Appendix

18

APPENDIX Planning Forms A set of standard forms can be helpful in presenting strategy recommendations and supporting analyses. The forms can encourage the useful consistency of the presentation over time and across businesses within an organization. They can also provide a checklist of areas to consider in strategy development and make communication easier. The following sample forms are intended to provide a point of departure in designing forms for a specific context. The external analysis in the example is drawn from the pet food industry. The forms are for illustration purposes only. Planning forms need to be adapted to the context involved: the industry, the firm, and the planning context. They may well be different and shorter or longer given a particular context. Forms for use with other product types—an industrial product, for example— could be modified to include information such as current and potential applications or key existing or potential customers. THE PET FOOD INDUSTRY Section 1. Customer Analysis A. Segments

-

Upload

master-mind -

Category

Business

-

view

1 -

download

0

Transcript of Appendix

APPENDIX

Planning Forms

A set of standard forms can be helpful in presenting strategy recommendations and supporting analyses. The forms can encourage the useful consistency of the presentation over time and across businesses within an organization. They can also provide a checklist of areas to consider in strategy development and make communication easier. The following sample forms are intended to provide a point of departure in designing forms for a specific context. The external analysis in the example is drawn from the pet food industry. The forms are for illustration purposes only.Planning forms need to be adapted to the context involved: the industry, the firm, and the planning context. They may well be different and shorter or longer given a particular context. Forms for use with other product types—an industrial product, for example—could be modified to include information such as current and potential applications or key existing or potential customers.

THE PET FOOD INDUSTRY

Section 1. Customer Analysis

A. Segments

B. Customer Motivations

Segment Motivations

Dog—dry Nutrition, convenience, teeth cleaning, often better value than canned pet food in grocery and mass channels

Dog—canned

For finicky dogs, taste and nutrition, variety

Cat—dry Nutrition, convenience, complement to meal, teeth cleaning

Cat—canned Taste, convenient sizes, easy to serve, for finicky cats, variety of textures and flavors

Treats Complement to meal, reward, animal likes it, functional nutritional benefits (e.g., tartar control)

Pet specialty Health concern, scientific nutrition, perceived superior ingredients

C. Unmet Needs

Information on petsFurther subneeds of segments (as defined by human nutrition, e.g., allergies)

