ARDS AND NORTH DOWN BOROUGH COUNCIL · 2015 Section 75 Compliant Yes ☐No Not Applicable ☒ ......

112

ARDS AND NORTH DOWN BOROUGH COUNCIL 11 December 2018 Dear Sir/Madam You are hereby invited to attend a meeting of the Audit Committee of the Ards and North Down Borough Council which will be held in the Council Chamber, 2 Church Street, Newtownards on MONDAY, 17 DECEMBER 2018 commencing at 7.00pm. Tea, coffee and sandwiches will be available from 6.00pm. Yours faithfully Stephen Reid Chief Executive Ards and North Down Borough Council A G E N D A 1. Apologies 2. Chairman’s Remarks 3. Declarations of Interest 4. Meeting with NI Audit Office & Internal Audit Service in the Absence of Management 5. Matters Arising from Previous Meeting a) Minutes of Audit Committee held on 25 September 2018 (Copy attached) b) Actions Register (Copy attached) 6. Performance Improvement Report (Copy attached) 7. External Audit a) Final Report to those Charged with Governance 2017/18 (Copy attached) b) Improvement Audit and Assessment (Copy attached) c) Final Annual Audit Letter 2017/18 (Copy to follow)

Transcript of ARDS AND NORTH DOWN BOROUGH COUNCIL · 2015 Section 75 Compliant Yes ☐No Not Applicable ☒ ......

ARDS AND NORTH DOWN BOROUGH COUNCIL

11 December 2018 Dear Sir/Madam You are hereby invited to attend a meeting of the Audit Committee of the Ards and North Down Borough Council which will be held in the Council Chamber, 2 Church Street, Newtownards on MONDAY, 17 DECEMBER 2018 commencing at 7.00pm. Tea, coffee and sandwiches will be available from 6.00pm. Yours faithfully Stephen Reid Chief Executive Ards and North Down Borough Council

A G E N D A

1. Apologies

2. Chairman’s Remarks

3. Declarations of Interest

4. Meeting with NI Audit Office & Internal Audit Service in the Absence of Management

5. Matters Arising from Previous Meeting a) Minutes of Audit Committee held on 25 September 2018 (Copy attached) b) Actions Register (Copy attached)

6. Performance Improvement Report (Copy attached)

7. External Audit a) Final Report to those Charged with Governance 2017/18 (Copy attached) b) Improvement Audit and Assessment (Copy attached) c) Final Annual Audit Letter 2017/18 (Copy to follow)

8. Internal Audit a) Internal Audit Progress Report (Copy to follow) b) Recently completed audits:

i. Grant Funding (Copy attached) ii. Building Control (Copy attached) iii. Staff Performance Management (Copy attached) iv. Planning (Copy attached) v. Travel and Subsistence (Copy attached)

9. Corporate Governance

a) Corporate Risk Register (Copy attached) b) Interim Statements of Assurance (Copy attached)

ITEMS 10 – 13 ***IN CONFIDENCE***

10. Single Tender Actions Update (Copy attached)

11. Fraud, Whistleblowing and Data-protection Matters (Verbal Update)

11.1 General Data Protection Regulation & Data Protection Act 2018 (Report attached)

12. Internal Audit and Corporate Governance Contract Update (Copy attached)

13. Any Other Notified Business.

MEMBERSHIP OF AUDIT COMMITTEE (11 MEMBERS)

Alderman Carson Councillor Armstrong-Cotter

Alderman Gibson Councillor Chambers

Alderman Fletcher (Vice Chairman) Councillor Douglas

Alderman Irvine (Chairman) Councillor Dunlop

Alderman Keery Councillor Muir

Mr S Hagen

Unclassified

Page 1 of 2

ITEM 5b

Ards and North Down Borough Council

Report Classification Unclassified

Council/Committee Audit Committee

Date of Meeting 17 December 2018

Responsible Director Director of Finance and Performance

Responsible Head of Service

Date of Report 12 December 2018

File Reference AUD02

Legislation Local Government (Accounts and Audit) Regulations 2015

Section 75 Compliant Yes ☐ No ☐ Not Applicable ☒

Subject Follow up actions from previous meetings - Action Register

Attachments Follow up actions register

In line with best practice, the purpose of this report is to make the Audit Committee aware of the status of outstanding recommendations of any outstanding actions from the previous Audit Committee meetings. The Committee will note that 5 actions are required from previous committee meetings, these are detailed in the appendix. RECOMMENDATION It is recommended that Committee notes the report.

Unclassified

Page 2 of 2

Appendix

Item

Title Action Status

January 2018

7 Outstanding External Audit Recommendations

• Clear legacy issues by December 2018

• Income policy to be progressed before June audit committee meeting

Head of Finance Mar 2019

June 2018

9a

Single Tender Actions

• Numbers of Direct award contracts to be reported to Committee

Head of Performance and Projects & Head of Administration Mar 2019

11 Draft Financial Statements • Completion of the Bank reconciliation process for 2017/18 financial year.

Head of Finance Dec 2018

September 2018

5a

Matter arising from Previous minutes

• Report to RDC on Brexit preparations

Complete Item 3 RDC 8 Nov 2018

8c(i) FOI Internal Audit Report • Report to CSC regarding update of FOI page on website

Complete Item 12 CSC 9 Oct 2018

1

Audit Committee PIP Quarter 2 : 2018-19 Progress Report

Performance Key

The key outlined below provides definitions for the three Red, Amber, Green (RAG) status levels which have been chosen to measure progress.

RAG Status Definition

Target/standard, actions and measures are on track

Target/standard, actions and measures are mostly on track but some are falling short of plan

Target/standard, actions and measures are of concern and are mostly falling short of plan

2

Corporate objective

PEOPLE: We will ensure we engage with, and support, all local communities to deliver real social benefits

Improvement Objective 1 : We will support local communities to develop community resilience for emergency planning.

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability Efficiency Innovation

What are we going to do this year?

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

1. Engage with local communities and form at least one Community Resilience Group

Not yet commenced Council is currently collaborating with Street Pastors and Civil Aid Corps NI to initially build resilience in Holywood and Newtownards with a view to further rollout across the Borough.

2. Conduct a series of Community Resilience talks

Not yet commenced Community talk at PCSP Community Safety Event is scheduled to be held in December.

3. Update the Emergency Planning section of Council’s website to signpost to information and advice

Not yet commenced The Council’s Emergency Planning section of the website has been updated to signpost users to information and advice on:

• Home insurance

• Emergency contact telephone numbers such as NIHE, NI Water, Flooding Incident Line

• Severe weather

• Homeowner flood protection grant scheme

The Council’s social media sites are also utilised in the event of emergencies.

3

Corporate objective

PLACE: We will ensure we make the very best of the natural, cultural and environmental assets in our Borough

Improvement Objective 2 : We will increase recycling and divert waste from landfill.

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability Efficiency Innovation

What are we going to do this year? Promote the recently introduced Kerbside glass recycling scheme through:

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

1. Raise awareness by leafleting every household to encourage glass diversion from residual waste bins

Leaflets have been issued by glass collection teams to householders not presenting their glass box.

This is an ongoing project, where crews will monitor glass box presentation at each collection date and record perceived change in set out rate. The tonnage will also be monitored to assess if the leaflets are having any impact.

2. Introducing a Glass collection calendar on Bin-ovation App

Glass collection calendar now live. The Bin-ovation App received 1,546 new users in the period and since its launch the “New glass collection service update” article has had 4,485 views via the App. Officers have requested an indicator for visits to the ‘calendar’ link through bin-ovation. However, they have been advised that it cannot go specifically to waste types as it is a simple link to the calendar linked to the address.

3. Continue implementation of route optimisation.

Majority of in-cab devices now live in RCV’s

All in-cab devices are now live, and drivers have received training regarding their use. The in-cab devices enable drivers to communicate directly with the Depot regarding issues they encounter such as blocked access, road works, contaminated bins, etc. This in turn means that when a member of the public rings in, the Admin staff have information to hand to advise why collections have been disrupted and what alternative arrangement is in place.

