Fuzzy Logic and Fuzzy Cognitive Map - Simon Fraser University

Upload

zahir-iraniCategory

view

212download

0

Int. J. Production Economics 75 (2002) 199–211

Applying concepts of fuzzy cognitive mapping to model:The IT/IS investment evaluation process

Zahir Irania,*, Amir Sharif b, Peter E.D. Lovec, Cengiz Kahramand

a Information Systems Evaluation and Integration Group (ISEIG), Department of Information Systems and Computing,

Brunel University, Uxbridge, Middlesex UB8 3PH, UKbKPMG Consulting, 8 Salisbury Square, London EC4Y 8BB, UK

cSchool of Architecture and Building, Deakin University, Geelong, Victoria 3217, Australiad Istanbul Technical University, Istanbul, Turkey

Abstract

The justification process is a major concern for those organisations considering the development of an informationtechnology (IT)/information systems (IS) infrastructure, which in turn is putting the competitive advantage of manycompanies at risk. The reason for this centers around management’s inability to evaluate the holistic implication of

adopting new technology, both in terms of the benefit and cost portfolios. In attempting to investigate this, the authorsof this paper identify a number of well-known project appraisal techniques used during the IT/IS investmentjustification process. In establishing a number of limitations inherent in traditional appraisal techniques, the concept ofmultivalent, or fuzzy logic, is used to demonstrate how inter-relationships can be modeled between key dimensions

identified in a proposed conceptual model for investment evaluation. The authors highlight this using fuzzy cognitivemapping (FCM) as a technique to model each IT/IS evaluation factor (integrating strategic, tactical, operational andinvestment considerations). The use of an FCM is then shown to be as a complementary tool that can serve to highlight

interdependencies between contributory justification factors. r 2002 Elsevier Science B.V. All rights reserved.

Keywords: Investment justification; Management of IT; Project appraisal; Fuzzy logic

1. Introduction

Information technology (IT) and informationsystems (IS) are widely acknowledged as one of themajor enablers of business change. However,despite enormous capital IT/IS investments, orga-nisations have not always been able to enjoycommensurate financial returns. Indeed, the pro-liferation of IT/IS has often coincided with lower

macroeconomic figures of productivity and profit-ability in both the manufacturing and servicesectors [1,2]. As a result, Brynjolfsson [3] proposedthe term ‘IT productivity paradox’, which is used todescribe the alleged inability of IT/IS to deliverin practice the benefits they promise in theory.Increasingly, for senior management to fullycommit to the increasing levels of IT/IS expendi-ture, they need to be convinced of the businessjustification of such investments [4]. Small andChen [5] have identified a variety of industriesunderlying concerns with regard to the justifica-tion of new technology. These center around: (i)

*Corresponding author. Tel.: +44-1895-274000x2133; fax:

+44-1895-251-686.

E-mail address: [email protected] (Z. Irani).

0925-5273/02/$ - see front matter r 2002 Elsevier Science B.V. All rights reserved.

PII: S 0 9 2 5 - 5 2 7 3 ( 0 1 ) 0 0 1 9 2 - X

many of the achievable benefits are considered tobe qualitative and hence difficult to quantify; (ii) alack of readily accessible and acceptable techni-ques for appraising all project costs and benefits;(iii) the ability to assess the true performance of asystem: as it is diminished if all benefits are notquantified during the justification process; and (iv)an insufficient level of internal skills (managerialand technical) to appraise proposed systems. As aresult of the above concerns, many corporatemanagers have been forced to adopt one of thefollowing strategies:

* not to undertake IT projects that could bebeneficial to the long-term future of theorganisation;

* invest in projects as an ‘act of faith’; or* use creative accounting as a means of passing

the budgetary process.

The adoption of new technology is clearly oneof the most lengthy, expensive and complextasks that a firm can undertake. The level ofinvestment and high degree of uncertainty asso-ciated with the adoption of this technologyimplies that issues involving project justificationshould assume great importance. Yet, in reality,much evidence is offered by Irani and Love [6],Serafeimidis and Smithson [7], Khalifa et al. [8],Remenyi et al. [9], Smithson and Hirschheim [10],Hochstrasser [11] and Farbey et al. [12] to supportthe lack of structure in the approaches toinvestment evaluation.

To provide an insight into the complexity ofinter-relationships amongst IT/IS decision-makingvariables, this paper identifies and classifies anumber of project appraisal techniques used tojustify investments in IT/IS projects. A holisticconceptual evaluation model that integrates stra-tegic, tactical, operational and financial considera-tions is presented. Fuzzy logic is then used todemonstrate inter-relationships that may existbetween key dimensions identified in the proposedmodel. The use of a fuzzy cognitive mapping(FCM) as a tool for investment justification is usedto highlight pertinent aspects of the modelpresented.

2. Investment justification of IT/IS

The problems associated with IT/IS evaluationare not new but continue to receive surges ofinterest from industry and academe. Informationsystems have always been taking too long todevelop, cost too much to implement and main-tain, and are frequently not perceived to bedelivering those business benefits which wereinitially intended [13,3,14]. However, in recentyears the changing role of IT/IS in organisationshas given new impetus to the problem of IT/ISevaluation. The high expenditure on IT/IS, grow-ing usage that penetrates to the core of organisa-tional functioning, together with disappointedexpectations about IT/IS impact, have all servedto raise the profile of how IS investments can andshould be evaluated. According to Willcocks [15],‘IS evaluation is not only an under-developed, butalso an under-managed area which organizationscan increasingly ill-afford to neglect’. The increasedcomplexity of IT/IS combined with the uncertaintyassociated with IT/IS benefits and costs[16,17,6,18] point to the need for improvedevaluation processes.

In many companies, a formal justificationproposal must be prepared and accepted bydecision-makers, prior to any expenditure. Pri-mose [19] identifies industry’s perception ofinvestment justification as a budgetary processthat gives a final ‘Yes’ or ‘No’, ‘pass’ or ‘fail’verdict on the success of a project’s proposal. As aresult, managers may view project justification as ahurdle that has to be overcome, and not as atechnique for evaluating the project’s worth. Thishas significant implications, as during the pre-paration of a project’s proposal, managersspend much time and effort investigating itstechnical aspects and become committed to thebelief that the project is essential. Therefore, teammembers may be easily susceptible to persuasionby vendors and consultants, and be prepared toaccept untypical demonstrations that show un-realistically high levels of savings. Hence, projectmembers may focus their efforts on trying toidentify and estimate maximum benefits andsavings at the expense of overlooking full costimplications.

