Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

21

9-405-050 REV: JULY 22, 2010 ________________________________________________________________________________________________________________ Professor Bill George and Research Associate Andrew N. McLean prepared this case. HBS cases are developed solely as the basis for class discussion. Cases are not intended to serve as endorsements, sources of primary data, or illustrations of effective or ineffective management. Copyright © 2005, 2010 President and Fellows of Harvard College. To order copies or request permission to reproduce materials, call 1-800-545- 7685, write Harvard Business School Publishing, Boston, MA 02163, or go to http://www.hbsp.harvard.edu. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by any means—electronic, mechanical, photocopying, recording, or otherwise—without the permission of Harvard Business School. BILL GEORGE ANDREW N. McLEAN Anne Mulcahy: Leading Xerox through the Perfect Storm (A) The normally confident Anne Mulcahy, chief operating officer of Xerox Corporation, was worried as she prepared to meet with her top management team on Monday, October 23, 2000. She was preparing to announce Xerox’s first annual loss in five years at the quarterly earnings announcement the following day. On a telephonic briefing on October 3, 2000, Mulcahy had forewarned security analysts and investors of the losses, stating candidly that “Xerox’s business model is unsustainable.” Her remarks had set off a firestorm, causing Xerox stock to plunge 26% that day alone. Ten days later Reuters reported the rumors circulating in Europe that Xerox was preparing to declare bankruptcy. Shortly thereafter, Moody’s and Standard and Poor’s downgraded the company’s debt ratings, further roiling the financial markets and shaking Xerox’s customers and its employees. Xerox was not only losing money, but facing a major liquidity crisis that threatened its survival. As a result of stiffened competition and a major sales organization realignment, which followed an administrative reorganization, Xerox sales had plunged into a sharp decline. The crisis was compounded by rapidly rising interest expenses and the collapse in the company’s Latin American business amid a series of currency devaluations. As one executive put it, Xerox was facing “the perfect storm.” With $18 billion in debt, a market capitalization that had dropped to $5 billion, and a string of earnings disappointments, Xerox was in deep trouble. (See Exhibit 1 for company financials.) As the storm was building, Xerox stock had tanked, plunging from $65 per share in 1999 to $27 when Mulcahy became COO in May 2000, and all the way to $6.88 on October 19. As the stock price fell, outside advisors placed increasing pressure on Mulcahy to take the company into bankruptcy and relieve the enormous debt burden and the associated interest expense. As Mulcahy met with her key executives and outside advisors that afternoon, she was deeply concerned about whether the company she loved so much could stay afloat long enough to avoid bankruptcy and give her time to implement plans to restore the company to its former greatness. Company History Xerox was built on the foundation of one of the most successful product launches ever. After a decade of development, Xerox had introduced the model 914 copier in 1959, leasing the refrigerator-

Transcript of Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

9-405-050R E V : J U L Y 2 2 , 2 0 1 0

________________________________________________________________________________________________________________ Professor Bill George and Research Associate Andrew N. McLean prepared this case. HBS cases are developed solely as the basis for class discussion. Cases are not intended to serve as endorsements, sources of primary data, or illustrations of effective or ineffective management. Copyright © 2005, 2010 President and Fellows of Harvard College. To order copies or request permission to reproduce materials, call 1-800-545-7685, write Harvard Business School Publishing, Boston, MA 02163, or go to http://www.hbsp.harvard.edu. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by any means—electronic, mechanical, photocopying, recording, or otherwise—without the permission of Harvard Business School.

B I L L G E O R G E

A N D R E W N . M c L E A N

Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

The normally confident Anne Mulcahy, chief operating officer of Xerox Corporation, was worried as she prepared to meet with her top management team on Monday, October 23, 2000. She was preparing to announce Xerox’s first annual loss in five years at the quarterly earnings announcement the following day. On a telephonic briefing on October 3, 2000, Mulcahy had forewarned security analysts and investors of the losses, stating candidly that “Xerox’s business model is unsustainable.”

Her remarks had set off a firestorm, causing Xerox stock to plunge 26% that day alone. Ten days later Reuters reported the rumors circulating in Europe that Xerox was preparing to declare bankruptcy. Shortly thereafter, Moody’s and Standard and Poor’s downgraded the company’s debt ratings, further roiling the financial markets and shaking Xerox’s customers and its employees.

Xerox was not only losing money, but facing a major liquidity crisis that threatened its survival. As a result of stiffened competition and a major sales organization realignment, which followed an administrative reorganization, Xerox sales had plunged into a sharp decline. The crisis was compounded by rapidly rising interest expenses and the collapse in the company’s Latin American business amid a series of currency devaluations. As one executive put it, Xerox was facing “the perfect storm.”

With $18 billion in debt, a market capitalization that had dropped to $5 billion, and a string of earnings disappointments, Xerox was in deep trouble. (See Exhibit 1 for company financials.) As the storm was building, Xerox stock had tanked, plunging from $65 per share in 1999 to $27 when Mulcahy became COO in May 2000, and all the way to $6.88 on October 19. As the stock price fell, outside advisors placed increasing pressure on Mulcahy to take the company into bankruptcy and relieve the enormous debt burden and the associated interest expense.

As Mulcahy met with her key executives and outside advisors that afternoon, she was deeply concerned about whether the company she loved so much could stay afloat long enough to avoid bankruptcy and give her time to implement plans to restore the company to its former greatness.

Company History

Xerox was built on the foundation of one of the most successful product launches ever. After a decade of development, Xerox had introduced the model 914 copier in 1959, leasing the refrigerator-

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

2

sized office machine to customers in low-cost long-term agreements, under which Xerox collected a fixed price per page printed. Demand exploded for the new xerograph process, which replaced messy carbons and various wet process duplication methods. Initial sales of $32 million in 1959 grew to $1.1 billion in 1968, and employment increased from 900 to 24,000. By 1970 Xerox enjoyed a 95% share of the plain-paper copier market, with gross margins on key products ranging from 70% to 80%. Xerox joined trademarks like Yo-yo and Hoover as a household name.

Xerox was a model corporate citizen, especially in its hometown of Rochester, NY. Chief executive Joseph C. Wilson set the tone for Xerox’s focus on its customers, values-based leadership and roots in the community. Over time several generations of families came to work for the company. Xerox became a trendsetter in encouraging diversity in its workforce.

Sterling civic values and meticulous corporate controls were matched by heavy investment in R&D. Xerox was a research scientist’s dream job. One of its crown jewels was the renowned Palo Alto Research Center (PARC), established in 1970 when Xerox entered the computer industry. PARC originated many technologies that launched the information revolution: the graphic user interface, computer mouse, Ethernet protocol, first laser printer, bit mapping, advances in information theory, object oriented computer languages, and the idea of “windowing” computer applications.

While PARC’s research was important for company prestige, it had “little connection to the people who dealt with customers on a day-to-day basis,” explained a Xerox executive. “Our operating culture was focused on the next product to be introduced.” Product development was based near Rochester, where engineers worked on ink and paper movement technologies that applied directly to hard documents. Xerox carefully scripted the development of new technologies in a slow but exacting multi-stage process, extending from initial research to model introduction.

Reinvention

Xerox’s overwhelming success bred anti-monopoly pressures. Confronted by several lawsuits, Xerox negotiated a 1975 settlement with the Federal Trade Commission whereby it forfeited its formidable store of patent protections and agreed to license its technology to competitors. The next decade brought dizzying competition as new competitors Canon, Minolta, Ricoh and Sharp aggressively entered the U.S. market. Xerox’s share of U.S. copier installations fell from 80% to an estimated 13% by 1982.

