Anti-Corruption Management System - Swedfund · Corruption deepens poverty, undermines democracy...

33

Latest update August 2017 Anti-Corruption Management System

Transcript of Anti-Corruption Management System - Swedfund · Corruption deepens poverty, undermines democracy...

Latest update August 2017

Anti-Corruption Management System

2

Table of Content

PART 1: SWEDFUND’S ANTI-CORRUPTION COMMITMENT AND REQUIREMENTS ....... 3

1. Why is anti-corruption important for Swedfund? ................................................................ 3

2. Our commitment ...................................................................................................................... 3

3. Our requirements .................................................................................................................... 4

4. Advise for our Investment Managers ................................................................................... 4

5. Advise for our portfolio companies ....................................................................................... 5

5.1 The process to identify and mitigate corruption risks ..................................................... 5

5.2 Typical situations with high corruption risks ..................................................................... 7

PART 2: ANTI-CORRUPTION TOOLKIT FOR OUR PORTFOLIO COMPANIES ................. 10

1. Anti-Corruption Policy template .............................................................................................. 11

1. Commitment and scope of the policy ................................................................................ 11

2. Definition of (acts of) corruption ......................................................................................... 11

3. How to act if you come across (attempts at) acts of corruption ..................................... 12

4. Actions to take if acts of corruption are reported/observed ............................................ 12

5. Adoption of the Policy .......................................................................................................... 12

2. Role description of an Anti-Corruption Manager ................................................................. 13

3. Sample of routine descriptions ............................................................................................... 14

3.1 Routine for attestation ....................................................................................................... 15

3.2 Routine for contract signing .............................................................................................. 18

3.3 Routine for establishing a grievance mechanism.......................................................... 19

3.4 Routine for handling conflict of interest ........................................................................... 21

3.5 Routine for payment of salaries ....................................................................................... 23

3.6 Routine for handling payments to agents ....................................................................... 25

3.7 Routine for identifying appropriate gifts and hospitality ............................................... 27

3.8 Routine for payment to authorities................................................................................... 29

4. Recommended anti-corruption e-learnings .......................................................................... 31

5. Anti-Corruption Questionnaire included in Swedfund’s Annual Sustainability Report32

Further reading .................................................................................................................................. 33

3

PART 1: SWEDFUND’S ANTI-CORRUPTION COMMITMENT AND

REQUIREMENTS

Swedfund’s commitment to zero tolerance towards corruption applies to all

Swedfund’s employees, as well as board members and consultants, and for our

portfolio companies.

This document describes Swedfund’s anti-corruption management internally and

towards our portfolio companies. In addition, we provide some basic tools that can

support our portfolio companies’ anti-corruption work. This is a living document,

which will be continuously edited and updated based on our and our stakeholders’

expectations and feedback.

1. Why is anti-corruption important for Swedfund?

Corruption has political, economic, social, and environmental consequences.

Corruption deepens poverty, undermines democracy and the protection of human

rights, harms trade and deters investment, hinders good governance, and reduces

confidence in the institutions of society and the market economy.

Therefore Swedfund has adopted a zero tolerance towards corruption.

2. Our commitment

Swedfund has adopted four strategic sustainability goals. The fourth such goal

reads “Swedfund shall conduct active anti-corruption efforts, both internally and in

its portfolio companies.”

Swedfund is continuously working to improve our internal work against corruption.

Through the State owner policy, Swedfund is recommended to comply with the

Code on Gifts, Rewards and other Benefits (the “Business Code”) issued by the

Swedish Anti-Corruption Institute (Sw. Institutet mot mutor). During 2016 Swedfund

adopted an updated anti-corruption policy which applies to all employees of

Swedfund, board members, external board members representing Swedfund in our

portfolio companies and consultants. Swedfund has also adopted a policy on gifts,

hospitality and other benefits in line with the requirements in the Business Code. All

gifts to Swedfund’s employees (if to be received in accordance with said policy) are

registered in a gift registry. Furthermore, each employee is required to submit self-

declaration in case of a conflict of interest arises in an investment or in the daily

work in general. All employees have carried out an e-learning anti-corruption

training and further training is carried out on continuously basis. During 2016

Swedfund launched our whistleblowing system which can be used by both our

employees and our portfolio companies. The Chief Legal Counsel is responsible for

Swedfund anti-corruption work internally.

Within our investments, Swedfund shall work against corruption through assessing

and evaluating the risk of corruption prior to making an investment, by including

relevant covenants in legal agreements governing our investments and by

4

continuously monitoring adherence to these covenants. We will provide transparent

and relevant information regarding our activities when fighting corruption, while

taking into account our confidentiality commitment.

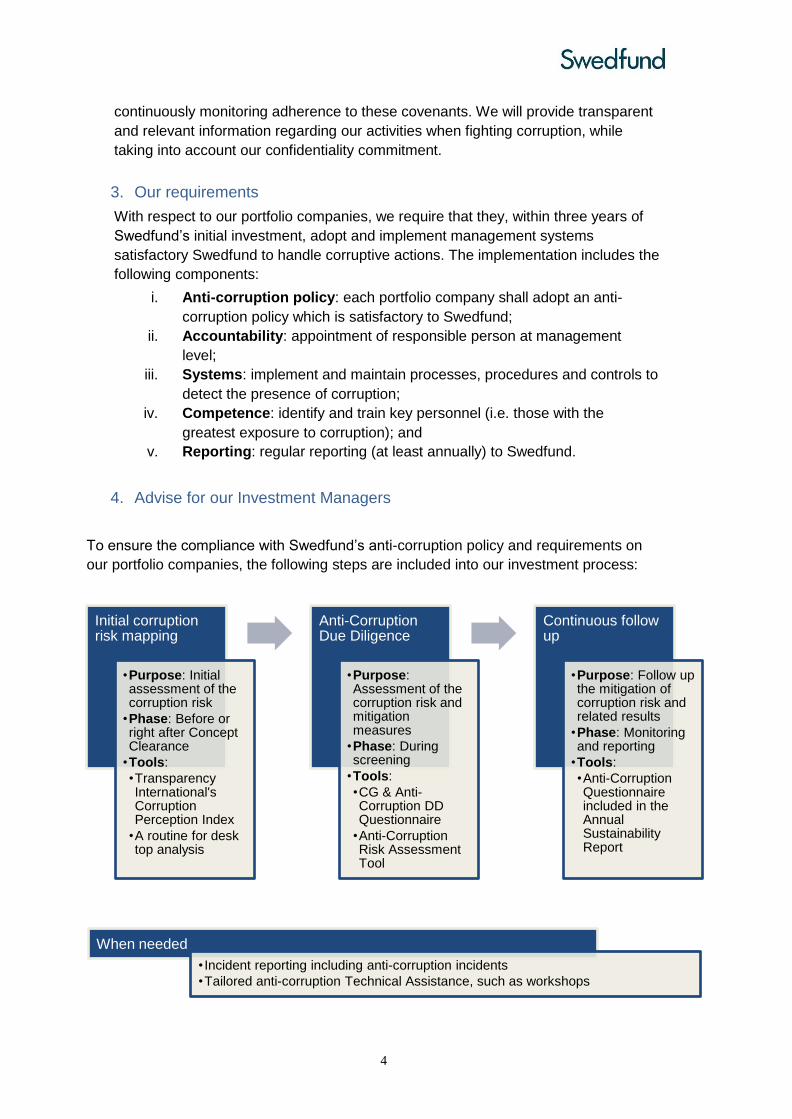

3. Our requirements

With respect to our portfolio companies, we require that they, within three years of

Swedfund’s initial investment, adopt and implement management systems

satisfactory Swedfund to handle corruptive actions. The implementation includes the

following components:

i. Anti-corruption policy: each portfolio company shall adopt an anti-

corruption policy which is satisfactory to Swedfund;

ii. Accountability: appointment of responsible person at management

level;

iii. Systems: implement and maintain processes, procedures and controls to

detect the presence of corruption;

iv. Competence: identify and train key personnel (i.e. those with the

greatest exposure to corruption); and

v. Reporting: regular reporting (at least annually) to Swedfund.

4. Advise for our Investment Managers

To ensure the compliance with Swedfund’s anti-corruption policy and requirements on

our portfolio companies, the following steps are included into our investment process:

Initial corruption risk mapping

•Purpose: Initial assessment of the corruption risk

•Phase: Before or right after Concept Clearance

•Tools:

•Transparency International's Corruption Perception Index

•A routine for desk top analysis

Anti-Corruption Due Diligence

•Purpose: Assessment of the corruption risk and mitigation measures

•Phase: During screening

•Tools:

•CG & Anti-Corruption DD Questionnaire

•Anti-Corruption Risk Assessment Tool

Continuous follow up

•Purpose: Follow up the mitigation of corruption risk and related results

•Phase: Monitoring and reporting

•Tools:

•Anti-Corruption Questionnaire included in the Annual Sustainability Report

When needed

• Incident reporting including anti-corruption incidents

•Tailored anti-corruption Technical Assistance, such as workshops

5

Swedfund’s Investment Manual and ESG Toolkit include detailed instructions and

templates for Investment Managers regarding the steps above.

