Annual Report 2011-12 - PMC Bank · Annual Report 2011-12 1 Compensation, INCOME 2011-12...

60

Transcript of Annual Report 2011-12 - PMC Bank · Annual Report 2011-12 1 Compensation, INCOME 2011-12...

Annual Report 2011-12

PERFORMANCE HIGHLIGHTS` in Crore

Particulars For The Year Ended31.03.2011 31.03.2012 % CHANGE

Total Income 325.46 427.28 31.28%Total Expenditure 278.49 355.53 27.66%Gross Profi t 46.97 71.75 52.76%Less : Provisions 7.24 11.58 59.94%Net Profi t Before Tax 39.73 60.17 51.45%Less : Income Tax 10.57 21.44 102.84%Net Profi t 29.16 38.73 32.82%

At The Year EndOwn Funds 246.92 343.29 39.03%Share Capital 79.83 85.46 7.05%Reserves and Surplus 167.09 257.83 54.31%Deposits 2827.38 3418.05 20.89%Current 255.32 319.00 24.94%Savings 513.87 566.56 10.25%Term 2058.19 2532.49 23.04%Advances 2079.88 2523.30 21.32%Secured 2054.12 2501.17 21.76%Unsecured 25.76 22.13 -14.09%Priority Sector 865.45 1058.66 22.32%% to Advances 41.61 41.96Working Capital 3401.21 4151.21 22.05%Investments 879.52 988.75 12.42%Borrowings and Refi nance 89.47 133.33 49.02%Net NPAs (%) 0.47 0.16Capital Adequacy (%) 13.23 13.28Number of Members 48485 47697Number of Branches & Extension Counters 54 63Profi t per Employee ( ` In lac) 3.90 4.47Return on Average Assets (%) 0.86 0.93Average Net Interest Margin (%) 4.40 5.28

Founder ChairmanLate. S. Gurcharan Singh Kochhar

Annual Report 2011-12

1

INCOME 2011-12

EXPENDITURE 2011-12

Bank Charges

0.99%

Interest Received on

Investments

16.06%

Interest Received on

Advances

77.40%

Printing, Stationery & Adverisement 1.50%

Depreciation 2.69%

Provision 7.73%

Other Expenses 9.28%

Rent & Taxes, Compensation, Insurance, Electricity 2.92%

Inerest Paid on Deposits & Borrowings 59.04%

Salary & Allowance, Bonus & Ex-gratia 7.78%

Net Profit 9.06%

Misc. Receipts

5.55%

2

Members of Board S. Charanjit Singh Chadha S. Waryam Singh Chairman Vice-Chairman

DirectorsS. Resham Singh S. Balbir Singh Kochhar S. Surjit Singh NarangS. Daljit Singh Bal S. Joginder Singh Palla S. Surjit Singh AroraS. Rajneet Singh Shri. Jagdish Mookhey S. Gurnam Singh HothiSmt. Trupti Bane Smt. Parmeet Sodhi S. Jasvinder Singh BanwaitShri. Brij Bhushan Handa Smt. Mukti Bavisi

EXECUTIVEs

Managing DirectorShri. Joy Thomas

General ManagersShri. H. K. Karanth Shri. L.M. Kamble

Dy. General Managers Smt. Manjit Kaur I.S. Smt. Meghana Gokhale Shri. Surinderpal Singh R.S. Shri. Atul Thakker

Asst. General ManagersShri. Charanjit Singh Bhatia Smt. Sunita Gouthaman Smt Manisha NerurkarShri. Amarjit Singh Matta Shri. Sanjeev Shere Smt Aarti DesaiSmt. Karmen Rebello Smt. Shiny Mithbaokar Smt. Jasvinder Kaur AnandShri. Parag Dalvi Smt. Rebecca Solomon Smt. Geeta K. SinghShri. Satish Bendre

statutory Auditors solicitorsM/s. D.B. Ketkar & Co. M/s. Purnanand & Co.

Arbitrators BankersShri. S.V. Tinaikar Reserve Bank of IndiaShri. J.S. Patil Saraswat Co-operative Bank Ltd. Bank of India HDFC Bank

BOARD OF DIRECTORs

Annual Report 2011-12

3

NOTICE TO MEMBERsNotice is hereby given that the Twenty-Ninth Annual General Body Meeting of the Members of Punjab & Maharashtra Co-op Bank Ltd. Mumbai will be held on saturday, the 28th of July, 2012 at 11.00 a.m. at Dreams Banquet, 2nd Floor, Dreams Mall, L.B.S.Marg, Bhandup (West), Mumbai – 400 078 to transact the following business:

1. Reading and Confirming the Minutes of the Last Annual General Body Meeting held on 27th August 2011.

2. Adoption of Annual Report with Audited Balance Sheet, the Profit & Loss Account as at March 31, 2012 and Statutory Audit Report for the financial year 2011-12.

3. Declaration of Dividend and Allocation of Profits for the Financial Year 2011-2012.4. Appointment of Statutory Auditors for the Financial Year 2012-13 and fix their

remuneration.5. To consider and approve the amendment to the bye-laws of the bank as notified by

the Board in the Annual Report for the year 2011-12 circulated to all the members.6. Disposal of any other business that may be brought before the meeting and replying

to Members’ questions, relating to the working of the Bank during the Financial Year 2011-12, permissible under the Bank’s Bye-Laws and Rules and about which at least 8. days notice, in writing, has been furnished to the Chief Executive Officer, at the Bank’s Central Office.

Place : Mumbai. JOY THOMAsDated: 4th July 2012 Managing Director

Note: If there is no quorum within half an hour after the appointed time, the meeting shall stand adjourned upto 11.30 a.m. on the same day and the agenda of the meeting shall be transacted at the same venue irrespective of the quorum in terms of bye-law no. 24(i).

Note

1. Members desiring to offer any suggestion at the Annual General Meeting or put any question pertaining to the Annual Report & Accounts are requested to write to the Bank on or before 20th July 2012, addressed to the Managing Director at the Central office.

2. Members who carry with them the identity card issued by the Bank only will be allowed to attend the General Body Meeting of the Bank.

3. Members who have not collected their dividends for the previous three years are requested to collect the same immediately.

4. Members are requested to intimate any change in name of nominee, office and residential address, status etc., so as to keep our records up-to-date.

5. Members are requested to introduce the Bank to their friends and relatives so that they can also avail of the various services rendered by the Bank.

6. Members are requested to give instructions for crediting the dividend directly to their Saving Bank / Current Account with any of the Branches of the Bank.

4

meomÙeeW kesâ efueS metÛevee:SceÉeje metefÛele efkeâÙee peelee nw efkeâ hebpeeye SC[ ceneje°^ menkeâejer yeQkeâ efueefcešs[, cegbyeF& kesâ meomÙeeW keâer GveeflemeJeer Jeeef<e&keâ Deece yew"keâ, ef[^cme yeBkeäJesš, 2 je ceeuee, ef[^cme cee@ue, Sve.yeer.Sme. ceeie&, Yeeb[ghe (he.), cegbyeF& - 400 078, MeefveJeej 28 pegueeF&, 2012 keâes megyen 11.00 yepes nesieer, efpemeceW efvecveefueefKele Sbpe[s hej keâejJeeF& nesieer ~

1. 27 Deiemle 2012 keâes megyen 11.00 keâes ngF& efheÚueer Deece yew"keâ kesâ keâeÙe&Je=òe keâes he{vee Deewj Gmekeâer heg°er ~

2. 31 ceeÛe&, 2012 keâes meceehle ngS efJeòeerÙe Je<e& 2011-2012 kesâ efueS DeefYeuesefKele efJeòeerÙe heefjCeeceeW DeLee&le leguevee he$e, ueeYe-neveer uesKeeheefjef#ele efjheesš& keâe DeefOe«enCe ~

3. efJeòeerÙe Je<e& 2011-2012 kesâ efueS ueeYeebMe keâer Iees<eCee SJebce ueeYe keâe efJelejCe ~

4. efJeòeerÙe Je<e& 2012-2013 kesâ efueS uesKeeheefj#ekeâ keâer efveÙegòeâer SJebce Gvekesâ heefjßeefcekeâ efveOee&jCe keâjvee ~

5. meefceleer Éeje ØemleeefJele ye@keâ kesâ GheefveÙeceeW kesâ mebMeesOeve hej efJeÛeej efJeceMe& keâjvee SJeb Gmes ceevÙelee osvee ~

6. yeBkeâ kesâ GheefveÙeceeW Je efveÙeceeW kesâ lenle efJeòeerÙe Je<e& 2011-2012 kesâ oewjeve yeBkeâ kesâ keâecekeâepe keâes ueskeâj Ssmes cegöeW keâe efveyešeje pees Fme yew"keâ ceW G"eÙes veÙes nes leLee meomÙeeW kesâ ØeMveeW kesâ peyeeye keâe me$e ~ efpemekesâ nsleg yeBkeâ kesâ ceOÙeJeleea keâeÙee&ueÙe ceW ØecegKe keâeÙe&keâejer DeefOekeâejer keâes 8 efove keâer efueefKele metÛevee os oer ieF& nw ~

mLeeve: cegbyeF& DeeosMeevegmeej

leeefjKe: 4 pegueeF& 2012 pee@Ùe Lee@ceme

efšhheCeer: Ùeefo efveOee&jerle meceÙe mes DeeOes Iebšs kesâ Deboj keâesjce vener neslee nw lees yew"keâ Gme efove megyen 11.30 yepes lekeâ mLeefiele ceeveer peeSieer Deewj Gmekeâ yeeo keâesjce keâe efuenepe efkeâS efyevee Gmeer mLeeve hej yew"keâ keâer keâeÙe&metÛeer hej keâejJeeF& keâer peeSieer ~

metÛevee:

1. Ùeefo keâesF& DebMeOeejkeâ uesKees mebyebOeer metÛevee Øeehle keâjves keâe FÛÚgkeâ nw lees Gvemes DevegjesOe nw keâer Jes Fme yeeyele 20 pegueeF& 2012 keâes Ùee Gmemes henues efveosMekeâ keâes efueKes, leeefkeâ DeeJeMÙekeâ metÛevee Deemeeveer mes GheueyOe keâjeF& pee mekesâ, Ùen ve kesâJeue mebyebefOele DebMeOeejkeâeW kesâ efueS Deefheleg Gvekesâ efueS Yeer megefJeOeepevekeâ nesiee pees yew"keâ ceW GheefmLele neWies ~

2. yew"keâ keâes yew"keâ ceW Yeeie uesveskeâer Devegceefle kesâJeue Gvner meomÙeeW keâes oer peeÙesieer pees Deheves meeLe yeQkeâ Éeje peejer efkeâS ieS henÛeeve-he$e ueskeâj DeeSbies ~

3. efpeve meomÙeeW ves efheÚues leerve meeue ceW Dehevee ueeYeebMe yeBkeâ mes vener efueÙee nw ke=âheÙee legjble Øeehle keâjW ~

4. meomÙeeW mes efJevebleer nw keâer, efpevekesâ Iej, keâeÙee&ueÙe kesâ mLeeve leLee veeceebkeâve ceW keâesF& heefjJele&ve nw lees Jes ke=âheÙee efueefKele ¤he ceW yeBkeâ keâes megefÛele keâjW ~

5. meomÙeeW mes efJevebleer nw keâer, Deheves efce$e hejerJeej meomÙe Je DevÙe heefjpevees keâes yew"keâ keâer megefJeOeeDeeW mes heefjefÛele keâjeS efpememes Jes Yeer yeBkeâ keâer megefJeOeeDeeW keâe ueeYe G"e mekeWâ ~

6. meomÙeeW mes efJevebleer nw keâer, Deheves ueeYeebMe keâer jkeäkeâce meerOes Deheves yeÛele Ùee Ûeeueg Keeles ceW pecee keâjeves keâer megÛevee yeBkeâ keâer efkeâmeer Yeer MeeKee ceW oW ~

Annual Report 2011-12

5

Dear Members,

Your Directors are pleased to present the 29th Annual Report of your Bank together with

the audited accounts for the year ended March 31, 2012.