4. Revise and improve the range of commercial recycling collection services, including kerbside, available to businesses

Following consultation with commercial waste customers, revisions to service have been agreed by Environment Committee.

Strand 4 of the SWRMS working group was established on the proposed revisions to the commercial waste service have been agreed by Council and will go live in April 2019. This will largely result in commercial collections mirroring household collections i.e. fortnightly residual and recycling collection services and 4 weekly glass collections. The expected impact of these revisions will be a saving to the trade customer; a decrease in waste going to landfill and an increase in recycling.

5. Further refinements to kerbside recycling initiatives and revision of access rules at Council HRCs

Additional measures being introduced at the HRCs to ensure materials that can be recycled are placed in the appropriate containers.

A Working group has been established and met on 29 August – the ToR for the group are to take forward Strand 3 of the Sustainable Waste Resource Management Strategy

Actions from the initial meeting included:

• Communicating with all multi-use permit holders regarding breach of use;

• Collating visitor numbers to sites to evidence period of high usage to assist with prioritising supervision/monitor/resource deployment;

• Communications campaign.

Work is ongoing to review layout of HRC’s to optimise recycling engagement/outcomes.

4

Corporate objective

PLACE: We will ensure we make the very best of the natural, cultural and environmental assets in our Borough

Improvement Objective 3 : We will ensure we make the very best of the natural, cultural and environmental assets in our Borough

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability Efficiency Innovation

What are we going to do this year? Promote the recently introduced Kerbside glass recycling scheme through:

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

1. Maintain ISO 14001 accreditation for 22 sites

Accreditation maintained.

• Following accreditation the Auditor remarked on the Council’s environmental performance improvement: Increased recycling has saved £200,000, this money is then used to fund other environmental improvement initiatives without any increased cost to the council. The borough are investigating the possibility of becoming a water refill borough, to reduce the use of plastic water bottles in the borough. The council is also planning to eliminate the purchase of single use plastics within the council operations – demonstrates proactive initiatives.

• The Council has improved its Sustainability and Environment Policy

• A communication strategy has been developed

• It should be noted that accreditation now applies to 21 sites as Donaghadee Parks Depot is no longer council owned.

2. Increase the amount of compostable waste produced by Council buildings

Internal Waste Management Strategy drafted and with HoST for consultation.

The Internal Waste Management Strategy was approved by Corporate Committee on 19 June and ratified on 27 June. Monitoring across all Council buildings indicates 13.8% of waste was compostable and 25.03% was recyclable. Work continues to encourage a reduction in the waste going to landfill.

3. Increase the amount of waste for recycling produced by Council buildings

5

Corporate objective

PLACE: We will ensure we make the very best of the natural, cultural and environmental assets in our Borough

Improvement Objective 4 : We will improve street cleanliness.

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability Efficiency Innovation

What are we going to do this year? Introduce Town Centre Wardens in five towns and revise sweeping schedules to focus more on litter hot spots.

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

1. Introduce Town Centre Wardens in five towns

Not yet commenced. Assimilation process for remaining cleansing staff commenced in October with the target to complete by end of March 2019. This process will include the filling of the Town Warden posts

All drivers have been assimilated and the majority of generic Refuse, Recycling and Street Cleansing Operative posts. Job Descriptions have been drafted for the Town Centre Wardens? Once in post the TCWs will deal with any cleansing issues in town centre areas, cleaning down street furniture, removal of fly posters, graffiti, etc. and will act as a contact point for traders regarding any cleansing issues.

2. Revise sweeping schedules to focus more on litter hot spots.

Sweeping schedules been not yet been revised. However, surveys have been carried out by the Neighbourhood Team and through reviewing complaints received 30 dog fouling hot spots have been identified which will be the focus of the new schedules.

6

Corporate objective

PROSPERITY: We will ensure the Borough’s towns and rural localities are prosperous, vibrant and attractive.

Improvement Objective 5 – We will support and invest in our Borough to promote economic growth, regeneration and sustainability

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability Efficiency Innovation

What are we going to do this year?

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

1. Support women to move into business creation and development through the NI Women in Enterprise Challenge Programme which is replacing the previous planned action in order to better meet needs and to complement existing business start provision.

Agreement to proceed with programme for year 1 agreed by Council in April 2018. Collaboration agreement drafted and with legal – programme scheduled to commence November 2018

Further legal advice was sought on the details for the implementation of the NI Women in Enterprise Challenge Fund programme. Collaboration document between all participating Councils has been prepared and to be issued to Councils for approval. It is now anticipated that the programme will only get underway in January 2019.

2. Feed into a borough marketing strategy with the creation of a proposition to promote Ards and North Down as an attractive destination to do business and invest

Terms of Reference in development for Borough proposition.

Terms of reference

• Visitor element of Borough Proposition in development

• investor element of Borough Proposition in development

3. Create an Economic Development Forum

Inaugural meeting held 18 June 2018. 22 of the 54 companies invited were available to attend. Terms of Reference have been agreed. Next meeting scheduled for 2 October 2018.

There were no meetings of the ED Forum in Q2. Preparatory work was undertaken to confirm membership and data sharing. Planning activity was undertaken to prepare for meeting on 2 October.

7

Corporate objective

PERFORMANCE: We will ensure we take time to understand our customer’s needs and manage our people, money and assets effectively so we can deliver on our objectives for the Borough.

Improvement Objective 6 – We will improve customer access to services and functions provided by the Council and improve their efficiency

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability Efficiency Innovation

What are we going to do this year? We will improve customer access to services through:

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

1. Launching an online application service for licensing.

In progress. Discussions have been held with Tascomi but at the present this is not high on their priorities to provide. Work is ongoing to better utilise the current online Tascomi licensing package to improve the service provided to licensees. It is expected that the service will be available by March 2019.

2. Implementing an electronic Grant Management System.

In progress A number of meetings have taken place with the Performance Improvement Unit to develop a business case for the project. The draft business case has now been developed and will be presented to committee in January for consideration.

3. Developing the Planning Service webpages to include FAQs on popular topic areas

Work is ongoing to update the Planning Service webpages to enable fast sourcing of information and self-service, and will cover trees, enforcement, permitted development and the application process

The Planning Service webpages have been updated to include information on Planning Enforcement, Trees ie. TPO’s, Conservation and How to make a request for a TPO, and information on the Pre-planning Application Discussions. Work on updating the website continues and will shortly include a portal for the public to query locations of TPO’s.

4. Introducing online reporting for environmental based issues.

In progress The decision has been made to pause these plans for the following reasons:

• We are in the process of reassessing the response to service requests particularly in relation to dog fouling and littering/fly tipping. The current process sees all such requests automatically assigned to NET to assess whether there are any enforcement opportunities. Evidence suggests that in the majority of cases the member of the public is in fact simply making a cleansing request. Before any new system is implemented this decision would need finalized at HOS level.

• An Elected Member brought forward a query with regard to the ReportAll system used by some Councils. This was investigated and concerns were raised that there could be a significant increase in workload for our Admin team as ReportAll is not linked to our current software solution resulting in each report requiring manual entry to Te-Care. Further clarification is to be sought as to whether the systems could be linked and at what cost.

• Utilisation of Council Direct has also been considered and an anonymous reporting form created by the software supplier. However, there concerns that anonymous reporting may result in a high volume of potentially unfounded incidents being created and the associated issues around the resourcing of this.

In view of the above it is unlikely that online reporting for environmental based issues will be in place by March 2019.

5. Implement Mobile working for Environmental Health Service

Awaiting input from Supplier with regard to mobile working for Environmental Health

Owing to software functionality issues we are reviewing the situation with the current vendor. In view of this and potential issues around EU exit it is unlikely that Mobile working for EHS will be in place by March 2019.

6. Introduce a Purchase-2-Pay system Purchase-2-Pay Project commenced 7/9/2018

The Purchase-2-Pay project commenced on 7 September and is progressing. It is expected that the system will be in place by March 2019.

8

Corporate objective

PERFORMANCE: We will ensure we take time to understand our customer’s needs and manage our people, money and assets effectively so we can deliver on our objectives for the Borough.

