Annual Report - ECB Reports/EC… · · 2017-10-192.2 Board Governance and Performance Agreements...

92

Annual Report

Transcript of Annual Report - ECB Reports/EC… · · 2017-10-192.2 Board Governance and Performance Agreements...

Annual Report

1

ECB Vision, Mission and Values 5 ECB Members of the Board 6 ECB Management 7 Board Chairperson’s Report 8 Chief Executive Officer’s Report 12

1 ECB Legislative Mandate 15 1.1 Electricity and Namibia Energy Regulatory Authority Bills 16

1.2 Gas Bill 16

1.3 Regulatory Instruments 16

2 Corporate Governance Matters 18 2.1 Corporate Governance Information 19

2.2 Board Governance and Performance Agreements 19

2.3 Board Meetings and Attendance 19

2.4 Board Committees 20

2.5 Board Appraisal 20

3 Legal 21 3.1 Legal Projects 22

3.2 Litigation 22

3.3 Future Outlook 22

4 Financial Planning, Monitoring and Reporting 23 4.1 Revenue 24

4.2 Investments 24

4.3 Financial operations 25

4.3.1 Operational Expenditure 25

4.3.2 Capital Expenditure 25

4.4 Internal Audit 25

4.5 Projects 25

4.6 Future Outlook 25

5 Human Resources (HR) 26 5.1 Organisational Structure (Current status) 27

5.2 Performance Management Implementation 27

5.3 Organisational Transformation 27

5.4 Future Outlook 28

5.4.1 Organisational design 28

5.4.2 Capacity 28

Contents

2

6 Corporate Communications & Stakeholder Management 29 6.1 Corporate Communications 30

6.2 Stakeholder Management 30

6.2.1 Public Awareness and Sensitisation 30

6.2.2 Corporate Social Responsibility 30

6.3 Future Outlook 30

7 Information Technology 31 7.1 Major Developments in IT Operations 32

7.2 IT Projects 32

7.3 Future Outlook 32

8 Economic Regulation 33 8.1 Tariffs 34

8.1.1 Bulk Tariffs 34

8.1.2 Distribution Tariffs 37

8.1.3 IPP Tariffs 38

8.1.4 Renewable Energy Feed-in Tariffs (REFIT) 38

8.2 Economic Regulation Projects 39

8.2.1 Transformation of the Single Buyer Market Model (SBMM) 39

8.2.2 Net Metering Rules 39

8.2.3 Review of NamPower Transmission Assets 39

8.2.4 Projects approved by Cabinet 39

8.3 Future Outlook 40

9 Technical Regulation 41 9.1 Quality of Supply Standards 42

9.2 Quality of Service Standards 42

9.3 DemandSideManagement(DSM)andEnergyEfficiency(EE)StudyReviewandUpdate 42

9.4 Technical Regulation Projects 42

9.4.1 Technical Compliance Audits 42

9.4.2 The National Integrated Resource Plan (NIRP) 42

9.4.3 NamPower (NP) Transmission Losses 42

9.4.4 Distribution Losses 42

9.4.5 Contestable Customers Project 43

9.4.6 Technical Regulatory Tools 43

9.4.7 Wiremen’s Licensing Project 43

9.4.8 Renewable Energy Grid Integration Study Project 43

9.4.9 Electrical Installation Standards Project 43

9.5 Future Outlook 43

10 Regulatory Support Services 44 10.1 LicensingStatusandUpdate 45

10.1.1 Licences Issued 45

10.1.2 Licences Amended 45

10.1.3 Licences Transferred 45 10.1.4 Licences Renewed 45

10.1.5 LicencesUnderReview 46

10.2 Independent Power Producers 46

10.2.1 Interim REFIT Programme 46

3

10.2.2 UnsolicitedIPPs 46

10.2.3 Solicited IPPs 46

10.3 Licensee Compliance 48

10.3.1 Licensee Compliance Audits Conducted 48

10.4 Customer Complaints 49

10.5 Industry Performance Analysis 49

10.5.1 NamPower Performance Review 49

10.5.1.1RevenueStreams,ProfitabilityandOperatingLeverage 49

10.5.1.2 NamPower Returns 50

10.5.2 NamPower Accounts Receivable and Solvency 51

10.5.3 NamPower Gearing / Cash Flow and Liquidity 52

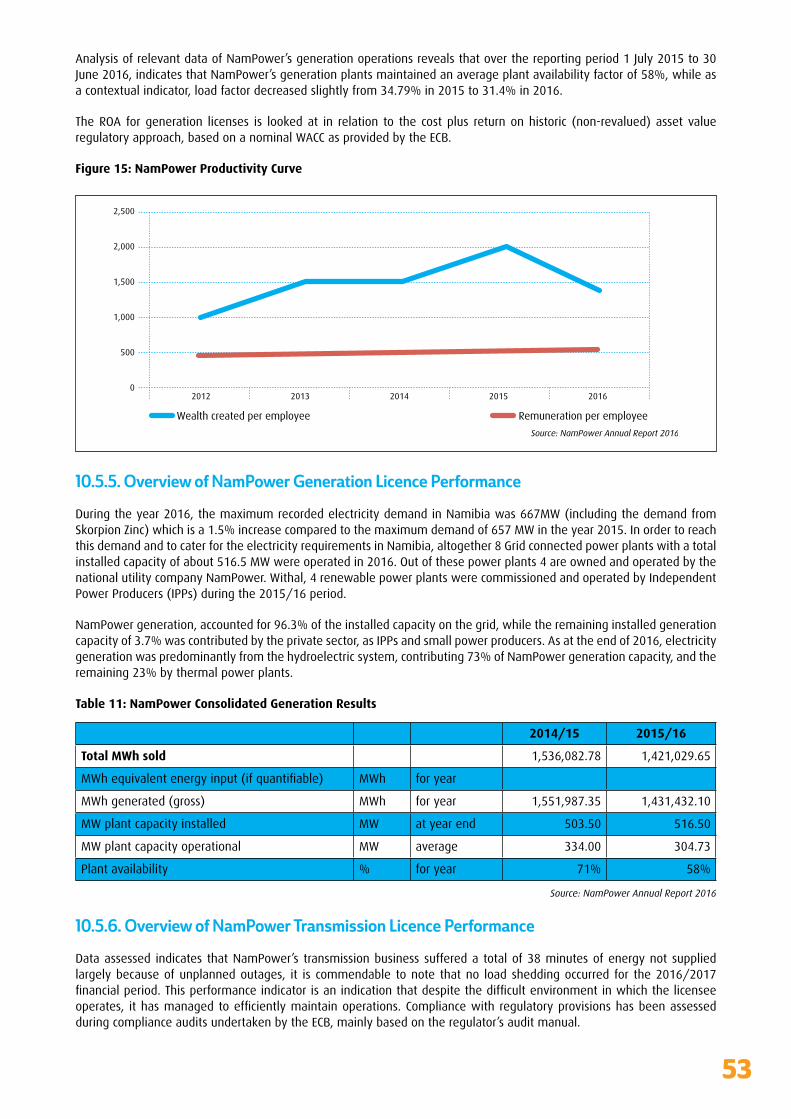

10.5.4 NamPowerProductivity&Efficiency 52

10.5.5 Overview of NamPower Generation Licence Performance 53

10.5.6 Overview of NamPower Transmission Licence Performance 53

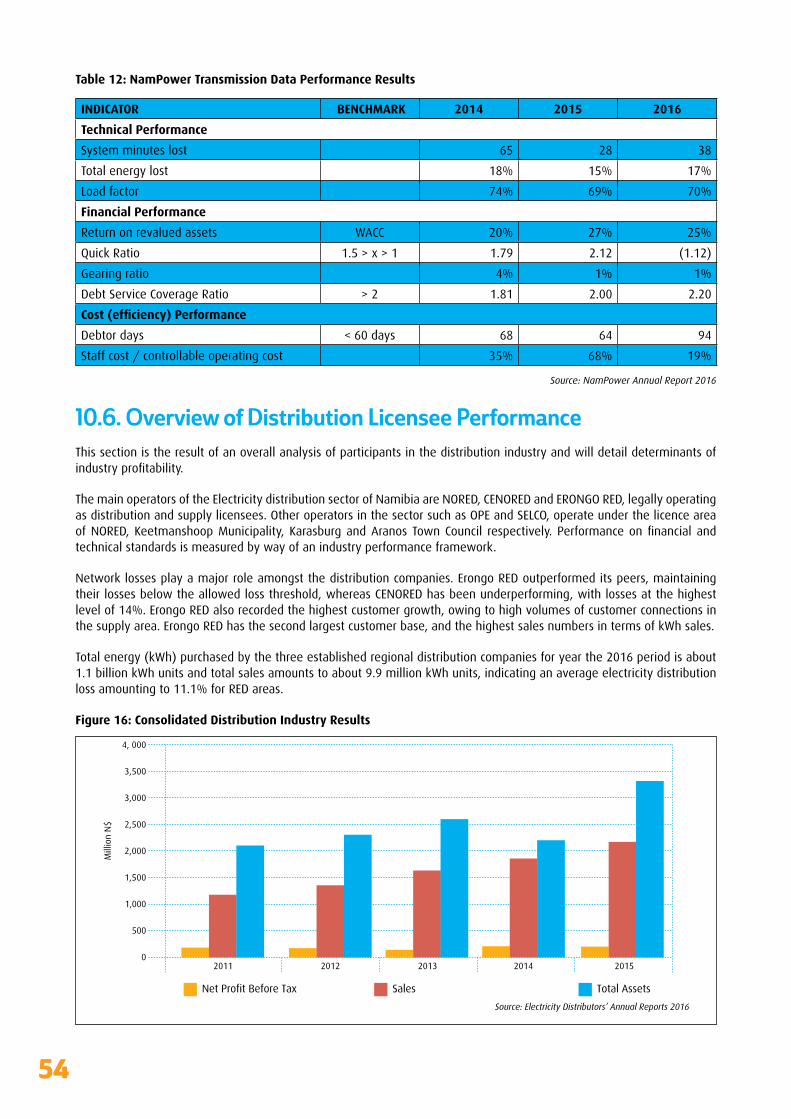

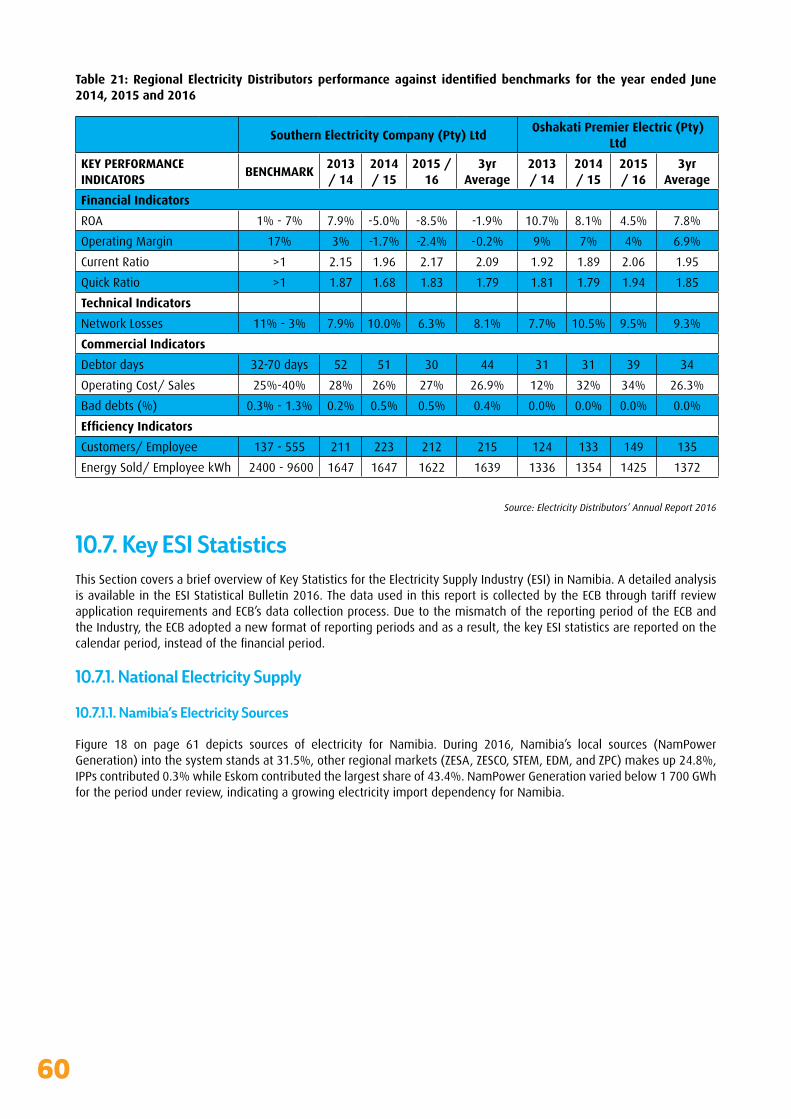

10.6 Overview of Distribution Licensee Performance 54

10.6.1 Erongo RED Performance Results 55

10.6.2 NORED Performance Results 57

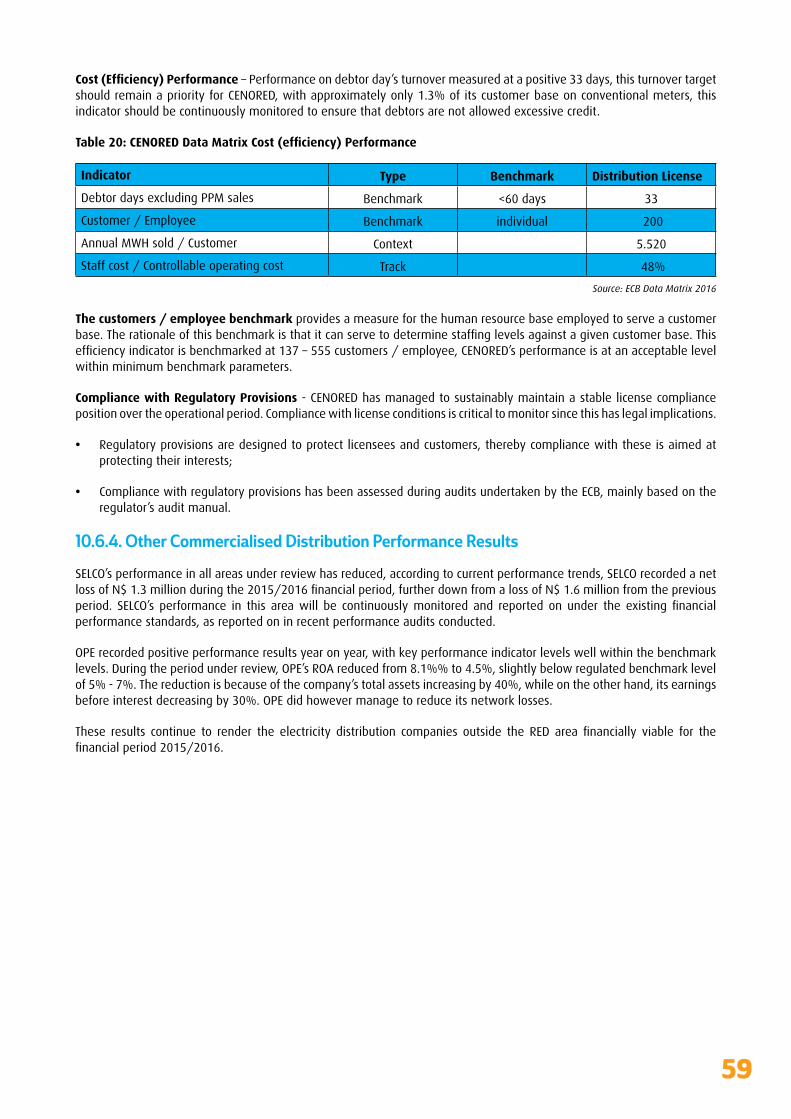

10.6.3 CENORED Performance Results 57

10.6.4 Other Commercialised Distribution Performance Results 59

10.7 Key ESI Statistics 60

10.7.1 National Electricity Supply 60

10.7.1.1 Namibia’s Electricity Sources 60

10.7.1.2 Annual Peak Demand vs Generation Capacity 61

10.7.1.3 Imports vs Exports of Electricity in Namibia 61

10.7.2 Electricity Distribution 62

10.7.2.1 Total Number of Customers in the Distribution Sector 62

10.7.2.2 Total Electricity Consumption 62

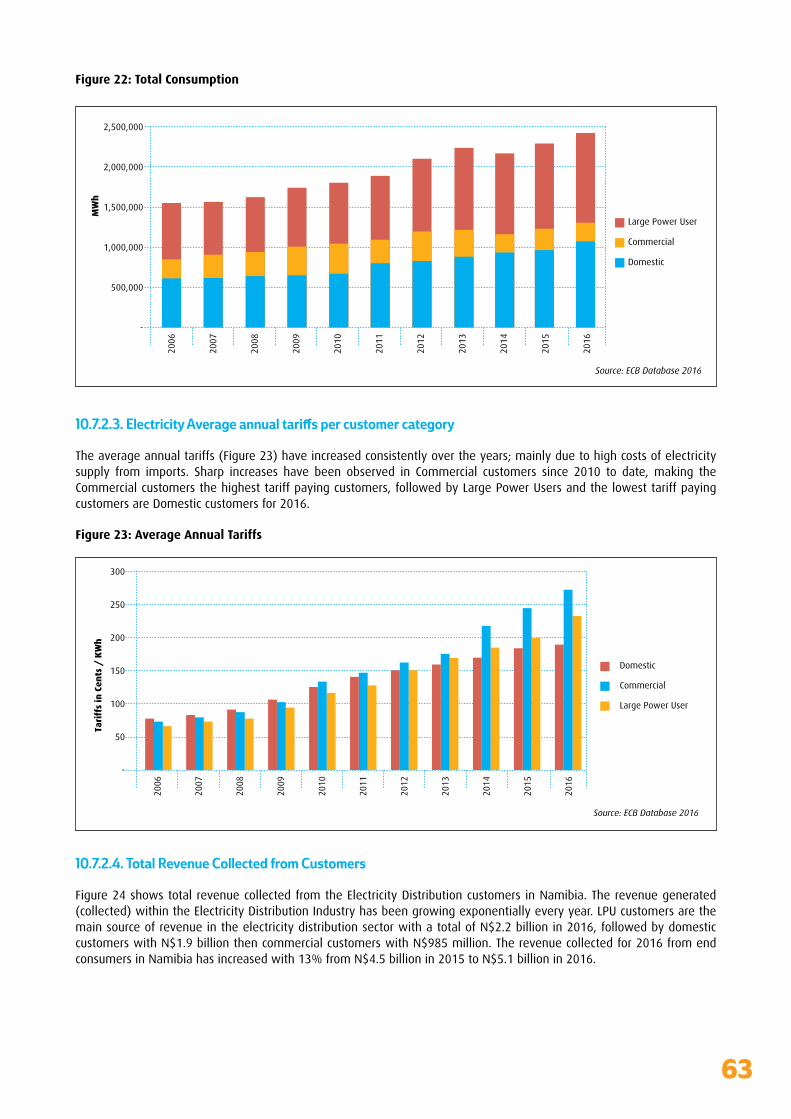

10.7.2.3 Electricity Average Annual Tariffs per Customer Category 63

10.7.2.4 Total Revenue Collected from Customers 63

10.7.2.5 Total Revenue as per Customer Category 64

10.8 Regulatory Support Services Projects 64

10.8.1 The Establishment of the Knowledge Hub 64

10.8.2 National Policies Developed and Finalised 64

10.8.3 IPP Policy 65

10.8.4 Renewable Energy Policy 65

10.8.5 National Energy Policy 65

10.8.6 EDI Reform 65 10.9 Future Outlook 65

11. Regional And International Activities 66 11.1 Regional Electricity Regulators Association of Southern Africa (RERA) 67

11.2 AfricanForumforUtilityRegulators(AFUR) 67

11.3 African Electrotechnical Standardisation Commission (AFSEC) and

International Electrotechnical Commission (IEC) 67

11.4 World Energy Council (WEC) 67

Annual Financial Statements 68

4

Figure 1: Revenue Composition 24Figure 2: ECB Bulk Tariff Review Process 34Figure 3: Share of Energy Source (Energy MWh and percentage) in 2016/17 35Figure 4: Percentage share energy local generation vs import 35Figure 5: Energy Cost component 36Figure 6: Average Generation Cost 36Figure 7: Projected NamPower electricity price path between 2016/2017 and 2022/2023. 37Figure 8: Total end-user tariff is composed of the components 37Figure 9: Average Distribution tariff increases and pre-paid tariff levels 38Figure 10: REFIT Tariffs 2016/2017 38Figure 11: NamPower Operating Leverage 50Figure 12: Operating Leverage 50Figure 13: NamPower ROA vs Benchmark 51Figure 14: NamPower Accounts Receivable & Solvency 51Figure 15: NamPower Productivity Curve 53Figure 16: Consolidated Distribution Industry Results 54Figure17:DistributionIndustryProfitability 55Figure 18: Namibia’s Electricity Sources 61Figure 19: Namibia Demand vs Generation Capacity 61Figure 20: Imports vs Exports 62Figure 21: Number of Customers 62Figure 22: Total Consumption 63Figure 23: Average Annual Tariffs 63Figure 24: Total Revenue 64Figure 25: Revenue as per Customer Category 64

Tables

Figures

Table 1: Overview of ESI Regulatory Instruments 16Table 2: Appointment dates and terms of the Board Members 19Table 3: Board Meeting Attendance 19Table 4: Membership of Board Committees (1 April 2016 – 31 March 2017) 20Table 5: Summary of ECB’s investments 24Table 6: Summary of Budget and Actual Financial Results 25Table 7: Interim REFIT and other IPPs 47Table 8: NamPower Key Statistics 49Table 9: Gearing and Liquidity 52Table 10: NamPower Cash Flow From Operations 52Table 11: NamPower Consolidated Generation Results 53Table 12: NamPower Transmission Data Performance Results 54Table13:RegionalElectricityDistributorsperformanceagainstidentifiedbenchmarks 56Table 14: Erongo RED Data Matrix Financial Performance 56Table15:ERONGOREDDataMatrixCost(efficiency)Performance 57Table16:NOREDperformanceagainstidentifiedbenchmarks 57Table17:CENOREDperformanceagainstidentifiedbenchmarks 58Table 18: CENORED Data Matrix Financial Performance 58Table 19: CENORED Data Matrix Technical Performance 58Table20:CENOREDDataMatrixCost(efficiency)Performance 59Table21:RegionalElectricityDistributorsperformanceagainstidentifiedbenchmarks 60