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211200

Traditional project appraisal techniques such asreturn on investment (RoI), internal rate of return(IRR), net present value (NPV) and paybackapproaches are often used to assess capitalinvestments [15]. These methodologies are basedon conventional accountancy frameworks andoften facilitated under the auspices of the financedirector. Specifically, they are designed to assessthe bottom-line financial impact of an investment,by often setting project costs against quantifiablebenefits and savings predicted to be achievable.However, the vast array of traditional and non-traditional appraisal techniques leaves manyorganisations with the quandary of decidingwhich approach to use, if any [5,20]. Conse-quently, many debates about the types of techni-ques that constitute meaningful justification havebeen ubiquitous.

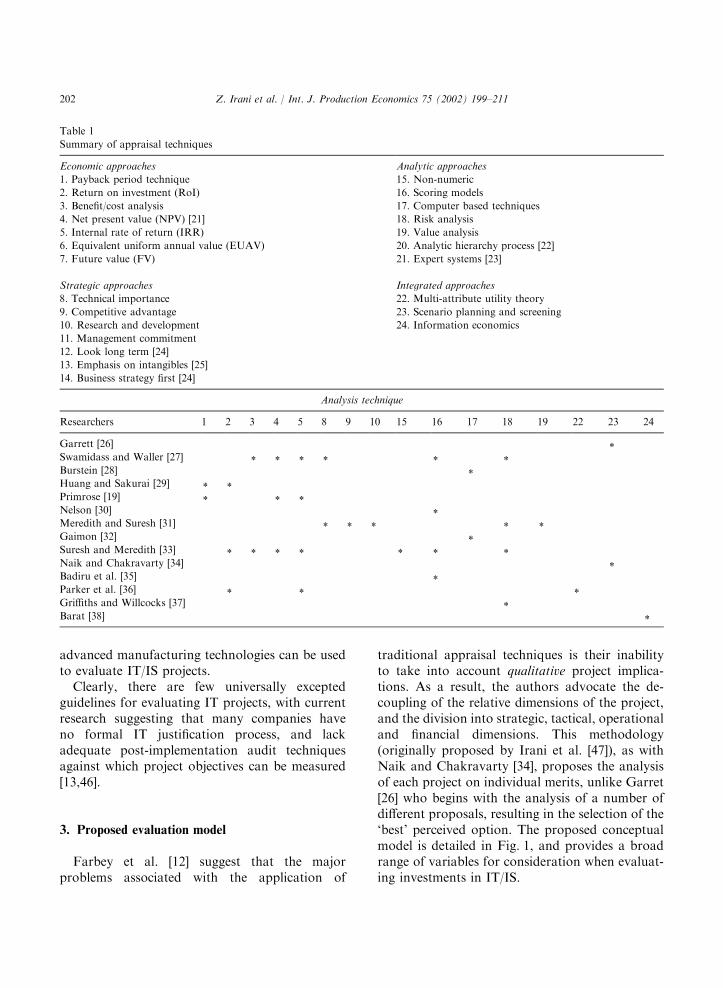

Table 1 categorises many of the availableinvestment appraisal methodologies into appro-priate groups. These various approaches have beencompressed into four principal classifications;economic approaches, analytic approaches, strate-gic approaches and integrated approaches. Theclassification of economic and analytic approachesto project justification has been further dividedinto two respective groups. Appraisal techniquesthat fall into each of the four classifications havebeen identified. These are summarised in Table 1.

Farbey et al. [39] state that those companiesusing traditional approaches to project appraisal,often indicate an uncertainty of how to measurethe full impact of their investments in IT/IS.Furthermore, Hochstrasser and Griffiths [40]suggests that those evaluation techniques exclu-sively based on standard accounting methodssimply do not work for organisations working insophisticated IT/IS environments. Many managersappear to have become too absorbed with financialappraisal, to the extent that practical strategicconsiderations have been overlooked [41].

In a similar fashion, Hochstrasser and Griffiths[40] identified industries overwhelming belief thatthey are faced with outdated and inappropriateprocedures for investment appraisal and that allresponsible executives can do is cast them aside ina bold ‘leap of strategic faith’. However, when thepurpose of IT/IS investment is to support an

operational efficiency drive, the benefits of reducedcosts and headcounts may be easy to quantifyin financial terms. Therefore, the use of manytraditional approaches to project justificationare often the natural choice, as they are usuallyin widespread use appraising other types ofcapital expenditure, such as the purchase of newmachinery [19].

Maskell [42] and Farbey et al. [12] suggest thattraditional approaches to project justification areoften unable to capture many of the intangiblebenefits that IT/IS brings. They suggest that thesetechniques ignore the impact that the system mayhave in human and organisational terms. As aresult, many companies are often left questioninghow to compare a strategic investment in IT/ISthat delivers a wide range of intangibles, withother corporate investments whose benefits aremore tangible. Hill [43] suggests a shift in currentjustification emphasis, towards a strategic basedreview process. It is proposed that project focusshould be placed on where progress can bemeasured against its contribution towards thecorporate strategy, and not how well it meets thecriteria determined by accounting rules andregulations. Similarly, Hares and Royle [44]suggest that companies should identify opportu-nities for making strategic investments in projectspertinent to the objectives of their business, andthat investment decisions should not be made onthe sole basis of monetary return alone. However,Kaplan [45] explains that, if companies, even forgood strategic reasons, consistently invest inprojects whose financial returns are below its costof capital, they will inevitably be on the road toinsolvency.

The apparent success of traditional appraisaltechniques on non-IT based projects has led manypractitioners to search for appropriate evaluationmethods that can deal with all IT projects, in allcircumstances. Farbey et al. [12] explain that thisquest for the ‘one best method’ is fruitless becausethe range of circumstances to which the techniquewould be applied, is so wide and varied that no onetechnique can cope. Primrose [19] suggests analternative perspective, claiming that there isnothing special about IT/IS projects, and thattraditional appraisal techniques used for other

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211 201

advanced manufacturing technologies can be usedto evaluate IT/IS projects.

Clearly, there are few universally exceptedguidelines for evaluating IT projects, with currentresearch suggesting that many companies haveno formal IT justification process, and lackadequate post-implementation audit techniquesagainst which project objectives can be measured[13,46].