Economic scenarioIt is unfortunately an undisputed fact that the Indian Economy has to report the weakest fiscal performance since 2002-2003. The tail telling indices of decline in the GDP growth to 6.5% against 8.4% the concern causing rise in the fiscal deficit from 5.1% last year to 5.9% in the current year are sufficient to underline the gravity of the situation. Current Account deficit, which is a measure of difference between the value of exports and imports has also widened dangerously from 2.7% of GDP from 4.2%. The only small consolation is in the area of inflation which has marginally decreased from 9.68% to 7.69% still not sufficient for Reserve Bank of India comfort level. In this scenario rupee has continued to depreciate in comparison to $ and has crossed the mark of even ` 57 on certain occasions. Urgent measures are required to be initiated to address the issues of heavy subsidies and continued flight of dollar($).

One fervently hopes that the recent expression of determination by the government to take corrective measures without further delay will bear fruits to reverse this overall trend of traveling south in all the major segments.

Financial sectorAnybody associated with the countries financial sector will be proud to reminisce about the manner in which our Central Bank the country’s financial regulator was acclaimed and admired world over for its deft handling of the situation arising from the aftermath of the global financial crises in 2008, described as the greatest after the recession of 1930’s. In the current scenario Reserve Bank of India seems to be playing its role in an extremely prudent manner by striking a fine balance between twin objectives of containing inflation and spurring growth. After a hike in policy rates for record 13 times in 19 months, it cut Repo rate by 50 basis points on 17th April’ 2012, in immediate response to the signs of moderation of inflation rate. Though the exercise was not repeated during the last policy review inspite of the great expectations, one hopes that fiscal policy initiatives will result in containing inflation to Reserve Bank’s comfort level for it to initiate further policy measures for stimulating growth through demand side management.

share Capital & DividendThe Paid-up Share Capital of your Bank as on March 31, 2012 is ` 85.46 crore registering a growth of 7.05%. In keeping with the consistent track record of uninterrupted payment of dividend, the Board of Directors recommend to the General Body, payment of Dividend

DIRECTORs’ REPORT

6

@ 12% p.a. on pro-rata basis for the year ended 31.03.2012. Your Directors are aware there is a heavy payout of dividend out of the Net Profit resulting out of a steep rise in the Subscribed Capital of the Bank. This policy of liberal issue of Capital has been adopted with a view to increase the net worth of a your young and ambitious Bank in the short run and is the only option available for a CRAR necessary for a sustained and healthy growth.

Profitability

Despite the challenging financial year under review, your Bank has been able to record a commendable performance. This could be achieved perhaps due to an excellent teamwork and a confluence of professionalism, commitment, zeal and passion.

The Net Profit of the Bank is arrived at ` 38.73 crore, after provisioning for BDDR, Standard Assets and Amortization cost of acquired banks.

Your Directors recommend the following appropriations of the Net Profit of the Bank :

(Amount in `)

2010-2011 2011-12Statutory Reserve Fund 7,29,00,000.00 9,68,50,000.00

Proposed Dividend * 8,46,43,000.00 9,60,00,000.00

Building Fund 1,00,00,000.00 2,00,00,000.00

Dividend Equilisation Fund 2,00,000.00 2,00,000.00

Investment Fluctuation Fund 3,00,00,000.00 3,00,00,000.00

Members Welfare Fund 16,50,000.00 16,50,000.00

Staff Welfare Fund 16,00,000.00 16,00,000.00

Charity Fund 29,15,900.00 38,73,000.00

Education fund 29,15,900.00 38,73,000.00

Reserve fund for Unforeseen Losses 2,91,59,500.00 3,87,30,000.00

General Reserve Fund 3,16,10,000.00 6,15,47,000.00

Technology Reserve Fund 0.00 50,00,000.00

Net Open Foreign Currency Position Reserve 0.00 10,00,000.00

Balance transfer to Statutory Reserve Fund 94.41 1,545.65

Provision for Bonus & Ex-gratia payment to

the employees **

2,40,00,000.00 2,70,00,000.00

Total 29,15,94,394.41 38,73,24,545.65

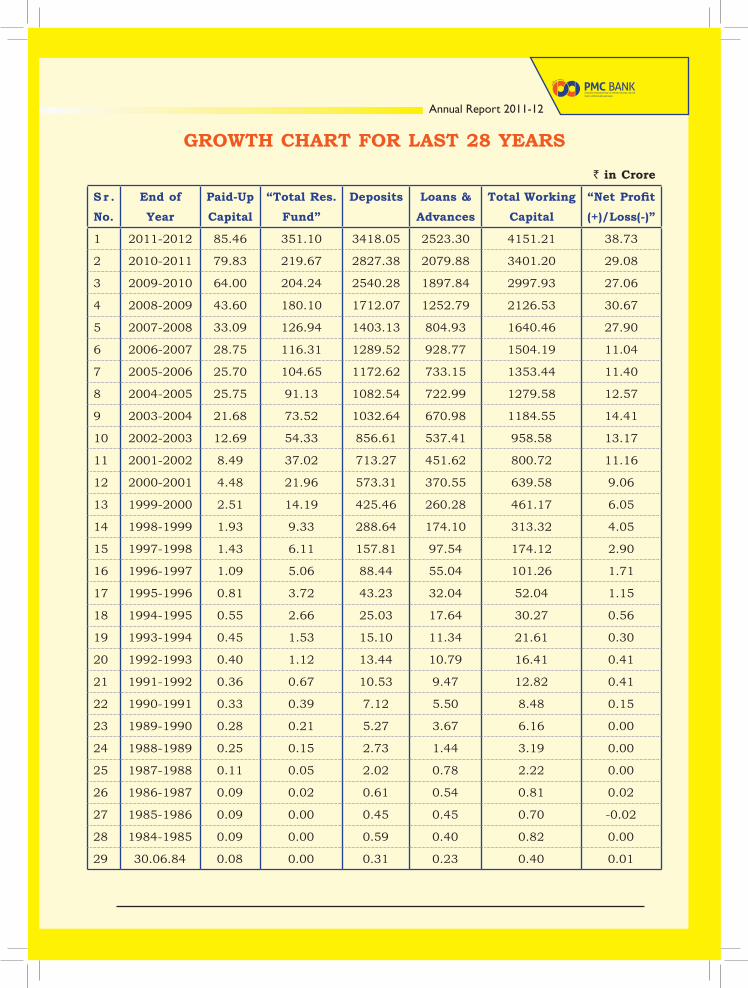

Resource Bank has registered a growth of 20.89% in deposits to reach ` 3418.05crore as on 31st March, 2012 despite the adverse market conditions.

The cost of deposits is likely to remain above 6.72% during the current financial year due the hike in interest on deposits.

Annual Report 2011-12

7

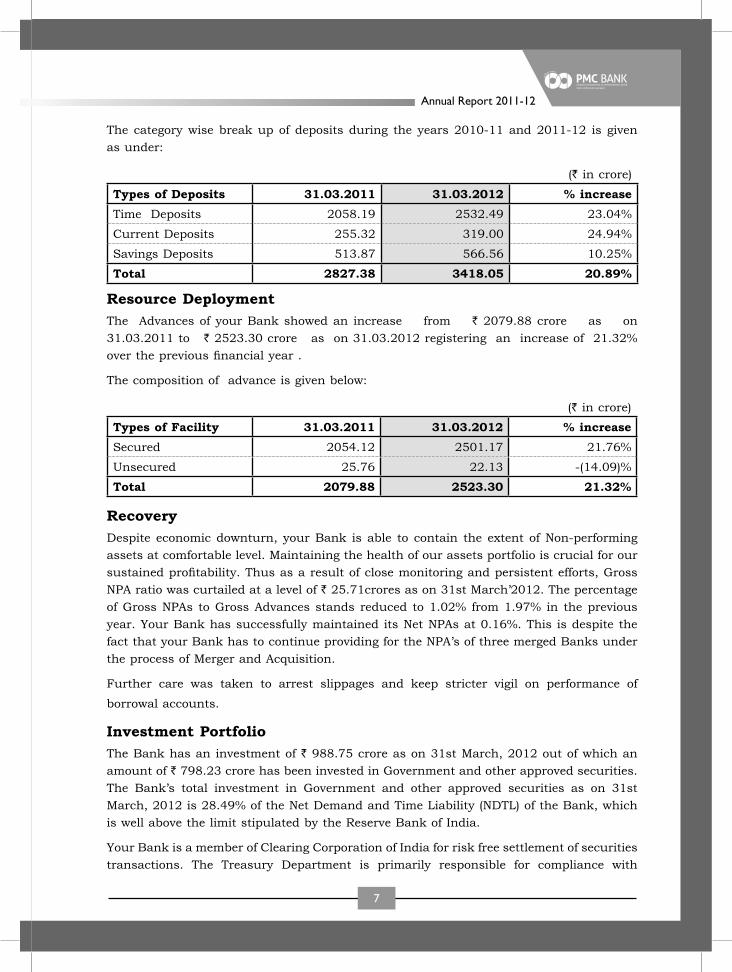

The category wise break up of deposits during the years 2010-11 and 2011-12 is given as under:

(` in crore)

Types of Deposits 31.03.2011 31.03.2012 % increaseTime Deposits 2058.19 2532.49 23.04%

Current Deposits 255.32 319.00 24.94%

Savings Deposits 513.87 566.56 10.25%

Total 2827.38 3418.05 20.89%

Resource Deployment The Advances of your Bank showed an increase from ` 2079.88 crore as on 31.03.2011 to ` 2523.30 crore as on 31.03.2012 registering an increase of 21.32% over the previous financial year .

The composition of advance is given below:

(` in crore)

Types of Facility 31.03.2011 31.03.2012 % increaseSecured 2054.12 2501.17 21.76%

Unsecured 25.76 22.13 -(14.09)%

Total 2079.88 2523.30 21.32%

Recovery Despite economic downturn, your Bank is able to contain the extent of Non-performing assets at comfortable level. Maintaining the health of our assets portfolio is crucial for our sustained profitability. Thus as a result of close monitoring and persistent efforts, Gross NPA ratio was curtailed at a level of ` 25.71crores as on 31st March’2012. The percentage of Gross NPAs to Gross Advances stands reduced to 1.02% from 1.97% in the previous year. Your Bank has successfully maintained its Net NPAs at 0.16%. This is despite the fact that your Bank has to continue providing for the NPA’s of three merged Banks under the process of Merger and Acquisition.

Further care was taken to arrest slippages and keep stricter vigil on performance of

borrowal accounts.

Investment PortfolioThe Bank has an investment of ` 988.75 crore as on 31st March, 2012 out of which an amount of ` 798.23 crore has been invested in Government and other approved securities. The Bank’s total investment in Government and other approved securities as on 31st March, 2012 is 28.49% of the Net Demand and Time Liability (NDTL) of the Bank, which is well above the limit stipulated by the Reserve Bank of India.

Your Bank is a member of Clearing Corporation of India for risk free settlement of securities transactions. The Treasury Department is primarily responsible for compliance with

8

reserve requirements, management of liquidity and interest rate risk on bank’s balance sheet. The Bank has an investment policy in place, which is reviewed in accordance with

the guidelines issued by the Reserve Bank of India.

New Products

Pmc AshaOur Bank has always taken keen interest towards the upliftment of women like its conscious decision of giving them more job opportunities in your Bank and all possible steps to enhance their empowerment.

On the event of Women’s Day on 8th of March, Bank had launched a Special Saving Bank deposit scheme called “PMC ASHA” featuring it as a Zero Balance account with Free Personalised Cheque Book Facility, Demand Draft/Pay Order, RTGS /NEFT facility, ATM/ATM cum-Visa Debit Card , Internet Banking facility, Demat Account, SMS Banking etc,

subject to women be the first holder.

Pmc DoubleA Scheme specially tailored with a view to ensure that our customers get maximum returns on their investment in 79 months. This Scheme is well suited for those customers who intend to get a pre-determined amount as the maturity value.

The Deposit is in the form of Cash Certificate and accepted at discounted values. The minimum amount to be invested was ` 50,000/- and subsequently reduce to ` 25,000/-

This Scheme is applicable for all categories of customers at par.

