Annual Equivalent Worth Criterion Engineering Economy.

46

Annual Equivalent Worth Criterion Engineering Economy

-

Upload

caroline-george -

Category

Documents

-

view

247 -

download

2

Transcript of Annual Equivalent Worth Criterion Engineering Economy.

Annual Equivalent Worth Criterion

Engineering Economy

Annual Equivalence AnalysisAnnual equivalent criterion

Provides basis for measuring investment worth by determining equal payments on an annual basis

We first find the NPV for the original series then multiply that by the capital recovery factor

Applying annual worth analysis We use the following formula to evaluate the investment

AE(i)= PW(i)(A/P, i, N)

When evaluating a single project if AE(i)>0 accept if equal to zero indifferent if less than zero reject investment

Mutually exclusive projects If we are comparing a service project we choose the one with the

least annual equivalent cost

Example Computing Annual Equivalent Worth

$15$3.5

$5$12

$80

2 3 4 5 61

A = $1.835

2 3 4 5 61

AE= $6.946(A/P, 15%, 6) = $1.835

$6.946

00

PW(15%) = $6.946

$9.0 $10

Example Economics of Installing A Feed-water Heater

• Install a 150MW unit:– Initial cost = $1,650,000– Service life = 25 years– Salvage value = 0– Efficiency 55%– Expected improvement in fuel efficiency = 1%– Fuel cost = $0.05kWh– Load factor = 85%

• Determine the annual worth for installing the unit at i = 12%.

• If the fuel cost increases at the annual rate of 4%, what is AE(12%)?

Calculation of Annual Fuel SavingsRequired input power before adding the second unit:

Required input power after adding the second unit:

Reduction in energy consumption: 4,870kW

Annual operating hours:

Annual Fuel Savings

:

.

fuel savings (reduction in fuel requirement) (fuel cost)

(operating hours per year)=(4,870kW) ($0.05/kWh)

7,446 hours/year

=$1,813,101/year

A

150,000kW272,727kW

0.55

150,000kW267,857kW

0.56

Operating hours = (365)(24)(0.85) =7,446 hours/year

Annual Worth Calculations

(a) with constant fuel price:

(b) with escalating fuel price:

• Cash Flow Diagrams

1

1

=$1,813,101(12%) $1,650,000 $1,813,101( / ,4%,12%,25)

$17,459,783(12%) $17,459,783( / ,12%,25)

$2,226,122

APW P A

AE A P

PW(12%) $1,650,000 $1,813,101( / ,12%,25)$12,570,403

AE(12%) $12,573,321( / ,12%,25)$1,602,726

P A

A P

Benefits of Annual Worth Analysis

• Why use Annual worth while we know that the project is accepted or rejected by looking at the PW?

• Principle: Measure investment worth on annual basis

• Benefit: By knowing annual equivalent worth, we can:

• Seek consistency of report format• Determine unit cost (or unit profit)• Facilitate unequal project life comparison