3. Proposed evaluation model

Farbey et al. [12] suggest that the majorproblems associated with the application of

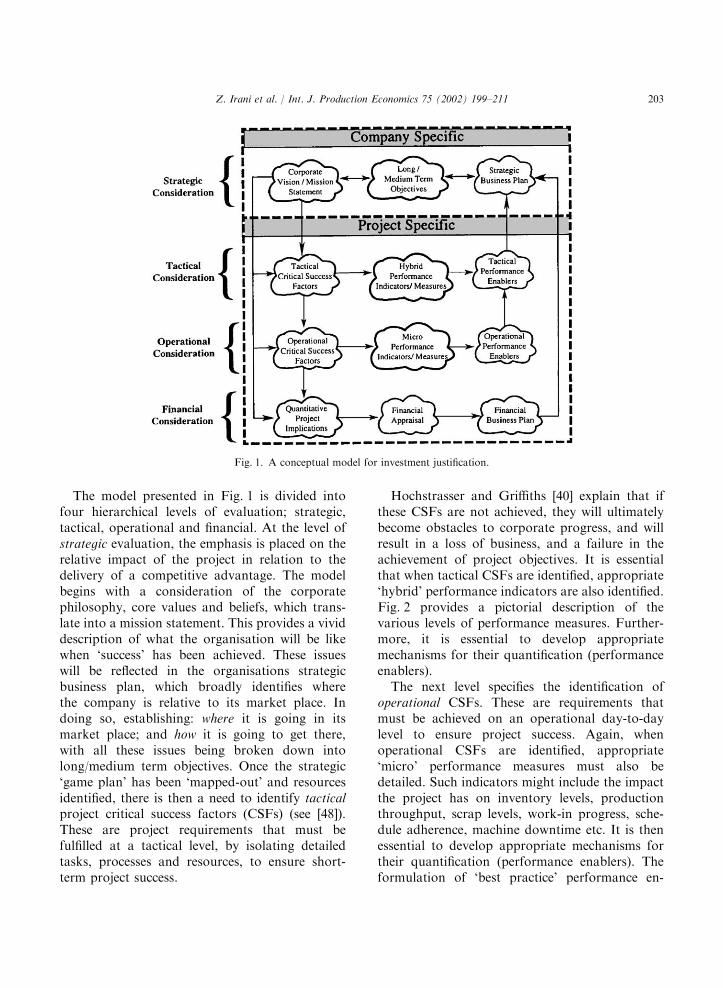

traditional appraisal techniques is their inabilityto take into account qualitative project implica-tions. As a result, the authors advocate the de-coupling of the relative dimensions of the project,and the division into strategic, tactical, operationaland financial dimensions. This methodology(originally proposed by Irani et al. [47]), as withNaik and Chakravarty [34], proposes the analysisof each project on individual merits, unlike Garret[26] who begins with the analysis of a number ofdifferent proposals, resulting in the selection of the‘best’ perceived option. The proposed conceptualmodel is detailed in Fig. 1, and provides a broadrange of variables for consideration when evaluat-ing investments in IT/IS.

Table 1

Summary of appraisal techniques

Economic approaches Analytic approaches

1. Payback period technique 15. Non-numeric

2. Return on investment (RoI) 16. Scoring models

3. Benefit/cost analysis 17. Computer based techniques

4. Net present value (NPV) [21] 18. Risk analysis

5. Internal rate of return (IRR) 19. Value analysis

6. Equivalent uniform annual value (EUAV) 20. Analytic hierarchy process [22]

7. Future value (FV) 21. Expert systems [23]

Strategic approaches Integrated approaches

8. Technical importance 22. Multi-attribute utility theory

9. Competitive advantage 23. Scenario planning and screening

10. Research and development 24. Information economics

11. Management commitment

12. Look long term [24]

13. Emphasis on intangibles [25]

14. Business strategy first [24]

Analysis technique

Researchers 1 2 3 4 5 8 9 10 15 16 17 18 19 22 23 24

Garrett [26] *Swamidass and Waller [27] * * * * * *Burstein [28] *Huang and Sakurai [29] * *Primrose [19] * * *Nelson [30] *Meredith and Suresh [31] * * * * *Gaimon [32] *Suresh and Meredith [33] * * * * * * *Naik and Chakravarty [34] *Badiru et al. [35] *Parker et al. [36] * * *Griffiths and Willcocks [37] *Barat [38] *

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211202

The model presented in Fig. 1 is divided intofour hierarchical levels of evaluation; strategic,tactical, operational and financial. At the level ofstrategic evaluation, the emphasis is placed on therelative impact of the project in relation to thedelivery of a competitive advantage. The modelbegins with a consideration of the corporatephilosophy, core values and beliefs, which trans-late into a mission statement. This provides a vividdescription of what the organisation will be likewhen ‘success’ has been achieved. These issueswill be reflected in the organisations strategicbusiness plan, which broadly identifies wherethe company is relative to its market place. Indoing so, establishing: where it is going in itsmarket place; and how it is going to get there,with all these issues being broken down intolong/medium term objectives. Once the strategic‘game plan’ has been ‘mapped-out’ and resourcesidentified, there is then a need to identify tacticalproject critical success factors (CSFs) (see [48]).These are project requirements that must befulfilled at a tactical level, by isolating detailedtasks, processes and resources, to ensure short-term project success.

Hochstrasser and Griffiths [40] explain that ifthese CSFs are not achieved, they will ultimatelybecome obstacles to corporate progress, and willresult in a loss of business, and a failure in theachievement of project objectives. It is essentialthat when tactical CSFs are identified, appropriate‘hybrid’ performance indicators are also identified.Fig. 2 provides a pictorial description of thevarious levels of performance measures. Further-more, it is essential to develop appropriatemechanisms for their quantification (performanceenablers).

The next level specifies the identification ofoperational CSFs. These are requirements thatmust be achieved on an operational day-to-daylevel to ensure project success. Again, whenoperational CSFs are identified, appropriate‘micro’ performance measures must also bedetailed. Such indicators might include the impactthe project has on inventory levels, productionthroughput, scrap levels, work-in progress, sche-dule adherence, machine downtime etc. It is thenessential to develop appropriate mechanisms fortheir quantification (performance enablers). Theformulation of ‘best practice’ performance en-

Fig. 1. A conceptual model for investment justification.

