ANNUAL REPORT 08 - eurobankpb.lueurobankpb.lu/IMG/pdf/EUROBANK_RA08.pdf · Eurobank EFG Private...

48

Transcript of ANNUAL REPORT 08 - eurobankpb.lueurobankpb.lu/IMG/pdf/EUROBANK_RA08.pdf · Eurobank EFG Private...

Eurobank EFG Private Bank Luxembourg S.A. 5, rue Jean Monnet – L-2180 Luxembourg — P.O. Box 897 L-2018 Luxembourg

Telephone (+352) 42 07 24-1 — Facsimile (+352) 42 07 24-650www.eurobankefg.lu

R.C. B 24724 registered office as above Eu

rob

ank

EFG

Pri

vate

Ban

k Lu

xem

bo

urg

S.A

.A

NN

UA

L R

EP

OR

T 0

8

2 - 3 Introduction

4 Board of Directors

5 - 9 Directors’ report

10 - 11 Independent auditor’s report

12 - 13 Balance Sheet

14 Off Balance Sheet

15 Profit and Loss Account

16 - 40 Notes to the annual accounts

42 - 43 Principal Offices

contents

1eurobank eFG Private Bank Luxembourg s.A.

2 --- Annual Report 08

3eurobank eFG Private Bank Luxembourg s.A.

Eurobank EFG Private Bank Luxembourg S.A. (formerly EFG Private

Bank (Luxembourg) S.A.) is engaged in the business of providing

private banking and investment advisory services for corporate and

private clients as well as administration and custody of investment

funds. The Bank is active in the money market (both deposit taking

and lending), spot and forward foreign exchange business, securities

transactions and off balance sheet instruments, both on its own account

and on behalf of customers.

The Bank is a subsidiary of EFG Eurobank Ergasias S.A., one of

Greece’s leading banking and financial institutions, and a member of

the Geneva-based EFG Group.

The EFG Group has expanded rapidly over the years to become the

third largest Swiss-based banking group with, as at 31 December 2008,

shareholders’ equity amounting to CHF 8.7 billion, customers’ assets

under management and administration in excess of CHF 167 billion

and around 27,000 employees in 40 countries.

EFG Eurobank Ergasias S.A., Athens, the 100% shareholder of the

Bank, is 43.6% controlled by EFG Bank European Financial Group S.A.,

the parent bank of the EFG Group based in Geneva, Switzerland. The

profit and loss account and balance sheet of the Bank are included in

the consolidated financial statements of EFG Bank European Financial

Group S.A. and EFG Eurobank Ergasias S.A.

intRoduction

3eurobank eFG Private Bank Luxembourg s.A.

4 --- Annual Report 08

Board of directors

Mr. François RIES Chairman

Mrs. Lena LASCARI Managing Director

Mr. Dimosthenis ARCHONTIDIS Director

Mr. René FALTZ Director

Mr. Nicholas KARAMOUZIS Director

Mr. Nicholas NANOPOULOS Director

Mr. Périclès PETALAS Director

Mr. Jean-Louis de POTESTA Director

Mr. Giorgio PRADELLI Director

Mrs. Yasmine RALLI Director

Mr. Vincenzo LOMONACO Secretary to the Board

and General Manager

Management

Mrs. Lena LASCARI Managing Director, CEO

Mr. Vincenzo LOMONACO General Manager, COO

senior officers

Mr. Robert BERBEE First Vice-President

Mr. Ioannis SAKIOTIS First Vice-President

Mrs. Helen FOTINEAS Vice-President

Mr. Markos FOURMOUZIS Vice-President

Mr. Christophe LANGUE Vice-President

Mr. Fabio MACCHINI Vice-President

Auditors

PricewaterhouseCoopers, Luxembourg

introduction ( continued )

5eurobank eFG Private Bank Luxembourg s.A.

We are pleased to present our report for the year

ended December 31, 2008.

In October 2008 our company name and corporate

identity was changed to Eurobank EFG Private Bank

Luxembourg S.A. in order to illustrate our current

growth and international position and at the same time

assuring our Greek identity and our Swiss roots.

y

2008 overview

The deterioration in the US economic trajectory,

which emanated from its subprime sector, accelerated

in 2008 instigating a further massive sell-off in credit

markets and sharp decline in government bond

yields. After expanding by 2.0% in 2007, US real

GDP growth decelerated to 1.3%, on the back of a

further significant correction in the housing market,

tightening lending standards and persisting credit

jitters. Market optimism that the negative effects from

the global credit crunch were confined mainly to the

US and other major industrialized countries and that

the big emerging economies would be able to decouple

finally proved unfounded. Following positive real GDP

reading in Q1, the Euro zone economy contracted in

both Q2 and Q3 with Germany and Spain the most

hit. The EU Commission estimates that the Euro

zone economy has grown by a meager 0.9% in 2008

following hefty growth rates of 2.7% and 2.9% in 2007

and 2006 respectively. On the same gloomy note, the

rapidly slowing US economy and the global crunch

took their toll on the export-driven Japanese economy,

with a substantial real effective appreciation of the JPY

exerting a substantial drag on economic activity.

With regard to price developments, US inflation

dropped sharply reaching a nearly 50-yr low of 0.1%yoy

in December from a peak of 4.3%yoy early last year

mainly on the back of lower oil and commodity prices.

The noteworthy easing in price pressures and the

risk of a deep economic downturn allowed the Fed to

pursue additional rate easing in 2008. The committee

trimmed the Fed Funds target rate to a target range

of 0.0-0.25% in December from 4.25% in early 2008

having delivered more than 500bps of cumulative rate

easing since September 2007, when the global financial

crisis began to flare up.

Convincing signs of abating price pressures were also

evident in the Eurozone economy with the headline

CPI dropping to a multi-year low of 1.6%yoy in late

2008 following a peak of 4.0% last July. This along with

mounting worries over Eurozone’s growth outlook

since late summer saw the ECB embarking upon an

easing cycle in October in a coordinated move.

y

Key Financials Review of financial statements 2008

a) Balance Sheet Total Assets at the end of 2008 have increased by

45% to a figure of EUR 19,076 million versus EUR

13,174 million at the end of 2007, an increase due to

the cooperation with Eurobank Group and the strong

evolution of the business.

diRectoRs’ RePoRt

6 --- Annual Report 08

Our Loans and advances to customers have also

increased by 45% to record EUR 12,654.0 million from

EUR 8,726.5 million at the end of 2007. The majority of

the Loans and Advances EUR 10,039.2 million (79%)

versus EUR 7,015.4 million (80%) in 2007 are with

intra-group entities and are fully cash collateralized.

The remaining of the Loans and Advances are to third

party clients and are either fully collateralized or fully

guaranteed. It should be noted that it is the Bank’s

objective that strong growth comes along with further

improvement of loan portfolio quality, which is ensured

through strict controls and an effective streamlined

credit risk management policy.

Customer deposits increased by 68.6% and amounted

to EUR 2,633.8 million from EUR 1,562.1 million.

Shareholder funds amount to EUR 70 million Tier one

capital and EUR 116.7 million subordinated loan of

Tier two capital. Therefore, total own funds including

subscribed capital, subordinated liabilities, reserves,

profit for the financial year and profit brought forward

reached EUR 271.1 million which reflects a strong

capital position and allows for a high rate of growth

in the foreseeable future.

b) Income StatementThe net interest income between the two years 2008

and 2007 has remained stable. The net interest income

for the year ending 2008 amounted to EUR 17.8 million

in comparison to EUR 17.9 million in 2007.

Net commission income decreased from EUR 5.9

million in 2007 to EUR 5.3 million in 2008 due to the

increase in commissions paid for the issuance of L/G’s

by our Parent Group as a result of the increase in the

number of loans.

Net profit on Financial Operations increased by EUR

16.9 million from 2007 to EUR 21.5 million in 2008

and this is due to the increase in income deriving

from treasury transactions.

Hence, in 2008 the total net operating income increased

by 57% versus 2007.

Total operating expenses between the two years

increased by only 3%. This led to a significant

decrease in the cost to income ratio falling to 25%

vis-à-vis 40% last year.

The Bank’s net profits after taxation for the year 2008

amounted to EUR 22.604 million.

y

distribution of Profits

The Board of Directors proposes that the 2008 annual

accounts be approved, and that the Total Net Profit

available for distribution be appropriated as follows:

Profit for the financial year EUR 22,604,230

Profit brought forward EUR 44,019,891

Total net profit available

for distribution EUR 66,624,121

Allocation to Legal Reserve EUR 1,130,212

Allocation to Net Wealth Tax Special Reserve EUR 2,143,340

Profit carried forward EUR 63,350,569

y

Risk Management overview

The strategy of the Bank is based on its core

activities: Private Banking, General Banking and

Fund Administration.

In the year 2008 the Internal Control procedures and

controls in operation within the Bank ensured:

X the attainment of the objectives set by the Bank;

X the effective and efficient use of resources;

directors’ Report ( continued )

7eurobank eFG Private Bank Luxembourg s.A.

X the proper control of risks and safeguarding

of assets; and

X the compliance with the legislation

and regulations.

Management has ensured that all resources (human

and technical) are used efficiently and effectively.

They have placed on site a sufficient number of

competent staff to take decisions in line with the

policies defined and based on the powers delegated

to them, and to execute the decisions taken.

The general framework of the organisational

responsibilities, monitoring and control for each

department of the Bank is further defined by the

relevant procedures manuals.

During 2008, the Board of Directors approved the

Bank’s Risk Management and Capital Management

Policy. During 2009 the first yearly review of the

Internal Capital Adequacy Assessment Process –

ICAAP will be submitted to the Board for their

validation. The ICAAP will be evaluated by the

Luxembourg Banks regulatory authority on a yearly

basis in the context of their supervisory review

process. The Bank during the year 2008 achieved

the targets of its capital management policy that is,

to maintain a strong capital base in order to support

business development and to meet regulatory capital

requirements at all times.

The Risk Policy of the Bank describes in detail the

risk appetite, which is determined by the Board of

Directors and Senior Management of the Bank. The

aim of the Bank’s risk appetite is to balance risk and

return on available capital.

The Bank’s risk management function covers the

measures for early identification of risk, risk control

and risk monitoring with regard to banking risks,

which include but are not limited to:

X credit risk;

X market risk for trading book;

X operational risk;

X business risk;

X interest rate risk for banking book;

X liquidity risk;

X compliance risk; and

X reputation risk.

In addition to the local risk management function there

is also periodic monitoring by the Group of various

risks on a daily, weekly, monthly, and quarterly basis

thus enhancing the Bank’s risk monitoring process.

The risk management policies are re-examined

annually by the Board of Directors. All risks are

subject to detailed limits, which are monitored on an

ongoing basis. The Board of Directors also sets limits

to control market risk on a value at risk basis.

Exposure to credit risk is managed through regular

analysis of the ability of borrowers and potential

borrowers to meet interest and capital repayment

obligations and by regularly reviewing these limits

where appropriate. Exposure to credit risk is primarily

managed by obtaining eligible collateral, as well as

corporate and personal guarantees.

The interest rate risk of the Bank remains relatively

low. The volume of assets and liabilities with a

maturity of more than one year remains low. Interest

rate risk is monitored daily and reported to local

Management and the Group Treasurer.

Controls over market risks arising from open positions

in interest rate, currency and equity positions all of

which are exposed to general and specific market

movements are in place.

The Bank has decided to invest in government

securities or securities issued by high rated corporates.

The very prudent principles which we have always

used for credit assessment have continued to be

applied and the general credit exposure for the Bank

8 --- Annual Report 08

has even been improved. The Bank’s investments

have mainly focused on the purchase of government

securities and securities issued by first-rate

companies.

Liquidity risk is closely monitored. The majority

of assets (77%) and liabilities (79%) reach maturity

within 3 months.

y

economic outlook for 2009

As we enter the second year of the global financial

crisis, real activity data and sentiment surveys

continue to deteriorate sharply while the deleveraging

process is still under way, aggravating market worries

over a deep and prolonged world recession. According

to most recent IMF forecasts, world real GDP growth

will decelerate to 0.5% in 2009, the lowest rate since

World War II, from 3.3% in 2008 despite repeated

attempts from CBs and international organizations

(through aggressive interest rate cuts and/or massive

stimulus packages) to support sentiment and address

ongoing disfunctionalities in financial and credit

markets.

