Annual Report and Financial Statements - Al Rayan Bank | Islamic banking …€¦ · ·...

40

Annual Report and Financial Statements 31 December 2006 Registered number 4483430

Transcript of Annual Report and Financial Statements - Al Rayan Bank | Islamic banking …€¦ · ·...

Annual Report and Financial Statements31 December 2006Registered number 4483430

Chairman’s statement 1

Report of the Sharia’a Supervisory Committee 3

Directors’ report 4

Statement of directors’ responsibilities in respect

of the Annual Report and the financial statements 7

Independent Auditors’ Report to the

Members of Islamic Bank of Britain PLC 8

Income statement 9

Balance sheet 10

Statement of changes in equity 11

Statement of cash flows 12

Notes to the financial statements 13

Contents

Chairman’s Statement

I am pleased to present the Annual Report of the IslamicBank of Britain PLC (the ‘Bank’) for the financial year ended31 December 2006.

In 2006 the emphasis has been on developing theBank’s business to build on our achievements in 2005.These efforts resulted in:

• The number of customers increased by 120% to 30,814 (2005: 14,023)

• Number of accounts more than doubled to 51,032 (2005: 25,403)

• Deposits grew by 76% to £83.9m (2005: £47.7m)

• Total customer financing (personal and commercial) advanced by 131% to £10.4m (2005: £4.5m)

A number of key initiatives contributed tothis performance:

• We opened two branches, Manchester in January 2006 and East Ham in November 2006. The Bank now has a total of eight branches.

• We strengthened our distribution capabilities in line with our strategic objectives by launching Internet Banking in September 2006.

• We launched our Commercial Property Finance product in the third quarter of 2006, having worked pro-actively with Her Majesty’s Revenue and Customs to incorporate the Diminishing Musharaka contract in the Finance Bill 2006.

• We enhanced our relationship management team to develop business from Private Clients, SME’s,and Charities.

• We launched Home financing in conjunction with other partners in Islamic Banking.

• We upgraded our debit cards to MasterCard’s Maestro platform which now allows our customers access to a global network of ATMs and pointsof sale.

In June 2006, the Chairman of the FSA, in the presenceof the Chancellor of the Exchequer, cited Islamic Bank ofBritain PLC as a positive initiative and expressed theview that the UK was proud to have supported theintroduction and development of the first Sharia’a-compliant bank in the Western world.

The loss for the year ended 31 December 2006 was£8.8m (2005: £6.4m). This represents an increase inoperating income of 36% to £3m, offset by operatingcosts which increased by 32% to £11.4m andimpairment charges of £0.45m. The growth in incomewas lower than plan mainly due to the delay in thelaunch of Commercial Property Finance which wasdependent on the Finance Bill 2006. This becameeffective in July 2006. The growth in costs representsplanned costs associated with the extension of ourdistribution capability, both branches and internet, andthe introduction of new products aimed at the businesssector. Staff costs were up by £1m, due to an increasein average staff numbers from 102 to 144. Depreciationand amortisation charges were up by £0.2m. Increasesin occupancy, IT costs and volume related costs, werepartly offset by lower professional and legal costs.Credit criteria were further tightened in December 2005taking into account our arrears experience and theincreased level of arrears on unsecured finance inthe UK.

1

We continue to be optimistic about the prospects forIslamic Banking in the UK. The Bank now has acomprehensive range of products and offers a realalternative to conventional banking. In 2007 we aim tobuild on our customer base and focus on furtherstrengthening our service delivery channels. We areworking with external providers to develop newMurabaha finance products in the consumer market.Although our main focus remains in the UK we are alsoengaging in dialogue with interested parties aiming tolaunch Islamic Banking services into otherEuropean countries.

In February 2007 we were the principal sponsor of theinaugural UK Muslim Power 100 awards whichrecognised the significant positive impact the Muslimpopulation contributes in the social and economicspheres. The event highlighted the £31bn annualcontribution to GDP made by the UK Muslim communityand recognised achievers in business, education,professional services, health, and the arts. The event,which was well received, was attended by a wide rangeof individuals and businesses and attracted glowingnational press coverage.

In December 2006, Michael Hanlon retired from hisposition as Managing Director. I would like to thank himfor his contribution and work in establishing Islamic Bankof Britain and setting up a sound infrastructure to takethe Bank into the future. I would like to welcome GerryDeegan to our Board as Managing Director. Gerrycomes with 35 years of experience in retail banking anda strong track record of delivery in his previous roles. Iwould also like to extend my thanks to Ashraf Piranie,who resigned as Finance Director in March 2007 topursue another career opportunity. Ashraf worked

diligently to enhance both the profile and development ofthe Bank’s product range and distribution capability.Additionally, I would like to welcome Robert Owen asSenior Independent Non-Executive Director to the Boardreplacing Chris Davis who resigned in February 2007.Robert brings 35 years of UK financial servicesexperience to our Board. I would like to thank Chris forhis positive contribution to the Bank.

I would like to thank Islamic Bank of Britain’sshareholders for their continued support andcommitment to the Bank. I would also like to thankAbdul Rahman Abdul Malik, who resigned as Chairmanin March 2007, for his guidance and leadership that wereessential in establishing Islamic Bank of Britain as thefirst full service Sharia’a-compliant bank in Europe.Finally, I would like to thank the Bank’s management andstaff for their hard work and dedication.

I am pleased the Bank was awarded, for a secondsuccessive year, the ‘Best Islamic Bank in Europe’award. We are now looking forward to the next phase ofour development with optimism and vigour. May Allahgrant us success in our endeavours.

Mohsen MoustafaChairman

2

5

Report of the Sharia’a Supervisory Committee

In the name of Allah, the Most Gracious, the Most Merciful

Report of the Sharia’a Supervisory Committee

To the Shareholders of the Islamic Bank of Britain PLC For the period from 1 January 2005 to 31 December 2005

In compliance with the Terms of Reference of our Committee, we submit the following report:

We have reviewed the documentation relating to the products entered into by the Islamic Bank ofBritain PLC for the period from 1 January 2005 to 31 December 2005. According to management,the funds were raised and invested in this period on the basis of agreements approved by us.

Therefore, based on the report of our representative and representations received from management,in our opinion the transactions and the products entered into by the Company during the periodfrom 1 Januar y 2005 to 31 December 2005 are in compliance with the Islamic Sharia’a rules andprinciples and also the specific directives, rulings and guidelines issued by us.

We beg Allah the Almighty to grant us all the success and straightforwardness.

Dr Abdul Sattar Abu Ghuddah Chairman of the Sharia’a Supervisory Committee

22 March 2006

Report of the Sharia’a Supervisory Committee

(In the name of Allah, the Most Gracious, the Most Merciful)

To the Shareholders of the Islamic Bank of Britain PLC

For the period from 1 January 2006 to 31 December 2006

In compliance with the Terms of Reference of the Bank’s Sharia’a Supervisory Committee, we submitthe following report:

We have reviewed the documentation relating to the products and transactions entered into by theIslamic Bank of Britain PLC for the period from 1 January 2006 to 31 December 2006.

According to Management, the Sharia’a Compliance Officer of the Bank and documents evidencing thefact, the funds were raised and invested in this period on the basis of agreements approved by us.

Therefore, based on the report of our representative and representations received from management, inour opinion the transactions and the products entered into by the Bank during the period from 1 January2006 to 31 December 2006 are in compliance with the Islamic Sharia’a rules and principles and fulfil thespecific directives, rulings and guidelines issued by us.

We beg Allah the Almighty to grant us all the success and straightforwardness.

Dr Abdul Sattar Abu GhuddahChairman of the Sharia’a Supervisory Committee

01 March 2007

3

Directors’ report

The directors present their report and financial statementsfor the year ended 31 December 2006.

Principal ActivitiesIslamic Bank of Britain PLC (the ‘Company’) was incorporated with the intention of becoming thefirst independent Islamic bank in the United Kingdom established and managed on a whollySharia’a compliant basis providing banking services to Muslims in the United Kingdom and otherparts of Europe, and received authorisation in August 2004 by the Financial Services Authority(FSA). The first branch was opened on Edgware Road London on 22 September 2004.

A further seven branches have subsequently been opened: Small Heath Birmingham, Leicester,Whitechapel London, Southall London, Alum Rock Birmingham, Manchester and East HamLondon. A direct telephone and postal banking capability is also in place and during the currentyear Internet Banking has been launched to further compliment the Branch network.

In addition, the product offering was further developed in 2006 and at the end of the year the Bankoffers a range of Sharia’a compliant banking solutions for both individual and business customersincluding current accounts, savings accounts, high net worth treasury placement accounts andconsumer and business financing. During the year the major new product launches were theCommercial Property Finance and Home Finance products.

Financial ResultsFor all periods up to and including the 5 month period ended 31 December 2004, Islamic Bank ofBritain PLC prepared its financial statements in accordance with UK Generally AcceptedAccounting Principles (‘UK GAAP’). From 1 January 2005, Islamic Bank of Britain PLC elected toprepare its financial statements in accordance with International Financial Reporting Standards asadopted by the EU (‘adopted IFRSs’). Consequently, within these financial statements bothcurrent year and prior year comparatives have been prepared in accordance with InternationalFinancial Reporting Standards as adopted by the EU (‘adopted IFRSs’).

The financial statements for the year ended 31 December 2006 are shown on pages 9 to 35. Theloss for the year amounts to £8,833,253 (2005: £6,449,507).

The directors do not recommend the payment of a dividend (2005: £nil).

Enhanced Business ReviewDetails of the Company’s performance and prospects are given within the Chairman’s statementon page 1.

Details of the financial and operational risk management objectives and policies and theCompany’s indicative exposure to financial risk are given in note 4 on page 21.

4

Directors’ report (continued)

Directors and directors’ interestsThe directors who held office during the year were as follows:

Mr Abdul Rahman Abdul Malik (Chairman)^

Mr Abdulaziz Al-Khulaifi+

Mr Christopher Davis*+^

Mr David Gates (Resigned as director 26 April 2006)

Mr Michael Hanlon (Resigned as director 31 December 2006)

Mr Mohsen Moustafa*^

Mr Ashraf Piranie (also Company Secretary)

Mr Shabir Randeree*+

Mr Ahmad Salam (Resigned as director 26 April 2006)

*Denotes member of Audit Committee+Denotes member of Remuneration Committee^Denotes member of Nomination Committee

Subsequent to the reporting date the following changes have occurred; Mr Gerry Deeganappointed as director on 26 January 2007, Mr Robert Owen appointed as director (and will also bea member of the Audit Committee) on 12 February 2007, Mr Christopher Davis resigned asdirector on 12 February 2007. Mr Abdul Rahman Abdul Malik resigned as Chairman on 8 March2007 and Mr Mohsen Moustafa appointed as Chairman on the same date. Mr Abdul RahmanAbdul Malik will resign as director with effect from 31 March 2007. Mr Ashraf Piranie will resign asdirector and company secretary with effect from 31 March 2007.

