Annual Report 2002 - E+S Rück · Gräber Dr. Pickel Arrago Zeller Chairman of the Executive Board...

62

e+s rück Annual Report 2002

Transcript of Annual Report 2002 - E+S Rück · Gräber Dr. Pickel Arrago Zeller Chairman of the Executive Board...

e+s rück

Annual Report 2002

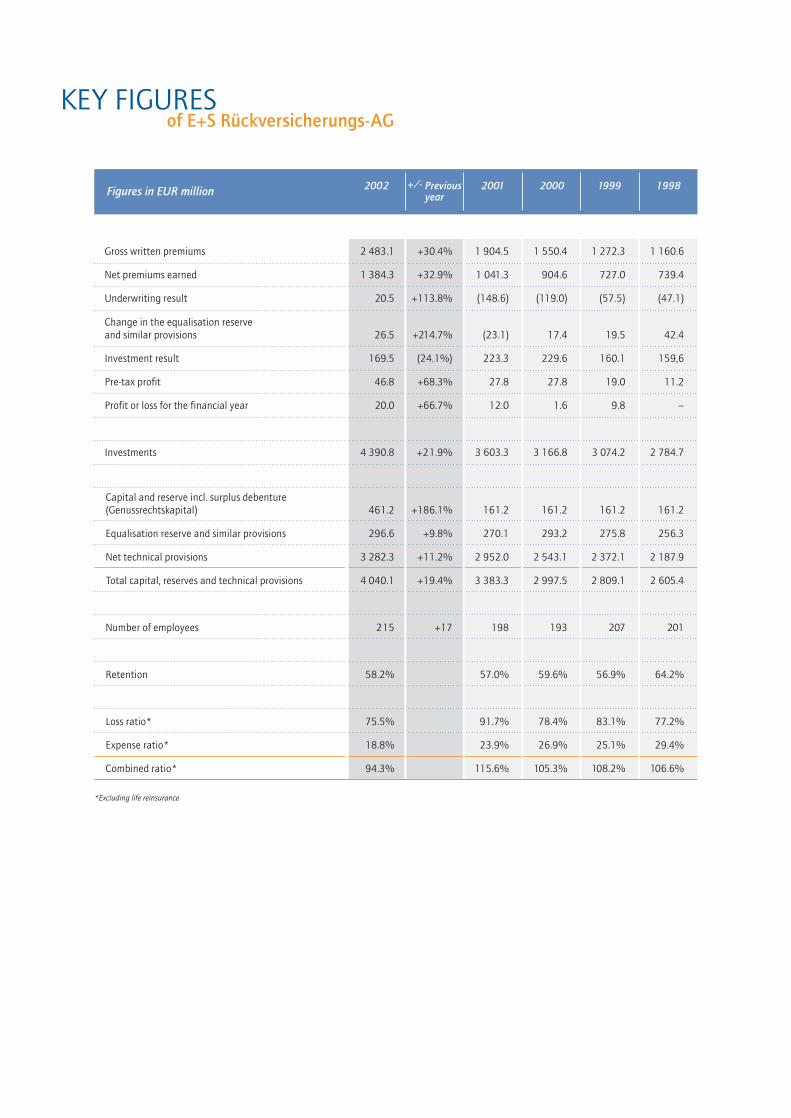

KEY FIGURESof E+S Rückversicherungs-AG

2002 +/- Previous 2001 2000 1999 1998year

Gross written premiums 2 483.1 +30.4% 1 904.5 1 550.4 1 272.3 1 160.6

Net premiums earned 1 384.3 +32.9% 1 041.3 904.6 727.0 739.4

Underwriting result 20.5 +113.8% (148.6) (119.0) (57.5) (47.1)

Change in the equalisation reserve and similar provisions 26.5 +214.7% (23.1) 17.4 19.5 42.4

Investment result 169.5 (24.1%) 223.3 229.6 160.1 159,6

Pre-tax profit 46.8 +68.3% 27.8 27.8 19.0 11.2

Profit or loss for the financial year 20.0 +66.7% 12.0 1.6 9.8 –

Investments 4 390.8 +21.9% 3 603.3 3 166.8 3 074.2 2 784.7

Capital and reserve incl. surplus debenture (Genussrechtskapital) 461.2 +186.1% 161.2 161.2 161.2 161.2

Equalisation reserve and similar provisions 296.6 +9.8% 270.1 293.2 275.8 256.3

Net technical provisions 3 282.3 +11.2% 2 952.0 2 543.1 2 372.1 2 187.9

Total capital, reserves and technical provisions 4 040.1 +19.4% 3 383.3 2 997.5 2 809.1 2 605.4

Number of employees 215 +17 198 193 207 201

Retention 58.2% 57.0% 59.6% 56.9% 64.2%

Loss ratio* 75.5% 91.7% 78.4% 83.1% 77.2%

Expense ratio* 18.8% 23.9% 26.9% 25.1% 29.4%

Combined ratio* 94.3% 115.6% 105.3% 108.2% 106.6%

*Excluding life reinsurance

Figures in EUR million

1 Address of the Executive Board

4 Boards and officers

6 Executive Board

8 Management report

8 Economic climate

9 Business development

11 Premium growth and results

20 Investments

22 Risk report

25 Human resources report

26 Outlook

27 Affiliated companies

28 Other information

28 Capital, reserves, and technical provisions

28 Proposal for the distribution of profits

29 Accounts of E+S Rückversicherungs-AG

30 Balance sheet as at 31 December 2002

34 Profit and loss account for the 2002 financial year

36 Notes

39 Notes on assets

43 Notes on liabilities

47 Notes on the profit and loss account

51 Auditors' report

52 Report of the Supervisory Board

54 Glossary

CONTENTS

1

Dear clients and shareholders of E+S Rück,

We are pleased to report that E+S Rück enjoyed another successful financial year.

In 2002 we were highly successful in further expanding our position as a profitablespecialist reinsurer for the German market.

With a market share now in excess of 8% we are the third-largest reinsurer in theworld’s second-largest non-life reinsurance market, while at the same time we assertour position as the second-largest reinsurer in the German life reinsurance market.In the recent renewal season the German reinsurance market in general and E+SRück in particular have enjoyed a marked resurgence. Against this backdrop, however,a number of renowned market players discontinued their business activities – forreasons that are explained in greater detail below. This led to a capacity shortageon the German reinsurance market, from which we were able to profit – not leastthanks to our "AA" rating confirmed last year by Standard & Poor’s. We made themost of the market situation, enlarging existing accounts and acquiring numerousnew clients. Thanks to our selective underwriting policy in property and casualtyreinsurance – focusing on non-proportional covers – and the attractive terms andconditions under which we wrote new business, we succeeded in substantially en-hancing the profitability of our portfolio. The combined ratio of 94.3% speaks foritself.

We were highly satisfied with the performance of life and health reinsurance. Inthe German market we now rank among the most prominent life reinsurers. With a volume of EUR 727.2 million life reinsurance business accounts for around one-third of our total gross premium income. Our experienced team of health professionalsin the life sector offers our clients comprehensive product development support aswell as advice on assessing claims and benefits. In the year under review we cooper-ated with clients as part of a product partnership to develop an innovative productin the field of personal accident insurance with assistance benefits for senior citizens.

The development of capital markets was less favourable, and our portfolio, too, wasnot left unscathed. Although regular income increased due to the growth in the in-vestment portfolio, the total investment result fell short of our planned targets dueto write-offs on our equity portfolio.

Despite exceptional loss burdens – the insurance industry suffered a previously unparalleled accumulation of natural catastrophes in the year under review – andthe strained state of the capital markets, we closed the year just-ended with an excellent result. We are pleased once again to have generated a remarkable profitfor the financial year, which we shall distribute to our shareholders.

1

In order to safeguard our excellent rating on a long-term basis, we responded toour growth by significantly strengthening our capital and reserves to EUR 4.0 billion in December 2002 through a capital increase of EUR 300.0 million.

We would like to take this opportunity to thank our shareholders for their uncondi-tional support and the confidence that they have shown in our business policy.

Quite apart from the implications of the disastrous flooding of 2002 for our under-writing account, our staff were also greatly distressed by the associated humansuffering. We therefore immediately launched an appeal in which the companydoubled the donations made by our employees. We hope that in this way we playedat least a small part in alleviating this tragedy.

During the past two years of crisis for the reinsurance industry we have demonstratedthat we are a partner on whom you can rely – not only in fair weather but also intimes of extraordinarily heavy loss burdens. Our proven business policy and notleast the motivation and commitment of our staff and management team will ensurethat this success is sustained in the future.

We look forward to continuing our successful cooperation.

Yours sincerely,

2

Gräber

Dr. Pickel Arrago

Zeller Chairman of the Executive Board

Dr. König

Wallin

Dr. Becke

4

Wolf-Dieter Baumgartl Chairman of the Board of Management of Hannover HDI Haftpflichtverband derChairman Deutschen Industrie V.a.G.

Gerd Kettler Chairman of the Executive Board ofMünster LVM Landwirtschaftlicher Versicherungs-Deputy Chairman verein Münster a.G.

Manfred Bieber*Hannover

R. Claus Bingemer Former Chairman of the Executive BoardsHannover of Hannover Rückversicherungs-AG,(until 19 April 2002) E+S Rückversicherungs-AG

Dr. Heinrich Dickmann Chairman of the Executive Board ofBurgwedel Vereinigte Haftpflichtversicherung V.a.G.

