Arbitrage and interest rates on currency baskets

15

Arbitrage and Interest Rates on Currency Baskets By Martin Klein C o n t e n t s: I. Introduction. - II. Assumptions and Definitions. - III. Arbitrage and Interest Rates. - IV. Generalization: The Term Structure of Interest Rates. - V. Conclusions. I. Introduction T his paper uses an arbitrage theoretic approach to reexamine the interest rate determination for basket currencies.~ The two major basket curren- cies presently in use, the European Currency Unit (ECU) and the Special Drawing Right (SDR), are used as units of account in multilateral institutions and - to a lesser extent - as means of payment by which inter-offi- cial obligations at these institutions are settled. Within the European Monetary System the ECU serves to settle obligations resulting from intervention in one of the member currencies. At the International Monetary Fund and at a considerable number of other international institutions the SDR serves as the unit of account for lending operations and various other purposes, such as the calculation of members' quotas, staff salaries etc. At the IMF the SDR is also used as a means of payment to settle obligations between members resulting from transactions within the Fund. In addition to their use for inter-official transactions, the ECU and the SDR are also used in the private sector and for transactions between the private and the official sector. Private use of the ECU is considerably more widespread, albeit essentially limited to European finan- cial markets. 2 Because of the extensive use of basket currencies like the ECU and the SDR and their importance for a large and growing number of official and private transactions, the determination of their interest rates warrants careful study. These interest rates are important factors in the inter-official financial relations at the institutions where the currency baskets are in use and in the relations Remark: I am indebted to George von Fiirstenberg and Reinhard W. Fiirstenberg (not related) for comments. The usual disclaimer applies. Although the terms "basket currency" and "currency basket" potentially denote different concepts, they are used interchangeably in the context of the present paper. 2 For surveys of private ECU markets, see Lomax [1989] and Walton [1988].

-

Upload

martin-klein -

Category

Documents

-

view

218 -

download

0

Transcript of Arbitrage and interest rates on currency baskets

Arbitrage and Interest Rates

on Currency Baskets

By

Martin Klein

C o n t e n t s: I. Introduction. - II. Assumptions and Definitions. - III. Arbitrage and Interest Rates. - IV. Generalization: The Term Structure of Interest Rates. - V. Conclusions.

I. Introduction

T his paper uses an arbi t rage theoret ic a p p r o a c h to reexamine the interest rate de terminat ion for basket currencies.~ The two majo r basket curren- cies presently in use, the European Currency Unit (ECU) and the

Special Drawing Right (SDR), are used as units o f account in mul t i la tera l insti tutions and - to a lesser extent - as means o f payment by which inter-offi- cial obl igat ions at these insti tutions are settled. With in the European Mone ta ry System the ECU serves to settle obl igat ions resulting f rom intervention in one o f the member currencies. At the In te rna t iona l Mone ta ry F u n d and at a considerable number of o ther in ternat ional inst i tut ions the S D R serves as the unit o f account for lending opera t ions and var ious o the r purposes , such as the calculat ion of members ' quotas , s taff salaries etc. At the I M F the S D R is also used as a means o f payment to settle obl igat ions between members result ing f rom t ransact ions within the Fund . In add i t ion to their use for inter-official t ransact ions, the ECU and the S D R are also used in the private sector and for t ransact ions between the private and the official sector. Private use o f the E C U is considerably more widespread, albeit essentially l imited to European f inan- cial markets. 2

Because of the extensive use o f basket currencies like the E C U and the S D R and their impor tance for a large and growing number o f official and pr ivate t ransact ions, the de terminat ion o f their interest rates warrants careful study. These interest rates are impor tan t factors in the inter-official f inancial relat ions at the inst i tut ions where the currency baskets are in use and in the re la t ions

Remark: I am indebted to George von Fiirstenberg and Reinhard W. Fiirstenberg (not related) for comments. The usual disclaimer applies.

Although the terms "basket currency" and "currency basket" potentially denote different concepts, they are used interchangeably in the context of the present paper.

2 For surveys of private ECU markets, see Lomax [1989] and Walton [1988].

Klein: Currency Baskets 297

between official and private users of basket currencies. In particular, the determination of these interest rates has immediate consequences on the chances for a more widespread private use of the basket currencies.

In this paper we analyze the determination of basket currency interest rates. At first glance it seems obvious that the formula currently in use (the weighted arithmetic average of the member currency interest rates) is based on an essentially non-controversial method. Moreover, it appears that this me- thod is based on what could be called a "market valuation principle", that is, if currency baskets were freely traded in private markets then their interest rates would settle at this value. However, we will show in this paper that this is not the case and that the correct formula derived from the market valuation principle (i) is mathematically different and (ii) has implications for basket currency interest rates which differ significantly from the current practice.

