Annual Report 2015 - Camposol€¦ · Annual Report 2015. 2 1 ... by increasing the conversion of...

79

Annual Report 2015

Transcript of Annual Report 2015 - Camposol€¦ · Annual Report 2015. 2 1 ... by increasing the conversion of...

Annual Report

2015

12

Annual Report 2015 CAMPOSOL

Annual Report

2015

2

Content1. Letter from the CEO ........................................................ 4

2. Overview .............................................................................. 62.1 Vision2.2 Mission 2.3 Corporate Values 2.4 Business Principles 2.5 Our People2.6 Board of Directors 2.7 Management Team 2.8 Organizational Chart2.9 Legal Structure 2.10 Brief History

3. Products & Categories ..................................................... 20

4. Board Of Directors Report ............................................. 304.1 Main Activities 4.2 Market Situation 4.3 Company Strategy 4.4 Summary of the Year4.5 Operations 4.6 Working Environment4.7 Code of Ethics & Conduct4.8 Social Responsibility 4.9 Research, Development and Innovation 4.10 Supply Chain 4.11 Financial Results 4.12 Allocation of Net Income 4.13 Internal Audit and Internal Control4.14 Financial Calendar4.15 Future Prospects 4.16 External Auditors 4.17 Corporate Governance

5. Key Investment Considerations ................................... 46

6. Independent Auditor’s Report And

Audited Financial Statements ....................................... 48

54

Annual Report 2015 CAMPOSOL

Twenty-fifteen was a challenging year for CAMPOSOL, as well as for the Peruvian agricultural exporting sector in general, due to lower volumes as a result of the “El Niño” phenomena.

However, we have been able to keep our leadership in the Peruvian agro-industrial sector and face these situations with fast answers and a clear view of the company strengths, which we address with fresh and healthy products that, we believe, have the best perspectives in the future.

In this sense, in 2015, CAMPOSOL’s total sales amounted to USD 272.9 million (vs. USD 253.5 million in 2014) and EBITDA amounted to USD 42.4 million (vs. USD 34.0 million in 2014). In 2015, profit amounted to USD 12.5 million compared to the loss of USD 34.4 million during the same period last year.

The main reasons for the increased revenues for all 2015 were higher volumes of blueberries and shrimp, and in the prices of avocados to 1.97 per net KG (1.81 in 2014), mangos to 1.68 per net KG (1.48 in 2014) and blueberries to 10.84 per net KG (10.46 in 2014). This represents up 8.8%, 13.5% and 4%, respectively.

Selling expenses decreased from USD 37.6 million in 2014 to USD 30.3 million in 2015 due to changes in financial conditions of sale (change of FOB to CFR / CIF terms) applied to higher volumes sold. This decrease was primarily as a result of a USD 3.5 million decrease in 2015 selling expenses from freight and customs duties, a USD1.3 million decrease in 2015 selling expenses from representation expenses, USD 2.1 million no provision for amortization of intangible management portfolio, which occurred in 2014.

Total inventories decreased from USD 95.2 million at December 31st, 2014, to USD 47.1 million by the end of the fourth quarter of 2015. The variation of USD 48.1 million is explained mainly by the decrease of finished product such as artichokes, asparagus, and peppers. Also, trade accounts receivable decreased from USD 46.0 million at the end of 2014 to USD 40.7 million at the end of 2015, explained by higher collections to clients.

As a result, the total working capital (accounts receivable + inventories - accounts payable) decreased to USD 53.4

million at the end of 2015 from USD 92.9 million at the end of 2014. Current working capital as of December 31st, 2015 is 19.8% of sales (34.7%). Such significant reduction is the result of the company´s effort to improve working capital needs.

In the future, the Company expects to continue its diversification strategy by increasing the blueberries production in the Fruits & Vegetables (F&V) segment and by increasing the conversion of shrimp ponds in the Seafood segment. The Company also expects to continue to reinforce the Trading segment through more direct sales to retailers, adding value to its clients through commercial, marketing and service initiatives, which should result in higher margins.

In line with this strategy, the Company has invested significantly in specializing the company in the F&V segment, diversifying its portfolio of products and customers, as well as increasing its presence in key markets with favorable and encouraging results. In line with this vision, the Company has decided to continue empowering its fresh and frozen business segments, and exit the preserved business. The Company considers these strategic changes in CAMPOSOL’S businesses will allow for greater specialization, efficiency and focus on product categories in which the Company has made significant investments in recent years, and thus maximize opportunities for growth and consolidation of its business.

Likewise, 2016 will require us also to focus on consolidating CAMPOSOL’S structure, processes, and policies, as well as reinforcing aspects regarding good corporate governance, internal control, forecasts, and project development, among others.

Based on CAMPOSOL’s solid fundamentals and market perspectives we believe that we will be able to position as a worldwide and leading healthy food company shortly.

Yours sincerely,

Manuel Salazar Diez CansecoCEOCamposol Holding Ltd.

01 Letter from the CEO

IN THE FUTURE, THE COMPANY ExPECTS TO CONTINUE ITS DIVERSIFICATION STRATEGY BY INCREASING THE BLUEBERRIES PRODUCTION IN THE FRUITS & VEGETABLES (F&V) SEGMENT AND BY INCREASING THE CONVERSION OF SHRIMP PONDS IN THE SEAFOOD SEGMENT.

DEAR ShAREhOLDERS, PARtnERS AnD COLLAbORAtORS

76

Annual Report 2015 CAMPOSOL

CAMPOSOL is the leading agro industrial company in Peru, the largest avocado grower and soon the largest blueberry producer in the world. It is involved in the harvest, processing, and marketing of high-quality agriculture and marine products, such as avocados, blueberries, grapes, mangos, tangerines, shrimp, scallops, among other, which are exported to Europe, the United States of America and Asia.

CAMPOSOL is a vertically integrated company located in Peru, it is the third largest private employer in the country, with more than 15 thousand workers in high production seasons, and is committed to supporting sustainable development through social responsibility policies and projects aimed to increase the shared value for all of its stakeholders.

CAMPOSOL was the first Peruvian agro-industrial company to be a member of the United Nations Global Compact, the first to present annual Sustainability Reports (aligned to GRI indicators) and has achieved the following international certifications: BSCI, Global Gap, IFS, HACCP and BRC among others.

2.1 ViSiOn

Our vision is to become one of the main five leaders to provide healthy food to families worldwide.

2.2 MiSSiOn

Our mission is to provide the world healthy day-to-day food with guaranteed quality, seeking the welfare of people and the environment through innovation, research, and care in all details of its processes.

2.3 VALuES

CAMPOSOL has established the following corporate values:

integrity: We are honest. We honor our commitments and are responsible for the consequences of our actions, always contemplating the triple bottom line: economic, social and environmental.

02Overview

CAMPOSOL IS THE LEADING AGRO INDUSTRIAL COMPANY IN PERU, THE LARGEST AVOCADO GROWER AND SOON THE LARGEST BLUEBERRY PRODUCER IN THE WORLD.

98

Annual Report 2015 CAMPOSOL

Respect: We appreciate and esteem people. We foster good relations within an environment where ideas and feedback are highly appreciated.

teamwork: We share our objectives and strategies, and we strive to be communicative and transparent, creating an open and flexible atmosphere where team objectives take precedence over personal goals.

Excellence: We all work to attain the highest standards of performance, innovation, and quality in all stages of our processes, activities and products. We pay close attention to details and endeavor to comply with the international market demands and expectations.

Austerity: We work towards achieving efficiency along the whole chain of value while maintaining strict discipline on our cost management and implementing policies that impede questionable spending.

2.4 buSinESS PRinCiPLES

CAMPOSOL acts according to four primary principles that guide its activity and interaction with society.

human Resources Management: CAMPOSOL recognizes its commitment with its collaborators to establish the best working conditions that allow their well-being as well as their professional and personal development, in a pleasant environment. Further, CAMPOSOL provides permanent training opportunities and seeks to identify and acknowledge its most outstanding workers.

Ethics: CAMPOSOL is convinced that each one of its members must apply ethical principles to all of its relations with clients, suppliers, shareholders, employees and the society in general, as they guarantee CAMPOSOL’s reputation in the markets.

Honesty, dignity, respect, loyalty, proper behavior, efficiency, and transparency are the highest values that guide CAMPOSOL’s relationship with its stakeholders.

Social Development and Community Relations:CAMPOSOL is committed to balancing its impact caused by its operations, as well as improving the positive impact that creates value for the community in general. Thus, we work under social responsibility guidelines in our areas of influence.

CAMPOSOL promotes ethical relations based on trust to our community in general, its inhabitants, local, regional and national government, as well as the support organizations and other involved actors, to establish a permanent dialog and mutual respect with our neighbors.

Quality, Environment, Safety and health: CAMPOSOL’s products directly affect its clients’ health, which demands CAMPOSOL to be aligned to the primary international standards that guarantee that its products are free of risks for human consumption. Thus, the concept of innocuousness is of inestimable value in all of CAMPOSOL’s industry and chain of value.

All of CAMPOSOL’s products are manufactured with processes that comply with legal norms and stringent regulations related to its activities that include local laws and destination countries’ regulations, world-recognized international standards, requirements, protocols, standards and specifications from clients and the internal norms and procedures established in CAMPOSOL’s integrated management system.

