ANNUAL REPORT 2016s2.q4cdn.com/889465930/files/doc_financials/annual/... · · 2017-03-28ANNUAL...

63

ANNUAL REPORT 2016

Transcript of ANNUAL REPORT 2016s2.q4cdn.com/889465930/files/doc_financials/annual/... · · 2017-03-28ANNUAL...

ANNUAL REPORT 2016

Contents

Letter from the Chief Executive Officer 4 Management’s Discussion and Analysis 6

Introduction 6 The Company 9 Operational Review 10 Summary of Investments 14 Financial Review 16 Results of Operations for the Year Ended December 31, 2016 20 Fourth Quarter Results 22 Summary of Quarterly Results 23 Liquidity, Capital Resources and Off-Balance Sheet Arrangements 24 Proposed Transactions 26 Transactions with Related Parties 26 Changes in Accounting Policies and Critical Accounting Estimates 26 Factors that May Affect Future Results 29 Controls and Procedures 29 Outlook 30 Financial Risk Management and Risk Factors 31

Financial Statements Independent Auditors Report FS 1-2 Consolidated Statements of Financial Position FS 3 Consolidated Statements of Loss FS 4 Consolidated Statements of Comprehensive Loss FS 5 Consolidated Statements of Changes in Equity FS 6 Consolidated Statements of Cash Flows FS 7 Notes to the Consolidated Financial Statements FS 8-24

Company Directory Back Cover

1

Crosswinds is a publicly traded private equity firm and asset manager targeting strategic and opportunistic investments in the financial services sector with a particular focus on the insurance industry. Crosswinds is in the business of developing unique opportunities and intelligently structuring investments to create and unlock synergistic value. Our disciplined approach to insurance investment structuring and asset management is designed to achieve long-term value creation for our shareholders.

2

Ø Strategic niche

We focus on investments in insurance, reinsurance and asset management, a valuable niche that is further leveraged through strategic partnerships with industry experts. Crosswinds is building a platform with a sourcing and structuring advantage to provide access to unique insurance venture opportunities.

Ø Long-Cycle Continuous Cash Flow Streams We are able to earn income and capital gains from our direct investments, as well as management fees from the money that we manage. This established business model provides diversified revenue and strong potential to generate shareholder value. We believe that artificial exit dates create subpar investment returns. We enter into investments with the view that our investments are worth owning for many years over a longer-term investment cycle.

Ø Platform For Future Growth Our investments are made as platforms for future growth both organically and through the development and implementation of complementary business segments.

Ø Skill and Experience With decades of shared experience among our executives and board members, we have the broad skill set and depth of experience to recognize and capitalize on unique opportunities.

Ø Managing Risk Our approach to risk management is based on intensive due diligence, creative deal structuring and the careful selection of investment partners and opportunities.

Ø Partnership-Based Approach Our partnership-based approach is core to our strategy. Developing relationships with strong industry partners will allow us to source and structure future accretive insurance investment opportunities.

3

Crosswinds is managed and stewarded by a skilled team, with

extensive investment banking and asset management experience. We focus our resources on niche, fragmented, and

complex opportunities in the insurance industry and we seek to actively structure our investments

to capitalize on identified synergies. Crosswinds is working to grow and expand its business across 3 key pillars:

Insurance! Reinsurance! Asset Management!

4

Letter from the Chief Executive Officer As we reflect back on 2016, it was a year spent finalizing the Crosswinds platform including adding a licensed and nominally capitalized resinsurer to its Florida based property and casualty homeowners insurance company, Monarch, and its asset management vehicle, Crosswinds AUM. We are active in the Florida market and are looking to grow our presence there. We have also been active developing liquidity options for our one remaining legacy asset, Salbro so we can narrow in on insurance and investing activities which represent the strategic focus of the company and its near-term growth. Monarch, as with all private equity investments, is subject to stages of development and growth. The best formulated plans never unfold in a linear manner but require constant revisiting, modification and improvement. The guarantee of strong returns is not possible without carefully building, monitoring and transparent reporting on progress. Crosswinds is patient but intends to be flexible and open to pursuing change as required to achieve our objectives and safeguard our capital. This is simply a function of the fact that capital demands a return. Too often the same investment mistake is made confusing being patient with patiently building value. Monarch is Crosswinds’ primary investment and it was profitable in 2016 with premiums growing strongly in the second half of the year. This is good news. However, growth in the near term is more challenging and by design to respond to market challenges and concentration of available business, we have stepped back on premium writing. In 2017 we face headwinds: pricing is unfavorable and there has been no regulatory or legislative response to the damaging effects of rising claims costs associated with assignment of benefits (AOB). Monarch does not want to be the taker of risks that are known to have artificially high loss rates attached to them. Actuarial reserves projections suggest that attritional losses will be unacceptably high. As I mentioned, we are patient and we will wait. While we recognize that Crosswinds cannot change how a USD$10 billion per year premium market in homeowners property and casualty insurance behaves, we can identify that there are required legislative and/or regulatory fixes needed for a statewide industry problem. If changes are not made, the private market will adjust and we expect that homeowner insurance premiums will rise and consumers will have fewer choices. Our intended approach is to avoid irrational behavior while seeking underwriting improvements that protect our investment. The best type of insurance market is one where insurers pay legitimate claims quickly and fairly and they equally push back against organized fraud. From our vantage point, much of the AOB activity is tantamount to organized fraud. It is not a question of an insureds proper assignment of a property right to fix a broken sink or toilet but rather a scheme to create an inflated claim and line the pockets of third party non-insureds. There is no legitimate reason for these third parties to enter into the insured to insurer relationship other than fraud. It sounds dire but it is not: it’s a tax on the consumer. Insurers will raise their rates. As we observe these developments, it is not lost upon us that eventually as prices rise, these AOB practices will be seen as unsustainable. Perhaps it will take longer than some would like but Floridians aren’t interested in paying more than required for homeowners insurance due to unscrupulous bad actors. At Crosswinds AUM, we profitably invested the Monarch float with a focus on low portfolio duration and high credit quality. We believe ultimately that higher interest rates will help us, as we have cash to deploy and are actively seeking to add to the portfolio. Part of Crosswinds’ initial attraction to the primary insurance business is equally going to be its biggest risk going forward. Attraction: slow to change; Risk: change is inevitable. The insurance industry has

5

been a slow embracer of technology. The industry does buy and use software tools improve certain functions but it has not to date fully harnessed its capacity to use, analyze and synthesize its own data. It buys stale industry data and tries to match proprietary data to industry wide data. It seems for many in the industry, rather than their own data working for them, they are working for the data. This lack of data management is allowing creative disruptive upstarts to gain market share in many areas including:

1) Distribution; 2) Underwriting Systems; 3) Claims Management; and 4) Risk Management.

We at Crosswinds are excited about these opportunities as they will permit small new players to build innovative models without the industry’s high-cost baggage. Both Monarch and Crosswinds Re are variable cost models. High fixed cost legacy models are hard to fix and disruptive to existing businesses. For 2017, we are not going to hope and pray AOB gets better. We will seek change to improve underwriting procedures to pre-identify the propensity and we will work with our partner to handle these types of claims aggressively. At the same time, we will assess the amount of rate required to stay ahead of the loss curve. On the reinsurance front, pricing is unfavorable and innovation is required. We get asked frequently why Crosswinds has established a reinsurer and why it would seek to “double” its risk by being exposed to both primary insurance and reinsurance. The simple answer is that that is not what we want to do nor what we are doing. In our model, we focus on each dollar of premium generated and its associated risk. Reinsurance is our offensive risk management tool that will allow us to originate premiums. Without a reinsurance vehicle, too many third parties will be taking those premiums and managing our risk. We don’t like that model. We want to control our likely outcomes. We will do so in a low cost and capital efficient manner. If reinsurance rates are insufficient to meet our risk adjusted return targets then we will invest our capital prudently and wait. As we look forward into 2017, we are focused on the following:

• continue to profitably improve the operating performance of Monarch; • activating Crosswinds Re for the 2017 Florida reinsurance renewal season; • raising private capital so we are ready to move on opportunities as they present themselves; • developing a strategy and opportunities in the InsurTech space; • focusing on subsidiary-level contributions to net income and cash flows to achieve sustainable

growing levels in 2018 and beyond. Sincerely, “Colin King” Colin King Chief Executive Officer

6

Management’s Discussion and Analysis Introduction This management’s discussion and analysis (“MD&A”) for Crosswinds Holdings Inc. (“Crosswinds” or the “Company”) includes information designed to help you understand management’s perspective of our audited consolidated financial statements and notes thereto for the year ended December 31, 2016 (“Financial Statements”). This commentary in this MD&A is presented as at December 31, 2016 and updated based on information available up to March 27, 2017.

We encourage you to read our audited consolidated financial statements and the related notes as you review this MD&A. You can find more information about Crosswinds, including our financial statements and our most recent annual information form dated as at March 27, 2017, on our website at www.crosswindsinc.com or on The System for Electronic Document Analysis and Retrieval (“SEDAR”) at www.sedar.com.

The Company’s common shares (“Shares”) are listed and traded on the Toronto Stock Exchange (“TSX”) under the symbol “CWI”.

Unless we have specified otherwise, all dollar amounts in this MD&A are in Canadian dollars. Certain amounts are shown in U.S. dollars (“USD”).

The USD to Canadian dollar closing exchange rate on December 31, 2016 was USD$1.00 = CDN $1.3427 and averaged USD$1.00 = CDN $1.3245 for the year ended December 31, 2016, based in each case on the Bank of Canada closing exchange rates for the applicable period. The Company reports its Financial Statements using accounting policies consistent with International Financial Reporting Standards (“IFRS”).

7

FINANCIAL HIGHLIGHTS FOR THE YEAR ENDED DECEMBER 31, 2016

§ Revenues of $434,570 compared to $595,075 for the same period in 2015; § Net gain from results of investments of $958,675 compared to $19,186 for the same period in 2015;

and § Net loss of $(824,822) or $(0.16) per Share attributable to Crosswinds’ shareholders compared to

net loss of $(1,906,850) or $(0.36) per Share attributable to Crosswinds’ shareholders for the same period in 2015.

FINANCIAL POSITION AS AT DECEMBER 31, 2016

§ Cash of $1,566,053 or $0.30 per Share; § Investment in Monarch of $18,269,925 or $3.44 per Share; § Investment in Salbro valued at $3,052,140 or $0.58 per Share; and § Net book value of $22,812,582 or $4.30 per Share2 of which $20,202,732 or $3.81 per Share2 is

attributable to the shareholders of Crosswinds. 2Net book value per share is a non-IFRS financial measure and is calculated as total shareholders’ equity under IFRS divided by the number of Shares outstanding at period-end. The Company has reported two net book value measures: one reflecting net book value on a consolidated basis including non-controlling interests with respect to the Company’s investment in Monarch and the other reflecting the net book value attributable solely to the Company’s shareholders without non-controlling interests. See the cautionary statement regarding use of non-IFRS financial measures on page 9 of this MD&A.

CAUTION REGARDING FORWARD-LOOKING INFORMATION

This MD&A contains information that is forward-looking and is subject to risks and uncertainties. Forward-looking information includes information concerning the Company’s possible or assumed future operations, financial performance, achievements, results, business strategy, plans, goals, and objectives. Often, but not always, forward-looking statements can be identified by the use of forward-looking words such as “will”, “expect”, “intend”, “plan”, “estimate”, “anticipate”, “believe”, “potential” or “continue”, similar words or words with similar connotation or the negative thereof. These statements are subject to known and unknown risks, uncertainties and other factors that could cause actual results to differ materially from anticipated future results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements are not guarantees and there can be no assurance that the plans, intentions or expectations upon which these forward-looking statements are based will occur.