The directors who held office at the end of the financial year had the following interests in theordinary shares of the Company according to the register of directors’ interests:

Class of share Interest at end Interest at startof year of year

Mr Abdul Rahman Abdul Malik Ordinary 1,000,000 1,000,000(Chairman)

Mr Shabir Randeree Ordinary 30,058,013 30,058,013(held in the name of DCDLondon & Mutual PLC)

None of the other directors who held office at the end of the financial year had any disclosableinterest in the shares of the company.

According to the register of directors’ interests, no rights to subscribe for shares in or debenturesof the company were granted to any of the directors or their immediate families, or exercised bythem, during the financial year.

5

Directors’ report (continued)

Significant shareholdersThe following shareholders had interests in the ordinary shares of the Company in excess of 3%as at 31 December 2006 (comparatives only shown if holding as at 31 December 2005 wasgreater than 3%):

2006 % 2005 %

HRH Sheikh Hamad Bin Khalifa Bin Hamad Al Thani 17.37 17.37Qatar International Islamic Bank 14.63 17.37HE Sheikh Thani Bin Abdulla Bin Thani Jasim Al Thani 8.69 8.69Hanover Nominees Ltd 8.24 8.57DCD London & Mutual PLC 7.17 7.17Qatar Islamic Insurance 4.93 -HSBC Global Custody Nominee (UK) Ltd 982409 4.64 3.10HSBC Global Custody Nominee (UK) Ltd 813259 3.83 -Securities Services Nominees Ltd 2710000 3.72 -N.Y. Nominees Ltd 3.40 -

Sharia’a Supervisory Committee members The Sharia’a Supervisory Committee members during the year were as follows:

Dr. Abdul Sattar Abu Ghuddah (Chairman)Sheikh Nizam YacoubyMufti Abdul Kadir Barkatullah

The report of the Sharia’a Supervisory Committee for the year is set out on page 3.

Creditor payment policyThe Company seeks to settle trade invoices in line with their payment terms. The amount due tothe Company’s trade creditors as at 31 December 2006 represented 19 days (2005: 20 days)average daily purchases of goods and services calculated in accordance with the Companies Act1985, as amended by Statutory Instrument 1997/571.

Political and charitable contributionsThe Company made no political contributions during the year (2005: £nil). Donations to UKcharities amounted to £1,720 (2005: £8,250). Payments in 2006 include £1,090 of fees andcharges relating to late payment on personal finance accounts that were paid to charity inaccordance with product terms as agreed with the Sharia’a Supervisory Committee. A furtherpayment of £4,000 is to be made in 2007 in respect of similar charges incurred in 2006.

Disclosure of information to auditorsThe directors who held office at the date of approval of this directors’ report confirm that, so far asthey are each aware, there is no relevant audit information of which the Company’s auditors areunaware; and each director has taken all the steps that he ought to have taken as a director tomake himself aware of any relevant audit information and to establish that the Company’s auditorsare aware of that information.

AuditorsIn accordance with Section 384 of the Companies Act 1985, a resolution for the re-appointment ofKPMG Audit Plc as auditors of the Company is to be proposed at the forthcomingAnnual General Meeting.

By order of the board Islamic Bank of Britain PLC

Ashraf Piranie Edgbaston HouseFinance Director and Company Secretary 3 Duchess Place

Hagley Road08 March 2007 Birmingham B16 8NH

6

Statement of directors’ responsibilities

Statement of directors’ responsibilities in respect of theAnnual Report and the financial statements The directors are responsible for preparing the Annual Report and the financial statements inaccordance with applicable law and regulations.

Company law requires the directors to prepare financial statements for each financial year. Underthat law they have elected to prepare the financial statements in accordance with IFRSs asadopted by the EU and applicable laws.

The financial statements are required by law to present fairly the financial position and theperformance of the Company; the Companies Act 1985 provides in relation to such financialstatements that references in the relevant part of that Act to financial statements giving a true andfair view are references to their achieving a fair presentation.

In preparing these financial statements, the directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgments and estimates that are reasonable and prudent;

• state whether they have been prepared in accordance with IFRSs as adopted by the EU; and

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in business.

The directors are responsible for keeping proper accounting records that disclose with reasonableaccuracy at any time the financial position of the Company and enable them to ensure that itsfinancial statements comply with the Companies Act 1985. They have general responsibility fortaking such steps as are reasonably open to them to safeguard the assets of the company and toprevent and detect fraud and other irregularities.

The directors are responsible for the maintenance and integrity of the corporate and financialinformation included on the Company’s website. Legislation in the UK governing the preparationand dissemination of financial statements may differ from legislation in other jurisdictions.

7

Independent Auditors’ Report

Independent Auditors’ Report to the Members ofIslamic Bank of Britain PLC

We have audited the financial statements of Islamic Bankof Britain PLC (‘the Company’) for the year ended 31December 2006 which comprise the Income Statement,the Balance Sheet, the Cash Flow Statement, theStatement of Changes in Equity and the related notes.These financial statements have been prepared underthe accounting policies set out therein.

This report is made solely to the Company’s members,as a body, in accordance with section 235 of theCompanies Act 1985. Our audit work has beenundertaken so that we might state to the Company’smembers those matters we are required to state to themin an auditor’s report and for no other purpose. To thefullest extent permitted by law, we do not accept orassume responsibility to anyone other than the Companyand the Company’s members as a body, for our auditwork, for this report, or for the opinions we have formed.

Respective responsibilities of directorsand auditorsThe directors' responsibilities for preparing the financialstatements in accordance with applicable law andInternational Financial Reporting Standards (IFRSs) asadopted by the EU are set out in the Statement ofDirectors' Responsibilities on page 7.

Our responsibility is to audit the financial statements inaccordance with relevant legal and regulatoryrequirements and International Standards on Auditing(UK and Ireland).

We report to you our opinion as to whether the financialstatements give a true and fair view and whether thefinancial statements have been properly prepared inaccordance with the Companies Act 1985. We alsoreport to you whether in our opinion the informationgiven in the Director’s Report is consistent with thefinancial statements.

In addition we report to you if, in our opinion, theCompany has not kept proper accounting records, if wehave not received all the information and explanationswe require for our audit, or if information specified by lawregarding directors' remuneration and other transactionsis not disclosed.

We read the other information contained in the AnnualReport and consider whether it is consistent with theaudited financial statements. We consider theimplications for our report if we become aware of anyapparent misstatements or material inconsistencies withthe financial statements. Our responsibilities do notextend to any other information.

Basis of audit opinion We conducted our audit in accordance with InternationalStandards on Auditing (UK and Ireland) issued by theAuditing Practices Board. An audit includesexamination, on a test basis, of evidence relevant to theamounts and disclosures in the financial statements. Italso includes an assessment of the significant estimatesand judgments made by the directors in the preparationof the financial statements, and of whether theaccounting policies are appropriate to the Company’scircumstances, consistently applied andadequately disclosed.

We planned and performed our audit so as to obtain allthe information and explanations which we considerednecessary in order to provide us with sufficient evidenceto give reasonable assurance that the financialstatements are free from material misstatement, whethercaused by fraud or other irregularity or error. In formingour opinion we also evaluated the overall adequacy ofthe presentation of information in thefinancial statements.

OpinionIn our opinion:

• the financial statements give a true and fair view, in accordance with IFRSs as adopted by the EU, of the state of the Company's affairs as at 31 December 2006 and of its loss for the year then ended;

• the financial statements have been properly preparedin accordance with the Companies Act 1985; and

• the information given in the Directors' Report is consistent with the financial statements.

KPMG Audit Plc8 Salisbury SquareLondon, EC4Y 8BBChartered AccountantsRegistered Auditor

8

08 March 2007

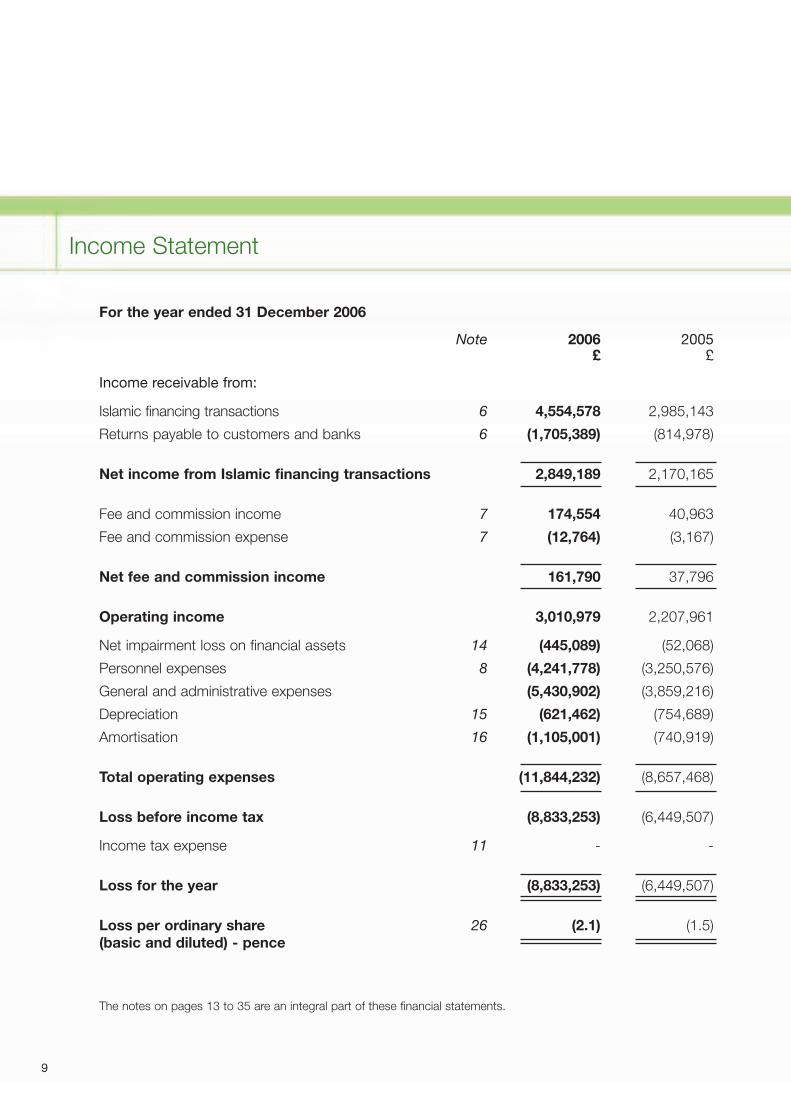

Income Statement

For the year ended 31 December 2006

Note 2006 2005£ £

Income receivable from:

Islamic financing transactions 6 4,554,578 2,985,143

Returns payable to customers and banks 6 (1,705,389) (814,978)

Net income from Islamic financing transactions 2,849,189 2,170,165

Fee and commission income 7 174,554 40,963

Fee and commission expense 7 (12,764) (3,167)

Net fee and commission income 161,790 37,796

Operating income 3,010,979 2,207,961

Net impairment loss on financial assets 14 (445,089) (52,068)

Personnel expenses 8 (4,241,778) (3,250,576)

General and administrative expenses (5,430,902) (3,859,216)

Depreciation 15 (621,462) (754,689)

Amortisation 16 (1,105,001) (740,919)

Total operating expenses (11,844,232) (8,657,468)

Loss before income tax (8,833,253) (6,449,507)

Income tax expense 11 - -

Loss for the year (8,833,253) (6,449,507)

Loss per ordinary share 26 (2.1) (1.5)(basic and diluted) - pence

The notes on pages 13 to 35 are an integral part of these financial statements.

9

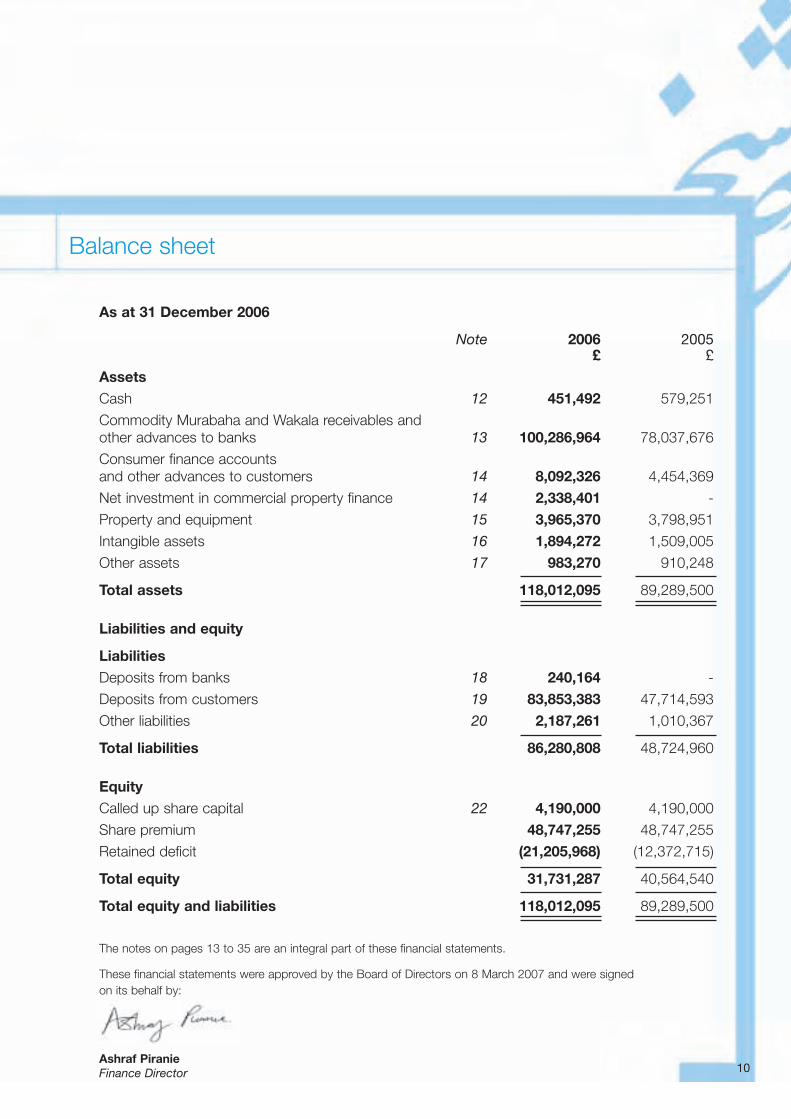

Balance sheet

As at 31 December 2006

Note 2006 2005£ £

AssetsCash 12 451,492 579,251

Commodity Murabaha and Wakala receivables andother advances to banks 13 100,286,964 78,037,676

Consumer finance accountsand other advances to customers 14 8,092,326 4,454,369

Net investment in commercial property finance 14 2,338,401 -

Property and equipment 15 3,965,370 3,798,951

Intangible assets 16 1,894,272 1,509,005

Other assets 17 983,270 910,248

Total assets 118,012,095 89,289,500

Liabilities and equity

LiabilitiesDeposits from banks 18 240,164 -

Deposits from customers 19 83,853,383 47,714,593

Other liabilities 20 2,187,261 1,010,367

Total liabilities 86,280,808 48,724,960

EquityCalled up share capital 22 4,190,000 4,190,000

Share premium 48,747,255 48,747,255

Retained deficit (21,205,968) (12,372,715)

Total equity 31,731,287 40,564,540

Total equity and liabilities 118,012,095 89,289,500

The notes on pages 13 to 35 are an integral part of these financial statements.

These financial statements were approved by the Board of Directors on 8 March 2007 and were signedon its behalf by:

Ashraf PiranieFinance Director 10

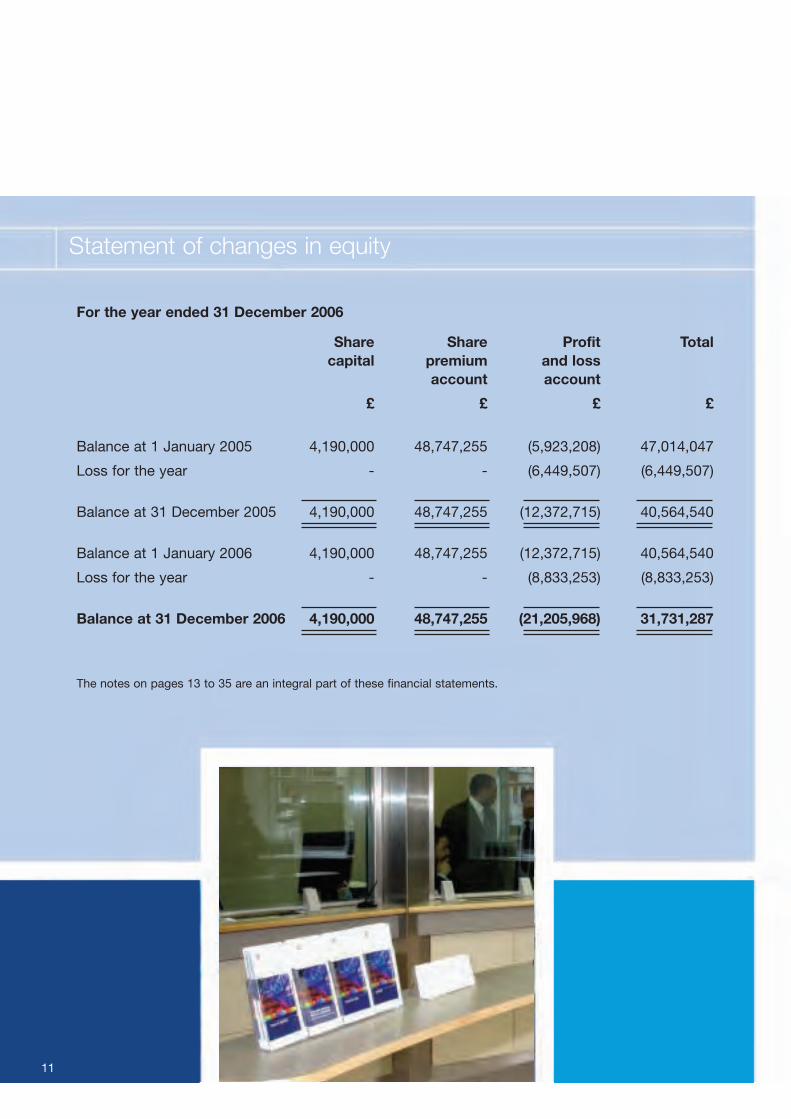

Statement of changes in equity

For the year ended 31 December 2006

Share Share Profit Totalcapital premium and loss

account account

£ £ £ £

Balance at 1 January 2005 4,190,000 48,747,255 (5,923,208) 47,014,047

Loss for the year - - (6,449,507) (6,449,507)

Balance at 31 December 2005 4,190,000 48,747,255 (12,372,715) 40,564,540

Balance at 1 January 2006 4,190,000 48,747,255 (12,372,715) 40,564,540

Loss for the year - - (8,833,253) (8,833,253)

Balance at 31 December 2006 4,190,000 48,747,255 (21,205,968) 31,731,287

The notes on pages 13 to 35 are an integral part of these financial statements.

