Annex - World Banksiteresources.worldbank.org/INTAFRREGTOPHIVAIDS/... · Web viewCapacity to track...

105

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES Annex 1 A Financial Management Self Assessment Questionnaire for Category A Organizations Name of Organization: Assessment completed by: Date: Bank Review/Assessment completed by: Date: Note: If there is more than one implementing entity, a Questionnaire should be completed for each entity Topic Yes No N/A Review* Remarks/Comments 1.Implementing Entity 1.1 What is the legal status/registration of the entity? 1.2 Has the entity implemented a Bank- financed project in the past? 1.3 What are the statutory reporting requirements for the entity? 1.4 Is the governing body for the project independent? 1.5 Is the organizational structure appropriate for the needs of the project ? Risk Assessment (Implementing Entity) H S M N 2. Funds Flow Yes No N/A Review* 2.1 Describe the funds flow arrangements, including a chart and explanation of the flow of funds from the World Bank, government, and other financiers. 1

Transcript of Annex - World Banksiteresources.worldbank.org/INTAFRREGTOPHIVAIDS/... · Web viewCapacity to track...

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Annex 1 A

Financial Management Self Assessment Questionnaire for Category A Organizations

Name of Organization:

Assessment completed by: Date:

Bank Review/Assessment completed by: Date:

Note: If there is more than one implementing entity, a Questionnaire should be completed for each en-tity

Topic Yes No N/A Review* Remarks/Comments1.Implementing Entity1.1 What is the legal status/registra-tion of the entity?1.2 Has the entity implemented a Bank-financed project in the past?1.3 What are the statutory reporting requirements for the entity?1.4 Is the governing body for the pro-ject independent?1.5 Is the organizational structure ap-propriate for the needs of the project ?

Risk Assessment (Implementing En-tity)

H S M N

2. Funds Flow Yes No N/A Review*2.1 Describe the funds flow arrange-ments, including a chart and explana-tion of the flow of funds from the World Bank, government, and other financiers.

2.2. Are the arrangements to transfer the proceeds of the loan (from the government / ministry of finance) to the entity satisfactory?

2.3 Have there been major problems in the past in receipt of funds by the entity?2.4 In which bank will the Special Ac-count be opened?2.5 Does the PIU have experience in the management of disbursements from the World Bank?

2.7 Does the entity have/need a capa-city to manage foreign exchange risks?2.8 How are the counterpart funds ac-cessed?

1

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

2.9 How are payments made from the counterpart funds?2.10 If part of the project is implemen-ted by communities or NGOs, does PIU have the necessary reporting and monitoring features built into its sys-tems to track the use of project pro-ceeds by such agencies?2.11 Are the beneficiaries required to contribute to project costs? If benefi-ciaries have an option to contribute in kind (in the form of labor), are proper guidelines formulated to record and value the labor contribution?

Risk Assessment (Funds Flow) H S M N

3. Staffing Yes No N/A Review*3.1 What is the organizational struc-ture of the accounting department? At-tach an organization chart.3.2 Identify the accounts staff, includ-ing job title, responsibilities, educa-tional background and professional experience. Attach job descriptions and CVs of key accounting staff.

3.3 Is the project finance and accounts function staffed adequately?

3.4 Is the finance and accounts staff adequately qualified and experienced?

3.5 Is the project accounts and finance staff trained in Bank procedures?

3.6 What is the duration of the con-tract with the finance and accounts staff?3.7 Indicate key positions not contrac-ted yet, and the estimated date of ap-pointment.

3.10 Does the project have written po-sition descriptions that clearly define duties, responsibilities, lines of super-vision, and limits of authority for all of the officers, managers, and staff ?3.11 At what frequency is the staff transferred?3.12 What is training policy for the finance and accounting staff?

Risk Assessment (Staffing) H S M N

4. Accounting Policies and Proced-ures

Yes No N/A Review*

4.1 Does the entity have an accounting system that allows for the proper re-

2

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

cording of project financial transac-tions, including the allocation of ex-penditures in accordance with the re-spective components, disbursement categories, and sources of funds? Will the project use the entity accounting system?

4.2 Are controls in place concerning the preparation and approval of trans-actions, ensuring that all transactions are correctly made and adequately ex-plained?4.3 Is the chart of accounts adequate to properly account for and report on project activities and disbursement categories?4.4 Are cost allocations to the various funding sources made accurately and in accordance with established agree-ments?4.5 Are the General Ledger and subsi-diary ledgers reconciled and in bal-ance?

4.6 Are all accounting and supporting documents retained on a permanent basis in a defined system that allows authorized users easy access?

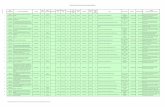

Segregation of Duties

4.7 Are the following functional re-sponsibilities performed by different units or persons: (a) authorization to execute a transaction; (b) recording of the transaction; and (c) custody of as-sets involved in the transaction?

4.8 Are the functions of ordering, re-ceiving, accounting for, and paying for goods and services appropriately segregated?

4.9 Are bank reconciliations prepared by someone other than those who make or approve payments?

Budgeting System4.10 Do the budgets lay down phys-ical and financial targets? 4.11 Are budgets prepared for all sig-nificant activities in sufficient detail to provide a meaningful tool with which to monitor subsequent performance?4.12 Are actual expenditures com-pared to the budget with reasonable frequency, and explanations required

3

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

for significant variations from the budget?4.13 Are approvals for variations from the budget required in advance or after the fact?

4.14 Who is responsible for prepara-tion and approval of budgets?

4.15 Are procedures in place to plan project activities, collect information from the units in charge of the differ-ent components, and prepare the budgets?4.16 Are the project plans and budgets of project activities realistic, based on valid assumptions, and developed by knowledgeable individuals ?

Payments4.17 Do invoice processing proced-ures provide for:Copies of purchase orders and re-ceiving reports to be obtained directly from issuing departments?Comparison of invoice quantities, prices, and terms, with those indicated on the purchase order and with records of goods actually received?Comparison of invoice quantities with those indicated on the receiving reports?Checking the accuracy of calcula-tions?4.18 Are all invoices stamped PAID, dated, reviewed and approved, and clearly marked for account code as-signment? 4.19 Do controls exist for the prepara-tion of the payroll and are changes to the payroll properly authorized?

Policies And Procedures

4.20 What is the basis of accounting (e.g., cash, accrual)?

4.21 What accounting standards are followed?

4.22 Does the project have an ad-equate policies and procedures manual to guide activities and ensure staff ac-countability?

4.23 Is the accounting policy and pro-cedure manual updated for the project activities?4.24 Do procedures exist to ensure

4

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

that only authorized persons can alter or establish a new accounting prin-ciple, policy, or procedure to be used by the entity?4.25 Are there written policies and procedures covering all routine finan-cial management and related adminis-trative activities?4.26 Do policies and procedures clearly define conflict of interest and related party transactions (real and apparent) and provide safeguards to protect the organization from them?

4.27 Are manuals distributed to appro-priate personnel?

Cash and Bank

4.28 Are there any project bank ac-counts opened yet?

4.29 Indicate names and positions of authorized signatories in the bank ac-counts.4.30 Does the project maintain an ad-equate, up-to-date cash book, record-ing receipts and payments?

4.31 Do controls exist for the collec-tion, timely deposit, and recording of receipts at each collection location?4.32 Are bank and cash reconciled on a monthly basis?4.33 Are all unusual items on the bank reconciliation reviewed and approved by a responsible official?

4.34 Are all receipts deposited on a timely basis?

Safeguard over Assets

4.35 Is there a system of adequate safeguards to protect assets from fraud, waste, and abuse?4.36 Are subsidiary records of fixed assets and stocks kept up to date and reconciled with control accounts?

4.38 Are there periodic physical in-ventories of fixed assets and stocks?

4.39 Are assets sufficiently covered by insurance policies?

Other Offices and Implementing En-tities4.40 Are there any other regional of-

5

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

fices or executing entities participating in implementation?4.41 Has the project established con-trols and procedures for flow of funds, financial information, accountability, and audits in relation to the other of-fices or entities?

4.42 Does information among the dif-ferent offices/implementing agencies flow in an accurate and timely fash-ion?

4.43 Are periodic reconciliations per-formed among the different offices/implementing agencies?

Other4.44 Has the project advised employ-ees, beneficiaries, and other recipients to whom to report if they suspect fraud, waste, or misuse of project re-sources or property?

Risk Assessment (Accounting Policies and Procedures)

H S M N

5. Internal Audit Yes No N/A Review*5.1 Is there a internal audit department in the entity?5.2 What are the qualifications and ex-perience of audit department staff? 5.3 To whom does the internal auditor report?5.4 Will the internal audit department include the project in its work pro-gram?

5.5 Are actions taken on the internal audit findings?

Risk Assessment (Internal Audit) H S M N

6. External Audit Yes No N/A Review*6.1 Is the entity financial statement audited regularly by an independent auditor? Who is the auditor?

6.2 Are there any delays in audit of the entity? When are the audit reports issued?6.3 Is the audit of the entity conducted according to the International Stand-ards on Auditing?

6.4 Were there any major accountabil-ity issues brought out in the audit re-

6

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

port of the past three years?

6.5 Will the entity auditor audit the project accounts or will a separate auditor be appointed to audit the pro-ject financial statements?

6.6 Are there any recommendations made by the auditors in prior audit re-ports or management letters that have not yet been implemented?

6.7 Is the project subject to any kind of audit from an independent govern-mental entity (e.g., the supreme audit institution) in addition to the external audit?6.8 Has the project prepared accept-able terms of reference for an annual project audit?

Risk Assessment (External Audit) H S M N

7. Reporting and Monitoring Yes No N/A Review*7.1 Are financial statements prepared for the entity? In accordance with which accounting standards?

