ANNUAL REPORT 2015 - abbank.vn · VND 16,000 billion regarding the exchange rate of 2007). ......

92

2015 ANNUAL REPORT

Transcript of ANNUAL REPORT 2015 - abbank.vn · VND 16,000 billion regarding the exchange rate of 2007). ......

1 Annual Report 2015TOGETHER WE CAN

2015ANNUAL REPORT

2

3 Annual Report 2015TOGETHER WE CAN

CONTENT

VISION AND MISSION

GENERAL INFORMATION

OPERATIONAL STATUS IN YEAR 2015

BOARD OF MANAGEMENT’S REPORT AND ASSESSMENT

ASSESSMENTS OF THE BOARD OF DIRECTORS ON THE BANK’S OPERATION

FINANCIAL REPORTS

BRANCH/TRANSACTION OFFICE NETWORK

04

06

30

54

64

70

84

4

VISION:

“To be a leading joint-stock commercial bank in Vietnam, focusing on retail banking”.

MISSION:

“To provide friendly, effective and efficient financial solutions to customers”.

05 CORE VALUES OF ABBANK IN BUSINESS ACTIVITIES. Results Orientation. Accountability. Value - Added Creativity. High touch. Servant mindset customer service

- Trading name: An Binh Commercial Joint Stock Bank

- Certificate of business registration No: 0301412222

- Charter capital: VND 4,797,999,760,000- Address: 170 Hai Ba Trung St., Dakao Wd., Dist. 1, HCMC

- Telephone: 08. 38 244 855

- Website: http://www.abbank.vn/

5 Annual Report 2015TOGETHER WE CAN

- Trading name: An Binh Commercial Joint Stock Bank

- Certificate of business registration No: 0301412222

- Charter capital: VND 4,797,999,760,000- Address: 170 Hai Ba Trung St., Dakao Wd., Dist. 1, HCMC

- Telephone: 08. 38 244 855

- Website: http://www.abbank.vn/

6

GENERAL INFORMATION

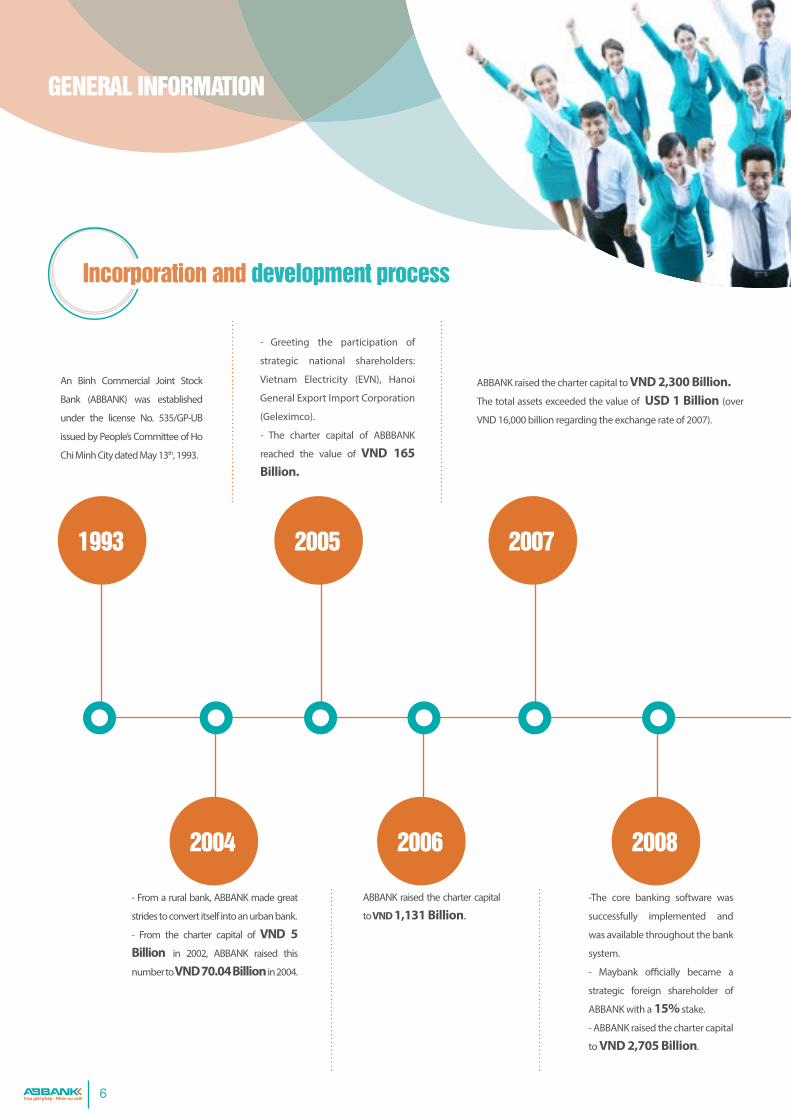

An Binh Commercial Joint Stock

Bank (ABBANK) was established

under the license No. 535/GP-UB

issued by People’s Committee of Ho

Chi Minh City dated May 13th, 1993.

- From a rural bank, ABBANK made great

strides to convert itself into an urban bank.

- From the charter capital of VND 5 Billion in 2002, ABBANK raised this

number to VND 70.04 Billion in 2004.

- Greeting the participation of

strategic national shareholders:

Vietnam Electricity (EVN), Hanoi

General Export Import Corporation

(Geleximco).

- The charter capital of ABBBANK

reached the value of VND 165 Billion.

ABBANK raised the charter capital to VND 2,300 Billion. The total assets exceeded the value of USD 1 Billion (over

VND 16,000 billion regarding the exchange rate of 2007).

ABBANK raised the charter capital

to VND 1,131 Billion.-The core banking software was

successfully implemented and

was available throughout the bank

system.

- Maybank officially became a

strategic foreign shareholder of

ABBANK with a 15% stake.

- ABBANK raised the charter capital

to VND 2,705 Billion.

1993

2004

2005 2007

2006 2008

Incorporation and development process

7 Annual Report 2015TOGETHER WE CAN

- ABBANK raised the charter capital

from VND 2,850 billion in July, 2009

to VND 3,482 Billion at the end

of 2009..

- Maybank raised its stake in

ABBANK from 15% to 20% at

the end of 2009.

ABBANK raised the charter capital

to VND 4,200 Billion.

- On April 26th, 2013, ABBANK raised

the charter capital to nearly VND

4,800 billion. IFC officially became a

major shareholder of ABBANK with

10% stake. Maybank maintained

the possession of 20% stake and

remained the strategic shareholder

of ABBANK.

- On May 28th, 2013, ABBANK 20th

anniversary of establishment was

ceremonially organized in Hanoi.

- On October 15th, 2015, Moody’s

has assigned its first-time ratings for

03 important indexes to ABBANK

(which were the highest values

among the Vietnamese banking

system): local and foreign currency

issuer ratings (B2); local and foreign

currency deposit ratings (B2); and

baseline credit assessment - BCA

(B3). Meanwhile, the ABBANK’s

outlook has been rated stable.

- ABBBANK is the first bank in Vietnam

to provide EVN bill payment service in

the ATM/ POS system of ABBANK for

VISA cardholders.

- ABBANK succesfuly issued convertible

bonds with the value of VND 600 billion

for the International Finance Corporation (IFC)

and Maybank. Maybank still maintained the

possession of 20% stake at ABBANK.

- ABBANK raised the charter capital to

VND 3,831 Billion..

- The ABBANK banking network had a

system of more than 140 transaction units

in 29 cities/provinces nationwide.

- ABBANK has published its Vision, Mission,

Goals and strategic innitiatives for the period

of 2014 – 2018.

- In December 2014, ABBANK was honored to

be one of the first four banks in Vietnam to im-

plement Cross Border Fund Transfer (CBFT).

2009 2011 2013 2015

2010 2012 2014

8

On September 24th, 2015, ABBANK organized the launching ceremony for the international credit card ABBANK VISA Platinum.

Jan 15th, 2015

Mar 20th, 2015

May 13th, 2015Apr 27th, 2015

Sep 24th, 2015

On January 15th, 2015, ABBANK organized

the Gala “An Binh Tet – Empathy for Ocean

and Island”, which went live on HTV9 – a

channel of HCMC television station.

On May 13th, 2015, ABBANK 22nd

anniversary of establishment marked the

journey of 22 years building, growing, and

developing the prestigious brandname in

the Vietnamese financial market.

On April 27th, 2015, ABBANK

organized the Annual Shareholders’

Meeting of 2015 in Novotel, HCM City.

On March 20th, 2015, ABBANK and International Finance Corporation (IFC) co-signed a consulting contract and started off the project “Improving the competitiveness of small and medium-sized enterprises (SMEs) segment”.

GENERAL INFORMATION

Remarkable events

January Febuary March April May June

9 Annual Report 2015TOGETHER WE CAN

Nov 20th, 2015

Nov 20th, 2015

Oct 15th, 2015

Oct 31st, 2015

On October 31st, 2015, ABBBANK was

honored with the accredited award of

“Enterprise with the Quality Qmix 100”

issued by the cooperative election from

three organizations: IER - Institute of

Economics Research (Vietnam), GTA Global

Trade Alliance (UK), and InterConformity

Assessment and Certification (Germany).

On November 26th, 2015, ABBANK was prized with the award of “Leadership in Customer Solution – The Bank who succesfully implements the EVN bill payment with Visa Card”.

On October 15th, 2015, Moody’s - one of the three most prestigious credit rating organizations in the world - has assigned its first-time ratings to ABBANK.