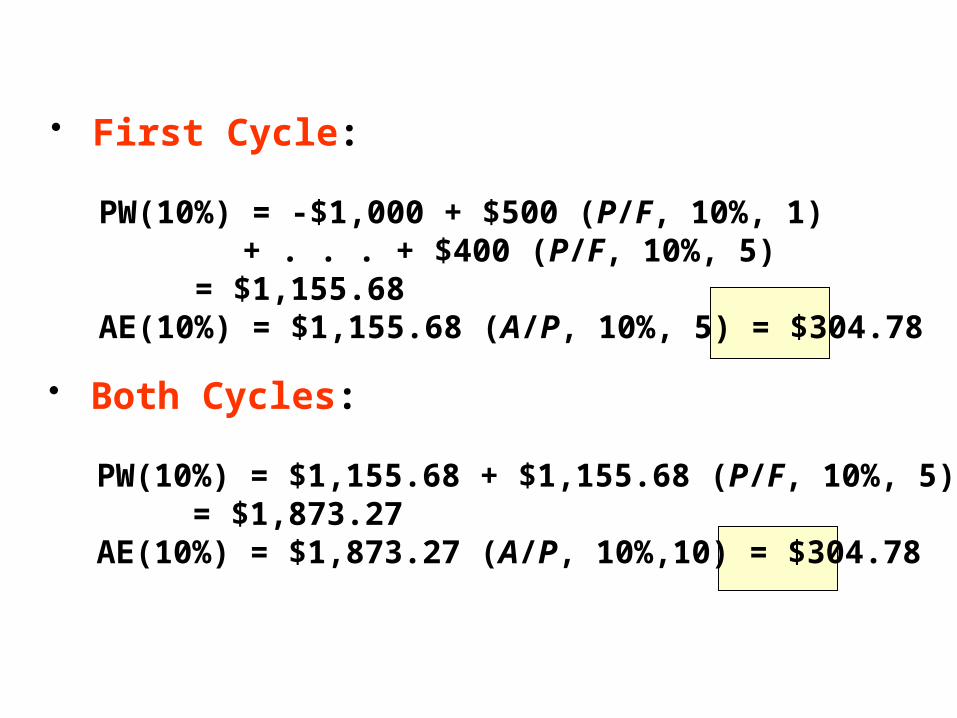

Annual Equivalent Worth - Repeating Cash Flow Cycles

$500$700

$800

$400 $400 $500

$700$800

$400 $400

$1,000 $1,000

Repeating cycle

• First Cycle:

PW(10%) = -$1,000 + $500 (P/F, 10%, 1)+ . . . + $400 (P/F, 10%, 5)

= $1,155.68AE(10%) = $1,155.68 (A/P, 10%, 5) = $304.78

• Both Cycles:

PW(10%) = $1,155.68 + $1,155.68 (P/F, 10%, 5)= $1,873.27

AE(10%) = $1,873.27 (A/P, 10%,10) = $304.78

Annual Equivalent Cost• When only costs are

involved, the AE method is called the annual equivalent cost.

• Revenues must cover two kinds of costs: Operating costs and capital costs.

Capital costs

Operating costs

+

Ann

ual E

quiv

alen

t Cos

ts

Capital (Ownership) Costs

• Def: Owning of an equipment is associated with two transactions—(1) its initial cost (I) and (2) its salvage value (S).

• Capital costs: Taking these items into consideration, we calculate the capital recovery costs as: 0 1 2 3 N

0N

I

S

CR(i)CR i I A P i N S A F i N

I S A P i N iS

( ) ( / , , ) ( / , , )

( )( / , , )

Remember from Ch2 that:

(A/F, i, N)= (A/P, i, N)-i

Vehicle Value after three years

Monthly lease

Acura MDX 4WD $21,375 588

Toyota 4Runner 4WD 4-door Limited (with moonroof)

$18,750 646

Lexus RX300 2 WD $18,750 651

GMC Envoy 4WD 4door SLT (with Bose audio, CD changer and moonroof)

$15,050 733

Mitsubishi Montero 4WD 4 door Limited

$15,225 743

Ford Explorer 4WD 4-door Eddie Bauer edition (with moonroof, rear air and third seat)

$14,425 754

Isuzu Trooper 4WD 4-door Limited

$11,675 823

Source: Automotive Lease Guide

Will Your Car Hold its Value?