In order to make our point, we have to give operational meaning to the concept of "interest rates that would prevail if basket currencies were freely traded in private markets". For this purpose we employ the technical apparatus of arbitrage theory which is essentially the study of derivative assets) Our starting point is the observation that currency baskets are simple examples of derivative assets. Indeed, as currency baskets are ex ante fixed bundles of n member currencies, their properties should be exhaustively explained by the properties of these currencies. Specifically, their interest rates should be une- quivocally determined by the interest rates and basket weights of, and the exchange rates between, the member currencies.

The remainder of the paper is organized as follows. After developing the fundamentals of our analysis in Section II, we demonstrate our basic proposi- tion for the example of one-period maturities in Section III. Section IV generalizes the results to a multi-period framework and Section V presents the conclusions.

II. A s s u m p t i o n s and D e f i n i t i o n s

1. A r b i t r a g e a n d F r e e L u n c h e s

The unifying principle of the following assumptions is that they guarantee costless arbitrage in the foreign exchange and asset markets of all currencies that are included in the currency basket. The minimal assumptions necessary to ensure this are: - Transaction costs in the foreign exchange and asset markets are zero.

3 For surveys of arbitrage theory, see Rubinstein [ 1987] and Varian [ 1987]. For more technical summaries of arbitrage pricing theory, see Miiller [ 1985] and Wilhelm [1985].

298 Weltwirtschaftliches Archiv

- There are no restrictions on buying and selling in the foreign exchange or asset markets.

- Buying and selling rates in all these markets are identical. Of particular importance in this respect is the concept of a free lunch which

was formalized by Harrison and Kreps [ 1979]. A free lunch exists whenever it is possible to trade one combination of assets for another one which either has (i) the same payoff but a lower price, or (ii) the same price but a higher payoff. Whenever a free lunch exists, riskless arbitrage is possible. By implication, if arbitrage is costless so that all arbitrage opportunities are exploited, no free lunches can exist in equilibrium. This "no-arbitrage principle" can be used to determine equilibrium asset prices. In the present paper it will be used to determine equilibrium interest rates on currency baskets.

2. D e f i n i t i o n o f B a s k e t C u r r e n c i e s

Basket currencies can be defined in two different ways. The first definition is based on quantities and can be phrased as follows:

Definition 1: One unit of the basket currency is equivalent to a bundle (a~, o~2, � 9 a,) of units of its member currencies.

The second definition is based on exchange rates and can be stated as follows:

Definition 2." One unit of the basket currency is worth e~ units of member currency i, where ei is defined by the formula

n

ei---- ~t~jeij. (1) J

The amounts oq . . . . a~ are identical to the ones in Definition 1 and eij is the cross rate in the spot exchange market between currencies i and j.

According to the first definition, holders of basket currency actually receive a bundle of member currencies if they present one unit of basket currency to the issuer. According to the second definition, owners of basket currency receive the total value of the basket in one currency. The important point is that in a world without transaction costs in the foreign exchange markets the two definitions are equivalent�9 For instance, if the value of the basket is disbursed in currency i, the amount e~ can be converted into the bundle (oq, . . , o~n) through n-1 costless transactions in the foreign exchange market. Conversely, if the basket currency is disbursed as the bundle (O~l . . . . . t~n), it can be costlessly converted into the amount ei in any member currency. Rational agents should therefore be indifferent between the two definitions of basket currencies.

Klein: Currency Baskets 299

3. T r i a n g u l a r A r b i t r a g e in the S p o t a n d F o r w a r d E x c h a n g e M a r k e t s

Triangular arbitrage allows important simplifications of pricing rules of basket currencies. Triangular arbitrage between the basket currency and its member currencies implies that the cross rates can be written as follows: e i j : ei/ej.

Substituting this in (1) yields:

ei : ~ otjei/ej. (2) j : l

Dividing both sides of this equation by e~ yields the identity

1 --J:, t h / e j = ~ toj. (3) j = l

Here we have defined

r = aj/ej (4)

as the "spot market weight" of currencyj in the basket. A similar relationship can be derived for the forward exchange markets,

where the currency basket has the value of

rl

i = ~, ~J iJ (5)

in currency L where)% is the cross rate between currencies i andj in the forward market. Triangular arbitrage in the forward exchange market between the currency basket and the member currencies implies that the forward cross rates can be written as follows:j~ =f/J~. Proceeding as above yields

r 1 j = l O/jl/j~ = L Oj, (6) j = l

where

% = a/. ,5 (7)

has been defined as the "forward market weight" of currency i in the basket.