7.2 Are financial statements prepared for the implementing unit?

7.3 What is the frequency of prepara-tion of financial statements? Are the reports prepared in a timely fashion so as to useful to management for de-cision making? 7.4 Does the reporting system need to be adapted to report on the project components?

7.5 Does the reporting system have the capacity to link the financial in-formation with the project's physical progress? If separate systems are used to gather and compile physical data, what controls are in place to reduce the risk that the physical data may not synchronize with the financial data?

7.6 Does the project have established financial management reporting re-sponsibilities that specify what reports are to be prepared, what they are to contain, and how they are to be used?7.7 Are financial management reports used by management?7.8 Do the financial reports compare actual expenditures with budgeted and programmed allocations?

7.9 Are financial reports prepared dir-ectly by the automated accounting

7

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

system or are they prepared by spread-sheets or some other means?

Risk Assessment (Monitoring and Re-porting)

H S M N

8.Information Systems Yes No N/A Review*8.1 Is the financial management sys-tem computerized?8.2 Can the system produce the neces-sary project financial reports?8.3 Is the staff adequately trained to maintain the system?8.4 Does the management organiza-tion and processing system safeguard the confidentiality, integrity, and availability of the data?

Risk Assessment (Monitoring and Re-porting)

H S M N

8

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

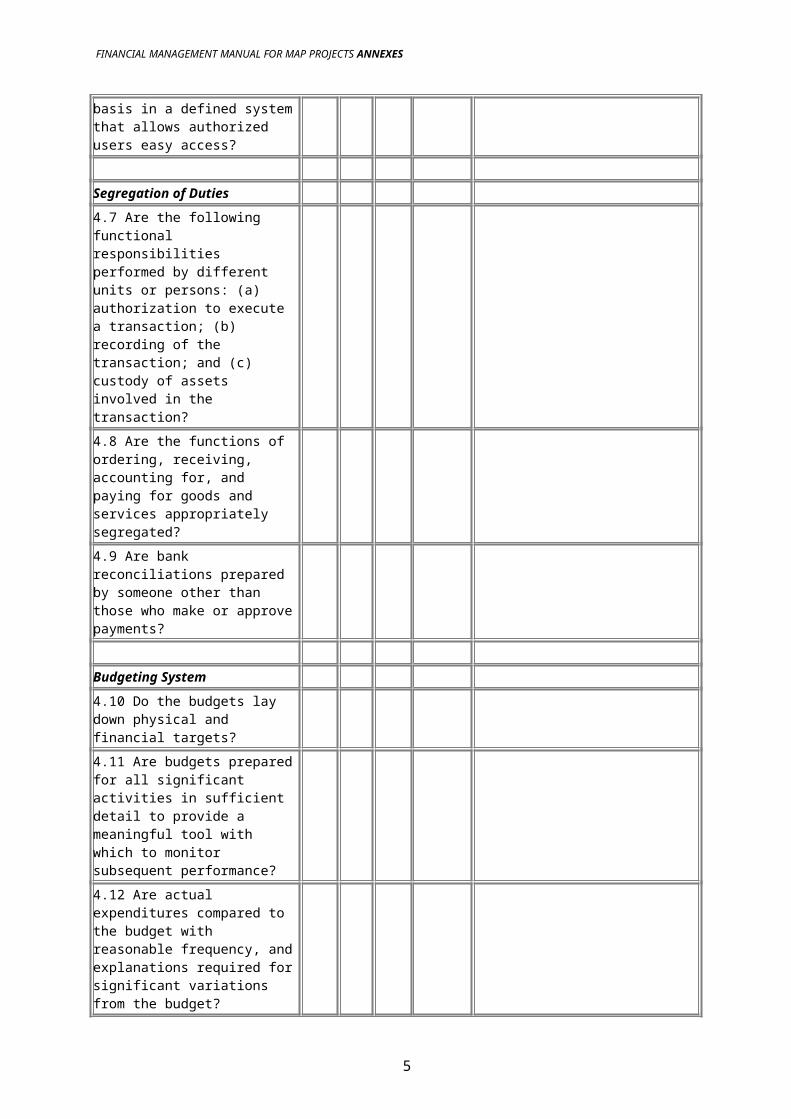

Annex 1 B

Financial Management Assessment Questionnaire for Category B Organizations

Project:

Self-Assessment completed by: Date:

Bank Review/Assessment completed by: Date:

Note: If there is more than one implementing entity, a Questionnaire should be completed for each en-tity

Topic Yes No N/A Review* Remarks/Comments1.Implementing Entity1.1 What is the legal status/regis-tration of the entity?1.2 Has the entity been involved with a Bank-financed project in the past?

1.3 What are the reporting require-ments for the entity?

1.4 Is the organizational structure appropriate for the needs of the project ?

Risk Assessment (Implementing Entity)

H S M N

2. Funds Flow Yes No N/A Review*2.1 Describe the funds flow ar-rangements from the Category A organization.

2.2. Does the entity have a bank account with an acceptable foinan-cial institution and are the arrange-ments to transfer project funds sat-isfactory?2.3 Have there been major prob-lems in the past in receipt of funds by the entity?

2.4 In which bank will the project account be opened?

2.5 Does the entity have experi-ence in the management of dis-bursements from the World Bank financed projects

2.6 Does the organization have the necessary reporting and monitoring features built into its systems to track the use of project proceeds?

2.7 Are proper guidelines formu-lated to record and value in-kind

9

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

contributions by communities?

Risk Assessment (Funds Flow) H S M N

3. Staffing Yes No N/A Review*3.1 Does the organization have an accounting department? 3.2 Identify the accounts staff, in-cluding job title, responsibilities, educational background and pro-fessional experience.3.3 Is the accounts function staffed adequately?3.4 Is the accounts staff adequately qualified?3.5 What is the duration of the contract with the accounts staff?3.6 What is training policy for the accounting staff?

Risk Assessment (Staffing) H S M N

4. Accounting Policies and Pro-cedures

Yes No N/A Review*

4.1 Does the entity have an ac-counting system that allows for the proper recording of project finan-cial transactions?4.2 Are controls in place concern-ing the preparation and approval of transactions?

4.3 Is the chart of accounts ad-equate to properly account for and report on project activities and dis-bursement categories?

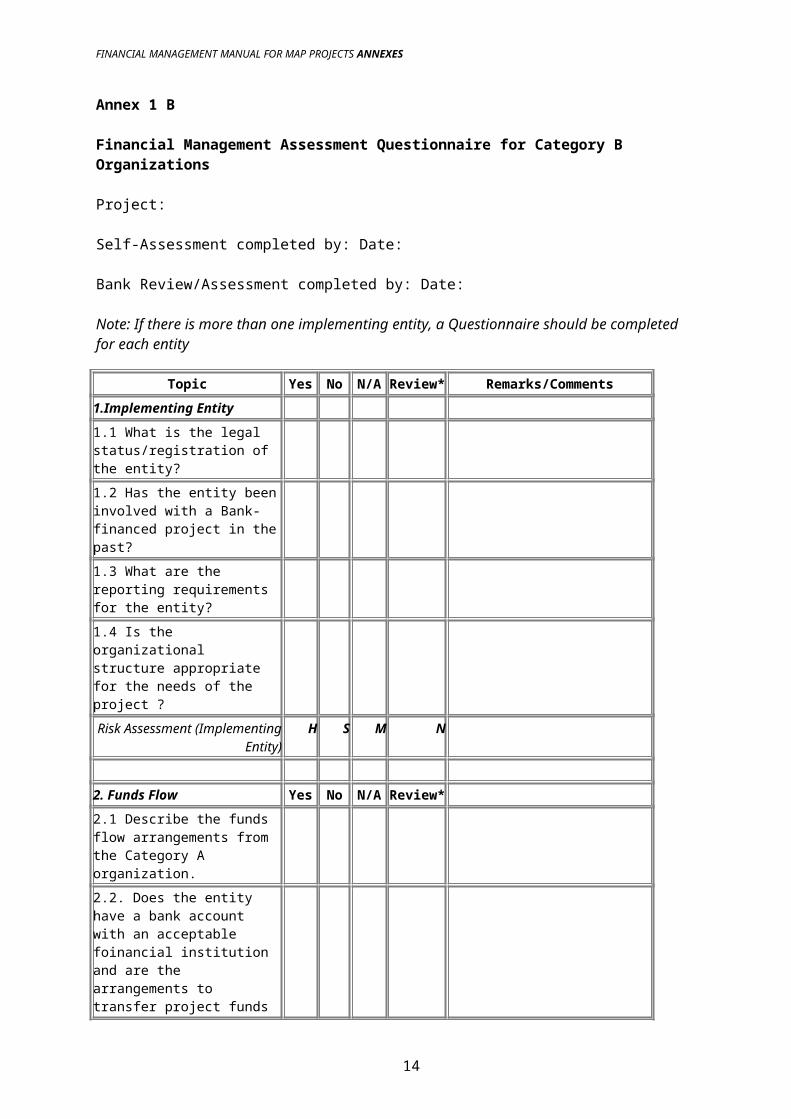

4.4 Are all accounting and support-ing documents retained on a per-manent basis in a defined system that allows authorized users easy access? 4.5 Are internal control procedures adequate?4.6 What is the basis of accounting (e.g., cash, accrual)?4.7 What accounting standards are followed?4.8 Does the organization have an financial management manual to guide activities and ensure staff ac-countability and are these distrib-uted to appropriate personnel?

4.9 Does the organization maintain an adequate, up-to-date cash book?

10

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

4.10 Do controls exist for the col-lection, timely deposit, and record-ing of receipts at each collection location?4.11 Are bank and cash reconciled on a monthly basis?4.12 Is there a system of adequate safeguards to protect assets from fraud, waste, and abuse?

Risk Assessment (Accounting Policies and Procedures)

H S M N

5. External Audit Yes No N/A Review*5.1 Is the entity financial statement audited regularly by an independ-ent auditor? Who is the auditor?5.2 When are the audit reports is-sued?5.3 Is the audit of the entity con-ducted according to the Interna-tional Standards on Auditing?