TechnologyYour Bank has always been one of the front runner in adapting to the technology up-gradations. With large expansion round the corner, the Bank has set up a modern Data center to suit the futuristic needs at its Central office, DREAMS MALL, Bhandup. Your Bank has also set-up an Disaster Recovery Site at Bengaluru.

In order to automate several processes Banks in-house team has developed its own applications like INTRANET for inter-communication of the Bank.

Facilities such as VISA branded PMC Debit cards, IMPS-Inter Mobile Payment Service, 24 hours ATM onsite and Offsite, Co-operative Housing Society Module, more services added in SMS Banking, further your Bank is also equipped for handling Cheque Truncation System initiated by the Reserve Bank of India in a phased manner all over the country. Your Bank has already initialised Mobile Banking Services, which will be available to the customers in due course.

In coming year we plan to serve with Ru-Pay branded Debit card in addition to the VISA Debit card, ATM Sharing for other Banks who do not have ATM infrastructure & become their sponsor bank, for making them part of NFS ATM network. Lobby Banking and a advance system of operating lockers.

Annual Report 2011-12

9

Branch ExpansionThe Board of Directors are pleased to inform that the Reserve Bank of India has given permission for opening of 20 new branches under the Annual Action Plan 2012-13, which includes 3 in Delhi, 2 in Bengaluru, 5 in Goa, 2 in Thane, 2 in Pune, 2 in Navi Mumbai, each at Dharwad and Aurangabad. Appropriate steps have been initiated to complete the process of opening all these branches by the end of year.

Your Bank has opened branches at Bengaluru, Hubli, Ratnagiri, Pune, Nerul, Kalyan in the year under review. With this the total branch network of your Bank stands at 60

branches and 2 extension counters.

Area of OperationYour Bank is pleased to inform you that it has received permission from the Reserve Bank of India, for including the State of Andhra Pradesh in its Area of operation, which already have the State of Maharashtra, Delhi, Karnataka, Gujarat and Goa. With this permission the Area of Operation of your Bank stands extended to the entire State of Maharashtra, Delhi, Karnataka, Gujarat, Goa and Andhra Pradesh after carrying out the required amendments to the Bye-laws and approval of the Central Registrar.

M.R. Pai Memorial Award The M. R. Pai Memorial Award instituted by your Bank since the year 2005 in memory of the great consumer activist, will be presented to Smt. Ela Bhatt, well known social worker who have also has established a co-operative bank for women many years ago in Gujarat. Her organization, SEWA (Self-Employed Women’s Association), has great credibility in the country. The function is proposed to be held on 6th September’2012 at Indian Merchants’ Chamber, Churchgate.

Corporate social ResponsibilityApart from the normal banking operations, the Bank, as a responsible and responsive organization has rendered a helping hand for education, nutrition and healthcare assistance in the form of donations. During the year 2011-12, the Bank made donations aggregating to ` 14.00lacs, to NGO’s like CRY and SAVE THE CHILDREN.

Members Welfare FundThe Board of your Bank has recommended an amount of ` 16.50 lakh towards the Members Welfare Fund, wherein it provides a sum of ` 7500/- towards re-imbursement of medical expenses incurred for Cataract operation by Senior citizen members who have completed five years from the date of admission as a member and also recognition to children of the members who have excelled academically and also to children who have won a Medal at State level or National Level in the field of sports an amount of ` 10000/- per child is paid per.

During the year 2011-12, total 18 members have availed benefit under these schemes.

10

Amendment To Bye LawsAmendment to the bye-laws have been proposed and presented for your consideration, elsewhere in this report. In deference to the wish of Ministry of Corporate Affairs, Govt of India for “Green Initiative in the Corporate Governance” wherein it permits servicing of notice/documents etc., to its members through electronic mode in lines, we propose to amend bye-law no. 22(i) and expect to receive your support and co-operation in helping your Bank to contribute its share to the said initiative.

International Banking Division It was indeed a Red letter day in the history of your Bank when it received the licence for Authorised Dealer Category- I from Reserve Bank of India to deal in foreign exchange directly in the first week of September 2011. With this permission your Bank has been able to cross the last hurdle in its path towards achieving full-fledged banking services at par with other members of the fraternity and look forward to an ambitious growth plan.

Your Bank’s “International Banking Division” was inaugurated at the hands of Shri. S. Karuppasamy, Executive Director, Reserve Bank of India on November 12, 2011. We wish to inform the members that it was no ordinary function. There were reverberations of jubilation and ecstasy all over the place. Indescribable joy and fulfillment were writ large on all the faces glowing with a feeling of a dream come true, engulfing the whole atmosphere. Such moments come rarely which holds great promises for your Bank and all those associated with it.

Although your Bank is a new entrant in this field, it offers all the products for Foreign Exchange Business, which are available with other Public Sector/ Private Sector Banks.

Your Bank has established full-fledged and well equipped Forex Treasury with requisite infrastructure and has commenced independent forex operations w.e.f. December 1, 2011. Your Bank has opened NOSTRO Accounts in four major currencies namely, US Dollar, Great Britain Pounds, EURO and Japanese Yen in order to undertake FX Business. Your Bank has also entered into Correspondent Banking relationship with leading International Banks as well as Overseas branches of Indian Banks at major International centers.

Your Bank extends facilities for financing of Exports - both Pre-shipment and Post-shipment Credit in Indian Rupees as well as Foreign Currency. To facilitate imports into the Country, your Bank offers various products like Import Letter of Credit, Advance payment against Imports, extending Buyer’s Credit, Import Bills on collection basis, Booking of Forward Contract in order to hedge Exchange risk etc. Your Bank also provides remittance facility towards Non-Trade related transactions.

Your Bank is now accepting deposits from Non-Resident Indians under various schemes like Foreign Currency Non-Resident Deposit Scheme (FCNR), Non-Resident External (NRE), Non-Resident Ordinary (NRO). Your Bank also open and maintains Exchange Earner’s Foreign Currency accounts (EEFC), Resident Foreign Currency Account (RFC) etc for Resident Indians.

Your Bank has made tie up arrangement with M/s UAE Exchange and Financial Services

Annual Report 2011-12

11

Limited for prompt receipt of personal remittances from abroad favoring Customers, their friends and relatives etc. under Money Transfer Services Scheme viz., “MONEYGRAM” and “XPRESSMONEY” at all branches.

Human ResourcesHuman Capital represents the human factor in the organization; the combined intelligence, skills and expertise that gives the organization its distinctive character. Your Bank’s human capital is remarkable in terms of quality.

The Human Resource Department of your Bank is well equipped with effective means to select, recruit and retain a high performing workforce, choosing right fit for the right job and preserving a dynamic culture for employees that foster achievement.

The total number of employees of your bank were 867 as of March 31,2012. Your Bank lists ‘people’ as one of its stated core values. The Bank believes in empowering its employees

and constantly takes various measures to achieve this.

Training & Development The Bank continued to focus on training its human resource. Your Bank has put in place a training policy and a calibrated action plan, prominently focusing on the vision of the Bank and the emerging challenges. Your Bank has a dedicated Training Team as part of HRM which undertakes training needs analysis, plans appropriate training programs and conducts the same in-house or nominates employees for apt external training programs.

Training is considered as on an investment rather than an expense.

Audit and InspectionThe Audit & Inspection Department continues to monitor adherence to systems and procedures and compliance of statutory and regulatory requirements. The effective functioning of the departments and internal control systems of the bank are closely monitored by the Audit committee, and remedial measures are initiated, wherever required on an ongoing basis.

In addition to this Executives and Sr. Officials visit branches at regular intervals to monitor functioning of the branches and departments.

At the Annual General Meeting held on 27.08.2011, M/s. D.B. Ketkar & Co., were appointed as Statutory Auditors of the Bank for the financial year 2011-12. The Statutory

Auditors have completed their audit assignment and submitted their report.

Advertising & Publicity The Planning and Marketing department astutely utilized all available channels for promotion i.e Branch Display, Banners, Handouts, Press publicity through articles and features in leading newspapers, through television media – advertising both product centric as well as corporate ads to propagate our products/ schemes , cultural events, hoardings etc, which generated overwhelming response.

12

Your Bank has also sponsored some of the popular dramas, shows, musical events and

awards ceremonies on TV channels like ME MARATHI and LIVE INDIA.

Tribute to Departed soulsThe Board of Directors and Management express their profound sorrow at the sad demise

of the Shareholders who passed away during the year and pray for their eternal peace.

Acknowledgements• The Board of Directors place on record its gratitude to the Shareholders, Customers

and clients for their co-operation and support. Without their support such tremendous growth Land development would not have been possible.

• We place on record our thanks to the Chief General Manager and Chief General Manager-In Charge of Urban Banks Department, the Reserve Bank of India, and his staff for their valuable guidance.

• We place on record our thanks to the Central Registrar, Delhi, Govt. of India, the Commissioner for Co-operation and Registrar of Co-operative Societies, Pune and Maharashtra State, and Registrar – State of Delhi, Registrar – State of Karnataka for the guidance and assistance extended to the Bank.

• The Board of Directors thank the Management of all the Gurudwaras, Schools, Sewak Jathas, Societies and other institutions for their support and co-operation.

• The Board thanks the President and General Secretary of Co-operative Bank Employee’s Union for their support and co-operation.

• The Bank is thankful for the co-operation and support extended by the office and staff of: (1) Maharashtra Urban Co-operative Bank’s Federation Ltd. (2) Brihan Mumbai Nagari Sahakari Bank’s Association Ltd. (3) Maharashtra State Co-operative Bank’s Association Ltd.

• We also thank the various institutions and individuals who have extended their co-operation and assisted us, directly and indirectly in the overall growth, development and prosperity of the Bank.

For and on behalf of the Board of Directors

CHARANJIT sINGH CHADHA

Chairman

Annual Report 2011-12

13

Comparative position of growth over the last one year is as given below :

(` in Crore)

March 2011 March 2012 Comparative % over last year

Share Capital 79.83 85.46 7.05

Reserves 219.80 351.10 59.74

Deposits 2827.38 3418.05 20.89

Cash Investments & Bank Balance

1095.95 1218.62 11.19

Advances 2079.88 2523.30 21.32

Gross Income 325.46 427.28 31.28

Working Capital 3401.21 4151.21 22.05

Net Profit Before Tax 39.73 60.17 51.45

Net Profit After Tax 29.16 38.73 32.82

No. of Branches 52 61

Extension Counters 2 2

14

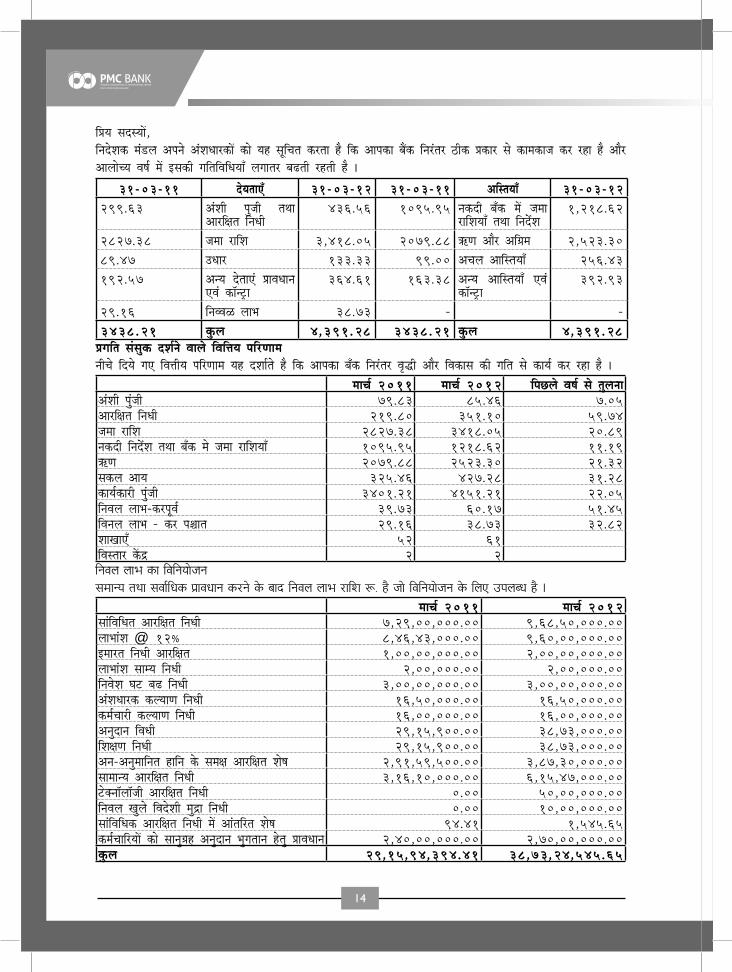

efØeÙe meomÙeeW,efveosMekeâ ceb[ue Deheves DebMeOeejkeâeW keâes Ùen metefÛele keâjlee nw efkeâ Deehekeâe yeQkeâ efvejblej "erkeâ Øekeâej mes keâecekeâepe keâj jne nw Deewj DeeueesÛÙe Je<e& ceW Fmekeâer ieefleefJeefOeÙeeB ueieelej ye{leer jnleer nw ~