Factors which could cause actual results to differ materially from those set forth in the forward-looking statements include (but are not limited to): risks associated with general economic conditions; the Company’s dependence on management of portfolio companies and joint venture partners; the limited number and concentration of the Company’s investments; equity prices and credit spreads that could negatively impact the investment portfolio of our investee; heavy regulation of the insurance business and risk of changes in regulation which could reduce the profitability of investments and limit growth; concentration of credit risk; ability to maintain minimum capital and surplus requirements for insurance investments; performance of investments being impacted by business cycles in the property and

8

casualty insurance industry; ratings received by investees by insurance rating agencies and the ability of Monarch to maintain financial or claims paying ability ratings; cycles of insurance market and general economic conditions which can substantially influence Monarch and Monarch’s competitors premium rates and capacity to write new business; exposure to credit risk in the event reinsurers fail to make payments under reinsurance agreements or the insured or Monarch’s general managing agent failing to remit to Monarch premiums owed; timing of claims payments being sooner, or receipt of reinsurance payments being later than anticipated; occurrence of catastrophic events with frequency or severity exceeding our estimates; the Company’s dependence on key personnel and contractors; leverage of the businesses in which the Company invests; the market for the Company’s Shares, limited liquidity and volatility of the Company’s trading price; the trading price of the Company’s Shares relative to the net book value (net asset value); risks affecting the Company’s investments; the need for the Company to make follow-on investments in portfolio companies; use of investment proceeds; investments by the Company in illiquid securities including private issuers; joint investments with third parties; conflicts of interest; no guaranteed returns; risks associated with the implementation of our business, growth and investment strategies; availability and available terms of any required capital to implement corporate objectives and those of portfolio companies; availability and terms of any required financing; availability and timing for receipt of any required regulatory, shareholder or other approvals; the potential loss of investment in Shares; management of the future prospects of the Company; the availability of suitable acquisition opportunities; competition for investments; the Company’s limited operating history in certain segments where it invests; shifts in target exit dates and investment rates of return for investments; tax treatment; fluctuation of currency exchange; remaining eligibility and continued qualification for exchange listing on the stock exchange on which the Company’s Shares trade; changes in market variables including foreign exchange rates, and other risks detailed from time to time in the Company’s continuous disclosure documents.

The reader should not place undue reliance on forward-looking statements and information because they involve significant and diverse risks and uncertainties. By its nature, forward-looking information involves numerous assumptions, inherent risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections and various future events will not occur. Unless otherwise stated, all forward-looking statements speak only as of the date of this MD&A. The Company undertakes no obligation to update publicly or otherwise revise any forward-looking information whether as a result of new information, future events or other such factors which affect this information, except as required by law. These cautionary statements expressly qualify all forward-looking information in this MD&A.

CAUTIONARY STATEMENT REGARDING THE VALUATION OF INVESTMENT IN SALBRO

In the absence of an active market for its investment in Salbro, fair values for this investment are determined by management using the appropriate valuation methodologies after considering the history and nature of the business, operating results and financial conditions, outlook and prospects, general economic, industry and market conditions, capital market and transaction market conditions, contractual rights relating to the investment, public market comparables, private market transaction multiples and, where applicable, other pertinent considerations. The process of valuing investments for which no active market exists is inevitably based on inherent uncertainties and the resulting values may differ from values that would have been used had an active market existed. The amounts at which the Company's investments in private entities could be disposed of may differ from the fair value assigned and the differences could be material.

9

CAUTIONARY STATEMENT REGARDING USE OF NON-IFRS FINANCIAL MEASURES

This MD&A makes reference to the net book value per Share, both on a consolidated basis including non-controlling interests with respect to the Company’s investment in Monarch and on a non-consolidated basis attributable solely to the Company’s shareholders without non-controlling interests. These measures are non-IFRS financial measures. The Company calculates the net book values per Share as it believes it to be an important metric that shareholders use and frequently request and refer to because shareholders often view the Company as a holding company of investments. These non-IFRS financial measures do not have any standardized meaning prescribed by IFRS and therefore are unlikely to be comparable to a similar measure presented by other issuers. This classification is not an IFRS measure and should not be considered either in isolation of, or as a substitute for, a measure prepared in accordance with IFRS.

The Company The following provides a brief overview of the Company and its operations.

Crosswinds is a publicly traded private equity firm and asset manager targeting strategic and opportunistic investments in the financial services sector with a particular focus on the insurance industry. Crosswinds is working to develop a hybrid structure of traditional private equity and a holding company with a view to future flexibility to attract cost effective capital with which to execute its investment strategies, as further described herein. The Company has three key segments to its business which have been designed to work together to capture various components of the value chain of the insurance business: 1. Primary Insurance:

The Company’s investment in Monarch National Insurance Company (“Monarch Insurance”), a Florida-based property and casualty insurance carrier, represents its platform investment in the insurance sector. In the Company’s view, the insurance market in Florida is well positioned for consolidation and greater capital efficiency and presents a number of future opportunities.

In March 2015, the Company completed the formation of a joint venture, creating Monarch Insurance, together with Federated National Holding Company (“Federated National”), an insurance holding company (the “Monarch Joint Venture”). Transatlantic Reinsurance Company (“TransRe”) has a minority position in the Monarch Joint Venture. Monarch Insurance is licensed as an admitted carrier in the State of Florida. An admitted carrier is an insurance company that has received a license from the state department of insurance giving the company the authority to write specific lines of insurance in that state. These companies are also bound by rate and form regulations and are strictly regulated.

The Monarch Joint Venture includes the following entities: Monarch Delaware LLC (“Monarch Parent”), Monarch National Holding Company (“Monarch Holding”) and Monarch Insurance. Monarch Parent, Monarch Holding and Monarch Insurance are referred to collectively as the “Monarch Entities”. The Monarch Entities are a significant investee of the Company. Monarch Parent had an initial equity capitalization of USD $33million. Crosswinds’ economic interest in Monarch Parent is approximately

10

36.4% and Crosswinds controls 50% of the voting rights of Monarch Parent.

2. Reinsurance: The Company established and licensed Crosswinds Re, a specialty reinsurer in the Cayman Islands during 2016. Crosswinds Re has not commenced active business but expects to do so for wind season in Q2 of 2017.

Reinsurance is the highest cost of goods for the insurance industry. Crosswinds Re is expected to be additive to the Company’s primary insurance business and the Monarch Joint Venture, it is intended to profitably enhance the risk management of Monarch and forms an integral part of the Company’s future growth and acquisition strategies. The Company plans to use Crosswinds Re to provide servicing capabilities to the Company’s investees and to be a capital efficient and risk sensitive vehicle with portions of risk retention being redistributed through various channels such as insurance linked securities and retrocessional markets. Initially, Crosswinds Re intends to provide reinsurance to Monarch subject to market conditions and regulatory and other approvals. There can be no assurance that conditions will be favorable or that such approvals will be received. 3. Asset Management: The Company’s wholly-owned subsidiary, Crosswinds AUM LLC (“Crosswinds AUM”) conducts its asset management activities. Crosswinds AUM is a registered investment advisor with the United States Securities and Exchange Commission and manages the assets of the Monarch Entities. Subject to the receipt of any required approvals, Crosswinds AUM is expected to manage the assets of Crosswinds Re once it is further capitalized and active in its operations. The Monarch Entities are party to an Investment Management Agreement (the “Investment Agreement”) with Crosswinds AUM. Crosswinds AUM manages the Monarch Entities’ investment portfolio for an annual management fee calculated as 0.75% of assets under management up to $100 million; 0.50% of assets under management of more than $100 million but less than $200 million; and 0.30% of assets under management of more than $200 million.

4. Legacy: The Company continues to be invested in a legacy private equity investment in Salbro Bottle Inc. and related companies (collectively referred to as “Salbro”) and is actively seeking to monetize this position and focus on growing and expanding its core business segments described above. For a more comprehensive review of the Company and its operations, please refer to other sections of this MD&A including the “Outlook” section and the Company’s most recent annual information form as updated by periodic news releases, all available under the Company’s profile on SEDAR at www.sedar.com.

Operational Review Consolidated Performance Crosswinds achieved profitability in the fourth quarter of 2016. Although the Company’s largest investment, Monarch, has been operating in a challenging environment in Florida and has not grown at the rate initially expected by the Company, Monarch did achieve profitability throughout 2016.

11

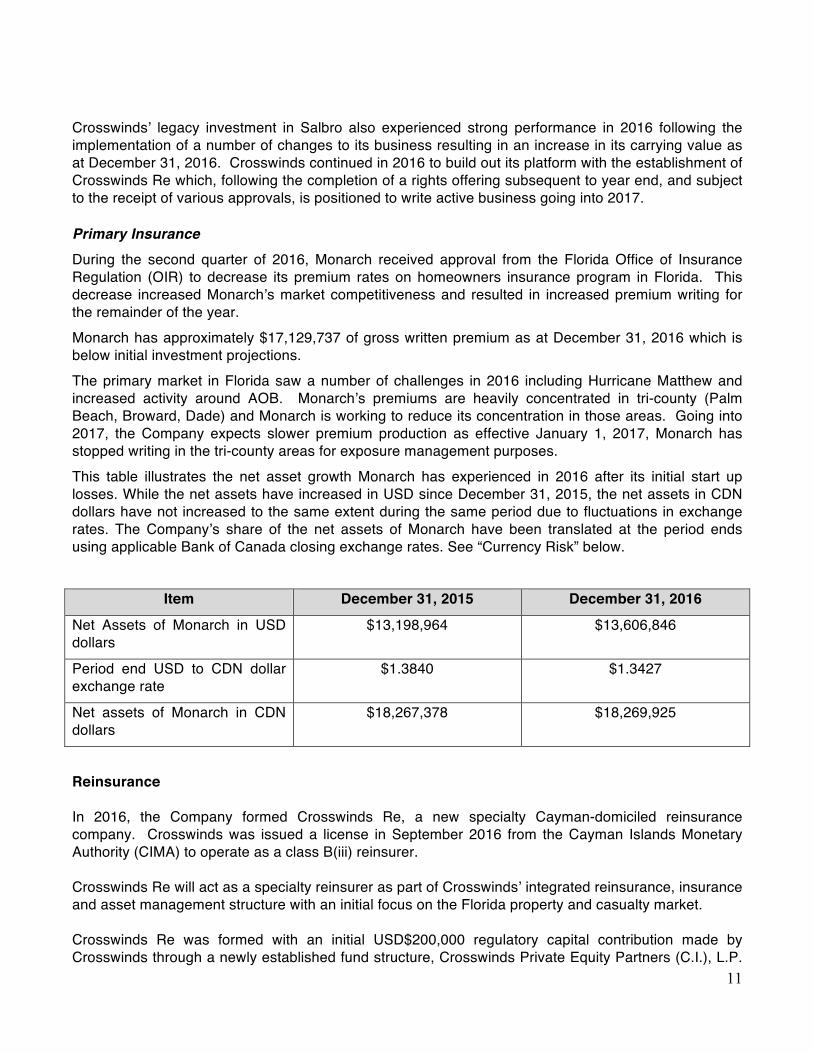

Crosswinds’ legacy investment in Salbro also experienced strong performance in 2016 following the implementation of a number of changes to its business resulting in an increase in its carrying value as at December 31, 2016. Crosswinds continued in 2016 to build out its platform with the establishment of Crosswinds Re which, following the completion of a rights offering subsequent to year end, and subject to the receipt of various approvals, is positioned to write active business going into 2017. Primary Insurance During the second quarter of 2016, Monarch received approval from the Florida Office of Insurance Regulation (OIR) to decrease its premium rates on homeowners insurance program in Florida. This decrease increased Monarch’s market competitiveness and resulted in increased premium writing for the remainder of the year. Monarch has approximately $17,129,737 of gross written premium as at December 31, 2016 which is below initial investment projections. The primary market in Florida saw a number of challenges in 2016 including Hurricane Matthew and increased activity around AOB. Monarch’s premiums are heavily concentrated in tri-county (Palm Beach, Broward, Dade) and Monarch is working to reduce its concentration in those areas. Going into 2017, the Company expects slower premium production as effective January 1, 2017, Monarch has stopped writing in the tri-county areas for exposure management purposes. This table illustrates the net asset growth Monarch has experienced in 2016 after its initial start up losses. While the net assets have increased in USD since December 31, 2015, the net assets in CDN dollars have not increased to the same extent during the same period due to fluctuations in exchange rates. The Company’s share of the net assets of Monarch have been translated at the period ends using applicable Bank of Canada closing exchange rates. See “Currency Risk” below.

