Annexes - tables and graphs FvH · Policy Research Corporation SOUND SOLUTIONS BASED ON SCIENTIFIC...

97

Policy Research Corporation Policy Research Corporation SOUND SOUND SOLUTIONS BASED ON SCIENTIFIC RESEARCH SOLUTIONS BASED ON SCIENTIFIC RESEARCH The role of Maritime Clusters to enhance the strength and development of European maritime sectors Annexes 13 November 2008

Transcript of Annexes - tables and graphs FvH · Policy Research Corporation SOUND SOLUTIONS BASED ON SCIENTIFIC...

Policy Research CorporationPolicy Research CorporationSOUNDSOUND SOLUTIONS BASED ON SCIENTIFIC RESEARCHSOLUTIONS BASED ON SCIENTIFIC RESEARCH

The role of Maritime Clusters to enhance the strength and development of European maritime sectors

Annexes

13 November 2008

Policy Research Corporation 28 July 200813 November 2008

ANNEXES

Annex 1: Definitions of the sea-related sectors (Area 1, 2 and 3)Annex 2: Production value, value added and employment on EU-level: absolute figures and stars (overall + per

Area)Annex 3: Overview of employment and value added in the sea-related sectors in the EU’s member states and

NorwayAnnex 4: Analysis of differences in employment figures per countryAnnex 5: Results to be integrated in the European Cluster Observatory’s database (Area 1, 2 and 3 + cluster

organisations)Annex 6: Employment summary pages per country (in alphabetical order)Annex 7: Main trends & policies in the national maritime clusters in Europe (overall & per sector) and relevant EU

policyAnnex 8: Trends and policies in the maritime clusters of Singapore and Dubai Annex 9: Archetypes of maritime cluster organisationsAnnex 10: Similarities and differences between maritime cluster organisationsAnnex 11: Main differences and similarities between cluster organisations and sector associationsAnnex 12: Overview of main benefits of clustering and good practices of maritime cluster organisationsAnnex 13: The link between cluster policies and sector performanceAnnex 14: SWOT-analysis of top-down and bottom-up maritime cluster organisationsAnnex 15: Contacted persons Annex 16: List of abbreviationsAnnex 17: References

Policy Research Corporation 38 July 200813 November 2008

ANNEX 1: DEFINITIONS OF THE SEA-RELATED SECTORS

The above definitions for the sea-related sectors are used in order to map the economic impact of the maritime sectors on a European scale although some member

states’ definitions may differ from the above

Area 1: Traditional maritime sectors– Inland navigation: Inland shipping and ship management; chartering-out; inland cruises and ferries; harbour and river towage; freighting– Marine equipment: Manufacturing and wholesale trade in maritime equipment for all maritime (sub-)sectors (no building, repair and/or conversion and

no offshore supply)– Maritime services: Research and development; education; classification and inspection; bunkering; maritime insurance; maritime financing; maritime

brokerage; maritime law; crewing; associations; government services; rescue; diving; ship supply (no port services)– Maritime works: Dredging; nautical cable and pipelines; river works; construction of canals, dykes and ports; support vessels; sand transport– Navy and coastguard (no shipbuilding)– Offshore supply: Construction and installation of platforms, storage vessels and equipment; drilling; offshore-related transport, engineering,

communication, consultancy and other support; seismic research; manufacturing, installation and maintenance of offshore and coastal wind turbines (no extraction of oil such as operators of oil rigs)

– Recreational boating: Boat chartering and renting; marinas; inland boat basins; supporting services concerning the construction of and trade in recreational vessels; boating-related training and trade (no manufacturing)

– Seaports: Cargo-handling; shipping related storage, agency, maritime logistics and forwarding; port authorities; pilotage– Shipbuilding: Construction and repair of sea-going vessels (commercial ships, fishing boats and naval ships), recreational boats and inland vessels; ship

scrapping; floating sections; dry docks (no offshore-rigs and/or -vessels)– Shipping: Merchant shipping and ship management; short-sea shipping; chartering-out; ferry services; ocean towage (only national seafarers and

onshore persons employed)– Marine aggregates: Exploitation of marine aggregates

Area 2: Coastal and sea-related (marine) recreation and tourism:– Coastal tourism: Tourism within 10 km from the coast– Cruise tourism: Service on board of cruise ships (no land-based tourism and/or related services)

Area 3: Fisheries– Fisheries: Maritime and inland fishing; fish processing; aquaculture

Policy Research Corporation 48 July 200813 November 2008

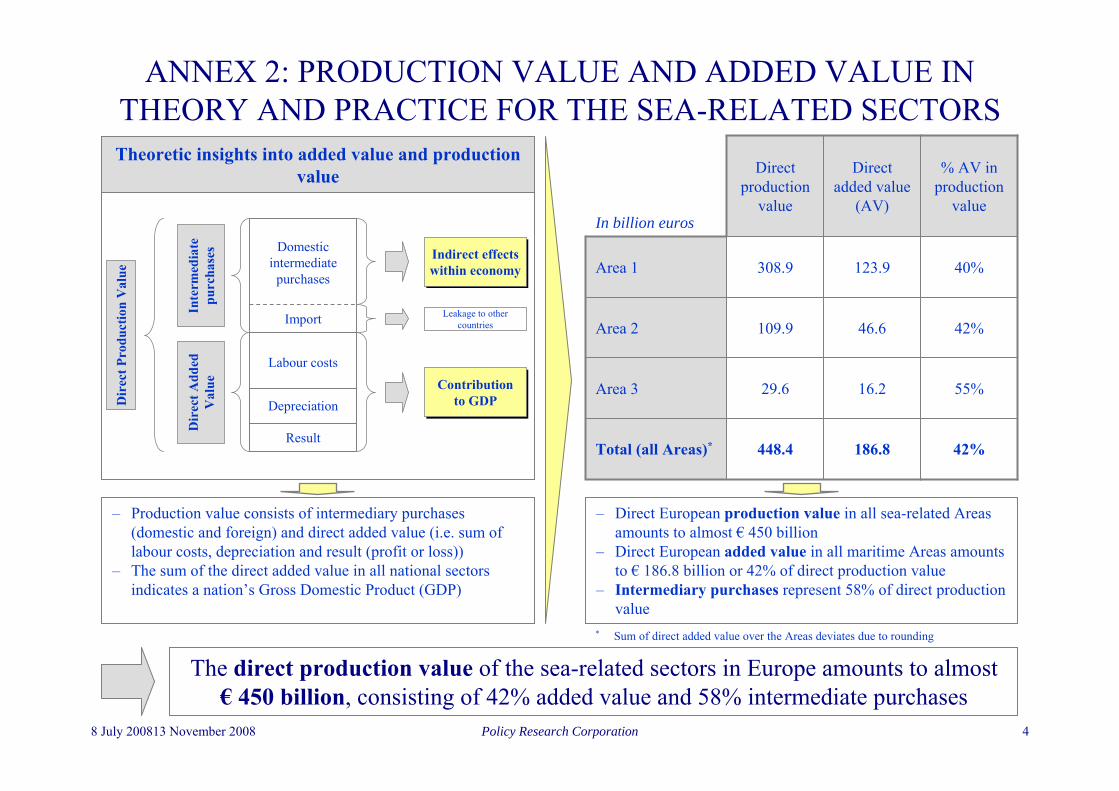

ANNEX 2: PRODUCTION VALUE AND ADDED VALUE IN THEORY AND PRACTICE FOR THE SEA-RELATED SECTORS

The direct production value of the sea-related sectors in Europe amounts to almost€ 450 billion, consisting of 42% added value and 58% intermediate purchases

42%

55%

42%

40%

% AV in production

value

186.8

16.2

46.6

123.9

Direct added value

(AV)

448.4Total (all Areas)*

29.6Area 3

109.9Area 2

308.9Area 1

Direct production

valueIn billion euros

Theoretic insights into added value and production value

– Direct European production value in all sea-related Areas amounts to almost € 450 billion

– Direct European added value in all maritime Areas amounts to € 186.8 billion or 42% of direct production value

– Intermediary purchases represent 58% of direct production value

– Production value consists of intermediary purchases (domestic and foreign) and direct added value (i.e. sum of labour costs, depreciation and result (profit or loss))

– The sum of the direct added value in all national sectors indicates a nation’s Gross Domestic Product (GDP)

Import

Domestic intermediate

purchases

Result

Depreciation

Labour costs

Dir

ect P

rodu

ctio

n V

alue

Dir

ect A

dded

V

alue

Inte

rmed

iate

pu

rcha

ses

Contribution to GDP

Contribution to GDP

Indirect effects within economyIndirect effects within economy

Leakage to other countries

* Sum of direct added value over the Areas deviates due to rounding

Policy Research Corporation 58 July 200813 November 2008

ANNEX 2: PRODUCTION VALUE AND ADDED VALUE IN THE TRADITIONAL MARITIME SECTORS (AREA 1)

Significant differences in the share of added value in the production value reflect the differences in the use of production means (capital and labour) and the level of in-house

production and outsourcing

48%2 0004 200Inland navigation

38%332870Marine aggregates

40%

63%

51%

34%

55%

68%

28%

32%

30%

% AV in production value

2 1005 300Maritime works

9 40015 000Maritime services

9 00017 900Offshore supply

8 100

15 400

22 700

10 000

17 600

27 300

Direct added value (AV)

23 500Recreational boating

27 900Navy

33 300Seaports

35 200Shipbuilding

54 200Marine equipment

91 500Shipping

Direct production valueIn million euros

More information on the relation between added value and production value is provided in the ‘Overview of applied research methodology’

Policy Research Corporation 68 July 200813 November 2008

ANNEX 2: ADDED VALUE AND EMPLOYMENT IN ALL SEA-RELATED AREAS FOR EUROPEAN UNION AND NORWAY

The top-10 countries account for 88% of added value and 83% of employment in all sea-related sectors