2.5 OuR PEOPLE

The development of a competitive agro-exporting industry is essential for Peru because of, amongst other reasons, its great contribution to the generation of formal employment opportunities in the country. During the last ten years, Peru has been able to create more than 800,000 jobs in modern agriculture. Such development provides income and promotes economic clusters in areas where there are no other major employment options. CAMPOSOL is highly committed to its people and their development, even more, when the Company is on its way to becoming the largest employer in the country in the next few years. A characteristic of our industry is the seasonal

employment due to the diversification of our production that depends on factors such as weather patterns, each product´s harvest periods and contingencies that arise throughout its cycles.

In 2015, CAMPOSOL´s family was comprised of over 15,000 collaborators during high production seasons. The largest number of our workers come from adjacent areas to our orchards in the district of Chao, province of Virú, region of La Libertad, followed by our operations in the Piura region; both of which present high unemployment and low education rates.

CAMPOSOL also generates an impact on the indirect employment of the areas in which it operates because it also hires third-party companies for transportation, food service, lab and health services, amongst others, most of which are rendered by companies established by members of its communities. Please refer to the Section “Working Environment” in this report, for more detailed information on these matters.

IN 2015, CAMPOSOL´S FAMILY WAS COMPRISED OF OVER 15,000 COLLABORATORS DURING HIGH PRODUCTION

SEASON. THE LARGEST NUMBER OF OUR WORKERS COME FROM ADjACENT AREAS TO OUR ORCHARDS.

1110

Annual Report 2015 CAMPOSOL

RAúL ubALDO FERnánDEzDeputy Chairman

Mr. Fernández holds a master ’s degree in Industrial Safety and Health and a bachelor’s of Science degree in Mechanical and Marine Engineering from the University of Buenos Aires, Argentina. He is considered a visionary leader, an accomplished executive and also an internationally recognized results-driven operations and technology expert. He brings 40 years of food industry experience, leading business units, new products and business development teams in multinational corporations. Lately, he has focused on developing and implementing revenue enhancing strategies for companies involved in international food trading and commercialization. He is named in 11 patents regarding fresh food preservation, packaging, and handling. He is a member of the CAMPOSOL Holding Ltd. board since November 2015.

Mr. Dyer Coriat obtained his degree in Business Administration at University of Miami (Florida) with a specialization in Finance and Administration. He has vast experience in the fishing industry; he initiated his career at Copeinca as Fleet Assistant and held subsequently various positions, including Fleet Manager, Operations Manager, and CEO since 2002 to 2011. Mr. Dyer was appointed a member of the Board of Directors of CAMPOSOL, an agro-industrial company of the Group, in 2008, a position which allowed him to contribute to the transformation of the business into a leading commercial organization that uses the principles of Corporate Governance and Social Responsibility. Since 2011, he is the Chairman of CAMPOSOL’s Board, as well as CEO of D&C Group. He was also CEO of CAMPOSOL from October 2011 to October 2015.

SAMuEL DyER CORiAt Chairman of the Board of Camposol Holding Ltd.

PiERO DyER CORiAt Director

Mr. Dyer Coriat obtained his Master in Business Administration and Bachelor in Mechanical Engineering of the University of Miami (Florida). He worked as the technical and financial analyst for the new business division at D&C Group. He was General Manager at Apurimac Ferrum, an iron exploration project. He has been a member of Copeinca ASA’s Board of Directors, as well as CFO, Research, and Development Manager and Chief Strategy Officer at CAMPOSOL. He is currently a member of the CAMPOSOL’s Board of Directors.

WiLLiAM DyER OSORiO Director

Mr. Dyer Osorio has a degree in International Business Administration from the International University of Florida (Florida), with a specialization in Economics and a master ’s degree in Business Administration from Thunderbird University, Arizona, and Tecnológico de Monterrey (Mexico). He has broad experience in the Peruvian fishing industry, and began his career at Copeinca as Plant Assistant and held different positions, including Warehouse Assistant, Procurement Assistant, Finance Assistant, Logistics Manager, and Raw Material Procurement Superintendent from 2002 to 2010. He currently serves as General Manager of Octopus Holding S.A.C. and Inka Comfort Hoteles del Peru SAC. Mr. Dyer is also a member of the Board of Directors and shareholder of Aceros y Techos S.A., Galvanizadora Peruana S.A., and Octagon Holding S.A.C, companies from Duferco Swiss Group.

ShEyLA DyER CORiAt Director

Mrs. Dyer earned a bachelor´s degree in Business Administration at the University of Miami (Florida) in 1996. She is a senior executive with experience in international trade, operations, and logistics at international companies. In 2014, she founded Comma; a Peruvian restaurant focused on healthy food. She is a member of CAMPOSOL Holding Ltd.’s board since November 2015.

2.6 bOARD OF DiRECtORS

1312

Annual Report 2015 CAMPOSOL

PEDRO JAViER MORALES GARCéSCamposol Fruits & Vegetables CEO

MAnuEL SALAzAR DiEz CAnSECOCEO of Camposol Holding Ltd.

JORGE RAMiREz RubiOCamposol Seafood CEO

Mr. Morales is an agricultural engineer from the Universidad Nacional Agraria La Molina with an MBA from ESAN University. Mr. Morales has vast experience in the agro-industrial sector. He began his career at CAMPOSOL 15 years ago as Head of Parcel; he subsequently became Head of Farm and was appointed Superintendent of New Areas in 2004, responsible for sowing 2,000 ha of asparagus. In 2009 he was promoted to Manager of New Crops and was responsible for managing 1,400 ha plantation of avocados, grapes, and tangerines in La Libertad. Then, in 2011, he was appointed Manager of the Asparagus Business Unit. Later in 2013, he took over the Blueberry Business Unit and at the end of 2013 has been named Deputy CEO at CAMPOSOL, until 2014 when he was appointed CEO of CAMPOSOL Fruits & Vegetables.

Mr. Ramirez holds a bachelor’s degree in Business Administration with a specialization in Finance from the Loyola University (New Orleans, USA) and an MBA from ITESM (México) - ESPOL (Ecuador). He has vast international experience in Strategic Planning, Corporate Finance, Mergers & Acquisitions and International Affairs. Mr. Ramirez worked previously at Amanco Group and Mexichem (1995-2008) and held various positions in Ecuador, Costa Rica and Brazil, his last one being CFO for Latin America. He has also served as CFO at CAMPOSOL Holding Ltd. (2008-2013), Copeinca ASA (2012) and Grupo EFE (2014-2015).

CARMEn ROSA GRAhAM AyLLón Director

Mrs. Graham is a business manager graduated from the Universidad del Pacífico, IBM Systems Engineer, and MBA from the Adolfo Ibáñez School of Management in Miami. She has advanced studies in management, corporate responsibility, and innovation at universities of Harvard, Georgetown, Monterrey, and Piura. She has been General Manager at IBM Colombia in 1999, General Manager at IBM Peru and Bolivia in 2011, and IBM Regional Strategy Manager in 2004. Mrs. Graham has been rector of the Universidad del Pacífico in 2007. She is currently an advisor in governance and member of the Board of Directors of Ferreycorp S.A., Interbank, and Nextel del Perú, as well as a member of the Consultative Committee at APM Terminals and Chairwoman at Fundación Backus and WCD Peru (Women Corporate Directors).

SuSAnA ELéSPuRu GuERRERO Director

Mrs. Eléspuru became a member of CAMPOSOL’s Board of Directors in May 2014. She developed her career as a senior executive, business consultant and search of managers for more than 30 years. She began her career at Procter & Gamble, where she was Deputy Corporate Chairwoman, Chairwoman of the Board of Directors, and General Manager for Peru, Ecuador, and Bolivia. Ms. Eléspuru chaired Eléspuru Consultores, a company related to strategic management for multinational and local companies. She has vast experience in corporate governance, strategic planning, business competitiveness, and organizational development. She was chairwoman of IPAE from 2011 to 2013, chaired the CADE 2001, and led the Escuela de Empresarios of IPAE.

2.7 MAnAGEMEnt tEAM

Mr. Salazar holds a bachelor’s degree in Economics from Clark University (Massachusetts, USA), an MBA from Georgetown University (Washington, USA), and a Ph.D. in Management from the University of Lleida (Spain). He has more than 20 years of professional experience in managerial roles of local and regional responsibility in large companies with an exceptional career. His previous position was as CEO of Louis Dreyfus Commodities for Peru and Chile. Mr. Salazar began his career at Banco de Crédito del Perú in 1991 and consolidated in the banking sector. He ultimately assumed the position of Risk Manager for the Andean region at West Merchant Bank. He Later was Manager of Planning and Strategy at Corporation Lindley - after the acquisition of ELSA. He has a solid background as CEO, including the design of strategic, commercial and financial planning for large and complex organizations that operates in different markets, as well as broad experience in leadership, culture transformation management and control systems.

1514

Annual Report 2015 CAMPOSOL

ALEJAnDRO ARRiEtA POnGOLegal & Corporate Affairs Manager

MARíA CRiStinA COutuRiER LLEREnAFinance and Administration Manager

GuiLLERMO DEFiLiPPi RODRíGuEzHuman Resources & Development Manager

JOSé AntOniO GóMEz bAzánCamposol Trading CEO

FRAnCESCA CARnESELLA FiGuEROLAMarketing, Communications and Sustainability Manager

MARiO MELGAR DE LA PuEntESupply Chain Manager

Mr. Arrieta is an attorney graduated from the Universidad de Piura. He has previously worked as Senior Associate at Rodrigo, Elías & Medrano and Lazo, and De Romaña & Gagliuffi. His excellence and performance on these law firms have been recognized in the 2014 issue of the “The Legal 500 Latin America”, an international magazine specialized in the research of performance of law firms worldwide. He has also been a counsellor at the Ministry of Economy and Finance (National Council for Competitiveness) and has worked as a professor at the Faculty of Law at the Universidad de Piura and associate professor at the Faculty of Law in the Pontificia Universidad Católica del Perú. Mr. Arrieta has published research papers in different specialized magazines and newspapers. He currently participates as a speaker in different programs.

