Annual results 2015 - and December October November ... Includes compensation for the tariff freeze...

58

Annual results 2015 Financial analysts’ meeting 24 February 2016

Transcript of Annual results 2015 - and December October November ... Includes compensation for the tariff freeze...

Annual results 2015

Financial analysts’ meeting

24 February 2016

Highlights

Benoît de Ruffray

Chairman and Chief Executive Officer

Highlights - Contracting

3

Ongoing recovery of marginsEnergy

Margin resilienceConstruction

Record in reservations and first operation in LuxembourgProperty

development

Highlights - Contracting

4

Sharp drop in activity, reorganization of production facilities in FranceMetal

Stable activity in FranceCivil

engineering

Decrease in volume in France and improvement in EuropeRoads

Major projects under control: BPL HSR and PPPsIntegrated

offering

Highlights - APRR and AREA

Initial concession

maturity

Motorway

Stimulus Package

Maurice Lemaire

tunnel integration Actual concession

maturity

APRR 31-12-2032 +25 months +10 months 30-11-2035

AREA 31-12-2032 +45 months No impacts 30-09-2036

Effective date 23rd August 2015 31st January 2016

5

Successive lengthening of the concessions contracts Exceptional events

• Traffic growth +2.7%

• EBITDA margin improvement to the record level of 71.8% (+ 110 bps)

• Decrease of 16% of APRR and Eiffarie financial expenses

Operation

6

Highlights - Other concessions

• Further improvement in traffic and profitability of the A65

• Integration of the Viaduct service area in the Viaduct of Millau concession

• Important traffic growth of « Autoroute de l’Avenir » in Senegal and

opening of the new extension during 2016

Motorways

concessions

• Commercial successes in building in France and infrastructure in Germany

• Opening of the University of Grenoble and disposal of Eifficentre

PPP

portfolio

Eiffage - 2015

Revenue €M-0.6%

13,73214,035

14,26413,987 13,909

2011 2012 2013 2014 2015

Financial Net debt €M

-423 €M12,645 12,469 12,579

12,01411,591

2011 2012 2013 2014 2015

Order Book €bn

-2.8%(+1.2% Exc. BPL)

13.512.2 11.7 11.8 11.4

2011 2012 2013 2014 2015

Ongoing profit growth - WCR improvements - Deleveraging - Slight decrease in order book

Operating profit €M+6.2%

1,1041,200

1,318 1,347 1,431

2011 2012 2013 2014 2015

205 221257 275 312

2011 2012 2013 2014 2015

Net profit group share €M+13.5%

Change in WCR €M+46 €M+279

+138

-160

+47 +46

2011 2012 2013 2014 2015

7

Slight decrease of activity

New profit growth

Proposal of a dividend of €1.50 per share (+25%)

Outlook - 2016

8

Results by business line and financial results

Christian Cassayre

Chief Financial Officer

11,609 11,466

2,378 2,443

13,987 13,909

2014 2015

10

Revenue (excluding IFRIC 12)

-1.2%

+2.7%

BREAKDOWN CONCESSIONS / CONTRACTING (€M)

ContractingConcessions

11,56811,272

2,1002,234

319 403

13,987 13,909

2014 2015

-2.6%

+6.4%

BREAKDOWN BY GEOGRAPHICAL AREA (€M)

+26.3%

-0.6% -0.6%

∆15/14 ∆15/14

International excluding Europe

France Europe excluding France

+9.0 %

11

Contracting revenue (excluding IFRIC 12)CONTRACTING BREAKDOWN

BY GEOGRAPHICAL AREA (€M) AND % OF TOTAL

3,306 3,578

4,570 4,374

3,733 3,514

11,609 11,466

2014 2015

+8.2%

-4.3%

-5.9%

BREAKDOWN BY DIVISION (€M)

Construction Infrastructures Energy

-3.9%

+6.3%

+27%

-1.2% -1.2%

∆15/14 ∆15/14

9,2098,852

2,100 2,233

300381

11,609 11,466

2014 2015

(3%)

(18%)

(79%)(77%)

(20%)

(3%)

International excluding Europe

France Europe excluding France

12

Operating profit on ordinary activities and margins

Growth of operating profit on ordinary activities of 6.2% to €1,431M (+€84M)

Operating margin increase by 70 bps to 10.3% of revenue

2014 2015∆ 15/14

€M % revenue €M % revenue

Construction 156 4.2% 136 3.9% -12.8%

Infrastructures 108 2.4% 75 1.7% -30.6%

Energy 116 3.5% 132 3.7% +13.8%

Sub-total Contracting 380 3.3% 343 3.0% -9.7%

Concessions 985 41.4% 1,106 45.3% +12.3%

Holding -18 -18

GROUP TOTAL 1,347 9.6% 1,431 10.3% +6.2%

1,1041,200

1,318 1,3471,431

8.0%

8.6%

9.2%9.6%

10.3%

2011 2012 2013 2014 2015

13

Evolution of the operating margin

Continuous growth of the operating profit and margin to the level of 10.3%

Operating profit (M€) and margin (%)

14

Construction: activity and results

Revenue down 5.9% (-5.8% lfl)

France -8.1%, Europe (excluding France) +4.0%

Property development

Record high in reservations with 3,671 units to be compared to 3,395

in 2014

First significant operation in Luxembourg

New significant operation: “ZAC Paris Affaires” in Asnières

Works

Decrease in revenue but strong reactivity in organizational

restructuring

Good execution of major works and iconic deliveries:

– The Cannes palace of festivals, “Tour des finances” in Liège and

“Le Garance” in Paris

Significant order intake

Renovation of the Hall 7 of Paris “parc des expositions”, City of

Gastronomy of Dijon, Lyon University Pole and PPP buildings

3,781 3,798 3,715 3,733 3,514

4.3% 4.2% 4.2% 4.2% 3.9%

2011 2012 2013 2014 2015

2011 2012 2013 2014 2015

Works 85% 84% 82% 80% 79%

Property 15% 16% 18% 20% 21%

BREAKDOWN OF REVENUE

Upholding of the operating margin at the high level of 3.9%

REVENUE (€M) - OPERATING MARGIN ON ORDINARY ACTIVITIES

Le Garance - Paris Pyrénées - Paris 20e

15

4,390 4,5274,854

4,570 4,374

0.7%

1.8%

2.6% 2.4%

1.7%

2011 2012 2013 2014 2015

Decrease of the operating margin by 70 bps to 1.7%

Deterioration of the metal construction in France

16

Infrastructures(1): activity and results

Revenue down 4.3% (-6.1% lfl)

France -7.7%, Europe excluding France +9.1% and outside

Europe -2.8%

Drop in the metal construction activities in France

Margin evolution

Stable margin in civil engineering

Reorganization in roads

Reorganization in Metal construction works

Major projects

Bretagne-Pays de la Loire HSR: progress in line with

expectations

International development

A94 Motorway in Germany (PPP)

Metal walkways in Angola

REVENUE (€M) - OPERATING MARGIN ON ORDINARY ACTIVITIES

(1) Previously Public works and Metallic construction

Industries 2011 2012 2013 2014 2015

Coatings-M tons 9 8 9 9 9

Quarries-M tons 21 19 21 20 19

Binders -K tons 183 162 174 177 174

VOLUME FIGURES

Short lived street Art on the Paris ring road

17

Energy(1): activity and results

3,417 3,535 3,434 3,306 3,578

2.2%2.6%

3.0%

3.5%3.7%

2011 2012 2013 2014 2015

Continuous growth of the operating margin over the last 5 years

Increase of the operating margin by 20 bps over the year to 3.7%

Revenue up 8.2% (+7.5% lfl)

France +5.9%, Europe excluding France +4.8% and

x2 outside Europe

Increased operating margins

Good performance of the system divisions

Gradual acquisition (mainly in France regions)

Iconic delivery

Successful realization of the largest photovoltaic farm in

Europe (Cestas)

Major Projects

Photovoltaic farms in Chili

Bretagne-Pays de la Loire HSR: ramping up

18

REVENUE (€M) - OPERATING MARGIN ON ORDINARY ACTIVITIES

(1) Previously Energy and Industrial maintenance

Deployment of optical fiber

19

2,144 2,175 2,2612,378 2,443

40.4%41.1%

42.2%41.4%

45.3%

2011 2012 2013 2014 2015

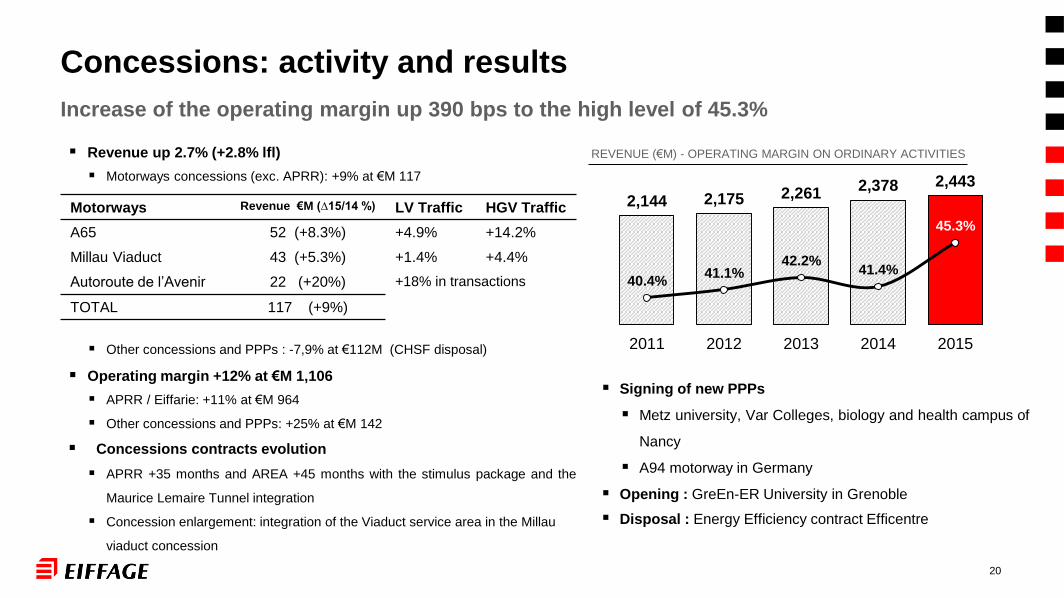

Revenue up 2.7% (+2.8% lfl)

Motorways concessions (exc. APRR): +9% at €M 117

117

Other concessions and PPPs : -7,9% at €112M (CHSF disposal)

