable,suchasemail,areheavilyaccessedbyallusertypes.Differentiationemergesinutilizationpatternsasmorecomplexbusinessandtransactionalprocessescome“online,”andmorecurrenttechnologiesspawnenhancedornewcapabilities.Thetwomostsignificantfactorsinbroadbandutilizationlevelsaresizeoforganizationandindustrialclassificationtowhichanorganizationbelongs.10Broadbandoffersprocessesandapplicationsthatcantransformthewaybusinessesconducttheiroperations.Nearly4in5(79%)businessesusebroadbandforcoordinationwithsuppliers,while66%usebroadbandforemployeetrainingandanother66%forimprovingcustomerservice.Likewise,79.9%ofbusinessesusetheInternettopurchasegoodsandservicesonline.Incontrast,only40.3%ofbusinessessellgoodsandservicesonlineandjustover36.8%deliverservicesandcontentonline.

1.3.1.1 UtilizationofMobilityServicesBusinessesreportaveryhighutilizationofmobiledevicesforInternetaccess,whichhighlightstheimportanceformobilityfunctionsandservicesinternaltotheirorganizationforusewhenawayfromtheofficeorplaceofbusiness.Mobilityservicesallowremoteworkerstoaccessbusinessresourceswhenworkingatoff-sitelocations,suchasataclient’slocation.Thesehighutilizationpercentagesareexpectedtoincreaseasmoremobileaccessisavailable,moredevicesareadopted,andmorebusinessapplicationsaredeveloped.Differentindustrysectorsfromnon-metropolitan

10ThisfindingcanbeseeninthedatafromArkansasanditsconsistentwithassessmentscarriedoutbyStrategicNetworksGroupinsixotherstates.

45.6%

63.1%

63.8%

66.0%

71.9%

74.6%

75.3%

79.4%

85.9%

7.3%

11.0%

6.1%

10.2%

7.9%

6.0%

4.7%

5.0%

4.7%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Teleworking

Accesscollaboraivetools

Governmenttransacions

Stafftraining

Socialnetworking

Accessgov'tinformaion

Bankingandfinancial

Suppliercommunicaion

Electronicdocumenttransfer

Currentlyuse PlantouseN=1,087

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page18of36

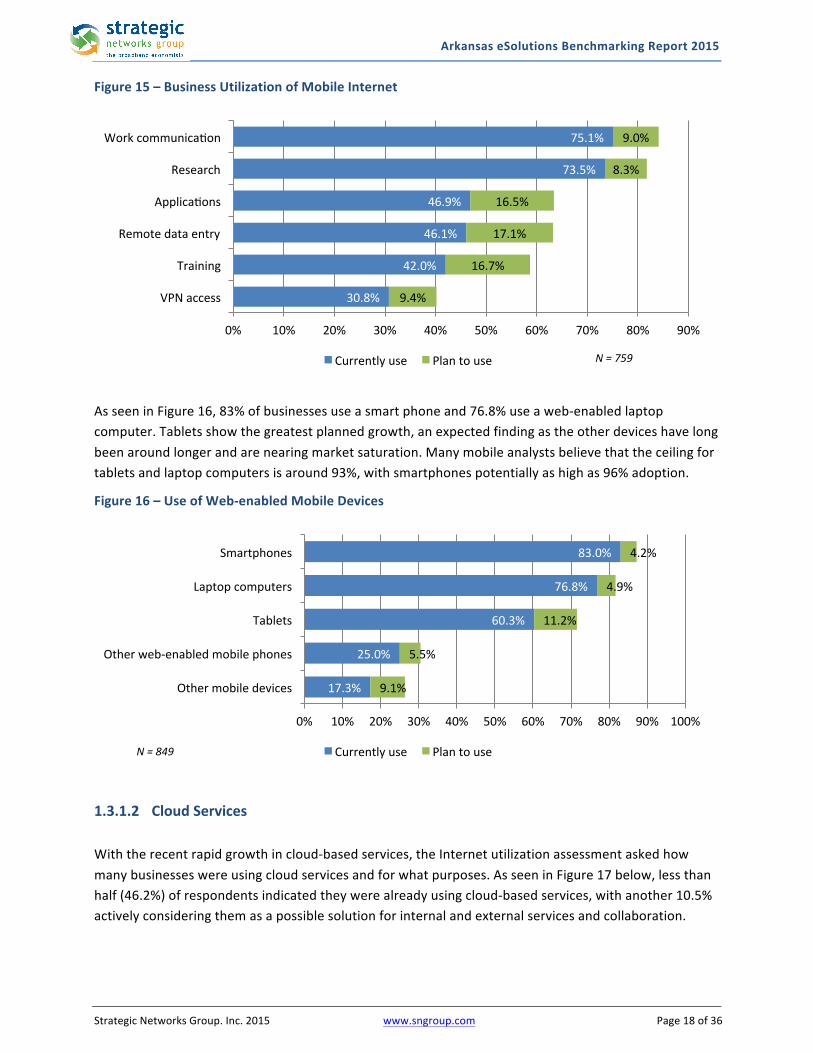

Figure15–BusinessUtilizationofMobileInternet

AsseeninFigure16,83%ofbusinessesuseasmartphoneand76.8%useaweb-enabledlaptopcomputer.Tabletsshowthegreatestplannedgrowth,anexpectedfindingastheotherdeviceshavelongbeenaroundlongerandarenearingmarketsaturation.Manymobileanalystsbelievethattheceilingfortabletsandlaptopcomputersisaround93%,withsmartphonespotentiallyashighas96%adoption.

Figure16–UseofWeb-enabledMobileDevices

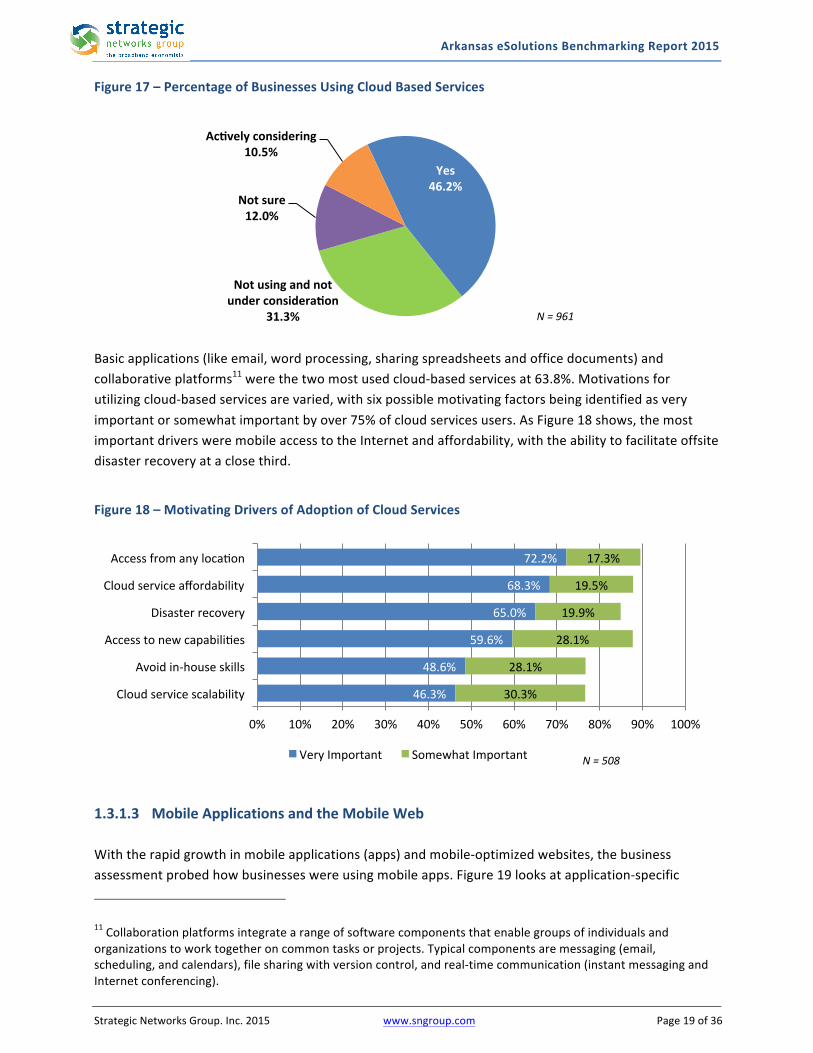

1.3.1.2 CloudServicesWiththerecentrapidgrowthincloud-basedservices,theInternetutilizationassessmentaskedhowmanybusinesseswereusingcloudservicesandforwhatpurposes.AsseeninFigure17below,lessthanhalf(46.2%)ofrespondentsindicatedtheywerealreadyusingcloud-basedservices,withanother10.5%activelyconsideringthemasapossiblesolutionforinternalandexternalservicesandcollaboration.

30.8%

42.0%

46.1%

46.9%

73.5%

75.1%

9.4%

16.7%

17.1%

16.5%

8.3%

9.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

VPNaccess

Training

Remotedataentry

Applicaions

Research

Workcommunicaion

Currentlyuse Plantouse N=759

17.3%

25.0%

60.3%

76.8%

83.0%

9.1%

5.5%

11.2%

4.9%

4.2%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Othermobiledevices

Otherweb-enabledmobilephones

Tablets

Laptopcomputers

Smartphones

Currentlyuse PlantouseN=849

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page19of36

Figure17–PercentageofBusinessesUsingCloudBasedServices

Basicapplications(likeemail,wordprocessing,sharingspreadsheetsandofficedocuments)andcollaborativeplatforms11werethetwomostusedcloud-basedservicesat63.8%.Motivationsforutilizingcloud-basedservicesarevaried,withsixpossiblemotivatingfactorsbeingidentifiedasveryimportantorsomewhatimportantbyover75%ofcloudservicesusers.AsFigure18shows,themostimportantdriversweremobileaccesstotheInternetandaffordability,withtheabilitytofacilitateoffsitedisasterrecoveryataclosethird.

Figure18–MotivatingDriversofAdoptionofCloudServices

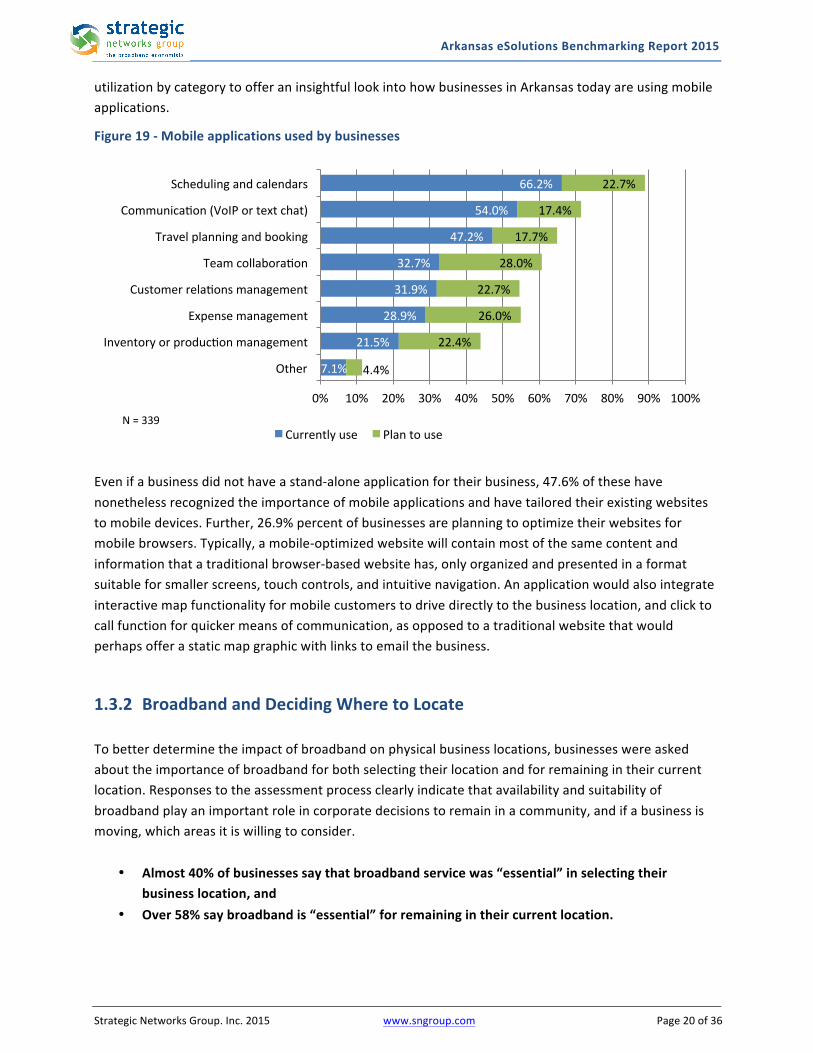

1.3.1.3 MobileApplicationsandtheMobileWebWiththerapidgrowthinmobileapplications(apps)andmobile-optimizedwebsites,thebusinessassessmentprobedhowbusinesseswereusingmobileapps.Figure19looksatapplication-specific

11Collaborationplatformsintegratearangeofsoftwarecomponentsthatenablegroupsofindividualsandorganizationstoworktogetheroncommontasksorprojects.Typicalcomponentsaremessaging(email,scheduling,andcalendars),filesharingwithversioncontrol,andreal-timecommunication(instantmessagingandInternetconferencing).