Section 2. Competitor Analysis

A. Competitor Identification

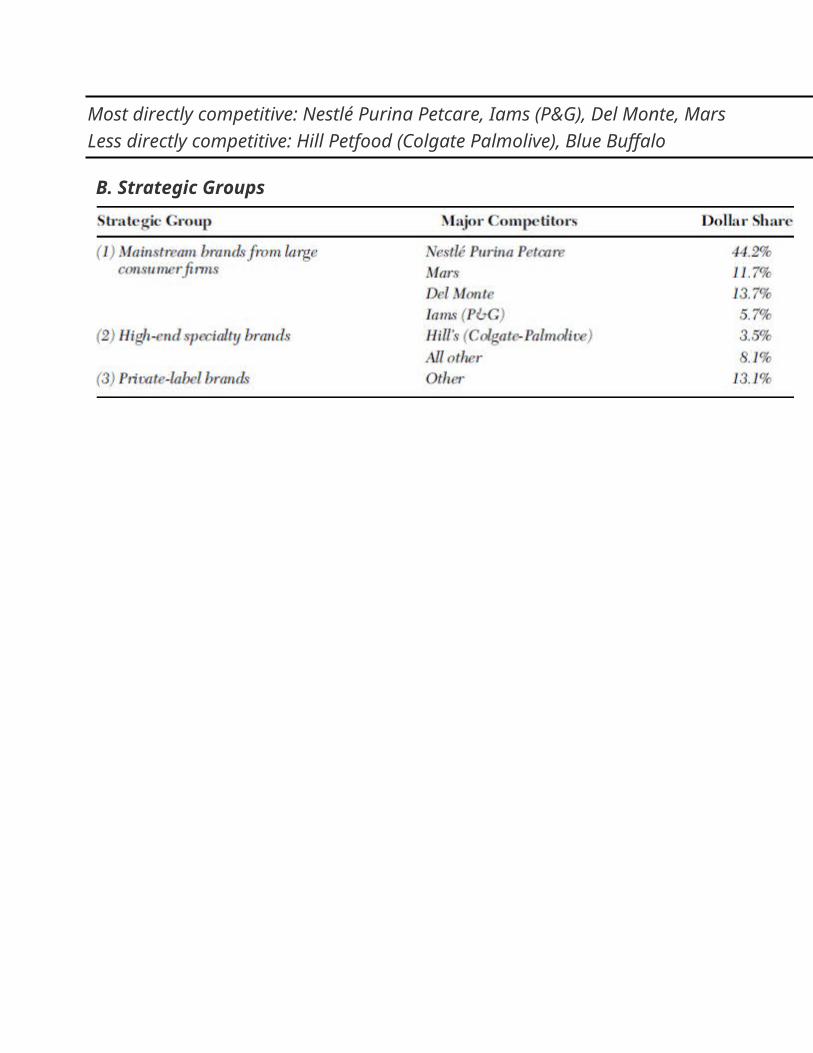

Most directly competitive: Nestlé Purina Petcare, Iams (P&G), Del Monte, MarsLess directly competitive: Hill Petfood (Colgate Palmolive), Blue Buffalo

B. Strategic Groups

C. Major Competitors

D. Competitor Strength Grid

Section 3. Market Analysis

A. Market Identification: The U.S. Pet Food Market

B. Market Size

Emerging Submarkets

o Special diet-based productso Wal-Mart and other private-label productso Wellness-focused items (e.g., Naturals)o Product “humanization”

Market Growth (in Dollars vs. 2011)

o Overall pet—growing at 5 percento Supermarket—growing at 3 percento Specialty store—growing at 3 percent annuallyo Mass merchandisers—growing at 7 percent annuallyo Drug—growing at 5 percent

Factors Affecting Sales Levels

o Growth of pet populationo Growth of higher-value productso General economic consumer pressure, especially at low end

of the market

C. Market Profitability Analysis

Barriers to Entry

o Brand awareness, budget for marketing programs, access to distribution channels, large investment required for manufacturing, science, and technology.

o For pet specialty segment—loyalty to Hill's Science Diet and other entrenched specialty brands; difficulty of getting recommendations of vets and other influentials

Potential Entrants

o The probability of new entrants is quite low because the pet food industry is already very competitive, with lots of incumbents, and barriers to entry are high.

Threats of Substitutes

o Human food leftoverso Food cooked especially for pets

Bargaining Power of Suppliers

o Growing.o Raw materials shared with human food markets.o Consolidation of suppliers.o Quality of raw ingredients requirements growing.

Bargaining Power of Customers

o Grocery stores and warehouse clubs have strong bargaining power over pet food suppliers.

o Specialty stores and veterinarians might have moderate bargaining power.

o Mass merchandisers (especially Wal-Mart, with around 24 percent of the volume in this category) have very strong bargaining power.

D. Cost Structure

o Diversified firms have lower cost because of economies in advertising, manufacturing, promotion, and distribution.

o Specialized firms have higher costs and often are required to co-manufacture their products.

E. Distribution System

Major Channels

o Supermarkets are dominant in terms of quantity they deal with (35 percent).

o Mass merchandisers handle about 29 percent of market and are growing.

o Pet foods are effective traffic builders in supermarkets and mass merchandisers.

o Farm-supply stores are generally located in suburbso Pet stores handle most premium brands and many

“mainstream” national brands.o Veterinarians handle only superpremium brands.

Observations/Major Trends

o Vets' sales are flat and have very high margins both for producers and for themselves.

o Specialty stores' sales are growing at approximately 6 percent.

o These two channels have captured high-involvement customers' needs to feed their pets healthier foods.

o Warehouses have gained footholds in market-leader brands.o Innovations in packaging are begging to address unmet

needs around convenienceo Product innovations are creating subcategories.

F. Market Trends and Developments

o Premium and superpremium brands have grown, and most producers are introducing new products in this area.

o Large manufacturers are introducing new products continuously.