III. Arbitrage and Interest Rates

1. T h e Bas i c Case : O n e - P e r i o d Z e r o C o u p o n B o n d s

We now use the "no-arbitrage principle" to derive an interest rate formula

300 Weltwirtschaftliches Archiv

for basket currencies. In order to begin with the most simple case we assume that identical financial assets - zero-coupon discounted bonds with a maturity of one period - exist in each member currency. The prices of these bonds are denoted by x~, i = 1 . . . . . n. For further simplicity we assume that all bonds have a face value of one unit of their respective currency at the end of the period. We then seek to determine the price Xb of an equivalent bond in the basket currency. According to our assumptions, the investment of Xb units of basket currency at the beginning of the period turns into 1 unit of basket currency at the end of the period. Equivalently we can say that the end-of-period portfolio (ctl, a2 . . . . . a ,) has the beginning-of-period price ofxb units of basket curren- cy. 4 The no-arbitrage principle can then be stated as follows: I fa given beginning- of-period portfolio yields the same end-of-period portfolio as the basket currency bond, its value in any given currency must be identical to the price of this bond in the same currency. If such a portfolio exists it is called the "replicating portfolio". The value Of Xb can thus be determined in two steps: (1) Find a replicating portfolio for the basket currency bond, (2) determine its value in an arbitrary unit of account.

Step 1: Given our assumption about the member currency bonds, it is immediately obvious that the member bond portfolio (t~l, c~2 . . . . . t~,) yields the same end-of-period portfolio as one basket currency bond. This is thus the replicating portfolio.

Step 2: As the selection of the unit of account is irrelevant, we can choose the basket currency as the unit of account. The value of the replicating portfolio in units of basket currency is:

Xb j=l ej j=l o~xj. (8)

The no-arbitrage principle thus implies that the price of a discounted bond in the basket currency should be equal to the weighted average of prices of similar discounted bonds in its member currencies, where the weights are the spot market weights of the member currencies at the beginning of the period.

2. I n t e r e s t R a t e s

The argument developed above immediately generalizes to all types of assets yielding an ex ante risk-free rate of interest. We only have to replace Xb by 1/(1 + rb) and x~ by 1/(1 -t- ri), where rb and ri denote the risk-free interest rates in the basket currency and the member currencies, respectively. These substitu- tions can also be used to derive a formula linking the interest rate in the basket currency with the interest rates in the member currencies:

4 We assume that the currency amounts a~ are not changed before the bonds have matured.

Klein: Currency Baskets 301

1 - i l + r b j=l l + r i

or equivalently,

-1

l - k r b = ( j ~ , l+~ri )

(9)

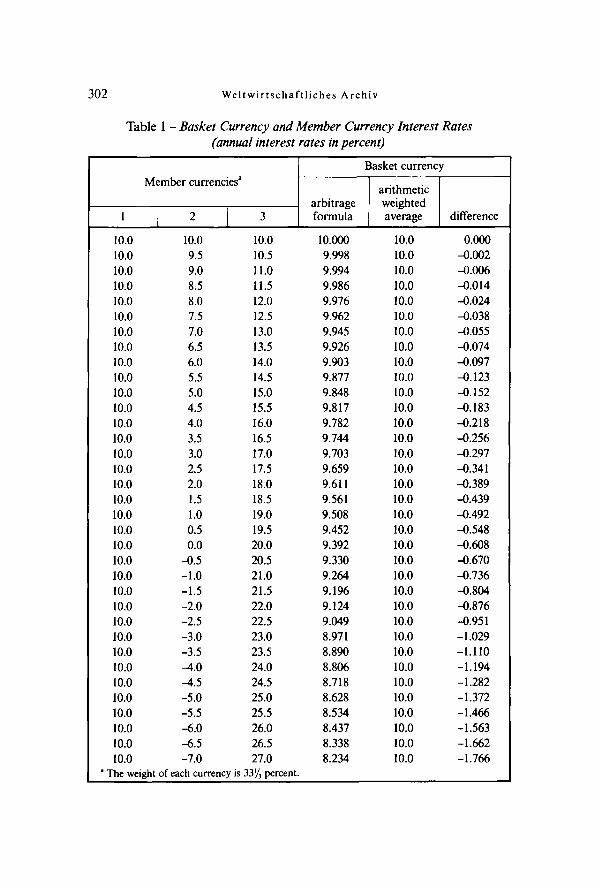

The no-arbitrage principle thus implies that the interest factor - i.e. one plus the interest r a t e - in the basket currency is equal to the weighted harmonic average o f the interest factors in the member currencies. Note that the basket currency interest rate calculated this way is smaller than or at most equal to the interest rate calculated as the weighted arithmetic average, using the same weights. 5 As illustrated in Table 1 for the case o f a 3-currency basket, the discrepancy between the two formulae increases with increasing dispersion o f the member currency interest rates.