The US economy is projected to contract by 1.6% this

year following a growth rate of 1.2% in 2008 with the

unemployment rate expected to rise well above 8%

from 4.9% early last year. Meanwhile, after FOMC

monetary policy has been eased aggressively since

August 2007, the committee has now shifted its focus

to quantitative easing measures and has emphasized

its commitment to continue to increase the size of

its balance sheet in order to support credit markets

and economic activity. On the same gloomy note, the

EU Commission projects the Eurozone economy to

contract by 1.9% in 2009 after growing by 0.9% last

year with the economic downturn expected to be more

pronounced in Spain. The EU Commission has already

proposed a 1.5% of GDP stimulus package while

individual countries may need to act more forcefully

to support their economies in an environment where

several EU members expected to breach the 3% of

GDP fiscal-deficit threshold this year.

y

Business outlook 2009

Our Parent Bank, Eurobank EFG today is a large and

strong, capital-wise, international banking Group,

with over 1,700 branches in Greece and abroad. It

is the second largest bank in Greece. Eurobank EFG

is a member of EFG Group, which is the 3rd biggest

Geneva-based banking group in Switzerland. It is

worth pointing out that only in September (2007) a

timely share capital increase by 1.25 billion euro was

completed and thus capital sufficiency for the Bank

is very strong. We follow a consistent credit policy

which accounts for our optimum credit ratings by

international firms.

In the last twelve months Eurobank EFG has

intensified its efforts in deposit gathering and has

managed to grow its deposit base at a faster pace than

its loans. Moving forward, the Group aims to be self-

funded both in Greece and New Europe.

The Bank’s priority in today's environment lies

with the selective growth of its activities, an even

more effective exploitation of its capital and further

enhancing its liquidity. Most importantly, the first

priority of our Group is to encourage the deepening of

a relationship of trust and creative cooperation with

our customers and to provide real and qualitative

service to jointly overcome the impact of the crisis in

the financial sphere as smoothly as possible.

In Luxembourg, our Bank’s strategy for the current

year will continue to focus on the Bank’s core activities:

Wealth Management and Private Banking, Fund

Administration and General Banking. In particular

we will focus on growth and business development

directors’ Report ( continued )

9eurobank eFG Private Bank Luxembourg s.A.

to expand our customer base in the Private Banking

area and will further exploit the synergies and expand

our cross selling potential within the Group’s enlarged

network. Furthermore, our Bank will endeavour to

further expand the offering of its high quality services

to Third Party Funds. On the Loan business side

the lending will continue to be granted on a fully

guaranteed and / or collateralized basis.

Our parent bank, Eurobank EFG, in 2008 once

again secured international and local distinctions.

Specifically:

It was selected as the “Bank of the Year in Greece”

for 2008 by the internationally acclaimed journal

“The Banker”, which is owned by the Financial

Times publishing Group. This distinction has been

awarded in terms of the annual institution, which the

authoritative journal has instituted in order to select

the most successful and effective banking institution

in each country.

This distinction has been awarded to Eurobank

EFG further to an evaluation by the journal of

its performance and development in the current

environment which has been defined by restlessness

and challenges. This distinction has been accompanied

by the pointing out that: “After five years of strong

development in the credit financial sector the

international crises has been manifested with an

exceptional intensity and the banks throughout the

world have felt the consequences. However, despite

the credit financial crisis, many organizations have

achieved noteworthy performances and excellent

results. The award by the journal for the ‘Bank of

the Year’ reflects the success and the financial credit

performance by the leading banks internationally.”

It is reminded that Eurobank EFG has also been

proclaimed as the “Best Bank in Greece” for 2008 by

the internationally acclaimed “Euromoney” journal.

There has been no significant subsequent event as of

the date of this report which could have a material

impact on the 2008 Annual Accounts.

On behalf of the Board of Directors, we would like

to express our deep appreciation to our customers

for their loyalty to the Bank and our gratitude to the

management and personnel for their enthusiasm,

consistency and dedication.

24th February, 2009

François ries Lena Lascari

Chairman Managing Director

10 --- Annual Report 08

Report on the annual accounts

We have audited the accompanying annual accounts of Eurobank EFG Private Bank Luxembourg S.A., which

comprise the balance sheet as at December 31, 2008, the profit and loss account for the year then ended and a

summary of significant accounting policies and other explanatory notes.

y

Board of directors’ responsibility for the annual accounts

The Board of Directors is responsible for the preparation and fair presentation of these annual accounts in

accordance with Luxembourg legal and regulatory requirements relating to the preparation of the annual

accounts. This responsibility includes: designing, implementing and maintaining internal control relevant to

the preparation and fair presentation of annual accounts that are free from material misstatement, whether due

to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that

are reasonable in the circumstances.

y

Auditor’s responsibility

Our responsibility is to express an opinion on these annual accounts based on our audit. We conducted our audit

in accordance with International Standards on Auditing as adopted by the “Institut des Réviseurs d’Entreprises”.

Those standards require that we comply with ethical requirements and plan and perform the audit to obtain

reasonable assurance whether the annual accounts are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

annual accounts. The procedures selected depend on the Auditor’s judgment, including the assessment of the

risks of material misstatement of the annual accounts, whether due to fraud or error. In making those risk

To the Board of Directors of Eurobank EFG Private Bank Luxembourg S.A.

indePendentAuditoR’s RePoRt

11eurobank eFG Private Bank Luxembourg s.A.

assessments, the Auditor considers internal control relevant to the entity’s preparation and fair presentation of

the annual accounts in order to design audit procedures that are appropriate in the circumstances, but not for

the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made

by the Board of Directors, as well as evaluating the overall presentation of the annual accounts.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our

audit opinion.

y

opinion

In our opinion, these annual accounts give a true and fair view of the financial position of Eurobank EFG

Private Bank Luxembourg S.A. as of December 31, 2008, and of the results of its operations for the year then

ended in accordance with Luxembourg legal and regulatory requirements relating to the preparation of the

annual accounts.

y

Report on other legal and regulatory requirements

The Director’s report, which is the responsibility of the Board of Directors, is in accordance with the annual

accounts.

PricewaterhouseCoopers S.à r.l. Luxembourg, February 24, 2009

Réviseur d’entreprises

Represented by

Pierre Krier

12 --- Annual Report 08

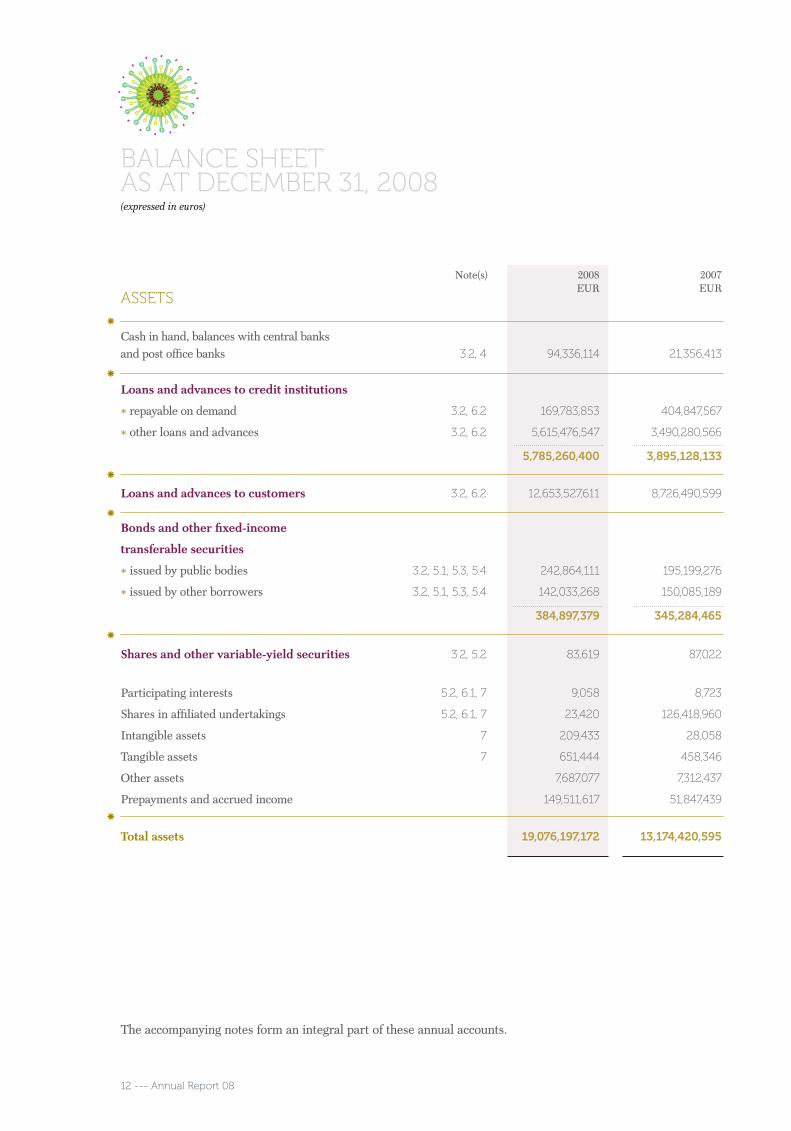

Assets

Cash in hand, balances with central banks and post office banks 3.2, 4 94,336,114 21,356,413

Loans and advances to credit institutions

X repayable on demand 3.2, 6.2 169,783,853 404,847,567

X other loans and advances 3.2, 6.2 5,615,476,547 3,490,280,566

5,785,260,400 3,895,128,133

Loans and advances to customers 3.2, 6.2 12,653,527,611 8,726,490,599

Bonds and other fixed-income

transferable securities

X issued by public bodies 3.2, 5.1, 5.3, 5.4 242,864,111 195,199,276

X issued by other borrowers 3.2, 5.1, 5.3, 5.4 142,033,268 150,085,189

384,897,379 345,284,465

Shares and other variable-yield securities 3.2, 5.2 83,619 87,022

Participating interests 5.2, 6.1, 7 9,058 8,723

Shares in affiliated undertakings 5.2, 6.1, 7 23,420 126,418,960

Intangible assets 7 209,433 28,058

Tangible assets 7 651,444 458,346

Other assets 7,687,077 7,312,437

Prepayments and accrued income 149,511,617 51,847,439

Total assets 19,076,197,172 13,174,420,595

Note(s) 2008 2007 EUR EUR

BALAnce sheet As At deceMBeR 31, 2008(expressed in euros)

y

y

y

y

y

The accompanying notes form an integral part of these annual accounts.

y

13eurobank eFG Private Bank Luxembourg s.A.

LiABiLities

Amounts owed to credit institutions

X repayable on demand 3.2, 6.2 223,164,987 29,481,503

X with agreed maturity dates or periods of notice 3.2, 6.2 15,789,160,910 11,282,837,125

16,012,325,897 11,312,318,628

Amounts owed to customers

other debts

X repayable on demand 3.2, 6.2 144,192,607 149,552,376

X with agreed maturity dates or periods of notice 3.2, 6.2 2,489,599,317 1,412,576,967

2,633,791,924 1,562,129,343

Other liabilities 756,019 2,401,725

Accruals and deferred income 151,302,723 44,571,711

Provisions

X provisions for taxation 3,676,399 1,619,915

X other provisions 3,243,846 2,883,139

6,920,245 4,503,054

Subordinated liabilities 8, 6.2 116,752,491 116,752,491

Subscribed capital 9, 11 70,000,000 70,000,000

Reserves 10, 11 17,723,752 16,018,083

Profit brought forward 11 44,019,891 30,734,406

Profit for the financial year 22,604,230 14,991,154

Total liabilities 19,076,197,172 13,174,420,595

Note(s) 2008 2007 EUR EUR

y

y

y

y

y

y

y

y

y

y

The accompanying notes form an integral part of these annual accounts.

y

14 --- Annual Report 08

Contingent liabilities

of which: 13.1 16,603,089 36,321,445

X guarantees and assets pledged as collateral security 16,603,089 36,321,445

Commitments 13.2 1,336,340,086 1,373,977,261

Fiduciary transactions 13.2 72,601,773 49,353,181

Note(s) 2008 2007 EUR EUR

oFF BALAnce sheet As At deceMBeR 31, 2008(expressed in euros)

y

y

The accompanying notes form an integral part of these annual accounts.

y

15eurobank eFG Private Bank Luxembourg s.A.