Unprepared for price competition, Xerox was unable to adapt to smaller margins and appeared to be headed for insolvency in the early 1980s. In response, new CEO David T. Kearns introduced several companywide initiatives in the areas of benchmarking, employee involvement, and quality to help Xerox build a competitive position. Kearns rallied employees under the moniker of Team Xerox and Leadership Through Quality, and they responded enthusiastically. Between 1984 and 1993 Xerox improved its share of low-end copiers from 8% to 18%, as mid- and high-end share rose from 26% to 35%.1 As its copier businesses rebounded, Xerox diversified, launching a computer business competing directly with IBM. It also acquired insurance and finance arms.

Despite improvements in market share, profit growth stalled in the early 1990s. Amid the networked office and digital computer printing revolution, Xerox’s entire product line consisted of stand-alone, analog machines. In manufacturing, employment levels were fixed by union contracts and production was vertically integrated down to plastics molding and screw turning, making it difficult for Xerox to compete on cost. Named Kearns’s successor in 1992, CEO Paul Allaire was determined to spread a sense of urgency throughout the company. Allaire created three geographically defined sales organizations selling products from nine product divisions organized

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

3

around market segments. Each division assumed “end-to-end” responsibility for a set of products and service and had its own manufacturing, income statement and balance sheet. Allaire eliminated 10,000 jobs across the company, modernized Xerox core technologies, and divested the insurance business.

Over the next five years, the nine divisions were reduced to four, and companywide management of manufacturing was reinstated. But while the organization was fine-tuned, Xerox urgently needed a new strategy. Beginning in the 1990s, Xerox sales had accelerated as installed leases began to be replaced with purchased machines. “This created incredible sales revenue,” explained a senior executive, “as we spent five years selling off our lease base. By 1997 we’d run out of steam on the conversions. A lot of the skills required to build new revenues – market development, attracting customers, and training salespeople – weren’t in the company.”

New Strategy ... and a New Leader

In 1997, Allaire announced that Xerox’s digital systems revolution had achieved critical mass. He again reorganized the company, this time into four business divisions. Production printing and retail channels businesses were new business forays, each targeted at a new market with new competitors, and all used new technologies in networking, color ink and digital processing. Xerox took direct aim at H-P with its desktop printer business.

On the threshold of a new digital era, investor expectations for Xerox ran high. To spark profit growth, the Xerox board turned to an outsider as Allaire’s successor. Richard Thoman, then CFO at IBM, was appointed president of Xerox in 1997 to undertake a sales and process reorganization and shake up the slow, cumbersome bureaucracy critics called ‘Burox.’ “Everyone knew we needed the new strategy and a greater sense of urgency in our culture,” explained a senior Xerox executive, “but no one had the intestinal fortitude to do it.” A protégé of Lou Gerstner, with experience in IBM’s storied turnaround, Thoman was greeted with optimism by investors. His track record in IBM’s transformation from hardware to services reflected Xerox’s aspirations.

Thoman’s election as president put him in line to become CEO when Allaire retired in 1999. “We were going to be something fundamentally different from our history – a systems and IT company,” explained Xerox veteran Ursula Burns. Working with a team of senior Xerox executives and key senior hires from IBM and elsewhere, Thoman oversaw the implementation of further reorganizations. Four geographically oriented customer administration centers which handled billing and collections were consolidated into three customer business centers organized by business segment. Customer-facing order entry personnel from more than 30 geographic customer business units were moved to the three customer business centers to capture advantages of scale. Later, in 2000, geography-based sales team members were reassigned to sell Xerox’s solutions tailor-fitted for industry groups, and another layer of senior management was added.

Thoman attempted to build a service business through a series of acquisitions and continued to buy out partners’ stakes in overseas joint ventures, looking to buy Fuji’s share of Fuji Xerox. Xerox expected to pay for major business investments in color and ink technology, desktop machines, production printing, and services with cost savings from process streamlining in sales, fulfillment, and billing. The stock market responded enthusiastically. Investors bid Xerox stock up from $30 per share in 1997 to over $60 when Thoman was officially elected CEO in April, 1999.

Inside Xerox, the changes were not going as well as hoped:

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

4

• The sales reorganization so disrupted customer relationships that revenue and profits suffered. Sales team members lost client relationships they had cultivated over the years. Many of them took advantage of the strong job market and left the company.

• Xerox customers not only lost their sales contact, but also began experiencing increased billing issues due, in part, to the customer administration changes and more complicated pricing plans. With the two strong customer ties to Xerox broken, competitors exploited the opening for new business and stole market share from Xerox.

• As the Xerox sales team scrambled to find new business, it cut prices sharply and wound up closing fewer and fewer profitable contracts.

The extent of the crisis was not apparent to management until the second half of 1999, when declining results caused Xerox to miss its earnings targets in both the third and fourth quarters. Xerox stock declined sharply from its high of $60 to $20 per share in early 2000, before a brief rally brought it back to $27.

Just as Xerox was confronting these problems in its core business, the company encountered external profit challenges. Among them, Xerox’s domination in production printing ended with the entry of foreign-rival Heidelberg, and competition from Canon and Ricoh began to heat up as well. Second, the global financial crisis that began in Asia in 1998 spread to Latin America in the second half of 1998, where currency devaluation in Brazil put a hole in a particularly profitable operation for Xerox. Third, the market began shifting toward products with lower margins.

After confirming through September of 1999 in-line earnings expectations for the third quarter of 1999, Xerox stunned investors by warning of a steep reduction in expected earnings in early October. (See Exhibit 2 for quarterly results.) With the share price in freefall and revenue and profits shrinking, morale was in disarray, and massive defections were plaguing the sales organization. At the same time, internal auditors found misclassified revenues and spiraling doubtful accounts in Xerox Mexico, triggering sweeping dismissals and a notice to the Securities and Exchange Commission. The SEC began inquiries across the company, suspicious that practices uncovered in Mexico were more widespread.

The sudden change in Xerox’s prospects was a shock. The management team was shaken by the sudden downturn, and began to lose confidence in Xerox’s direction. As a result, several senior executives made plans to leave. As news of this disarray filtered back to Allaire, he took steps to stabilize senior management, trying to prevent the damaging defection of old Xerox hands.

Changing Leadership…Again

Allaire decided to replace Thoman, canvassing the Board regarding another leadership change. Having just elected Thoman CEO, the board did not have an obvious successor. Allaire suggested Anne Mulcahy, president of the General Markets Organization division (GMO). As Mulcahy was preparing for a business trip to Japan on May 11, 2000, Allaire dropped by her office. “He came in and he said, ‘Hey, sit down,’” Mulcahy recalled:

Paul said, ‘I don’t think you ought to go to Japan today.’ He asked me to be COO and his successor and indicated the board had approved it. I asked him for a day. I knew I would do it, but I wanted to go home and chat with my family to make sure they understood the consequences and I had their support.

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

5

That evening Mulcahy talked over the opportunity with her family. “Having worked for 35 years for Xerox, my husband has the same passion for the company as I do,” she said. “He said, ‘You go do what you have to do.’ Our two sons were somewhat enlightened in the topic of women leaders, so they were excited. Their support solidified my resolve and gave me energy for the task. I don’t think I would have been able to do this job without that support.”

The next day, Allaire secured Thoman’s resignation and resumed the position of chief executive as the board elected Mulcahy president and chief operating officer. “I was certainly not focused on having this happen,” Mulcahy said. “It was a little like going to war, in terms of knowing that this was the right thing for the company and there was a lot at stake. This was a job that would dramatically change my life, requiring every ounce of energy that I had. I never expected to be CEO, nor was I groomed to be CEO. It was a total surprise to everyone, including me.”2

My biggest fear was that perhaps I was sitting on the deck of the Titanic and I’d get to drive it to the bottom of the ocean—not exactly a moment to be proud of. Nothing spooked me so much as waking up in the middle of the night and thinking about 96,000 employees and retirees and what would happen if this thing went south. Entire families work for Xerox.3

The Making of Anne Mulcahy

It had been clear to senior management that a change was in the air, but Mulcahy’s appointment came as a surprise. She had been running a business far removed from the challenges of the reorganization. “I wasn’t surprised that there was a change,” said Mulcahy. “I was surprised they came after me because I never expressed an aspiration to be there. I didn’t know the board at all, so it wasn’t exactly a vote of confidence. I was the only option left to them.”