On November 20th ABBANK was invited to present the prize in Vietnamese Talent Awards - Year 11. This is the eighth consecutive year in which ABBANK is the companion of the ceremony.

July August September October November December

10

The business of ABBANK specializes in mobilizing short-term, medium-term and long-term capital in the forms of deposits, deposit certificates, entrusted capital for development and investment from organizations, loans obtained from the State Bank of Vietnam and other credit institutions, other economic organizations; providing short-term, medium-term and long-term loans for economic development; commercial paper, bond and other valuable documents discounting; capital contribution and joint ventures, providing payment services, treasury and other banking services.

Business Lines and locations

GENERAL INFORMATION

Lines of the business

11 Annual Report 2015TOGETHER WE CAN

Location of business

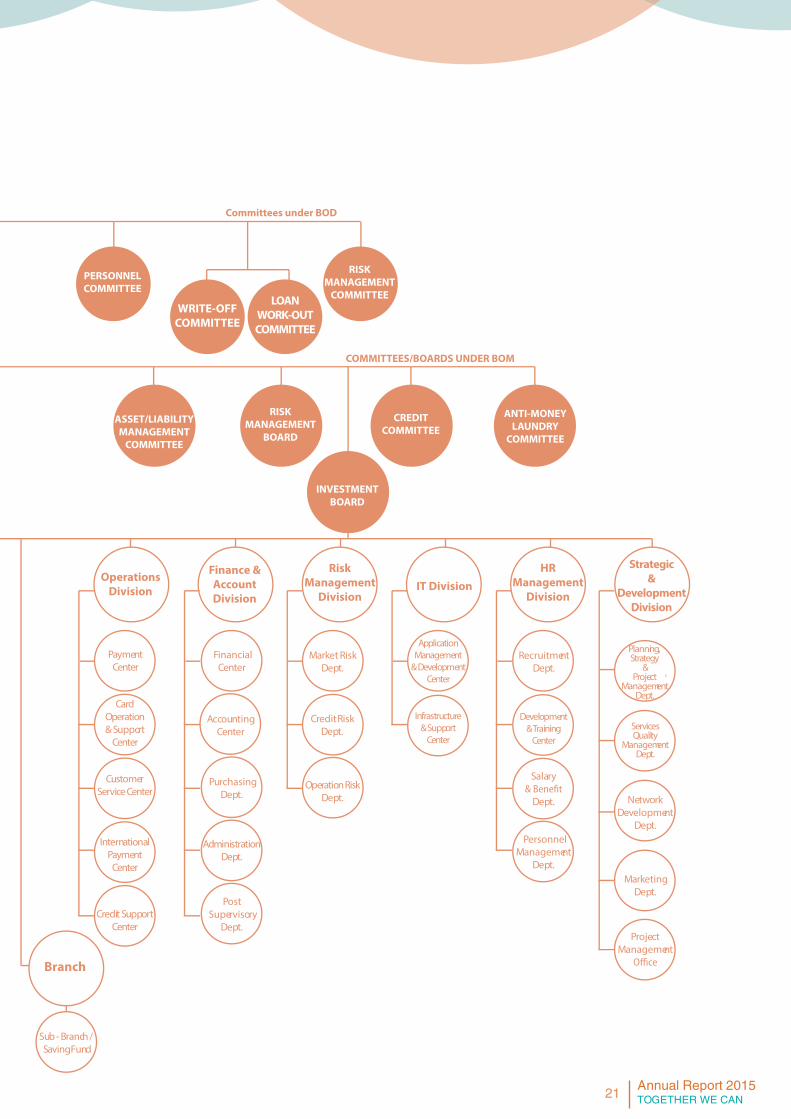

Up to the end of 2015, the ABBANK banking network had a system of more than 146 transaction units in 29 cities/provinces nationwide including 30 branches, 101 sub-branches, and 15 saving funds. The ABBANK banking network is distributed into three regions as specified in the following diagram:

In the last two years, the branches/ transaction units of ABBANK in 03 regions all stably developed, contributing to

leverage the business activities of the whole system. Especially, the total income of the branches/transaction units in the North and North Central Areas achieved the high developing rate of more than 34% in 2015, helping increase their contribution rate to more than 32% among the total system revenue. The income of the South Region with 68 branches/ transaction units also achieved a good developing rate of more than 9% in 2015 and accounted for 60% of the total system revenue.

In the following years, with the strategic objective to be a leading joint-stock commercial bank in Vietnam, focusing on retail banking, ABBANK shall continue to focus on the development and exploitation of the existing banking network; at the same time to expand the network to critical areas, especially in the cities/provinces which obtain high growing rate as well as high evaluation of business and investment environment.

Considering the revenue structure based on income sources, interest income still occupies the highest proportion, as 84%, in 2015. Other incomes from service activities,

foreign currencies trading, securities trading, investment securities trading, capital contribution, equity investments account for 16%.

Diagram of ABBANK transaction units

North and North Central Areas

Midland &Highlands

Southern

Sub - Branch / Saving Fund

Branch

0102030405060708090

100

50

8 166

14

52

12

Governance model

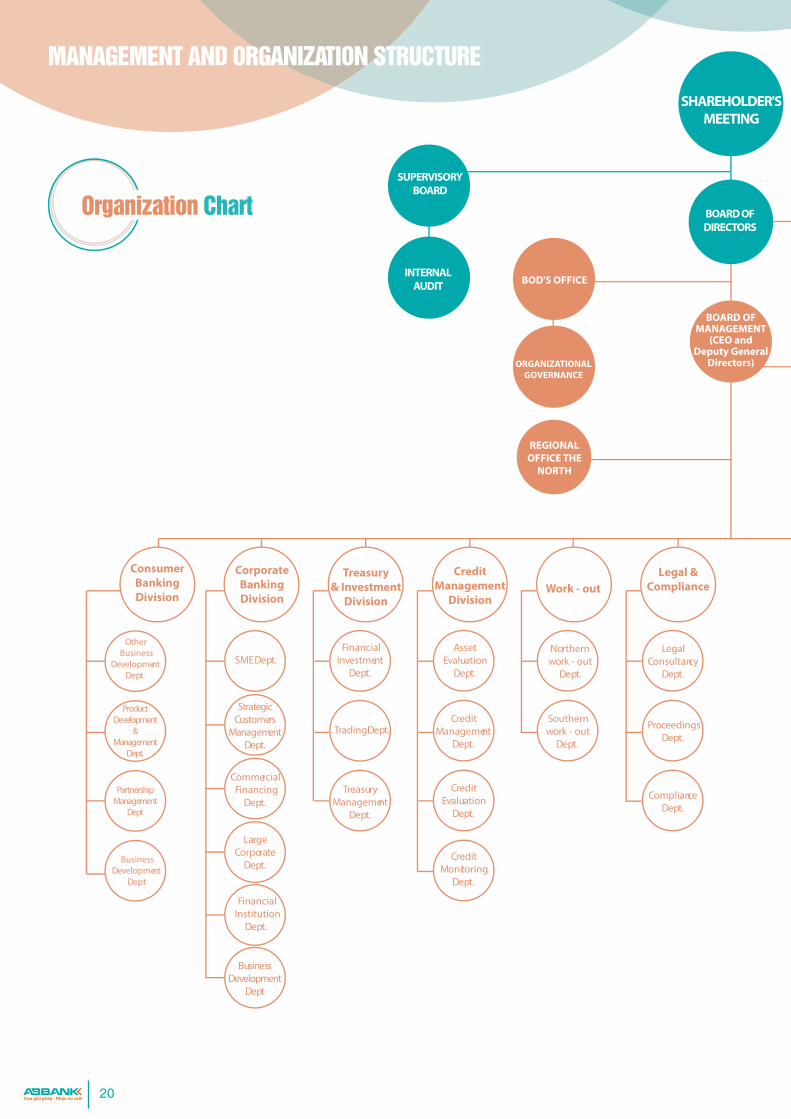

According to ABBANK’s Charter and the regulations of National Law, the management structure of ABBANK is built as follow:

1. General Meeting of Shareholders2. The Board of Directors3.The Supervisory Board4. The committees under the Board of Directors: Risk Management Committee, HR Committee, Write-off Committee, Loan work-out Committee.5.The Board of Management

GENERAL MEETING OF SHAREHOLDERS

In 2015, the Annual General Meeting of Shareholders was held on Apirl 27th in Ho Chi Minh City.

All shareholders were eligible to attend the GSM as stipulated under Section VI, Article 32 of the Bank Charter.

The shareholders eligible for the meeting were informed by post, through website and national newspapers in accordance with regulations on procedures to hold the GSM.

MANAGEMENT AND ORGANIZATION STRUCTURE

The procedures to inform the meeting’s agenda and the methods to access the meeting’s documents are stipulated in the Bank Charter and published on the website: www.abbank.vn.

The agenda, the voting form, the voting results and the minutes of the GSM were published on the bank’s website: www.abbank.vn. In addition, the meeting’s related documents were provided along with the agenda (or were provided to those who were eligible for the meeting).

Mr VU VAN TIEN Chairman

Chairman of ABBANK’s Personnel CommitteeBorn in 1959

Annual Report 2015TOGETHER WE CAN

Mr VU VAN TIEN Chairman

Chairman of ABBANK’s Personnel CommitteeBorn in 1959

Bachelor of Economics – National University of Economics

Mr. Vu Van Tien is one of the most successful and prestigious entrepreneurs in Vietnam. He has been honored with many awards by the Government and the State of Vietnam for his contribution to the development of the country’s economy.