5

VisionTo be a leading regulator for achieving optimum viability and competition in the Namibian energy industry, whilst upholding the principles of

fairness, integrity and transparency.

MissionTo exercise control over and regulate the Namibian energy industry in a sustainable manner, in the interest of all stakeholders with regards to

price, quality, reliability, viability and safety.

ValuesProfessionalism

To conduct every task to a standard of excellence and to maintain the highest level of competence andpersonalintegrity/efficiencysoastoensurethesatisfactionofallstakeholders;

IntegrityTo be transparent, open, honest and fair in all dealings and communications with stakeholders,

AccountabilityTo be accountable and act in accordance with government policy and accept full responsibility

fordecisionsandactions;

InnovationTo innovate through continuous learning, knowledge-sharing and teamwork while delivering

excellentservice;and

SustainabilityTo ensure the endowment of Namibia’s energy resources are available to present and future

generations by considering our economic, environmental and social responsibility.

6

Board

From left to right

Mr. Gottlieb HindaChairperson

Ms. Panduleni Shimutwikeni Vice Chairperson

Ms. Helene Vosloo - Member

Ms. Evangelina Nailenge - Member

Mr. Albertus Basson - Member

Members of the

7

Seated from left to right

Ms. Foibe L. Namene Chief Executive Officer

Mr. Rojas Manyame General Manager Regulation

Mr. Johann Malan Manager Corporate Communication

and Legal Services

Ms. Mara Uazenga General Manager Finance & Admin

ECBManagement

Standing from left to right

Mr. Francois Robinson Manager Regulatory Support Services

Ms. Rachel BooisManager Finance

Mr. Pinehas Mutota Manager Economic Regulation

Dr. Maxwell Muyambo Manager Technical Regulation

Mr John Mukoya Manager Human Resources & Admin

8

ReportThe ECB has made big strides in coming to

grips with the challenges of a dynamic industry.

We responded by anticipating industry

trends bearing economic, technological,

environmental and social impact, and developed

regulatory tools and policies.

Board Chairperson’s

9

In my maiden Report as Chairperson of the Board of Directors of the ECB, I committed to the following:

• Securityofsupplythroughthecreationofanequitableandfairinvestmentenvironment;

• Faircompetitionintheindustry,leadingtoaffordabletariffsintheend;

• Benchmarkingandcontinuousreferencetointernationalbestpractices;

• Developmentandeffectiveimplementationofresponsiveregulatorytools;

• Strengthenindustrycompliancetoregulatorydirectives;and

• Adherence to the highest standards of corporate governance.

I also pledged to enhance:

• Licensee accountability on matters relating to safety, security and quality of supply and service;

• Sector sustainability through cost-reflective tariffs, compliance monitoring andenforcement;

• Internal as well as industry competency levels through supporting capacity building initiatives;and

• Participation of Namibians in the energy industry.

Havingreiteratedtheearlierpromise,Ireflectwithhumilitytheprogressmadeontheroadtravelled and the challenges encountered. Our dedicated efforts were towards a robust electricity industry that contributes to national growth, employment creation and poverty eradication. I wish to acknowledge with graciousness the role played by the Namibian Government, the electricity supply industry as well as end users in achieving such a feat. Through their active participation in the industry, including its regulation, these players called for pro-activeness in harnessing the full potential of the electricity industry in transforming the economy and the lives of ordinary Namibians.

The ECB has made big strides in coming to grips with the challenges of a dynamic industry. We responded by anticipating industry trends bearing economic, technological, environmental and social impact, and developed regulatory tools and policies.

To ensure that the ECB delivers on its mandate, some of these regulatory processes, procedures and systems have already come into effect. Linking these responses with the earlier promise, I wish to report on:

Security of supply through the creation of equitable and fair investment environment: TheECBempoweredthenationalelectricityutility,NamPower,tofulfillitsmandateandensurecontinued, uninterrupted supply of electricity, as well as honour its business obligations. The ECB decided that the bulk tariff for NamPower be increased to 16.71%. NamPower’s application was received on 4 February 2016. Stakeholder workshops were held where NamPower presented its application. Stakeholders were afforded the opportunity to present

It gives me immense pleasure to present the Annual Report for 2016/2017 on behalf of the Electricity Control Board (ECB).

10

their views, facts and evidence by giving written submissions. It is the intention of the ECB to, in future, conduct public

hearings. In this regard, the Public Hearing Rules are being finalised.

Fair competition in the industry, leading to affordable tariffs in the end: Private sector role in energy generation

is crucial, because it creates competition, reduces the funding burden on the Government, relieves NamPower’s borrowing

requirements and it also introduces generation technology traditionally outside the utility’s core functions. The ECB

allowed orderly development in the energy sector through the greater participation of Independent Power Producers

(IPPs), with a fair regulated return. This is in line with the commitment to put up a strong regulatory system which

allows for certainty, encourages international investment and confidenceinthelong-termreliabilityofsupplyrequiredby

industries, and lay down a transparent system that can be benchmarked against any similar system in the world.

Strengthen industry compliance to regulatory directives: The ECB operationalised its Market Performance Framework

which has been well received by regulated entities. On internal as well as industry competency levels through

supporting capacity building initiatives, the ECB continues to aid struggling licensees, while allowing cross-capacitation in

the industry where Memoranda of Agreements exist.

Licensee accountability on matters relating to safety, security and quality of supply and service: the ECB

implemented its Industry Performance and Maintenance Plan which increased its audits of licensees, who continue

to cooperate.

Sector sustainability through cost-reflective tariffs, compliance monitoring and enforcement: The ECB continues to keepNamibia on a cost-reflective tariff path,

and with no licensee worse-off. The ECB operates in a rapidly changing environment. Electricity has always been,

and will always be the catalyst for economic development. It is constantly evolving and continuously changing, with

potentially far-reaching consequences for the energy market. We therefore remain aware of the need to continuously reviewandimprovetheeffectivenessandefficiencyofour

functions as a Regulator.

Participation of Namibians in the energy industry: The ECB issued licenses to Namibian companies, some of which

participated in the Interim Renewable Energy Feed-In Tariffs (REFIT) Programme. These companies are listed on Table 7

on page 47 and 48. I am glad to report that of those 14 REFIT participants, two, namely Osona Energy and Hopsol Energy

successfully commissioned their plants during the period under review.