3. F o r w a r d M a r k e t s

Al though the no-arbitrage principle used in the previous section does not assume the existence of forward exchange markets it can be shown that the interest rate formulae derived f rom it are consistent with arbitrage in these markets. In order to demonstrate this we now assume that forward markets exist in the basket currency and all the member currencies. Arbitrage then ensures that covered interest parity holds between all currencies, including the basket currency. This can be written as follows: 6

f___ _ 1-t-r~ (10) ei 1 + rb "

Moreover, (3), (4) and (10) can be used to derive the following equation for the interest rate in the basket currency:

- - i - - i n l + r b j = , ~ ( l + r b ) j=,toj(l+rj)e/fj=~lOj(l+rj). (11)

Here the interest rate in the basket currency is determined as the weighted arithmetic average of the interest rates in the member currencies, using forward market weights. Although this equation appears to differ considerably f rom

5 This reflects a general inequality that holds between harmonic and arithmetic averages. See Hardy et al. [1952, section 2.9].

6 Note that this implies that the interest rate on the basket currency can be determined from the interest rate and the spot and forward exchange rates in one member currency. It is straightfor- ward to show that if the implied interest rate rb is different for two currencies, then covered interest parity between them is violated.

302 Weltwir tschaft l iches Archiv

Table 1 - Basket Currency and Member Currency Interest Rates (annual interest rates in percent)

Member currencies"

1 2 3

Basket currency

arithmetic arbitrage weighted formula average difference

a The weight of each currency is 33 4 percent.

10.0 10.0 10.0 10.000 10.0 0.000 10.0 9.5 10.5 9.998 10.0 -0.002 10.0 9.0 11.0 9.994 10.0 -0.006 10.0 8.5 11.5 9.986 10.0 -0.014 10.0 8.0 12.0 9.976 10.0 --0.024 10.0 7.5 12.5 9.962 10.0 -0.038 10.0 7.0 13.0 9.945 10.0 -0.055 10.0 6.5 13.5 9.926 10.0 -0.074 10.0 6.0 14.0 9.903 10.0 --0.097 10.0 5.5 14.5 9.877 10.0 -0.123 10.0 5.0 i 5.0 9.848 10.0 -0.152 10.0 4.5 15.5 9.817 10.0 -0.183 10.0 4.0 16.0 9.782 10.0 -0.218 10.0 3.5 16.5 9.744 10.0 -0.256 10.0 3.0 17.0 9. 703 10.0 -0.297 10.0 2.5 17.5 9.659 10.0 -0.341 10.0 2.0 18.0 9.611 10.0 -0.389 10.0 1.5 18.5 9.561 10.0 -0.439 10.0 1.0 19.0 9.508 10.0 -0.492 10.0 0.5 19.5 9.452 10.0 -0.548 10.0 0.0 20.0 9.392 10.0 -0.608 10.0 -0.5 20.5 9.330 10.0 -0.670 10.0 -1.0 21.0 9.264 10.0 -0.736 10.0 -1.5 21.5 9.196 10.0 -0.804 10.0 -2.0 22.0 9.124 10.0 -0.876 10.0 -2.5 22.5 9.049 10.0 -0.951 10.0 -3.0 23.0 8.971 10.0 -1.029 10.0 -3.5 23.5 8.890 10.0 - 1.110 10.0 --4.0 24.0 8.806 10.0 -1.194 10.0 -4.5 24.5 8.718 10.0 -1.282 10.0 -5.0 25.0 8.628 10.0 -1.372 10.0 -5.5 25.5 8.534 10.0 -1.466

10.0 -6.0 26.0 8.437 10.0 -1.563 10.0 -6.5 26.5 8.338 10.0 -1.662 10.0 -7.0 27.0 8.234 10.0 -1.766

Klein: Currency Baskets 303

the harmonic average formula derived above it is in fact consistent with it and leads to the same value for the basket currency interest rate. Equating the right hand sides of (9) and (11) yields

-1 ot/ej ) , (a/-t~) ( l + rj) = ~ l l + r j j = l

and it is straightforward to verify that under covered interest parity this equation indeed holds. The interest rate in the basket currency can therefore be calculated in two different but equivalent ways: - General case: As a weighted harmonic average, using spot market weights. 7 - With covered interest parity: As a weighted arithmetic average, using forward market weights.

However, it should be noted that the harmonic average formula is more general as it does not depend on the existence of forward markets in order to be valid.