Dr. Heiner Feldhaus Chairman of the Executive Board ofHannover CONCORDIA Versicherungs-Gesellschaft a.G.(since 19 April 2002)

Herbert K. Haas Member of the Board of Management of Burgwedel HDI Haftpflichtverband der (since 19 April 2002) Deutschen Industrie V.a.G.

Frauke Heitmüller*Hannover(since 19 April 2002)

Ass. jur. Tilman Hess*Hannover

Rolf-Peter Hoenen Speaker of the Executive Boards ofCoburg HUK-Coburg Versicherungsgruppe

Dr. Ing. Manfred Mücke Chairman of the Executive Boards ofHamburg - KRAVAG-SACH VaG,(until 19 April 2002) - KRAVAG-LOGISTIC Versicherungs-AG

Member of the Executive Board of- R+V Versicherung AG- R+V Allgemeine Versicherung

Anita Suing-Hoping*Godshorn(until 19 April 2002)

Supervisory Board (Aufsichtsrat)

*Staff representative

BOARDS AND OFFICERSof E+S Rückversicherungs-AG

5

Dr. Edo Benedetti President of the Trento ITAS Istituto Trentino-Alto Adige

per Assicurazioni, Trento, Italy

Wolfgang Bitter Chairman of the Executive Board of Itzehoe Itzehoer Versicherungsverein –

Brandgilde von 1691 VVaG

Dieter Holl Chairman of the Executive Board ofStuttgart Württembergische Gemeinde-Versicherung a.G.

Ernst Köller General Director and chairman of the Hannover Executive Board of (until 19 April 2002) CONCORDIA Versicherungs-

Gesellschaft a.G.(until 28 February 2002)

Dr. Erwin Möller Member of the Board of Management of Hannover HDI Haftpflichtverband der

Deutschen Industrie V.a.G.and Talanx AG(until 28 February 2002)

Adolf Morsbach Former Chairman of the Board of ManagementWedemark of HDI Haftpflichtverband der (until 19 April 2002) Deutschen Industrie V.a.G.

Advisory Board (Beirat)

Boards and officers Advisory Board

6 E+S_englisch 05.05.2003 + xx.xx Uhr

André Arrago

Property and Casualty Treaty ReinsuranceArab, European Romance and LatinAmerican countries, Northern and Eastern Europe, Asia and Australasia

Dr. Wolf Becke

Life and Health markets worldwide

Wilhelm ZellerChairman

Controlling, Internal Auditing, Investor Relations, Public Relations,Corporate Development; Human Resources; Underwriting & Actuarial Services; Program Business

EXECUTIVE BOARDof E+S Rückversicherungs-AG

Dr. Elke König

Finance and Accounting, Asset Management; Information Technology;Facility Management

Dr. Michael Pickel

Property and Casualty TreatyReinsurance Germany, Austria, Switzerland and Italy; Credit and Bonds worldwide; Claims Management; Legal Department

Ulrich Wallin

Specialty Division (worldwide FacultativeBusiness; worldwide Treaty and FacultativeBusiness Marine, Aviation and Space);Property and Casualty Treaty ReinsuranceGreat Britain and Ireland; Retrocessions

Herbert K. Haas(until 31 January 2002)

Jürgen Gräber

Coordination of entire Non-Life Reinsurance; Property andCasualty Treaty ReinsuranceNorth America and English-speaking Africa; FinancialReinsurance worldwide

Boards and officers Executive Board

8

Economic climate

The global economic situation was over-shadowed by considerable uncertainty in 2002.Slumps on equity markets towards the middle ofthe year, political uncertainties including specu-lations about a war on Iraq, and the fear of furtherterrorist attacks had a paralysing effect and damp-ened consumer habits.

After brightening up at the beginning ofthe year, the economic climate began to cloudover again in the second half of the year. Sup-ported by an expansionary fiscal policy, the USFederal Reserve Board sought to avert the loomingrecession in the United States with massive inter-est cuts. In the United Kingdom full employmentand a sustained low rate of inflation contributedto respectable economic growth. Economic ac-tivities in the Asian emerging and developingnations promoted cyclical growth in the globaleconomy. It was only in the European economicarea that the expansion of production outputlagged behind. An unusually sharp rise in foodprices early in the year, a sense of insecurity as-sociated with the launch of euro notes and coins

The German insurance industry

The state of the capital markets, the strainsimposed by natural catastrophes, and the tenseeconomic and political situation adversely im-pacted the outcome of the 2002 financial year.Despite this difficult environment, the Germaninsurance industry was able to maintain its ex-pansionary course of the previous years. For theyear under review the German Insurance Asso-ciation (GDV) expects premium volume to growby 4.0% (previous year: 2.7%) to EUR 140.8billion (EUR 135.4 billion). Benefits and claimsexpenditure increased in the year under review byroughly 6.0% to EUR 158.1 billion (EUR 149.5billion).

The poor performance of the capital marketshit life insurers especially hard. Falling prices onequity markets and a low interest rate level onbond markets caused considerable problems at

numerous companies. Surplus distributions hadto be cut again market-wide. In several cases theFederal Financial Supervisory Authority (BAFin)had to intervene in proceedings, usually behindthe scenes.

Life insurance nevertheless proved to be ahigh-growth line. The structural reform of the pen-sion system implemented by the Federal Gov-ernment was a particularly crucial factor in thisgratifying development. While the sales figuresactually recorded fell short of forecasts, the "Ries-ter effect" was still reflected in a 4.5% rise inpremium income. In the first half-year of 2002the number of new annuity and pension insur-ance policies increased by more than 250%.

Property and casualty insurers generatedpremium increases for the third year in succession.

and – as the year progressed – the upward re-valuation of the euro were a drag on economicgrowth in Europe. The European Central Bankwas initially cautious in its response to the inter-est rate cuts in the USA, waiting until Decemberto trim the prime rate by 50 basis points.

In Germany, contrary to expectations, theupswing failed to gather momentum and fellshort of the forecasts made by leading economicresearch institutes. The primary factor here wasthe depressed state of the domestic economy.Private consumption was extremely weak duringthe past year, not least influenced by dubiousassessments of Germany’s economic future. Cap-ital spending in the industrial sector – on machin-ery and equipment as well as buildings – wasparticularly soft throughout the year. The weakstate of the German business climate was clearlyreflected on the labour market, where unemploy-ment surpassed 4 million as the year progressed.

Economic growth in

Germany fell short of

expectations

German insurance

industry continued its

expansionary course

despite weak economy

Growth in annuity and

pension insurance

products through the

”Riester effect”

MANAGEMENT REPORTof E+S Rück

9

However, a combined ratio of around 100% high-lights the marked pressure on profit margins.Claims expenditure climbed by 8.2% (0.9%) inthe financial year to EUR 43.5 billion. This risewas due to a tightening of liability law, severalnatural catastrophes, and further major claims.

Motor insurance, the growth driver of theindustry prior to the turn of the year, lagged be-hind the gains of the previous year. Hopes ofbeing able to further trim the underwriting def-icit in the year under review were not fulfilled.Numerous storms and the disastrous floodingin August of 2002 had a significant adverse im-pact on the result; own damage insurance wasmost heavily hit. Despite the natural catastrophes,the underwriting loss in the order of EUR 0.5billion was on a par with the relatively low levelof the previous year.

The prolonged premium decline in industrialproperty insurance was halted in the year underreview. What is more, the positive premium trendof the previous year was appreciably enhancedin the year under review. Premium income is ex-pected to climb by 11.2% to roughly EUR 3.4billion. However, the consequences of the flood-ing on the Elbe and the Danube caused claimsexpenditure to rise sharply, and industrial busi-ness therefore closed with an underwriting deficit.

The appreciable hardening on the reinsur-ance market, which had already manifested itselfin 2001, was sustained in the year under review.One prominent development was the cessationof underwriting activities by a major German

competitor. Additional reserves constituted forasbestos-related claims and write-downs on in-vestments pushed more than a few marketplayers into the red again. Highly reputed mar-ket players were downgraded by the ratingagencies. One consequence of this market de-velopment was also reflected in the treatystructuring; it became increasingly common torequire provision of security for loss reserves. Asa general rule, reinsurers with good ratings weresought-after partners.

The floods in August clearly demonstratedthat such risks had not been adequately priced.The German Insurance Association (GDV) conse-quently developed insurance software for pricingnatural catastrophes, the "Zoning System forFlooding, Backwater and Heavy Rainfall" (ZÜRS),which can be used to retrieve flood risks for Ger-many on an individual risk basis. There are plansto enhance the program in cooperation with anumber of reinsurers so that it can be used toprecisely assess accumulation risks.

Property insurance experienced a changewith respect to the coverage of terrorism losses.While terrorism coverage for major risks was ex-cluded, the state felt compelled to become in-volved in providing insurance for terrorism risks.This led to the establishment of Extremus AG, aspecialist insurer for terrorism covers, which re-ceives reinsurance support from our company.

Motor line heavily im-

pacted by disastrous

flooding; underwriting loss

nevertheless relatively low

In response to the

disastrous flooding

insurance software

"ZÜRS" developed for

pricing risks

Extremus AG established

as a specialist reinsurer

for terrorism covers

E+S Rück again

increased gross

premium volume

Management report business development

Business development

An accumulation of natural catastrophes inGermany during the year under review impactedunderwriting results throughout the entire insur-ance and reinsurance industry, in some cases to asignificant extent. The Czech Republic and easternparts of Germany suffered flooding on a hithertounseen scale. However, the good diversificationof our portfolio, not least thanks to internationalrisk spreading with Hannover Re, ensured that

these natural disasters did not materially impairour results.