G. Key Success Factors

Present

o Brand recognitiono Product qualityo Access to major channelso Gain market share in premium brandso Introduction of new productso Breadth of product lineo Marketing programo Cost reductiono Awareness or recommendation by specialistso Packagingo Capitalizing on relevant human trends (naturals; shift to

healthier, higher-quality ingredients)

Future

o Continue to capture the trends of consumerso Packagingo Follow the trends of distributors Ability to demonstrate

corporate responsibility (e.g., environmental sustainability)

Section 4. Environmental Analysis

A. Trends and Potential Events

B. Scenario Analysis

Two most likely are:1. Little growth in specialty-store and superpremium segments2. High growth in both specialty-store and superpremium

segments

C. Key Strategic Uncertainties

o Will growth in demand for superpremium specialty products continue?

o What new subcategories will emerge as significant markets?

Section 5. Internal Analysis

A. Performance Analysis

B. Summary of Past Strategy

C. Strategic Problems

Problem Possible Action

D. Characteristics of Internal Organization

Component* Description—Fit with Current/Proposed Strategy

*Structure, systems, culture, and people.

E. Portfolio Analysis

F. Analysis of Strengths and Weaknesses

Reference Competencies/Competency Deficiencies, Assets/Liabilities,

Strategic Group Strengths/Weaknesses with Respect to Strategic Groups

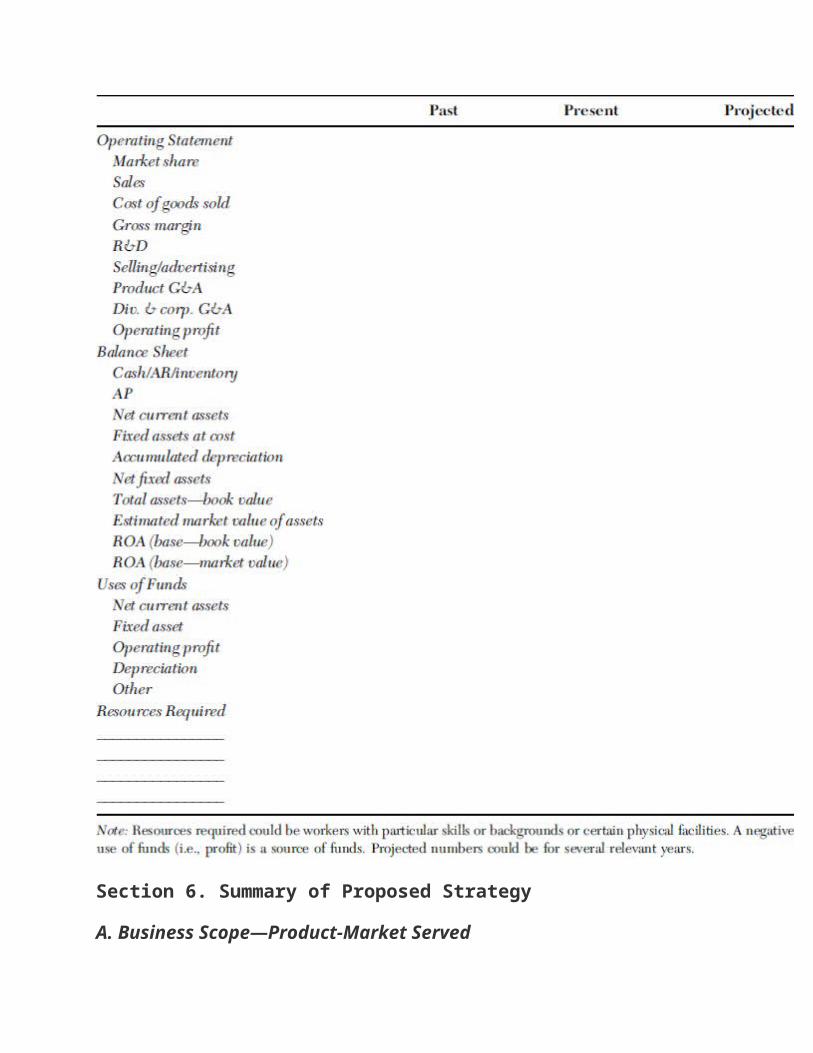

G. Financial Projections Based on Existing Strategy

Section 6. Summary of Proposed Strategy

A. Business Scope—Product-Market Served

B. Strategy Description

C. Key Strategy Initiatives

D. Financial Projections Based on Proposed Strategy