31-03-11 osÙeleeSB 31-03-12 31-03-11 DeefmleÙeeB 31-03-12299.63 DebMeer hegpeer leLee

Deejef#ele efveOeer 436.56 1095.95 vekeâoer yeBkeâ ceW pecee

jeefMeÙeeB leLee efveoxMe 1,218.62

2827.38 pecee jeefMe 3,418.05 2079.88 $e+Ce Deewj Deef«ece 2,523.30 89.47 GOeej 133.33 99.00 DeÛeue DeeefmleÙeeB 256.43 192.57 DevÙe osleeSb ØeeJeOeeve

SJeb keâe@vš^e 364.61 163.38 DevÙe DeeefmleÙeeB SJeb

keâe@vš^e 392.93

29.16 efveJJeU ueeYe 38.73 - -3438.21 kegâue 4,391.28 3438.21 kegâue 4,391.28Øeieefle mebmegkeâ oMe&ves Jeeues efJeefòeÙe heefjCeeceveerÛes efoÙes ieS efJeòeerÙe heefjCeece Ùen oMee&les nw efkeâ Deehekeâe yeBkeâ efvejblej Je=æer Deewj efJekeâeme keâer ieefle mes keâeÙe& keâj jne nw ~

ceeÛe& 2011 ceeÛe& 2012 efheÚues Je<e& mes legueveeDebMeer hegbpeer 79.83 85.46 7.05Deejef#ele efveOeer 219.80 351.10 59.74pecee jeefMe 2827.38 3418.05 20.89vekeâoer efveoxMe leLee yeBkeâ ces pecee jeefMeÙeeB 1095.95 1218.62 11.19 $e+Ce 2079.88 2523.30 21.32mekeâue DeeÙe 325.46 427.28 31.28keâeÙe&keâejer hegbpeer 3401.21 4151.21 22.05efveJeue ueeYe-keâjhetJe& 39.73 60.17 51.45efJeveue ueeYe - keâj he§eele 29.16 38.73 32.82 MeeKeeSB 52 61efJemleej keWâõ 2 2efveJeue ueeYe keâe efJeefveÙeespevemeceevÙe leLee meJee&efOekeâ ØeeJeOeeve keâjves kesâ yeeo efveJeue ueeYe jeefMe ¤. nw pees efJeefveÙeespeve kesâ efueS GheueyOe nw ~

ceeÛe& 2011 ceeÛe& 2012 meebefJeefOele Deejef#ele efveOeer 7,29,00,000.00 9,68,50,000.00ueeYeebMe @ 12³ 8,46,43,000.00 9,60,00,000.00Fceejle efveOeer Deejef#ele 1,00,00,000.00 2,00,00,000.00ueeYeebMe meecÙe efveOeer 2,00,000.00 2,00,000.00efveJesMe Ieš ye{ efveOeer 3,00,00,000.00 3,00,00,000.00DebMeOeejkeâ keâuÙeeCe efveOeer 16,50,000.00 16,50,000.00keâce&Ûeejer keâuÙeeCe efveOeer 16,00,000.00 16,00,000.00Devegoeve efJeOeer 29,15,900.00 38,73,000.00efMe#eCe efveOeer 29,15,900.00 38,73,000.00Deve-Devegceeefvele neefve kesâ mece#e Deejef#ele Mes<e 2,91,59,500.00 3,87,30,000.00meeceevÙe Deejef#ele efveOeer 3,16,10,000.00 6,15,47,000.00šskeävee@uee@peer Deejef#ele efveOeer 0.00 50,00,000.00efveJeue Kegues efJeosMeer cegõe efveOeer 0.00 10,00,000.00meebefJeefOekeâ Deejef#ele efveOeer ceW Deebleefjle Mes<e 94.41 1,545.65keâce&ÛeeefjÙeeW keâes meeveg«en Devegoeve Yegieleeve nsleg ØeeJeOeeve 2,40,00,000.00 2,70,00,000.00kegâue 29,15,94,394.41 38,73,24,545.65

Annual Report 2011-12

15

sTATUTORY AUDITORs REPORT FOR THE YEAR ENDED 31ST MARCH 2012.

(Under Section 31 of Banking Regulation Act, 1949 and Section 73(4) of Multi State Co-operative Societies Act, 2002 and Rule 27 of Multi-State Co-operative Societies Rules)We have audited the attached Balance Sheet of “PUNJAB & MAHARASHTRA CO-OPERATIVE BANK LTD” at 31st March, 2012 and also the Profit and Loss Account of the Bank for the year ended on that date annexed thereto. These financial statements are the responsibility of the Bank’s management. Our responsibility is to express an opinion on these financial statements based on our audit.We conducted our audit in accordance with auditing standards generally accepted in India. Those standards required that we plan and perform the audit to obtain reasonable assurance whether the financial statements are free of material misstatements. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.The schedules giving the particulars referred to in Rule 27 (3) of the Multi State Co-Operative Society’s Rule 2002 to the extent applicable are attached to this report . Further to our comments and observations in the Audit Report of even date, we report that :1. We have obtained all the information and explanations, which to the best of our knowledge

and belief were necessary for the purpose of our audit;2. In our opinion, proper books of accounts as required by the Multi-State Co-operative

Societies Act, Rule 27 of the Multi State Co-Operative Societies Rules 2002 and Bye Laws of the Bank have been kept by the Bank, so far as appears from our examination of those books and proper returns adequate for the purposes of our audit have been received from the branches and offices of the Bank, not visited by us.

3. To the best of our knowledge and belief and according to the information and explanations given to us, there is no material impropriety and irregularities in the expenditure or in the realization of monies due to the Bank.

4. To the best of our information and explanations given to us, the transactions of the Bank, which have come to our notice have been within the competence of the Bank and are in compliance with RBI guidelines, as applicable to Multi-State Co-Operative Banks.

5. The Balance Sheet and Profit and Loss Account are in agreement with the Books of Account maintained by the Bank.

6. In our opinion and to the best of our information and according to the explanations given to us, the said accounts subject to Significant Accounting Policies and Notes on Accounts forming part of accounts and our comments and observations contained in Audit Memorandum, give all the information as required by the Multi-State Co-operative Societies Act, 2002, and rules made there under, in the manner so required, in conformity with the accounting principles generally accepted in India and give a true and fair view:a. In the case of the Balance Sheet, of the State of Affairs of the Bank as at 31st March

2012 andb. In the case of the Profit and Loss Account of the profit for the year ended on that date.c. In the case of the Cash Flow Statement of the Cash Flows of the Bank for the year

ended on that date.Place: Mumbai For D.B.Ketkar & CoDate: 31/05/2012 Chartered Accountants

Firm Regn. No. 105007W

s.G.KHARE(PARTNER)

M. No. 36680Statutory Auditors

16

BALANCE sHEET As AT MARCH 31, 2012

CAPITAL & LIABILITIEs schedule Current Year Previous Year

31.03.2012 31.03.2011

1 Capital 1 85,46,05,525.00 79,82,99,400.00

2 Reserve Fund & Other Reserves

2 351,10,02,806.84 219,79,74,536.25

3 Deposits & Other Accounts

3 3418,05,42,780.31 2827,38,00,397.56

4 Borrowings 4 133,32,90,132.48 89,47,36,000.00

5 Bills For Collection Being Bills Receivable as per Contra

217,59,50,557.79 2,17,67,257.68

6 Branch Adjustments 16,04,668.22 27,16,885.91

7 Overdue Interest Reserve

22,47,39,379.25 34,82,43,919.31

8 Interest Payable 22,38,43,297.46 15,97,74,844.51

9 Other Liabilities 5 101,98,92,157.65 139,31,62,404.87

10 Profit & Loss 6 38,73,24,545.65 29,15,94,394.41

Total 4391,27,95,850.65 3438,20,70,040.50

Contingent Liabilities 13 326,60,05,913.00 187,98,48,648.00

As per our Report of even date attached

For D.B.Ketkar & Co s. Charanjit singh Chadha

Chartered Accountants Chairman

s.G.Khare s. Waryam singh

Partner Vice Chairman

Membership No. 36680

Statutory Auditors shri. Joy Thomas

Date: 31st May 2012 Managing Director

Annual Report 2011-12

17

BALANCE sHEET As AT MARCH 31, 2012

PROPERTY & AssETs schedule Current Year Previous Year

31.03.2012 31.03.2011

1 Cash 7 222,31,07,264.14 211,48,23,009.79

2 Balances With Other Banks

8 115,04,09,718.65 159,61,57,960.90

3 Investments 9 881,26,63,395.97 724,84,92,651.95

4 Advances 10 2523,30,22,220.34 2079,87,57,908.66

5 Bills For Collection Being Bills Receivable as per Contra

217,59,50,557.79 2,17,67,257.68

6 Interest Receivable 39,43,43,293.99 28,48,36,841.16

7 Overdue Interest Reserve

22,47,39,379.25 34,82,43,919.31

8 Fixed Assets 11 256,43,43,131.26 99,00,02,670.10

9 Other Assets 12 101,25,30,866.49 87,11,21,798.18

10 Non Banking Assets Acquired in Satisfaction Of Claims

12,16,86,022.77 10,78,66,022.77

Total 4391,27,95,850.65 3438,20,70,040.50

Directors

S. Resham Singh S. Balbir Singh Kochhar S. Surjit Singh Narang

S. Daljit Singh Bal S. Joginder Singh Palla S. Surjit Singh Arora

S. Rajneet Singh Shri. Jagdish Mookhey S. Gurnam Singh Hothi

Smt. Trupti Bane Smt. Parmeet Sodhi S. Jasvinder Singh Banwait

Shri. Brij Bhushan Handa Smt. Mukti Bavisi

18

PROFIT & LOss ACCOUNT FOR THE YEAR ENDED MARCH 31, 2012

EXPENDITURECurrent Year Previous Year

31.03.2012 31.03.20111 Interest on Deposits, Borrowings, etc 252,28,49,909.72 180,59,96,961.102 Salaries and allowances 33,24,28,837.13 29,78,77,279.633 Rent, Taxes, Insurance, Lightning, etc 9,65,09,943.82 7,04,93,265.744 Legal Charges 1,05,205.00 1,75,600.005 Postage, Telegram and Telephone charges 1,92,46,721.60 1,30,21,125.066 Audit fees & Professional Charges 1,83,76,965.96 1,76,18,937.867 Depreciation / Amortisation of Assets 11,47,17,871.18 9,85,27,055.498 Printing Stationery and Advertisement

i) Printing and Stationery 1,45,52,189.04 1,26,60,678.28ii) Advertisements 4,95,68,454.51 2,99,03,099.35

6,41,20,643.55 4,25,63,777.639 Other Expenditure:

i) Repairs and Maintenance of assets 4,26,88,166.83 3,41,96,382.27ii) Premium paid to DICGC 2,81,39,051.00 2,53,16,382.00iii) Travelling and Conveyance 36,76,759.00 37,99,121.50iv) Security Charges 1,91,13,204.00 2,05,41,421.28v) Amortisation of Investments 64,48,300.10 63,13,661.09vi) Amortisation of Cost of Acquired Bank 11,31,08,000.00 11,31,08,000.00vii) Bad Debts Written Off 9,75,43,774.04 17,41,56,007.99viii) Other Expenses 7,62,43,922.20 6,11,91,608.40