5.4 Were there any major account-ability issues brought out in the audit report of the past three years?5.5 Will the entity auditor audit the project accounts or will the NAS auditor be appointed to audit the project financial statements?5.6 Are there any recommenda-tions made by the auditors in prior audit reports or management letters that have not yet been implemen-ted?

5.7 Is the project subject to any kind of audit from an independent governmental entity (e.g., the su-preme audit institution) in addition to the external audit?

Risk Assessment (External Audit) H S M N

6. Reporting and Monitoring Yes No N/A Review*6.1 Are financial statements pre-pared for the entity? In accordance with which accounting standards?6.2 What is the frequency of pre-paration of financial statements? Are the reports prepared in a timely? 6.3 Does the reporting system need to be adapted to report on the pro-ject components?

6.4 Does the reporting system have

11

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

the capacity to link the financial information with the project's physical progress?

6.5 Does the project have estab-lished financial management re-porting responsibilities that specify what reports are to be prepared, what they are to contain, and how they are to be used?

6.6 Are financial management re-ports used by management?

6.7 Do the financial reports com-pare actual expenditures with budget?6.8 Are financial reports prepared directly by the automated account-ing system or are they prepared by spreadsheets or some other means?

Risk Assessment (Monitoring and Reporting)

H S M N

7.Information Systems Yes No N/A Review*7.1 Is the financial management system computerized?7.2 Can the system produce the ne-cessary project financial reports?7.3 Is the staff adequately trained to maintain the system?7.4 Does the management organiz-ation and processing system safe-guard the confidentiality, integrity, and availability of the data?

Risk Assessment (Monitoring and Reporting)

H S M N

12

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Annex 2

Terms of Reference for the Financial Management Agency of the HIV/AIDS Community Initiative Account

A. Background

The Government of Kenya has obtained assistance from the International Development Agency (IDA) in financing the Kenya HIV/AIDS Disaster Response Project. The project contributes to the partnership against HIV/AIDS in Kenya by supporting the Government’s program as articulated in the National HIV/AIDS Strategic Plan. The purpose of this program is to reduce the spread of HIV/AIDS, to mitigate the socio-economic impact of the disease, and to increase access to care and support for people infected or affected by the HIV/AIDS epidemic in Kenya. The National HIV/AIDS Strategic Plan is the reference for both the program and the project.

For the specific purpose of involving civil society organizations, the private sector and re-search institutions in the national response to the HIV/AIDS epidemic, and making financial resources under the project available to these organizations, the National AIDS Control Council (NACC) will establish an HIV/AIDS Community Initiative Account. Resources advanced by the NACC to this Ac-count will be used for the financing of sub-projects to be proposed and implemented by civil society organizations after approval by the NACC Secretariat or its decentralized entities at provincial, dis-trict or constituency level (PACCs, DACCs and CACCs). Allocations of resources among the various organizations underline the strong priority that will be given to community driven local initiatives. Initiatives with a national or regional coverage, private sector activities and research will only receive modest support.

The HIV/AIDS Community Initiative Account will contribute to the improvement of the wel-fare of communities by increasing their access to financial and human resources to prevent further spread of HIV and to address the impact of the epidemic on individuals and households. The sub-pro-jects will be identified, prepared, implemented, managed and maintained by beneficiary communities or organizations. The responsibility for operation and maintenance of the sub-projects will depend on the nature of the sub-project, but is likely to be that of the community and supporting Community Based Organizations, Non-Governmental Organizations and Religious Organizations.

The HIV/AIDS Community Initiative Account will respond to demands for sub-projects, which aim to address the prevention of HIV infection or the problems related to the impact of HIV/AIDS on those infected or affected. These may include:

activities aimed at behavior modeling or behavior change. Examples include peer programs, formal and informal education programs for out-of-school children, con-dom promotion;

social support to those affected by HIV/AIDS, including orphans. Assistance to or-phans in the form of psychosocial support, school fees, school uniforms, health care, food, and shelter are among the anticipated activities;

training programs for community volunteers and support to training for counselors and home based care-givers, procurement of supplies for home based care such as gloves and essential medical supplies;

support to organizations of people who are HIV positive or affected by the epidemic, seed funding to start income generating activities, establish patient support centers.

13

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

The NACC is a newly established parastatal, mandated to lead, co-ordinate and monitor the national, multi-sectoral response to the HIV/AIDS epidemic. In view of the anticipated volume of sub-projects to be supported, the need for rapid disbursement of the funds, the limited experience of NACC admin-istering sub-projects, and the need for the highest degree of transparency and accountability, the NACC, in consultation with the Office of the President, the Ministry of Finance, and the International Development Association, intends to seek local and international expertise to implement the financial management responsibilities of the HIV/AIDS Community Initiative Account. Proposals will be sought from a short-list of qualified local and international firms.

The successful bidder will set-up and manage the Financial Management Agency (FMA) for the HIV/AIDS Community Initiative Account. This agency will be responsible for the disbursement and accounting of funds made available to organizations implementing sub-projects. The FMA will also provide a procurement specialist for the first year of the project to work closely with the procurement officer of the NACC Secretariat.

The NACC Secretariat will monitor the execution of the contract with the successful bidder and the performance of the Financial Management Agency will be reviewed periodically and during the regular external audit of NACC.

Organizations implementing sub-projects will be grouped into two:

Category 1 will report directly to the Financial Management Agency and will consist of those

1. presenting financial proposal in excess of US $15,000 that are reviewed and approved by PACCs or NACC

2. presenting financial proposals of up to US$ 15,000 that are reviewed and approved by DACCs or CACCs, but whose financial management capability is confirmed adequate.

Category 2 will report through a facilitating NGO and will consist of those presenting financial pro-posals of up to US$ 15,000 and whose financial management capacity is considered inadequate. The FMA will not deal directly with CBOs reporting through a facilitating NGO. It will be the responsib-ility of the facilitating NGO to manage and train them appropriately.

The NACC Secretariat and the decentralized entities of NACC will be responsible for the review and approval of proposals submitted by implementing organizations, according to the value of the proposal submitted and as reflected in the table below.

14

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Approval of Work-programs and Budgets for National, Regional, Local and Private Initiat-ives

Initiative Cate-Gory

Proposal ValueIn US $

Detailed Review and Approval By

To be ap-proved within

1. Local Initia-tives

1.1 Up-to 5,000 CACC 2 weeks

1.2 From 5,001 to 15,000

DACC 2 weeks

1.3 From 15,001 to 25,000

PACC 3 weeks

1.4 From 25,001 to 100,000

NACC 4 weeks

1.5 Above 100,000 NACC in con-sultation with the World Bank

4 weeks

2. National, Re-gional, Re-search and Private Sector Initiatives

2.1 Up-to 100,000 NACC 4 weeks

2.2 Above 100,000 NACC in con-sultation with the World Bank

4 weeks

The threshold of proposals for both local and national initiatives to be funded through the HIV/AIDS Community Initiative Account is US$200,000.

All costs associated with setting up and operating the Financial Management Agency will be defined by the bidders and should be included in the Financial Proposal. The bidders will have com-plete responsibility for identifying and hiring all local and international staff deemed necessary to ful-fil the responsibilities of the FMA. The Agency will be managed by a qualified and experienced senior professional with experience in the design and implementation of an appropriate financial man-agement and internal control system for projects of this nature. Additional staff of accountants and other professionals will be required as necessary to assist with disbursement, accounting, expenditure reviews, reporting, expenditure forecasts, internal control and sub-project issues. An illustrative list of professional for the FMA is presented in these ToRs, however the specific staffing arrangements for the Agency are at the discretion of the consultant firm bidding on these services.

The remaining pages outline in greater detail the Terms of Reference for the Financial Manage-ment Agency; required qualifications of mandatory and recommended staff; and the timing, duration, and duty post for the Agency’s staff.

B. Overall Responsibilities

The Financial Management Agency will support the National AIDS Control Council in all as-pects of financial management, disbursement and accounting related to the operations of the HIV/AIDS Community Initiative Account. The Agency will be responsible for the following:

1. Develop appropriate financial procedures in line with the directions spelled out in the Operational Manual for the HIV/AIDS Community Initiative Account; implement and enforce an adequate control system; and provide training and support to NGOs.

15

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

2. Design and set up a computerized financial management system for the adequate capture, analy-sis, and reporting of financial information in an accurate and timely fashion for all the funds ad-vanced to the Agency by NACC for which the FMA will have full responsibility. The system should be designed to be able to segregate all disbursements and accounts by implementing insti-tution, by geographic location (province, district, constituency, location and village), by type of implementing institution, by categories of expenditure, and by area of interest (prevention, care and support, capacity building, other).

3. Review all disbursement requests submitted by implementing and facilitating organizations and ensure propriety and eligibility.

4. Open and maintain a local currency HIV/AIDS Community Initiative Account, complete monthly reconciliation reports, and prepare monthly and quarterly reports of disbursements and accounts.

5. Document accounting and reporting procedures for implementing and facilitating organizations.

6. Effect payments to appropriate implementing and facilitating organizations upon authorization by NACC (CACC, DACC, PACC) and verification of the availability of funds, according to the pro-cedures outlined in the Operational Manual of the HIV/AIDS Community Initiative Account.

7. Ensure that all payment documentation is in order and in accordance with any special require-ments of NACC or IDA.

8. Monitor utilization of payments made to implementing and facilitating organizations and monitor actual expenditures against budgets and disbursements.

9. Maintain up-to-date accounting records and ledgers and record all financial transactions pertain-ing to the HIV/AIDS Community Initiative Account.

10. Prepare appropriate applications for replenishment of the HIV/AIDS Community Initiative Ac-count, to be submitted to NACC with quarterly financial reports of disbursements and accounts, and disbursement forecasts for the next quarter.