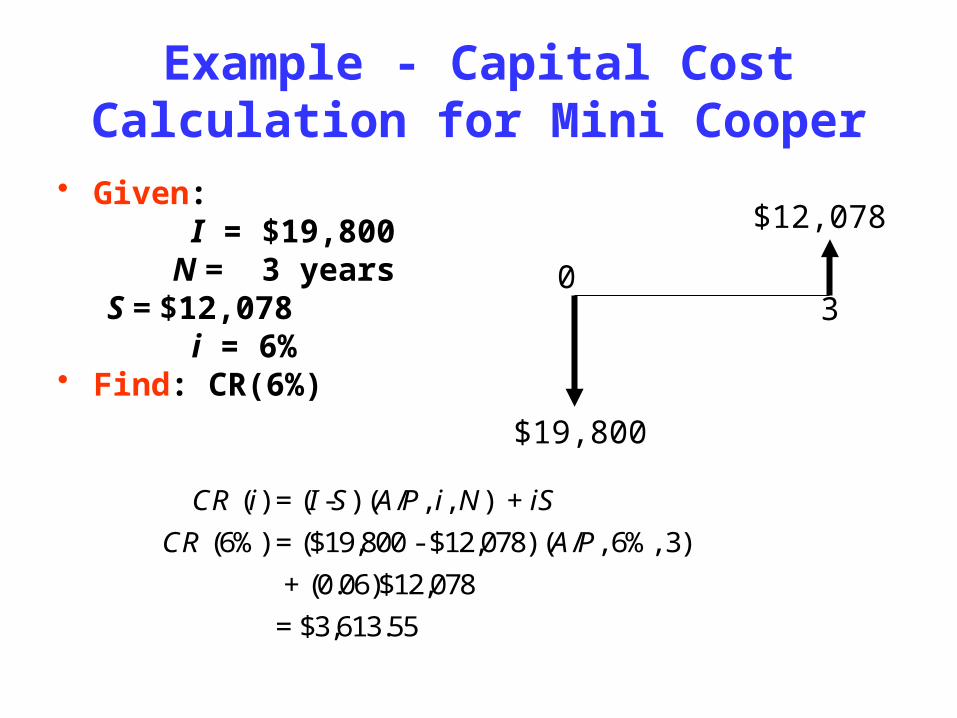

Example - Capital Cost Calculation for Mini Cooper

• Given: I = $19,800 N = 3 years S = $12,078 i = 6%• Find: CR(6%)

$19,800

$12,078

30

( ) = ( - ) ( / , , ) +

(6%) = ($19,800 - $12,078) ( / , 6%, 3)

+ (0.06)$12,078

= $3,613.55

CR i I S A P i N iS

CR A P

SEGMENT BEST MODELS

ASKING PRICE

PRICE AFTER 3 YEARS

CR (6%)

Compact car Mini Cooper $19,800 $12,078 $3,614

Midsize car Volkswagen Passat

$28,872 $15,013 $6,086

Sports car Porsche 911 $87,500 $48,125 $17,618

Near luxury car BMW 3 Series $39,257 $20,806 $8,151

Luxury car Mercedes CLK $51,275 $30,765 $9,519

Minivan Honda Odyssey

$26,876 $15,051 $5,327

Subcompact SUV Honda CR-V $20,540 $10,681 $4,329

Compact SUV Acura MDX $37,500 $21,375 $7,315

Full size SUV Toyota Sequoia

$37,842 $18,921 $8,214

Compact truck Toyota Tacoma

$21,200 $10,812 $4,535

Full size truck Toyota Tundra $25,653 $13,083 $5,488

The Cost of Owning the Rest of a Vehicle

The Cost of Owning the Rest of a Vehicle

Justifying an investment based on AE Method

• Given: I = $20,000, S = $4,000, N = 5 years, i = 10%

• Find: see if an annual revenue of $4,400 is enough to cover the capital costs.

• Solution:CR(10%) = $4,620.76

• Conclusion: Need an additional annual revenue in the amount of $220.76.

0

1 2 3 4 5

$20,000

$4,000

$4,400

0

1 2 3 4 5

$20,000

$4,000

0

1 2 3 4 5

$4,400

+

Example

Where to Apply the AE Analysis

• Unit cost (or profit) calculation

• Outsourcing (Make-Buy) Decision

• Pricing the Use of an Asset

Contemporary Engineering Economics, 5th edition, © 2010

Unit Cost (Unit Profit) Calculations

• Determine the number of units to be produced each year

• Identify the cash flow series associated with production

• Calculate the present worth of the project’s cash flow series at a given (i)

• Determine the equivalent annual worth• Divide the equivalent annual worth by the

number of units to be produced or serviced during each year

Example Unit Profit per Machine Hour When Annual Operating Hours remain Constant

• Step 1: Determine the annual volume.• 3,000 hours per year

• Step 2: Obtain the equivalent annual worth.• PW (12%) = $30,065• AE (12%) = $30,065 (A/P, 12%,

4) = $9,898

• Step 3: Determine the unit profit (savings per machine hour).

