Intake/Interview & Quality Review Training 2021 Filing Season

Annual Filing Season ProgramBy: Genaro S. Cardaropoli, CPA and Ben Kotenberg

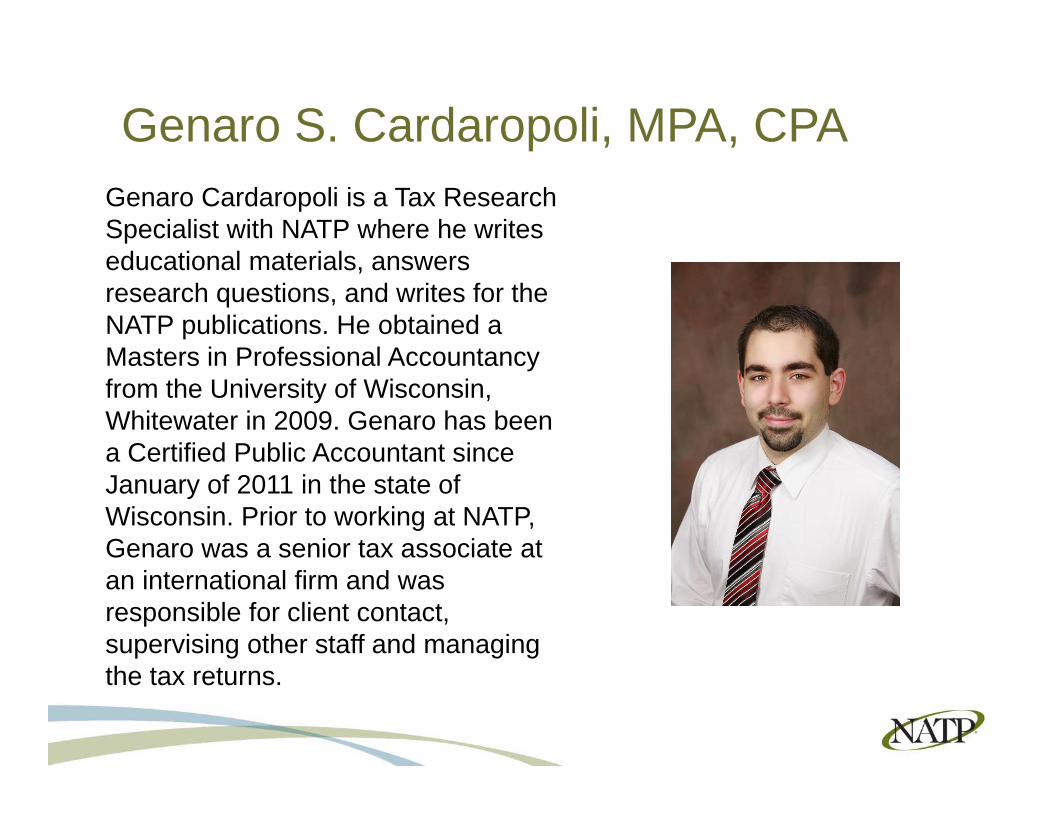

Genaro S. Cardaropoli, MPA, CPAGenaro Cardaropoli is a Tax Research Specialist with NATP where he writes educational materials, answers research questions, and writes for the NATP publications. He obtained a Masters in Professional Accountancy from the University of Wisconsin, Whitewater in 2009. Genaro has been a Certified Public Accountant since January of 2011 in the state of Wisconsin. Prior to working at NATP, Genaro was a senior tax associate at an international firm and was responsible for client contact, supervising other staff and managing the tax returns.

Benjamin T. Kotenberg

Ben Kotenberg is an Instructional Designer with NATP where he creates educational and multimedia materials for self-study and live courses, webinars and conference sessions. Ben obtained his Master of Science degree in Communication from Illinois State University in 2010. Prior to joining NATP, Ben was a Professor at the University of Wisconsin and Corporate Trainer at the J. F. Ahern Co..

