Annual Results Presentation Period Ended 30 June 2005 · 6/30/2005 · Annual Results Presentation...

47

Annual Results Presentation Period Ended 30 June 2005 Kirby Adams, Managing Director and Chief Executive Officer Brian Kruger, President Australian Manufacturing Markets (formerly Chief Financial Officer) 23 August, 2005 ASX Code: BSL

Transcript of Annual Results Presentation Period Ended 30 June 2005 · 6/30/2005 · Annual Results Presentation...

Annual Results Presentation Period Ended 30 June 2005Kirby Adams, Managing Director and Chief Executive OfficerBrian Kruger, President Australian Manufacturing Markets (formerly Chief Financial Officer)23 August, 2005

ASX Code: BSL

Page 2

Important Notice

THIS PRESENTATION IS NOT AND DOES NOT FORM PART OF ANY OFFER, INVITATION OR RECOMMENDATION IN RESPECT OF SECURITIES. ANY DECISION TO BUY OR SELL BLUESCOPE STEEL LIMITED SECURITIES OR OTHER PRODUCTS SHOULD BE MADE ONLY AFTER SEEKING APPROPRIATE FINANCIAL ADVICE. RELIANCE SHOULD NOT BE PLACED ON INFORMATION OR OPINIONS CONTAINED IN THIS PRESENTATION AND, SUBJECT ONLY TO ANY LEGAL OBLIGATION TO DO SO, BLUESCOPE STEEL DOES NOT ACCEPT ANY OBLIGATION TO CORRECT OR UPDATE THEM. THIS PRESENTATION DOES NOT TAKE INTO CONSIDERATION THE INVESTMENT OBJECTIVES, FINANCIAL SITUATION OR PARTICULAR NEEDS OF ANY PARTICULAR INVESTOR.

TO THE FULLEST EXTENT PERMITTED BY LAW, BLUESCOPE STEEL AND ITS AFFILIATES AND THEIR RESPECTIVE OFFICERS, DIRECTORS, EMPLOYEES AND AGENTS, ACCEPT NO RESPONSIBILITY FOR ANY INFORMATION PROVIDED IN THIS PRESENTATION, INCLUDING ANY FORWARD LOOKING INFORMATION, AND DISCLAIM ANY LIABILITY WHATSOEVER (INCLUDING FOR NEGLIGENCE) FOR ANY LOSS HOWSOEVER ARISING FROM ANY USE OF THIS PRESENTATION OR RELIANCE ON ANYTHING CONTAINED IN OR OMITTED FROM IT OR OTHERWISE ARISING IN CONNECTION WITH THIS.

Page 3

Rewarding Shareholders Rewarding Shareholders As We GrowAs We Grow

Delivering on our Delivering on our StrategyStrategy

Page 4

Capital management – Rewarding shareholders as we grow

• Share Buybacks – Public Listing to 30 June 2005- Purchased and cancelled 102m shares

* on market – 76m shares* off market – 26m shares

• Dividends - All Fully Franked

9 13 1218 18

247

10

20

0

510

15

2025

30

35

4045

50

FY2003-1H FY2003-2H FY2004-1H FY2004-2H FY2005-1H FY2005-2H

¢

¢¢

Cent

s Per

Sha

re

Total return to shareholders since BSL’spublic listing (July 2002):

• Share buybacks $ 612m• Dividends paid $ 656m• Final & special dividend

(to be paid Oct 05) $ 312m$1,580m

$2.09 share or 77% payout ratio

¢

29¢40¢

¢

¢

¢

SpecialOrdinary:- Interim- Final

62¢

¢

¢

Page 5

Safety –”Taking Care” as we grow - Our goal remains Zero Harm

17,500 Employees, 84 manufacturing sites, 17 countries

35

29

1614

84.8

3.4 4.1 3.4 2.8 1.8 1.9 0.8 0.61.40

5

10

15

20

25

30

35

40

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005FY

52.247.1

29.122.4 21.9

12.2 9.3 9.2

1711.3

60

68

80

4.46.8

0

10

20

30

40

50

60

70

80

90

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005FY

* Includes contractors from 1996

Injur

ies re

sultin

g in l

ost ti

me pe

r milli

on m

an-h

ours

worke

d

Medic

ally t

reate

d inju

ries p

er m

illion

man

-hou

rs wo

rked

* Includes contractors from 2004

Medically Treated Injury Frequency RateLost Time Injury Frequency Rate

Includes Butler performance from July 2003Excludes Butler performance

Includes Butler performance from July 2003Excludes Butler performance

Minerals Council of Australia (2004) – 7.0IISI (2003) – 9.4

Page 6

Group headlines FY2005 – diversified portfolio delivers another outstanding result