Savings per Machine Hour

= $9,898/3,000

= $3.30/hour

• Project Cash Flows & Operating Hours

• 3,000• hours

Year 1

• 3,000• hours

Year 2

• 3,000• hours

Year 3

• 3,000• hours

Year 4

$76,000

$35,560 $37,360$31,850 $34,400

0

1 2 3 4

Example 6.6 Unit Profit per Machine Hour When Annual Operating Hours Fluctuate

• Step 1: Determine the annual volume.

• Year 1: 3,500 hours• Year 2: 4,000 hours• Year 3: 1,700 hours• Year 4: 2,800 hours

• Step 2: Obtain the equivalent annual worth.

• AE (12%) = $30,065 (A/P, 12%, 4) = $9,898

• C[(3,500)(P/F,12%,1) + (4,000)(P/F,12%,2) + (1,700)(P/F,12%,3) + (2,800)(P/F,12%,4)](A/P,12%,4) = 3,062.95C

• Step 3: Determine the unit profit (savings per machine hour).

Savings per Machine Hour

C = $9,898/3,062.95

= $3.23/hour

Project Cash Flows & Operating Hours

• 3,500• hours

Year 1

• 4,000• hours

Year 2

• 1,700• hours

Year 3

• 2,800• hours

Year 4

$76,000

$35,560 $37,360$31,850 $34,400

0

1 2 3 4

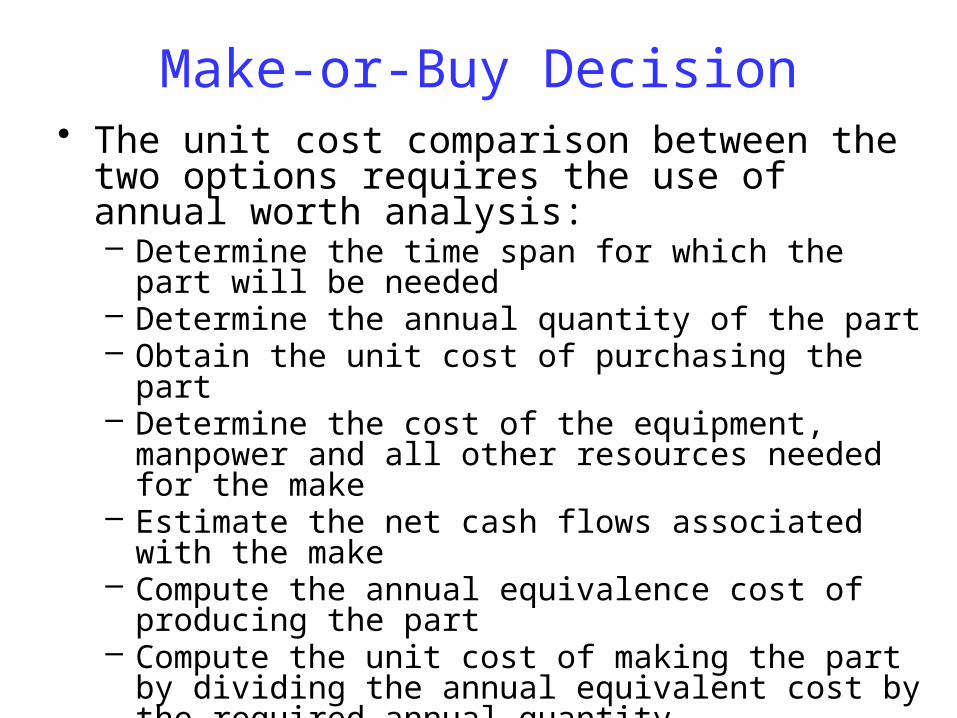

Make-or-Buy Decision• The unit cost comparison between the two options

requires the use of annual worth analysis:– Determine the time span for which the part will be

needed– Determine the annual quantity of the part– Obtain the unit cost of purchasing the part– Determine the cost of the equipment, manpower and all

other resources needed for the make– Estimate the net cash flows associated with the make– Compute the annual equivalence cost of producing the

part– Compute the unit cost of making the part by dividing the

annual equivalent cost by the required annual quantity– Choose the option with the smallest unit cost