11

While we pride ourselves on these achievements, we remain cognisant of the complex challenges that must be conquered

in 2018 and beyond. The challenges of security of supply and investment in infrastructure, as well as affordability and access

to energy resources. We are also aware of the challenges facing the energy sector in the region. As part of the regional grouping,

we continue to play our part in the programmes and initiatives of the Regional Electricity Regulators Association of Southern Africa

(RERA), such as Cross-Border Energy Trading.

“These are the aspirations of our National Development Plans. Energy security is essential if we are to achieve the economic

growth target of NDP 4. Our role in realising this goal is pivotal, and we will draw all our internal and external resources to ensure

that it is achieved,” President Hage Geingob emphasised in his State of the Nation Address.

In conclusion, the year under review was challenging for the industry and the country. It is clear that we face a multitude of

challenges as we attempt to balance between the interests of the consumers and those of regulated parties. But we continue

moving forward to remain relevant and sustainable, adhere to internationally accepted regulatory principles of transparency,

neutrality, consistency and predictability, independence, accountability,integrityandefficiency.Weareconfidentthatwith

the support and guidance of the Minister of Mines and Energy, Hon. Obeth Kandjoze, we will effectively address the challenges

we face whilst striving towards achieving our Vision of being “a leading Regulator for achieving optimum viability and competition

in the Namibian energy industry, whilst upholding the principles of fairness, integrity and transparency.”

The success of the past year could not have been achieved without the dedication of Management and staff. We are fortunate to

have an excellent relationship. The envisaged transformation of the ECB into the Namibia Energy Regulatory Authority (NERA)

remains both exciting and challenging. The promulgation of both the Electricity Bill and the Namibia Energy Regulatory Authority

(NERA) Bill remains of utmost importance to the ECB.

While we pride ourselves on these achievements,

we remain cognisant of the complex challenges

that must be conquered in 2018 and beyond.

12

ReportChief Executive Officer’s

The current and future impact of technological

innovation on the energy sector, places the ECB

in a position where it will have to assist

utilities to align their ambitions with those of

their customers in a new energy future.

13

Regulators around the world have been challenged to proactively engage the future and ensuretheirrelevance.Thatchallengehasmainlybeenonfourfronts:technologicalinnovation;private sector participation, demand for stakeholder engagement and customer service and reliability and safety and security of supply, and climate or environmental concerns. Just like any regulator, the ECB has not been spared and had to dig deep during the reporting period. As a Regulator, it is expected of us to conduct business in a fair, just and equitable manner. It is therefore imperative that we place strong emphasis on individual and organizational integrity.

While the conversation on renewable energy came a long way, technological innovation has changed market and customer behaviour towards renewable energy. It has given impetus in Namibia to calls for the acceleration of renewable energy power to play its role in the country’s generation mix. The realisation led to a rush in rooftop system installations by customers. This development triggered the ECB to develop the Net Metering Rules that were promulgated in November 2016. The Rules have since been gazetted and implemented, and their effectiveness is being monitored.

The innovation in renewable technologies, especially solar photovoltaics (PV), has opened the possibilityofelectrificationof thoseruralcommunitiesin Namibia that are currently not served by the grid.

The shift in market and customer behaviour brought about by technological innovation in the electricity sector

challenges the ECB to proactively regulate and ensure its relevance. As highlighted in the Chairperson’s report we

operate in a rapidly changing environment and over a dynamic industry. It requires continuous review and improvement as

well as the development and implementation of regulatory methodologies, procedures, processes and systems. I am proud

to report that we have done that and will strive to continuously deliver on that promise. We have come a long way and ECB has

matured into an organization that truly subscribes to continuous improvement.

Opportunities in renewable energy, especially in solar and wind energy, attracted Independent Power Producers (IPPs) and other

investors. Private sector participation in the energy sector is crucial to the Namibian economy and bringing the much-needed Foreign Direct

Investment (FDI). The ECB commissioned the development of Namibia’s IPP Policy, and implementation of the Interim Renewable Energy Feed-in Tariffs(REFIT)Programme.FourteenIPPswereselectedonafirstcome–first

served basis to participate in the Interim REFIT Program. During the reporting period, three IPPs, namely Hopsol Power Generation (Grootfontein), Osona

Sun Energy and Metdecci Energy Investment were commissioned and now feedsintothenationalelectricitygrid.WeareconfidentthattheremainingIPPs

will achieve the same success during the 2017/2018 Financial Year.

This year’s highlights include the approval by Cabinet of the National Electricity Support Mechanism(NEST)andtheNationalSupportMechanismfor Improving theElectrificationofHouseholds in Un-Electrified Urban and Rural Areas Projects. The first mechanism aims toaddress the issue of affordability of electricity to low consuming households on a connection capacity below 15 Amps through a subsidized tariff. The National Support Mechanism for ImprovingtheElectrificationofHouseholdsinUn-ElectrifiedUrbanandRuralAreasProjectonthe other hand is intended to assist distribution licensees to substantially electrify households in urban and rural Namibia. The mechanism will complement the efforts of the Ministry’s rural electrificationprogram. The ECB is looking forward to the implementationof the twomechanisms.

The ECB developed a Strategic Plan for 2016 - 2021 which was approved by the Board and the Ministeron6September2016.ThestrategicobjectivesintheECBstrategicplanarespecific,measurable, realistic and timely achievable. These objectives are cross cutting over regulatory and organisational functions and remains the bedrock of our performance and Performance Management System. All our business decisions are informed by these strategic objectives.

14

We look forward to share progress on the implementation of the Plan as we continue to implement the Strategic Plan.

Thedemandforelectricitycontinuetorisesignificantly.Howeverthecountry’ssupplyfromitsown resources remain unbalanced with the demand not fully met by local supply. We are still dependent on imported electricity. Although this is a concern for the Regulator, we remain optimisticthatthefinalisationoftheNationalIntegratedResourcePlan(NIRP)anditsfinalimplementation will successfully address this challenge.

Another challenge remains the slow pace in the Electricity Distribution Industry (EDI) restructuring process following the EDI Summit held in October 2014. Various stakeholder consultations on how best to address the EDI Reform took place. These platforms were overwhelmingly in favour of the establishment of Southern RED (SORED). The ECB is hopeful that efforts towards the creation of SORED will bear fruits, and thereafter allow the Ministry of Mines and Energy and the Regulator to concentrate on the remaining RED, namely Central RED.

In line with the focus on public awareness, education and branding several workshops and initiatives on the Electricity Bill; IPP Policy and InvestmentFramework;RenewableEnergyPolicy;EnergyPolicy;InterimREFITProgramme;NetMeteringRules;SupportTariffMechanism;NationalIntegratedResourcePlan(NIRP) and Low Voltage Installation Wiring License amongst other were held.

As a responsible corporate citizen, we have contributed to various social and community projects to the value of N$ 250 000.00 and will ensure to deliver on this promise with the resources at our disposal.

Finally, the current and future impact of technological innovation on the energy sector, places the ECB in a position where it will have to assist utilities to align their ambitions with those of their customers in a new energy future. Such interventions will have to be geared towardsensuringthatutilitiesremaincost-reflectiveandtheirservicesrelevant.

As we continue our journey to being transformed into an Energy Regulator responsible for downstream gas pipelines and storage, downstream petroleum pipelines and storage in addition to electricity, we continue leveraging on our unique position and experience to bring about change in the industry. The ECB is fortunate to have access to expertise (internal or external) in the electricity regulation sector whose knowledge, expertise and experience is matched only by their dedication, passion and energy. It is through the dedication of each and every ECB employee that we are able to ensure that the ECB acquits itself excellently against the demanding targets and high expectations set by the industry, and that the ECB is able to deliver on its objectives and mandate.

We could also not have made the achievements without the support of the industry, the public, state organs and other stakeholders. I take this opportunity to thank all the individuals and institutions that supported us, to ensure that we effectively discharge our national duties of regulating the electricity industry. The ECB appreciates the efforts of all the stakeholders in the ESI to help transform the ECB in an efficient regulatorwhich drives changes in and responds to the demands of the industry.

15

MandateThe main objectives of the ECB are to

exercise control over and regulating the

provision, use and consumption of electricity

in Namibia, overseeing the efficient functioning

and development of the electricity industry and

security of electricity provision, amongst

others.

Electricity Control Board Legislative

1

16

The regulator of the electricity industry in Namibia, the Electricity Control Board (ECB), was created under the Electricity Act, Act No 2 of 2000, an Act which was repealed by the Electricity Act No. 4 of 2007. The main objectives of the ECB are to exercisecontroloverandregulatingtheprovision,useandconsumptionofelectricityinNamibia,overseeingtheefficientfunctioning and development of the electricity industry and security of electricity provision, amongst others. The Electricity Act also provides for a licensing system for operators in the electricity industry (generation, trading, transmission, supply, distribution, import and export) as well as for independent tariff regulation by the ECB. There were no changes to the ECB’s legislative mandate during 2016/2017. Net Metering Rules that regulate the generation of electricity by customer-generators and the export of surplus electricity generated into the grid were published in November 2016. The Rules are expected to become operational in May 2017.

1.1. Electricity and Namibia Energy Regulatory Authority Bills

The Electricity Act is currently under revision. The new Electricity Bill will introduce the required changes to give effect to theenvisagedestablishmentoftheNamibiaEnergyRegulatoryAuthority(NERA).UndertheNamibiaEnergyRegulatoryAuthority Bill, the ECB will be transformed into the Energy Regulatory Authority (NERA). NERA will, in addition to electricity, regulate downstream gas pipelines and storage, downstream petroleum pipelines and storage and renewable energy. Each sectorwillberegulatedinaccordancewithenergy-specificlegislation.

TheMinister’sfinalcommentsonthedraftElectricityandtheNamibiaEnergyRegulatoryAuthorityBillsareawaited.TheBillsareexpectedtobefinalisedinthe2017/2018reportingperiod.

1.2. Gas BillThe draft Gas Bill provides for the establishment of a regulatory and licensing framework for gas transportation and distributionnetworks,licensingforthedownstreamgasindustrytoensuresafety,efficiencyandenvironmentalresponsibilityin the transportation and distribution of natural gas, and to create a framework to encourage investment in the sector and to promote competition. During the reporting period, no progress was made on the development of the Gas Bill. Direction from the Ministry of Mines and Energy is awaited.

1.3. Regulatory Instruments

Table 1 below provides an overview of current and envisaged legal instruments by which the electricity supply industry (ESI) is regulated.

Table 1: Overview of ESI Regulatory Instruments

No Name Of Instrument Nature Status

A Legislation and Draft Bills

A1 Electricity Act, 4 of 2007 Legislation Promulgated

A2Namibia Energy Regulatory Authority Bill, 2017

Bill Draft

A3 Electricity Bill, 2017 Bill Draft

A4 Gas Bill, 2005 Bill Awaiting MME instructions on way forward

B Government Notices

B1Imposition of Levy on Electricity under Electricity Act

Notice by Minister in Government Gazette

ECB levy on electricity in operation

C Regulations

C1Electricity Regulations: Administrative, 2011

Regulations In operation

D Policies

17

No Name Of Instrument Nature Status

D1 National Integrated Resource Plan Approved by Board To be approved by Cabinet

D2 Renewable Energy Policy Approved by Board To be approved by Cabinet

D3 National Energy Policy Approved by Board To be approved by Cabinet

D4 IPP Policy Underdevelopment

D5 National Connection Charge Policy Policy Adopted by Cabinet in 2012

E ECB Rules, Codes, Standards and Guidelines

E1 Technical Rules, 2016 ECB Rules In operation

E2 Economic Rules, 2016 ECB Rules In operation

E3 Net Metering Rules, 2016 ECB Rules Promulgated on 15 November 2016

E4 Reseller Rules ECB Rules Underdevelopment

E5 REFIT Rules ECB Rules Underdevelopment

E6 Support Tariff Mechanism Mechanism

Support Tariff Mechanism approved by Cabinet in 2016. Implementation to start in Oshakati in 2017 with national roll-out in 2018

E7 ElectrificationSupportMechanism MechanismSupport Tariff Mechanism approved by Cabinet in 2016

E8 Transmission Grid Code ECB Code Awaiting promulgation

E9 Distribution Grid Code ECB Code Awaiting promulgation

E10 Safety Code ECB Code In operation

E11 Distribution Infrastructure Standards ECB Standards Awaiting promulgation

E12 Maintenance Guidelines ECB Guidelines Awaiting promulgation

E13 Quality of Supply and Service Standards ECB Standards Awaiting promulgation

E14 GuidelinesforFarmers’ElectricityUtilities ECB Guidelines Awaiting promulgation

F ECB Methodologies

F1 Generation Tariff MethodologyInternal ECB methodology

Approved by Board in 2001

F2 Transmission Tariff MethodologyInternal ECB methodology

Approved by Board in 2001

F3 Distribution Tariff MethodologyInternal ECB methodology

Approved by Board in 2001

G ECB Internal Procedures

G1 ECB Complaints Procedure Internal ECB procedure Approved by Board in 2010

G2 Mediation Procedures Internal ECB procedure Approved by Board in 2010

G3 Public Hearing Rules Internal ECB procedure ApprovedbyBoardin2010.Underreview.

18

MattersThe ECB is committed to complying with principles

of good corporate governance and

applicable legislation, most notably the

Electricity Act, Act No 4 of 2007 and the Public

Enterprises Governance Act, Act No 2 of 2006.

Corporate Governance

2

19

2.1. Corporate Governance Information

The ECB is committed to complying with principles of good corporate governance and applicable legislation, most notably the Electricity Act, Act No 4 of 2007 and the Public Enterprises Governance Act, Act No 2 of 2006.

In addition to the legislation mentioned above, the ECB applies the principles of the Corporate Governance Code for Namibia (NamCode) and its guidance on best practice principles in its operations insofar as applicable to the ECB.

The Board approved a Board Charter in 2010 and a Governance Framework in 2012. These documents have been reviewed duringthereportingperiod,andwillbesubmittedtotheBoardforapprovalinthenewfinancialyear.

2.2. Board Governance and Performance Agreements

In line with Sections 17 and 18 of the Public Enterprises Governance Act, a governance agreement between the portfolio MinisterandtheBoardwasfinalisedandexecuted.PerformanceagreementsbetweentheportfolioMinisterandindividualBoard members were also concluded.