IV. Generalization: The Term Structure of Interest Rates

1. M u l t i - P e r i o d Z e r o C o u p o n B o n d s

The harmonic average formula implies that the term structure in the basket currency differs systematically from the term structure of its member curren- cies. Before we show this we first generalize the results of Section I II to include discounted zero-coupon bonds with maturities of more than one period. We assume that in the basket currency and all its member currencies bonds with the same maturity are available. As in Section III we assume that their face value at maturity is one unit of their respective currency.

x~(t,m) is the price of a currency i bond in period t with m periods remaining until maturity. The no-arbitrage value of the basket currency bond with the same maturity, xb(t,m), is then equal to the current value of the replicating portfolio consisting of member currency bonds with the same maturity. Pro- ceeding as in Section III we can write

n

xb(t,m) ---- j=l ~" xj(t,m) aj/ej(t) = jE__ l toj(t) x~(t,m). (12)

Here ei(t) is the spot exchange rate in period t and the currency weights are defined by

toj(t) = t~/ej(t). (13)

7 Strictly speaking the harmonic average concerns the interest factors in all currencies.

304 Weltwirtschaftliches Archiv

The m-period compound interest rate in the basket currency can then be determined from the equation

1 l/m 1 + rb(t,m) = ( xb(t,m ) ) (14)

If forward exchange markets exist for a given maturity m, (14) could for that maturity be rewritten with forward market weights as (11) in the previous section. However, it should be noted that the forward weighted formula can only be applied for maturities where forward markets exist in all member currencies. This implies that for practical purposes - where complete forward exchange markets exist only for a limited number of standard maturities - the current weighted formula is considerably more general as it is not restricted to these maturities.

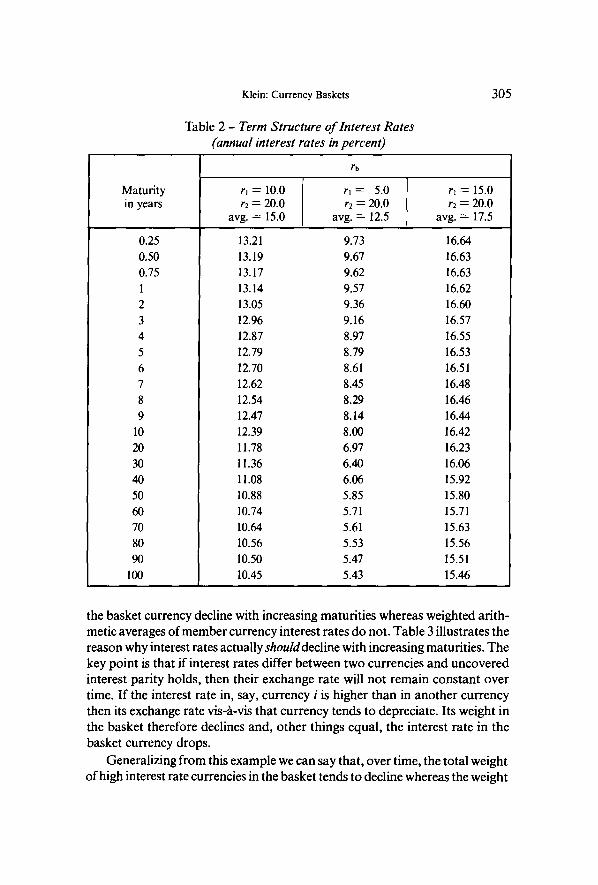

The implications for the term structure of interest rates of the m-period current-weight formula are illustrated in Table 2, which provides three simple examples based on simulated data. In all three cases the currency basket consists of two currencies whose interest rate term structure is "flat", i.e. interest rates for all maturities are identical. In spite of this the term structure of interest rates in the basket currency is not fiat. In fact, the table shows that interest rates decrease with increasing maturities so that the discrepancy be- tween the interest rate in the basket currency and the weighted arithmetic average of the member currency interest rates increases with increasing maturi- ties. s

2. T h e T e r m S t r u c t u r e o f I n t e r e s t R a t e s a n d I n t e r t e m p o r a l A r b i t r a g e

In this sub-section we provide a rationale for the discrepancy between the interest rate term structure in the basket currency and those in its member currencies. We show that the arbitrage based interest rate formula correctly takes into account future devaluations of high-interest currencies and that this is consistent with arbitrage in the forward exchange markets under perfect foresight. 9