Improvement Objective 6 – We will improve customer access to services and functions provided by the Council and improve their efficiency

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability Efficiency Innovation

What are we going to do this year? We will improve customer access to services through:

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

7. Integration of back-office systems (HR, Employee Payments, Time and Attendance)

Integration of back-office systems (HR, Payroll, Time and Attendance) Project commenced 3/9/2018

Integration of back-office system commenced on 3 September and the mobilisation phase of the project was completed by the due date. Work on the Information Gathering and Data Migration phases is ongoing.

8. Develop protocol with Building Control to ensure submitted applications have benefit of appropriate planning approval where necessary

Building Control protocol project commenced 03/09/2018

The project commenced on 3 September and an employee has been put in place to check Planning Approval status on new Building Control Applications being received. Work is ongoing between Planning and Building Control to update the BC Application Forms to ensure appropriate Planning Approval information is received.

9

Corporate objective

PERFORMANCE: We will ensure we take time to understand our customer’s needs and manage our people, money and assets effectively so we can deliver on our objectives for the Borough.

Improvement objective 7 - We will reduce staff absence levels across the Council.

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability

Efficiency Innovation

What are we going to do this year?

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

1. Continue to monitor and manage absence to reduce the average days lost per employee

• Average days lost per employee with sickness absence has decreased and is getting closer to the target set.

• % absence is 6.49% -v- Target of 5%. Although there has been some improvement regarding short term absenteeism in the first quarter, it is critical that there is continual monitoring of procedures and processes in order to bring the % target in line with the target of 5%.

• HoST is currently setting up a Managing Absence working group to get innovative ideas from across the Council to address high absenteeism.

Average days lost in Q2 : 12.2 an improvement on Q1 of 0.4%. YTD figure is 16.17. Absence in Q2 is 6.67% an improvement of 0.18% on. Short term absence shows a slight improvement of 0.03% (Q2 1.46% -v- Q1 1.49%), long term absence continues to rise 0.20% increase in the period. In the period there was an increase in absence due to:

• Stress, depression, mental health and fatigue of 11.27%

• Back and neck problems 18.36% However, absence due to Musculo-skeletal problems decreased by 13.84%.

The HR and OD service continues to manage absence through its Absence Management policy via the following initiatives:

• Employees identified as suffering from stress are immediately referred to occupational health;

• Employees absent due to stress are offered to attend a ‘stress Management programme’ run by the South-Eastern Health and Social Care Trust;

• Employees absent from work for a period of 4 weeks are referred to occupational health;

• Regular counselling meetings take place with staff who are ill in an attempt to enable them to return to work;

• Flu vaccine has been offered, free of charge, to all staff in an attempt to reduce flu-related absence;

• Council has recently had a Mental Health Charter agreed at Committee and consultation is currently taking place with unions and staff regarding this;

• A number of events have been organised to encourage staff to improve their health and wellbeing eg the step challenge;

• Refresher training on the Staff Absence Management Policy has recently taken place to ensure managers are well equipped to deal with staff absences.

Year one of ‘Our People Plan’ aims to improve staff engagement which in turn it is anticipated by having a more motivated and engaged workforce will reduce absenteeism. A number of events e.g. sports day, staff breakfasts etc have been held to encourage more engagement.

2. Delivery of Our People Plan Delivery of Our People Plan is in progress.

Part of the overall OD Strategy, Our People Plan launched in June 2018 focusses on 4 high level promises that were the result of employee engagement sessions in January 2018 - a copy of the plan is attached for

10

Corporate objective

PERFORMANCE: We will ensure we take time to understand our customer’s needs and manage our people, money and assets effectively so we can deliver on our objectives for the Borough.

Improvement objective 7 - We will reduce staff absence levels across the Council.

Improvement aspects:

Strategic Effectiveness

Service Quality

Service Availability

Fairness Sustainability

Efficiency Innovation

What are we going to do this year?

Action: Progress at Q1 2018/19 Progress at Q2 2018/19 Current RAG Status

reference. Progress against the promises in Quarter 2 is as follows:

• Consultation on Service Plans – a number of workshops have been held with teams;

• Assimilations ongoing – 81% of employees are either recruited or assimilated into the AND structure;

• Survey on Employee Awards has been prepared for circulation and promoted in News AND Info;

• 4 Social events were held in the period at locations across the Borough and involved participation of 302 employees. Members of CLT and HoST attended these sessions

Work to progress the delivery of Our People Plan is ongoing.

3. Roll out of the Organisational Development Strategy

Roll out of the Organisational Development Strategy is in progress.

Work continues to progress the delivery of the OD Strategy with the following actions having been carried out in Quarter 2:

• Employee engagement continues via joint CLT/HOST workshop, Business Conference and Health and Wellbeing events;

• Citizen Space Survey on Review of Pride in Performance Conversation Scheme;

• Customer Excellence Working Group Year 1 Action Plan completed;

• Launch of Behaviour Charter Guidance via special team briefs.

11

STATUTORY INDICATORS

PLANNING STATUTORY INDICATORS – latest available figures refer to Q1 April-June 2018/19

Average processing time of local planning applications

Processing time for local planning applications was 15.9 weeks (an improvement of 1.5 weeks on the same period last year).

In the period the Council received 243 applications with 204 applications being decided. Processing times dependent on front loading by applicants, response times by consultees and volume of objections received.

Average processing time of major planning applications

267.8 weeks (an increase of 170 weeks on the same period last year).

The 2 applications decided comprised a 2013 application for the redevelopment of Crawfordsburn Country Club which underwent a large number of revisions and required a legal agreement; and a 2015 quarrying application which had an associated enforcement case. Determination of these two major cases represented further reduction in the number of outstanding legacy DOE applications which transferred to the Council – from 577 to 12.

Percentage of enforcements cases processed and concluded within 39 weeks.

72.6% (a reduction of 3.7% on the same period last year).

Ards and North Down had the fourth highest number of enforcement cases opened across the 11 councils. An enforcement case is opened when a member of the public or a planning officer reports an alleged breach. An enforcement case is concluded when one of the following occurs: a notice is issued; legal proceedings commence; a planning application is received; or the case is closed. The number of cases concluded in each quarter depends greatly on the particulars of each case.

WASTE STATUTORY INDICATORS – latest available figures refer to Q1 April-June 2018/19

Percentage of household waste collected by the district council that is sent for recycling (including waste prepared for re-use)

54.8% (Q1 same period last year 52.3 an increase of 2.5%)

The amount (tonnage) of biodegradable Local Authority collected municipal waste that is landfilled

4,814 (Q1 same period last year 4,796 – increase of 18 tonnes)

The amount (tonnage) of Local Authority collected municipal waste arisings

25,138 (Q1 same period last year 24,987)

ECONOMIC DEVELOPMENT INDICATOR – latest available figures refer to YTD 30 September 2018/19

Number of jobs promoted through start-up activity via the Go for It Programme

The current number of jobs promoted between 1 April and 30 September is 56 and remains on target to achieve or exceed 85 by end March 2019.

Unclassified

Page 1 of 2

ITEM 6

Ards and North Down Borough Council

Report Classification Unclassified

Council/Committee Audit

Date of Meeting 17 December 2018

Responsible Director Director of Finance and Performance

Responsible Head of Service

Head of Performance and Projects

Date of Report 03 December 2018

File Reference 260501 - Performance Management

Legislation Local Government Act (2014) Northern Ireland

Section 75 Compliant Yes ☒ No ☐ Other ☐

If other, please add comment below:

Subject Performance Improvement Plan 2018/19 - Update on Key Actions

Attachments Audit Committee progress update - Quarter 2 2018-19

The Local Government Act (Northern Ireland) 2014 Part 12 put in place a new framework to support continuous improvement in the delivery of council services. The Council is required each year to determine its priorities for improvement which are aligned to the Community Plan and Corporate Objectives and to publish these in the format of an Improvement Plan.