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211 203

ablers at both tactical and operational levelprovides an opportunity to identify and developperformance-measuring mechanisms. This willoffer an accurate and consistent way to measurethe performance of the project, which is correlatedto the benefits and costs used to justify theinvestment. This process will therefore, assist inculminating investment justification and post-implementation evaluation into one continuousactivity.

Finally, financial evaluation is addressed. Theobjective here is to match the most appropriatefinancial appraisal technique to the characteristicsof the project being implemented. Preliminaryresearch [49,50] suggests that this may be possible,as project characteristics affect the way in which aninvestment decision is made, and therefore indi-cates which of the available appraisal techniquesmight be more appropriate for a particularinvestment. The financial performance of theinvestment is then examined to see whether thefinancial returns achievable meet the specificrequirements of the organisation (paybackperiod, hurdle rates, etc). It is essential to considerthe financial implications of the project, as asuccessful investment decision must yield a returnin excess of the cost of capital invested. If afterfinancial analysis the outcome is positive, theproject may be selected, otherwise, the evaluationprocess is repeated, starting again with a strategicanalysis.

4. Investment decision-making: An expert or fuzzy

view

4.1. An expert systems view

Investment justification is notoriously subjec-tive, complex and time consuming. Yet, manycomputational approaches attempt to address thisproblem, such as expert systems. The use of thismethod entails asking a series of ‘Yes’ or ‘No’answer type questions, with various chains ofinferences held within a database. Expert systemshave been widely used in many different fields ofmanagement and engineering to increase knowl-edge about a problem domain [51,52] and hence,provide a means to a structured answer. Theseresults are then analysed using IF–THEN–ELSEtype structure [53] and some level of inferenceabout what the nature of the problem is. Apossible scenario solution can then be elicited.

Coats [54] notes that expert systems cannotcapture and deal with erroneous, inconsistent orincomplete knowledge, due to their reliance uponabstracted domain rules. Therefore, Coats viewssuch systems as providing knowledge assistancerather than executing decision-making insight.To try and overcome some of the limitationsidentified above, a more sophisticated level of‘intelligence’ was sought, which prompted theinvestigation and subsequent application of fuzzylogic. The application of this technique offered acrucial contribution in providing a further insightinto the relationships between the key variablespertinent to the proposed conceptual modeldetailed in Fig. 1. One of the reasons for choosingthis approach was to try and overcome the issue ofbrittleness, that is having an adaptable intelligentsystem that would be able to cope with increasesin the knowledge domain without producingerroneous solutions and/or ceasing to functioneffectively [55]. This AI approach is a methodwhich is generally applied when vague or ‘fuzzy’problems can be abstracted, simplified and over-come by using a derivative of standard mathema-tical set theory. These concepts have been usedsuccessfully in many areas of technology andscience, and when used in the context of aninvestment justification framework, could help to

Fig. 2. Tangible and intangible performance measures

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211204

increase the ‘intelligence’ of the decision-makingprocess.

4.2. A fuzzy logic view – FCM

Fuzzy logic dictates that everything is a matterof degree. Instead of variables/answers in a systembeing either ‘Yes’ or ‘No’ to some user-specifiedquestion, variables can be ‘Yes’ and ‘No’ to somedegree. The principles that form the genesis offuzzy logic are built on the notion of variable(s)existing/belonging to a set of numerical values tosome degree. Membership of variables to a certainset can be both associative and distributive: thewhole can also be a part [56]. By extending thisview further, fuzzy logic allows a membership ofmore than one set of concepts and consequently,let sets of statements overlap and merge with oneanother. It is not within the scope of this paper topresent an overview of fuzzy logic and the reader isdirected to the seminal work on the subject byZadeh [57] and in the more recent non-mathema-tical text by Kosko [56].

In this paper, the concept of an FCM is used todefine the state of a set of variables/objectives.Cognitive and causal rules model the system andthus, allow some of the inherent qualitativeobjectives to be related in a non-hierarchicalmanner. It should be noted that this is not thesame idea as proposed by Zadeh [58], with respectto ‘computing with words’ (CW) where words andsemantic structure are used instead of numbers toachieve a better modelling of reality. The FCM isessentially an artificial neural system (ANS) [59]which seeks to mimic how the human brainassociates and deals with different inputs andevents, and is best summarised by Kosko [56, p.222]:

An FCM draws a causal picture. It ties factsand things and processes to values and policiesand objectives... it lets you predict how complexevents interact and play out.

Typically, an FCM is a non-hierarchic flowgraph from which the effect of subsequent changesin local parameter values can be seen to effectglobal parameters. Each parameter is a statementor concept that can be linked to another such

statement or concept to produce the nodes of theFCM. This can be achieved via some direct butusually indirect and vague association that theanalyst of the system understands but cannotreadily quantify in numerical terms. Changes toeach statement, hence the fuzzy concept, can begoverned by a series of causal increases ordecreases.

These incremental variances are generally in theform of a normalised weighing measure (in theordinal range of 0.0–1.0). The advantage with anFCM is that even if the initial mapping of theproblem concepts is incomplete or incorrect,further additions to the map can be included,and the effects of new parameters can be quicklyseen. This has the advantage over many quantita-tive methods in that no laborious ‘accounting’ ofeach parameter needs to be done. Each concept isjudged not only on its own merits but also on theassociated merits that link to it via the causal fuzzyweights. Furthermore, and most importantly, theanalysis of a particular problem allows the analystto view the holistic picture, as the systemparameters evolve, therefore allowing the incor-poration of the wider strategic perspective.

However, certain aspects of the problem beingmodelled may appear to be unimportant in thelight of the so-called ‘hidden patterns of inference’,within the causal links relating to each statement.As such, an FCM is a dynamic system model,which thrives on feedback from each concept (i.e.intercommunication). This is a key differencebetween the FCM and other cognitive maps thathave been used frequently in psychology, such asthose described by Axelrod [60] and Montazemiand Conrath [61].

From an AI perspective, an FCM is a supervisedlearning neural system, where as more andmore data becomes available to model theproblem, the FCM becomes better at adapt-ing itself and developing a solution [62]. Hence,FCMs (and their neural network counterparts,neuro-fuzzy systems) are very good at producingresponses from a given set of initial conditions.A more rigorous appraisal of what is knownas supervised learning in the context of themathematical basis of FCMs can be found inRef. [63].