EmploymentDirect (Σ direct) employment = 4.78 million persons**

* Added value is formulated in € million; the definition of added value is provided in the ‘Overview of the applied research methodology’** For a detailed breakdown of added value and employment for all sea-related Areas and sectors see Annex 3; Annex 4 explains the differences in employment with national

maritime cluster studies*** Top-10 countries in terms of share of maritime added value (and employment) in all sea-related Areas are listed; for other countries % share is well below 2.5% (and 3%)

15 000 = 15 000 million euros of added value 500 000 = 500 000 persons employed

Added valueDirect (Σ direct) added value = 186.8 billion euros**

200

300300

50100

100

4 000

4 000

6 000

1 100

10 000

4 000

Percentage maritimeemployment in natio-

nal employment***

Percentage maritimeemployment in natio-

nal employment***

Europe: 2.25%MT: 13.51%CY: 12.02%NO: 6.85%EE: 6.54%GR: 6.39%LV: 5.36%DK: 5.26%ES: 4.62%BG: 3.46%PT: 3.34%

Europe: 2.25%MT: 13.51%CY: 12.02%NO: 6.85%EE: 6.54%GR: 6.39%LV: 5.36%DK: 5.26%ES: 4.62%BG: 3.46%PT: 3.34%

Percentage maritimeadded value in

national GDP***

Percentage maritimeadded value in

national GDP***

Europe: 1.65%MT: 11.36%CY: 9.07%EE: 8.83%LV: 7.71%NO: 6.23%DK: 4.19%GR: 3.24%LT: 2.59%ES: 2.53%NL: 2.25%

Europe: 1.65%MT: 11.36%CY: 9.07%EE: 8.83%LV: 7.71%NO: 6.23%DK: 4.19%GR: 3.24%LT: 2.59%ES: 2.53%NL: 2.25%

Average valueadded/employee =

€ 39 000

Average valueadded/employee =

€ 39 000

48 100

103 300

41 800

287 300

144 700

39 700

876 400

50 100

503 700

279 200

38 400

724 700

34 500

55 400

20 100

190 500

156 300

147 000

171 200

136 600

70 400

634 400

4 000

1 200

17 200

8 700

23 000

3 200

25 400

6 400

2 100

24 300

1 000

500

11 500

15 100

3 400

2 800

1 200

3 800

28 400

1 000

500

500

Policy Research Corporation 78 July 200813 November 2008

ANNEX 2: EUROPEAN OVERVIEW OF ADDED VALUE AND EMPLOYMENT IN THE TRADITIONAL MARITIME SECTORS

The top-10 countries account for 87% of value added and 80% of employmentin the traditional maritime sectors

EmploymentDirect (Σ direct) employment = 1.92 million persons**

Added value*

Direct (Σ direct) added value = 123.9 billion euros**

Average valueadded/employee =

€ 64 600

Average valueadded/employee =

€ 64 600

* Added value is formulated in million euros** For a detailed breakdown of added value and employment for all sea-related sectors see Annex 3; Annex 4 explains the differences in employment with national

maritime cluster studies

10 000 = 10 000 million euros of added value = 200 000 persons employed200 000

100

200

30100100

3 000

2 000

4 000

1 000

2 000

4 000

Area 1Area 1

36 700

29 700

10 100

197 500

82 600

25 900

136 700

42 100

230 700

76 200

6 400

196 100

21 600

38 900

7 600

128 100

110 000

117 000

29 000

80 400

48 300

253 600

3 700

300

400

14 900

6 900

800

7 400

2 900

16 000

3 400

300

900

13 300

400

900

9 900

12 900

3 100

1 000

1 000

3 200

20 200

300

Policy Research Corporation 88 July 200813 November 2008

ANNEX 2: STAR METHOD APPLIED WITH REGARD TO EMPLOYMENTIN TRADITIONAL MARITIME SECTORS ON EUROPEAN LEVEL*

Three-star regions in the traditional maritime sectors are Sud-Est (Ro), Pomorskie (Pl), Liguria (It), Haute-Normandie (Fr) and Vestlandet (No)

Stars based on strength indicators size, specialisation and focus**

Maritime employment(> 50 000)

Maritime employment

(25 000-50 000)

Maritime employment (< 25 000)

3 3 3

2 2 2

1 1 1

* Stars for regions on country-level are analysed in the country-reports** Detailed data on size, specialisation and focus of star-regions are provided in Annex 5

Region excels in three strength indicators

Region excels in two out of three strength

indicators

Region excels in one out of three strength

indicators

Area 1Area 1

PT

FR

DE

SE

FI

PL

CZ

AT

IT

SI

GR

SK

HU

RO

BG

ES

MTCY

IE

LU

33

2

3

3

2

2

2

2

2

22

2

2

1

1

1

1

1

1

2

1

11

1

1

1

1

1

Policy Research Corporation 98 July 200813 November 2008

In comparison to employment-stars in the traditional maritime sectors, value added stars shift to regions in north-western Europe

ANNEX 2: STAR METHOD APPLIED WITH REGARD TO ADDED VALUEIN TRADITIONAL MARITIME SECTORS ON EUROPEAN LEVEL

Stars based on strength indicators size, specialisation and focus

Maritime added value

(> € 3 billion)

Maritime added value

(€ 2 - 3 billion)

Maritime added value

(< € 2 billion)

Region excels in three strength indicators

Region excels in two out of three strength

indicators

Region excels in one out of three strength

indicators

3 3 3

2 2 2

1 1 1

Area 1Area 1

PT

FR

DE

SE

FI

PL

CZ

AT

IT

SI

GR

SK

HU

RO

BG

ES

MTCY

IE

LU

2

2

22

1

2

2

1

21

3

1

2

1

1

1

1

1

1

1

1

1

3

3

3

2

3

1

1

Policy Research Corporation 108 July 200813 November 2008

Top-10 countries account for more than 93% of total added value in Area 2

ANNEX 2: EUROPEAN OVERVIEW OF ADDED VALUE AND EMPLOYMENT IN COASTAL (AND MARINE) TOURISM

EmploymentDirect (Σ direct) employment = 2.42 million persons**

Added value*

Direct (Σ direct) added value = 46.6 billion euros**

* Added value is formulated in million euros** For a detailed breakdown of added value and employment for all sea-related sectors see Annex 3

2 000 = 2 000 million euros of added value = 300 000 persons employed300 000

Average valueadded/employee =

€ 19 300

Average valueadded/employee =

€ 19 30060

20

30

70

100

Area 2Area 2

9 700

72 700

30 600

73 300

48 0007 200

652 400

5 300

208 200

165 300

21 400

480 700

6 300

6 000

11 000

53 400

29 600

10 100

109 100

45 600

18 200

7 400

347 300

200

800

1 600

1 000

12 700

200

6 300

1 900

500

8 900

200

1 200

1 000

1 200

200

500

7 800

200

Policy Research Corporation 118 July 200813 November 2008

ANNEX 2: STAR METHOD APPLIED WITH REGARD TO EMPLOYMENTIN COASTAL TOURISM ON EUROPEAN LEVEL

Main regions in terms of employment in coastal tourism and recreation are situated in the Mediterranean

* Stars for regions on country-level are analysed in the country-reports** Detailed data on size, specialisation and focus of star-regions are provided in Annex 5

Stars based on strength indicators size, specialisation and focus**

Maritime employment(> 50 000)

Maritime employment

(25 000-50 000)

Maritime employment (< 25 000)

Region excels in three strength indicators

Region excels in two out of three strength

indicators

Region excels in one out of three strength

indicators

PT

FR

DE

SE

FI

PL

CZ

AT

SI

SK

HU

RO

BG

ES

IE

LU

UK

NO

BE

3

3

3

2

2

2

2

2

2

2

2

2

2

1

1

1

1

1

1

1

1

1

1

1

11

11

1

1

Canarias (ES)

EE

LV

LT

3 3 3

2 2 2

1 1 1

Area 2Area 2

Policy Research Corporation 128 July 200813 November 2008

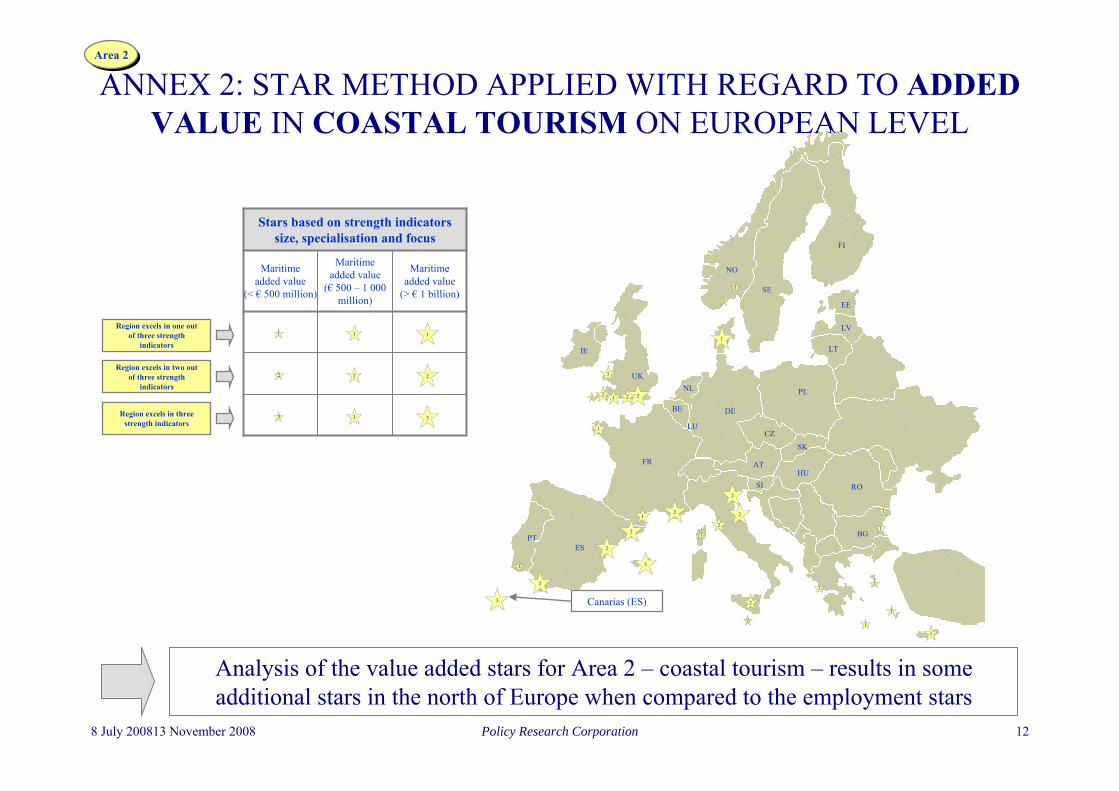

ANNEX 2: STAR METHOD APPLIED WITH REGARD TO ADDED VALUE IN COASTAL TOURISM ON EUROPEAN LEVEL

Analysis of the value added stars for Area 2 – coastal tourism – results in some additional stars in the north of Europe when compared to the employment stars