Yes46.2%

Notusingandnotunderconsideradon

31.3%

Notsure12.0%

Acdvelyconsidering10.5%

N=961

46.3%

48.6%

59.6%

65.0%

68.3%

72.2%

30.3%

28.1%

28.1%

19.9%

19.5%

17.3%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Cloudservicescalability

Avoidin-houseskills

Accesstonewcapabiliies

Disasterrecovery

Cloudserviceaffordability

Accessfromanylocaion

VeryImportant SomewhatImportant N=508

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page20of36

utilizationbycategorytoofferaninsightfullookintohowbusinessesinArkansastodayareusingmobileapplications.

Figure19-Mobileapplicationsusedbybusinesses

Evenifabusinessdidnothaveastand-aloneapplicationfortheirbusiness,47.6%ofthesehavenonethelessrecognizedtheimportanceofmobileapplicationsandhavetailoredtheirexistingwebsitestomobiledevices.Further,26.9%percentofbusinessesareplanningtooptimizetheirwebsitesformobilebrowsers.Typically,amobile-optimizedwebsitewillcontainmostofthesamecontentandinformationthatatraditionalbrowser-basedwebsitehas,onlyorganizedandpresentedinaformatsuitableforsmallerscreens,touchcontrols,andintuitivenavigation.Anapplicationwouldalsointegrateinteractivemapfunctionalityformobilecustomerstodrivedirectlytothebusinesslocation,andclicktocallfunctionforquickermeansofcommunication,asopposedtoatraditionalwebsitethatwouldperhapsofferastaticmapgraphicwithlinkstoemailthebusiness.1.3.2 BroadbandandDecidingWheretoLocateTobetterdeterminetheimpactofbroadbandonphysicalbusinesslocations,businesseswereaskedabouttheimportanceofbroadbandforbothselectingtheirlocationandforremainingintheircurrentlocation.Responsestotheassessmentprocessclearlyindicatethatavailabilityandsuitabilityofbroadbandplayanimportantroleincorporatedecisionstoremaininacommunity,andifabusinessismoving,whichareasitiswillingtoconsider.

• Almost40%ofbusinessessaythatbroadbandservicewas“essential”inselectingtheirbusinesslocation,and

• Over58%saybroadbandis“essential”forremainingintheircurrentlocation.

7.1%

21.5%

28.9%

31.9%

32.7%

47.2%

54.0%

66.2%

4.4%

22.4%

26.0%

22.7%

28.0%

17.7%

17.4%

22.7%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Other

Inventoryorproducionmanagement

Expensemanagement

Customerrelaionsmanagement

Teamcollaboraion

Travelplanningandbooking

Communicaion(VoIPortextchat)

Schedulingandcalendars

Currentlyuse PlantouseN=339

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page21of36

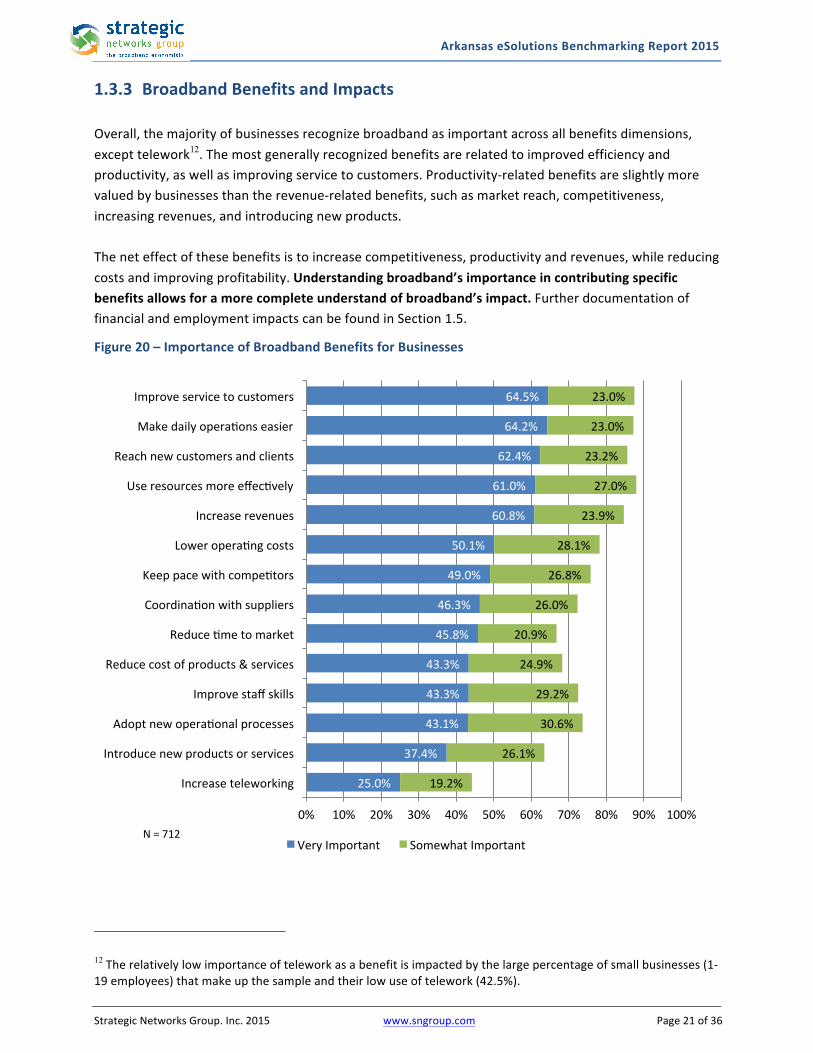

1.3.3 BroadbandBenefitsandImpactsOverall,themajorityofbusinessesrecognizebroadbandasimportantacrossallbenefitsdimensions,excepttelework12.Themostgenerallyrecognizedbenefitsarerelatedtoimprovedefficiencyandproductivity,aswellasimprovingservicetocustomers.Productivity-relatedbenefitsareslightlymorevaluedbybusinessesthantherevenue-relatedbenefits,suchasmarketreach,competitiveness,increasingrevenues,andintroducingnewproducts.Theneteffectofthesebenefitsistoincreasecompetitiveness,productivityandrevenues,whilereducingcostsandimprovingprofitability.Understandingbroadband’simportanceincontributingspecificbenefitsallowsforamorecompleteunderstandofbroadband’simpact.FurtherdocumentationoffinancialandemploymentimpactscanbefoundinSection1.5.

Figure20–ImportanceofBroadbandBenefitsforBusinesses

12Therelativelylowimportanceofteleworkasabenefitisimpactedbythelargepercentageofsmallbusinesses(1-19employees)thatmakeupthesampleandtheirlowuseoftelework(42.5%).

25.0%

37.4%

43.1%

43.3%

43.3%

45.8%

46.3%

49.0%

50.1%

60.8%

61.0%

62.4%

64.2%

64.5%

19.2%

26.1%

30.6%

29.2%

24.9%

20.9%

26.0%

26.8%

28.1%

23.9%

27.0%

23.2%

23.0%

23.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Increaseteleworking

Introducenewproductsorservices

Adoptnewoperaionalprocesses

Improvestaffskills

Reducecostofproducts&services

Reduceimetomarket

Coordinaionwithsuppliers

Keeppacewithcompeitors

Loweroperaingcosts

Increaserevenues

Useresourcesmoreeffecively

Reachnewcustomersandclients

Makedailyoperaionseasier

Improveservicetocustomers

VeryImportant SomewhatImportantN=712

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page22of36

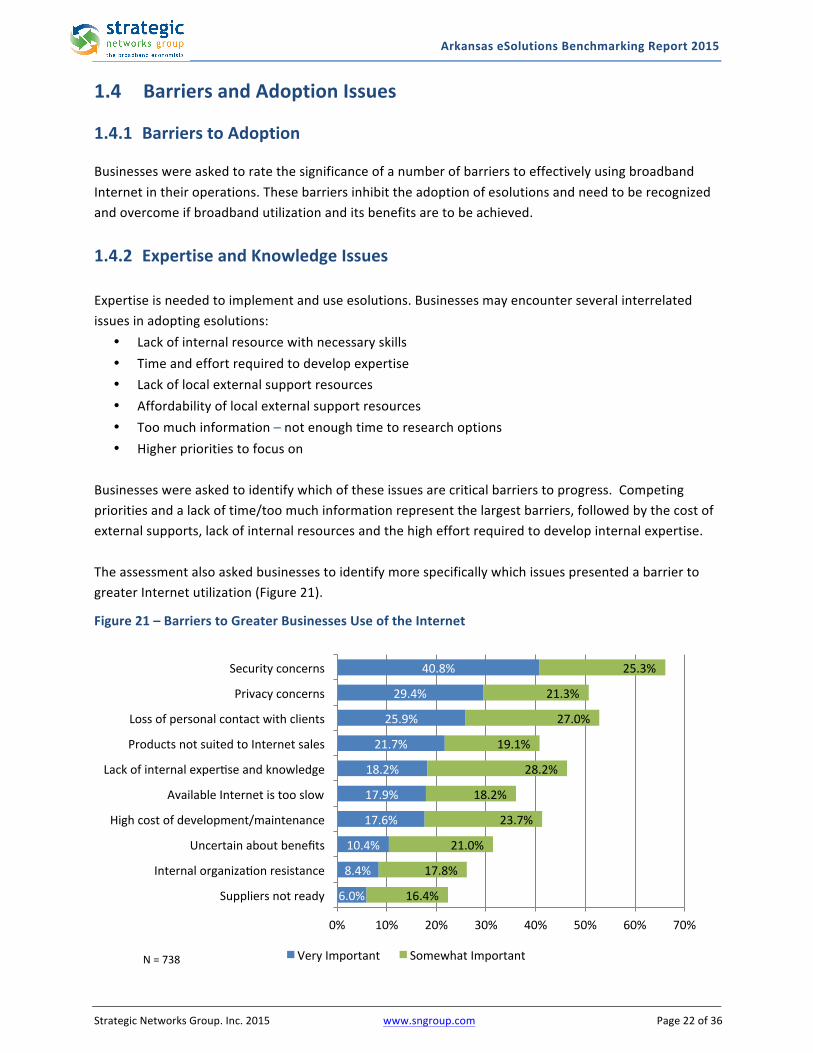

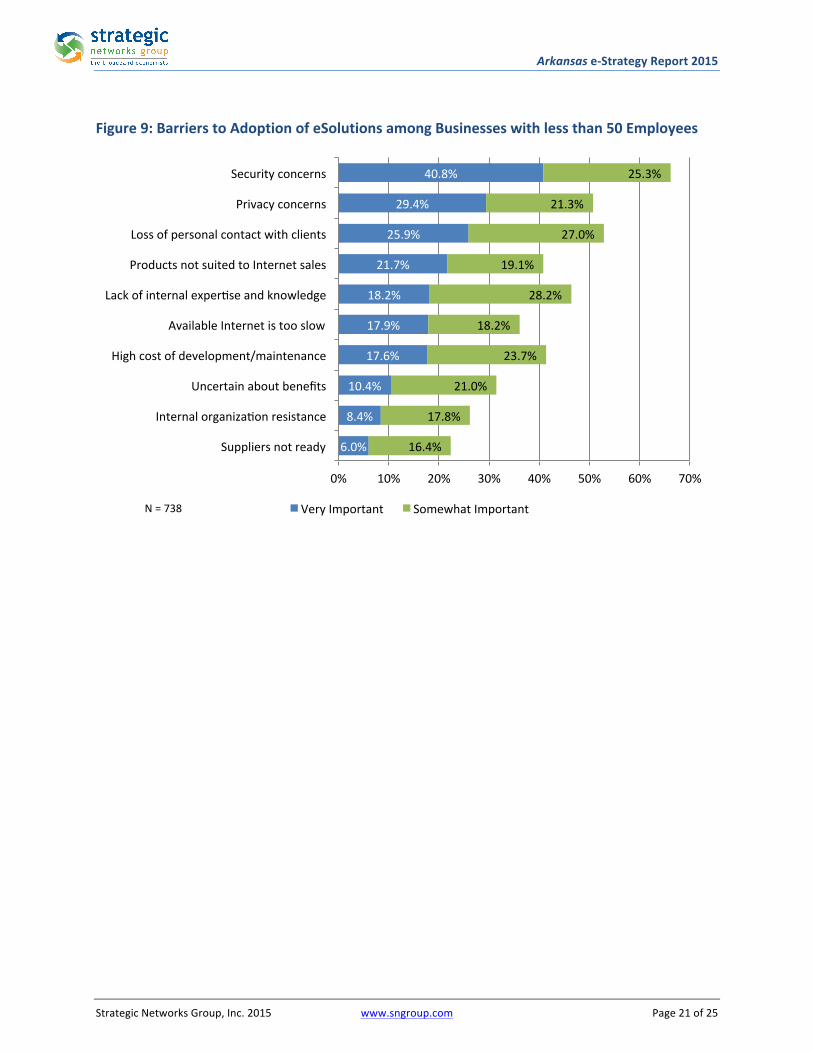

1.4 BarriersandAdoptionIssues1.4.1 BarrierstoAdoptionBusinesseswereaskedtoratethesignificanceofanumberofbarrierstoeffectivelyusingbroadbandInternetintheiroperations.Thesebarriersinhibittheadoptionofesolutionsandneedtoberecognizedandovercomeifbroadbandutilizationanditsbenefitsaretobeachieved.