• Revenue A$7,982 million Up 38% to record

• External despatches 7.2 million metric tonnes Up 4% to record

• EBITDA A$1,694 million Up 53% to record

• EBIT A$1,388 million Up 70% to record

• NPAT A$1,007 million Up 72% to record

• EPS 137.4¢ Up 77% to record

• After tax Return on Invested Capital 25.4% Up 37% to record

• Return on Equity 30.0% Up 53% to record

• Net operating Cashflow A$1,225 million 50/50 to shareholders / CAPEX

• Final Ordinary Dividend 24¢ per share Up 33%(fully franked)

• Special dividend (fully franked) 20¢ per share Doubled

• Gearing (net debt) 18.4% - vs. 12.9% (30 June 2004)- net debt up A$318 million since June 04

Page 7

Our strategy – unchanged and continuing to deliver

Hot Rolled Coil,Plate

Cold Rolled

Painted

Roll-forming

Metallic Coated

PEB /Solutions

• Cost competitive steelmaker – PKSW, NZ Steel and North Star BlueScope.

• Maximise asset life at optimum capacity.

• Strategic conversion alliances in Asia and USA.

• Reassess raw materials appoach.

Downstream

Midstream

Upstream

Steelmaking, Slab

WaterChina

Thailand

India

VietnamChina

ChinaThailand

Vietnam

Australia

NZAustralia

NZAustralia

• Strengthening the world’s largest construction steel roll former, eg. India, China, USA.

• Growing the world’s largest PEB manufacturer, eg. Thailand, India, China.

• Water – solutions for a global issue.

• Grow metal coated and painted capabilities, principally in the world’s growth corridor – Asia and Far East.

• Maintain focus on branded products and new product / market offers.

• Research and Development focus to meet future customer needs.

Page 8

Implementing our strategy – more than 20 major projects in 8 countries

• Bringing balance to our product portfolio FY2006 FY2007

Downstream

Midstream

Upstream

USA- New Vistawall extrusion plant- New Buildings speciality plantAustralia- Water, Lysaght, WA Service CentreThailand- First Pre-Engineered Building (PEB)China- New Panels, residential plants, new beam facility

India- New PEB and Lysaght plants

China- New PEB and Lysaght plants open

New Zealand- Brownfields (increased metal coating & paint capacities)Australia- Brownfields (increased metal coating and paint capacities)Vietnam- New 125kt Metal Coating Line and 50kt Paint LineThailand- 200kt Metal Coating expansionIndia- Potential JV in Coating / Painting

Australia- Colorbond® plant opensChina- 250kt Metal Coating Line and 150kt Paint Line commissions

New Zealand Steel- Front end studyUSA- North Star BlueScope Steel – new bag house- CastripInformation Systems- SAP

Australia- 400kt HSM Expansion- BF No. 5 Reline

“Brownfields” – ongoing work to generate small capacity increases at all existing operations at minimal / no capital cost

Page 9

Our strategy includes Business Excellence

Continue the focus on:

- Manufacturing excellence > reduce costs> capital efficient capacity increments> improve yields

- Improving our market offer > technical support> improved delivery & lead times

- New and colourful products> research and development> product development> global alliances> acquisitions

Page 10

Tennessee Butler Speciality Plant, USA – July 2005

Page 11

Vistawall Extrusion Plant, USA – November 2005

Page 12

Metal Coating Line Upgrade - Induction Furnace, New Zealand – FY2005

Page 13

West Sydney Colorbond® plant site, Australia – H1 CY2007

Page 14

Logistics and Service Centre, Western Australia – August 2005

Page 15

Sheds and Pre-Engineered Buildings – Australia

• Ranbuild acquired FY2005

Page 16

BlueScope Water developing capabilities – Australia and export

• Pioneer Water Tanks – acquired FY2005

Page 17

Hot Strip Mill Expansion, Port Kembla Steelworks – Q1 FY2007

Page 18

New 125,000t Metallic Coating & Painting, Vietnam – early CY2006

Page 19

Additional 200,000t Metallic Coating Capacity, Thailand – August 2005

Page 20

BlueScope Buildings PEB for Lysaght at Cibitung, Indonesia - FY2005

Page 21

Asia – Suzhou MCLNew 250,000t Metallic Coating & Painting complex at Suzhou, China – mid CY2006

Page 22

New Welded Beam Plant at BlueScope Building‘s PEB and Beam Facility, Tianjin, China - FY2006