11

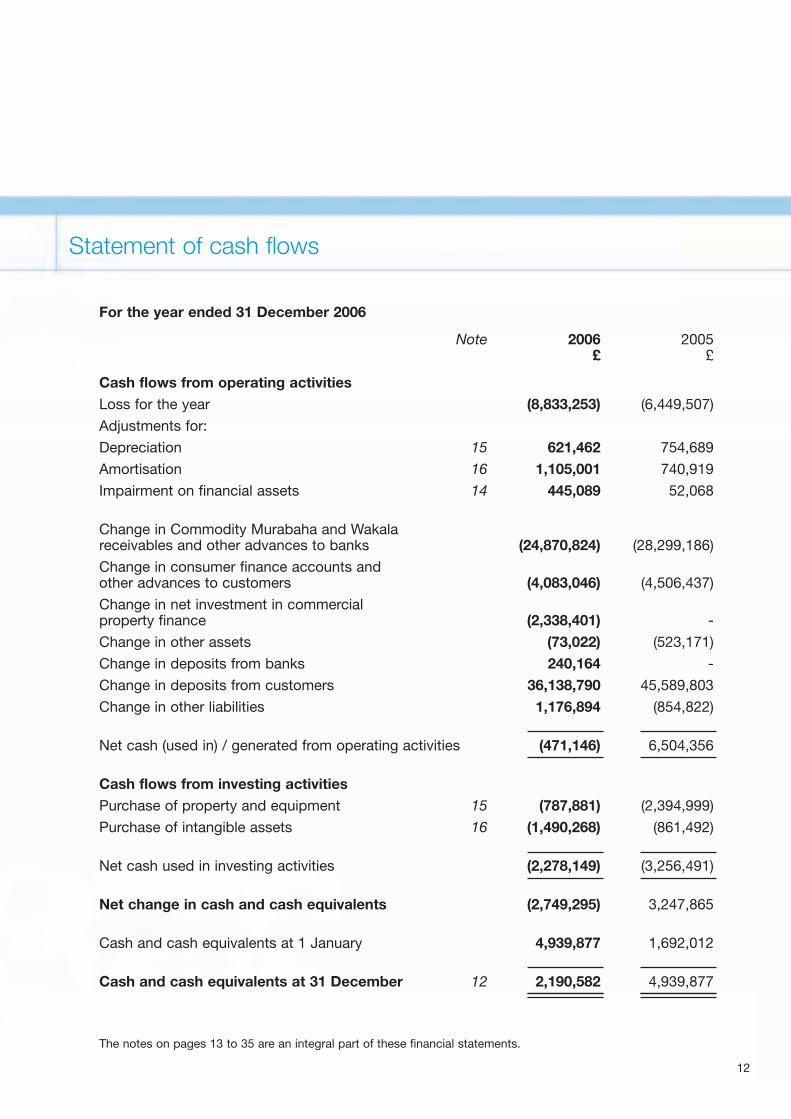

Statement of cash flows

For the year ended 31 December 2006

Note 2006 2005£ £

Cash flows from operating activitiesLoss for the year (8,833,253) (6,449,507)

Adjustments for:

Depreciation 15 621,462 754,689

Amortisation 16 1,105,001 740,919

Impairment on financial assets 14 445,089 52,068

Change in Commodity Murabaha and Wakala receivables and other advances to banks (24,870,824) (28,299,186)

Change in consumer finance accounts andother advances to customers (4,083,046) (4,506,437)

Change in net investment in commercialproperty finance (2,338,401) -

Change in other assets (73,022) (523,171)

Change in deposits from banks 240,164 -

Change in deposits from customers 36,138,790 45,589,803

Change in other liabilities 1,176,894 (854,822)

Net cash (used in) / generated from operating activities (471,146) 6,504,356

Cash flows from investing activitiesPurchase of property and equipment 15 (787,881) (2,394,999)

Purchase of intangible assets 16 (1,490,268) (861,492)

Net cash used in investing activities (2,278,149) (3,256,491)

Net change in cash and cash equivalents (2,749,295) 3,247,865

Cash and cash equivalents at 1 January 4,939,877 1,692,012

Cash and cash equivalents at 31 December 12 2,190,582 4,939,877

The notes on pages 13 to 35 are an integral part of these financial statements.

12

1 Reporting Entity

Islamic Bank of Britain PLC (‘the Company’) is a company domiciled in the UK. The address of the Company’sregistered office is Edgbaston House, 3 Duchess Place, Hagley Road, Birmingham B16 8NH. The financialstatements of the company are presented as at and for the year ended 31 December 2006. The Company is aretail bank offering Sharia’a compliant banking products and services.

2 Basis of preparation

(a) Statement of compliance

These financial statements have been prepared in accordance with International Financial Reporting Standards(IFRSs) as adopted by the EU and approved by the directors.

In preparing these financial statements, the Company has adopted IFRS 7 Financial Instruments: Disclosures priorto the required application date of 1 January 2007. The adoption of IFRS 7 impacted the type and amount ofdisclosures made in these financial statements, but had no impact on the reported profits or financial position ofthe Company. In accordance with the transitional requirements of the standards, the Company has provided fullcomparative information.

The financial statements were approved by the Board of Directors on 8 March 2007.

The accounting policies set out below have, unless otherwise stated, been applied consistently to all periodspresented in these financial statements.

Computer software, both purchased and developed, and computer licences have been presented separately asintangible assets (note 16) within these financial statements. Previously computer software and licences had beenshown as part of computer equipment. This change in presentation has had no impact upon the current year andcomparative totals. The comparative information for 2005 has been reclassified to be presented on a consistentand comparable basis with 2006. Details of the amount of the reclassification are given in note 16. There was noimpact on the income statement or equity.

(b) Basis of measurement

The financial statements have been prepared on the historical cost basis.

(c) Functional and presentation currency

The financial statements are presented in Sterling, which is the Company’s functional currency.

(d) Use of estimates and judgements

The preparation of financial statements requires management to make judgements, estimates and assumptionsthat affect the application of accounting policies and the reported amounts of assets, liabilities, income andexpenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates arerecognised in the period in which the estimate is revised and in any future periods affected.

In particular, information about significant areas of estimation, uncertainty and critical judgements in applyingaccounting policies that have the most significant effect on the amount recognised in the financial statements aredescribed in notes 4 and 5.

Notes to the financial statements

13

Notes to the financial statements

3 Significant accounting policies

The accounting policies set out below have been applied consistently to all periods presented in thesefinancial statements.

(a) Property and equipment

(i) Recognition and measurement

Items of property and equipment are measured at cost less accumulated depreciation and impairment losses.Cost includes expenditure that is directly attributable to the acquisition of the asset.

(ii) Subsequent costs

The cost of replacing part of an item of property or equipment is recognised in the carrying amount of the item if itis probable that the future economic benefits embodied within the part will flow to the Company and its cost canbe measured reliably. The costs of the day-to-day servicing of property and equipment are recognised in theincome statement as incurred.

(iii) Depreciation

Depreciation is recognised in profit or loss on a straight line basis over the estimated useful lives of each part ofan item of property and equipment. Leased assets are depreciated over the shorter of the lease term and theiruseful lives.

Computer equipment 3 years

Fixtures, fittings and office equipment 5 years

Leasehold improvements 10 years or over the life of the lease whicheveris shorter

Depreciation methods, useful lives and residual values are reassessed at the reporting date.

(iv) Change in Presentation

Computer software, both purchased and developed, and computer licences have been presented separately asintangible assets (note 16) within these financial statements. Previously computer software and licences havebeen shown as part of computer equipment. This change in presentation has had no impact upon the currentyear or comparative totals.

(b) Intangible assets

Software and computer licences acquired by the group are stated at cost less accumulated amortisation andaccumulated impairment losses.

Expenditure on internally developed software is recognised as an asset when the Company is able to completethe development and use the software in a manner that will generate future economic benefits, and can reliablymeasure the costs to complete the development. The capitalised costs of internally developed software includeall costs directly attributable to developing the software, and are amortised over its useful life. Internallydeveloped software is stated at capitalised cost less accumulated amortisation and impairment.

Subsequent expenditure on software assets and computer licences is capitalised only when it increases the futureeconomic benefits embodied in the specific asset to which it relates. All other expenditure is expensedas incurred.

Amortisation is recognised in profit or loss on a straight line basis over the estimated useful life of the software orthe licence term, from the date that it is available for use. The estimated useful life of software is three years.

14

Notes to the financial statements

3 Significant accounting policies (continued)

(c) Commodity Murabaha and Wakala receivables and other advances to banks

Commodity Murabaha is an Islamic financing transaction, which represents an agreement whereby the Companybuys a commodity and sells it to a counterparty based on a promise received from that counterparty to buy thecommodity according to specific terms and conditions. The selling price comprises of the cost of the commodityand a pre-agreed upon profit margin.

Wakala is an Islamic financing transaction, which represents an agreement whereby the Company provides acertain sum of money to an agent, who invests it according to specific conditions in order to achieve a certainspecified return. The agent is obliged to return the invested amount in case of default, negligence or violation ofany of the terms and conditions of the Wakala.

Commodity Murabaha receivables are recognised upon the sale of the commodity to the counterparty. Wakalareceivables are recognised upon placement of funds with other institutions.

Income, on both Commodity Murabaha and Wakala receivables, is recognised on an effective yield basis. Theeffective yield rate is the rate that exactly discounts the estimated future cash payments and receipts through theagreed payment term of the contract to the carrying amount of the receivable. The effective yield is establishedon initial recognition of the asset and is not revised subsequently.

The calculation of the effective yield rate includes all fees paid or received, transaction costs, and discounts orpremiums that are an integral part of the effective yield rate. Transaction costs are incremental costs that aredirectly attributable to the acquisition, issue or disposal of a financial asset or liability.

Commodity Murabaha and Wakala receivables are initially recorded at fair value and are subsequently measuredat amortised cost using the effective yield method, less impairment losses. The accrued income receivable isclassified under other assets.

Other advances to banks are stated at cost and are non-return bearing.

(d) Consumer finance accounts

Islamic consumer financing transactions represent an agreement whereby the Company buys a commodity orgoods and then sells it to the customer with an agreed profit mark-up with settlement of the sale price beingdeferred for an agreed period. The customer may subsequently sell the commodity purchased to generate cash.

Consumer finance assets will be recognised on the date that the commodity or good is sold by the Company.Consumer finance account balances are initially recorded at fair value and are subsequently measured atamortised cost. The amortised cost is the amount at which the asset is measured at initial recognition, minusrepayments received relating to the initial recognised amount, plus the cumulative amortisation using an effectiveyield method of any difference between the initial amount recognised and the agreed sales price to the customer,minus any reduction for impairment.

Income is recognised on an effective yield basis over the period of the contract. The effective yield rate is the ratethat exactly discounts the estimated future cash payments and receipts through the agreed payment term of thecontract to the carrying amount of receivable. The effective yield is established on initial recognition of the assetand is not revised subsequently.

The calculation of the effective yield rate includes all fees paid or received, transaction costs, and discounts orpremiums that are an integral part of the effective yield rate. Transaction costs are incremental costs that aredirectly attributable to the acquisition, issue or disposal of a financial asset or liability.

The accrued income receivable from the customer is classified under other assets.15

Notes to the financial statements

3 Significant accounting policies (continued)

(e) Commercial property finance

Commercial property finance is provided using the Diminishing Musharaka (reducing partnership) principle ofIslamic financing. The Company will enter into an agreement to jointly purchase a property with another party andrental income will be received by the Company relating to that proportion of the property owned by the Companyat any point in time. The other party to the agreement will make separate payments to purchase additionalproportions of the property from the Company, thereby reducing the Company’s effective share.