Joining Xerox

While long recognized as high potential within Xerox, Mulcahy had followed a circuitous path to the ranks of senior management. Growing up with four brothers in suburban Long Island, Mulcahy attended Catholic schools and graduated in 1974 from Marymount College with a joint major in English and Journalism. (See Exhibit 3 for her account of her early family life.)

After working initially at Chase Manhattan, Mulcahy said, “I came to Xerox because I needed a job. Not with aspirations, that’s for sure. I started out in sales and literally hounded the streets for the first ten years of my career,” she recalled. “There were only a handful of women sales reps at that time. I remember taking these little puddle-jumpers up to Presque Isle, Maine, to call on the paper mills. This was baptism by fire.” Despite Mulcahy’s lack of sales experience, Xerox had recognized her competitive instinct. “She would go and dig in the bowels of a territory to find things,” recalled Tom Horn, her Boston sales manager.4

By the early 1980s, Mulcahy was promoted to management, charged with organizing a sales team that included older and more experienced employees. She had married Joe Mulcahy, who was also a Xerox sales executive, and started a family. “A lot of what drove my career was actually work and family balance,” she explained. “We both wanted to play out our careers, yet still raise our kids in one place. We’d figure this out without one person’s career taking priority over the other. This was difficult because in a company like Xerox, relocation was part of the game.”

Joe ran Xerox’s major account organization until 1988, which required extensive global travel, while Anne stayed in positions not requiring travel. Later their roles were reversed. “We made a

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

6

deal that one of us would always be home with the kids,” said Mulcahy. “It’s hard on the person traveling, but at least you don’t have to worry about what’s happening at home.”

From their home base outside New York City, Mulcahy commuted to Boston, Hartford, Rochester, and corporate headquarters in Stamford, Connecticut. Said Mulcahy, “Xerox tried hard to make this work for me. They were respectful of my decision to keep my roots around my family.”

Mulcahy’s sales management experience developed her skills in building teams. “The key to managing a sales team is the ability to set goals and motivate your team,” she said. “People have to feel good about getting out of bed every day. It’s a tough job. You can learn a lot by thinking about the business from the customer’s perspective every day.”

Moving to Corporate

As greater responsibilities came Mulcahy’s way, she was eventually promoted to vice president for human resources in 1992 during the 1990s restructuring. Mulcahy found she had a passion and flair for the job, and it enabled her to refine her communications skills. “When there are tough messages to deliver,” she said, “it’s important to communicate the good and the bad. Respect people by delivering the truth. Help them work through their choices. This is where I learned how to make tough choices, but still value people.”

When her former boss, Barry Rand, became vice president for worldwide operations in 1996, he took Mulcahy with him as his deputy. “I made a point of traveling everywhere and getting to know the operations and the people who led them,” she said. “When you work in North America, you think it defines the company. I learned just how rich and talented our international operations were.”

In 1997 Mulcahy became chief staff officer, reporting directly to CEO Allaire. “I’d known Paul throughout my career,” said Mulcahy, “He had been helpful in making sure opportunities were there for me.” Mulcahy had impressed Allaire with her range of experience and decisiveness. “I liked the way she handled things in a forthright manner, stepping up to the issue and deciding what to do and saying, ‘Let’s just go do it,’” commented Allaire.5

While the chief staff officer job was a development experience, with responsibility for functions ranging from human resources to strategy, Mulcahy was not deeply interested in the role. Consequently, she leapt at the opportunity to run GMO, Xerox’s new venture in web and retail sales, as a key member of Thoman’s executive team.

On to General Management

In leading GMO, Mulcahy had her first opportunity to run her own business. She launched a small office and home office (SOHO) venture in desktop printing that competed with industry leader Hewlett-Packard. The challenge was exhilarating. “I loved starting a new business from scratch, building the organization, and choosing people to staff it.”

Mulcahy and her team spent the next two years developing channels and products in areas in which Xerox had traditionally been weak. In late 1999, Xerox acquired Tektronix’s color imaging division for $925 million. Learning from Xerox’s history on prior acquisitions, Mulcahy integrated Xerox’s printer business into Tektronix, headquartered the unified business in Tektronix’s Oregon location and commuted to Oregon several times a month. In this general management role, Mulcahy reported directly to Thoman, but was removed from the core business. “Historically, Xerox is an integrated, single brand company,” Mulcahy explained: “In running GMO, with a different

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

7

headquarters, sales model and operational challenges, I was isolated and didn’t have a clear view of the main business.”

Leading Xerox

When Mulcahy became COO in May, 2000, Xerox stock was in freefall, having dropped from $63 per share to $27 in the previous year (see Exhibit 4). She became part of the new office of the chief executive, working with Allaire, CFO Romeril, and outgoing vice chairman Bill Buehler. Mulcahy took charge of internal business, including operations, solutions and worldwide business services (see Exhibit 5 for management directives in the announcement), and Allaire made it clear inside and outside the company that the CEO’s job was hers to lose.

Sizing up the Challenge

Mulcahy’s first goal was to assemble her team. She met personally with 100 top executives to see if they would stay with the company despite the challenges ahead. “At Anne’s first meeting as COO,” recalled former head of marketing Diane McGarry, “it was obvious a couple of people weren’t happy and weren’t staying. Hours later both of those folks were replaced.” “I knew there would be people who certainly wouldn’t be supportive of me,” said Mulcahy:

So I confronted a couple of them and said, “Hey, no games. Let’s just talk. You can’t be thrilled. If you choose to stay, either we’re totally in synch or when you go it won’t be pleasant, because I have no appetite for managing right now. This has got to be about the company.” Two people who ran big operating companies came forward and said they would prefer to leave.

Those who stayed did so for various reasons: some were personally invested in the company, others relished the challenge, and other stayed because Mulcahy appealed to their character. Ursula Burns, president of worldwide business services, said she was loyal to the company that had given her so much. “I have been to almost every country in the world,” explained Burns. “I have a wonderful life and great friends, more than I ever imagined. It all came from a partnership between me and this company. What do you say when times are tough? ‘Thank you very much, I’ll see you later?’ That’s not what my mother taught me.”6

After the initial conversations with Mulcahy, the team came together quickly and members were heartened by the number of their colleagues who stayed on. “We had a dinner in the conference room off the cafeteria,” said Burns, “and we all looked around, pleased at how many stayed, and said okay, fine, we’re in this together. Let’s go. What do we have to do to survive?”

Mulcahy then embarked on extensive fact-finding tours in the business, visiting employee operations and major customers. “When I came in,” Mulcahy later explained, “Paul had a very clear agenda. He was coming back, but not for long. He wanted to position the company so that we had a chance going forward. He kept the title of CEO but gave me the experience immediately of having accountability.”

Allaire did not formally separate his responsibilities from Mulcahy’s, and asked her to participate in every ongoing decision. As Mulcahy noted, “I couldn’t sit back and say, ‘Oh, well, I don’t have to deal with that.’ In fact, the only thing that I didn’t do, which was intentional, was deal with the SEC for that first year as the investigation sparked by irregularities in Mexico ground on. That was because I hadn’t been a part of any of the issues.”