11. Facilitate any and all financial reviews of the funds and accounts under the authority of the Min-istry of Finance, including periodic audits and financial reviews by the Auditor General, or inde-pendent accounting agencies as appointed by the Auditor General.

12. Ensure that a proper internal control system is in place to achieve accountability at all levels.

13. Review financial management capacity of implementing or facilitating organizations that have submitted approved proposals with a value in excess of US$15,000. If deemed appropriate and necessary, provide training in financial management to these organizations.

14. Receive and examine financial reports from implementing and facilitating organizations.

15. Conduct periodic spot checks of implementing and facilitating organizations to ensure that ade-quate financial management controls are enforced.

16. On a sample basis conduct financial audits of implementing organizations receiving up to US$25,000, either directly or by subcontracting an audit firm. Ensure other implementing or fa-cilitating organizations submit audited accounts as specified in the respective funding agreements.

17. During the first year of operations, provide technical assistance to NACC to process procurements of goods, works, and services, in accordance with World Bank guidelines.

16

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

18. Receive and review independent audit reports from those implementing organizations receiving more than $25,000.

19. During the first year of operations, provide training in procurement for NACC staff.

20. During the first year of operations, elaborate simplified procurement guidelines for community based programs.

21. During the first year of operations, provide training for district based staff in procurement accord-ing to accepted, simplifies procurement guidelines at that level.

C. Reporting Responsibilities

The Financial Agency will be an autonomous body that provides services for, and reports to, the National AIDS Control Council. The Agency will ensure that all financial management functions required to operationalize the HIV/AIDS Community Initiative Account are carried out in accordance with international standards and according to the guidelines described in the Operational Manual for the HIV/AIDS Community Initiative Account. The Manager of the Agency will report to the Director of the NACC Secretariat for all the funds advanced by NACC to the HIV/AIDS Community Initiative Account.

The Agency will be responsible for the following reports:

1. Monthly disbursement reports, number of proposals reviewed, value of proposals reviewed and remaining balance.

2. Quarterly consolidated reports of disbursements and accounts, and disbursement forecasts for the next quarter.

3. Quarterly reports on number of proposals funded and total value of disbursements effected, by ge-ographic location (province, district, constituency, location and village), by type of implementing institution (not-for-profit non-government organization; community based organization, religious organization, for profit organization, facilitating NGO, research institution) , by categories of ex-penditure (goods, services, civil works, personnel emoluments, other recurrent expenditure), and by area of interest (prevention, care and support, capacity building, other).

4. Additional operational manuals, procedural guidelines and ad hoc reports as may be reasonably requested by NACC.

5. Performance against agreed upon performance criteria.

D. Resource Management Responsibilities

It is estimated that the Agency will have responsibility for overseeing the management of up to US$30 million. Of this total, approximately US$27.9 million will finance sub-projects at the local (village to district) level implemented by partner organizations at that level. These activities will be financed through sub-project financing agreements ranging from US$5,000 to US$25,000 in value. The remaining US$2.1 million will go toward the financing of proposals submitted by research insti-tutions (US$0.6 million), the corporate sector (US$0.3 million), and to civil society organizations with a regional or national coverage (US$1.2 million), The proposed review, approval and financial mech-anisms for these sub-projects is discussed in detail in the Operational Manual for the HIV/AIDS Com-munity Initiative Account.

E. Performance Criteria

17

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

The following performance criteria will be used to assess the performance of the Agency at regular intervals and based upon which the contract with the Agency can be continued or terminated:

1. timeliness of disbursement after reception of approved proposals and interim reports2. timeliness and quality of assistance provided to implementing organizations3. timeliness of audit report (i.e., sample audits of implementing organizations) submissions4. number and content of issues arising in the annual audit or periodic review of the FMA5. timeliness of submission of monthly and quarterly reports6. the quality of monthly and quarterly reports

F. Key Staff

Key staff of the Agency will include:

1. a Financial Management Specialist as the Program Manager2. an Accounting Manager3. an Internal Control Officer4. a Disbursement Officer5. a Procurement Specialist (for the first year only)

18

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Annex 3

Sample Terms of Reference for Financial Management Agency1

The Financial Management Agency (FMA) will support the National AIDS Control Council in all aspects of financial management, disbursement and accounting related to the operations of the HIV/AIDS Community Initiative Account. The Agency will be responsible for the following:

1. Develop appropriate financial procedures in line with directions spelled out in the Opera-tions Manual for the HIV/AIDS Community Initiative Account and the National AIDS Councils (NAC) Financial Manuals; implement and enforce an adequate control system; and provide training and support to Non Government Organizations.

2. Design and set up a computerised financial management system for the adequate capture, analysis, and reporting of financial information in an ac curate and timely fashion for all the funds advanced to the FMA by NAC for which the FMA will have full responsibility. The system should be designed to segregate all disbursement accounts by implementing institution, by geographic location (province, district, constituency, location, and village), categories of expenditure, and by area of interest (prevention, care and support, capacity building, and others).

3. Verify all disbursement requests submitted by implementing and facilitating organiza-tions and ensure propriety and eligibility.

4. Open and maintain a local currency HIV/AIDS Community Initiative Account, complete and submit monthly reconciliation reports, and prepare monthly and quarterly reports of disbursement and accounts.

5. Document accounting and reporting procedures for implementing and facilitating organ-izations in manual and electronic form.

6. Effect payments to appropriate implementing and facilitating organizations upon author-isation by NAC and verification of the availability of funds, according to to the proced-ures outlined in the Operational Manual of the HIV/AIDS Community Initiative Account.

7. Ensure that all payment documentation is in order and in accordance with any special re-quirements of NAC or the International Development Association (IDA).

8. Monitor utilisation of payments made to implementing and facilitating organizations and actual expenditures against budgets and disbursements.

9. Maintain up-to-date accounting records, ledgers and record all financial transactions per-taining to the HIV/AIDS Community Initiative Account.

10. Prepare appropriate applications for replenishment of the HIV/AIDS Community Initiat-ive Account, to be submitted to the NAC with quarterly financial reports of disbursements and accounts, and disbursement forecasts for the next quarter.

11. Facilitate any and all financial reviews of the funds and accounts under the authority of the Minister of Finance, including periodic audits and financial reviews of the Auditor General, or independent accounting agencies as appointed by the Auditor General.

1 Source: Kenyan Financial management Procedures Manual dated September 2002

19

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

12. Ensure that a proper internal control system is in place to achieve accountability at all levels.

13. review financial management capacity of implementing or facilitating organizations that have submitted approved proposals with a value in excess of Kshs. 1.2 million (about $US16,000). If deemed appropriate or necessary, provide training in financial manage-ment to these organizations.

14. Receive and examine financial reports from implementing and facilitating organizations.

15. Conduct periodic spot checks of implementing and facilitating organizations to ensure that adequate financial management controls are enforced.

16. On a sample basis conduct financial audits of implementing organizations receiving up to Kshs. 1.9 million (about $US 25,000) by subcontracting an audit firm. Ensure other im-plementing or facilitating organizations submit audited accounts as specified in the re-spective funding agreements.

17. During the first year of operations, provide technical assistance to CACC’s to process procurement of goods, works and services in accordance with World Bank Guidelines.

18. Receive and review independent audit reports from those implementing organizations re-ceiving more than Kshs. 1.9 million.

19. During the first year of operations, provide training in procurement for CACC’s.

20. During the first year of operations, elaborate simplified procurement guidelines for com-munity based programs.

21. During the first year of operations, provide training for district based staff in procurement according to accepted, simplified procurement guidelines at that level.

20

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Annex 4

Sample Internal Control Procedures

Accountable Documents Control

The objective of accountable documents control is to maintain a simple, permanent record of the purchase, issue, return, and ultimate disposal of all accountable documents.

Basic Controls Cheques, purchase orders, receipts and credit notes can be used to commit theft if they fall into the wrong hands. Thus, a high degree of security is required, with only limited access by staff to the books and boxes in use. New stocks should be held in a strong room and a designated person should be control their issue. Books and boxes in this category currently in use must be secured overnight and must not be left on unattended desks during working hours. A reliable member of staff who is not responsible for stationery use should control of new stationery. Storage should be in a locked stationery storeroom and not in an office cupboard.

Cancelled Cheques Where a cheque is cancelled due to an error (manual) or misprint (computer generated), the cheque will be cancelled using two diagonal lines across the whole face, with the word “cancelled” inserted between the lines. The signature portion at the bottom right of the cheque should be cut away neatly and destroyed. Additionally:

(i) The cash book payment voucher which is identified by the cheque number, must be cancelled also in the same way. A new voucher will be required to effect payment us-ing the replacement cheque number.

(ii) Where a manual cheque book is in use, cancelled cheques must be filed away immedi-ately and not retained in the cheque books.

Cancellation of all other numbered stationery It is possible to commit fraud by the manipulation of purchase orders, receipts, invoices, credit notes, and goods received vouchers, partic-ularly where these are shown as cancelled but the cancelled copy is missing. Therefore:

(i) Where a purchase order is cancelled, all copies must be stapled together and filed away in a file created for that purpose. The order must be cancelled diagonally as with cheque cancellation above.

(ii) The cancellation of receipts, invoices, credit notes, and goods received vouchers must be signed by a senior staff member, with carbon imprint on all copies.

(iii) The use of correcting fluids should not permitted by any staff, and physical checks must be made periodically to ensure that this stricture is enforced.

Storage of used, numbered stationery Insofar as possible, officers using accountable docu-ments should never have more than one book or box of pre-printed forms of any one type in their pos-session at any time. To obtain a new book or box, the last one must be returned for retention or be fully accounted for to the issuing officer.