The transaction is recognised as a financial asset upon legal completion of the property purchase and the amountreceivable is recognised at an amount equal to the net investment in the transaction. Where initial direct costs areincurred by the Company such as commissions, legal fees and internal costs that are incremental and directlyattributable to negotiating and arranging the transaction, these costs are included in the initial measurement of thereceivable and the amount of income over the term will be reduced. Rental income is recognised at a constantperiodic rate of return on the Company’s net investment.

(f) Deposits from customers

Profit sharing accounts are based on the principle of Mudaraba whereby the Company and the customer share anagreed percentage of any profit earned on the customer deposits. The customer’s share of profit is paid inaccordance with the terms and conditions of the account. The profit calculation is undertaken at the end of eachcalendar month.

Customer Murabaha deposits consist of an Islamic financing transaction involving the Company arranging thepurchase of an asset on behalf of the customer and the purchase thereof from the same customer by theCompany at cost plus an agreed profit mark-up with settlement on a deferred payment basis. CustomerMurabaha deposit balances are included in the balance sheet under deposits from customers and the accruedreturns payable to the customer are classified under other liabilities. Returns payable on Customer Murabahadeposits are recognised on an effective yield basis over the period of the contract.

(g) Derecognition of financial assets and liabilities

The Company derecognises a financial asset when the contractual rights to the cash flows from the asset expire,or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in whichsubstantially all the risks and rewards or ownership of the financial asset are transferred. Any remaining interest intransferred financial assets that is created or retained by the Company is recognised as a separate asset orliability.

The Company derecognises a financial liability when its contractual obligations are discharged or cancelledor expire.

16

Notes to the financial statements

3 Significant accounting policies (continued)

(h) Impairment of financial assets

At each balance sheet date the Company assesses whether there is objective evidence that financial assets notcarried at fair value through profit or loss are impaired. Financial assets are impaired when objective evidencedemonstrates that a loss event has occurred after the initial recognition of the asset, and that the loss event hasan impact on the future cash flows on the asset that can be estimated readily.

The Company considers evidence of impairment at both a specific asset and collective level. All individuallysignificant financial assets are assessed for specific impairment. All significant assets found not to be specificallyimpaired are then collectively assessed for any impairment that has been incurred but not yet identified. Assetsthat are not individually significant are then collectively assessed for impairment by grouping together financialassets (carried at amortised cost) with similar risk characteristics.

Objective evidence that financial assets are impaired include default or delinquency by the counterparty,extending or changing repayment terms, indications that a counterparty may go into bankruptcy, or otherobservable data relating to a group of assets such as adverse changes in the payment status of counterparties, oreconomic conditions that correlate with defaults in the group.

In assessing collective impairment the Company uses analysis of historical trends to identify the probability ofdefault, timing of recoveries and the amount of loss incurred, adjusted for management’s judgement as to whethercurrent economic conditions are such that the actual losses are likely to be greater or less than suggested byhistorical analysis. Default rates, loss rates and the expected timing of future recoveries are regularlybenchmarked against actual outcomes to ensure that they remain appropriate.

Impairment losses on assets carried at amortised cost are measured as the difference between the carryingamount of the financial asset and the present value of estimated cash flows discounted at the assets’ originaleffective yield rate. Losses are recognised in the income statement and reflected against the asset carrying value.

When a subsequent event causes the amount of impairment losses to decrease, the impairment loss is reversedthrough profit or loss.

(i) Impairment of non-financial assets

The carrying amounts of the Company’s non-financial assets are reviewed at each reporting date to determinewhether there is any indication of impairment. If any such indication exists then the asset’s recoverable amountis estimated.

An impairment loss is recognised if the carrying amount of an asset or its cash-generating unit exceeds itsrecoverable amount. A cash-generating unit is the smallest identifiable asset group that generates cash flows thatlargely are independent from other assets and groups. Impairment losses are recognised in the profit or loss.

The recoverable amount of an asset is the greater of its value in use and its fair value less costs to resell. Inassessing value in use, the estimated future cash flows are discounted to their present value. An impairment lossis reversed if there has been a change in the estimates used to determine the recoverable amount. An impairmentloss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount thatwould have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

17

Notes to the financial statements

3 Significant accounting policies (continued)

(j) Provisions

A provision is recognised if, as a result of a past event, the Company has a present legal or constructiveobligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required tosettle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax ratethat reflects current market assessments of cost of funds and, where appropriate, the risks specific to the liability.

(k) Fees and commissions

Fees and commission income that relate mainly to transaction and service fees are recognised as the relatedservices are performed. Fees and commission expenses that relate mainly to transaction and service fees areexpensed as incurred.

Arrangement fees for commercial property finance deals are amortised over the expected life of the transaction.

(l) Income tax expense

Income tax expense comprises current and deferred tax. Income tax expense is recognised in the incomestatement except to the extent that it relates to items recognised directly in equity, in which case it is recognisedin equity.

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted orsubstantively enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

Deferred tax is provided using the balance sheet method, providing for temporary differences between thecarrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxationpurposes. Deferred tax is measured at the tax rates that are expected to be applied to the temporary differenceswhen they reverse, based on laws that have been enacted or substantively enacted by the reporting date.

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be availableagainst which the asset can be utilised. Deferred tax assets are reviewed at each reporting date and are reducedto the extent that it is no longer probable that the related tax benefit will be realised.

(m) Lease payments made

Payments made under operating leases are recognised in the income statement on a straight-line basis over theterm of the lease. Lease incentives received are recognised as an integral part of the total lease expensed, overthe term of the lease.

18

Notes to the financial statements

3 Significant accounting policies (continued)

(n) Employee benefits

Obligations for contributions to defined contribution pension plans are recognised as an expense in the incomestatement when they are due.

Short-term employee benefits, such as salaries, paid absences, and other benefits, are accounted for on anaccruals basis over the period for which employees have provided services. Bonuses are recognised to theextent that the Company has a present obligation to its employees that can be measured reliably.

(o) Cash and cash equivalents

Cash and cash equivalents include notes and coins on hand, unrestrictive balances held with central banks andhighly liquid financial assets with original maturities of less than three months, which are subject to insignificantrisk of changes in their fair value, and are used by the Company in the management of its short-termcommitments.

Commodity Murabaha and Wakala transactions, used by the Company for investment purposes, are not includedwithin cash and cash equivalents.

Cash and cash equivalents are carried at amortised cost in the balance sheet.

(p) Other receivables

Trade and other receivables are stated at their nominal amount (discounted if material) less impairment losses.

(q) Earnings per share

The Company presents basic and diluted earnings per share (EPS) data for its ordinary shares. Basic EPS iscalculated by dividing the profit or loss attributable to ordinary shareholders of the Company by the weightedaverage number of ordinary shares outstanding during the period. Diluted EPS is determined by adjusting theprofit or loss attributable to ordinary shareholders and the weighted average number of ordinary sharesoutstanding for the effects of all dilutive potential ordinary shares.

(r) Foreign currency transactions

Transactions in foreign currencies are translated to the functional currency at exchange rates at the date oftransaction. Monetary assets and liabilities denominated in foreign currencies at the reporting date areretranslated to the functional currency at the exchange rate at that date. The foreign currency gain or loss onmonetary items is the difference between amortised cost in the functional currency at the beginning of the periodand the amortised cost in foreign currency translated at the exchange rate at the end of the period. Foreigncurrency differences arising on retranslation are recognised in the income statement.

19

Notes to the financial statements

3 Significant accounting policies (continued)

(s) New standards and interpretations not yet adopted

A number of new standards, amendments to standards and interpretations relevant to the Company are not yeteffective for the year ended 31 December 2006 and have not been applied in preparing thesefinancial statements.

• IFRIC 9 Reassessment of Embedded Derivatives requires that an assessment of whether embedded derivatives should be separated from the underlying host contract should be made only when there are changes to the contract. IFRIC 9, which becomes mandatory for the Company’s 2007 financial statements, is not expected to have any impact on the financial statements.

• IFRIC 10 Interim Financial Reporting and Impairment prohibits the reversal of an impairment loss recognised in a previous interim period in respect of goodwill, an investment in an equity instrument or a financial asset carried at cost. IFRIC 10 will become mandatory for the Company’s 2007 financial statements, and will applyto goodwill, investments in equity instruments, and financial assets carried at cost prospectively from the date that the Company first applied the measurement criteria of IAS 36 and IAS 39 respectively. The adoption of IFRIC 10 is not currently expected to have any impact on the financial statements.

20

Notes to the financial statements

4 Financial risk management

The Company has exposure to the following risks arising from its use of financial instruments:

• credit risk• liquidity risk• market risks• operational risks

The Company is not exposed to any material foreign currency risk.

This note presents information about the Company’s exposure to each of the above risks, the Company’sobjectives, policies and processes for measuring and managing these risks, and the Company’s managementof capital.

Risk management framework

The Board of Directors has overall responsibility for the establishment and oversight of the Company’s riskmanagement framework. The Company has established the Asset and Liability (ALCO), Credit and OperationsCommittees, which are responsible for developing and monitoring risk management policies in their specific areas.

The Company’s risk management policies are established to identify and analyse the risks faced by the Company,to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policiesand systems are reviewed regularly to reflect changes in market conditions, products and services offered. TheCompany, through its training and management standards and procedures, aims to develop a disciplined andconstructive control environment, in which all employees understand their roles and obligations.

Risk management controls and procedures are reviewed by Internal Audit, both as part of the regular audit reviewprogramme and through ad-hoc reviews. The results of these reviews are reported to the Audit Committee.

(a) Credit risk

Credit risk is the risk of financial loss to the Company if a customer or counterparty to a financial instrument fails tomeet its contractual obligations. The Company’s credit risk arises principally from its financing products but alsofrom other advances to customers and banks.

(i) Management of credit risk

The Company seeks to manage credit risk by monitoring credit exposures, limiting transactions with specificcounterparties, countries or sectors and continually assessing the creditworthiness of counterparties.

The Board of Directors has delegated responsibility for the management of credit risk to the Credit Committee. Aseparate Credit Risk department, reporting to the Credit Committee is responsible for oversight of the Company’scredit risk, including:

• Formulating credit policies in consultation with other business units, covering credit assessments, collateral requirements, risk reporting, legal requirements and compliance with regulatory and statutory requirements.