- Third-class Labor Medal.- Medal of “Devotion for the Young Generation”.- Certificate of Merit from the Prime Minister of Vietnam.- Certificate of Merit from the People’s Committee of Hanoi.- Red Star Award.- Brilliant Citizen Award in 2015.

The Board of Directors

14

Mr Mai Quoc Hoi Vice ChairmanMember of ABBANK’s Personnel CommitteeBorn in 1962

Mr Đao Manh Khang Member of the Board of Directors Chairman of ABBANK’s Steering Committee on Strategic Innitiatives.

Ông Lee Tien Poh Member of the Board of Directors Member of ABBANK’s Risk Management Committee Born in 1962, Nationality: Malaysian

Bachelor of Accounting – Academy of Finance and AccountingMaster of Business Administration – Irvine University. Ph.D in Economics – Vietnam

University of Commerce.

Bachelor of Mathematics – Malaya University of MalaysiaCertificate of Accounting – the Institute of Chartered Accountants of MalaysiaHe is also a member of the Board

Member - Electricity of Vietnam Corporation (EVN). He has 32 years of experience in the field of Finance and Accounting.

Mr. Dao Manh Khang has 22 years of experience in Finance and Banking, and nearly 10 years working at ABBANK.

Mr. Lee Tien Poh has 22 years of experience in Banking in Malaysia and is currently the Deputy General Director responsible for financial management of the Corporation and Malaysia territory, the Community Financial Service Division of MayBank.

Mr. Mai Quoc Hoi was honored with the Third-class Labor Medal awarded by the Government of Vietnam and a Certificate of Merit from the Prime Minister.

Chairman of ABBANK’s Risk Management CommitteeMember of ABBANK’s Human Resource CommitteeBorn in 1969

15 Annual Report 2015TOGETHER WE CAN

Mr Tran Ba Vinh Member of the Board of Directors Member of ABBANK’s Risk Management CommitteeBorn in 1957

Mr Gayle McGuigan Member of the Board of DirectorsBorn in1944Nationality: American.

Bachelor of Economics – University of Waterway Transportation (as now the Vietnam Maritime University, Hai Phong)Bachelor of English Studies – College of Foreign Languages, Hanoi Pedagogical University.

Master of Finance – Wharton University, Philadelphia, PABachelor of History – Pennsylvania University, Philadelphia, PA

Mr. Tran Ba Vinh has 12 years of experience in teaching economics in Vietnam Maritime University and 22 years working in the banking sector.

In 2005, he was awarded with the Certificate of Merit by Vietnam General Federation of Labor for his outstanding achievement contributing to build up a strong union.He was the CEO of Maritime Bank, the CEO and member of the Board of Directors of Mekong Bank.

Mr. Gayle Mc Guigan has more than 44 years of experience in finance, currency & stock trading, and banking in the US and other international organizations.From 1971 to 1995, he worked for many banks, financial and securities institutions in the US and other countries. He has been working for IFC in Washington (US) since 1996.

16

MANAGEMENT AND ORGANIZATION STRUCTURE

The role of the Board of Directors (BOD)

The authority and the responsibility of the BOD are clearly defined in Section II – Principle of Corporate Governance and Article 55 of the Bank Charter.

Members of the BOD

ABBANK’s BOD consists of 6 members, in which there are 5 non-executive board members and 1 independent member, tenure of 2013 – 2017.

According to Article 43 of the Bank Charter, an independent member must meet the following criteria:

• Currently not working for either ABBANK or its subsidiaries or has not worked for either ABBANK or its subsidiaries for the past 03 (three) years.

• Not receiving any payment, allowances or compensation from ABBANK except for pay-ments for working as a member of the BOD.

• The fiancée, parents, children, brothers, sisters and their fiancée must not be major shareholders, managers, or members of the ABBANK’s Supervisory Board or ABBANK’s subsidiaries.

• Not having been a manager, a member of ABBANK’s Supervisory Board at any time in the past 5 years; not directly or indirectly holding or representing to hold more than 1% (one percent) of the bank’s charter capital or the equity capital eligible for voting at ABBANK.

• The total possession of any member of BOD and their related people toward the ABBANK’s charter capital must not be more than 5% (five percent) or the total possession toward the equity capital must not be enough for the voting eligibility at ABBANK.

BOARD OF DIRECTORS Name and position *Executive **Non-

ExecutiveIndependent Member of BOD since

Chairman: Vu Van Tien x 10/06/2003

Vice Chairman: Mai Quoc Hoi x 01/08/2010

Member: Đao Manh Khang x 27/05/2011

Member: Lee Tien Poh x 27/05/2011

Member: Gayle McGuigan x 28/04/2013

Member: Tran Ba Vinh x 28/04/2013

Notes:

*An executive member is responsible for daily management of ABBANK.** A non-executive member is not responsible for daily management of ABBANK or any ABBANK subsidiaries.

COMMITTEES UNDER CONTROL OF THE BOARD OF DIRECTORS The BOD controls the following Committees:• The Risk Management Committee (RMC) was established to assist the BOD – the highest governing authority of the bank – to execute their authority and responsibility in making decisions for risk management strategies and monitoring the implementation of measures to prevent risks (except for issues under the jurisdiction of the General Meeting of Shareholders).

• The Human Resource Committee (HRC) was established to help the BOD – the highest governing authority of the bank – to execute their authority and responsibility in making decision for management policies and personnel structure of the bank (except for issues under the jurisdiction of the General Meeting of Shareholders).

• In addition, in order to ensure obedience of national laws and ABBANK’s own policies, in 2015 the Board of Directors founded 2 directly-affiliated committes, the Write-off Committee and the Loan work-out Committee.

17 Annual Report 2015TOGETHER WE CAN

Name and position Meetings attended Meetings not attended Meetings eligible to attend

Chairman: Vu Van Tien 2 2

Vice Chairman: Mai Quoc Hoi 1 1 2

Member: Đao Manh Khang 2 2

Member: Lee Tien Poh 2 2

Member: Gayle McGuigan 2 2

Member: Tran Ba Vinh 2 2

Activities of the BOD

In 2015, there were two meetings of the BOD and the results were voted in written form.The attendance information of each BOD member is as follow:

Name and position Total voting documents for members Not voting Voting

Chairman: Vu Van Tien 56 0 56

Vice Chairman: Mai Quoc Hoi 49 3 46

Member: Đao Manh Khang 56 0 56

Member: Lee Tien Poh 69 1 68

Member: Gayle McGuigan 69 0 69

Member: Tran Ba Vinh 69 0 69

The voting information (in written form) of each BOD member is as follow:

Assessment for the BOD’s performance :

The BOD implemented assessment and self-assessment in accordance with Article 2.67 and 2.68 of the Regulations on Corporate Governance and the Regulation of Vietnam Law as well as the International Practice.

18

Ms Nguyen Thi Hanh Tam Chief SupervisorBorn in 1972

Bachelor of Finance and Credit – the Banking AcademyBachelor of Accounting – the Banking AcademyChief Accountant Certificate Master of Business Administration

Ms. Nguyen Thi Hanh Tam has 23 years of experience in the field of Banking and Finance.

Members of ABBANK’s Supervisory Board (tenure of 2013 – 2017)

1. Ms. Nguyen Thi Hanh Tam - Chief Supervisor

2. Mr. Hadenan A. Jalil - Member

3. Mr. Cap Tuan Anh - Member

4. Mr Nguyen Phan Long - Dedicated Member

The Supervisory Board directly manages the Internal Auditing Team.

MANAGEMENT AND ORGANIZATION STRUCTURE

The Supervisory board

19 Annual Report 2015TOGETHER WE CAN

Mr. Nguyen Phan LongDedicated memberBorn in 1962

Mr Cap Tuan AnhMember of the Supervisory BoardBorn in 1977

Mr Hadenam bin A.Jalil Member of the Supervisory BoardBorn in 1946, Nationality: Malaysian

Bachelor of Economics – University of Finance and Accounting in HCMCBachelor of Law – University of Law in Hanoi

Master of Finance – University of Houston-Clear Lake Bachelor of Economics – Hons

University of MalaysiaMaster of Business Administration – Asian Institute of Management, ManilaPhD at Henley – The management College/Brunel University, the United Kingdom

Mr. Nguyen Phan Long has 31 years of experience in the field of Finance and Accounting, including 10 years working as a general and chief accountant.

Mr. Cap Tuan Anh has 15 years of experience in the field of Finance and Accounting.

Mr. Hadenan bin A.Jalil has 45 years of experience in the field of Finance, Taxation, Audit, and Banking.He is a member of Maybank’s Board of Directors and a member of the Board of Directors of Maybank Islamic Berhad.He is also the Chairman of ICB Islamic Bank LTd.Dhaka Bangladesh.He has taken senior positions in many Malaysian companies such as member of JCorp’s Internal Auditing Board and the Chairman of Malaysian Anticorruption Committee.

20

SHAREHOLDER'S MEETING

INTERNAL AUDIT

PERSONNEL COMMITTEE

ASSET/LIABILITYMANAGEMENT

COMMITTEE

RISK MANAGEMENT

BOARD

CREDIT COMMITTEE

INVESTMENT BOARD

Consumer Banking Division

Other Business

Development Dept.

SME Dept.

Strategic Customers

Management Dept.

Large Corporate

Dept.

Commercial Financing

Dept.

Financial Investment

Dept.

AssetEvaluation

Dept.

Planning, Strategy

&Project

Management Dept.

Services Quality

Management Dept.