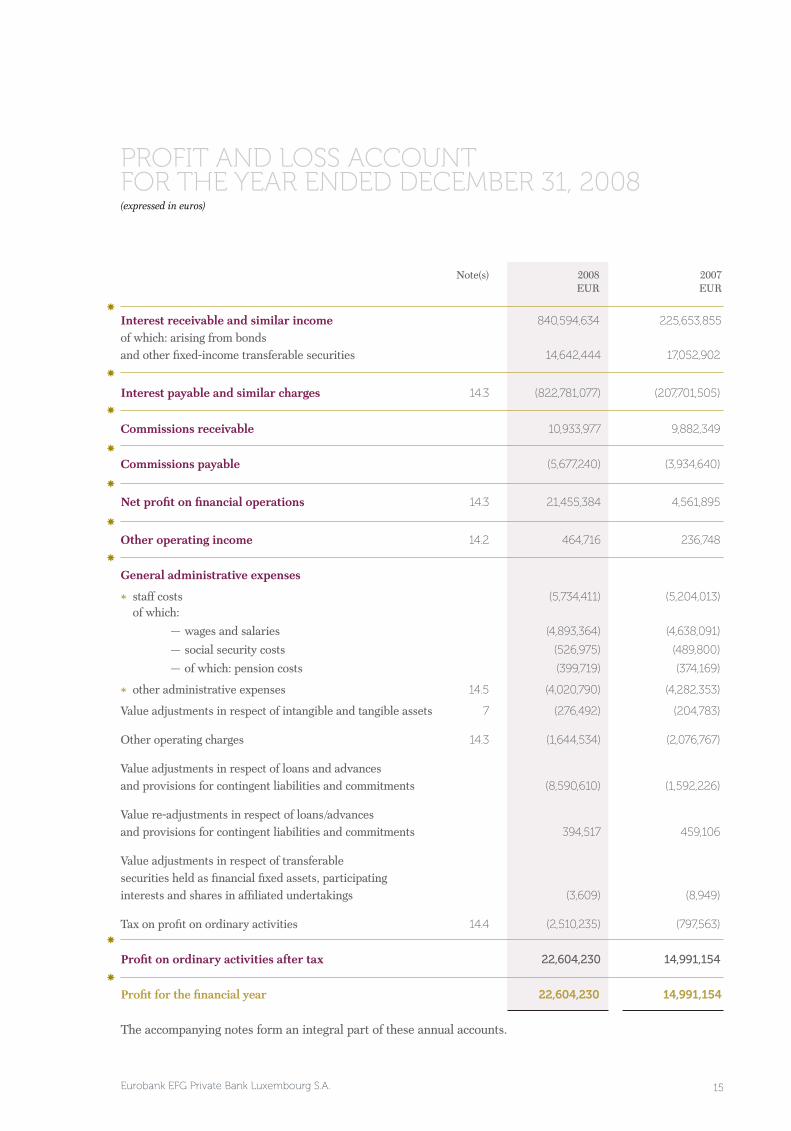

Interest receivable and similar income 840,594,634 225,653,855

of which: arising from bonds and other fixed-income transferable securities 14,642,444 17,052,902

Interest payable and similar charges 14.3 (822,781,077) (207,701,505)

Commissions receivable 10,933,977 9,882,349

Commissions payable (5,677,240) (3,934,640)

Net profit on financial operations 14.3 21,455,384 4,561,895

Other operating income 14.2 464,716 236,748

General administrative expenses

X staff costs (5,734,411) (5,204,013) of which:

— wages and salaries (4,893,364) (4,638,091)

— social security costs (526,975) (489,800)

— of which: pension costs (399,719) (374,169)

X other administrative expenses 14.5 (4,020,790) (4,282,353)

Value adjustments in respect of intangible and tangible assets 7 (276,492) (204,783)

Other operating charges 14.3 (1,644,534) (2,076,767)

Value adjustments in respect of loans and advances and provisions for contingent liabilities and commitments (8,590,610) (1,592,226)

Value re-adjustments in respect of loans/advances and provisions for contingent liabilities and commitments 394,517 459,106

Value adjustments in respect of transferablesecurities held as financial fixed assets, participatinginterests and shares in affiliated undertakings (3,609) (8,949)

Tax on profit on ordinary activities 14.4 (2,510,235) (797,563)

Profit on ordinary activities after tax 22,604,230 14,991,154

Profit for the financial year 22,604,230 14,991,154

Note(s) 2008 2007 EUR EUR

y

y

y

y

y

y

y

PRoFit And Loss Account FoR the yeAR ended deceMBeR 31, 2008(expressed in euros)

y

The accompanying notes form an integral part of these annual accounts.

y

17eurobank eFG Private Bank Luxembourg s.A.

note 1 – General

Eurobank EFG Private Bank Luxembourg S.A.

(the “Bank”) was incorporated in Luxembourg on

August 26, 1986, as a “Société Anonyme” under the

name of Banque de Dépôts (Luxembourg) S.A. The

Extraordinary General Meeting of Shareholders held

on August 6, 1997 resolved to change the name of the

Bank to EFG Private Bank (Luxembourg) S.A. with

effect from September 10, 1997.

The Extraordinary General Meeting of Shareholders

held on 17th September, 2008 resolved to change the

name of the Bank to Eurobank EFG Private Bank

Luxembourg S.A. with effect from October 1, 2008.

The Bank is engaged in the business of providing

private banking, investment and advisory services for

corporate and private clients as well as administrative

and custody services for investment funds. The Bank

is active in the money markets, deposit taking and

lending and engages in spot and forward foreign

exchange business as well as undertaking transactions

in securities and off balance sheet instruments, both

for its own account and on behalf of customers.

Eurobank EFG Private Bank Luxembourg S.A. is

included in the consolidated annual accounts of EFG

Bank European Financial Group, whose registered

office is in Geneva, where the consolidated annual

accounts are available. These annual accounts

represent the biggest group of companies, which the

Bank belongs to as a subsidiary.

Eurobank EFG Private Bank Luxembourg S.A. is

also included in the consolidated annual accounts

of its Mother Company, EFG Eurobank Ergasias

S.A., whose registered office is in Athens, where the

consolidated annual accounts are available. These

annual accounts represent the smallest group of

companies, which the Bank belongs to as a subsidiary.

EFG Eurobank Ergasias S.A. is listed on the Athens

Stock Exchange.

y

note 2 – summary of significant accounting policies

2.1 – Basis of presentation These annual accounts have been prepared in

conformity with accounting principles generally

accepted in the banking sector in the Grand Duchy

of Luxembourg. The accounting policies and the

principles of valuation are determined and applied

by the Board of Directors, except those, which are

defined by Luxembourg law and regulations.

On the bases of the criteria set out by the Luxembourg

law, the Bank is exempted from preparing consolidated

annual accounts. In accordance with the amended

as at December 31, 2008

notes to the AnnuAL Accounts

17eurobank eFG Private Bank Luxembourg s.A.

18 --- Annual Report 08

law of June 17, 1992, the present annual accounts

are consequently prepared on an unconsolidated

basis for approval by the Annual General Meeting of

Shareholders.

2.2 – Foreign currenciesThe Bank has adopted a multicurrency accounting

system, as a result of which assets and liabilities

are recorded in the currencies in which they have

occurred. For the preparation of the annual accounts,

amounts in foreign currencies are translated into euro

(EUR) on the following bases:

2.2.1 Spot transactionsAssets and liabilities in foreign currencies are

translated into euro at exchange rates applicable at

the balance sheet date.

Income, charges and purchases of fixed assets are

recorded in the currency in which they are collected or

disbursed and are translated into euro at rates approx-

imating those ruling at the time of the transaction.

Exchange gains and losses arising from the Bank’s net

open currency spot position are taken to the profit

and loss account in the current year.

Unsettled spot foreign exchange transactions are

translated into euro at the spot rate of exchange

prevailing on the balance sheet date.

Foreign exchange gains and losses resulting from

spot transactions hedged by forward transactions

are neutralised through “prepayments and accrued

income” and “accruals and deferred income” accounts.

Premiums or discounts arising due to the difference

between spot and forward exchange rates are amortised

in the profit and loss account on a pro-rata basis.

2.2.2 Forward transactionsUnsettled forward exchange transactions are

translated into euro at the forward rate prevailing on

the balance sheet date for the remaining maturity.

Unrealised exchange losses on un-hedged forward

exchange contracts are recognised in the profit and

loss account at the forward rate prevailing on the

balance sheet date for the remaining term of the

contract. Unrealised exchange gains on forward

exchange contracts are not included, and are only

recognised when ultimately realised, except when

such contracts form an economic unit with offsetting

foreign exchange transactions.

2.2.3 SwapsGains and losses on currency swap transactions are

accrued on the straight-line basis over the period of the

swap contract and are included in interest receivable or

payable in the profit and loss account, as appropriate.

2.3 – Loans and advancesLoans and advances are stated at disbursement value

less repayments made and any value adjustments

required. Accrued interest are recorded in balance

sheet caption “prepayments and accrued income”.

The policy of the Bank is to establish specific value

adjustments for doubtful debts in accordance with the

circumstances and for amounts specified by the Board

of Directors. These value adjustments are deducted

from the appropriate asset account balances.

2.4 – Valuation of fixed-income transferable securities The Bank has divided its portfolio of fixed-income

transferable securities into three categories for

valuation purposes:

2.4.1 Investment portfolio of financial fixed assetsThis portfolio comprises fixed-income transferable

securities, which are intended to be held on a long-

term basis.

notes to the annual accounts ( continued )

19eurobank eFG Private Bank Luxembourg s.A.

X Principle of valuation at acquisition cost

Fixed-income transferable securities are recorded at

historical acquisition cost in their original currency.

The acquisition cost includes the costs to purchase

the asset. A value adjustment is made where the

market value at the balance sheet date is lower than

the acquisition cost and when the Board of Directors

considers the depreciation to be permanent.

The premium resulting from the purchase of bonds

and other fixed-income transferable securities having

the characteristics of financial fixed assets, at a

price exceeding the amount repayable at maturity,

is amortised in the profit and loss account over the

period remaining until final repayment.

The discount resulting from the acquisition of bonds

and other fixed-income transferable securities having

the characteristics of financial fixed assets, at a price

less than the amount repayable at maturity, is released

to income in instalments over the period remaining

until repayment.

X Principle of valuation at “lower of cost or market”

Fixed-income transferable securities having the charac-

teristics of financial fixed assets are valued at lower of

their amortised acquisition cost and their market value.

The value adjustment, corresponding to the negative

difference between the market value and the acquisi-

tion cost, is not maintained if the reasons for which the

value adjustment was made no longer exist.

During the year, the Bank did not hold fixed-income

transferable securities in its investment portfolio.

2.4.2 Trading portfolioThis portfolio comprises fixed-income transferable

securities purchased with the intention of selling

them in the immediate short term. These securities

are traded on a market whose liquidity can be

assumed to be certain and their market price is at all

times available to third parties. These securities are

valued at the lower of their acquisition cost and their

market value.

During the year, the Bank did not hold any trading

portfolio.

2.4.3 Structural portfolioThis portfolio comprises fixed-income transferable

securities and asset swaps purchased for their

investment return or yield or held to establish a

particular asset structure or a secondary source of

liquidity. It also includes fixed-income transferable

securities not contained in the other two categories.

Securities in this portfolio are valued at the lower

of their amortised acquisition cost and their market

value. The value adjustments, corresponding to the

negative difference between the market value and the

amortised acquisition cost, are not maintained if the

reasons for which the value adjustments were made

no longer exist.

Premiums included in the acquisition cost and

resulting from the purchase of bonds and other

fixed-income transferable securities included in this

portfolio at a price exceeding the amount repayable at

maturity are amortised in the profit and loss account

over the period remaining until repayment.

Asset swaps held in this portfolio are packaged deals

made of a fixed income transferable security and

a perfect cash flow swap, swapping the fixed rate

received on the fixed income transferable security for

a short term floating rate. Consequently, asset swaps

held in the structural portfolio are booked at their

par value and maintained at their par value.

20 --- Annual Report 08

2.5 – Valuation of variable-yield transferable securitiesParticipating interests and shares in affiliated

undertakings are recorded in the balance sheet at

their acquisition cost in their original currency. The

acquisition cost includes the costs to purchase the

assets. A value adjustment is made if the Board of

Directors considers that a permanent impairment exists

in their carrying value at the balance sheet date.