Mrs. Couturier is CFO and is responsible for Corporate Finance, Accounting, Treasury, Information Technologies, Business Planning and Administration. Mrs. Couturier holds an MBA in finance and a BA in Economics from Hofstra University (New York, USA). Mrs. Couturier has over 23 years of experience and has held positions in various multinational corporations. She was Chief Financial Officer at SN Power Peru S.A. (Statkraft) from 2008 through 2013. She has also worked in other industries and companies such as Electroandes S.A., PSEG (USA), jP Morgan Chase/Flemings (UK), Prisma SAB, and Southern Copper Corporation. Mrs. Couturier has extensive experience in corporate finance, mergers and acquisitions, and change management.

Mrs. Carnesella is an economist from the Universidad del Pacífico and has an MBA from the Universidad de Piura and post-graduate studies in communications and social responsibility at the Pontificia Universidad Católica del Peru and ESAN, respectively. She has served as counselor to the Minister of Economy and Finance, as well as to the Minister of Energy and Mines, and Chairman of the Private Investment Promotion Commission. She was appointed Press & Communications Director of the Ministry of Foreign Affairs in Peru. She was the Image and Communications Manager at BBVA and General Manager at the BBVA Foundation, as well as Corporate Image Manager at TIM Peru (now Claro).

Mr. Melgar is a corporate communication specialist graduated from Universidad de Lima and has a master’s degree in Transport and Logistics (the Blue MBA) from Copenhagen Business School (Copenhague, Denmark). He has also taken a post-graduate course in Project Management from the Implement Consulting Group (Denmark). Throughout his experience at Maersk Line, he developed the Areas of Marketing, e-Commerce, and sale of transport services for perishable goods. Mr. Melgar has also worked as Managing Director for Logistics Operations at Geodis Wilson. He has a 20-year experience leading projects related to international transport and logistics solutions in Peru and Europe.

Mr. Defilippi is an attorney graduated from the Pontificia Universidad Católica del Perú, has a degree in Human Resources Management from CENTRUM and the Universidad de Barcelona (Spain). Mr. Defilippi has more than 20-year experience in Human Resources Management and has developed strategies and implemented programs for attracting, retaining and developing talent in companies such as Warner-Lambert Peru, Colgate-Palmolive Peru, Mission Hills (Mexico), Yanbal International and Minsur. He has also led programs for talent management and employee engagement.

Mr. Gómez has extensive international experience in the food industry and international trade. He is a PMA board member and past chair of the Institute of Asparagus and Vegetables. His previous experience includes management positions at Chiquita Brands International in the U.S.A., Costa Rica, and Europe, and most recently as General Manager with headquarters in Florida. He was formerly Director of Corporate Banking Projects at Banco de Crédito del Perú and Project Manager at IBM Peru.

1716

Annual Report 2015 CAMPOSOL

BOARD OF DIRECTORS

CFO

SUPPLY CHAIN MANAGEMENT

INTERNAL AUDIT

MANGOES & GRAPES

BUSINESS UNIT

ASPARAGUS & MANDARINS

BUSINESS UNIT

AVOCADOBUSINESS

UNIT

BLUEBERRYBUSINESS

UNITTRADE OFFICE

EUTRADE OFFICE

USAOPERATIONSCOMMERCIAL

CORPORATE GENERAL MANAGER

FRUITS & VEGETABLESGENERAL MANAGER

TRADINGGENERAL MANAGER

SEAFOODGENERAL MANAGER

HUMAN MANAGEMENT AND DEVELOPMENT

LEGAL AND CORPORATE AFFAIRS

INFORMATIONTECHNOLOGY

CORPORATE FINANCE

ADMINISTRATION

FOREIGN TRADE

HUMAN DEVELOPMENT

MARKETING, COMMUNICATIONAND SUSTAINABILITY

PROCESS AND CONTINUOUS IMPROVEMENT

CORPORATECOMMUNICATIONS

OPERATIONS

LOGISTICS

COMMERCIAL FRESH & FROZEN

IMS - R&D

FINANCE

HUMAN RESOURCESMANAGEMENT

OPERATIONS SOUTH AREA

SALES MANAGER

OPERATIONSMANAGER

OFFICE MANAGER

INTENSIVE GROW

SEMI- INTENSIVE

GROW

LAB

MAINTENANCE

FINANCE

IMS

HUMAN RESOURCES AND ADMINISTRATION

FRESH PRODUCTS

STOCK UP ON

SALES MANAGER

OPERATIONSMANAGER

OFFICE MANAGER

LOCAL SALESOFFICE

INVESTOR RELATIONS

GENERAL ACCOUNTING

SHRIMP BUSINESS

UNIT

2.8 ORGAnizAtiOnAL ChARt

1918

Annual Report 2015 CAMPOSOL

2.9 LEGAL StRuCtuRE 2.10 bRiEF hiStORy

CAMPOSOL began operating in 1997 after purchasing its first land stock in La Libertad region located in the north of Peru, approximately 600 Kms. from Lima. During that same year, the company was able to acquire more land in the same region through a public option in the context of the Chavimochic Special Irrigation Project.

In its first and second stage, the Chavimochic Special Irrigation Project has supplied water to more than 78,000 Has of the desert on the northern coast of Peru. Nowadays, the third stage of the project is expected to allow the development of another 60,000 Has in its area of influence by several private companies.

In 1998 the Company began to acquire and develop land in Piura, located 1,000 Kms. North of Lima, and by the end of 1999, CAMPOSOL began exporting agro-industrial products.

The vision and the commitment of everyone involved in the objectives of the Company resulted in CAMPOSOL rapidly becoming the leading agro-industrial company in Peru, annually occupying the first place in agro-exports and generating approximately 15,000 direct work positions during the high production seasons. Today, the Company has more than 24,000 own Has between Chao, Virú, and Piura.

In 2006, CAMPOSOL founded Marinazul with which it began an aquaculture business producing and exporting shrimp in the Tumbes region, located in the extreme north of Peru. This Company has grown and diversified consistently ever since becoming the leader in the country occupying today more than 2,000 own hectares, as well as having the most modern private biotechnology research and development installations in Peru.

At present, CAMPOSOL is the largest grower of Hass Avocados in the world, soon to be the largest producer of blueberries in the world. It is involved in the harvest, processing, and marketing of other high quality agricultural and marine products such as avocados, blueberries, grapes,

mangos, tangerines, asparagus, shrimps, with commercial offices in the United States of America (Florida) and Europe (Rotterdam).

As a more mature company, CAMPOSOL is orienting its efforts towards innovation and biotechnological research. At the same time, CAMPOSOL is looking to increase its skills in the marketing programs using an even greater international presence as well as alliances with companies and clients that have significant experience, leadership, and coverage in important markets around the world. Given the performance, CAMPOSOL has had during the last decade and the growing preference of consumers for quality food that contributes to good health, the Company can look towards the future with optimism, supported fundamentally on the solidness of its operations, the professionalism of its employees and its good corporate practices.

(1) Includes 100% ownership of Camarones S.A.C., Pacífico Azul S.A., Marante Investment S.A.C., Palmas Hill Investments S.A. and Congelados y Frescos S.A.C.; a 80% stake in Corporación Refrigerados INY S.A. and a 75% in Pesquera ABC S.A.C.

(2) Includes 100% ownership of Muelles y Servicios S.A.C. and Nor Agro Perú S.A.C., and 69.76% stake in Marinasol S.A. (with the remainging 30.24% owned by Madoca Corp.)

CAMPOSOL HOLDING LTD. (CY)

CAMPOSOL S.A. (2)

MARINAZULS.A. (1)

CAMPOINCAS.A.

CAMPOSOL EUROPA S.L. (SP)

CAMPOSOL FRESH B.V. (NL)

PERSEA INC(US)

CAMPOSOL FRESH (US)

GRAINLENS LTD. (CY)

SIBOURE HOLDINGS LTD. (CY)

BLACKLOCUSTLTD. (CY)

MADOCA CORP. (PA)

99.999999%

0.02% 0.000001%

99.98%

27.38%

87.27%

12.73%

46% 0.2%

54%

61.33%

94.55%

100%

100%

100%

63.94%

8.6%

0.004%

38.665%

99.80%

2120

Annual Report 2015 CAMPOSOL03

Products and categories

CAMPOSOL considers paramount to maintain a diversified portfolio of products, to exploit the selling windows better and optimize its harvesting, packing, sales and marketing efforts.

CAMPOSOL’s main products are avocados, blueberries, asparagus (white and green), mangoes, grapes, and tangerines. The Company also has a shrimp production center (Marinazul) in the north of Peru. All production is currently oriented to the export markets.

PRODUCTS CATEGORIES MAIN DESTINATIONS

Avocados Fresh and frozen

The US, the Netherlands, France, Japan and Spain.

Blueberries Fresh The US and the Netherlands.

Green and White Asparagus

Fresh, preserved and frozen

The Netherlands, US, France, Spain and Germany.