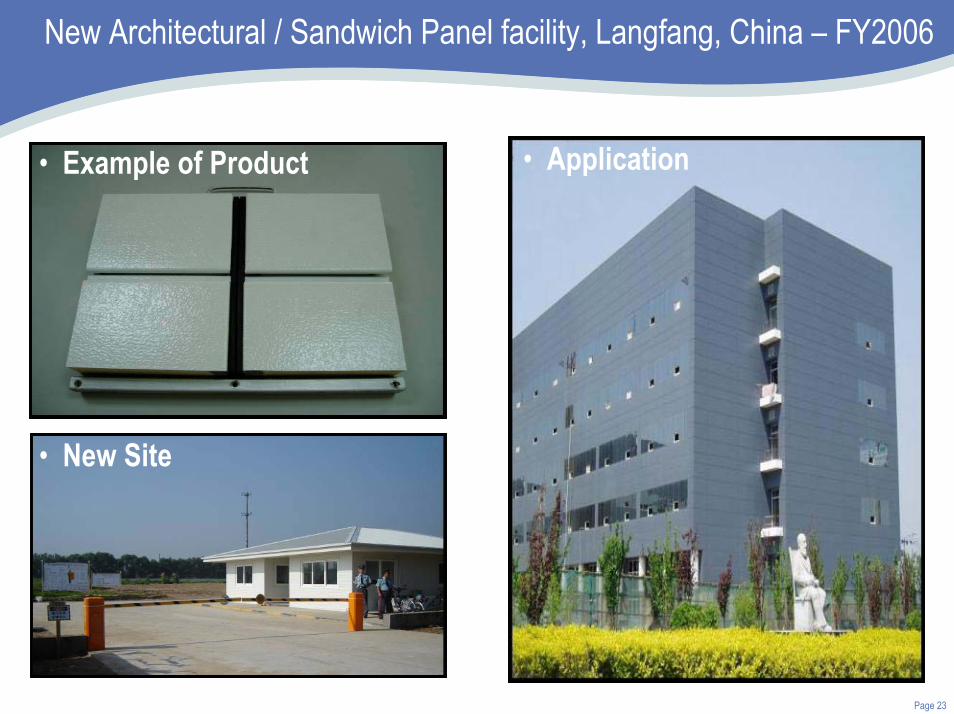

Page 23

New Architectural / Sandwich Panel facility, Langfang, China – FY2006

• New Site

• Example of Product • Application

Page 24

Butler PEB and Design Centre at Pune, India – 2H CY2006

• SITE

• RENDERING

Page 25

Building the BlueScope Footprint

China

USA

Mexico

Australia New Zealand

ThailandMalaysia

Indonesia

Vietnam

SingaporeBrunei

Taiwan

Sri Lanka Fiji

New Caledonia

VanuatuIndia(under

development)

China

USA

Mexico

Australia New Zealand

ThailandMalaysia

Indonesia

Vietnam

SingaporeBrunei

Taiwan

Sri Lanka Fiji

New Caledonia

VanuatuIndia(under

development)

Page 26

Steelmaking drives strong regional performance in FY2005

104 82 62174

62

183

659

1024

0

150

300

450

600

750

900

1050

Asia Americas New Zealand Australia

FY04 FY05

EBIT

A$ M

illion

s

• Port Kembla• Coated & Building Products Australia

• NZS & Pacific Steel Products

• Coated & Building Products Asia

• North Star BlueScope (50%)• Coated and Building Products

North America

Based on source of production

Sales Revenue +50% +180% +28% +18%($m): 699 / 1,051 678 / 1,897 590 / 756 4,328 / 5,126

Page 27

Coated and Building Products Asia – continues to be the growth engine

Fastest Growing Steel Market in the World

• FY2005 return on net assets annualised (pre-tax) 11%

Market> Twelve months BlueScope Butler PEB> Strong demand in Thailand and Indonesia> Malaysia – softer construction market> China – volatile building market

Performance> EBIT reduced by capex pre-operating costs

and business development costs of A$27m> Higher coating metal costs (zn, al)> FX, stronger A$> Sales price increases offset higher feed costs> 16 million hours LTI free

104

4537

82

0

20

40

60

80

100

120

FY04 FY05-1H FY05-2H FY05

EBIT

A$ M

illion

s

BlueScope Butler

88

16

• Sales revenue up 50% = A$1,051m, including A$254m from BlueScope Butler China

3

Page 28

Coated and Building Products North America – re-establishing BlueScope’s presence

• Sales revenue = A$1,134m up 19%

Markets> Buildings – volumes down in 2nd half

- softer overall industrial market- market share stable

> Vistawall – improved sales and market share

Performance> Overall improvement on prior year – but not to target> Buildings (negative contribution but transformation well

underway)- integration and regionalisation complete- high cost Galesburg plant closed- new speciality plant, Tennessee, started on time

but subsequent delay and cost over-run (cost $15m)- remedial action taken

- High feed costs, although steel supply stabilised> Vistawall (stable and growing)

- Another strong performance- Overcame higher feed costs- Aluminium product despatches up 12% YOY

> Worldwide: EBIT breakeven

-28

0

-20 -20-30

-20

-10

0

10

20

30

FY04 FY05-1H FY05-2H FY05

EBIT

A$ M

illion

s

(1)

(2)

(1) Normalised(2) Equates to (A$15m) normalised, principally

excluding integration costs.