Companies in which the Bank directly and indirectly

exercises a significant influence are considered to

be affiliated undertakings. Participating interests

comprise rights in the capital of other undertakings,

the purpose of which is to contribute to the activity of

the company through a durable link.

In 2006 and 2007, the Bank participated in the

proportion of the capital held for two affiliated banks

in Serbia and Ukraine respectively. These share

participation however were totally controlled and

monitored by the Mother Company, EFG Eurobank

Ergasias S.A., and did not have the characteristics of

financial fixed assets and did not need impairment,

as the sale of these shares was already scheduled

with a predefined price. These participations were

not consolidated at the Bank level but at the Mother

Company level. In 2008, the participations held

in Serbia and Ukraine were sold at the scheduled

predefined price.

2.6 – Intangible and tangible fixed assetsIntangible and tangible fixed assets are valued at

cost less accumulated amortisation/depreciation.

Amortisation/depreciation is calculated on a straight-

line basis over the estimated useful life of individual

fixed assets.

2.6.1 Intangible assetsIntangible assets are represented by formation

expenses which are amortised on a straight-line basis

over 5 years and intangible assets in the form of

software and consultancy.

2.6.2 Tangible assetsTangible assets are used by the Bank for its own

operations. Tangible assets are valued at cost less

depreciation to date. Depreciation is calculated on a

straight-line basis over the life of the assets concerned.

The rates used for this purpose are:

2008 2007

% %

Furniture 18.0 18.0

Machinery and equipment 25.0 25.0

Vehicles 20.0 20.0

Hardware and software 25.0 25.0

Premises fixtures 10.0 10.0

Premises fixtures in leased offices are amortised over

the remaining lease period but not over more than

10 years.

2.7 – Derivative instruments2.7.1 Interest rate swapsInterest on interest rate swaps is included in the

balance sheet captions “Prepayments and accrued

income” and “Accruals and deferred income”. It is

credited or charged to interest receivable or payable

in the profit and loss account.

Interest rate swaps, which are not held for hedging

purposes, are marked to market. Provisions are made

for unrealised valuation losses whereas unrealised

valuation gains are not taken into account until

maturity. Interest rate swaps entered into for hedging

purposes are not valued.

2.7.2 Cross currency interest rate swaps (CCIRS)The currency element in a CCIRS is recorded as

explained in note 2.2.3 and the interest element as

stated in note 2.7.1 above.

notes to the annual accounts ( continued )

21eurobank eFG Private Bank Luxembourg s.A.

2.8 – Lump-sum provisionA general provision for potential losses on assets and

off balance sheet items is recorded on a risk weighted

basis. This provision, which is tax deductible, is

compensated with the related assets; the portion

of the provision relating to the off balance sheet

items is included in the provision for liabilities and

charges.

y

note 3 – use of financial instruments

3.1 – Strategy in using financial instruments The Bank’s treasury activities are primarily related to

the use of financial instruments including derivatives.

Since 2006 all treasury activities of the Bank are

carried out with the Treasury Department of the

Bank’s parent company in Athens, EFG Eurobank

Ergasias S.A.

Asset/Liability Management of the Bank is taking

into account other banking activities including private

banking client accounts, investment funds and inter-

bank activity mainly with EFG Eurobank Ergasias

S.A., Athens.

The Bank aims to use funds from customer operations,

investment funds operations and other market deposits

that have been raised at fixed and floating rates and

for various periods seeking to earn profitable margins

by investing these funds in high quality assets. Such

operations are only executed following the limits, as

well as defined products determined with the approval

of the Board of Directors. Limits are currently set in

such a way that restricts the Treasury and Foreign

Exchange Department of the Bank from taking large

exposures.

During periods of falling interest rates, the Bank

seeks to increase its margins by favouring short-term

funding and lending for longer periods at higher

rates whilst maintaining sufficient liquidity to meet

all claims that might fall due. During periods of

increasing interest rates, the Bank aims to increase

these margins by lending and borrowing in the short

term and by hedging its assets and liabilities.

Related issues and decisions are taken by the Asset

and Liability Management Committee of the Bank.

The Bank also raises its interest margin by obtaining

profitable margins through lending to business and

retail borrowers with a good credit standing. Loans

are given only when adequate collateral exists and

after the approval by the Credit Committee of the

Bank. The Bank also enters into guarantees and other

commitments such as letters of credit and letters of

guarantee.

The monitoring of limits and margins is carried out by

the Middle Office of the Bank on the basis of the daily

positions provided by the IT department. Middle

Office reports are communicated daily amongst

others to Local Management and the Head of Group

Treasury in Athens.

When limits are exceeded and margins not respected,

Local Management as well as the responsible Manager

are informed immediately. The excesses are also

reported to the Board of Directors on a quarterly basis.

HedgingThe Bank hedges part of its existing interest rate

risk resulting from any potential decrease in the fair

value of fixed rate assets denominated both in local

and foreign currencies using interest rate and cross

currency interest rate swaps.

The Bank hedges a proportion of foreign exchange

risk it expects to assume as a result of cash flows from

debt securities using currency swaps.

22 --- Annual Report 08

y

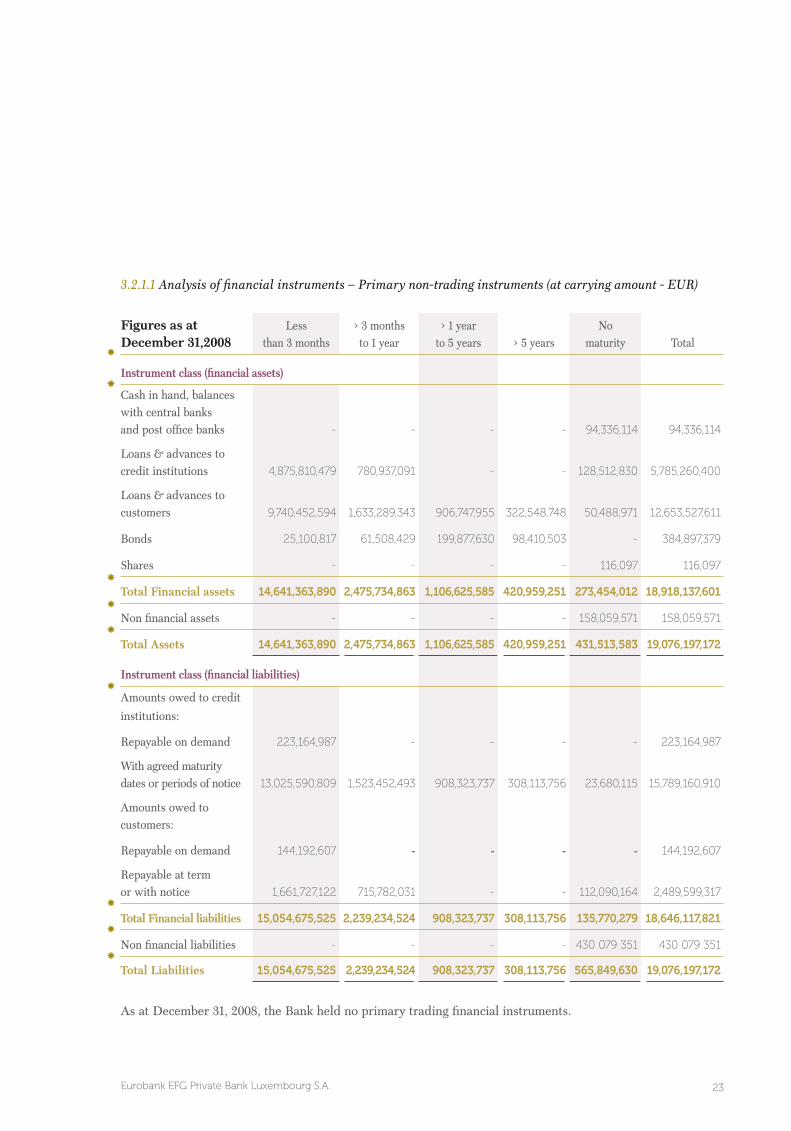

3.2 – Analysis of financial instruments3.2.1 Information on primary financial instrumentsThe table below analyses the level of primary financial

instruments (primary non-trading instruments and

primary trading instruments) of the Bank, in terms of

carrying amounts, into relevant maturity groupings

based on the remaining period at balance sheet date to

the contractual maturity date. Additional indication of

aggregate fair values of trading instruments is disclosed

where they differ materially from the amounts at which

they are included in the accounts.

“Fair value” is understood as being the amount at

which an asset could be exchanged or a liability settled

as part of an ordinary transaction entered into under

normal terms and conditions between independent,

informed and willing parties, other than in a forced or

liquidation sale.

notes to the annual accounts ( continued )

23eurobank eFG Private Bank Luxembourg s.A.

3.2.1.1 Analysis of financial instruments – Primary non-trading instruments (at carrying amount - EUR)

Figures as at December 31,2008

Less than 3 months

> 3 months to 1 year

> 1 year to 5 years > 5 years

No maturity Total

Instrument class (financial assets)

Cash in hand, balances with central banks and post office banks - - - - 94,336,114 94,336,114

Loans & advances to credit institutions 4,875,810,479 780,937,091 - - 128,512,830 5,785,260,400

Loans & advances to customers 9,740,452,594 1,633,289,343 906,747,955 322,548,748 50,488,971 12,653,527,611

Bonds 25,100,817 61,508,429 199,877,630 98,410,503 - 384,897,379

Shares - - - - 116,097 116,097

Total Financial assets 14,641,363,890 2,475,734,863 1,106,625,585 420,959,251 273,454,012 18,918,137,601

Non financial assets - - - - 158,059,571 158,059,571

Total Assets 14,641,363,890 2,475,734,863 1,106,625,585 420,959,251 431,513,583 19,076,197,172

Instrument class (financial liabilities)

Amounts owed to credit

institutions:

Repayable on demand 223,164,987 - - - - 223,164,987

With agreed maturity dates or periods of notice 13,025,590,809 1,523,452,493 908,323,737 308,113,756 23,680,115 15,789,160,910

Amounts owed to customers:

Repayable on demand 144,192,607 - - - - 144,192,607

Repayable at term or with notice 1,661,727,122 715,782,031 - - 112,090,164 2,489,599,317

Total Financial liabilities 15,054,675,525 2,239,234,524 908,323,737 308,113,756 135,770,279 18,646,117,821

Non financial liabilities - - - - 430 079 351 430 079 351

Total Liabilities 15,054,675,525 2,239,234,524 908,323,737 308,113,756 565,849,630 19,076,197,172

As at December 31, 2008, the Bank held no primary trading financial instruments.

y

y

y

y

y

y

y

y

y

24 --- Annual Report 08

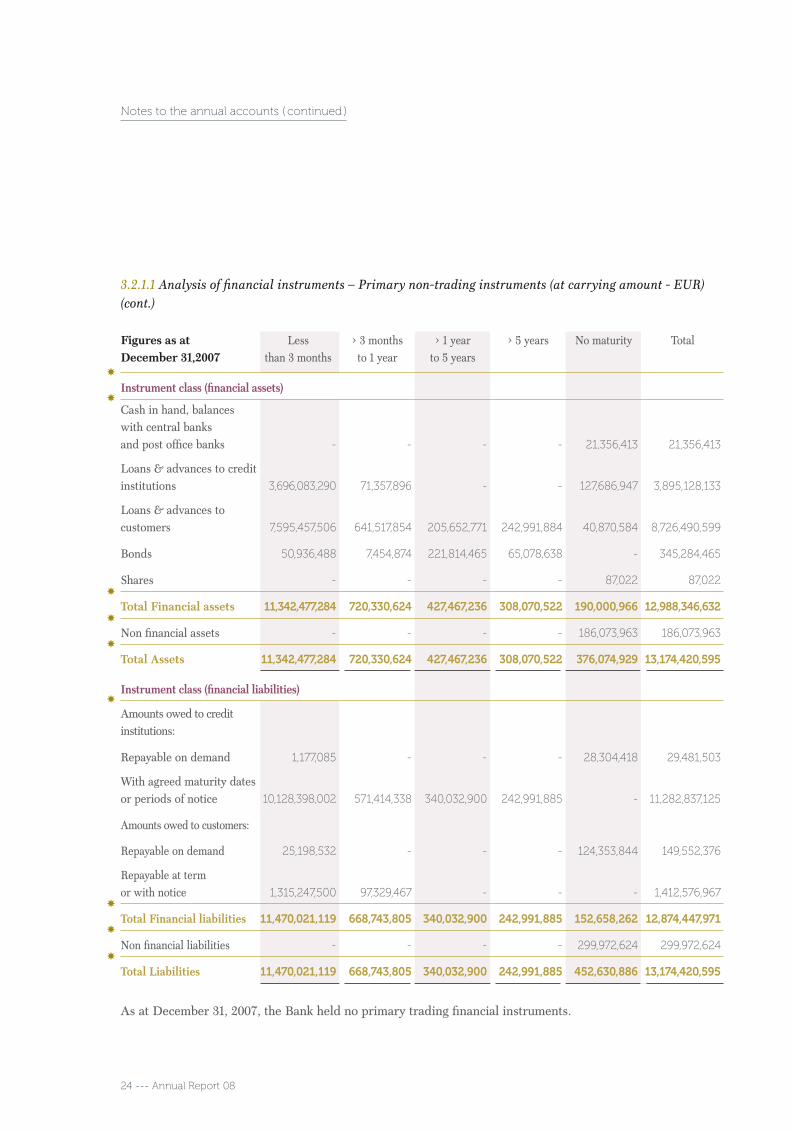

3.2.1.1 Analysis of financial instruments – Primary non-trading instruments (at carrying amount - EUR) (cont.)

Figures as at December 31,2007

Less than 3 months

> 3 months to 1 year

> 1 year to 5 years

> 5 years No maturity Total

Instrument class (financial assets)