1.4.2 ExpertiseandKnowledgeIssuesExpertiseisneededtoimplementanduseesolutions.Businessesmayencounterseveralinterrelatedissuesinadoptingesolutions:

• Lackofinternalresourcewithnecessaryskills• Timeandeffortrequiredtodevelopexpertise• Lackoflocalexternalsupportresources• Affordabilityoflocalexternalsupportresources• Toomuchinformation–notenoughtimetoresearchoptions• Higherprioritiestofocuson

Businesseswereaskedtoidentifywhichoftheseissuesarecriticalbarrierstoprogress.Competingprioritiesandalackoftime/toomuchinformationrepresentthelargestbarriers,followedbythecostofexternalsupports,lackofinternalresourcesandthehigheffortrequiredtodevelopinternalexpertise.TheassessmentalsoaskedbusinessestoidentifymorespecificallywhichissuespresentedabarriertogreaterInternetutilization(Figure21).

Figure21–BarrierstoGreaterBusinessesUseoftheInternet

6.0%

8.4%

10.4%

17.6%

17.9%

18.2%

21.7%

25.9%

29.4%

40.8%

16.4%

17.8%

21.0%

23.7%

18.2%

28.2%

19.1%

27.0%

21.3%

25.3%

0% 10% 20% 30% 40% 50% 60% 70%

Suppliersnotready

Internalorganizaionresistance

Uncertainaboutbenefits

Highcostofdevelopment/maintenance

AvailableInternetistooslow

Lackofinternalexperiseandknowledge

ProductsnotsuitedtoInternetsales

Lossofpersonalcontactwithclients

Privacyconcerns

Securityconcerns

VeryImportant SomewhatImportantN=738

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page23of36

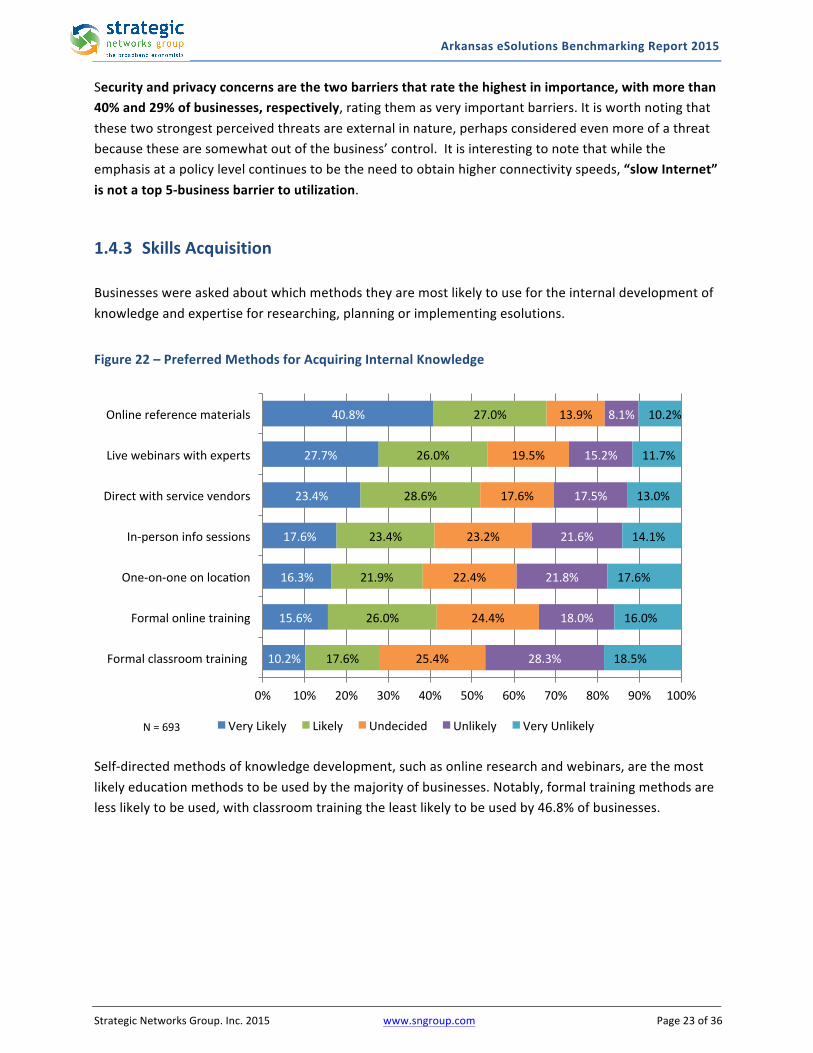

Securityandprivacyconcernsarethetwobarriersthatratethehighestinimportance,withmorethan40%and29%ofbusinesses,respectively,ratingthemasveryimportantbarriers.Itisworthnotingthatthesetwostrongestperceivedthreatsareexternalinnature,perhapsconsideredevenmoreofathreatbecausethesearesomewhatoutofthebusiness’control.Itisinterestingtonotethatwhiletheemphasisatapolicylevelcontinuestobetheneedtoobtainhigherconnectivityspeeds,“slowInternet”isnotatop5-businessbarriertoutilization.1.4.3 SkillsAcquisitionBusinesseswereaskedaboutwhichmethodstheyaremostlikelytousefortheinternaldevelopmentofknowledgeandexpertiseforresearching,planningorimplementingesolutions.

Figure22–PreferredMethodsforAcquiringInternalKnowledge

Self-directedmethodsofknowledgedevelopment,suchasonlineresearchandwebinars,arethemostlikelyeducationmethodstobeusedbythemajorityofbusinesses.Notably,formaltrainingmethodsarelesslikelytobeused,withclassroomtrainingtheleastlikelytobeusedby46.8%ofbusinesses.

10.2%

15.6%

16.3%

17.6%

23.4%

27.7%

40.8%

17.6%

26.0%

21.9%

23.4%

28.6%

26.0%

27.0%

25.4%

24.4%

22.4%

23.2%

17.6%

19.5%

13.9%

28.3%

18.0%

21.8%

21.6%

17.5%

15.2%

8.1%

18.5%

16.0%

17.6%

14.1%

13.0%

11.7%

10.2%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Formalclassroomtraining

Formalonlinetraining

One-on-oneonlocaion

In-personinfosessions

Directwithservicevendors

Livewebinarswithexperts

Onlinereferencematerials

VeryLikely Likely Undecided Unlikely VeryUnlikelyN=693

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page24of36

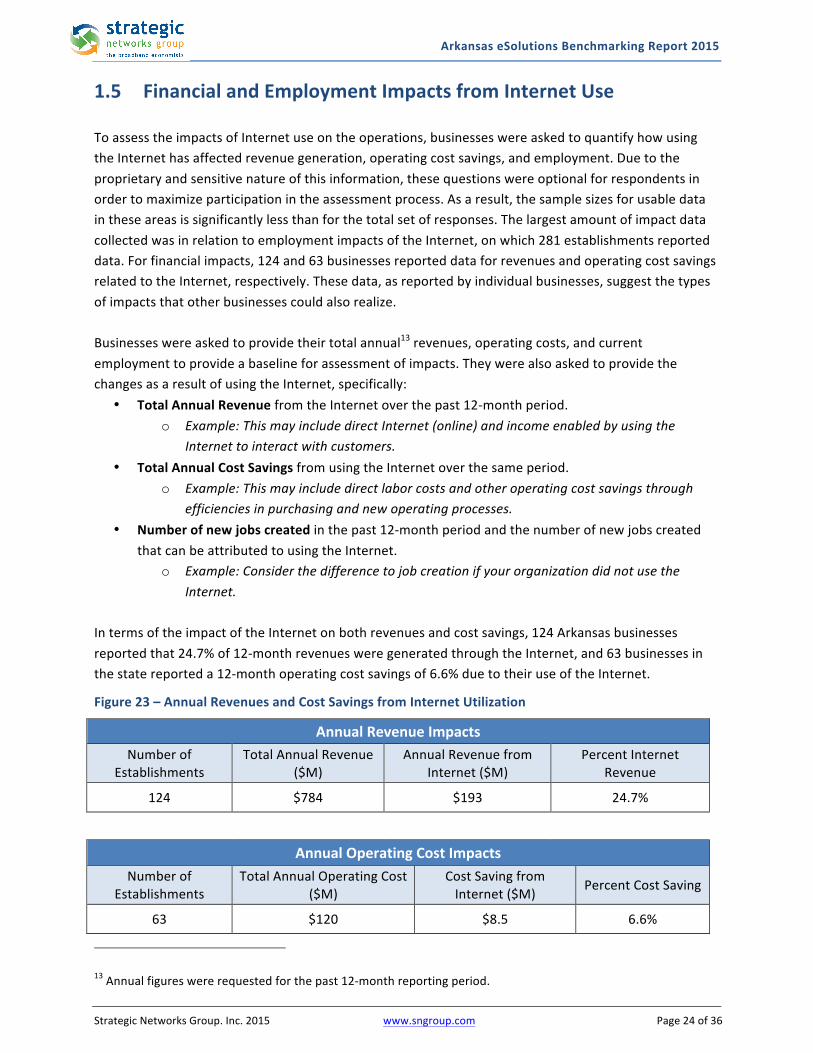

1.5 FinancialandEmploymentImpactsfromInternetUseToassesstheimpactsofInternetuseontheoperations,businesseswereaskedtoquantifyhowusingtheInternethasaffectedrevenuegeneration,operatingcostsavings,andemployment.Duetotheproprietaryandsensitivenatureofthisinformation,thesequestionswereoptionalforrespondentsinordertomaximizeparticipationintheassessmentprocess.Asaresult,thesamplesizesforusabledataintheseareasissignificantlylessthanforthetotalsetofresponses.ThelargestamountofimpactdatacollectedwasinrelationtoemploymentimpactsoftheInternet,onwhich281establishmentsreporteddata.Forfinancialimpacts,124and63businessesreporteddataforrevenuesandoperatingcostsavingsrelatedtotheInternet,respectively.Thesedata,asreportedbyindividualbusinesses,suggestthetypesofimpactsthatotherbusinessescouldalsorealize.Businesseswereaskedtoprovidetheirtotalannual13revenues,operatingcosts,andcurrentemploymenttoprovideabaselineforassessmentofimpacts.TheywerealsoaskedtoprovidethechangesasaresultofusingtheInternet,specifically:

• TotalAnnualRevenuefromtheInternetoverthepast12-monthperiod.o Example:ThismayincludedirectInternet(online)andincomeenabledbyusingthe

Internettointeractwithcustomers.• TotalAnnualCostSavingsfromusingtheInternetoverthesameperiod.

o Example:Thismayincludedirectlaborcostsandotheroperatingcostsavingsthroughefficienciesinpurchasingandnewoperatingprocesses.

• Numberofnewjobscreatedinthepast12-monthperiodandthenumberofnewjobscreatedthatcanbeattributedtousingtheInternet.

o Example:ConsiderthedifferencetojobcreationifyourorganizationdidnotusetheInternet.

IntermsoftheimpactoftheInternetonbothrevenuesandcostsavings,124Arkansasbusinessesreportedthat24.7%of12-monthrevenuesweregeneratedthroughtheInternet,and63businessesinthestatereporteda12-monthoperatingcostsavingsof6.6%duetotheiruseoftheInternet.