Operating margin +12% at €M 1,106

APRR / Eiffarie: +11% at €M 964

Other concessions and PPPs: +25% at €M 142

Concessions contracts evolution

APRR +35 months and AREA +45 months with the stimulus package and the

Maurice Lemaire Tunnel integration

Concession enlargement: integration of the Viaduct service area in the Millau

viaduct concession

Concessions: activity and results

Increase of the operating margin up 390 bps to the high level of 45.3%

Motorways Revenue €M (∆15/14 %) LV Traffic HGV Traffic

A65 52 (+8.3%) +4.9% +14.2%

Millau Viaduct 43 (+5.3%) +1.4% +4.4%

Autoroute de l’Avenir 22 (+20%) +18% in transactions

TOTAL 117 (+9%)

Signing of new PPPs

Metz university, Var Colleges, biology and health campus of

Nancy

A94 motorway in Germany

Opening : GreEn-ER University in Grenoble

Disposal : Energy Efficiency contract Efficentre

20

REVENUE (€M) - OPERATING MARGIN ON ORDINARY ACTIVITIES

21

Eiffage Marathon of the Dakar motorway

Revenue (Exc. Ifric 12) up 3.0%

Total traffic increase up 2.7%

LV +2.6% and HGV +2.9%

Operating margin up

Ongoing optimization of the structures

Productivity gains in the core operations

Extension to the concessions contracts

APRR +35 months

AREA +45 months

Application of the contractual toll increase in 2016

Openings

A719 Vichy / Gannat (January)

A466 north of Lyon (July)

REVENUE (€M) – EBITDA / REVENUE

22

APRR: activity and results

2,022 2,0392,099

2,1492,214

69.2%

70.0%70.3%

70.7%

71.8%

2011 2012 2013 2014 2015

Continuous growth of EBITDA and EBITDA margin over the last 5 years

Increase of the EBITDA margin by 110 bps to the record level of 71.8%

TRAFFIC TOLL RECEIPTS REVENUE MIX

HGV

15%

LV

85%

HGV

33%

LV

67%

Other

3%

Tolls

97%

Winter Activities - APRR

23

24

APRR & Eiffarie: Refinancing in 2015

New credit facilities and bonds issues for APRR and Eiffarie for a total of €bn 4.6

Bank debt(*)

APRR

Bank debt

Eiffarie

EIB

APRR

Bonds

APRR

Bonds

APRRTOTAL

Date February FebruaryJune and

DecemberOctober November

Amount (€bn) 1.8 1.5 0.3 0.5 0.5 4.6

CostFloating

+45 bps

Floating

+100 bps

Floating

+40 bps

Fixed rate

1.5%

Floating

+70 bps

Maturity5 years + 2x1

year

5 years + 2x1

year7 years 8 years 4 years

Reimbursement On maturity

Progressive

€100M/year an

average

On maturity On maturity On maturity

* Revolving credit facility (RCF)

25

APRR & AREA: Tariff formulae 2016 - 2023

2017 2018 2019 2020 2021 2022 2023

Tariff increase 1st of February 2016

85% x I 85% x I 70% x I 70% x I 70% x I 70% x I 70% x I

+ + + + + + +

APRR 1.23% 0.59% 1.13% 0.25% 0.25% 0.25% 0.25% 0.25%

AREA 1.27% 0.62% 1.17% 0.26% 0.26% 0.26% 0.26% 0.26%

Includes management contract tariff formulae 2014-2018

Includes compensation for the Increase in the land tax

rates since 2013

Absent of new management contract

Includes compensation for the tariff freeze of 2015

I = Inflation

Contractual tariff increase and compensations

26

Consolidated income statement

Increase in the operating profit on ordinary activities of 6.2% and of the net results of 13.5%

Decrease in the financial expenses of 15.3%

In €M 2014 2015 Δ 15/14

Revenue(1) 13,987 13,909 -0.6%

Operating profit on ordinary activities (% of revenue) 1,347 (9.6%) 1,431 (10.3%) +6.2%

Other operating income and expenses (67) (94)

Operating income 1,280 1,337 +4.5%

Cost of net debt (726) (615) -15.3%

Other financial income and expenses (26) (38)

Net financial expenses (752) (653) -13.2%

Share of profit of associates (2) (5)

Income tax (172) (220)

Net profit 354 458 +29.4%

Minority interests 79 146

Net profit (group share) 275 312 +13.5%

Net profit per share 3.10 3.42

(1) Exc. IFRIC 12

o/w Concessions (718) o/w Concessions (612)

205 €M221 €M

257 €M275 €M

312 €M

2.36€

2.59€

2.96€3.10€

3.42€

2011 2012 2013 2014 2015

Total capital’s shares in millions

87.1 87.1 89.4 92.3 95.4

Continuous growth of the net profit and profit per share over the last 5 years

Net profit (group share) and profit per share

27

2,5692,631

710737

11,59112,014

3,4722,978

18,34218,360

Capital and reserves

FND

WCR

Other liabilities Inc. Mtm of CNA debt and the swaps

4,3914,350

13,95114,010

18,34218,360

Non current assets Concessions

Non current assets Holding & Contracting

Consolidated and simplified balance sheet

ASSETS

In €M

31/12/2014 31/12/2015

EQUITY AND LIABILITIES

Exc. Mtm of CNA debt and the swaps

28Pro forma IFRIC 21

33 (55) 81

(2,074)

(46)

890 111

637

Capex

748

Acquisitions

& disposals

Financial net debt evolution (€M)

EBITDAChange in WCR:

Holding & Contracting (93)

Concessions 47

Net Capex

Contracting

& Holding

Capex

Concessions

Dividends

&

Capital

transactions

12,014

11,591

FND 31/12/2014* FND 31/12/2015**Exc. Mtm of the CNA debt and the swaps :

M€ 799 M€ 603

(2,035) (47) 987 81 642 (306) 55 58

Operation

(1,230)