Stars based on strength indicators size, specialisation and focus

Maritime added value

(> € 1 billion)

Maritime added value

(€ 500 – 1 000 million)

Maritime added value

(< € 500 million)

Region excels in three strength indicators

Region excels in two out of three strength

indicators

Region excels in one out of three strength

indicators

PT

FR

DE

SE

FI

PL

CZ

AT

SI

SK

HU

RO

BG

ES

IE

LU

UK

NO

BE

1

1

1

1

1

1

1

1

1

1

1

1

1

11

1

1

2

2

2

2 2

22

2

2

2

2

3

3

3 Canarias (ES)

NL

EE

LV

LT

3 3 3

2 2 2

1 1 1

Area 2Area 2

Policy Research Corporation 138 July 200813 November 2008

ANNEX 2: ADDED VALUE AND EMPLOYMENT OF THE MAJOR TEN EUROPEAN COUNTRIES IN FISHERIES

The top-10 countries account for almost 85% of employment and over 90% of value added in Area 3

EmploymentDirect (Σ direct) employment = 444 000 persons**

= 1 000 million euros of added value 50 000 = 50 000 persons employed

Added value*

Direct (Σ direct) added value = 16.2 billion euros**

1 000

* Added value is formulated in million euros** For a detailed breakdown of added value and employment for all sea-related sectors see Annex 3; Annex 4 explains the differences in employment with national

maritime cluster studies

Average valueadded/employee =

€ 36 600

Average valueadded/employee =

€ 36 600

120

80

60

5

3030

60

90

10

30

90

30

20

10

600

700

1 700

1 200

1 700

1 400

1 200

900

Area 3Area 3

16 400

14 100

6 700

87 300

2 700

64 700

37 700

10 600

48 000

6 600

10 600

9 000

16 700

19 900

33 200

10 600

4 000

33 500

2 300

700

2 900

3 100

1 200

600

2 100

400

1 200

200

700

200

1 500

700

Policy Research Corporation 148 July 200813 November 2008

ANNEX 2: STAR METHOD APPLIED WITH REGARD TO EMPLOYMENT IN FISHERIES ON EUROPEAN LEVEL

Main regions in terms of employment in fisheries are located at the Atlantic Ocean with Galicia (Es), Bretagne (Fr) and Algarve (Pt) as three-star regions

PT

FR

DE

SE

FI

PL

CZ

AT

IT

SI

SK

HU

RO

BG

ES

MTCY

IE

LU

UK

NO

BE

3

3

3

2

2

2

2

2

2

2

2

2

2

2

1

1

1

1

1

1

1 1

1

1

1 1

1

1

1 1

1

* Stars for regions on country-level are analysed in the country-reports** Detailed data on size, specialisation and focus of star-regions are provided in Annex 5

Stars based on strength indicators size, specialisation and focus**

Maritime employment(> 10 000)

Maritime employment

(5 000-10 000)

Maritime employment

(< 5 000)

Region excels in three strength indicators

Region excels in two out of three strength

indicators

Region excels in one out of three strength

indicators

3 3 3

2 2 2

1 1 1

Area 3Area 3

Policy Research Corporation 158 July 200813 November 2008

ANNEX 2: STAR METHOD APPLIED WITH REGARD TO ADDED VALUE IN FISHERIES ON EUROPEAN LEVEL

Compared to employment stars, value added stars for fisheries show about the same stars in southern Europe, but additional stars in north-western Europe

PT

FR

DE

SE

FI

PL

CZ

AT

IT

SI

SK

HU

RO

BG

ES

MTCY

IE

LU

UK

NO

BE

3

3

3

3

2

2

2

2

2

2

2

2

2

2 1

1

1

1

1

1

1

1

11

1

1

1

1

1

1

Stars based on strength indicators size, specialisation and focus

Maritime added value

(> € 300 million)

Maritime added value(€ 200 – 300

million)

Maritime added value

(< € 200 million)

Region excels in three strength indicators

Region excels in two out of three strength

indicators

Region excels in one out of three strength

indicators

3 3 3

2 2 2

1 1 1

Area 3Area 3

Policy Research Corporation 168 July 200813 November 2008

ANNEX 3: OVERVIEW OF EMPLOYMENT IN THE SEA-RELATED SECTORS IN ALL COUNTRIES

Employment in the sea-related sectors amounts to 2.25% of total employment in the European Union and Norway

Area 1 Area 2 Area 3

Σ= 1 920 000Σ= 444 000

* Shipping includes only EU-resident seafarers because although non-resident seafarers receive their income from EU-based companies, they – in general – transfer a very large share of that income to non-EU countries resulting in expenditures outside the EU; e.g. non-resident seafarers working for Dutch shipping companies amount to 13 710 (6 140 resident shipping personnel) and non-EU seafarers working for Italian-based companies amount to 14 000 (22 800 resident shipping personnel) (Source: Ecotec (2006))

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, LEI (2006) – Employment in the fisheries sector, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Industry, Trade and Services (Annual enterprise statistics) 2005, G.P. Wild and Business Research and Economic Advisors (2007) – Contribution of cruise tourism to the economies of Europe and Eurostat – Tourism indicators 2005

NavyMarine equipment Shipping Seaports Shipbuilding

Recreational boating

Offshore supply

Maritime services

Inland navigation

Maritime works

at Austria - 1 709 52 - 383 634 - - 379 -be Belgium 2 400 894 866 16 651 1 170 565 - 9 865 788 3 460bg Bulgaria 10 000 8 172 5 405 - 6 147 - - - - -cy Cyprus 330 - 5 100 3 909 157 407 - 116 - 97cz Czech Republic - - 689 - 512 114 - - 723 -de Germany 24 559 72 000 11 072 7 500 23 600 15 602 17 220 13 720 9 075 3 150dk Denmark 300 20 626 11 244 - 7 423 2 539 7 887 32 460 - 150ee Estonia 300 1 500 10 191 10 300 3 031 218 - 312 - -es Spain 47 300 14 523 10 506 35 000 8 953 17 920 - 1 562 227 742fi Finland 2 300 19 000 6 806 3 559 6 083 1 575 661 1 657 207 249fr France 55 293 30 000 18 240 27 259 30 764 24 000 26 800 11 041 3 454 3 564gr Greece 19 500 3 281 36 594 - 3 601 3 288 - 9 961 - -hu Hungary - - 2 027 - 411 179 - - 1 228 -ie Ireland - - 3 637 1 958 48 512 - 210 - 12it Italy 35 261 24 000 22 772 26 048 23 295 60 334 - 1 477 2 858 30lt Lithuania 644 - 6 428 2 730 4 967 40 3 514 1 738 141 1 426lu Luxembourg - - 917 - - - - 136 47 -lv Latvia 630 1 435 17 890 11 046 2 670 260 - 3 243 20 1 700mt Malta - - 118 5 536 1 763 200 - - - -nl Netherlands 14 500 13 140 6 140 27 130 10 090 12 160 18 750 9 550 11 500 5 100no Norway 3 700 9 646 18 036 2 200 27 729 - 40 000 8 700 31 -pl Poland 16 000 34 517 30 418 9 727 20 230 900 475 3 185 1 249 303pt Portugal 14 745 - 2 397 2 002 4 782 1 761 1 300 - 1 467 509ro Romania 6 800 17 709 13 327 18 000 19 855 - - - 3 097 1 575se Sweden 5 670 12 470 14 447 6 500 3 485 2 200 - 2 401 1 063 35si Slovenia - - 698 - 428 380 - 150 28 -sk Slovakia - - 578 - 950 55 - - 733 -uk United Kingdom 61 500 16 604 26 550 42 150 32 582 13 158 30 000 27 402 1 167 -Total 321 732 301 226 283 145 259 205 245 107 159 000 146 607 138 886 39 482 22 102

Σ=2 420 000

*Marine aggregates

----------

300----------------

2 5002 800

Coastal tourism Cruise tourism Fisheries

- 168 7349 707 - 1 743

72 653 - 89530 555 - 1 175

- - 2 26770 385 2 963 16 40947 950 67 14 060

7 198 - 6 700651 116 1 279 87 310

5 280 - 2 740207 634 606 64 712165 291 - 37 701

- 101 1 68021 158 236 10 584

468 612 12 086 47 9576 350 - 6 565

- - -5 976 - 10 580

11 000 - 1 44152 968 438 9 04925 881 3 670 16 700

9 795 269 19 923108 147 909 33 229

45 610 - 10 60018 061 101 3 955

7 393 - 623- 67 1 180

336 786 10 470 33 5342 385 505 33 430 444 046

Policy Research Corporation 178 July 200813 November 2008

Added value in the sea-related sectors amounts to 1.65% of total added value (GDP at market price) in the European Union and Norway