Tangerine FreshThe UK, The Netherlands and Canada

MangoesFresh, preserved and frozen

The US, the Netherlands, Germany, and Japan.

Grapes Fresh The Netherlands, US and China.

Peppers Preserved Spain, Germany and the US.

Shrimp Frozen US, France, Spain and Italy.

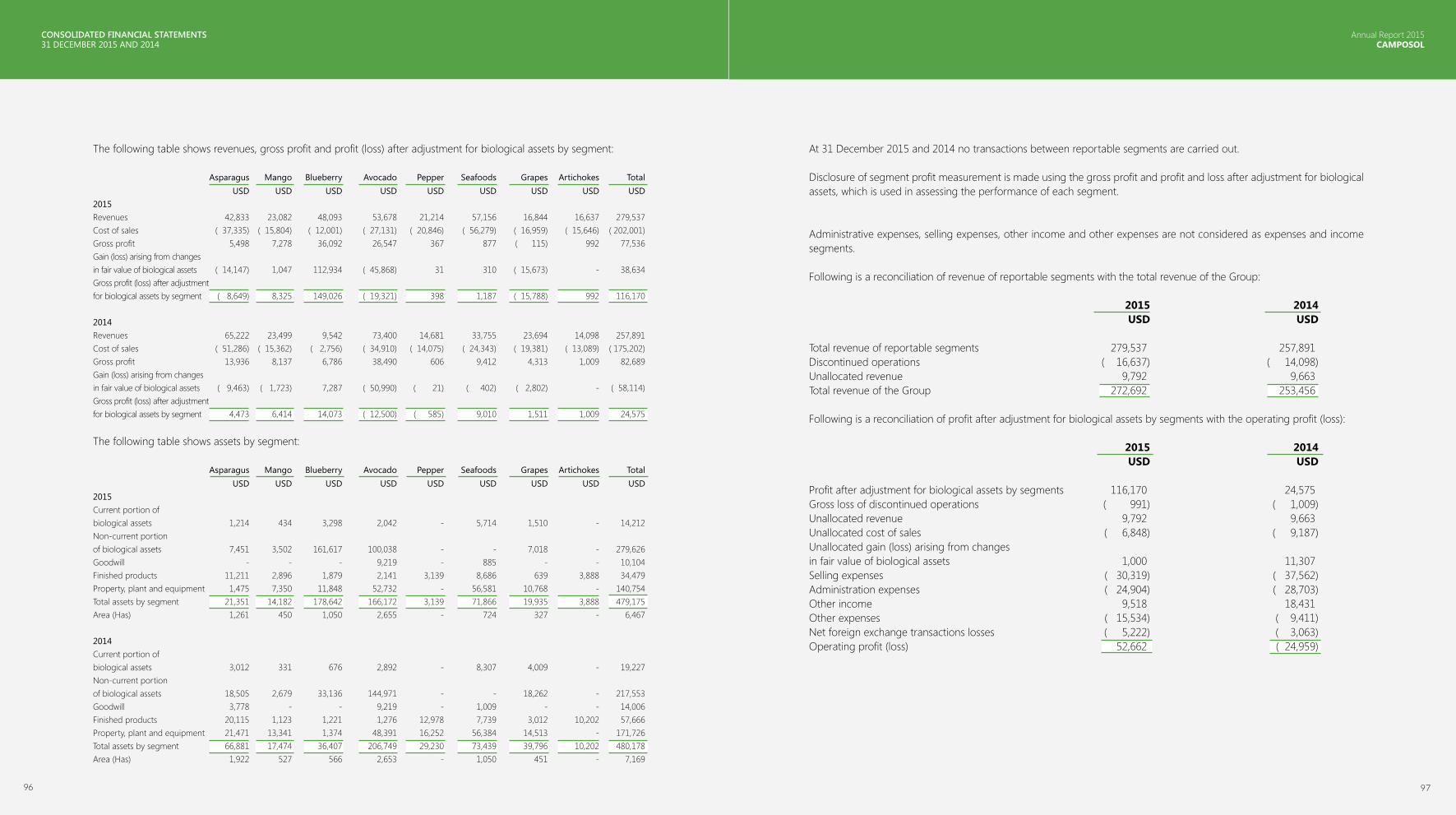

At December 31st, 2015, the Group has seven operating segments which are: avocado, blueberry, asparagus, mango, grapes, pepper and seafood. Artichoke, which produced this single presentation is not considered a reportable segment anymore, considering that from Management’s perspective artichoke will not be relevant in the decision-making; therefore Artichoke’s CGU is presented as discontinued operations. These products are further distinguished in fresh and frozen products.

The seven operating segments are engaged in producing, processing and commercializing some agricultural products, presented in fresh, preserved (until 2015) and frozen, which are mainly exported to European markets and the United States of America.

All production and related assets are in Peru.

CAMPOSOL CONSIDERS PARAMOUNT TO MAINTAIN A DIVERSIFIED PORTFOLIO OF PRODUCTS, TO ExPLOIT THE SELLING WINDOWS BETTER AND OPTIMIzE ITS HARVESTING, PACKING, SALES AND MARKETING EFFORTS.

AT DECEMBER 31ST 2015, THE GROUP HAS SEVEN OPERATING SEGMENTS WHICH ARE: AvOCADO, BLUEBERRY, ASPARAGUS, MANGO, GRAPES, PEPPER AND SEAFOOD.

2322

Annual Report 2015 CAMPOSOL

CAMPOSOL continues to be a leading company in the Peruvian non- traditional agro-industry exports and has three main product categories: Fresh, Preserved, and Frozen. 56% of total revenues in 2015 came from fresh products, 27% from preserved products and 15% from frozen products.

AvocadosAvocados are one of the most profitable crops on CAMPOSOL’s portfolio, with a gross margin in 2015 of 49.5% and thus, reductions of price affect the profitability of the Company much more than any other crop.In 2015, revenues from our avocados segment were USD53.7 million and represented 19.7% of our total revenues, which represented a decrease of USD19.7 million from USD73.4 million in 2014 (29.0% of our total revenues in 2014).

Fresh avocados are our main avocado product, which in 2015 represented 16.8% of our total sales (USD 46.1 million) and 85.5% of our total avocado sales.

The decrease in revenues from our avocados segment in 2015 was primarily a result of

• A 32.2% decrease in volumes sold, from 40,204 net MT in 2014 to 27,274 net MT in 2015. Volume decrease mainly due to both the presence of a weak El Niño phenomenon during 2014 and a moderated El Niño phenomenon during 2015, which took place during months in which the plant required cold temperatures to secure its natural flowering process, and a reduction of expected yields because of seasonality.

• Decrease in revenues was partially offset by an 8.8% increase in average prices for avocados in 2015, from USD1.81 per net kg in 2014 to USD1.97 per net kg in 2015. Price increase mainly due to (i) the implementation of our new commercial strategy, which increased the participation of retail channels, (ii) a 5.0% increase in average prices for fresh avocados and (iii) a 2.6% increase in average prices for frozen avocados.

CAMPOSOL sold 25,344 net MT of fresh avocados in 2015 (38,424 MT in 2014), at an average price of USD 1.81 per net KG during 2015 (USD 1.72 in 2014) representing a

decrease of 34.0% in volume sold and an increase of 5% in price levels compared to 2014.

CAMPOSOL sold 1,930 net MT of frozen avocados in 2015 (1,780 MT in 2014) at an average price of USD 3.93 per net KG during 2015 (USD 3.83 in 2014), representing an increase of 8.4% in volume sold and an increase of 2.6% in price levels compared to 2014.

During 2015, total gross margin for avocados was 49.5%, down 2.9 pp (percentage points) from the year before.

Principal destinies for our avocados:

Market 2015Revenues % 2014

Revenues %

Asia 3,909 7% 2,918 4%

United States 24,252 45% 48,351 66%

Europe 22,803 42% 19,521 27%

Others 2,714 5% 2,610 4%

53,678 73,400

2524

Annual Report 2015 CAMPOSOL

blueberriesBlueberries are the most profitable crop on CAMPOSOL’s portfolio, with a gross margin of 75.0% in 2015. The largest investments during the last two years were made in this crop.

In 2015, revenues from our blueberries segment were USD48.1 million and represented 17.6% of our total revenues, which represented an increase of USD38.6 million, or 404.0 %, from USD9.5 million in 2014 (3.8% of total revenues in 2014).

Fresh blueberries are our principal blueberry product, which in 2015 represented 17.5% of our total sales (USD 47.7 million) and 99.3% of our total blueberries sales.

The increase in revenues from our blueberries segment in 2015 was primarily a result of

• A 386.4% increase in volumes sold, from 912 net MT in 2014 to 4,436 net MT in 2015, due to increased production in 532 has; and

• A 3.6% increase in average prices for blueberries in 2015, from USD10.46 per net kg in 2014 to USD10.84 per net kg in 2015, due to the implementation of our new commercial strategy, which increased the participation of retail channels.

During 2015, total gross margin for blueberries was 75.0%, down 3.9 pp (percentage points) from the year before.

Principal destinies for our blueberries:

Market 2015Revenues % 2014

Revenues %

Asia 129 0% 752 8%

United States 28,447 59% 5,940 62%

Europe 18,702 39% 2,850 30%

Others 793 2% 0 0%

48,071 9,542

Market 2015Revenues % 2014

Revenues %

Asia 1,343 2% 1,327 2%

United States 7,866 21% 13,695 21%

Europe 32,032 75% 48,702 75%

Others 1,591 2% 1,498 2%

42,833 65,222

AsparagusPeru is the most important supplier of asparagus in the world. Peruvian asparagus production is highly efficient given the country’s geographic location and climatic advantage, with one of the highest yields among asparagus producers (11.4 MT per hectare in 2013).