Cash in hand, balances with central banks and post office banks - - - - 21,356,413 21,356,413

Loans & advances to credit institutions 3,696,083,290 71,357,896 - - 127,686,947 3,895,128,133

Loans & advances to customers 7,595,457,506 641,517,854 205,652,771 242,991,884 40,870,584 8,726,490,599

Bonds 50,936,488 7,454,874 221,814,465 65,078,638 - 345,284,465

Shares - - - - 87,022 87,022

Total Financial assets 11,342,477,284 720,330,624 427,467,236 308,070,522 190,000,966 12,988,346,632

Non financial assets - - - - 186,073,963 186,073,963

Total Assets 11,342,477,284 720,330,624 427,467,236 308,070,522 376,074,929 13,174,420,595

Instrument class (financial liabilities)

Amounts owed to credit institutions:

Repayable on demand 1,177,085 - - - 28,304,418 29,481,503

With agreed maturity dates or periods of notice 10,128,398,002 571,414,338 340,032,900 242,991,885 - 11,282,837,125

Amounts owed to customers:

Repayable on demand 25,198,532 - - - 124,353,844 149,552,376

Repayable at term or with notice 1,315,247,500 97,329,467 - - - 1,412,576,967

Total Financial liabilities 11,470,021,119 668,743,805 340,032,900 242,991,885 152,658,262 12,874,447,971

Non financial liabilities - - - - 299,972,624 299,972,624

Total Liabilities 11,470,021,119 668,743,805 340,032,900 242,991,885 452,630,886 13,174,420,595

As at December 31, 2007, the Bank held no primary trading financial instruments.

y

y

y

y

y

y

y

y

y

notes to the annual accounts ( continued )

25Eurobank EFG Private Bank Luxembourg S.A.

y

y

y

y

y

3.2.1.2 Description of derivative financial instruments used The Bank enters into the following derivative financial

instruments:

Currency forwards represent commitments to

purchase foreign and domestic currency, including

undelivered spot transactions.

Currency and interest rate swaps are commitments

to exchange one set of cash flows for another. Swaps

result in an economic exchange of currencies or

interest rates (for example, fixed rate for floating

rate) or a combination of all these (i.e. cross-currency

interest rate swaps). Except for certain currency

swaps, no exchange of principal takes place.

3.2.1.3 Analysis of derivative financial instrumentsThe table below analyses the level of derivative

financial instruments (trading and non-trading) of the

Bank, broken down in terms of notional amount, into

relevant maturity groupings based on the remaining

period at balance sheet date to the contractual

maturity date. The Bank held only OTC derivative

financial instruments as at December 31, 2008.

The notional amounts of certain types of financial

instruments provide a basis for comparison with

instruments recognised on the balance sheet but

do not necessarily indicate the amounts of future

cash flows involved or the current fair value of the

instruments and, therefore, do not indicate the Bank’s

exposure to credit or price risks. The derivative

instruments become favourable or unfavourable as

a result of fluctuations in market interest rates or

foreign exchange rates relative to their terms. The

aggregate contractual or notional amount of derivative

financial instruments on hand, the extent to which

instruments are favourable or unfavourable and, thus

the aggregate fair values of derivative financial assets

and liabilities can fluctuate significantly from time

to time.

y

Derivative non-trading instruments OTC as at December 31, 2008

Nominal amounts Net fair value

Figures as at December 31,2008

Less than 3 months

> 3 months to 1 year

> 1 year to 5 years > 5 years Total Total

Interest rates

Swaps (1) 22,107,117 - 117,029,820 - 139,136,937 (11,794,173)

Foreign exchange

Forwards 171,464,234 1,215,528 6,626,487 - 179,306,249 -

Swaps 198,658,523 - - 198,658,523 -

Total 392,229,874 1,215,528 123,656,307 - 517,101,709 (11,794,173)

(1) These correspond to the package deals mentioned in the note 2.4.3. The net fair value of the underlying securities amounts to EUR 111.5 mios.

The Bank held no exchange-traded derivative financial instrument and no trading OTC derivative financial

instrument as at December 31, 2008.

y

26 --- Annual Report 08

derivative non-trading instruments otc as at december 31, 2007

Nominal amounts Net fair value

Figures as at December 31, 2007

Less than 3 months

> 3 months to 1 year

> 1 year to 5 years > 5 years Total Total

Interest rates

Swaps (1) 23,893,257 - 84,862,228 - 108,755,485 (5,579,787)

Foreign exchange

Forwards 17,991,678 21,785,519 - - 39,777,197 3,104

Swaps 114,884,873 100,000 - - 114,984,873 (624,374)

Total 156,769,808 21,885,519 84,862,228 - 263,517,555 (6,201,057)

(1) These correspond to the package deals mentioned in the note 2.4.3. The net fair value of the underlying securities amounts to EUR 111.5 mios.

The Bank held no exchange-traded derivative financial instrument and no trading OTC derivative financial

instrument as at December 31, 2007.

y

3.3 – Credit risk3.3.1 Description of credit risk The Bank takes on exposure to credit risk. The Bank

structures the levels of credit risk it undertakes

by placing limits on the amount of risk accepted in

relation to one borrower or groups of borrowers, and

to geographical segments. Such risks are monitored

on a revolving basis and subject to monthly reviews.

Limits are approved by the Board of Directors and

reviewed at least annually. Under delegation of the

Board of Directors, Management has the possibility

to approve country limits up to a predetermined level.

The Board of Directors also determines who has the

authority to approve excesses and up to what level. The

excesses exceeding amounts and tenor defined within

Group Risk Guidelines are immediately reported

to Local Management and the Group Risk Unit in

Geneva (EFG Bank European Financial Group).

The exposure to any borrower including banks and

brokers is further restricted by sub-limits covering

on-and off balance sheet exposures. Actual exposures

against limits are monitored daily.

Exposure to credit risk is managed through regular

analysis of the ability of borrowers and potential

borrowers to meet interest and capital repayment

obligations and by changing these lending limits

where appropriate. Exposure to credit risk is primarily

managed by obtaining collateral and corporate and

personal guarantees.

The Group Risk Unit is setting types of collateral as

well as minimum margins. The Bank imposes more

strict collateral rules than those set by the group

based on careful analysis, internal policies and the

market environment. The Bank has a clear procedure

to approve “eligible” collateral and it periodically

reviews approved collateral.

On currency and interest rate swaps, the Bank’s

credit risk represents the potential cost to replace

y

y

y

y

y

notes to the annual accounts ( continued )

y

27eurobank eFG Private Bank Luxembourg s.A.

the swap contracts if counterparties fail to perform

their obligation. This risk is monitored on an ongoing

basis with reference to the current fair value and the

liquidity of the market. To control the level of credit

risk taken, the Bank assesses counterparties using the

same techniques as for its lending activities.

3.3.2 Measures of credit risk exposureInformation on credit risk as it relates to financial

instruments is disclosed on the basis of the carrying

amount that best represents the maximum credit risk

exposure at the balance sheet date without taking

account of any collateral.

With respect to derivative instruments not dealt on

a recognised, regulated market (OTC), the carrying

amount (principal or notional amount) does not reflect

the maximum risk exposure. The maximum exposure

to credit risk is determined by the value of the overall

replacement cost.

The table below discloses the level of credit exposure

in terms of notional amounts, replacement cost,

potential future credit exposure and net risk exposure

adjusted for any collateral, broken down by the

degree of creditworthiness of the counterparty based

on internal or external ratings.

y

credit Risk on otc derivative instruments (use of market risk method) as at december 31, 2008

Counterparty solvency (based on external/internal ratings)

Notional amount

Current Replacement

cost

Potential future

replacement cost

Overall replacement

cost CollateralNet risk exposure

(1) (2) (3)(4)=(2) + (3) -

Provision (5) (6) = (4) - (5)

External rating

A 429,092,279 4,986,367 4,024,703 9,011,979 - 9,011,979

Sub-total 1 9,011,979

Internal Rating

Customer & Fund

2 31,614,314 542,742 227,947 770,689 - 770,689

4 56,395,115 437,870 317,322 755,192 - 755,192

Sub-total 2 1,525,881

Total 10,537,860

y

y

y

y

y

28 --- Annual Report 08

credit Risk on otc derivative instruments (use of market risk method) as at december 31, 2007

Counterparty solvency (based on external/internal ratings)

Notional amount

Current Replacement

cost

Potential future

replacement cost

Overall replacement cost Collateral

Net risk exposure

(1) (2) (3)(4)=(2) + (3) -

Provision (5) (6) = (4) - (5)

External rating

A 227,079,765 175,866 1,768,501 1,944,367 - 1,944,367

AA 16,094,694 - - - - -

Sub-total 1 1,944,367

Internal Rating

Customer & Fund

2 19,496,744 - 79,673 79,673 - 79,673

4 493,188 14,036 4,932 12,853 - 12,853

Sub-total 1 92,526

Total 2,036,893

y

3.3.3 Concentrations of credit riskThe table below shows credit risk concentration as it relates to financial instruments from on- and off balance

sheet exposures by geographic location and economic sector.

Geographic credit risk concentrations

Geographical zone (by country or zone)

Credits and other balance sheet OTC derivatives

2008 2007 2008 2007

Luxembourg 8,396,334,392 5,456,947,515 56,395,116 -

Other European Monetary Union (EMU) countries 7,031,083,182 4,688,072,493 434,504,594 224,182,324

Other countries 3,648,779,598 3,029,400,587 26,202,000 39,335,231

Total 19,076,197,172 13,174,420,595 517,101,709 263,517,555

y

y

y

y

y

y

y

y

y

y

notes to the annual accounts ( continued )

y

y

y

29eurobank eFG Private Bank Luxembourg s.A.