723(1 095)

29

2014 figures Pro forma of Capex reclassification

Interest &

taxes paid

Variations

without

flows of

funds

&

misc

Financial net debt structure (€M)

Financial net debt down €0.4bn over 1 year €1bn over 2 years

Exc. Mtm of the CNA debt and the swaps :

€M 1,065 €M 1,302 €M 860 €M 799 €M 603

12,294

13144 27

166

31/12/12 31/12/13

12,57912,469

FND Holding

& Contracting

FND

Concessions

with recourse

DFN

Concessions

without recourse

12 386

12,014

31/12/14

12,386 7

-31

12,038 12 386

11,591

31/12/15

-334

11,925

12,472

13241

31/12/11

12,645

30

Pierre-Mauroy Stadium

155

BPL HSR744

DGGN121

Grande Arche

99

Education289

APRR7,420

Macquarie Quasi equity

396

Eiffarie1,246

PPPs1,408

Other Motorway

concessions1,455

APRR and Eiffarie9,062

NON RECOURSE FND STRUCTURE (€M)NON RECOURSE FND BREAKDOWN (€M)

Concession financial net debt breakdown

Non recourse debt raised in dedicated SPVs for €11.9bn(*)

Millau Viaduct

581A65834

Autoroute de l'Avenir (Senegal)

40

(*) Exc. Mtm of the CNA debt and the swaps : €M 603

31

13.512.1 11.7 11.8 11.4

31/12/11 31/12/12 31/12/13 31/12/14 31/12/15

ORDER BOOK (€bn) AND EQUIVALENT NUMBER OF

MONTHS OF THE CONTRACTING TURNOVER

32

Activity and commercial dynamism

3.1 2.8

4.0 3.9

4.7 4.8

11.8 11.4

31/12/14 31/12/15

BREAKDOWN BY DIVISION (€bn)

12 MONTHS VARIATIONS

Construction Infrastructures Energy

-7.8%

-4.6%

+2.1%

Strong order book at €11.4bn down 2.8% over one year (+1.2% Exc. BPL)

-2.8%

∆15/14

13.9

months

12.3

months12.0

months

12.2

months12.0

months

Appendices

Free float47.6%

Employees24.3%

Treasury shares3.0%

BPI18.8%

BlackRock6.3%

SHAREHOLDERS AT 31/12/2015 (95,4 M Shares)SHAREHOLDERS at 30/06/2015 (95,4 M Shares)

34

Group shareholding structure

Free float51.2%

Employees23.7%

Treasury shares4.9%

BPI13.9%

BlackRock6.3%

Benelux797

Germany657

Spain344

Poland199

Other237

France11,272

Europe Excluding

France2,234

International Excluding

Europe403

REVENUE BREAKDOWN IN EUROPE

EXCLUDING FRANCE (€M)REVENUE BREAKDOWN (€M)

35

Revenue (excluding IFRIC 12)

36

Consolidated balance sheet - Assets

In €M 31/12/2013 (*) 31/12/2014(*) 31/12/2015

Property, plant and equipment 1,474 1,463 1,481

Investment property 6 5 4

Fixed assets held under concessions 12,415 12,069 11,701

Goodwill on acquisition 2,849 2,873 2,904

Other intangible assets 172 175 172

Investment accounted for using the equity method 107 102 82

Financial assets on service concessions non-current 1,374 1,406 1,732

Other financial assets 273 267 266

Deferred tax assets 296 301 292

Total non current assets 18,966 18,661 18,634

Inventories 556 518 600

Trade receivables 4,151 3,962 3,966

Current tax receivables 5 90 137

Financial assets on service concessions current 15 17 20

Other current assets 1,457 1,259 1,116

Cash and cash equivalent 2,097 4,265 3,641

Asset held for sale 83 49 -

Total current assets 8,364 10,160 9,480

Total assets 27,330 28,821 28,114

* Pro forma IFRIC 21

37

Consolidated balance sheet - Equity and liabilities

In €M 31/12/2013(*) 31/12/2014(*) 31/12/2015

Share capital 358 369 382

Consolidated reserves 2,430 2,617 2,789

Profit & losses directly accounted for in equity (340) (359) (286)

Net profit for the period 257 275 312

Total capital and reserves, attributable to the Group 2,705 2,902 3,197

Minority interests (7) 87 275

Total capital and reserves 2,698 2,989 3,472

Long-term debt 13,261 14,140 12,847

Deferred tax liabilities 1,050 1,077 1,159

Non current provisions 529 599 581

Other non current liabilities 52 51 46

Total non current liabilities 14,892 15,867 14,633

Trade creditors 3,169 2,884 2,924

Short-term loans and other borrowings 1,184 1,337 1,520

Non current borrowings due with in one year 1,091 1,601 1,468

Current tax liabilities 74 65 106

Current provisions 475 477 523

Other creditors and accruals 3,693 3,592 3,468

Liabilities held for sale 54 20 -

Total current liabilities 9,740 9,976 10,009

Total liabilities and share holder’s equity 27,330 28,821 28,114

* Pro forma IFRIC 21

38

Consolidated income statement

In €M 2013 2014 2015

Revenue 14,272 13,948 14,060

Other income 6 6 6

Raw materials and consumables used (2,627) (2,463) (2,775)

Staff costs (3,357) (3,314) (3,240)

Other expenses (5,767) (5,631) (5,463)

Taxes other than corporate tax (398) (408) (426)

Amortisation and depreciation expense (845) (858) (833)