Due to Peru´s climate characteristics, asparagus is harvested all year‐long, but fresh asparagus´s sales are stronger in the first and fourth quarter. CAMPOSOL and the other Peruvian producers have an advantage regarding other producing countries since they can offer product outside the traditional windows of the northern hemisphere consumption.

In 2015, revenues from our asparagus segment were USD42.8 million and represented 15.7% of our total revenues, which represented a decrease of USD22.4 million, or 34.4%, from USD65.2 million in 2014 (25.7% of total revenues in 2014).

White asparagus is our principal asparagus product, which in 2015 represented 12.1% of our total sales (USD 32.9 million) and 76.8% of our total asparagus sales.

The decrease in revenues from our asparagus segment in 2015 was primarily a result of

• A 35.8% decrease in volumes sold, from 16,600 net MT in 2014 to 10,653 net MT in 2015, due to both the presence of a weak El Niño phenomenon during 2014 and a moderated El Niño event during 2015, and a reduction of average yields because of older fields. The lower harvested volumes resulted in lower volumes of white asparagus sold and lower volumes of preserved asparagus sold.

CAMPOSOL sold 4,107 net MT of fresh asparagus in 2015 (6,588 MT in 2014), at an average price of USD 4.66 per net KG during 2015 (USD 4.36 in 2014), representing a decrease of 37.7% in volume sold and a decrease of 0.7% in price levels compared to 2014.

CAMPOSOL sold 6,158 net MT of preserved asparagus in 2015 (9,408 MT in 2014), at an average price of USD 3.62 per net KG during 2015 (USD 3.56 in 2014), representing a decrease of 34.55% in volume sold and an increase of 1.7%

in price levels compared to 2014. CAMPOSOL sold 388 net MT of frozen asparagus in 2015 (604 MT in 2014), at an average price of USD 4.80 per net KG during 2015 (USD 4.22 in 2014), representing a decrease of 35.8% in volume sold and an increase of 13.7% in price levels compared to 2014.

During 2015, total gross margin for asparagus was 12.8%, down 8.7 pp (percentage points) from the year before.

Principal destinies for our asparagus:

2726

Annual Report 2015 CAMPOSOL

MangosIn 2015, revenues from our mangos segment were USD 23.1 million and represented 8.5% of our total revenues, which represented a decrease of USD 0.4 million, or 1.8%, from USD 23.5 million in 2014 (9.3% of our total revenues in 2014)

Fresh and frozen mangos are our principal mango products, which in 2015 represented 64.4% and 31.3%, respectively, of our total mango sales.

CAMPOSOL sold 10,063 net MT of fresh mangos in 2015 (9,993 MTs in 2014) at an average price of USD 1.48 per net KG during 2015 (USD 1.31 in 2014), representing a decrease of 7.0% in volume sold and an increase of 11.5% in price levels compared to 2014.

CAMPOSOL sold 3,406 net MT of frozen mangos in 2015 (5,714 MTs in 2014) at an average price of USD 2.12 per net KG during 2015 (USD 1.75 in 2014), representing an increase of 42.4% in volume sold and a decrease of 21.1% in price levels compared to 2014.

Market 2015Revenues % 2014

Revenues %

Asia 1,967 9% 2,729 12%

United States 7,841 34% 10,205 43%

Europe 11,226 49% 9,215 39%

Others 2,048 9% 1,350 6%

23,082 23,499

Market 2015Revenues % 2014

Revenues %

Asia 5,148 31% 10,528 44%

United States 1,276 8% 3,419 14%

Europe 6,729 40% 7,721 33%

Others 3,691 22% 2,026 9%

16,844 23,694

During 2015, total gross margin for mango was 31.5%, down 3.1 pp (percentage points) from the year before.

Principal destinies for our mangos:

GrapesIn 2015 revenues from our grapes segment were USD 16.8 million, and represented 6.2% of our total revenues, which represented a decrease of USD 6.9 million, or 28.9 %, from USD 23.7 million in 2014 (9.3% of our total revenues in 2014). Grapes are only sold in the fresh category.

The decrease in revenues from our grapes segment in 2015 was primarily a result of

• A 12.9% decrease in volumes sold, from 11,798 net MT in 2014 to 9,806 net MT in 2015, due to both the presence of a weak El Niño phenomenon during 2014 and a moderate El Niño event during 2015, affecting harvested volumes; and

• A 14.4% decrease in average prices for grapes in 2015, from USD 2.01 per net kg in 2014 to USD 1.72 per net kg in 2015, due to an increase in sold fresh product presentations with lower prices.

During 2015, total gross margin for grapes was -1.0%, down 19.2 pp (percentage points) from the year before. Principal destinies for our grapes:

2928

Annual Report 2015 CAMPOSOL

ShrimpIn 2015, revenues from our seafood segment were USD 57.2 million, which represented 21.0% of our total revenues, which represented an increase of USD 23.4 million, or 69.2%, from USD 33.8 million in 2014 (13.3% of our total revenues in 2014).

Frozen shrimp are our principal seafood product, which represented 94.5% of our total seafood sales, in 2015.

The increase in revenues from our seafood segment in 2015 was primarily a result of

• A 244.4% increase in volumes sold, from 2,993 net MT in 2014 to 10,309 net MT in 2015, due to an increase in shrimp production and the incorporation of other seafood

products. The increase in production due to acquisitions compensated the reduction in yields observed in semi-intensive shrimp ponds as a result of the occurrence of a moderate El Niño phenomenon during 2015;

• A 50.9% decrease in average prices in 2015, from USD 11.28 per net kg in 2014 to USD 5.54 per net kg in 2015, mainly due to a decrease in shrimp prices of 26.0%, from USD 9.80 per net kg in 2014 to USD 7.25 per net kg in 2015. The decrease in prices corresponds to the recovery of global production after the effect of EMS on shrimp ponds around the world.

During 2015 total gross margin for shrimp was 1.5%, down 26.4pp (percentage points) from the year before.

Principal destinies for our shrimp:

Market 2015Revenues % 2014

Revenues %

Asia 3,043 5% 2,260 7%

United States 18,945 33% 24,920 74%

Europe 27,449 48% 353 1%

Others 7,719 14% 6,222 18%

57,156 33,755

ArtichokesOn 17 December 2015, the Group signed a contract of sale in which transfers the ownership of his line of preserved products to a third party (Sociedad Agrícola Virú S.A.C.), the same that will be effective in january 2016.

As a result of the disposal of the preserved products line, Artichoke’s CGU, which produced this single presentation, is not considered a reportable segment anymore, considering that from management’s perspective artichoke will not be relevant in the decision making. Therefore, Artichoke’s CGU is presented as discontinued operations. The results of the sale of this product are not shown with the other segments in revenues and is presented in a separate line in the Income Statement.

CAMPOSOL sold 6,448 net MT of artichoke during 2015 (5,548 MT in 2014), at an average price of USD 2.58 per net KG during 2015 (USD 2.54 in 2014) representing an increase of 16.2% in volume sold and an increase of 0.2% in price levels compared to 2014.

During 2015, total gross margin for artichoke was 6.0%, down 1.2 pp (percentage points) from the year before.

IN 2015, REVENUES FROM OUR SEAFOOD SEGMENT WERE USD 57.2 MILLION, WHICH REPRESENTED 21.0% OF OUR TOTAL REVENUES, WHICH REPRESENTED AN INCREASE OF USD 23.4 MILLION, OR 69.2%, FROM USD 33.8 MILLION IN 2014.

PeppersIn 2015, revenues from our peppers segment were USD21.2 million and represented 7.8% of our total revenues, which represented an increase of USD 6.5 million from USD 14.7 in 2014 (5.5% of our total revenues in 2014).

Frozen and preserved piquillo peppers were our principal pepper product, which in 2015 represented 13.2% and 83.4%, respectively, of our total peppers sales.

CAMPOSOL sold 9,053 net MT of preserved piquillo peppers in 2015 (6,485 MT in 2014) at an average price of USD 1.92

per net KG during 2015 (USD 1.87 in 2014), representing an increase of 39.6% in volume sold and a decrease of 2.7% in price levels compared to 2014.

CAMPOSOL sold 732 net MT of frozen piquillo peppers in 2015 (20 MTs in 2014) at an average price of USD 3.22 per net KG during 2015 (USD 2.63 in 2014), representing an increase of 22% in price levels compared to 2014.

During 2015, total gross margin for peppers was 1.7% down 2.4 pp (percentage points) from the year before.

3130

Annual Report 2015 CAMPOSOL04

board of Directors Report

4.1 MAin ACtiVitiES

CAMPOSOL is a global healthy food provider that integrally manages its supply chain: its fields, processing, and distribution. CAMPOSOL’s portfolio includes the following products: blueberries, avocados, mangos, grapes, tangerines, asparagus, shrimps and other marine products, all exported to the world.

The planted fields and packaging facilities are located in Peru, in La Libertad, Piura and Tumbes regions. The Company owns most of the fields where its products are sowed and harvested, having total control of the growing, harvesting and packing phases of its final products. It also has alliances and industrial relations with other growers to process and commercialize their products, assuring the same quality standards to clients.