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

8

Mulcahy’s goal was to fully understand the challenges facing Xerox. “When I took over as COO, I was amazed at just how unaware everyone was of the seriousness of the issues,” she explained:

No one understood, and I mean no one. Maybe you see it and you don’t acknowledge how serious it is. It was shocking for the Xerox executive team to find out how dismal the outlook was. Speaking for myself, I did a billion dollar acquisition one year before the company almost went bankrupt. I had no idea of our financial condition. Fortunately, it was a success.

Leading the Team

Mulcahy’s leadership contrasted sharply with her predecessors. She made people publicly accountable for their results and set realistic expectations, despite the tremendous pressures the company was under. “You can’t wish your way to good performance,” said Mulcahy. “If you set the bar someplace that buys you ninety days of external esteem, then you will get killed. Boy, is it ugly.”

She also encouraged senior managers to engage each other directly. “We talk about everything,” said Burns. “Anne is really clear: ‘Make sure you get it.’” Mulcahy did not take the lead in every discussion, playing what Burns described as a more orchestrating role. “Anne sits in the room and she’ll listen and watch,” Burns explained. “When she jumps in, it’s because we need to be pulled together or because something unsaid needs to be said. She’s really good at reading people, and she’s really good at explaining how important it is that we work together.”

Mulcahy’s knowledge about the full range of Xerox’s business was incomplete, and she lacked a fully engaged CFO. So she asked more junior staff members to tutor her on finance. “Folks in the controller’s department would spend hours with me just making sure I was prepared to answer all the ugly, tough questions from the bankers,” said Mulcahy. “They did the same in product development, engineering and research.”

Reflecting on the pressures of her new job, Mulcahy explained:

Month after month there was not a single piece of good news. We asked ourselves, could it get any worse? Yes. And it did. You have the combination of operational weakness, revenues declining like a rock, the SEC investigation, and the liquidity problem. Some companies lose money all the time, but they have $6 or $8 billion in the coffers. When you’re losing money, and you have no cash, it’s a much uglier story.

This was her first taste of the loneliness of leadership at the top. By nature Mulcahy drew inspiration and energy from interacting with fellow Xerox employees. “I’m never happier than when I’m milling around with a group of Xerox people, in a town hall meeting, or a Q&A,” Mulcahy said:

I don’t like giving speeches, but I love dialogue. That’s when I’m happiest. You have to like it, because people can see the difference. Visiting with Xerox people gives me the motivation to keep going. They tell you these incredible stories. When you see the pride in their eyes about what they’ve accomplished, you’ve just got to love the place. There is such a connection in sharing a passion about making a contribution. It’s not a skill, it’s not training. It’s just an affinity for people. That’s where I’d rather spend my time.

While Mulcahy had traditionally drawn support from interacting with her peers, in her new role she knew how important it was to provide her team with confidence that the company could survive, in spite of any personal doubts she may have had.

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

9

The hardest thing for me, as a touchy-feely people person, was that my new role required some distance that I wasn’t prepared for. When you’re worried and when you’re really wondering whether you’re going to make it, at times like that people need a sense of direction. They want leadership and clarity, and the confidence that we can succeed.

Mulcahy was not immune from uncertainty and stress. “One day I had just flown back from Japan,” Mulcahy recalled:

I came back to the office and found it had been a dismal day. At around 8:30pm on my way home, I pulled over to the side of the Merritt Parkway, and said to myself, “I don’t know where to go. I don’t want to go home. There’s just no place to go.” For some reason, I picked up my voicemail, and chief strategist Jim Firestone had left a message: “This may seem like it’s the worst day, hopefully it is, but we believe in you. This company will have a great future. Let tomorrow be a good day.” That was all I needed to just drive home and get up again the next morning. The team gave me incredible supportive strength. We fight, we debate, but at the end of the day, they’ve been extremely loyal and supportive.

Mulcahy explained that she was motivated by her sense of obligation to the company as a whole:

I didn’t expect to be here, so I didn’t feel like I had a lot to lose personally. The loss for me would have been having this company that I love so much go under, or if it didn’t resemble its previous self. If Xerox became a Polaroid, that would have been a huge failure because of the implications for the people. I get things done by identifying with the people in the company and by trusting them. I care most about building a good team to lead the company.

Initial Results

In her first months as COO, Mulcahy spent most of her time talking with customers and employees. “Anne appealed to employees with missionary zeal, in person and through videos,” recalled vice president of finance for North America Leslie Varon. “She implored them to ‘save each dollar as if it were your own.’ She ended every appearance with a nudge: ‘Remember, by my calculations, there are just so many selling days left in the quarter.’ She rewarded those who stuck it out by refusing to abolish raises and with symbolic gestures like giving all employees their birthdays off.”7

While employees responded immediately to Mulcahy, customers were a tougher case. Many large companies excluded Xerox from bidding on their office contracts for fear that the company was headed for bankruptcy. In order to galvanize the sales force, Mulcahy issued a blanket promise that she would fly anywhere to save any customer. “I won more than I lost in those situations. It’s amazing how much customers are willing to work with you if they know you’re there for them.”

During one call, the CEO of a major customer gave Mulcahy some free advice: she would have to kill the Xerox culture – which he viewed as meticulous with quality, but slow, inefficient and complacent – in order to save the company. “I am the culture,” she shot back. “If I can’t figure out how to bring the culture with me, I’m the wrong person for the job.”8

In order to stop the hemorrhaging in the sales organization, Mulcahy stripped out matrix management, clarified accountability, and sweetened salaries and incentive programs in key geographies. Despite being short on cash, Mulcahy approved a plan to boost retention in the sales force by offering generous development and training benefits to key sales personnel.

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

10

By August, there was very little good news to report to anxious employees. In the second quarter of 2000, Xerox lost 11 points of market share in their core high-end office business. Mid-market copiers were mired in a price war with Ricoh and Canon. Production sales were harder to close because of competition from Heidelberg. The desktop business was rolling out products, but had yet to become profitable and was up against intense competition from H-P. Yet Xerox’s color offerings sales grew 59%, led by Tektronix’s Phaser line of office color printers. Communiqués focused on this glimmer of competitive advantage even as employees were exhorted to save money. Bottled water deliveries were halted, office plants were left unwatered, and employees were told endlessly to focus on profitable revenue and cost savings.

Mulcahy relied on some longstanding habits to sustain her energy. “Even during the worst of times, I can sleep, get up the next day and go at it,” said Mulcahy. “It’s probably my Catholic upbringing, but I have this thing that I go to sleep with every night. If you review the day and can’t think of a thing you would have done differently, then you just need to be at peace and get up the next day. Simple things like that work for me.”

Survival?

Business in the third quarter of 2000, Mulcahy’s first full quarter as COO, was even more difficult than the previous one. External events compounded with shrinking profits had a disastrous effect on Xerox’ liquidity. Accustomed to strong cash flow from long-term lease contracts, Xerox had turned to short term debt vehicles to shave interest expenses. This tactic backfired when the commercial paper market dried up. Xerox’s commercial paper rating was cut in the middle of 2000,9 forcing Xerox to draw down its last liquidity provision, an unsecured $7 billion revolving credit line held by a consortium of 58 banks. At any one time Xerox had only about a week’s cash on hand. Standard & Poor’s cut the company’s senior debt rating to A- in July, and again to BBB on September 19, one step above junk. Several of Xerox’s key advisors thought the company should prepare to file for bankruptcy.

In early October, 2000, Mulcahy prepared to pre-announce earnings, stating that Xerox was on its way to its first annual loss since 1995. Mulcahy called this her “baptism by fire.” “Revenues declined in double digits and margins slipped by six points in the quarter,” she said. “The company was clearly out of control and things were heading south. I decided the most important thing was to acknowledge where we were.”