Provisions (20) (53) (37)

Changes in inventories (25) (49) 43

Other operating income and expenses 79 169 96

Operating profit on ordinary activities 1,318 1,347 1,431

Other operating income and expenses (56) (67) (94)

Operating profit 1,262 1,280 1,337

Income from cash and cash equivalent 34 44 33

Cost of gross debt (761) (770) (648)

Net finance costs (727) (726) (615)

Other financial income (expenses) (51) (26) (39)

Share of profit (loss) of associates 5 (2) (5)

Corporation tax (167) (172) (220)

Net profit 322 354 458

Attributable to the Group 257 275 312

Minority interests 65 79 146

39

Consolidated cash flow statement

In M€ 2014* 2015

Cash flow generated by operations 1,143 1,261

Change in working capital in operating activities 47 46

Change in working capital interests and taxes (95) (77)

Net Capital expenditure Contracting & Holding (81) (111)

Capital expenditure Concessions (642) (637)

Free Cash Flow 372 482

Acquisition of minorities shares (9) -

Acquisitions & disposals 306 (33)

Dividends (115) (121)

Change in equity 57 40

Change in net bank debt 611 368

Changes without flow of funds (25) 33

Changes in finance leases (21) 22

Change in financial net debt (1) 565 423

of which concessions 368 120

of which Contracting and Holding 197 303

* Pro forma of Capex reclassification(1) Exc. Mtm of the CNA debt and the swaps: 799 603

40

Group financial structure

In €M 31/12/2011 31/12/2012 31/12/2013 31/12/2014 31/12/2015

Concessions

- Financial debt 11,762 11,565 11,678 11,458 11,529

- Macquarie quasi equity 710 729 708 580 396

Sub-total without recourse 12,472 12,294 12,386 12,038 11,925

- With recourse 41 44 27 7 -

Concessions financial net debt 12,513 12,338 12,413 12,045 11,925

Holding & Contracting

- Net cash (656) (759) (921) (1,678) (1,804)

- Gross debt 788 890 1,087 1,647 1,470

Holding & Contracting financial net debt 132 131 166 -31 -334

Total financial net debt (1) 12,645 12,469 12,579 12,014 11,591

(1) Exc.Mtm of the CNA debt and the swaps: 1,065 1,302 860 799 603

Financial expenses and resultsIn €M 2013 2014 2015 Δ 15/14

Concessions (367) (718) (612) -14.8%

of which:

APRR (302) (292) (252)

Eiffarie & Financière Eiffarie (277) (287) (233)

Financière Eiffarie Group (579) (579) (485) -16.2%

A'Liénor (A65) (44) (44) (20) -54.6%

VP1 (Millau Viaduct) (27) (23) (21)

Héveil, Hanvol et H'ennez (Hospitals) (23) (12) -

ERE (BPL HSR) (17) (32) (46) +41.4%

Elisa (Pierre-Mauroy stadium) (14) (14) (14)

Eiffigen (National Police HQ) (6) (6) (6)

Armaneo (Grande Arche) - - (3)

Other PPPs and concessions (13) (8) (18)

Holding & Contracting (5) (8) (2)

Cost of net debt (727) (726) (614) -15.4%

Other financial income and expenses (15) (26) (39)

Financial result (388) (752) (653) -13.1%41

42

Operational Capex

In €M 2014* 2015

Contracting and Holding net Capex 81 111

Concession Capex 642 637

Total operational Capex 723 748

* Pro forma of Capex reclassification

43

Roads56%

Civil Engineering

20%

Earthworks6%

Environment8%

Railways and other

10%

INFRASTRUCTURES

Electric Engineering

70%

Climatic Engineering

13%

O&M17%

ENERGY

Equipements / Non residential50%

Civil engineering

11%

Residential39%

CONSTRUCTION

Contracting: market segmentation

44

Private62%

Public38%

CONSTRUCTION

Private75%

Public25%

ENERGY

Private48%

Public52%

INFRASTRUCTURES

Contracting: customer segmentation

Concessions length Tariffs Development of Investments Regulation

Motorway stimulus Package

and Integration of the Tunnel

Maurice Lemaire in the APRR

concession

Compensation of the 2015

tariff freeze by an additional

toll increase between 2019

and 2023

€720M of investments

Establishment of an

independent authority

(ARAFER) and increased

transparency

APRR: 35 months lengthening

to the end of November 2035

Compensation of the raise

in the land tax rates since

2013 by an additional toll

increase between 2016 and

2018

Contribution to a dedicated

investment fund which will

invest in the ecological

modernization of transportation

Strengthening of the

protection against further

taxation

AREA: 45 months lengthening

to the end of September 2036

Commercial policies:

carpooling, ecological vehicle,

student and youth, “Macron”

bus.