NetworkDevelopment

Dept.

Marketing Dept.

Credit Management

Dept.

CreditEvaluation

Dept.

CreditMonitoring

Dept.

Trading Dept.

Treasury Management

Dept.

Product Development

& Management

Dept.

Partnership Management

Dept

Business Development

Dept

Financial Institution

Dept.

Business Development

Dept

Northernwork - out

Dept.

Southernwork - out

Dept.

LegalConsultancy

Dept.

Proceedings Dept.

Compliance Dept.

Card Operation & Support

Center

CustomerService Center

International Payment Center

Payment Center

Credit SupportCenter

Financial Center

Accounting Center

Purchasing Dept.

Administration Dept.

Post Supervisory

Dept.

Market Risk Dept.

Credit Risk Dept.

Operation Risk Dept.

Application Management

& Development Center

Infrastructure& Support

Center

Recruitment Dept.

Development& Training

Center

Salary

Dept.

PersonnelManagement

Dept.

Project Management

Corporate Banking Division

Treasury & Investment

Division

Credit Management

DivisionWork - out

Legal & Compliance

OperationsDivision

Finance & Account Division

Risk Management

DivisionIT Division

HR Management

Division

Strategic &

Development Division

ANTI-MONEYLAUNDRY

COMMITTEE

BOD'S OFFICE

REGIONAL OFFICE THE

NORTH

ORGANIZATIONAL GOVERNANCE

RISK MANAGEMENT

COMMITTEE

Committees under BOD

COMMITTEES/BOARDS UNDER BOM

BOARD OF DIRECTORS

SUPERVISORY BOARD

BOARD OF MANAGEMENT

(CEO and Deputy General

Directors)

Sub - Branch / Saving Fund

Branch

WRITE-OFF COMMITTEE

LOAN WORK-OUT COMMITTEE

MANAGEMENT AND ORGANIZATION STRUCTURE

Organization Chart

21 Annual Report 2015TOGETHER WE CAN

SHAREHOLDER'S MEETING

INTERNAL AUDIT

PERSONNEL COMMITTEE

ASSET/LIABILITYMANAGEMENT

COMMITTEE

RISK MANAGEMENT

BOARD

CREDIT COMMITTEE

INVESTMENT BOARD

Consumer Banking Division

Other Business

Development Dept.

SME Dept.

Strategic Customers

Management Dept.

Large Corporate

Dept.

Commercial Financing

Dept.

Financial Investment

Dept.

AssetEvaluation

Dept.

Planning, Strategy

&Project

Management Dept.

Services Quality

Management Dept.

NetworkDevelopment

Dept.

Marketing Dept.

Credit Management

Dept.

CreditEvaluation

Dept.

CreditMonitoring

Dept.

Trading Dept.

Treasury Management

Dept.

Product Development

& Management

Dept.

Partnership Management

Dept

Business Development

Dept

Financial Institution

Dept.

Business Development

Dept

Northernwork - out

Dept.

Southernwork - out

Dept.

LegalConsultancy

Dept.

Proceedings Dept.

Compliance Dept.

Card Operation & Support

Center

CustomerService Center

International Payment Center

Payment Center

Credit SupportCenter

Financial Center

Accounting Center

Purchasing Dept.

Administration Dept.

Post Supervisory

Dept.

Market Risk Dept.

Credit Risk Dept.

Operation Risk Dept.

Application Management

& Development Center

Infrastructure& Support

Center

Recruitment Dept.

Development& Training

Center

Salary

Dept.

PersonnelManagement

Dept.

Project Management

Corporate Banking Division

Treasury & Investment

Division

Credit Management

DivisionWork - out

Legal & Compliance

OperationsDivision

Finance & Account Division

Risk Management

DivisionIT Division

HR Management

Division

Strategic &

Development Division

ANTI-MONEYLAUNDRY

COMMITTEE

BOD'S OFFICE

REGIONAL OFFICE THE

NORTH

ORGANIZATIONAL GOVERNANCE

RISK MANAGEMENT

COMMITTEE

Committees under BOD

COMMITTEES/BOARDS UNDER BOM

BOARD OF DIRECTORS

SUPERVISORY BOARD

BOARD OF MANAGEMENT

(CEO and Deputy General

Directors)

Sub - Branch / Saving Fund

Branch

WRITE-OFF COMMITTEE

LOAN WORK-OUT COMMITTEE

,

22

23 Annual Report 2015TOGETHER WE CAN

HIGH TOUCH

24

SUBSIDIARIES, ASSOCIATED COMPANY

Company name Relationship with ABBANK Address Major fields of business

Charter capital

contributed (VND million)

ABBANK Rate of Possession

ABBANK Asset Management One Member Company

Limited(ABBA)

Subsidiary

Floor 2, Geleximco Building, 36 Hoang Cau St., O Cho Dua

Wd., Dong Da Dist., HN

Liquidating the collateral assets; Debt restructuring; Providing

resolutions for collateral assets: repairing, upgrading for trading,

leasing, or commercial exploiting; Trading debts of credit institutions

or companies managing debts and exploiting collateral

assets; Real estate trading; Hotel commerce; CLeasing machines and equipments;

Leasing transportation means (with engine); Leasing tools and

instruments for personal use or for families; Assist financial services:

Entrusting and supervising services based on fee and

agreement; Debt brokerage; Stock and warehouse services; Leasing machines, equipments,

and other material items.

260,000 100%

ABBA Security Co., Ltd (ABBAS)

Subsidiary of ABBANK,

indirectly invested through ABBA

Floor 2, Geleximco Building, 36 Hoang Cau St., O Cho Dua

Wd., Dong Da Dist., HN

Personal bodyguard activities: Providing security services. 2,000 100%

An Binh Securi-ties Joint Stock Company (ABS)

Assiociated company

101 Lang Ha St., Lang Ha Wd., Dong

Da Dist., HN

Stock brokerage, securities proprietary dealing, stoke

custody, securities underwriting, stock investment advisory, enterprise finance advisory.

397,000 5.2%

25 Annual Report 2015TOGETHER WE CAN

Subsidiary:

ABBANK ASSET MANAGEMENT(ABBA)

Assiociated company:

AN BINH SECURITIES JOINT STOCK COMPANY

ABBANKRate of

Possession

ABBANKRate of

Possession

ABBANKRate of

Possession

100%

100%

5.2%

ABBA Security Co., Ltd (ABBAS)

26

VISION:“To be a leading joint-stock commercial bank in Vietnam, focusing on retail banking.”.

MISSION:

“To provide friendly, effective and efficient financial solutions to customers”.

With advantages of the young, enthusiastic, and dynamic human resource, the nationwide banking system, and the support from strategic local and foreign partners, especially the strong ability and experience of two stakeholders Maybank and IFC in retail banking, ABBANK firmly obtains essential potentials to achieve its goal toward 2018 – to become a leading joint-stock commercial bank in Vietnam, focusing on retail banking.

In order to fulfill the Vision, Missions, Goals and Strategic Innitiatives toward 2018, ABBANK’s Board of Directors have approved 23 projects, which are implemented in various fields and strictly monitored by the Steering Committee (SC) and supported by the Project Management Office (PMO).

With the developing perspective focusing on retail banking, ABBANK differentiates itself by the orientation of sustainable development and by the risk evaluation and risk management; so that the bank’s activities are safety and efficiently maintained and the profitability of related parties including stakeholder, customers, community, and ABBANK’s staff… is harmonized.

ORIENTATION FOR DEVELOPMENT

27 Annual Report 2015TOGETHER WE CAN

Credit risks

Risks are caused in the case that the party granted credit, the party with obligation or partners do not partially or fully carried out the obligatory payment committed. In addition, credit risks are also caused internally (inside the credit institution) in the case that the regulations are not strictly followed.

Market risks, liquidity risks, interest risks

Market risks are the possibilities of losses in internal and external items of accounting balance sheet caused by fluctuation of market price.

Interest risks are the risk caused by the unfavorable fluctuation of interest rate toward the revenue and the economical value of ABBANK.

Liquidity risks are the risk that the bank is unable (not enough financial resources) to meet due financial demands or has to tolerate an unsual high cost for these obligations.

Operational risks

Operational risks are the risk related to all operational aspects of the bank, difficult to control and lead to unexpected losses. Operational risks are caused by the losses, incurred for inadequate or failed internal processes, people and systems, or from external events such as natural disasters (storm, flood …)

Risk management is a crucial (extremely important) part in all business decisions of the bank. Risk management activities are carried out through a series of major risk management principles and through risk management procedures: identifying, assessing, controlling and minimizing, monitoring and reporting.

Risk is an intrinsic factor in any business operation that the bank always has to face with. Risk management, therefore, has become an essential and crucial activity in all business decision, even in the safest business circumstances, in order to balance the risk taking level and the expected profitable rate. In daily business operations, the bank has to face with the main following risks:

Risks

28

RESULTSORIENTATION

Annual Report 2015TOGETHER WE CAN

30

OPERATIONAL STATUS IN THE YEAR 2015

Business operation status

In 2015, ABBANK continued to operate in line with its strategic goals set for the period 2014 – 2018 to reinforce and improve its position in the market to conduct business effectively and safely, and transform the bank in compliance with approved 20 strategic innitiatives in order to make ABBANK the leading joint-stock commercial bank in Vietnam, focusing on the retail banking. Overcoming the difficulties and challenges in the banking industry as well as the general economy in Vietnam, the business operations of ABBANK in 2015 reached certain achievements.