Area 1 Area 2 Area 3

Σ= € 123.9 billionΣ= € 16.2 billion

ANNEX 3: OVERVIEW OF ADDED VALUE IN THE SEA-RELATED SECTORS IN ALL COUNTRIES

Σ= € 46.6 billion

Shipping SeaportsMarine equipment Navy Shipbuilding

Offshore supply

Maritime services

Recreational boating

Maritime works

Inland navigation

at Austria 9 - 126 - 18 - - 35 - 21be Belgium 152 2 011 75 134 55 - 752 35 452 41bg Bulgaria 127 - 45 58 38 - - - - -cy Cyprus 159 260 - 10 4 - 5 - 7 -cz Czech Republic 90 - - - 4 - - 2 - 10de Germany 2 788 778 5 120 1 179 1 261 952 927 827 354 738dk Denmark 1 972 - 1 448 18 334 522 2 621 - 21 -ee Estonia 446 322 30 4 36 - 9 - - -es Spain 838 2 839 764 1 775 318 - 82 742 65 5fi Finland 437 395 1 412 118 290 36 95 89 30 8fr France 1 957 3 187 1 980 2 990 1 583 1 485 708 1 433 451 162gr Greece 2 125 - 96 695 99 - 363 - - -hu Hungary 266 - - - 3 - - 4 - 17ie Ireland 638 274 - - 2 - 19 - 2 -it Italy 2 535 2 794 1 610 1 749 1 158 - 65 3 304 3 120lt Lithuania 208 65 - 7 54 44 30 0 37 2lu Luxembourg 125 - - - - - 7 - - 6lv Latvia 456 236 27 6 23 - 90 3 39 0mt Malta 6 300 - - 40 - - - - -nl Netherlands 1 077 2 884 913 713 548 1 143 683 660 587 704no Norway 3 125 397 753 1 918 2 095 2 944 785 - - 2pl Poland 1 330 285 859 217 312 8 58 13 10 39pt Portugal 305 99 - 336 101 53 - 44 27 15ro Romania 312 266 164 47 125 - - - 25 24se Sweden 864 746 841 301 105 - 125 129 4 38si Slovenia 34 - - - 10 - 5 10 - 0sk Slovakia 11 - - - 7 - - 1 - 14uk United Kingdom 4 906 4 571 1 298 3 085 1 406 1 839 2 007 729 - 44Total 27 300 22 700 17 600 15 400 10 000 9 000 9 400 8 100 2 100 2 000

Marine aggregates

---

2 -4 -0 -

--

9 -4 -0 382 -6 -

-9 -

-- -2 -2 -4 -6 -

-6 -

-6 -

-4 -9 2940 300

Coastal tourism Cruise tourism Fisheries

- 17 33224 - 87185 - 5762 - 32

- - 341 245 373 7001 019 7 735

58 - 8512 652 51 2 889

170 - 1246 285 33 3 1001 879 - 1 182

- 7 26513 23 608

8 217 673 2 10924 - 63

- - -32 - 92

162 - 321 111 43 394

706 318 1 23660 6 243

1 139 58 666172 - 65466 3 186109 - 13

- 1 146 878 967 1 489

44 100 2 600 16 200

Policy Research Corporation 188 July 200813 November 2008

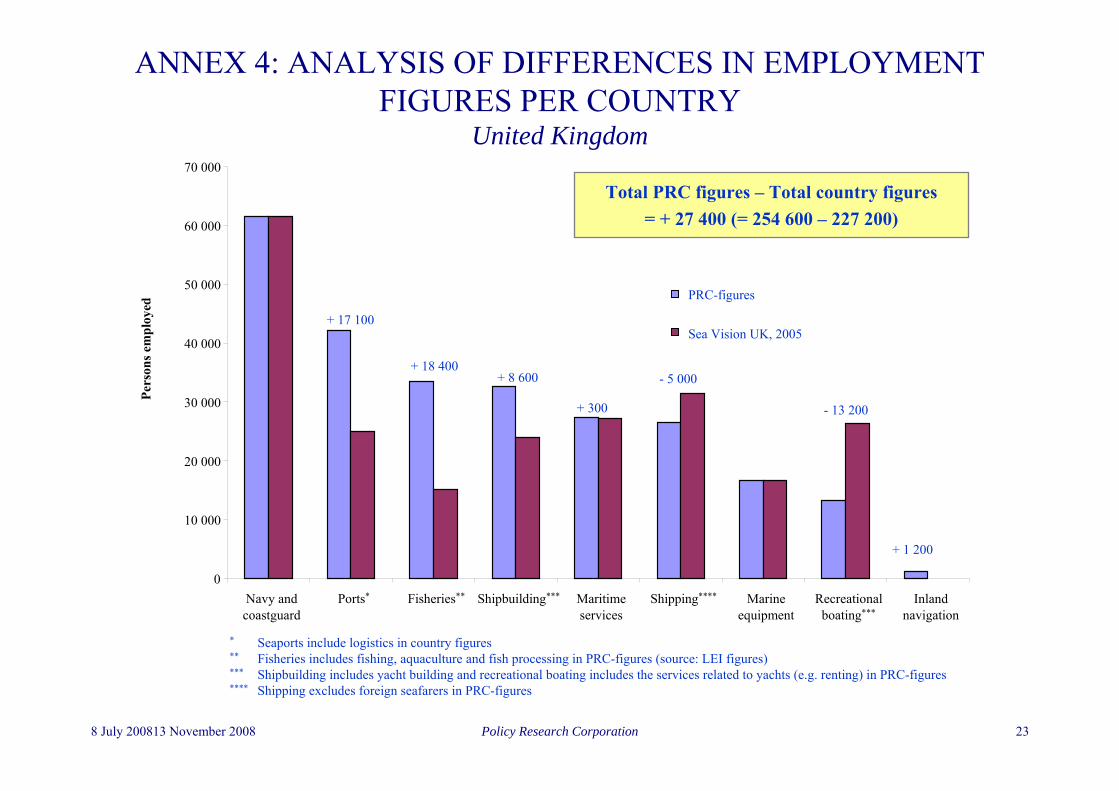

ANNEX 4: ANALYSIS OF DIFFERENCES IN EMPLOYMENT FIGURES PER COUNTRY

PRC-figures - Country figures

+ 6%+ 73 800+ 67 200+ 21 200+ 40 300+4 400+5 400- 61 200+ 7 000+ 15 800- 10 200- 16 100Total (28 countries)

+ 27 400

+ 3 900

- 23 700

- 7 600

- 7 100

+ 10 100

+ 21 000

Total

- 13 200

0

+ 2 900

- 21 900

- 21 000

(+1 600)

(+2 500)

Recre-ational

boating**

+ 11%+ 18 4000(+1 200)n.a.+ 17 10000+ 8 600+ 300- 5 000UK

+ 3%+ 3 900000000000Netherlands

- 11%+ 23 300(+47 300)(+200)(+ 700)- 63 000n.a.- 23 500+ 2 800- 13 900- 500Spain

- 3%+ 1 700- 4 000(+2 900)n.a.-1 200n.a.+ 6 900+ 11 300+ 400- 3 500Italy

- 2%+ 3 200- 4 700(+3 500)(+3 600)- 12 700- 500+ 21 800+ 1 000- 1 300France

+ 23%(+2 700)(+2 300)(+200)(+200)- 2 400+ 700+ 8 200- 6000- 2 800Finland

(+14 100)

Fishe-ries***

(+200)

Maritime works

n.a.

Inland navi-gation

n.a.

Seaports

(+ 300)

Navy and

coast-guard

0

Marine equip-ment

+ 6 600

Offshore

+ 22%+ 9000- 3 600Denmark

% of PRC-

figures

Shipbuil-ding**

Maritime services

Ship-ping*

Sector

Country****

Legend* Shipping excludes foreign seafarers** Shipbuilding includes yacht building and recreational boating includes the services related to yachts (e.g. renting)*** Fisheries includes fishing, aquaculture and fish processing (LEI figures)**** Denmark: offshore and coastal wind energy is excluded in country figures (source: Ministry of Economics and Business Affairs

(2006) – The Danish Maritime Cluster: an agenda for growth)Finland: marine equipment: not all equipment manufacturing companies are inquired to obtain country figures (source: Association of Finnish Maritime Industries (2003) – The Finnish maritime cluster)France: seaports include non-maritime port services in country figures (source: Cluster Maritime Français, 2005)Italy: source: Federazione del Mare (2006) – Rapporto sull’ economia del mareSpain: in country figures maritime services includes non-maritime part of services, shipbuilding includes indirect employment, marine equipment includes non-maritime part and ports include logistics (source: Spanish Maritime Cluster (2005) – Quantification and economic impact of the maritime sector and CEET estimates)The Netherlands: source: Policy Research Corporation (2006) – Economic monitor of Dutch maritime clusterUnited Kingdom: in country figures seaports exclude maritime port related services (source: Sea Vision UK, 2005)

∆ = PRC - Country figures+ = PRC > Country figure- = PRC < Country figure0 = PRC = Country figure( ) = not included in country figuresn.a. = not available