5. Advise for our portfolio companies

5.1 The process to identify and mitigate corruption risks

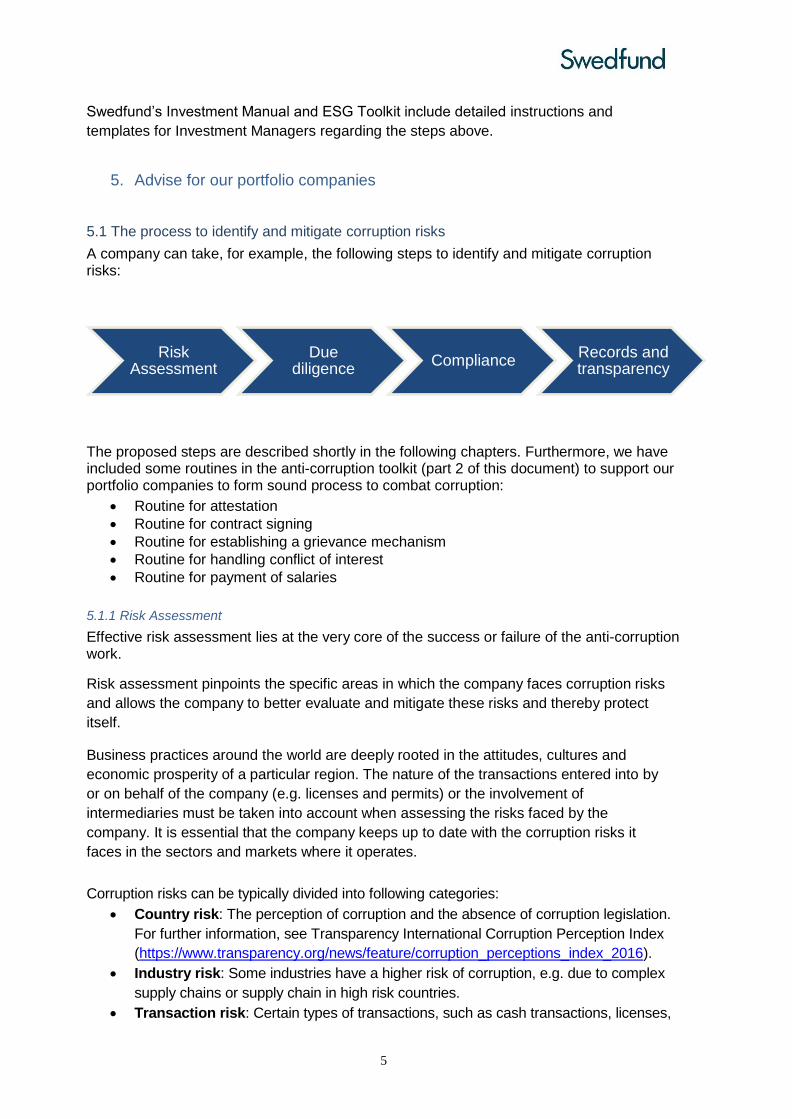

A company can take, for example, the following steps to identify and mitigate corruption risks:

The proposed steps are described shortly in the following chapters. Furthermore, we have included some routines in the anti-corruption toolkit (part 2 of this document) to support our portfolio companies to form sound process to combat corruption:

Routine for attestation

Routine for contract signing

Routine for establishing a grievance mechanism

Routine for handling conflict of interest

Routine for payment of salaries

5.1.1 Risk Assessment

Effective risk assessment lies at the very core of the success or failure of the anti-corruption work.

Risk assessment pinpoints the specific areas in which the company faces corruption risks

and allows the company to better evaluate and mitigate these risks and thereby protect

itself.

Business practices around the world are deeply rooted in the attitudes, cultures and

economic prosperity of a particular region. The nature of the transactions entered into by

or on behalf of the company (e.g. licenses and permits) or the involvement of

intermediaries must be taken into account when assessing the risks faced by the

company. It is essential that the company keeps up to date with the corruption risks it

faces in the sectors and markets where it operates.

Corruption risks can be typically divided into following categories:

Country risk: The perception of corruption and the absence of corruption legislation.

For further information, see Transparency International Corruption Perception Index

(https://www.transparency.org/news/feature/corruption_perceptions_index_2016).

Industry risk: Some industries have a higher risk of corruption, e.g. due to complex

supply chains or supply chain in high risk countries.

Transaction risk: Certain types of transactions, such as cash transactions, licenses,

Risk Assessment

Due diligence

ComplianceRecords and transparency

6

or transaction with authorities, involves a higher level of risk.

Business risk: Business risks can arise in project with a high value and in projects

where intermediaries are used.

Relationship risk: Relationships such as joint ventures increase the risk.

5.1.2 Due Diligence

In order to effectively combat corruption, the company needs to:

Know who it is doing business with;

Why, when and to whom funds are released; and

In certain circumstances, seek and monitor mutual anti-corruption agreements.

A company should make the following enquiries before embarking on a particular

business venture:

The risks that a particular business opportunity could trigger; and

The reputation of individuals or organizations involved in key decisions (e.g. intermediaries or joint-venture partners).

Due diligence is a foundation for designing and implementing processes and controls to detect and combat the presence of corruption.

5.1.3 Compliance

In order to minimize the risk of the company’s employees (in particular, members of

management including sales and purchasing staff) giving or accepting bribes, all

employees (at the defined level) should read and agree in writing that they will follow the

company’s anti-corruption policy, as amended from time to time, for as long as they work

for the company.

All employees with positions considered to be “risky” shall be evaluated and interviewed

regarding any previous experience of (and attitude towards) corruption during the

recruitment process.

In addition, sufficient internal control routines should be established to ensure the

compliance with the company’s anti-corruption policy and relevant anti-corruption

legislation.

5.1.4 Records and transparency

The company must maintain accurate books, records and financial reporting covering all

its activities and including all transactions with third party representatives working on the

company´s behalf. Books, records and overall financial reporting must be transparent and

accurately reflect each of the underlying transactions. False, misleading or inaccurate

records of any kind could potentially damage the company.

All material purchasing decisions (such as change of supplier) are to be reviewed

based on objective criteria before any decision is made.

The company’s employees shall avoid any situation that may present a conflict of interest.

This includes situations in which the employee’s relationship with another person may

interfere with the employee’s ability to make sound business decisions in the best interest

of the company.

Employees must also avoid conflicts of interest between their personal financial interests

and their involvement in the company’s business. Any company employee in a position to

7

influence a company decision with respect to a transaction with any entity in which the

employee has a financial interest (other than portfolio investments in public companies’

securities) shall disclose to his or her immediate superior such financial interest and refrain

from participation in the transaction.

5.2 Typical situations with high corruption risks

The following chapters describe situations, where the corruption risk is generally considered higher and provides general guidance in those situations. Furthermore, we have included the following routines in the anti-corruption toolkit (part 2 of this document) to support our portfolio companies to mitigate the heightened corruption risk:

Routine for handling payments to agents

Routine for identifying appropriate gifts and hospitability

Routine for payment to authorities

5.2.1 Use of third party representatives and intermediaries

The definition of a third party or an intermediary is broad, and applies, but is not limited to

the following: customers, business agents, business development consultants, lobbyists,

advisors or other persons or entities serving a similar function as well as distributors,

contractors, suppliers, employees, or governmental officials.

Potential risks exist whenever a third party conducts business activities on the company´s

behalf, so that the result of their actions can be seen as benefitting the company.

Companies shall exercise great diligence in assessing the reputation for business integrity

of prospective intermediaries. Third parties, who pose significant risks and act on the

company´s behalf, must at all times operate in accordance with the policy of the company.

The company´s management is responsible for the evaluation of each third party

relationship and shall determine whether or not it falls into this category. Prior approval by

the board of the company can required before entering into an agreement with an

intermediary.

Where a risk regarding a third party arrangement has been identified, management should:

Evaluate the background, experience, and reputation of the third party;

Understand the services to be provided, and methods of compensation and payment such as commission payments;

Evaluate the business rationale for engaging the third party;

Take reasonable steps to monitor the transactions of third parties appropriately; and

Ensure there is a written agreement in place which acknowledges the third party’s understanding and compliance with the company’s anti-corruption policy.

All illegal payments or gifts made through or by intermediaries for the purpose of

obtaining, retaining, or directing business for the company is prohibited. Any commission

or fee to be paid to an intermediary must be:

Reasonable in amount in relation to the extent and nature of the services actually performed by the intermediary;

Paid in accordance with the company’s customary payment procedures and

recorded properly on the company’s accounts; and

Governed by a written agreement with the intermediary, which specifically prohibits

8

illegal payments or gifts and provides for immediate termination of the agreement

and cessation of future fee payments in the event of misconduct.