38,69,61,177.17 43,86,22,584.5310 Provisions

i) Provision Against Std. Assets 1,80,00,000.00 45,50,976.45ii) Provision for Other Contingent Liabilities 2,56,550.00 26,23,023.00iii) Prov for Investment Depreciation Reserve 9,58,10,066.16 6,52,24,141.74iv) Special Reserve u/s. 36(1) (viii) 17,00,000.00 0.00

11,57,66,616.16 7,23,98,141.1911 Income Tax Expenses

i) Current Tax 20,18,80,000.00 10,03,76,709.00ii) Deffered Tax 1,25,10,120.00 53,44,075.00

21,43,90,120.00 10,57,20,784.0012 Total Expenses 388,54,74,011.29 296,30,15,512.2313 Net Profit after Tax 38,73,24,545.65 29,15,94,394.41

Total 427,27,98,556.94 325,46,09,906.64As per our Report of even date attachedFor D.B.Ketkar & Co s. Charanjit singh ChadhaChartered Accountants Chairman

s.G.Khare s. Waryam singhPartner Vice ChairmanMembership No. 36680Statutory Auditors shri. Joy ThomasDate: 31st May 2012 Managing Director

Annual Report 2011-12

19

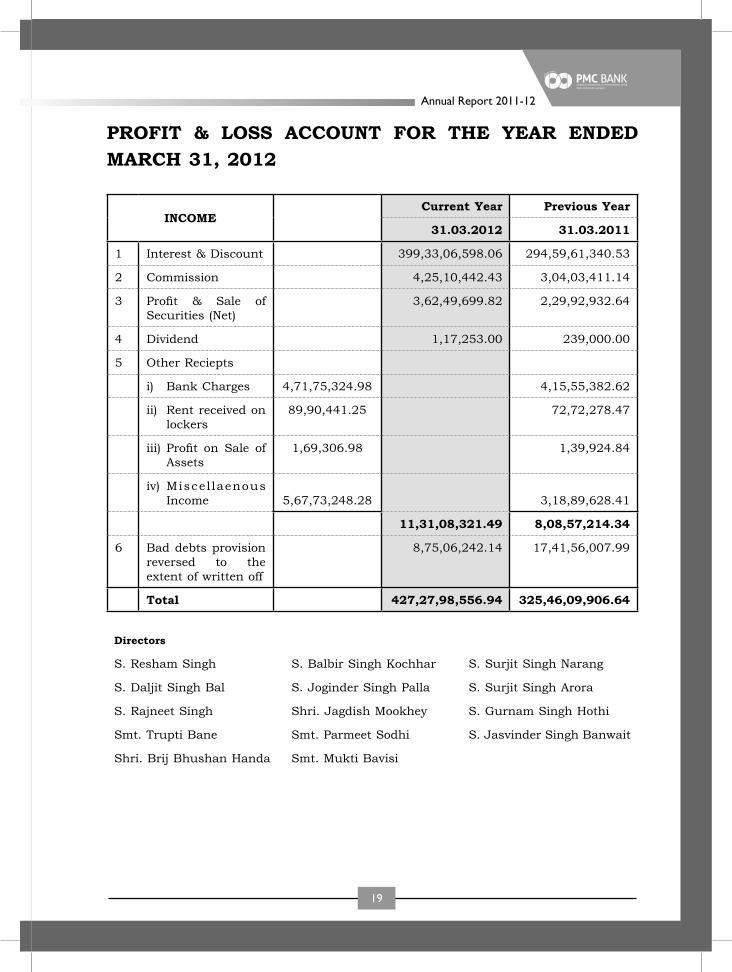

PROFIT & LOss ACCOUNT FOR THE YEAR ENDED MARCH 31, 2012

INCOMECurrent Year Previous Year

31.03.2012 31.03.2011

1 Interest & Discount 399,33,06,598.06 294,59,61,340.53

2 Commission 4,25,10,442.43 3,04,03,411.14

3 Profit & Sale of Securities (Net)

3,62,49,699.82 2,29,92,932.64

4 Dividend 1,17,253.00 239,000.00

5 Other Reciepts

i) Bank Charges 4,71,75,324.98 4,15,55,382.62

ii) Rent received on lockers

89,90,441.25 72,72,278.47

iii) Profit on Sale of Assets

1,69,306.98 1,39,924.84

iv) Miscel laenous Income 5,67,73,248.28 3,18,89,628.41

11,31,08,321.49 8,08,57,214.34

6 Bad debts provision reversed to the extent of written off

8,75,06,242.14 17,41,56,007.99

Total 427,27,98,556.94 325,46,09,906.64

Directors

S. Resham Singh S. Balbir Singh Kochhar S. Surjit Singh Narang

S. Daljit Singh Bal S. Joginder Singh Palla S. Surjit Singh Arora

S. Rajneet Singh Shri. Jagdish Mookhey S. Gurnam Singh Hothi

Smt. Trupti Bane Smt. Parmeet Sodhi S. Jasvinder Singh Banwait

Shri. Brij Bhushan Handa Smt. Mukti Bavisi

20

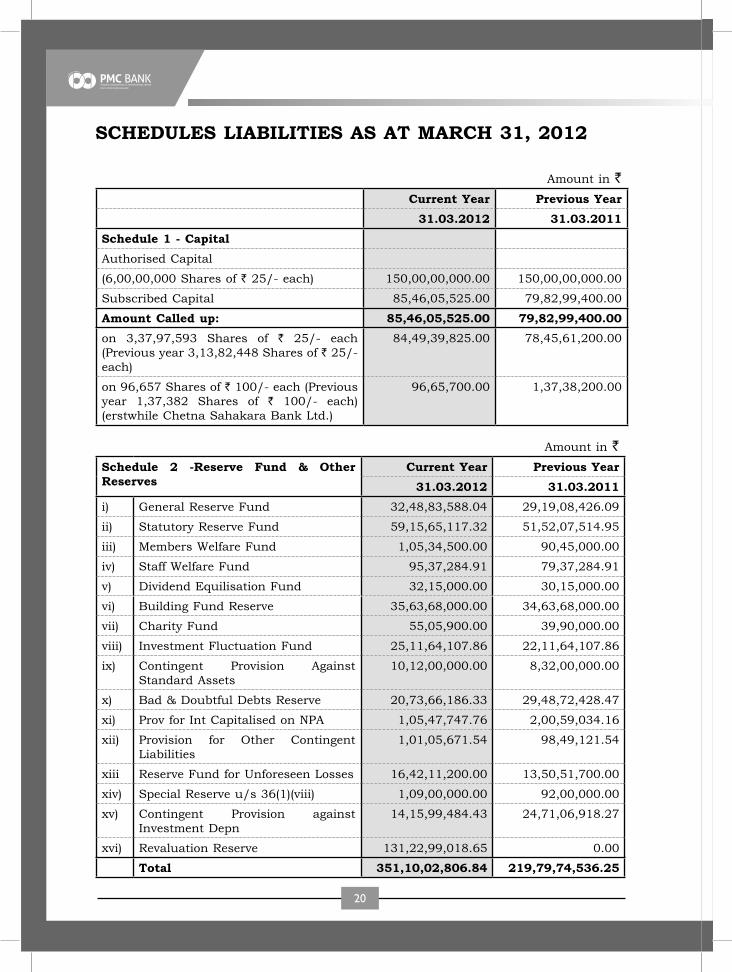

sCHEDULEs LIABILITIEs As AT MARCH 31, 2012

Amount in `

Current Year Previous Year 31.03.2012 31.03.2011

schedule 1 - Capital Authorised Capital

(6,00,00,000 Shares of ` 25/- each) 150,00,00,000.00 150,00,00,000.00

Subscribed Capital 85,46,05,525.00 79,82,99,400.00

Amount Called up: 85,46,05,525.00 79,82,99,400.00on 3,37,97,593 Shares of ` 25/- each (Previous year 3,13,82,448 Shares of ` 25/- each)

84,49,39,825.00 78,45,61,200.00

on 96,657 Shares of ` 100/- each (Previous year 1,37,382 Shares of ` 100/- each) (erstwhile Chetna Sahakara Bank Ltd.)

96,65,700.00 1,37,38,200.00

Amount in `

schedule 2 -Reserve Fund & Other Reserves

Current Year Previous Year 31.03.2012 31.03.2011

i) General Reserve Fund 32,48,83,588.04 29,19,08,426.09

ii) Statutory Reserve Fund 59,15,65,117.32 51,52,07,514.95

iii) Members Welfare Fund 1,05,34,500.00 90,45,000.00

iv) Staff Welfare Fund 95,37,284.91 79,37,284.91

v) Dividend Equilisation Fund 32,15,000.00 30,15,000.00

vi) Building Fund Reserve 35,63,68,000.00 34,63,68,000.00

vii) Charity Fund 55,05,900.00 39,90,000.00

viii) Investment Fluctuation Fund 25,11,64,107.86 22,11,64,107.86

ix) Contingent Provision Against Standard Assets

10,12,00,000.00 8,32,00,000.00

x) Bad & Doubtful Debts Reserve 20,73,66,186.33 29,48,72,428.47

xi) Prov for Int Capitalised on NPA 1,05,47,747.76 2,00,59,034.16

xii) Provision for Other Contingent Liabilities

1,01,05,671.54 98,49,121.54

xiii Reserve Fund for Unforeseen Losses 16,42,11,200.00 13,50,51,700.00

xiv) Special Reserve u/s 36(1)(viii) 1,09,00,000.00 92,00,000.00

xv) Contingent Provision against Investment Depn

14,15,99,484.43 24,71,06,918.27

xvi) Revaluation Reserve 131,22,99,018.65 0.00

Total 351,10,02,806.84 219,79,74,536.25

Annual Report 2011-12

21

Amount in `

Current Year Previous Year 31.03.2012 31.03.2011

schedule 3 - Deposits & Other Accounts :i) Fixed Deposits :

a) Individuals & Others 2240,60,01,602.80 1931,74,43,947.95

b) Co-operative Institutions 273,56,17,949.30 103,20,48,018.50

sub Total 2514,16,19,552.10 2034,94,91,966.45

ii) saving Bank Deposits :a) Individuals & Others 546,23,57,159.32 500,18,00,187.71

b) Co-operative Institutions 20,32,11,378.39 13,68,52,032.31

sub Total 566,55,68,537.71 513,86,52,220.02

iii) Current Deposits :a) Individuals & Others 317,22,22,211.32 253,63,19,130.36

b) Co-operative Institutions 1,78,24,526.61 1,69,32,342.54

sub Total 319,00,46,737.93 255,32,51,472.90

vi) Matured Deposits 18,33,07,952.57 23,24,04,738.19

sub Total 18,33,07,952.57 23,24,04,738.19Total 3418,05,42,780.31 2827,38,00,397.56

Amount in `

Current Year Previous Year 31.03.2012 31.03.2011

schedule 4 -Borrowings i) From NHB: Refinance from

National Housing Bank Finance131,57,88,000.00 89,47,36,000.00

ii) Loans from other sourcesa) Overdraft from Banks 1,75,02,132.48 0.00

b) CBLO Borrowings 0.00 0.00

Total 133,32,90,132.48 89,47,36,000.00

22

Amount in ` Current Year Previous Year

31.03.2012 31.03.2011 schedule 5 -Other Liabilities a) Pay orders 11,15,61,306.56 15,86,01,048.67b) Unclaimed Dividend 52,23,053.00 53,21,741.00c) Miscellaneous Accounts 34,51,90,875.04 88,42,03,075.10d) Advance Interest on Bills Discounted 0.00 199.36e) Advance Rent Received on lockers 47,14,051.28 43,01,823.33f) Advance commission on Bank

Gurantee65,05,364.59 36,31,406.92

g) Tax deducted at source 105,89,351.70 90,17,387.01h) Provision for Taxes 48,29,80,000.00 28,11,00,000.00i) Collection Account - Jai Shivrai