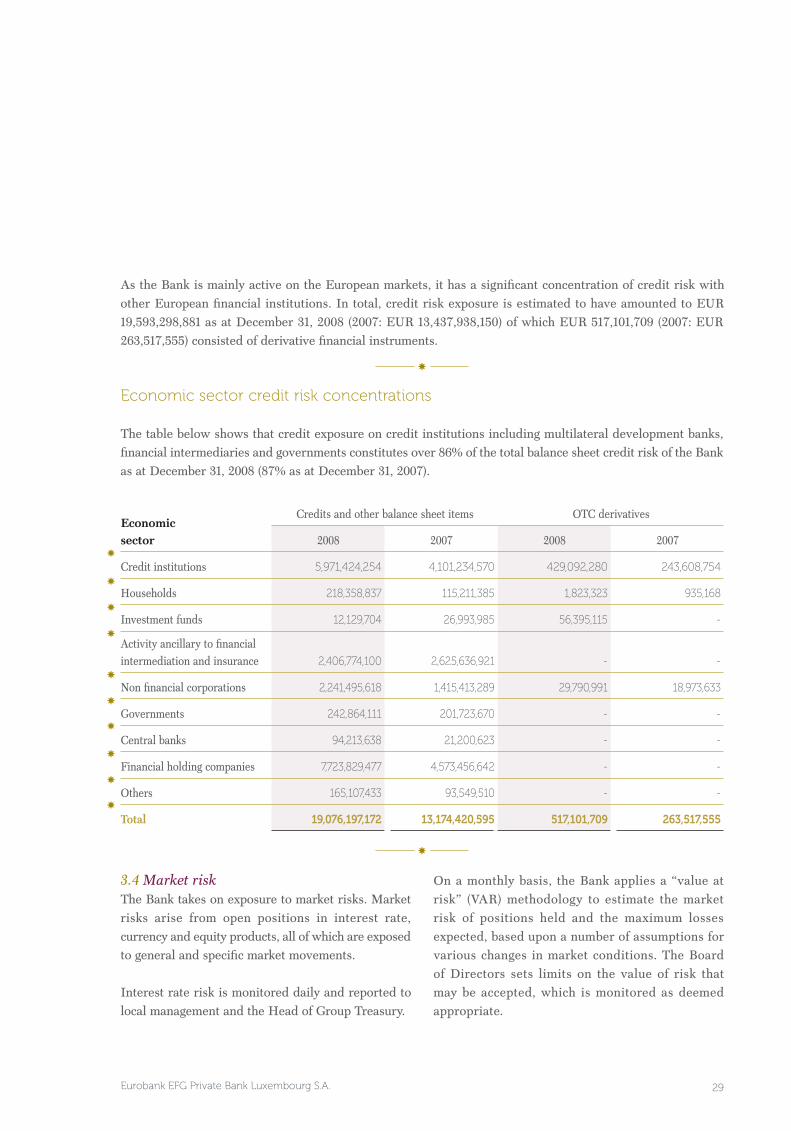

As the Bank is mainly active on the European markets, it has a significant concentration of credit risk with

other European financial institutions. In total, credit risk exposure is estimated to have amounted to EUR

19,593,298,881 as at December 31, 2008 (2007: EUR 13,437,938,150) of which EUR 517,101,709 (2007: EUR

263,517,555) consisted of derivative financial instruments.

y

economic sector credit risk concentrations

The table below shows that credit exposure on credit institutions including multilateral development banks,

financial intermediaries and governments constitutes over 86% of the total balance sheet credit risk of the Bank

as at December 31, 2008 (87% as at December 31, 2007).

Economic sector

Credits and other balance sheet items OTC derivatives

2008 2007 2008 2007

Credit institutions 5,971,424,254 4,101,234,570 429,092,280 243,608,754

Households 218,358,837 115,211,385 1,823,323 935,168

Investment funds 12,129,704 26,993,985 56,395,115 -

Activity ancillary to financial intermediation and insurance 2,406,774,100 2,625,636,921 - -

Non financial corporations 2,241,495,618 1,415,413,289 29,790,991 18,973,633

Governments 242,864,111 201,723,670 - -

Central banks 94,213,638 21,200,623 - -

Financial holding companies 7,723,829,477 4,573,456,642 - -

Others 165,107,433 93,549,510 - -

Total 19,076,197,172 13,174,420,595 517,101,709 263,517,555

y

3.4 Market riskThe Bank takes on exposure to market risks. Market

risks arise from open positions in interest rate,

currency and equity products, all of which are exposed

to general and specific market movements.

Interest rate risk is monitored daily and reported to

local management and the Head of Group Treasury.

On a monthly basis, the Bank applies a “value at

risk” (VAR) methodology to estimate the market

risk of positions held and the maximum losses

expected, based upon a number of assumptions for

various changes in market conditions. The Board

of Directors sets limits on the value of risk that

may be accepted, which is monitored as deemed

appropriate.

y

y

y

y

y

y

y

y

y

y

30 --- Annual Report 08

The Bank’s market risk reporting and the limit

structure is based on a measure of potential loss under

normal market conditions. The parameters used are:

X A 95% one tailed confidence level. This means that

the potential loss amount is the maximum amount

that could be lost, on average, on 95% of trading

days. Conversely it is the minimum loss that should

be expected on 5% of trading days;

X A 10-day holding period. This means that the Bank

measures risk assuming that exposures could not be

hedged or unwound in less than 10 working days; and

X A 180-day time series of changes in market variables.

This means that a 6-month history of market

movements is used to estimate likely changes in

market risk factors (volatilities and correlations).

Since VAR constitutes an integral part of the Bank’s

market risk control system, VAR limits are established

by the Board on all portfolio operations including

interest rate, FX and equities.

Exchange rate risk measurement incorporates factors

corresponding to individual foreign currencies in

which the Bank has material positions.

Interest rate risk measurement includes a set of risk

factors corresponding to interest rates in each of the

currencies in which the Bank has material interest

rate sensitive positions. For each currency, the yield

curve is divided into a number of maturity segments

in order to capture the variation in volatility of interest

rates at different points on the yield curve.

Equity prices risk measurement includes risk factors

corresponding to each of the national markets in

which the Bank has a material position. A market

index captures market-wide movement in equity

prices.

y

note 4 – cash in hand, balances with central banks and post office banks

In accordance with the requirements of the European

Central Bank, the Luxembourg Central Bank

implemented, effective January 1, 1999, a system

of mandatory minimum reserves which applies to

all Luxembourg credit institutions. The minimum

reserve balance as at December 31, 2008 held by the

Bank with the Luxembourg Central Bank amounted

to EUR 94,213,638 (2007: EUR 21,200,623).

y

notes to the annual accounts ( continued )

31eurobank eFG Private Bank Luxembourg s.A.

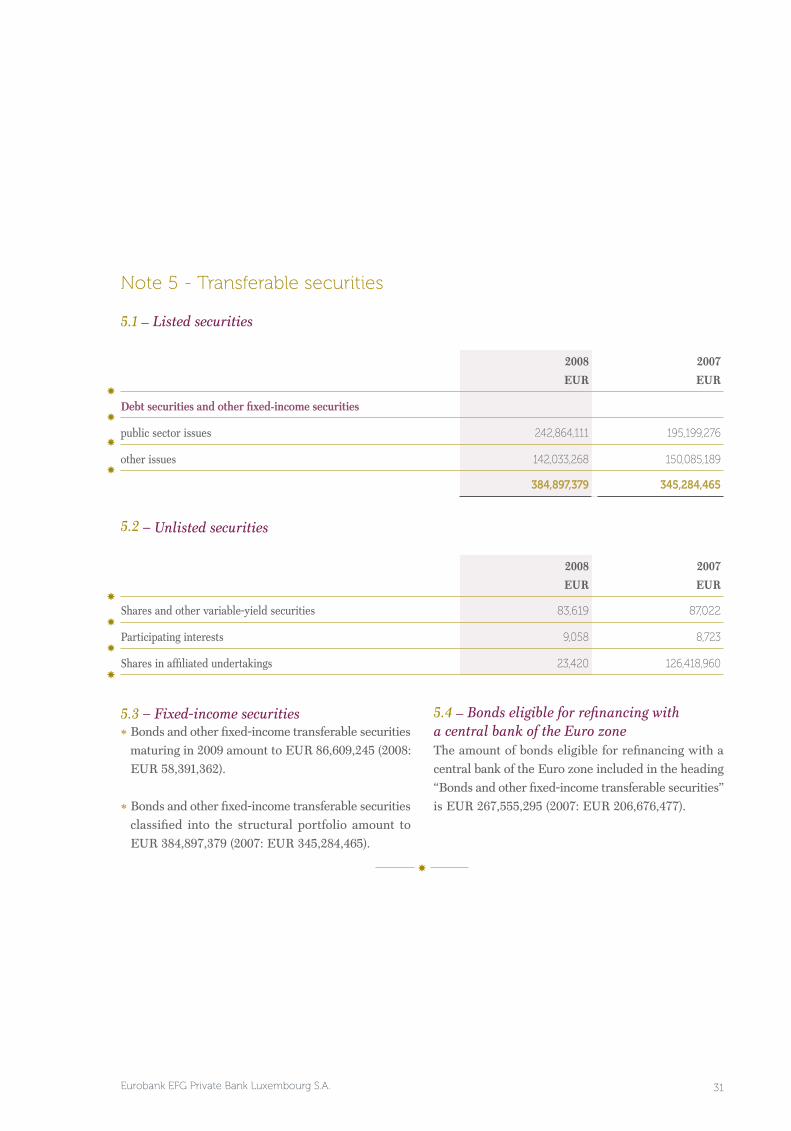

note 5 - transferable securities

5.1 – Listed securities

2008

EUR

2007

EUR

Debt securities and other fixed-income securities

public sector issues 242,864,111 195,199,276

other issues 142,033,268 150,085,189

384,897,379 345,284,465

5.2 – Unlisted securities

2008

EUR

2007

EUR

Shares and other variable-yield securities 83,619 87,022

Participating interests 9,058 8,723

Shares in affiliated undertakings 23,420 126,418,960

5.3 – Fixed-income securitiesX Bonds and other fixed-income transferable securities

maturing in 2009 amount to EUR 86,609,245 (2008:

EUR 58,391,362).

X Bonds and other fixed-income transferable securities

classified into the structural portfolio amount to

EUR 384,897,379 (2007: EUR 345,284,465).

5.4 – Bonds eligible for refinancing with a central bank of the Euro zoneThe amount of bonds eligible for refinancing with a

central bank of the Euro zone included in the heading

“Bonds and other fixed-income transferable securities”

is EUR 267,555,295 (2007: EUR 206,676,477).

y

y

y

y

y

y

y

y

y

32 --- Annual Report 08

notes to the annual accounts ( continued )

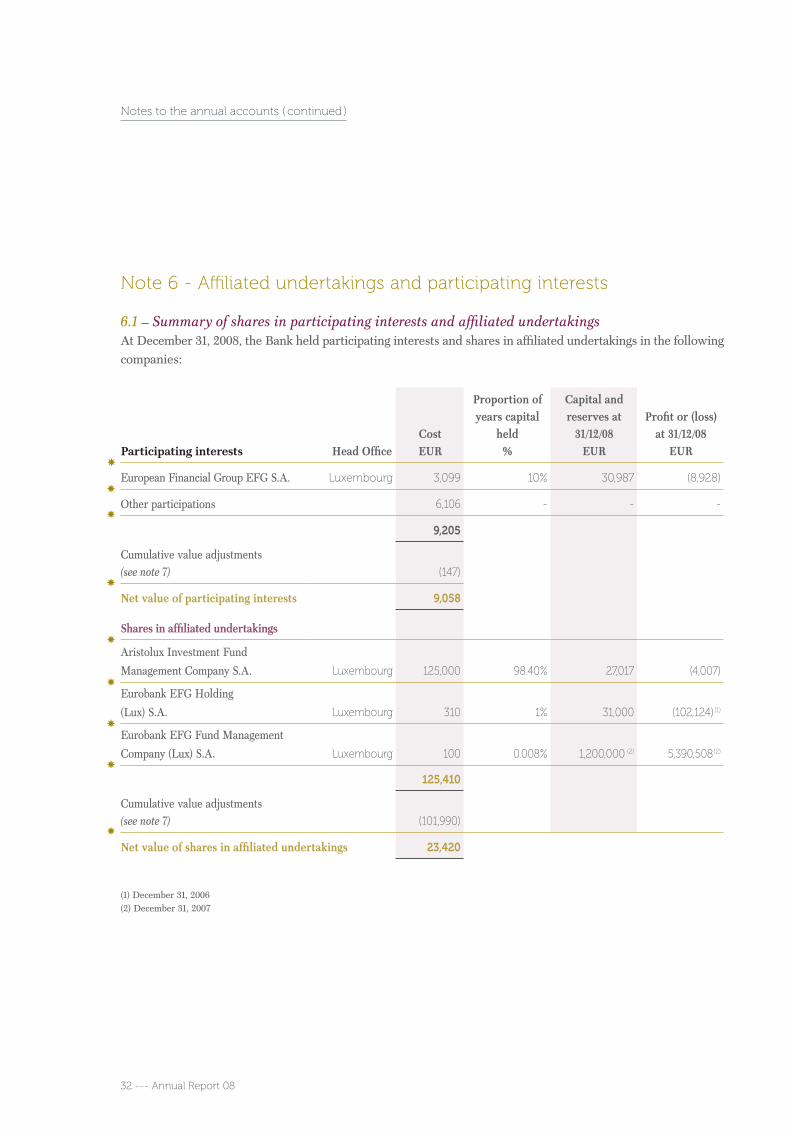

note 6 - Affiliated undertakings and participating interests

6.1 – Summary of shares in participating interests and affiliated undertakingsAt December 31, 2008, the Bank held participating interests and shares in affiliated undertakings in the following

companies:

Participating interests Head OfficeCostEUR

Proportion of years capital

held%

Capital and reserves at

31/12/08EUR

Profit or (loss) at 31/12/08

EUR

European Financial Group EFG S.A. Luxembourg 3,099 10% 30,987 (8,928)

Other participations 6,106 - - -

9,205

Cumulative value adjustments (see note 7) (147)

Net value of participating interests 9,058

Shares in affiliated undertakings

Aristolux Investment Fund

Management Company S.A. Luxembourg 125,000 98.40% 27,017 (4,007)

Eurobank EFG Holding

(Lux) S.A. Luxembourg 310 1% 31,000 (102,124) (1)

Eurobank EFG Fund Management

Company (Lux) S.A. Luxembourg 100 0.008% 1,200,000 (2) 5,390,508 (2)

125,410

Cumulative value adjustments (see note 7) (101,990)

Net value of shares in affiliated undertakings 23,420

(1) December 31, 2006(2) December 31, 2007

y

y

y

y

y

y

y

y

y

33eurobank eFG Private Bank Luxembourg s.A.