If a third party is thought to engage in corruption despite all these measures, the

company´s management shall take action as outlined in the anti-corruption policy.

5.2.2 Gifts, entertainment and hospitality

Limited corporate hospitality is a widely accepted aspect of building good business

relationships, and the company should allow its employees to make or accept hospitality

or gifts provided that they:

Conform to local laws and customs;

Do not place the recipient under any obligation to the donor or appear to do so; and

Are not prohibited by the policies of the recipient’s employer.

Gifts, entertainment and hospitality include the receipt or offer of gifts, meals or tokens of

appreciation and gratitude, or invitations to events, functions or other social gatherings in

connection with matters related to business activities. These activities are acceptable

provided they fall within reasonable bounds of value and occurrence and are

received/given for advertising or representative goals without receiving/giving back any

material profit.

In order to evaluate what is acceptable in terms of gifts, entertainment and hospitality, go

through the following check-list before giving or receiving the type of items described in

this section:

What is the intent - Is it to build a relationship or is it something else?

How would you look if these details were on the front page of a newspapers?

What if the situation were to be reversed – Would there be a double standard?

If you find it difficult to answer one of the above questions, there may be a risk involved,

which could potentially damage the company’s reputation and business. The action may

even be illegal.

Transparency is key and often removes any doubts about corrupt intent. Therefore, the

company shall maintain monetary thresholds and inform suppliers, subcontractors,

intermediaries, joint venture partners and other cooperation partners about these

thresholds. The company shall create and monitor a gift, entertainment and hospitality

register (control sheet). Any form of gift, entertainment or hospitality – given, received or

offered, shall be recorded in this register.

Gifts given by the company to its employees, shall handled in accordance with the

country’s tax code.

6.2.3 Facilitation payments

In many countries, it is customary business practice to make payments or give gifts of

small value to junior government/municipal officials in order to speed up or facilitate a

routine action or process.

These so called “facilitation payments” as are against Swedfund’s Anti-Corruption policy

and illegal within most of the countries. Facilitation payments is thus not permitted. Lawful

payments to a government agency are not “facilitation payments”.

9

However, in the event that a facilitation payment is being extorted, or if an employee is

forced to pay under duress or faced with potential safety issues or harm, such a payment

may be made, provided that certain steps are followed. In such situations, the company

employees should immediately inform the management of the company. The company

management will then, together with the company´s lawyers, decide on what appropriate

actions to take. Any payment made must be recorded in the company´s books in order to

reflect the substance of the underlying transaction. The record of the payment might also

be used in court.

Charitable contributions and sponsorships shall not be used to circumvent the bribery nor

facilitation prohibition. Therefore charitable contributions and sponsorships should require

prior approval of management.

5.2.4 Engagement with public officers

We encourage our portfolio companies to be aware also of the following situations:

Allowing the participation of public officers (state public officers or of the

territorial subjects or municipal public officers) in the activities of the company

on a paid basis.

Engaging in business activities with public officers (state public officers or of

the territorial subjects or municipal public officers) or with their trustees.

Lending money (loans, credits) or give money without compensation, render

services or provide works without compensation, pay entertainments;

amusements; rest, holidays, vacations, travel or transport costs, business related

expenses (which could be regarded as a bribe) to public officers (state public

officers or of the territorial subjects or municipal public officers) or to persons in

commercial and other organizations.

10

PART 2: ANTI-CORRUPTION TOOLKIT FOR OUR PORTFOLIO

COMPANIES This toolkit includes some basic tools and templates that our portfolio companies may adopt

and use as an inspiration. These tools and templates have been selected to support our

portfolio companies to fulfill Swedfund’s requirements on anti-corruption, but also based on

typical anti-corruption risks and mitigation measures.

This toolkit includes the following tools and templates:

Swedfund’s anti-corruption requirements to our portfolio companies

Tools and templates

Anti-corruption policy: each portfolio company shall adopt an anti-corruption policy which is satisfactory to Swedfund

Anti-Corruption Policy template

Accountability: appointment of responsible person at management level

Role description of an Anti-Corruption Manager

Systems: implement and maintain processes, procedures and controls to detect the presence of corruption

Sample of routine descriptions

Routine for attestation

Routine for contract signing

Routine for establishing a grievance mechanism

Routine for handling payments to agents

Routine for handling conflict of interest

Routine for payment of salaries

Routine for payment tot authorities

Competence: identify and train key personnel (i.e. those with the greatest exposure to corruption)

Examples of anti-corruption e-learnings

Reporting: regular reporting (at least annually) to Swedfund

Anti-Corruption Questionnaire included in Swedfund’s Annual Sustainability Report

11

1. Anti-Corruption Policy template

A template for an anti-corruption policy, which is satisfactory to Swedfund.

[name of the company]’s Anti-Corruption Policy

1. Commitment and scope of the policy

[name of company], in what follows referred to as the “Company” is committed to

conducting its business honestly and transparently, at all times in accordance with

applicable legislation and in line with the highest standards of business ethics.

This policy prescribes a zero tolerance to corruption for all Company employees and third

party representatives and intermediaries acting on behalf of the Company.

2. Definition of (acts of) corruption

Corruption can broadly be defined as the abuse of entrusted power for private gain. Any type

of corruption involves an unlawful benefit for one individual and damage for another. The

Company defines any of the following acts as “Corruption” and this applies to both public

officials and private entities:

Bribery

A bribe occurs when a person requests, receives, accepts, offer, pay, seek or accept an offer or an improper advantage or reward in connection with his or her position, office or assignment.

Extortion

Extortion is a, direct or indirect, act of utilising, power position or knowledge to demand unmerited cooperation or compensation as a result of coercive threats.

Facilitation payments

A facilitation payment is a, direct or indirect, unofficial payment made to secure or expedite a performance of a routine or necessary action to which the payer of the facilitation payment has legal or other entitlement.

Nepotism and cronyism

Nepotism and cronyism is a form of favoritism based on familiar and acquaintances relationships where someone in an official position exploits his or her power and authority to provide a job or favor to a family member or friend, even though he or she may not be qualified or deserving.

Fraud

Fraud includes any intentional or deliberate act to deprive the company of property or money by deception or other unfair means.

Money laundering

Money laundering includes any act or attempted act to conceal or disguise the identity of

illegally obtained proceeds so that they appear to have originated from legitimate sources.

Financing of terrorism

Funds that are used for terrorist activities. It may involve funds raised from legitimate sources, such as profits from businesses and as well as from criminal sources.

Political contributions

Political contributions includes contributions made in cash or in services. For example gifts of property or services, advertising or promotional activities, endorsing a political party.

12

Who can be engaged in corruption?

Corruption can be committed by:

an employee of the Company

any person acting on behalf of the Company (e.g. third party representatives)

3. How to act if you come across (attempts at) acts of corruption

All employees of the Company have a responsibility to help detect, prevent and report

instances of corruption.

i. Employees who come across suspected instances of corruption (either

within the Company, by any third party affiliated with the Company or by

any of the Company´s competitors), shall report this to the managing

director at once.

ii. Suspected acts of corruption may be (anonymously) reported to an

independent representative within the Company who is not a member of

Management. This representative shall be elected by the employees

(excluding Management). Name, contact details and function of the

representative in question shall be visibly posted in an area of the Company

available to all employees.

iii. If suspected acts of corruption are sensitive or serious, employees at the

Company can report though Swedfund’s whistleblower system, available on

Swedfund’s website.

4. Actions to take if acts of corruption are reported/observed

The Company´s management will follow the below procedure in case acts of

corruption are reported/suspected/observed:

i. Evaluate the evidence. If the evidence is deemed to be insufficient, make

sure that the person/party in question has read and agreed with this policy in

writing. Keep the person/party under observation if any doubt about his/her

actions remains.

ii. If the evidence for acts of corruption carried out by the Company’s employees

or third parties on behalf of the Company is strong, consult with the

Company´s lawyers, which appropriate actions to take in accordance with

country legislation. Possible actions include:

Disciplinary measures such as formal warnings and dismissal (including

termination of labor contracts);

Cancellation of contracts (with third parties); and

Police investigation/court procedures depending on the case and

circumstances in question.

5. Adoption of the Policy

This Anti-Corruption Policy has been adopted and approved by the Board of the Company

on the [date].

13

2. Role description of an Anti-Corruption Manager

The purpose of the role of an Anti-Corruption Manager is to enable the company to mitigate

the risk of corruption and to ensure that the company meets the related commitments, laws

and regulations.

The responsibilities of an Anti-Corruption Manager include for example:

Ensure that the company’s anti-corruption policy meets the expectations of the main

stakeholders, related commitments, laws, regulations, and good international

practice;

Implementation of the anti-corruption policy through appropriate systems, processes

and procedures;

Ensure the internal awareness and competence on anti-corruption through trainings,

information sharing and advice;

Regular reporting on anti-corruption measures to the Board, Management and other

stakeholders;

Specific anti-corruption projects; and

Assisting in investigating allegations of corruption.