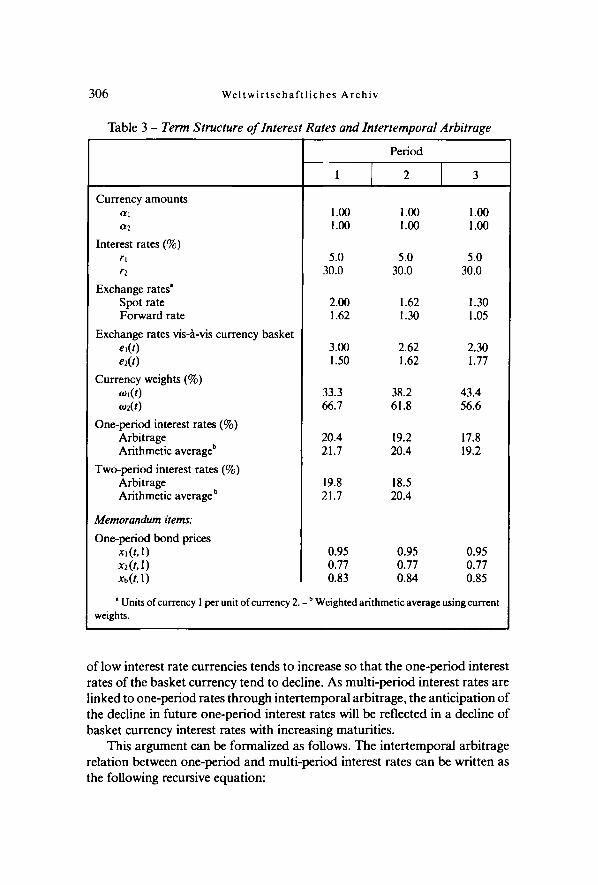

To illustrate the relationship between the term structure and intertemporal arbitrage we consider a simple example of a two-currency basket and three time periods (see Table 3). We assume again that interest rates are constant and the term structure in both member countries is flat but that interest rates differ between countries. With these assumptions, arbitrage-based interest rates in

s A necessary condition for this is that the interest rates in the member currencies are different. 9 We limit the following discussion to the case of perfect foresight. The stochastic case will be

treated in a separate paper.

Klein: Currency Baskets

Table 2 - Term Structure of Interest Rates (annual interest rates in percent)

305

Maturity in years

0.25 0.50 0.75 I

2 3 4 5 6 7 8 9

10 20 30 40 50 60 70 80 90

100

rb

rj = 10.0 r2 -- 20.0

avg. = 15.0

r, = 5.0 r2 = 20.0

avg. -- 12.5

r~ = 15.0 r2 = 20.0

avg. = 17.5

13.21 9.73 16.64 13.19 9.67 16.63 13.17 9.62 16.63 13.14 9.57 16.62 13.05 9.36 16.60 12.96 9.16 16.57 12.87 8.97 16.55 12.79 8.79 16.53 12.70 8.61 16.51 12.62 8.45 16.48 12.54 8.29 16.46 12.47 8.14 16.44 12.39 8.00 16.42 11.78 6.97 16.23 ! 1.36 6.40 16.06 11.08 6.06 15.92 10.88 5.85 15.80 10.74 5.71 15.71 10.64 5.61 15.63 10.56 5.53 15.56 10.50 5.47 15.51 10.45 5.43 15.46

the basket currency decline with increasing maturi t ies whereas weighted ar i th- metic averages of member currency interest rates do not. Table 3 i l lustrates the reason why interest rates actually should decline with increasing maturit ies. The key po in t is that if interest rates differ between two currencies and uncovered interest par i ty holds, then their exchange rate will not remain cons tant over time. I f the interest rate in, say, currency i is higher than in another currency then its exchange rate vis-h-vis that currency tends to depreciate. Its weight in the basket therefore declines and, o ther things equal , the interest rate in the basket currency drops.

General iz ing f rom this example we can say that , over time, the total weight o f high interest rate currencies in the basket tends to decline whereas the weight

306 Wel twir t schaf t l iches Archiv

Table 3 - Term Structure of Interest Rates and lntertemporal Arbitrage

Currency amounts Otl Or2

Interest rates (%) rl rz

Exchange rates" Spot rate Forward rate

Exchange rates vis-b.-vis currency basket el(t) e2(t)

Currency weights (%) OJl(/) ,o~(t)

One-period interest rates (%) Arbitrage Arithmetic average b

Two-period interest rates (%) Arbitrage Arithmetic average b

Memorandum items:

One-period bond prices Xl(/,l) x2(t,l) Xb(t, 1)

Period

1 2 3

1.~ 1 .~ 1 .~ 1 .~ 1 .~ 1 .~

5.0 5.0 5.0 30.0 30.0 30.0

2.00 1.62 1.30 1.62 1.30 1.05

3.00 2.62 2.30 1.50 1.62 1.77

33.3 38.2 43.4 66.7 61.8 56.6

20.4 19.2 17.8 21.7 20.4 19.2

19.8 18.5 21.7 20.4

0.95 0.95 0.95 0.77 0.77 0.77 0.83 0.84 0.85

' Units of currency I per unit of currency 2. - b Weighted arithmetic average using current weights.

of low interest rate currencies tends to increase so that the one-per iod interest rates of the basket currency tend to decline. As mul t i -per iod interest rates are l inked to one-per iod rates th rough in te r tempora l arb i t rage , the ant ic ipat ion of the decline in future one-per iod interest rates will be reflected in a decline o f basket currency interest rates with increasing maturit ies.