Page 29

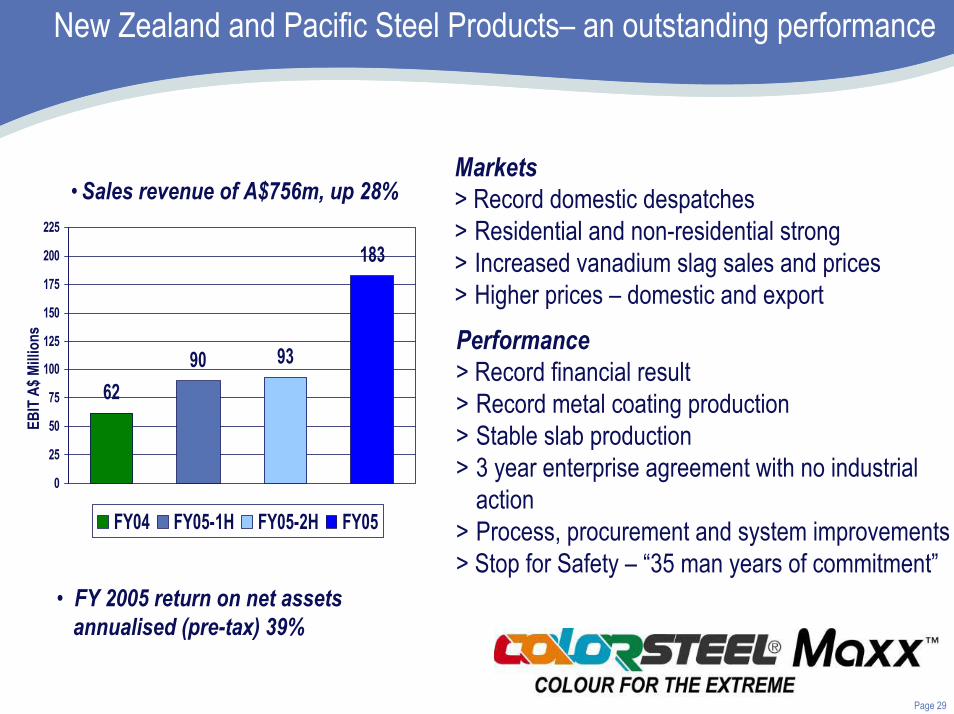

New Zealand and Pacific Steel Products– an outstanding performance

Performance> Record financial result> Record metal coating production> Stable slab production> 3 year enterprise agreement with no industrial

action> Process, procurement and system improvements> Stop for Safety – “35 man years of commitment”

6290 93

183

0

25

50

75

100

125

150

175

200

225

FY04 FY05-1H FY05-2H FY05

EBIT

A$ M

illion

s

• Sales revenue of A$756m, up 28%Markets> Record domestic despatches> Residential and non-residential strong> Increased vanadium slag sales and prices> Higher prices – domestic and export

• FY 2005 return on net assets annualised (pre-tax) 39%

Page 30

Coated & Building Products Australia – recovery underway

Markets> Record domestic despatches> Higher domestic and export prices> Residential softening> Non-dwelling and auto / manufacturing holding193

-91

-25

-116-150

-100

-50

0

50

100

150

200

250

FY04 FY05-1H FY05-2H FY05

EBIT

A$ M

illion

s

• Sales revenue of A$3,190m, up 11%

Performance> Higher steel feed and coating metal costs> Packaging Products

- honoured customer contracts- FY05 results ($109m), incl. ($25m) H2 restructure- withdrawing from export / continue domestic- improved pricing and profitability

> Annual production records achieved> Industrial disruption / strikes

- Western Port, Service Centres & Lysaght- cost to BlueScope Steel approximately $40m - also cost customers and employees

> West Sydney Colorbond® Centre underway> Service Centres and Lysaght stronger

• FY2005 return on net assets annualised (pre-tax) (9)%

Page 31

Hot Rolled Products – “steeling the show”