The Anti-Corruption Manager role should be authorized to a person, who has the

appropriate competence, status, authority and independence.

In a small company, the Anti-Corruption Manager is likely to be a person with the

responsibility on a part-time basis. In this case, it should be ensured that the other

responsibilities of the Anti-Corruption Manager are not in conflict with the anti-corruption

responsibilities.

Where the anti-corruption work load is large, for example due to high corruption risk, full-

time resources may be assigned to the Anti-Corruption Manager role.

In any case, the The Anti-Corruption Manager should have direct access to the board in

order to communicate relevant information.

14

3. Sample of routine descriptions

The following routine descriptions are created to support our portfolio companies to form a sound process to combat corruption:

Routine for attestation

Routine for contract signing

Routine for establishing a grievance mechanism

Routine for handling conflict of interest

Routine for payment of salaries

The following routine descriptions are created to mitigate corruption risks in situations, where the corruption risk is generally higher:

Routine for handling payments to agents

Routine for identifying appropriate gifts and hospitability

Routine for payment to authorities

15

3.1 Routine for attestation

Purpose

The purpose of an attestation routine is to ensure that payments and transactions are made

according to payment details and correspond to delivered goods and services.

An attestation routine minimizes the risk of paying false invoices, ensuring payments are

made to the correct company and individual, as well as ensuring that the amount is correct.

All in all, attestation reduces the risk of corruption through the internal control mechanisms

of payments and transactions in place.

Prerequisites

The routine, should be implemented into the daily procedure of payments and transactions

to ensure a stable procedure with minimized risks of corruption. This document will specify

what documents should be attested, who is eligible for attesting, payments which comes

with specific conditions, and finally the process of attestation.

Before the routine is implemented a line of responsibility has to be established. The line of

responsibility is preferably built on the “Grandfather principle” which states that decisions

has to be approved by the manager’s manager (the “grandfather”).

Documents for attestation

Documents that should be attested are the following:

All documentation needed for accounting/bookkeeping

Order and purchasing forms for goods and services

Invoices and crediting documents for goods and services

The above listed documents are henceforth referred to as “documents”.

Eligible individual for attestation

The Chief Executive Officer (CEO) and/or the Vice President always have the right to attest

documents. Depending on the Company structure, the Head of Department/Department

Manager also have the right to attest documents derived from their own department.

The Chief Financial Officer (CFO) is eligible to attest invoices in those cases where the

invoice clearly states that the responsible manager has approved the following:

a) The invoice corresponds to the ordered goods or services b) The invoice price and payment conditions correspond with the contract, agreement,

order or other similar documentation related to the made order

Before attestation, a sample of the eligible individual with right to attest documents,

signature (as an original), should be documented and stored together with a note on the

conditions for attestation the individual has. Conditions that should be stated are:

The types of documents, payments, transactions etc. that the individual is authorized to attest

If the individual can only attest documents, payments, transactions etc. that are within a certain spend limit

16

If the individual can only attest documents, payments, transactions etc. that are ordered within a certain time period

Or other conditions that apply to the individual

The purpose of documenting the signature together with the conditions is to ensure

individuals attesting payments, transactions and documents is eligible.

Payments with specific conditions

There are some payments and transactions that comes with specific conditions regarding

who is eligible for attesting those documents.

a) The individual who decided on contracting a business partner, does not have the right to attest payments or transaction to the same supplier. This is to reduce the risk of false payments, incorrect payment details and price fixing.

b) An individual does not have the right to attest his or her own travel and representation costs. The reason being to minimize the risk of the company paying for personal travel expenses and other expenses such as: vacation travels, meals and accommodation.

c) The third condition concerns cases when an individual is not eligible to attest payments or transactions due to the connection between him/her self and the company or person receiving the payment. The purpose is to reduce the risk of bribery, fraud, facilitation payments and payments to political officials.

The individual eligible to attest documents cannot attest payments or transactions that are

in any way:

related or connected to his or hers own personal e.g. payments to a company where the person is owner or co-owner, or payments directly to that individual

related or connected to a close1 relative to him/her e.g. a company that is owned by a uncle, or directly to the uncle

related or connected to a person under the individuals legal guardianship

The process of attestation

1. The first step of attestation is to identify two persons who are eligible for attesting the documents. The individuals attesting the documents is recommended to be: one who is connected to the payment or transaction e.g. who made the order of goods/services, and the second individual should be the manager of the other individual.

2. The attestation is then made by both individuals signing the document(s) and/or its underlying document(s). A date for attestation is also required together with the signature. The individuals attesting document(s) are legally liable for the accuracy of the document(s) signed. Note that attestation cannot be made after a payment or transaction.

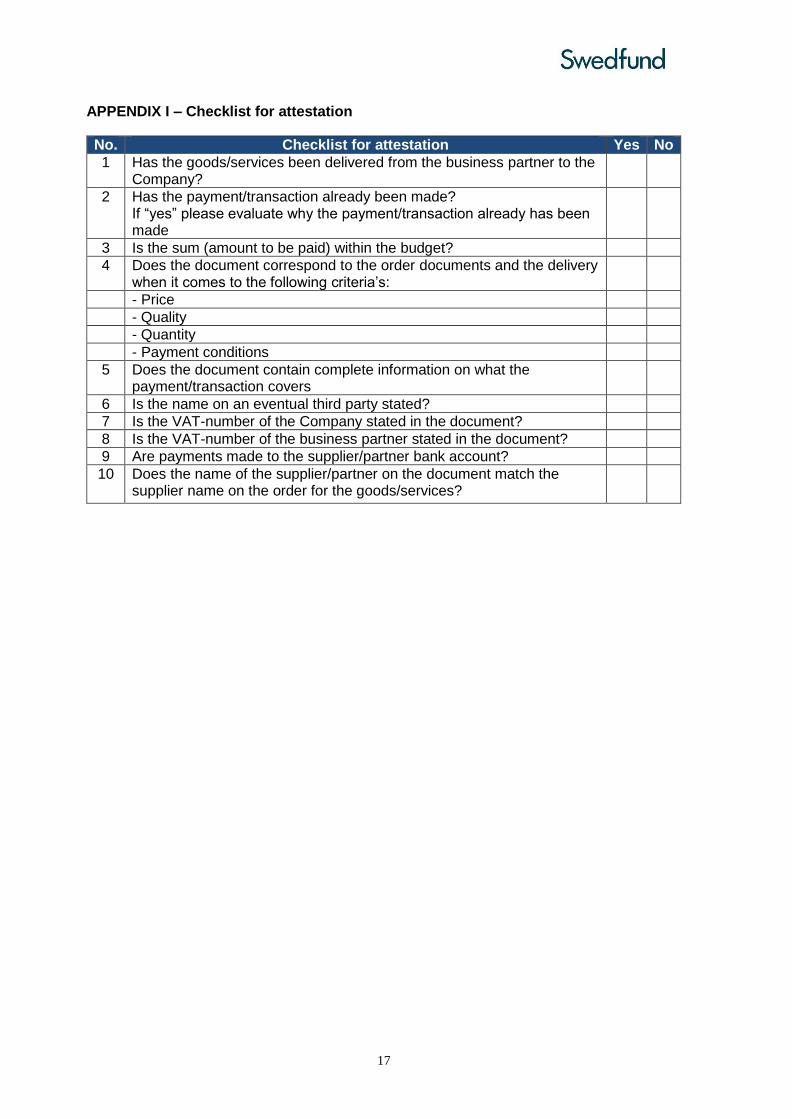

3. A checklist, found in Appendix I, can be used to study what to look for before attesting a document or can be directly used as a checklist during the attestation. The checklist consists of 10 questions that are to be answered with “Yes” or “No”. If any of the questions in the check list are answered with “No”, it is recommended to find the reason and resolve any uncertainties before attesting the document and going further with the payment or transaction.

1 Close is defined as: mother/father, brother/sister, grandparent(s), aunt(s)/uncle(s), cousin(s)

17

APPENDIX I – Checklist for attestation

No. Checklist for attestation Yes No

1 Has the goods/services been delivered from the business partner to the Company?

2 Has the payment/transaction already been made? If “yes” please evaluate why the payment/transaction already has been made

3 Is the sum (amount to be paid) within the budget?

4 Does the document correspond to the order documents and the delivery when it comes to the following criteria’s:

- Price

- Quality

- Quantity

- Payment conditions

5 Does the document contain complete information on what the payment/transaction covers

6 Is the name on an eventual third party stated?

7 Is the VAT-number of the Company stated in the document?

8 Is the VAT-number of the business partner stated in the document?

9 Are payments made to the supplier/partner bank account?

10 Does the name of the supplier/partner on the document match the supplier name on the order for the goods/services?

18

3.2 Routine for contract signing

Purpose

The purpose of a routine for contract signing is to ensure that important business decisions

are made according to Company principles and standards. The routine for contract signing

is based on the “Four-eyes principle”. A routine for contract signing minimizes the risk of

signing in-correct documents, making decisions that are not in line with Company business

practice and to reduce the risk of bribery and corruption.