To ensure high service levels to its clients and to monitor in a close manner trends in its main markets, CAMPOSOL has strengthened its commercial arms through direct offices in Europe (the Netherlands) and the US (Florida).

4.2 MARkEt SituAtiOn

AGROinDuStRy:

Peruvian agricultural exports amounted to USD 5,285 million in 2015, 26% more than in the previous year. Peru has become one of the world’s top-10 food supplier countries by exporting asparagus, coffee, mangoes, maca, quinoa, olives, grapes, avocados, artichoke, dried peppers, beans, tangerines, gingers, broad beans, onions, fresh peas, and berries.

Some products experienced important growth versus 2014, like fresh mangoes (+42%), frozen mangoes (+49%), non-frozen prepared vegetables (+37%), cocoa grain (+21%), fresh asparagus (+9%) and grapes (+9%) stood out.

Also some countries experienced significant growth, like Vietnam (+74%), Puerto Rico (+30%), Mexico (+17%), Chile (+17%), England (+13%), Netherlands (+10%), United

States (+8%), and other nations increased their demand for Peruvian products during 2015.The major exporting companies in 2015 were Camposol SA, Persales Huancaruna SAC, Sociedad Agricola Virú SA, Complejo Industrial Beta SA, DanPer Trujillo SAC and Gloria SA, among others.

CAMPOSOL’s products were exported to 53 countries. The main markets were the USA, which in 2015 accounted for 50% of total volume, followed by Germany with 12% and Spain with 8%.

AvocadosPeru is the second largest exporter of avocados in the World. La Libertad region is the first producer of avocado in Peru, with 36% of the total exports.

Avocados sales between january-November shows an 8% decrease versus the same period in 2014 when exports totaled USD306.2, total tonnage shipped last year were 169,694 tons.

Camposol continued to lead avocado exports with the 14% of the total volume, followed by Soc. Agricola Drokasa (11%) and Cerro Prieto (11%).

Camposol exported 25,300 MT of fresh avocados to 22 countries during 2015, representing a decrease of 34% versus 2014, due to the alternate bearing nature of the fruit. USA and Europe were the main destinations, with 46% sales and 42% respectively, sales to Asia accounted for 7% and 4% to Chile.

There are high expectations for the Asian Market, especially after signing the Phytosanitary Protocol that allows Peruvian avocados into China, and after Peru sent its first shipment to japan in August 2015. blueberriesOver the past four years, the growth of Peruvian blueberry exports has been impressive. It went from almost zero in 2011 to USD 0.5 million in 2012; then jumped to USD 15 million in 2013 and then to USD 29 million in 2014. Total sales in 2015 were over USD 94 million, which is three times more than in 2014.

CAMPOSOL IS A GLOBAL HEALTHY FOOD PROVIDER THAT INTEGRALLY MANAGES ITS SUPPLY CHAIN: ITS FIELDS, PROCESSING, AND DISTRIBUTION

CAMPOSOL IS A GLOBAL HEALTHY FOOD PROVIDER THAT INTEGRALLY MANAGES ITS SUPPLY CHAIN: ITS FIELDS, PROCESSING, AND DISTRIBUTION.

3332

Annual Report 2015 CAMPOSOL

The number of markets demanding the fruit has also increased. In 2015, Peru shipped to 20 countries, ten more than in 2014. The United States remains the biggest customer, accounting for more than half of the purchases (USD 53.2 million), followed by the Netherlands (USD 25.7 million), the United Kingdom (USD 11,5 million), and Hong Kong (USD 6.0 million).

Blueberry exports were one of La Libertad’s most notorious increases in agricultural product exports. Blueberry exports from La Libertad accounted for over 90% of national exports, then Ancash with 3%, Lima with 2%, and Ica with 1%. The 80% of the total volume of Peruvian blueberries was exported by Camposol and Talsa with the 42% and 38% respectively.

Camposol exported 4,400 MT of fresh blueberries to 20 countries. The USA is the leading market for Camposol’s blueberries exports (60%) followed by Germany (20%) and UK (15%).

AsparagusPerú: Fresh Asparagus exports in 2014 totaled USD 380 million at an average price downward USD 2.89 kilo, representing a decrease of 6 % and 12 % respectively over 2013.

One of Camposol’s main products, which represented 15.7% of the company’s total sales during 2015.

Camposol sold 10,600 MT of asparagus, 4,100 MT of fresh, 6,000 preserved and 400 of frozen, representing a decrease of 37.6%, 34.5%, and 35.7% respectively.

Mango In 2015, Peruvian mango exports not only increased in value and prices but also arrived in new destinations.

Peruvian mango exports grew by 34% in value in 2015, amounting to USD 187 million and an average price of USD 1.49 per kilo. The volume achieved amounted to 125,800 MT. These results are good when compared to the previous

PRODUCTS CATEGORIES MAIN MARKETS

Avocados Fresh and frozen

The USA, Germany, Spain, France, and The Netherlands

Blueberries Fresh The USA, Germany, UK and The Netherlands

Green and White Asparagus

Fresh, preserved and frozen

Germany, USA, France, Spain and The Netherlands

Tangerine FreshThe UK, The Netherlands and Canada

Mangoes FreshThe USA, Germany, The Netherlands, Canada and Japan

Grapes Fresh Russia, Poland and USA

Peppers Preserved Spain, Germany and USA

Artichokes Preserved USA

Shrimp Frozen USA

year, in which the export value amounted to approximately USD139 million, the average price was USD1.15 per kilo, and the export volume totaled 120,800 MT.

Mango exports reached a total of 28 destinations. However, the two main markets, i.e. the Netherlands and the United States, have accounted for nearly 70% of the total export volume value and 55% of its volume since 2011.

The number of companies exporting mangoes also increased, as it went from 152 in 2014 to 178 in 2015, however only three of them continued to lead exports. These companies are Dominus SAC, Sunshine Export SAC, and Camposol SA. However, their share in the overall total value and volume exported decreased.

GrapesFresh grapes were deemed as Peru’s top non-traditional agro-exports produce” having ousted asparagus for a third consecutive year.

In 2015, fresh grape exports amounted USD 699.1 million, 8.8% of the sales in 2014 and 309,926 MT, 17% more than the last year.

The two regions that produce the most grapes in Peru are Ica and Piura, while the main exporters are El Pedregal, Sociedad Agricola Rapel, Complejo Agroindustrial Beta, and Agricultural Ecosac, among others.

Camposol has 326 grape hectares, 90% of which are Redglobe varieties; the remaining grapes are of the Flame Seedless variety, and other varieties are being tested (the former are not being exported yet).

The larger production of the Company is of the Redglobe variety; the main markets destination are Western Europe, Russia, China and, generally, the entire Asian market.In 2015, Camposol exported 9,800 TM of grapes to 35 countries.

Camposol sold 9,800 TM of grapes during 2015; revenues were USD 16.8 million representing 6.2% of Camposol’s total revenue during 2015.

CAMPOSOLMain

Destinations

Other 17%

France 4%

Netherlands 4%

UK 4%

Spain 8%

Germany 12%

50% USA

3534

Annual Report 2015 CAMPOSOL

ShRiMP inDuStRy:

According to the Food & Agriculture Organization of the United Nations (FAO), world production of shrimp, both captured and farmed, is approximately 8 million MT, while modern world shrimp farming is about 4.5 million MT per year. Shrimp is now one of the most important internationally traded fishery commodity in terms of value, accounting for about 15% of the total value of internationally traded fish products in 2011. In many tropical developing countries like Honduras, Ecuador, and Brazil, it is the most valuable fishery export.

World demand for shrimp peaked in 2011, with the value of global shrimp imports growing 17%, as a result of the economic recovery and a slight decrease in international

4.4 SuMMARy OF thE yEAR

2015 was a challenging year for CAMPOSOL, as well as for the Peruvian agricultural exporting sector in general due to lower volumes as a result of the “El Niño” natural phenomenon.

However, we have been able to keep our leadership in the Peruvian agro-industrial sector and face these situations with fast answers and a clear view of the company strengths, which are focused on fresh and healthy products that, we believe, have the best perspectives in the future. In this sense, in 2015, CAMPOSOL’s total sales amounted to USD 272.9 million (vs. USD 253.5 million in 2014) and EBITDA amounted to USD 42.5 million (vs. USD 34.0 million in 2014). In 2015, profit amounted to USD 12.5 million compared to a loss of USD 34.4 million during the same period last year.

The main reasons for the increased revenues for 2015 were higher volumes of blueberries, shrimp, and other seafood products. Also, the increase in prices of avocados to 1.97 per net KG (1.81 in 2014), mangos to 1.68 per net KG (1.48 in 2014), and blueberries to 10.84 per net KG (10.46 in 2014). This represents up 8.8%, 13.5% and 4%, respectively.

In the future, the Company expects to continue its diversification strategy by increasing the blueberries production in the Fruits & Vegetables (F&V) segment and by increasing the conversion of shrimp ponds in the Seafood segment. The Company also expects to continue to reinforce the Trading segment through more direct sales to retailers, adding value to its clients through commercial, marketing and service initiatives which should result in higher margins.