Policy Research Corporation 198 July 200813 November 2008

ANNEX 4: ANALYSIS OF DIFFERENCES IN EMPLOYMENT FIGURES PER COUNTRY

France

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

Fisheries* Navy andcoastguard**

Recreationalboating***

Ports**** Shipbuildingand marine

equipment***

Offshoresupply*****

Shipping****** Maritimeservices

Maritimeworks

Inlandnavigation

PRC-figures

Information from Cluster Maritime Français, 2005

- 1 300

+ 1 000

+ 21 800

- 500

- 12 700

+ 3 600 +3 500

- 4 700

- 21 000

+ 3 200

Pers

ons e

mpl

oyed

* Fisheries includes fishing, aquaculture and fish processing in PRC-figures (source: LEI figures)** Navy and coastguard includes all government action at sea (from sea rescue to aircraft carriers) in country figures; aircraft carriers are excluded in PRC-figures*** Shipbuilding includes yacht building and recreational boating includes the services related to yachts (e.g. renting) in PRC-figures**** Seaports include non-maritime port services in country figures***** Offshore supply includes a part of maritime services in country figures****** Shipping excludes foreign seafarers in PRC-figures

Total PRC figures – Total country figures = - 7 100 ( = 295 200 – 302 300)

Policy Research Corporation 208 July 200813 November 2008

ANNEX 4: ANALYSIS OF DIFFERENCES IN EMPLOYMENT FIGURES PER COUNTRY

Italy

* Shipbuilding and marine equipment includes yacht building and recreational boating includes the services related to yachts (e.g. renting) in PRC-figures; recreational boating in country figures is based upon direct and indirect effects of the sector and marine equipment is based upon indirect effects of shipbuilding industry in Federazione del Mare (2002) – Rapporto sull’ economia del mare

** Fisheries includes fishing, aquaculture and fish processing in PRC-figures (source: LEI figures)*** Navy and coastguard includes all government action at sea (from sea rescue to aircraft carriers) in country figures**** Ports include a part of maritime services***** Shipping excludes foreign seafarers in PRC-figures

Total PRC figures – Total country figures = - 7 600 (= 244 100 – 251 700)

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

Recreationalboating*

Fisheries** Navy andcoastguard***

Ports**** Marineequipment*

Shipbuilding* Shipping***** Inlandnavigation

Maritimeservices

Federazione del Mare (2006) – Rapporto sull’economia del mare

PRC-figures

Pers

ons e

mpl

oyed

+ 1 700

- 4 000

- 21 900

- 1 200+ 6 900 + 11 300 - 3 500

+ 2 900 + 400

Policy Research Corporation 218 July 200813 November 2008

ANNEX 4: ANALYSIS OF DIFFERENCES IN EMPLOYMENT FIGURES PER COUNTRY

Spain

Spanish Maritime Cluster (2005) – Quantification and economic impact of the maritime sector and CEET estimates

* Fisheries includes fishing, aquaculture and fish processing in PRC-figures (source: LEI figures)** Seaports include logistics in country figures*** Recreational boating includes services in PRC-figures, not yacht building **** Marine equipment includes non-maritime part in country figures***** Shipbuilding includes yacht building in PRC-figures****** Maritime services includes non-maritime part of services in country figures

Total PRC figures – Total country figures*

= - 23 700 ( = 224 000 – 247 700)

Pers

ons e

mpl

oyed

PRC-figures

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

Fisheries* Navy andcoastguard

Ports** Recreationalboating***

Marineequipment****

Shipping Shipbuilding***** Maritimeservices******

Maritimeworks

Inlandnavigation

Ecotec

* Commerce and distribution and other activities related are excluded in this figure; total country figure including these sectors amounts to 345 800

Policy Research Corporation 228 July 200813 November 2008

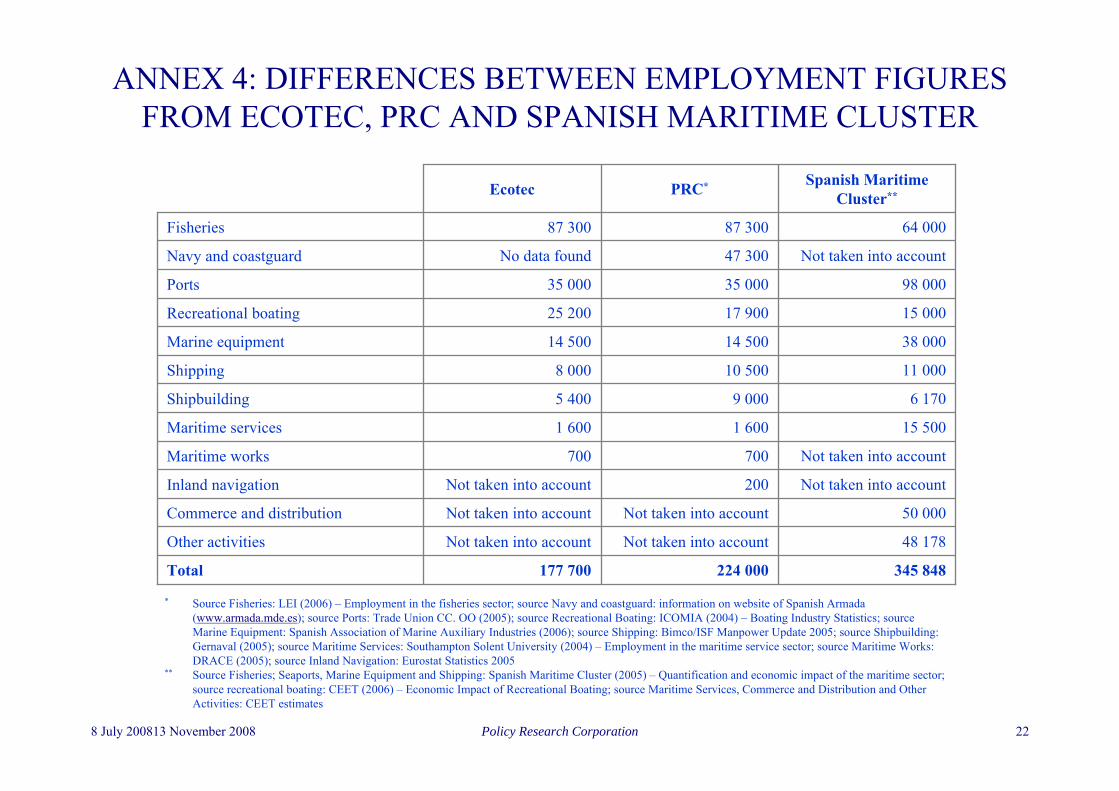

ANNEX 4: DIFFERENCES BETWEEN EMPLOYMENT FIGURES FROM ECOTEC, PRC AND SPANISH MARITIME CLUSTER

345 848224 000177 700Total

48 178Not taken into accountNot taken into accountOther activities

50 000Not taken into accountNot taken into accountCommerce and distribution

Not taken into account

No data found

Not taken into account200Inland navigation

Not taken into account700700Maritime works

15 5001 6001 600Maritime services

6 1709 0005 400Shipbuilding

11 00010 5008 000Shipping

38 00014 50014 500Marine equipment

15 00017 90025 200Recreational boating

98 00035 00035 000Ports

Not taken into account47 300Navy and coastguard

64 00087 30087 300Fisheries

Spanish Maritime Cluster**PRC*Ecotec

* Source Fisheries: LEI (2006) – Employment in the fisheries sector; source Navy and coastguard: information on website of Spanish Armada (www.armada.mde.es); source Ports: Trade Union CC. OO (2005); source Recreational Boating: ICOMIA (2004) – Boating Industry Statistics; source Marine Equipment: Spanish Association of Marine Auxiliary Industries (2006); source Shipping: Bimco/ISF Manpower Update 2005; source Shipbuilding: Gernaval (2005); source Maritime Services: Southampton Solent University (2004) – Employment in the maritime service sector; source Maritime Works: DRACE (2005); source Inland Navigation: Eurostat Statistics 2005

** Source Fisheries; Seaports, Marine Equipment and Shipping: Spanish Maritime Cluster (2005) – Quantification and economic impact of the maritime sector; source recreational boating: CEET (2006) – Economic Impact of Recreational Boating; source Maritime Services, Commerce and Distribution and Other Activities: CEET estimates

Policy Research Corporation 238 July 200813 November 2008

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

Navy andcoastguard

Ports* Fisheries** Shipbuilding*** Maritimeservices

Shipping**** Marineequipment

Recreationalboating***

Inlandnavigation

ANNEX 4: ANALYSIS OF DIFFERENCES IN EMPLOYMENT FIGURES PER COUNTRY

United Kingdom

Sea Vision UK, 2005

- 13 200+ 300

- 5 000+ 8 600

+ 1 200

+ 17 100

+ 18 400

* Seaports include logistics in country figures** Fisheries includes fishing, aquaculture and fish processing in PRC-figures (source: LEI figures)*** Shipbuilding includes yacht building and recreational boating includes the services related to yachts (e.g. renting) in PRC-figures**** Shipping excludes foreign seafarers in PRC-figures

Total PRC figures – Total country figures = + 27 400 (= 254 600 – 227 200)

Pers

ons e

mpl

oyed

PRC-figures

Policy Research Corporation 248 July 200813 November 2008

ANNEX 5: AREA 1 RESULTS TO BE INTEGRATED IN THE EUROPEAN CLUSTER OBSERVATORY’S DATABASE

0.21%

0.40%

0.59%

0.67%

0.70%

0.71%

0.91%

1.22%

1.26%

1.33%

1.35%

1.72%

2.12%

2.16%

1.14%

1.36%

1.54%

1.70%

1.89%

1.97%

2.03%

3.00%

3.11%

3.46%

4.31%

1.75%

2.40%

2.60%

4.19%

Size

StrongHigh28.61%0.71%59 757Area 1pl63 Pomorskie

StrongN/A10.67%0.75%4 106Area 1be23 Prov. Oost-Vlaanderen

StrongLow15.13%0.05%7 617Area 1mt Malta

StrongN/A16.29%0.08%11 392Area 1nl34 Zeeland

WeakMedium14.87%0.14%12 770Area 1de50 Bremen

StrongN/A11.71%0.93%13 516Area 1ukl1 West Wales and The Valleys

StrongMedium12.79%1.17%13 633Area 1ukc1 Tees Valley and Durham

Very strongLow14.09%0.07%17 507Area 1bg34 Yugoiztochen

Very strongHigh14.35%0.35%23 354Area 1no01 Oslo og Akershus

StrongHigh12.67%0.92%24 203Area 1ukj3 Hampshire and Isle of Wight

StrongHigh13.63%1.07%25 581Area 1be21 Prov. Antwerpen

StrongLow25.90%0.25%32 553Area 1pl42 ZachodniopomorskieWeakHigh29.58%0.24%29 598Area 1fi18 Etelä-Suomi