Definition

The “Four-eyes principle” states that two individuals have to approve the same business

decision before the decision can be made. The principle also applies to business meeting

where decisions will be made, such as important business meeting with suppliers and

partners. The Four-eyes principle is a control mechanism to ensure transparency, reduce

the risk of bribery and corruption and also ensures a segregation of duties, meaning that no

one shall alone manage all the steps in a chain of events.

Process

The routine recommends the Company to apply the principle when important business

decisions has to be signed off and during significant business meetings with business

partners.

The two individuals are recommended to be one manger and one individual who has

knowledge about the decision that is about to be made.

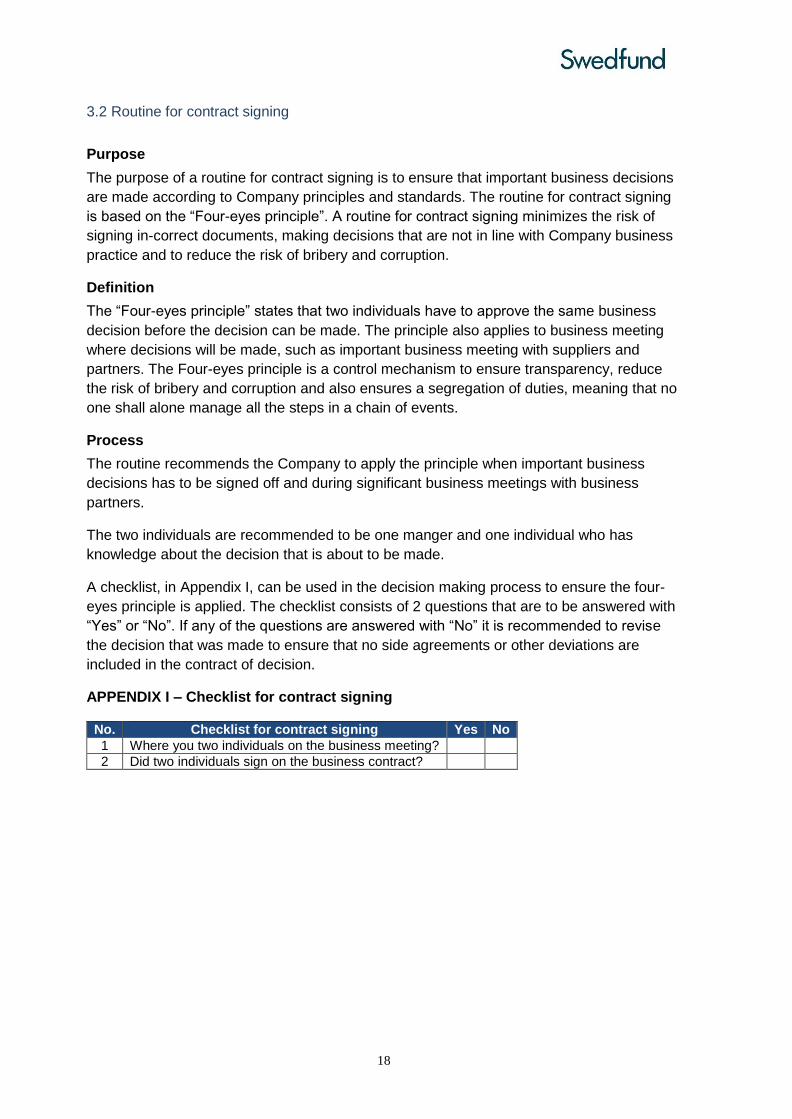

A checklist, in Appendix I, can be used in the decision making process to ensure the four-

eyes principle is applied. The checklist consists of 2 questions that are to be answered with

“Yes” or “No”. If any of the questions are answered with “No” it is recommended to revise

the decision that was made to ensure that no side agreements or other deviations are

included in the contract of decision.

APPENDIX I – Checklist for contract signing

No. Checklist for contract signing Yes No

1 Where you two individuals on the business meeting?

2 Did two individuals sign on the business contract?

19

3.3 Routine for establishing a grievance mechanism

Purpose

The purpose of this document is to assist the Company in establishing a grievance

mechanism which can be used to detect and prevent corruption within the Company. The

mechanism will serve as an alternative communication channel for employees and

individuals affiliated with the Company.

Definition

A grievance mechanism is an alternative communication channel which allows employees

and third party individuals to express their concerns or raise awareness to eventual cases

of corruption within the Company.

Process of establishing a grievance mechanism

Guiding policies

The Company should define and establish what guiding polices and principles the Company

and its employees are to adhere to. It could be policies such as a Code of Conduct, anti-

corruption policy or manuals and instructions on how to act in different situations. The

definition of guiding polices set a good foundation for the grievance mechanism to rely on.

Grievance mechanism policy

A specific policy regarding the grievance mechanism should be developed and established.

The policy should contain the following information:

The grievance mechanism is for all employees within the Company and individuals working on behalf of the Company.

Employees and individuals working on behalf of the Company are to report suspected instances of corruption.

Suspected and observed instances of corruption can occur within the Company, by a third party affiliated by the Company or by any of the competitors to the Company.

The grievance mechanism is anonymous. This means that neither name, position, age nor any other information that could reveal the identity of the individual has to be stated on the case provided through the grievance mechanism.

The grievance mechanism has appointed [Manger] who is responsible for collecting the reported grievances. [Manager] will directly report the cases to the top management or Board of Directors.

Managers has to report cases of corruption to the responsible Investment Manager at Swedfund.

Management of the grievances mechanism

Channels for the grievance mechanism can be both physical and digital. Regardless of

which method is chosen, the system has to provide the possibility to be anonymous and

everyone has to be able to access the mechanism, both as an employee and an individual

affiliated with the company.

The person responsible for handling the reported grievances is recommended to be Manger

20

who has direct contact with the top management or Board of Directors. When cases are

reported, the Manager is to go through the case together with the top management or

Board of Directors to evaluate the case and identify what breaches has been made.

Actions to be taken if a case of corruption has occurred are to be decided by the top

management or the Board of Directors together with the Company lawyer.

Report directly to Swedfund

If the case is specifically sensitive e.g. concerns top management or Board of Directors, or

the employee/individual affiliated with the Company feel they don’t receive any support on

the case, Swedfund’s whistle-blower system can be used. More information on Swedfund’s

whistle-blower system can be found on Swedfund’s website.

21

3.4 Routine for handling conflict of interest

Purpose

The purpose of the following routine is to define conflict of interest and provide

recommendations on how to handle cases of conflict of interest. The reason for establishing

a routine for handling conflict of interest is to increase the Company’s ability to handle

situations that could negatively affect the Company and also to increase the transparency

which in turn will minimize the risk of corruption.

Definition

A conflict of interest is a situation in which an individual has competing interests or loyalties

due to his or her connection to both sides of a relationship. In other words he or she is

“wearing two hats”.

A conflict of interest arises were an individual has an interest, usually a personal one, which

could affect the impartiality of that individual in the performance of his or her duties to the

Company. Such a person is called a disqualified individual. Just because a conflict of

interest has arisen, it does not mean that the disqualified individual in question has acted or

will act in a biased way. It simply means that there are circumstances in which this could

happen.

Disqualified individual

A disqualified individual has personal connections to e.g. another employee, third party or

other individual/entity which can affect the individual’s neutrality.

Example 1

The Company is in the process of procuring a supplier of IT-services. One suggested

supplier is owned by the purchasing manager’s brother. The purchasing manager in this

case is in a conflict of interest and he/she is a disqualified individual due to his/her

connection to one of the suppliers - there is a risk of favoring the brother’s company and

therefore the risk of acting biased increase.

Example 2

An individual works for a company and on his/hers spare time the individual provides

through its own company similar kind of services as the company, where the individual

works. The individual is in a conflict of interest and a disqualified individual due to the

competing loyalties between the company the individual works for and the individual’s own

company. There is an increased risk of the employee providing biased decisions that are to

the advantage of the individual’s own company and to the disadvantage of the Company.

Process for handling conflict of interest

There are different ways of handling a conflict of interest. Depending on the type of

operation the Company conducts, the risk of conflict of interest lies within different situations

and circumstances. It is suggested that the Company identifies, which situations regarding

conflict of interest might arise. It will be easier to avoid such situations, if they are identified.

22

A suggested process of handling conflict of interest is stated in four steps.

Step 1 – List of possible conflict of interest

Identify situations within the Company, where conflict of interest could arise. These

situations should be noted down in an internal document completed with a list of actions

that should be taken, if a conflict of interest is identified.

Step 2 – Internal record

Establish an internal record, where situations of conflict of interest can be recorded. The

record will assist the company in avoiding future situations, where conflict of interest have

previously been identified.