564692 646

1338

0

200

400

600

800

1000

1200

1400

FY04 FY05-1H FY05-2H FY05

Performance> Maintained record slab production> Record HRC production> Best plate production since FY1997> Partly offset by:

- higher iron ore, coal and scrap costs- planned repair and maintenance spending

> PKSW Hot Strip Mill expansion on schedule> Additional iron ore purchase Q4> 18 month coal arrangement> North Star BlueScope Steel

- production record- paid off debt and first dividend- Jacobsen Award No. 1 again

• FY2005 return on net assets annualised (pre-tax) 66%

EBIT

A$ M

illion

s

71104

North Star BlueScope Steel

Port Kembla Steelworks

90

194

• Sales revenue (excluding NSBSL) = A$3,940m, up 39%

• NSBS revenue US$573m (50%), up 65%

Markets> Strong global demand> Record prices and margins

Page 32

FinancialsFinancials

Page 33

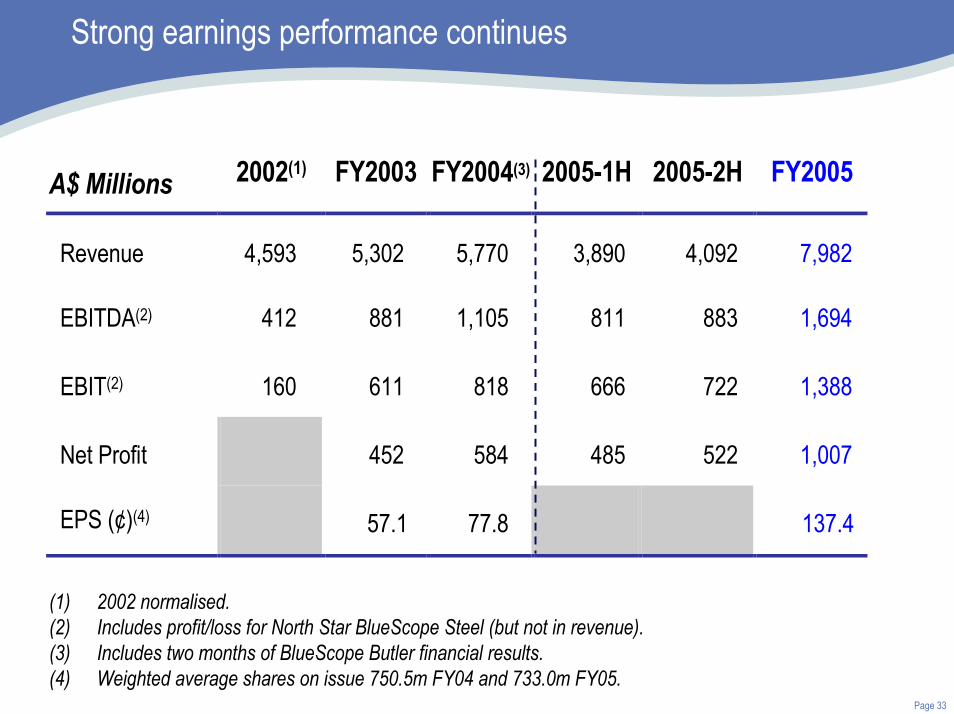

Strong earnings performance continues

A$ Millions 2002(1) FY2003 FY2004(3) 2005-1H 2005-2H FY2005

Revenue 4,593 5,302 5,770 3,890 4,092 7,982

EBITDA(2) 412 881 1,105 811 883 1,694

EBIT(2) 160 611 818 666 722 1,388

Net Profit 452 584 485 522 1,007

EPS (¢)(4) 57.1 77.8 137.4

(1) 2002 normalised.(2) Includes profit/loss for North Star BlueScope Steel (but not in revenue).(3) Includes two months of BlueScope Butler financial results.(4) Weighted average shares on issue 750.5m FY04 and 733.0m FY05.