In the 2018/19 year council’s Performance Improvement Plan (PIP) identified 7 improvement objectives with a corresponding 27 actions together with 7 Statutory Indicators, all of which are included in the Council’s Service Plans which are monitored and reported on through each Service’s respective Standing Committee.

The following table gives an overall assessment of the status across all actions in the PIP the detail of which can be found in the attached progress report.

Unclassified

Page 2 of 2

Summary Table of Progress against Our Improvement Objectives for 2018/19

Corporate Plan Theme

Improvement Objective Aggregated RAG Status across all actions

PEOPLE We will support local communities to develop community

resilience for emergency planning.

PLACE We will increase recycling and divert waste from landfill We will ensure we make the very best of the natural, cultural

and environmental assets in our Borough

We will improve street cleanliness PROSPERITY We will support and invest in our Borough to promote

economic growth, regeneration and sustainability

PERFORMANCE We will improve customer access to services and functions

provided by the Council and improve their efficiency

We will reduce staff absence levels across the Council

OVERALL

RECOMMENDATION

It is recommended that the report is noted.

1

Ards and North Down Borough Council

Audit and Assessment Report 2018-19

Report to the Council and the Department for Communities

under Section 95 of the Local Government (Northern

Ireland) Act 2014

Draft: 30 November 2018

2

Contents

1. Key Messages

2. Audit Scope

Page

3

5

3. Audit Findings 6

4. Annexes 8

We have prepared this report for sole use of the Ards and North Down Borough Council and the Department for

Communities. You must not disclose it to any third party, quote or refer to it, without our written consent and we

assume no responsibility to any other person.

3

1. Key Messages

Summary of the audit

Audit outcome

Status

Audit opinion

Unqualified opinion

Audit assessment

The Local Government Auditor (LGA) has not drawn a conclusion [this year only]

Statutory recommendations

The LGA made no statutory recommendations

Proposals for improvement

The LGA made two new proposals for improvement

This report summaries the work of the LGA on the 2018-19 performance improvement audit and

assessment undertaken on Ards and North Down Borough Council. We would like to thank the Chief

Executive and his staff, particularly the Performance Improvement Manager, for their assistance

during this work.

We consider that we comply with the Financial Reporting Council (FRC) ethical standards and that, in

our professional judgment, we are independent and our objectivity is not compromised.

Audit Opinion

The LGA has certified the performance arrangements with an unqualified audit opinion, without

modification. She certifies that an improvement audit and improvement assessment has been

conducted. The LGA also states that, as a result, she believes that Ards and North Down Borough

Council (the Council) has discharged its performance improvement and reporting duties, including its

assessment of performance for 2017-18 and its 2018-19 improvement plan, and has acted in

accordance with the Guidance.

Audit Assessment

The LGA has assessed whether the Council is likely to comply with its performance improvement

responsibilities under Part 12 of the Local Government Act (Northern Ireland) 2014 (the Act). This is

called the ‘improvement assessment’.

4

The Council has discharged its duties in respect of Part 12 of the Act as far as possible, in that its

arrangements continue to mature. It remains too early for the Council to demonstrate a track

record of improvement: consequently, it is not possible for the LGA to conclude as to the extent of

improvement that may be made. The LGA did not exercise her discretion to assess and report

whether the council is likely to comply with these arrangements in future years.

This is the second year in which councils have been required to fulfil their full statutory

responsibilities under Part 12 of the Act. In the LGA’s opinion councils should be able to

demonstrate a track record of improvement in 2019 to allow a full assessment to be made.

Audit Findings

During the audit and assessment we identified no issues requiring a formal recommendation under

the Act. We made two proposals for improvement (see Section 3). These represent good practice

which should assist the Council in meeting its responsibilities for performance improvement.

Detailed observations on thematic areas are provided in Annex C and progress on proposals for

improvement raised in prior years has been noted in Annex B.

Status of the Audit

The LGA’s audit and assessment work on the Council’s performance improvement arrangements is

now concluded. By March 2019 she will publish an Annual Improvement Report on the Council on

the NIAO website, making it publicly available. This will summarise the key outcomes in this report.

The LGA did not undertake any Special Inspections under the Act in the current year.

The total audit fee charged is in line with that set out in our Audit Strategy.

Management of information and personal data

During the course of our audit we have access to personal data to support our audit testing. We

have established processes to hold this data securely within encrypted files and to destroy it where

relevant at the conclusion of our audit. We can confirm that we have discharged those

responsibilities communicated to you in accordance with the requirements of the General Data

Protection Regulations (GDPR) and the Data Protection Act 2018.

5

2. Audit Scope

Part 12 of the Act provides all councils with a general duty to make arrangements to secure

continuous improvement in the exercise of their functions. It sets out:

a number of council responsibilities under a performance framework; and

key responsibilities for the LGA.

The Department for Communities (the Department) has published ‘Guidance for Local Government

Performance Improvement 2016’ (the Guidance) which the Act requires councils and the LGA to

follow. A multi-stakeholder group comprising of representatives of the Department and councils has

been established and a subgroup of this has drafted guidance to clarify the requirements of the

general duty to improve. A working draft has been agreed and further improvements to reporting

on the general duty are expected in 2019.

The improvement audit and assessment work is planned and conducted in accordance with the

Audit Strategy issued to the Council, the LGA’s Code of Audit Practice for Local Government Bodies

in Northern Ireland and the Statement of Responsibilities.

The improvement audit

Each year the LGA has to report whether each council has discharged its duties in relation to

improvement planning, the publication of improvement information and the extent to which each

council has acted in accordance with the Department’s Guidance. The procedures conducted in

undertaking this work are referred to as an “improvement audit”. During the course of this work the

LGA may make statutory recommendations under section 95 of the Act.

The improvement assessment

The LGA also has to assess annually whether a council is likely to comply with the requirements of

Part 12 of the Act, including consideration of the arrangements to secure continuous improvement

in that year. This is called the ‘improvement assessment’. She also has the discretion to assess and

report whether a council is likely to comply with these arrangements in future years.

The annual improvement report on the Council

The Act requires the LGA to summarise all of her work (in relation to her responsibilities under the

Act) at the Council, in an ‘annual improvement report’. This will be published on the NIAO website

by March 2019, making it publicly available.

Special inspections

The LGA may also, in some circumstances, carry out special inspections which will be reported to the

Council and the Department, and which she may publish.