Step 3 - The conflict is clearly declared to management

In terms of declaring the conflict, it should be communicated openly and as soon as

possible to the immediate manager. The manager should in turn advice, how to proceed

and maintain a record of conflicts of interest. The reasoning behind this is to increase the

transparency within the Company, thus reducing the risk of corruption.

Step 4- The individual is removed from the activity or situation that has given rise to the

conflict

When removing an individual from an activity, ensure to remove him/her from all

preparatory work, negotiations, internal discussions, decision-making, and administration

connected to the activity or situation. When removing the employee form the situation, the

conflict of interest is immediately brought to a halt and the risk of further involvement and

biased decisions is reduced.

In a checklist, in Appendix I, above mentioned four steps are concluded into 6 questions.

The questions can be answered with “Yes” or “No”. If a question is answered with “No” it is

recommended to revise the internal process for handling conflict of interest.

APPENDIX I – Checklist for handling conflict of interest

No. Checklist for handling conflict of interest Yes No

1 Has the Company identified situations where conflict of interest might arise?

2 Has the Company decided on what actions to take if a conflict of interest arise?

3 Has the Company established an internal record for registration incidents of conflicts of interest?

In case of identified conflict of interest, the following checklist also applies

4 Has the conflict of interest been reported to the immediate manager?

5 Has the immediate manager registered the conflict of interest in the internal record?

6 Has the individual been removed from the activity/situation where the conflicted of interest arose?

23

3.5 Routine for payment of salaries

Purpose

The purpose of this routine is to provide a suggestion to ensure the payments of salaries in

a structured and a transparent way. The reasoning behind this is to minimize the risk of in-

correct salary payments, meaning payments, which are not in line with the decided salary

for that individual.

Payment of salary

Salaries are recommended to be paid directly to the individuals’ bank accounts, never in

cash. Cash payments are not recommended due to the high probability of in-correct

payments, the risk of bribery, and the risk of undeclared wages. A suggested procedure of

payment of salaries is stated below:

1. The first step is to ensure the Company has a list of all employees including full time and part time employees. The list will function as an insurance that all employees are paid, but also as a way to store bank and contact details to the employees.

2. Divide the responsibility of paying out the salaries between different managers. The reasoning for dividing the responsibility is to ensure that the correct salary is paid and to minimize the risk of bribery.

a. A suggested division of responsibility is that the financial department pays out the salaries to the employees’ bank accounts, and the top management or Board of Directors are responsible for deciding the salary to be paid.

3. When the salary is paid, make sure that every employee receives a pay slip. The pay slips are to state the following:

The name of the employee

The date of payment

The amount of hours worked for the period paid

Specify the hours of overtime if any

The amount of salary before tax and insurances

Specified how much of the salary is paid in tax and insurance

4. Salary payments should be attested in accordance with the routine for attestation.

5. Finally, ensure that salaries are registered in the Company accounting system.

Appendix I presents a checklist, which can be used when paying out salaries to ensure that

the above recommended procedure is applied. The 5 questions can be answered with “Yes”

or “No”. If “No” is stated, please revise the payments and ensure that everything has been

done accordingly.

24

APPENDIX I – Checklist for payment of salaries

No. Checklist for payment of salaries Yes No

1 Does the Company have a list of all employees?

2 Is the responsibility of paying out salaries divided between two individuals?

3 Does the pay slip contain the following information:

- Employee name

- Date of payment

- The amount of hours worked for the period paid

- Specify the hours of overtime if any

- The amount of salary before tax and insurances

- Specified how much of the salary is paid in tax and insurance

4 Have the payment of salaries been attested?

5 Are the salaries registered in the Company accounting system?

25

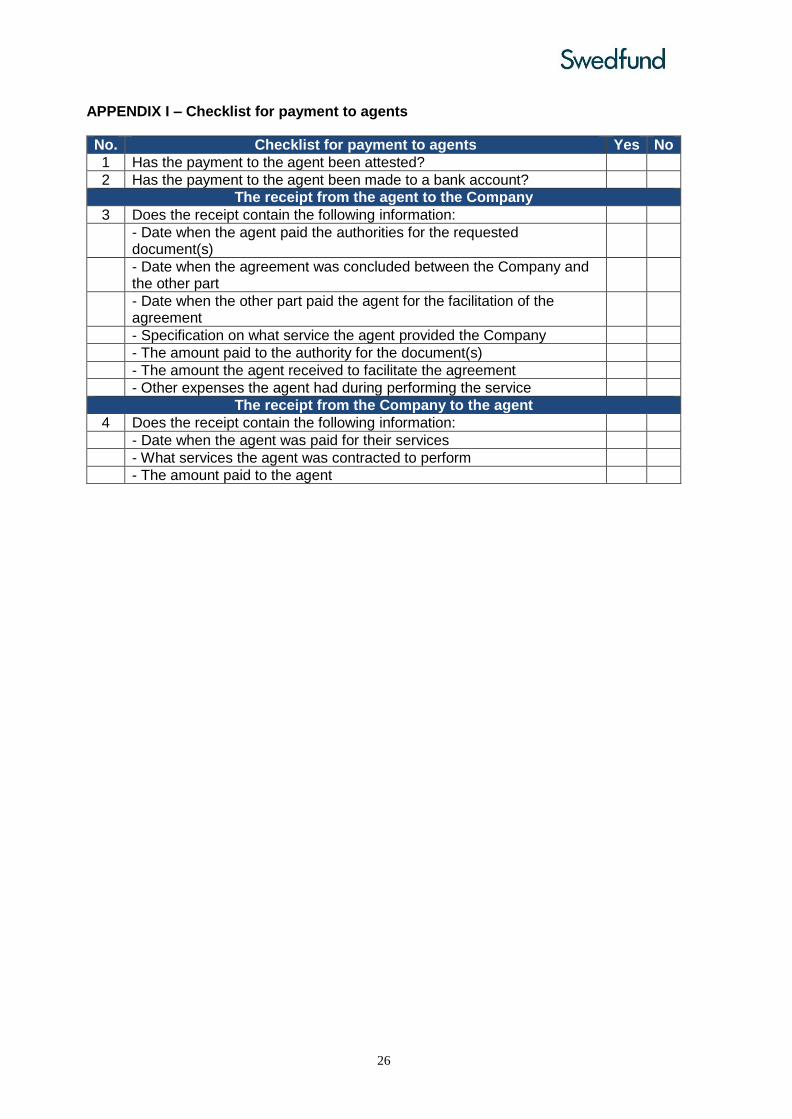

3.6 Routine for handling payments to agents

Purpose

This routine will assist the company in establishing a structured way of handling payments

between the Company and the agent, and payments between the agent and the other part.

The reasoning for establishing a routine for handling agents is to increase the transparency

between the Company and the agents thus minimizing the risk facilitation payments and

bribery.

Definition

An agent can be used by the Company in situations where e.g. a permit, license or other

governmental documentation is needed or when concluding agreements between the

Company and another part. Another part can be an authority or another company.

Process

It is recommended that the Company does not use agents, however Swedfund

acknowledges that agents are used to facilitate requisition of documents and concluding

agreements. When using agents it is suggested that the following process is applied. A

checklist, in Appendix I, can be used to ensure that payments between the Company and

the agent, the agent and the other part, are handled according to this routine. The checklist

consists of 4 questions that are to be answered with “Yes” or “No”.

1. All payments to agents should follow the routine for attestation 2. The payment of the agent is recommended to be made to the agents’ bank accounts

and not in cash. 3. When the agent has conducted his/her services, a receipt should be provided from

the agent to the Company and one receipt should be provided from the Company to the agent.

a. The receipt from the agent to the Company should include the following information:

o Date when the agent paid the authorities for the requested documents or date when the agreement was concluded between the Company and the other part, and when the agent was paid for the facilitation of the agreement

o Specification on the service the agent provided the Company o The amount paid to the authority for the document o What other expenses the agent had during performing the service

b. The receipt from the Company to the agent should include the following information:

o Date when the agent was paid for their services o What services the agent was contracted to perform o The amount paid to the agent

26

APPENDIX I – Checklist for payment to agents

No. Checklist for payment to agents Yes No

1 Has the payment to the agent been attested?

2 Has the payment to the agent been made to a bank account?

The receipt from the agent to the Company

3 Does the receipt contain the following information:

- Date when the agent paid the authorities for the requested document(s)

- Date when the agreement was concluded between the Company and the other part

- Date when the other part paid the agent for the facilitation of the agreement

- Specification on what service the agent provided the Company

- The amount paid to the authority for the document(s)

- The amount the agent received to facilitate the agreement

- Other expenses the agent had during performing the service

The receipt from the Company to the agent

4 Does the receipt contain the following information:

- Date when the agent was paid for their services

- What services the agent was contracted to perform

- The amount paid to the agent

27

3.7 Routine for identifying appropriate gifts and hospitality

Purpose

The routine for gifts and hospitality has the purpose of providing guidance to the Company

in dealing with gifts and hospitality offered by the Company or provided to the Company.