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211 205

4.3. The FCM for investment evaluation

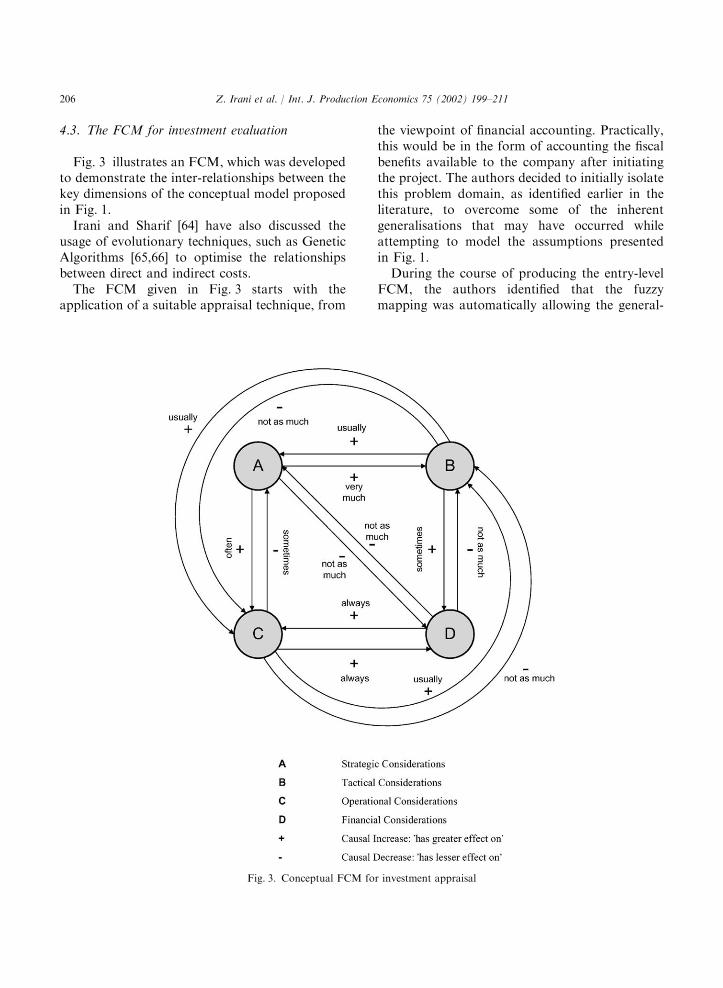

Fig. 3 illustrates an FCM, which was developedto demonstrate the inter-relationships between thekey dimensions of the conceptual model proposedin Fig. 1.

Irani and Sharif [64] have also discussed theusage of evolutionary techniques, such as GeneticAlgorithms [65,66] to optimise the relationshipsbetween direct and indirect costs.

The FCM given in Fig. 3 starts with theapplication of a suitable appraisal technique, from

the viewpoint of financial accounting. Practically,this would be in the form of accounting the fiscalbenefits available to the company after initiatingthe project. The authors decided to initially isolatethis problem domain, as identified earlier in theliterature, to overcome some of the inherentgeneralisations that may have occurred whileattempting to model the assumptions presentedin Fig. 1.

During the course of producing the entry-levelFCM, the authors identified that the fuzzymapping was automatically allowing the general-

Fig. 3. Conceptual FCM for investment appraisal

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211206

isation of the key concepts included in theconceptual framework, presented earlier in thispaper. This meant that by modelling a simplesystem via this fuzzy mapping technique, it ispossible to extend the dimensionality of theproblem quite easily.

In the FCM explanation that follows, the readeris directed to the legend shown in Fig. 3, wherestrategic, tactical, operational and financial con-siderations are denoted by the letters ‘A’, ‘B’, ‘C’and ‘D’, respectively. Each consideration, hereby afuzzy concept in the FCM, is related to every otherconcept (i.e. to each fuzzy node) by linking it withan arrow, which shows where a relationship exists.It should be noted that there is no hierarchybetween these fuzzy concepts and the letters (A, B,C and D) which have been represented in the mapfor brevity. Further, the ‘+’ and ‘�’ signs locatedabove the lines connecting the encircled variablesare not numerical operators or substantiators, inthat they do not show (absolute) scalar quantityincreases or decreases between each system con-cept. Instead these signs denote causal relation-ships in terms of descriptors, which in this casemean ‘has greater effect on’, and ‘has lesser effecton’, respectively. Additional fuzzy terms can alsobe used to delimit the meaning of these operators,e.g. ‘+ often’ would be read as ‘often has greatereffect on’, etc.

The map can be read in any direction andrelationships can be viewed in terms of any rootconcept, as it is a non-hierarchic flow diagram (asstated earlier). However, in order to clarify andhighlight pertinent relationships between the keyvariables in the map, it is often easier to beginfrom a starting/root concept. The map is read byseeing which concept is linked together withanother one, and uses the ‘+’ or ‘�’ signs aboveeach arrowed line to provide a causal relation-ship between them. For brevity in what follows, wewill denote such relationships in the followingmanner:

‘oconcept 1 > oconcept 2 > ½þor��’

For example, ‘AB�’ would mean an arrowed lineconnects ‘A’ to ‘B’ and would be read as ‘conceptA has little effect on concept B’. Taking a finance-

orientated viewpoint to project justification (‘D’),we can read the map shown in Fig. 3 as follows:

(i) Justifying a project purely on financial termshas little effect on the strategic considerations(‘A’). This has been read as the arrow goingfrom (‘D’) to (‘A’) and taking the ‘�’ signabove the line means ‘has less effect on’, i.e.‘DA�’. Similarly, strategic considerationshave little impact on the financial justificationprocess as many of the benefits are largelyqualitative and hence, not financially quantifi-able (i.e. ‘AD�’).

(ii) Justifying a project based upon tactical con-siderations, is more quantitative than asses-sing a project based upon strategic investmentcriteria (but less so than an operationalinvestment) (i.e. ‘BD+’).

(iii) Operational considerations can be appraisedfinancially without much difficulty as ‘day-to-day’ operations can be quantified in terms ofcurrent resources and operational CSFs (i.e.‘DC+’ and ‘DC�’).