Issues to consider when buying

• The quality of the product• The reliability of the supplier providing the

needed quantities in time• If the difference is not much and we are

looking for good quality we can ignore the difference

Example Outsourcing the Manufacture of Cassettes and Tapes

Make OptionBuy Option

Solution:• Make Option:

AEC(14%) = $4,582,254

Unit cost: $4,582,254/3,831,120 = $1.20

• Buy Option:AEC(14%) = $4,421,376

Unit cost: $4,421,376/3,831,120 = $1.15

Pricing the Use of an Asset

• The cost per square foot for owning and operating a real property (example, rental fee)

• The cost of using a private car for business (cost per mile)

• The cost of flying a private jet (cost per seat)

• The cost of using a parking deck (cost per hour)

Example: Pricing an Apartment Rental Fee

Investment Problem: Building a 50-unit Apartment Complex At Issue: How to price the monthly rental per unit?

Contemporary Engineering Economics, 5th edition, © 2010

Land investment cost = $1,000,000

Building investment cost = $2,500,000

Annual upkeep cost = $150,000Property taxes and insurance =

5% of total investment

Occupancy rate = 85%Study period = 25 yearsSalvage value = Only land cost

can be recovered in fullInterest rate = 15%

Solution:

• Ownership cost:

• Annual O&M Cost

• Total Equivalent Annual Cost

• Required Monthly Charge

O&M cost = (0.05)($3,500,000) + $150,000 = $325,000

CR(15%) = ($3,500,000 - $1,000,000)(A/P, 15%, 25) + ($1,000,000)(0.15) = $536,749

AEC(15%) = $536,749 + $325,000 =$861,749

Example Mutually Exclusive Alternativeswith Equal Project Lives

Standard Premium Motor Efficient Motor25 HP 25 HP$13,000 $15,60020 Years 20 Years$0 $089.5% 93%$0.07/kWh $0.07/kWh3,120 hrs/yr. 3,120 hrs/yr.

SizeCostLifeSalvageEfficiencyEnergy CostOperating Hours

(a) At i= 13%, determine the operating cost per kWh for each motor.(b) At what operating hours are they equivalent?

Solution:(a) Operating cost per kWh per unit

Determine total input power

Conventional motor:

input power = 18.650 kW/ 0.895 = 20.838kW

PE motor:

input power = 18.650 kW/ 0.93 = 20.054kW

Input power =output power

% efficiency

Determine total kWh per year with 3120 hours of operation

Conventional motor:

(3120 hrs/yr)* (20.838 kW) = 65,018 kWh/yr

PE motor:

( 3120 hrs/yr) *(20.054 kW) = 62,568 kWh/yr

Determine annual energy costs at $0.07/kwh: Conventional motor:

$0.07/kwh 65,018 kwh/yr = $4,551/yr PE motor:

$0.07/kwh 62,568 kwh/yr = $4,380/yr

Capital cost: Conventional motor:

$13,000(A/P, 13%, 20) = $1,851 PE motor:

$15,600(A/P, 13%, 20) = $2,221 Total annual equivalent cost:

Conventional motor: Notice that the total output power is 25HP X 0.746KW/HP X 3120 hours/year = 58,188 KWh/year