The reason for identifying and defining what is considered to be an appropriate gift and

hospitality within the Company minimizes the risks of bribery and conflict of interest.

Definition

Gifts and hospitality can be given, received, or offered to show appreciation or thanks to or

from someone, who does business with your Company. However, it can be unclear what is

acceptable and what might be considered a bribe and conflict of interest. Two suggestions

on how to identify and define the line between a gift and a bribe are stated below.

1. Defining value limits

Gifts of lower value

A gift of low monetary value such as corporate giveaways, consumables, or other items with

a nominal value is acceptable to receive/give, given that you do not ask for it, it does not

influence you or your Company, or have the appearance of influencing your objectivity or

decision-making. The gift can be received/given for advertising or representative goals

without receiving/giving back any material profit.

If accepting a gift could cause you or your Company to feel an obligation towards the giver,

do not accept the gift.

Gifts of higher value

Gifts of higher value are more likely to raise concern and increase the risk of conflict of

interest and thus the risk of corruption. The Company should decide internally, based on

local law and regulation, where to draw the line between a low and high value gift and

clarify, how to act when gifts of larger value is received or given. See the example below for

a suggested statement.

Example

An approval from your manager’s manager is required prior giving or accepting gifts worth

of more than [xx USD] from a single source (i.e. company, person, etc.) in any twelve-

month period. Factors considered in determining the appropriateness of a gift over this

amount is whether the gift is customary in the particular region or industry concerned and

openly given without any expectation or realization of special advantage.

Hospitality

Hospitality includes giving, receiving, and offering invitations to events, functions, or other social gatherings in connection with business activities. The same reasoning behind giving and receiving gifts applies to hospitality, these activities are acceptable provided they fall

28

within the definition of reasonable value and occurrence and are received/given for advertising or representation without receiving/giving back any material profit.

2. Identifying the intention behind the gift or hospitality

General guidelines and checklist

In all circumstances, regardless if it is a low or high value gift, or an invitation to an event or

other tokes of hospitality, it should be reasonable and justifiable. The intention behind

should always be considered. For example, a corporate gift, such as a traditional thank you

from one company to another, which may be display in your office, e.g. a card or fruit

basket is acceptable. However, a more personal gift, which you might take home or enjoy

personally, that could influence your objectivity or impartial judgment, should not be

accepted.

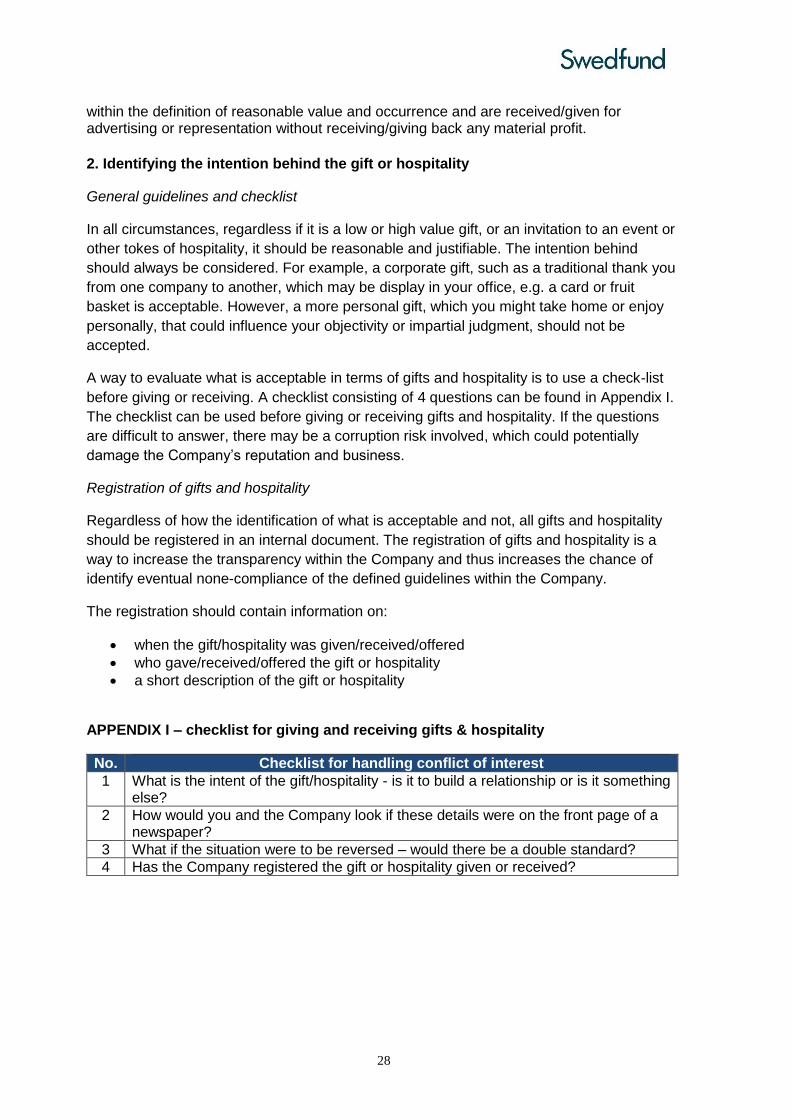

A way to evaluate what is acceptable in terms of gifts and hospitality is to use a check-list

before giving or receiving. A checklist consisting of 4 questions can be found in Appendix I.

The checklist can be used before giving or receiving gifts and hospitality. If the questions

are difficult to answer, there may be a corruption risk involved, which could potentially

damage the Company’s reputation and business.

Registration of gifts and hospitality

Regardless of how the identification of what is acceptable and not, all gifts and hospitality

should be registered in an internal document. The registration of gifts and hospitality is a

way to increase the transparency within the Company and thus increases the chance of

identify eventual none-compliance of the defined guidelines within the Company.

The registration should contain information on:

when the gift/hospitality was given/received/offered

who gave/received/offered the gift or hospitality

a short description of the gift or hospitality

APPENDIX I – checklist for giving and receiving gifts & hospitality

No. Checklist for handling conflict of interest

1 What is the intent of the gift/hospitality - is it to build a relationship or is it something else?

2 How would you and the Company look if these details were on the front page of a newspaper?

3 What if the situation were to be reversed – would there be a double standard?

4 Has the Company registered the gift or hospitality given or received?

29

3.8 Routine for payment to authorities

Purpose

The purpose of the routine is to assist the Company in establishing an internal procedure to

ensure payments to authorities are made correctly and in accordance with payment details.

The routine will minimize the risk of conflict of interest, facilitation payments and bribery of

public official.

Definition

Payments to authorities could occur when the Company requires a permit, licenses, or

other governmental documents to operate. Payments of such documentation could either

be by cash or to a bank account.

Process

1. All payments to authorities should follow the routine for attestation

2. Payment to bank account has to be made to a bank account belonging to the authority and not a specific individual. This is ensured by directly contacting the authority e.g. the financial department, and asking for the bank account details.

3. Payment to authorities in cash has to take place at the office of the authority, two persons from the Company has to attend and try to ensure that there are two responsible individuals from the authority present as well.

4. When the payment is done, directly to a bank account or in cash, make sure to receive a receipt where the following is specified:

Date of payment

The cost of the permit, licenses, or other governmental document

The amount the authority received

The amount the Company might get back

What the payment was for

Who the payment was between i.e. the name of the Company and the name of the authority, and in cases of cash payment the names of the individuals collecting the cash payment

A checklist, in Appendix I, can be used, when making payments to authorities. The checklist

consists of 6 questions that can be answered with “Yes” or “No”. If a questions is answered

with “No”, please revise the payment to ensure that the payment was made correctly and no

side payments or agreements were made.