Page 34

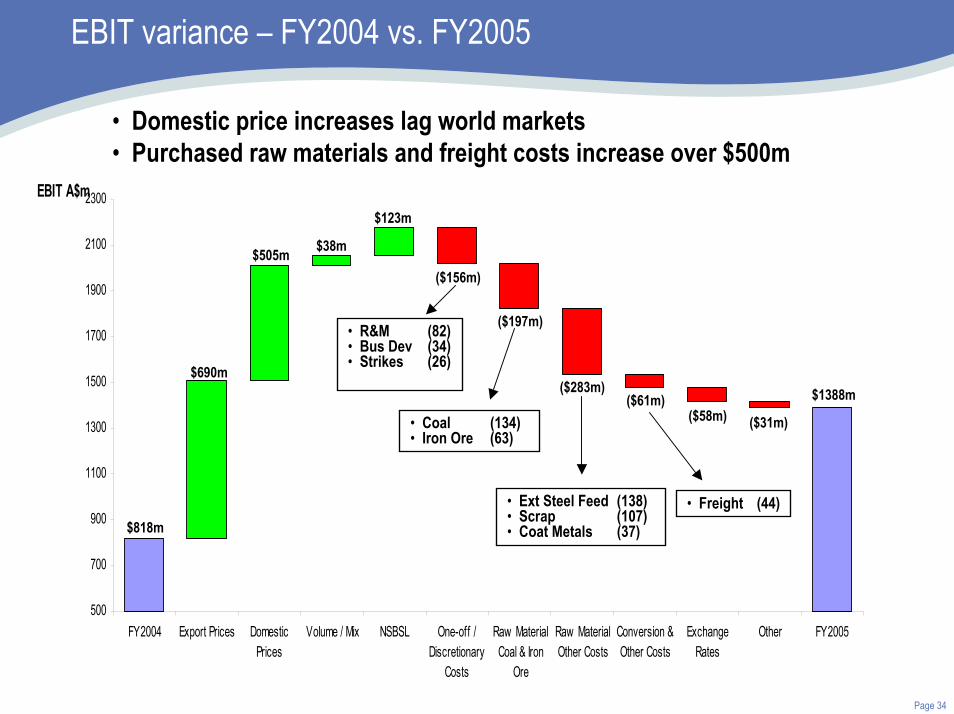

EBIT variance – FY2004 vs. FY2005

500

700

900

1100

1300

1500

1700

1900

2100

2300

FY2004 Export Prices DomesticPrices

Volume / Mix NSBSL One-off /Discretionary

Costs

Raw MaterialCoal & Iron

Ore

Raw MaterialOther Costs

Conversion &Other Costs

ExchangeRates

Other FY2005

EBIT A$m

$818m

$690m$1388m($283m)

$38m

($31m)

($156m)

($58m)

$123m

$505m

($61m)

($197m)• R&M (82)• Bus Dev (34) • Strikes (26)

• Freight (44)

• Coal (134)• Iron Ore (63)

• Ext Steel Feed (138)• Scrap (107)• Coat Metals (37)

• Domestic price increases lag world markets• Purchased raw materials and freight costs increase over $500m

Page 35

Balance Sheet – growing and maintaining flexibility

A s A t A $ M i l l io n s 3 0 J u n e 2 0 0 4 3 0 J u n e 2 0 0 5

A s s e t s C a s h 1 1 9 8 5 R e c e iv a b le s 9 9 6 1 ,0 6 0 In v e n to r y 9 6 3 1 ,2 1 1 O th e r A s s e ts 4 1 5 4 7 9 N e t F ix e d A s s e ts 3 ,2 8 9 3 ,6 2 9

T o t a l A s s e t s 5 ,7 8 2 6 ,4 6 4

L ia b i l i t ie s C r e d ito r s 7 2 8 8 2 4 In te r e s t B e a r in g L ia b i l i t ie s 5 9 3 8 7 6 P r o v is io n s 1 ,2 6 7 1 ,2 6 3 T o t a l L ia b i l i t ie s 2 ,5 8 8 2 ,9 6 3

N e t A s s e ts 3 ,1 9 4 3 ,5 0 1

• Net Debt / (Net Debt + Equity) 12.9% 18.4%(excluding off balance sheet items)

Page 36

Investing for the future – major project capital spending profile

1,170

100300(3)

120

90

28040

80

160

-274122India – Butler / Lysaght facilities(1)

--

45-

8034

1556

China(1)

- Coating and Painting Facility- Guangzhou Butler / Lysaght

Upstream Projects

--44116Vietnam – Coating / Painting(1)

316

-226(3)

18

-

FY2007

-

-

FY2008

401453Total spending on these projects

4070(3)

604(3)

Port Kembla:- HSM expansion- Blast Furnace No. 5 Reline(3)

9012West Sydney Colorbond®

278Thailand(1)

- Metallic Coating Facility

Mid and Downstream Projects

FY2006Actual to 30/06/05(2)

Total Est. Capex/Cost

All in A$million

(1) Estimated capital costs based on forecast exchange rate assumptions at time of project approval.(2) Capital spent from approval to 30/06/05.(3) Indicative, based on project study. Final cost and phasing confirmed later in FY2006.