Item December 31, 2015 December 31, 2016

Net Assets of Monarch in USD dollars

$13,198,964 $13,606,846

Period end USD to CDN dollar exchange rate

$1.3840 $1.3427

Net assets of Monarch in CDN dollars

$18,267,378 $18,269,925

Reinsurance In 2016, the Company formed Crosswinds Re, a new specialty Cayman-domiciled reinsurance company. Crosswinds was issued a license in September 2016 from the Cayman Islands Monetary Authority (CIMA) to operate as a class B(iii) reinsurer. Crosswinds Re will act as a specialty reinsurer as part of Crosswinds’ integrated reinsurance, insurance and asset management structure with an initial focus on the Florida property and casualty market. Crosswinds Re was formed with an initial USD$200,000 regulatory capital contribution made by Crosswinds through a newly established fund structure, Crosswinds Private Equity Partners (C.I.), L.P.

12

(the “Fund”). The Company is the sole initial limited partner of the Fund and its general partner, Crosswinds Private Equity Partners (C.I.), G.P. is also wholly-owned by Crosswinds. The Fund is intended to be a vehicle for raising additional capital in the future. Crosswinds intends to capitalize Crosswinds Re with approximately $4 million of the proceeds from its rights offering completed in February 2017 to be in a position to write business commencing in Q2 of 2017. Crosswinds Re’s ability to write business will be contingent on market conditions and regulatory and other approvals. Asset Management Crosswinds AUM continued during 2016 to manage the assets for the Monarch Entities. Crosswinds AUM expects to also manage assets for Crosswinds Re as it begins active business operations in 2017. Legacy The Company’s investment in Salbro performed well in 2016, realizing the benefit of a number of operational changes implemented following the repositioning of the investment in December 2015. Material and Significant Events in 2016 The following is a summary of the Company’s material and significant events in 2016, updated for any subsequent events to the date hereof.

13

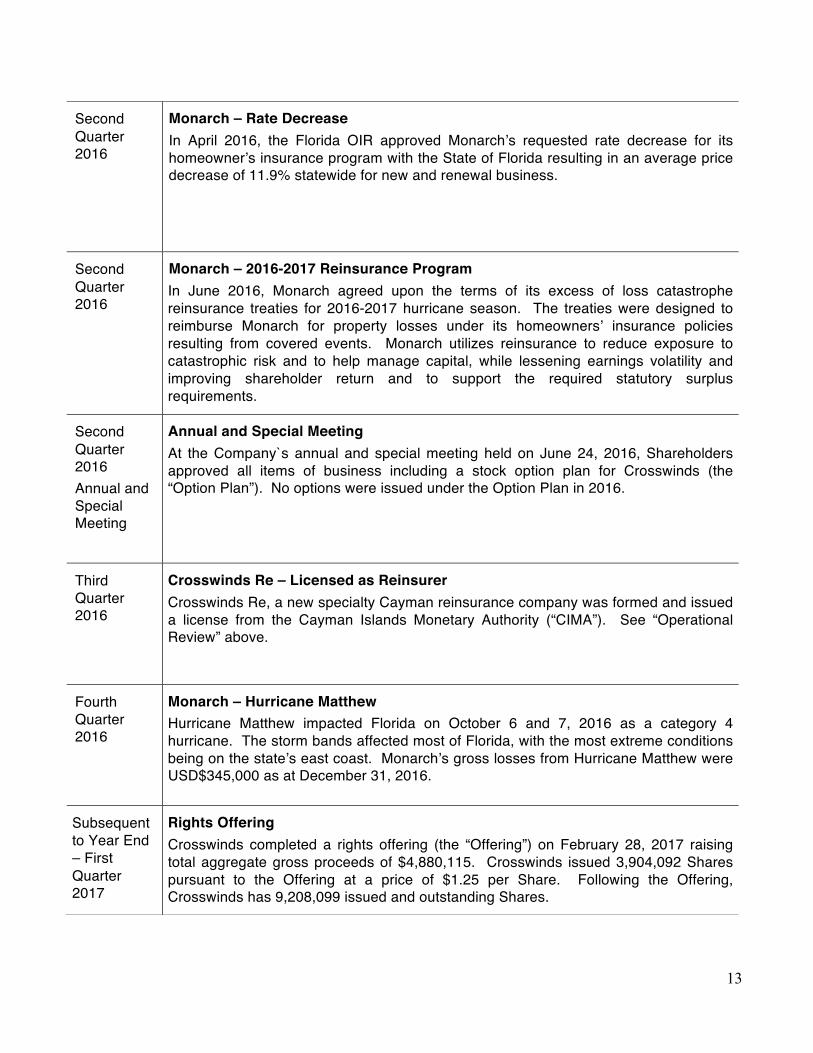

Second Quarter 2016

Monarch – Rate Decrease In April 2016, the Florida OIR approved Monarch’s requested rate decrease for its homeowner’s insurance program with the State of Florida resulting in an average price decrease of 11.9% statewide for new and renewal business.

Second Quarter 2016

Monarch – 2016-2017 Reinsurance Program In June 2016, Monarch agreed upon the terms of its excess of loss catastrophe reinsurance treaties for 2016-2017 hurricane season. The treaties were designed to reimburse Monarch for property losses under its homeowners’ insurance policies resulting from covered events. Monarch utilizes reinsurance to reduce exposure to catastrophic risk and to help manage capital, while lessening earnings volatility and improving shareholder return and to support the required statutory surplus requirements.

Second Quarter 2016 Annual and Special Meeting

Annual and Special Meeting At the Company`s annual and special meeting held on June 24, 2016, Shareholders approved all items of business including a stock option plan for Crosswinds (the “Option Plan”). No options were issued under the Option Plan in 2016.

Third Quarter 2016

Crosswinds Re – Licensed as Reinsurer Crosswinds Re, a new specialty Cayman reinsurance company was formed and issued a license from the Cayman Islands Monetary Authority (“CIMA”). See “Operational Review” above.

Fourth Quarter 2016

Monarch – Hurricane Matthew Hurricane Matthew impacted Florida on October 6 and 7, 2016 as a category 4 hurricane. The storm bands affected most of Florida, with the most extreme conditions being on the state’s east coast. Monarch’s gross losses from Hurricane Matthew were USD$345,000 as at December 31, 2016.

Subsequent to Year End – First Quarter 2017

Rights Offering Crosswinds completed a rights offering (the “Offering”) on February 28, 2017 raising total aggregate gross proceeds of $4,880,115. Crosswinds issued 3,904,092 Shares pursuant to the Offering at a price of $1.25 per Share. Following the Offering, Crosswinds has 9,208,099 issued and outstanding Shares.

14

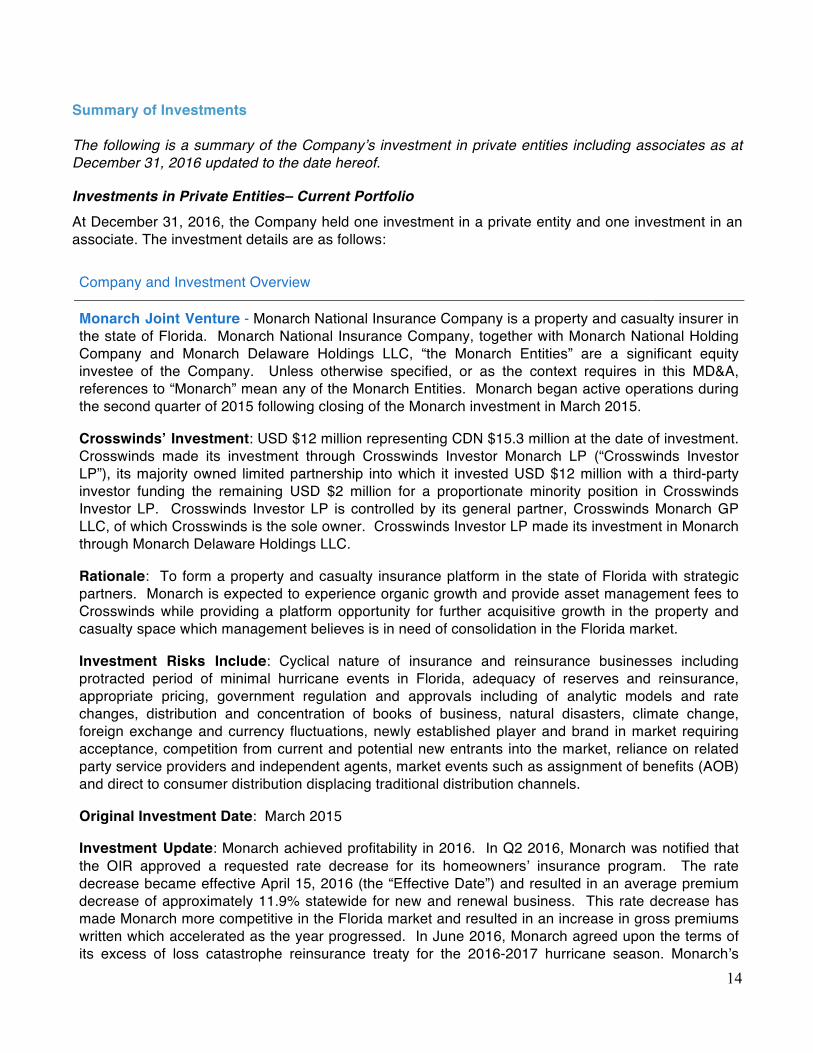

Summary of Investments The following is a summary of the Company’s investment in private entities including associates as at December 31, 2016 updated to the date hereof.

Investments in Private Entities– Current Portfolio At December 31, 2016, the Company held one investment in a private entity and one investment in an associate. The investment details are as follows:

Company and Investment Overview

Monarch Joint Venture - Monarch National Insurance Company is a property and casualty insurer in the state of Florida. Monarch National Insurance Company, together with Monarch National Holding Company and Monarch Delaware Holdings LLC, “the Monarch Entities” are a significant equity investee of the Company. Unless otherwise specified, or as the context requires in this MD&A, references to “Monarch” mean any of the Monarch Entities. Monarch began active operations during the second quarter of 2015 following closing of the Monarch investment in March 2015.

Crosswinds’ Investment: USD $12 million representing CDN $15.3 million at the date of investment. Crosswinds made its investment through Crosswinds Investor Monarch LP (“Crosswinds Investor LP”), its majority owned limited partnership into which it invested USD $12 million with a third-party investor funding the remaining USD $2 million for a proportionate minority position in Crosswinds Investor LP. Crosswinds Investor LP is controlled by its general partner, Crosswinds Monarch GP LLC, of which Crosswinds is the sole owner. Crosswinds Investor LP made its investment in Monarch through Monarch Delaware Holdings LLC.

Rationale: To form a property and casualty insurance platform in the state of Florida with strategic partners. Monarch is expected to experience organic growth and provide asset management fees to Crosswinds while providing a platform opportunity for further acquisitive growth in the property and casualty space which management believes is in need of consolidation in the Florida market.

Investment Risks Include: Cyclical nature of insurance and reinsurance businesses including protracted period of minimal hurricane events in Florida, adequacy of reserves and reinsurance, appropriate pricing, government regulation and approvals including of analytic models and rate changes, distribution and concentration of books of business, natural disasters, climate change, foreign exchange and currency fluctuations, newly established player and brand in market requiring acceptance, competition from current and potential new entrants into the market, reliance on related party service providers and independent agents, market events such as assignment of benefits (AOB) and direct to consumer distribution displacing traditional distribution channels.