2.3. Board Meetings and Attendance

Table 2: Appointment dates and terms of the Board Members

Board Member StatusDate of Current Appointment

Date of Expiry of Term

Current Term

Mr Gottlieb Hinda Chairperson 14 December 2015 13 December 2019 4 years

Ms Panduleni N. Shimutwikeni Vice-Chairperson 14 December 2015 13 December 2019 4 years

Mr Albertus Basson Member 14 December 2015 13 December 2019 4 years

Ms Evangelina Nailenge Member 14 December 2015 13 December 2019 4 years

Ms Helene Vosloo Member 14 December 2015 13 December 2019 4 years

Ms Foibe L Namene* Ex-officio member 1 June 2014 31 May 2019 5 Years

*In terms of Section 11(2)(a) of the Electricity Act, the ECB’s CEO is an ex officio member of the Board but has no right to vote.

In terms of Section 7(1) of the Electricity Act, the Board is required to meet at least once every three months. During the period covered by this Annual Report (1 April 2016 – 31 March 2017), the Board held four ordinary meetings.

The attendance at the Board meetings is as shown in Table 3.

Table 3: Board Meeting Attendance

ELECTRICITY CONTROL BOARD MEETINGS 2016/17

Board Member Status Meetings Attended

Mr Gottlieb Hinda Chairperson 4

Ms Panduleni N. Shimutwikeni Vice-Chairperson 4

Mr Albertus Basson Member 4

Ms Evangelina Nailenge Member 3

Ms Helene Vosloo Member 4

Ms Foibe L. Namene* CEO 4

*In terms of Section 11(2)(a) of the Electricity Act, the CEO is an ex- officio member of the Board but has no right to vote.

20

2.4. Board Committees

The Board established three Board Committees - the Regulation Committee, the Finance, Audit and Risk Committee, and the Human Resources and Remuneration Committee. Membership of Committees and attendance of meetings are set out intheTable4.Duringthefinancialyear,sixRegulationCommitteemeetingstookplace,andfoureachinrespectoftheHRand Remuneration Committee, and the Finance, Audit and Risk Committee.

Table 4: Membership of Board Committees (1 April 2016 – 31 March 2017)

Finance, Audit and Risk Committee

Regulation CommitteeHuman Resources and Remuneration Committee

Mr Albertus Basson (Chairperson)

Ms Evangelina Nailenge (Chairperson)

Ms Panduleni Shimutwikeni (Chairperson)

Ms Evangelina Nailenge Mr Gottlieb Hinda Mr Albertus Basson

Ms Helene Vosloo Ms Helene Vosloo Mr Gottlieb Hinda

Ms Foibe L Namene* Ms Foibe L Namene* Ms Foibe L Namene*

*The CEO is an ex- officio member of the Board Committees but has no right to vote.

2.5. Board Appraisal

Inlinewithcorporategovernancebestpractices,BoardandBoardCommitteeappraisalswilltakeplaceinthenewfinancialyear with the aim of enhancing the effectiveness of the Board.

21

LegalThe promulgation of the NERA and Electricity

Bills will require changes in the regulatory

framework. Following the outcome of the

market framework study that was commenced in

February 2017, market rules and attendant

licences will be developed in the new financial year.

3

22

3.1. Legal Projects

3.1.1. Drafting of NERA and Electricity Bills

Steady progress has been made on the drafting of the above Bills. The draft Bills were presented to the Minister on two occasions during the reporting

period, and his comments were incorporated in revisions of the Bills. The public was called upon to comment on the powers of the Minister in respect

of the clause on procurement of new generation.

Themainoutstandingissuestobefinalisedarethefinallicensingauthorityunder the Electricity Bill and the strengthening of the compliance enforcement

procedures under the two Bills. Proposals have been submitted to the Minister for consideration.

TheBillswillbefinalisedinthenewreportingperiod.

3.1.2. Farmer Schemes Project

Progress was made during the year on the Farmers’ Schemes Project. The finalprojectreport,draftfarmerschemesguidelines,amodelshareholders’

agreement and a model supply agreement were submitted. These documents willbefinalisedinthenextfinancialyear.

3.1.3. Enforcement Mechanisms Project

Little progress was made on the Enforcement Mechanisms Project. Enforcement procedures have been strengthened in the Electricity Bill

through the introduction of directives and administrative penalties. The Projectwillbefinalisedinthe2017/2018financialyear.

3.2. Litigation

Arandis Power lodged a review of the award of the 250MW tender to Xaris Energy by NamPower in the High Court of Namibia, which matter was heard duringthe2016/2017financialyear.ArandisPowerappealedthedecision.

The appeal has not yet been heard.

3.3. Future Outlook

The promulgation of the NERA and Electricity Bills will require changes in the regulatory framework. Following the outcome of the market framework

study that was commenced in February 2017, market rules and attendant licenceswillbedevelopedinthenewfinancialyear.

23

ReportingOnce transformed into NERA, alternative

funding sources will be needed for the additional

sectors of gas and petroleum. A study will

be carried out in the next financial year to explore

suitable funding models.

Financial Planning, Monitoring and

4

24

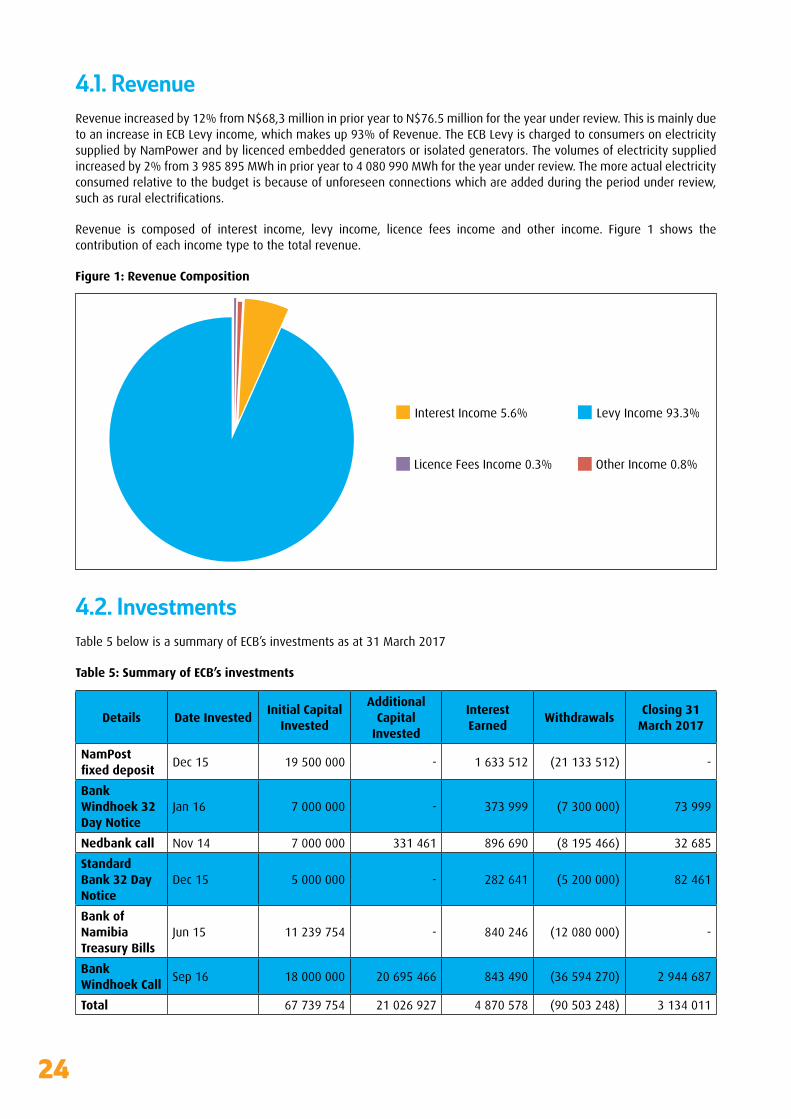

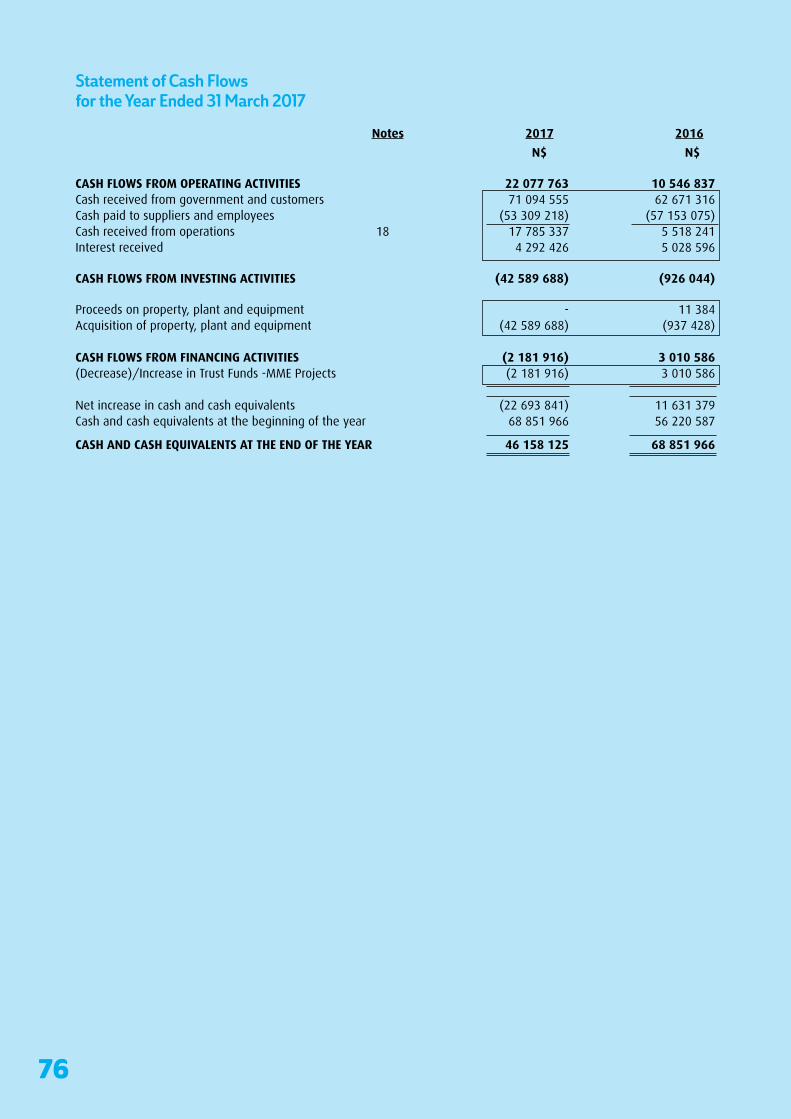

4.1. Revenue

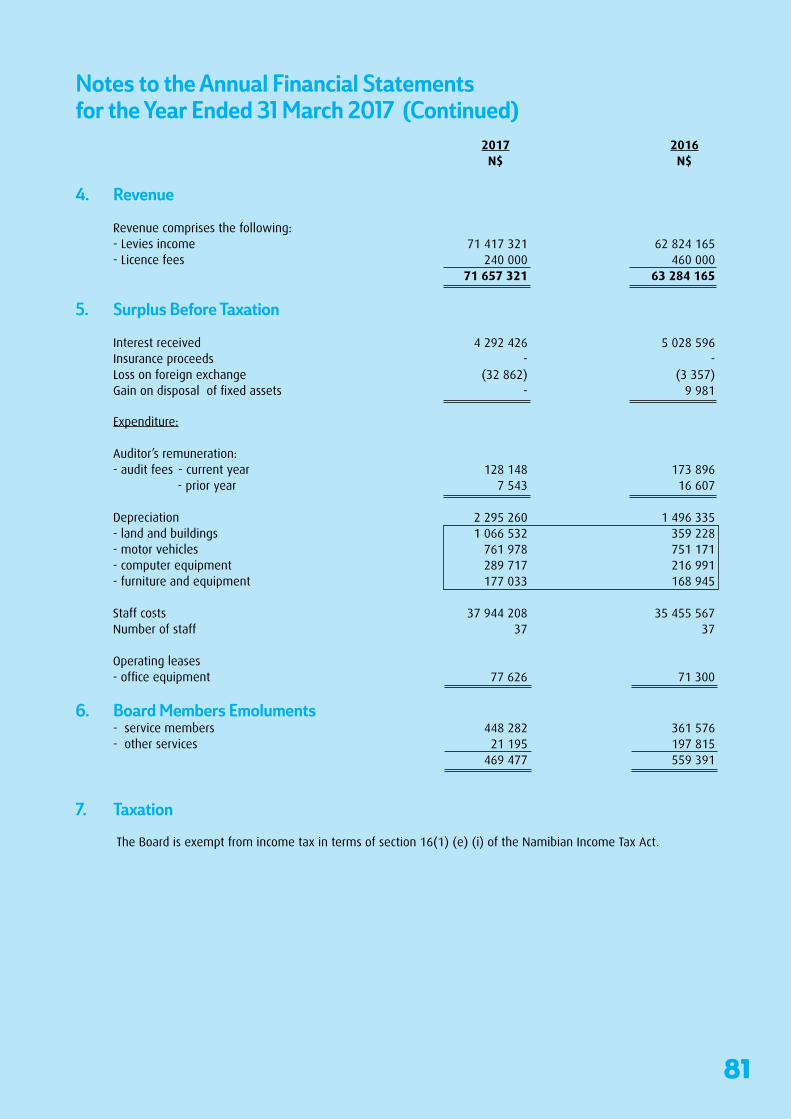

Revenue increased by 12% from N$68,3 million in prior year to N$76.5 million for the year under review. This is mainly due to an increase in ECB Levy income, which makes up 93% of Revenue. The ECB Levy is charged to consumers on electricity supplied by NamPower and by licenced embedded generators or isolated generators. The volumes of electricity supplied increasedby2%from3 985 895MWhinprioryearto4 080 990MWhfortheyearunderreview.Themoreactualelectricityconsumed relative to the budget is because of unforeseen connections which are added during the period under review, suchasruralelectrifications.

Revenue is composed of interest income, levy income, licence fees income and other income. Figure 1 shows the contribution of each income type to the total revenue.