Figure23–AnnualRevenuesandCostSavingsfromInternetUtilization

AnnualRevenueImpactsNumberof

EstablishmentsTotalAnnualRevenue

($M)AnnualRevenuefrom

Internet($M)PercentInternet

Revenue

124 $784 $193 24.7%

AnnualOperatingCostImpacts

NumberofEstablishments

TotalAnnualOperatingCost($M)

CostSavingfromInternet($M) PercentCostSaving

63 $120 $8.5 6.6%

13Annualfigureswererequestedforthepast12-monthreportingperiod.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page25of36

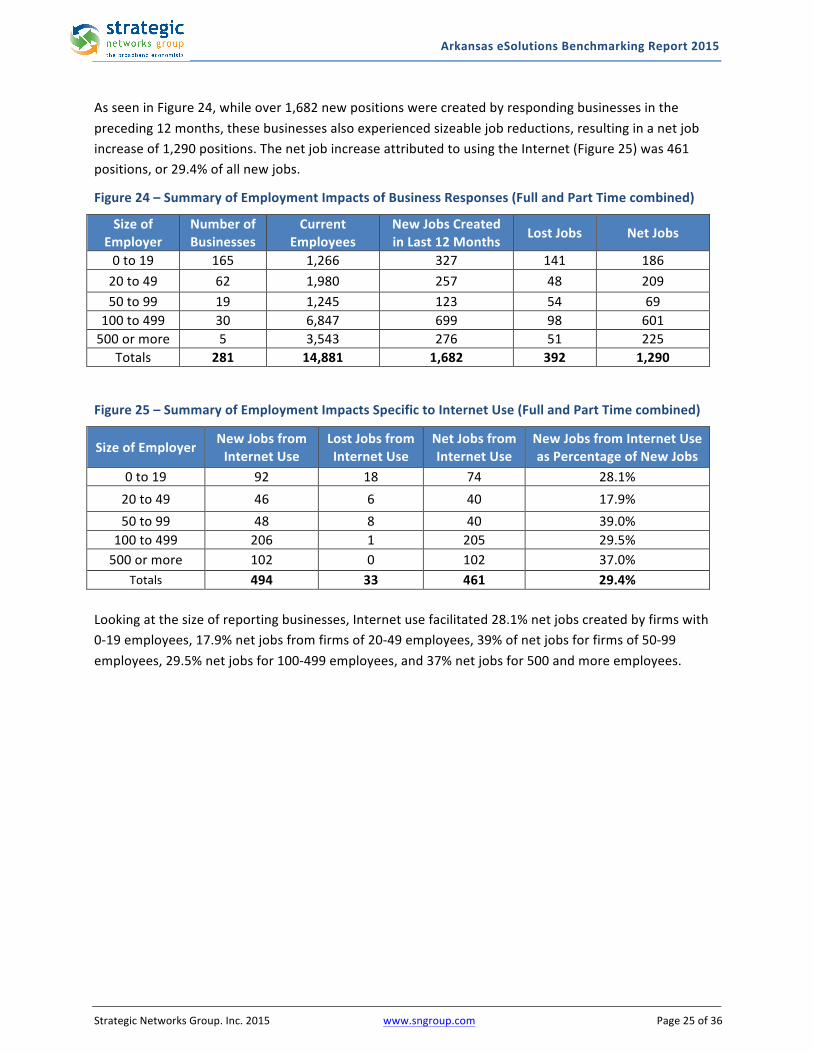

AsseeninFigure24,whileover1,682newpositionswerecreatedbyrespondingbusinessesinthepreceding12months,thesebusinessesalsoexperiencedsizeablejobreductions,resultinginanetjobincreaseof1,290positions.ThenetjobincreaseattributedtousingtheInternet(Figure25)was461positions,or29.4%ofallnewjobs.

Figure24–SummaryofEmploymentImpactsofBusinessResponses(FullandPartTimecombined)

SizeofEmployer

NumberofBusinesses

CurrentEmployees

NewJobsCreatedinLast12Months LostJobs NetJobs

0to19 165 1,266 327 141 18620to49 62 1,980 257 48 20950to99 19 1,245 123 54 69

100to499 30 6,847 699 98 601500ormore 5 3,543 276 51 225

Totals 281 14,881 1,682 392 1,290

Figure25–SummaryofEmploymentImpactsSpecifictoInternetUse(FullandPartTimecombined)

SizeofEmployer NewJobsfromInternetUse

LostJobsfromInternetUse

NetJobsfromInternetUse

NewJobsfromInternetUseasPercentageofNewJobs

0to19 92 18 74 28.1%20to49 46 6 40 17.9%50to99 48 8 40 39.0%

100to499 206 1 205 29.5%500ormore 102 0 102 37.0%

Totals 494 33 461 29.4%Lookingatthesizeofreportingbusinesses,Internetusefacilitated28.1%netjobscreatedbyfirmswith0-19employees,17.9%netjobsfromfirmsof20-49employees,39%ofnetjobsforfirmsof50-99employees,29.5%netjobsfor100-499employees,and37%netjobsfor500andmoreemployees.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page26of36

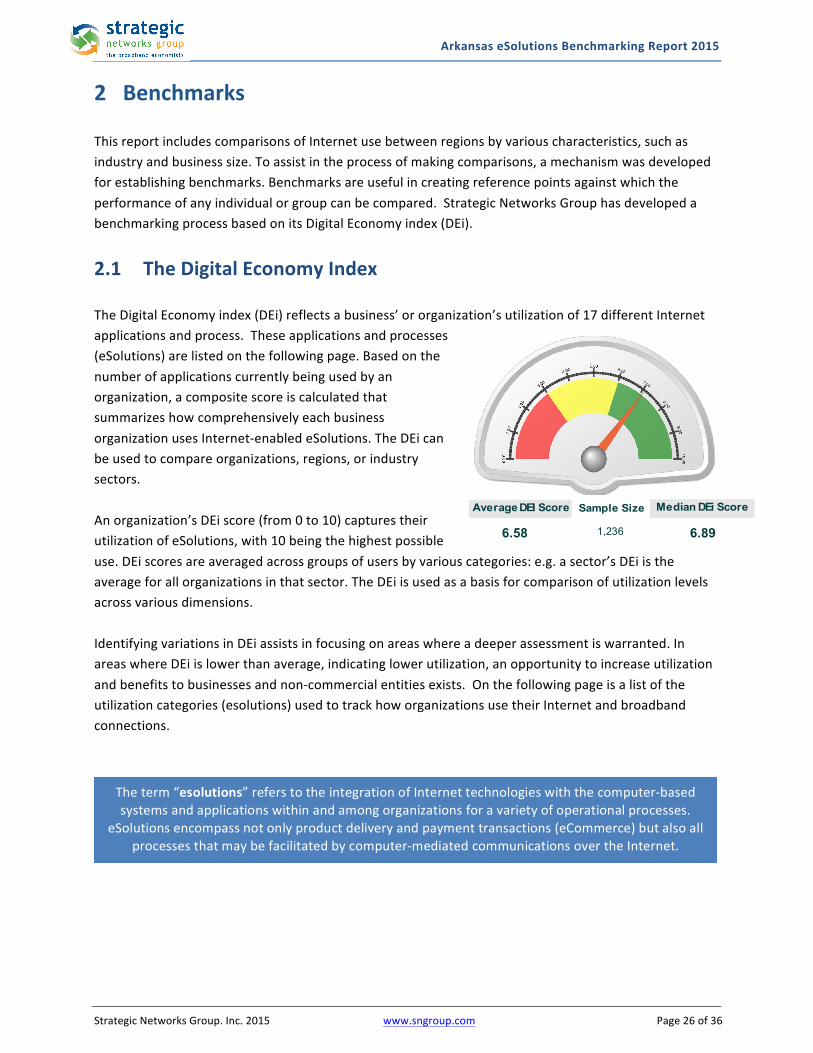

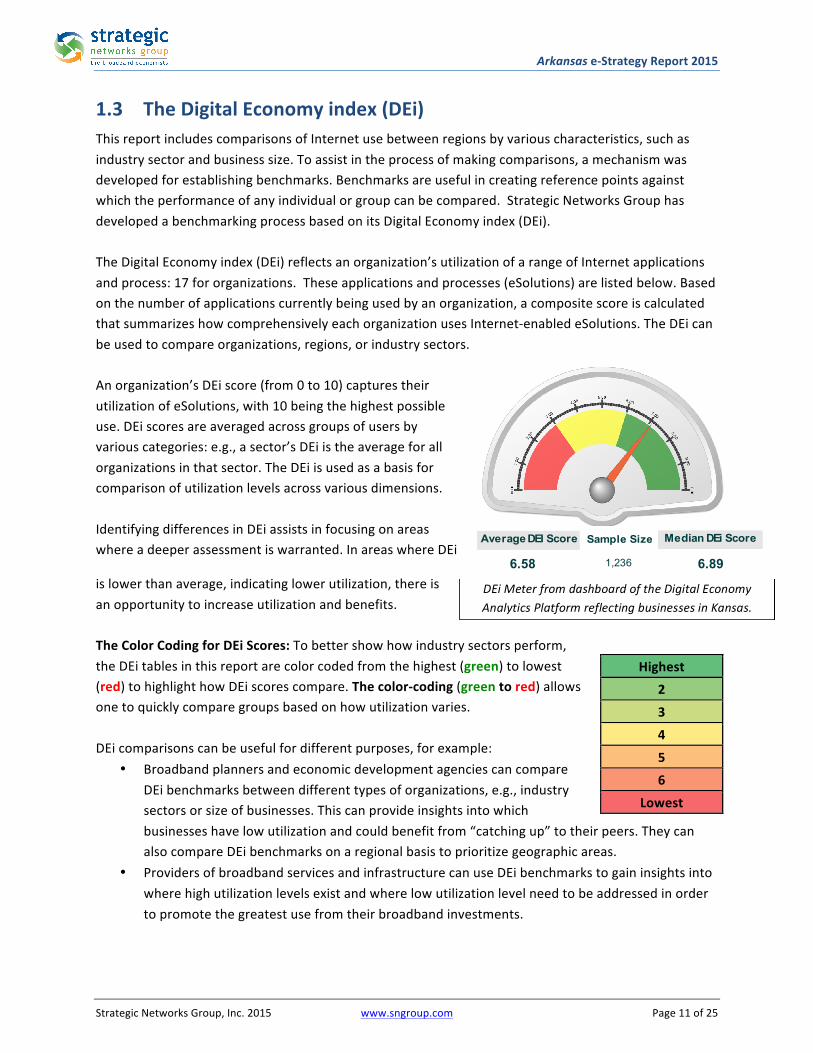

2 BenchmarksThisreportincludescomparisonsofInternetusebetweenregionsbyvariouscharacteristics,suchasindustryandbusinesssize.Toassistintheprocessofmakingcomparisons,amechanismwasdevelopedforestablishingbenchmarks.Benchmarksareusefulincreatingreferencepointsagainstwhichtheperformanceofanyindividualorgroupcanbecompared.StrategicNetworksGrouphasdevelopedabenchmarkingprocessbasedonitsDigitalEconomyindex(DEi).