6

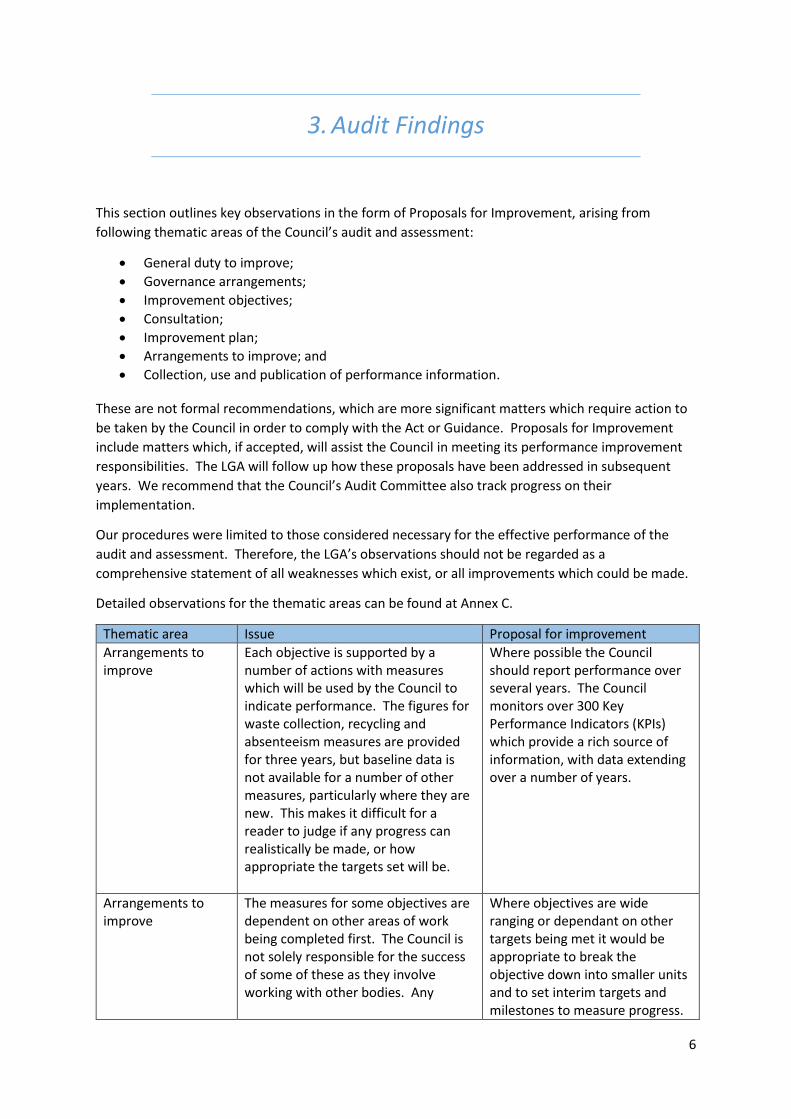

3. Audit Findings

This section outlines key observations in the form of Proposals for Improvement, arising from

following thematic areas of the Council’s audit and assessment:

General duty to improve;

Governance arrangements;

Improvement objectives;

Consultation;

Improvement plan;

Arrangements to improve; and

Collection, use and publication of performance information.

These are not formal recommendations, which are more significant matters which require action to

be taken by the Council in order to comply with the Act or Guidance. Proposals for Improvement

include matters which, if accepted, will assist the Council in meeting its performance improvement

responsibilities. The LGA will follow up how these proposals have been addressed in subsequent

years. We recommend that the Council’s Audit Committee also track progress on their

implementation.

Our procedures were limited to those considered necessary for the effective performance of the

audit and assessment. Therefore, the LGA’s observations should not be regarded as a

comprehensive statement of all weaknesses which exist, or all improvements which could be made.

Detailed observations for the thematic areas can be found at Annex C.

Thematic area Issue Proposal for improvement

Arrangements to improve

Each objective is supported by a number of actions with measures which will be used by the Council to indicate performance. The figures for waste collection, recycling and absenteeism measures are provided for three years, but baseline data is not available for a number of other measures, particularly where they are new. This makes it difficult for a reader to judge if any progress can realistically be made, or how appropriate the targets set will be.

Where possible the Council should report performance over several years. The Council monitors over 300 Key Performance Indicators (KPIs) which provide a rich source of information, with data extending over a number of years.

Arrangements to improve

The measures for some objectives are dependent on other areas of work being completed first. The Council is not solely responsible for the success of some of these as they involve working with other bodies. Any

Where objectives are wide ranging or dependant on other targets being met it would be appropriate to break the objective down into smaller units and to set interim targets and milestones to measure progress.

7

Thematic area Issue Proposal for improvement

slippage will impact on the achievement of the overall objective.

8

4. Annexes

9

Annex A – Audit and Assessment Certificate

Audit and assessment of Ards and North Down Borough Council’s performance improvement

arrangements

Certificate of Compliance

I certify that I have audited Ards and North Down Borough Council’s (the Council) assessment of its

performance for 2017-18 and its 2018-19 improvement plan in accordance with section 93 of the

Local Government Act (Northern Ireland) 2014 (the Act) and the Code of Audit Practice for local

government bodies.

I also certify that I have performed an improvement assessment for 2018-19 at the Council in

accordance with Section 94 of the Act and the Code of Audit Practice.

This is a report to comply with the requirement of section 95(2) of the Act.

Respective responsibilities of the Council and the Local Government Auditor

Under the Act, the Council has a general duty to make arrangements to secure continuous

improvement in the exercise of its functions and to set improvement objectives for each financial

year. The Council is required to gather information to assess improvements in its services and to

issue a report annually on its performance against indicators and standards which it has set itself or

which have been set for it by Government departments.

The Act requires the Council to publish a self-assessment before 30 September in the financial year

following that to which the information relates, or by any other such date as the Department for

Communities (the Department) may specify by order. The Act also requires that the Council has

regard to any guidance issued by the Department in publishing its assessment.

As the Council’s auditor, I am required by the Act to determine and report each year on whether:

The Council has discharged its duties in relation to improvement planning, published the required improvement information and the extent to which the Council has acted in accordance with the Department’s Guidance in relation to those duties; and

The Council is likely to comply with the requirements of Part 12 of the Act.

Scope of the audit and assessment

For the audit I am not required to form a view on the completeness or accuracy of information or

whether the improvement plan published by the Council can be achieved. My audits of the Council’s

improvement plan and assessment of performance, therefore, comprised a review of the Council’s

publications to ascertain whether they included elements prescribed in legislation. I also assessed

whether the arrangements for publishing the documents complied with the requirements of the

legislation, and that the Council had regard to statutory guidance in preparing and publishing them.

For the improvement assessment I am required to form a view on whether the Council is likely to

comply with the requirements of Part 12 of the Act, informed by:

A forward looking assessment of the Council’s likelihood to comply with its duty to make arrangements to secure continuous improvement; and

A retrospective assessment of whether the Council has achieved its planned improvements to inform a view as to its track record of improvement.

10

My assessment of the Council’s improvement responsibilities and arrangements, therefore,

comprised a review of certain improvement arrangements within the Council, along with

information gathered from my improvement audit.

The work I have carried out in order to report and make recommendations in accordance with

sections 93 to 95 of the Act cannot solely be relied upon to identify all weaknesses or opportunities

for improvement.

Audit opinion

Improvement planning and publication of improvement information

As a result of my audit, I believe the Council has discharged its duties in connection with (1)

improvement planning and (2) publication of improvement information in accordance with section

92 of the Act and has acted in accordance with the Department for Communities’ guidance

sufficiently.

Improvement assessment

As a result of my assessment, I believe the Council has as far as possible discharged its duties under

Part 12 of the Act and has acted in accordance with the Department for Communities’ guidance

sufficiently.

The 2018-19 year was the third in which councils were required to implement the new performance

improvement framework. The Council’s arrangements to secure continuous improvement, as is to

be expected, are still developing and embedding. The Council continues to strengthen its

arrangements to secure continuous improvement, and has delivered some measurable

improvements to its services in 2017-18. However, until the Council’s arrangements mature and it

can demonstrate a track record of ongoing improvement in relation to the framework, I am unable

to determine the extent to which improvements will be made.

I have not conducted an assessment to determine whether the Council is likely to comply with the

requirements of Part 12 of the Act in subsequent years. I will keep the need for this under review as

arrangements become more fully established.

Other matters

I have no recommendations to make under section 95(2) of the Local Government (Northern

Ireland) Act 2014.

I am not minded to carry out a special inspection under section 95(2) of the Act.

Pamela McCreedy

Local Government Auditor

Northern Ireland Audit Office

106 University Street

Belfast

BT7 1EU

30 November 2018

11

Annex B – Follow up of implementation of prior year proposals for improvement

Year of report

Reference Proposal for improvement Action taken by Council Status

General Duty to Improve

2016-17 GD1/2017 Linking the forthcoming community plan, and the ongoing processes that underpin it, with the Council’s improvement processes.

Implemented

2016-17 GD2/2017 Analyse any trends from the performance management system as further data becomes available. This will help identify those functions/services which would benefit most from improvement.

Implemented

2017-18

GD1/2018

The Council should continue the development of its performance management system to achieve the best measurement of all its functions and services, to ensure identification of those areas which would benefit most from improvement.

The Council has continued to work in this area and this is an ongoing process. Performance management is continuing to develop.

In progress

2017-18 GD2/2018 The Council should ensure that the process through which functions are prioritised and selected for improvement forms the basis for objective-setting in a ‘bottom up’ approach. This should provide a better link between objective and actions, help to improve transparency, and help with the measurement of the objective outcomes.