Original Investment Date: March 2015

Investment Update: Monarch achieved profitability in 2016. In Q2 2016, Monarch was notified that the OIR approved a requested rate decrease for its homeowners’ insurance program. The rate decrease became effective April 15, 2016 (the “Effective Date”) and resulted in an average premium decrease of approximately 11.9% statewide for new and renewal business. This rate decrease has made Monarch more competitive in the Florida market and resulted in an increase in gross premiums written which accelerated as the year progressed. In June 2016, Monarch agreed upon the terms of its excess of loss catastrophe reinsurance treaty for the 2016-2017 hurricane season. Monarch’s

15

existing book of business is heavily concentrated in the tri-county areas of Florida. Subsequent to year end, as Monarch works to redistribute its book outside of those areas, premium growth has slowed. In 2017, Monarch has turned off production in areas where it has over-concentration. In addition, Florida homeowner insurance companies have been negatively impacted by assignment of benefits (“AOB”), an agreement that, when signed, transfers (“assigns”) a homeowner’s policy rights to a third party such as a contractor. Some contractors have been misusing these provisions to inflate claims. AOB has become an issue for primary insurance companies in Florida as those companies pay inflated claims and also for the insureds as inflated claims costs will eventually be passed on in the form of a rate increase to policyholders. As Monarch is a relatively new business, it has not yet seen a significant impact from AOB however this is an issue that can be expected to impact Monarch in the future, as it has other carriers in Florida, until a broader industry wide solution is found.

Salbro Bottle Inc. and Related Companies (Salbro) is an established designer, manufacturer and distributor of packaging components, specializing in glass and plastic bottles.

Crosswinds’ Investment: Original $4,000,000 investment structured as debentures paying 12% per annum (“Debentures”) and nominal cost common share warrants exercisable into common shares of Salbro (“Warrants”). Following, 2012 and 2015, Salbro made partial repayments to the Company of $1,700,000 and $1,800,000, respectively under the Salbro Debentures. As at December 31, 2016, the aggregate amount outstanding under the Debentures was $1,590,140. The Debentures mature in December 2021 and bear interest at 6% per annum.

Rationale: Growth capital investment in a company with a diversified customer base, an experienced management team, and a combination of complementary manufacturing and distribution businesses to reduce volatility and risk.

Investment Risks Include: Long-term economic slowdown, use of leverage, commodity prices, customer concentration and management execution.

Original Investment Date: February 2008

Investment Update: During 2016, Salbro implemented strategic initiatives and efficiencies including a premises move and certain capital expenditures. Overall, management continues to be of the view that Salbro is performing well and is on track to achieve its budgeted objectives. Following the restructuring of its investment in December 2015, Crosswinds is continuously evaluating opportunities for a realization of its remaining investment in Salbro and during the third quarter of 2016, Crosswinds instituted certain incentives at Salbro to facilitate such a realization in the near to medium term. Crosswinds has written up the carrying value of its investment in Salbro by $608,000 at December 31, 2016. This increase in carrying value reflects management’s view of the improved performance and prospects for the business.

16

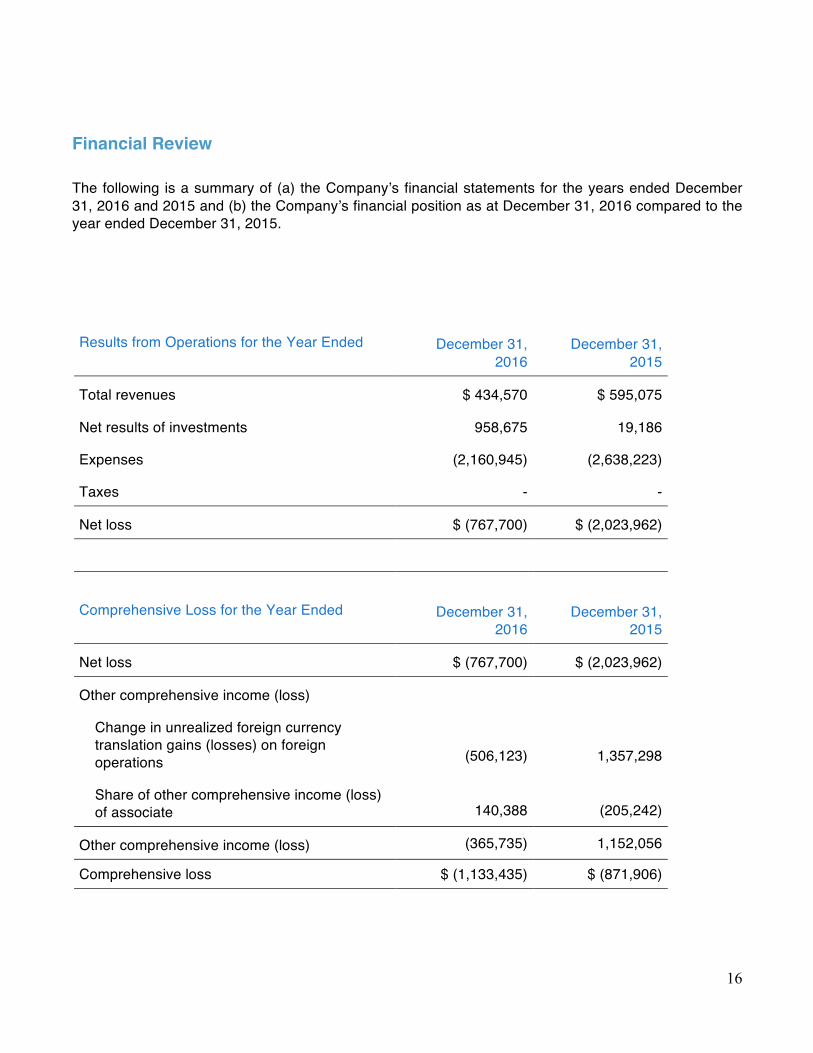

Financial Review The following is a summary of (a) the Company’s financial statements for the years ended December 31, 2016 and 2015 and (b) the Company’s financial position as at December 31, 2016 compared to the year ended December 31, 2015.

Results from Operations for the Year Ended

December 31, 2016

December 31, 2015

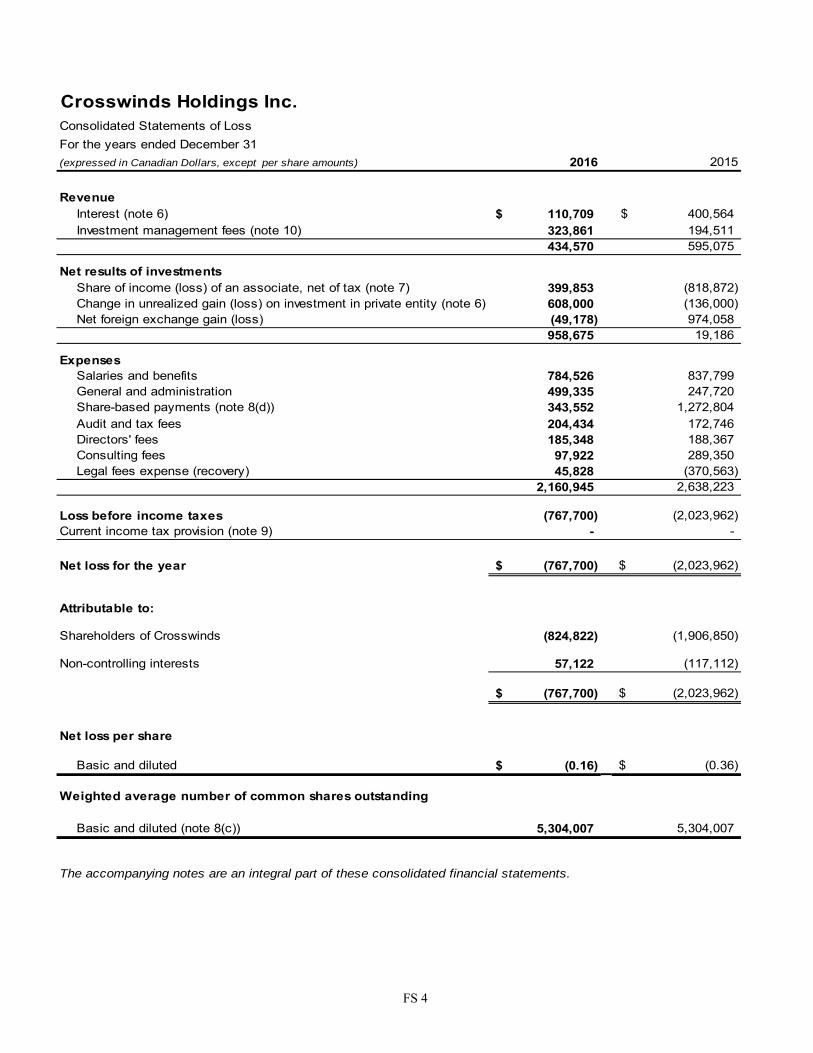

Total revenues $ 434,570 $ 595,075

Net results of investments 958,675 19,186

Expenses (2,160,945) (2,638,223)

Taxes - -

Net loss $ (767,700) $ (2,023,962)

Comprehensive Loss for the Year Ended

December 31, 2016

December 31,

2015

Net loss $ (767,700) $ (2,023,962)

Other comprehensive income (loss)

Change in unrealized foreign currency translation gains (losses) on foreign operations

(506,123)

1,357,298

Share of other comprehensive income (loss) of associate

140,388

(205,242)

Other comprehensive income (loss) (365,735) 1,152,056

Comprehensive loss $ (1,133,435) $ (871,906)

17

Earnings (loss) Per Share (EPS)

Loss per share $ (0.16) $ (0.36)