In line with this strategy, the Company has invested significantly in specializing the company in the F&v segment, diversifying its portfolio of products and customers, as well as increasing its presence in key markets with favorable and encouraging results. In line with this vision, the Company has decided to continue empowering its fresh and frozen business segments, and exit the preserved business. The Company considers these strategic changes in CAMPOSOL’S businesses will allow for greater specialization, efficiency and focus on product categories in which the Company has made significant investments in recent years, and thus maximize opportunities for growth and consolidation of its business.

production that caused a sharp increase in prices. World farmed shrimp production volumes decreased in 2012 and particularly in 2013, mainly because of disease-related problems, such as early mortality syndrome (EMS), in some countries in Asia and Latin America.

The (EMS) is a serious emerging disease of cultured shrimp. The impacts of EMS -include production losses, loss of income and profit for small-scale producers and commercial enterprises, higher shrimp prices owing to supply shortages, and impacts on trade. However, the recovery began in late 2014 and 2015, where production returned to steady levels, and prices descend to the standard of the period 2011 to 2012.

Provide the world healthy high quality food, seaking the welfare of the people and the environment throug innovation, research

and putting special care in all the details of the process.

ViSiOn

MiSSiOn

DRiVERS

VALuES

IN THE FUTURE, THE COMPANY ExPECTS TO CONTINUE ITS DIVERSIFICATION STRATEGY BY INCREASING THE BLUEBERRIES PRODUCTION IN THE FRUITS & VEGETABLES (F&V) SEGMENT AND BY INCREASING THE CONVERSION OF SHRIMP PONDS IN THE SEAFOOD SEGMENT.

Be a world leader in providinghealthy food

to the families of the world.

Profi

tabi

lity

Effic

ienc

y

Qua

lity

Envi

ronm

enta

l &So

cial

Res

pons

ibili

ty

Honesty Respect Austerity Excelence Team Work

Inno

vatio

n

4.3 COMPAny StRAtEGy

In line with the Company’s vision of becoming a global company that provides families all over the world with healthy food, CAMPOSOL´s strategy is supported by the following rationale:

3736

Annual Report 2015 CAMPOSOL

Segment/Crop Has

FRUITS &VEGETABLES

Asparagus 1,262

Avocados 2,655

Mangos 450

Grapes 326

Tangerines 145

Blueberries 1,050

TOTAL 5,887

SEAFOOD

Shrimp 724

4.5 OPERAtiOnS

As of December 2015, operations were located mainly in the regions of La Libertad, Piura and Tumbes with 26,489 own Has: 24,35o Has for fruits & vegetables, and 2,139 Has for seafood. The Company had a total of 5,888 productive Has in La Libertad and Piura regions as of December 31, 2015, where asparagus, avocados, mangos, grapes, tangerines and blueberries are harvested. It also had 724 productive Has in Tumbes where it produces shrimps.

During 2015, the Company invested USD 28.6 million (USD 63.3 million in 2014), of which USD 10.9 million were invested in additional planting and blueberries fields maintenance, USD 1.5 million in planting of grapes, USD 0.5 million in planting of tangerines, USD 7.7 million were invested in equipment and infrastructure (USD 5.4 million in the plant and USD 2.3 million in farms),USD 8.0 million were invested in its shrimp and other seafood products business (USD 5.2 million in intensive planting and other minor investments and USD 2.8 million in purchase of land).

Location Own Rented

FRUITS &VEGETABLES

Trujillo Planta Chao

Piura NorAgro SAVSA

Piura Empafrut

Piura Don Packing

Huaral Torre Blanca

Chincha Emapac

SEAFOOD

Tumbes San Isidro

Tumbes La Cruz

Tumbes Cofresac

Paita ABC

Chimbote Centinela

PROCESSING PLANTSPRODUCTIVE HAS AS OF DECEMBER 31ST 2015 4.6 WORkinG EnViROnMEnt

CAMPOSOL is the third largest private employer of Peru reaching over 15,000 workers during peak production seasons. As an active member of the Global Compact of the United Nations, it acts by the highest ethical principles, aiming to be an example of compliance with labor and social standards, both local and internationally, with a clear orientation to promote the wellbeing of all of our employees.

Thus, CAMPOSOL provides equal opportunities and working conditions for all employees, regardless of race, color, gender, religion, sexual or political orientation in all of its operations.During the last three years, CAMPOSOL has had a remarkable growth in its level of employees, from 10,000 to over 15,000 workers during peak seasons. We expect to continue growing the number of employees, based on the Company’s growth strategy in new products, like blueberries and tangerines, and the consolidation of our frozen business, among others.

During 2015, we have strengthened our employer brand in our areas of influence to attract workers we require for our operations, based on fair treatment, safe working environment, competitive salaries and training opportunities. Also, CAMPOSOL has continued with its efforts to develop strategic skills for our workers to train and guide them through their personal growth, with the support of a continuous process of acquisition, strengthening and transformation of individual expertise and commitment to corporate motivation.

In this sense, more than 3,750 training programs were held during 2015, covering several matters as quality, safety, hygiene, environmental care, sexual harassment prevention, as well technical courses for sanitization, irrigation, fertilization, pest control, maintenance, production improvement, and executive programs developing leadership and management skills.

3938

Annual Report 2015 CAMPOSOL

Safety and health at workCAMPOSOL provides a safe, hygienic and healthy workplace and takes the necessary measures to prevent accidents and injuries that may arise, be related to or take place during work or as a result of the Company´s operations. CAMPOSOL has systems to detect, avoid or respond to possible risks to the safety and health of its employees. Employees could refuse to conduct any unsafe work or any work that risks their life.

Freedom of association and collective bargainingCAMPOSOL respects the decisions of its employees and the right of association and collective bargaining. The Company does not interfere in any way in the establishment, operation or administration of such organizations of employees, neither in the collective bargaining activities.

Prohibition of child laborCAMPOSOL forbids child labor. Employees must be at least 18 years old when hired. Child labor refers to any mental, physical, social or morally dangerous or harmful activity for children or any activity that directly interferes in their compulsory education needs defined as such by the equal authority as well as the highest international standards.

Prohibition of deprivation of freedom and forced laborCAMPOSOL forbids any enslaving servitude or any form of forced labor. CAMPOSOL shall neither require any deposits nor withhold original ID documents as a work condition. Likewise, the Company shall not subcontract suppliers or production facilities that force work to be conducted by employees under any exploitation or forced labor.

In particular, the CAMPOSOL’S 2015 Training Program completed more than 210,000 training hours, 95% delivered to field or plant workers and 5% of professionals and executives, resulting in 127 workers with job skills certifications. Also, 182 employees attended the Management and Leadership Development Program, and more than 500 employees benefited from discount agreements to study various management, technical and updated programs in Universities and Technical Schools.

Similarly, CAMPOSOL has implemented programs that will foster the potential of its employees in order to assure their adequacy with the required job profile, while developing the skills needed for certification programs regarding various tasks performed by the Company, such as HACCP, Tesco Nurture, Kosher, BASC, IPM, Global Compact, BRC, IFS, USGMP, NSF Cook and Thurber, Global Gap, USGAP, BSCI and Code of Conduct Audits.It is worth mentioning that during 2015, there were none labor disruptions nor strikes or workdays lost. The Company was able to handle good relationships with its Labor Unions, using improved communication with union leaders and workers. CAMPOSOL’S collective bargaining conducted in 2015 achieved labor agreements with its three labor unions for a three years labor peace.

On the other hand, during 2015, CAMPOSOL reviewed with Hay Group its salary structure aimed to internal equity and competitiveness among agribusiness companies. Also, CAMPOSOL joined the “Agribusiness Club” promoted by Hay Group for wages and benefits researches and analysis for the agro-exporting industry.

Additionally, CAMPOSOL offers services and benefits to its employees such as personal loans for health or housing, financial benefits for the schooling of their children, as well as counseling and economic benefits to support a death in their families, amongst others. In the same manner, the Company pays close attention to its employees’ family health, or work problems, which are attended by skilled personnel. Also, the Social Welfare area coordinates various integration, wellness, sports and recognition activities during the year, as well as celebrations such as Labor Day, Mother’s and Father’s Day, Christmas, etc. CAMPOSOL strongly encourages sports activities, by always providing the time and infrastructure to perform them.

As an example, CAMPOSOL’s internal “Olympic Games,” which includes a diverse range of sports, have a significant participation and are very enthusiastic and competitive.

4.7 CODE OF EthiCS & COnDuCt

During 2015 CAMPOSOL formally issued its Code of Ethics and Conduct to strengthen ethical behavior at all levels of the Company and improve the control environment, thus making it a more stable and prosperous organization. In this sense, the Code of Ethics and Conduct CAMPOSOL describes the way we work and behave with each of the stakeholders with whom we interact. Its content is a reflection of our values and summarizes the fundamental beliefs of CAMPOSOL. During 2015, the company has been conducting a comprehensive training program by which a deployment is assured to all staff.

Additionally, the Company has various mechanisms for detecting potential irregular situations related to deviations to the Code of Ethics and internal regulations of CAMPOSOL, including reviews of Internal Audit and External Audit, management oversight and our Confidential Reporting System, or “Ethics Line.”

This system was developed in 2014 and is administered by a third party -in this case, the firm Ernst & Young- to ensure the anonymity of all allegations. Through this channel, all complaints are reviewed and have an attention mechanism that ensures strict confidentiality on the identity of the person who reports a complaint, providing a workplace free of retaliation of any kind, seeking to ensure that investigations are objective and receive the same treatment of confidentiality.

According to our social responsibility policy, which is aligned with international standards such as ISO2600, SA 8000 and BSCI, among other, CAMPOSOL acts according to the following ethical criteria:

4140

Annual Report 2015 CAMPOSOL

non-Discrimination CAMPOSOL forbids discrimination practices in contracting personnel and in their professional behavior due to race, color, religion, sex, age, physical capacities, nationality or any other legally prohibited condition.