Figure 1: Revenue Composition

4.2. InvestmentsTable 5 below is a summary of ECB’s investments as at 31 March 2017

Table 5: Summary of ECB’s investments

Details Date InvestedInitial Capital

Invested

Additional Capital

Invested

Interest Earned

WithdrawalsClosing 31

March 2017

NamPost fixed deposit

Dec 15 19 500 000 - 1 633 512 (21 133 512) -

Bank Windhoek 32 Day Notice

Jan 16 7 000 000 - 373 999 (7 300 000) 73 999

Nedbank call Nov 14 7 000 000 331 461 896 690 (8 195 466) 32 685

Standard Bank 32 Day Notice

Dec 15 5 000 000 - 282 641 (5 200 000) 82 461

Bank of Namibia Treasury Bills

Jun 15 11 239 754 - 840 246 (12 080 000) -

Bank Windhoek Call

Sep 16 18 000 000 20 695 466 843 490 (36 594 270) 2 944 687

Total 67 739 754 21 026 927 4 870 578 (90 503 248) 3 134 011

25

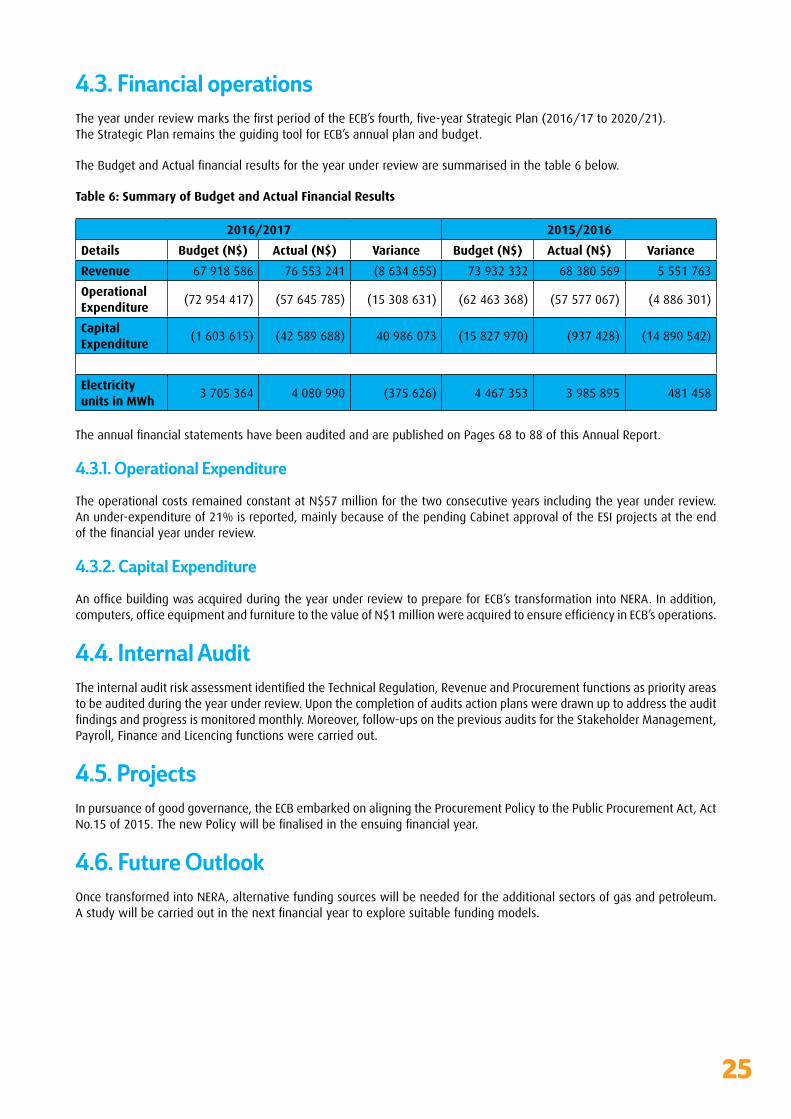

4.3. Financial operationsTheyearunderreviewmarksthefirstperiodoftheECB’sfourth,five-yearStrategicPlan(2016/17to2020/21).The Strategic Plan remains the guiding tool for ECB’s annual plan and budget.

TheBudgetandActualfinancialresultsfortheyearunderreviewaresummarisedinthetable6below.

Table 6: Summary of Budget and Actual Financial Results

2016/2017 2015/2016

Details Budget (N$) Actual (N$) Variance Budget (N$) Actual (N$) Variance

Revenue 67 918 586 76 553 241 (8 634 655) 73 932 332 68 380 569 5 551 763

Operational Expenditure

(72 954 417) (57 645 785) (15 308 631) (62 463 368) (57 577 067) (4 886 301)

Capital Expenditure

(1 603 615) (42 589 688) 40 986 073 (15 827 970) (937 428) (14 890 542)

Electricity units in MWh

3 705 364 4 080 990 (375 626) 4 467 353 3 985 895 481 458

TheannualfinancialstatementshavebeenauditedandarepublishedonPages68to88ofthisAnnualReport.

4.3.1. Operational Expenditure

The operational costs remained constant at N$57 million for the two consecutive years including the year under review. An under-expenditure of 21% is reported, mainly because of the pending Cabinet approval of the ESI projects at the end ofthefinancialyearunderreview.

4.3.2. Capital Expenditure

AnofficebuildingwasacquiredduringtheyearunderreviewtoprepareforECB’stransformationintoNERA.Inaddition,computers,officeequipmentandfurnituretothevalueofN$1millionwereacquiredtoensureefficiencyinECB’soperations.

4.4. Internal AuditTheinternalauditriskassessmentidentifiedtheTechnicalRegulation,RevenueandProcurementfunctionsaspriorityareastobeauditedduringtheyearunderreview.Uponthecompletionofauditsactionplansweredrawnuptoaddresstheauditfindingsandprogressismonitoredmonthly.Moreover,follow-upsonthepreviousauditsfortheStakeholderManagement,Payroll, Finance and Licencing functions were carried out.

4.5. ProjectsIn pursuance of good governance, the ECB embarked on aligning the Procurement Policy to the Public Procurement Act, Act No.15of2015.ThenewPolicywillbefinalisedintheensuingfinancialyear.

4.6. Future OutlookOnce transformed into NERA, alternative funding sources will be needed for the additional sectors of gas and petroleum. Astudywillbecarriedoutinthenextfinancialyeartoexploresuitablefundingmodels.

26

ResourcesFollowing the approval of the Performance

Management Policy, the new Performance

Management System (PMS) was rolled out

and implemented. The objective of the PMS is to

inculcate a performance driven culture in the ECB.

Human

5

27

5.1. Organisational Structure (Current status)The staff complement stands at 37. The ECB organisational structure comprises of the Officeof the Chief Executive wherein the corporate communication and legal / company secretariat services sections are embedded, and two departments, namely Regulation, and Finance and Administration. The Regulation Department is responsible for Regulation of the Electricity Supply Chain, namely the Generation, Transmission, Distribution and Supply, whereas the Finance and AdministrationDepartmentisresponsibleforthefinance,HR,administration,fleetmanagement,logistics, cleaning service, security, and maintenance of the ECB buildings.

During the period under review, the HR manual was reviewed and new key HR policies were developed and approved by the Board in September and November 2017 respectively. The objective of the policy development was to ensure that the organisation has sound HR systems in place, to ensure consistent decision making and compliance with the relevant labour legislations. The ultimate goal is to have sound employment relations, resulting in a great work environment.

5.2. Performance Management ImplementationFollowing the approval of the Performance Management Policy, the new Performance Management System (PMS) was rolled out and implemented. The objective of the PMS is to inculcate a performancedrivenculture intheECB.ThePMSisalignedtothefinancialyear.Thealignmentbetweenthefinancialcycleandtheperformancemanagementcycleprocessisimperative,asitdemonstratesthelinkbetweentheplannedperformanceobjectives/goals,financialresourcesand the measurable outcomes for the period under review - thus giving meaning to the intrinsic and extrinsic rewards paid to employees.

5.3. Organisational TransformationOwing to the imminent enactment of the National Energy Regulatory Authority bill (NERA Bill), the ECB is preparing for the transformation of the ECB from an electricity control board to the national energy regulatory authority.

28

Due to the anticipated transition to NERA, it was necessary for ECB to initiate an organisational change process. Thus, during the period under review the HR Department embarked upon the design / re-design of the organisational structure.

5.4. Future OutlookThe future outlook is categorised in the following components:

5.4.1. Organisational design

The expected change of organisational structure is due to the anticipated additional functions that will result in new roles. The staff complement is expected to increase two-fold. The said change is expected to affect the organisational design and span of control.

5.4.2. Capacity

The envisaged organisational change is expected to have a domino effect on both human and technological capacity. To address the pressure on the organisational capacity, the ECB therefore will embark upon a Business Process Review exercise. This exercise will analyse the current status of the business processes and develop and plan for new process that canimprovethebusinessprocessestoensureefficiencyandorganisationaleffectiveness.

To ensure a smooth transition, the ECB will embark upon the following projects:

• Conduct a COPS (Culture, Organisation, People, Systems) Analysis

• Develop a Transformation Blue Print

• Finalise the development and design or re-design of the organisational structure

• Develop a Change Management Strategy & Plan

• Develop and implement a Strategic Talent Management Plan

Based on the processes mentioned above, and in anticipation of such change we are developing a transformation blue print which will have organisational elements, systems, policy and procedures.

29

Corporate

Public awareness and sensitisation were

achieved through the use of mainstream print

and electronic media, routine audit inspections

as well as participation in local exhibitions such

as the Ongwediva Trade Fair and the

Windhoek Industrial and Agricultural Show.

Communications & Stakeholder Management

6

30

6.1. Corporate Communications

Corporate Communications and stakeholder engagements were more targeted during the period under review in line with the 2016 – 2021

Business and Strategic Plan. Emphasis was placed on communication with stakeholders through the Corporate Communications Strategy and

the Stakeholder Engagement Framework. The underlying principles of the two documents are transparency, clear, accurate and timely

communication, and meaningful participation of stakeholders in the regulation of the Namibian ESI. Such participation was evident during

the development of rules, codes and policies such as the National Energy Policy (NEP), Renewable Energy Policy (REP) and the Independent

Power Producers (IPP) Framework, as well as implementation of other ECB projects.

6.2. Stakeholder Management6.2.1. Public Awareness and Sensitisation

Public awareness and sensitisation were achieved through the use of mainstream print and electronic media, routine audit inspections as

well as participation in local exhibitions such as the Ongwediva Trade Fair and the Windhoek Industrial and Agricultural Show. Key messages

were communicated via the ECB website, media articles, informative advertorials,brochuresandleafletsaswellastheSPARKnewsletterand

Statistical Bulletin. The Bulletin, which is published annually, is based onactualdatacollectedbytheECBandvalidatedfromauditedfinancial

statements. The main data sources are the Regional Electricity Distributors (REDs), Local Authorities (LAs), NamPower, Namibia Statistics Agency,

Bank of Namibia as well as other external sources. The publication is compiled with government decision makers, REDs, LAs, investors,

scholars, researchers, planners and all other stakeholders in mind, to help them make informed decisions on the future of the Namibian ESI.

Feedback from these interventions were used to develop new messages for effective public awareness and sensitisation campaigns.

6.2.2. Corporate Social Responsibility

The ECB takes pride in its Corporate Social Responsibility contributions during the reporting period, which totalled over N$500 000. Of this

amount, more than N$360 000 was committed for bursaries while approximately N$230 000 benefitted individuals in need, welfare

organisations and tertiary institutions for research and benchmarking.

6.3 Future OutlookContinued efforts will be made for the structured and coherent

implementation of approved communications and stakeholder engagement instruments to maintain the desired rapport with

stakeholder groups, and in the process improved brand perception and understanding.

31

Technology

Going forward, the ECB’s IT section will endeavour

to increase the value derived from IT services

by the ECB by exploiting new technologies, and

reinforcing governance and risk management

practices.

Information

7

32

7.1. Major Developments in IT OperationsDuring the period under review the ECB’s IT security was strengthened with the implementation of a new Firewall that enhanced internal and external network access controls. In addition, a new server was purchased to improve application availability and responsiveness.

7.2. IT Projects7.2.1. Electronic Document and Records Management System (EDRMS)

The aim of this project is to establish a Filing Policy, develop a File Plan that meets the requirements of the National Archives of Namibia and to implement an Electronic Document and Records Management System (EDRMS).

A File Plan was developed and workshopped by ECB staff to solicit buy-in and ensure that it meets the needs of the variousECBfunctions.TheFilePlaniscurrentlybeingfine-

tuned before submission to the National Archives for approval.

7.2.2. ESI Investor Information Portal

The ESI Investor Portal will be a section of the ECB website that will serve as a repository for information required by potential

and current investors in the Namibian ESI. A list of documents and resources has been compiled and will be available on the website in thenextfinancialyear.

7.2.3. Customer Complaints Handling System (CCHS) Project

The outcome of this project is the creation of a web-based system that accepts external customer complaints as per the ECB’s Customer Complaints

policy. Furthermore, it will also assist ECB staff to track and resolve complaints received from the public regarding licensees. The system is currently being

piloted internally and new features are being added.

7.3. Future OutlookGoing forward, the ECB’s IT section will endeavour to increase the value derived

from IT services by the ECB by exploiting new technologies, and reinforcing governance and risk management practices.

33

Regulation

The Economic Regulation department continues

to monitor the impact of the tariff on the customer

and the economy at large and will strive always

to balance the interest of the supplier and the

customer.

Economic

8

34

8.1. TariffsTariff regulation is a core responsibility of the ECB. Tariffs are regulated in accordance with the White Paper on Energy Policy of1998,whichstatesthattariffsshouldbecostreflective,reflecttheLong-RunMarginalCost(LRMC)ofsupply,andbebased on sound economic principles.

The ECB applies a tariff methodology known as “cost plus” method in determining the electricity tariffs. This methodology implies that the revenue requirement (i.e. the cost) of a utility plus a regulated return (i.e. the Weighted Average Cost of Capital) are considered to determine the end-user tariff. The revenue requirement includes all allowable costs of the licensee to cover the cost of supply including the primary energy generation, energy imports, bulk purchases, operating and maintenance costs, customer service costs, overheads, asset-related costs and investment costs.

In reviewing and determining the electricity tariff levels, the ECB consults and takes into consideration the expectations of key stakeholders including the Government, private sector, licensees and consumers. The Regulator further considers many factors including National Developmental Plans, Government Policies and Cabinet directives such as the 2005 Cabinet decisionthatresolvedthatNamPowertariffsshouldreachandremaincostreflectivebytheyear2012.