Implementation of a

mechanism capping the

profitability via the revenues

Voluntary exceptional annual

contribution to the AFITF

45

APRR & AREA - 2015 & 2016 evolutions

€500M of capex covering growth and modernization of the network

Major infrastructure projects

Construction of the A89-A6 junction north of Lyon

A43 / A41 / high speed urban road of Chambéry

Three widenings on the A6 at Auxerre (southbound), on the A71 north of

Clermont-Ferrand (northbound), and on the A41 north of Annecy

(in both directions)

Operating investments

Renovation of rest areas

Environmental protection

Improvement of service and security

46

APRR & AREA - 2014 - 2018 Management contracts

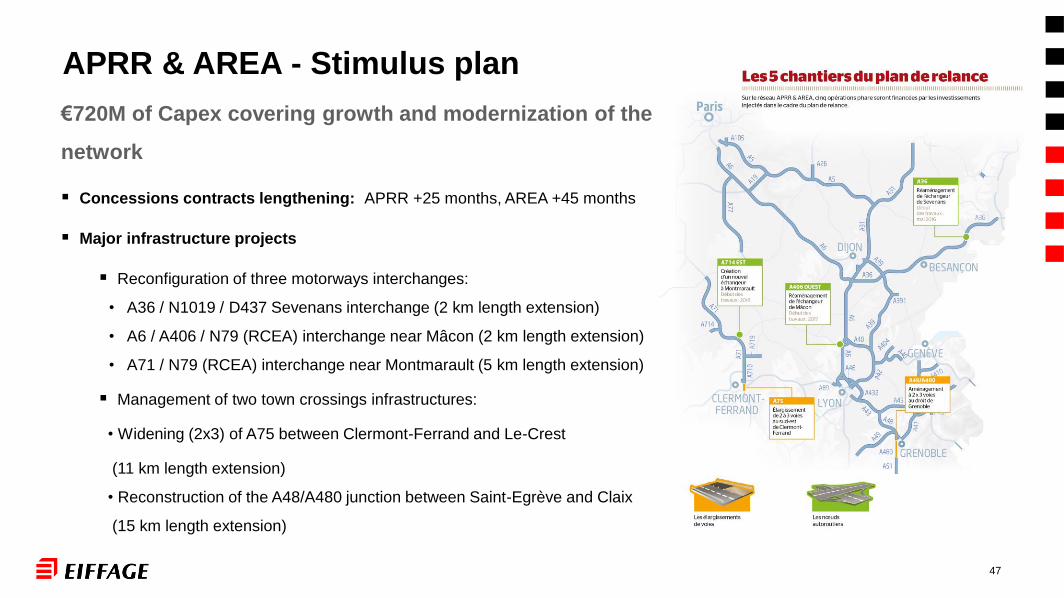

€720M of Capex covering growth and modernization of the

network

Concessions contracts lengthening: APRR +25 months, AREA +45 months

Major infrastructure projects

Reconfiguration of three motorways interchanges:

• A36 / N1019 / D437 Sevenans interchange (2 km length extension)

• A6 / A406 / N79 (RCEA) interchange near Mâcon (2 km length extension)

• A71 / N79 (RCEA) interchange near Montmarault (5 km length extension)

Management of two town crossings infrastructures:

• Widening (2x3) of A75 between Clermont-Ferrand and Le-Crest

(11 km length extension)

• Reconstruction of the A48/A480 junction between Saint-Egrève and Claix

(15 km length extension)

47

APRR & AREA - Stimulus plan

Exc. Mtm of the CNA debt and the swaps

€M 800 €M 931 €M 656 €M 592 €M 431

APRR & Eiffarie – Financial structure (€M)

6,0966,760 6,751 6,696

7,420

3,522 2,482 2,331 2,2201,246

710729 708

580396

10,3289,971 9,790

9,4969,062

31/12/2011 31/12/2012 31/12/2013 31/12/2014 31/12/2015

Macquarie quasiequity

Eiffarie

APRR

48

49

APRR - Debt profile

Debt profile as at 31/12/2015 (€M)