The Council’s service planning template was updated in October 2017 to improve quality and focus during the early stages of service planning and to ensure performance improvement initiatives were identified. Further development of service planning is underway and in the 2018-19 year will be combined with the budget planning

In progress

12

Year of report

Reference Proposal for improvement Action taken by Council Status

process to ensure that appropriate financial resources are allocated to both business as usual and performance initiatives. While the Council consults with residents and stakeholder groups and encourages responses from them during the year, many of the actions are corporate and inward looking. The council needs to continue to work on the “bottom up” approach and to make the link between objectives and actions very clear to ensure that the actions identified will provide measurable benefits to ratepayers.

2017-18 GD3/2018 The Council should ensure that performance framework documentation is updated in line with documented procedures and that evidence of review is recorded (even where no changes have occurred).

The Performance Framework documentation is currently being updated to reflect the process changes mentioned above.

In progress

Governance Arrangements

2016-17 GA1/2017 Terms of Reference for the Audit Committee should be updated to reflect its specific performance improvement responsibilities.

Implemented

2016-17 GA2/2017

Performance improvement should feature as a regular item on the Audit Committee agenda.

Implemented

13

Year of report

Reference Proposal for improvement Action taken by Council Status

2016-17 GA3/2017 The Corporate Leadership Team should facilitate Members on each of the relevant standing committees and the Audit Committee with training and support to discharge the performance improvement responsibilities.

Implemented

2016-17 GA4/2017

The Audit Committee should monitor the activity of any committee specifically charged with the scrutiny of performance improvement.

Implemented

2016-17 GA5/2017 The Audit Committee should consider the benefit of using internal audit, where required, to provide it with future assurance on the integrity and operation of the Council's performance framework and identify areas for improvement.

The Audit Committee receives internal audit reports at each quarterly meeting. The internal audit plan for 2018-19 does not refer specifically to work being carried out on improvement, or on auditing the measures associated with it. Such work would provide the Committee with valuable assurance and additional insight on these areas.

Partially implemented

2017-18 GA1/2018 Senior management should establish a central review role at committee level and ensure that all relevant Committees and the Audit Committee are provided with more detailed performance improvement documentation to carry out their scrutiny and monitoring functions.

Implemented

14

Year of report

Reference Proposal for improvement Action taken by Council Status

Improvement Objectives

2016-17 IO1/2017 Going forward, ensure that each improvement objective is focused on outcomes for citizens in relation to improved functions and/or services rather than focusing primarily on achieving corporate efficiencies.

While six of the seven 2018-19 improvement objectives do focus on outcomes for citizens, at the action level it is not always clear how citizens will benefit from some specific actions, or how they relate directly to the overall objective. There is a possibility that actions may not be directly relevant to the achievement of the objective.

Partially implemented

2016-17 IO2/2017 In relation to the improvement objectives, more detail is required in the ‘performance improvement plan’ so that it is clear to a reader how citizens will be better off if the Council improves as it intends to.

Implemented

2016-17 IO3/2017 Ensure that improvement can be demonstrated and, where possible, measured through the use of meaningful performance indicators and data collection and/or other qualitative methods. These indicators should not just concentrate around, nor be limited to, the statutory indicators and standards imposed by central government. Where possible and relevant, the Council should use baseline performance data/information against which future improvement can be demonstrated.

The use of indicators and data collection was also raised in 2017-18 – see IO2/2018 and IO3/2018 below. The 2018-19 objectives include a wider range of measures and are not limited to statutory indicators. However, because these have not been used in the past, there is no historic data available to provide a baseline or to justify the proposed target. Further work in this area will be required.

In progress

15

Year of report

Reference Proposal for improvement Action taken by Council Status

2017-18 IO1/2018 The Council should link the improvement objectives more closely to the identified actions, keeping in mind the intended outcomes. A bottom-up approach to objective setting may help the Council to avoid improvement objectives that are too broad and open-ended. It should also narrow the gap in the council’s ability to clearly demonstrate the impact on the outcomes for citizens.

The revised service planning template introduced for 2018-19 was designed to assist officers to identify performance improvement initiatives at an early stage, to clearly link them through the Corporate and Community Plans and to identify the outcome of the initiative and what difference it would make to stakeholders. However, objectives remain broad and it is not always clear from the measures that an action should be started or completed by a particular date. More consideration should be given to breaking down objectives, and ensuring that the related actions will deliver progress towards meeting them.

In progress

2017-18 IO2/2018 The Council should ensure that underlying projects are more focused on outcomes or that the collective outputs contribute to an evidence-based outcome at the objective level. The outcome(s) should always be clearly stated so that citizens can understand how they will benefit.

The self-assessment report for the 2017-18 Performance Improvement Plan shows that the indicators or standards selected have not always been suitable for measuring progress against outcomes. The Council has acknowledged this.

In progress

2017-18 IO3/2018 Where possible and relevant, the Council should use baseline performance data/information (and set standards which it hopes to achieve) against which future improvement can be demonstrated.

Where available baseline data has been introduced, however there are a number of objectives where outturn data is not available for previous years.

In progress

16

Year of report

Reference Proposal for improvement Action taken by Council Status

The Council should continue to work on identifying appropriate indicators and standards which will demonstrate clearly that improvement has been achieved. The Council should also continue to work towards identifying benchmarks with other councils.

Consultation

2016-17 C1/2017 Continue to raise the profile and transparency of the performance improvement framework throughout the year on the Council's website and other communication channels for example social media, citizen magazines etc.

Implemented

2016-17 C2/2017 Encourage citizens and stakeholders to contribute at any time during the year by providing contact details on the Council website.

Implemented

2016-17 C3/2017 Consider other methods of obtaining views (as well as service level feedback) from citizens and organisations, for example, a citizen panel, staff and councillor workshops and focus groups.

Implemented

17

Year of report

Reference Proposal for improvement Action taken by Council Status

Collection, use and publication of performance information

2017- 2018

CUP1/2018 In addition to the local indicators and standards relating specifically to improvement objectives, the Council should select a range of local indicators and standards to enable it to measure and monitor improvement across its full range of functions, as part of its general duty arrangements to continuously improve. This information should be included in the published Performance Improvement Plan and Annual Self-Assessment Report and provide year on year comparisons. The Council should continue working with other councils and the Department to agree a suite of self-imposed indicators and standards. This will enable meaningful comparisons to be made and published in line with its statutory responsibility.

The Council has 16 individual service plans that include over 300 KPIs that are monitored in the quarterly service plan reports brought before committees. It is the Council’s view that if the corporate performance and service plans are aligned and integrated then the KPIs at the lowest level ensures that all plans are monitored. However, this detailed information is not included in the Performance Improvement Plan or the self-assessment report. The Improvement Plan includes three non-statutory measures apart from those used in the objectives, but these do not cover the whole range of Council activities. The Council continues to work with the sector, the Association of Public Sector Excellence (APSE) and the Department for Communities in order to inform future self-imposed indicators and to explore potential bench-marking opportunities. A sub group of the Multi-Stakeholder group was tasked with drafting guidance to

In progress

18

Year of report

Reference Proposal for improvement Action taken by Council Status

clarify the requirements of the General Duty to Improve. A working draft has now been agreed and we expect that further improvements to reporting on the General Duty will be made in 2019.

2017-18 CUP2/2018 Self-assessment reports must clearly set out a section on performance in relation to its general duty to improve as required under the legislation.

To better show compliance with legislation the Council should clearly set out its assessment of its performance under Part 12 of the Local Government Act (NI) 2014 regarding the General Duty to Improve in the next self-assessment report.

Not implemented

2017-18 CUP3/2018 Self-assessments should not focus solely on the underlying projects but also include an assessment of the Council’s progress in delivering its improvement objectives.

The self-assessment reviews progress on each of the objectives set for 2017-18 however the focus is at a detailed operational level rather than looking at the achievement of the overall improvement objectives and it is difficult in some cases to gauge how successful it was. The Council should review the reporting of its objectives to ensure that it addresses this appropriately.