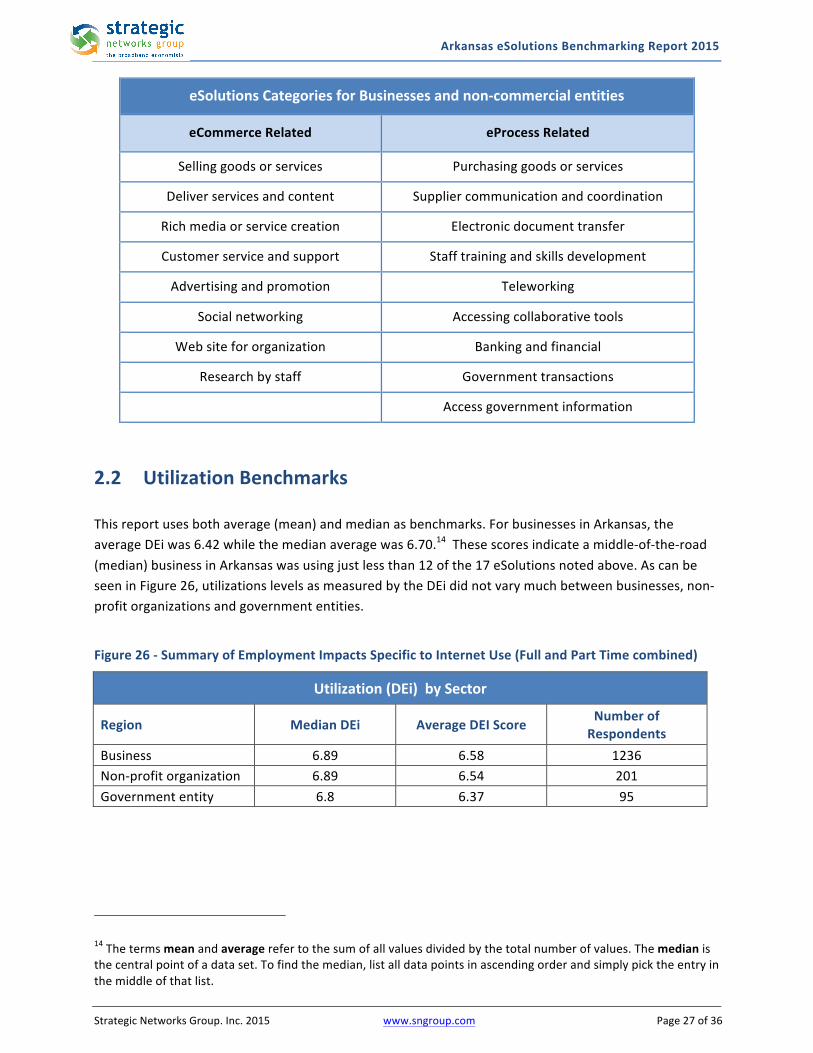

2.1 TheDigitalEconomyIndexTheDigitalEconomyindex(DEi)reflectsabusiness’ororganization’sutilizationof17differentInternetapplicationsandprocess.Theseapplicationsandprocesses(eSolutions)arelistedonthefollowingpage.Basedonthenumberofapplicationscurrentlybeingusedbyanorganization,acompositescoreiscalculatedthatsummarizeshowcomprehensivelyeachbusinessorganizationusesInternet-enabledeSolutions.TheDEicanbeusedtocompareorganizations,regions,orindustrysectors.Anorganization’sDEiscore(from0to10)capturestheirutilizationofeSolutions,with10beingthehighestpossibleuse.DEiscoresareaveragedacrossgroupsofusersbyvariouscategories:e.g.asector’sDEiistheaverageforallorganizationsinthatsector.TheDEiisusedasabasisforcomparisonofutilizationlevelsacrossvariousdimensions.IdentifyingvariationsinDEiassistsinfocusingonareaswhereadeeperassessmentiswarranted.InareaswhereDEiislowerthanaverage,indicatinglowerutilization,anopportunitytoincreaseutilizationandbenefitstobusinessesandnon-commercialentitiesexists.Onthefollowingpageisalistoftheutilizationcategories(esolutions)usedtotrackhoworganizationsusetheirInternetandbroadbandconnections.

Theterm“esolutions”referstotheintegrationofInternettechnologieswiththecomputer-basedsystemsandapplicationswithinandamongorganizationsforavarietyofoperationalprocesses.

eSolutionsencompassnotonlyproductdeliveryandpaymenttransactions(eCommerce)butalsoallprocessesthatmaybefacilitatedbycomputer-mediatedcommunicationsovertheInternet.

Average DEI Score Sample Size Median DEi Score

6.58 6.89 1,236

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page27of36

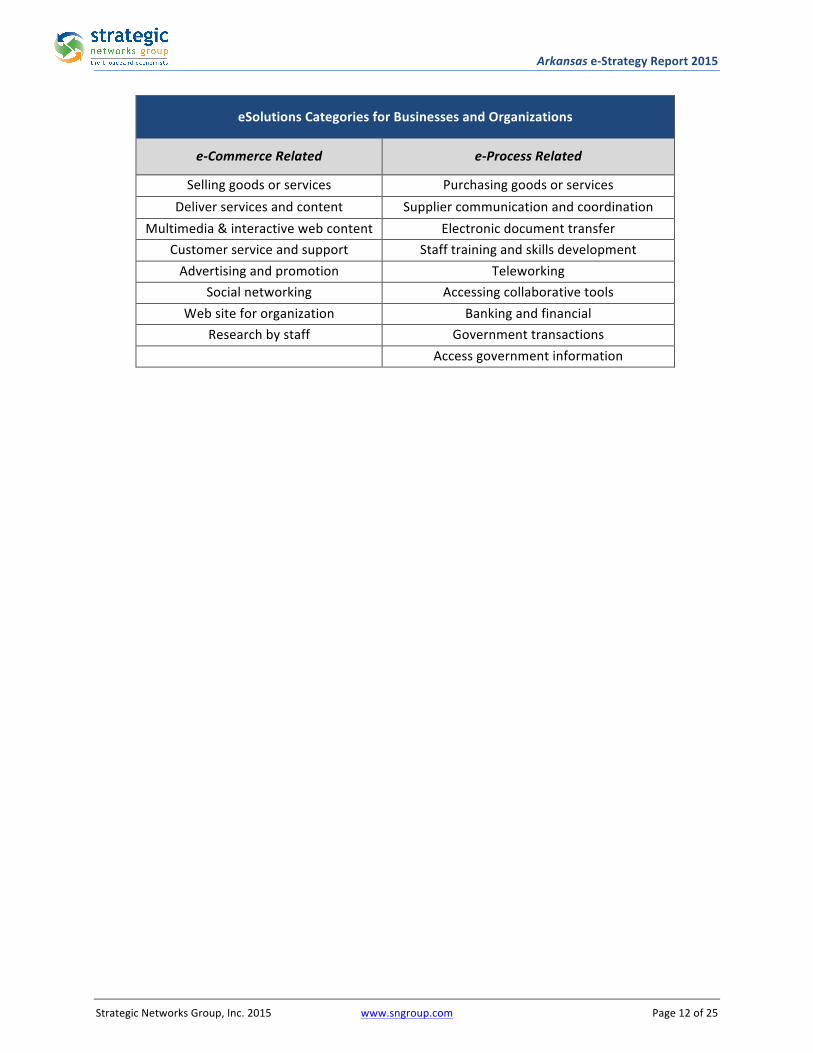

eSolutionsCategoriesforBusinessesandnon-commercialentities

eCommerceRelated eProcessRelated

Sellinggoodsorservices Purchasinggoodsorservices

Deliverservicesandcontent Suppliercommunicationandcoordination

Richmediaorservicecreation Electronicdocumenttransfer

Customerserviceandsupport Stafftrainingandskillsdevelopment

Advertisingandpromotion Teleworking

Socialnetworking Accessingcollaborativetools

Websitefororganization Bankingandfinancial

Researchbystaff Governmenttransactions

Accessgovernmentinformation

2.2 UtilizationBenchmarksThisreportusesbothaverage(mean)andmedianasbenchmarks.ForbusinessesinArkansas,theaverageDEiwas6.42whilethemedianaveragewas6.70.14Thesescoresindicateamiddle-of-the-road(median)businessinArkansaswasusingjustlessthan12ofthe17eSolutionsnotedabove.AscanbeseeninFigure26,utilizationslevelsasmeasuredbytheDEididnotvarymuchbetweenbusinesses,non-profitorganizationsandgovernmententities.

Figure26-SummaryofEmploymentImpactsSpecifictoInternetUse(FullandPartTimecombined)

Utilization(DEi)bySector

Region MedianDEi AverageDEIScore NumberofRespondents

Business 6.89 6.58 1236Non-profitorganization 6.89 6.54 201Governmententity 6.8 6.37 95

14Thetermsmeanandaveragerefertothesumofallvaluesdividedbythetotalnumberofvalues.Themedianisthecentralpointofadataset.Tofindthemedian,listalldatapointsinascendingorderandsimplypicktheentryinthemiddleofthatlist.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page28of36

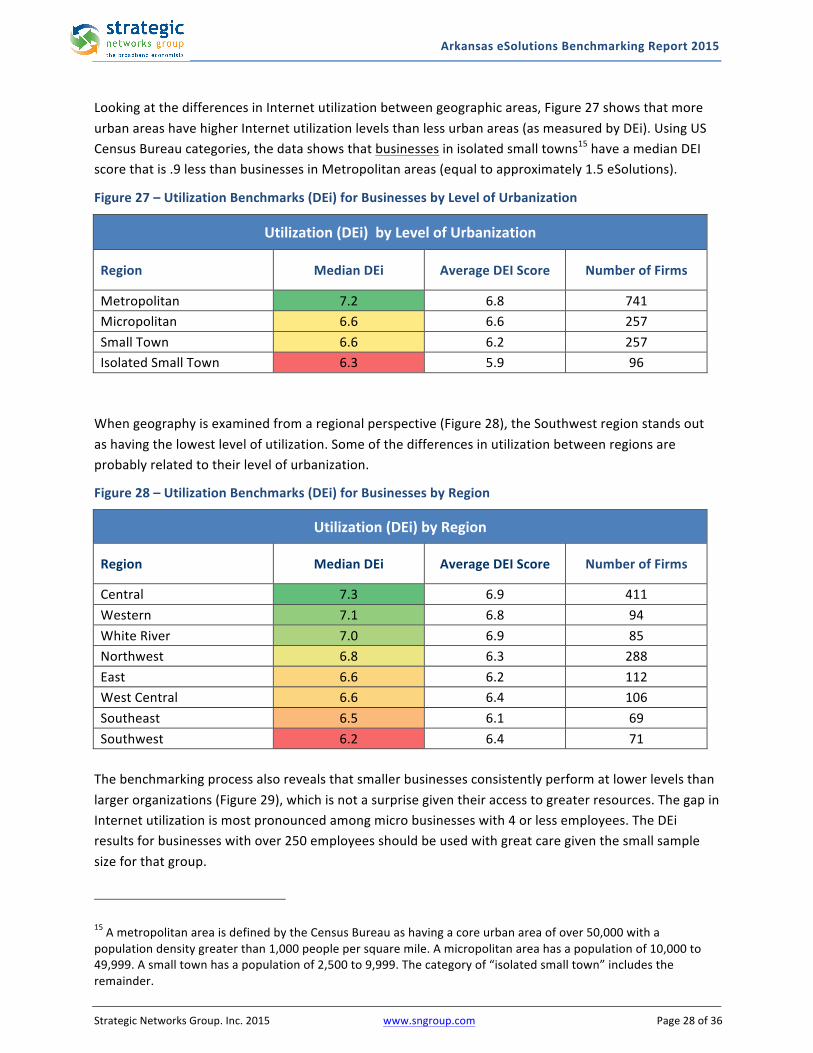

LookingatthedifferencesinInternetutilizationbetweengeographicareas,Figure27showsthatmoreurbanareashavehigherInternetutilizationlevelsthanlessurbanareas(asmeasuredbyDEi).UsingUSCensusBureaucategories,thedatashowsthatbusinessesinisolatedsmalltowns15haveamedianDEIscorethatis.9lessthanbusinessesinMetropolitanareas(equaltoapproximately1.5eSolutions).

Figure27–UtilizationBenchmarks(DEi)forBusinessesbyLevelofUrbanization

Utilization(DEi)byLevelofUrbanization

Region MedianDEi AverageDEIScore NumberofFirms

Metropolitan 7.2 6.8 741Micropolitan 6.6 6.6 257SmallTown 6.6 6.2 257IsolatedSmallTown 6.3 5.9 96Whengeographyisexaminedfromaregionalperspective(Figure28),theSouthwestregionstandsoutashavingthelowestlevelofutilization.Someofthedifferencesinutilizationbetweenregionsareprobablyrelatedtotheirlevelofurbanization.

Figure28–UtilizationBenchmarks(DEi)forBusinessesbyRegion

Utilization(DEi)byRegion

Region MedianDEi AverageDEIScore NumberofFirms

Central 7.3 6.9 411Western 7.1 6.8 94WhiteRiver 7.0 6.9 85Northwest 6.8 6.3 288East 6.6 6.2 112WestCentral 6.6 6.4 106Southeast 6.5 6.1 69Southwest 6.2 6.4 71Thebenchmarkingprocessalsorevealsthatsmallerbusinessesconsistentlyperformatlowerlevelsthanlargerorganizations(Figure29),whichisnotasurprisegiventheiraccesstogreaterresources.ThegapinInternetutilizationismostpronouncedamongmicrobusinesseswith4orlessemployees.TheDEiresultsforbusinesseswithover250employeesshouldbeusedwithgreatcaregiventhesmallsamplesizeforthatgroup.