6.2 – Transactions with other Group Companies

2008

EUR

2007

EUR

Assets

Loans and advances to credit institutions 5,784,504,488 3,848,750,053

Loans and advances to customers 10,039,199,009 7,015,415,234

15,823,703,497 10,864,165,287

Liabilities

Amounts owed to credit institutions 13,208,720,032 10,297,781,073

Amounts owed to customers 2,008,801,000 845,457,605

Subordinated liabilities 116,752,491 116,752,491

15,334,273,523 11,259,991,169

y

y

y

y

y

y

y

y

y

34 --- Annual Report 08

notes to the annual accounts ( continued )

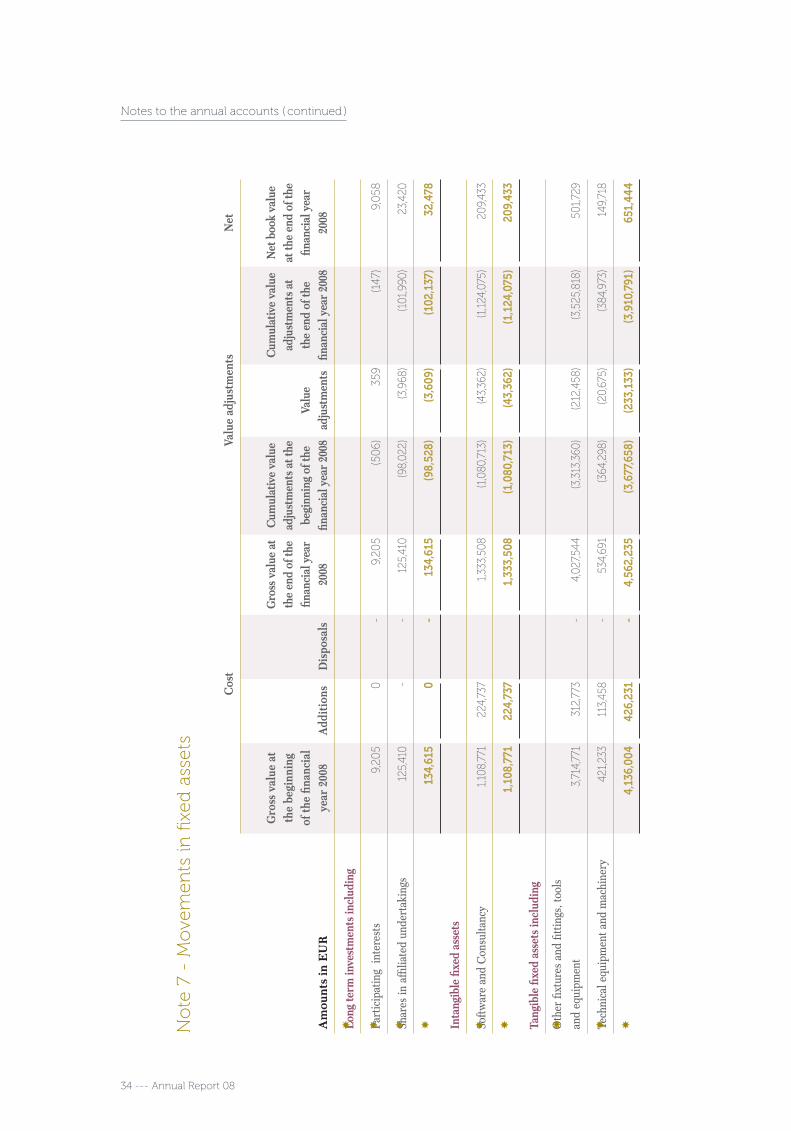

no

te 7

- M

ove

men

ts in

fixe

d a

sset

s

Cos

tVa

lue

adju

stm

ents

Net

Am

oun

ts in

EU

R

Gro

ss v

alue

at

the

begi

nnin

g of

the

finan

cial

ye

ar 2

008

Add

itio

nsD

ispo

sals

Gro

ss v

alue

at

the

end

of th

e fin

anci

al y

ear

2008

Cum

ulat

ive

valu

e ad

just

men

ts a

t the

be

ginn

ing

of th

e fin

anci

al y

ear

2008

Valu

e ad

just

men

ts

Cum

ulat

ive

valu

e ad

just

men

ts a

t th

e en

d of

the

finan

cial

yea

r 20

08

Net

boo

k va

lue

at th

e en

d of

the

finan

cial

yea

r 20

08

Long

term

inve

stm

ents

incl

udin

g

Part

icip

atin

g in

tere

sts

9,20

50

-9,

205

(50

6)35

9(1

47)

9,0

58

Shar

es in

affi

liate

d un

dert

akin

gs12

5,41

0-

-12

5,41

0(9

8,02

2)(3

,968

)(1

01,9

90)

23,4

20

134

,615

0-

134,

615

(98,

528)

(3,6

09)

(102

,137

)32

,478

Inta

ngib

le fi

xed

asse

ts

Softw

are

and

Con

sulta

ncy

1,10

8,77

122

4,73

71,

333,

508

(1,0

80,7

13)

(43,

362)

(1,1

24,0

75)

209,

433

1,10

8,77

122

4,73

71,

333,

508

(1,0

80,7

13)

(43,

362)

(1,1

24,0

75)

209,

433

Tang

ible

fixe

d as

sets

incl

udin

g

Oth

er fi

xtur

es a

nd fi

tting

s, to

ols

and

equi

pmen

t3,

714,

771

312,

773

-4,

027,5

44(3

,313

,360

)(2

12,4

58)

(3,5

25,8

18)

501,7

29

Tech

nica

l equ

ipm

ent a

nd m

achi

nery

421,

233

113,

458

-53

4,69

1(3

64,2

98)

(20,

675)

(384

,973

)14

9,71

8

4,13

6,00

442

6,23

1-

4,56

2,23

5(3

,677

,658

)(2

33,1

33)

(3,9

10,7

91)

651,

444

y y y y y y y y y

35eurobank eFG Private Bank Luxembourg s.A.

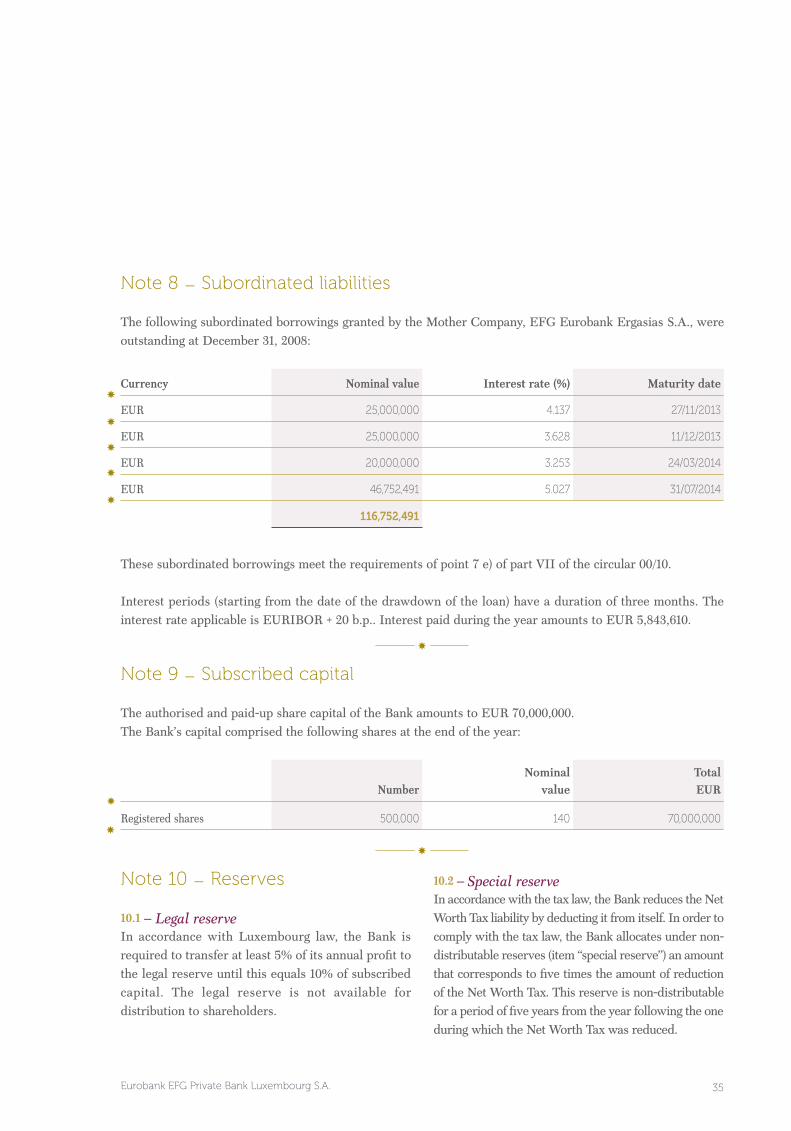

note 8 – subordinated liabilities

The following subordinated borrowings granted by the Mother Company, EFG Eurobank Ergasias S.A., were

outstanding at December 31, 2008:

Currency Nominal value Interest rate (%) Maturity date

EUR 25,000,000 4.137 27/11/2013

EUR 25,000,000 3.628 11/12/2013

EUR 20,000,000 3.253 24/03/2014

EUR 46,752,491 5.027 31/07/2014

116,752,491

These subordinated borrowings meet the requirements of point 7 e) of part VII of the circular 00/10.

Interest periods (starting from the date of the drawdown of the loan) have a duration of three months. The

interest rate applicable is EURIBOR + 20 b.p.. Interest paid during the year amounts to EUR 5,843,610.

y

note 9 – subscribed capital

The authorised and paid-up share capital of the Bank amounts to EUR 70,000,000.

The Bank’s capital comprised the following shares at the end of the year:

NumberNominal

valueTotalEUR

Registered shares 500,000 140 70,000,000

y

note 10 – Reserves

10.1 – Legal reserveIn accordance with Luxembourg law, the Bank is

required to transfer at least 5% of its annual profit to

the legal reserve until this equals 10% of subscribed

capital. The legal reserve is not available for

distribution to shareholders.