Financial Position as at Dec 31, 2016 Dec 31, 2015

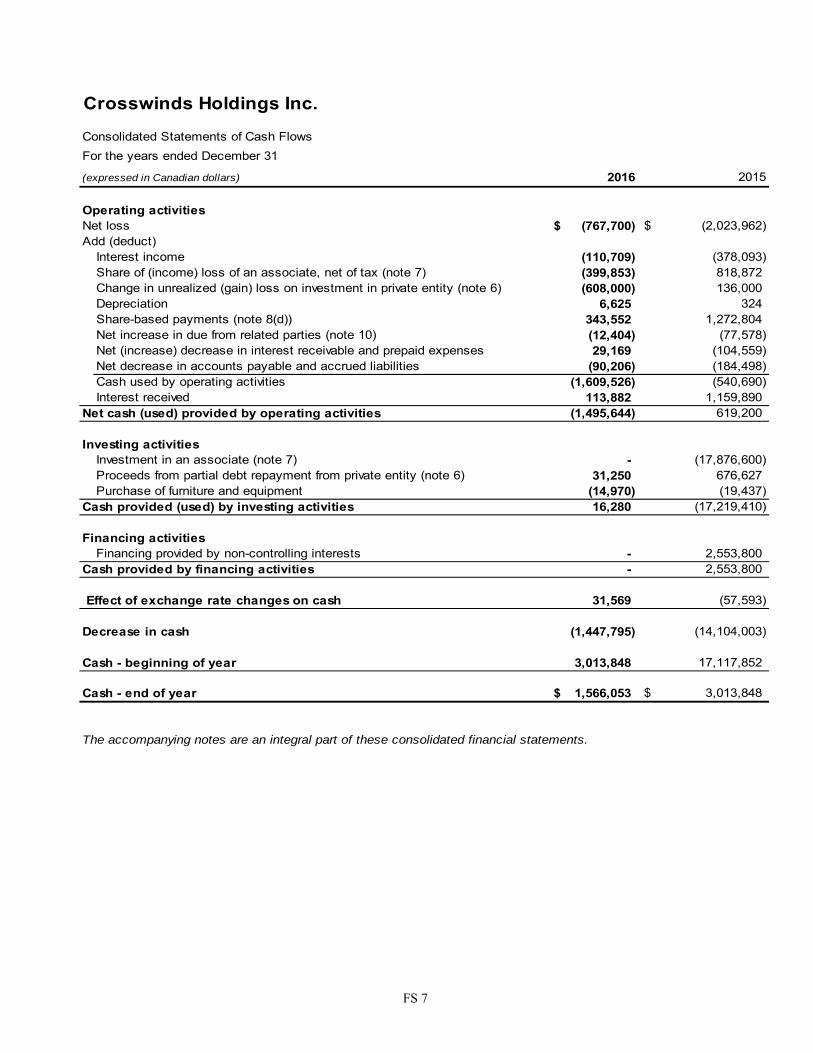

Cash $1,566,053 $ 3,013,848

Total assets 23,089,935 23,970,024

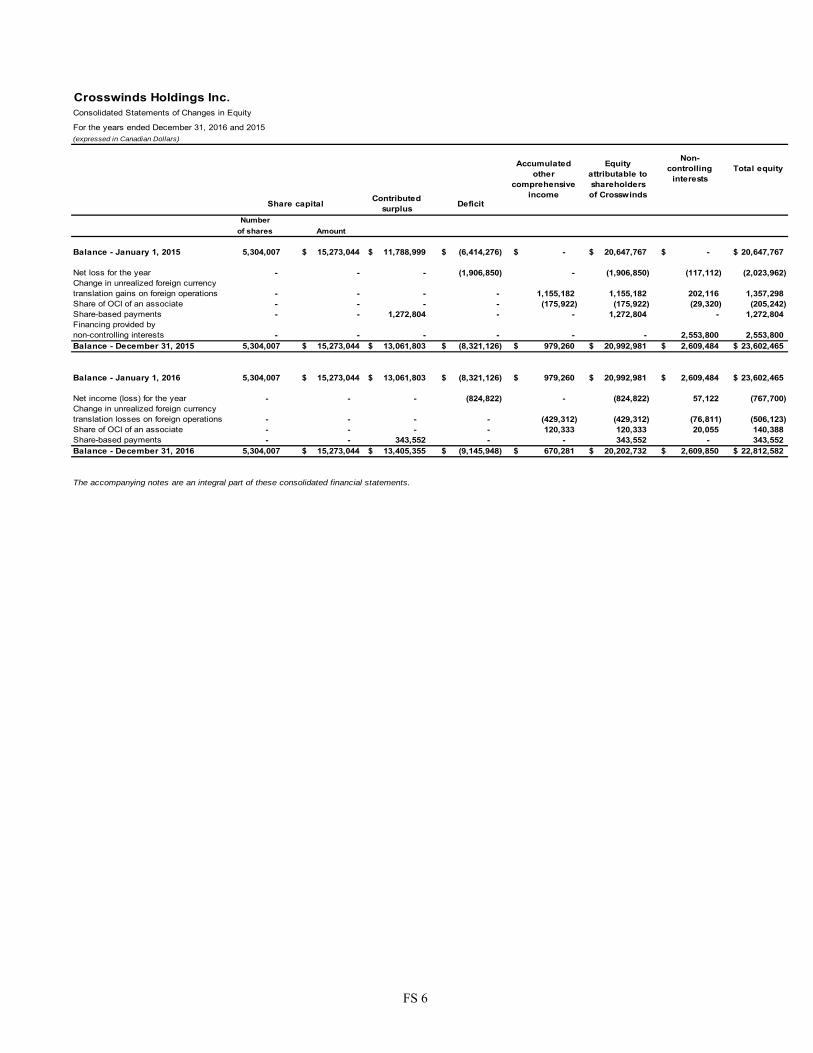

Shareholders’ equity attributable to shareholders of Crosswinds 20,202,732 20,992,981

Number of shares outstanding 5,304,007 5,304,007

Net Book Value Per Share1

Net book value per Share1 $ 4.30 $ 4.45

Attributable to shareholders of Crosswinds Non-controlling interests

3.81 0.49

3.96 0.49

Closing market price on TSX $2.20 $ 5.44

Market price premium/(discount) to net book value attributable to shareholders of Crosswinds

(42.3) %

37.4%

1Net book value per Share is a non-IFRS financial measure and is calculated as total shareholders’ equity under IFRS divided by the number of Shares outstanding at period-end. The Company has reported two net book value measures: one reflecting net book value on a consolidated basis including non-controlling interests with respect to the Company’s investment in Monarch and the other reflecting the net book value attributable solely to the Company’s shareholders without non-controlling interests. See the cautionary statement regarding use of non-IFRS financial measures on page 9 of this MD&A.

Results of Operations Highlights The Company’s operating results reflect (i) revenue recognized primarily from the income generated from the Company’s investments in private entities including Monarch and related asset management activities; (ii) changes in the value of the Company’s assets; and (iii) the expenses required to deploy and manage the Company’s invested capital.

18

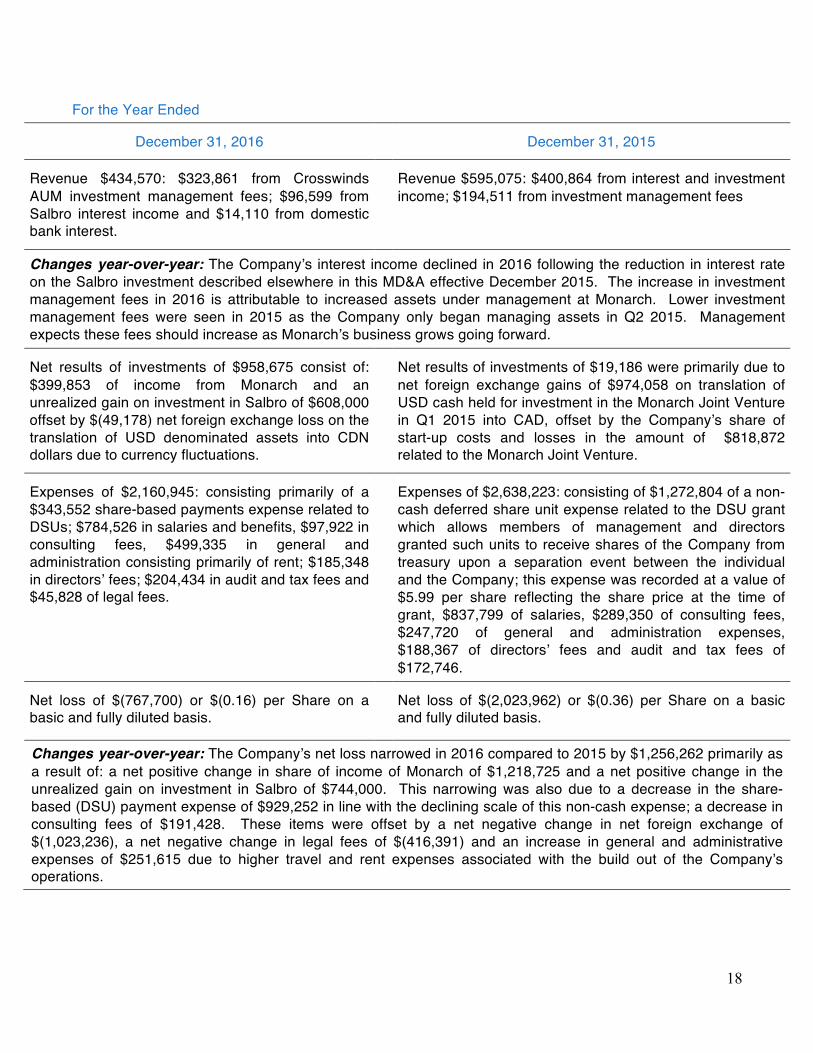

For the Year Ended

December 31, 2016 December 31, 2015

Revenue $434,570: $323,861 from Crosswinds AUM investment management fees; $96,599 from Salbro interest income and $14,110 from domestic bank interest.

Revenue $595,075: $400,864 from interest and investment income; $194,511 from investment management fees

Changes year-over-year: The Company’s interest income declined in 2016 following the reduction in interest rate on the Salbro investment described elsewhere in this MD&A effective December 2015. The increase in investment management fees in 2016 is attributable to increased assets under management at Monarch. Lower investment management fees were seen in 2015 as the Company only began managing assets in Q2 2015. Management expects these fees should increase as Monarch’s business grows going forward.

Net results of investments of $958,675 consist of: $399,853 of income from Monarch and an unrealized gain on investment in Salbro of $608,000 offset by $(49,178) net foreign exchange loss on the translation of USD denominated assets into CDN dollars due to currency fluctuations.

Net results of investments of $19,186 were primarily due to net foreign exchange gains of $974,058 on translation of USD cash held for investment in the Monarch Joint Venture in Q1 2015 into CAD, offset by the Company’s share of start-up costs and losses in the amount of $818,872 related to the Monarch Joint Venture.

Expenses of $2,160,945: consisting primarily of a $343,552 share-based payments expense related to DSUs; $784,526 in salaries and benefits, $97,922 in consulting fees, $499,335 in general and administration consisting primarily of rent; $185,348 in directors’ fees; $204,434 in audit and tax fees and $45,828 of legal fees.

Expenses of $2,638,223: consisting of $1,272,804 of a non-cash deferred share unit expense related to the DSU grant which allows members of management and directors granted such units to receive shares of the Company from treasury upon a separation event between the individual and the Company; this expense was recorded at a value of $5.99 per share reflecting the share price at the time of grant, $837,799 of salaries, $289,350 of consulting fees, $247,720 of general and administration expenses, $188,367 of directors’ fees and audit and tax fees of $172,746.

Net loss of $(767,700) or $(0.16) per Share on a basic and fully diluted basis.

Net loss of $(2,023,962) or $(0.36) per Share on a basic and fully diluted basis.

Changes year-over-year: The Company’s net loss narrowed in 2016 compared to 2015 by $1,256,262 primarily as a result of: a net positive change in share of income of Monarch of $1,218,725 and a net positive change in the unrealized gain on investment in Salbro of $744,000. This narrowing was also due to a decrease in the share-based (DSU) payment expense of $929,252 in line with the declining scale of this non-cash expense; a decrease in consulting fees of $191,428. These items were offset by a net negative change in net foreign exchange of $(1,023,236), a net negative change in legal fees of $(416,391) and an increase in general and administrative expenses of $251,615 due to higher travel and rent expenses associated with the build out of the Company’s operations.

19

Balance Sheet Highlights As at December 31, 2016, the Company’s assets consisted primarily of cash and its investments in Monarch and Salbro. The Company had working capital of $1,463,058 for commitments and general working capital purposes.

In March 2015, the Company, through Crosswinds Investor LP, invested USD $14,000,000 (USD $2,000,000 of which was funded by a third-party investor) in Monarch. In this MD&A, references to equity attributable to Crosswinds refers to the portion of the Monarch investment attributable to Crosswinds, which excludes the third-party investor’s minority interest. At the date of funding of the Monarch investment, the total commitment in CDN dollars was $17,876,600, $15,322,800 of which was funded by and attributable to the Company. The Company is subject to the risk of currency fluctuations. See “Risk Factors” below.

December 31, 2016 December 31, 2015

Total assets of $ 23,089,935 Total assets of $ 23,970,024

Changes: The decrease in assets from December 2015 to 2016 was driven by a decline in cash of $1,447,795 due to payment of corporate expenses offset by the increase in the unrealized gain on investment in Salbro of $574,044.

Equity attributable to shareholders of Crosswinds $ 20,202,732

Equity attributable to shareholders of Crosswinds $20,992,981

Changes: The decrease in equity attributable to shareholders of Crosswinds from December 2015 to 2016 of $790,249 is due to the comprehensive loss attributable to the shareholders of Crosswinds (including the unrealized foreign currency translation loss on the Company’s investment in Monarch) of $1,133,801 offset by an increase in contributed surplus of $343,552 as a result of the share-based payments expense for 2016 related to the issuance of DSUs.

The Company had no debt during any of the periods noted in the table above.