15AmetropolitanareaisdefinedbytheCensusBureauashavingacoreurbanareaofover50,000withapopulationdensitygreaterthan1,000peoplepersquaremile.Amicropolitanareahasapopulationof10,000to49,999.Asmalltownhasapopulationof2,500to9,999.Thecategoryof“isolatedsmalltown”includestheremainder.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page29of36

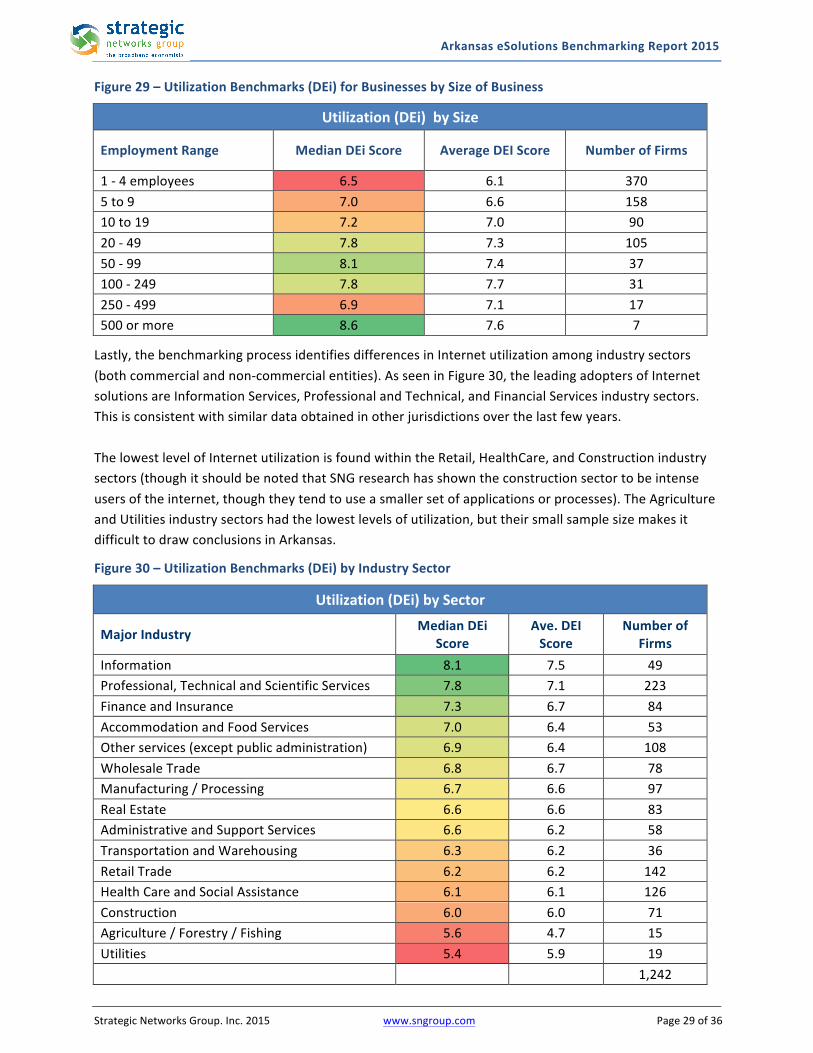

Figure29–UtilizationBenchmarks(DEi)forBusinessesbySizeofBusiness

Utilization(DEi)bySize

EmploymentRange MedianDEiScore AverageDEIScore NumberofFirms

1-4employees 6.5 6.1 3705to9 7.0 6.6 15810to19 7.2 7.0 9020-49 7.8 7.3 10550-99 8.1 7.4 37100-249 7.8 7.7 31250-499 6.9 7.1 17500ormore 8.6 7.6 7

Lastly,thebenchmarkingprocessidentifiesdifferencesinInternetutilizationamongindustrysectors(bothcommercialandnon-commercialentities).AsseeninFigure30,theleadingadoptersofInternetsolutionsareInformationServices,ProfessionalandTechnical,andFinancialServicesindustrysectors.Thisisconsistentwithsimilardataobtainedinotherjurisdictionsoverthelastfewyears.ThelowestlevelofInternetutilizationisfoundwithintheRetail,HealthCare,andConstructionindustrysectors(thoughitshouldbenotedthatSNGresearchhasshowntheconstructionsectortobeintenseusersoftheinternet,thoughtheytendtouseasmallersetofapplicationsorprocesses).TheAgricultureandUtilitiesindustrysectorshadthelowestlevelsofutilization,buttheirsmallsamplesizemakesitdifficulttodrawconclusionsinArkansas.

Figure30–UtilizationBenchmarks(DEi)byIndustrySector

Utilization(DEi)bySector

MajorIndustry MedianDEiScore

Ave.DEIScore

NumberofFirms

Information 8.1 7.5 49Professional,TechnicalandScientificServices 7.8 7.1 223FinanceandInsurance 7.3 6.7 84AccommodationandFoodServices 7.0 6.4 53Otherservices(exceptpublicadministration) 6.9 6.4 108WholesaleTrade 6.8 6.7 78Manufacturing/Processing 6.7 6.6 97RealEstate 6.6 6.6 83AdministrativeandSupportServices 6.6 6.2 58TransportationandWarehousing 6.3 6.2 36RetailTrade 6.2 6.2 142HealthCareandSocialAssistance 6.1 6.1 126Construction 6.0 6.0 71Agriculture/Forestry/Fishing 5.6 4.7 15Utilities 5.4 5.9 19 1,242

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page30of36

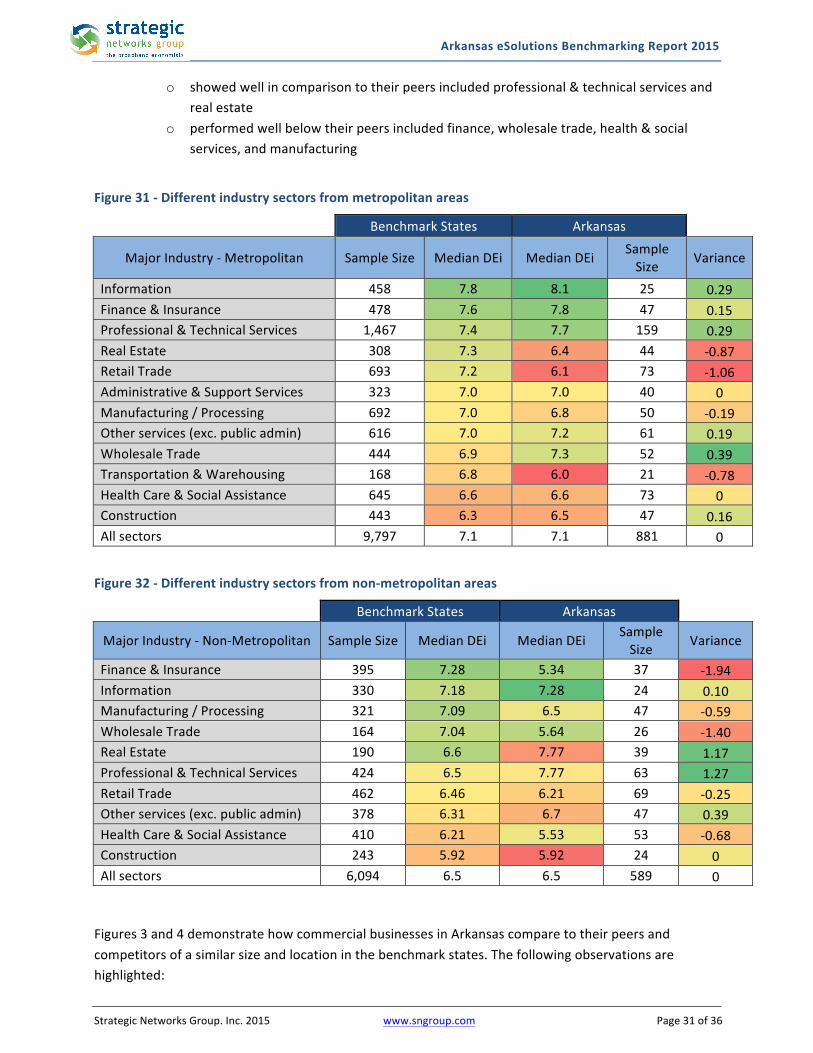

3 ComparativeAnalysisThissectionprovidesacomparativeanalysisofthelevelsofInternetutilizationbybusinessesandorganizationsinArkansasascomparedtofivebenchmarkstates.ThetablesinthisdocumentincluderesultsfromanassessmentcarriedoutacrossArkansasfromNovember2014toFebruary2015.Theseresultsarecomparedtoresultsfromstatewideassessmentscarriedoutinfivestatesbetween2012andJanuary2015.Thesefivestatesarereferredtoas“benchmarkstates”andincludeoneeasternseaboardstateandfourmid-westernstates.Resultsfromthesecomparisonsneedtobeusedcautiously.Eachstatewillhaveadifferentsocio-economicprofile,whichstronglyinfluencesInternetuse.Moreover,datacollectedinArkansasismorerecentthanthatfromthebenchmarkstates.Allthingsbeingotherwiseequal,onewouldexpectresultsfromArkansastoshowhigherlevelsofInternetutilizationasSNGanalysisshowsthatInternetutilizationincreaseswithtime.ThetablesinthissectionaredesignedtocompareresultsfromArkansasandthebenchmarkstates.Thefourtableswerechosenbecausetheycontrolforandisolatethekeyfactorsofsize,location,andindustrysector,therebycomparing“applestoapples”,asmuchaspossible.Withtheprecedingdesignconsiderationsinmind,thissectioncontainsfourtableswithcomparisonsof:

1. Differentindustrysectors16frommetropolitanareas(populationsover50,000);2. Differentindustrysectorsfromnon-metropolitanareas(populationsunder50,000);3. Businessesfromfivedifferentsizeranges(numberofemployees)inmetropolitanareas;and4. Businessesfromfivedifferentsizerangesinnon-metropolitanareas.

InordertomakecomparisonsofInternetutilization,thisaddendumusestheDigitalEconomyindex(DEi)asdescribedinSection2.KeepinginmindthatutilizationlevelswouldhaveincreasedbetweenwhendatawascollectedinArkansasandtheBenchmarkStates(2012–2015),thefollowingobservationscanbemade:

• Inbothmetropolitanandnon-metropolitanareas,benchmarkstateshadsimilaroverallDEiscorestoArkansas.(Note:anumberofindustrysectorsareascontainedsamplesizestoosmallforcomparisons).

• Inmetropolitanareas,mostindustrysectorsinArkansas:o hadutilizationlevelssimilartotheirpeersininformation,finance,professional&

technical,manufacturingo performedwellbelowtheirpeersinretail,realestate,andtransport&warehousing

• Innon-metropolitanareas,Arkansasindustrysectorsthat:

16Industriesarebasedon2-digitNAICScodeleveldatafromUSCBCountyBusinessPatterns2011.FullnamesofindustriesfromNAICSdefinitionsareabbreviatedforthistable.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page31of36

o showedwellincomparisontotheirpeersincludedprofessional&technicalservicesandrealestate

o performedwellbelowtheirpeersincludedfinance,wholesaletrade,health&socialservices,andmanufacturing

Figure31-Differentindustrysectorsfrommetropolitanareas

BenchmarkStates Arkansas

MajorIndustry-Metropolitan SampleSize MedianDEi MedianDEi Sample

Size Variance

Information 458 7.8 8.1 25 0.29Finance&Insurance 478 7.6 7.8 47 0.15Professional&TechnicalServices 1,467 7.4 7.7 159 0.29RealEstate 308 7.3 6.4 44 -0.87RetailTrade 693 7.2 6.1 73 -1.06Administrative&SupportServices 323 7.0 7.0 40 0Manufacturing/Processing 692 7.0 6.8 50 -0.19Otherservices(exc.publicadmin) 616 7.0 7.2 61 0.19WholesaleTrade 444 6.9 7.3 52 0.39Transportation&Warehousing 168 6.8 6.0 21 -0.78HealthCare&SocialAssistance 645 6.6 6.6 73 0Construction 443 6.3 6.5 47 0.16Allsectors 9,797 7.1 7.1 881 0

Figure32-Differentindustrysectorsfromnon-metropolitanareas

BenchmarkStates Arkansas

MajorIndustry-Non-Metropolitan SampleSize MedianDEi MedianDEi Sample

Size Variance

Finance&Insurance 395 7.28 5.34 37 -1.94Information 330 7.18 7.28 24 0.10Manufacturing/Processing 321 7.09 6.5 47 -0.59WholesaleTrade 164 7.04 5.64 26 -1.40RealEstate 190 6.6 7.77 39 1.17Professional&TechnicalServices 424 6.5 7.77 63 1.27RetailTrade 462 6.46 6.21 69 -0.25Otherservices(exc.publicadmin) 378 6.31 6.7 47 0.39HealthCare&SocialAssistance 410 6.21 5.53 53 -0.68Construction 243 5.92 5.92 24 0Allsectors 6,094 6.5 6.5 589 0Figures3and4demonstratehowcommercialbusinessesinArkansascomparetotheirpeersandcompetitorsofasimilarsizeandlocationinthebenchmarkstates.Thefollowingobservationsarehighlighted:

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page32of36

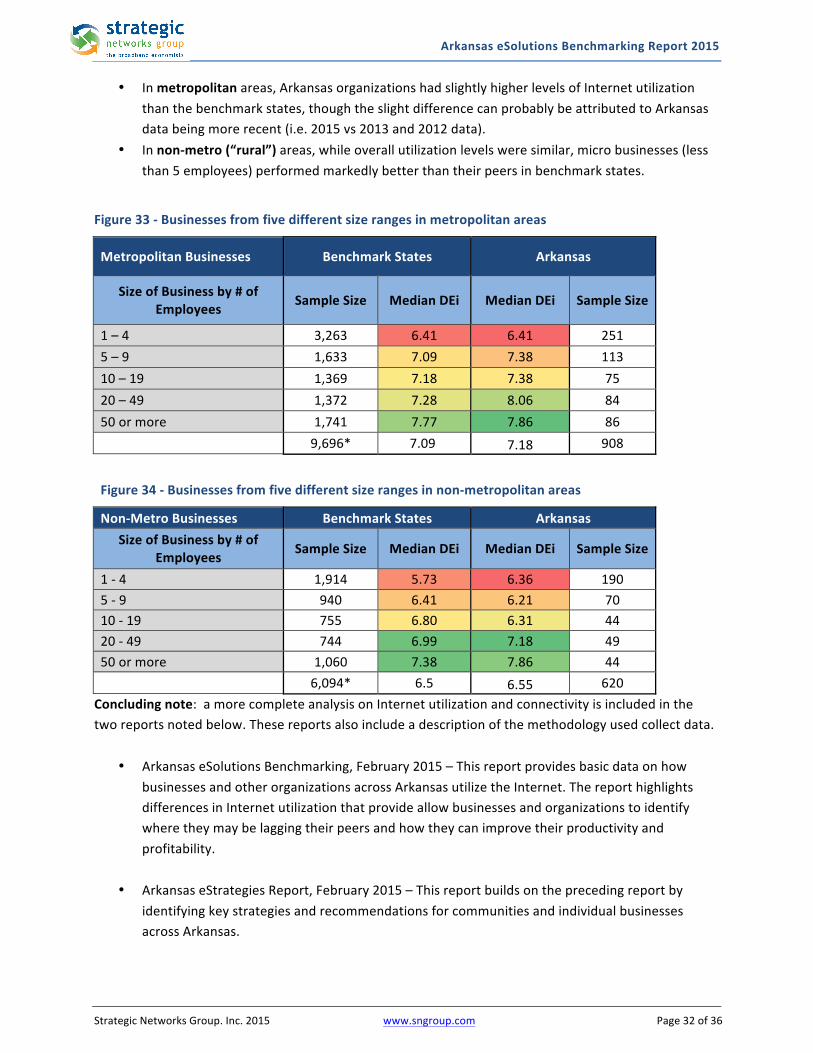

• Inmetropolitanareas,ArkansasorganizationshadslightlyhigherlevelsofInternetutilizationthanthebenchmarkstates,thoughtheslightdifferencecanprobablybeattributedtoArkansasdatabeingmorerecent(i.e.2015vs2013and2012data).

• Innon-metro(“rural”)areas,whileoverallutilizationlevelsweresimilar,microbusinesses(lessthan5employees)performedmarkedlybetterthantheirpeersinbenchmarkstates.

Figure33-Businessesfromfivedifferentsizerangesinmetropolitanareas

MetropolitanBusinesses BenchmarkStates Arkansas

SizeofBusinessby#ofEmployees SampleSize MedianDEi MedianDEi SampleSize

1–4 3,263 6.41 6.41 2515–9 1,633 7.09 7.38 11310–19 1,369 7.18 7.38 7520–49 1,372 7.28 8.06 8450ormore 1,741 7.77 7.86 86

9,696* 7.09 7.18 908

Figure34-Businessesfromfivedifferentsizerangesinnon-metropolitanareas

Non-MetroBusinesses BenchmarkStates ArkansasSizeofBusinessby#of

Employees SampleSize MedianDEi MedianDEi SampleSize

1-4 1,914 5.73 6.36 1905-9 940 6.41 6.21 7010-19 755 6.80 6.31 4420-49 744 6.99 7.18 4950ormore 1,060 7.38 7.86 44 6,094* 6.5 6.55 620Concludingnote:amorecompleteanalysisonInternetutilizationandconnectivityisincludedinthetworeportsnotedbelow.Thesereportsalsoincludeadescriptionofthemethodologyusedcollectdata.

• ArkansaseSolutionsBenchmarking,February2015–ThisreportprovidesbasicdataonhowbusinessesandotherorganizationsacrossArkansasutilizetheInternet.ThereporthighlightsdifferencesinInternetutilizationthatprovideallowbusinessesandorganizationstoidentifywheretheymaybelaggingtheirpeersandhowtheycanimprovetheirproductivityandprofitability.

• ArkansaseStrategiesReport,February2015–Thisreportbuildsontheprecedingreportby

identifyingkeystrategiesandrecommendationsforcommunitiesandindividualbusinessesacrossArkansas.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page33of36

AppendixA- DataCollectionMethodsandResultsThecoremethodologyisfoundedonprimaryresearchviadatacollectionthroughonlineassessmentsofbusinessesandnon-commercialorganizations.TheassessmentcollectsinformationdirectlyfromInternetusersinthefollowingcategories:UserProfile–informationthatcharacterizeeachrespondentforpurposesofstatisticalanalysisbasedonusercharacteristics,e.g.organizationsizebyemployment,timeofInternetuse;orlocation.InternetUtilization–thecurrentandplannedusesoftheInternetacrossmultiplecategoriesrelevanttohowbusinessesandnon-commercialentitiesmayusetheInternet.TheprimarytypeofInternetconnectionusedisalsoidentifiedforselectedcrosstabulationswithotherresponsedata.InternetBenefits–informationonhowbusinessesandnon-commercialentitiesassessthebenefitsofusingtheInternet.Barriers-informationontheimportanceoffactorsthatpreventorinhibitbusinessesandnon-commercialentitiesfromtakingfulladvantageoftheInternet.Theassessmentsaremadeavailableforonlineaccessthroughoneoftwomeans:

• Individualbusinessesandnon-commercialorganizationswereinvitedtoparticipateviadirectemailinvitationssentfromalarge,statewidecontactlist.

• Inaddition,businessesandnon-commercialorganizationswereencouragedthroughavarietyofothercommunicationschannelstoaccessalinktotheassessment.

Theoverallerrormarginforstatisticalanalysisis+/-2.9%(witha95%ConfidenceInterval).17Thesampleerrormarginindicatestheaccuracyofthestatisticsderivedinrelationtohowtheyrepresentthelargerpopulation.Usinga95%ConfidenceInterval,astatisticshouldfallwithintheerrormarginfor95%ofanyrandomsamplesofthepopulation.Thesampleerrormarginiscalculatedbasedonthesamplesize,thepopulationsize,andtheconfidenceinterval.For95%confidenceintervalandforpopulationsmuchlargerthanthesample,thesamplingerroris0.98dividedbythesquarerootofN,whereNisthesamplesize.Forthisreportallpopulationsizesaremuchlargerthanthesamplesizes.Thefollowingisanexampleforinterpretationofstatisticsprovidedinthisreport:

• 61.9%oforganizationsusetheInternetforsellinggoodsorservicesonline.• ThesamplesizefororganizationsreportingInternetutilizationis745,providingasampleerror

marginof+/-3.6%witha95%confidenceinterval.Thismeansthatanysimilarsampleofthepopulationoforganizationsacrossthestatewillresultinastatisticforsellinggoodsorservicesonebetween58.3%and65.5%(61.9%+/-3.6%)95%ofthetime.Thestatisticwouldfalloutsidethisrange5%ofthetimeforotherrandomsamplesofthepopulation.Inpracticaltermsthesamplingerrorcanbetakenastheaccuracyofthestatisticasitappliestotheentirepopulation.

17Theerrormarginat95%ConfidenceIntervalisoftenreferredtoas+/-X%accuracy,19timesoutof20.Errormarginsincreasefordetailedanalysisthatusessubsetsoftheoverallsample.Whereapplicable,samplesizesandsampleerrormarginsareindicated–example:N=1,428[2.6%].

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page34of36

Smallersamplesizesresultinlargersamplingerrors.Whencomparingstatisticsbetweentwoindependentsamples,thesampleerrorsforeachsamplemustbeconsideredtodetermineifthedifferenceissignificant.Wherethehigherendofastatistic(X%+errormargin)forsampleAislessthanthelowerendofthesamestatistic(Y%–errormargin)forsampleB,thedifferencecanbeconsideredstatisticallysignificant.Wherethedifferencebetweenstatisticsiswithinthesamplingerrormarginranges,thensuchdifferencesmaynotberealorsignificantforotherrandomsamplesofthesamesizes.Forsimplicityofreportingthestatisticsarestatedasgivenwithsamplesizesandsamplingerrormarginsprovidedforinterpretation.

ArkansaseSolutionsBenchmarkingReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page35of36

AppendixB- GlossaryArkansaseSolutionsBenchmarkingReport:ThisreportpresentstheresultsofassessmentsofInternetusecarriedoutfortheStateofArkansas.Theassessmentscollectedinformationfrombusinessesandnon-commercialorganizationsregardingtheavailabilityofbroadband(highspeedInternetaccess)anditsuses,benefits,driversandbarriers.Thislargelydescriptivereportresultsprovideinsightintogapsandopportunitiesforincreasingbroadbandutilizationbybusinessesandnon-commercialentities.DigitalEconomyAnalysisPlatform(DEAP):TheDEAPhasbeendevelopedasanonlineresourcethatprovidesclientswithaccesstothedatacollectionresultsandtheabilitytocustomizetheiranalysisacrossarangeofvariables,includingindustrysectororgeographicregion.TheDEAPisaccessedonlinebyauthorizedusers.UsersarepresentedwithdashboardsforbusinessesandCAIs.Eachdashboardisorganizedaroundaseriesofpagesfocusedonspecifictopics,e.g.Connectivity,Utilization,DEi,Impacts,etc.Withineachpageisasetofpredefinedreportsthatpresentachartand/ortableofprocessedresultsfromthedatasets.eSolutions:referstotheintegrationofInternettechnologieswiththeinternalcomputer-basedsystemsandapplicationswithinoramongorganizationsforavarietyofoperationalprocesses.eSolutionsencompassnotonlyproductdeliveryandpaymenttransactions(e-commerce)butalsoallprocessesthatmaybefacilitatedbycomputer-mediatedcommunicationsovertheInternet.eProcess:usesoftheInternetwhichincludeinternaloperationaluses,suchassuppliercoordination,trainingandteleworking.eCommerce:usesoftheInternetwhichincludeactivitiesrelatedtothesales,marketinganddeliveryofproductsandservices;and,ArkansasDigitalEconomyIndex:TheDigitalEconomyindex(DEi)ispartofthebenchmarkingprocessandprovidesreferencepointsagainstwhichtheperformanceofanyindividualorgroupcanbecompared.TheDEisummarizesanorganization’sutilizationof17Internetapplicationsandprocess.BasedonthenumberofapplicationscurrentlybeingusedbyabusinessesorCAI,acompositescoreiscalculatedthatsummarizeshowcomprehensivelyeachorganizationusesInternet-enabledeSolutions.TheDEicanbeusedtocompareorganizations,regions,orindustrysectors.Utilizationreferstothethirdstageinthebroadbanddevelopmentprocess.Thefirststageisprovidingacommunityororganizationwithaccess(availability)totheInternet.ThesecondstageisadoptionortheprocesswherebyapersonororganizationstartstoactuallyusetheInternet.ThethirdstageisutilizationwherebyapersonororganizationusestheirInternetconnectiontocreatevalue.ManypeopleandorganizationshaveaccessandhaveadoptedtheInternet,butarerelativelyineffectiveinhowtheyuseandderivebenefitsfromtheInternet.Thefieldofanalysislabeled“utilization”explorespatternsofInternetuseandhowthesepatternscanbeenhanced.