Page 37

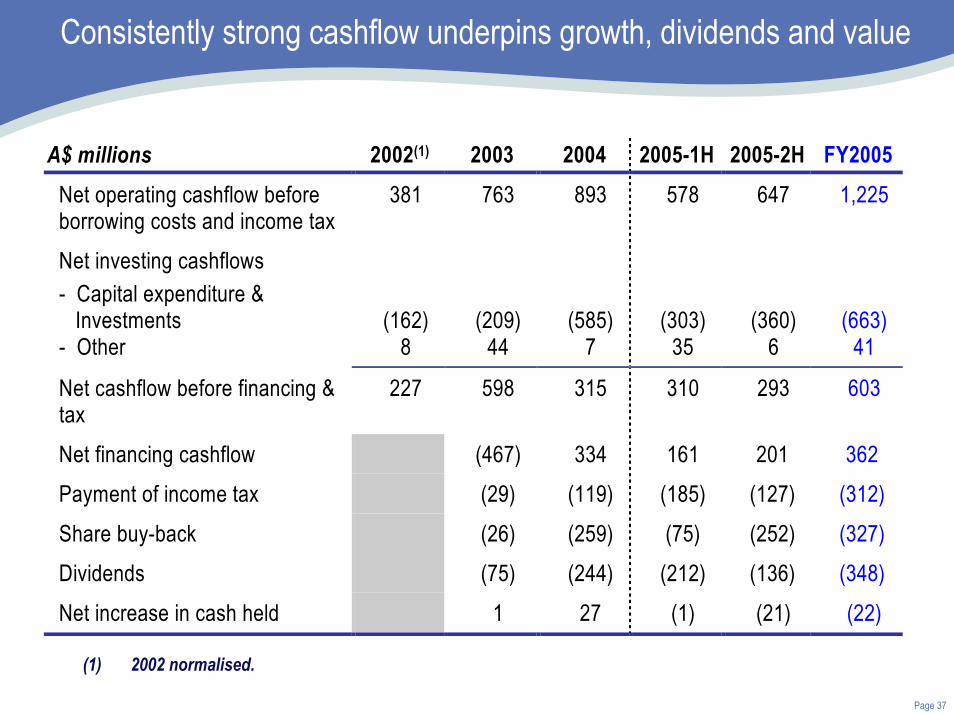

Consistently strong cashflow underpins growth, dividends and value

A$ millions 2002(1) 2003 2004 2005-1H 2005-2H FY2005 Net operating cashflow before borrowing costs and income tax

381 763 893 578 647 1,225

Net investing cashflows - Capital expenditure & Investments - Other

(162) 8

(209) 44

(585) 7

(303) 35

(360) 6

(663) 41

Net cashflow before financing & tax

227 598 315 310 293 603

Net financing cashflow (467) 334 161 201 362 Payment of income tax (29) (119) (185) (127) (312) Share buy-back (26) (259) (75) (252) (327) Dividends (75) (244) (212) (136) (348) Net increase in cash held 1 27 (1) (21) (22)

(1) 2002 normalised.

Page 38

Australian International Financial Reporting Standards

(77)2022(3)13

982

Estimated adjustments:(1) Impairment of assets(2) Defined Benefit Superannuation(3) Foreign currency translation(4) Other(5) Tax (expense) / benefit on above itemsEstimated AIFRS Net Profit After Tax

1,007Reported AGAAP Net Profit After TaxNPAT (A$m)FY2005 Earnings

(1) Impairment write-down of Packaging Products assets. The operational assets are fully written down at 30 June 2005 under AIFRS.

(2) Lower superannuation expense as the unfunded liability is now fully recognised on the balance sheet.

(3) Exchange gains and losses on loans that do not qualify as a hedge of a net foreign investment under AIFRS. Note: The company has taken steps to mitigate this exposure from 1 July 2005.

Page 39

Australian International Financial Reporting Standards

(131)(72)812

3,073(3.8%)

(193)(126)

86(8)

3,260(6.9%)

Estimated adjustments to total equity (net of tax)(1) Defined Benefit Superannuation(2) Impairment of assets(3) Income tax methology(4) OtherEstimated total equity under AIFRSEstimated change (%)

3,501

30 June 2005(A$m)

3,193Total equity under AGAAP

1 July 2004(A$m)

Equity

(1) Recognition of unfunded defined benefit superannuation liability, discounted at corporate bond rate (or equivalent) and grossed-up for contributions tax.

(2) Treatment of Packaging Products as a separate Cash Generating Unit in the opening balance sheet (1 July 2004) and a further impairment at 30 June 2005 associated with domestic margin compression and the withdrawal from export tinplate.

(3) Recognition of additional tax assets due to change in recognition test from “virtually certain” to “probable”. Likely result inrecognition of New Zealand tax expense in 2H of FY2006.