This argument can be formal ized as follows. The in ter tempora l arbi t rage relation between one-per iod and mul t i -per iod interest rates can be writ ten as the following recursive equation:

Klein: Currency Baskets 307

xb(t,m) -'- xb (t ,l) Xb (t +1, m - 1). (15)

The decline of one-period interest rates in the basket currency can be captured by the inequality

rn - I ~ t l /m

xb(t-~ re, l ) > ( I l x b ( t + k , 1)) , (16)

which states that the price of a one-period bond in period t + m exceeds the geometric average of the bond prices in the previous m periods.I~ Using (15) we can write

xb(t, m + 1) m-I xb (t q* m, 1) -- xb(t, m) and Xb (t ,m) = k=011 Xb (t + k, 1).

Substituting both these equations in (16) and rearranging we get

xb (t, m + 1) J/~m+J~ > x~(t, m) ~/m .

Applying (14) to this we immediately get

rb(t, m t- 1) < rb(t, m),

which proves that basket interest rates decline with increasing maturities. There are, however, two remaining questions:

(1) Does the intertemporal arbitrage relation of(15) actually hold for our arbitrage-based definition of bond prices in the basket currency?

(2) How can the arbitrage-based pricing formula, (which is not based on exchange rate expectations), correctly anticipate future depreciations of the member currencies?

These two questions are closely related and by answering the first question we also find an answer for the second. The following proposit ion answers the first question:

Proposition: If bond prices in the basket currency are defined by (12) for m > 1 and if the intertemporal arbitrage condition

x~(t, m) --- xi(t, 1) Xi(t -{- 1, m -1), (17)

as well as covered interest parity hold in each currency i, then bond prices in the basket currency also fulfill the intertemporal arbitrage condition (14).

Proof" Using (12) we can write n

xb(t, 1)-- i~ toi(/) X,(t, 1), (18)

and tl

xb(t + 1, m - 1) = ,~ x~(t + 1) x~(t + 1, m - 1). (19)

to Note that this condition is actually weaker than the requirement of a continuous decline in x b. It holds also in situations where x~ does not decline monotonically.

308 Weltwirtschaftliches Archiv

Next we note that under perfect foresight intertemporal arbitrage ensures that the forward exchange rate is equal to the future spot exchange rate. Covered interest parity between the basket currency and its member currencies can therefore be written as follows

e~(t + 1) _ 1 + ri(t, 1) Xb(t, 1) el(t) 1 + rb(t, 1) xi(t, 1)

With this the intertemporal evolution of the currency weights defined in (13) can be written as follows

xi(t, 1) toi(t + 1) --- ~(t) Xb(t, 1)

Substituting this in (19) we get

n xb(t + 1, m - 1) = ~ o~(t) xi(t, 1) x~(t + 1, m -1) (20) xb(t, 1)

Combining (17) through (20) we can now write

n Xb(t, 1) Xb(l + l , m - l ) ~--- ~ o)i(1) xi(t, 1) Xi(t + 1, m - 1 )

n : i~ o~(t) xi(t, m) : xb(t, m).

This proves the proposition. The proof shows that the validity of the intertemporal arbitrage relationship in the basket currency depends crucially on its validity in the member currencies. Answering our second question above, we can thus say that the arbitrage pricing principle by itself does not guarantee that bond prices (or interest rates) in the basket currency satisfy the intertem- poral arbitrage relation. However, it implies that they are consistent with intertemporal arbitrage i f it holds in the member currencies.

V . C o n c l u s i o n

The main results of this paper can be summarized as follows: - The weighted arithmetic average commonly used to calculate official inter-

est rates for currency baskets is not consistent with arbitrage pricing. The arbitrage-based interest rate determination leads to a harmonic average formula.

- Interest rates calculated as weighted arithmetic averages are (i) higher than those calculated with the formula derived from arbitrage pricing and (ii) not consistent with intertemporal arbitrage in the asset markets of the basket currency and its member currencies. With increasing maturities, arbitrage-

Klein: Currency Baskets 309

based interest rates in the basket currency decline relative to the interest rates in the member currencies, reflecting the anticipation o f a future decline in the weights of high-interest currencies in the basket.

In this paper we have essentially concentrated on the "positive" question as to how basket currency interest rates would be determined if they were freely traded in private markets. However, the market valuation principle referred to in the introduction can also be given a "normative" orientation by postulating that official interest rates in basket currencies should equal the interest rates that would prevail if the basket currencies were freely traded in private mar- kets. A more detailed discussion of this proposal provides an interesting agenda for future research.

References

Cox, John C., Mark Rubinstein, Options Markets. Englewood Cliffs 1985.