Very strongHigh28.04%1.21%26 096Area 1no04 Agder og RogalandStrongMedium25.71%2.86%21 950Area 1uke1 East Yorkshire and Northern LincolnshireWeakMedium13.28%0.39%41 503Area 1fr52 Bretagne

Very strongMedium13.23%0.48%40 634Area 1def0 Schleswig-Holstein

Very strongMedium14.26%0.29%25 852Area 1ee00 Estonia

WeakHigh12.02%0.40%32 988Area 1gr30 Attiki

StrongHigh22.83%2.36%36 200Area 1uki1 Inner London

WeakLow25.16%0.37%37 731Area 1de80 Mecklenburg-Vorpommern

Very strongLow23.76%1.23%38 894Area 1lv Latvia

StrongMedium23.70%1.35%57 545Area 1fr82 Provence-Alpes-Côte d'Azur

Very strongHigh 23.86%4.58%66 491Area 1nl33 Zuid-Holland

StrongMedium23.00%6.41%82 632Area 1dk0 Denmark

Very strongHigh34.48%0.96%33 545Area 1fr23 Haute-Normandie

WeakMedium311.71%1.33%46 139Area 1no05 Vestlandet

49 864

80 366

Persons employed

3

3

Stars

Low

N/A

Innovation

0.76%

2.22%

Specialisation

8.04%

7.04%

Focus

StrongArea 1itc3 Liguria

WeakArea 1ro22 Sud-Est

ExportsCategoryNUTS II region

Policy Research Corporation 258 July 200813 November 2008

Very StrongN/A18.00%0.00%0.23%5 566Area 2gr41 Voreio AigaioStrongLow111.24%0.00%0.30%7 204Area 2fr83 Corse

0.45%0.57%0.57%0.65%1.00%1.01%1.24%1.26%1.39%1.39%1.46%1.51%1.55%1.89%1.99%1.64%1.69%1.85%1.96%1.99%2.22%2.35%3.24%3.94%4.12%6.87%1.77%3.52%3.66%

Size

StrongMedium24.19%0.56%78 391Area 2itd5 Emilia-Romagna

Very StrongLow17.41%0.01%11 000Area 2mt MaltaStrongHigh15.86%0.02%13 706Area 2ukk3 Cornwall and Isles of Scilly

Very strongN/A15.68%0.01%13 840Area 2gr25 PeloponnisosVery strongN/A117.29%0.01%15 684Area 2gr22 Ionia NisiaVery strongN/A120.14%0.02%24 243Area 2gr42 Notio AigaioVery strongN/A19.52%0.02%24 474Area 2gr43 Kriti

StrongHigh15.92%0.10%29 941Area 2ukk4 DevonVery StrongLow18.78%0.06%30 555Area 2cy00 CyprusVery StrongLow117.30%0.04%33 548Area 2pt15 Algarve

StrongMedium15.41%0.10%33 554Area 2itc3 Liguria

StrongMedium22.97%0.18%44 839Area 2ite1 ToscanaStrongLow22.37%0.15%40 894Area 2itf3 CampaniaStrongHigh24.38%0.17%39 789Area 2ukj3 Hampshire and Isle of WightWeakHigh11.74%0.08%48 017Area 2dk0 DenmarkWeakN/A14.00%0.09%45 610Area 2ro22 Sud-Est

Very strongN/A19.62%0.05%37 456Area 2bg33 Severoiztochen

Very StrongN/A18.22%0.05%35 197Area 2bg34 YugoiztochenStrongLow13.00%0.12%36 635Area 2itf4 Puglia

StrongLow23.23%0.21%47 505Area 2itg1 SiciliaStrongHigh23.81%0.26%48 138Area 2ukj2 Surrey, East and West SussexStrongMedium23.45%0.12%53 582Area 2fr82 Provence-Alpes-Côte d'AzurStrongMedium22.75%0.29%56 740Area 2itd3 Veneto

Very strongLow24.64%0.31%95 250Area 2es52 Comunidad ValencianaVery strongLow23.31%0.34%99 679Area 2es61 AndaluciaVery strongMedium25.05%0.93%166 161Area 2es51 Cataluña

StrongHigh35.42%0.20%42 891Area 2ukl1 West Wales and The Valleys85 19088 457

Persons employed

33

Stars

LowLow

Innovation

0.25%0.26%

Specialisation

18.20%10.58%

Focus

Very strongArea 2es53 Illes BalearsVery strongArea 2es70 Canarias (ES)

ExportsCategoryNUTS II region

ANNEX 5: AREA 2 RESULTS TO BE INTEGRATED IN THE EUROPEAN CLUSTER OBSERVATORY’S DATABASE

Policy Research Corporation 268 July 200813 November 2008

N/AN/A11.27%0.02%0.53%2 337Area 3nl23 FlevolandStrongN/A12.75%0.01%0.56%2 493Area 3gr22 Ionia Nisia

0.62%0.65%0.68%0.71%0.76%0.84%0.91%0.98%1.04%1.05%1.17%1.17%1.44%1.48%1.54%1.10%1.37%1.51%1.60%1.78%2.15%2.38%2.39%2.70%3.11%3.17%2.20%4.17%

10.24%

Size

N/AN/A20.93%0.28%10 600Area 3ro22 Sud-Est

Very strongN/A11.40%0.02%2 738Area 3no06 TrøndelagStrongN/A11.26%0.01%2 875Area 3gr11 Anatoliki Makedonia, Thraki

Very strongN/A11.35%0.02%3 009Area 3no07 Nord-NorgeStrongN/A11.29%0.02%3 154Area 3gr25 PeloponnisosWeakMedium11.29%0.05%3 375Area 3de50 BremenStrongN/A13.10%0.03%3 733Area 3gr42 Notio AigaioStrongLow11.70%0.03%4 056Area 3es13 CantabriaStrongN/A16.24%0.04%4 346Area 3gr41 Voreio AigaioStrongN/A12.12%0.07%4 612Area 3gr24 Sterea ElladaWeakMedium11.21%0.09%4 658Area 3uke1 East Yorkshire and Northern Lincolnshire

StrongMedium21.10%0.09%6 700Area 3ee00 EstoniaWeakMedium21.12%0.21%6 063Area 3fr25 Basse-NormandieWeakMedium22.29%0.12%4 887Area 3ukm6 Highlands and IslandsStrongMedium10.21%0.08%6 841Area 3es51 Cataluña

Very strongLow10.45%0.08%6 565Area 3lt LithuaniaWeakLow10.52%0.08%6 401Area 3itf4 Puglia

WeakMedium11.79%0.06%5 184Area 3ukm5 North Eastern ScotlandWeakMedium10.33%0.10%5 187Area 3fr51 Pays de la Loire

WeakLow21.02%0.09%7 104Area 3pl63 PomorskieStrongLow20.44%0.10%7 892Area 3pt11 NorteWeakMedium21.23%1.71%9 532Area 3fr53 Poitou-Charentes

Very strongLow21.02%0.23%10 580Area 3lv Latvia

WeakLow20.82%0.27%12 005Area 3itg1 SiciliaStrongLow20.46%0.27%13 821Area 3es61 Andalucia

Very strongHigh20.51%0.43%14 060Area 3dk0 DenmarkStrongLow35.03%1.04%9 754Area 3pt15 Algarve