Disciplinary measuresCAMPOSOL must treat all its employees with dignity and respect. The use of corporal punishments, psychological punishments, confinement, violent threatening, or any other form of harassment or abuse as a method of discipline and control is neither practiced nor tolerated.

Work scheduleCAMPOSOL is responsible for guaranteeing its employees to work according to the applicable laws and labor standards regarding the number of working hours and days. If there is any conflict between a statute and a mandatory industrial standard, CAMPOSOL must solve this situation according to what is established regarding which standard provides a larger benefit for the employee. Personnel must have at least one day off after a consecutive period of six working days.

SalaryCAMPOSOL must provide its employees with salaries and benefits that comply with the applicable laws and corresponding collective agreements, including those referring to the payment of overtime and other extra pay agreements.

SustainabilityCAMPOSOL develops an integral Social Responsibility Policy having as a priority: its employees and the communities, the proper use of its resources in all its operations and especially emphasizing the use of water and energy.

EnvironmentCAMPOSOL conducts its operations under the applicable norms and its environmental commitments that include monitoring of emissions, management of sewage waters, environmental noise, and solid waste, among other; this allows us to mitigate its significant environmental impacts and helps to improve its environmental performance continually.

4.8 SOCiAL RESPOnSibiLity

CAMPOSOL believes that to guarantee the sustainability of its business; it is essential to ensure that it operates in full compliance with ethical principles, respecting people and the environment. This guarantee is achieved by acting by the social responsibility policy of our organization and in line with the principles and objectives of the UN World Global Compact, of which we are an active member since 2008.

As a result, the Company contemplates in all its decisions the triple result: economic, social and environmental and is transparent when sharing its results in these aspects. In this sense, CAMPOSOL was the first agro-industrial company to publish annual sustainability reports aligned with the GRI indicators, which are available on our web page: www.camposol.com.pe. The aim of this report is to reflect in a transparent and systematic way the main indicators that show the environmental and social performance of the Company, as well as the programs and activities carried out regarding social responsibility each year.

Also, the Company tries hard to communicate and put into practice social responsibility principles and values in all the processes, operations and areas of the Company transversally and makes efforts to attend to the contributions and comments of its stakeholders, which leads the Company to regularly carry out investigative studies on the attitudes and perceptions of these groups, in order to understand

CAMPOSOL DEVELOPS AN INTEGRAL SOCIAL RESPONSIBILITY POLICY HAVING AS PRIORITY: ITS EMPLOYEES AND THE COMMUNITIES, THE PROPER USE OF ITS RESOURCES IN ALL ITS OPERATIONS AND ESPECIALLY EMPHASIzING IN THE USE OF WATER AND ENERGY.

their opinions and points of view with regard to our performance, and to permit us to take the adequate measures to correct if necessary.

We invite you to share our sustainability reports with us at:

http://www.CAMPOSOL.com.pe/espanol/en_investors_sustainability_reports

4342

Annual Report 2015 CAMPOSOL

4.9 RESEARCh, DEVELOPMEnt AnD innOVAtiOn

CAMPOSOL believes that innovation is a key aspect to boost competitiveness and growth in the mid and long term. We do so through policies, projects, investigations, market research, and analysis of potential new products and development of new technology. The focus is on products that could benefit from the Peruvian climatic advantages and also help diversify its portfolio of products and clients.

The Research, Development, and Innovation area also seeks to find innovative solutions to extend the shelf life of fresh produce and reduce production costs and research for new alternatives for pest control and new food presentations. CAMPOSOL is proud to say that, during 2015, the company started a large scale production of blueberries which began as an R&D project back in 2008.

It is also worth noting that CAMPOSOL has been successfully executing funded projects by Innovate Peru, as well as FINCyT, Government institutions aimed to promote innovation, which results are used for other potential beneficiaries. CAMPOSOL is also performing a sustainable management system through insect biological control agents – pests-, and it counts, since 2006, with a laboratory of “Beneficial Insects and Entomopathogenic Growing.”

CAMPOSOL’ s investigation lines are mainly focused on: • Production improvement.• Pest control and diseases.• New agricultural growing, products or packing developments.• Molecular biotechnology.• Research and Development Laboratory.

4.10 SuPPLy ChAin

CAMPOSOL shall guarantee its suppliers to be informed of CAMPOSOL’S Code of Ethics & Conduct, its terms and conditions, its meaning and what its implementation implies.

4.11 FinAnCiAL RESuLtS

In 2015, CAMPOSOL’s total sales amounted to USD 272.9 million (USD 253.5 million in 2014). The main reasons for the increased revenues for the full year 2015 were higher volumes of blueberries, shrimp and other seafood products, and the increase prices of avocados to 1.97 per net KG (1.81 in 2014), mangos to 1.68 per net KG (1.48 in 2014) and blueberries to 10.84 per net KG (10.46 in 2014). This represent up 8.8%, 13.5% and 4%.

Total Cost of Goods Sold was USD 193.2 million (USD 171.3 million in 2014), representing around 62.8% of total sales (67.6% in 2014).

Gross profit decreased to USD 79.5 million (USD 82.2 million in 2014), which resulted in a gross margin of 29.1% compared to 32.4% in 2014. The main reasons for the decreased gross profit and margin were the higher cost of productions relation to grapes and shrimp.Administrative expenses decreased from USD 28.7 million in 2014 to USD 24.9 million in 2015. The variation of USD 3.8 million is explained mainly by lower professional fees, travel and representation expenses.

Selling expenses decreased from USD 37.6 million in 2014 to USD 30.3 million in 2015 due to changes in commercial conditions of sale (change of FOB to CFR / CIF terms) applied to higher volumes sold. This decrease was primarily as a result of a USD 3.5 million decrease in 2015 selling expenses from freight and customs duties, a USD1.3 million decrease in 2015 selling expenses from representation expenses, USD 2.1 million no provision for amortization of intangible management portfolio, which occurred in 2014.

In 2015, financial costs amounted to USD 25.0 million (USD 22.8 million in 2014). Such increase is mainly explained by the interest incurred from the additional USD 75 million,

9,875% senior unsecured noted issued during the second quarter of 2014.

In 2015, profit amounted to USD 12.5 million compared to a loss of USD 34.4 million during the same period last year.

EBITDA amounts to USD 42.5 million (USD 34.0 million in 2014).

During 2015, non-current assets increased to USD 497.6 million compared to USD 452.9 million at the end of 2014. Such increase as a consequence of calculating fair value biological assets IAS 41.

Total inventories decreased from USD 95.2 million at December 31st, 2014, to USD 47.1 million by the end of the fourth quarter of 2015. The variation of USD 48.1 million is explained mainly by the decrease of finished product such as artichokes, asparagus, and peppers.

Trade accounts receivable decreased from USD 46.0 million at the end of 2014 to USD 40.7 million at the end of 2015, explained by higher collections to clients.As of December 31st, 2015, trade accounts payables decreased to USD 34.4 million at the end of 2015 from USD 48.3 million at the end of 2014. Such decrease is due primarily contracted payments to the supplier.

As a result, the total working capital (accounts receivable + inventories - accounts payable) decreased to USD 53.4 million at the end of 2015 from USD 92.9 million at the end of 2014. Current working capital as of December 31st, 2015 is 19.8% of sales (34.7%). Such significant reduction is the result of the company´s effort to improve working capital needs

Total liabilities decreased to USD 347.0 million in 2015 compared to USD 377.7 million at the end of 2015.

The Company’s debt, gross of capitalized fees, decreased from USD 277.4 million at the end of 2014 to USD 250.9 million at the end of 2015, mainly due to the paid off interest of senior unsecured notes and bank loans. The Company’s debt includes USD 200.0 million of senior unsecured notes at 9.875%, bond interest for paid USD 6.7 million (USD

THE RESEARCH, DEVELOPMENT AND INNOVATION AREA ALSO SEEKS TO FIND INNOVATIVE SOLUTIONS TO ExTEND THE SHELF LIFE OF FRESH PRODUCE AND REDUCE PRODUCTION COSTS AND RESEARCHES FOR NEW ALTERNATIVES FOR PEST CONTROL AND NEW FOOD PRESENTATIONS.

4544

Annual Report 2015 CAMPOSOL

5.6 million in 2014), USD 36.1 million of working capital financing (59.6), USD 7.3 million in leasing and other (10.5) and USD 0.8 million to sellers of acquired companies (1.7).

During 2015, the Company generated USD 33.6 million (used -30.8 million in 2014) in operations and invested USD -9.8 million (-62.3 million in 2014) in financing activities, the Company paid USD -27.6 million (USD 96.4 million in 2014), resulting in a net decrease in cash of USD -3.9 million (increase of 3.3 million in 2014). The Company ended the year with USD 26.7 million in cash (USD 30.5 million in 2014).

4.12 ALLOCAtiOn OF nEt inCOME

The Board of Directors has proposed that the net loss of CAMPOSOL is attributable to retained result. The proposal reflects display the current accumulated profit or loss.

4.13 intERnAL AuDit AnD intERnAL COntROL

The Company’s Internal Audit Management (“IA”) reports to the Board of Directors’ Audit Committee. Its mission is to evaluate the Company’s internal control system, by assisting to identify and minimize risks to achieve the Company’s main objectives and comply with its policies.