Target(Billion VND) Achievements of 2014 (*) Achievements of 2015 (*) Planning target of 2015

Total assets 67,198 64,662 71,104

Outstanding Loans 25,969 30,915 28,570

Mobilization 45,404 47,881 46,500

Pre-tax Profit 133.6 107.7 65.6

ABBANK financial results in 2015 in comparison with 2014 and the plan 2015

Up to the end of December 2015, the total assets of ABBANK reached VND 64,662 Billion (91% of the planning target 2015). The total mobilization of Martket 1 attained VND 47,881 Billion corresponding to 103% of the 2015 plan; the total loans of Market 1 reached to VND 30,915 Billion,

19% higher than 2014 and equivalent to 108% planning target of 2015. The credit quality also improved remarkably with the bad debt rate controlled under 3%, 1.72% in 2015 in comparison with 2.75% in 2014. The operational expense was remarkably controlled as there was only an increase of 9% as compared to 2014.

The total operational revenue achieved VND 1,967 Billion in value, 19% higher than 2014 and equivalent to 113% of the planning target of 2015. The profit before provisions for credit losses (PCL) in 2015 attained VND 770.9 Billion, 37% higher compared to 2014. With the full compliance toward the Regulation, the provisions for credit losses (PCL) in 2015 was VND 663.2 Billion (including the provisions for credit

losses (PCL), the bonds from VAMC), the profit before tax VND 107.7 Billion.

The system operations continued to improve and accomplished positive results

With focus on completing the centralization of Credit Support Center, Financial and Accounting, as well as procurement throughout the system, ABBANK has achieved positive progress in cost control and credit disbursement. Specifically, the Cost to income ratio (CIR) has decreased to under 60% with the ratio of 57.8% at the end of 2015 in comparison with the ratio of 60.7% at the end of 2014 and it was lower than the average level of the industry.

*Data of the separate financial reports

31 Annual Report 2015TOGETHER WE CAN

OPERATIONS OF THE CONSUMER BANKING DIVISION

OPERATIONS OF CORPORATE BANKING DIVISION

There were also many achievements in Corporate Banking Division in 2015. Specifically, the mobilization reached VND 26,191 Billion, slightly decreased in comparison with 2014, and attained 99% of the plan in order to control the cost of interest payment and raise the effectiveness of capital management. The proportion between payment deposit and the total mobilization was always maintained at a high level of 36%, contributing to the decrease of the system’s average mobilizing cost. The loans of SME customers also exceeded the planning target with VND 19,682 Billion, 11% higher than 2014.

In addition, activities for developing product/services also got numerous

Target Achievement in 2014 (*)

Achievement in 2015 (*)

Target in 2015

Mobilization 18,940 21,690 20,000

Loan 8,258 11,233 9,530

Total number of Individual Customers

506,188 576,000 535,596

Card (Number of new issued cards in the year)

56,606 58,760 55,132

Target Achievement in 2014 (*)

Achievement in 2015 (*)

Target in 2015

Mobilization 26,464 26,191 26,500

Loan 17,711 19,682 19,040

Number of SME customers 18,041 20,017 21,649

accomplishments; following the strategy of increasing income form service and focusing on SME customers sector, ABBANK has standardized and improved product bundles such as: the bundle for money management incuding services to manage the receivables and payables, the bundle for supporting import/export, the bundle

In 2015, almost all results of Consumer Banking Division outperformed compared to the original targets. Specifically, the mobilization of individual customers achieved VND 21,690 Billion, increasing 14.5% compared to 2014, attaining 108.5% of the plan; the loans of individual customers in 2015 surpassed the value VND 10,000 Billion and VND 11,000 Billion for the first time and reached VND 11,233 Billion, increasing 36% compared to 2014, attaining 118% of the plan; the total number of Individual Customers also gained an increase of 13.8% with 576,000 (7.5% higher than the planning target).

for bidder/tenderer, the bundle for issuing guarantee. Meanwhile, ABBANK pushed the bundles with high technology such as, online collecting and issuing guarantee for import/export tax throughout the system contributing the enhancement of the credit and brand name of ABBANK in the market.

In addition, in 2015, the Consumer Banking Division has successfully implemented the International Credit Card ABBANK VISA Platinum project, contributing to the value of the brandname and service of ABBANK in the credit card market. Mobilization and credit product has been continuously

improved and upgraded to satisfy the increasing demands of the market. Meanwhile, services like interbank money transfer, EVN bill payment, e-banking… have been continuously invested in and upgraded to enhance the convenience in customer transaction.

*Data of the separate financial reports

*Data of the separate financial reports

32

OPERATIONAL STATUS IN THE YEAR 2015

In terms of developing and managing the applications:

- The activities of managing, operating the applications maintained continuous, stable, and safe performance.

- Successfully developed the applications and products for business development and banking management in accordance to the requirement other Divisions, especially the bank’s Project in 20 approved strategic innitiatives.

- Cooperated with others Divisions to make plan, research, invest, and implement IT system to support the bank operation in the future such as creating and approving loans (Loan Originating System LOS), Internet/Mobile Banking, Enterprise Service Bus (ESB), Data Warehousing and Business Intelligence (DW/BI) …

In terms of the IT infrastructure operation

IT Division maintained the IT infrastructure’s stability, continuous optimization and enhancements through applying new technologies and solutions and providing IT infrastructure’s availability, in order to meet

the objectives of long-term and continuant development in banking operations. • Officially put the IT infrastructure (servers, transmission links) into service to support the developing application outside Corebanking at Data Center in 36 Hoang Cau – Hanoi.

•Standardized the system to meet the security – information safety req dards, fully complying the Payment Card Industry Data Security Standard (PCI DSS), implementing the log collecting project, the project of Internet centralization.

• Improved the service quality, cooprated to implement the project Upgrading Switching Center for Permanent Customer Service 24/7.

• Maintained important IT equipments and systems in good condition for stable and safe operation: Permanently monitored the system running; Built a communication channel for receiving and support through the Service Management application; Maintained the information security and monitoring the compliance toward the IT policies through updating patches, security solutions and applications, implemented the project of increasing the prevention and ability of anti-external-attacks.

In 2015, IT of ABBANK continued to gain some achievements

Information technology

33 Annual Report 2015TOGETHER WE CAN

34

Mr Cu Anh TuanDeputy General Director acting

as The General DirectorBorn in 1972.

Bachelor of Credit, the Banking Academy. Master of Finance and Accounting, Swinburne University, Australia.Member of CPA Australia

Mr. Cu Anh Tuan has 23 years of experience in the field of Finance and Accounting in different groups/ corporations in Vietnam, including Director of Finance at SCIC (2007 – 2011) and Techcombank (2011 – 2014). Since April 2014, he has taken the position of Deputy General Director of ABBANK, and the BOD has assigned him to the position of Acting General Director of ABBANK since May 2015.On February 2nd, 2016, Mr. Cu Anh Tuan was officially appointed CEO of ABBANK.

35 Annual Report 2015TOGETHER WE CAN

Ms Pham Thi Hien Deputy General DirectorBorn in1973.

Mr Bui Trung Kien Deputy General DirectorBorn in1973.

Ms Nguyen Thị Ngoc Mai Deputy General DirectorBorn in1974.

Bachelor of the Banking Academy.Master of Economics of Banking and Finance (MEBF) CFVG Hanoi.

Bachelor of Banking and Finance – National Economics University, Hanoi.Bachelor of Law, Hanoi Open University .Master in Public Policy (National University of Singapore).

Bachelor of Energy Economics – Hanoi University of Technology.Master of Energy Economics – Asian Institute of Technology.PhD of economics – Kwansei Gakuin, Japan.

Ms. Pham Thi Hien has 22 years of experience in Banking and Finance industry, including 13 years working at Vietcombank, 4 years at HSBC Vietnam and 5 years at ABBANK.

Mr. Bui Trung Kien has more than 22 years of experiences in the field of Banking and Finance in Vietnam, including 12 years working at The State Bank of Vietnam and 9 years at ABBANK.

Ms. Nguyen Thi Ngoc Mai has 20 years of experience in the field of Banking and Finance, including 12 years working in the field of corporate finance and project finance in EVN corporation and more than 9 years working in ABBANK.

ORGANIZATION AND HUMAN RESOURCE

Board of Management

36

ORGANIZATION AND HUMAN RESOURCE

Mr Nguyen Manh Quan Deputy General DirectorBorn in 1973

Mr Tran XeDeputy General Director Sinh năm 1955

Bachelor of Economy, Trade UniversityMaster of Business Administration – AIT

Bachelor of Hanoi University of TechnologyBachelor of Business Administration – Da Nang University of EconomicsMr. Nguyen Manh Quan has more

than 20 years of experience in the field of banking; he had taken key positions at VID Public Bank; CitiBank; HSBC, Seabank, HDBank, and MDBank; he has been assigned to be the Deputy General Director of ABBANK since June 2015.

Mr. Tran Xe has more than 18 years of experience in banking and finance in Vietnam (especially at Techcombank and ABBANK). Since 2007, he had held the positions of Deputy General Director and Director of ABBANK Branch in Da Nang.

Board of Management

37 Annual Report 2015TOGETHER WE CAN

38

ORGANIZATION AND HUMAN RESOURCE

Since May 4th, 2015, BOD had deciced to assign Mr Cu Anh Tuan, Deputy General Director, for the authority and responsibility of the General Director of ABBANK.