In the year under review we again substan-tially enlarged our premium volume: gross pre-mium income increased by 30.4% to EUR 2.5billion, while net premiums earned climbed by32.9% to EUR 1.4 billion. This growth derivedfrom the expansion of both property/casualty

10

and life reinsurance. Gross premium income in thelatter line grew by EUR 177.2 million to EUR727.2 million, primarily due to the successfulsale of annuity products. The general premiumincreases and the enlargement of our marketshare ensured a favourable business develop-ment.

The premium income from our total portfolioof property and casualty reinsurance amountedto EUR 1,755.8 million. This corresponds to 70.7%of the total gross premium volume.

In motor reinsurance, one of our largest linesby premium volume, we built upon the favourablepremium situation of the previous year: premiumsgrew by 10% to EUR 506.9 million (previousyear: EUR 461.5 million). The substantial claimsburden in own damage business due to theflooding affected not only insurers but also ourportfolio and impacted the underwriting result.

The rehabilitation measures initiated 18months ago in industrial fire and liability insur-ance left a favourable mark on the result for thefirst time. This success was, however, diminishedby the disastrous flooding in the summer.

With a slightly increased retention of 58.2%,our total net premiums grew in the year underreview to EUR 1.4 billion. Net loss expenditureamounted to EUR 855.8 million in the year underreview (EUR 838.6 million), while the loss ratioexcluding life insurance improved to 75.5%(91.7%) – the lowest level in the last five years.

Operating expenses, consisting of commis-sions and profit commissions as well as our ownadministrative expenses, were reduced in theyear under review by EUR 11.4 million to EUR257.9 million on a net basis. We transformedthe previous year’s underwriting loss of EUR148.6 million before changes in the equalisation

Management report business development

Technical provisionsCapital, reserves and technical provisions Net premiums

Capital and reserves (excl. disposable profit)

Growth in capital, reserves, technical provisions and in net premiums

in EUR million

1500

2000

2500

3000

1000

500

0

3500

4000

19941995

19961997

19981999

20002001

19932002

Equalisation reserve and similar provisions

Life reinsurance was one

of the strongest lines in

terms of premium volume

1111

reserve into a profit in the year under review. Thenet underwriting result before changes in theequalisation reserve improved by EUR 169.1 mil-lion to a gratifying EUR 20.5 million. An amountof EUR 26.5 million was allocated to the equal-isation reserve due to the favourable loss experi-ence.

We also strengthened the IBNR reserve inthe year under review with an allocation ofroughly EUR 54.0 million.

The run-off of our liability treaties confirmedthat we have a comfortable level of reserves. Inthe area of asbestos-related claims – which is inany case scarcely of significance to our company– there was also no need to establish additionalreserves.

The adverse state of the capital markets leftits mark on our investment result, too. While in-vestment income fell to EUR 241.3 million (EUR259.1 million), expenditure increased by EUR 35.9million to EUR 71.8 million; the investment re-sult consequently deteriorated by EUR 53.7 mil-lion to EUR 169.5 million. This unsatisfactory de-cline was primarily attributable to write-downson our investment portfolio.

After higher tax expenditure of EUR 26.8million (EUR 15.8 million), we boosted our profitfor the financial year from EUR 12.0 million to agratifying EUR 20.0 million.

The substantial increase of 30.4% in ourgross written premiums to EUR 2.5 billion can beattributed to the market developments as wellas to our business policy: On the one hand, thenational and international market conditionsimproved, while on the other hand we were ableto profitably enlarge both the German portfoliothat we write ourselves and the foreign businessaccepted from Hannover Re. We assume the latterunder an internal retrocession agreement thatenables us – by adding foreign risks – to signifi-cantly improve the geographical spread and riskdiversification of our portfolio across all lines ofbusiness.

Given the general circumstances outlinedabove, the development of our portfolio washighly satisfactory. With a profit of EUR 20.5 mil-lion we were able for the first time to restore theunderwriting result to positive territory.

Trend reversal in the

underwriting result

achieved in the year

under review

Increase of more than

30% in gross written

premiums achieved in

the year under review

Premium growth and results

Management report premium growth and results

In property and casualty

reinsurance we success-

fully built on the low

loss level of previous

years despite natural

catastrophes

12

The following sections explain the develop-ment of each line of business. Due to our orienta-tion as a specialist reinsurer for the German mar-ket, we have subdivided our management reporton underwriting business into two sections. Thefollowing commentaries on the various lines of

Development of the individual lines of business in Germany

business refer solely to our German portfolio; wethen provide a summary of our international busi-ness accepted from Hannover Re under retro-cession arrangements. Due to the internationalnature of aviation business, this is also describedwithin the foreign section.

Fire

The positive trend in premium income in in-dustrial property insurance was maintained in theyear under review. The traditional insurance linesof industrial fire and fire loss of profits showedconsiderable gains thanks to the steps taken torehabilitate the business. Overall, the premiumvolume booked by German insurers in industrialproperty business climbed by around 12% toapproximately EUR 3.5 billion.

Not least under pressure from the reinsurers,insurers initiated a far-reaching streamlining oftheir industrial portfolio. The success of this re-habilitation was already reflected in sharplyhigher premiums, reduced scope of coverage, andincreased deductibles. Premium income conse-quently grew, most notably in the traditional in-dustrial fire and fire loss of profits lines, by around18% to more than EUR 1 billion.

Management report premium growth and results

* Underwriting result: gross before internal administrative expenses, allocatedinvestment return, and the change in the equalisation reserve

2 000

200

400

1 200

800

600

1 000

1 400

1 600

1 800

2 200

2 400

0

in EUR million

2001 2002

1061 1404

844 1079

Germany

Foreign

1905 2483Total

Development of gross premium income – breakdowninto German and foreign business

100

0

(100)

(200)

(300)

(400)

(500)

200

in EUR million

2001 2002

(157) 27

(361) 119

Germany

Foreign

(518) 146Total

Development of underwriting results* – breakdowninto German and foreign business

1313

The otherwise good result recorded in indus-trial fire insurance was overshadowed by thehigh expenditure for the flooding in the summerof 2002. Losses for the financial year in indus-trial fire and fire loss of profits – including ex-tended coverage and all risks covers – increasedto roughly EUR 2.4 billion (EUR 1.96 billion).

In view of the attractive market situation, wewere able to boost our gross premium income byEUR 16.8 million to EUR 52.1 million. The ad-verse experience of our competitors due to thecatastrophe losses of previous years safeguardedan uninterrupted trend towards non-proportionalcovers. We, too, were successful in writing profit-able business on a non-proportional basis, thusfurther improving the quality of the margin on ourassumed portfolio. In this context, we cooperatefor the most part with companies with whomwe already enjoy long-standing business relation-ships. We continued to scale back our proportionalacceptances since conditions were in some casesinadequate.

Despite our cautious underwriting policy, ourunderwriting result, too, was not able to escape

the poor performance of German fire insuranceunscathed.

Although the year under review passed with-out spectacular major claims, the considerableloss expenditure associatedwith the flooding pushed theloss ratio up to 91.5% (77.6%).Comparatively speaking, how-ever, our loss ratio was stillgood. Yet the premium in-crease of 47.6% was insuffi-cient to offset the higher lossburden, in which non-propor-tional covers – particularlyhard hit by the flood event – were also a factor.The underwriting deficit consequently grew byEUR 6.9 million to EUR 10.6 million.

An amount of EUR 23.4 million was allo-cated to the equalisation reserve.

in EUR million 2002 2001

Fire

Gross written premiums 52.1 35.3

Loss ratio (%) 91.5 77.6

Underwriting result(gross) (10.6) (3.7)

Management report premium growth and results

Liability

In the year under review premiums in generalthird party liability insurance on the Germanmarket increased by roughly 1% compared tothe previous year to reach EUR 6 billion. Thepremium trend in industrial liability insurancestabilised, whereas in commercial and personalliability business premiums continued to fall.The year under review experienced a significantlylighter load of major claims than the previousyear. Expenditure on claims in the financial yearwas only marginally higher than in the year be-fore, rising by a mere 0.4% to EUR 5.1 billion.Paralleling moves in industrial property insur-ance, portfolios in industrial liability businesshave been rehabilitated over the past two years.A further improvement was achieved throughthe definition of the coverage trigger. The switchfrom the "losses-occurring" to "claims-made" prin-

ciple when renewing liability treaties for certainparticularly exposed industries was just as sig-nificant a factor as the removal of US permanentestablishments from German policies.

In accordance with ourselective underwriting policythat is not guided by marketshare targets, we continuedto hold back from problemat-ic segments in German liabil-ity business such as liabilityfor pure financial losses.Having already withdrawnfrom unprofitable segments of German liabilitybusiness in the previous year, the developmentof our portfolio in the year under review was ex-tremely gratifying. In light of the favourable state

in EUR million 2002 2001

Liability

Gross written premiums 160.3 105.5

Loss ratio (%) 78.4 212.6

Underwriting result(gross) (2.0) (141.4)

1414

of the market, we enlarged our gross premiumvolume by 51.9% to EUR 160.3 million. At thesame time, we were spared any sizeable claimsin the year just-ended. The loss ratio in this linecontracted to a normal level of 78.4% after theprevious year (212.6%) had been burdened byclaims in the pharmaceutical sector. Liabilitybusiness performed well compared to the pre-vious year and closed with a near-breakeven

Personal accident

Premiums throughout the entire primaryinsurance market increased as in the previousyear by 1.5% to EUR 5.5 billion. In terms of thetotal premium volume of the German insurancemarket the personal accident line is of relatively

minor importance, and hence theproportion of personal accidentbusiness in our German portfoliois correspondingly small – around3% – but profitable.