(iv) Strategic issues help to justify investments andsubstantiate tactical considerations/tacticalCSFs and vice versa: since tactical andstrategic dimension can be viewed as beinglong/medium term processes. Appraising aproject in terms of any of these two wouldmean that a tactically based justificationwould be well suited to meeting the strategicgoals of the company eschewed in the corpo-rate mission/vision statement (i.e. ‘AB+’ and‘AB�’).

(v) Since strategic considerations take account oflong-term objectives and goals, appraising aproject based on operational factors is bestsuited to traditional methodologies, largelybecause of their quantitative nature. If anoperational project was to be appraised solelyon its operational characteristics, the strategicconsideration for this would be weak, orrather would not be substantial enough tojustify a project by itself (i.e. ‘CA�’).

(vi) In order to justify projects solely on opera-tional or tactical grounds, via a financialproject appraisal impetus, it can be arguedthat operational considerations have greater

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211 207

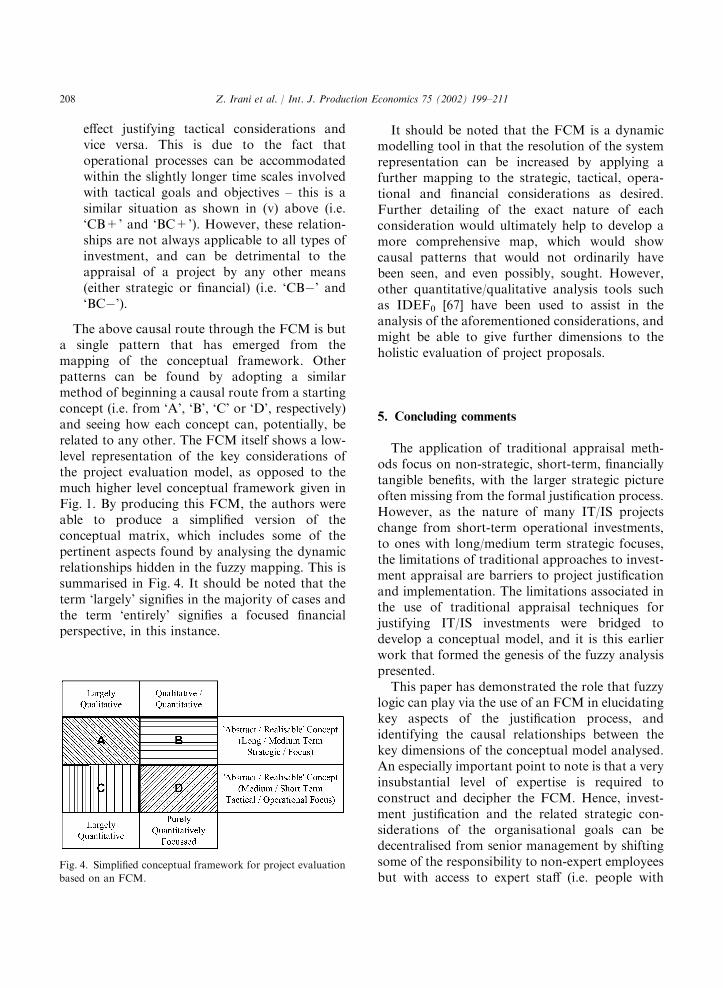

The above causal route through the FCM is buta single pattern that has emerged from themapping of the conceptual framework. Otherpatterns can be found by adopting a similarmethod of beginning a causal route from a startingconcept (i.e. from ‘A’, ‘B’, ‘C’ or ‘D’, respectively)and seeing how each concept can, potentially, berelated to any other. The FCM itself shows a low-level representation of the key considerations ofthe project evaluation model, as opposed to themuch higher level conceptual framework given inFig. 1. By producing this FCM, the authors wereable to produce a simplified version of theconceptual matrix, which includes some of thepertinent aspects found by analysing the dynamicrelationships hidden in the fuzzy mapping. This issummarised in Fig. 4. It should be noted that theterm ‘largely’ signifies in the majority of cases andthe term ‘entirely’ signifies a focused financialperspective, in this instance.

It should be noted that the FCM is a dynamicmodelling tool in that the resolution of the systemrepresentation can be increased by applying afurther mapping to the strategic, tactical, opera-tional and financial considerations as desired.Further detailing of the exact nature of eachconsideration would ultimately help to develop amore comprehensive map, which would showcausal patterns that would not ordinarily havebeen seen, and even possibly, sought. However,other quantitative/qualitative analysis tools suchas IDEF0 [67] have been used to assist in theanalysis of the aforementioned considerations, andmight be able to give further dimensions to theholistic evaluation of project proposals.

5. Concluding comments

The application of traditional appraisal meth-ods focus on non-strategic, short-term, financiallytangible benefits, with the larger strategic pictureoften missing from the formal justification process.However, as the nature of many IT/IS projectschange from short-term operational investments,to ones with long/medium term strategic focuses,the limitations of traditional approaches to invest-ment appraisal are barriers to project justificationand implementation. The limitations associated inthe use of traditional appraisal techniques forjustifying IT/IS investments were bridged todevelop a conceptual model, and it is this earlierwork that formed the genesis of the fuzzy analysispresented.

This paper has demonstrated the role that fuzzylogic can play via the use of an FCM in elucidatingkey aspects of the justification process, andidentifying the causal relationships between thekey dimensions of the conceptual model analysed.An especially important point to note is that a veryinsubstantial level of expertise is required toconstruct and decipher the FCM. Hence, invest-ment justification and the related strategic con-siderations of the organisational goals can bedecentralised from senior management by shiftingsome of the responsibility to non-expert employeesbut with access to expert staff (i.e. people with

Fig. 4. Simplified conceptual framework for project evaluation

based on an FCM.

effect justifying tactical considerations andvice versa. This is due to the fact thatoperational processes can be accommodatedwithin the slightly longer time scales involvedwith tactical goals and objectives – this is asimilar situation as shown in (v) above (i.e.‘CB+’ and ‘BC+’). However, these relation-ships are not always applicable to all types ofinvestment, and can be detrimental to theappraisal of a project by any other means(either strategic or financial) (i.e. ‘CB�’ and‘BC�’).

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211208

special appraisal skills within IT/IS and manufac-turing).