In the middle of her October 3rd remarks, Mulcahy said candidly that Xerox’s business model was “unsustainable.” Expenses were too high, margins were too low, and revenue was insufficient to yield profitability. (See Exhibit 5 for her remarks). Her communications team had warned her that this was a red flag to the media and an explicit repudiation of past leaders, some of whom were still on the executive team. Believing straight talk, Mulcahy stuck to her remarks. As she later described it:

The only thing that ever made it to press was the headline: ‘Xerox COO says company has an unsustainable business model.’ That was it. It didn’t even occur to me that this would be a dangerous thing to say. I thought that it was far more credible to acknowledge that the company was badly broken, dramatic actions had to be taken, and I was prepared to do so. Instead of building confidence, I spent the next three days trying to explain what I meant to our shareholders. Obviously, they weren’t happy about it. Lesson learned.

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

11

Ten days later another bombshell exploded. On October 13, Reuters reported rumors circulating in European securities markets and on internet chat rooms that Xerox was planning to file for bankruptcy protection (see Exhibit 6). The company chose not to comment on the rumors – neither admitting nor denying them – since there was a very real possibility that Xerox would file for bankruptcy.

At an operations group meeting that week an outside financial firm presented Xerox’s equity position and debt ratings. As Diane McGrary recalled, “It was serious, critical and life-changing. That was the first time we absolutely understood we were in real jeopardy. We said, ‘Holy cow, we better band together to save this company.’ ”

Mulcahy was particularly concerned with the effect of wave after wave of bad news on the rank and file organization. “You just couldn’t get out in front of it fast enough,” she said. “The news kept breaking in the press, and they read it. Every day we were cleaning up, trying to give them the straight scoop but also to let them feel a sense of confidence that we could save the place.”

Cognizant of the damage bankruptcy would do to Xerox’s brand, its customers, employees, and shareholders, Mulcahy challenged her advisors: “‘Tell me a brand company that went into bankruptcy and emerged as a great company. Give me the names. Tell me the history.’ They came up with these bad examples. Sure some survived, but that wasn’t what we were about.”

Joe Mancini was a staffer in the controller’s office who had tutored Mulcahy in the details of finance after she became COO and watched the confrontations with outside advisors. He realized that the advisors believed that Mulcahy – like her predecessors – would not take the necessary actions to turn the business around or sell it off. Mancini even worried that the advisors might quit because they thought Mulcahy “just didn’t have the guts to make the tough decisions.”

The issue came to a head in the third week of October when external legal advisors argued that the decision not to put teams in place for bankruptcy was a disservice to the company. “I sat there and listened for ten minutes while they went on and on, and then I sort of exploded,” Mulcahy recalled:

I said, “You just don’t get it. You don’t understand what it’s like to be an employee in this company. To fight and come out and win. Bankruptcy’s never a win. You know what? I’m not going there until there’s no other decision to be made. There are a lot more cards to play.” I was angry that anybody could comprehend the passion and drive that’s required to succeed and not understand the impact of filing for bankruptcy on a company’s employees. I said, “What we have going for us is that our people believe we are in a war that we can win.”

The October 23 Meeting

On Monday, October 23, Allaire, Mulcahy, and the executive team gathered with key advisors to prepare for the earnings announcement the following day. Having worked to restore empowerment and accountability, it was time to set the course for recovery. Mulcahy knew that Xerox had to commit to a focused strategy in order to have a chance of surviving. She told her team that all they would talk about for the foreseeable future would be cash, restructuring the business model, and investing for the future. Those three pillars would screen out other interesting but distracting issues. Mulcahy knew it would have to be “the same agenda, every time we talk to shareholders, customers, or employees until we’re out of the woods.”

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

12

Mulcahy asked her team for their opinions about the announcement of significant losses and what course they should take, knowing that she had to have a clear sense of direction on the conference call.

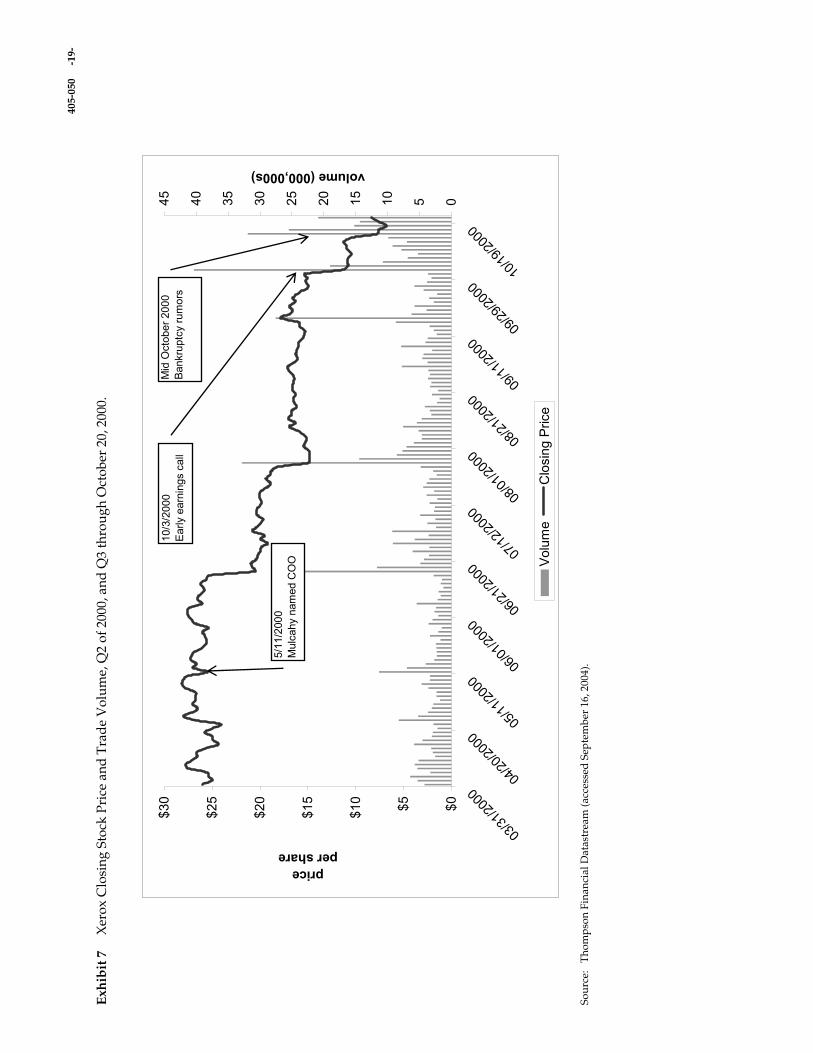

• CFO Romeril reviewed the earnings announcements – $235 million in losses – and reported the board had voted to cut Xerox’s quarterly dividend from 20 to 5 cents, saving $400 million a year. He also commented on the stock market’s reactions to Mulcahy’s October 3 comments, stock price declines (see Exhibit 7), and Moody’s October 20 announcement that they had placed Xerox debt under review for yet another downgrade. Xerox debt was trading at 60 cents on the dollar.10

• External advisors recommended that Xerox consider a Chapter 11 filing to relieve the debt burden. The team also reviewed the on-going SEC investigation that had recently spread from Mexico (where the company had previously taken a $115 million charge and was now recording an additional $55 million charge) to a thorough review of U.S. revenue recognition.

• Ursula Burns reviewed the latest draft of an operational turnaround plan, presenting the starkest picture yet of necessary changes to Xerox’s core businesses (see Exhibit 8). Burns questioned whether it was realistic to protect Xerox’s huge R&D budget and field sales force. As she said candidly, “Without deeper cuts in R&D and field sales, I don’t know if we can stay afloat long enough to implement the turnaround plan before we exhaust our cash.”