Nagari Sahakari Bank Ltd 86,75,062.00 86,75,062.00

j) Customer Liability for Legal Expenses 74,20,457.48 55,71,605.48k) NFS Network Account 20,70,600.00 86,10,600.00l) Interest Payable on NHB Loan 3,32,98,877.00 2,05,91,187.00m) Income Tax Payable 16,63,159.00 35,37,269.00

Total 101,98,92,157.65 139,31,62,404.87

Amount in ` Current Year Previous Year

31.03.2012 31.03.2011 Schedule 6- Profit & LossProfit as per last Balance Sheet 29,15,94,394.41 27,06,42,034.64Less : Appropriation of profit Statutory Reserve Fund 7,29,00,094.41 6,77,01,934.64Dividend 8,46,43,000.00 5,66,69,500.00Building Fund 1,00,00,000.00 1,00,00,000.00Dividend Equalisation Fund 2,00,000.00 2,00,000.00Investment Fluctuation Fund 3,00,00,000.00 3,00,00,000.00Member Welfare Fund 16,50,000.00 16,50,000.00Staff Welfare Fund 16,00,000.00 16,00,000.00Charity Fund 29,15,900.00 27,00,000.00Education Fund 29,15,900.00 27,06,400.00Reserve Fund for Unforeseen Losses 2,91,59,500.00 2,70,64,200.00Provision for Ex-Gratia payment to the Employees

2,40,00,000.00 2,00,00,000.00

General Reserve Fund 3,16,10,000.00 5,03,50,000.00Add : Profit for the year as per Profit & Loss Account

38,73,24,545.65 29,15,94,394.41

Annual Report 2011-12

23

sCHEDULEs AssETs As AT MARCH 31, 2012

Amount in ` Current Year Previous Year

31.03.2012 31.03.2011 schedule 7 - Cash i) Cash in hand 14,44,44,931.84 17,00,62,097.76

(including Foreign currency Notes)ii) Balance with RBI

in Current A/c 200,82,70,761.31 189,73,12,776.63iii) Balance with SBI & SBI Associates

in Current A/c 5,02,53,560.01 2,48,51,991.49iv) Balance with State Co-operative

Banks 22,397.73 30,85,290.30

v) Balance with District Central Co-operative Banks

2,01,15,613.25 1,95,10,853.61

Total 222,31,07,264.14 211,48,23,009.79

Amount in ` Current Year Previous Year

31.03.2012 31.03.2011 schedule 8 - Balance With Other Banks & Foreign Banks i) Current Deposits 7,01,71,029.83 4,94,69,340.86ii) Current Deposits with Banks Abroad 53,60,390.55 0.00iii) Fixed Deposits 107,48,78,298.27 154,66,88,620.04

Total 115,04,09,718.65 159,61,57,960.90

Amount in ` Current Year Previous Year

31.03.2012 31.03.2011 schedule 9 - Investments(A) i) In Central & State Government

Securities 798,08,08,147.85 651,79,94,244.42

Face Value 804,51,27,000.00 637,45,02,000.00Market Value 768,92,97,204.67 608,99,32,712.60

ii) Shares in Co-operative Institutions

1,48,701.00 1,48,701.00

iii) Units of UTI/Other Mutual Funds

0.00 25,00,000.00

iv) Collateral Borrowing Lending Obligation (CBLO)

64,95,56,547.12 44,95,68,906.53

v) PSU Bonds & Bonds of All India Financial Institutions

18,06,50,000.00 18,06,50,000.00

vi) Investment in Bonds (SLR) 15,00,000.00 1,500,000.00vii) Investment in Certificate of

Deposit 0.00 9,61,30,800.00

Total 881,26,63,395.97 724,84,92,651.95

24

Amount in ` Current Year Previous Year

31.03.2012 31.03.2011 schedule 10 - Advances i) short Term Loans :

a) Secured 2091,88,76,883.19 1691,67,84,075.37b) Unsecured 10,46,29,767.25 11,32,86,814.28

2102,35,06,650.44 1703,00,70,889.65ii) Medium Term Advances :

a) Secured 93,00,23,744.14 74,25,12,676.82b) Unsecured 9,66,58,985.28 10,82,18,510.27

102,66,82,729.42 85,07,31,187.09iii) Long Term Advances :

a) Secured 184,16,46,446.06 197,90,39,872.38b) Unsecured 1,99,70,015.99 3,61,13,953.09

186,16,16,462.05 201,51,53,825.47iv) Loans Earmarked Against NHB

Refinance

132,12,16,378.43 90,28,02,006.45

Total 2523,30,22,220.34 2079,87,57,908.66

Amount in ` Current Year Previous Year

31.03.2012 31.03.2011 schedule 11 - Fixed Assets :i) Furniture & Fixtures & Office

Equipment

20,04,98,730.30 15,45,64,798.74

Add: Additions during the year (Net) 17,24,19,786.87 9,25,34,394.96Less: Depreciation 5,66,92,678.78 4,66,00,463.40subtotal 31,62,25,838.39 20,04,98,730.30

ii) Capital Expenditure on Rented Premises 4,19,93,647.46 3,12,04,257.40Add: Additions during the year (Net) 5,37,42,914.84 2,50,89,834.24Less: Depreciation 1,95,84,122.48 1,43,00,444.18subtotal 7,61,52,439.82 4,19,93,647.46

iii) Land & Premises Account 74,12,65,540.30 74,93,12,585.65Add: Additions during the year (Net) 145,85,21,836.65 2,80,85,550.00Less: Depreciation 3,63,97,367.65 3,61,32,595.35subtotal 216,33,90,009.30 74,12,65,540.30

iv) Office Vehicle 62,44,752.04 23,07,605.76Add: Additions during the year (Net) 43,73,793.98 54,30,698.84Less: Depreciation 20,43,702.27 14,93,552.56subtotal 85,74,843.75 62,44,752.04Total 256,43,43,131.26 99,00,02,670.10

Annual Report 2011-12

25

Amount in `

Current Year Previous Year

31.03.2012 31.03.2011

schedule 12 - Other Assets

i) Prepaid Expenses 2,26,36,193.81 1,18,71,577.55

ii) Stock of Stationery 49,52,482.48 57,85,534.25

iii) Stock of Stamped Documents & Lockers

92,79,222.00 2,43,28,628.00

iv) Deposit & Advance with LandLord 15,65,48,876.60 9,43,99,806.60

v) Sundry Receivable 1,99,22,831.40 3,85,16,411.30

vi) Clearing House Receivable 3,62,114.00 40,000.00

vii) Security Deposit with Companies/Authorities

7,85,50,032.44 6,00,63,778.94

viii) Library 25,795.61 25,975.61

ix) Tax Deducted at Source 1,34,77,451.40 74,24,951.18

x) Advance Taxes 48,16,51,900.00 27,97,71,900.00

xi) Deferred Tax Assets 6,21,24,380.00 7,46,34,500.00

xii) Legal Expenses Receivable 74,20,457.48 55,71,605.48

xiii) Cost of Acquisition 15,55,79,129.27 26,86,87,129.27

Total 101,25,30,866.49 87,11,21,798.18

Amount in `

Current Year Previous Year

31.03.2012 31.03.2011

schedule 13 - Contingent Liabilities

i) Bank Guarantee Issued 138,32,81,134.61 65,86,06,238.00

ii) Letter of Credit Issued 143,81,95,368.00 122,12,42,410.00

iii) Forward exchange contracts 44,45,29,410.39 0.00

Total 326,60,05,913.00 187,98,48,648.00

26

NOTEs FORMING PART OF THE PROFIT AND LOss ACCOUNT FOR THE YEAR ENDED 31sT MARCH, 2012 AND BALANCE sHEET As ON EVEN DATE

I. 1) Overview The Punjab & Maharashtra Co-op Bank Ltd was incorporated in 1984 and has

completed its 28 years of providing wide range of Banking and Financial Services

including commercial Banking, Treasury & Forex Operations.

2) Basis of Preparation The financial statements have been prepared and presented under the historical cost

convention on the accrual basis of accounting, unless otherwise stated, and comply with generally accepted accounting principles, statutory requirements prescribed under the Banking Regulation Act, 1949, and the Multi-State Co-operative Societies Act, 2002, circulars and guidelines issued by the Reserve Bank of India(‘RBI’) from time to time, the Accounting Standards (‘AS’) issued by the Institute of Chartered Accountants of India (‘ICAI’) and current practices prevailing within the banking industry of India.

3) Use of Estimates The preparation of the financial statements, in conformity with generally accepted

accounting principles, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, revenues and expenses and disclosure of contingent liabilities at the financial statements. Actual results could differ from those estimates. Management believes that the estimates used in the preparation of the financial statements are prudent and reasonable. Any

revisions to the accounting estimates are recognized prospectively.

II. Significant Accounting Policies:

1) Accounting Convention: The financial statements are drawn up keeping in mind the historical cost and going

concern concept and in accordance with generally accepted accounting principles

and practices prevailing in the Co-operative Banks in India except otherwise stated.

2) Revenue Recognition: Income and expenditure are accounted for on accrual basis except stated below.

i) Income from non-performing assets is recognized to the extent realized, as per the directives issued by Reserve Bank of India.

ii) Dividend received from shares of co-operative institutions is accounted on receipt basis.

Annual Report 2011-12

27

iii) Interest on Securities which is due and not received for a period of more than 90 days is recognized on realization basis as per Reserve Bank of India guidelines.

iv) Commission exchange and brokerage is recognized on realization, except for guarantee commission which is recognized on a straight line basis over the period of contract.

v) Income from distribution of insurance products is recognized on the basis of business booked.

vi) Recoveries in suit filed accounts, accounts under securitization & arbitration are appropriated first towards principal and thereafter towards recorded

interest and other dues.

3) Loans And Advances: The classification of advances into Standard, Sub-standard, Doubtful & Loss assets

as well as provision on non-performing advances has been arrived at in accordance with the directive issued by the Reserve Bank of India from time to time.

The overdue interest in respect of advances classified as Non-performing Assets is provided separately under “Overdue Interest Reserve” as per the directives issued by the RBI.

The Bank has been lending under Collateralized Lending and Borrowing Obligations (CBLO) facility. Any lending under this facility repayable beyond 15 days is classified under Advances (Short Term) Secured against Government and Other Approved Securities. Other lending repayable within 15 days are classified under “Money at

Call and Short Notice.”

4) Investments: i) The Bank has categorized the investments in accordance with the RBI

guidelines applicable to Urban Co-operative Banks. Accordingly, classification of investments for the purpose of valuation is done under the following categories.

ii) Investments have been classified under five groups as required under RBI guidelines – Government securities, Other approved Securities, Shares in co-op. Institutions, PSU Bonds & Bonds of All India Financial Institutions and Certificate of Deposits & others for the purpose of disclosure in the Balance Sheet.

iii) Investment under “Held to Maturity” category has been valued at acquisition cost. Premium, if any, on such investments is amortized over the residual life of the particular investment.

iv) Investments under “Held for Trading” category have been marked to market on the basis of guidelines issued by the RBI. While net depreciation, if any,

28

under each classification has been provided for, net appreciation, if any, has been ignored.

v) Investment under “Available for Sale” category have been marked to market on the basis of guidelines issued by the RBI. While net depreciation, if any, under each classification has been provided form net appreciation, if any, has been ignored.

vi) Treasury Bills and Certificate of Deposits under all the classifications have been valued at carrying cost.

vii) Market value in case of State Govt. and other Securities, for which quotes are not available is determined on the basis of the “Yield to Maturity” indicated by Primary Dealers Association of India(PDAI) jointly with Fixed Income and

Money Market Derivatives Association of India(FIMMDA).

5) Foreign Exchange Transactions: The Bank started its foreign exchange operations w.e.f. December 01, 2011 as

authorized dealer under AD Category-I licence issued by RBI and the following accounting policy has been adopted by the bank for recording foreign currency transactions:

1. All foreign exchange transactions are accounted for at the ongoing market rates prevailing on the date & time of transactions. Monetary foreign currency assets and liabilities reflected in the Balance sheet on the date are at the rates notified by Foreign Exchange Dealers Association of India (FEDAI). All profits/losses due to revaluations are recognized in the profit & loss account.