Before approving a tariff, the Regulator assesses the likely impacts that tariffs may have on the end-consumers and the Namibian economy at large. Each licensee needs to have all its tariffs approved by the ECB Board.

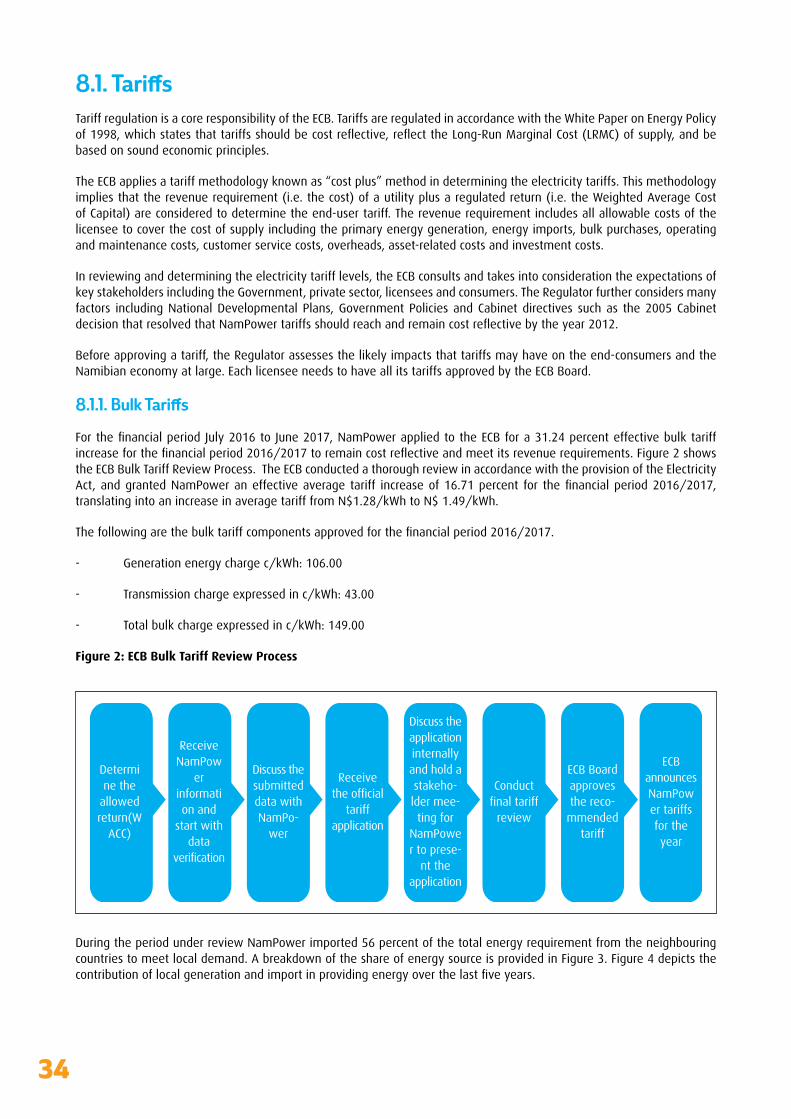

8.1.1. Bulk Tariffs

ForthefinancialperiodJuly2016to June2017,NamPowerappliedtotheECBfora31.24percenteffectivebulktariffincreaseforthefinancialperiod2016/2017toremaincostreflectiveandmeetitsrevenuerequirements.Figure2showsthe ECB Bulk Tariff Review Process. The ECB conducted a thorough review in accordance with the provision of the Electricity Act,andgrantedNamPoweraneffectiveaverage tariff increaseof16.71percent for thefinancialperiod2016/2017,translating into an increase in average tariff from N$1.28/kWh to N$ 1.49/kWh.

Thefollowingarethebulktariffcomponentsapprovedforthefinancialperiod2016/2017.

- Generation energy charge c/kWh: 106.00

- Transmission charge expressed in c/kWh: 43.00

- Total bulk charge expressed in c/kWh: 149.00

Figure 2: ECB Bulk Tariff Review Process

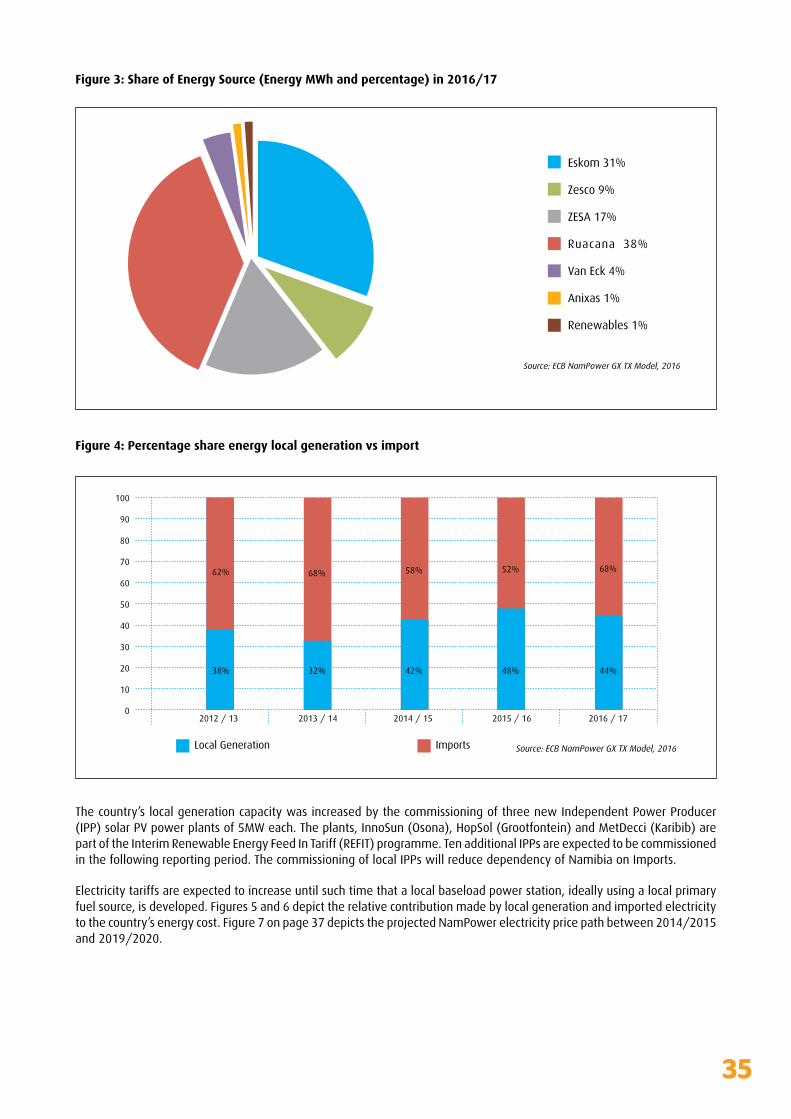

During the period under review NamPower imported 56 percent of the total energy requirement from the neighbouring countries to meet local demand. A breakdown of the share of energy source is provided in Figure 3. Figure 4 depicts the contributionoflocalgenerationandimportinprovidingenergyoverthelastfiveyears.

35

Figure 3: Share of Energy Source (Energy MWh and percentage) in 2016/17

Figure 4: Percentage share energy local generation vs import

The country’s local generation capacity was increased by the commissioning of three new Independent Power Producer (IPP) solar PV power plants of 5MW each. The plants, InnoSun (Osona), HopSol (Grootfontein) and MetDecci (Karibib) are part of the Interim Renewable Energy Feed In Tariff (REFIT) programme. Ten additional IPPs are expected to be commissioned in the following reporting period. The commissioning of local IPPs will reduce dependency of Namibia on Imports.

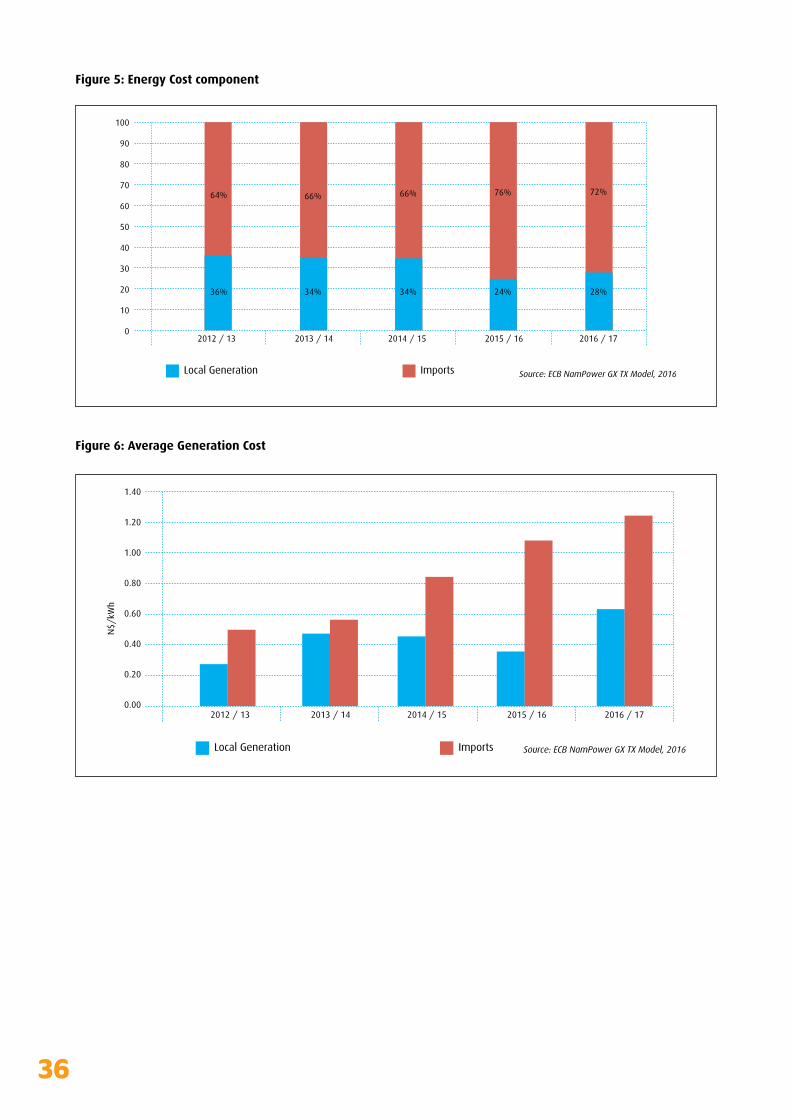

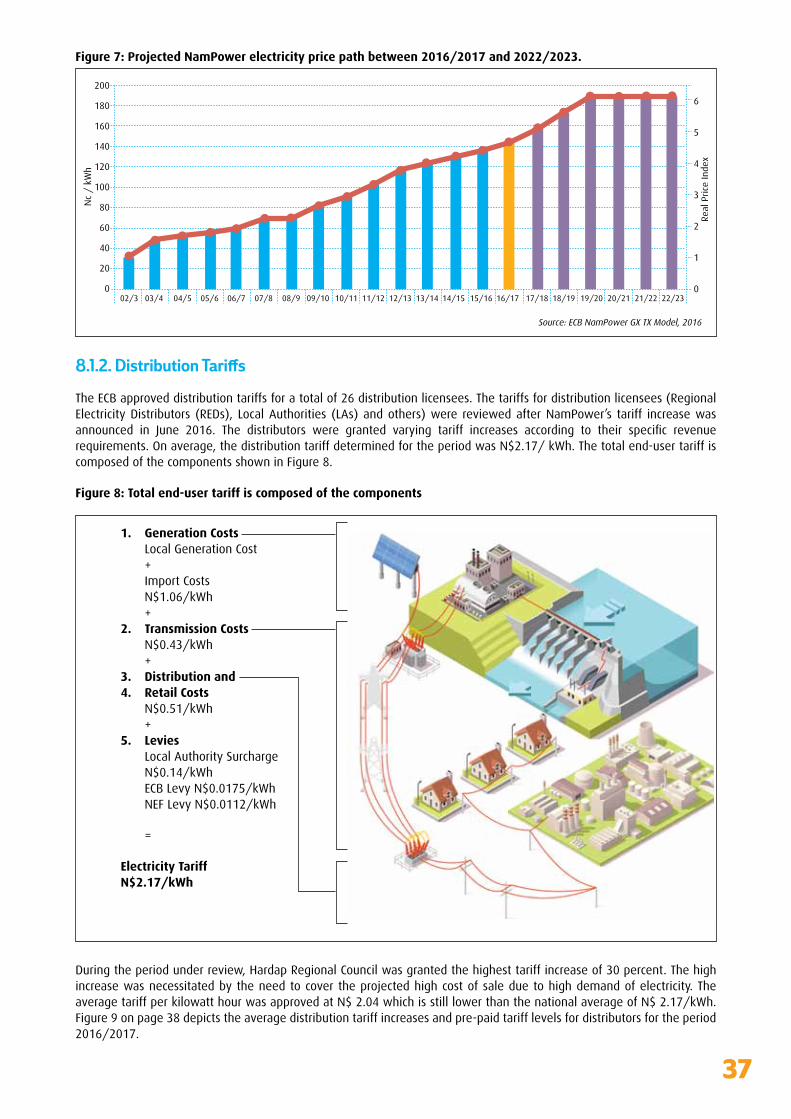

Electricity tariffs are expected to increase until such time that a local baseload power station, ideally using a local primary fuel source, is developed. Figures 5 and 6 depict the relative contribution made by local generation and imported electricity to the country’s energy cost. Figure 7 on page 37 depicts the projected NamPower electricity price path between 2014/2015 and 2019/2020.

36

Figure 5: Energy Cost component

Figure 6: Average Generation Cost

37

Figure 7: Projected NamPower electricity price path between 2016/2017 and 2022/2023.

8.1.2. Distribution Tariffs

The ECB approved distribution tariffs for a total of 26 distribution licensees. The tariffs for distribution licensees (Regional Electricity Distributors (REDs), Local Authorities (LAs) and others) were reviewed after NamPower’s tariff increase was announced in June 2016. The distributors were granted varying tariff increases according to their specific revenuerequirements. On average, the distribution tariff determined for the period was N$2.17/ kWh. The total end-user tariff is composed of the components shown in Figure 8.