Our mission is simple — to serve our members by providing the support, education, products, and services they need to succeed in the tax profession. The National Association of Tax Professionals

(NATP) is the largest nonprofit organization that serves individuals specializing in tax preparation.

About NATP

In this information-packed session, you will learn: The details of the Annual Filing Season Program

(AFSP) If you are exempt from the Annual Federal Tax

Refresher (AFTR) course and exam How to participate in the AFSP, whether you are

credentialed or non-credentialed The benefits of participating in the AFSP Important changes to your representation rights

Objectives

A voluntary program for tax preparers building on similar concepts established under the registered tax return preparer program (RTRP) targeting unenrolled preparers Encourages continuing education

and competency in federal tax law Record of Completion Public Directory Effective January 2015

What is the Annual Filing Season Program?

You must have a valid PTIN You must take a six (6) credit hour Annual Federal Tax

Refresher (AFTR) course You must pass an annual 100-question comprehensive exam

with a 70% or higher passing score In addition to the AFTR course, you must complete ten (10)

credit hours of federal tax law and two (2) credit hours of ethics annually

The 18 CPE and a passing score on the annual exam must be completed no later than December 31 effective for the following filing season

You must consent, under penalties of perjury, to the duties and responsibilities under Subpart B of Circular 230

Requirements

Enrolled agents CPAs Attorneys Those who have successfully passed the RTRP exam Those who have successfully passed Part I of the Special

Enrollment Exam (EA exam) during the two year eligibility window

Those who have successfully passed state based return preparer testing programs (i.e., Oregon and California)

Those who have successfully passed the Accredited Tax Preparer (ATP) test offered by the Accreditation Council for Accountancy/Taxation (ACAT)

Successful VITA program participants, reviewers and instructors

Who is exempt?

If you are exempt from the annual exam and refresher course you can still receive a record of

completion by completing the continuing education requirements

Exempt Individuals

In 2014 RTRP’s must complete: 3 Hours – Federal Tax Updates 3 Hours – Federal Tax Law 2 Hours – Ethics Renew PTIN Sign Circular 230 Consent

2015 15 Hours of CPE Renew PTIN Sign Circular 230 Consent

RTRP’s are not required to complete the AFTR course or exam

RTRP’s

Annual course designed to help Tax Professionals work efficiently and effectively with clients on their annual returns Covers the latest taw law theory and key

information that is critical to preparing an accurate return Focuses on important aspects of

representation and ethics

What is the AFTR Course?

A maximum of 6 CPE Offered by IRS-approved

Continuing Education Providers Covers tax law across three

domains New Tax Law/Recent Updates Federal Tax Law General Review Ethics, Practices and Procedures

Minimum 70% passing score on 100-question comprehension exam

AFTR Course Requirements

Includes all tax law topics covered in the AFTR course Consists of a minimum of 100

questions made up of multiple choice and True/False style questions You will have a maximum of 3

hours to complete the exam You will have unlimited attempts to

pass You must complete the course

before taking the exam

The exam

CPE is prorated for 2014 only. All CPE obtained since January 1, 2014 that

meets the AFSP requirements will count toward your total CPE requirement.

How much CPE do I need for 2014?