Chief strategist Jim Firestone concluded that Xerox faced “the perfect storm,” with everything moving against it at once. He presented three primary strategic options:

1. Implement asset sales of ‘live wood’ and painful cost cutting while continuing to fund R&D and field sales and service, in order to restore credibility to the Xerox brand and its market share.

2. Make deep cuts in R&D, product development, and field sales and service in order to save the company, in spite of the long-term ramifications.

3. Follow the recommendations of outside advisors to declare Chapter 11. Then initiate an aggressive turn-around plan to come out of bankruptcy without the $18 billion in debt hanging over every decision.

CEO Allaire engaged Mulcahy to chart the decision. As she listened to the inputs, her mind raced with conflicting thoughts of determination to achieve her goal of restoring Xerox to a great company pitted against the real possibility that the cash would run out before she could get it done. Maybe bankruptcy was the wisest course after all. She thought back on her twenty-five years with Xerox and all the people who were depending on her to save the company. Would the board support her through these dark days? Was she really the right person to pull it off?

Before drawing her own conclusions, she went around the table and asked each person for recommendations on which course Xerox should follow.

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

13

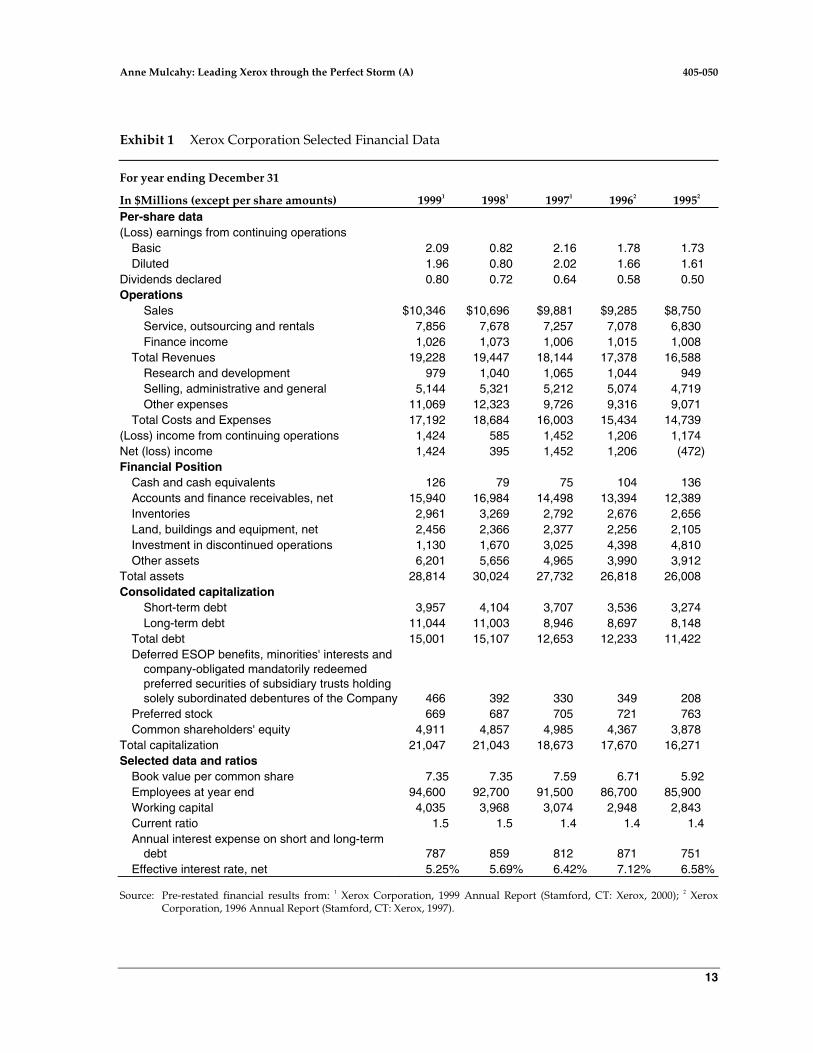

Exhibit 1 Xerox Corporation Selected Financial Data

For year ending December 31

In $Millions (except per share amounts) 19991 19981 19971 19962 19952

Per-share data (Loss) earnings from continuing operations

Basic 2.09 0.82 2.16 1.78 1.73 Diluted 1.96 0.80 2.02 1.66 1.61

Dividends declared 0.80 0.72 0.64 0.58 0.50 Operations

Sales $10,346 $10,696 $9,881 $9,285 $8,750 Service, outsourcing and rentals 7,856 7,678 7,257 7,078 6,830 Finance income 1,026 1,073 1,006 1,015 1,008

Total Revenues 19,228 19,447 18,144 17,378 16,588 Research and development 979 1,040 1,065 1,044 949 Selling, administrative and general 5,144 5,321 5,212 5,074 4,719 Other expenses 11,069 12,323 9,726 9,316 9,071

Total Costs and Expenses 17,192 18,684 16,003 15,434 14,739 (Loss) income from continuing operations 1,424 585 1,452 1,206 1,174 Net (loss) income 1,424 395 1,452 1,206 (472) Financial Position

Cash and cash equivalents 126 79 75 104 136 Accounts and finance receivables, net 15,940 16,984 14,498 13,394 12,389 Inventories 2,961 3,269 2,792 2,676 2,656 Land, buildings and equipment, net 2,456 2,366 2,377 2,256 2,105 Investment in discontinued operations 1,130 1,670 3,025 4,398 4,810 Other assets 6,201 5,656 4,965 3,990 3,912

Total assets 28,814 30,024 27,732 26,818 26,008 Consolidated capitalization

Short-term debt 3,957 4,104 3,707 3,536 3,274 Long-term debt 11,044 11,003 8,946 8,697 8,148

Total debt 15,001 15,107 12,653 12,233 11,422 Deferred ESOP benefits, minorities' interests and

company-obligated mandatorily redeemed preferred securities of subsidiary trusts holding solely subordinated debentures of the Company 466 392 330 349 208

Preferred stock 669 687 705 721 763 Common shareholders' equity 4,911 4,857 4,985 4,367 3,878

Total capitalization 21,047 21,043 18,673 17,670 16,271 Selected data and ratios

Book value per common share 7.35 7.35 7.59 6.71 5.92 Employees at year end 94,600 92,700 91,500 86,700 85,900 Working capital 4,035 3,968 3,074 2,948 2,843 Current ratio 1.5 1.5 1.4 1.4 1.4 Annual interest expense on short and long-term

debt 787 859 812 871 751 Effective interest rate, net 5.25% 5.69% 6.42% 7.12% 6.58%

Source: Pre-restated financial results from: 1 Xerox Corporation, 1999 Annual Report (Stamford, CT: Xerox, 2000); 2 Xerox Corporation, 1996 Annual Report (Stamford, CT: Xerox, 1997).