EMTN bonds details

Amount in €M Coupon Maturity Yield on 31/12/2015

300 Eur3m+0.87% 18/1/2016 0.22%

500 4.375% 25/1/2016 0.27%

1,000 5 % 12/1/2017 0.28%

500 5.125% 18/1/2018 0.45%

500 4.875% 21/1/2019 0.63%

500 Eur3m+0.75% 31/3/2019 0.62%

500 Eur3m+0.70% 3/1/2020 0.65%

500 2.25% 16/1/2020 0.81%

700 1.125% 15/1/2021 0.98%

52 RPI indexed 25/1/2021

500 1.50% 15/01/2024 1.45%

700 1.875% 15/1/2025 1.66%

435 391

714

1,000

52

500

500

500

300

500

500

700700

500

500

275

75 75

100

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

CNA EMTN program EIB*Reimbursed at the end of January 2016

2036

*

*

Km travelled, 12 months rolling average, rebased to Q4 2007

50

APRR - Traffic evolution

84

88

92

96

100

104

108

112

HGV

LV

Total

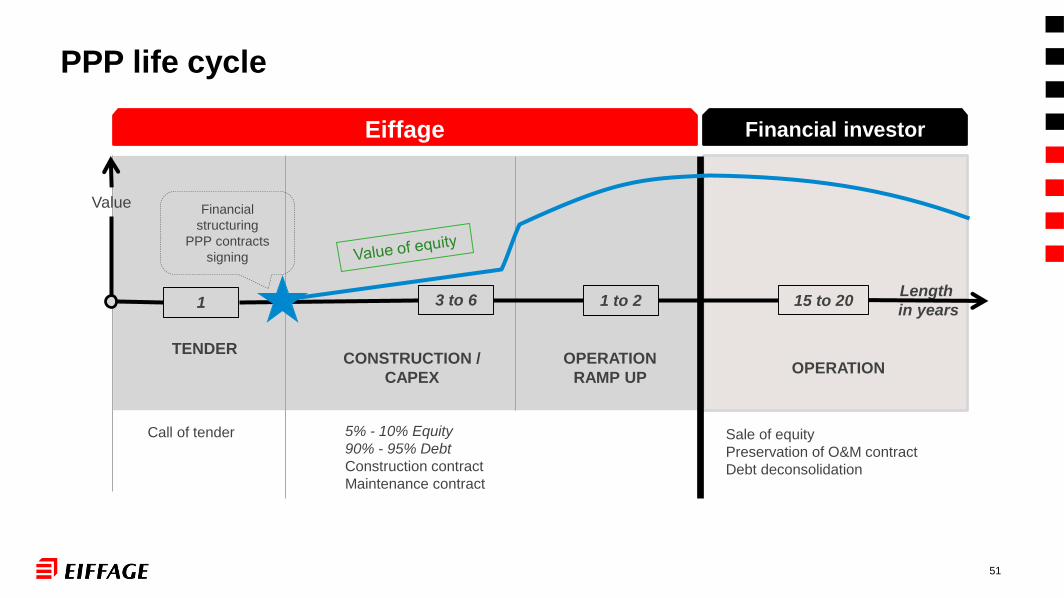

CONSTRUCTION /

CAPEX

TENDEROPERATION

RAMP UP

51

PPP life cycle

Eiffage

Call of tender 5% - 10% Equity

90% - 95% Debt

Construction contract

Maintenance contract

Sale of equity

Preservation of O&M contract

Debt deconsolidation

Financial investor

Length

in years1 3 to 6 1 to 2 15 to 20

Value Financial

structuring

PPP contracts

signing

OPERATION

Assets in concession

Name Type CountryEnd of

concessionStatus % Shares

Consolidation

method

APRR Toll Concession FR 2035/2036 Operational 50.1% Full consolidation

A65 Toll Concession FR 2067 Operational 65.0% Full consolidation

Millau viaduct Toll Concession FR 2079 Operational 51.0% Full consolidation

Norscut Toll Concession PT 2037 Operational 36.0% Equity method

Prado Carénage Tunnel Toll Concession FR 2025 Operational 32.9% Equity method

Prado Sud Tunnel Toll Concession FR 2054 Operational 41.5% Equity method

“Autoroute de l’Avenir” motorway Toll Concession SEN 2040 Operational 100.0% Full consolidation

HSR Perpignan-Figueras Railroad in concession FR / SP 2057 Operational 50.0% Equity method

HSR Bretagne-Pays de la Loire Railroad in PPP FR 2036 Under construction 100.0% Full consolidation

Prison Lot 1 PPP FR 2037 Operational 19.9% Not consolidated

Marche-en-Famenne prison PPP BEL 2038 Operational 19.0% Not consolidated

Le Plessis-Robinson (92) covered market PPP FR 2030 Operational 100.0% Full consolidation

National police HQ PPP FR 2043 Operational 100.0% Full consolidation

Pierre-Mauroy stadium PPP FR 2043 Operational 100.0% Full consolidation

Jean-Zay high school - Lorraine PPP FR 2034 Operational 100.0% Full consolidation

GreEn-ER university - Grenoble PPP FR 2041 Operational 100.0% Full consolidation

Bretagne university PPP FR 2038 Under construction 10.0% Not consolidated

Lille university PPP FR 2041 Under construction 100.0% Full consolidation

Aix-en-Provence university PPP FR 2042 Under construction 100.0% Full consolidation

Metz university PPP FR 2042 Under construction 100.0% Full consolidation

Seine-St-Denis colleges lot 1 PPP FR 2034 Operational 100.0% Full consolidation

Seine-St-Denis colleges lot 3 PPP FR 2034 Operational 100.0% Full consolidation

Var colleges PPP FR 2043 Under construction 100.0% Full consolidation

Kreis Lippe road network PPP GER 2033 Operational 100.0% Full consolidation

“La Grande Arche La Défense” renovation PPP FR 2034 Under construction 100.0% Full consolidation

52

Assets in concessionCarrying value of assets held under concession (€M)* 31/12/2013 31/12/2014 31/12/2015