2 hours of ethics 3 hours of federal tax topics 3 hours of federal update

Total of 8 CPE for 2014

Exempt Individuals

6 hours of AFTR 3 hours of federal tax topics 2 hours of ethics

Total of 11 CPE for 2014

Non-Exempt Individuals

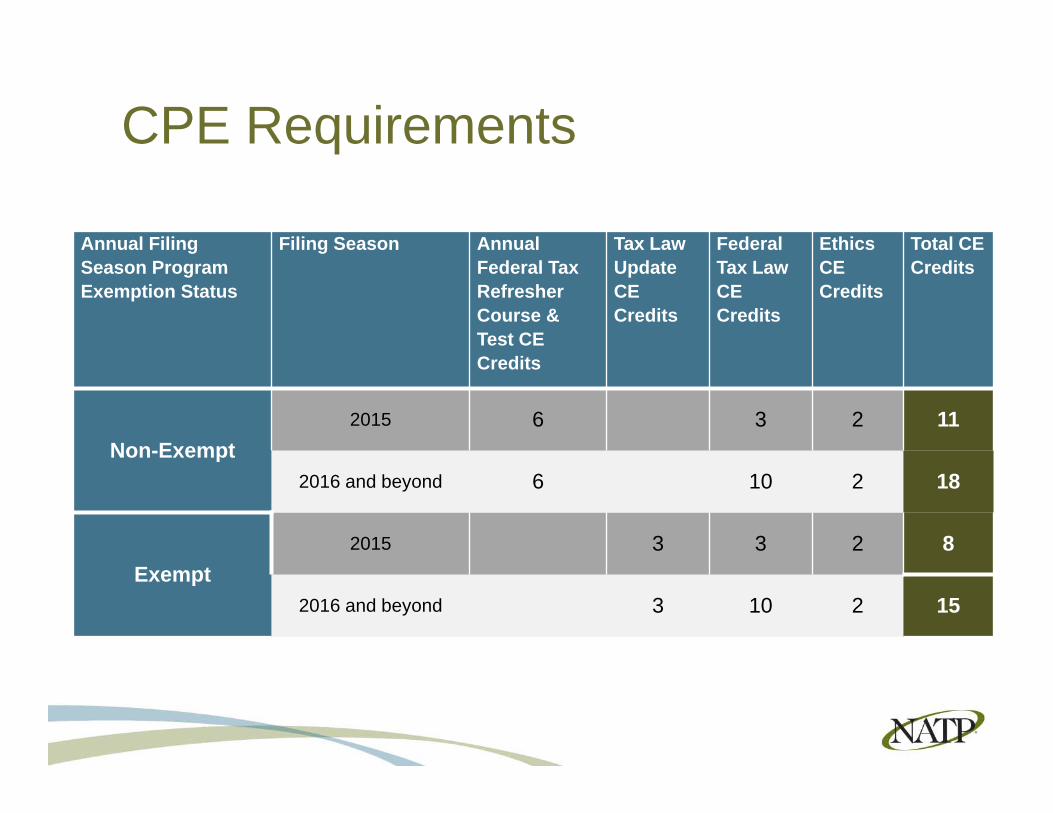

Annual Filing Season Program Exemption Status

Filing Season Annual Federal Tax Refresher Course & Test CE Credits

Tax Law Update CE Credits

Federal Tax Law CE Credits

Ethics CE Credits

Total CE Credits

Non-Exempt2015 6 3 2 11

2016 and beyond 6 10 2 18

Exempt2015 3 3 2 8

2016 and beyond 3 10 2 15

CPE Requirements

Your name will be included in a public IRS database of approved tax return preparers You will have limited

representation rights for returns you prepared and signed Encourages you to remain

current with changing tax laws You will receive a record of

completion certificate from the IRS

What’s in it for you?

A searchable, sortable public directory available on IRS.gov January 2015

Will include the name, city, state and zip code of all attorneys, CPAs, EAs and AFSP participants who have obtained a Record of Completion and who have a valid PTIN

After 2015 RTRPs will NOT be included unless they participated in the AFSP program

Allows taxpayers to find a preparer based on location and credentials

IRS database

You must have a valid PTIN You must complete all

required CPE You must pass the exam

Record of completion

Exempt individuals with a valid PTIN will automatically receive a record of completion