• Establishing authorisation limits and structures for the approval and renewal of credit exposure limits.• Reviewing and assessing credit risk prior to agreements being entered into with customers.• Limiting concentrations of exposure to counterparties and reviewing these limits.• Ongoing assessment of exposure and implementation of procedures to reduce this exposure.

• Providing advice, guidance and specialist skills to all business areas to promote best practice throughout the Company in the management of credit risk.

Adherence to country and counterparty limits, for amounts due to other banks, is monitored on an ongoing basisby the Company’s Treasury department, with a detailed review of all limits at least annually. Senior managementreceives regular reports on the utilisation of these limits.

Regular reviews of the Credit Risk department’s processes are undertaken by Internal Audit.21

Notes to the financial statements

22

4 Financial risk management (continued)

(a) Credit risk (continued)

(ii) Exposure to credit risk

Consumer finance accounts Net investment Totaland other advances in commercial

to customers property finance

Note 2006 2005 2006 2005 2006 2005

Total Gross 8,589,483 4,506,437 2,338,401 - 10,927,884 4,506,437Individually impaired - 14 (357,081) - - - (357,081) -allowance for impairmentCollectively impaired - 14 (140,076) (52,068) - - (140,076) (52,068)allowance for impairmentCarrying amount 14 8,092,326 4,454,369 2,338,401 - 10,430,727 4,454,369

As at 31 December 2006, the amount of unimpaired balances stood at £10,570,803 (2005: £4,506,437). The maximumexposure to credit risk is the carrying amount of the financial asset receivable balances as at 31 December 2006 and31 December 2005.

(iii) Write-off policy

The Company writes off a balance (and any related allowances for impairment) when the Credit Risk departmentdetermines that the balance is uncollectible. This determination is reached after considering information such as theoccurrence of significant changes in the counterparty’s financial position such that the counterparty can no longer paythe obligation, or that proceeds from collateral will not be sufficient to pay back the entire exposure.

(iv) Collateral

The Company holds collateral against secured advances made to businesses, as shown within the corporate sectionbelow, in the form of charges over properties, other registered securities over assets, and guarantees. Estimates of fairvalue are based on the value of collateral assessed at the time of financing and are updated on a periodic basis. Theestimated fair value of collateral held against financial assets as at 31 December 2006 is £5.3m (2005: £nil). None ofthis amount was held against impaired assets.

(v) Concentration of credit risk

The Company monitors concentrations of credit risk by sector and geographical location. An analysis ofconcentrations of credit risk at the reporting date is shown below:

Consumer finance accounts Net investment Commodity Murabaha & and other advances in commercial Wakala receivables and

to customers property finance other advances to banks

2006 2005 2006 2005 2006 2005

Concentrationby sector:

Individuals 7,989,887 4,454,369 - - - -Corporate 102,439 - 2,338,401 - - -Bank - - - - 100,286,964 78,037,676

8,092,326 4,454,369 2,338,401 - 100,286,964 78,037,676

Concentrationby location:

United Kingdom 8,092,326 4,454,369 2,338,401 - 26,087,038 21,034,065Europe - - - - 64,922,142 47,697,552Middle East - - - - 9,277,784 9,306,059

8,092,326 4,454,369 2,338,401 - 100,286,964 78,037,676

Notes to the financial statements

4 Financial risk management (continued)

(b) Liquidity risk

Liquidity risk is the risk that the Company will encounter difficulty in meeting obligations from its financialliabilities. The Company’s approach to managing liquidity is to ensure that it will always have sufficient liquidity tomeet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses orrisking damage to the Company’s reputation.

The Treasury department is responsible for monitoring the liquidity profile of financial assets and liabilities anddetails of projected cash flows arising from projected future business. The Treasury department will maintain aportfolio of short-term liquid assets, made up of cash on demand and short term commodity Murabaha andWakala transactions to ensure that sufficient liquidity is maintained. All liquidity policies and procedures aresubject to review and approval by ALCO.

The key measure used by the Company for managing liquidity risk is the comparison of liquid assets and maturityof assets against customer deposits. This analysis is completed on a daily basis and reports are submitted forreview to ALCO. A similar calculation of mismatches is submitted to the FSA as part of the Company’s quarterlyregulatory reporting.

(i) Residual contractual maturities of financial liabilities

Note Carrying Gross nominal Less than 1-3 3 months More thanamount inflow/(outflow) 1 month months - 1 year 1 year

£ £ £ £ £ £

31 December 2006

Deposits from banks 18 240,164 240,164 240,164 - - -

Deposits from customers 19 83,853,383 84,349,000 70,259,000 6,889,000 7,201,000 -

84,093,547 84,589,164 70,499,164 6,889,000 7,201,000 -

31 December 2005

Deposits from banks 18 - - - - - -

Deposits from customers 19 47,714,593 48,112,000 35,302,000 8,335,000 4,475,000 -

The table above shows the undiscounted cash flows on the Company’s financial liabilities on the basis of theirearliest possible contractual maturity. However, based on behavioural experience demand deposits fromcustomers are expected to maintain an increasing balance. A breakdown of the Company’s CommodityMurabaha and Wakala receivables by maturity date is shown in note 13.

23

Notes to the financial statements

24

4 Financial risk management (continued)

(c) Market risk

Market risk is the risk that changes in market prices will affect the Company’s income. The objective of marketrisk management is to manage and control exposures within acceptable parameters, whilst optimising returns.Given the Company’s current profile of financial instruments, the principle exposure is the risk of loss arising fromfluctuations in the future cash flows or fair values of these financial instruments because of a change in achievablerates. This is managed principally through monitoring gaps between effective profit and rental rates and byhaving approved rates and bands reviewed at regular re-pricing meetings:

• Profit rates for commodity Murabaha and Wakala receivables are agreed with the counterparty bank at the time of each transaction and the profit mark-up and effective yield rate is consequently fixed for the duration of the contract. Risk exposure is managed by reviewing maturity profiles of transactions entered into.

• Effective rates applied to new consumer finance transactions are agreed on a monthly basis by ALCO and the profit mark-up will then be fixed for each individual transaction for the agreed deferred payment term.

• Rental for longer term commercial property financing is benchmarked against a market measure, in agreement with the Company’s Sharia’a Supervisory Committee, and therefore amounts receivable are reassessed every six months.

• Rates of return payable on customer deposit accounts are calculated at each month-end in line with the Mudaraba profit model and the customer terms and conditions.

All rates and re-pricings are reviewed and agreed at ALCO, which is principally responsible for monitoring marketrisk. ALCO will also review sensitivities of the Company’s assets and liabilities to standard and non-standardchanges in achievable effective rates. Standard scenarios that are considered on a monthly basis include a1.00% or 0.50% rise or fall in effective average rates. An analysis of the Company’s income statement sensitivityto an increase or decrease in effective rates (assuming no asymmetrical movement and a constant balance sheetposition) is as follows:

1.00% parallel 1.00% parallel 0.50% parallel 0.50% parallelincrease decrease increase decrease

31 December 2006 1,219,894 (1,219,894) 609,947 (609,947)

31 December 2005 1,788,430 (1,788,430) 894,215 (894,215)

(d) Operational risk

Operational risk is the risk of direct or indirect loss arising from a wide variety of causes associated with theCompany’s processes, personnel, technology and infrastructure, and from external factors other than credit,market and liquidity risks.

The Company’s objective in managing operational risk is to implement an integrated internal control structure thatsupports process efficiency and customer needs, whilst effectively reducing the risk of error and financial loss in acost effective manner. The overall operational risk framework is set by the Board of Directors. Primaryresponsibility for the development and implementation of internal controls is assigned to senior managementwithin each businesss department. Adherence to overall operational risk policies and procedures is regularlyreviewed by Internal Audit and findings are reported to the Audit Committee.

Notes to the financial statements

25

4 Financial risk management (continued)

(e) Settlement risk

The Company’s activities may give rise to risk at the time of settlement of transactions and trades. Settlementrisk is the risk of loss due to the failure of a company to honour its obligations to deliver cash or other assets ascontractually agreed.

For certain types of transactions the Company mitigates this risk by conducting settlements through a settlement/ clearing agent to ensure that a trade is settled only when both parties have fulfilled their contractual settlementobligations. Settlement limits form part of the credit approval / limit monitoring process described earlier.

(f) Capital management

The Company’s capital requirements are set and monitored by the Financial Services Authority (FSA). Regulatorycapital is analysed into two tiers:

• Tier 1 capital, which includes ordinary share capital, share premium andretained earnings.

• Tier 2 capital, which includes collective impairment allowances, restricted to amaximum amount.

The level of total capital is matched against risk-weighted assets which are determined according to specifiedrequirements that seek to reflect the varying levels of risk attached to assets.

The Company has complied with all capital requirements throughout the year. There have been no materialchanges in the Company’s management of capital during the year.

The Company’s regulatory capital position as at 31 December was as follows:

Note 2006 2005£ £

Tier 1 capital

Ordinary share capital 22 4,190,000 4,190,000

Share premium 48,747,255 48,747,255

Retained earnings (21,205,968) (12,372,715)

31,731,287 40,564,540

Tier 2 capital

Collective allowances for impairment 14 140,076 52,068

Total regulatory capital (b) 31,871,363 40,616,608

Risk-weighted assets (a) 37,690,732 26,387,874

Total regulatory capital expressed as (b)/(a) 84.56% 153.92%a percentage of risk-weighted assets

The Basel Committee on Banking Supervision has published the Basel II framework for calculating minimumcapital requirements. The EU Capital Requirements Directive is the means by which Basel II will be implementedin the EU. The Company will adopt provisions relating to the calculation of minimum capital requirements on 1January 2008. Work is currently ongoing to implement requirements relating to these provisions and therefore it iscurrently premature to establish the precise effect of Basel II on the Company’s capital ratios.

Notes to the financial statements

26

5 Use of estimates and judgments

Management discussed with the Audit Committee the development, selection and disclosure of the Company’scritical accounting policies and estimates, and the application of these policies and estimates. This disclosuresupplements the commentary on financial risk management (see note 4)

Key sources of estimation uncertainty

Allowance for credit losses

Assets accounted for at amortised cost are evaluated for impairment on a basis described in accountingpolicy (h).

The specific counterparty component of the total allowances for impairment applies to claims evaluatedindividually for impairment and is based upon management’s best estimate of the present value of the cash flowsthat are expected to be received. In estimating these cash flows, management makes judgements about eachcounterparty’s financial situation and the realisable value of any underlying collateral. Each impaired asset isassessed on its merits, and the estimates of cash flows considered recoverable are approved by the CreditRisk function.