30

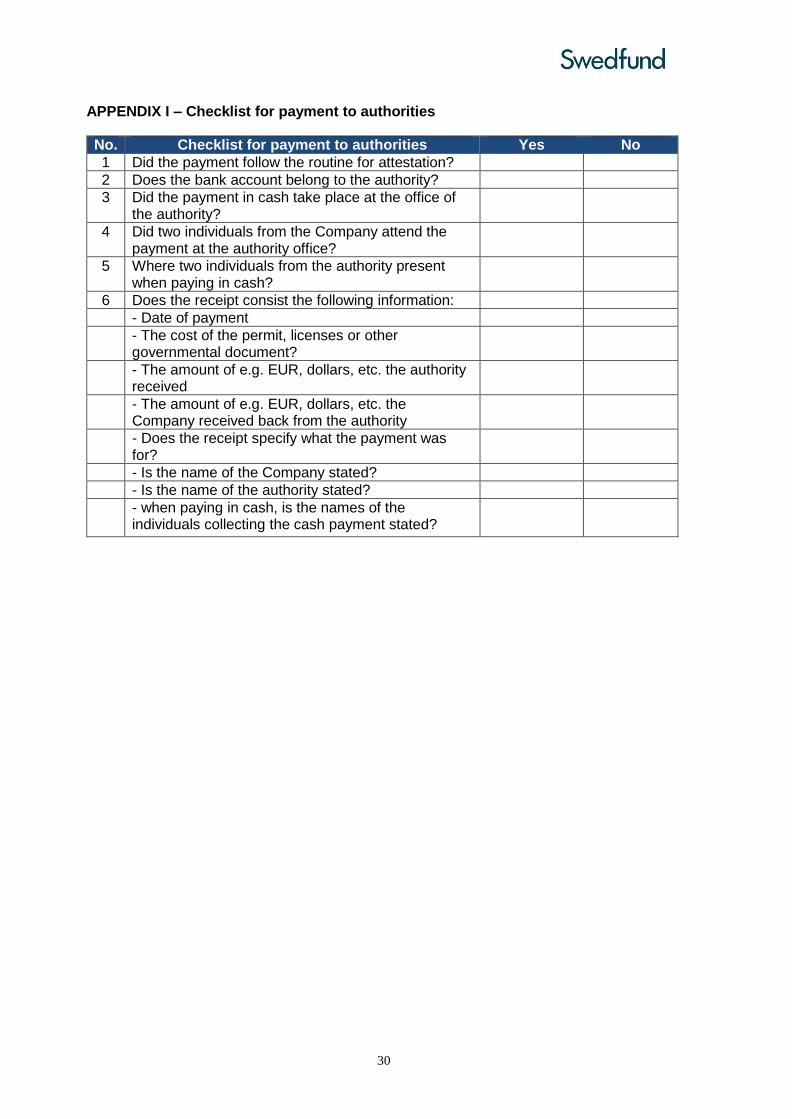

APPENDIX I – Checklist for payment to authorities

No. Checklist for payment to authorities Yes No

1 Did the payment follow the routine for attestation?

2 Does the bank account belong to the authority?

3 Did the payment in cash take place at the office of the authority?

4 Did two individuals from the Company attend the payment at the authority office?

5 Where two individuals from the authority present when paying in cash?

6 Does the receipt consist the following information:

- Date of payment

- The cost of the permit, licenses or other governmental document?

- The amount of e.g. EUR, dollars, etc. the authority received

- The amount of e.g. EUR, dollars, etc. the Company received back from the authority

- Does the receipt specify what the payment was for?

- Is the name of the Company stated?

- Is the name of the authority stated?

- when paying in cash, is the names of the individuals collecting the cash payment stated?

31

4. Recommended anti-corruption e-learnings

There are several anti-corruption e-learnings available online either free of charge or to be

purchased. We recommend that selected employees of our portfolio companies conduct

one of the following e-learnings (free of charge):

United Nations Global Compact: The Fight Against Corruption E-Learning Tool

An online learning platform to obtain practical guidance on how to fight corruption in

all forms through six interactive-video dilemma scenarios. Recommended for all.

Access: http://thefightagainstcorruption.org/certificate/

UNODC Anti-corruption eLearning Course

The course consists of two eLearning modules - "Introduction to Anti-corruption" and "Advanced Anti-corruption: Prevention of Corruption". The course has the objective to improve the learners' understanding of the provisions of the United Nations Convention against Corruption (UNCAC). Recommended for people, who need deeper understanding of anti-corruption mechanisms and prevention.

Access: https://www.unodc.org/unodc/en/corruption/news-elearning-course.html

32

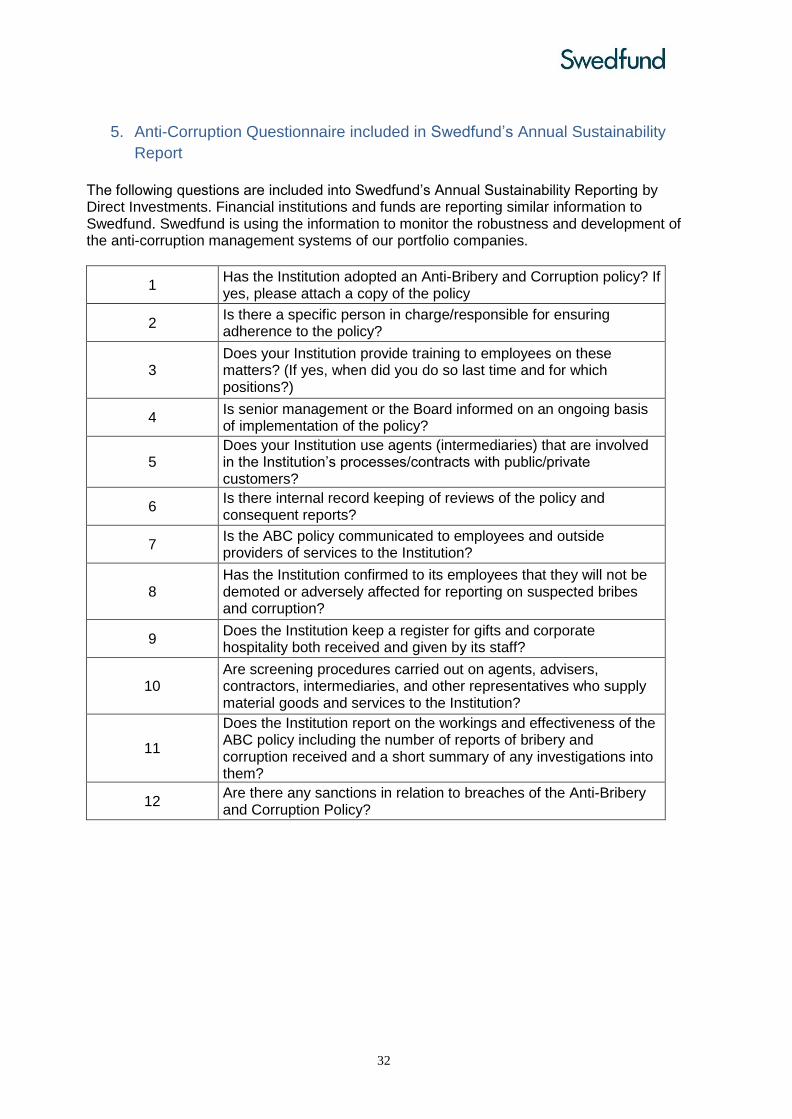

5. Anti-Corruption Questionnaire included in Swedfund’s Annual Sustainability

Report

The following questions are included into Swedfund’s Annual Sustainability Reporting by Direct Investments. Financial institutions and funds are reporting similar information to Swedfund. Swedfund is using the information to monitor the robustness and development of the anti-corruption management systems of our portfolio companies.

1 Has the Institution adopted an Anti-Bribery and Corruption policy? If yes, please attach a copy of the policy

2 Is there a specific person in charge/responsible for ensuring adherence to the policy?

3 Does your Institution provide training to employees on these matters? (If yes, when did you do so last time and for which positions?)

4 Is senior management or the Board informed on an ongoing basis of implementation of the policy?

5 Does your Institution use agents (intermediaries) that are involved in the Institution’s processes/contracts with public/private customers?

6 Is there internal record keeping of reviews of the policy and consequent reports?

7 Is the ABC policy communicated to employees and outside providers of services to the Institution?

8 Has the Institution confirmed to its employees that they will not be demoted or adversely affected for reporting on suspected bribes and corruption?

9 Does the Institution keep a register for gifts and corporate hospitality both received and given by its staff?

10 Are screening procedures carried out on agents, advisers, contractors, intermediaries, and other representatives who supply material goods and services to the Institution?

11

Does the Institution report on the workings and effectiveness of the ABC policy including the number of reports of bribery and corruption received and a short summary of any investigations into them?

12 Are there any sanctions in relation to breaches of the Anti-Bribery and Corruption Policy?

33

Further reading Further information on Corruption and Anti-Corruption work can be found for example from

the following sources:

Business Anti-Corruption Portal: http://www.business-anti-corruption.com/

IFC Combating Fraud and Corruption:

http://www.ifc.org/wps/wcm/connect/Topics_Ext_Content/IFC_External_Corporate_Site/AC

_Home

OECD Bribery in international business: http://www.oecd.org/daf/anti-bribery/

United Nations Convention against Corruption:

https://www.unodc.org/documents/brussels/UN_Convention_Against_Corruption.pdf

The UN Global Compact’s and the Principles for Responsible Investment (PRI)’s Guide on

Anti-Bribery and Corruption:

file:///C:/Users/johannar/Downloads/PRI_Engaging%20on%20anti-

bribery%20and%20corruption.pdf

Transparency International: https://www.transparency.org/

The US Foreign Corrupt Practices Act (FCPA) of 1977: http://www.business-anti-

corruption.com/anti-corruption-legislation/fcpa-foreign-corrupt-practices-act

The Bribery Act 2010: http://www.legislation.gov.uk/ukpga/2010/23/contents