As a reinsurer we tradition-ally support our clients withspecial services. We offer themadvice on innovative products as

well as on risk assessment and claims settlement.Working together with key clients, we developed– in addition to already existing personal accidentproducts aimed at children and senior citizens –a new product in the area of personal accidentinsurance with assistance components for seniorcitizens. In the year under review we further en-

Motor

The disastrous flooding, the windstorm"Jeanett", and summer hailstorms all took a se-vere toll on the result of German motor insurance.

Although this line was affectedconsiderably more heavily bynatural catastrophes in the yearunder review, the underwritingdeficit of around EUR 0.5 billionwas only slightly smaller thanin the previous year. Gross pre-mium earned grew by 3% toEUR 22.0 billion, while the loss

larged our business share guided by profitabilityconsiderations and expanded the range of servicesthat we provide to support our clients.

In order to fulfil the required margins thatwe set for our treaties we concentrated on profit-able business. Consequently, our gross premiumincome decreased slightly by 1.8% to EUR 38.7million.

The quality of our treaties was reflected mostclearly in the low loss ratio and the favourableunderwriting result. The loss ratio fell by 21.8percentage points to 32.0%, thus reverting tothe level of earlier years after the increase in2001. We therefore succeeded in generating agood result of EUR 4.5 million in the year underreview that surpassed our expectations. On thebasis of this good performance we allocated anamount of EUR 11.9 million to the equalisationreserve.

ratio remained virtually unchanged at 84.2%(84.4%).

Whereas the loss ratio in own damage in-surance increased by 7.5 percentage points to85.2% due to the extensive natural hazardsclaims, it fell to 84.8% (89.7%) in motor thirdparty liability insurance. Thanks to the rise of3% in gross premium income, it was thus possibleto substantially reduce the deficit in motor thirdparty liability insurance.

underwriting result for gross account of -EUR 2.0million in the year under review.

The relatively good result enabled us tomake an allocation of EUR 37.1 million to theequalisation reserve. We also strengthened ourIBNR reserve by an amount of EUR 34.1 millionin the year under review.

in EUR million 2002 2001

Personal accident

Gross writtenpremiums 38.7 39.4

Loss ratio (%) 32.0 53.8

Underwriting result(gross) 4.5 (1.1)

Management report premium growth and results

in EUR million 2002 2001

Motor

Gross writtenpremiums 407.9 382.1

Loss ratio (%) 89.1 70.3

Underwriting result(gross) (18.3) 62.0

15

Accounting for around 30% of our Germanportfolio, motor reinsurance is a high priorityfor our company and one of our most importantlines. Motor liability premiums climbed by 4.7%year-on-year to EUR 291.0 million.

Echoing the trend in the primary insurancesector, we profited from the lower claims fre-quency in the proportional motor liability mar-ket. We received risk-adequate remuneration forour non-proportional covers in the year underreview thanks to the increased premiums.

With the exception of hail damage, the na-tural hazards events did not produce any excessivestrains in motor own damage reinsurance sincewe write this business predominantly as non-proportional catastrophe covers in conjunction

with high priorities. The premium volume grewby EUR 12.7 million to EUR 115.7 million.

Gross premium income in our total Germanmotor business increased by EUR 25.8 millionto EUR 407.9 million, while the loss ratio climbedto 89.1% (70.3%) due to higher overall loss ex-penditure. The bulk of the premium growth wasattributable to new accounts.

The underwriting deficit of EUR 18.3 millionin the motor line fell well short of the previousyear's profit of EUR 62.0 million. An amount ofEUR 61.7 million was withdrawn from the equal-isation reserve. We strengthened the IBNR reservewith an allocation of EUR 19.9 million from thenon-technical account.

15

Management report premium growth and results

Marine

The situation in German marine insuranceremained difficult in the year under review. Still,a tendency towards hardening market conditionscould be observed. The rehabilitation measuresinitiated by numerous insurers slowly began tobear fruit as a trend emerged towards premiumscommensurate with the risk. Premium growth inGerman marine insurance was lower in the yearunder review than in the previous year, whileclaims expenditure remained consistent.

In accordance with our general underwritingstrategy the majority of our treaties are writtenon a non-proportional basis. Our approach toproportional covers remains cautious, since theanticipated profit potential fails to meet our ex-pectations despite the rehabilitation measuresimplemented in the primary market.

Contrary to the general trend, we achievedappreciably improved premium volume thanks toE+S Rück’s good market positioning – supportedby our "AA" rating. We boosted gross premiumincome by 16.3% to EUR 10.7million. While the loss ratiohad been as high as 93.4% inthe previous year, it decreasedto 85.9% due to the favour-able premium development –but was still unsatisfactory. Anallocation of EUR 15.3 millionwas made to the equalisationreserve.

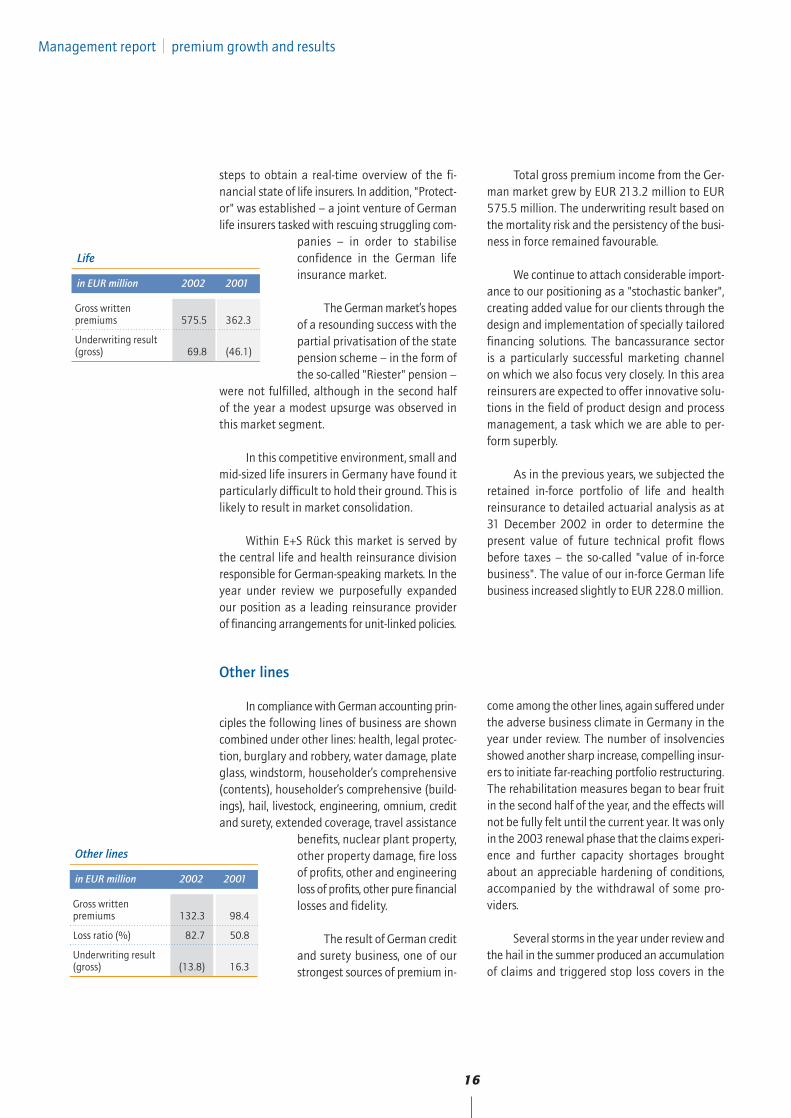

Life

Characterised by a shift in demand towardsconventional products with guaranteed benefitsdue to a sharp decline in the market value of divi-dend-bearing securities – the leading DAX stockindex lost more than 40% of its value in thecourse of 2002 – and a falling interest rate level,the German life insurance market – served by

around 120 companies – was a difficult climatein which to operate in 2002. Although the effectsvaried from company to company, these develop-ments had generally unfavourable repercussionson the financial strength and solvency of life in-surers. Against this backdrop, the Federal Finan-cial Supervisory Authority (BAFin) took additional

in EUR million 2002 2001

Marine

Gross writtenpremiums 10.7 9.2

Loss ratio (%) 85.9 93.4

Underwriting result(gross) (0.8) (2.2)

16

steps to obtain a real-time overview of the fi-nancial state of life insurers. In addition, "Protect-or" was established – a joint venture of Germanlife insurers tasked with rescuing struggling com-

panies – in order to stabiliseconfidence in the German lifeinsurance market.

The German market’s hopesof a resounding success with thepartial privatisation of the statepension scheme – in the form ofthe so-called "Riester" pension –

were not fulfilled, although in the second halfof the year a modest upsurge was observed inthis market segment.

In this competitive environment, small andmid-sized life insurers in Germany have found itparticularly difficult to hold their ground. This islikely to result in market consolidation.

Within E+S Rück this market is served bythe central life and health reinsurance divisionresponsible for German-speaking markets. In theyear under review we purposefully expandedour position as a leading reinsurance providerof financing arrangements for unit-linked policies.

Total gross premium income from the Ger-man market grew by EUR 213.2 million to EUR575.5 million. The underwriting result based onthe mortality risk and the persistency of the busi-ness in force remained favourable.

We continue to attach considerable import-ance to our positioning as a "stochastic banker",creating added value for our clients through thedesign and implementation of specially tailoredfinancing solutions. The bancassurance sectoris a particularly successful marketing channelon which we also focus very closely. In this areareinsurers are expected to offer innovative solu-tions in the field of product design and processmanagement, a task which we are able to per-form superbly.