Fama, Eugene F., Melton H. Miller, The Theory of Finance. New York 1972.

Garman, Mark B., "Towards a Semigroup Pricing Theory". Journal of Finance, Vol. 40, 1985, pp. 847-861.

Hardy, G.H., J.E. Littlewood, G. Prlya, Inequalities. Cambridge 1952.

Harrison, J.M., D.M. Kreps, "Martingales and Arbitrage in Multi-Period Securities Markets". Journal of Economic Theory, Vol. 20, 1979, pp. 381--408.

Lomax, David F., "The ECU as an Investment Currency". In: De Grauwe, Paul, Theo Peeters (Eds.), The ECU and European Monetary Integration. Basingstoke 1989, pp. i 19-138.

Miiller, Sigrid, Arbitrage Pricing of Contingent Claims. Berlin 1985.

Rubinstein, Mark, "Derivative Assets Analysis". Economic Perspectives, Vol. 1, 1987, pp. 73-93.

Varian, Hal R., "The Arbitrage Principle in Financial Economics". Economic Perspec- tives, Vol. 1, 1987, pp. 55-72.

Walton R.J., ~ECU Financial Activity". Bank of England Quarterly Bulletin, Nov. 1988, pp. 509-516.

Wilhelm, Jochen E.M., Arbitrage Theory. Berlin 1985.

Z u s a m m e n fa s s u n g: Arbitrage und Zinsen auf W~hrungskrrbe. - In diesem Aufsatz wird mit Hilfe der Arbitragetheorie die Zinsformel for Korbw/ihrungen iiber- priift. Der Ansatz basiert aufder Beobachtung, dab W~hrungskrrbe eigentlich abgelei- tete Vermfgenswerte sind, deren Eigenschaften ausschliel31ich durch die Eigenschaften ihrer Mitgliedsw~ihrungen erkl~rt werden sollten. Es wird gezeigt, dab die iiblicherweise angewandte Formel for die Berechnung der Zinss/i.tze for die Korbw/ihrung - das gewogene arithmetische Mittel aus den Zinss~tzen der Mitgliedsw/ihrungen - erstens mit der vollst~indigen Arbitrage zwischen den W~hrungen nicht konsistent ist, zweitens

310 W e l t w i r t s c h a f t l i c h e s Arch iv

zu h6heren Zinss~tzen ftihrt, als sich ergeben wiirde, wenn bei der Berechnung Arbi- tragepreise zugrundegelegt wtirden, und drittens eine Terminstruktur der Zinssiitze voraussetzt, die nicht konsistent ist mit einer perfekten Terminarbitrage auf den Fi- nanzm~irkten der Korbwii.hrung und cler Mitgliedswiihrungen.

R 6 s u m 6: Arbitrage et taux d'int~r& pour des monnaies de panier. - Cet article applique une approche th6orique d'arbitrage pour r6examiner la formule du taux d'int6r~t pour des monnaies de panier, l . 'approche est fond6e sur l 'observation que des relies monnaies sont des valeurs actives intrins~quement d6riv6es dont les caract6risti- ques doivent &re expliqu6es exclusivement par celles des monnaies membres. I1 est d~montr6 que la formule normalement appl iqu& pour calculer les taux d'int6r& des monnaies de panier - la moyenne arithm&ique pond&& des taux d'int~r~t des monna- ies membres - (i) n'est pas consistante avec l'arbitrage parfaite entre des monnaies, (ii) m~ne aux taux d'int&& plus hauts que ceux qui sont calcul6s par un arbitragiste, et (iii) implique une structure de terme des taux d'int6r& qui n'est pas consistante avec l'arbitrage parfaite intertemporale sur les march6s des valeurs actives des monnaies de panier et ses monnaies membres.

R e s u m e n : Arbitraje y tasas de inter6s sobre canastas de monedas. - En este trabajo se utiliza un enfoque te6rico de arbitraje para examinar la f6rmula de tasa de inter6s para canastas de monedas. El enfoque estfi basado en la observaci6n de que las canastas de monedas son intrl'nsecamente activos derivados cuyas propiedades debe- r/an explicarse a partir de las propiedades de las monedas participantes. Se demuestra que la f6rmula comfinmente empleada para calcular tasas de inter6s para canastas de monedas - el promedio arittm&ico ponderado de las tasas de inter6s de las monedas participantes - 1) no es consistente con un arbitraje perfecto entre las monedas, 2) arroja tasas de inter6s mils altas que las calculadas con la f6rmula defivada de precios de arbitraje e 3) implica una estructura temporal de tasas de inter6s que no es consistente con un arbitraje intertemporal perfecto en los mercados de activos correspondientes a la canasta de monedas y a las monedas participantes.