Not Implemented

19

Annex C – Detailed observations

Thematic area Observations

General duty to improve The Council has continued to work on the General Duty to Improve. The service planning template has been updated and in 2018-19 this will be combined with the budget planning process to ensure a joined up approach. The council has aligned the Improvement Plan and its objectives to The Big Plan 2017-32 (the Council’s Community Plan) and also to the Council Corporate Plan 2015-19. These documents are clearly referred to in the Improvement Plan and are easily accessed from the Council website. However, in the Self-Assessment Report the council has not clearly set out a section on performance in relation to its general duty to improve as required under the legislation. The Council should ensure that it complies with all of the requirements to ensure that there is transparent reporting of the work carried out for performance improvement. A sub group of the Multi-Stakeholder group was tasked with drafting guidance to clarify the requirements of the General Duty to Improve. A working draft has now been agreed and we would expect that further improvements to reporting on the General Duty will be made in 2019.

Governance arrangements In response to a recommendation made last year by NIAO that senior management should establish a central review role to ensure that improvement objectives are subject to appropriate and consistent scrutiny and challenge, the Council has amended the Terms of Reference for the Audit Committee so that a report on progress against the Performance Improvement Plan will be brought to future Audit Committee meetings, and, that going forward, the Audit Committee will be responsible for monitoring progress in respect of the Performance Improvement Plan. The Council should consider the role internal audit could play in providing independent validation and assurance on the integrity and operation of the Performance Improvement Framework and the processes in place which feed into it.

Improvement objectives The 2018-19 Improvement Plan contains seven objectives. These are clearly linked to the Corporate Plan priorities and also to the associated Big Plan – the Council’s Community Plan. Each of the objectives has associated actions and outcomes, as well as measures, and there is a lead officer for each objective.

20

Thematic area Observations

In last year’s report we commented that not all of the projects, outcomes and targets were outcome based, some of the objectives were at a strategic level and were broad and open ended. The objectives set out for 2018-19, however, remain at a high level and the detail for each objective lies in the actions. A number of these actions are strategic or refer to administrative processes within the council, and it therefore is not always clear how they relate to an improvement in performance which will benefit ratepayers.

Consultation The Council has continued to consult with stakeholders and citizens and encourages them to engage in the performance improvement process. This is being addressed pro-actively, though “Your Opinion Matters” which is an ongoing campaign which will run continuously and is advertised in the Borough Magazine, and on line. The Performance Improvement Plan presents a summary of responses received from consultations but states that “As the majority of feedback was in agreement with the proposals no changes have been made to the Plan”. It is important that stakeholders see that their input is accepted and that changes can be made as a result of it. In future Plans it would be beneficial if proposals submitted under “Your Opinion Matters” could be summarised, with information on which of these suggestions were accepted. If no suggestions are accepted, or no changes are made to the plan following feedback then interested parties may cease to engage with the process as it will not be seen as a valid consultation exercise.

Improvement plan NIAO noted in 2017-18 that although the Performance Improvement Plan did include published statutory indicators and standards it was not clear how it intended to achieve these as there was no description of its plans to meet them, and as a result it was not fully compliant with the legislation. In addition the Council did not publish a range of local (non-statutory) indicators and standards in its plan (other than those relating directly to its improvement objectives and underlying activities). A paragraph headed “Corporate Indicators” has been included in the 2018-19 Performance Improvement Plan with an explanation that the Council has a suite of corporate indicators and that these include statutory indicators and also non statutory indicators. There is also a table showing statutory indicators and four non statutory indicators. Some of the statutory indicators are used to measure performance in the Council’s Performance Improvement Objectives, for example recycling and diverting waste from landfill, but there is no narrative to explain this, nor is there

21

Thematic area Observations

an explanation on how the Council intends to improve its performance on either the statutory indicators, or the non-statutory indicators. In order to comply with the legislation the Council should provide clear information on how it is working to monitor progress on statutory indicators and set out its arrangements to monitor progress against its own self-imposed performance indicators.

Arrangements to improve Each objective is supported by a number of measures which will be used by the council to indicate performance. The Council template allows disclosure of 2016-17 performance, 2017-18 performance to date, and the 2018-19 target. The figures for each of these categories is available primarily for the waste collection and recycling measures, and for absenteeism, but in other objectives, particularly where there are new measures, they are left blank or marked not applicable. There is no indication that alternative measures were explored, either from within the Council or from other comparable bodies. This makes it difficult for the reader to judge if any progress can realistically be made, or how appropriate the targets set will be. The measures for some objectives are dependent on other areas of work being completed first. The achievement of some of these measures is also dependant either on other bodies, or on wider projects in the Council. Any slippage in these will impact on the achievement of the Objective. In some instances it might have been more appropriate to break the objective down into smaller pieces or to set interim targets and milestones to measure progress. In one instance the measure was to begin work by a certain date, without stating a completion date.

Collection, use and publication of performance information

In 2017-18 NIAO noted that in addition to indicators and standards relating specifically to improvement objectives the Council should select a range of local indicators to enable it to measure and monitor improvement across its full range of functions and to publish them in the Performance Improvement Plan (see CUP1/2018 above). The council has published three non-statutory indicators in the Performance Improvement Plan for 2018-19 but it has not set out how it plans to improve performance for these indicators and they do not cover the full range of functions.

22

Thematic area Observations

To date the Council has not provided information which would allow performance improvement to be compared with progress in other councils other than for the statutory indicators. It is important that work to identify comparative information from other bodies continues so that this can be identified and published allowing stakeholders to make an informed assessment of progress on these areas. We note that a Multi-Stakeholder Group has been established which comprises of representatives from the Department for Communities and the Councils, and is also attended by NIAO. The work plan of the group includes consideration of benchmarking. We hope that sufficient progress will be made by September 2019 to allow a broader range of functions to be compared with other councils. The self-assessment report could be improved by:

having a separate section on performance in relation to the general duty to improve; and

ensuring that the review of progress on each of the objectives set for 2017-18, looks at the achievement of the objectives, rather than focussing at an operational level as it currently does. The Council should review its reporting to ensure that it addresses the delivery of the objectives.

Making sure public money is spent properly

Northern Ireland Audit Office 106 University Street

Belfast BT7 1EU

Direct Line : (028) 9025 1076 Fax : (028) 9025 1051 E-mail : [email protected]

www.niauditoffice.gov.uk @NIAuditOffice Stephen Reid Chief Executive Ards and North Down Borough Council Town Hall The Castle Bangor BT20 4BT

13 December 2018 Dear Stephen, Annual Audit Letter 2017-18: Ards and North Down Borough Council Please find enclosed the Annual Audit Letter issued under Regulation 17 of the Local Government (Accounts and Audit) Regulations (Northern Ireland) 2015 and the Code of Audit Practice 2016. Regulation 17 requires a local government body to:

publish (as a minimum on the local government body’s website) the letter; notify the local government auditor of the date of publication, and make copies available for purchase by any person on payment of a reasonable sum.

The Code of Audit Practice 2016 states that whilst it is the responsibility of the Council to publish the annual audit letter, the Local Government Auditor may publish each annual audit letter on the NIAO website to enhance the transparency of public reporting. I would be grateful if you would arrange to include the Annual Audit Letter on the agenda of the next meeting of the Audit Committee. I would like to take this opportunity to thank you and your staff for the assistance and co-operation received throughout the audit. Yours sincerely