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

14

Exhibit 2 Xerox Quarterly Results of Operations

In $Millions (except per share amounts) First

QuarterSecond Quarter

Third Quarter

Fourth Quarter Full Year

20001

Revenues $4,540 $4,778 $4,503Costs and Expenses 4,901 4,531 4,738 Income (Loss) before Income Taxes (Benefits),

Equity Income and Minorities' Interests ($361) $247 ($235) Income Taxes (Benefits) (120) 79 (44) Equity in Net Income of Unconsolidated Affiliates 4 46 10 Minorities' Interests in Earnings of Subsidiaries 11 12 10 Net Income (Loss) ($248) $202 ($191) Basic Earnings (Loss) per Share ($0.39) $0.29 ($0.30)

19992

Revenues $4,300 $4,862 $4,628 $5,438 $19,228Costs and Expenses 3,806 4,229 4,123 5,034 17,192Income (Loss) before Income Taxes (Benefits),

Equity Income and Minorities' Interests $494 $633 $505 $404 $2,036Income Taxes (Benefits) 153 196 157 125 631Equity in Net Income of Unconsolidated Affiliates 10 24 5 29 68Minorities' Interests in Earnings of Subsidiaries 8 13 14 14 49Net Income (Loss) $343 $448 $339 $294 $1,424Basic Earnings (Loss) per Share $0.50 $0.66 $0.50 $0.43 $2.09

19982

Revenues $4,304 $4,742 $4,607 $5,794 $19,447Costs and Expenses 3,859 5,841 4,067 4,917 18,684Income (Loss) before Income Taxes (Benefits),

Equity Income and Minorities' Interests $445 ($1,099) $540 $877 $763Income Taxes (Benefits) 147 (385) 173 272 207Equity in Net Income of Unconsolidated Affiliates 14 12 28 20 74Minorities' Interests in Earnings of Subsidiaries 11 10 14 10 45Net Income (Loss) from Continuing Operations $301 ($712) $381 $615 $395Discontinued Operations (190) Net Income (Loss) $111 ($712) $381 $615 $395Basic Earnings (Loss) per Share

Continuing Operations $0.44 ($1.10) $0.56 $0.92 $0.80Discontinued Operations (0.29) (0.28)

Basic Earnings (Loss) per Share $0.15 ($1.10) $0.56 $0.92 $0.52

Source: Pre-restated financial results from: 1 Xerox Corporation, 2000 Annual Report (Stamford, CT: Xerox, 2001); 2 Xerox Corporation, 1999 Annual Report (Stamford, CT: Xerox, 2000).

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

15

Exhibit 3 Anne Mulcahy Describes Her Early Family Life

Shaped by Family Debates

People often ask: What has it been like, carving out a career in what has traditionally been a man's world? For me, it always felt absolutely natural to be the only woman in a room full of men.

I grew up in a home that did not differentiate between being a man or being a woman. I had four brothers, but I was never assigned "female" responsibilities. I wasn't the one who cleaned up the dishes every night, or set the table while the boys were taking out the garbage. Today, I realize how unusual that is, but as a kid, it seemed perfectly normal.

My mother had as much to do with that as my father. She was the oldest of five sisters, but she had an older brother who was The King. She's the smartest person I know, yet she was never encouraged to go to college. She was brought up to believe that men were more valuable, and she wanted to be sure I never felt that.

In choosing my father, my mother deliberately chose a man who would see her as an equal. When she spoke, he listened. She handled the family's finances, and I never heard him question how she spent a dollar. Seeing how influential she was helped me immeasurably in developing my own independence.

My father loved words and ideas, and taught us to speak our minds without seeking approval for our opinions. To him, dinner was a time to be provocative, to discuss politics, religion, current events, anything that was contentious. You had to participate, you had to be armed with information from reading

newspapers. He pushed and pushed, and it could get really heated. It wasn't always fun for guests, but I thrived on it. I learned that you can disagree, even fight, without confusing theoretical arguments with personal attacks. If only those who were behind the Sept. 11 terrorist attacks had understood that concept.

Sure, we all sometimes said things we wished we hadn't. Maybe we called one another stupid in the heat of the moment, and maybe we left the table in total irritation. But if you seemed hurt, he'd always pat you on the back, suggest a walk around the block to calm down.

Probably because of all those dinner-table debates, and that gender-neutral household, I have expected to be defined by -- and succeed because of -- values, character and intellect. That removes a huge burden, not having to act in a way or prove something that isn't natural. So many people screw up their careers, just by trying to project what they think other people want to see.

That belief, that it's O.K. to just be who I am, has made it easier for me to work well with and for people who are different and to enjoy the diversity, not just tolerate it.

I'm no longer entirely a product of my upbringing. I used to be more comfortable with men. I didn't have sisters, I never had lots of girlfriends, and even now, I have two sons, no daughters. Still, early in my career, I started to understand that a network of women colleagues was important. So, like my parents, I don't differentiate by gender.

Source: Anne M. Mulcahy with Claudia Deutsch, “Shaped by Family Debates,” The New York Times (October 1, 2001): C6. Copyright © 2001 by The New York Times Company. Reprinted by permission.

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

16

Exhibit 4 Xerox Weekly Closing Share Price to October 20, 2000 (adjusted for splits)

$0

$10

$20

$30

$40

$50

$60

$70

1/5/90

7/5/90

1/5/91

7/5/91

1/5/92

7/5/92

1/5/93

7/5/93

1/5/94

7/5/94

1/5/95

7/5/95

1/5/96

7/5/96

1/5/97

7/5/97

1/5/98

7/5/98

1/5/99

7/5/99

1/5/00

7/5/00

pric

e pe

r sha

re

Source: Thompson Financial Datastream (accessed September 16, 2004).

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

17

Exhibit 5 Anne Mulcahy’s Comments for Third Quarter 2000 Earnings Pre-Announcement (as delivered), 8:30am, October 3, 2000

When Paul and I took on our leadership roles at Xerox in May we knew at the time that our internal issues were clouding our company’s understanding of the external issues. As Paul indicated, we have since made considerable progress on several fronts, although we haven’t yet seen the financial return we expected.

First, we’ve achieved stability in our sales force. We’ve reduced turnover from the high-water marks early this year.

Second, we now have a much better understanding of the depth and magnitude of our internal problems.

Third, we’ve implemented some critical management changes – we’ve put the right people in the right jobs. I have confidence in this team. They have strong and proven track records. They are able to address the serious issues we face.

And finally, we not only changed people but changed expectations. We’ve cut through the complex structure that was layered on over the past several years, eliminated much of the matrix management – which allows our managers increased responsibility – and at the same time increased accountability.

As we worked through these internal changes, it became clear to Paul and me that based upon the external market challenges and the realities of our results, we had an even bigger problem. We had an unsustainable business model.

We understand that stronger competition is here to stay. We are focusing on higher growth in services and solutions versus just hardware. We will follow the migration from copies to prints. And we will price our offerings based on the economics of the digital world.

As a result, our recent energies have been focused on implementing a business model that will yield the appropriate financial returns. This means implementing a business model that allows us to be competitive in the marketplace and at the same time delivers shareholder value. We’re moving forward now on three fronts to make some critical – but informed and knowledge-based decisions – on resizing our business and our cost base to meet the realities of the marketplace.

First, we’re pulling out the stops to re-size our company and re-scale our costs.

Second, we’re moving on asset dispositions beyond those originally contemplated so that we drive cash flow and improve the balance sheet.

Finally, we’re reviewing the company’s dividend level, which is ultimately the responsibility of our Board of Directors. We’ll have more to say about this later in the month.

All told, we’re not talking about an evolution in our business. We’re talking about a transformation.

It’s a transformation whose benefits, we believe, will be measured not in the tens of millions, or hundreds of millions of dollars. But in the billions.

As I indicated, a critical factor in enabling this new business model is lowering our cost base. That means: driving down not only SAG as a percentage of our revenue, but in absolute terms, focusing on product costs, service costs, overhead and management infrastructure. No stone is being left unturned related to explicit cost-reduction efforts.

Simultaneously, let me assure you that there will be no changes as a result of these initiatives in the current territory configurations of the sales force. We must focus on sales force stability to ensure profitable revenue growth. While we will continue to invest in research and development activities that are core to our business, we are also making the tough choices on those aspects of our business where we will no longer invest.

In short, we are not focused on restoring the Xerox of the past. But we are re-orienting our business model to win in the context of the realities we face in today’s increasingly competitive marketplace. I would also like to underscore that we are acting with a sense of urgency.

We are already pursuing many of these actions as we speak. Our intention is to implement them in a disciplined, orderly, and timely manner. We understand the seriousness of the business issues we face and we believe our response is commensurate to address the scope of the problem.