ArkansaseStrategyReport

March2015

Preparedfor

StrategicNetworksGroup,Inc.|www.sngroup.com|CONFIDENTIAL

Arkansase-StrategyReport2015

StrategicNetworksGroup.Inc.2015 www.sngroup.com Page2of25

TableofContents

TableofFigures.....................................................................................................2

SummaryandRecommendations..........................................................................3

1. StartingPoints.................................................................................................91.1 OrganizationandObjectivesoftheReport............................................................................91.2 WhatisBroadband?............................................................................................................101.3 TheDigitalEconomyindex(DEi)..........................................................................................11

2. BroadbandUtilizationbyOrganizations.........................................................132.1.1 InternetConnectivity..........................................................................................................132.1.2 UtilizationbyIndustry........................................................................................................142.1.3 DifferencesinUtilization:GapsandOpportunities............................................................15

2.2 WhatContributestotheDifferentLevelsofUtilization?......................................................152.3 IdentifyingPriorityInternetApplications.............................................................................172.4 TheAdoptionProcess..........................................................................................................192.5 BarrierstoImprovedUtilization..........................................................................................20

3. SummaryandNextSteps...............................................................................22

Appendix1:Glossary..........................................................................................23

TableofFiguresFigure1:TopIndustrySectorsInArkansas...............................................................................................14Figure2:AverageInternetUtilizationbyIndustrySector........................................................................14Figure3:BusinessInternetUsagebyLevelofUrbanization......................................................................16Figure4:BusinessInternetUsagebyRegion.............................................................................................16Figure5:Utilization(medianDEiScore)byOrganizationalSize................................................................16Figure6:ImpactofLocationonUtilization,bySizeofOrganization.......................................................17Figure7:DifferenceinUtilizationofSpecificeSolutionsbySizeofOrganization...................................18Figure8:PlannedAdoptionofSpecificeSolutionsbySmallBusinesses.................................................19Figure9:BarrierstoAdoptionofeSolutionsamongBusinesseswithlessthan50Employees..............21

Arkansase-StrategyReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page3of25

SummaryandRecommendationsManycommunitiesandcountiesacrossArkansasaredealingwitheconomicdislocationandanagingpopulation1.Mostruralareasfacetheadditionalchallengeofthesteadyshiftofpopulationfromruraltourbanareas2.Inthefaceofthesechallenges,howcancommunitiesandbusinessesmaximizetheircompetitiveness,whileimprovingtheirqualityoflife?Oneareawithsignificantpotentialisbroadband(seeSection2.2foradefinition),whichcanbeleveragedintotangiblebenefitsforcommunitiesandbothcommercialandnon-commercialorganizations.Thisreportanditscompaniondocument,ArkansaseSolutionsBenchmarking3,demonstrateshowbusinessescanbecomemoreproductive,competitive,andreachintonewmarkets.ThefirststepinbenefitingfrombroadbandisacquiringconnectivityoraccesstotheInternet.Andonceaccessisacquired,thesecondstepisadoption,wherebybusinessesandotherorganizationsbegintousetheirhigh-speedInternetaccessonaregularbasis.Thethird(andsometimesmostdifficulttoachieve)stageinbroadbanddevelopmentisutilization.ThismeansusingtheInternetinincreasinglyproductivewaysthatbringconcretebenefits,suchasjobs,newsavingsandrevenues,andimprovedqualityoflife.Thisreportfocusesonutilizationasthethirdstageofbroadbanddevelopment.

UtilizingBroadbandThisreportrevealsthattheabilitytoutilizeorleveragebroadbandvariessignificantlyacrosscommercialandnon-commercialorganizations.Notallcommunitieshavebeenabletoturnthepotentialofbroadbandintomeasurablesuccessintermsofjobs,companyattractionandretention,anincreasedtaxbaseandmoreefficientandeffectivecitizenservices.ManybusinessesandorganizationsstruggleintheireffortstousetheInternettogenerateincreasedrevenues.Turningpotentialintorealityrequiresskills,training,andbothformalandinformalsupport.Incommunitiesthatalreadyhavealarge,diverse,andmoderneconomyandworkforce,buildingbroadbandinfrastructuremaybesufficienttorealizethepotentialofbroadband.However,manyindustrysectors,communities,andbusinesseshavelimitedInternetrelatedskillsandcapacity.Benchmarkingdatashowthatformanycommunities,especiallyinnon-metropolitanareas,utilizing

1RuralProfileofArkansas2013–Social&EconomicTrendsAffectingRuralArkansas:UniversityofArkansas,DivisionofAgriculture,ResearchandExtension.2SeevariouspublicationsofDavidMcGranahanfromtheUSDA:http://www.ers.usda.gov/ers-staff-directory/david-mcgranahan.aspx.3Asummaryofthefindingsfromthe2015benchmarkingeffortcanbefoundintheArkansaseSolutionsBenchmarkingReport(February2015)whichislargelydescriptiveanddoesnotincludesomeoftheanalysisnortherecommendationsinthisreport.

Arkansase-StrategyReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page4of25

broadbandoftenlags(Section2.2),evenwithstate-of-the-artconnectivity4available.Theresultisthatthesecommunitiesandbusinessesmissoutonmanyofthebenefitsofbroadband.Moreimportantly,overtime,thesecommunitiesareatriskofbecomingeconomicallylesscompetitiveandgenerallylessattractivetohouseholdsandbusinesses5.Itisautilizationgapthatcancreatebothaneconomicdivideaswellasopportunitiesforunder-utilizers.Thisreportexamineshowbusinessesandnon-commercialorganizationsinArkansasdifferintheirutilizationofbroadbandandwheretheycanlooktomakeimprovements.Thereportshowsindetailhowdifferentindustrysectorsandbusinesstypescomparetoeachother,especiallybetweenandwithinregions.Thereportprovidesinsightsanddatathatallowcommunitiesandorganizationstoassesswheretheystandandidentifywhatkindsofactionswillimprovetheirperformanceandbenefits.ThereportincludesrecommendationsforhowtheStateofArkansasanditscommunitiescanimproveutilizationofbroadbandbyitsbusinessesandnon-commercialorganizations,therebyimprovingtheireconomiesandqualityoflife.Recommendationsarebrokendownintothreeareas:

1. GapsandopportunitiesinuseoftheInternetandbroadband;2. KeybarrierstoimprovingtheuseandbenefitsoftheInternetandbroadband;and3. Thebestwaystobuildskillsandabilities.

Analysisandrecommendationsfocusprimarilyonbusinesses,althoughtherecommendationsmayalsobeappliedtonon-profitorganizationsandgovernmententities.AmoredetaileddescriptionoftheimpactsofInternetutilizationonbusinessrevenuesandemploymentcanbefoundintheArkansaseSolutionsBenchmarkingReport(February2015)whichisamorecompleteanddescriptivepresentationoftheassessment/surveyresults,whereasthisdocumentismorestrategicandprescriptive.

4ThisstatementissupportedbydatafromeSolutionsBenchmarkingeffortsundertakenbyStrategicNetworksGroups(SNG)innon-metropolitancommunitiesthathavehadbroadbandforanextendedperiodoftime.ThestatementisalsosupportedbycommentsmadebyInternetServiceProvidersduringruralbroadbandplanningworkshopsfacilitatedbySNG.5Almost40%ofbusinessesparticipatinginthebroadbandbenchmarkingeffortinArkansasstatedthatbroadbandservicewas“essential”inselectingtheirbusinesslocation,andover58%saybroadbandis“essential”forremainingintheircurrentlocation.ArkansaseSolutionsBenchmarkingReport(February2015),page20.

ThisreportusesdatacollectedbetweenNovember2014andFebruary2015acrossArkansas.Atotalof1,532organizationscontributedtothebroadbandbenchmarkingeffort.Theorganizationsconsistedof1,236businesses,95governmententitiesand201nonprofits.

Arkansase-StrategyReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page5of25

RecommendationsTohelpstakeholdersandcommunitiesbetterunderstandandusethisreport,recommendationshavebeenstructuredaroundfundamentalquestionsthatleadersanddecision-makersfaceintermsofleveragingbroadbandforthesocio-economicbenefitoftheircommunitiesandconstituents.ThebasisfortheserecommendationscanbefoundinSection2ofthisReport.1.Howimportantishigh-speedInternetaccesstoArkansas,itscommunities,anditsresidents?Inthe21stcentury,broadbandaccesshasbecomeanessentialpartofacommunity’sinfrastructure,abusiness’internalandexternaloperations,andahousehold’sparticipationintheircommunitylife.Availabilityandmeaningfuluseofhigh-speedInternetaccessaredirectlytiedtoacommunity’sviability,competitiveness,andqualityoflife.However,therearesignificantdifferencesbetweencommunitiesinqualityofInternetconnectivityandtheirproductiveuseoftheInternet.CurrentInternetusagevarieswidelyandisexploredinthevarioussectionsofthisreport.Eachcountyorcommunityhasitsownuniquecharacteristics,assets,andchallenges.Consequently,eachcountyorcommunityrequiresstrategiesandinitiativesthataddressitsuniquesituation.Recommendation#1:Eachcountyorcommunityshoulddevelopitsownstrategyandinitiativesbased

onitsowncharacteristics,values,andpriorities.Prioritiesandtargetsshouldincludeinfrastructurecoverageandcapabilities,aswellashighlevelsofadoptionofthoseeSolutionsneededtoremaincompetitive.Whilefocustendstorevolvearoundattractingbetteravailabilityandspeed–spendtimetodriveutilizationofwhatisavailable.

2.Istheavailabilityofhigh-speedInternetaccessstillanissueformanyareasofArkansas?Whilethevastmajorityofbusinessesandnon-commercialorganizationsreportthattheyhaveInternetconnectivity,63.1%ofrespondentshaduploadspeedsoflessthantheFCC’snewbroadbandstandardof3mbps,while80%failedtomeettheFCCbroadbanddownloadstandardof25mbps.Moreover,muchofthephysicalInternetinfrastructureinnon-metroareasconsistsofoldertechnologythatprovidesInternetspeedsandcapacitywellbelowthatofmostArkansasmetropolitanareas.Theissue

Broadbandwasalsoconsidered“essential”forselectinglocationby

40%ofbusinesses,aswellas“essential”forremaininginlocation

by58%ofbusinesses.BenchmarkingDataforAransas,

February2015.

Arkansase-StrategyReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page6of25

ofpoorornoInternetservicesalsoremainsacriticalissueinsomeruralresidentialareas.Toremaincompetitive,communitiesneedrobust6andaffordableconnectivitythatalsosupportsmobiledevices.Theuseofmobiledevicesandapplicationsfor“untetheredaccess”isexpectedtocontinuetogrowandbecomeincreasinglyintegratedintohoworganizationsusetheInternettoenableadditionalopportunitiesforincreasingworkeffectivenessandproductivity.TheavailabilityofeffectivemobileInternetaccesswillbecomeincreasinglyimportantasanadjuncttowiredaccessformanyorganizations,especiallythosewithmobileworkers.Recommendation#2:Undertakeeffortsatthelocalleveltoidentifyareaswithouthigh-speedInternet

andtodeveloplocalsolutionsthataddresstheproblem.LocalandregionalinitiativesshouldencouragemobilewirelessInternetServiceProvidersandtelecommunicationscompaniestoextend4GandLTEcapabilitiestoareascurrentlywithoutsuchservice.

3.WherearethemajorgapsorweaknessesinutilizationoftheInternetanditsapplications?KeygapsinInternetutilizationarerelatedtodegreeof“rurality,”businesssize,andindustrysector.Prioritizingindustrysectorsandothereconomicgroupsmustbedonewithinalocal,orregionalcontext.Localandcountylevelplanningwillneedtoconsideradditionalfactorsandconsiderations,suchasindustrysectorsindecline,orregionalstrategiesfordevelopingspecificsectors.Ingeneral,focusshouldbeonindustrysectorsthatmakethelargestcontributiontotheeconomyandthathavethegreatestgrowthpotential.Recommendation#3: Ratherthanundertakingbroadbutuntargetedefforts,broadbandinitiatives

shouldfocusonindustriesthathavethehighesteconomiccontributionandhighestgrowthpotentialwithineachregion.Threesectorsthatshouldbegivenpriorityarehealthandsocialservices,retail,andconstruction.

4.HowcanweusetheInternet’spotentialtomaximizejobcreation?Smalltomediumsizedorganizationswith1to49employeesshouldbeafocusforallregions.Thissegmentisimportantforthefollowingreasons:

• Itincludes95.2%ofallestablishmentsinArkansas.• Theseorganizationsexperiencetheweakestutilizationlevelscomparedtoorganizationswith

largernumbersofemployees.

6RobustconnectivitycanbedefinedasInternetconnectivitythatisreliable24hoursaday,withconsistenthighuploadanddownloadspeedsthatmeettheFCCdefinitionofbroadband.

Arkansase-StrategyReport2015

StrategicNetworksGroup,Inc.2015 www.sngroup.com Page7of25

eSolutionsisthetermusedinthisreporttorefertotheintegrationof