Figure 8: Total end-user tariff is composed of the components

During the period under review, Hardap Regional Council was granted the highest tariff increase of 30 percent. The high increase was necessitated by the need to cover the projected high cost of sale due to high demand of electricity. The average tariff per kilowatt hour was approved at N$ 2.04 which is still lower than the national average of N$ 2.17/kWh. Figure 9 on page 38 depicts the average distribution tariff increases and pre-paid tariff levels for distributors for the period 2016/2017.

1. Generation Costs Local Generation Cost + Import Costs N$1.06/kWh +2. Transmission Costs N$0.43/kWh +3. Distribution and4. Retail Costs N$0.51/kWh +5. Levies Local Authority Surcharge N$0.14/kWh ECB Levy N$0.0175/kWh NEF Levy N$0.0112/kWh

=

Electricity TariffN$2.17/kWh

38

Figure 9: Average Distribution tariff increases and pre-paid tariff levels

8.1.3. IPP Tariffs

During the review period, the ECB Board approved tariffs for the following IPPs:

• Omburu 4.5MW

• OLC Arandis Solar Energy 3MW,

• GreeNam (Mariental 10MW) and (Kokerboom 10MW),

• Diaz Wind Power 44MW

8.1.4. Renewable Energy Feed-In Tariffs (REFIT)

During the period under review the applicable tariffs for the Interim REFIT programme are as per Figure 10 that illustrates the level of tariffs per technology.

Figure 10: REFIT Tariffs 2016/2017

39

8.2. Economic Regulation Projects

8.2.1. Transformation of the Single Buyer Market Model (SBMM)

In view of Namibia’s experiences in engaging with IPPs, the emergence of different market structures, funding requirements, significant cost reductions in photovoltaic and windtechnologies and the emergence of new storage technologies have prompted the ECB to re-examine the suitability of an exclusive Single Buyer Market Model for Namibia.

During the current period, the ECB commenced with the review of the current SBMM in light of the emerging market forces mentioned above. Based on the review, Namibia will either continue with the current model, albeit more vigorously enforced or possibly another model if deemed appropriate may be proposed. The project includes the development of market rules.

8.2.2. Net Metering Rules

The Rules are mainly intended to allow customers to reduce their electricity purchases from distribution networks through generating electricity for own consumption. Under the Net

Metering Rules, customers with small solar photovoltaic (solar PV) and micro-wind generators will be allowed to be connected to

the local distribution grids (less than 500kW). Net Metering Rules were promulgated in November 2016 and will become effective in

May 2017.

8.2.3. Review of NamPower Transmission Assets

The adopted cost-plus rate of return tariff methodology is based on the Weighted Average Cost of Capital (WACC) as the tariff methodology for theutilities.Thetransmissionundertaking(definedprincipallyasvoltage

levels of 66kV and above) is licensed to NamPower under the transmission license. The methodology allows a return on utility funded assets based on

the depreciated replacement value of transmission assets (substations and lines).ThetransmissionassetsarerevaluedbyNamPowerinfive-yearintervals

and the asset rate base is adjusted accordingly for the tariff by the Regulator.

The latest NamPower transmission asset revaluation was conducted in May 2011. NamPower conducted an asset revaluation for the period ended June 2015, for

inclusion in the tariff review 2017/2018 period.

The ECB reviewed NamPower’s revaluation report to ensure that the methodology has been applied correctly. The project has been completed.

8.2.4. Projects approved by Cabinet

The following projects were approved by Cabinet and implementation will commence in the following reporting period:

• National Electricity Support Tariff Mechanism (NEST)

• NationalSupportMechanismforImprovingElectrificationforNamibia(ESM)

• The NEST will be implemented on a pilot basis in Oshakati in 2017, followed by the planned national implementation in 2018.

40

8.3. Future Outlook

Namibia continues to import a large share of electricity needed, at times importing up to 70% of electricity requirements from the SADC region depending on the availability of water at the Ruacana Power Station. To address the situation several generation projects are planned in line with the National Integrated Resource Plan (NIRP).

During the period under review the power supply situation for Namibia and the Southern Africa region at large has been stable. This has been mainly attributed to new generation capacity added on the grid locally and regionally, as well as good rainfall received toward the end of 2016 for hydro power for Ruacana Power Station.

The Economic Regulation department continues to monitor the impact of the tariff on the customer and the economy at large and will always strive to balance the interests of the supplier and those of the customer. Electricity tariffs are expected toincreaseuntilsuchtimethatalocalbaseloadpowerstationisdeveloped,dependingonasufficientavailabilityofhydropower in the country complimented by thermal (coal) from the region. The ECB is optimistic that the tariff increases will be moderate in the coming years.

41

RegulationProgress was made in addressing critical issues

pertaining to network integrity, operational

capacity and safety concerns.

Technical

9

42

9.1. Quality of Supply Standards

During the period under review, the Quality of Supply Standards were submitted to the Legal Drafters for commencement of the promulgation process.

9.2. Quality of Service Standards

During the period under review, the Quality of Service Standards were submitted to the Legal Drafters for commencement of the promulgation process.

9.3. Demand Side Management (DSM) and Energy Efficiency (EE) Study Review and Update

The project was finalised and handed over to theNamibia Energy Institute (NEI) for complete takeover and implementationof specific recommendationsdocumented in

the project report, including establishment of a national DSM and EE Framework.

As an initial milestone, NEI presented an action plan which was accepted by the Minister for funding.

All matters pertaining to DSM and EE will fall under the custodianship of the NEI.

9.4. Technical Regulation Projects

9.4.1. Technical Compliance Audits

As per the audit plan, continued compliance monitoring and cooperation of keystakeholdersisexpectedtoenhanceimprovementofefficiency,safetyand

reliability of supply in the industry. Numerous technical compliance audits were conductedduringtheperiodunderreview.Asummaryofkeyfindingsforeach

audited entity is provided in the tracking sheet included in each report.

9.4.2. The National Integrated Resource Plan (NIRP)

Theprojectwasfinalisedincorporatingcommentsfromstakeholders.Boardapprovalwas secured and the presentation to the Minister of Mines and Energy was done in

December 2016. In March 2017, the Cabinet Committee on Trade and Economic Development (CCTED) endorsed the NIRP and made recommendations for submission to Cabinet for approval within a period of 4 months.

9.4.3. NamPower (NP) Transmission Losses

The outcome of the project on review of transmission losses recommended 8.62% as the value to be used in all NP tariff review processes. The 8.62% value was used for the 2016/2017 tariff review. It was concluded that for all future reviews, no value exceeding 8.62% will be accepted.

9.4.4. Distribution Losses

The project was discontinued before completion due to unforeseen challenges. It was concluded that the project would be resubmitted for tendering once all requisite data required for quantifying technical losses becomes available.

43

9.4.5. Contestable Customers Project

The economic impact analysis outcome recommended that it was not economically and financiallyjustifiablefortransmissioncustomerstomigratefromNamPowertotheREDs.TheECB informed all relevant stakeholders about the outcomes.

9.4.6. Technical Regulatory Tools

Information on the status of regulatory tools is summarised in table 1 under section 1.3 of the report. ECB engaged MME on the issue of delays experienced in the promulgation process. Going forward, it was agreed that the two parties would formulate concrete measures to fast track the promulgation process.

9.4.7. Wiremen’s Licensing Project

The Stakeholder Working Committee (SWC) finalised development of the draft Bill, draftRegulations and Guidelines. These draft documents will be submitted to the Ministry of Labour, Industrial Relations and Employment Creation (MLIREC) for promulgation before implementation, where necessary and applicable.

9.4.8. Renewable Energy Grid Integration Study Project

The ECB commissioned a project to assess the impact of grid integration of intermittent renewable energy. Following appointment of the consultant, an inception meeting was held in February 2017. The project is progressing well.

9.4.9. Electrical Installation Standards Project

The ECB advertised a tender to procure services of a consultant for developing Electrical InstallationStandards.Thetenderevaluationprocesswasfinalisedbythetenderevaluationcommittee which made recommendations for consideration by the Tender Committee and subsequently by the Board for approval before appointment of the Consultant.

9.5. Future OutlookProgress was made in addressing critical issues pertaining to network integrity, operational capacity and safety concerns. The commissioning of a network rehabilitation project in Maltahohe Village Council and the CENORED takeover of Okahandja Municipality Electricity Supply Business brought significant relief to concerned stakeholders. These developmentsbrought hope and anticipation to conclusively deal with the previously prevailing issues pertaining to safety, illegal connections and network maintenance.

44

Services

Regulatory Support Service will continue

to offer support to ESI stakeholders and

ensure that security of supply remains the

focus by ensuring that all interested investors

are afforded the same opportunity to enter the

sector.

Regulatory Support

10

45

10.1. Licensing Status and UpdateAs per the Electricity Act, Section 17, no person may establish or conduct any generation, trading, transmission, supply, distribution, import, or export of electricity without a licence (unless formally exempted under the Act).

During the year under review, the ECB issued a total of 3 new licences, of which 2 licences were issued for generation and 1 licence was issued for supply. The ECB amended 4 supply licences, transferred 1 licence, renewed 13 licences and 4 licenses are under review.

10.1.1. Licences issued

• AVENG Water Treatment (Pty) Ltd

• OLC Arandis Solar Energy (Pty) Ltd

• Mariental Bioenergy (Pty) Ltd

10.1.2. Licences amended

• NamEnergy Solar (Pty) Ltd,

• Xaris Energy (Pty) Ltd,

• Arandis Power (Pty) Ltd,

• Kokerboom Solar Power (Pty) Ltd,

10.1.3. Licences transferred

• Cenored-Okahandja Electricity Joint Venture

10.1.4. Licences renewed

• City of Windhoek

• Luderitz Town Council

• Keetmanshoop Municipality

• Gobabis Municipality

• Mariental Municipality

• Karasburg Town Council

• Okahandja Municipality

• Rehoboth Town Council

• Namibia Airport Company

• NamPower Distribution

• Namdeb Diamond Corporation

• Ongopolo Mine (Otjihase)

• RoshSkor Township

46

10.1.5. Licences under review

• Alten Solar Power (Hardap) Holdings (Pty) Ltd

• Maerua Mall (Pty) Ltd

• Phase Two Properties (Pty) Ltd

• Grove Mall (Pty) Ltd

10.2. Independent Power Producers

Introduction of IPPs in the Namibian Electricity Supply Industry (ESI) is crucial for adding to the generation capacity of Namibia in a sustainable manner. The ESI in Namibia needs to keep pace with the changing energy requirements and regional and global developments in the power sector including the global nature of the IPP industry.

Namibia has a well-developed ESI and the reforms introduced by the Government of Namibia, including the establishment of REDs, places the Namibian ESI at par with some of the best-run power systems internationally. NamPower, as the Government-owned utility, continues to be the dominant player in Namibia’s generation sector. Currently, NamPower acts as a single buyer with the responsibility for both indigenous power generation as well as power trading with the neighbouring countries. As a single buyer, NamPower is currently responsible for negotiating all Power Purchase Agreements (PPAs) and Transmission Connection Agreements (TCAs) with any power generators in the country. The review of the current SBMM is eminent to attract more IPPs into the Namibian ESI.

Current developments in the ESI see the role of IPPs increasing. NamPower recently signed Power Purchase Agreements (PPAs) with a number of individual companies that plan to develop some 70 MW of renewable power under the interim REFIT programme. Other additional IPP generation projects are also in the pipeline.

10.2.1. Interim REFIT Programme

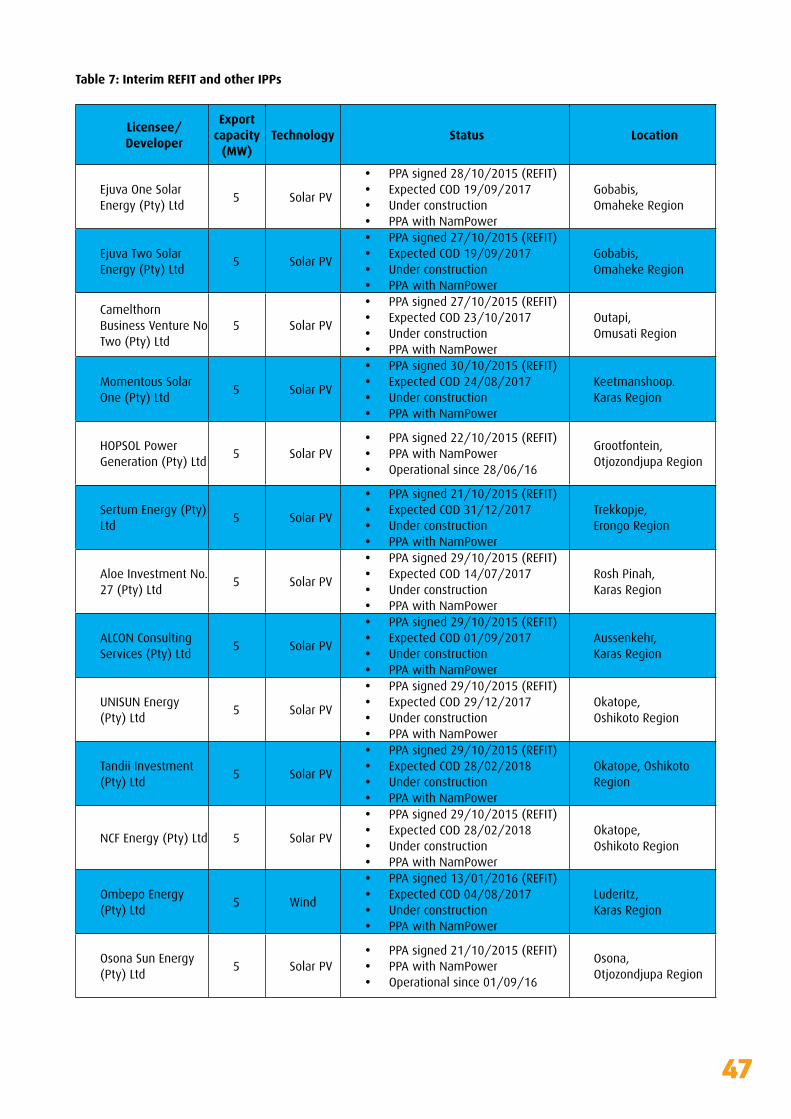

The REFIT programme is designed to accelerate investment in renewable energy technologies by offering long-term contracts to renewable energy Independent Power Producers (IPPs).