AE(13%) = $4,551 + $1,851 = $6,402 Cost per kwh = $6,402/58,188 kwh = $0.11/kwh

PE motor: AE(13%) = $4,380 + $2,221 = $6,601 Cost per kwh = $6,601/58,188 kwh

= $0.1134/kwh

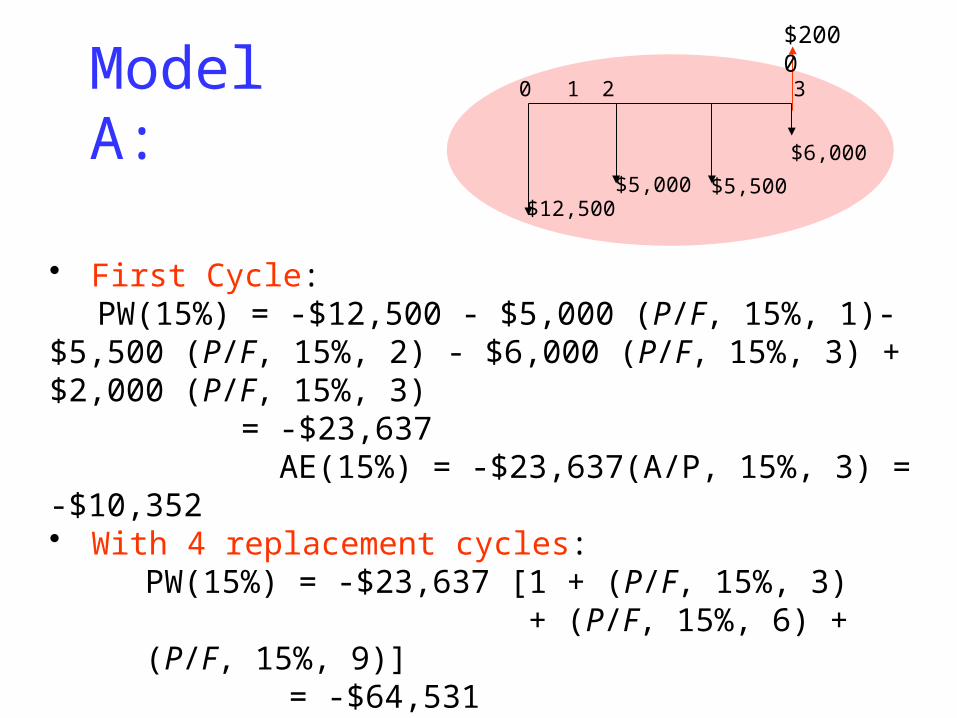

Model A: 0 1 2 3

$12,500

$5,000 $5,500$6,000

Model B: 0 1 2 3 4

$15,000

$4,000 $4,500 $5,000$5,500

Example Mutually Exclusive Alternatives with Unequal Project Lives

Required servicePeriod = Indefinite

Analysis period =LCM (3,4) = 12 years

$2000

$1500

• First Cycle: PW(15%) = -$12,500 - $5,000 (P/F, 15%, 1)- $5,500 (P/F, 15%, 2) - $6,000 (P/F, 15%, 3) + $2,000 (P/F, 15%, 3)

= -$23,637 AE(15%) = -$23,637(A/P, 15%, 3) = -$10,352• With 4 replacement cycles:

PW(15%) = -$23,637 [1 + (P/F, 15%, 3) + (P/F, 15%, 6) + (P/F, 15%, 9)]

= -$64,531AE(15%) = -$64,531(A/P, 15%, 12) = -$10,352

Model A:$12,500

$5,000 $5,500

$6,000

0 1 2 3

$2000

• With 3 replacement cycles:PW(15%) = -$27,456 [1 + (P/F, 15%, 4) + (P/F, 15%, 8)]

= -$74,954AE(15%) = -$74,954(A/P, 15%, 12) = -$12,024

• First Cycle:PW(15%) = - $15,000 - $4,000 (P/F, 15%, 1) - $4,500 (P/F, 15%, 2) - $5,000 (P/F, 15%, 3)- $4,000 (P/F, 15%, 4)

= -$27,456AE(15%) = -$27,456(A/P, 15%, 4) = -$12,024

Model B:$15,000

$4,000 $4,500

$4,000

0 1 2 3 4

$5,000

$15,000

$4,000$4,500

$4,000

$5,000$15,000

$4,000$4,500

$4,000

$5,000

$12,500

$5,000 $5,500

$4,000

$12,500

$5,000 $5,500

$4,000

$15,000

$4,000 $4,500

$4,000

$5,000$15,000

$4,000 $4,500

$4,000

$5,000

$15,000

$4,000$4,500

$4,000

$5,000$15,000

$4,000$4,500

$4,000

$5,000

$12,500

$5,000$5,500

$4,000

$12,500

$5,000$5,500

$4,000

$12,500

$5,000$5,500

$4,000

$12,500

$5,000$5,500

$4,000

$12,500

$5,000$5,500

$4,000

$12,500

$5,000$5,500

$4,000

0 1 2 3

4 5 6

7 8 9

10 11 12

0 1 2 3 4

5 6 7 8

9 10 11 12

Model A

Model B

We choose Model A since it has less cost although it has shorter life-spans

Minimum Cost Analysis

• Concept: Total cost is given in terms of a specific design parameter (provide required functional quality with the lowest cost)