As in the previous years, we subjected theretained in-force portfolio of life and healthreinsurance to detailed actuarial analysis as at31 December 2002 in order to determine thepresent value of future technical profit flowsbefore taxes – the so-called "value of in-forcebusiness". The value of our in-force German lifebusiness increased slightly to EUR 228.0 million.

in EUR million 2002 2001

Life

Gross writtenpremiums 575.5 362.3

Underwriting result(gross) 69.8 (46.1)

Management report premium growth and results

Other lines

In compliance with German accounting prin-ciples the following lines of business are showncombined under other lines: health, legal protec-tion, burglary and robbery, water damage, plateglass, windstorm, householder’s comprehensive(contents), householder’s comprehensive (build-ings), hail, livestock, engineering, omnium, creditand surety, extended coverage, travel assistance

benefits, nuclear plant property,other property damage, fire lossof profits, other and engineeringloss of profits, other pure financiallosses and fidelity.

The result of German creditand surety business, one of ourstrongest sources of premium in-

come among the other lines, again suffered underthe adverse business climate in Germany in theyear under review. The number of insolvenciesshowed another sharp increase, compelling insur-ers to initiate far-reaching portfolio restructuring.The rehabilitation measures began to bear fruitin the second half of the year, and the effects willnot be fully felt until the current year. It was onlyin the 2003 renewal phase that the claims experi-ence and further capacity shortages broughtabout an appreciable hardening of conditions,accompanied by the withdrawal of some pro-viders.

Several storms in the year under review andthe hail in the summer produced an accumulationof claims and triggered stop loss covers in the

in EUR million 2002 2001

Other lines

Gross writtenpremiums 132.3 98.4

Loss ratio (%) 82.7 50.8

Underwriting result(gross) (13.8) 16.3

17

reinsurance sector, especially in the area of wind-storm insurance. This left a corresponding markon the insurers’ loss ratios. After the previousyear had been relatively unencumbered by size-able natural hazards losses, loss ratios deterior-ated appreciably in the year under review.

Our windstorm portfolio is traditionally dom-inated by non-proportional covers, in which weprefer to write the less loss-prone middle and

upper layers. The accumulation of losses withinthe year prevented us building on the previousyear’s good result. An amount of EUR 11.8 millionwas withdrawn from the equalisation reserve.

Management report premium growth and results

Results of our foreign business

As a member of the Hannover Re Group, weshare in the experience of the international (re-)insurance markets via internal retrocessions withinthe Group. By adding blocks of foreign business toour portfolio, we are able to ensure better geo-graphical diversification, which serves to stabiliseresults from the medium- to long-term perspective.

The results of the previous year were heavilyimpaired by the terrorist attacks of 11 Septem-ber 2001. The impact of these events on theHannover Re Group was also significant. Lookingback, however, we can assert that we withstoodthese losses well. Our forecast that we would re-

US liability business

posts an outstanding

result

coup the loss payments within two to three yearsappears to be proving correct. We have observedextraordinary premium increases in some lines dueto the hardening of markets. Particularly prom-inent was the development of our US liabilitybusiness, with increases in excess of 50%. In avi-ation business, on the other hand, some policiessaw initial premium declines in contrast to thesharp rise in the previous year.

The following sections note developmentsin the markets with the largest premium volume,with special emphasis on the key lines of business.

Europe

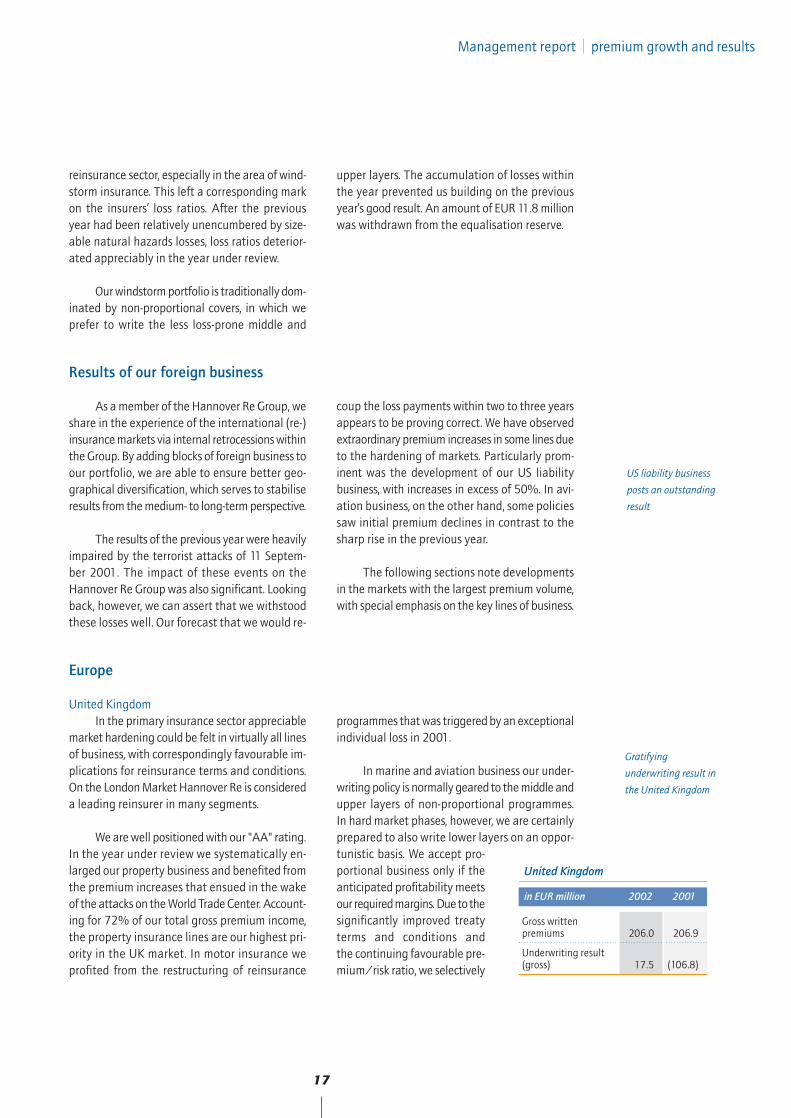

United KingdomIn the primary insurance sector appreciable

market hardening could be felt in virtually all linesof business, with correspondingly favourable im-plications for reinsurance terms and conditions.On the London Market Hannover Re is considereda leading reinsurer in many segments.

We are well positioned with our "AA" rating.In the year under review we systematically en-larged our property business and benefited fromthe premium increases that ensued in the wakeof the attacks on the World Trade Center. Account-ing for 72% of our total gross premium income,the property insurance lines are our highest pri-ority in the UK market. In motor insurance weprofited from the restructuring of reinsurance

programmes that was triggered by an exceptionalindividual loss in 2001.

In marine and aviation business our under-writing policy is normally geared to the middle andupper layers of non-proportional programmes.In hard market phases, however, we are certainlyprepared to also write lower layers on an oppor-tunistic basis. We accept pro-portional business only if theanticipated profitability meetsour required margins. Due to thesignificantly improved treatyterms and conditions andthe continuing favourable pre-mium/risk ratio, we selectively

Gratifying

underwriting result in

the United Kingdom

in EUR million 2002 2001

United Kingdom

Gross writtenpremiums 206.0 206.9

Underwriting result(gross) 17.5 (106.8)

18

France The situation as regards premiums and con-

ditions was similar to that on other markets. In gen-eral terms, reinsurers benefitedfrom the withdrawal of a numberof competitors from the marketand enlarged their shares.

Along with liability busi-ness, property insurance is themost important line in our port-folio. Given the rather hesitant

recovery of liability business we adopted a morecautious approach to writing this line. Our focus

in the year under review was on property insur-ance, which we substantially expanded. We pre-ferred to write non-proportional covers, the pre-mium development of which played a gratifyingpart in our premium growth. Our total premiumvolume in France grew to EUR 40.9 million (EUR29.9 million). The claims frequency was consid-erably lower than in previous years. It was onlythe disastrous flooding in the south of France inSeptember 2002 that weighed down the result.Overall, we were highly satisfied with the perfor-mance of our French portfolio.

Management report premium growth and results

Late entry into US

business means E+S

Rück has no need to

constitute additional

reserves for asbestos and

liability risks

North America

The focus of interest was on US liability busi-ness as the year progressed. Also noteworthywas the need for several insurers and reinsurersto constitute substantial additional reserves forasbestos-related claims as well as the overly op-timistic reserving policy in liability business dur-ing the "soft" market years of 1997-2001.

Owing to Hannover Re’s relatively late entryinto the US market and its adherence to a conser-vative reserving policy, E+S Rück was not com-

pelled to constitute additionalreserves for asbestos-related risksor liability risks from earlier oc-currence years.

Liability business is the lar-gest single line in our US port-folio. The premium increases inthe year under review meant

that our portfolio, too, showed a substantial risein premium income.

Having written business only cautiouslyduring the soft market, we had already stepped

up our activities in the liability sector in the pre-vious year as the market began to harden – amove that we continued in the year under re-view. Thanks to our profit-oriented underwritingpolicy we substantially enhanced the profitabilityof our portfolio.

In addition to the conventional propertyand casualty reinsurance business, our Bermuda-based company established in 2001 offers naturalcatastrophe covers. The market for reinsuranceof natural catastrophe losses has been steadilyhardening since the events of 11 September2001. What is more, those attacks prompted someceding companies to pull out of the LondonMarket and to increasingly turn to the newlyestablished companies in Bermuda. We were su-perbly successful in exploiting the favourablemarket situation and enlarging our premiumvolume by writing primarily the middle and upperlayers of natural catastrophe reinsurance pro-grammes.