APRR 11,134 10,837 10,469

A65 1,028 1,021 1,013

Millau viaduct 373 369 365

Norscut 30 39 18

Prado Carénage Tunnel 22 22 23

Prado Sud Tunnel 9 8 8

“Autoroute de l’Avenir” motorway 80 40 93

HSR Perpignan-Figueras 54 55 46

HSR Bretagne-Pays de la Loire 428 660 867

Prisons Optimep 4 2 3 1

Le Plessis-Robinson (92) covered market 11 11 11

CHSF Hospital 333 - -

National police HQ 130 128 125

Pierre-Mauroy stadium 302 353 348

Jean-Zay high school – Lorraine 58 59 57

GreEn-ER university – Grenoble 16 50 61

Lille university - 4 33

Aix-en-Provence university - 10 34

Metz university 66 105 105

Seine-St-Denis colleges lot 1 62 106 102

Energy efficiency contract EFFIGEN 32 30 -

“La Grande Arche La Défense” renovation - 15 104

Other concessions & PPPs 130 84 67

Total 14,299 14,009 13,951

* Fully consolidated: 100% of asset/ Equity method: group share

53

54

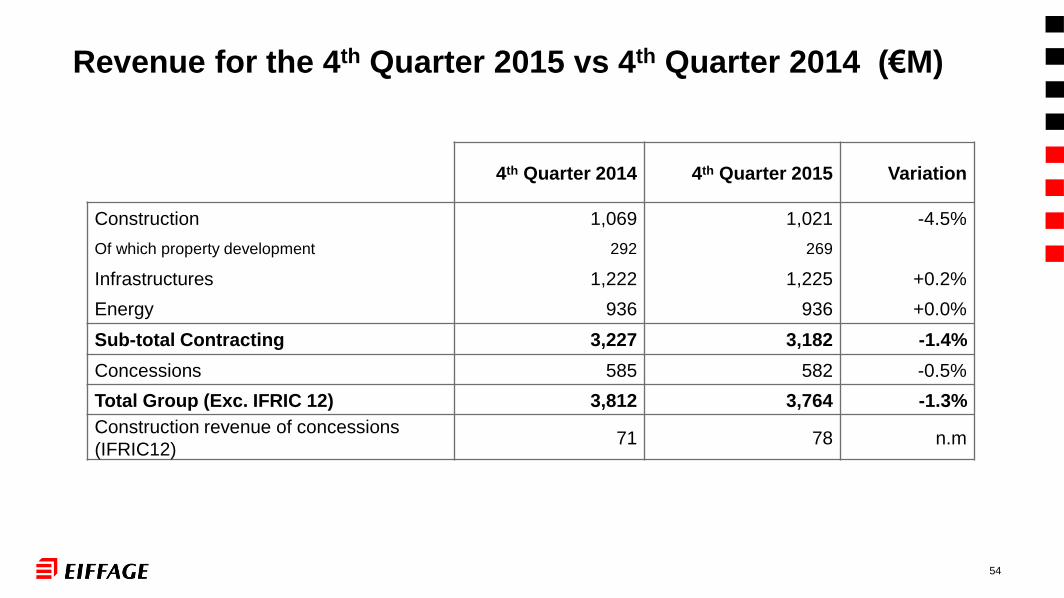

Revenue for the 4th Quarter 2015 vs 4th Quarter 2014 (€M)

4th Quarter 2014 4th Quarter 2015 Variation

Construction 1,069 1,021 -4.5%

Of which property development 292 269

Infrastructures 1,222 1,225 +0.2%

Energy 936 936 +0.0%

Sub-total Contracting 3,227 3,182 -1.4%

Concessions 585 582 -0.5%

Total Group (Exc. IFRIC 12) 3,812 3,764 -1.3%

Construction revenue of concessions

(IFRIC12)71 78 n.m

55

Summary revenue and operational profit on ordinary activities

2011-2015 (€M)

RevenueOperational profit on ordinary

activitiesOperational margin

2011 2012 2013 2014 2015 2011 2012 2013 2014 2015 2011 2012 2013 2014 2015

Construction 3,781 3,798 3,715 3,733 3,514 163 160 156 156 136 4.3% 4.2% 4.2% 4.2% 3.9%

Infrastructures 4,390 4,527 4,854 4,570 4,374 29 83 125 108 75 0.7% 1.8% 2.6% 2.4% 1.7%

Energy 3,417 3,535 3,434 3,306 3,578 75 92 103 116 132 2.2% 2.6% 3.0% 3.5% 3.7%

Sub-total

Contracting11,588 11,860 12,003 11,609 11,466 267 335 384 380 343 2.3% 2.8% 3.2% 3.3% 3.0%

Concessions 2,144 2,175 2,261 2,378 2,443 866 893 954 985 1,106 40.4% 41.1% 42.2% 41.4% 45.3%

Holding (29) (28) (20) (18) (18)

Total Group 13,732 14,035 14,264 13,987 13,909 1,104 1,200 1,318 1,347 1,431 8.0% 8.6% 9.2% 9.6% 10.3%

56

Restated revenue and operational profit on ordinary activities

for 2014 (€M)

RevenueOperational profit on ordinary

activitiesOperational margin

Published Metal division Restated Published Metal division Restated Published Restated

Construction 3,733 3,733 156 156 4.2% 4.2%

Infrastructures 3,957 613 4,570 95 13 108 2.4% 2.4%

Energy 3,025 281 3,306 112 4 116 3.7% 3.5%

Metal 894 (894) - 17 (17) - 1.9% -

Sub-total Contracting 11,609 0 11,609 380 380 3.3% 3.3%

Concessions 2,378 2,378 985 985 41.4% 41.4%

Holding (18) (18)

Total Group 13, 987 13,987 1,347 1,347 9.6% 9.6%

Xavier Ombrédanne

Phone: +33 (0)1 71 59 10 56

Register to receive press release at http://www.eiffage.com/press-releases

57

Investor relations contact and Agenda

Eiffage APRR

Quarterly information and turnover for the 4th quarter of 2015 24.02.2016 21.01.2016

2015 annual results and analysts presentation 24.02.2016 24.02.2016

General Meeting of shareholders 20.04.2016

Quarterly information and turnover for the 1st quarter of 2016 09.05.2016 19.04.2016

Quarterly information and turnover for the 2nd quarter of 2016 31.08.2016 21.07.2016

2016 half-year results 29.08.2016

2016 half-year results and Analysts presentation 31.08.2016

Quarterly information and turnover for the 3rd quarter of 2016 07.11.2016 20.10.2016

58

Disclaimer

This presentation may contain forward-looking statements and information about the financial situation, operating

results, activities and development strategy of Eiffage. These statements and this information are based on

assumptions that may prove incorrect and that are subject to major risks and uncertainties. This information is

pertinent only on the day it was formulated. Eiffage assumes no responsibility to update this information or to revise

the statements on becoming privy to new information or because of future or other events taking place, subject to

applicable regulations in this matter. Additional information on factors that could influence the financial results of

Eiffage are contained in the document filed by the Group with the French financial markets supervisor (Autorité des

Marchés Financiers - AMF), which is available on the Group’s website www.eiffage.com or on request from the

company’s registered office.