2. The Outstanding spot and forward contracts are revalued at the monthly rates notified by FEDAI. The resulting profits/losses are included in profit & Loss account as per FEDAI/RBI guidelines.

3. The Contingent liabilities on account of foreign exchange contracts and other obligations denominated in foreign currency are disclosed at monthly closing

rates of exchange declared by FEDAI.

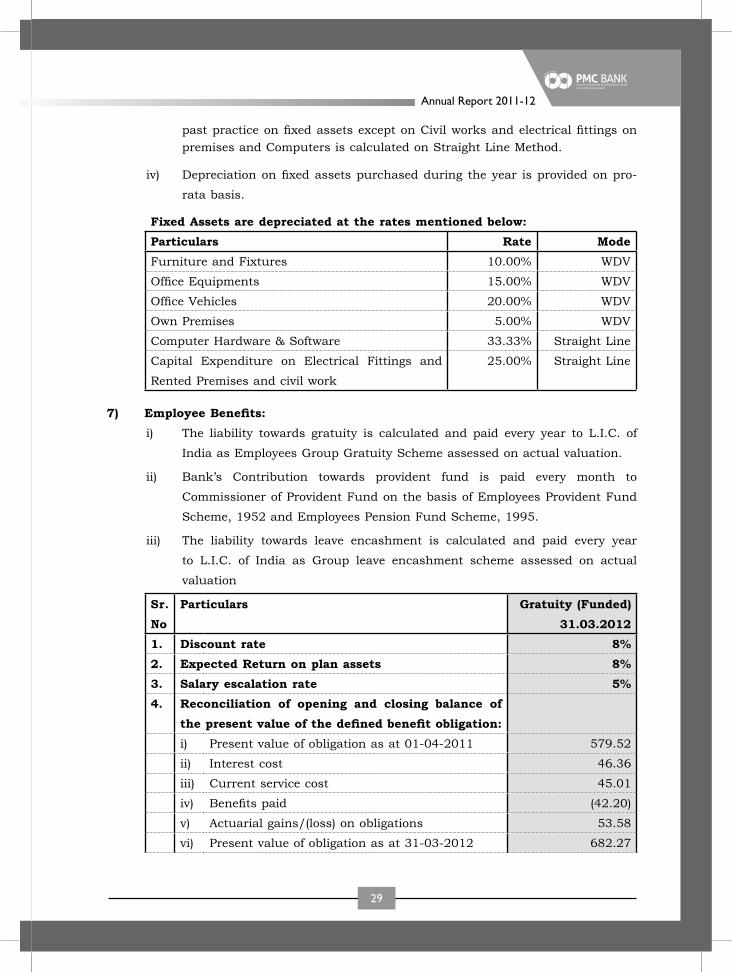

6) Fixed Assets And Depreciation:

i) During the year Bank has got valued its premises by an approved valuer. The premises having book value of ` 6675.41 lacs have been revalued at ` 19798.40 lacs. The Bank has created revaluation reserve amounting to ` 13122.99 lacs.

ii) Fixed Assets are stated at historical cost less accumulated depreciation in accordance with AS-6 and AS-10 issued by Institute of Chartered Accountants of India (ICAI). Fixed Assets include incidental expenses incurred on acquisition and installation of the assets.

iii) Depreciation is calculated on written down value basis in consistency with

Annual Report 2011-12

29

past practice on fixed assets except on Civil works and electrical fittings on premises and Computers is calculated on Straight Line Method.

iv) Depreciation on fixed assets purchased during the year is provided on pro-

rata basis.

Fixed Assets are depreciated at the rates mentioned below:Particulars Rate ModeFurniture and Fixtures 10.00% WDV

Office Equipments 15.00% WDV

Office Vehicles 20.00% WDV

Own Premises 5.00% WDV

Computer Hardware & Software 33.33% Straight Line

Capital Expenditure on Electrical Fittings and

Rented Premises and civil work

25.00% Straight Line

7) Employee Benefits:i) The liability towards gratuity is calculated and paid every year to L.I.C. of

India as Employees Group Gratuity Scheme assessed on actual valuation.

ii) Bank’s Contribution towards provident fund is paid every month to

Commissioner of Provident Fund on the basis of Employees Provident Fund

Scheme, 1952 and Employees Pension Fund Scheme, 1995.

iii) The liability towards leave encashment is calculated and paid every year

to L.I.C. of India as Group leave encashment scheme assessed on actual

valuation

sr. No

Particulars Gratuity (Funded) 31.03.2012

1. Discount rate 8%2. Expected Return on plan assets 8%3. salary escalation rate 5%4. Reconciliation of opening and closing balance of

the present value of the defined benefit obligation:i) Present value of obligation as at 01-04-2011 579.52

ii) Interest cost 46.36

iii) Current service cost 45.01

iv) Benefits paid (42.20)

v) Actuarial gains/(loss) on obligations 53.58

vi) Present value of obligation as at 31-03-2012 682.27

30

5. Reconciliation of opening and closing balance of fair value of fair plan assets:i) Fair value of plan assets as at 01-04-2011 554.11

ii) Expected return on plan assets 52.12

iii) Contributions 30.89

iv) Benefits paid (42.20)

v) Actuarial gain/(loss) on plan assets Nil

vi) Fair value of plan assets as at 31-03-2012 594.92

6. Amount recognized in Balance sheeti) Present value of obligations as at 31-03-2012 682.27

ii) Fair value of Plan Assets as at 31-03-2012 594.92

iii) Assets/liability as at 31-03-2012 87.35

7. Expenses recognized in Profit and Loss Accounti) Current service cost 45.01

ii) Interest cost 46.36

iii) Return on planned Assets (52.12)

iv) Net actuarial gain/(loss) 53.58

8. Expenses recognized in Profit & Loss Account 92.83

8) Taxation:

i) Tax expense comprises both deferred and current taxes. Deferred Income Tax reflects the impact of current year timing differences between taxable income and accounting income for the year and reversal of timing differences of earlier years.

ii) Deferred Tax is based on tax rates and the tax laws effective at the Balance Sheet date.

iii) Deferred Tax Assets are recognized only to the extent that there is reasonable certainty that sufficient future taxable income will be available against which

such Deferred Tax Assets can be realized.

9) segment Reporting:

In accordance with the guidelines issued by RBI, Segment Reporting is made as under:i) Treasury includes all investment portfolio, profit/loss on sale of investments,

profit/loss on foreign exchange transactions, equities and money market operations. The expenses of this segment consist of interest expenses on funds borrowed from external sources as well as internal sources and depreciation/ amortization of premium on Held to Maturity category investments.

ii) Other Banking Operations include all other operations not covered under

Treasury operations.

Annual Report 2011-12

31

10) Reserve Fund And Other Reserves:

As per the requirement of Multi-State Co-op. Soc. Act, 2002, the Statutory Reserve Fund has been bifurcated into 3 Categories viz.

a) Regular Statutory Reserve (comprising 25% of Net Profit)

b) Contingency Reserve Fund (comprising 10% of Net Profit)

c) Co-operative Education Fund maintained by National Co-operative Union of India (comprising 1% of Net Profit)

d) Charity Fund (comprising 1% of Net Profit)

Dividend and Stale Demand Drafts remaining unclaimed over 3 years are transferred to Statutory Reserve Fund. Nominal Membership and Entrance Fees are transferred to Statutory Reserve Fund every year. Amounts under pay-orders

remaining unclaimed for over 3 years are transferred to General Reserve Fund.

11) Impairment Of Assets (Accounting standard 28):

An asset is treated as impaired when the carrying cost of asset exceeds its recoverable value. An impairment loss is charged to profit and loss account in the year in which an asset is identified as impaired. The impairment loss recognized in prior accounting period is reversed if there has been a change in the estimate of

recoverable amount.

12) Provisions, Contingent Liabilities And Contingent Assets:

A provision is recognized when the Bank has a present obligation as a result of past event where it is probable that an outflow of resources will be required to settle the obligation, in respect of which a reliable estimate can be made. Provisions are not discounted to its present value and are determined based on best estimate required to settle the obligation at the balance sheet date. These are reviewed at each balance sheet date and adjusted to reflect the current best estimates.

When there is a possible or a present obligation in respect of which the likelihood of outflow of resources is remote, no provision or disclosure is made.

Contingent assets are not recognized in the financial statements. However, contingent assets are assessed continually and if it is virtually certain that an inflow of economic benefits will arise, the asset and related income are recognized

in the period in which the change occurs.

III. Notes Forming Part of the Accounts for the year ended 31st March 2012.

1) Prior Period Items (Accounting standard 5): There are no items of material significance in the prior period account requiring

disclosure.

32

2) Fixed Asset And Depreciation (Accounting standard 6 And Accounting standard 10)

The Bank has accounted and made disclosure of gross and net block of fixed assets and depreciation in accordance with AS-6 and AS-10 issued by ICAI.

3) The Disclosure under Accounting standard 17 on “segment reporting” issued by ICAI is as follows:

(` in lacs)

Particulars Treasury Other banking operations

Total 31/03/2012

Revenue 7442.20 35285.79 42727.99

Result 1428.48 4588.67 6017.15

Unallocated Expenses 0.00

Profit before Tax 6017.15

Income Tax 2143.90

Net Profit After Tax 3873.25

Other Information

Segment Assets 124288.32 288583.00 412871.32

Unallocated Assets 2249.74

Total Assets 415121.06

Segment Liabilities 13332.90 354242.78 367575.68

Unallocated Liabilities 47545.38

Total Liabilities 415121.06

i) The Bank is organized into two main business segments, namely:

• Treasury primarily comprising of Dealing Room operations, trading/investments in Bonds and Government securities and Foreign exchange.

• Other Banking Operations primarily comprising of Loans and Advances to Corporate, and retails loans & advances to customers.

ii) The above segments are based on the currently identified segments taking into account the nature of services provided, the risks and returns, overall organization structure of the Bank and the internal financial reporting system.

iii) Segment revenue, results, assets and liabilities include the respective amounts identifiable to each of the segments and amounts apportioned/allocated on a reasonable basis.

4) Related Parties And Disclosure (Accounting standard 18): The Bank is a Co-operative Society under the Multi-State Co-operative Societies Act,

Annual Report 2011-12

33

2002 and there are no related parties requiring a disclosure under Accounting Standard 18 (AS-18) issued by The Institute of Chartered Accountants of India, other than one Key Management Personnel, viz. Mr. Joy K Thomas, Chief Executive Officer of the Bank. However in terms of RBI circular dated March 29, 2003, he being single party

coming under the category, no further details thereon need to be disclosed

5) Lease Rents (Accounting standard 19):

The bank has cancellable operating leases and the disclosures under AS 19 on

‘Leases’ issued by ICAI are as follows:

i) Lease rent (inclusive of municipal taxes and compensation) payments of

` 866.58 lacs have been recognized in the statement of profit and loss for the

year ended March 2012.

ii) The lease agreements entered into pertain to use of premises at the branch.

The lease agreements do not have any undue restrictive or onerous clauses

other than those normally prevalent in similar agreement regarding use of

assets, lease escalations, renewals and a restriction on sub-leases.

6) Details of loans subjected to restructuring during the year ended March 31, 2012 are given below:

sr. No

Particulars

1. Standard advances

Restructured

No. of Borrowers

Amount outstanding

3

7.29 lacs

2. Sub-standard advances

restructured

No. of Borrowers

Amount outstanding

-

-

3. Doubtful advances

Restructured

No. of Borrowers

Amount outstanding

-

-

Total Advances

Restructured

Total No. of Borrowers

Total Amount outstanding

3

7.29 lacs

These restructured loans have continued to remain in standard category during the

year 2011-12.