Recruiting and assigning Mr. Nguyen Manh Quan for the position of Deputy General Director since June 19th,2015

Name Position ABBANK ownership percentage

Cu Anh Tuan Deputy General Director 0.07%

Pham Thi Hien Deputy General Director 0%

Nguyen Thi Ngoc Mai Deputy General Director 0%

Bui Trung Kien Deputy General Director 0.01%

Nguyen Manh Quan Deputy General Director 0%

Tran Xe Deputy General Director 0%

Bui Quoc Viet Chief Accountant 0.01%

Committees under control of the BOM • The Credit Committee (CC): was set up to ensure stability and efficiency in credit management of the whole system.

• The Executive Risk Committee (ERC): was appointed to monitor all management risks except market and liquidity risk; and to report to RMC problems which are beyond the jurisdiction of the ERC for decision making and settlement.

• The Investment Committee (IC): was created with the aim of increasing the professionalism and precaution in investment process,

enhancing monitoring the effectiveness and quality of investment projects; ensuring the control mode and risk management in the investing activities.

• The Asset –Liability Committee (ALCO): Was set up to assists the BOD in managing liquidity and market risks. ALCO is responsible for the development, implementation, and reviewing regulations, strategies and policies relating to the bank’s management of balance sheet, capital, market and liquidity risks.

• Anti-Money Laundering Council: was established to perform the task of preventing and combating money laundering under the laws of Vietnam, the international commitments and the provisions of ABBANK.

The list of BOM, Chief Accountant and ABBANK ownership percentage

Board of Management

Changes in the Board of Management - BOM

39 Annual Report 2015TOGETHER WE CAN

Recruitment

In order to improve recruitment quality and attract relevant and experienced employees, ABBANK focused on improving and innovating of the recruitment process:

- Applied IT solutions for enhancing online recruitment capability and managing the recruitment requirements based on the management software.

- Established the centralized and systematically consistent management mechanism by issuing adequate process, regulations, and procedures for recruitment in which the roles and duties of the related individuals and divisions are clearly defined.

- Focused on improving the employer’s image, and brand reputation, increasing ABBANK’s brand awareness to potential candidates, thereby expanding the candidate network by multiple approaches.

Salary and policies for contribution acknowledgement of ABBANK staffs:

ABBANK adjusted and issued the Salary and Compensation Policies to be suitable with the current regulation of Vietnam Law; these polices have shown the bank’s innovative attitude in management and compensation for the employees. In 2015, ABBANK also conducted the research on incentive payment to customer relation officer based on the result and ranking, and the policy for timely acknowledging the outstanding staff as well as forming a modern compensation policy for talented human resources – Talent Pool.

In 2015, in order to increase the productivity and cultivate a result-oriented culture, ABBANK updated the Performance Assessment Regulation, and simultaneously adjusted and standardized the criteria system for working result so that the employee evaluation could be consistent. The criteria system for working performance has also been developed and improved with the application range from the supreme leaders to the individual

employees. This is the basis to evaluate the accomplishment in the working results and the productivity of each member.

In addition, ABBANK issued the Regulation for Competition and Award to manage and organized competitive activities and awards in the bank in order to promote the potential members and the innovation among individuals, with the aim to increase productivity and effectiveness as well as creating a dynamic and creative business environment at ABBANK.

The number of staff up to December 31st

2,838 members

Eductional rate of the human resources: - Post graduation

3.5%-Bachelor 85.8%

40

ORGANIZATION AND HUMAN RESOURCE

Labor relationship Establishing a positive Labor relationship to create a friendly and attached working environment has been one of ABBANK’s important goals. The bank regularly carried out innovative programs to: reinforce the core values and cultures of ABBANK; reviewed the performance evaluation system to identify staffs’ roles and responsibilities at different levels, which thus created well-organised and consistent workflow, and enhanced cooperation; design and organize training programs for staff and managers to foster the creativity and innovation. ABBANK encourages high ethical standards and every employee must understand ABBANK’s Code of Ethics.

In addition, the bank aims to improve the quality of human resource (HR) services by creating the simple mechanism to access such services and applying IT solutions in human capital management. Especially, information about policies, procedures and new human resource programs that directly influence each staff were shared and introduced regularly to encourage staff’s contribution and to increase the quality of HR service in general.

ABBANK’s appreciation towards human resource activities was shown in its survey on staff satisfaction which demonstrated that ABBANKers were satisfied with the work environment, the managers, the training programs and the human resource development programs. Through this survey, all members also contributed ideas to improve the bank’s working environment to make ABBANK a place where “Employees always choose to work”.

41 Annual Report 2015TOGETHER WE CAN

Training and development the human resources

At ABBANK, training and development are always attached to the aim of standardizing staff, fostering succession employees, and improving the capabilities of managers and leaders. The HR development programs focused on:

- Enhancing management skills, leadership skills, communication skills and team working spirit;- Reinforcing and updating specialized knowledge; Training on product and customer developing skills;- Training programs, curriculums and career development programs with the aim of improving capabilities and behaviors for teamwork, thus leading to a cooperative working environment.- Provided total 10,569 training sessions from 270 skill classes and 307 professional courses. This included 500 courses taught by internal lecturers.

Training regulations, documents and related procedures were promulgated in 2015 and in previous years have clearly defined the career development policies (including staff transfer, position assignment…) and eliminated barriers by preparing human resources for the

internal staff transfer. ABBANK also held discussions with managers and staffs on the career and profession development to formulate the annual plan for professional trainings regarding career development as a highly important matter.

In terms of developing the succession, ABBANK applied the scientific, and practical measurements in order to select successive staff and design the training programs, giving priority to on-job trainings and tutorials for the potential candidates. To retain the skilled members for the succession resource and encourage them to maintain the working quality and continuously contribute added value to ABBANK, the bank has conducted “ABBANK Talent Pool” campaign with the message “Every ABBANKer can be a talent”. In the first year, there were nearly 250 staffs selected in the Talent Pool through several evaluation stages about characteristics, capabilities, and suitability to the developing requirements of the bank. Members of the Talent Pool are from many working positions: Tellers, Customer Relation Staff, Expert/Staff of the Branches to Departmant Manager/Vice Managers, Directors of the Branches/Sub-branches.

ABBANK also diversified training methods to provide their staffs better information access and self-studying opportunities. Online training programs and softwares were conducted under the coorperation between Training & Development Center and IT Management Center have been officially implemented throughout the system with the applications relevant to ABBANK’s current scale and requirements.

42

OPERATIONAL STATUS IN THE YEAR 2015

In 2015, there were positive movements of the macro economic and the banking industry and optimistic results were achieved. However, with the safe and effective investment policy of the BOD and the BOM, ABBANK has carefully rechecked and evaluated the efficiency of all investment items. On that basis, ABBANK has successfully figured out the plans to withdraw the investment capital for the low profitable items; for instant, in 2015, ABBANK has successfully withdrew the capital in An Binh Real Estate with the transfer fee equivalent to the face value, the total withdrawing value is VND 10 Billion. Last year, ABBANK has invested additional capital of VND 60 Billion to its subsidiary, ABBANK Asset Management One Member Company Limited, to increase the financial capability of this company as there were potential conditions for the market to develop in this period.

In addition, ABBANK did not invest in new project and refused to contribute the capital to organizations which did not make expected profit. Meanwhile, in 2015, ABBANK has taken a good opportunity in the market to transfer all listed securities in the stock market (633,733 stocks of PGI - Petrolimex Insurance Corporation).

While the stock market tended to fluctuate slightly in a narrow band, ABBANK sold the PGI securities with the price higher than expected, collecting the amount of VND 9,166,645,376 and brought back a remarkable provision amount of VND 1,167,708,800. At the end of the year 2015, the list of capital invested to other organisations reached VND 626.15 Billion, nearly 9% higher than 2014 occupying 12.3% of the sum of charter capital and the reserving fund. The financial status of the companies receiving joint capital of ABBANK is stable with the average dividend payout ratio was nearly 6%. This section is still well-profitable in a near future.

In terms of the investment on corperate bonds, ABBANK concentrated on strictly managing the portfolio, maintaining the suitable proportion of the asset for risk management and improving the efficiency. ABBANK closely monitored and regularly evaluated the financial results and business activities of the bond issuing organizations; carried out both the capital and the interest of investment collection at due time. Meanwhile, the bank actively searched and expanded the investment range for new economic corporate bonds issued by stable organizations

with reputable brandname in the market to meet the investing requirements on projects with high feasibility, transparency, and efficiency.

In 2015, ABBANK invested VND 850 Billion to corporate bond issued by major and reputable enterprises with the high asset guarantee, liquidity, or with principal and interest guarantee by prestigious CIs. At 31st Dec 2015, the portfolio of economic organisations bonds attained VND 1,200 Billion, occupying 1.79% of total assets.

With the activeness in evaluating the market interest, ABBANK investment and trading on Government bonds were very positive in 2015; the outstanding invested amount in government bonds was nearly VND 9,000 Billion at the year end. ABBANK is one of the leading banks who did self trading Government bonds in a specialized market. The trading of Government bonds significantly contributed to the profit of ABBANK in 2015.