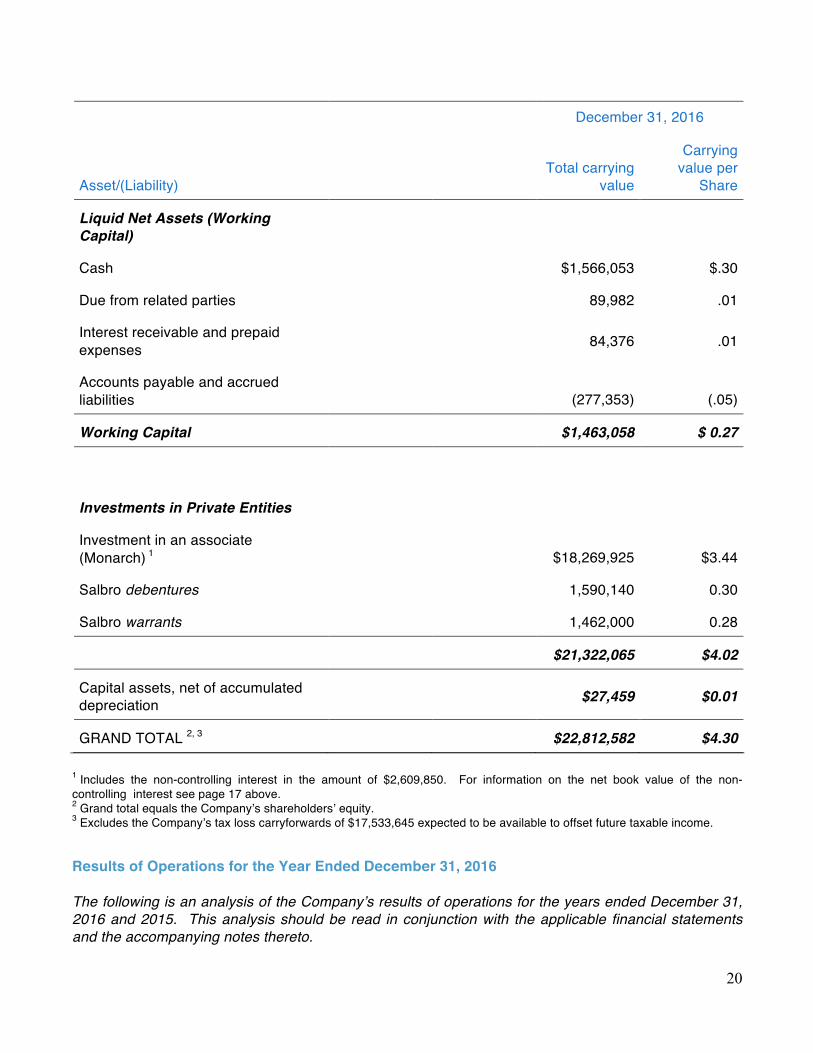

Carrying Value Set out below is the carrying value including carrying value per Share of each of the Company’s assets and liabilities as at December 31, 2016.

20

Asset/(Liability)

December 31, 2016

Total carrying

value

Carrying value per

Share

Liquid Net Assets (Working Capital)

Cash $1,566,053 $.30

Due from related parties 89,982 .01

Interest receivable and prepaid expenses

84,376 .01

Accounts payable and accrued liabilities

(277,353) (.05)

Working Capital $1,463,058 $ 0.27

Investments in Private Entities

Investment in an associate (Monarch) 1 $18,269,925 $3.44

Salbro debentures 1,590,140 0.30

Salbro warrants 1,462,000 0.28

$21,322,065 $4.02

Capital assets, net of accumulated depreciation

$27,459 $0.01

GRAND TOTAL 2, 3 $22,812,582 $4.30 1 Includes the non-controlling interest in the amount of $2,609,850. For information on the net book value of the non-controlling interest see page 17 above. 2 Grand total equals the Company’s shareholders’ equity. 3 Excludes the Company’s tax loss carryforwards of $17,533,645 expected to be available to offset future taxable income.

Results of Operations for the Year Ended December 31, 2016 The following is an analysis of the Company’s results of operations for the years ended December 31, 2016 and 2015. This analysis should be read in conjunction with the applicable financial statements and the accompanying notes thereto.

21

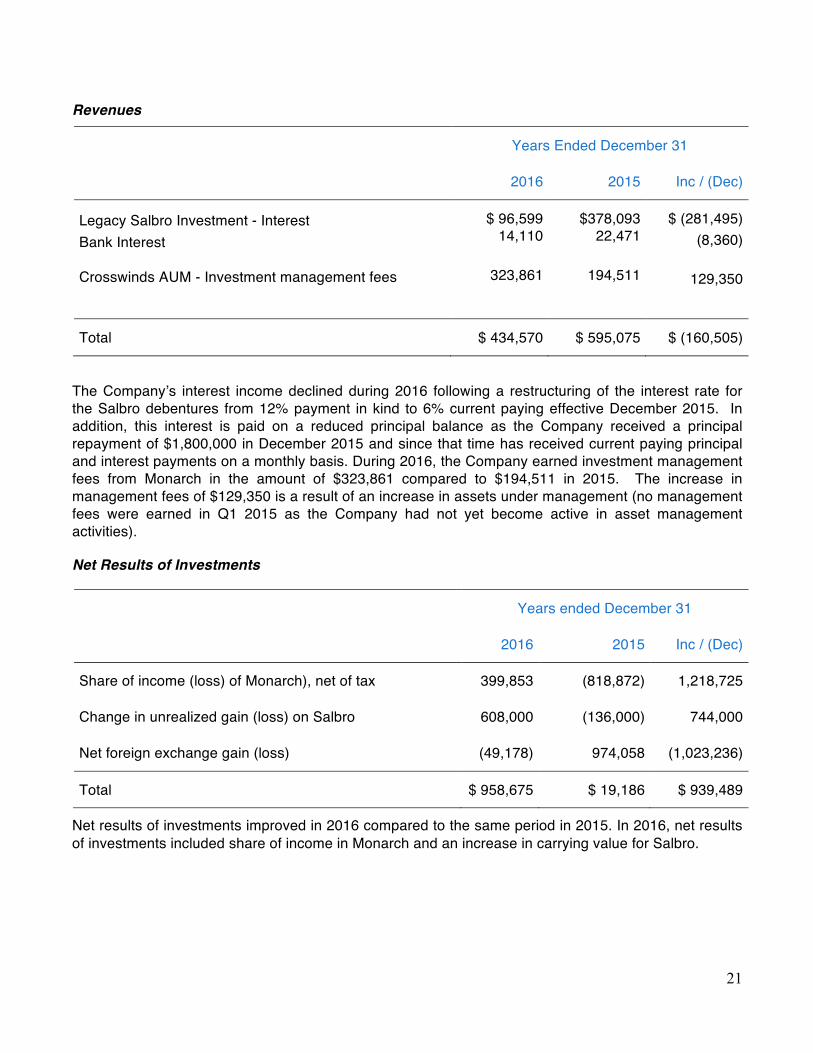

Revenues

Years Ended December 31

2016 2015 Inc / (Dec)

Legacy Salbro Investment - Interest Bank Interest Crosswinds AUM - Investment management fees

$ 96,599 14,110

323,861

$378,093 22,471

194,511

$ (281,495) (8,360)

129,350

Total $ 434,570 $ 595,075 $ (160,505)

The Company’s interest income declined during 2016 following a restructuring of the interest rate for the Salbro debentures from 12% payment in kind to 6% current paying effective December 2015. In addition, this interest is paid on a reduced principal balance as the Company received a principal repayment of $1,800,000 in December 2015 and since that time has received current paying principal and interest payments on a monthly basis. During 2016, the Company earned investment management fees from Monarch in the amount of $323,861 compared to $194,511 in 2015. The increase in management fees of $129,350 is a result of an increase in assets under management (no management fees were earned in Q1 2015 as the Company had not yet become active in asset management activities).

Net Results of Investments

Years ended December 31

2016 2015 Inc / (Dec)

Share of income (loss) of Monarch), net of tax 399,853 (818,872) 1,218,725

Change in unrealized gain (loss) on Salbro 608,000 (136,000) 744,000

Net foreign exchange gain (loss) (49,178) 974,058 (1,023,236)

Total $ 958,675 $ 19,186 $ 939,489

Net results of investments improved in 2016 compared to the same period in 2015. In 2016, net results of investments included share of income in Monarch and an increase in carrying value for Salbro.

22

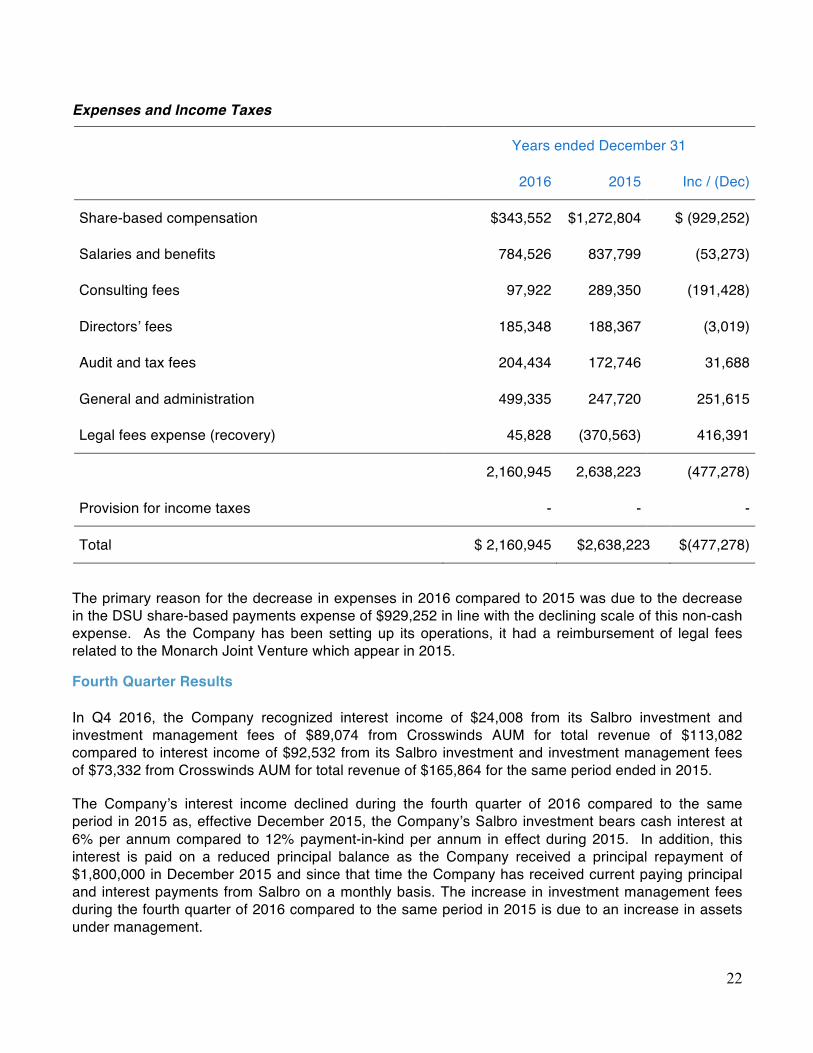

Expenses and Income Taxes

Years ended December 31

2016 2015 Inc / (Dec)

Share-based compensation $343,552 $1,272,804 $ (929,252)

Salaries and benefits 784,526 837,799 (53,273)

Consulting fees 97,922 289,350 (191,428)

Directors’ fees 185,348 188,367 (3,019)

Audit and tax fees 204,434 172,746 31,688

General and administration 499,335 247,720 251,615

Legal fees expense (recovery) 45,828 (370,563) 416,391

2,160,945 2,638,223 (477,278)

Provision for income taxes - - -

Total $ 2,160,945 $2,638,223 $(477,278)

The primary reason for the decrease in expenses in 2016 compared to 2015 was due to the decrease in the DSU share-based payments expense of $929,252 in line with the declining scale of this non-cash expense. As the Company has been setting up its operations, it had a reimbursement of legal fees related to the Monarch Joint Venture which appear in 2015.

Fourth Quarter Results In Q4 2016, the Company recognized interest income of $24,008 from its Salbro investment and investment management fees of $89,074 from Crosswinds AUM for total revenue of $113,082 compared to interest income of $92,532 from its Salbro investment and investment management fees of $73,332 from Crosswinds AUM for total revenue of $165,864 for the same period ended in 2015.