Numbering To assist overall control, particularly at the NAS/NAC center, all boxes of numbered stationery should be sequentially numbered in ink at the top, using a separate sequence for each type of record. In addition:

(i) The cover should be endorsed with the first and last numbers of the documents inside.(ii) Both of operations should be carried out by the officer receiving the stationery from

the commercial printer.(iii) Users should endorse the front cover with start and completion dates, to speed sub-

sequent research.

21

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Register A bound book should be used to record the initial ordering, receiving, issue, and subsequent return of fast/file copies to the person controlling stationery issues.

Cash Controls- Bank Reconciliations

At least every month, the responsible officer must compare the bank statement entries with the corresponding month’s entries in the cash book. Entries on the bank statement not yet entered in the cash book must be so entered that they do not appear as reconciling items more than once. All other differences must be followed up and cleared. The financial controller must review the reconcili-ation and indicate this by signing and dating the reconciliation.

Cash- Cheque Payments

For accounting purposes, cash payments are deemed to include cheques, bank drafts, and transfers of funds out of the project’s bank account. Payments follow a World Bank approved pro-curement process.

Objective of Cash Payment Control The objective of a sound system of internal control over cash payments is that disbursements from bank accounts should be made only in respect of valid transactions.

FMA Role Where a Financial Management Agent (FMA) is part of the structure, dis-bursements to participating projects and implementing agents and partners will be made by the FMA, following agreed processes. The controls featured below apply to payments by the NAC/NAS to its own suppliers and service providers, as well as to the payments made to the FMA.

Basic Controls The features of internal control over cash payments are:

(i) Preparation of cheques and bank transfers Cheques and bank transfers should only be prepared on the basis of evidence that the transactions are valid (for instance, authorized invoices, approved payrolls, and authorized creditors payments).

(ii) Comparison of disbursement records All cheques and bank drafts should be com-pared in detail with transactions processed through the bank accounts as evidenced by the bank statements (for instance, as part of the bank reconciliation procedures).

In order to establish that all cash payments are in respect of valid transactions and have been

properly accounted for by proper entries in the cash book, the procedures outlined in the following paragraphs should be applied:

Unissued Cheques The supply of unissued cheques should be properly safeguarded against unauthorized access. They should be kept under strict control in a strong room under the con-trol of a senior official who must maintain a register of unused cheque forms/cheque books. The re-gister must show a record of the cheque forms/books received from the printers and those issued to the officer responsible for issuing cheques. All numbers issued must be accounted for, and the follow-ing procedures followed:

(i) An officer, other than the one who has custody over the unissued cheques, must mon-itor the status of the cheque forms and books.

(ii) Cheques and bank transfers must be prepared by persons other than those who initi-ated or approved any documents giving rise to a disbursement (for instance, in the case of purchases and payroll).

Cheque Invoices Cheques should only be drawn against a properly authorized cheque payment voucher supported by a valid invoice or other acceptable proof of debt. The invoice should be stamped with a processing stamp showing the following:

22

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

(i) Local purchase order number A copy of the order should be attached to the invoice, and the two matched. The order must be authorized only by a person designated to make out and sign orders.

(ii) Allocation Allocation must be clearly stated. Cheque signatories should only sign cheques when the payment voucher clearly indicates the ledger account code for the payment.

(iii) Checked Items The sections for “checked by” and “passed by” are extremely import-ant and should only be completed when the person signing the allocation stamp is sat-isfied that the right goods/service have been supplied, the cost is in accordance with that shown on the order, and, where applicable, the costs and extensions have been correctly calculated. The invoice should be passed for payment only after the signat-ory is satisfied that all these requirements have been met and that the allocation is cor-rect.

(iv) Cancelled Items All vouchers should be stamped “Cancelled - Cheque No…..” after processing to ensure that they are not re-presented for payment.

Civil Works Contracts Civil works contracts will be awarded in accordance with World Bank guidelines, and the payments will be based on authorized completion certificates. The re-sponsible person should also approve payment of any retention amount due to contractors. The con-tract details and the corresponding disbursements must be captured in the contract account in the gen-eral ledger in the currency of disbursement.

Filling-in cheques The cheque should be made out in the full name of the supplier (without abbreviations) for the exact amount authorized on the cheque payment voucher. The cheque number and payee should be entered on the cheque payment voucher. Any blank spaces on the lines for the payee and the amount should be blocked to avoid any additions to these lines after the signa-ture.

Pre-Printed Controls Cheque should be pre-printed with “Account payee only--Not Nego-tiable,” to avoid the possibility of loss to the project if the cheques are misappropriated. Bearer or cash cheques, and the signing of blank cheques, must be prohibited.

Cheque Signatures Cheques must be signed by two duly authorized officials. The pro-ject could have up to six signatories, divided into say two panels, where any member of one panel can sign with a member from another panel. The one panel must consist of the program/executive dir-ector, the financial controller, and the accountant, while the other panel can be made up of other senior managers. In addition:

(i) The signatories must carefully examine all supporting documentation relating to the cheque payment to satisfy themselves that the payment is for a valid transaction. The signatories must ensure the supporting documentation has been stamped “cancelled” with the relevant cheque number to prevent resubmission in support of additional pay-ments.

(ii) Where practical to do so, signed cheques should be dispatched by a person other than the preparer. Where suppliers physically collect cheques, this must be acknowledged by a signature in the “Cheque Collections” register, which indicates not only payment cheque details, but also the date and details of the person collecting the cheque.

Incoming Invoice Register An “Incoming Invoice” register must be maintained to record all invoices received. This register must be updated with the payment details of the cheque, once it has been signed.

Entry into Cash Book The computerized accounting system will automatically post the cheque (if printed out of the system) in the cash book.

23

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Filing and Checking Bank statements and paid cheques (or images) received from the bank must be delivered to the financial controller for examination before being handed over to the ac-countant for use in the bank reconciliation process. The financial controller must examine the cheques for evidence of renegotiation (change of payee), and must follow up where this occurs.

Cash Controls- Petty Cash Payments

A sound system of internal control over petty cash is important because disbursements should be made only for valid transactions, and these transactions should be accurately entered in the ac-counting records.

Basic Controls Three features of internal control are used to achieve these objectives:

(i) Petty cash must be kept on the imprest system. In this system the cashier is advanced a float of cash of a fixed amount that is replenished regularly by the amount of pay-ments made and on production of paid expense vouchers.

(ii) The cash in hand plus the paid expenses vouchers due for reimbursement should al-ways be equal to the amount of the float.

(iii) When the float is replenished, the relevant accounting record for petty cash and vouchers should be produced to the signatories of the reimbursement cheque, who should initial the accounting record concerned as evidence of approval of the reim-bursement.

Expenditure from Petty Cash Payments should be made only on the production of prop-erly completed and, where appropriate, authorized vouchers. These should be cancelled immediately to prevent their further use. This control is facilitated by numbering the vouchers sequentially at the time they are presented for payment. Generally, large items should not be paid through petty cash or similar funds and a limit should be imposed on the amount for any one payment.

Entering Transactions in the Accounting Records The coding or classification of expenditure for posting to the nominal ledger should be checked by the accountant, and should apply the following procedures:

(i) The arithmetical accuracy of the summaries of expenditure of petty cash used as a basis for making the general ledger entries should be checked before input into the general ledger.

(ii) The balance in the petty cash book must be checked against the balance in the nom-inal ledger at the end of each month.

(iii) After checking the coding expense summaries and the general ledger balance, the ac-countant – or his nominated alternate – should sign and date the actual petty cash book to indicate that this procedure has been followed.

Overall Control of Funds The first overall control feature to be applied is to ensure that fund balances are kept at reasonable amounts in relation to the level of expenditure. Other critical control features include the following:

(i) Imprest or similar funds should not be under the control of persons who have access to non-imprest funds.

(ii) Funds should be verified periodically and reconciled with the general ledger control account by a person other than the custodian. All funds in the custody of the same person should be verified at the same time.

(iii) While cash counts should take place regularly, the actual time and day of the count should be varied; the unpredictability of monitoring enhances its effectiveness.

24

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

(iv) Under no circumstances should any amounts be receipted into petty cash funds other than reimbursements under imprest.

Cash Controls- Receipts

Project funds derive from the Bank, the borrower’s contribution, other donors, and sales re-ceipts in cases where the project sells certain items (e.g., subsidized drugs). The guiding control prin-ciples to control receipts are that :

(i) An incoming cheque register is maintained to record all cheques received by the per-son(s) receiving/opening mail.

(ii) All receipts must be banked intact in the shortest possible time.(iii) Funds received from different donors must be accounted for separately, with a Source

and Uses of Funds statement produced for each donor at the end of the reporting period.

Replenishment of Special Accounts Special accounts are replenished in accordance with Bank guidelines.

Contracts

It is critical to ensure that only persons who have the authority to do so enter into agreements contractually binding the project.

Contract Review All contracts that purport to bind the project must be vetted by the project’s legal advisors before being signed by the designated officer to ensure that, from a legal standpoint, the project’s interests are not prejudiced.

Contract Copies A copy of every contract should be lodged with the project’s finan-cial controller for permanent reference.

Distinction Between a Contract and a Normal Purchase Order Although the policy stated above is relatively simple, there are some grey areas – especially concerning the point at which a nor-mal purchase order becomes a contract. Four factors must be borne in mind in this regard:

(i) Minor items such as a service contract on a photocopier need not be referred the law-yers.

(ii) On the other hand, it is important that an expert scrutinize any material binding agree-ment properly.

(iii) Any “standard” type of contract form produced by another party, that one might be asked to sign, has been written by, and for the benefit of, that party.

(iv) When in doubt, purchase orders and contracts should be referred to the project’s fin-ancial controller, who will decide whether the matter needs to be reviewed by law-yers.

As a rough guideline, any arrangement whereby the project incurs obligations other than simply to pay for goods or services, should be considered prima facie a contract, and subject to the guidance contained above in the Contract Review paragraph above.