once all CPE requirements are met

Differentiates you from other preparers

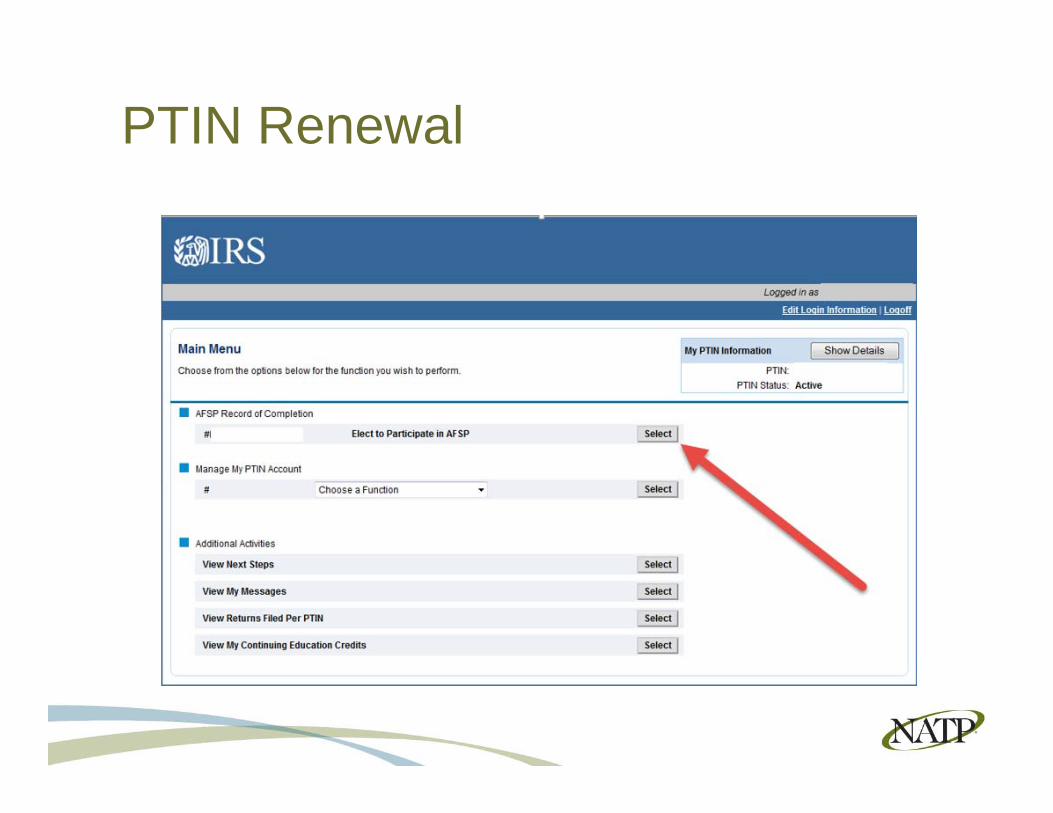

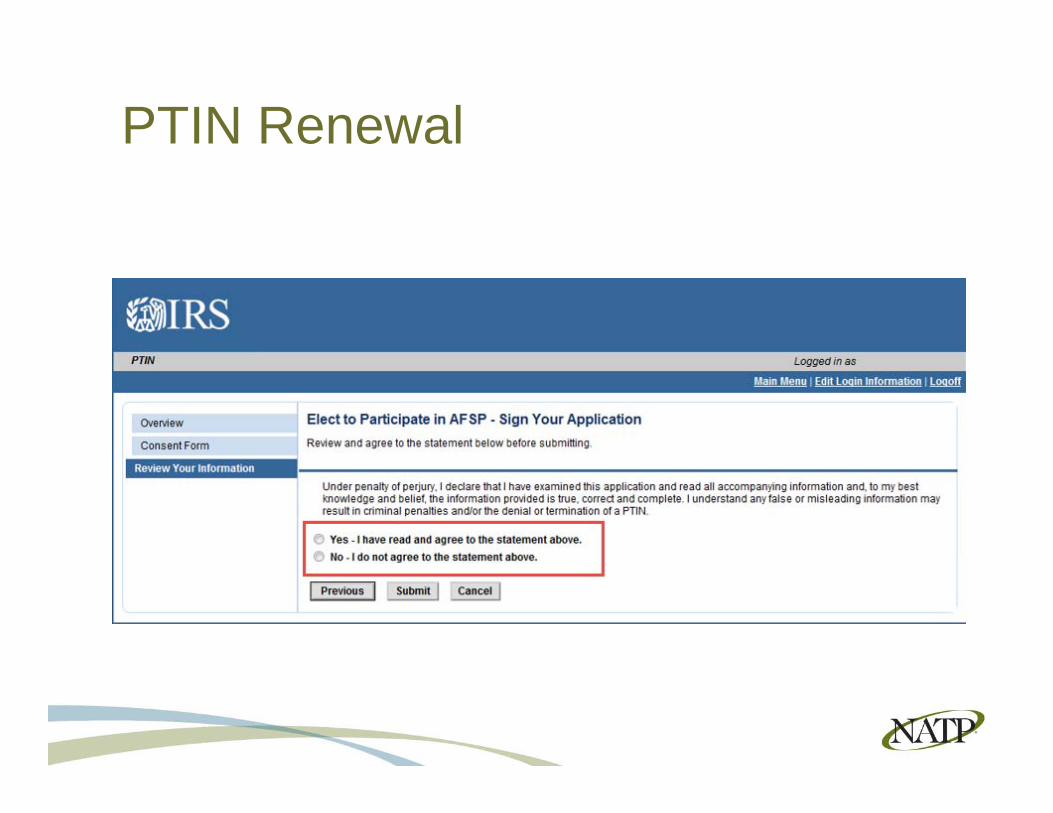

PTIN Renewal

PTIN Renewal

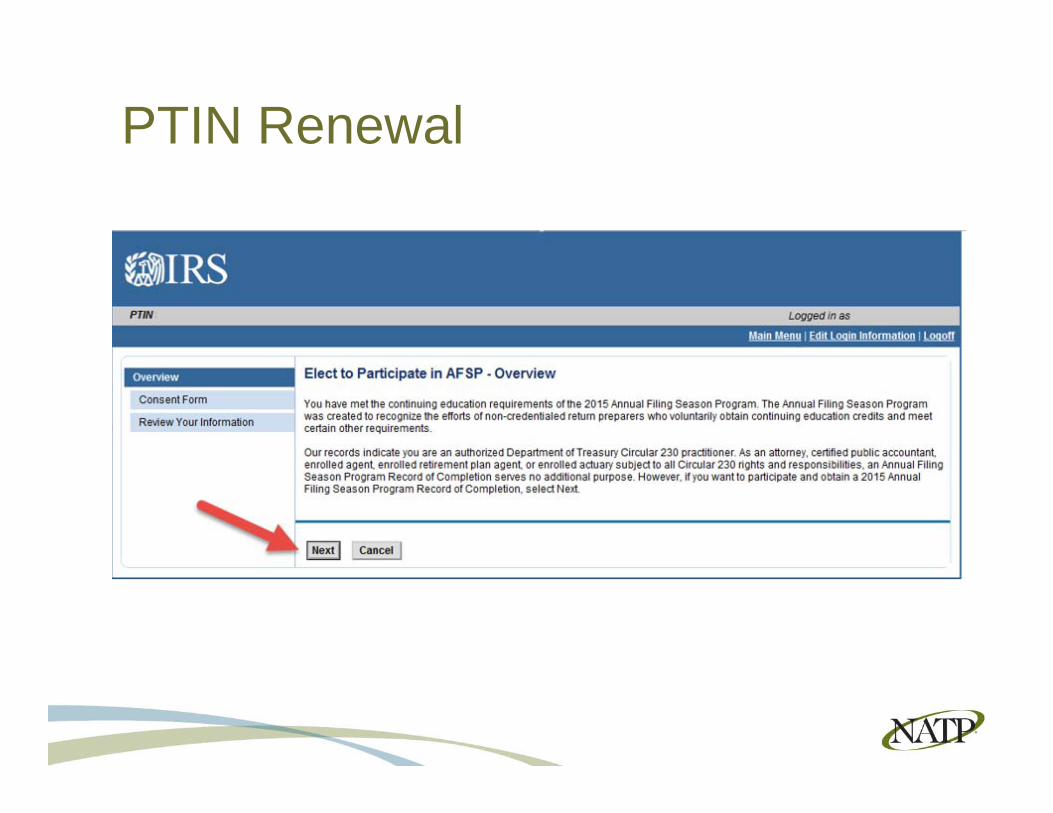

PTIN Renewal

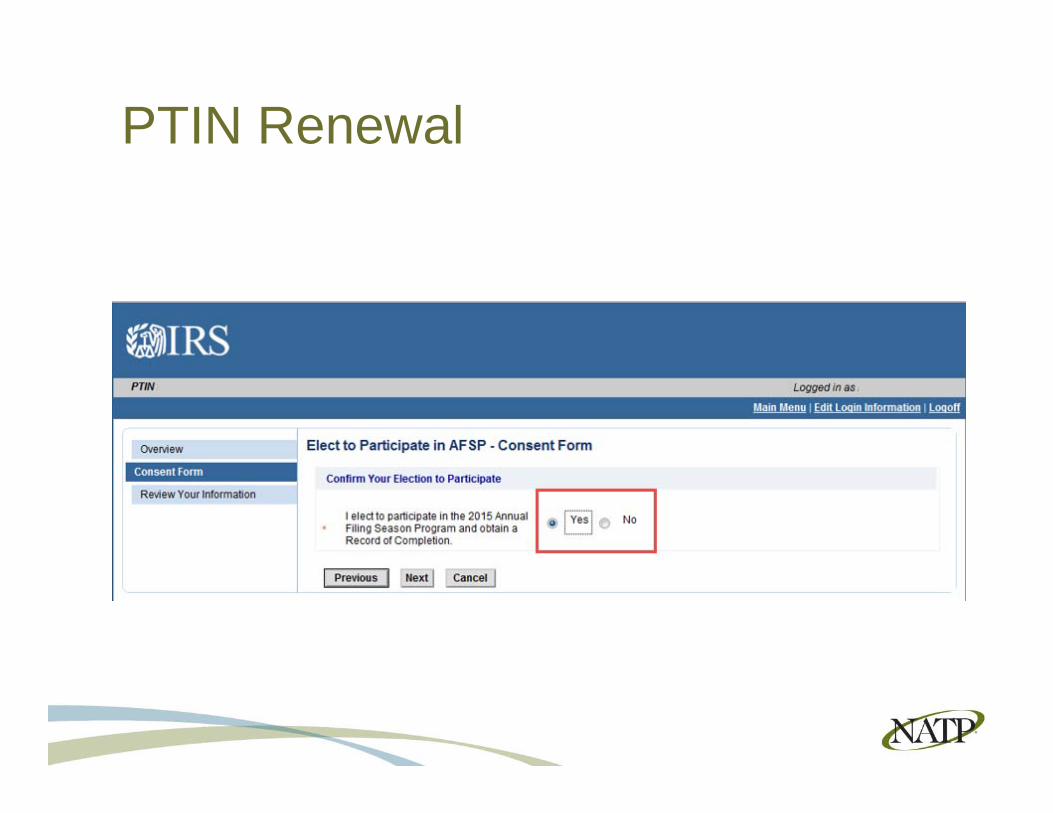

PTIN Renewal

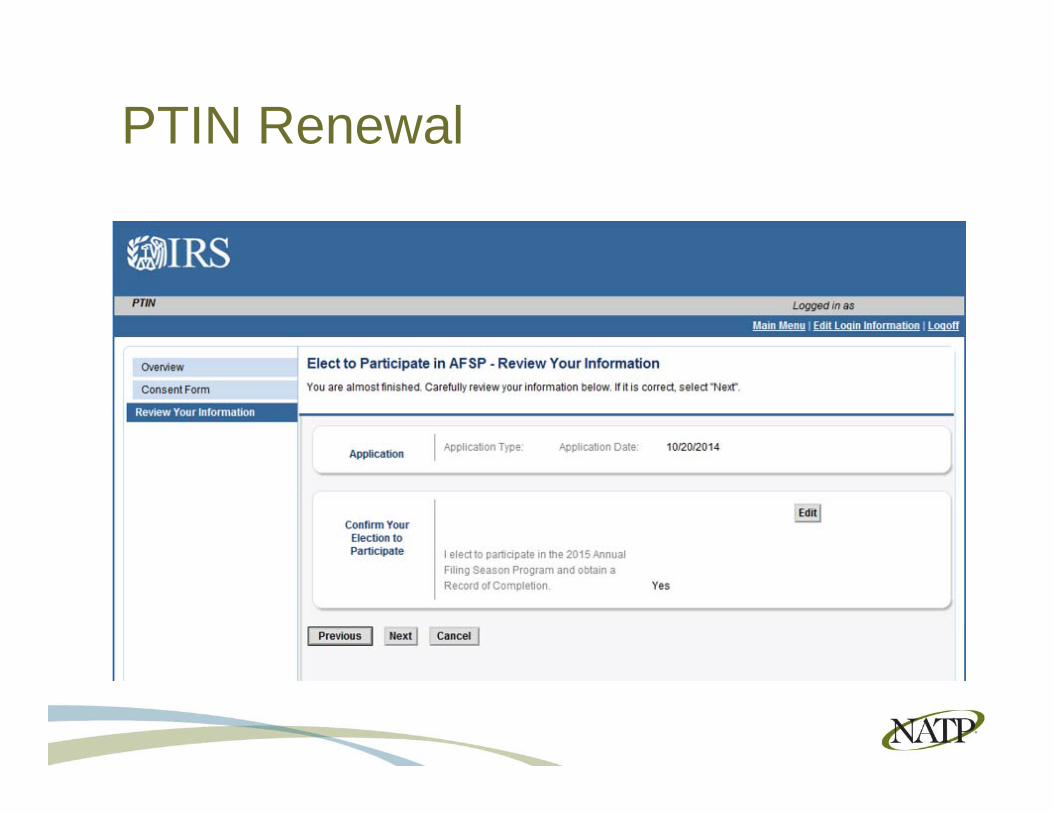

PTIN Renewal

PTIN Renewal

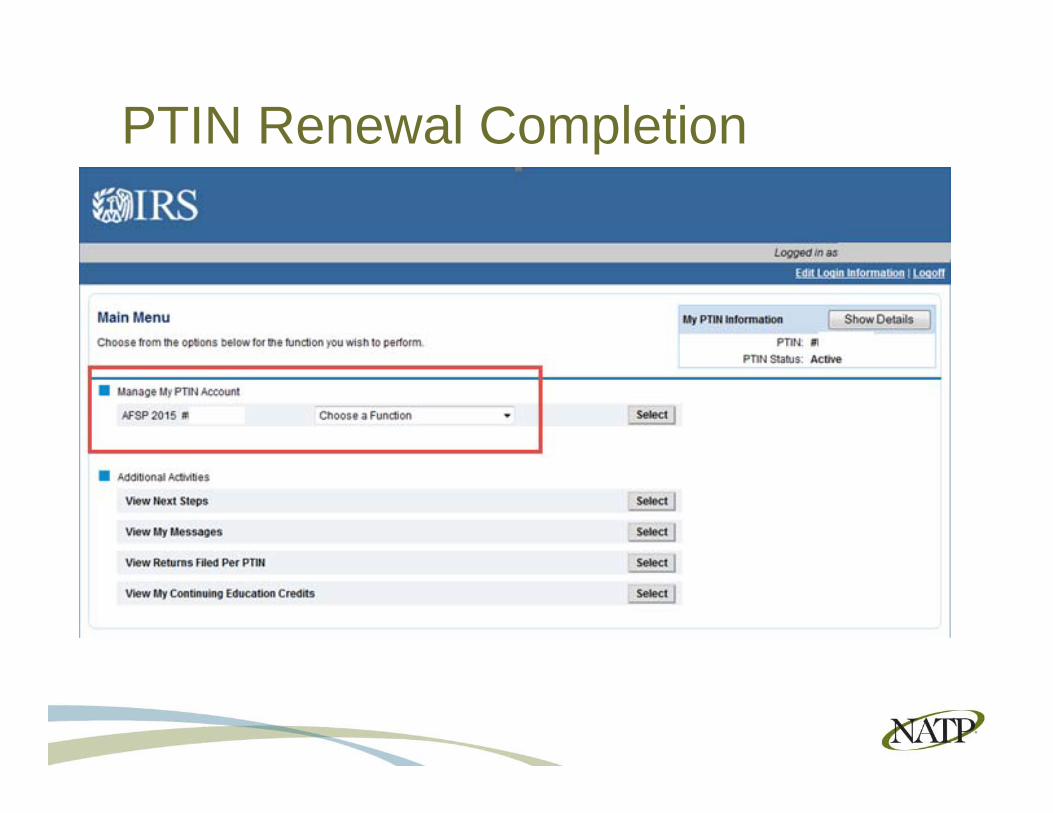

PTIN Renewal Completion

Valid for one calendar year Effective for tax returns prepared and signed

from the later of January 1 of the year covered by the Record of Completion or the date it’s issued until December 31 of that year

Example: If a Record of Completion is issued on February 25, 2015, your 2015 Record of Completion will be effective for tax