• Goal: Used to determine optimal engineering design parameter that will minimize the total cost

• Typical Mathematical Equation:

where x is common design parameter• Analytical (optimal) Solution:

* cx

b

Typical Graphical Relationship

O & M Cost

Capital Cost

Total Cost

Design Parameter (x)

Optimal Value (x*)

Cost ($)

Example Optimal Cross-Sectional Area Decision Problem: A constant electric current of 5,000 amps is to be transmitted a distance of 1,000 feet from a power station to a substation. Find: the optimal size of a copper conductor

Relevant Physical and Financial Data •Copper price: $8.25/lb• Resistance: 0.8145x10-5in2/ft• Cost of energy: $0.05/kWh• Density of copper: 555 lb/ft• Useful life: 25 years• Salvage value: $0.75/lb• Interest rate: 9%

• Power Transmission

Power Plant

Substation

1,000 ft.5,000 amps24 hours365 days

Cross-sectional area

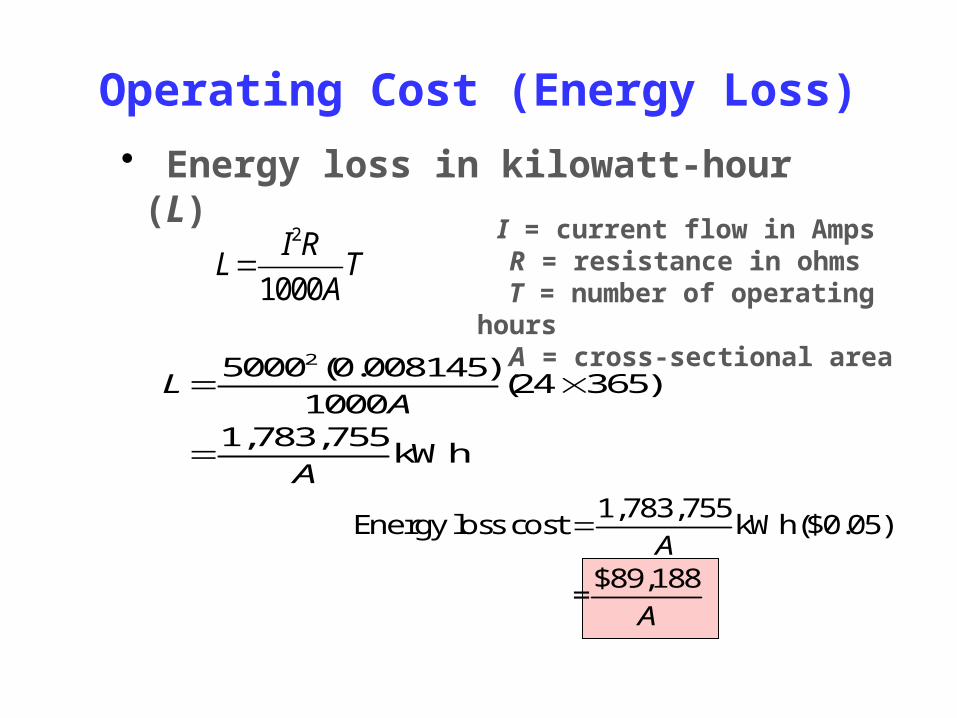

Operating Cost (Energy Loss)

• Energy loss in kilowatt-hour (L)

2

1000I R

L TA

25000 (0.008145)(24 365)

10001,783,755

kWh

LA

A

I = current flow in Amps R = resistance in ohms T = number of operating hours A = cross-sectional area

1,783,755

Energy loss cost kWh($0.05)

