Anti - Money laundering

12

ANTI - MONEY LAUNDERING Presented by the Inspired Learning Regulatory Academy

description

Anti - Money laundering. Presented by the Inspired Learning Regulatory Academy. Anti Money laundering. Source: Section 2 General Code of Conduct. - PowerPoint PPT Presentation

Transcript of Anti - Money laundering

ANTI - MONEY LAUNDERING

Presented by the Inspired Learning Regulatory Academy

ANTI MONEY LAUNDERINGSource: Section 2 General Code of Conduct

Anti money laundering (AML) is a term

mainly used in the financial and legal

industries to describe the legal controls that

require financial institutions and other

regulated entities to prevent or report

money laundering activities. Anti-money

laundering guidelines came into prominence

globally after the September 11, 2001

attacks and the subsequent enactment of

the USA PATRIOT Act

AML does not deal with the crime itself

but the illegal proceeds of the crime

OUTCOME 50

ANTI-MONEY LAUNDERING

Protection of Constitutional

Democracy against Terrorist and Related

Activities

Prevention of Organized Crime

Act

Financial Intelligence Centre

Act

Deals with organised crime, money laundering and criminal gang activities

Introduces obligation to report terrorist related

activitiesIntroduces control measures

to assist in detection and investigation of money laundering activities

OUTCOME 50

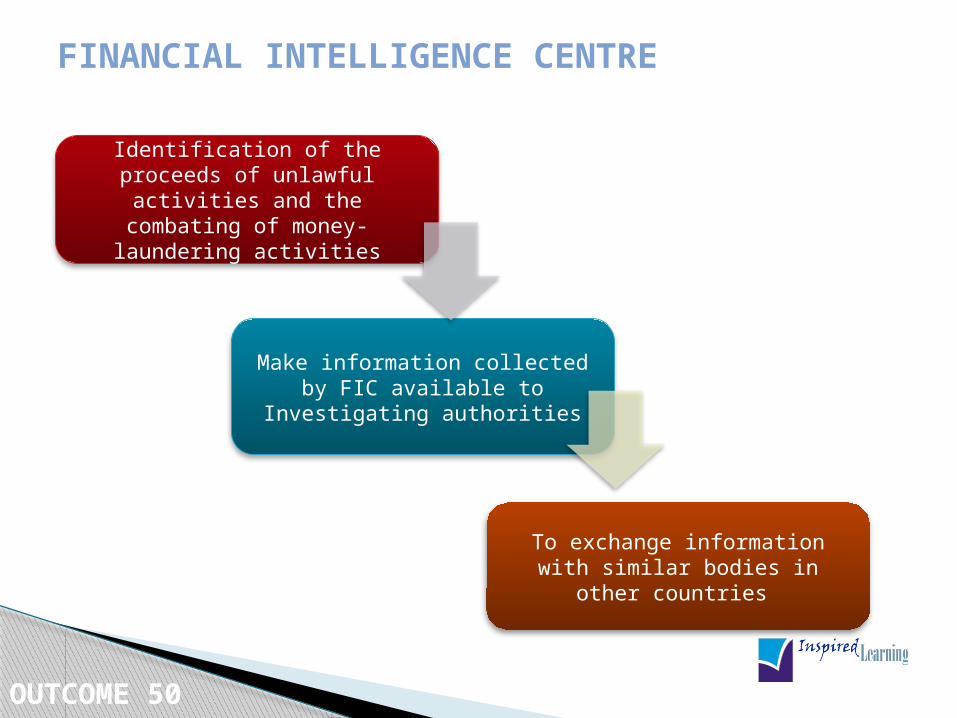

FINANCIAL INTELLIGENCE CENTRE

Identification of the proceeds of unlawful activities and the combating of

money-laundering activities

Make information collected by FIC available to Investigating authorities

To exchange information with similar bodies in other countries

OUTCOME 50

FINANCIAL INTELLIGENCE CENTRE

Bank

Insurance

Casino

Accountable Institutions

Trusts

NDPP

SARS

Investigative Authorities e.g..

SAPS

ML Advisory Council

Reports Reports

Investigations

Awareness & training

InternationalLinks

CoordinationSharing

Supervisory Bodies (FSB)

Compliance

Data storageAnalysisReports

FIC

FIC Overall Architecture

KNOW YOUR CLIENT DOCUMENTS

FSP

Natural Person

Company

Partnerships

Trusts & Foreign entities

Stokvels

Minors

Acting on another’s authority

Close Corporation

OUTCOME 50

FICA RECORD KEEPING

Keep 5 years after last TX

Update within 3 days of change notice

All changes must have proof

Confirm in writing every 2 years

Copies of all transactions

OUTCOME 50

50. FICA REPORTING

Suspicious or unusual transaction

Reported by internet or method

developed by FIC

STR’s (suspicious transaction report)

are guaranteed protection against

prosecution

Reported within 5 days of detection

Source: Sections 22,23,24,38 of FICA

ACCOUNTABLE INSTITUTIONSSource: FICA

An attorney A board of executors or a trust company …

An estate agent

A financial instrument trader…

A management company registered in terms of the Unit Trusts Control Act…

A person who carries on the "business of a bank”…

A mutual bank

A person who carries on a "long-term insurance business" …

A gambling business (license)…

A person … business of dealing in foreign exchange…

A person who carries on the business of lending money against the security of securities.

OUTCOME 50

ACCOUNTABLE INSTITUTIONSSource: FICA

A person who carries on the business of rendering investment advice or investment broking services … A public accountant … A person who issues, sells or redeems travelers' cheques, money The Postbank… A member of a stock exchange… The Ithala Development Finance Corporation … A person who has been approved … by the Registrar of Stock Exchanges A person who has been approved … by the Registrar of Financial Markets A person who carries on the business of a money remitter.

OUTCOME 50

51. FSP’S FICA RESPONSIBILITIES

Identify and verify clientsSteps taken to safeguard

funds and that funds dealt with ito mandateDistinguished from FSP funds

Adequate staff training

Outsource record keeping to 3rd parties

Electronic copies

Systems and procedures for FAIS/FICA compliance

Client identificationID and report suspicious

transactionRisk rating of client

Keep records of business

relationships and

transactions

Adopt measures

designed to promote

compliance by accountable institution

Reporting duties and

obligations to give and allow

access to information

OUTCOME 51

INTERNAL RULESSource: Section 42 of FICA

The purpose of internal rules is to regulate compliance with money- laundering legislation by the FSP,

Representatives, Agents, Staff and Key Individuals

To arrange responsibilities of each person in business and put in place

systems and procedures

Rules must be formulated for: Identification and verification of clients

Identifying and reporting suspicious transactions

Keeping records

OUTCOME 51