The Company’s interest income declined during the fourth quarter of 2016 compared to the same period in 2015 as, effective December 2015, the Company’s Salbro investment bears cash interest at 6% per annum compared to 12% payment-in-kind per annum in effect during 2015. In addition, this interest is paid on a reduced principal balance as the Company received a principal repayment of $1,800,000 in December 2015 and since that time the Company has received current paying principal and interest payments from Salbro on a monthly basis. The increase in investment management fees during the fourth quarter of 2016 compared to the same period in 2015 is due to an increase in assets under management.

23

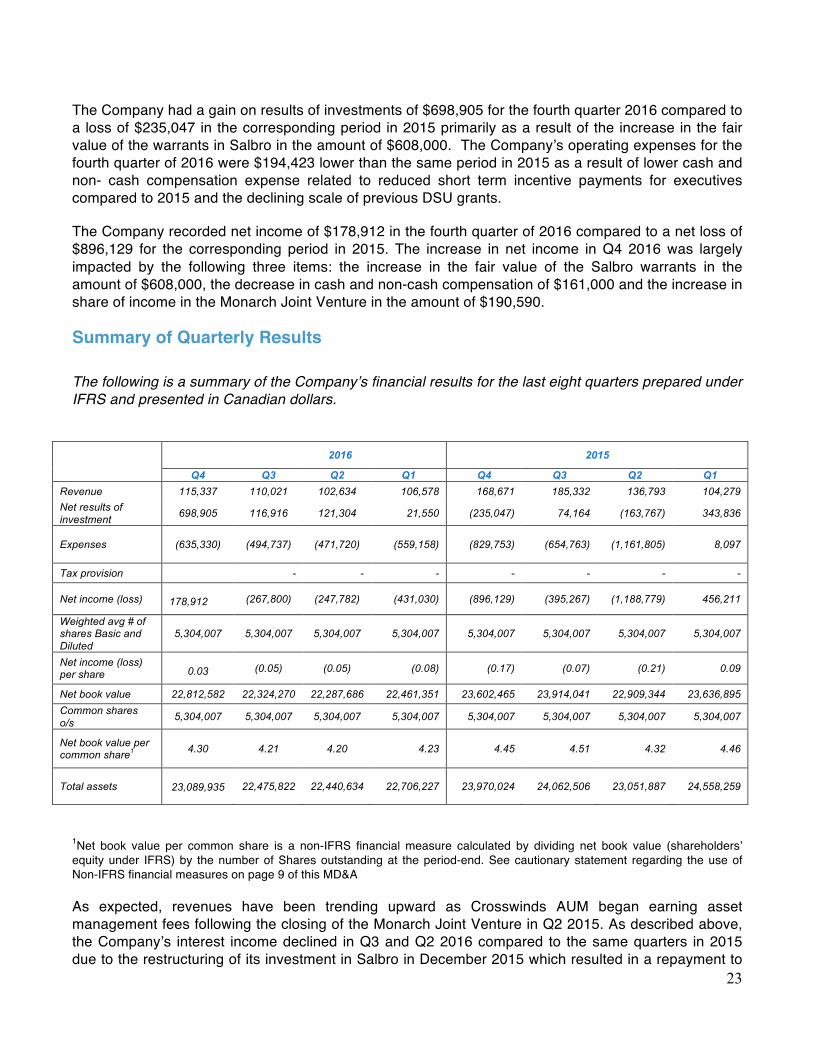

The Company had a gain on results of investments of $698,905 for the fourth quarter 2016 compared to a loss of $235,047 in the corresponding period in 2015 primarily as a result of the increase in the fair value of the warrants in Salbro in the amount of $608,000. The Company’s operating expenses for the fourth quarter of 2016 were $194,423 lower than the same period in 2015 as a result of lower cash and non- cash compensation expense related to reduced short term incentive payments for executives compared to 2015 and the declining scale of previous DSU grants.

The Company recorded net income of $178,912 in the fourth quarter of 2016 compared to a net loss of $896,129 for the corresponding period in 2015. The increase in net income in Q4 2016 was largely impacted by the following three items: the increase in the fair value of the Salbro warrants in the amount of $608,000, the decrease in cash and non-cash compensation of $161,000 and the increase in share of income in the Monarch Joint Venture in the amount of $190,590.

Summary of Quarterly Results The following is a summary of the Company’s financial results for the last eight quarters prepared under IFRS and presented in Canadian dollars.

2016 2015

Q4 Q3 Q2 Q1 Q4 Q3 Q2 Q1 Revenue 115,337 110,021 102,634 106,578 168,671 185,332 136,793 104,279 Net results of investment 698,905 116,916 121,304 21,550 (235,047) 74,164 (163,767) 343,836

Expenses

(635,330)

(494,737) (471,720) (559,158) (829,753) (654,763) (1,161,805) 8,097

Tax provision - - - - - - -

Net income (loss) 178,912 (267,800) (247,782) (431,030) (896,129) (395,267) (1,188,779) 456,211

Weighted avg # of shares Basic and Diluted

5,304,007 5,304,007 5,304,007 5,304,007 5,304,007 5,304,007 5,304,007 5,304,007

Net income (loss) per share

0.03 (0.05) (0.05) (0.08) (0.17) (0.07) (0.21) 0.09

Net book value 22,812,582 22,324,270 22,287,686 22,461,351 23,602,465 23,914,041 22,909,344 23,636,895 Common shares o/s 5,304,007 5,304,007 5,304,007 5,304,007 5,304,007 5,304,007 5,304,007 5,304,007

Net book value per common share1 4.30 4.21 4.20 4.23 4.45 4.51 4.32 4.46

Total assets

23,089,935 22,475,822 22,440,634 22,706,227 23,970,024 24,062,506 23,051,887 24,558,259

1Net book value per common share is a non-IFRS financial measure calculated by dividing net book value (shareholders’ equity under IFRS) by the number of Shares outstanding at the period-end. See cautionary statement regarding the use of Non-IFRS financial measures on page 9 of this MD&A

As expected, revenues have been trending upward as Crosswinds AUM began earning asset management fees following the closing of the Monarch Joint Venture in Q2 2015. As described above, the Company’s interest income declined in Q3 and Q2 2016 compared to the same quarters in 2015 due to the restructuring of its investment in Salbro in December 2015 which resulted in a repayment to

24

the Company of $1,800,000 and a reduction in interest rate on the remaining debenture amount outstanding from 12% to 6%.

Net results of investments vary on a quarter-to-quarter basis due to net foreign exchange gains related to USD denominated assets, realized gains or losses on investments and also due to unrealized gains or losses on investments being measured at fair value on the balance sheet.

During 2015, the Company’s results reflect a number of one-time expenses including foreign exchange fluctuations and start-up and other one-time costs related to the Monarch Joint Venture which have caused variability in the Company’s performance. The non-cash DSU grant also had an impact on the Company’s expenses on a declining scale basis in each of the quarters after Q1 2015. Foreign exchange fluctuations have also caused significant variation in reported performance for the Company as described herein.

Liquidity, Capital Resources and Off-Balance Sheet Arrangements The following is an analysis of the liquidity, capital resources and off-balance sheet arrangements of the Company and should be read in conjunction with the audited annual financial statements for the years ended December 31, 2016 and 2015 and the corresponding notes thereto.

Liquidity The Company had working capital of $1,463,058 at December 31, 2016 (December 31, 2015 - $2,837,878). The Company’s cash consists of deposits with chartered banks in Canada and the U.S.

The Company calculates its working capital as follows:

Working Capital December 31, 2016 December 31, 2015

Cash $1,566,053 $ 3,013,848

Due from related parties 89,982 77,578

Interest receivable and prepaid expenses

84,376 114,011

Accounts payable and accrued liabilities (277,353) (367,559)

Working capital $1,463,058 $ 2,837,878

Total per Share $ 0.29 $ 0.54

The Company worked on developing a strategy to generate liquidity in 2016 and as a part of that strategy completed a rights offering in the first quarter of 2017 raising gross proceeds of $4,880,115. See “Operational Review – Material and Significant Events – Rights Offering” above. The Company believes it now has sufficient working capital to support its near-term needs having monetized a portion of its Salbro investment in the amount of $1,800,000 at the end of 2015 and, subsequent to year end,

25

having raised funds in the rights offering. At year end, prior to the rights offering, the Company had sufficient funds for its near term needs but was constrained in its ability to begin active operations for Crosswinds Re. The Company is expending cash in excess of its revenues as it continues to build out its infrastructure. As the Company works to implement its planned growth activities, management expects it will need to raise new capital and continues to explore options to do so through additional private and/or public fund raising.

The Company established Crosswinds Re during the Q3 2016 and made a regulatory capital contribution through a newly established fund structure, Crosswinds Private Equity Partners (C.I.), L.P. (the “Fund”). Crosswinds is the sole initial limited partner of the Fund. The Fund’s general partner, Crosswinds Private Equity Partners (C.I.). G.P. is wholly-owned by Crosswinds. Crosswinds currently intends to use the Fund as a vehicle to raise additional capital for Crosswinds Re to execute its business plan of acting as a specialty reinsurer as part of Crosswinds’ integrated insurance, reinsurance and asset management structure with an initial focus on the Florida property and casualty insurance market. There can be no assurance that such funds will be available or if they are available that they will be available on commercially favorable terms.

There are contractual and legal restrictions on the ability of Monarch to transfer funds to its owners including Crosswinds. As Crosswinds regards Monarch as a long-term investment, this is not expected to have an impact on the Company’s short term liquidity. Our reinsurance subsidiary, Crosswinds Re, which is domiciled in Cayman Islands, is required by CIMA to maintain minimum capital levels. As of December 31, 2016, the capital maintained by Crosswinds Re was in excess of the regulatory capital requirement in Cayman Islands. USD $200,000 of the amount shown as cash in the table above is required to meet Crosswinds Re’s minimum capital requirements and as such is not accessible cash to Crosswinds for such time as Crosswinds desires to maintain its licensed reinsurance entity. The Company intends to invest approximately $4 million in Crosswinds Re from the proceeds of the rights offering completed subsequent to year end.

Capital Resources

At December 31, 2016, the Company had no long-term debt or capital lease obligations. The Company entered into a premises lease agreement in Q3 of 2015 for approximately 3,000 square feet of office space located at 14 Wall Street, New York, New York. The Company’s payment commitments under the premises lease are set out below:

Share Capital As at the date hereof, following completion of the Rights Offering, there are 9,208,099 Shares outstanding and as at December 31, 2016, there were 5,304,007 (2015 – 5,304,007) Shares were outstanding. The Company reported a net book value at December 31, 2016 of $22,812,582 (2015 – $23,602,465) or $4.30 per Share (2015 - $4.45) of which $20,202,732 (2015 – $20,992,981) or $3.81

Payments due by period

At December 31, 2016 TOTAL < 1 year 1-2 years 3-5 years after 5 years

Operating lease 785,722$ 197,199$ 202,661$ 385,862$ -$

26

per Share (2015 - $3.96) is attributable to shareholders of the Company1. See the cautionary statement regarding the use of non-IFRS financial measures on page 9 of this MD&A.

1 Net book value per share is a non-IFRS financial measure and is calculated as total shareholders’ equity under IFRS divided by the number of Shares outstanding at period-end. The Company has reported two net book value measures: one reflecting net book value on a consolidated basis including non-controlling interests with respect to the Company’s investment in the Monarch Joint Venture and the other reflecting the net book value attributable solely to the Company’s shareholders without non-controlling interests.

The Company has adopted an Option Plan which was approved by the Company’s shareholders on June 24, 2016. No options are outstanding under the Stock Option Plan as at December 31, 2016.

The Company also has a DSU Plan. On April 15, 2015, the Company issued an aggregate of 260,000 DSUs to certain of its directors and officers pursuant to the terms of the DSU Plan. As at December 31, 2016, all DSUs from this grant had vested. On November 17, 2016, the Company granted 34,332 units to certain directors as part of their annual retainer fees at a grant price of $2.81. At December 31, 2016, an aggregate of 11,444 DSUs had vested under this grant with the remaining 22,888 DSUs vesting in equal amounts in the first and second quarters of 2017.