While the 2001 underwriting result in NorthAmerica was weighed down by the loss expend-

expanded our portfolio on the UK market. Thepremium volume remained virtually unchangedyear-on-year, although the underwriting resultshowed gratifying improvement. Having reporteda loss only last year, we achieved an underwriting

profit for gross account in the year under review.In the aviation line we allocated an amount ofEUR 12.4 million to the equalisation reserve.

in EUR million 2002 2001

France

Gross writtenpremiums 40.9 29.9

Underwriting result(gross) 6.3 (16.9)

in EUR million 2002 2001

North America

Gross writtenpremiums 467.3 283.8

Underwriting result(gross) 37.8 (207.8)

Good result due to low

loss expenditure

19

Asia

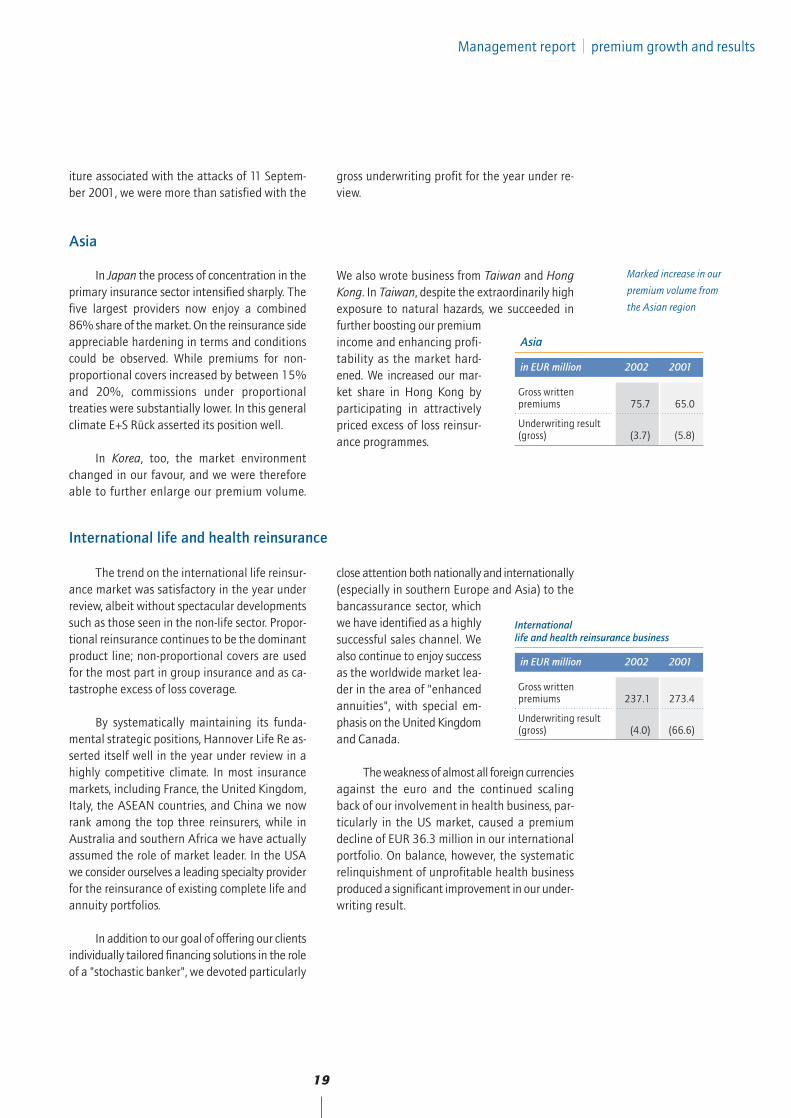

In Japan the process of concentration in theprimary insurance sector intensified sharply. Thefive largest providers now enjoy a combined86% share of the market. On the reinsurance sideappreciable hardening in terms and conditionscould be observed. While premiums for non-proportional covers increased by between 15%and 20%, commissions under proportionaltreaties were substantially lower. In this generalclimate E+S Rück asserted its position well.

In Korea, too, the market environmentchanged in our favour, and we were thereforeable to further enlarge our premium volume.

We also wrote business from Taiwan and HongKong. In Taiwan, despite the extraordinarily highexposure to natural hazards, we succeeded infurther boosting our premiumincome and enhancing profi-tability as the market hard-ened. We increased our mar-ket share in Hong Kong byparticipating in attractivelypriced excess of loss reinsur-ance programmes.

Management report premium growth and results

International life and health reinsurance

The trend on the international life reinsur-ance market was satisfactory in the year underreview, albeit without spectacular developmentssuch as those seen in the non-life sector. Propor-tional reinsurance continues to be the dominantproduct line; non-proportional covers are usedfor the most part in group insurance and as ca-tastrophe excess of loss coverage.

By systematically maintaining its funda-mental strategic positions, Hannover Life Re as-serted itself well in the year under review in ahighly competitive climate. In most insurancemarkets, including France, the United Kingdom,Italy, the ASEAN countries, and China we nowrank among the top three reinsurers, while inAustralia and southern Africa we have actuallyassumed the role of market leader. In the USAwe consider ourselves a leading specialty providerfor the reinsurance of existing complete life andannuity portfolios.

In addition to our goal of offering our clientsindividually tailored financing solutions in the roleof a "stochastic banker", we devoted particularly

close attention both nationally and internationally(especially in southern Europe and Asia) to thebancassurance sector, whichwe have identified as a highlysuccessful sales channel. Wealso continue to enjoy successas the worldwide market lea-der in the area of "enhancedannuities", with special em-phasis on the United Kingdomand Canada.

The weakness of almost all foreign currenciesagainst the euro and the continued scalingback of our involvement in health business, par-ticularly in the US market, caused a premiumdecline of EUR 36.3 million in our internationalportfolio. On balance, however, the systematicrelinquishment of unprofitable health businessproduced a significant improvement in our under-writing result.

iture associated with the attacks of 11 Septem-ber 2001, we were more than satisfied with the

gross underwriting profit for the year under re-view.

in EUR million 2002 2001

Asia

Gross writtenpremiums 75.7 65.0

Underwriting result(gross) (3.7) (5.8)

in EUR million 2002 2001

International life and health reinsurance business

Gross writtenpremiums 237.1 273.4

Underwriting result(gross) (4.0) (66.6)

Marked increase in our

premium volume from

the Asian region

20

Investments

The first quarter of 2002 was one of generalconsolidation on the international equity mar-kets, with share prices for the most part caughtin a sideways movement. Subsequently a declineset in, however, dragging the major indices downto fourth-quarter levels, even lower than thosewitnessed after 11 September 2001. This slumpwas triggered not only by the general uncertaintyconcerning the future direction of the economy,but also – and more specifically – by the erosionof confidence due to certain manipulations offinancial statements and by the fear of furtherterrorist attacks. The markets remained unsettleduntil year-end. Geopolitical crises, such as thelooming war on Iraq and the repercussions ofthe general strike in Venezuela, were the finalnail in the coffin for any hopes of a year-end rally.For the third year in succession the major stockindices closed in negative territory.

Bond markets profited from the uncertaintyon equity markets and the sluggish cyclical trendin Europe and the USA. While the US FederalReserve Board cut the reference interest rateseveral times in the course of the year, ultimatelytrimming it to an all-time low of 1.25%, the Euro-pean Central Bank waited until December to cutthe key interest rate by 50 basis points to 2.75%.

Despite opposing effects associated withexchange rate movements, our total portfolio ofself-managed assets (i.e. excluding deposits withceding companies) grew in the reporting periodby 12.7% to EUR 3.2 billion. The excellent per-formance of our reinsurance business, especiallyin property and casualty reinsurance, and thereinvestment of investment income generateda cash inflow of around EUR 360.0 million. Theweakness of the equity markets was more thanoffset in our portfolio by the favourable perfor-mance of our bond holdings. On balance webooked unrealised gains of EUR 37.2 million onour other financial investments.

Since we continue to view equity marketswith scepticism, we initially further reduced ourequity allocation as the year progressed. We usedthe market softness at year-end to boost our

portfolio in the short term. Our investment uni-verse remains unchanged, comprising liquid BlueChips listed on major indices (Euro Stoxx, Nikkei,S&P 500). As at year-end a mere 10.7% of our in-vestments were in listed stocks. Thanks to thisapproach, we suffered considerably less heavilythan many of our competitors under the depressedstate of the equity markets. Yet, our account, too,was not spared diminutions in value. Total write-downs on exchange-listed equities amounted toEUR 41.6 million in the year under review. Theunrealised losses on our equity portfolio totalledEUR 49.5 million as at year-end.

Fixed-income securities were once againour preferred asset category in the year underreview. In the course of the year we investedfree liquidity from maturities and cash inflowsprimarily in instruments with a short or mediumtime to maturity so as to minimise the interestrate risk. Our portfolio of fixed-income securitiesincreased year-on-year from EUR 1.9 billion toroughly EUR 2.1 billion.

In view of the considerable volatility anduncertainty prevailing on the credit marketsthe excellent quality of our fixed-income securitiesproved its worth. The proportion of the totalportfolio rated "AA" or better stood at 85.5%.The minimal strain produced by the spectacularbusiness failures witnessed in the year under re-view demonstrated the quality of our corporatebonds.