18 50245 487

Persons employed

33

Stars

MediumLow

Innovation

0.99%4.38%

Specialisation

1.46%4.03%

Focus

WeakArea 3fr52 BretagneStrongArea 3es11 Galicia

ExportsCategoryNUTS II region

ANNEX 5: AREA 3 RESULTS TO BE INTEGRATED IN THE EUROPEAN CLUSTER OBSERVATORY’S DATABASE

Policy Research Corporation 278 July 200813 November 2008

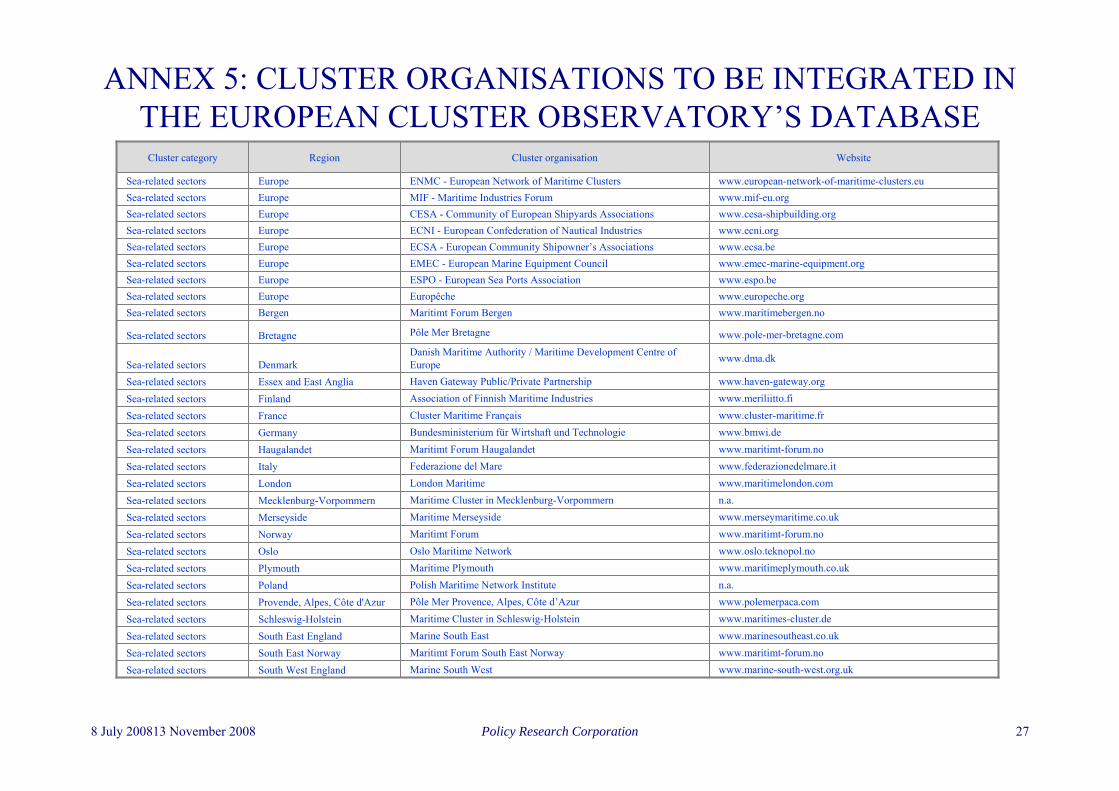

ANNEX 5: CLUSTER ORGANISATIONS TO BE INTEGRATED IN THE EUROPEAN CLUSTER OBSERVATORY’S DATABASE

www.espo.beESPO - European Sea Ports AssociationEuropeSea-related sectors

www.marine-south-west.org.ukMarine South WestSouth West EnglandSea-related sectorswww.maritimt-forum.noMaritimt Forum South East NorwaySouth East NorwaySea-related sectorswww.marinesoutheast.co.ukMarine South EastSouth East EnglandSea-related sectorswww.maritimes-cluster.deMaritime Cluster in Schleswig-HolsteinSchleswig-HolsteinSea-related sectorswww.polemerpaca.comPôle Mer Provence, Alpes, Côte d’AzurProvende, Alpes, Côte d'AzurSea-related sectorsn.a.Polish Maritime Network InstitutePolandSea-related sectorswww.maritimeplymouth.co.ukMaritime PlymouthPlymouthSea-related sectorswww.oslo.teknopol.noOslo Maritime NetworkOsloSea-related sectorswww.maritimt-forum.noMaritimt ForumNorwaySea-related sectorswww.merseymaritime.co.ukMaritime MerseysideMerseysideSea-related sectors

www.haven-gateway.orgHaven Gateway Public/Private PartnershipEssex and East AngliaSea-related sectorswww.meriliitto.fiAssociation of Finnish Maritime IndustriesFinlandSea-related sectorswww.cluster-maritime.frCluster Maritime FrançaisFranceSea-related sectorswww.bmwi.deBundesministerium für Wirtshaft und TechnologieGermanySea-related sectorswww.maritimt-forum.noMaritimt Forum HaugalandetHaugalandetSea-related sectorswww.federazionedelmare.itFederazione del MareItalySea-related sectors

n.a.Maritime Cluster in Mecklenburg-VorpommernMecklenburg-VorpommernSea-related sectorswww.maritimelondon.comLondon MaritimeLondonSea-related sectors

www.dma.dkDanish Maritime Authority / Maritime Development Centre of EuropeDenmarkSea-related sectors

www.pole-mer-bretagne.comPôle Mer BretagneBretagneSea-related sectors

www.maritimebergen.noMaritimt Forum BergenBergenSea-related sectorswww.europeche.orgEuropêcheEuropeSea-related sectors

www.emec-marine-equipment.orgEMEC - European Marine Equipment CouncilEuropeSea-related sectorswww.ecsa.beECSA - European Community Shipowner’s AssociationsEuropeSea-related sectorswww.ecni.orgECNI - European Confederation of Nautical IndustriesEuropeSea-related sectorswww.cesa-shipbuilding.orgCESA - Community of European Shipyards AssociationsEuropeSea-related sectors

MIF - Maritime Industries ForumENMC - European Network of Maritime Clusters

Cluster organisation

www.mif-eu.orgEuropeSea-related sectorswww.european-network-of-maritime-clusters.euEuropeSea-related sectors

WebsiteRegionCluster category

Policy Research Corporation 288 July 200813 November 2008

FR

North SeaNL

Brussels

ANNEX 6: EMPLOYMENT IN ALL SEA-RELATED SECTORS ON NUTS II-LEVEL IN BELGIUM

Belgium employs 36 700 persons in Area 1, 9 700 persons in Area 2 and1 700 persons in Area 3

Employment figures for Belgium in all Areas

Employment figures for Belgium in all Areas

36 700

9 700

1 700

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Vlaamse Havencommissie (2005) –Jaaroverzicht van de Vlaamse Havens 2005, BIMCO/ISF (2005) – Manpower 2005 update, and Eurostat – Industry, Trade and Services (Annual enterprise statistics) 2005, Eurostat – Maritime Transport 2005, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

4 100

25 600

7 000 9 700 1 700

∑ = 48 100

Belgium

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 298 July 200813 November 2008

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN BULGARIA

Bulgaria employs 29 700 persons in Area 1, 72 700 persons in Area 2 and900 persons in Area 3

Employment figures for Bulgaria in all Areas

Employment figures for Bulgaria in all Areas

Source: Policy Research based on Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat –Maritime Transport Statistics 2005, Eurostat – Industry, Trade and Services (Annual enterprise statistics) 2005, Eurostat – Tourism indicators 2005, and United Nations (2004) – Fishery country profile

17 50035 200

500

29 700

72 700

9000

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

12 200

37 500

400

∑ = 103 300

Bulgaria

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 308 July 200813 November 2008

Employment figures for Cyprus in all Areas

Employment figures for Cyprus in all Areas

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN CYPRUS

Cyprus employs 10 100 persons in Area 1, 30 600 persons in Area 2 and1 200 persons in Area 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

10 100

30 600

1 200

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

10 10030 600

1 200

∑ = 41 900

Cyprus

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 318 July 200813 November 2008

DE

Baltic Sea

Kattegat

Skagerrak

Copenhagen

Employment figures for Denmark in all Areas

Employment figures for Denmark in all Areas

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN DENMARK

82 600

48 000

14 100

82 600

48 000

14 100

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

Denmark employs 82 600 persons in Area 1, 48 000 persons in Area 2 and14 100 persons in Area 3

Source: Policy Research based on Ecotec (2006), the Danish Maritime Authority (2007) – Fakta om søfart, Eurostat – Tourism indicators 2005 and LEI (2006) –Employment in the fisheries sector

∑ = 144 700

Denmark

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 328 July 200813 November 2008

Employment figures for Estonia in all Areas

Employment figures for Estonia in all Areas

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORSON NUTS II-LEVEL IN ESTONIA

Estonia employs 25 900 persons in Area 1, 7 200 persons in Area 2 and6 700 persons in Area 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

25 9007 200 6 700

25 900

7 200 6 700

0

5 000

10 000

15 000

20 000

25 000

30 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

∑ = 39 800

Estonia

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 338 July 200813 November 2008

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN FINLAND

Finland employs 42 100 persons in Area 1, 5 300 persons in Area 2 and2 700 persons in Area 3

Employment figures for Finland in all Areas*

Employment figures for Finland in all Areas*

42 100

5 3002 700

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

10 400500 1 200

* Annex 4 shows the differences in employment with the Finnish maritime cluster studies; in this country map only the most significant regions with regard to employ-ment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, CESA – Annual Report 2006-2007, Eurostat – Industry, Trade and Services (Annual enterprise statistics) 2005, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

∑ = 50 100

29 600

3 400 600

Finland

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 348 July 200813 November 2008

Paris

Employment figures for France in all Areas*

Employment figures for France in all Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN FRANCE

57 40053 600

2 100

22 30012 5004 600

41 50030 400

18 500

20 80014 1005 500

33 40011 3002 400

20 00010 3006 100

16 00017 8005 200

7 70012 3009 500

6 10026 100

4 400

1 400 7 200 400

France employs 230 700 persons in Area 1, 208 200 persons in Area 2 and64 700 persons in Area 3

* Annex 4 explains the differences in employment with the French maritime cluster study; in this country map only the most significant regions with regard to employ-ment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Information of French Maritime Cluster organisation, L’Insee (2006) – Ports Maritimes Autonomes, Eurostat – Tourism indicators 2005 and LEI (2006) – Employment in the fisheries sector

∑ = 503 600

France

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

230 700

208 200

64 700

0

50 000

100 000

150 000

200 000

250 000

Area 1 Area 2 Area 3

Pers

onse

mpl

oyed

Policy Research Corporation 358 July 200813 November 2008

Berlin

Employment figures for Germany in all Areas*

Employment figures for Germany in all Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN GERMANY

197 500

73 300

16 400

0

50 000

100 000

150 000

200 000

250 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

40 60025 300

2 900

25 30012 300

1 800

37 70026 100

1 90027 100

800

12 800800 3 400

Germany employs 197 500 persons in Area 1, 73 300 persons in Area 2 and16 400 persons in Area 3

* In this country map only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research based on information of German maritime cluster organisation, Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Zentralverband der deutschen Seehafenbetriebe (2005) – Seegüterumschlag ausgewählter Häfen, and Eurostat – Tourism Indicators 2005 and LEI (2006) –Employment in the fisheries sector

∑ = 286 900

45 000

Germany

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 368 July 200813 November 2008