The delegation of responsibilities from apprais-ing and justifying new investment in IT/IS mightcause concern for many line managers but thebenefits of allowing cross-functional teams to getinvolved in the justification process will clearly addsynergy and value to the decision making process.Hence, by increasing the level of known dataabout such a vague and, to some extent, intrinsi-cally incalculable problem, a causal route tojustifying a project has been found via an FCM.Although more research is required to furtherrefine and apply the framework developed, theadoption of the proposed methodology andfurther application of fuzzy logic could clearlyavoid some of the difficulties encounteredwhile using traditional approaches to projectjustification.

References

[1] M.N. Baily, A. Chakrabarti, Innovation and the Produc-

tivity Crisis, Brookings Institution, Washington, DC,

1988.

[2] S.S. Roach, Services under siege: The restructuring

imperative, Harvard Business Review 69 (1991) 83–91.

[3] E. Brynjolfsson, The productivity paradox of information

technology, Communications of the ACM 36 (12) (1993)

67–77.

[4] R.F. Huber, CIM: Inevitable but not easy, Production

Engineer (1986) 52–57.

[5] M.H. Small, J. Chen, Investment justification of advanced

manufacturing technology: An empirical analysis, Journal

of Engineering and Technology Management 12 (1–2)

(1995) 27–55.

[6] Z. Irani, P.E.D. Love, The propagation of technology

management taxonomies for evaluating investments in

information systems, Journal of Management Information

System 17 (3) (2001) 161–177.

[7] V. Serafeimidis, S. Smithson, Information systems evalua-

tion in practice: A case study of organisational change,

Journal of Information Technology 15 (2) (2000) 93–105.

[8] G. Khalifa, Z. Irani, L.P. Baldwin, IT evaluation methods:

drivers and consequences, Association for Information

System, 2000 Americas Conference on Information Sys-

tems (AMCIS2000) [CD Proceedings], Long Beach, CA,

USA, August 10–13, 2000.

[9] D. Remenyi, A. Money, M. Sherwood-Smith, Z. Irani, The

Effective Measurement and Management of IT Costs and

Benefits, 2nd Edition, Butterworth Heinemann/Computer

Weekly–Professional Information Systems Text Books

Series, London, UK, 2000, ISBN 0 7506 4420 6.

[10] S. Smithson, R. Hirschheim, Analysing information

systems evaluation: Another look at an old problem,

European Journal of Information Systems 7 (3) (1998)

158–174.

[11] B. Hochstrasser, Justifying IT investments, Conference

Proceedings on Advanced Information Systems; The New

Technologies in Today’s Business Environment, 1992,

pp. 17–28.

[12] B. Farbey, F. Land, D. Targett, IT Investment: A Study of

Methods and Practices, Published in association with

Management Today and Butterworth-Heinemann Ltd.,

London, UK, 1993.

[13] J.-N. Ezingeard, Z. Irani, P. Race, Assessing the value and

cost implications of manufacturing information and data

systems: An empirical study, European Journal of

Information Systems 7 (4) (1999) 252–260.

[14] O.M. Burns, D. Turnipseed, W.E. Riggs, Critical success

factors in manufacturing resource planning implementa-

tion, International Journal of Operations and Production

Management 11 (4) (1991) 5–19.

[15] L. Willcocks, Information Management: The Evaluation

of Information Systems Investments, Chapman & Hall,

London, UK, 1994.

[16] Z. Irani, J.-N. Ezingeard, R.J. Grieve, Integrating the

costs of an IT/IS infrastructure into the investment

decision making process, The International Journal of

Technological Innovation, Entrepreneurship and Techno-

logy Management (Technovation) 17 (11/12) (1997)

695–706.

[17] Z. Irani, P.E.D. Love, M.T. Hides, Investment evaluation

of new technology: Integrating IT/IS cost management

into a model, Association for Information System, 2000

Americas Conference on Information Systems (AMCIS

2000) [CD Proceedings], Long Beach, CA, USA, August

10–13, 2000.

[18] R.J. Boaden, B. Dale, Justification of computer integrated

manufacturing: some insights into the practice, IEEE

Transactions on Engineering Management 37 (4) (1990)

291–296.

[19] P.L. Primrose, Investment in Manufacturing Technology,

Total Technology Department, UMIST, Manchester,

Chapman & Hall, London, UK, 1991.

[20] Z. Irani, Investment justification of information systems: A

focus on the evaluation of MRPII, Ph.D., Department of

Manufacturing and Engineering Systems, Brunel Univer-

sity, Uxbridge, UK, 1998.

[21] J.G. Demmel, R.G. Askin, Integrating financial, strategic,

and tactical factors in advanced manufacturing system

technology investment decisions, in: H.R. Parsei, W.G.

Sullivan, T.R. Hanley (Eds.), Economic and Financial

Justification of Advanced Manufacturing Technologies,

Elsevier, Amsterdam, 1992, pp. 209–243.

[22] V. Datta, K.V. Sambasivarao, R. Kodali, S.G. Deskmukh,

Multi-attribute decision model using the analytic hierarchy

process for the justification of manufacturing systems,

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211 209

International Journal of Production Economics 28 (2)

(1992) 227–234.

[23] W.G. Sullivan, J.M. Reeve, XVENTURE: expert systems

to the rescue – they can help justify investments in new

technology, Management Accounting (1988) 51–58.

[24] R.F. Huber, Justification – barrier to competitive manu-

facturing, Production (1985) 46–51.

[25] R.S. Kaplan, Must CIM be justified on faith alone?

Harvard Business Review (1986) 87–95.

[26] S.E. Garrett, Strategy first: A case in FMS justification,

Proceedings of the Second ORSA/TIMS Conference on

Flexible Manufacturing Systems, 1986 pp. 17–29.

[27] P. Swamidass, M. Waller, A classification of approaches to

planning and justifying new manufacturing technologies,

Journal of Manufacturing Systems 9 (2) (1991) 181–193.

[28] M.C. Burstein, Finding the economical mix of rigid and

flexible automation for manufacturing systems, Proceed-

ings of the Second ORSA/TIMS Conference on Flexible

Manufacturing Systems, 1986, pp. 69–81.

[29] P. Huang, M. Sakurai, Factory automation: The Japanese

experience, IEEE Transactions on Engineering Manage-

ment 37 (2) (1990) 102–108.

[30] C.A. Nelson, A scoring model for flexible manufacturing

systems project selection, European Journal of Operational

Research 24 (3) (1986) 346–359.