The maximum number of Shares that can be issued on exercise of options granted under the Option Plan may not exceed 10% of the issued and outstanding Shares of the Company from time to time, less the number of Shares issued under all other security based compensation arrangements of the Company including the DSU Plan.

Off-Balance Sheet Arrangements Except as otherwise described herein, the Company currently has no off-balance sheet arrangements

Proposed Transactions The Company has no proposed asset or business acquisitions or dispositions at this time.

Transactions with Related Parties Investment Management Services Agreement In conjunction with the closing of the Monarch Joint Venture, Crosswinds AUM, entered into an investment management services agreement with Monarch. Under the agreement, Crosswinds AUM has agreed to act as investment advisor and to manage the assets of the Monarch entities for a management fee paid quarterly in arrears. For the year ended December 31, 2016, Crosswinds AUM earned investment management fee income in the amount of $323,861 (2015 - $ 194,511). As at December 31, 2016, $89,982 (2015 - $77,578) was still owed to the Company and was included in due from related parties on the consolidated statements of financial position.

Changes in Accounting Policies and Critical Accounting Estimates The Company’s financial statements have been prepared in accordance with IFRS.

27

Critical Accounting Estimates

In the application of the Company’s accounting policies, management is required to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily available from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

(a) Critical judgments in applying accounting policies The following are the critical judgments, apart from those involving estimations (see below), that management has made in the process of applying the Company’s accounting policies and that have the most significant effect on the amounts recognized in the Company’s financial statements for the year ended December 31, 2016. Functional currency The currency of the primary economic environment in which the Company operates is the Canadian dollar as this is the currency in which the Company measures its performance and also issues and purchases for cancellation its Shares. Interests in other entities

As part of its process in determining the classification of its interests in other entities, the Company applies judgment in interpreting these interests such as (i) the determination of the level of control or significant influence held by the Company; (ii) the applicability of relevant IFRS standards to the operations; (iii) the legal structure and contractual terms of the arrangement; and (iv) when relevant, other facts and circumstances. The Company has concluded that its investment in Monarch Parent represents an investment in an associate as described in IAS 28, “Investments in Associates and Joint Ventures”. All other interests in other entities have been determined to be subsidiaries as described in IFRS 10, “Consolidated Financial Statements”.

(b) Key sources of estimation uncertainty

The following are the key assumptions concerning the future, and other key sources of estimation uncertainty at the Company’s statements of financial position date reflected in the Company’s financial statements as at December 31, 2016, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year. Fair value of securities not quoted in an active market and over-the-counter derivative instruments. Management uses its judgment in selecting an appropriate valuation technique for financial

28

instruments that are not quoted in an active market. Valuation techniques commonly used by market practitioners are applied. For derivative financial instruments, assumptions are made based on quoted market rates adjusted for specific features of the instrument. Other financial instruments are valued using a discounted cash flow analysis based on assumptions supported, where possible, by observable market prices or rates. The estimation of fair value of unlisted shares includes some assumptions not supported by observable market prices or rates.

The Company’s critical accounting estimates are primarily limited to valuing its investments. The valuation methods and the techniques it employs in valuing its investments and the assumptions used are described below. Salbro Bottle Inc. and Related Companies (“Salbro”) The fair market value of Salbro was determined on a going concern basis under an income approach on the assumption that a hypothetical purchaser would acquire Salbro on the expectation of future earnings and cash flows. Specifically, the Company selected an EBITDA multiple method as the valuation methodology given that Salbro is a mature business and is expected to continue to operate as a going concern and historical EBITDA is a good approximation of expected profitability going forward. This valuation method estimates the net enterprise value by (i) performing an analysis of the maintainable EBITDA; (ii) applying an enterprise value/twelve-month trailing EBITDA multiple; and (iii) deducting any indebtedness. Where the Company uses a multiple of publicly traded companies or precedent transactions to derive an appropriate range of multiples it will apply, the multiples chosen are typically below the average comparables surveyed to recognize the Company’s minority equity position and the fact that Salbro is privately held. An EBITDA multiple of 8.5 was used to value Salbro as at December 31, 2016. Different assumptions were used to derive a range of valuations used to arrive at an estimate. A 1x change in the EBITDA multiple would have increased or decreased the value of the investment by approximately $262,000 at December 31, 2016. The carrying amount of the Salbro investment at December 31, 2016 was $3,052,140 (2015 - $2,478,096).

Recent accounting pronouncements

This section describes standards, amendments and interpretations that have been issued but are not yet effective for annual reporting periods ended December 31, 2016.

The International Accounting Standards Board (“IASB”) has issued the following new accounting pronouncements that will be applicable to the Company: IFRS 9 Financial Instruments

The standard was issued in its final version by the International Accounting Standards Board (“IASB”) in July 2014 bringing together the classification and measurement, impairment and hedge accounting phases of the IASB’s project to replace IAS 39, “Financial instruments: recognition and measurement” (“IAS 39”). The standard retains but simplifies the mixed measurement model and establishes two

29

primary measurement categories for financial assets: amortized cost and fair value. The mandatory effective date of IFRS 9 is for annual periods beginning on or after January 1, 2018, with early adoption permitted. The Company is assessing the impact of this standard.

IFRS 15 - Revenue from Contracts with Customers

This standard was issued by the IASB on May 28, 2014, and amended on April 12, 2016, and will replace IAS 18, “Revenue”, IAS 11 “Construction Contracts”, and related interpretations on revenue. IFRS 15 sets out the requirements for recognizing revenue that apply to all contracts with customers, except for contracts that are within the scope of the standards on leases, insurance contracts and financial instruments. IFRS 15 uses a control based approach to recognize revenue which is a change from the risk and reward approach under the current standard. Companies can elect to use either a full or modified retrospective approach when adopting this standard and it is effective for annual periods beginning on or after January 1, 2018 with early adoption permitted. The Company is assessing the impact of this standard.

IFRS 16 – Leases

The standard was issued by the IASB on January 13, 2016, and will replace IAS 17, “Leases”. IFRS 16 will bring most leases on-balance sheet for lessees under a single model, eliminating the distinction between operating and financing leases. Lessor accounting however remains largely unchanged and the distinction between operating and finance leases is retained. The new standard is effective for annual periods beginning on or after January 1, 2019 with early adoption permitted if IFRS 15 has also been applied. The Company is assessing the impact of this standard.

Factors that May Affect Future Results Future results of the Company will depend on the strategies it implements from time to time including the Company’s ability to execute on its intentions with respect to growth of its complementary business lines and the success of any capital raising activities. The Company will require additional capital to complete some of its initiatives including capitalizing on investment opportunities as they arise and its ability to raise that capital will depend among other things on general economic conditions. As the Company is working to develop additional lines of business, past performance should not generally be viewed as indicative of future results.

The Company continues to seek investment opportunities meeting the criteria set out elsewhere in this MD&A and its AIF. There can be no guarantee that any prospective initiatives or transactions described herein will be successfully executed and, if executed, yield satisfactory risk-adjusted returns. While seeking new investment opportunities, the Company’s revenues will be constrained.

Controls and Procedures Disclosure Controls and Procedures The Company’s controls and procedures are designed to provide reasonable assurance that information required to be disclosed by the Company in its corporate filings is recorded, processed, summarized and reported within the time periods specified under securities laws and include controls and procedures that are designed to ensure that information is accumulated and communicated to management including the Chief Executive Officer and Interim Chief Financial Officer (collectively, the Certifying Officers) to allow timely decisions regarding disclosure. As at December 31, 2016 the Certifying Officers evaluated the effectiveness of the Company’s disclosure controls and procedures as defined under National Instrument 52-109 – Certification of Disclosure in Issuer’s Annual and Interim

30

Filings. Based on that evaluation, the Certifying Officers concluded that the Company’s disclosure controls and procedures were appropriately designed as at December 31, 2016.

Consistent with the concept of reasonable assurance, the Company recognizes that the relative cost of maintaining these controls should not exceed their expected benefits. In addition, a control system, no matter how well conceived and operated can provide only reasonable, not absolute, assurance that its objectives are met. Due to inherent limitations in all such systems, no evaluations of controls can provide absolute assurance that all control issues, if any, within a company have been detected. As such, the Company’s disclosure controls and procedures can only provide reasonable, and not absolute, assurance that the objectives of such controls and procedures are met.

Internal Controls over Financial Reporting The Company’s internal controls over financial reporting are a process designed under the supervision of the Certifying Officers to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with IFRS. However, because of its inherent limitations, internal controls over financial reporting may not prevent or detect misstatements on a timely basis. The Certifying Officers evaluated the effectiveness of the Company’s internal controls over financial reporting as at December 31, 2016, based on the framework and criteria established in the Internal Control – Integrated Framework published by the Committee of Sponsoring Organizations of the Treadway Commission (COSO 2013 Framework). Based on that evaluation, the Certifying Officers concluded that the Company’s internal control over financial reporting was appropriately designed as at December 31, 2016. There were no material weaknesses that have been identified by the Certifying Officers as at December 31, 2016. There have been no changes during the year ended December 31, 2015 in the Company’s internal controls over financial reporting that have materially affected, or are reasonably likely to materially affect, the Company’s internal controls over financial reporting.

Consistent with the concept of reasonable assurance, the Company recognizes that the relative cost of maintaining these controls should not exceed their expected benefits. In addition, a control system, no matter how well conceived and operated can provide only reasonable, not absolute, assurance that its objectives are met. Due to inherent limitations in all such systems, no evaluations of controls can provide absolute assurance that all control issues, if any, within a company have been detected. As such, the Company’s internal controls over financial reporting can only provide reasonable, and not absolute, assurance that the objectives of such controls are met.

Outlook The Company has a number of initiatives it is targeting for advancement in 2017 and management views (i) Monarch Insurance company’s growth and earnings, (ii) increasing asset management fees, (iii) earnings from Crosswinds Re once actively writing business; and (iii) fees (if any) associated with any future fund vehicles as all being key to the Company’s near term future results. Monarch’s performance is an important component of the implementation of Crosswinds’ broader strategy integrating insurance, reinsurance and asset management and the related revenue to be generated by each component of that strategy. Increased market acceptance and premium growth in Monarch will be key to Crosswinds’ overall performance in the short term. After some initial benefit in premium writing following the rate decrease in April 2016, concentration of Monarch’s book of business has had a negative impact on premium writing and management currently expects slow organic growth for Monarch in 2017.

31

In order to fully execute its acquisition strategy and support the funding of its reinsurance entity, the Company will need to raise significant amounts of additional capital. The Company started this process with the Rights Offering raising approximately $4 million which it plans to deploy in 2017. The Company is exploring options to raise additional capital and/or create one or more private equity funds. Without such additional capital, the Company’s ability to expand its business and capitalize on identified opportunities will be constrained. Management believes that Crosswinds is well positioned for growth in Crosswinds Re in 2017, having raised funds for its initial capitalization which should enable it, subject to market conditions and other approvals, to write some business during wind season. Following completion of the Monarch Joint Venture, as the majority of the Company’s assets are valued in USD, the overall value of the Company expressed in Canadian dollars will fluctuate based on the relative value of the Canadian dollar to the USD. Results may vary substantially from year to year and quarter to quarter due to the stage of development of the Company’s business and its new investment activities.

Financial Risk Management and Risk Factors Financial Risk Management The Company’s business is affected by a number of economic factors, including changing economic environments, capital markets and interest rates. As a result, the Company faces various risk factors, inherent in its normal business activities. These risk factors and the management thereof are described below.

The Company attempts to manage the risks associated with its business and investment portfolio through planning, significant due diligence of investment opportunities, and active involvement in and monitoring of its investments.

Investments in private entities are less liquid than public securities as there is no readily available market in which to sell an investment. There is a possibility that when an investment is to be sold, the price received may not be equal to its intrinsic value or its fair value for financial reporting purposes.

The Company is exposed to a number of risks due to the nature of its activities. These risks include market risk (including currency risk, interest rate risk and price risk), credit risk and liquidity risk. The Company’s objective in managing these risks is the protection and enhancement of shareholder value.