Collectively assessed impairment allowances cover credit losses inherent in portfolios of claims with similareconomic characteristics when there is objective evidence to suggest that they contain impaired claims, but theindividual impaired items cannot yet be identified. In assessing the need for collective loss allowances,management considers factors such as credit quality, portfolio size, concentrations, and economic factors. Inorder to estimate the required allowance, assumptions are made to define the way inherent losses are modelledand to determine the required input parameters, based on historical experience and current economic conditions.

6 Net income from Islamic financing transactions

2006 2005Income received

Commodity Murabaha and Wakala transactions 3,880,252 2,783,604Consumer finance accounts 640,257 201,539Commercial property finance 34,069 -Total income received from Islamic financing transactions 4,554,578 2,985,143

Returns payable

Deposits from banks (4,988) -Deposits from customers (1,700,401) (814,978)Total returns payable to customers and banks (1,705,389) (814,978)Net income from Islamic financing transactions 2,849,189 2,170,165

7 Net fee and commission income

2006 2005Fee and commission income

Retail customer banking fees 130,585 33,916Home finance introduction fees 1,750 -Arrangement fees 633 -ATM commission 34,719 7,047Other 6,867 -Total fee and commission income 174,554 40,963

Fee and commission expense

Electronic transaction fees (12,764) (3,167)Total fee and commission expense (12,764) (3,167)Net fee and commission income 161,790 37,796

Notes to the financial statements

8 Personnel costs

2006 2005£ £

Wages and salaries 3,777,164 2,914,193Social security costs 401,482 267,162Contributions to defined contribution plans 52,094 61,615Other staff costs 11,038 7,606

Total 4,241,778 3,250,576

The average number of persons employedby the Company during the year was: 144 102

9 Auditors’ remuneration

Included within operating losses are the following payments made to the auditors:

2006 2005£ £

Amounts receivable by the auditors and their associates in respect of:Audit of financial statements pursuant to legislation 90,000 88,362Other services pursuant to such legislation - -Under-accrual for prior year audit fees 35,403 -Other services relating to taxation 52,430 148,667Services relating to information technology - 20,223Internal audit services - -Valuation and actuarial services - -Services relating to litigation - -Services relating to recruitment and remuneration - -Services relating to corporate finance transactions entered into or proposed - -to be entered into by or on behalf of the Company or the Company’s subsidiaries All other services 30,390 9,956

Total 208,223 267,208

10 Directors’ emoluments

2006 2005£ £

Directors’ emoluments 503,492 393,966

Company contributions to pension plans 21,831 13,680

Total 525,323 407,646

The aggregate of emoluments of the highest paid director was £177,620 (2005: £173,800), and Company pensioncontributions of £12,561 (2005: £12,180) were made on his behalf.27

Notes to the financial statements

28

11 Income tax expense

There were no taxable profits or recoverable losses for the year ended 31 December 2006 (2005: £nil) and,accordingly, the Company has not provided for a tax charge or a tax debtor.

2006 2005£ £

Reconciliation of effective tax rate Loss before tax (8,833,253) (6,449,507)Income tax at UK corporation tax rate (30%) (2,649,978) (1,934,852)Non deductible expenses 47,108 47,621Depreciation in excess of capital allowanceson which deferred tax not recognised 417,939 448,642Adjustment to prior year tax (33,242) -Unutilised tax losses 2,218,173 1,438,589

- -Deferred tax assets have not been recognisedin respect of the following items:Capital allowances 1,064,584 646,645Tax losses 4,909,069 2,690,896

5,973,653 3,337,541

In respect of the recognition of deferred tax assets, for the purposes of applying the requirements of IAS 12(‘Income Taxes’), it has been considered that the Company is not currently at a sufficiently advanced stage in itsdevelopment to confidently assert future offsetting tax liabilities. Capital allowances to be claimed are beingfinalized and therefore the level of the asset shown above may change.

12 Cash and cash equivalents

2006 2005£ £

Cash 451,492 579,251Other advances to banks 1,739,090 4,360,626

Total cash and cash equivalents 2,190,582 4,939,877

13 Commodity Murabaha and Wakala receivables and other advances to banks

2006 2005£ £

Repayable on demand 1,739,090 4,360,6263 months or less but not repayable on demand 98,038,968 72,099,0151 year or less but over 3 months 508,906 1,578,035

Total Commodity Murabaha and Wakala receivables 100,286,964 78,037,676and other advances to banks

A breakdown of Commodity Murabaha and Wakala receivables and other advances to bank by geographicregions is shown in note 4. Balances maturing in 1 year or less but over 3 months include a balance of £508,906(2005: £578,035) representing a repayable security deposit held by a bank that has issued a guarantee to coverthe Company’s future customer card transactions with Mastercard. The deposit earns no return.

Notes to the financial statements

14 Advances to customers

Gross Impairment Carrying Gross Impairment Carryingamount allowance amount amount allowance amount

2006 2006 2006 2005 2005 2005£ £ £ £ £ £

Retail customers:

Consumer finance accounts 8,487,044 (497,157) 7,989,887 4,506,437 (52,068) 4,454,369and other advances to customersCorporate customers:Consumer finance accounts 102,439 - 102,439 - - -and other advances to customers

Total consumer finance accounts 8,589,483 (497,157) 8,092,326 4,506,437 (52,068) 4,454,369and other advances to customers

Net investment in commercial 2,338,401 - 2,338,401 - - -property finance

2006 2005£ £

Specific allowances for impairment

Balance at 1 January - -Charge for the year 357,081 -

Balance at 31 December 357,081 -

Collective allowances for impairment

Balance at 1 January 52,068 -Charge for the year 88,008 52,068

Balance at 31 December 140,076 52,068

Total allowances for impairment

Balance at 1 January 52,068 -Charge for the year 445,089 52,068

Balance at 31 December 497,157 52,068

£445,089 of the impairment charge in 2006 related to the retail consumer finance business and other advances toretail customers (2005: £52,068).

The gross investment in commercial property finance comprises:

Less than one year 242,367 -Between one and five years 954,392 -More than five years 3,055,194 -

Total gross investment in commercial property finance 4,251,953

Unearned future rental on commercial property finance (1,913,552)

Net investment in commercial property finance 2,338,401 -

The net investment in commercial property finance comprises:

Less than one year 141,331 -Between one and five years 552,668 -More than five years 1,644,402 -

2,338,401 -

As at 31 December 2006 there is no material difference between the carrying value and the fair value of any financialassets or liabilities (2005: £nil)

29

Notes to the financial statements

30

15 Property and equipment

Computer Office Leasehold Fixtures and Totalequipment equipment improvements fittings

£ £ £ £ £

Cost

Balance at 1 January 2006 1,078,144 78,882 3,470,753 216,539 4,844,318

Additions 173,471 8,735 564,809 40,866 787,881

Balance at 31 December 2006 1,251,615 87,617 4,035,562 257,405 5,632,199

Depreciation

Balance at 1 January 2006 427,440 18,231 562,079 37,617 1,045,367

Depreciation charge for the year 387,432 16,347 162,681 55,002 621,462

Balance at 31 December 2006 814,872 34,578 724,760 92,619 1,666,829

Net book value

At 31 December 2006 436,743 53,039 3,310,802 164,786 3,965,370

Cost

Balance at 1 January 2005 702,488 48,613 1,642,806 55,412 2,449,319

Additions 375,656 30,269 1,827,947 161,127 2,394,999

Balance at 31 December 2005 1,078,144 78,882 3,470,753 216,539 4,844,318

Depreciation

Balance at 1 January 2005 130,967 6,501 141,329 11,881 290,678

Depreciation charge for the year 296,473 11,730 420,750 25,736 754,689

Balance at 31 December 2005 427,440 18,231 562,079 37,617 1,045,367

Net book value

At 31 December 2005 650,704 60,651 2,908,674 178,922 3,798,951

Computer software, both purchased and developed, and computer licences have been presented separately asintangible assets (note 16) within these financial statements. Previously computer software and licences havebeen shown as part of computer equipment. This change in presentation has had no impact upon the currentyear and comparative totals.

The Company leases its branch and office premises under operating leases. The leases typically run for 10 years,with options to renew the lease after that date. Lease payments are reviewed after periods stipulated in theagreements to reflect market rentals.

Notes to the financial statements

16 Intangible assets

Computer Purchased and Totallicences developed software

£ £ £

Cost

Balance at 1 January 2006 363,507 2,297,171 2,660,678Additions 318,301 1,171,967 1,490,268

Balance at 31 December 2006 681,808 3,469,138 4,150,946

Amortisation

Balance at 1 January 2006 180,604 971,069 1,151,673Amortisation charge for the year 179,094 925,907 1,105,001

Balance at 31 December 2006 359,698 1,896,976 2,256,674

Net book value

At 31 December 2006 322,110 1,572,162 1,894,272

Cost

Balance at 1 January 2005 274,190 1,524,996 1,799,186Additions 89,317 772,175 861,492

Balance at 31 December 2005 363,507 2,297,171 2,660,678

Amortisation

Balance at 1 January 2005 92,985 317,769 410,754Amortisation charge for the year 87,619 653,300 740,919

Balance at 31 December 2005 180,604 971,069 1,151,673

Net book value

At 31 December 2005 182,903 1,326,102 1,509,005

17 Other assets

2006 2005£ £

VAT recoverable 505,611 353,047

Accrued income 105,414 173,199

Prepayments 372,245 339,734

Other receivables - 44,268

Total 983,270 910,248

There are no receivables within other assets that are expected to be recovered in more than 12 months(2005: £nil).