PAMELA McCREEDY Local Government Auditor

N I A O

Pamela McCreedy Chief Operating Officer

1

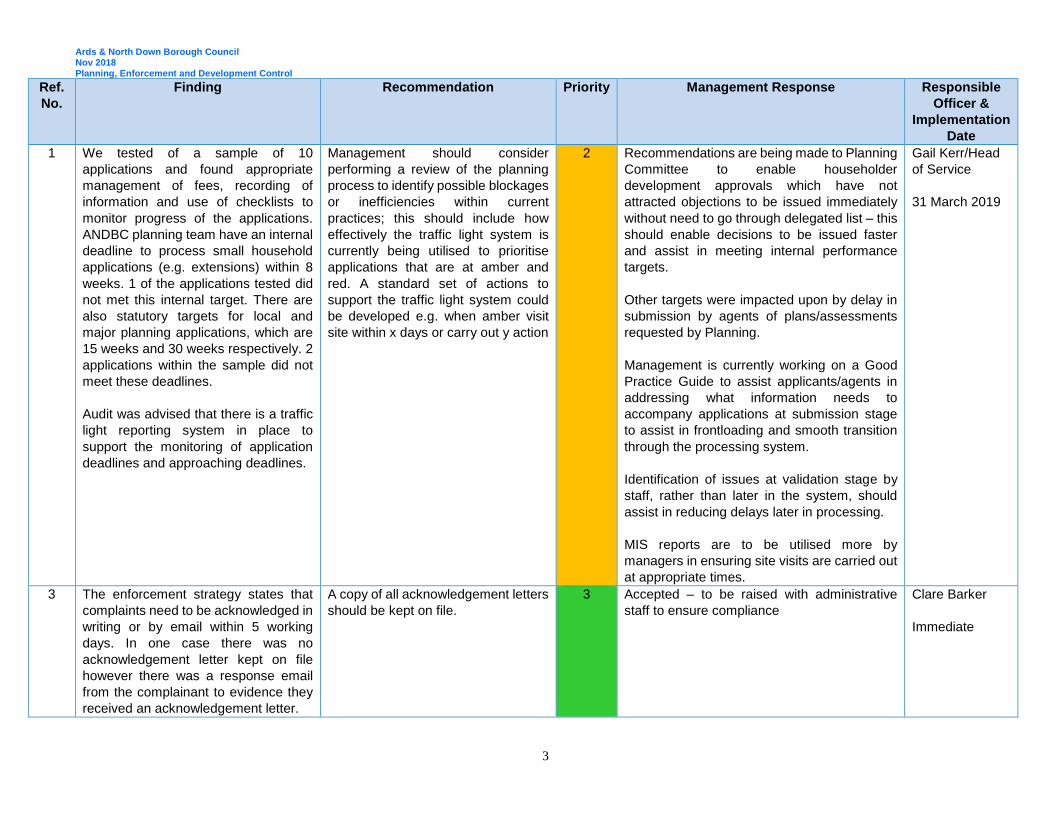

Ards and North Down Borough Council Audit Committee Internal Audit Progress Report September-November 2018 The purpose of this summary report is to inform members of the Audit Committee of work carried out by Internal Audit during the period September-November 2018. Details of the work carried out on completed assignments is contained in the Executive Summary Audit Reports presented to the Committee.

1 Background

Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organisation’s operations. It helps organisations accomplish their objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of the risk management, control and governance processes. The Internal Audit service is currently delivered by Moore Stephens.

2 Progress against Planned Work

During the months of April and May Internal Audit liaised with Council managers to agree proposed timings for each of the audits contained in the Audit Plan for 2018/19 (which was approved by the Audit Committee in March 2018). The current status of each planned audit to be completed by Internal Audit based on the Annual Audit Plan is shown in the table below.

Audit Area Proposed Schedule

Status Assurance Rating

Risk Management November

Fieldwork ongoing -

Partnership arrangements January 2019 - -

PCSP May complete Satisfactory

Information governance and data protection

November Fieldwork complete -

Freedom of Information May/June Complete Satisfactory

Capital project management September Fieldwork complete

and report drafted -

Contract management and contractor monitoring

June

Complete Satisfactory

Planning- enforcement and development control

September Complete and attached

Satisfactory

Building Control August

Complete and attached

Satisfactory

Contract management & operations; Exploris

August Postponed Fieldwork complete and report drafted

-

Staff performance management

September Complete and attached

Satisfactory

Ards & North Down Borough Council Internal Audit Quarterly Update

2

Audit Area Proposed Schedule

Status Assurance Rating

Workforce planning (from 2017/18)

February 2019 Postponed until 2019/20*

-

Travel and subsistence October Complete and

attached Satisfactory

Grant funding July Complete and

attached Satisfactory

Tenders & contracts December ToR agreed -

Income & Cash handling September Fieldwork complete

and report drafted -

Follow-up of prior year recommendations

Ongoing - -

Other

Support relating to risk management and assurance statements

Ongoing - -

Review of Governance Statement Framework

May/June 2018 ongoing -

* this audit is being postponed as the focus of HR has been to fill the posts in the new Council. HR have a

deadline to get all posts filled within the new structure by the end March 2019. For these reasons, an internal

audit of workforce planning is not timely or practical at this point.

3 Issues Arising from Work During Period Reported (September -November)

3.1 Outstanding Management Responses to Draft Reports

None

3.2 Reports Awaiting Sign-Off by the Head of Service

None

3.3 Limited or Unacceptable Assurance Opinion Audits

None.

4 Audits Planned for Next Period (December-March)

The following audits are planned for completion during the next period:

• Partnership Arrangements

• Tenders and Contracts

• Risk Management

Ards & North Down Borough Council Internal Audit Quarterly Update

3

• Information Governance and Data Protection

• Income and Cash Handling

• Follow-up prior year recommendations

5 Performance Indicators

The following sets out progress against performance indicators for the internal audit function.

5.1 Progress against Assurance Assignments in Revised Annual Audit Plan

Progress against Assurance Assignments in Annual Audit Plan

Description No of days

planned

No of days completed

to date

Variance

Risk Management 8 6 ongoing

Partnership arrangements 10 - -

PCSP 6 6 -

Information governance and data protection 10 9 ongoing

Freedom of Information 8 8 -

Capital project management 10 10 -

Contract management and contractor monitoring 10 10 -

Planning- enforcement and development control 10 10 -

Building Control 10 10 -

Contract management & operations; Exploris 10 9 ongoing

Staff performance management 8 8 -

Workforce planning (from 2017/18) * 8 - -

Travel and subsistence 9 9 -

Grant funding 10 10 -

Tenders & contracts 10 - -

Income & Cash handling 10 8 ongoing

Follow-up of prior year recommendations 10 1.5 ongoing

Total assurance days 157 114.5 42.5 days remaining

Support relating to risk management and assurance statements

10 - -

Review of Governance Statement Framework 12 4.5 ongoing

5.2 Acceptance of Audit Recommendations & Client Satisfaction

Other Performance Indicators Progress

Percentage of audit recommendations accepted by management

100%

Client Satisfaction Survey Results Survey’s issued – results will be reported when completed surveys received

Report Ref: ANDBC1819-4

Final December 2018

Ards and North Down Borough Council

INTERNAL AUDIT REPORT

EXECUTIVE SUMMARY

Area of Review: Grant Funding

To: Head of Community and Culture

Head of Regeneration

Head of Building Control, Licensing and Neighbourhood Environment

CC: Director of Community and Well-Being

Director of Regeneration, Development and Planning

Director of Environment

Director of Finance and Performance

From: Internal Audit Service

This report is a confidential internal document intended solely for the use of the above-named individual(s).

The disclosure, copying or contents of this report is strictly prohibited.

Ards & North Down Borough Council October 2018 Grants

TABLE OF CONTENTS

1. INTRODUCTION ................................................................................................................. 1

2. EXECUTIVE SUMMARY ..................................................................................................... 2 3. STATEMENT OF RESPONSIBILITY .................................................................................. 9 4. AUDIT APPROACH .......................................................................................................... 10 APPENDIX 1 - DEFINITIONS ................................................................................................ 12 APPENDIX 2 – POINTS FOR THE ATTENTION OF MANAGEMENT .................................. 13

This report is prepared on the basis of the limitations set out at Section 3.

Ards & North Down Borough Council October 2018 Grants

1

1. INTRODUCTION This internal audit was completed in accordance with the 2018/2019 Internal Audit Plan. General Audit Objectives Our aim is to provide assurance to Senior Management, the Chief Executive, and the Audit Committee Members on the contribution of control, risk management and governance processes of Ards and North Down Grant Funding to the achievement of the Council’s corporate objectives. The objective of this review was to form an opinion as to:

1. the level of internal controls in existence within Ards and North Down Grant Funding; and 2. whether or not these controls are operating effectively.