returns and claims for refund prepared and signed from February 25, 2015 through December 31, 2015.

Valid Records of Completion

Once you renew your PTIN beginning in October, you may obtain a Record of Completion You have an online PTIN account You will receive an email from [email protected] Your certificate will be sent to your secure mailbox. You do not have an online PTIN account You will receive a letter with instructions for

completing the application process and obtaining your certificate using Form W-12 Applications are due no later than April 15 for the

current year

How will I get my record of completion?

You are permitted to represent your clients before revenue agents, customer service representatives, or similar officers and employees of the IRS (including the Taxpayer Advocate Service) during an examination You must have a valid PTIN You must have prepared and

signed the taxpayers return This applies through 2015

What’s limited representation?

You must be an AFSP participant who obtained a Record of Completion You must prepare and sign the taxpayer’s return PTIN holders without an AFSP Record of

Completion or without other professional credentials will not be able to represent clients before the IRS in any matters

NOTE: CPAs, EAs and attorneys have unlimited representation rights

Limited representation after 2015

If you prepare and sign a taxpayer’s 2014 return and it’s selected for an examination after 2015, you are not permitted to represent that taxpayer unless you are an AFSP participant with a current Record of Completion. Power of Attorney will NOT give you limited

representation rights if you do not participate.

Limited representation after 2015

You must agree, under penalties of perjury, to adhere to the practice requirements outlined in Subpart B and §10.51 Subpart B - Duties and

Restrictions Relating to Practice Before the Internal Revenue Service §10.51 - Incompetence and

disreputable conduct CPAs, EAs and attorneys are

already subject to all parts of Circular 230

Circular 230

Available in the Tax Education Center 100 Question Exam

completed online Covers 3 Domains New Tax Law/Recent

Updates Federal Tax Law

General Review Ethics, Practices and

Procedures IRS Approved Provider

NATP Online AFTR Course

Included with NATP membership

Available NOW!

NATP Online AFTR Course

Essential 1040 8 CPE for EA, CPA, CRTP

6 CPE for CFP®

Beyond the 1040 8 CPE for EA, CPA, CRTP, CFP®

$370 NATP Members$450 Non-members

Live 1040 Workshops

Questions?

http://www.natptax.com/TaxKnowledgeCenter/annual-filing-season-program/Pages/default.aspx http://www.irs.gov/Tax-

Professionals/Frequently-Asked-Questions-Annual-Filing-Season-Program Revenue Procedure 2014-42 Circular 230

References