We used the decline in yields and diminishingyield advantage offered by corporate bonds torealise total price gains of EUR 53.7 million. Des-pite lower reinvestment returns the unrealisedprice gains in our portfolio of fixed-income se-curities climbed from EUR 35.0 million to EUR79.4 million.

As at year-end we held a total amount ofEUR 382.2 million (EUR 92.0 million) in short-term assets, including overnight money and timedeposits. Whereas in the previous year anticipatedclaims payments arising out of catastrophe losseshad prompted us to keep relatively high liquidity

Management report investments

Yields at historic lows

Poor performance of the

equity markets offset by

favourable development

of our bond portfolio

Reduction in the

proportion of dividend-

carrying securities

protected us against

excessive value

adjustments

21

Shares, units in unit trusts and other variable-yield securities as well as bearer debt securities and other fixed-income securities

Total

Deposits with ceding companies

Loans to affiliated companies and other loansOther investments

Investments

in EUR million

1500

2000

2500

3000

1000

500

0

3500

4500

4000

19941995

19961997

19981999

20002001

19932002

holdings, in the year under review this actionwas prompted by the state of the capital markets.We wanted to be able to respond flexibly to ad-vantageous market situations, on the one hand,while also limiting the potential for losses fromthe portfolio.

Ordinary income increased by EUR 27.3 mil-lion to EUR 183.2 million (EUR 155.9 million),while at the same time the total investmentportfolio (including deposits with ceding com-panies) grew by 21.9% to EUR 4,390.8 million(EUR 3,603.3 million). Although current yieldsdeclined worldwide in the year under review, thisrise in our income was attributable not least tolarger deposits with ceding companies.

The downward slide on equity markets hada significant adverse impact on the investmentperformance. Write-downs on our investments,primarily on equities, increased by EUR 40.0 mil-lion to EUR 60.3 million.

Profits on disposals of EUR 53.7 million(EUR 102.1 million) were generated through thesale of securities. This contrasted with losses ondisposals of EUR 3.1 mil-lion.

The total net invest-ment result fell from EUR223.3 million to EUR 169.5million. However, this de-cline includes currency ef-fects that were detrimentalto our investment resultin the year under review.Bearing in mind the currentmarket climate, we are en-tirely satisfied with the in-come from our investment portfolio. As in the pre-vious year, our strategic positioning was provencorrect.

Appreciable rise in

our ordinary income

compared to the

previous year

Management report investments

Rating of fixed-income securities

AA26%

A8%

AAA60%

BBB3%

< BBB3%

22

Annual risk inventory

safeguards up-to-date

status of the risk portfolio

Management report risk report

Risk report

The acceptance of risks and their profes-sional management constitute our core businessas a reinsurance company. To this extent, theprofessional assessment and handling of risks isa major competitive factor and a crucial elementin steering the company. Our corporate strategyis geared to generating a sustained increase inthe value of the company. This means that wepurposefully enter into entrepreneurial risks pro-vided the associated opportunities promise acommensurate increase in the value of the com-pany.

E+S Rück bears exclusive responsibility forGerman business within the Hannover Re Group.For its part, Hannover Re – together with its sub-sidiaries – writes the international business. Inorder to safeguard overall advantageous inter-national risk spreading, the two companies par-ticipate in each other’s respective business seg-ments. Our business is thus also influenced byrisks on the international reinsurance marketsvia these retrocessions.

Organisation of risk management

Risk management within E+S Rück is cen-trally coordinated, but based on local responsi-bility in the various areas of business. Overallresponsibility for risk management is determinedaccording to the specific strategic business groups,within which the responsible board members de-fine the operating objectives. The task of localrisk controllers is to identify increased risks in thevarious business groups as quickly as possibleand initiate counteraction without delay. Tothis end, we use a number of different quantifyingmethods that are tailored to individual risks andvary in their design and degree of reporting de-tail. Within the scope of our risk managementsystem all conceivable risks from the currentperspective which could jeopardise the perfor-mance and survival of our company are recordedcomprehensively and systematically. The up-to-date status of our risk portfolio, on the level ofboth individual risks and accumulation risks, isensured by means of defined reporting proced-ures and an annual risk inventory. Our risk re-porting consists primarily of standard and adhoc reports that are created using a speciallydeveloped IT application and enable manage-ment to assess the overall situation with con-siderable accuracy. The core risk managementelements are set out in guidelines which applythroughout the entire E+S Rück organisation.Acting independently of these clearly defined

procedures, Internal Auditing verifies compliancewith the stipulated processes in all functionalareas of our company.

Our company’s risk situation can be com-prehensively described by the following riskcategories:

• global risks, • strategic risks, • operating risks, which we subdivide into

- technical risks,- investment risks and- operational risks.

Global risksGlobal risks may arise, for example, as a re-

sult of changes in the legal framework (includingchanges in the general regulatory or tax situ-ation) which are beyond a reinsurer’s directsphere of influence. They may also derive fromsocial or demographic trends or ensue as a con-sequence of developments in the insurance in-dustry or changes in environmental and climatefactors. Such potential risks can scarcely be re-duced and there are limits to the extent towhich they can be avoided. Risk managementmeasures must therefore be geared to identifyingdangerous developments as early as possible inorder to be able to react promptly. It is for this

23

Claims trends are con-

stantly monitored for

early identification of

dangerous developments

Detailed simulation

models are used to

analyse the potential

for losses

Specific mechanisms

have been put in place to

control underwriting

risks

Retrocession is a tool

used to limit risks and

stabilise results

reason, for example, that we constantly monitorclaims trends. Currently notable in this contextare liability risks in the USA due to mould, as-bestos-related risks – again primarily in theUSA but recently in Europe, too – and the settle-ment trends in severe motor third party liabilitybodily injury claims in major European markets.

The various national economic environ-ments, on the other hand, are monitored firstand foremost on a local basis within our busi-ness groups, whose market intimacy and experi-ence ensure that even "weak signals" can bepromptly detected. One of the central problemsfacing the reinsurance industry is the growingnumber of natural disasters around the worldand the associated potential for losses. Usingdetailed simulation models we therefore analysethe increase in the frequency of natural catas-trophes caused by climate change and in theextent of the losses that they cause. On the basisof these analyses we are then in a position todetermine the maximum exposure that we areprepared to accept and can calculate our ownreinsurance requirements.

Strategic risksStrategic risks derive primarily from an im-

balance between the defined corporate strategyand the constantly fluctuating framework con-ditions – an environment shaped, on the onehand, by our clients’ requirements and, on theother, by the strategies of our competitors. Ouroverriding strategic objective is to generate dy-namic growth as an optimally diversified andeconomically independent reinsurer of above-average profitability. E+S Rück’s individual busi-ness groups thus pursue specific and inherentlyconsistent detailed strategies that are derivedfrom this strategic objective. Company-wide ratiosand controlling processes have been defined tomonitor achievement of the strategic targetsfrom the operating standpoint. They are usedto measure and control the contribution madeby each business group to the company’s over-all performance.

In the year under review we further ex-panded our value-oriented controlling and man-agement system. Through the progressive in-troduction of an IVC (intrinsic value creation)approach we are implementing a key ratio bymeans of which all company-wide manage-ment processes can be systematically geared tovalue creation. In this regard, IVC provides anobjective ratio that motivates managerial staff totake value-oriented actions and prevents value-destroying management errors.

Technical operating risksThe underwriting risk lies primarily in the

danger of accepting risks that surpass the avail-able financial resources, but also in such caseswhere the premiums calculated in advance areinsufficient to finance the resulting loss burdens.Possible reasons here may be inaccurate pricingassumptions or pricing models, unexpected claimsdevelopments, inadequate reserves, failure to ap-propriately tailor our own reinsurance, or defaulton the part of retrocessionaires. E+S Rück employsvarious mechanisms – both for the portfolio as awhole and geared to specific business groups –in order to control underwriting risks.

The loss reserves in property and casualtyreinsurance are determined on an actuarial basis.The point of departure is always the informationprovided by ceding companies. The reserve is cal-culated on the basis of a breakdown by risk classesand regions for the property, liability, and motorlines of business and on an aggregate basis forthe credit, aviation, and marine lines. The antici-pated ultimate loss ratios are calculated usingstatistical run-off triangles and actuarial methods.

A fundamental instrument of risk limitationand results stabilisation is retrocession. Whereaspremiums are always payable at the beginningof a contract, risks derive from the fact that longperiods – sometimes decades – may elapse untillosses are paid. It is therefore particularly im-portant that retrocession partners not only havea high credit rating at the time when a contract

Management report risk report

24

High level of IT security

will be maintained

Management report risk report

comes into being, but are also still able to meettheir obligations when loss payments are to bemade. Our assessment of the credit status of ourretrocessionaires is guided by the opinions ofinternationally recognised rating agencies andsupported by our own balance sheet and mar-ket analyses. Our Security Committee classifiesthe reinsurers used by E+S Rück with bindingeffect for all placements.

A further key component of our risk man-agement across business groups is the use ofdynamic, scenario-based financial analysis. Theseanalyses simulate the effects of hypotheticalscenarios (e.g. loss events and capital marketdevelopments) on the assets, net income, andfinancial situation. The findings produced by ourdynamic financial analysis enable us to prioritiserisk-policy measures.

The reserves in life and health reinsuranceare always based upon the information providedby our clients. The regulations of the local super-visory authorities ensure that the reserves calcu-lated by ceding companies satisfy all local re-quirements with respect to the actuarial methodsand assumptions (e.g. use of mortality and dis-ability tables, assumptions regarding the lapseprobability etc.).