31

Notes to the financial statements

32

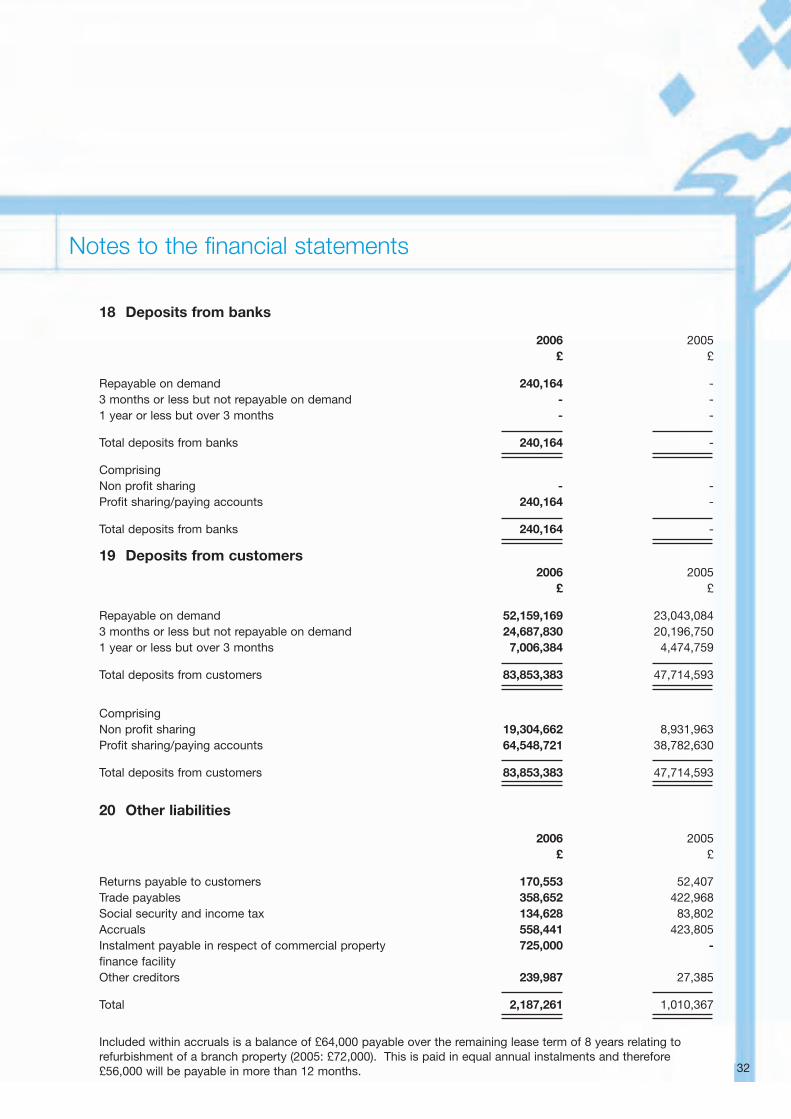

18 Deposits from banks

2006 2005£ £

Repayable on demand 240,164 -3 months or less but not repayable on demand - -1 year or less but over 3 months - -

Total deposits from banks 240,164 -

ComprisingNon profit sharing - -Profit sharing/paying accounts 240,164 -

Total deposits from banks 240,164 -

19 Deposits from customers2006 2005

£ £

Repayable on demand 52,159,169 23,043,0843 months or less but not repayable on demand 24,687,830 20,196,7501 year or less but over 3 months 7,006,384 4,474,759

Total deposits from customers 83,853,383 47,714,593

ComprisingNon profit sharing 19,304,662 8,931,963Profit sharing/paying accounts 64,548,721 38,782,630

Total deposits from customers 83,853,383 47,714,593

20 Other liabilities

2006 2005£ £

Returns payable to customers 170,553 52,407Trade payables 358,652 422,968Social security and income tax 134,628 83,802Accruals 558,441 423,805Instalment payable in respect of commercial property 725,000 -finance facilityOther creditors 239,987 27,385

Total 2,187,261 1,010,367

Included within accruals is a balance of £64,000 payable over the remaining lease term of 8 years relating torefurbishment of a branch property (2005: £72,000). This is paid in equal annual instalments and therefore£56,000 will be payable in more than 12 months.

Notes to the financial statements

33

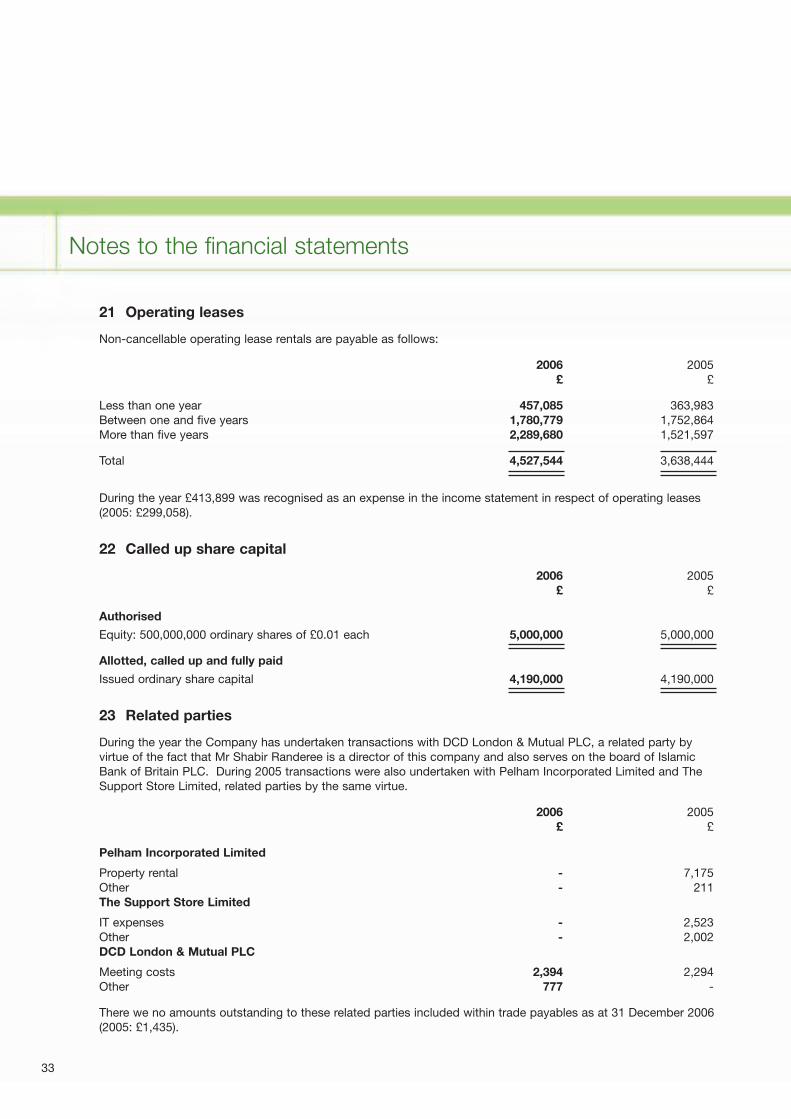

21 Operating leases

Non-cancellable operating lease rentals are payable as follows:

2006 2005£ £

Less than one year 457,085 363,983Between one and five years 1,780,779 1,752,864More than five years 2,289,680 1,521,597

Total 4,527,544 3,638,444

During the year £413,899 was recognised as an expense in the income statement in respect of operating leases(2005: £299,058).

22 Called up share capital

2006 2005£ £

Authorised

Equity: 500,000,000 ordinary shares of £0.01 each 5,000,000 5,000,000

Allotted, called up and fully paid

Issued ordinary share capital 4,190,000 4,190,000

23 Related parties

During the year the Company has undertaken transactions with DCD London & Mutual PLC, a related party byvirtue of the fact that Mr Shabir Randeree is a director of this company and also serves on the board of IslamicBank of Britain PLC. During 2005 transactions were also undertaken with Pelham Incorporated Limited and TheSupport Store Limited, related parties by the same virtue.

2006 2005£ £

Pelham Incorporated Limited

Property rental - 7,175Other - 211The Support Store Limited

IT expenses - 2,523Other - 2,002DCD London & Mutual PLC

Meeting costs 2,394 2,294Other 777 -

There we no amounts outstanding to these related parties included within trade payables as at 31 December 2006(2005: £1,435).

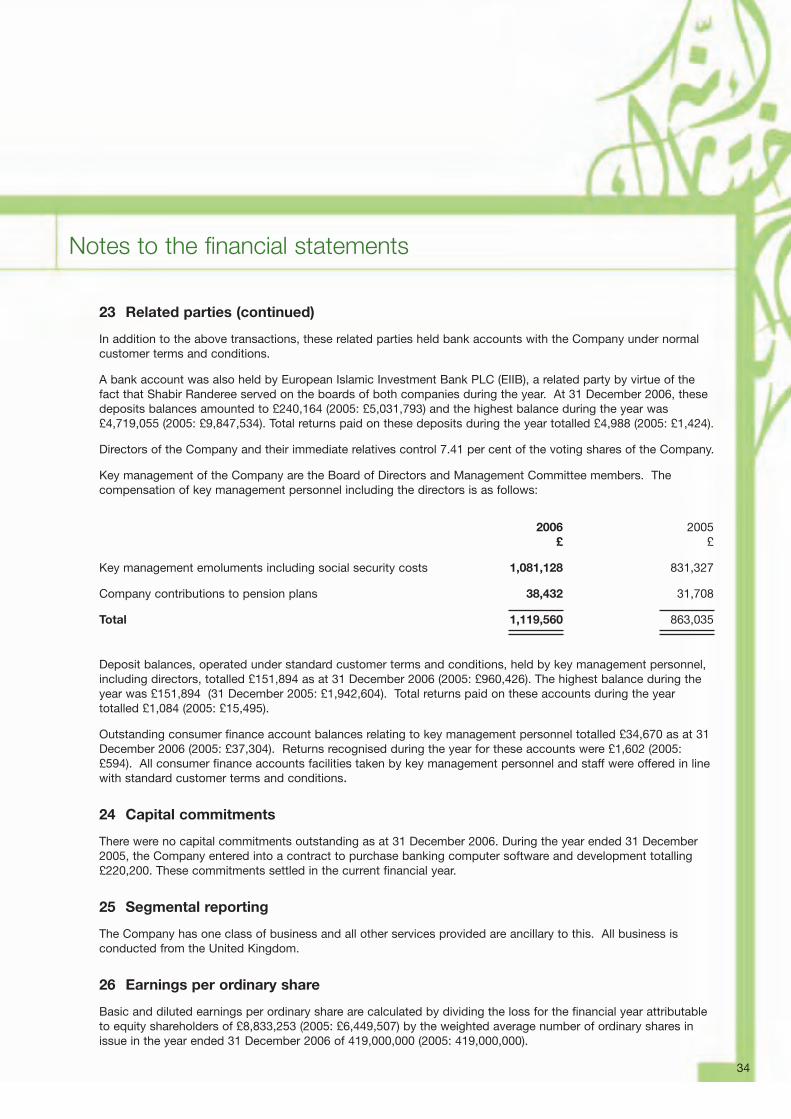

23 Related parties (continued)

In addition to the above transactions, these related parties held bank accounts with the Company under normalcustomer terms and conditions.