I’m sure you’d like more specifics on a number of these initiatives. We will fill in the details at our earnings announcement later this month, and as decisions are made and implemented. That said, Paul, Barry and I are prepared to open the phones and take your questions…

Source: Xerox Corporation company documents.

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

18

Exhibit 6 Bankruptcy Rumors Regarding Xerox as Reported by Reuters.

Xerox bonds smudged by rumours, downgrade. By Nancy Leinfuss NEW YORK, Oct 13 (Reuters) - Xerox Corp.'s

bonds remained at weak levels on Friday, even after the world’s No. 1 photocopier maker dismissed rumours it would seek bankruptcy protection.

Xerox’s investment-grade bonds, which like junk bonds are now quoted by price rather than by yield spreads, were quoted Friday at 77 cents on the dollar bid, 80 cents offered, traders said.

Xerox scotched rumours it was in more trouble than it has let on, saying in a statement that “it has adequate liquidity, including its $7 billion revolving credit agreement, which is available through October 2002.” Xerox recently tapped that credit line, it said in a filing this week with the Securities and Exchange Commission.

A company spokeswoman in Europe told Reuters that “these are misleading market rumours about our company filing for Chapter 11,” referring to the U.S. Bankruptcy Code section regarding reorganization.

Domenick Fumai, fixed-income analyst at BNP Paribas, does not expect Xerox to file for bankruptcy.

“I don’t think there’s any reason to believe they are in distress,” he said. “They are in compliance with the covenants of their revolving credit facility. The only way I envision Xerox filing for Chapter 11 is if there’s some material extenuating circumstances that no one is expecting.

“I still believe Xerox risks a downgrade to a ‘BB’ rating if it doesn’t do anything to appease the rating agencies, and improve revenues or earnings and cash flow,” he added.

On Friday, credit rating agency Fitch downgraded Xerox Corp. and its subsidiaries’ senior debt rating to “BBB-minus” from “A-minus,” just one notch above junk status.

Fitch also cut its ratings for the company’s U.S. commercial paper programme to “F3” from “F2.”

Its rating outlook is “negative.” The actions reflected the decline in Xerox’s financial performance, uncertainties surrounding the company’s business model and operating strategy going forward, and the potential for reduced liquidity, Fitch said.

Standard & Poor’s recently affirmed its “BBB” long-term ratings, two notches above junk, for Xerox and its units, with a “stable” outlook. Several weeks ago, S&P cut those ratings two notches from “A-minus.”

Moody’s Investors Service also cut its long-term ratings for Xerox two notches to “Baa2” from “A3,” several weeks ago, with a “stable” outlook.

The company, which has been struggling to address falling profit margins by implementing several costly restructurings in recent years, has shed some 85 percent of its stock market valuation since 1999.

Last week, the U.S.-based company said it expected a third-quarter loss of 15 to 20 cents a share, while analysts polled by First Call/Thomson Financial were expecting a profit of 12 cents a share. It was the company’s fourth profit warning in five quarters. Xerox should announce third-quarter results later this month.

This week the company also said it will cut its quarterly dividend to 5 cents per share from 20 cents to reduce its cash requirement by an annual $400 million.

However, the spokeswoman said these announcements did not mean Xerox is having cash problems.

Xerox stock closed at $10-7/16, down 11/16, on the New York Stock Exchange. The stock’s 52-week high is $32-3/4 and its year low is $10-1/4.

Xerox told analysts last week it is planning “bold actions” and “very dramatic changes” to “change the underpinning of (Xerox’s) business model.”

Source: Nancy Leinfuss, “Xerox Bonds Smudged by Rumors, Downgrade,” Reuters News Service (October 13, 2000). Copyright © 2000 by Reuters News Service. Reprinted by permission.

405-

050

-1

9-

Exh

ibit

7X

erox

Clo

sing

Sto

ck P

rice

and

Tra

de

Vol

ume,

Q2

of 2

000,

and

Q3

thro

ugh

Oct

ober

20,

200

0.

$0$5$10

$15

$20

$25

$30

03/31

/2000

04/20

/2000

05/11

/2000

06/01

/2000

06/21

/2000

07/12

/2000

08/01

/2000

08/21

/2000

09/11

/2000

09/29

/2000

10/19

/2000

price per share

051015202530354045

volume (000,000s)

Volu

me

Clo

sing

Pric

e

10/3

/200

0 E

arly

ear

ning

s ca

llM

id O

ctob

er 2

000

Bank

rupt

cy ru

mor

s

5/11

/200

0 M

ulca

hy n

amed

CO

O

Sour

ce:

Tho

mps

on F

inan

cial

Dat

astr

eam

(acc

esse

d S

epte

mbe

r 16

, 200

4).

405-050 Anne Mulcahy: Leading Xerox through the Perfect Storm (A)

20

Exhibit 8 Draft Operational Plan for Operation Turnaround.

Asset dispositions

Goal: To generate $2 to $4 billion in asset area

• Sell China operations to Fuji Xerox.

• Sell portion of Fuji Xerox to Fuji Photo Film.

• Sell around inkjet business.

• Build strategic partnership for US and Europe paper businesses that would involve partner having most of assets.

• Sell around engineering services business.

• Sell or outsource parts of manufacturing operations.

• Look for a customer financing vehicle that does not burden the balance sheet.

• Leverage asset of PARC by seeking joint venture with non-competitive partners, spinning-off non-core technologies and commercializing non-core technology with VC partnerships.

Cost reductions

Goal: To reduce additional $1 billion in costs.

• Cut dividend to 5 cents a share, saving $400 million a year.

• Cut SGA by $600 million: Remove industry and product sector overhead in North America and Europe sales (continue to go to market by industry); reducing headquarters operations; developing markets will resize and go to distributor relationships in non-strategic geographies.

• Cut $200 million in supply chain and manufacturing costs. Simply stated, we can no longer afford to be vertically integrated at every step of the value chain across our product line. It leads to a cost structure we can’t support and more importantly, a price structure our customers won’t support.

• Eliminate worldwide-service staff organization, moving activity into operating companies. Investigate service offerings to match cost to value received by customer.

• R&D. Narrowing R&D based on affordability and future profitability. Prioritizing high end businesses and color while rationalizing R&D with Fuji Xerox.

• Cut infrastructure and overhead $200 million. Reduce headquarters staff, simplify organizational structure and reduce number of P&Ls.

Note: This will require further employment reductions.

Source: Xerox Corporation company documents.

Anne Mulcahy: Leading Xerox through the Perfect Storm (A) 405-050

21

Endnotes

1 Gary Jacobsen and John Hillkirk, Xerox, American Samurai (New York: Macmillan, 1986); David T. Kearns and David A. Nadler, Prophets in the Dark: How Xerox Reinvented Itself and Beat Back the Japanese (New York: HarperCollins, 1992).

2 Betsy Morris, “The Accidental CEO,” Fortune (June 23, 2003): p. 58.

3 Last two sentences from Betsy Morris, “The Accidental CEO.”

4 Richard Mullins, “She’s Earned the Top Spot,” Rochester Democrat and Chronicle (November 4, 2001).

5 Ibid.

6 Betsy Morris, “The Accidental CEO.”

7 Ibid.

8 Ibid.

9 For background, see Rich Miller, Debra Sparks, Heather Timmons, Steve Rosenbush, Geoffrey Smith, Joseph Weber and Roger O. Crockett, “The Financing Squeeze: Both the Banks and the Markets Are Turning Off the Spigots,” BusinessWeek (October 30, 2000), p. 50.

10 Andrew Hill, “Moody’s Places Xerox Ratings under Review,” The Financial Times (October 20, 2000): p. 34.