7) Accounting For Taxes On Income (Accounting standard 22):

i) The major components of Deferred Tax Assets/Liabilities (net) arising on

account of timing differences between book profit and taxable profits as at

March 31, 2012 are as follows:

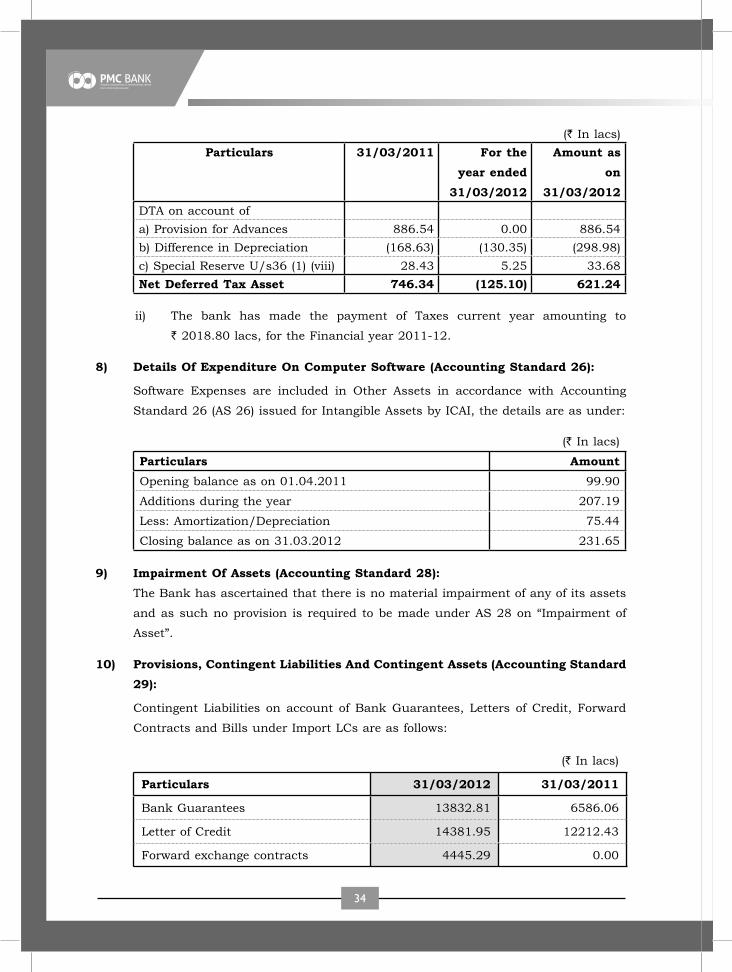

34

(` In lacs)Particulars 31/03/2011 For the

year ended 31/03/2012

Amount as on

31/03/2012DTA on account ofa) Provision for Advances 886.54 0.00 886.54b) Difference in Depreciation (168.63) (130.35) (298.98)c) Special Reserve U/s36 (1) (viii) 28.43 5.25 33.68Net Deferred Tax Asset 746.34 (125.10) 621.24

ii) The bank has made the payment of Taxes current year amounting to

` 2018.80 lacs, for the Financial year 2011-12.

8) Details Of Expenditure On Computer software (Accounting standard 26):

Software Expenses are included in Other Assets in accordance with Accounting

Standard 26 (AS 26) issued for Intangible Assets by ICAI, the details are as under:

(` In lacs)

Particulars AmountOpening balance as on 01.04.2011 99.90

Additions during the year 207.19

Less: Amortization/Depreciation 75.44

Closing balance as on 31.03.2012 231.65

9) Impairment Of Assets (Accounting standard 28): The Bank has ascertained that there is no material impairment of any of its assets

and as such no provision is required to be made under AS 28 on “Impairment of

Asset”.

10) Provisions, Contingent Liabilities And Contingent Assets (Accounting standard 29):

Contingent Liabilities on account of Bank Guarantees, Letters of Credit, Forward

Contracts and Bills under Import LCs are as follows:

(` In lacs)

Particulars 31/03/2012 31/03/2011

Bank Guarantees 13832.81 6586.06

Letter of Credit 14381.95 12212.43

Forward exchange contracts 4445.29 0.00

Annual Report 2011-12

35

IV) DIsCLOsURE As PER RBI GUIDELINEs

Amount in Lacs

s r . No.

Particular 31.03.2012 31.03.2011

1 Capital to Risk Asset Ratio(CRAR) 13.28% 13.23%

2 Movement of CRAR

a) Total Capital Funds 34328.61 24692.29

b) Risk Weighted Assets 258515.53 186690.68

3 Investments

a) Face Value 82,407.76 65,711.51

b) Book Value 81,631.07 67,027.94

c) Market Value 77,507.06 62,718.36

4 Advances against Real Estate, Construction

Business, Housing

37,734.11 34,373.57

5 Advances against Shares & debenture 2.94 4.46

Advances of ` 2,52,330.22 Lacs (Previous year ` 2,07,987.58 Lacs) shown in the Balance

Sheet includes:s r . No.

Particular 31.03.2012 31.03.2011

Fund Basedi) Advance to Directors. Nil Nil

ii) Advances to Relatives of Directors &

Companies/ firms in which they are

interested

3.94 4.48

iii) Advances to Managing Director (Mr. Joy

Thomas)

3.95 4.26

Non- Fund Basedi) Advance to Directors. Nil Nil

ii) Advances to Relatives of Directors &

Companies/ firms in which they are

interested

Nil Nil

iii) Advances to Managing Director (Mr. Joy

Thomas)

Nil Nil

6 Average Cost of Deposits 7.70% 6.67%

7 i) Gross NPAs 2,570.54 4,106.31

ii) Net NPAs 391.40 957.00

36

s r . No.

Particular 31.03.2012 31.03.2011

8 Movement in NPA

Opening Balance 4,106.31 4,802.19

Add : Additions during the year 986.33 2,671.73

Less : Closed/ Recovered /Written off 2,522.10 3,367.61

Closing Balance 2,570.54 4,106.31

9 Interest income as a percentage of working

funds

9.62% 8.66%

Non- Interest income as a percentage of

working funds

0.67% 0.91%

Operating profit as a percentage of working

funds

1.45% 1.17%

Return on Assets (Net Profit(Before Tax) /

Average of working funds)

1.63% 1.29%

Return on Assets (Net Profit(After Tax) /

Average of working funds)

1.05% 0.94%

Business (Deposits+Advances) per employee 685.28 656.05

Profit per employee (Before Tax) 6.94 5.31

Profit per employee (After Tax) 4.47 3.90

10 Provision on NPAs required to be made 1,430.84 2,390.31

Provision on NPAs actually made 2,073.66 2,948.72

Additional provision from last years profit 0.00 0.00

Provisions required to made for Overdue

interest taken into income

105.48 200.59

Provision actually made for Overdue

interest taken into income

105.48 200.59

11 Provision required to be made on

depreciation in investments

958.10 652.24

Provision actually made on Depreciation in

Investments

958.10 652.24

Provision made towards Price Fluctuation

Reserve

Nil Nil

12 Provisions required to be made for Inter -

Branch Account

Nil Nil

Provision actually made for Inter - Branch

Account

Nil Nil

Annual Report 2011-12

37

s r . No.

Particular 31.03.2012 31.03.2011

Provisions required to be made for Inter -

Bank Account

Nil Nil

Provision actually made for Inter - Bank

Account

Nil Nil

13 Towards NPAsOpening Balance 2,948.72 3,887.98

Add: Additions during the year

Fresh Provisions 333.82 901.58

Additional provisions from last years profit 0.00 0.00

Less : Closed / Recovered /Written Off 1,851.70 2,399.25

Provision Required to be made 1,430.84 2,390.31

Bad & Doubtful Debts Provision actually

made

2,073.66 2,948.72

Towards standard AssetsOpening Balance 832.00 776.32

Add: Additions during the year 180.00 55.68

Additional provisions from last years profit 0.00 0.00

Closing Balance 1,012.00 832.00

Towards Overdue Interest taken into incomeOpening Balance 200.59 170.07

Add: Additions during the year 46.35 90.47

Less : Reduction during the year 141.46 59.95

Closing Balance 105.48 200.59

14 Towards Depreciation on InvestmentsOpening Balance 2,471.07 2,036.66

Add: Additions during the year 334.29 434.41

Less : Reduction during the year 1,389.37 0.00

Closing Balance 1,415.99 2,471.07

Towards Investments Fluctuation ReserveOpening Balance 2,211.64 1,911.64

Add: Additions during the year 300.00 300.00

Closing Balance 2,511.64 2,211.64

15 Payment of insurance premium to the DICGC,

281.39 253.16

including arrears, if any

38

16 Composition of Non - sLR Investments. (31st March 2012)

sr. No.

Issuer Amount Extent of below

Investment grade

securities

Extent of ‘unrated

securities’

Extent of ‘unlisted’ securities

1 PSUs 1506.50 Nil Nil Nil

2 Fls 0.00 Nil Nil Nil

3 Public & Private Banks 0.00 Nil Nil Nil

4 Others 301.49 Nil Nil

5 Provision held towards

depreciation

Nil Nil Nil Nil

TOTAL 1807.99 Nil Nil Nil

17. Non Performing Non - sLR Investments NIL

18. Previous years figures have been regrouped / re-arranged wherever necessary to conform to the presentation of the accounts of the current year.

As per our Report of even date attachedFor D.B.Ketkar & Co s. Charanjit singh ChadhaChartered Accountants Chairman

s.G.Khare s. Waryam singhPartner Vice ChairmanMembership No. 36680Statutory Auditors shri. Joy ThomasDate: 31st May 2012 Managing Director

DirectorsS. Resham Singh S. Balbir Singh Kochhar S. Surjit Singh NarangS. Daljit Singh Bal S. Joginder Singh Palla S. Surjit Singh AroraS. Rajneet Singh Shri. Jagdish Mookhey S. Gurnam Singh HothiSmt. Trupti Bane Smt. Parmeet Sodhi S. Jasvinder Singh BanwaitShri. Brij Bhushan Handa Smt. Mukti Bavisi

Annual Report 2011-12

39

CAsH FLOW sTATEMENT FOR THE YEAR ENDED 31sT MARCH, 2012

(` in Lacs)

Particulars31.03.2012 31.03.2011

Amount Amount Amount AmountA) Cash Flow from Operating ActivitiesInterest, Commission &

Exchange etc

40,367.34 29,764.03

Interest payments (25,228.50) (18,059.97)Payments to Employees &

Others

(3,564.29) (3,178.77)

Other payments (3,774.68) (2,916.58)Other receipts 1,238.89 817.86 Operating profit before changes in operating assets

9,038.76 6,426.57

Increase / Decrease in operating assetsFunds advanced to customers (44,342.64) (21,580.81)Purchase of investments (12,285.88) (16,610.12)Other assets (2,819.86) (473.94)Proceeds from sale of

Investments

362.50 229.93

Increase / Decrease in operating liabilitiesDeposits from customers 59,067.42 28,709.81 Other liabilities (8,091.03) 8,490.91 Net Cash Flow from Operating Activities

929.27 5,192.35

B) Cash Flow from Investing ActivitiesDividend received 1.17 2.39 Purchase of fixed assets (3,712.83) (1,498.83)Net Cash Flow from Investing Activities

(3,711.66) (1,496.44)

40

(` in Lacs)

Particulars31.03.2012 31.03.2011

Amount Amount Amount AmountC) Cash Flow from Financing ActivitiesIncrease / Decrease in Share

Capital

563.06 1,656.40

Increase / Decrease in Reserves 15.61 0.25 Payment of Dividend (838.35) (531.02)Increase / Decrease in

Borrowings

4,385.54 (1,052.64)

Net Cash Flow from Financing Activities

4,125.86 72.99

1,343.47 3,768.90 Net Increase in Cash & Equivalents

1,343.47 3,768.90

Cash & Cash Equivalents at the

beginning of the year

21,642.92 17,874.02

Cash & Cash Equivalents at the

end of the year

22,986.39 21,642.92

Notes to the Cash Flow statements

31.03.2012 31.03.2011

Cash 1,444.45 1,700.62 Balance with RBI 20,082.71 18,973.13 Balance with Other Banks 1,459.23 969.17 Cash & Cash Equivalents as re-stated

22,986.39 21,642.92

As per our Report of even date attachedFor D.B.Ketkar & Co s. Charanjit singh ChadhaChartered Accountants Chairman

s.G.Khare s. Waryam singhPartner Vice ChairmanMembership No. 36680Statutory Auditors shri. Joy ThomasDate: 31st May 2012 Managing Director

Annual Report 2011-12

41

AMENDMENT TO BYE-LAWs

We propose the following amendment in the Bye-laws of our Bank.

Bye – law no.