Investment activities, project implementation

43 Annual Report 2015TOGETHER WE CAN

Financial Figures 2015 2014

Financial FiguresYear Year

% changeX X-1

* Applicable to credit institutions and non-bank financial institutions

Total asset 64,375 67,465 95.42%

Revenue 4,774 4,462 106.99%

Taxes and payables -26 -49 52.76%

Before tax profit 118 151 78.33%

After tax profit 91 117 78.03%

Financial Figures Year Year Note

X X-1

1. Capital

- Charter Capital 4,798 4,798

- Total assets 64,375 67,465

- Capital adequacy ratio 17.5% 14.9%

2. Operating results

- Deposits 56,626 60,911

- Lendings 41,195 42,633

- Debt collection 964 1,455

- Overdue debts 1,053 1,658

- Bad debt 735 1,171

- Capital Using Ratio (Lending/total asset) 64% 63%

- Overdue underwritten debt/ Total outstanding debt Ratio 0.9% 0.30%

-Overdue debts/ Total debt Ratio 2.6% 3.90%

- Bad debt/Total debt Ratio 1.8% 2.70%

Financial situation

FINANCIAL SITUATION

MAJOR FINANCIAL INDEXESFOR CREDIT INSTITUTIONS AND NON-BANK FINANCIAL INSTITUTIONS:

44

OPERATIONAL STATUS IN THE YEAR 2015

Shareholders structure, change in the owner’s equity (at 31st Dec 2015)

Total shares Type of shares Unlimited transferable number of shares Limited transferable shares

479,799,976 Ordinary shares 225,859,552 253,940,424

• Shares

• List of shareholders owning limited transferable shares

• Shareholders structure

Name of shareholders Total owned shares Ownership ratio Number of shareholders

State-owned shareholders 46,318,962 9.66% 2

Electricity of Vietnam (EVN) Corporation 41,586,990 8.67% 1

Electricity of Hanoi. 4,731,972 0.99% 1

Hanoi General Export - Import Company (Geleximco) 62,333,062 12.99% 1

Strategic foreign shareholders 143,961,422 30% 2

Malayan Banking Berhad (Maybank) 95,961,422 20% 1

International Finance Corporation (IFC) 48,000,000 10% 1

Other shareholders 227,186,530 47.35% 5,422

Other insitutional shareholders 41,727,333 8.72% 33

Individual shareholders 185,459,197 38.63% 5,389

Total 479,799,976 100% 5,427

Change in the owner’s equity:

In the fourth quarter of 2015, following the guidance of the Government, EVN carried out the capital divestment (from 16.02% to 8.67%); it is projected that EVN shall divest all the capital invested in ABBANK in the first quarter of 2016.

Name of shareholders Total shares Limited transferable shares Limited time for shares transfer

Electricity of Vietnam (EVN) Corporation 41,586,990 41,586,990

According to Item 1, Article 56, Law on Credit Institutions no. 47/2010/QH12:“Individual shareholders and institutional shareholders who’s representative person holding the position of member of the Board of Directors or Supervisory Board, General Director of Credit Institution are not allowed to transfer their shares during their incumbency.”

Hanoi General Export - Import Company (Geleximco)

62,333,062 62,333,062

Malayan Banking Berhad (Maybank) 95,961,422 95,961,422

International Finance Corporation (IFC) 48,000,000 48,000,000

Board of Directors 5,661,374 5,661,374

Supervisory Board 72,314 72,314

Gereral Director 325,262 325,262

Total 253,940,424 253,940,424

45 Annual Report 2015TOGETHER WE CAN

Shareholders structure, change in the owner’s equity (at 31st Dec 2015)

Increase the green credit growth with sustainable development:

The sustainable development incorporating with ecological environment protection has become a crutial requirement to maintain the development of the country. The banking and financial system as an important link for providing capital for the project of economical and social development, plays a significant role in supporting the economical sectors to plan for substainable development. On March 20th 2014, the Prime Minister issued the Decision No. 403/ QĐ-TTg approving the National Action Plan on Green Growth in Vietnam (GGAP) for the Period of 2014-2020 in order to implement the National Strategy about Green Growth or the Period of 2014-2020. Applying the National GGAP for the Period of 2014-2020, on March 24th 2014, the State Bank of Vietnam Governor issued the Directive No.03/CT-NHNN to promote the green credit growth and manage the environmental and social risks in credit granting activities.

Accordingly, from 2015, the banking sector is required to focus on protecting the environment, improving the efficiency of the utilization of natural resources and energy; improving environmental quality and human health, and ensuring sustainable development. Moreover, credit institutions are required to review, adjust and complete institutional framework in line with the objective of “green growth”; to provide funds for environmental friendly projects and plans on production and business, supporting enterprises to implement green growth.As one of the initial banks implementing the

system to manage the social environment risks in Vietnam under the consultancy of International Finance Corporation (IFC), ABBANK paid great attention to the contents of sustainable and comprehensive development. In 2011, with the support from IFC, ABBANK has widely informed its staff and officially built up and applied the system to manage the social environment risks in credit issuance based on a plan suggested by IFC and complying to the international standards of World Bank. This system was integrated into the business procedure, credit granting procedure, and was synchronously applied with other current risk management process in ABBANK. Specifically, the implementation process can be summarized as followed:

. Firstly, ABBANK created the orientation of green bank by issuing a decision to establish a team to supervise, manage, evaluate the social environment system in which ABBANK assigned Risk Management Division’s dedicated staffs to be responsible for following up the implementation of social environment risk management system in the whole ABBANK and regularly reported to IFC for review and evaluation.

. Secondly, ABBANK carried out the checking, adjusting and completing the internal mechanism and policy to direct to the targets as: checking, updating the contents of social & environmental management policy in

credit granting activities in accordance with ABBANK model; developing annual credit orientation which includes the content of social & environmental management; developing guideline to assess the social environment indicators during the credit granting.

Report the impacts of the Company on the environment and society

COMPLIANCE WITH THE LAW ON ENVIRONMENTAL PROTECTION

46

OPERATIONAL STATUS IN THE YEAR 2015

Report the impacts of the Company on the environment and society

Specifically, ABBANK applied the evaluation criteria of the projects, enterprises who are considered to have high risk operations on the environment in accordance with the international standards from IFC and will certainly refuse to grant credit.

.Thirdly, ABBANK enhanced the capability of the staff when building the orientation “green credit bank” with specific procedures such as organizing training courses, informative campaigns to raise the awareness of the staff about “green credit bank” activities; raising the concept of saving the power and energy efficiency to protect the environment.

According to the agreement between ABBANK and IFC, IFC cooperated with ABBANK dedicated team to organize training courses for ABBANK leaders and managers to effectively implement the policy of “green credit”.

ABBANK believed that with the companion and support from IFC, the attention towards the social and environmental issues in the credit granting activities is a realization of the National Action Plan on Green Growth and Sustainable Development.

47 Annual Report 2015TOGETHER WE CAN

ABBANK pays great attention to the policies releated to the employees to enhance their attachment with the company, acknowledges and encourages the employees to contribute their competence to the bank. ABBANK follows all labor policies regulated by Vietnam law.

- The Team building program is organized annually to encourage the working spirit of ABBANK employees and simultaneously connect all members of ABBANK together through after work communicating activities.

- Annual health check program is carried out to ensure that every employees are cared to maintain good health.

- In addition, members of Talent Pool receive higher priorities as an encouragement to develop this potential staff group.

Labor policies to ensure health, safety, and welfare for employees

Training activities for the employees

POLICIES RELATED TO EMPLOYEES

- ABBANK takes strong commitment to obey the national laws and policy for la-bours, ensuring them to receive sufficient compensation, welfare and insurance in accordance to the existing policies.

- The average annual training hours for employees is from 35 hours / head / year; that number for managers is from 38 hours / head /year.

- The continuous skill developing and training programs to support the employees in maintaining their job and developing their profession include: sales skill, customer service, time management skill, personal development planning skill, management and leadership skills.

The total number of employees at December 31st, 2015 is 2,838.

48

OPERATIONAL STATUS IN THE YEAR 2015

Along with maintaining the stable and efficient commercial activities with the strategic position of a friendly retail bank, ABBANK also pays great attention to the implementation of charity activities, programs / projects for social security to share and propagandize on the responsibility sharing with the community and the society.

With that orientation, ABBANK’s activities for charity, social security, and promotion programs for investment and development have been carried out in the poor and hard areas such as the North Western area, the Midland area, and the South Western area. ABBANK regularly devotes a quite a large budget for community activities such as An Binh Tet or Compassion Summer; sponsors for the social security projects with the with the desire of contributing to the country development. From 2011 to 2015, ABBANK has reserved a budget up to VND30 billion for social security and community activities.

ABBANK social security activities mainly focus on supporting for living and educational conditions for the residents in remote provinces: constructing traffic roads in Tan Trao district (Tuyen Quang province); building schools in Duc Co district (Gia Laiprovince), Meo Vac district (Ha Giang province), Kim Dong and Kim Son district (Ninh Binh province); building up charity houses in An Giang province; sponsoring the hospital equipments… these areas are the main points

of social security policies of the government.The sixth Lunar New Year Gala, An Binh Tet was organized at the beginning of 2015 with the topic “An Binh Tet – Sympathy for Ocean and Islands” is a spiritual present connecting people of the main land with those living in the distant islands. In the Gala, ABBANK leaders, together with the staff, directly deliver meaningful presents to encourage and support the preparation of the Tet holidays for 100 fisherman families living in Ly Son Island district (Quang Ngai province) and soldiers in Region 2 Command of Vietnam Coast Guard (Nui Thanh district, Quang Nam province). At Ly Son Island, ABBANK planted a Barringtonia asiatica tree, a symbol of Vietnamese island district, contributing to the improvement of the ocean and island green environment.