$89,188=

A

A

Material Costs

• Material weight in pounds

• Material cost (required investment)

Total material cost = 3,854A($8.25)

= $31,797A

• Salvage value after 25 years: ($0.75)(3,854A)

3

1000(12)(555)3,854

12A

A

Capital Recovery Cost

31,797 A

2,890.6 A

0

25

CR(9%) = (31,797 - 2,890.6 ) ( / , 9%, 25) + 2,890.6 (0.09)= 3,203

A A A PA

A

Given:Initial cost = $31,797ASalvage value = $2,890.6AProject life = 25 yearsInterest rate = 9%

Find: CR(9%)

Total Equivalent Annual Cost

• Total equivalent annual cost

AEC = Capital cost + Operating cost

= Material cost + Energy loss

• Find the minimum annual equivalent cost

2

*

2

89,188(9%) 3,203

(9%) 89,1883,203

0

89,188

3,203

5.276 in

AEC AA

dAEC

dA A

A

Example 6.10 Optimal Cross-Sectional Area

Input Parameter Input Data

Electric current (amperes) 5000

Transmission line length (feet) 1000

Annual operating hours 8760

Service life (years) 25

Material cost ($/lb) 8.25

Scrap value ($/lb) 0.75

Resistivity of the conductor (ohms-in^2/ft) 8.145E-06

Cost of energy ($/kWh) 0.05

Material Density (lb/ft^3) 555

MARR(%) 9

Cross- Capital Annual Total

Sectional Energy Material Material Salvage Recovery Energy AE

Area (A) Loss Weight Cost Value Cost Loss Cost

(in^2) (kWh) (lbs) ($) ($) ($) ($) ($)

1.000 1,783,755 3,854 31,797 2,891 3,203 89,188 92,391

1.500 1,189,170 5,781 47,695 4,336 4,804 59,459 64,263

2.000 891,878 7,708 63,594 5,781 6,406 44,594 51,000

2.500 713,502 9,635 79,492 7,227 8,007 35,675 43,683

3.000 594,585 11,563 95,391 8,672 9,609 29,729 39,338

3.500 509,644 13,490 111,289 10,117 11,210 25,482 36,693

4.000 445,939 15,417 127,188 11,563 12,812 22,297 35,109

4.500 396,390 17,344 143,086 13,008 14,413 19,820 34,233

5.000 356,751 19,271 158,984 14,453 16,015 17,838 33,853

5.275 338,153 20,331 167,729 15,248 16,896 16,908 33,803

5.500 324,319 21,198 174,883 15,898 17,616 16,216 33,832

6.000 297,293 23,125 190,781 17,344 19,218 14,865 34,083

Cell Formulas:

C22:=($F$6)^2*($F$12*$F$7)*($F$8)/(1000*B22)

D22:=($F$7)*(12)*($F$14)*(B22)/(12^3)

E22:=D22*$F$10

F22:=$F$11*D22

G22:=-PMT($F$15%,$F$9,E22-F22)+($F$15/100)*F22

H22:=C20*$F$11

I22:=G22+H22

Optimal Cross-Sectional Area

Optimal Cross-Sectional Area

Summary• Annual equivalent worth analysis, or AE, is—along with

present worth analysis—one of two main analysis techniques based on the concept of equivalence. The equation for AE is

AE(i) = PW(i)(A/P, i, N).

AE analysis yields the same decision result as PW analysis.• The capital recovery cost factor, or CR(i), is one of the most

important applications of AE analysis in that it allows managers to calculate an annual equivalent cost of capital for ease of itemization with annual operating costs.

• The equation for CR(i) is

CR(i)= (I – S)(A/P, i, N) + iS,

where I = initial cost and S = salvage value.

• AE analysis is recommended over NPW analysis in many key real-world situations for the following reasons:1. In many financial reports, an annual equivalent value is preferred to a present worth value.2. Calculation of unit costs is often required to determine

reasonable pricing for sale items.3. Calculation of cost per unit of use is required to

reimburse employees for business use of personal cars.

4. Make-or-buy decisions usually require the development of unit costs for the various alternatives.

Summary