Standard Contracts The project must engage its legal advisors to prepare a full range of standard contracts for use both by participating projects and the NAC.

Fixed Assets

Procurement of all assets must follow World Bank guidelines.

25

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Fixed assets purchased by and for the NAC/NAS Fixed assets purchased by and for the use of the NAC itself must be retained in the NAC’s books and be depreciated.

Fixed assets purchased with NAC/NAS Funds by Category B and C organizationsFixed assets purchased with NAC/NAS funds by implementing partners should be expensed directly and not carried on the books of the NAC/NAS. However, a program assets register must be main-tained by the category B or C organization for those higher value items whose cost exceeds an agreed threshold. This facilitates a level of physical control. The assets register should detail (a) location, (b) asset number, (c) asset type and description, (d) date of purchase, (e) cost, (f) information on applic-able donor, (g) date of first use, (h) depreciation rate, and (i) date and proceeds of disposal. The re-gister must be regularly reconciled to the general ledger fixed assets account.

Filing- Control of Old Records

The NAC will maintain the following records for the project:

(i) General File The signed loan agreement, the appraisal report, the list of authorized signatures, the categories of expenditure, and correspondence relating to the project should be kept in this file.

(ii) Method File Copies of disbursement applications submitted to the Bank should be kept in this file.

(iii) Other Files In addition, the following files should be maintained by the NAC:a. Separate files in respect of petty cash vouchers for respective financial years.b. Supporting documents for statements of expenditure, to be filed by application num-

ber to allow for easy access.c. All other used stationery must be sequentially filed and retained for at least the ap-

plicable minimum retention period.

Payroll

All project staff must be paid by the project. The payroll must be maintained by the NAC/NAS, and the following controls must be applied:

(i) All employee details are to be maintained on a payroll master file, which record de-tails such as engagement date, current salary, allowances, and salary review and re-view history.

(ii) All amendments to the payroll master file must be approved by the executive director and documented prior to entry on the payroll.

(iii) The financial controller will approve the payroll before payment.(iv) All deductions from the payroll on behalf of staff for contribution to social security,

income tax, medical insurance, and similar deductions must be promptly paid to the respective institutions concerned.

(v) Salaries for all staff (including temporary staff) must be paid by direct deposit into staff members’ bank accounts. Only where this is not possible will the practice of writing cheques to staff be adopted. In extreme cases, staff may be paid in cash. Any unpaid salary cash must be stored in a secure safe for no longer than a week. If it still remains unpaid after that period, it must be re-banked immediately.

Travel Expenses

The words “expense account” or “expense claim” cover any instance whereby an employee has to account for monies advanced to him or her by the project, or where he or she has incurred ex-penditure on behalf of the project that is not covered by an official purchase order.

26

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Objectives The accounting objectives of monitoring travel expenses are to ensure that (a) expense claims are submitted on time, (b) all funds are properly accounted for, and (c) no funds are spent without proper authorization.

Method of Operation The intention is to ensure that all cash advanced and expenditure so incurred will be automatically debited to an “expenses recoverable” account, and that this account will only be cleared out to the relevant ledger expense accounts by way of an authorized expense claim. Expenses recoverable accounts should be in the form of global (rather than individual) accounts in the nominal ledgers.

Advances All advances should be debited to the expenses recoverable account. The only exception to this rule is for advances from petty cash that are not for travel or entertainment, and which are outstanding for less than 24 hours and are covered by a purchase order; such advances may be debited direct to expenses.

Payments via creditors or cheque payments The creditors clerk will be instructed to debit the expenses recoverable account for all hotel, restaurant, and related expenses in the name of the per-son incurring the expense.

Direct debits to the project bank account These debits, which are usually in the form of travellers` cheques and the related bank charge, will be debited directly to the expenses recoverable account, again in the name of the person spending.

Clearing the expenses recoverable account The expenses recoverable account can only be cleared by credits arising from returned cash via the cash book or by an authorized expense claim. No other method of clearance is acceptable unless authorized by the financial controller.

Expense claims: time of submission Expense claims should be submitted no later than the second working day after the expense has been incurred or the employee returns to work, whichever occurs earlier. The principle involved is that all outstanding claims must be processed as soon as pos-sible and that no further advance will be considered until the previous one is cleared.

Expense claims: authorization Departmental managers are the lowest rank of authority per-mitted to authorize an expense. Accordingly, all employees will submit their claims to their respective managers for approval. Project executive directors authorize the claims of all managers, though they may delegate this authority to the financial controller. Under no circumstances may managers, other than the financial controller, authorize the claims of one another.

Contents of Claims Wherever possible, all claims should be substantiated by vouchers. This applies particularly to claims for hotel accommodation, food in hotels and restaurants, transport tickets, and petrol. All claims should reflect the following guidance:

(i) No claims should be made in respect of incidental small expenses, such as gratuities/tips. Instead, such expenses, as well as other incidentals, should be covered by a per diem allowance, to be claimed for each day claimants are away, including the day they leave and the day they return.

(ii) On long trips only, it is permissible to claim for laundry expenses, but laundry and dry cleaning expenses incurred on the claimant’s return should not be claimed.

(iii) Although a certain amount of latitude will be exercised by people responsible for au-thorizing claims, this is an area where strict discipline is essential. Employees of de-velopment projects should cost conscious when travelling.

Travel Claims Record keeping All travel claims should be compiled in triplicate on a stand-ard claim form. The person authorizing the expenditure should sign all copies. The top copy should be filed, with all relevant vouchers stapled neatly to it, in the appropriate journal file with other

27

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

journal vouchers. The second copy should be filed in the accounts department in alphabetical order (in date order within the alphabetical order). The third copy remains fast, in the Expense/Travel Claims Book.

28

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Annex 5

Project Internal Control Checklist

A project internal control checklist which may be used by management as a guide for assess-ing the adequacy of the NAC/NAS internal control system is detailed below. The checklist is inten-ded to serve as a guide. The first part is on the Control Environment and the second is on the Ac-counting System.

A Control Environment

The control environment should be assessed considering each of the following areas:

(i) Effectiveness of organizational structure. Is structure adequate, enabling NAC/NAS to monitor and control activities?

(ii) Board Management/Key Staff. Are these competent and is there sufficient coverage in key functions? Is there an independent board which is involved in monitoring the decisions and activities of management thus reducing the likelihood of unauthorized acts?

(iii) Budgets. Are strategic plans/budgets realistic and based on reasonable assumptions?(iv) Project Management Reports/Annual Reports. Does Management have sufficient re-

liable and relevant information produced on a timely basis to effectively monitor its activities?

(v) Adequate policies and procedures. Does the NAC/NAS have an adequate policies and procedures manual used to control activities and to ensure staff accountability? What measures has the NAC/NAS taken to control the possibility of fraud?

(vi) Risk of misstated accounts. Does the NAC/NAS have a review/approval process prior to submitting FMRs? To what extent are the FMRs used as a management re-porting tool?

(vii) Effectiveness of external auditors. Does the project have an effective and independ-ent auditor familiar with Bank requirements and with a good track record in working with the Bank?

B Accounting System

This check list addresses the accounting system of the project. The questions are designed to identify (i) the accounting controls which exist; and (ii) the risk of loss through undetected error or fraud. They can be used to identify issues for inclusion in action plans for improvement of project manage-ment systems.

General

(i) Does the entity have adequate written statements and explanations of its accounting policies and procedures such as:a. A chart of accounts?b. A specification of accounting records, accounting procedures and the required

supporting documentation?c. Assignment of responsibilities and delegation of authority, including specified

powers of authorization?d. Documentation and approval requirements for recording transactions and mak-

ing journal entries?(ii) Are accounting policy and procedure manuals updated as necessary?(iii) Are manuals distributed to appropriate personnel?

29

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

(iv) Do procedures exist to ensure that only authorized persons can alter or establish a new accounting principle, policy, or procedure to be used by the entity?

(v) Are controls in place concerning the preparation and approval of journal entries, en-suring that journal entries are correctly made and adequately explained?

(vi) Do all journal entries adequately identify the accounts in which accounting entries are to be made?

Bank and Cash balances

(i) Does the project maintain an adequate, up to date cashbook, recording receipts and payments?

(ii) Are all receipts deposited on a timely basis?(iii) Do controls exist for the collection, timely deposit, and recording of receipts at each

collection location?(iv) Do procedures exist for disbursement approval and for the signing of payment

orders/checks?(v) Are those who authorize payments appropriately controlled?(vi) Are checks paid/posted/delivered promptly?(vii) Are bank accounts properly authorized and opened with authorized banks and in ac-

cordance with Bank requirements?(viii) Do procedures exist for effective checks such as:

a. Comparison of payment orders/checks with disbursement records?b. Examination of actual signatures and endorsements with those authorized?c. Numerical sequence of payment orders/checks?d. Reconciliation of general ledger and other accounts?e. Comparison between bank statements and accounting records regarding

amounts and dates of sums received?f. Checking the calculations of the columns and rows of cashbooks, and reconcil-

ing the balances on the cashbook and bank statements at regular intervals?(ix) Are all unusual reconciling items reviewed and approved by a responsible official?(x) Are checks outstanding for a considerable time, periodically reviewed?

Procurement and Payables

For the Bank’s detailed procurement requirements see Procurement under IBRD Loans and IDA Credits, January 1995, and Selection and Employment of Consultants by World Bank Borrowers, January 1997.

(i) Are purchases of goods and services initiated by properly authorized requisitions bearing the approval of designated officials?

(ii) Are requisitions pre-numbered and are those numbers controlled?(iii) Are adequate procedures in place to ensure that procurement follows Bank require-

ments and the Loan Agreement?(iv) Are orders specific in terms of quality, quantity and description?(v) Are there procedures to ensure that goods are recorded as they are delivered to the

project or to its beneficiaries?(vi) Do invoice processing procedures provide for:

a. Copies of purchase orders and receiving reports to be obtained directly from is-suing departments?

b. Comparison of invoice quantities, prices and terms, with those indicated on the purchase order and with records of goods actually received?

c. Comparison of invoice quantities with those indicated on the receiving reports?d. Checking the accuracy of calculations?