Note: In addition, the Group’s sale of receivables program will not meet derecognition requirements under AIFRS ($140m at 30 June 2005). This together with the lower equity balance will increase reported gearing (net debt / net debt + equity) by approximately 4%.

Page 40

Results remain sensitive to raw material costs and realised hot rolled coil prices

Estimated impact on forecast EBIT (A$mil ) for FY06

Assumption+/– US$25 / tonne movement in BlueScope’s average realised export

HRC price (1) (73)66

7+/ 1¢ movement in Australian dollar / US dollar exchange rate(2) (18)+/– US$10 / tonne movement in NSBSS scrap to HRC price spread 12 (12)+/– 2% movement in slab production in Australia, New Zealand and U.S.A. 20 (46)+/– US$10 / tonne movement in coal costs 50 (50)+/– US$10 / tonne movement in iron ore costs 100 (100)(1) The change in export HRC price assumes proportional effect on export slab, and flow on to domestic pipe and tube market and to other

export products. (2) The movement in the Australian dollar/US dollar exchange rate includes the restatement of US dollar denominated receivables and

payables and the impact of translating the earnings of offshore operations to A$.

Page 41

Looking forward

Global steel industry – dynamic and different

Outlook – FY06

Page 42

Slab and HRC Prices (Index July 2002 = 100)

0

50

100

150

200

250

Jul-02 Oct-02 Jan-03 Apr-03 Jul-03 Oct-03 Jan-04 Apr-04 Jul-04 Oct-04 Jan-05 Apr-05 Jul-05

USA Midwest HRC1 Latin America Export Slab2

China growth continues

Extraordinary year in the global steel industry

Volatile Prices

FY03 FY04 FY05

15

20

25

30

35

40

45

50

55

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05US$ / DMT. Lump trend indicative of all iron ore types.

JSM Benchmark Prices, Lump Iron Ore

Raw material costs skyrocket

Extreme Deviation

Cyclical HighsLT Average

Unprecedented shipping costs

BDI Index

May-9

5

May-0

0

May-0

1

May-0

2

May-0

3

May-0

4

May-0

5

May-9

9

May-9

8

May-9

7

May-9

6

7000

6000

5000

4000

3000

2000

1000

0

Page 43

Global steel industry - dynamic and different

Current industry issues:- Excess inventory - China’s capacity growth- Soaring raw materials costs- Buyer uncertainty- Energy costs

Likely industry outcomes:- Inventory drawn down- Industry matching

production with demand- China introducing structural

reform- Further raw material investment- More stable pricing environment

Six Pillars of a stronger steel industry

1. Restructure / consolidate

2. Reduce price volatility

3. Address raw materials situation

4. Stand against steel subsidies

5. Spend on innovation and reward our investors

6. Become safer and reaffirm our licence to operate

Page 44

Financial outlook FY2006

Hot Rolled Coil,Plate

Cold Rolled

Painted

Roll-forming

Metallic Coated

PEB /Solutions Downstream

Midstream

Upstream

Steelmaking, Slab

WaterChina

Thailand

India

VietnamChina

ChinaThailand

Vietnam

Australia

NZAustralia

NZAustralia

• Significantly higher raw material costs• Global slab / HRC prices flat• Stable production• Costs / efficiency

• Australia- higher prices- lower feed costs- higher production

• Asia- stronger volumes- market growth- new projects commissioning

• Lower feed costs• Improved sales and grow• Restructured / efficiency• New ventures

EBITRevenueVolume

Page 45

A balanced approach for all our stakeholders

• SHAREHOLDERS • CUSTOMERS

• COMMUNITIES • EMPLOYEES

Page 46

Questions and Answers

Dynamic Global Steel

Market

Dynamic Global Steel

Market

Profitable Through the

Cycle

Profitable Through the

Cycle

Geographic and Product

Diversity

Geographic and Product

Diversity

Strong and Flexible Capital

Structure

Strong and Flexible Capital

Structure

Consistently Strong Cash

Flows

Consistently Strong Cash

Flows

Strong Board & Management

Team

Strong Board & Management

Team

Value Added Branded Products

Value Added Branded Products

Growth Opportunities in

Asia

Growth Opportunities in

Asia

Low Cost Producer

Low Cost Producer

Strong Operating

Track Record

Strong Operating

Track Record

A VERY DIFFERENT KIND OF STEEL

COMPANY

Annual Results Presentation Period Ended 30 June 2005Kirby Adams, Managing Director and Chief Executive OfficerBrian Kruger, President Australian Manufacturing Markets (formerly Chief Financial Officer)23 August, 2005

ASX Code: BSL