Investment operating risksOur investment strategy is shaped by the

duration of our commitments and our interestin generating an adequate return. Risks in theinvestment sector consist most notably of mar-ket, credit, and liquidity risks. The risks run by aninternationally operating reinsurer also include,however, the exchange risk – which we limit bymatching commitments in foreign currencies asfar as possible with assets in the correspondingcurrencies. This strategy very largely offsets ex-change gains and losses.

Asset portfolios are based to a significantextent on insurance premiums that are set asidefor future loss payments. Asset/liability man-agement provides the linkage between reinsur-

ance and investment activities. A strict separ-ation of functions – i.e. keeping a distinctionbetween trading, settlement and risk controlling– supported by defined reports and analyses isjust one of the ways in which compliance with theinvestment guidelines adopted by the ExecutiveBoard is ensured.

Risks in the investment sector are counteredusing a broad range of efficient managementand control mechanisms which are geared to therules adopted by the Federal Financial Super-visory Authority (BAFin).

Operational risksOperational risks include, inter alia, human

error, inadequate controls, and organisationalshortcomings. A major integral component of oursafeguards and controls is the Internal ControllingSystem (ICS), which encompasses all harmonisedand interlinked checks, activities, and rules. In-ternal Auditing regularly verifies that the ICS isworking correctly in all functional areas of ourcompany.

The dependence of the company’s core pro-cesses on information technology is rising sharply– a trend which goes hand-in-hand with a com-mensurately growing IT-related risk potential.Ensuring high availability of our IT applicationsand protecting the integrity of mission-criticalcorporate data are tasks to which we attach fun-damental economic importance. In the year underreview we initiated an Information Security pro-ject in order to ensure that the existing high levelof security is maintained in the future. This projectinvestigates and, where necessary, supplementsthe already existing security measures at E+SRück.

We also classify risks associated with humanresources management under operational risks.Fierce competition for qualified specialists andmanagers is a hallmark of all the markets in whichwe operate. Reinsurance is a highly complex fi-nancial service, the success of which is cruciallydependent on the expertise, motivation, and dedi-

Asset liability manage-

ment provides linkage

between reinsurance and

investment activities

25

Personnel management

tools are an important

element of our holistic

management strategy

We recruit talents

through university

contacts and career fairs

Management report human resources report

cation of our staff. With this in mind we maintainclose contacts with, inter alia, a number of uni-

versities and set great store by personnel devel-opment and training measures.

Assessment of the risk situation

As an internationally active reinsurer we areconfronted with numerous potential risks thatcould have a not inconsiderable impact on ournet income, financial position, and assets. Never-theless, on the basis of the information currently

available to us, we do not perceive any risks thatcould jeopardise the continued existence of ourcompany in the short or medium term or couldimpair the assets, financial position, or net incomein a significant or sustained manner.

Human resources report

The objectives derived from our corporatestrategy determine the requirements placed onthe Human Resources sector and on its activities.We enhanced our existing personnel tools andsubjected them to constant human resources con-trolling in order to ensure that they satisfy ourexacting quality standards – since quality is thekey to employee satisfaction and generates mo-tivation.

We use a newly developed three-part execu-tive training programme to promote the personalgrowth of our new managerial staff; after all, theability to manage oneself is a precondition for themanagement of others. In addition to conveyingbasic know-how relating to the manager’s role,this seminar focuses on guiding principles andthe skills needed to realistically assess one’s ownsituation. Further issues considered are how tobehave in groups and lead teams as well as con-flict management and the shaping of changeprocesses. Executives are also able to draw on thesupport of an experienced coach of their ownchoosing.

The complexity of reinsurance business andthe pressure of competition in the internationalmarkets necessitate a constant readiness to learn.We use state-of-the-art teaching methods to en-courage and support our staff. Programmed andstructured instruction and visual aids assist indi-vidual preparation for the subsequent workshops.

Computer-aided learning techniques are currentlyundergoing a trial phase. They are intended tofacilitate personal feedback on the acquired levelof knowledge and should enable staff to developtheir own study rhythm independently of otherlearners.

Our management simulation game de-veloped in 2000 is now a firmly established partof a complex, holistic system of learning. It pro-vides an excellent learning environment for par-ticipants and tutors from our own ranks.

With the introduction of "Employee Self-Service" we took another decisive step in the yearunder review towards electronic human resourcesmanagement. Our staff are now able to view on-line portions of their personal data record. Thisfosters trust and helps to quickly resolve possiblediscrepancies. In addition, we shall shortly makea broad range of management information avail-able online to executives via the "Manager Desk-top".

We devote special energy to cultivating ourexisting contacts with institutions of higher edu-cation and attending the relevant university car-eer fairs. The sharp increase in the number ofhighly qualified applicants bears out the positiveresponse to these efforts. Trainees at our com-pany pass through an 18-month programme forjunior executives and get to know many sides of

26

the organisation by spending periods of 6 to 12weeks in various departments. We also offer stu-dents the chance to gain insights into differentareas of the company through internships andwe support diploma students writing on reinsur-ance-related topics with appropriate stipends.

In dual courses of study conducted in cooper-ation with the internationally oriented Berufs-akademie Berlin and the Leibniz-Akademie Han-nover we train students of business administra-tion by providing on-the-job instruction.

As at the end of the year under review thenumber of staff had increased by 17 – or 8.6% –to 215 (198). At 58.6%, the proportion of femalestaff was on a par with previous years. Personnel

Management report outlook

Insurance industry

anticipates growth

impetus in Germany

due to increased

individual provision

expenses totalled EUR 15.9 million. Expenses forpensions and part-time working arrangementsfor older employees amounted to EUR 913,000.

We would like to thank our staff for theirconsiderable dedication and loyalty in the 2002financial year. Our gratitude also extends to theemployee council and the senior managementcommittee.

Outlook

The prevailing depressed phase of the Ger-man economy will be sustained at least in thefirst half of the current year, since a number offactors are hampering an appreciable acceler-ation of economic activity. Owing to the asseterosion caused by the collapse of equity pricesin the year under review, the higher burden ofsocial security charges and taxes as well as theunfavourable prospects on the job market, pri-vate households will expand their consumerspending only very modestly – if at all. A furtherfactor is the upward revaluation of the euro inreal terms, which will continue to slow exportswell into 2003. The future trend remains unclear,since thus far exports – on which every fifth job inGermany depends – have compensated for theslack domestic demand. The leading economicresearch institutes have already factored thisinto their forecasts and trimmed the anticipatedeconomic growth to well under 1%.

The insurance industry similarly expectsweaker premium growth in 2003. In personal in-surance lines growth impetus is anticipated in lifeand health business, in particular, as a conse-

quence of the general trend towards greater indi-vidual provision. Against this backdrop, premiumgrowth of around 3.5% is expected in life insur-ance and roughly 6% in health insurance. Prop-erty and casualty insurance in Germany will profitfrom heightened risk awareness among the popu-lation following the catastrophe loss events inthe year under review. Owing to the reduced levelof disposable income, however, premium growthof a mere 2% appears realistic. For the currentyear the insurance industry expects gross pre-mium income to rise by around 3%.

In contrast to the muted prospects for in-surers, we anticipate significant premium in-creases on the reinsurance side based on theexperience of this year’s renewal phase. We wereable to obtain substantially improved prices andconditions in our important markets. In addition,the market contracted due to the withdrawal ofcapacity and downgrading of some competitors.In this environment E+S Rück asserted its positionwell and with its "AA" rating from Standard &Poor’s was a sought-after provider in the 2003renewal season.

27

Life, health, and personal

accident reinsurance

as well as motor third

party liability business

the highest-premium

segments in the

current year

Management report affiliated companies

Particularly in liability business, we wereable to write treaties with significant rate in-creases. With an eye to the future development,a general tendency is emerging towards a far-reaching tightening of liability law on both thenational and European level, and this could proveproblematic for this line of business. It is our as-sumption that the loss ratio will stabilise on theprevious year’s level and that an adequate resultcan be generated in this line.

Our German motor third party liability port-folio is expected to deliver satisfactory resultsfor 2003. We renewed treaties with further in-creases in the rate level and initiated new busi-ness relationships. The scope of cover changedwith the 2003 renewals. Since 1 January 2003the illimité covers – which used to be standardpractice – were replaced by defined per-eventinsured limits of liability. The extent to whichthese changes will affect results remains to beseen.

Together with motor third party liabilitybusiness, life, health, and personal accident re-insurance will be our highest-premium segmentin the 2003 financial year. We shall further ex-pand our position as the leading German rein-surer providing financing arrangements for unit-linked policies. We shall also step up our involve-ment – working together with our clients – inthe development of innovative products for theGerman market. The focus here is first and fore-most on products for the senior citizens’ market.

We continue to take a thoroughly positiveview of the development of our foreign portfoliofor 2003. The renewal season concluded in Janu-

ary clearly showed that we were able to rene-gotiate most treaties with improved terms andconditions. We shall continue to concentrate onnon-proportional business in property and casu-alty reinsurance and write treaties on an oppor-tunistic basis guided strictly by profit considera-tions. In international life and health reinsur-ance we shall expand further our position as a"stochastic banker", offering clients individuallytailored financing solutions – a role which weexpect to generate a significant profit contribu-tion as in previous years.

In the absence of favourable corporate newsand the resulting impetus from the economy thetense situation on capital markets will continue.In view of the uncertain situation on the stockmarket we shall keep our equity allocation on alow level and further improve the quality of ourfixed-income securities. We intend to reinvestprimarily in securities with short to medium timesto maturity. The investment result is difficult toforecast in the current climate. Given our port-folio structure, considerably greater importancewould be attached to a yield increase than to afurther decline on equity markets.