(vii) Are amounts payable according to the accounting records compared regularly with the sums appearing in statements from suppliers?

30

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Employee Compensation Salaries and Wages

(i) Do controls exist for the preparation of the payroll and are changes to the payroll properly authorized?

(ii) Are payroll rosters reviewed and approved by management, before disbursements are made?

(iii) Are gross pay and deductions from pay reviewed independently for reasonableness?(iv) Are payroll advances to officials and employees prohibited or subject to appropriate

review?(v) Are there adequate procedures to ensure that payroll deductions are correct and that

the sums deducted are paid by the entity to the appropriate authority?

31

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Annex 6

Sample Financial Monitoring Reports

Please lift these from - Financial Monitoring Reports: Guidelines to Staff- Annex A Sample 3, pages 1 to 7. Note, this is the same as the reference in the GOM

32

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

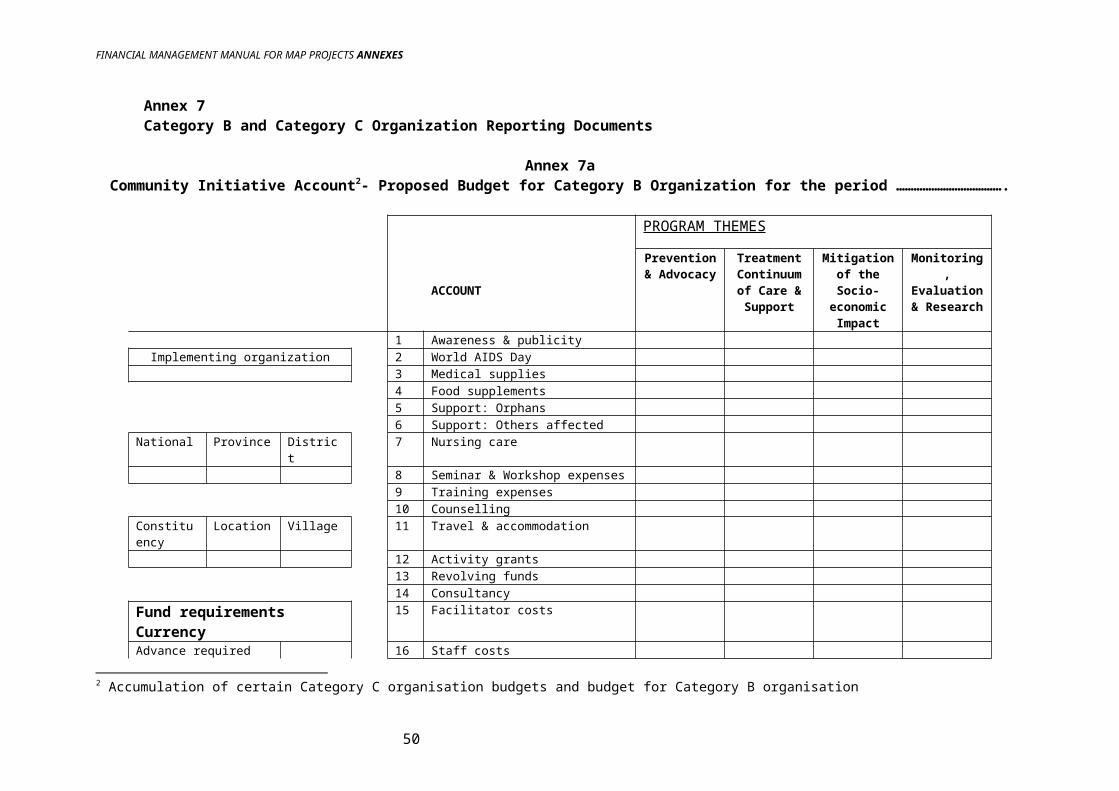

Annex 7Category B and Category C Organization Reporting Documents

Annex 7aCommunity Initiative Account2- Proposed Budget for Category B Organization for the period ……………………………….

PROGRAM THEMES

ACCOUNT

Prevention & Advocacy

Treatment Continuum of Care & Sup-

port

Mitigation of the Socio-eco-nomic Impact

Monitoring, Evaluation &

Research

1 Awareness & publicityImplementing organization 2 World AIDS Day

3 Medical supplies4 Food supplements5 Support: Orphans6 Support: Others affected

National Province District 7 Nursing care8 Seminar & Workshop expenses9 Training expenses10 Counselling

Constituency Location Village 11 Travel & accommodation12 Activity grants13 Revolving funds14 Consultancy

Fund requirements Currency

15 Facilitator costs

Advance required 16 Staff costsAnticipated other needs 17 Furniture, fittings & equipment- end 1st Quarter 18 Rent & rates- end 2nd Quarter 19 Communications costs- end 3rd Quarter 20 Motor vehicle running- end 4th Quarter 21 Printing & stationery

22 Courier & postageBanking details for deposit of funds

23 Repairs & maintenance

24 Office expenses

2 Accumulation of certain Category C organisation budgets and budget for Category B organisation

33

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

25 Power/water/security1st signature …………… ……… 26 Bank charges2nd signature …………… ……… Total

34

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

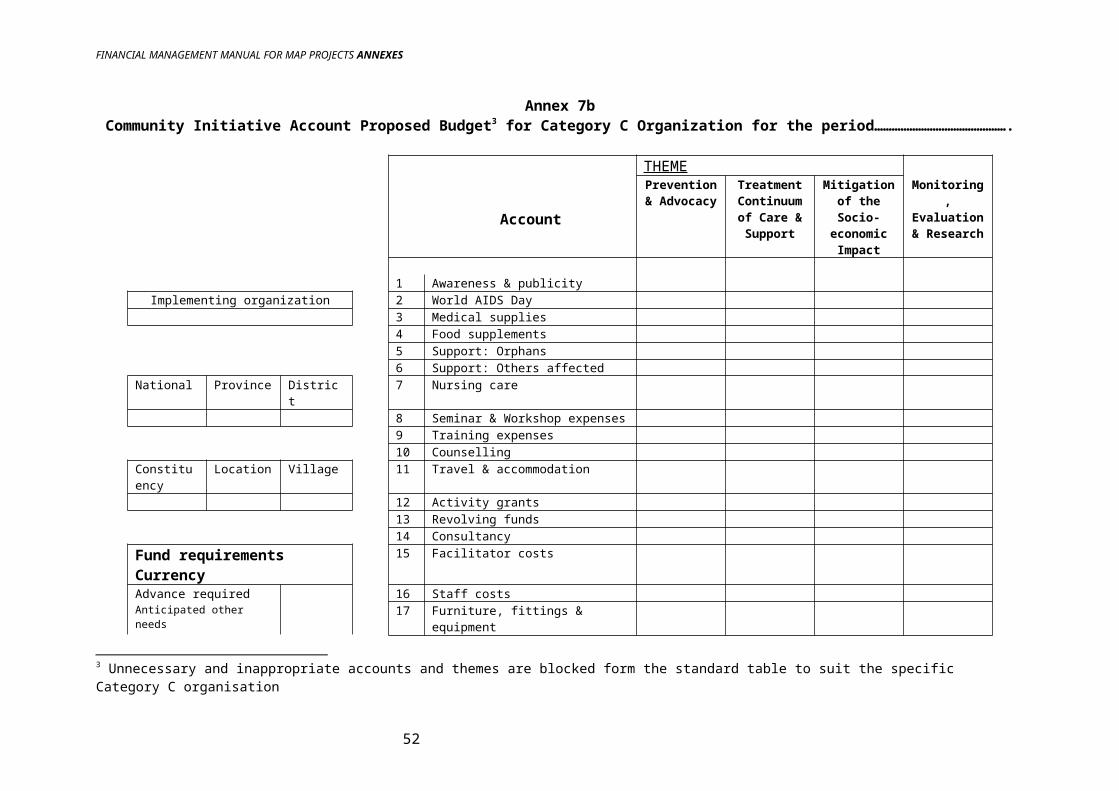

Annex 7bCommunity Initiative Account Proposed Budget3 for Category C Organization for the period……………………………………….

THEME

Account

Prevention & Advocacy

Treatment Continuum of Care & Sup-

port

Mitigation of the Socio-eco-nomic Impact

Monitoring, Evaluation &

Research

1 Awareness & publicityImplementing organization 2 World AIDS Day

3 Medical supplies4 Food supplements5 Support: Orphans6 Support: Others affected

National Province District 7 Nursing care8 Seminar & Workshop expenses9 Training expenses10 Counselling

Constituency Location Village 11 Travel & accommodation12 Activity grants13 Revolving funds14 Consultancy

Fund requirements Currency

15 Facilitator costs

Advance required 16 Staff costsAnticipated other needs 17 Furniture, fittings & equipment- end 1st Quarter 18 Rent & rates- end 2nd Quarter 19 Communications costs- end 3rd Quarter 20 Motor vehicle running- end 4th Quarter 21 Printing & stationery

22 Courier & postageBanking details for deposit of funds or

23 Repairs & maintenance

other arrangements 24 Office expenses25 Power/water/security

1st signature …………… ……… 26 Bank charges2nd signature …………… ……… Total

3 Unnecessary and inappropriate accounts and themes are blocked form the standard table to suit the specific Category C organisation