An installed generation capacity of 70 MW is expected to be added through the interim REFIT programme which translates to 14 IPPs (included in Table 7 below) each generating up to 5 MW. The 14 IPP projects will invest a combined total amount of approximately N$1.6 billion of foreign direct investment into the electricity sector and ultimately into the Namibian Economy.

10.2.2. Unsolicited IPPs

Several IPPs made unsolicited proposals to the ECB since 2007.

Since the country was in dire need of electricity generation capacity during the time, a number of licences were issued to prospective investors.

Many of the licenced companies could not bring their projects to fruition, and as a result the licences lapsed.

The companies that managed to meet the ECB’s requirements are provided on Table 7 below.

10.2.3. Solicited IPPs

NamPower as well as some of the REDs acquired the services of the IPPs through a solicited (tendering) process.

This solicitation process was mainly done through requests for proposals (RFP), or requests for quotations (RFQ), and requests for sealed bids, which were made public through advertising.

The companies that were awarded projects through the solicited means approached the ECB and were licenced as per the Electricity Act.

47

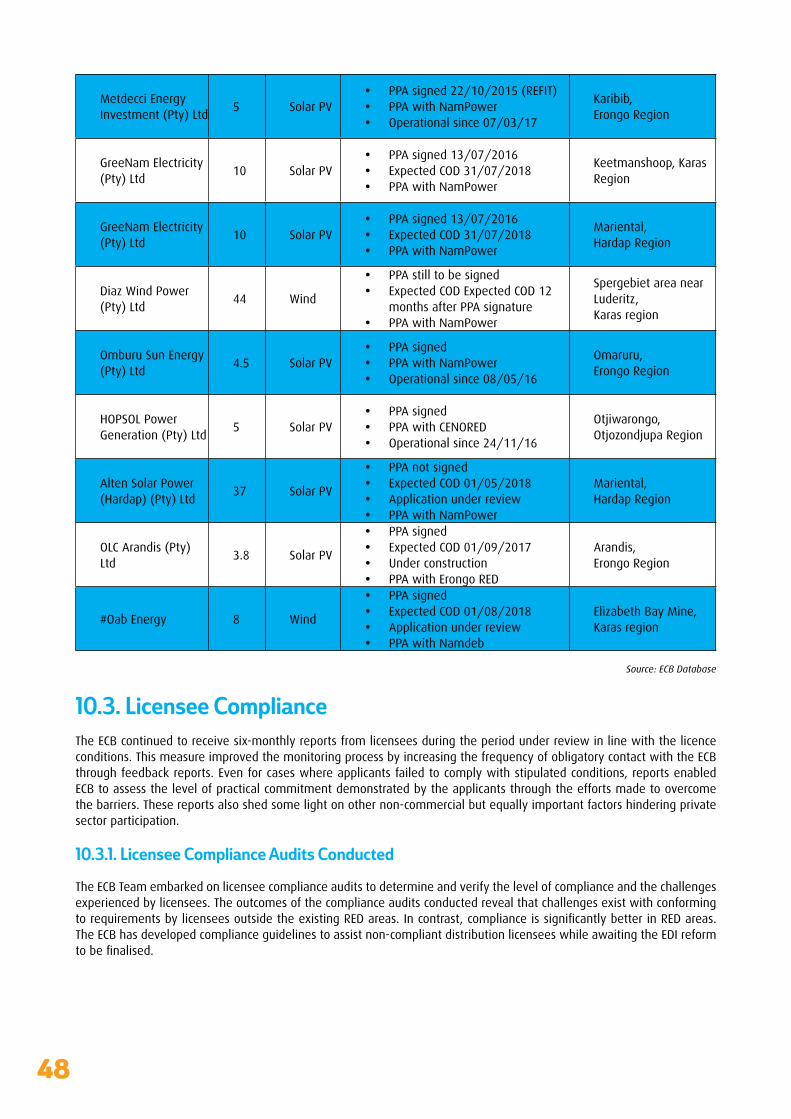

Table 7: Interim REFIT and other IPPs

Licensee/Developer

Export capacity

(MW)Technology Status Location

Ejuva One Solar Energy (Pty) Ltd

5 Solar PV

• PPA signed 28/10/2015 (REFIT)• Expected COD 19/09/2017• Underconstruction• PPA with NamPower

Gobabis,Omaheke Region

Ejuva Two Solar Energy (Pty) Ltd

5 Solar PV

• PPA signed 27/10/2015 (REFIT)• Expected COD 19/09/2017• Underconstruction• PPA with NamPower

Gobabis,Omaheke Region

Camelthorn Business Venture No Two (Pty) Ltd

5 Solar PV

• PPA signed 27/10/2015 (REFIT)• Expected COD 23/10/2017• Underconstruction• PPA with NamPower

Outapi,Omusati Region

Momentous Solar One (Pty) Ltd

5 Solar PV

• PPA signed 30/10/2015 (REFIT)• Expected COD 24/08/2017• Underconstruction• PPA with NamPower

Keetmanshoop.Karas Region

HOPSOL Power Generation (Pty) Ltd

5 Solar PV• PPA signed 22/10/2015 (REFIT)• PPA with NamPower• Operational since 28/06/16

Grootfontein,Otjozondjupa Region

Sertum Energy (Pty) Ltd

5 Solar PV

• PPA signed 21/10/2015 (REFIT)• Expected COD 31/12/2017• Underconstruction• PPA with NamPower

Trekkopje,Erongo Region

Aloe Investment No. 27 (Pty) Ltd

5 Solar PV

• PPA signed 29/10/2015 (REFIT)• Expected COD 14/07/2017• Underconstruction• PPA with NamPower

Rosh Pinah,Karas Region

ALCON Consulting Services (Pty) Ltd

5 Solar PV

• PPA signed 29/10/2015 (REFIT)• Expected COD 01/09/2017• Underconstruction• PPA with NamPower

Aussenkehr,Karas Region

UNISUNEnergy(Pty) Ltd

5 Solar PV

• PPA signed 29/10/2015 (REFIT)• Expected COD 29/12/2017• Underconstruction• PPA with NamPower

Okatope,Oshikoto Region

Tandii Investment (Pty) Ltd

5 Solar PV

• PPA signed 29/10/2015 (REFIT)• Expected COD 28/02/2018• Underconstruction• PPA with NamPower

Okatope, Oshikoto Region

NCF Energy (Pty) Ltd 5 Solar PV

• PPA signed 29/10/2015 (REFIT)• Expected COD 28/02/2018• Underconstruction• PPA with NamPower

Okatope,Oshikoto Region

Ombepo Energy (Pty) Ltd

5 Wind

• PPA signed 13/01/2016 (REFIT)• Expected COD 04/08/2017• Underconstruction• PPA with NamPower

Luderitz,Karas Region

Osona Sun Energy (Pty) Ltd

5 Solar PV• PPA signed 21/10/2015 (REFIT)• PPA with NamPower• Operational since 01/09/16

Osona,Otjozondjupa Region

48

Metdecci Energy Investment (Pty) Ltd

5 Solar PV• PPA signed 22/10/2015 (REFIT)• PPA with NamPower• Operational since 07/03/17

Karibib,Erongo Region

GreeNam Electricity (Pty) Ltd

10 Solar PV• PPA signed 13/07/2016• Expected COD 31/07/2018• PPA with NamPower

Keetmanshoop, Karas Region

GreeNam Electricity (Pty) Ltd

10 Solar PV• PPA signed 13/07/2016• Expected COD 31/07/2018• PPA with NamPower

Mariental,Hardap Region

Diaz Wind Power (Pty) Ltd

44 Wind

• PPA still to be signed • Expected COD Expected COD 12

months after PPA signature• PPA with NamPower

Spergebiet area near Luderitz,Karas region

Omburu Sun Energy (Pty) Ltd

4.5 Solar PV• PPA signed • PPA with NamPower• Operational since 08/05/16

Omaruru,Erongo Region

HOPSOL Power Generation (Pty) Ltd

5 Solar PV• PPA signed • PPA with CENORED• Operational since 24/11/16

Otjiwarongo, Otjozondjupa Region

Alten Solar Power (Hardap) (Pty) Ltd

37 Solar PV

• PPA not signed • Expected COD 01/05/2018• Application under review• PPA with NamPower

Mariental, Hardap Region

OLC Arandis (Pty) Ltd

3.8 Solar PV

• PPA signed • Expected COD 01/09/2017• Underconstruction• PPA with Erongo RED

Arandis,Erongo Region

#Oab Energy 8 Wind

• PPA signed • Expected COD 01/08/2018• Application under review• PPA with Namdeb

Elizabeth Bay Mine,Karas region

Source: ECB Database

10.3. Licensee Compliance

The ECB continued to receive six-monthly reports from licensees during the period under review in line with the licence conditions. This measure improved the monitoring process by increasing the frequency of obligatory contact with the ECB through feedback reports. Even for cases where applicants failed to comply with stipulated conditions, reports enabled ECB to assess the level of practical commitment demonstrated by the applicants through the efforts made to overcome the barriers. These reports also shed some light on other non-commercial but equally important factors hindering private sector participation.

10.3.1. Licensee Compliance Audits Conducted

The ECB Team embarked on licensee compliance audits to determine and verify the level of compliance and the challenges experienced by licensees. The outcomes of the compliance audits conducted reveal that challenges exist with conforming torequirementsbylicenseesoutsidetheexistingREDareas.Incontrast,complianceissignificantlybetterinREDareas.The ECB has developed compliance guidelines to assist non-compliant distribution licensees while awaiting the EDI reform tobefinalised.

49

10.4. Customer Complaints

In accordance with the Electricity Act, licensees are obligated to apply best practices to ensure high quality customer service levels. In addition to the licence conditions, the ECB uses the Quality of Supply and Service Standards, Safety Code, Grid Code, Technical and Economic Rules and maintenance guidelines as instruments to monitor and evaluate customer service levels across the industry.

During the period under review, the ECB received and investigated complaints from ESI consumers in the country. The complaints received involved issues ranging from tariffs, billing, power outages and to new connections.

10.5. Industry Performance Analysis

Thepurposeof the industryperformanceanalysis is tohighlight thefinancialperformanceof the regulatedElectricitySupplyIndustry(ESI)entitiesforthefinancialyearended30June2016,therebytoascertaintheperformanceoflicenseesagainst the set industry benchmarks.

Thissectionfocusesextensivelyonfigurespublishedintheauditedfinancialstatementsfromthelicensees,whereuponan analysis of trends for comparison with regulatory benchmarks is carried out.

The Namibian electricity sector continued to import more than the local supply of the energy requirement during the reporting period. This put a strain on the operating margins of the sector, resulting in exposure to rising electricity tariffs. Despite these challenges, the Namibian electricity sector is experiencing steady growth prospects across the value chain.

This section further elaborates on factors affecting performance as well as inherent characteristics of the Namibian electricity sector.

Secondary data collected on licensees continues to be the basis of the performance assessment of the licensees for the period of review. The provision of consistent and credible data remains a key challenge for most entities in the Namibian ESI, and as a result, the ECB will increasingly make use of benchmarking tools as the availability of accurate and consistent data becomes more and more apparent across the entire spectrum of the Electricity Supply Industry.

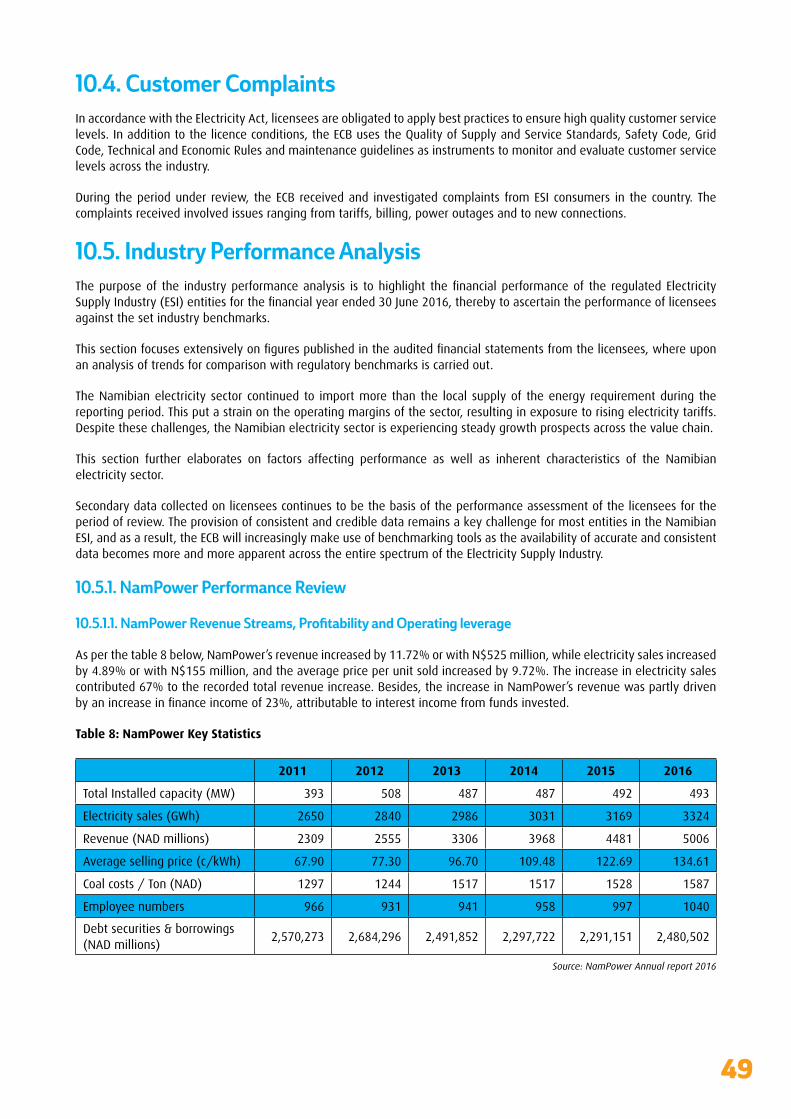

10.5.1. NamPower Performance Review

10.5.1.1. NamPower Revenue Streams, Profitability and Operating leverage

As per the table 8 below, NamPower’s revenue increased by 11.72% or with N$525 million, while electricity sales increased by 4.89% or with N$155 million, and the average price per unit sold increased by 9.72%. The increase in electricity sales contributed 67% to the recorded total revenue increase. Besides, the increase in NamPower’s revenue was partly driven byanincreaseinfinanceincomeof23%,attributabletointerestincomefromfundsinvested.

Table 8: NamPower Key Statistics