[31] J.R. Meredith, N.C. Suresh, Justification techniques for

advanced technologies, International Journal of Produc-

tion Research 24 (5) (1986) 1043–1057.

[32] C. Gaimon, The strategic decision to acquire flexible

technology, Proceedings of the Second ORSA/TIMS

Conference on Flexible Manufacturing Systems, 1986,

pp. 43–54.

[33] N.C. Suresh, J.R. Meredith, Justifying multi-machine

systems: An integrated strategic approach, Journal of

Manufacturing Systems 4 (2) (1985) 117–134.

[34] B. Naik, A.K. Chakravarty, Strategic acquisition of new

manufacturing technology: A review and research frame-

work, International Journal of Production Research 30 (7)

(1992) 1575–1601.

[35] A. Badiru, B. Foote, J. Chetupuzha, A multi-attribute

spreadsheet model for manufacturing technology

justification, Computer, Industrial Engineering 21 (1–4)

(1991) 29–33.

[36] M. Parker, R. Benson, H. Trainor, Information Econom-

ics: Linking Business Performance to Information Tech-

nology, Prentice-Hall International, Englewood Cliffs, NJ,

1988.

[37] C. Griffiths, L. Willcocks, Are major information technol-

ogy projects worth the risk? Proceedings of the First

European Conference on Information Technology Invest-

ment Evaluation, Henley Management College, Henley on

Thames, England, September 13–14, 1994.

[38] J. Barat, Scenario planning for critical success factor

analysis, Journal of Information Technology 7 (1992) 12–

19.

[39] B. Farbey, F. Land, D. Targett, Evaluating investments in

IT, Journal of Information Technology 7 (1992) 109–122.

[40] B. Hochstrasser, C. Griffiths, Controlling IT Investment;

Strategy and Management, Chapman & Hall, London,

UK, 1991.

[41] J. Van Blois, Economic models: the future of robotic

justification, Proceedings of the 13th ISIR/Robots 7

Conference, April 1983, pp. 17–21.

[42] B. Maskell, Performance Measurement for World Class

Manufacturing: A Model for American Companies,

Productivity Press, USA, 1991.

[43] T. Hill, Manufacturing Strategy; The Strategic Manage-

ment of the Manufacturing Function, 2nd Edition, The

Macmillan Press, UK, 1993.

[44] J. Hares, D. Royle, Measuring the Value of Information

Technology, Wiley, UK, 1994.

[45] R.S. Kaplan, Financial Justification for the Factory

of the Future, Harvard Business School, Boston, MA,

1985.

[46] K. Kumar, Post implementation evaluation of computer-

based information systems, Communications of the ACM

33 (2) (1990) 203–212.

[47] Z. Irani, J-N. Ezingeard, R.J. Grieve, P. Race, Investment

justification of information technology in manufacturing,

The International Journal of Computer Applications in

Technology 12 (2) (1999) 90–101.

[48] J.F. Rockart, Chief executives define their own data needs,

Harvard Business Review 57 (2) (1979) 81–93.

[49] B. Farbey, D. Targett, F. Land, Matching an IT project

with an appropriate method of evaluation: A research note

on evaluating investments in IT, Journal of Information

Technology 9 (3) (1994) 239–243.

[50] B. Farbey, F. Land, D. Targett, System–method–context:

A contribution towards the development of guidelines

for choosing a method of evaluating I/S investments,

Proceedings of the Second European Conference on

Information Technology Investment Evaluation, Henley

Management College, Henley on Thames, England, July

11–12, 1995.

[51] D.M. Dilts, D.G. Turowski, Strategic investment justifica-

tion of advanced manufacturing technology using a

knowledge-based system, Proceedings of Third Interna-

tional Conference Express System and the Leading Edge in

Production and Operation Management, University of

South Carolina Press, 1989, pp. 193–206.

[52] D.E. Grierson, G.E. Cameron, A knowledge based

expert system for computer automated structural

design, the application of artificial intelligence techni-

ques to civil and structural engineering, Proceedings of

the Third International Conference on Civil and

Structural Engineering, Civil Comp. Press, Swansea,

1987, pp. 93–97.

[53] P. Jackson, Introduction to Expert Systems, Addison-

Wesley, Reading, MA, 1990.

[54] P.K. Coats, A critical look at expert systems for business

information applications, Journal of Information Tech-

nology 6 (1991) 208–216.

[55] S. Goonatilake, S. Khebbal, Intelligent Hybrid Systems,

Wiley, New York, 1994.

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211210

[56] B. Kosko, Fuzzy Thinking: the New Science of Fuzzy

Logic, Flamingo Press, 1990.

[57] L.A. Zadeh, Fuzzy sets, Information and Control 8 (1965)

338–353.

[58] L.A. Zadeh, Fuzzy logic=computing with words, IEEE

Transactions on Fuzzy Systems 4 (2) (1996) 103–111.

[59] E. Hinton, How neural networks learn from experience,

Scientific American 267 (1992) 144–151.

[60] R. Axelrod, Structure of Design, Princeton University

Press, Princeton, NJ, 1976.

[61] A. Montazemi, D. Conrath, The use of cognitive mapping

for information requirement analysis, Management In-

formation Systems Quarterly 10 (1) (1986) 44–55.

[62] I. Aleksander, H. Morton, An Introduction to Neural

Computing, Chapman & Hall, London, UK, 1990.

[63] P.K. Simpson, Artificial Neural Systems: Foundations,

Paradigms and Applications, McGraw-Hill, New York,

1990.

[64] Z. Irani, A. Sharif, Genetic algorithm optimisation of

investment justification theory, Proceeding of the Late

Breaking Papers at Genetic Programming, Stanford

University, CA, USA, July 13–16, 1997.

[65] D.E. Goldberg, Genetic Algorithms in Search, Optimisa-

tion and Machine Learning, Addison-Wesley, Reading,

MA, 1989.

[66] J.H. Holland, Adaption in Natural and Artificial Systems:

An Introductory Analysis with Applications to Biology,

Control and Artificial Intelligence, MIT Press, Cambridge,

MA, 1992.

[67] J. Sarkis, D. Liles, Using IDEFO and QFD to develop

an organisational decision support methodology for the

strategic justification of computer-integrated technologies,

International Journal of Project Management 13 (3) (1995)

177–185.

Z. Irani et al. / Int. J. Production Economics 75 (2002) 199–211 211