35

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

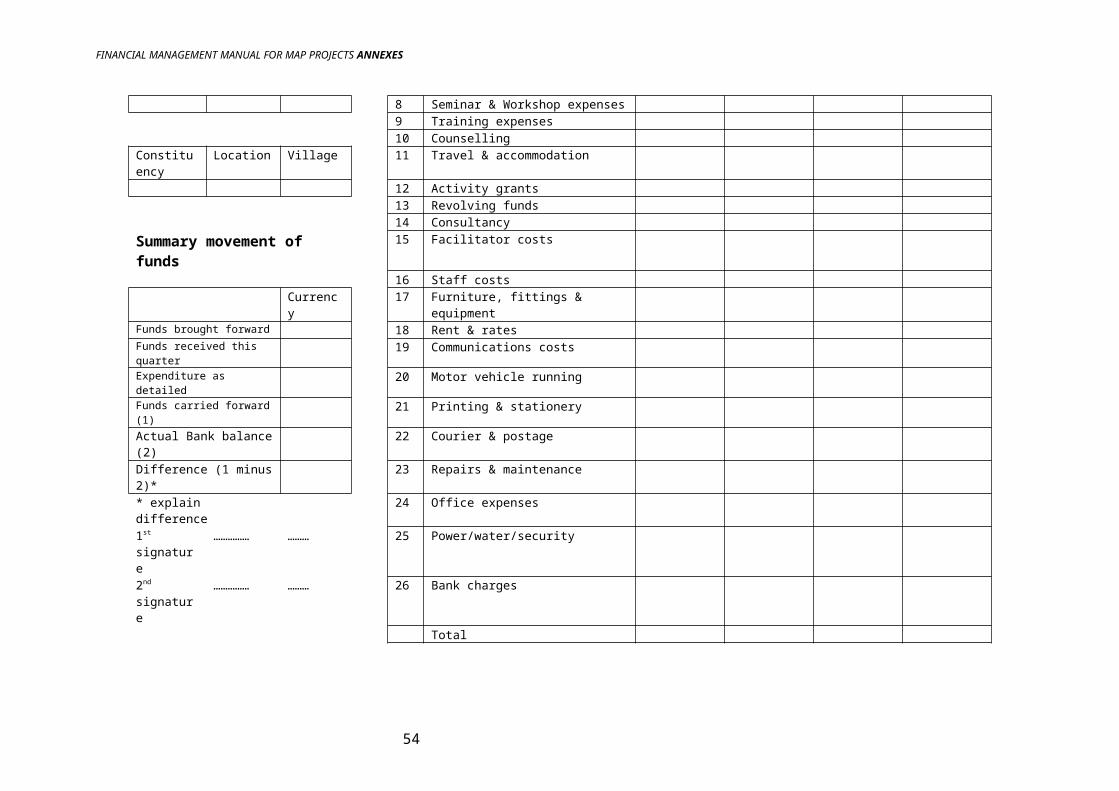

Annex 7cCommunity Initiative Account Statement of Expenditure for Category B Organization for Fund Replenishment

THEME

ACCOUNT

Prevention & Advocacy

Treatment Continuum of Care & Sup-

port

Mitigation of the Socio-eco-nomic Impact

Monitoring, Evaluation &

Research

1 Awareness & publicityImplementing organization 2 World AIDS Day

3 Medical supplies4 Food supplements5 Support: Orphans6 Support: Others affected

National Province District 7 Nursing care8 Seminar & Workshop expenses9 Training expenses10 Counselling

Constituency Location Village 11 Travel & accommodation12 Activity grants13 Revolving funds14 Consultancy

Summary movement of funds 15 Facilitator costs16 Staff costs

Currency 17 Furniture, fittings & equipmentFunds brought forward 18 Rent & ratesFunds received this quarter 19 Communications costsExpenditure as detailed 20 Motor vehicle runningFunds carried forward (1) 21 Printing & stationeryActual Bank balance (2) 22 Courier & postageDifference (1 minus 2)* 23 Repairs & maintenance* explain difference 24 Office expenses1st signature …………… ……… 25 Power/water/security2nd signature …………… ……… 26 Bank charges

Total

Annex 7d

36

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Community Initiative Account Statement of Expenditure for Category C Organization for Fund Replenishment

Prevention & Advocacy

Treatment Continuum of Care & Sup-

port

Mitigation of the Socio-eco-nomic Impact

Monitoring, Evaluation &

Research

1 Awareness & publicityImplementing organization 2 World AIDS Day

3 Medical supplies4 Food supplements5 Support: Orphans6 Support: Others affected

National Province District 7 Nursing care8 Seminar & Workshop expenses9 Training expenses10 Counselling

Constituency Location Village 11 Travel & accommodation12 Activity grants13 Revolving funds14 Consultancy

Summary movement of funds 15 Facilitator costs16 Staff costs

Currency 17 Furniture, fittings & equipmentFunds brought forward 18 Rent & ratesFunds received this quarter 19 Communications costsExpenditure as detailed 20 Motor vehicle runningFunds carried forward (1) 21 Printing & stationeryActual Bank balance (2) 22 Courier & postageDifference (1 minus 2)* 23 Repairs & maintenance* explain difference 24 Office expenses

25 Power/water/security1st signature …………… ……… 26 Bank charges2nd signature …………… ……… Total

37

FINANCIAL MANAGEMENT MANUAL FOR MAP PROJECTS ANNEXES

Annex 7eCommunity Initiative Account Sub-project Financial Completion Report

THEME

ACCOUNTPrevention & Ad-

vocacyTreatment Con-

tinuum of Care & Support

Mitigation of the So-cio-economic Impact

Monitoring, Evaluation & Research

Budget Actual Budget Actual Budget Actual

1 Awareness & publicityImplementing organization 2 World AIDS Day

3 Medical supplies4 Food supplements5 Support: Orphans6 Support: Others affected

National Province District 7 Nursing care8 Seminar expenses9 Training expenses10 Counselling

Constituency Location Village 11 Travel & accommodation12 Activity grants13 Revolving funds14 Consultancy

Funding summary Currency

15 Facilitator costs

Advance provided 16 Staff costsOther funds received from NAS 17 Furniture, & equipmentTotal funds provided 18 Rent & rates

19 Communications costsTotal sub-project cost 20 Motor vehicle runningBalance returned/owing 21 Printing & stationery

22 Courier & postage23 Repairs & maintenance24 Office expenses25 Power/water/security

1st signature …………… ……… 26 Bank charges2nd signature …………… ……… Total

38

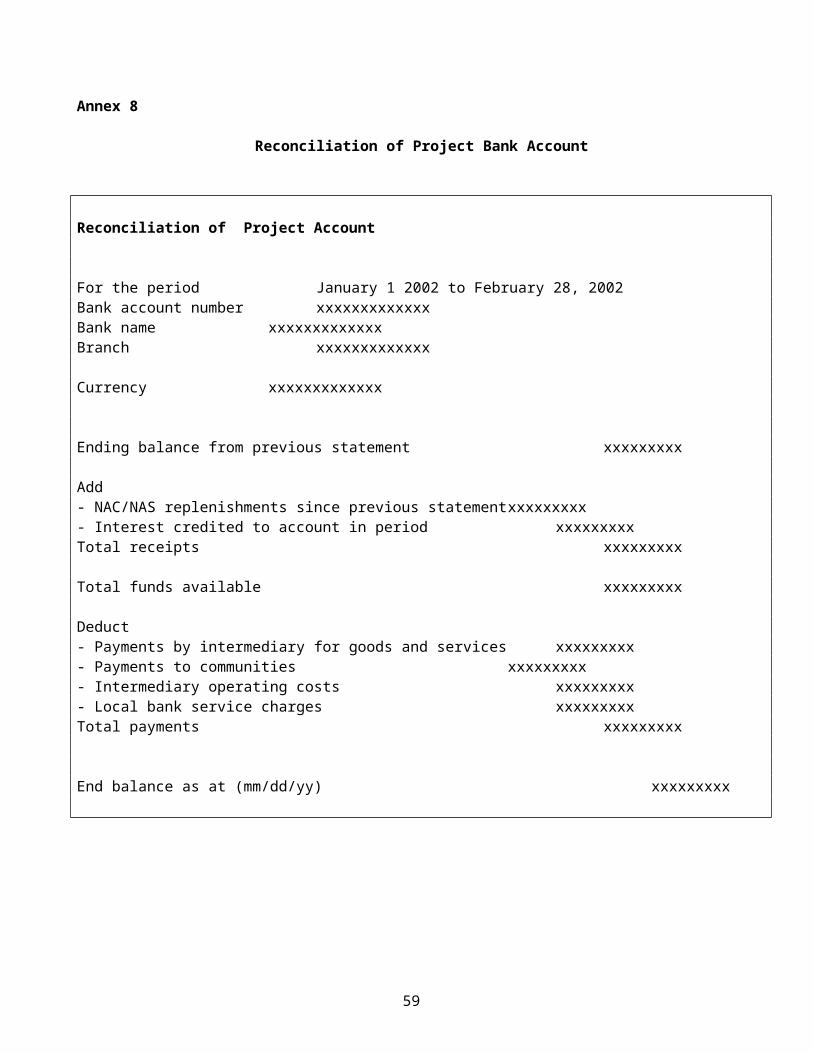

Annex 8

Reconciliation of Project Bank Account

Reconciliation of Project Account

For the period January 1 2002 to February 28, 2002Bank account number xxxxxxxxxxxxxBank name xxxxxxxxxxxxxBranch xxxxxxxxxxxxx

Currency xxxxxxxxxxxxx

Ending balance from previous statement xxxxxxxxx

Add- NAC/NAS replenishments since previous statement xxxxxxxxx- Interest credited to account in period xxxxxxxxxTotal receipts xxxxxxxxx

Total funds available xxxxxxxxx

Deduct- Payments by intermediary for goods and services xxxxxxxxx- Payments to communities xxxxxxxxx- Intermediary operating costs xxxxxxxxx- Local bank service charges xxxxxxxxxTotal payments xxxxxxxxx

End balance as at (mm/dd/yy) xxxxxxxxx

39

Annex 9