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN GREECE

Employment figures for Greece in all areas*

Employment figures for Greece in all areas*

Ionian Sea

Aegean Sea

Athens

5 90024 500

1 800

2 50024 200

3 700

200 5 600 4 300

33 000

4 700

5 500 7 800 4 60070015 700

2 500

10 600

35 900

5 100

76 200

165 300

37 700

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

180 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

Greece employs 76 200 persons in Area 1, 165 300 persons in Area 2 and37 700 persons in Area 3

* In the country maps only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the employment shown in this and following maps is somewhat lower than employment in Area 1, 2 and/or 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

∑ = 279 200

Greece

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 378 July 200813 November 2008

Employment figures for Ireland in all Areas

Employment figures for Ireland in all Areas

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN IRELAND

Ireland employs 6 400 persons in Area 1, 21 400 persons in Area 2 and10 600 persons in Area 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

6 400

21 400

10 600

0

5 000

10 000

15 000

20 000

25 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

6 100 14 900 5 700

300 6 500 4 900

∑ = 38 400

Ireland

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 388 July 200813 November 2008

Rome

Employment figures for Italy in all Areas*Employment figures for Italy in all Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN ITALY

196 100

480 700

48 000

0

100 000

200 000

300 000

400 000

500 000

600 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

49 90033 600

1 400

18 500

56 700

3 800

7 200

78 400

2 900

20 70044 800

1 500

10 900

40 900

3 40012 500

36 600

6 400

9 600

47 500

12 000

13 60026 300

3 800

Italy employs 196 100 persons in Area 1, 480 700 persons in Area 2 and48 000 persons in Area 3

* Annex 4 explains the differences in employment with the Italian maritime cluster studies; in this country map only the most significant regions with regard to employ-ment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Federazione del Mare (2006) –Rapporto sull’economia del mare, Assoporti and Censis (2008) – Analisi dell’ impatto economico e occupazionale dei porti commerciali italiani – La nautica in cifre, UCINA (2007), Information on website of Assonave, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

10 500 1 500

26 500

20 4001 300

21 100

2 900 3 50017 600

∑ = 724 80011 900 2 800

25 800

Italy

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 398 July 200813 November 2008

Employment figures for Latvia in all Areas

Employment figures for Latvia in all Areas

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN LATVIA

Latvia employs 38 900 persons in Area 1, 6 000 persons in Area 2 and10 600 persons in Area 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

38 900

6 000

10 600

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

38 900

6 000 10 600

∑ = 55 500

Latvia

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 408 July 200813 November 2008

Employment figures for Lithuania in all Areas

Employment figures for Lithuania in all Areas

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN LITHUANIA

Lithuania employs 21 600 persons in Area 1, 6 300 persons in Area 2 and6 600 persons in Area 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

21 6006 300 6 600

21 600

6 300 6 600

0

5 000

10 000

15 000

20 000

25 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

∑ = 34 500

Lithuania

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 418 July 200813 November 2008

Employment figures for Malta in all Areas

Employment figures for Malta in all Areas

ANNEX 6: EMPLOYMENT SEA-RELATED SECTORS ON NUTS II-LEVEL IN MALTA

Malta employs 7 600 persons in Area 1, 11 000 persons in Area 2 and1 400 persons in Area 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

7 600

11 000

1 400

0

2 000

4 000

6 000

8 000

10 000

12 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

Mediterranean Sea

7 600 11 000 1 400

∑ = 20 000

Malta

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 428 July 200813 November 2008

North

Sea

Employment figures for the Netherlands in all Areas*

Employment figures for the Netherlands in all Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORSON NUTS II-LEVEL IN THE NETHERLANDS

The Netherlands employ 128 100 persons in Area 1, 53 400 persons in Area 2 and 9 000 persons in Area 3

128 100

53 400

9 000

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

66 500

15 5001 600

25 00023 4001 700

600 2 300

11 4006 000 1 200

* Annex 4 explains the differences in employment with the Dutch maritime cluster study; in this country map only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research Corporation (2006) – Economic Monitor of the Dutch Maritime Cluster, Information from members of Scheepsbouw Nederland (VNSI and HME), Nationale Havenraad (2005), Eurostat, Tourism Indicators 2005 and LEI (2006)

∑ = 190 500

The Netherlands

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 438 July 200813 November 2008

SE

Norweg

ian S

ea

Employment figures for Norway in all Areas*

Employment figures for Norway in all Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN NORWAY

110 000

29 600

16 700

0

20 000

40 000

60 000

80 000

100 000

120 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

46 100

5 600 4 500

23 3007 500 1 100

26 1005 000 2 700

Norway employs 110 000 persons in Area 1, 29 600 persons in Area 2 and16 700 persons in Area 3

* In this country map only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research, also based on Maritimt Forum (2007) – Maritim Verdiskapingsbok, Statistics Norway, and Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study and Eurostat

∑ = 156 300

2 900 2 7003 100

7 800 3 0004 100

Norway

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 448 July 200813 November 2008

DE Warsaw

Baltic SeaEmployment figures for Poland in all

Areas*Employment figures for Poland in all

Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN POLAND

59 800

5 400 7 100

32 600

4 700 5 000

117 000

10 10019 900

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

Poland employs 117 000 persons in Area 1, 10 100 persons in Area 2 and19 900 persons in Area 3

* In this country map only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

∑ = 147 000

Poland

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 458 July 200813 November 2008

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN PORTUGAL

Portugal employs 29 000 persons in Area 1, 109 100 persons in Area 2 and33 200 persons in Area 3

Employment figures for Portugal in all Areas*

Employment figures for Portugal in all Areas*

29 000

109 100

33 200

0

20 000

40 000

60 000

80 000

100 000

120 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

11 600 21 2002 800

3 20019 500

5 500

100

33 5009 800

5 600 9 600 7 900

* In this country map only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, BIMCO/ISF (2005) – Manpower 2005 update, Members of Associação das Indústrias Marítimas, Eurostat – Maritime Transport Statistics 2005, Eurostat – Industry, Trade and Services (Annual enterprise statistics) 2005, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

∑ = 171 300

Portugal

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 468 July 200813 November 2008

Bucharest

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN ROMANIA

Romania employs 80 400 persons in Area 1, 45 600 persons in Area 2 and10 600 persons in Area 3

Employment figures for Romania in all Areas

Employment figures for Romania in all Areas

Source: Policy Research based on Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, European Foundation for the improvement of living and working conditions (2008) – Article concerning port workers in Romania, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Industry, Trade and Services (Annual enterprise statistics) 2005, Eurostat – Tourism indicators 2005, and United Nations (2004) – Fishery country profile

80 400

45 600

10 600

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

80 400

45 600

10 600

∑ = 136 600

Romania

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 478 July 200813 November 2008

Employment figures for Slovenia in all Areas

Employment figures for Slovenia in all Areas

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN SLOVENIA

Slovenia employs 1 700 persons in Area 1, 7 400 persons in Area 2 and600 persons in Area 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

1 700

7 400

600

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

1 700 7 400 600

∑ = 9 700

Slovenia

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 488 July 200813 November 2008

Madrid

Employment figures for Spain in all Areas*

Employment figures for Spain in all Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN SPAIN

136 700

652 400

87 300

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

14 100

88 500

4 900 28 700

99 700

13 800

6 900

85 200

1 3009 700

95 200

5 700

17 000 6 800

166 2008 200

38 300

5 20018 30039 10045 500 1 500

11 6004 100

Spain employs 136 700 persons in Area 1, 652 400 persons in Area 2 and87 300 persons in Area 3

13 6003 20012 300

* Annex 4 explains the differences in employment with the Spanish maritime cluster study; in this country map only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Cluster Maritimo Español (2005) Quantification and economic impact of the maritime sector, Information of Uninave and Asociación Española de Industrias Auxiliares Marítimas, Puertos del Estado (2005) – Anuario Estadístico, Eurostat – Tourism Indicators 2005, and LEI (2006) – Employment in the fisheries sector

∑ = 876 400

Spain

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 498 July 200813 November 2008

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORS ON NUTS II-LEVEL IN SWEDEN

Sweden employs 48 300 persons in Area 1, 18 200 persons in Area 2 and4 000 persons in Area 3

Employment figures for Sweden in all Areas*

Employment figures for Sweden in all Areas*

9 600 5 700 700

22 5002 400 2 300

48 300

18 200

4 000

0

10 000

20 000

30 000

40 000

50 000

60 000

Area 1 Area 2 Area 3

Pers

ons e

mpl

oyed

* In this country map only the most significant regions with regard to employment in Area 1, 2 and/or 3 are shown; hence the sum of employment figures shown in this map is somewhat lower than total employment in Area 1, 2 and/or 3

Source: Policy Research based on Ecotec (2006) – Employment trends in all sectors related to the sea or using sea-resources, Houthoff Buruma and Policy Research (2007) – IPR Shipbuilding study, BIMCO/ISF (2005) – Manpower 2005 update, Members of Sweden Ocean Industry Group, and Eurostat – Industry, Trade and Services (Annual enterprise statistics) 2005, Eurostat – Tourism indicators 2005, and LEI (2006) – Employment in the fisheries sector

∑ = 70 500

Sweden

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Area 1: Traditional maritime sectorsArea 2: Coastal (and marine) tourism and recreationArea 3: Fisheries

Policy Research Corporation 508 July 200813 November 2008

Employment figures for United Kingdom in all Areas*

Employment figures for United Kingdom in all Areas*

ANNEX 6: EMPLOYMENT IN SEA-RELATED SECTORSON NUTS II-LEVEL IN UNITED KINGDOM

35 900

3 100 8 100 5 200

13 300

42 900

1 000

8 80029 900

1 30010 400

26 800

500

24 00039 800

400

4 200

48 100

800

21 5005 400 4 700