In terms of environmental activities, ABBANK sponsored for the “For a green future” TV program broadcasted on VTV3, a program with short movies conveying meaningful messages about environment protection. Along with the companionship with the program, ABBANK proactively participated in charity and promotion activities to protect the environment such as the “Protecting the environment of ocean an island” campaign in Ly Son and Quang Ninh, the “Earth hour” campaign, the “Riding bicycle for the environment”, the “Recycling day” festival day, and held extra-curricular environmental class at the Giac Vien pagoda (HCMC)… Through

these activities, ABBANK contributed to the call for awareness of a green lifestyle respecting environment and natural resources.

Internal calls for saving clean energy and resources as well as building green offices and green life have become a positive way of life and habits of ABBANK staff.

REPORT ON THE BANK’S RESPONSIBILITIES TO WARDS LOCAL COMMUNITIES

49 Annual Report 2015TOGETHER WE CAN

50

OPERATIONAL STATUS IN THE YEAR 2015

FOR A GREEN FUTURE

51 Annual Report 2015TOGETHER WE CAN

AN BINH TET - 2015

EMPATHY BETWEEN THE TWO LEAVES

52

OPERATIONAL STATUS IN THE YEAR 2015

53 Annual Report 2015TOGETHER WE CAN

ABBANK positively participated in the meetings of green credit growth to share practical experiences from international institutions like IFC (a member of World Bank) or the Vietnam Bank Assiociation. ABBANK aims to increase the proportion of green credit in the credit portfolio list of the bank through researching and developing green credit products, credit programs with encouraging policies for production and commercial projects with green growth

goals, improving the service quality; creating favorable conditions for green credit growth, pay attention to production and commercial projects that aim for the green growth; preferring to grant green credit for economical fields that carry out preservation, development and efficient exploitation for the natural resources, for modern technological achievements, saving energy, developing clean energy, renewable energy, using environmental friendly technologies

and equipments, producing environmental friendly products.

Regularly report to the State Bank of Vietnam about the implementation of green credit as requested.

REPORT ABOUT GREEN CREDIT

54

BOARD OF MANAGEMENT’S REPORTAND ASSESSMENT

Based on the situation of the nation’s economic improvements, stability of the macro-economy, as well as

the flexible and timely currency policies from the State Bank of Vietnam, the business operation of ABBANK

in 2015 achieved positive results.

The total outstanding loan in Market 1 exceeded the milestone of VND 30,000 Billion

In 2015, the total outstanding loan in Market 1 was VND 30,915 Billion, completing 108% of the 2015 plan, 19% higher than 2014, and officially exceeded the value of VND 30,000 Billion. Strictly following the orientation to become a leading bank in Vietnam focusing on retail banking in which the activities in Consumer Banking is the priority, the consumer outstanding loan early exceeded the milestone of VND 10,000 Billion at the end of Quarter 3, 2015 and reached the value of VND 11,233 Billion by the end of 2015, completing 118% of 2015 plan, increasing 36% as compared with 2014’s.

The operational profit gained remarkable improvement

The total operational income in 2015 achieved VND 1,972 Billion, increasing 17% in comparison with 2014’s. Meanwhile, the operational cost was strictly controlled; therefore, the operational profit before the risk provisions in 2015 reached VND 781.6 Billion, gaining an increase of 35% as compared to 2014’s; this is also the highest growth since 2011.

2006

2007

2008

2009

2010

2011

2012

2013

20142015

0 10.000 20.0003 0.000 40.000 50.000

1.551

6.776

6.674

15.002

23.45720.250

28.940 37.162

45.404 47.881

The figures of the years 2010, 2011, 2012, 2013, 2014, 2015 are based on the consolidated financial report. The statistic of Mobilization is only for Market 1.

Assessment of Bank operational results

TOTAL ASSETS

Unit: VND Billion

MOBILIZATION

Unit: VND Billion

64,375

67,465

57,628

46,013

41,542

38,016

26,518

13,494

17,174

3,113

20,000 40,000 60,000 80,000 100,000

2006

2007

2008

2009

2010

2011

2012

2013

20142015

01 0,000 20,000 30,000 40,000 50,000

1,551

6,981

6,674

15,002

25,94725,489

33,358

40,608 45,103

47,530

55 Annual Report 2015TOGETHER WE CAN

The debt work-out activities continued to be focused and strengthened,, the NPLs ratio was controlled under 3%

In 2015, the bad debt handling process was continued to treat with priority and speeded up by many flexible measures like collecting cash, receiving additional collateral, restructurizing, using provision fund to cover or selling debt to Vietnam Asset Management Corporation (VAMC). At December 31st, 2015, NPLs ratio has been reduced to less than 3% . At the end of 2015, the NPLs ratio remained 1.72% of the total loan, reduced from 2.75%% of 2014’s.

The first time ever ABBANK is ranked by Moody’s and was amongst the best credit rating banks in the market

Adding to the positive news of ABBANK operational result in 2015, the first time ABBANK was rated by Moody’s as one of best credit ratings in the market has contributed to enhance its prestige and affirmed its position in the banking industry. The system operation continued to be improved and achieved positive results

With the completion of the centralizing of Credit Support, Finance and Accounting, and Procurement activities, ABBANK has achieved positive progress in the effective cost control and disbursement.

2006

2007

2008

2009

2010

2011

2012

2013

20142015

0 10.000 20.000 30.000 40.000 50.000

1.131

6.858

6.538

12.883

20.01920.125

23.266

37.558

42.633

41.195

The figures of the years 2010, 2011, 2012, 2013, 2014, 2015 are based on consolidated financial report.

528,3

151,1118,4

Unit: VND Billion

Unit: VND Billion

OUTSTANDING LOAN (Consumer Banking & Corperate Banking)

PROFIT BEFORE TAX

2006

2007

2008

2009

2010

2011

2012

2013

20142015

0 10,000 20,000 30,000 40,000 50,000

1,131

6,858

6,539

12,883

19,87719,916

18,756

23,647

25,969

30,915

107.7

528.3

151.1

185.1

401.6661.4

412.6

230.865.4

80.8

118.4

56

Financial Situation

Assets

The total asset of ABBANK at the end of 2015 was VND 64,375 Billion, reducing VND 3,090 Billion (equivalent to 5%) as compared to the end of 2014, due to the reduction of inter-bank mobilizing capital in accordance to the State Bank of Vietnam’s orientation of substantial asset growth.

However, there was a remarkable increase in the mobilization from individual customers and economic institutions with VND 2,427 Billion (equivalent to 5%) higher than 2014’s, providing a capital resource for credit growth and the securities investment. Specifically:

+ By at the end of 2015, Loans in Market 1 increased by VND 4,946 Billion, equivalent to a rise of 19% in comparison to the end of the previous year. + There was an increase of VND 614 Billion on securities investment, equivalent to an increase of 4% as compared with the previous year.

This result indicated the flexibility in capital management, improving the efficiency and creating remarkable profit resource for the bank.

BOARD OF MANAGEMENT’S REPORT AND ASSESSMENT

Liabilities

Following the directive of the State Bank of Vietnam about the increasing the stability of the the inter-bank market, ABBANK restructurized the capital with the orientation of increasing the mobilization from Market 1, reducing the inter-bank transactions, re-balancing the capital resource.

In details, the capital mobilization from the inter-bank market reduced by VND 6,713 Billion, equivalent to 42% as compared to the previous year. This statistic showed that ABBANK reduced the dependence on the market 2, increasing the capital mobilization from the market 1, contributing to substainable development of the bank..

In addition, the bank has established a limitation system to control the currency position according to the risk management strategies in each period and permanently ensure the compliance towards the regulated limits. Therefore, the impact of the exchange rate changes on the bank was not much.

57 Annual Report 2015TOGETHER WE CAN

Improvements in organization, policies, and management structure

ABBANK has selected a modern management method aiming at the transparency and professionalism in operations, shown in the bank’s attempt of structurization. In 2015, ABBANK has implemented and improved the centralized accounting and payment model, and continued to implement the support for credit and payment to be centralized in the Head Office.

The organization structure of the business units was improved with the orientation of focusing on the business system, simplifying the operational part and supporting activities at branches in order to continue the orientation of centralization.

In order to improve the organizational structure to suit with the practical business requirements, ABBANK has establish the Write - off Committee and the Loan work - out committee which are directly affiliated to the Board of Director; the legal and Compliance Department, and Finance & Accounting Division that were restructurized from the Support and Service Division.

This change in structure shall increase the capability of financial management, provide the common services for the whole system, simultaneously enhance the

risk management capability and internal supervision, contributing to increase ABBANK’s operational safety.

The policies of HR management have been completed and promulgated in the sections such as recruitment, salary, compensation, competition, and awarding, efficiently

managed workloads, working disciplines, labor contracts, training and developing human resources. These policies have created a foundation for a systematic HR management with the aim of providing effective HR services for business, contributing to the enhancement of the organization management capability in general.

58

The Vietnam economy in the year 2016 is predicted to maintain stabability with continuous development, and the efficiency of national investments keeps improving.

In 2016, with the orientation of sustainable development in line with the expansion in scale, ABBANK continues to carry on restructuring projects, pushing the long-term developing strategy, and enhancing the added values to the shareholders, customers and employees in the up-coming years.

In order to achieve the financial targets, the core missions 2016 are stated below:

Continue to maintain the high credit ratings in the market2015 is the first year when Moody’s has granted high credits ratings to ABBANK amongts the Vietnamese joint commercial banks. In 2016, aiming to sustain this success, ABBANKwill continue to maintain the high credit ratings which is expected to bring positive results and raise the influentiality of the ABBANK brand in Vietnam banking industry, especially to raise ABBANK reputation and attract customers and partners to use ABBANK

services. In addition, in 2016 ABBANK also aims to achieve an internationally recognized award in retail banking.