10.2 – Special reserveIn accordance with the tax law, the Bank reduces the Net

Worth Tax liability by deducting it from itself. In order to

comply with the tax law, the Bank allocates under non-

distributable reserves (item “special reserve”) an amount

that corresponds to five times the amount of reduction

of the Net Worth Tax. This reserve is non-distributable

for a period of five years from the year following the one

during which the Net Worth Tax was reduced.

y

y

y

y

y

y

y

36 --- Annual Report 08

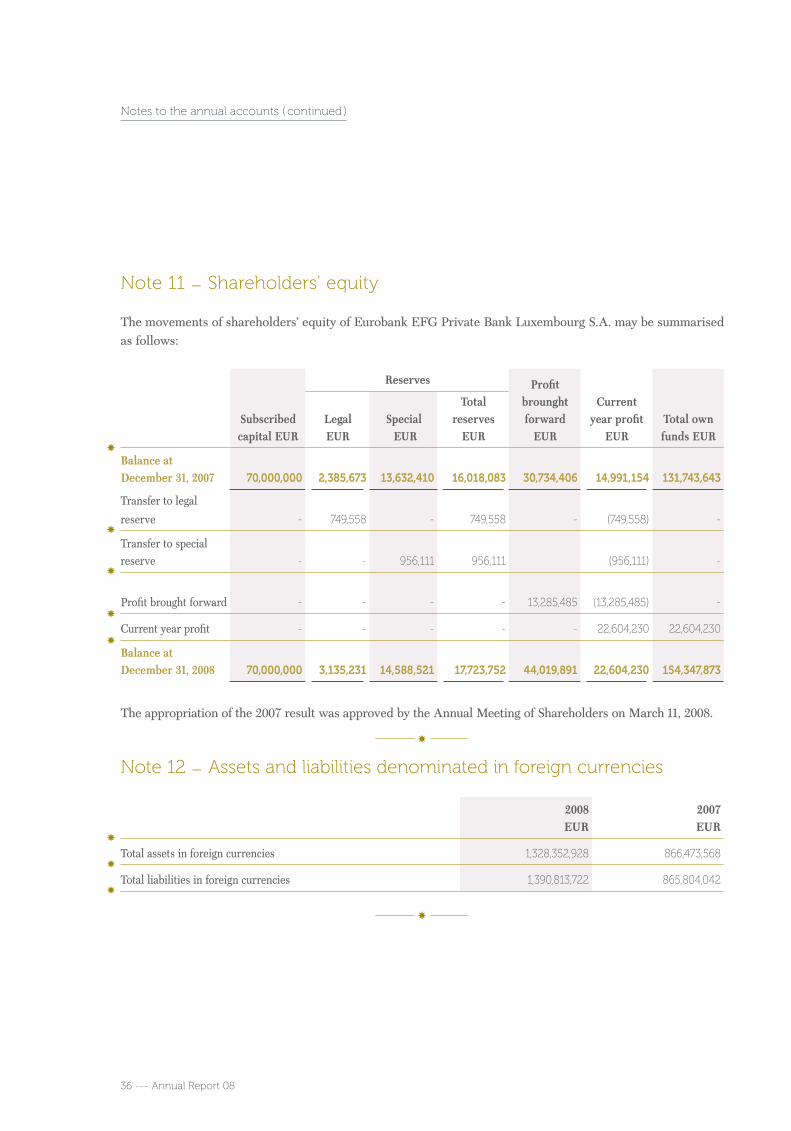

note 11 – shareholders’ equity

The movements of shareholders’ equity of Eurobank EFG Private Bank Luxembourg S.A. may be summarised

as follows:

Subscribed capital EUR

Reserves Profit brounght forward

EUR

Current year profit

EURTotal own funds EUR

Legal EUR

Special EUR

Total reserves

EUR

Balance at December 31, 2007 70,000,000 2,385,673 13,632,410 16,018,083 30,734,406 14,991,154 131,743,643

Transfer to legal

reserve - 749,558 - 749,558 - (749,558) -

Transfer to special reserve - - 956,111 956,111 (956,111) -

Profit brought forward - - - - 13,285,485 (13,285,485) -

Current year profit - - - - - 22,604,230 22,604,230

Balance at December 31, 2008 70,000,000 3,135,231 14,588,521 17,723,752 44,019,891 22,604,230 154,347,873

The appropriation of the 2007 result was approved by the Annual Meeting of Shareholders on March 11, 2008.

y

note 12 – Assets and liabilities denominated in foreign currencies

2008 EUR

2007 EUR

Total assets in foreign currencies 1,328,352,928 866,473,568

Total liabilities in foreign currencies 1,390,813,722 865,804,042

y

notes to the annual accounts ( continued )

y

y

y

y

y

y

y

y

37eurobank eFG Private Bank Luxembourg s.A.

note 13 – contingent liabilities and commitments

13.1 – Contingent liabilitiesContingent liabilities included in off balance sheet accounts at December 31, 2008 comprised:

2008

EUR

2007

EUR

Guarantees and other direct substitutes for credit 16,603,089 36,321,445

13.2 – Other off balance sheet commitments

2008

EUR

2007

EUR

Assets held on behalf of third parties 3,275,089,483 6,840,156,055

Credits confirmed but not used 1,336,340,086 1,373,977,261

Repurchase agreements 3,227,912,778 940,155,531

Interest rate swaps 139,136,236 108,755,486

Forward foreign exchange transactions 400,973,398 154,762,069

Fiduciary operations 72,601,773 49,353,181

Other 216,464 37,407

The repurchase agreements represent firm sales and repurchase contracts of securities mainly with the

Luxembourg Central Bank.

y

13.3 – Deposit Guarantee SchemeAll credit institutions in Luxembourg are a member of

the non-profit making “Association pour la Garantie

des Dépôts, Luxembourg” (AGDL).

The exclusive objective of the AGDL is the

establishment of a system of mutual guarantee of cash

deposits and of receivables arising from investment

operations made by individuals with members of

the AGDL, without distinction of their nationality

or residence, by corporations incorporated under

Luxembourg or another European Union member

state law, which are authorised, because of their size,

to prepare an abridged balance sheet in conformity

with the applicable law, as well as by those

corporations of a similar size as defined by law of

another European Union member state.

The AGDL reimburses to the deposit holder the

amount of his guaranteed cash deposits and to the

investor the amount of his guaranteed receivable with

a maximum foreign currency equivalent limit of EUR

20,000 per guaranteed cash deposit and EUR 20,000

per guaranteed receivable arising from investment

y

y

y

y

y

y

y

y

y

y

38 --- Annual Report 08

operations other than that relating to a cash deposit.

At December 31, 2008, the Bank has a remaining

provision (EUR 55,906; 2007: EUR 0) in connection

with this deposit guarantee and investor compensation

scheme corresponding to the maximum claim made

by the AGDL in 2008. The 2008 payments requested

by the AGDL (EUR 117,997; 2007: EUR 0) have been

recorded against the provision.

13.4 – Management and representative servicesThe Bank has provided the following management

and representative services to third parties in the

course of the financial year:

X Investment management and advice;

X Safekeeping and administration of securities;

X Fiduciary services;

X Agency services.

y

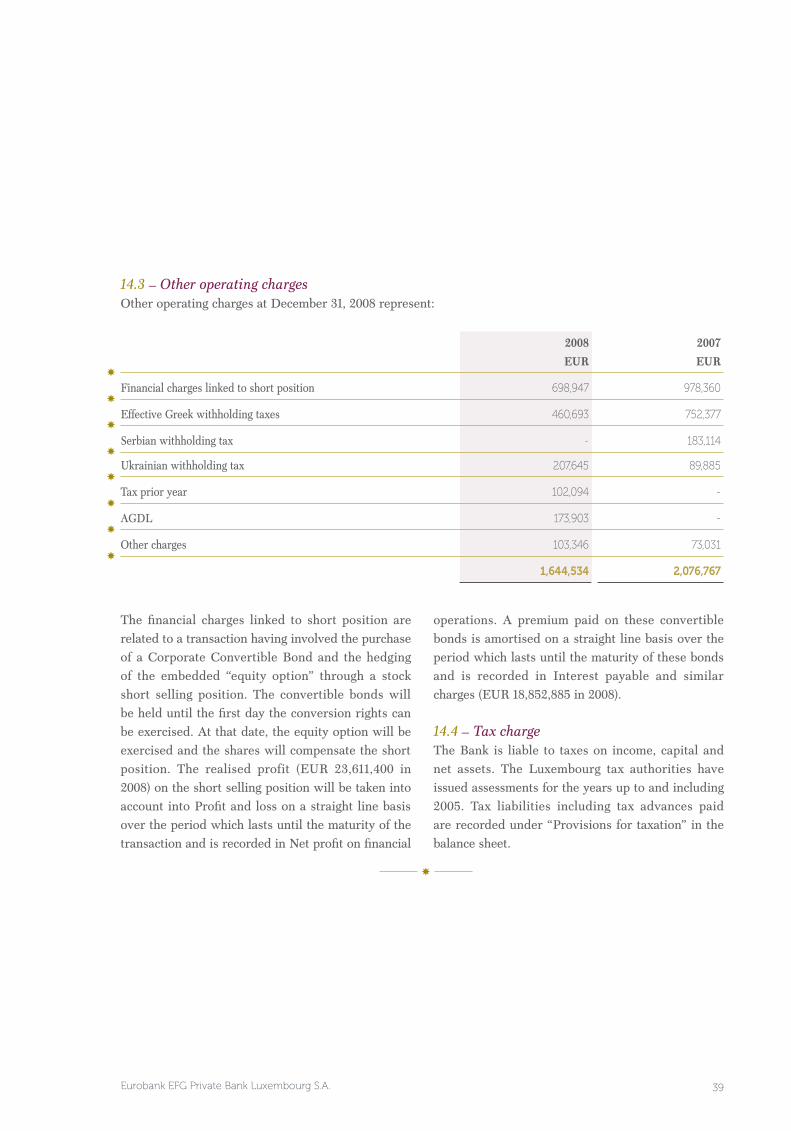

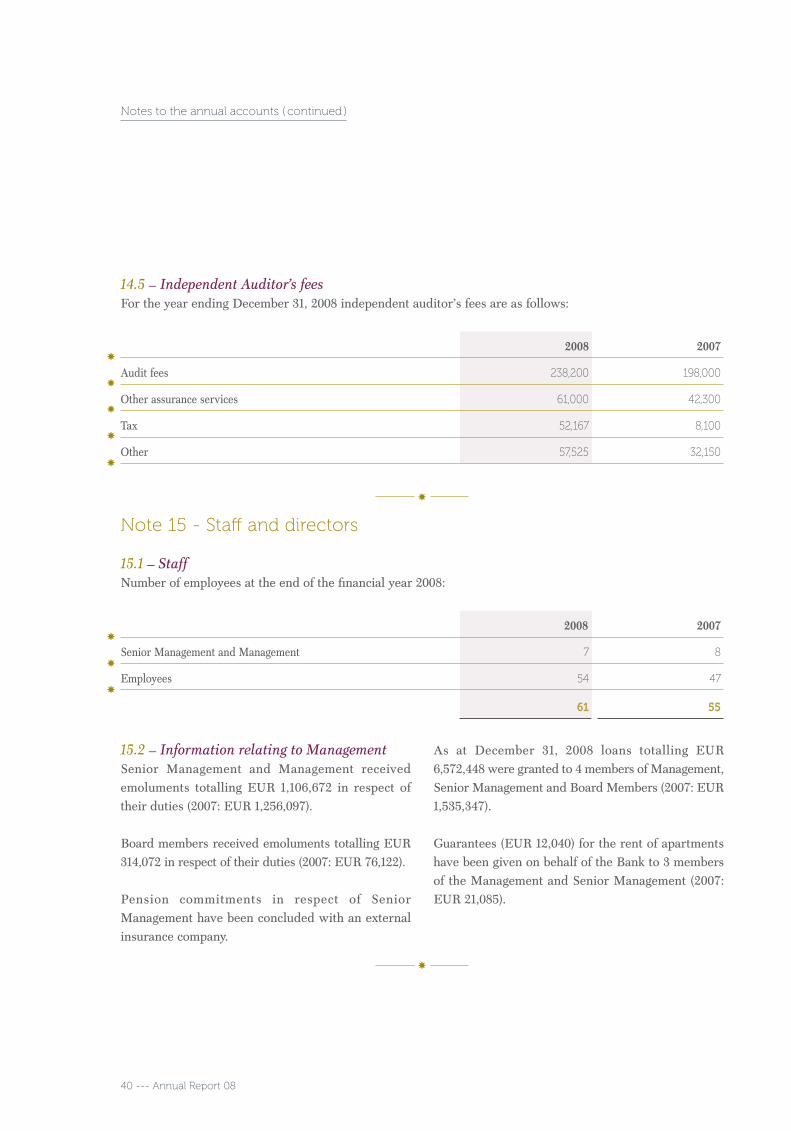

note 14 – Profit and loss account

14.1 – Sources of income by geographical region (OECD)By application of Article 69 of the law of June 17, 1992 on the annual accounts of credit institutions, sources of

income have not been analysed by geographical region.

14.2 – Other operating incomeOther operating income at December 31, 2008 represents:

2008

EUR

2007

EUR